UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-4367 |

|

Columbia Funds Series Trust I |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-617-426-3750 | |

|

Date of fiscal year end: | November 30, 2006 | |

|

Date of reporting period: | November 30, 2006 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Columbia Management®

Columbia Tax-Exempt Fund

Annual Report – November 30, 2006

NOT FDIC INSURED

May Lose Value

No Bank Guarantee

Table of contents

| Economic Update | | | 1 | | |

|

| Performance Information | | | 2 | | |

|

| Understanding Your Expenses | | | 3 | | |

|

| Portfolio Manager's Report | | | 4 | | |

|

| Fund Profile | | | 6 | | |

|

| Financial Statements | | | 7 | | |

|

| Investment Portfolio | | | 8 | | |

|

Statement of Assets and

Liabilities | | | 56 | | |

|

| Statement of Operations | | | 57 | | |

|

Statement of Changes in

Net Assets | | | 58 | | |

|

| Financial Highlights | | | 60 | | |

|

| Notes to Financial Statements | | | 64 | | |

|

Report of Independent

Registered Public Accounting

Firm | | | 73 | | |

|

| Unaudited Information | | | 74 | | |

|

| Fund Governance | | | 75 | | |

|

Board Consideration and

Approval of Investment Advisory Agreements | | | 79 | | |

|

Summary of Management Fee

Evaluation by Independent

Fee Consultant | | | 82 | | |

|

| Columbia Funds | | | 87 | | |

|

Important Information About

This Report | | | 89 | | |

|

The views expressed in the President's Message and Portfolio Manager's report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific securities should not be construed as a recommendation or investment advice.

President's Message

November 30, 2006

Dear Shareholder,

Over the past few years, you've heard a lot about change here at Columbia Funds as we've streamlined our fund offerings, reduced our expenses and enhanced the different ways that you can do business with us. Our goal in all these matters has been to make investing easier and more convenient—and to ensure that you find the range of financial choices and services that you expect from one of the nation's leading financial companies.

As 78 million baby boomers move closer to retirement, we are also mindful that retirement is the single most important financial goal for many Americans. To that end we have committed considerable resources to ensure that you can find a wide range of choices at Columbia Funds, whether you are just beginning to invest for retirement or preparing to turn your retirement savings into income. If you haven't done so already, we suggest that you work closely with your financial adviser to draw up a personal investment plan that is based on what you'll require for your future. We continue to look for new ways to help meet the unique needs of all our investors—especially those who are approaching retirement.

Change is a constant in our lives, but one thing that does not change is our commitment to continue to improve your investment and service experiences. At Columbia Funds, we understand that you have a choice of financial providers and we want you to remain satisfied with your decision to invest with us—now and in the years to come.

As you read the following message from the manager of your Columbia fund, keep in mind that investing is often a long-term undertaking. While it's important to review the performance and market environment of the most recent period, it's essential to evaluate this information with your goal, time horizon and risk tolerance in mind.

Sincerely,

Christopher L. Wilson

President, Columbia Funds

Economic Update – Columbia Tax-Exempt Fund

The US economy grew at a solid but uneven pace during the 12-month period that began December 1, 2005 and ended November 30, 2006. Gross domestic product (GDP) growth was robust in the first quarter of 2006, as businesses created jobs at a brisk pace, industrial production rose and both personal spending and personal income moved higher. However, a weak housing market began to weigh on the economy, and the manufacturing sector contracted late in the period—registering its first downturn since the spring of 2003. Against this backdrop, economic growth averaged 3.0% for the 12-month period.

Between December and June, the Federal Reserve Board (the Fed) raised a key short-term interest rate, the federal funds rate, five times—to 5.25%. But as economic growth slowed, the Fed turned cautious and passed on any further increases after its June meeting. Inflation also retreated during the period, which lent further support to the Fed's decision. Investors reacted favorably to the prospect of stable or possibly even lower interest rates and both the stock and bond markets rallied.

Bonds bounced back

Although bond yields moved higher early in the period, the US bond market delivered a respectable return, as prices rose and yields declined in reaction to the Fed's mid-year decision to put further short-term rate increases on hold. The yield on the 10-year US Treasury note, a bellwether for the bond market, ended the period at 4.4%—slightly lower than where it started. In this environment, the Lehman Brothers U.S. Aggregate Bond Index returned 5.94%. High-yield bonds led the fixed-income markets, reflecting investor confidence about the overall resilience of the economy despite its slower pace of growth. The Merrill Lynch U.S. High Yield, Cash Pay Index returned 11.46%.

Stocks moved solidly higher

After a lackluster start, stock prices moved solidly higher during the 12-month period covered by this report. The S&P 500 Index, a broad measure of common stock performance, rose 14.23%. Small- and mid-cap stocks outpaced large-cap stocks, although the margin of leadership narrowed as the period wore on. Value stocks outperformed growth stocks, as measured by their respective Russell indices.1 Foreign stock markets generally outperformed the US market. The MSCI EAFE Index,2 which tracks stock market performance in industrialized countries outside the United States and Canada, returned 28.20%. A declining US dollar also bolstered foreign returns for US investors.

1The Russell 1000 Value Index measures the performance of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell Midcap Value Index measures the performance of those Russell Midcap Index companies with lower price-to-book ratios and lower forecasted growth values. Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index.

2The MSCI EAFE (Europe, Australasia, Far East) Index is a free-float adjusted market capitalization index that is designed to measure developed market equity performance, excluding the US and Canada. Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index.

Summary

For the 12-month period ended November 30, 2006

g Investment-grade bonds rebounded as yields declined, lifting the Lehman Brothers U.S. Aggregate Bond Index to a respectable return. High-yield bonds, as measured by the Merrill Lynch U.S. High Yield, Cash Pay Index, led the fixed-income markets.

Lehman Index | | Merrill Lynch

Index | |

|

| |  | |

|

g The broad stock market, as measured by the S&P 500 Index, returned 14.23%. Small cap value stocks led the market, as measured by the Russell 2000 Value Index.

| S&P Index | | Russell Index | |

|

| |  | |

|

The Lehman Brothers U.S. Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

The Merrill Lynch U.S. High Yield, Cash Pay Index tracks the performance of non-investment-grade corporate bonds.

The S&P 500 Index tracks the performance of 500 widely held, large-capitalization US stocks.

The Russell 2000 Value Index measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index.

1

Performance Information – Columbia Tax-Exempt Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

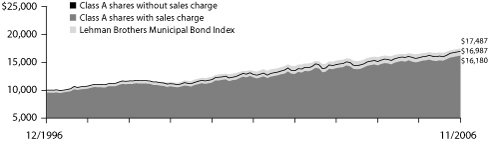

Performance of a $10,000 investment

12/01/96 – 11/30/06 ($)

| Sales charge | | without | | with | |

| Class A | | | 16,987 | | | | 16,180 | | |

| Class B | | | 15,765 | | | | 15,765 | | |

| Class C | | | 15,982 | | | | 15,982 | | |

| Class Z | | | 17,028 | | | | n/a | | |

Growth of a $10,000 investment 12/01/96 – 11/30/06 ($)

The chart above shows the growth in value of a hypothetical $10,000 investment in Class A shares of Columbia Tax-Exempt Fund during the stated time period, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Lehman Brothers Municipal Bond Index is considered representative of the broad market for investment-grade, tax exempt bonds with a maturity of at least one year. Indices are not investments, they do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index. Securities in the fund may not match those in an index.

Average annual total return as of 11/30/06 (%)

| Share class | | A | | B | | C | | Z | |

| Inception | | 11/21/78 | | 05/05/92 | | 08/01/97 | | 09/19/05 | |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | |

| 1-year | | | 7.53 | | | | 2.42 | | | | 6.73 | | | | 1.73 | | | | 6.89 | | | | 5.89 | | | | 7.75 | | |

| 5-year | | | 5.79 | | | | 4.77 | | | | 5.01 | | | | 4.67 | | | | 5.16 | | | | 5.16 | | | | 5.84 | | |

| 10-year | | | 5.44 | | | | 4.93 | | | | 4.66 | | | | 4.66 | | | | 4.80 | | | | 4.80 | | | | 5.47 | | |

Average annual total return as of 12/31/06 (%)

| Share class | | A | | B | | C | | Z | |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | |

| 1-year | | | 5.56 | | | | 0.55 | | | | 4.78 | | | | -0.22 | | | | 4.94 | | | | 3.94 | | | | 5.78 | | |

| 5-year | | | 5.97 | | | | 4.94 | | | | 5.18 | | | | 4.85 | | | | 5.34 | | | | 5.34 | | | | 6.03 | | |

| 10-year | | | 5.44 | | | | 4.93 | | | | 4.66 | | | | 4.66 | | | | 4.81 | | | | 4.81 | | | | 5.47 | | |

The "with sales charge" returns include the maximum initial sales charge of 4.75% for Class A shares, maximum contingent deferred sales charge of 5.00% in the first year, declining to 1.00% in the sixth year and eliminated thereafter for Class B shares and 1.00% for Class C shares for the first year only. The "without sales charge" returns do not include the effect of sales charges. If they had, returns would be lower.

All results shown assume reinvestment of distributions. Class Z shares are sold at net asset value with no 12b-1 fees. Class Z shares have limited eligibility and the investment minimum requirement may vary. Please see the fund's prospectus for details.

Performance results reflect any voluntary waivers or reimbursement of fund expenses by the investment advisor and/or its affiliates. Absent these waivers or reimbursement arrangements, performance results would have been lower.

The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Class Z is a newer class of shares. Its performance information includes returns of the fund's Class A shares (the oldest existing fund class). These returns have not been restated to reflect any differences in expenses (such as Rule 12b-1 fees) between Class A shares and the newer class of shares. The Class A share returns have been adjusted to take into account the fact that Class Z shares are sold without sales charges. If differences in expenses had been reflected, the returns shown for the period prior to the inception of the newer class of shares would have been higher, since Class Z shares are not subject to any Rule 12b-1 fees.

Class C is a newer class of shares. Its performance information includes returns of the fund's Class B shares for periods prior to the inception of Class C shares. Class B shares would have substantially similar annual returns because Class B and Class C shares generally have similar expense structures. Class A shares were initially offered on November 21, 1978, Class B shares were initially offered on May 5, 1992, Class C shares were initially offered on August 1, 1997, and Class Z shares were initially offered on September 19, 2005.

2

Understanding Your Expenses – Columbia Tax-Exempt Fund

As a fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory fees, Rule 12b-1 fees and other fund expenses. The information on this page is intended to help you understand your ongoing costs of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your fund's expenses by share class

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class during the period. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the reporting period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "actual" column is calculated using the fund's actual operating expenses and total return for the period. The amount listed in the "hypothetical" column for each share class assumes that the return each year is 5% before expenses and is calculated based on the fund's actual operating expenses. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during this reporting period.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other fund companies, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund and do not reflect any transaction costs, such as sales charges or redemption or exchange fees.

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period:

g For shareholders who receive their account statements from Columbia Management Services, Inc., your account balance is available online at www.columbiafunds.com or by calling Shareholder Services at 800.345.6611.

g For shareholders who receive their account statements from their brokerage firm, contact your brokerage firm to obtain your account balance.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table below titled "Expenses paid during the period," locate the amount for your share class. You will find this number in the column labeled "actual." Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

06/01/06 – 11/30/06

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid

during the period ($) | | Fund's annualized

expense ratio (%) | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | |

| Class A | | | 1,000.00 | | | | 1,000.00 | | | | 1,055.50 | | | | 1,020.96 | | | | 4.23 | | | | 4.15 | | | | 0.82 | | |

| Class B | | | 1,000.00 | | | | 1,000.00 | | | | 1,051.49 | | | | 1,017.20 | | | | 8.07 | | | | 7.94 | | | | 1.57 | | |

| Class C | | | 1,000.00 | | | | 1,000.00 | | | | 1,052.29 | | | | 1,017.95 | | | | 7.31 | | | | 7.18 | | | | 1.42 | | |

| Class Z | | | 1,000.00 | | | | 1,000.00 | | | | 1,056.50 | | | | 1,021.96 | | | | 3.20 | | | | 3.14 | | | | 0.62 | | |

Expenses paid during the period are equal to the annualized expense ratio for the share class, multiplied by the average account value over the period, then multiplied by the number of days in the fund's most recent fiscal half-year and divided by 365.

Had the investment advisor and/or any of its affiliates not waived or reimbursed a portion of expenses, total return would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the fund and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning shares of different funds. If these transaction costs were included, your costs would have been higher.

3

Portfolio Manager's Report – Columbia Tax-Exempt Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Net asset value per share

as of 11/30/06 ($)

| Class A | | | 13.88 | | |

| Class B | | | 13.88 | | |

| Class C | | | 13.88 | | |

| Class Z | | | 13.88 | | |

Distributions declared per share

12/01/05 – 11/30/06 ($)

| Class A | | | 0.60 | | |

| Class B | | | 0.50 | | |

| Class C | | | 0.52 | | |

| Class Z | | | 0.63 | | |

A portion of the fund's income may be subject to the alternative minimum tax. The fund may at times purchase tax-exempt securities at a discount. Some, or all, of this discount may be included in the fund's ordinary income, and is taxable when distributed.

SEC yields

as of 11/30/06 (%)

| Class A | | | 3.47 | | |

| Class B | | | 2.90 | | |

| Class C | | | 3.05 | | |

| Class Z | | | 3.84 | | |

The 30-day SEC yields reflect the portfolio's earning power, net of expenses, expressed as an annualized percentage of the public offering price per share at the end of the period.

Taxable-equivalent SEC yields

as of 11/30/06 (%)

| Class A | | | 5.34 | | |

| Class B | | | 4.46 | | |

| Class C | | | 4.69 | | |

| Class Z | | | 5.91 | | |

Taxable-equivalent SEC yields are based on the maximum effective 35.0% federal income tax rate. This tax rate does not reflect the phase out of exemptions or the reduction of the otherwise allowable deductions that occur when adjusted gross income exceeds certain levels.

For the 12-month period ended November 30, 2006, Columbia Tax-Exempt Fund Class A shares returned 7.53% without sales charge. The fund outperformed its benchmark, the Lehman Brothers Municipal Bond Index, which returned 6.12%.1 It also outpaced the average return of its peer group, the Lipper General Municipal Debt Funds Classification which was 5.77%.2 The fund's substantial holdings in securities that mature in 15 years or longer were a major factor in its performance. Declining long-term yields helped boost performance from the fund's zero coupon and non-callable holdings. Security selection in the high yield sector also contributed to returns. The reorganization of the Columbia Tax-Exempt Insured Fund and the Columbia Municipal Income Fund into Columbia Tax-Exempt Fund resulted in a small decline in the fund's holdings in non-rated bonds due to the composition of the other funds, which were otherwise si milarly structured.

Longer intermediate maturity bonds, zero coupon and non-callable issues boosted returns

As the pace of economic growth slowed, the Federal Reserve Board (the Fed) curtailed its streak of 17 consecutive increases in the federal funds rate—a key short-term interest rate. The Fed's last hike brought the federal funds rate to 5.25% in June, and that's where it remained throughout the period. While inflationary pressures remain, the Fed has said that it expects a slowing economy to keep inflation in check. The fixed income market also broadcasted muted inflationary expectations, sending prices higher and yields lower on bonds at the longer end of the maturity spectrum. As a result, our focus on bonds in the longer intermediate maturity range (15 years and longer) was rewarded during the period. We believed these issues had the potential to outperform short-term bonds.

Non-callable bonds and zero-coupon bonds maturing in longer than 10 years also performed well as longer-term yields declined. Non-callable bonds tend to perform true to their maturity dates as opposed to callable bonds, which give the issuer the option to redeem the bonds prior to their maturity date—an option that became more attractive as yields on all but the shortest-maturity bonds declined. Zero-coupon bonds, which are very sensitive to interest rate changes, do not pay income but are redeemed for full face value at maturity, also benefited because their value increased as yields declined.

High-yield holdings added to performance

During the period, the difference in yield between high quality bonds and lower quality issues narrowed, as investors were attracted to bonds that offered higher yields. This trend benefited the fund's high-yield holdings. Because many of the fund's high yield bonds were purchased several years ago at more attractive yields than are available today, these securities also helped boost the fund's income.

1The Lehman Brothers Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with maturity of at least one year. Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index.

2Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustment for the effect of sales loads.

4

Portfolio Manager's Report (continued) – Columbia Tax-Exempt Fund

Looking ahead

The Fed has indicated that it is likely to base any further actions with respect to short-term interest rates on evidence presented in the economic data. As a result, we plan to continue to monitor the economy—especially inflation, employment and wage statistics and housing market movements—to gauge our expectations for the direction of the market. Given the current environment of relatively slow growth and the Fed on hold, we plan to continue to focus on bonds with good call protection in the longer intermediate range of the maturity spectrum. However, we could alter our approach if our expectations for economic growth and inflation are not met.

Top 5 sectors

as of 11/30/06 (%)

| Refunded/Escrowed | | | 18.0 | | |

| Local General Obligations | | | 13.2 | | |

| Special Non-Property Tax | | | 7.7 | | |

| State Appropriated | | | 6.8 | | |

| Hospitals | | | 6.7 | | |

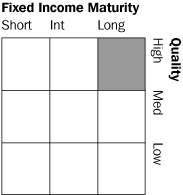

Quality breakdown

as of 11/30/06 (%)

| AAA | | | 68.1 | | |

| AA | | | 8.4 | | |

| A | | | 6.0 | | |

| BBB | | | 7.4 | | |

| BB | | | 0.2 | | |

| B | | | 0.3 | | |

| CCC | | | 0.2 | | |

| Non-Rated | | | 8.6 | | |

| Cash and Equivalents | | | 0.8 | | |

Maturity breakdown

as of 11/30/06 (%)

| 0-1 years | | | 0.3 | | |

| 1-3 years | | | 3.2 | | |

| 3-5 years | | | 7.1 | | |

| 5-7 years | | | 9.9 | | |

| 7-10 years | | | 13.5 | | |

| 10-15 years | | | 32.1 | | |

| 15-20 years | | | 18.1 | | |

| 20-25 years | | | 9.8 | | |

| 25 years and over | | | 5.2 | | |

| Cash and Equivalents | | | 0.8 | | |

Sector weightings are calculated as a percentage of net assets.

Quality and maturity breakdowns are calculated as a percentage of total investments. Ratings shown in the quality breakdown represent the rating assigned to a particular bond by one of the following nationally recognized rating agencies: Standard & Poor's, a division of The McGraw-Hill Companies, Inc., Moody's Investors Service, Inc. or Fitch Ratings Ltd. Ratings are relative and subjective and are not absolute standards of quality. The fund's credit quality does not remove market risk.

Because the fund is actively managed, there is no guarantee that the fund will continue to invest in these sectors or maintain these quality and maturity breakdowns in the future.

5

Fund Profile – Columbia Tax-Exempt Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Summary

1-year return as of 11/30/06

| | +7.53 | % | |

|

Class A shares Class A shares

(without sales charge) | |

|

| | +6.12 | % | |

|

Lehman Brothers Lehman Brothers

Municipal Bond Index | |

|

Management Style

Management style is determined by Columbia Management and is based on the investment strategy and process as outlined in the fund's prospectus.

Summary

g For the 12-month period ended November 30, 2006, the fund's Class A shares returned 7.53%, without sales charge.

g The fund outperformed both its benchmark and the average return of its peer group, the Lipper General Municipal Debt Funds Classification average.

g The fund's substantial allocation to bonds maturing in 15 or more years drove its performance; zero-coupon, non-callable and high-yield bond holdings also contributed to returns.

Portfolio Management

Kimberly Campbell has managed the Columbia Tax-Exempt Fund since December 2001. Ms. Campbell has been with the advisor or its predecessors or affiliate organizations since June 1995.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this fund may differ from that presented for other Columbia Funds mutual funds and portfolios. Performance for different classes of shares will vary based on differences in sales charges and fees associated with each class. For standardized performance, please refer to the Performance Information page.

Tax-exempt investing offers current tax-exempt income, but it also involves special risks. The value of the fund will be affected by interest rate changes and the creditworthiness of issues held in the fund. When interest rates go up, bond prices generally drop and vice versa. Interest income from certain tax-exempt bonds may be subject to certain state and local taxes and, if applicable, the alternative minimum tax. Capital gains are not exempt from income taxes.

Investing in high-yield or "junk" bonds offers the potential for higher income than investments in investment-grade bonds but also has a higher degree of risk. Changes in economic conditions or other circumstances may adversely affect a high-yield bond issuer's ability to make timely principal and interest payments.

6

Financial Statements – Columbia Tax Exempt Fund

November 30, 2006

A guide to understanding your fund's financial statements

| Investment Portfolio | | The investment portfolio details all of the fund's holdings and their values as of the last day of the reporting period. Portfolio holdings are organized by type of asset, industry, country or geographic region (if applicable) to demonstrate areas of concentration and diversification. | |

|

| Statement of Assets and Liabilities | | This statement details the fund's assets, liabilities, net assets and share price for each share class as of the last day of the reporting period. Net assets are calculated by subtracting all the fund's liabilities (including any unpaid expenses) from the total of the fund's investment and non-investment assets. The share price for each class is calculated by dividing net assets for that class by the number of shares outstanding in that class as of the last day of the reporting period. | |

|

| Statement of Operations | | This statement details income earned by the fund and the expenses accrued by the fund during the reporting period. The Statement of Operations also shows any net gain or loss the fund realized on the sales of its holdings during the period, as well as any unrealized gains or losses recognized over the period. The total of these results represents the fund's net increase or decrease in net assets from operations. | |

|

| Statement of Changes in Net Assets | | This statement demonstrates how the fund's net assets were affected by its operating results, distributions to shareholders and shareholder transactions (e.g., subscriptions, redemptions and dividend reinvestments) during the reporting period. The Statement of Changes in Net Assets also details changes in the number of shares outstanding. | |

|

| Financial Highlights | | The financial highlights demonstrate how the fund's net asset value per share was affected by the fund's operating results. The financial highlights table also discloses performance for each class of shares and certain key ratios (e.g., class expenses and net investment income as a percentage of average net assets). | |

|

| Notes to Financial Statements | | These notes disclose the organizational background of the fund, its significant accounting policies (including those surrounding security valuation, income recognition and distributions to shareholders), federal tax information, fees and compensation paid to affiliates and significant risks and contingencies. | |

|

7

Investment Portfolio – Columbia Tax-Exempt Fund

November 30, 2006

| | | | | Par ($) | | Value ($) | |

| Education – 3.3% | |

| Education – 2.8% | |

| CA Educational Facilities Authority | |

| | | Loyola Marymount University,

Series 2001,

Insured: MBIA:

(a) 10/01/17

(a) 10/01/20 | | |

2,525,000

2,000,000 | | | |

1,629,989

1,123,780 | | |

| CA Municipal Finance Authority | |

| | | Escondido Charter,

Series 2006 A,

5.250% 06/01/36 | | | 1,750,000 | | | | 1,831,287 | | |

| IN Ivy Technical State College | |

| | | Series 1997 E,

Insured: AMBAC

5.125% 07/01/12 | | | 2,000,000 | | | | 2,050,520 | | |

| MA College Building Authority | |

| | | Series 1994 A,

7.500% 05/01/14 | | | 3,500,000 | | | | 4,270,805 | | |

| MA Health & Educational Facilities Authority | |

| | | Harvard University,

Series 1991 N,

6.250% 04/01/20 | | | 2,000,000 | | | | 2,520,820 | | |

| | Massachusetts Institute of Technology:

Series 2002 K,

5.500% 07/01/22 | | | 8,000,000 | | | | 9,577,760 | | |

| | Series 2003 L,

5.000% 07/01/18 | | | 5,000,000 | | | | 5,607,800 | | |

| NC University North Carolina at Chapel Hill | |

| | | Series 1997,

(a) 08/01/13 | | |

2,000,000 | | | |

1,562,080 | | |

| NY Dormitory Authority | |

| | | Educational Housing Services,

Series 2005,

Insured: AMBAC

5.250% 07/01/30 | | | 3,000,000 | | | | 3,553,680 | | |

| | New York University,

Series 2001 1,

Insured: AMBAC

5.500% 07/01/40 | | | 4,000,000 | | | | 4,973,560 | | |

| | Upstate Community Colleges,

Series 2005 B,

Insured: FGIC

5.500% 07/01/23 | | | 2,000,000 | | | | 2,388,060 | | |

| TX University of Texas Permanent University | |

| | | Series 2004 B,

5.000% 07/01/26 | | | 2,500,000 | | | | 2,667,175 | | |

| UT Weber State University Revenue | |

| | | Series 2005,

Insured: MBIA

4.250% 04/01/29 | | | 5,100,000 | | | | 5,024,469 | | |

See Accompanying Notes to Financial Statements.

8

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Education – (continued) | |

| Education – (continued) | |

| VA College Building Authority | |

| | | Virginia Educational Facilities,

Washington & Lee University,

Series 2001,

5.375% 01/01/21 | | | 10,000,000 | | | | 11,622,100 | | |

| WV University of West Virginia | |

| | | Series 1998 A,

Insured: MBIA

5.250% 04/01/28 | | | 5,000,000 | | | | 5,931,000 | | |

| | Series 2000 A,

Insured: AMBAC:

(a) 04/01/16

(a) 04/01/17

(a) 04/01/18 | | | 3,300,000

2,480,000

3,800,000 | | | | 2,275,383

1,631,939

2,388,034 | | |

| | Education Total | | | | | | | 72,630,241 | | |

| Student Loan – 0.5% | |

| IA Student Loan Liquidity Corp. | |

| | | Series 1998 J, AMT,

Insured: AMBAC

4.800% 06/01/09 | | | 2,750,000 | | | | 2,817,705 | | |

| WY Student Loan Corp. | |

| | | Series 1999 A,

6.250% 06/01/29 | | | 10,000,000 | | | | 10,655,100 | | |

| | Student Loan Total | | | | | | | 13,472,805 | | |

| Education Total | | | | | | | | | 86,103,046 | | |

| Health Care – 9.5% | |

| Continuing Care Retirement – 0.4% | |

| FL Capital Projects Finance Authority | |

| | | Glenridge on Palmer Ranch,

Series 2002 A,

8.000% 06/01/32 | | | 4,500,000 | | | | 5,057,235 | | |

| FL Lee County Industrial Development Authority | |

| | | Shell Point Village Project,

Series 1999 A,

5.750% 11/15/15 | | | 250,000 | | | | 260,843 | | |

| NC Medical Care Commission | |

| | | Glenaire, Inc.,

Series 2006,

5.500% 10/01/31 | | | 2,500,000 | | | | 2,619,350 | | |

| OH Hamilton County Health Care Facilities Revenue | |

| | | Twin Towers,

Series 1998 A,

5.125% 10/01/18 | | | 500,000 | | | | 517,910 | | |

| PA Montgomery County Industrial Development Authority | |

| | | Whitemarsh Continuing Care Retirement Community,

Series 2005,

6.125% 02/01/28 | | | 2,000,000 | | | | 2,137,120 | | |

| | Continuing Care Retirement Total | | | | | | | 10,592,458 | | |

See Accompanying Notes to Financial Statements.

9

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Health Care – (continued) | |

| Health Services – 0.5% | |

| MA Development Finance Agency | |

| | | Boston Biomedical Research Institute,

Series 1999,

5.650% 02/01/19 | | | 1,310,000 | | | | 1,365,387 | | |

| MN Minneapolis & St. Paul Housing & Redevelopment Authority | |

| | | Group Health Plan, Inc.,

Series 2003:

5.250% 12/01/16

6.000% 12/01/17 | | | 1,250,000

1,650,000 | | | | 1,327,512

1,826,682 | | |

| WI Health & Educational Facilities Authority | |

| | | Marshfield Clinic,

Series 1999,

Insured: RAD

6.250% 02/15/29 | | | 7,200,000 | | | | 7,766,496 | | |

| | Health Services Total | | | | | | | 12,286,077 | | |

| Hospitals – 6.7% | |

| AL Huntsville Health Care Authority | |

| | | Series 2001 A,

5.750% 06/01/31 | | | 5,000,000 | | | | 5,377,700 | | |

| AZ Health Facilities Authority | |

| | | Catholic Heallthcare West,

Series 1999 A,

6.625% 07/01/20 | | | 3,700,000 | | | | 4,086,058 | | |

| AZ University Medical Center Corp. | |

| | | Series 2004,

5.250% 07/01/13 | | | 1,000,000 | | | | 1,068,430 | | |

| CA ABAG Finance Authority for Nonprofit Corps. | |

| | | San Diego Hospital Association,

Series 2003 C,

5.375% 03/01/20 | | | 1,320,000 | | | | 1,422,868 | | |

| CA Health Facilities Financing Authority | |

| | | Catholic Healthcare West,

Series 2004 G,

5.250% 07/01/23 | | | 500,000 | | | | 534,790 | | |

| CT Health & Educational Facility Authority | |

| | | Series 2000 A,

Insured: RAD

6.000% 07/01/25 | | | 1,740,000 | | | | 1,878,086 | | |

| FL Coral Gables Health Facilities Authority | |

| | | Mariners Hospital,

Series 2004,

Insured: FSA

5.000% 08/15/34 | | | 5,000,000 | | | | 5,376,650 | | |

| FL Hillsborough County Industrial Development Authority | |

| | | Tampa General Hospital,

Series 2003 A:

5.000% 10/01/18

5.250% 10/01/24 | | | 825,000

4,000,000 | | | | 867,471

4,274,040 | | |

| FL Orange County Health Facilities Authority | |

| | | Orlando Regional Healthcare System,

Series 1999 E,

6.000% 10/01/26 | | | 6,905,000 | | | | 7,346,506 | | |

See Accompanying Notes to Financial Statements.

10

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Health Care – (continued) | |

| Hospitals – (continued) | |

| | Series 1996 A,

Insured: MBIA

6.250% 10/01/16 | | |

825,000 | | | |

976,058 | | |

| FL West Orange Healthcare District | |

| | | Series 2001 A,

5.650% 02/01/22 | | | 3,650,000 | | | | 3,871,190 | | |

| GA Chatham County Hospital Authority | |

| | | Memorial Health University Medical Center,

Series 2004 A,

5.500% 01/01/34 | | | 2,500,000 | | | | 2,692,550 | | |

| | | Memorial Medical Center,

Series 2001 A,

6.125% 01/01/24 | | | 3,000,000 | | | | 3,296,880 | | |

| GA Gainesville & Hall County Hospital Authority | |

| | | Northeast Georgia Health Systems,

Series 2001:

5.000% 05/15/12

5.000% 05/15/13 | | | 1,610,000

1,560,000 | | | | 1,679,536

1,624,132 | | |

| LA Public Facilities Authority | |

| | | Touro Infirmary,

Series 1999 A,

5.625% 08/15/29 | | | 10,940,000 | | | | 11,134,623 | | |

| MA Health & Educational Facilities Authority | |

| | | South Shore Hospital,

Series 1999 F,

5.750% 07/01/29 | | | 13,000,000 | | | | 13,716,430 | | |

| MI Dickinson County | |

| | | Series 1999,

5.700% 11/01/18 | | | 1,800,000 | | | | 1,866,402 | | |

| MI University of Michigan | |

| | | Series 2002 D,

5.250% 12/01/20 | | | 6,310,000 | | | | 6,748,040 | | |

| MN St. Paul Housing & Redevelopment Authority | |

| | | HealthEast, Inc.,

Series 1997 A,

5.500% 11/01/09 | | | 250,000 | | | | 257,708 | | |

| MN Waconia | |

| | | Ridgeview Medical Center,

Series 1999 A,

Insured: RAD

6.125% 01/01/29 | | | 1,000,000 | | | | 1,067,060 | | |

| MO Health & Educational Facilities Authority | |

| | | Lake Regional Health Systems,

Series 2003,

5.600% 02/15/25 | | | 625,000 | | | | 672,294 | | |

| | | SSM Health Care Corp.,

Series 2002 A:

5.000% 06/01/11

5.250% 06/01/12 | | | 2,000,000

2,500,000 | | | | 2,104,380

2,684,900 | | |

See Accompanying Notes to Financial Statements.

11

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Health Care – (continued) | |

| Hospitals – (continued) | |

| MS Medical Center Building Corp. | |

| | | University of Mississippi Medical Center,

Series 1998,

Insured: AMBAC

5.500% 12/01/23 | | | 10,550,000 | | | | 12,474,214 | | |

| NC Medical Care Community Health Care Facility | |

| | | Wilson Memorial Hospital,

Series 1997,

Insured: AMBAC

(a) 11/01/14 | | | 1,380,000 | | | | 1,020,524 | | |

| ND Ward County Health Care Facility | |

| | | Trinity Health,

Series 2006,

5.125% 07/01/29 | | | 1,250,000 | | | | 1,320,212 | | |

| NH Higher Educational & Health | |

| | | Series 1998,

5.800% 05/01/18 | | | 1,470,000 | | | | 1,513,747 | | |

| NM Farmington | |

| | | San Juan Medical Center,

Series 2004 A,

5.000% 06/01/23 | | | 500,000 | | | | 522,570 | | |

| NV Henderson | |

| | | Catholic Healthcare West,

Series 1999 A,

6.750% 07/01/20 | | | 520,000 | | | | 570,908 | | |

| OH Highland County Joint Township | |

| | | Series 1999,

6.750% 12/01/29 | | | 1,850,000 | | | | 1,944,905 | | |

| SC Greenville Hospital System Board | |

| | | Series 2001,

Insured: AMBAC

5.500% 05/01/26 | | | 5,000,000 | | | | 5,387,100 | | |

| TN Johnson City Health & Educational Facilities Board | |

| | | Mountain States Health Alliance,

Series 2006 A,

5.500% 07/01/36 | | | 1,250,000 | | | | 1,355,525 | | |

| TN Knox County Health, Educational & Housing Facilities Authority | |

| | | East Tennessee Hospital,

Series 2003 B,

5.750% 07/01/33 | | | 650,000 | | | | 703,144 | | |

| | Fort Sanders Alliance,

Series 1993,

Insured: MBIA

5.250% 01/01/15 | | | 5,000,000 | | | | 5,496,850 | | |

| TN Sullivan County Health Educational & Housing Facilities Board | |

| | | Wellmont Health System,

Series 2006 C,

5.250% 09/01/36 | | | 7,000,000 | | | | 7,444,360 | | |

| TX Harris County Health Facilities Development Corp. | |

| | | Memorial Hermann Hospital Systems,

Series 1998,

Insured: FSA

5.500% 06/01/11 | | | 3,335,000 | | | | 3,580,456 | | |

See Accompanying Notes to Financial Statements.

12

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Health Care – (continued) | |

| Hospitals – (continued) | |

| UT Murray | |

| | | IHC Health Services, Inc.,

Series 1996,

Insured: MBIA

5.000% 05/15/22 | | | 4,000,000 | | | | 4,019,120 | | |

| VA Augusta County Industrial Development Authority | |

| | | Augusta Health Care, Inc.,

Series 2003,

5.250% 09/01/20 | | | 1,325,000 | | | | 1,469,133 | | |

| VA Fairfax County Industrial Development Authority | |

| | | Inova Health System,

Series 1993 A,

5.000% 08/15/23 | | | 10,000,000 | | | | 10,991,000 | | |

| VA Henrico County Industrial Development Authority | |

| | | Bon Secours Health,

Series 1996,

Insured: MBIA

6.000% 08/15/16 | | | 5,000,000 | | | | 5,732,850 | | |

| WI Health & Educational Facilities Authority | |

| | | Aurora Health Care, Inc.:

Series 1999 B:

5.500% 02/15/15

5.625% 02/15/20 | | | 3,500,000

5,500,000 | | | | 3,652,180

5,745,465 | | |

| | Series 1999 A,

5.600% 02/15/29 | | | 4,000,000 | | | | 4,164,160 | | |

| | Series 2003,

6.400% 04/15/33 | | | 4,250,000 | | | | 4,789,197 | | |

| | | Waukesha Memorial Hospital,

Series 1990 B,

Insured: AMBAC

7.250% 08/15/19 | | | 10,000 | | | | 10,027 | | |

| | | Wheaton Franciscan Services,

Series 2002,

5.750% 08/15/30 | | | 4,900,000 | | | | 5,281,563 | | |

| | Hospitals Total | | | | | | | 175,813,992 | | |

| Intermediate Care Facilities – 0.6% | |

| IL Development Finance Authority | |

| | | Hoosier Care, Inc.,

Series 1999 A,

7.125% 06/01/34 | | | 2,320,000 | | | | 2,403,567 | | |

| IN Health Facilities Financing Authority | |

| | | Hoosier Care, Inc.,

Series 1999 A,

7.125% 06/01/34 | | | 11,965,000 | | | | 12,395,979 | | |

| | Intermediate Care Facilities Total | | | | | | | 14,799,546 | | |

See Accompanying Notes to Financial Statements.

13

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Health Care – (continued) | |

| Nursing Homes – 1.3% | |

| CO Health Facilities Authority | |

| | | American Housing Foundation I, Inc.,

Series 2003 A,

8.500% 12/01/31 | | | 895,000 | | | | 956,612 | | |

| IA Finance Authority | |

| | | Care Initiatives,

Series 1998 B:

5.500% 07/01/08

5.750% 07/01/28 | | | 510,000

4,500,000 | | | | 519,971

4,552,515 | | |

| IA Marion | |

| | | Health Care Facilities Revenue,

Series 2003,

6.500% 01/01/29 | | | 200,000 | | | | 208,716 | | |

| MA Development Finance Agency | |

| | | AHF/Woodlawn Manor, Inc.:

Series 2000 A,

7.750% 12/01/27(b) | | | 2,397,000 | | | | 958,800 | | |

| | | Series 2000 B,

10.250% 06/01/27(b)(c) | | | 742,783 | | | | 22,283 | | |

| MA Industrial Finance Agency | |

| | | First Mortgage GF/Massachusetts, Inc.,

Series 1994,

8.300% 07/01/23 | | | 10,800,000 | | | | 10,714,248 | | |

| PA Chester County Industrial Development Authority | |

| | | Pennsylvania Nursing Home,

Series 2002,

8.500% 05/01/32 | | | 6,330,000 | | | | 6,624,978 | | |

| PA Delaware County Industrial Development Authority | |

| | | Care Institute-Main Line LLC,

Series 2005,

9.000% 08/01/31 | | | 8,395,000 | | | | 6,796,508 | | |

| PA Washington County Industrial Development Authority | |

| | | AHF Project,

Series 2003,

7.750% 01/01/29 | | | 2,218,000 | | | | 2,337,461 | | |

| TN Metropolitan Government Nashville & Davidson County Health & Education Board | |

| | | AHF Project,

Series 2003,

7.750% 01/01/29 | | | 508,000 | | | | 535,361 | | |

| | Nursing Homes Total | | | | | | | 34,227,453 | | |

| Health Care Total | | | | | | | | | 247,719,526 | | |

| Housing – 3.1% | |

| Assisted Living/Senior – 0.3% | |

| DE Kent County | |

| | | Heritage at Dover,

Series 1999, AMT,

7.625% 01/01/30 | | | 1,640,000 | | | | 1,530,743 | | |

| MN Roseville | |

| | | Care Institute, Inc.,

Series 1993,

7.750% 11/01/23 | | | 3,275,000 | | | | 2,878,234 | | |

See Accompanying Notes to Financial Statements.

14

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Housing – (continued) | |

| Assisted Living/Senior – (continued) | |

| NC Medical Care Commission | |

| | | DePaul Community Facilities, Inc.,

Series 1999,

7.625% 11/01/29 | | | 2,060,000 | | | | 2,170,951 | | |

| NY Suffolk County Industrial Development Agency | |

| | | Gurwin-Jewish Phase II,

Series 2004,

6.700% 05/01/39 | | | 900,000 | | | | 983,358 | | |

| | Assisted Living/Senior Total | | | | | | | 7,563,286 | | |

| Multi-Family – 2.2% | |

| CA ABAG Finance Authority for Nonprofit Corps. | |

| | | Northbay Properties II LP,

Series 2000 A, AMT,

6.400% 08/15/30(d) | | | 5,000,000 | | | | 5,165,850 | | |

| | | Winterland San Francisco,

Series 2000 B,

6.250% 08/15/30(d) | | | 2,000,000 | | | | 2,066,260 | | |

| FL Broward County Housing Finance Authority | |

| | | Chaves Lake Apartments Ltd.,

Series 2000 A, AMT,

7.500% 07/01/40 | | | 7,925,000 | | | | 8,456,292 | | |

| | | Cross Keys Apartments,

Series 1998 A, AMT,

5.750% 10/01/28 | | | 985,000 | | | | 1,010,768 | | |

| FL Capital Trust Agency | |

| | | Atlantic Housing Foundation, Inc.,

Series 2005 C,

5.875% 01/01/28 | | | 2,000,000 | | | | 2,051,460 | | |

| FL Clay County Housing Finance Authority | |

| | | Breckenridge Commons Ltd.,

Series 2000 A, AMT,

7.450% 07/01/40 | | | 3,900,000 | | | | 4,137,120 | | |

| MA Housing Finance Agency | |

| | | Series 2004 A, AMT,

Insured: FSA

5.250% 07/01/25 | | | 10,000,000 | | | | 10,359,600 | | |

| MD Economic Development Corp. | |

| | | Collegiate Housing Foundation,

Series 1999 A,

6.000% 06/01/30 | | | 3,000,000 | | | | 3,125,670 | | |

| MN Minneapolis | |

| | | Riverplace Project,

Series 1987 A,

7.100% 01/01/20 | | | 20,000 | | | | 20,267 | | |

| MN Washington County Housing & Redevelopment Authority | |

| | | Cottages of Aspen,

Series 1992, AMT,

9.250% 06/01/22 | | | 1,830,000 | | | | 1,868,759 | | |

| MN White Bear Lake | |

| | | Birch Lake Townhomes:

Series 1989 A,

9.750% 07/15/19 | | | 2,385,000 | | | | 2,262,173 | | |

| | | Series 1989 B,

(a) 07/15/19 | | | 265,000 | | | | 74,200 | | |

See Accompanying Notes to Financial Statements.

15

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Housing – (continued) | |

| Multi-Family – (continued) | |

| MO St. Louis Area Housing Finance Corp. | |

| | | Wellington Arms III,

Series 1979,

7.375% 01/01/21(e) | | | 1,598,790 | | | | 1,614,170 | | |

| NC Housing Finance Agency | |

| | | Series 1994 F,

Insured: FHA

6.600% 07/01/17 | | | 355,000 | | | | 355,586 | | |

| NC Medical Care Commission | |

| | | ARC Project,

Series 2004 A,

5.800% 10/01/34 | | | 1,400,000 | | | | 1,528,856 | | |

| NY New York City Housing Development Corp. | |

| | | Series 2005 F-1,

4.650% 11/01/25 | | | 5,000,000 | | | | 5,154,500 | | |

| Resolution Trust Corp. | |

| | | Pass-Through Certificates,

Series 1993 A,

8.500% 12/01/16(f) | | | 6,615,223 | | | | 6,604,241 | | |

| | Multi-Family Total | | | | | | | 55,855,772 | | |

| Single-Family – 0.6% | |

| CA Housing Finance Authority | |

| | | Series 1984 B,

(a) 08/01/16 | | | 275,000 | | | | 95,945 | | |

| CO El Paso County School District No. 11 | |

| | | Series 1988 A, AMT,

Insured: GNMA

8.375% 03/25/19 | | | 119,209 | | | | 121,544 | | |

| CO Housing Finance Authority | |

| | | Series 1996 B-1, AMT,

7.650% 11/01/26 | | | 60,000 | | | | 60,971 | | |

| FL Brevard County | |

| | | Series 1985,

Insured: FGIC

(a) 04/01/17 | | | 430,000 | | | | 153,519 | | |

| FL Lee County Housing Finance Authority | |

| | | Series 1998 A-2, AMT,

Insured: GNMA

6.300% 03/01/29 | | | 135,000 | | | | 136,382 | | |

| IL Chicago | |

| | | Series 1997 A, AMT,

Insured: GNMA

7.250% 09/01/28 | | | 30,000 | | | | 30,872 | | |

| LA Jefferson Parish Home Mortgage Authority | |

| | | Series 1999 B-1, AMT,

Insured: GNMA

6.750% 06/01/30 | | | 420,000 | | | | 420,025 | | |

| MA Housing Finance Agency | |

| | | Series 1992 21, AMT,

7.125% 06/01/25 | | | 665,000 | | | | 665,818 | | |

| | Series 1992, AMT,

Insured: AMBAC

7.125% 06/01/25 | | | 220,000 | | | | 220,279 | | |

See Accompanying Notes to Financial Statements.

16

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Housing – (continued) | |

| Single-Family – (continued) | |

| MD Community Development Administration Department of Housing & Community Development | |

| | | Series 2006 B, AMT,

4.900% 09/01/37 | | | 5,000,000 | | | | 5,123,400 | | |

| ME Housing Authority | |

| | | Series 2006 D, AMT,

4.950% 11/15/31 | | | 2,075,000 | | | | 2,139,782 | | |

| MO Housing Development Commission | |

| | | Series 2006, AMT,

Insured: GNMA

4.750% 09/01/21 | | | 1,000,000 | | | | 1,023,670 | | |

| NC Housing Finance Agency | |

| | | Series 1998, AMT,

5.250% 03/01/17 | | | 295,000 | | | | 303,859 | | |

| NM Mortgage Finance Authority | |

| | | Series 1997 C-2, AMT,

Insured: GNMA

6.050% 07/01/28 | | | 405,000 | | | | 412,687 | | |

| | Series 1999 D-2, AMT,

Insured: GNMA

6.750% 09/01/29 | | | 1,135,000 | | | | 1,157,814 | | |

| | | Series 2000 A-2, AMT,

Insured: FHA

7.100% 09/01/30 | | | 265,000 | | | | 272,910 | | |

| OH Housing Finance Agency | |

| | | Series 1997 A-1, AMT,

Insured: GNMA

6.050% 09/01/17 | | | 290,000 | | | | 298,500 | | |

| OK Housing Finance Agency | |

| | | Series 1999 B-1,

Insured: GNMA

6.800% 09/01/16 | | | 165,000 | | | | 169,582 | | |

| OR Department of Housing & Community Services | |

| | | Series 1998 A,

5.150% 07/01/15 | | | 35,000 | | | | 35,929 | | |

| WA Housing Finance Commission | |

| | | Series 2006 3A, AMT,

Insured: GNMA

5.000% 12/01/37 | | | 3,000,000 | | | | 3,080,970 | | |

| | Single-Family Total | | | | | | | 15,924,458 | | |

| Housing Total | | | | | | | | | 79,343,516 | | |

| Industrials – 2.4% | |

| Food Products – 0.5% | |

| FL Hendry County Industrial Development Authority | |

| | | Savannah Foods & Industries,

Series 1992, AMT,

6.400% 03/01/17 | | | 1,500,000 | | | | 1,518,690 | | |

| MI Strategic Fund | |

| | | Imperial Holly Corp.:

Series 1998 A,

6.250% 11/01/15 | | | 2,250,000 | | | | 2,324,385 | | |

See Accompanying Notes to Financial Statements.

17

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Industrials – (continued) | |

| Food Products – (continued) | |

| | Series 1998 B,

6.450% 11/01/25 | | | 3,500,000 | | | | 3,588,060 | | |

| | | Series 1998 C, AMT,

6.550% 11/01/25 | | | 4,250,000 | | | | 4,349,280 | | |

| | Food Products Total | | | | | | | 11,780,415 | | |

| Forest Products & Paper – 0.5% | |

| FL Escambia County Environmental Improvement Revenue | |

| | | International Paper Co.,

Series 2003 A, AMT,

5.750% 11/01/27 | | | 2,750,000 | | | | 2,933,810 | | |

| IA Cedar Rapids | |

| | | Weyerhaeuser Co.,

Series 1984,

9.000% 08/01/14 | | | 1,000,000 | | | | 1,258,290 | | |

| MS Lowndes County | |

| | | Weyerhaeuser Co.,

Series 1992,

6.800% 04/01/22 | | | 2,470,000 | | | | 3,023,576 | | |

| SC Georgetown County | |

| | | International Paper Co.,

Series 2000 A,

5.950% 03/15/14 | | | 4,000,000 | | | | 4,411,680 | | |

| SC Richland County | |

| | | International Paper Co.,

Series 2003, AMT,

6.100% 04/01/23 | | | 1,000,000 | | | | 1,093,440 | | |

| | Forest Products & Paper Total | | | | | | | 12,720,796 | | |

| Manufacturing – 0.6% | |

| AL McIntosh Industrial Development Board | |

| | | CIBA Specialty Chemicals,

Series 1998,

5.375% 06/01/28 | | | 1,000,000 | | | | 1,022,950 | | |

| IL Will-Kankakee Regional Development Authority | |

| | | Flanders Corp.,

Series 1997, AMT,

6.500% 12/15/17 | | | 2,220,000 | | | | 2,263,912 | | |

| KS Wichita Airport Authority | |

| | | Cessna Citation Service Center,

Series 2002 A, AMT,

GTY AGMT: Textron, Inc.

6.250% 06/15/32 | | | 5,000,000 | | | | 5,368,000 | | |

| MN Alexandria Industrial Development | |

| | | Seluemed LLP,

Series 1998, AMT,

5.850% 03/01/18 | | | 830,000 | | | | 832,772 | | |

| MO Development Finance Board | |

| | | Procter & Gamble Co.,

Series 1999, AMT,

5.200% 03/15/29 | | | 4,385,000 | | | | 5,022,316 | | |

See Accompanying Notes to Financial Statements.

18

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Industrials – (continued) | |

| Manufacturing – (continued) | |

| MO St. Louis Industrial Development Authority | |

| | | Anheuser-Busch Companies, Inc.,

Series 1991,

6.650% 05/01/16 | | | 1,400,000 | | | | 1,698,914 | | |

| | Manufacturing Total | | | | | | | 16,208,864 | | |

| Metals & Mining – 0.0% | |

| NV Department of Business & Industry | |

| | | Wheeling-Pittsburgh Steel Corp.,

Series 1999 A, AMT,

8.000% 09/01/14(f) | | | 1,030,000 | | | | 1,076,607 | | |

| | Metals & Mining Total | | | | | | | 1,076,607 | | |

| Oil & Gas – 0.5% | |

| NJ Middlesex County Pollution Control Authority | |

| | | Amerada Hess Corp.,

Series 2004,

6.050% 09/15/34 | | | 1,140,000 | | | | 1,256,189 | | |

| TN Maury County Industrial Development Board | |

| | | Occidental Petroleum Corp.,

Series 2001 A, AMT,

6.250% 08/01/18 | | | 4,000,000 | | | | 4,354,040 | | |

| TX Texas City Industrial Development Corp. | |

| | | BP Pipelines N.A., Inc.,

Series 1990,

7.375% 10/01/20 | | | 2,000,000 | | | | 2,632,460 | | |

| VI Virgin Islands Public Finance Authority | |

| | | Hovensa LLC,

Series 2003, AMT,

6.125% 07/01/22 | | | 2,975,000 | | | | 3,309,241 | | |

| | Oil & Gas Total | | | | | | | 11,551,930 | | |

| Other Industrial Development Bonds – 0.3% | |

| MI Strategic Fund Obligation Ltd. | |

| | | NSF International,

Series 2004,

5.250% 08/01/26 | | | 600,000 | | | | 630,228 | | |

| NJ Economic Development Authority | |

| | | GMT Realty LLC,

Series 2006 B, AMT,

6.875% 01/01/37 | | | 7,000,000 | | | | 7,138,180 | | |

| | Other Industrial Development Bonds Total | | | | | | | 7,768,408 | | |

| Industrials Total | | | | | | | | | 61,107,020 | | |

| Other – 19.8% | |

| Other – 0.0% | |

| PR Commonwealth of Puerto Rico Government Development Bank | |

| | | Series 2006 B,

5.000% 12/01/15 | | | 1,100,000 | | | | 1,192,169 | | |

| | Other Total | | | | | | | 1,192,169 | | |

See Accompanying Notes to Financial Statements.

19

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Pool/Bond Bank – 1.0% | |

| FL Municipal Loan Council | |

| | | Series 2000 A,

Insured: MBIA

(a) 04/01/21 | | | 1,000,000 | | | | 549,530 | | |

| MA Water Pollution Abatement Trust | |

| | | Series 1999 A,

6.000% 08/01/17 | | | 10,000,000 | | | | 12,000,000 | | |

| | | Series 2006,

5.250% 08/01/24(e) | | | 4,000,000 | | | | 4,656,680 | | |

| MI Municipal Bond Authority | |

| | | Series 1991 C,

Insured: FSA

(a) 06/15/15 | | | 3,380,000 | | | | 2,428,327 | | |

| | | Series 2001,

5.250% 10/01/19 | | | 1,000,000 | | | | 1,068,920 | | |

| OH Water Development Authority | |

| | | Water Pollution Control,

Series 2005 B,

4.750% 06/01/25 | | | 5,000,000 | | | | 5,260,650 | | |

| | Pool/Bond Bank Total | | | | | | | 25,964,107 | | |

| Refunded/Escrowed(g) – 18.0% | |

| AK Anchorage | |

| | | Ice Rink Revenue,

Series 1998,

Pre-refunded 07/01/10,

6.250% 01/01/12 | | | 1,430,000 | | | | 1,500,542 | | |

| AL Phoenix County Industrial Development Board | |

| | | Mead Coated Board, Inc.,

Series 1998 B,

Pre-refunded 04/01/08,

5.250% 04/01/28 | | | 6,750,000 | | | | 7,016,085 | | |

| AZ Maricopa County Industrial Development Authority | |

| | | Single Family,

Series 1984,

Escrowed to Maturity,

(a) 02/01/16 | | | 4,500,000 | | | | 3,157,650 | | |

| | | Windsor Housing,

Series 1996 A,

Escrowed to Maturity,

6.625% 07/01/26 | | | 2,750,000 | | | | 2,811,957 | | |

| AZ Pima County Industrial Development Authority | |

| | | Series 1989, AMT,

Escrowed to Maturity,

8.200% 09/01/21 | | | 12,370,000 | | | | 16,925,129 | | |

| AZ Tucson & Pima Counties Industrial Development Authority | |

| | | Series 1983 A,

Escrowed to Maturity,

(a) 12/01/14 | | | 5,000,000 | | | | 3,700,050 | | |

See Accompanying Notes to Financial Statements.

20

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| CA Department of Water Resources | |

| | | Series 2002 A,

Pre-refunded 05/01/12:

5.125% 05/01/18 | | | 2,500,000 | | | | 2,727,375 | | |

| | Insured: AMBAC

5.375% 05/01/18 | | | 1,000,000 | | | | 1,103,210 | | |

| CA Foothill Eastern Transportation Corridor Agency | |

| | | Series 1995 A,

Escrowed to Maturity,

(a) 01/01/18 | | | 10,000,000 | | | | 6,418,400 | | |

| CA Morgan Hill Unified School District | |

| | | Series 2002,

Insured: FGIC

(a) 08/01/22 | | | 3,345,000 | | | | 1,743,983 | | |

| CA Palmdale Community Redevelopment Agency | |

| | | Series 1986 A, AMT,

Escrowed to Maturity,

Insured: FHA

8.000% 03/01/16 | | | 3,000,000 | | | | 4,008,300 | | |

| | | Series 1986 D, AMT,

Escrowed to Maturity,

Insured: MBIA

8.000% 04/01/16 | | | 7,000,000 | | | | 9,370,550 | | |

| CA Perris Community Facilities District | |

| | | Series 1991 2-90,

Escrowed to Maturity,

8.750% 10/01/21 | | | 6,165,000 | | | | 9,514,999 | | |

| CA Pomona | |

| | | Series 1990 A,

Escrowed to Maturity,

Insured: GNMA

7.600% 05/01/23 | | | 9,710,000 | | | | 12,753,891 | | |

| CA Riverside County | |

| | | Series 1998, AMT,

Escrowed to Maturity,

Insured: GNMA

8.300% 11/01/12 | | | 10,000,000 | | | | 12,389,400 | | |

| CA San Francisco Bay Area Rapid Transit District | |

| | | Series 1999,

Pre-refunded 07/01/09,

5.500% 07/01/26(h) | | | 10,000,000 | | | | 10,609,600 | | |

| CO El Paso County School District No. 11 | |

| | | Series 1996:

7.100% 12/01/18

7.125% 12/01/20 | | | 2,000,000

7,350,000 | | | | 2,552,000

9,380,437 | | |

| CO Health Facilities Authority | |

| | | Catholic Health Initiatives,

Series 2002 A,

Escrowed to Maturity,

5.000% 03/01/11 | | | 1,350,000 | | | | 1,423,292 | | |

| CO Highlands Ranch Metropolitan District No. 2 | |

| | | Series 1996,

Escrowed to Maturity,

Insured: FSA

6.500% 06/15/12 | | | 530,000 | | | | 607,444 | | |

See Accompanying Notes to Financial Statements.

21

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| CO Mesa County | |

| | | Series 1992,

Escrowed to Maturity,

(a) 12/01/11 | | | 5,905,000 | | | | 4,903,394 | | |

| CT Health & Educational Facility Authority | |

| | | Series 2000 A,

Pre-refunded 07/01/10,

6.000% 07/01/25 | | | 3,260,000 | | | | 3,553,041 | | |

| DC Hospital Revenue | |

| | | Medlantic Healthcare,

Series 1997 A,

Escrowed to Maturity,

Insured: MBIA

5.375% 08/15/15 | | | 9,000,000 | | | | 9,284,400 | | |

| FL Highlands County Health Facilities Authority | |

| | | Adventist Health Systems,

Series 2003 D,

Pre-refunded 11/15/13,

5.375% 11/15/35 | | | 3,450,000 | | | | 3,817,218 | | |

| FL Jacksonville Transportation Authority | |

| | | Series 1985,

Escrowed to Maturity,

9.200% 01/01/15 | | | 2,000,000 | | | | 2,591,360 | | |

| FL Melbourne | |

| | | Series 2000 A,

Escrowed to Maturity,

Insured: FGIC

(a) 10/01/19 | | | 600,000 | | | | 362,706 | | |

| FL Mid-Bay Bridge Authority | |

| | | Series 1991 A,

Escrowed to Maturity,

6.875% 10/01/22 | | | 2,000,000 | | | | 2,655,400 | | |

| FL Orange County Health Facilities Authority | |

| | | Orlando Regional Healthcare System:

Series 1996 A,

Escrowed to Maturity,

Insured: MBIA

6.250% 10/01/16 | | | 2,120,000 | | | | 2,531,110 | | |

| | | Series 1999 E,

Pre-refunded 10/01/09,

6.000% 10/01/26 | | | 145,000 | | | | 155,565 | | |

| Series 1996 A, | | Escrowed to Maturity,

Insured: MBIA

6.250% 10/01/16 | | | 55,000 | | | | 65,071 | | |

| FL Orlando Utilities Commission Water & Electric Revenue | |

| | | Series 1989 D,

Escrowed to Maturity,

6.750% 10/01/17 | | | 3,750,000 | | | | 4,520,475 | | |

See Accompanying Notes to Financial Statements.

22

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| FL Seminole County | |

| | | Series 1992,

Escrowed to Maturity,

Insured: MBIA

6.000% 10/01/19 | | | 1,030,000 | | | | 1,218,099 | | |

| FL Tampa Bay Water Utility Systems | |

| | | Series 1999,

Pre-refunded 10/01/11,

5.750% 10/01/29(h) | | | 3,000,000 | | | | 3,290,760 | | |

| GA Forsyth County Hospital Authority | |

| | | Baptist Health Care System,

Series 1998,

Escrowed to Maturity,

6.000% 10/01/08 | | | 325,000 | | | | 334,217 | | |

| GA Fulton County Water & Sewer | |

| | | Series 1992,

Insured: FGIC

6.375% 01/01/14 | | | 19,080,000 | | | | Escrowed to Maturity,

21,592,264 | | |

| GA Municipal Electric Authority | |

| | | Series 1991,

Escrowed to Maturity,

Insured: MBIA:

6.600% 01/01/18

6.600% 01/01/18 | | | 420,000

3,600,000 | | | | 498,422

4,342,752 | | |

| | Series 1998 Y:

Escrowed to Maturity,

Insured: AMBAC

6.400% 01/01/13 | | | 55,000 | | | | 61,843 | | |

| | | Pre-refunded 01/01/11,

Insured: AMBAC

6.400% 01/01/13 | | | 10,000 | | | | 11,076 | | |

| ID Health Facilities Authority | |

| | | IHC Hospitals, Inc.,

Series 1992,

Escrowed to Maturity,

6.650% 02/15/21 | | | 6,000,000 | | | | 7,795,620 | | |

| IL Chicago Metropolitan Water Reclamation District-Greater Chicago | |

| | | Series 1993,

Escrowed to Maturity,

5.500% 12/01/12 | | | 3,000,000 | | | | 3,271,860 | | |

| IL Educational Facilities Authority | |

| | | Educational Advancement Fund, Inc.,

Series 2002,

Pre-refunded 05/01/12,

6.625% 05/01/17 | | | 4,500,000 | | | | 5,207,760 | | |

| IL Glendale Heights | |

| | | Series 1985 B,

Escrowed to Maturity,

7.100% 12/01/15 | | | 1,440,000 | | | | 1,668,845 | | |

See Accompanying Notes to Financial Statements.

23

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| IL Metropolitan Pier & Exposition Authority | |

| | | Series 1993 A,

Escrowed to Maturity,

Insured: FGIC

(a) 06/15/13 | | | 8,750,000 | | | | 6,853,262 | | |

| | Series 1996,

Escrowed to Maturity,

Insured: MBIA

(a) 06/15/12 | | | 2,655,000 | | | | 2,160,958 | | |

| IN Health Facility Financing Authority | |

| | | Daughters of Charity Health,

Series 1997 D,

Pre-refunded 11/01/07,

5.000% 11/01/26(d) | | | 3,195,000 | | | | 3,235,001 | | |

| MA College Building Authority | |

| | | Series 1999 A,

Escrowed to Maturity,

Insured: MBIA:

(a) 05/01/19

(a) 05/01/20 | | | 7,710,000

7,750,000 | | | | 4,708,728

4,531,037 | | |

| MA Port Authority | |

| | | Series 1999 C,

Pre-refunded 01/01/10,

5.750% 07/01/29(h) | | | 5,000,000 | | | | 5,366,600 | | |

| MA Turnpike Authority | |

| | | Series 1993 A,

Escrowed to Maturity:

5.000% 01/01/20 | | | 3,610,000 | | | | 3,972,408 | | |

| | Insured: FGIC:

5.000% 01/01/20

5.125% 01/01/23 | | | 12,665,000

3,600,000 | | | | 13,936,439

4,131,180 | | |

| MI Cornell Township Economic Development Corp. | |

| | | Mead Corp.,

Series 2002,

Pre-refunded 05/01/12,

5.875% 05/01/18 | | | 1,000,000 | | | | 1,113,150 | | |

| MI State | |

| | | 525 Redevco, Inc.,

Series 2000,

Escrowed to Maturity,

Insured: AMBAC

(a) 06/01/21 | | | 6,000,000 | | | | 3,297,660 | | |

| MN Dakota & Washington Counties Housing & Redevelopment Authority | |

| | | Series 1988, AMT,

Escrowed to Maturity,

Insured: GNMA

8.150% 09/01/16 | | | 235,000 | | | | 317,090 | | |

| MN Higher Education Facilities Authority | |

| | | College Art & Design,

Series 2000 5-D,

Pre-refunded 05/01/10,

6.750% 05/01/26 | | | 500,000 | | | | 537,230 | | |

| MN Moorhead | |

| | | Series 1979,

Escrowed to Maturity,

Insured: FHA

7.100% 08/01/11 | | | 20,000 | | | | 21,748 | | |

See Accompanying Notes to Financial Statements.

24

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| MN Robbinsdale Economic Development Authority | |

| | | Series 1999 A,

Pre-refunded 01/01/10,

6.875% 01/01/26 | | | 250,000 | | | | 273,528 | | |

| MN University of Minnesota | |

| | | Series 1996 A,

Escrowed to Maturity,

5.500% 07/01/21 | | | 1,000,000 | | | | 1,172,800 | | |

| MN Western Minnesota Municipal Power Agency | |

| | | Series 1983 A,

Escrowed to Maturity,

Insured: MBIA

9.750% 01/01/16 | | | 1,000,000 | | | | 1,439,960 | | |

| NC Eastern Municipal Power Agency | |

| | | Series 1987 A,

Pre-refunded 01/01/22,

4.500% 01/01/24 | | | 1,750,000 | | | | 1,870,417 | | |

| | Series 1991 A,

Escrowed to Maturity:

5.000% 01/01/21

6.500% 01/01/18 | | | 8,735,000

5,815,000 | | | | 9,759,790

7,272,413 | | |

| NC Lincoln County | |

| | | Lincoln County Hospital,

Series 1991,

Escrowed to Maturity,

9.000% 05/01/07 | | | 105,000 | | | | 107,219 | | |

| NE Omaha Public Power District | |

| | | Series 1992 B,

Escrowed to Maturity,

6.200% 02/01/17 | | | 1,600,000 | | | | 1,870,960 | | |

| NJ Highway Authority | |

| | | Series 1971,

Escrowed to Maturity,

6.500% 01/01/11 | | | 571,000 | | | | 600,789 | | |

| NJ Transportation Trust Fund Authority | |

| | | Series 1995 B,

Escrowed to Maturity,

Insured: MBIA

7.000% 06/15/12 | | | 10,135,000 | | | | 11,863,119 | | |

| NJ Turnpike Authority | |

| | | Series 1991 C,

Escrowed to Maturity,

Insured: MBIA

6.500% 01/01/16 | | | 11,000,000 | | | | 12,943,700 | | |

| | | Series 2005 C,

Escrowed to Maturity,

Insured: MBIA

6.500% 01/01/16 | | | 965,000 | | | | 1,135,516 | | |

| NV Henderson | |

| | | Catholic Healthcare West,

Series 1999 A,

Pre-refunded 07/01/10,

6.750% 07/01/20 | | | 3,680,000 | | | | 4,095,030 | | |

See Accompanying Notes to Financial Statements.

25

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| NY New York City Municipal Water Finance Authority | |

| | | Series 1999 A,

Pre-refunded 06/15/09,

5.500% 06/15/32(h) | | | 10,000,000 | | | | 10,581,300 | | |

| NY Triborough Bridge & Tunnel Authority | |

| | | Series 1992 Y,

Escrowed to Maturity,

6.125% 01/01/21 | | | 14,000,000 | | | | 17,313,380 | | |

| | Series 1992,

Escrowed to Maturity,

Insured: CAP

6.125% 01/01/21 | | | 7,000,000 | | | | 8,656,690 | | |

| OH Cleveland-Cuyahoga County Port Authority | |

| | | Oglebay Norton Co.,

Series 1997, AMT,

Escrowed to Maturity,

6.000% 03/01/07 | | | 115,000 | | | | 115,555 | | |

| OH Hilliard School District | |

| | | Series 1995 A,

Escrowed to Maturity,

Insured: FGIC

(a) 12/01/12 | | | 2,505,000 | | | | 2,008,985 | | |

| PA Cambria County Industrial Development Authority | |

| | | Beverly Enterprises,

Series 1987,

Escrowed to Maturity,

10.000% 06/18/12 | | | 900,000 | | | | 1,070,145 | | |

| PA Convention Center Authority | |

| | | Series 1989 A,

Escrowed to Maturity,

Insured: FGIC

6.000% 09/01/19 | | | 14,010,000 | | | | 16,931,365 | | |

| PA Pottstown Boro Authority | |

| | | Sewer Revenue,

Series 1991,

Escrowed to Maturity,

Insured: FGIC

(a) 11/01/16 | | | 1,000,000 | | | | 681,850 | | |

| PA Westmoreland County Municipal Authority | |

| | | Series 2000 A,

Escrowed to Maturity,

Insured: FGIC

(a) 08/15/23 | | | 5,000,000 | | | | 2,315,800 | | |

| PR Commonwealth of Puerto Rico Public Finance Corp. | |

| | | Series 2002 E,

Escrowed to Maturity,

6.000% 08/01/26 | | | 230,000 | | | | 295,125 | | |

| SC Piedmont Municipal Power Agency | |

| | | Series 1991 A,

Escrowed to Maturity,

Insured: FGIC

6.125% 01/01/07 | | | 75,000 | | | | 75,162 | | |

| | | Series 1993,

Escrowed to Maturity:

Insured: AMBAC

(a) 01/01/13 | | | 9,800,000 | | | | 7,440,258 | | |

See Accompanying Notes to Financial Statements.

26

Columbia Tax-Exempt Fund

November 30, 2006

| Municipal Bonds – (continued) | |

| | | | | Par ($) | | Value ($) | |

| Other – (continued) | |

| Refunded/Escrowed(g) – (continued) | |

| | Insured: MBIA

5.375% 01/01/25 | | | 3,960,000 | | | | 4,712,044 | | |

| | | Series 1998,

Escrowed to Maturity:

Insured: AMBAC