Securities Act File No. 333-[ ]

As filed with the Securities and Exchange Commission on August 14, 2019

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

| | | | |

| REGISTRATION STATEMENT | | | | |

UNDER

THE SECURITIES ACT OF 1933 | | ☒ | | |

| Pre-Effective Amendment No. | | ☐ | | |

| Post-Effective Amendment No. | | ☐ | | |

TRANSAMERICA SERIES TRUST

(Exact Name of Registrant as Specified in Charter)

1801 California Street, Suite 5200

Denver, CO 80202

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: 1-888-233-4339

Rhonda A. Mills, Esq.,

1801 California Street, Suite 5200

Denver, CO 80202

(Name and Address of Agent for Service)

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective.

Title of Securities Being Registered: Initial Class and Service Class shares of beneficial interest, no par value, of Transamerica JPMorgan Asset Allocation - Moderate VP; and Initial Class and Service Class shares of beneficial interest, no par value, of Transamerica JPMorgan Asset Allocation - Conservative VP.

It is proposed that this filing will become effective on September 13, 2019 pursuant to Rule 488 under the Securities Act of 1933.

No filing fee is required because an indefinite number of shares has previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940, as amended

The information in this Information Statement/Prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Information Statement/Prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION,

DATED AUGUST 14, 2019

COMBINED INFORMATION STATEMENT

OF

TRANSAMERICA SERIES TRUST

on behalf of its Series:

TRANSAMERICA MADISON CONSERVATIVE ALLOCATION VP

TRANSAMERICA MADISON BALANCED ALLOCATION VP

AND

PROSPECTUS

OF

TRANSAMERICA SERIES TRUST

on behalf of its Series:

TRANSAMERICA JPMORGAN ASSET ALLOCATION—CONSERVATIVE VP

TRANSAMERICA JPMORGAN ASSET ALLOCATION—MODERATE VP

The address and telephone number of each Portfolio is:

1801 California Street, Suite 5200

Denver, CO 80202

(Toll free) 1-800-851-9777

Transamerica Series Trust

1801 California Street, Suite 5200

Denver, CO 80202

[______], 2019

Dear Policyowner:

The Board of your Transamerica portfolio has approved the reorganization of your portfolio into another Transamerica portfolio. The reorganization is expected to occur on or about November [1], 2019. Upon completion of the reorganization, you will become a holder of the destination Transamerica portfolio, and you will receive shares of the destination portfolio equal in value to your shares of your current Transamerica portfolio.

The reorganization does not require holder approval, and you are not being asked to vote. We do, however, ask that you review the enclosed combined Information Statement/Prospectus, which contains information about the destination portfolio, including its investment objective, strategies, risks, performance, fees and expenses.

The Board of your portfolio has unanimously approved your portfolio’s reorganization and believes the reorganization is in the best interests of your portfolio and its shareholders.

If you have any questions, please call 1-800-851-9777 between 8 a.m. and 5 p.m., Eastern Time, Monday through Friday. Thank you for your investment in the Transamerica funds.

|

| Sincerely, |

|

| /s/ Marijn P. Smit |

| Marijn P. Smit |

| Chairman of the Board, President and Chief Executive Officer |

COMBINED INFORMATION STATEMENT

OF

TRANSAMERICA SERIES TRUST

on behalf of its Series:

TRANSAMERICA MADISON CONSERVATIVE ALLOCATION VP

TRANSAMERICA MADISON BALANCED ALLOCATION VP

(each, a “Target Portfolio” and together, the “Target Portfolios”)

AND

PROSPECTUS

OF

TRANSAMERICA SERIES TRUST

on behalf of its Series:

TRANSAMERICA JPMORGAN ASSET ALLOCATION—CONSERVATIVE VP

TRANSAMERICA JPMORGAN ASSET ALLOCATION—MODERATE VP

(each, a “Destination Portfolio” and together, the “Destination Portfolios”)

The address and telephone number of each Portfolio is:

1801 California Street, Suite 5200

Denver, CO 80202

(Toll free) 1-800-851-9777

Shares of the Destination Portfolios have not been approved or disapproved by the Securities and Exchange Commission (the “SEC”). The SEC has not passed upon the accuracy or adequacy of this Information Statement/Prospectus. Any representation to the contrary is a criminal offense.

An investment in any Target Portfolio or Destination Portfolio (each sometimes referred to herein as a “Portfolio”) is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money by investing in the Portfolios.

This Information Statement/Prospectus sets forth information about the Destination Portfolios that an investor ought to know before investing. Please read this Information Statement/Prospectus carefully before investing and keep it for future reference.

1

INTRODUCTION

This combined information statement and prospectus, dated [September 13], 2019 (the “Information Statement/Prospectus”), is being furnished in connection with the reorganizations (each, a “Reorganization,” and together the “Reorganizations”) of certain series of Transamerica Series Trust, a Delaware statutory trust (each, a “Target Portfolio,” and together the “Target Portfolios”), into certain other series of Transamerica Series Trust (each, a “Destination Portfolio,” and together the “Destination Portfolios”). The Information Statement/Prospectus is being mailed to Target Portfolio holders on or about [September 13], 2019.

Each Target Portfolio and Destination Portfolio is a series of Transamerica Series Trust (“TST”), an open-end management investment company organized as a Delaware statutory trust.

The Board of Trustees of TST (the “Board” or the “Trustees”) has determined that each Reorganization is in the best interests of the applicable Target Portfolio and corresponding Destination Portfolio. A copy of the form of Agreement and Plan of Reorganization (the “Plan”) for the Reorganizations is attached to this Information Statement/Prospectus as Exhibit A.

THIS INFORMATION STATEMENT/PROSPECTUS IS FOR INFORMATIONAL PURPOSES ONLY, AND YOU DO NOT NEED TO DO ANYTHING IN RESPONSE TO RECEIVING IT. WE ARE NOT ASKING YOU FOR A PROXY OR WRITTEN CONSENT, AND YOU ARE REQUESTED NOT TO SEND US A PROXY OR WRITTEN CONSENT.

The following table indicates (a) the Target Portfolio and the corresponding Destination Portfolio involved in each Reorganization, (b) the classes of Destination Portfolio shares that each applicable Target Portfolio holder will receive in exchange for the respective classes of Target Portfolio shares, and (c) on what page of this Information Statement/Prospectus the discussion regarding each Reorganization begins. The Reorganizations are numbered for convenience. The consummation of each Reorganization is not contingent on the consummation of the other Reorganization.

| | | | | | |

Reorganization | | Target Portfolios & Shares | | Destination Portfolios & Shares | | Page |

| 1 | | Transamerica Madison Conservative Allocation VP | | Transamerica JPMorgan Asset Allocation—Conservative VP | | 10 |

| | Initial Class* Service Class | | Initial Class Service Class | | |

| 2 | | Transamerica Madison Balanced Allocation VP | | Transamerica JPMorgan Asset Allocation—Moderate VP | | 26 |

| | Initial Class* Service Class | | Initial Class Service Class | | |

* Transamerica Madison Conservative Allocation VP and Transamerica Madison Balanced Allocation VP do not currently offer Initial Class shares.

Please read this Information Statement/Prospectus, including Exhibit A, carefully. Although each Reorganization is similar in structure, you should read carefully the specific discussion regarding your Target Portfolio’s Reorganization.

The date of this Information Statement/Prospectus is [September 13], 2019

2

For more complete information about each Portfolio, please read the Portfolio’s prospectus and statement of additional information, as they may be amended and/or supplemented. Each Portfolio’s prospectus and statement of additional information, and other additional information about each Portfolio, has been filed with the SEC (http://www.sec.gov) and is available upon oral or written request and without charge. See “Where to Get More Information” below.

| | |

| Where to Get More Information | | |

| Each Portfolio’s current prospectus and statement of additional information, including any applicable supplements thereto. | | On file with the SEC (http://www.sec.gov) (File Nos. 033-00507; 811-04419) and available at no charge by calling the Portfolios’ toll-free number: 1-800-851-9777 or visiting the Portfolios’ website at http://www.transamericaseriestrust.com/content/prospectus.aspx. |

| |

| Each Portfolio’s most recent annual and semi–annual reports to holders. | | On file with the SEC (http://www.sec.gov) (File No. 811-04419) and available at no charge by calling the Portfolios’ toll-free number: 1-800-851-9777 or by visiting the Portfolios’ website at http://www.transamericaseriestrust.com/content/prospectus.aspx. |

| |

| A statement of additional information for this Information Statement/Prospectus, dated [September 13], 2019 (the “SAI”). The SAI contains additional information about the Target Portfolios and the Destination Portfolios. | | On file with the SEC (http://www.sec.gov) (File No. [_________]) and available at no charge by calling the Portfolios’ toll-free number: 1-800-851-9777 or by visiting the Portfolios’ website at http://www.transamericaseriestrust.com/content/prospectus.aspx. The SAI is incorporated by reference into this Information Statement/Prospectus. |

| |

| To ask questions about this Information Statement/Prospectus. | | Call the following toll-free telephone number: 1-800-851-9777. |

The Target Portfolios’ prospectus, dated May 1, 2019, as supplemented, and statement of additional information dated May 1, 2019, as supplemented (File Nos. 033-00507 and 811-04419), are incorporated by reference into this Information Statement/Prospectus.

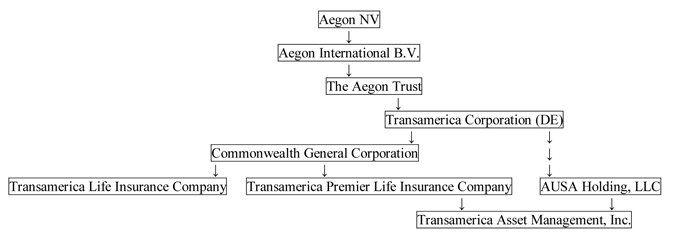

Shares of the Portfolios are not offered directly to the public but are sold only to (1) insurance companies and their separate accounts as the underlying investment medium for owners (each a “Policyowner,” collectively, “Policyowners”) of variable annuity contracts and variable life policies (collectively, the “Policies”) and (2) certain asset allocation portfolios that are series of TST (the “Asset Allocation Portfolios”). As such, Transamerica Life Insurance Company (“TLIC”), Transamerica Financial Life Insurance Company (“TFLIC”), Transamerica Premier Life Insurance Company (“TPLIC”) and Transamerica Advisors Life Insurance Company (“TALIC”) (collectively, the “Insurance Companies”) and certain Asset Allocation Portfolios are the only shareholders of the investment portfolios offered by TST. The Insurance Companies each offer the opportunity to invest in the Portfolios through their respective products.

Policyowners are not shareholders of the Portfolios. For ease of reference, throughout the Information Statement/Prospectus, shareholders and Policyowners may collectively be referred to as “shareholders” of the Portfolios.

TST has agreed to provide information to Policyowners invested in each Target Portfolio in connection with a Reorganization of that Portfolio into the applicable Destination Portfolio.

You have received this Information Statement/Prospectus because you own a Policy of one of these Insurance Companies and that Policy is invested in a Target Portfolio.

3

TABLE OF CONTENTS

4

QUESTIONS AND ANSWERS

For your convenience, we have provided a brief overview of the Reorganizations. Additional information is contained elsewhere in this Information Statement/Prospectus and the Agreement and Plan of Reorganization relating to each Reorganization, which is attached to this Information Statement/Prospectus as Exhibit A. Shareholders should read this entire Information Statement/Prospectus, including Exhibit A and Exhibit B, and the Destination Portfolios’ prospectus carefully for more complete information.

How Will the Reorganizations Work?

| | • | | Each Target Portfolio will transfer all of its property and assets to the corresponding Destination Portfolio. In exchange, each Destination Portfolio will assume all of the liabilities of the corresponding Target Portfolio and issue shares, as described below. |

| | • | | For each Reorganization, the Destination Portfolio will issue a number of its shares of the applicable class to the corresponding Target Portfolio on the closing date of the Reorganization (the “Closing Date”) having an aggregate net asset value equal to the aggregate net asset value of such Target Portfolio’s corresponding classes of shares, respectively. |

| | • | | Shares of the classes of the applicable Destination Portfolio corresponding to classes of the corresponding Target Portfolio will then be distributed on the Closing Date to the corresponding Target Portfolio’s shareholders in complete liquidation of the Target Portfolio in proportion to the relative net asset value of their holdings of the applicable classes of shares of the Target Portfolio. Therefore, on the Closing Date, upon completion of the applicable Reorganization, each Target Portfolio shareholder will hold shares of the applicable Destination Portfolio corresponding in class to, and having the same aggregate net asset value as, the Target Portfolio shares held by that shareholder immediately prior to the Reorganization. The net asset value attributable to each class of shares of the Target Portfolio will be determined using the Target Portfolio’s valuation policies and procedures and the net asset value attributable to a class of shares of a Destination Portfolio will be determined using the Destination Portfolio’s valuation policies and procedures. The portfolio assets of each Target Portfolio and corresponding Destination Portfolio are valued using the same valuation policies and procedures. |

| | • | | Each Target Portfolio will be terminated after the Closing Date. |

| | • | | The consummation of each Reorganization is not contingent on the consummation of the other Reorganization. |

| | • | | No sales load, contingent deferred sales charge, commission, redemption fee or other transactional fee will be charged as a result of the Reorganizations. Following a Reorganization, shareholders of the applicable Target Portfolio will be subject to the fees and expenses of the corresponding Destination Portfolio which, as is further discussed in this Information Statement/Prospectus, could be higher than those of the Target Portfolio. |

| | • | | Following the Reorganizations, (i) Transamerica Asset Management, Inc. (“TAM”) will continue to act as investment manager to each Destination Portfolio; and (ii) J.P. Morgan Investment Management, Inc. will continue to act as sub-adviser to the Destination Portfolios in Reorganization 1 and Reorganization 2. |

| | • | | The exchange of Target Portfolio shares for Destination Portfolio shares in a Reorganization is generally not expected to result in income, gain or loss being recognized for federal income tax purposes by an exchanging shareholder. Each Reorganization will generally not result in the recognition of gain or loss for federal income tax purposes by the applicable Target Portfolio or Destination Portfolio. |

Why did the Trustees Approve the Reorganizations?

The Board of the Target Portfolios, including all of the Trustees who are not “interested” persons (as defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of the Portfolios, TAM or Transamerica Capital, Inc. (“TCI”), the Portfolios’ distributor (the “Independent Trustees”), after careful consideration, has determined that the Reorganizations are in the best interests of the Target Portfolios and will not dilute the interests of the existing shareholders of the Target Portfolios. The Board also serves as the Board of each corresponding Destination Portfolio. The Board, including all of the Independent Trustees, approved the Reorganizations with respect to each Destination Portfolio. The Board determined that the Reorganizations are in the best interests of the Destination Portfolios and that the interests of the Destination Portfolios’ shareholders will not be diluted as a result of the Reorganizations.

5

In approving the Reorganizations of the Target Portfolios, the Board considered, among other things: (i) the similarities between the Portfolios’ investment objectives and strategies, (ii) the larger combined asset base resulting from the Reorganizations will offer the potential for greater operating efficiencies and economies of scale and eliminate redundancies in the Transamerica product line, (iii) the management fee of each Destination Portfolio following the Reorganizations will remain the same and will be lower than the management fee of each Target Portfolio, (iv) the fact that the net expense ratio of each class of each Destination Portfolio following the Reorganizations is expected to be lower than the current net expense ratio of the corresponding class of either Portfolio prior to the Reorganizations, (v) the anticipated tax treatment of each Reorganization as a “reorganization” within the meaning of Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”), and (vi) the generally better performance of the Destination Portfolios as compared to the Target Portfolios. See “Reasons for the Proposed Reorganization” for additional information regarding the Board’s considerations.

How do the Target Portfolios and the Destination Portfolios compare?

There are similarities between the Portfolios, as well as certain differences, including:

Reorganization 1: Transamerica Madison Conservative Allocation VP and Transamerica JPMorgan Asset Allocation – Conservative VP

| | • | | Investment Manager, Sub-Advisers and Portfolio Managers. Each Portfolio is managed by TAM. Madison Asset Management, LLC (“Madison”) serves as the sub-adviser to the Target Portfolio. David S. Hottmann and Patrick F. Ryan are portfolio managers responsible for the day-to-day management of the Target Portfolio. J.P. Morgan Investment Management Inc. (“JPMorgan”) serves as the sub-adviser to the Destination Portfolio. Michael Feser, Jeff Geller and Grace Koo are portfolio managers responsible for the day-to-day management of the Destination Portfolio. |

| | • | | Investment Objective. The investment objectives of the Portfolios are identical. Each Portfolio’s investment objective seeks current income and preservation of capital. |

| | • | | Investment Strategy. Both Portfolios expect to allocate assets among underlying portfolios with the goal of achieving exposure targets over time. Even though the investment strategies of the Target Portfolio and the Destination Portfolio are similar, there are differences in investment strategies. For example, the Target Portfolio is managed against a 30% target equity allocation and may allocate between 10% and 46% of assets to equity securities, whereas the Destination Portfolio is managed against a 35% target equity allocation and may allocate between zero and 50% of assets to equity securities. |

The Target Portfolio is subject to volatility constraints. Based on these constraints and the level of volatility of the equity markets, the sub-adviser may increase equity exposure to approximately 46% or may decrease equity exposure to approximately 10%. Notwithstanding the constraints, the Target Portfolio’s sub-adviser may elect to allocate fewer assets to equity underlying portfolio when it believes it is advisable to do so. The Destination Portfolio’s exposure is subject to its multifactor risk management framework, which incorporates quantitative models and signals. Under this framework, the Destination Portfolio’s maximum equity exposure may be limited in response to individual asset class momentum signals and a portfolio level volatility signal. Notwithstanding its equity target and any maximum equity exposure limit imposed under the risk management framework, the Destination Portfolio’s sub-adviser may elect to allocate fewer assets to equities and more assets to fixed income when it believes it is advisable to do so. The constraints of each Portfolio may result in the Portfolio not achieving its stated asset mix goal.

The Target Portfolio’s allocation to high yield bonds will not normally exceed 5% of the portfolio’s assets. The Destination Portfolio’s exposure to high yield bonds and floating rate loans together generally will not exceed 10% of its net assets.

The Target Portfolio may invest up to 10% of its assets in exchange-traded funds (“ETFs”) to gain exposure to asset classes or sectors not otherwise accessible through the underlying portfolios in which it otherwise invests. The Destination Fund does not utilize ETFs as part of its principal investment strategy.

The Target Portfolio does not utilize derivatives as part of its principal investment strategies. The Destination Portfolio may invest in derivatives instruments, such as options, futures or forward contracts and swaps, through its investments in underlying portfolios. The Destination Portfolio also may, but is not required to, invest in derivative instruments such as futures contracts for a variety of purposes, consistent with the Portfolio’s investment objective and other policies.

6

The Target Portfolio seeks to achieve the portfolio’s investment objective by investing its assets primarily in shares of underlying mutual funds advised by Madison and TAM-managed mutual funds. The Destination Portfolio currently seeks to achieve the portfolio’s investment objective by investing its assets in a broad mix of underlying TAM-managed mutual funds. Upon the closing of the Reorganization, the Destination Portfolio will seek to achieve the portfolio’s investment objective by investing its assets in a broad mix of underlying TAM-managed mutual funds and other unaffiliated funds, including Madison-advised funds.

| | • | | Principal Risks. The Target Portfolio and the Destination Portfolio are subject to a number of common principal risks, including active trading, allocation conflicts, asset allocation, commodities and commodity-related securities, convertible securities, counterparty, credit, currency, cybersecurity, derivatives, equity securities, extension, fixed-income securities, foreign investments, growth stocks, high-yield debt securities, interest rate, investments in affiliated portfolios, legal and regulatory, leveraging, liquidity, management, market, model and data, prepayment or call, real estate securities, REITs, small and medium capitalization companies, underlying portfolios, valuation and value investing. An investment in the Target Portfolio is also subject to money market funds risk, mortgage-related and asset-backed securities risk, underlying exchange-traded funds risk and volatility constraints risk. An investment in the Destination Portfolio is also subject to asset class variation risk, currency hedging risk, emerging markets risk, floating rate loans risk, focused investing risk, frontier markets risk, loans risk, preferred stock risk, risk management framework risk, short positions risk, sovereign debt risk and U.S. Government agency obligations risk. |

| | • | | Performance. JPMorgan began sub-advising the Destination Portfolio on July 1, 2016. As of March 31, 2019, the Destination Portfolio outperformed the Target Portfolio in the period since July 1, 2016. |

| | • | | Management Fee. The management fee schedule of the Destination Portfolio is lower than the management fee schedule of the Target Portfolio. |

| | • | | Total Operating Expenses. Following the Reorganization, the net expense ratio of each class of the combined Destination Portfolio is expected to be lower than the net expense ratio of the corresponding class of the Target Portfolio. |

Reorganization 2: Transamerica Madison Balanced Allocation VP and Transamerica JPMorgan Asset Allocation – Moderate VP

| | • | | Investment Manager, Sub-Advisers and Portfolio Managers. Each Portfolio is managed by TAM. Madison Asset Management, LLC (“Madison”) serves as the sub-adviser to the Target Portfolio. David S. Hottmann and Patrick F. Ryan are portfolio managers responsible for the day-to-day management of the Target Portfolio. J.P.Morgan Investment Management Inc. (“JPMorgan”) serves as the sub-adviser to the Destination Portfolio. Michael Feser, Jeff Geller and Grace Koo are portfolio managers responsible for the day-to-day management of the Destination Portfolio. |

| | • | | Investment Objective. The investment objectives of the Portfolios are identical. Each Portfolio’s investment objective seeks capital appreciation and current income. |

| | • | | Investment Strategy. Both Portfolios expect to allocate assets among underlying portfolios with the goal of achieving exposure targets over time. Even though the investment strategies of the Target Portfolio and the Destination Portfolio are similar, there are differences in investment strategies. For example, both the Target Portfolio and the Destination Portfolio are managed against a 50% equity target allocation, but the Target Portfolio may allocate between 30% and 66% of assets to equity securities whereas the Destination Portfolio may allocate between 15% and 70% of assets to equity securities. |

The Target Portfolio is subject to volatility constraints. Based on these constraints and the level of volatility of the equity markets, the sub-adviser may increase equity exposure to approximately 46% or may decrease equity exposure to approximately 10%. Notwithstanding the constraints, the Target Portfolio’s sub-adviser may elect to allocate fewer assets to equity underlying portfolio when it believes it is advisable to do so. The Destination Portfolio expects to allocate its assets among underlying portfolios with the goal of achieving exposure targets over time of approximately 50% of its net assets in equities, which may include stocks and real estate securities, and approximately 50% of its net assets in fixed income, which may include bonds, cash equivalents and other debt securities. Subject to the Destination Portfolio’s multi-factor risk management framework, the Destination Portfolio’s sub-adviser may increase equity exposure to approximately 70% of net assets or may decrease equity exposure to approximately 15%, and may increase fixed income exposure to approximately 85% of net assets or may decrease fixed income exposure to approximately 30% of net assets. Notwithstanding its equity target and any maximum equity exposure limit imposed under the risk management framework, the Destination Portfolio’s sub-adviser may elect to allocate fewer assets to equities and more assets to fixed income when it believes it is advisable to do so. The constraints of each Portfolio may result in the Portfolio not achieving its stated asset mix goal.

7

The Target Portfolio’s allocation to high yield bonds will normally not exceed 5% of the portfolio’s assets. The Destination Portfolio’s exposure to high yield bonds and floating rate loans together generally will not exceed 10% of its net assets.

The Target Portfolio may invest up to 10% of its assets in ETFs to gain exposure to asset classes or sectors not otherwise accessible through the underlying portfolios in which it otherwise invests. The Destination Portfolio does not utilize ETFs as part of its principal investment strategy.

The Target Portfolio does not utilize derivatives as part of its principal investment strategies. The Destination Portfolio may invest in derivatives instruments, such as options, futures or forward contracts and swaps, through its investments in underlying portfolios. The Destination Portfolio also may, but is not required to, invest in derivative instruments such as futures contracts for a variety of purposes, consistent with the Portfolio’s investment objective and other policies.

The Target Portfolio seeks to achieve the portfolio’s investment objective by investing its assets primarily in shares of underlying mutual funds advised by Madison and TAM-managed mutual funds. The Destination Portfolio currently seeks to achieve the portfolio’s investment objective by investing its assets in a broad mix of underlying TAM-managed mutual funds. Upon the closing of the Reorganization, the Destination Portfolio will seek to achieve the portfolio’s investment objective by investing its assets in a broad mix of underlying TAM-managed mutual funds and other unaffiliated funds, including Madison-advised funds.

| | • | | Principal Risks. The Target Portfolio and the Destination Portfolio are subject to a number of common principal risks, including active trading, allocation conflicts, asset allocation, commodities and commodity-related securities, convertible securities, counterparty, credit, currency, cybersecurity, derivatives, equity securities, extension, fixed-income securities, foreign investments, growth stocks, high-yield debt securities, interest rate, investments in affiliated portfolios, legal and regulatory, leveraging, liquidity, management, market, model and data, prepayment or call, real estate securities, REITs, small and medium capitalization companies, underlying portfolios, valuation and value investing. An investment in the Target Portfolio is also subject to money market funds risk, mortgage-related and asset-backed securities risk, underlying exchange-traded funds risk and volatility constraints risk. An investment in the Destination Portfolio is also subject to asset class variation risk, currency hedging risk, emerging markets risk, floating rate loans risk, focused investing risk, frontier markets risk, loans risk, preferred stock risk, risk management framework risk, short positions risk, sovereign debt risk and U.S. Government agency obligations risk. |

| | • | | Performance. JPMorgan began sub-advising the Destination Portfolio on July 1, 2016. As of March 31, 2019, the Destination Portfolio outperformed the Target Portfolio in the period since July 1, 2016. |

| | • | | Management Fee. The management fee schedule of the Destination Portfolio is lower than the management fee schedule of the Target Portfolio. |

| | • | | Total Operating Expenses. Following the Reorganization, the net expense ratio of each class of the combined Destination Portfolio is expected to be lower than the net expense ratio of the corresponding class of the Target Portfolio. |

Am I being asked to vote on anything?

Shareholder approval of the Reorganizations is not required. The Trust’s Declaration of Trust and state law governing the Trust do not require shareholder approval for fund reorganizations. Likewise, Rule 17a-8 under the 1940 Act does not require shareholder approval of reorganizations involving affiliated funds, so long as certain criteria are met. Because these criteria are met in this case, shareholder approval is not required for the Reorganizations.

Who Bears the Expenses Associated with the Reorganizations?

It is anticipated that the total cost of preparing, printing and mailing this Information Statement/Prospectus will range from approximately $55,000 to $65,000 for each Reorganization. The costs associated with each Reorganization will be borne by TAM.

8

What are the Federal Income Tax Consequences of the Reorganizations?

As a condition to the closing of each Reorganization, the applicable Target Portfolio and corresponding Destination Portfolio must receive an opinion of Morgan, Lewis & Bockius LLP to the effect that the Reorganization will constitute a “reorganization” within the meaning of Section 368 of the Code. Accordingly, it is expected that neither you nor the applicable Destination Portfolio nor, in general, the applicable Target Portfolio will recognize gain or loss as a direct result of the Reorganization of your Target Portfolio, and that the aggregate tax basis of the Destination Portfolio shares that you receive in the applicable Reorganization will equal the aggregate tax basis of the Target Portfolio shares that you surrender in that Reorganization. However, in order to maintain its qualification for tax treatment as a regulated investment company and avoid portfolio-level taxes, each Target Portfolio will declare and pay a distribution to its shareholders shortly before the applicable Reorganization that, together with all previous dividends for the taxable year, is intended to have the effect of distributing all of its realized net capital gains (taking into account available capital loss carryforwards), if any, all of its investment company taxable income (computed without regard to the dividends-paid deduction), if any, and all of its net tax-exempt income, if any, for the taxable year ending on the Closing Date. If you hold shares in a Target Portfolio when it makes such a distribution, the distribution may change the amount, timing and character of taxable income that you realize in respect of your Target Portfolio shares as compared to the amount, timing and character of income you would have realized had the applicable Reorganization not occurred. The corresponding Destination Portfolio may make a comparable distribution to its shareholders shortly before the applicable Reorganization. In addition, following the applicable Reorganization, the corresponding Destination Portfolio will declare and pay to its shareholders, for the taxable year in which the Reorganization occurs, a distribution of any remaining income and gains from such taxable year. All such distributions generally will be taxable to the shareholders, but as long as the Policies funded by the Target Portfolios or by the corresponding Destination Portfolios qualify to be treated as annuity contracts or life insurance policies under the Code, such distributions will not be currently taxable to the Policyowners and the Reorganizations should not otherwise result in any tax liability to the Policyowners. For more information, see “Tax Status of Each Reorganization” in this Information Statement/Prospectus.

9

REORGANIZATION 1

TRANSAMERICA MADISON CONSERVATIVE ALLOCATION VP

(the “Target Portfolio”)

TRANSAMERICA JPMORGAN ASSET ALLOCATION—CONSERVATIVE VP

(the “Destination Portfolio”)

Summary

The following is a summary of more complete information appearing later in this Information Statement/Prospectus or incorporated herein. You should read carefully the entire Information Statement/Prospectus, including the exhibits, which include additional information that is not included in the summary and is a part of this Information Statement/Prospectus. Exhibit A is the form of Agreement and Plan of Reorganization. For a discussion of the terms of the Agreement and Plan of Reorganization, please see the section entitled “Terms of the Agreement and Plan of Reorganization” in the back of this Information Statement/Prospectus, after the discussion of the Reorganizations.

In the Reorganization, the Destination Portfolio will issue a number of its Initial Class shares and a number of its Service Class shares to the Target Portfolio having aggregate net asset values equal to the respective aggregate net asset values of the Target Portfolio’s Initial Class and Service Class shares. Although the Target Portfolio has registered Initial Class shares, it does not currently offer Initial Class shares.

The consummation of the Reorganization is not contingent on the consummation of the other Reorganization.

Both the Target Portfolio and the Destination Portfolio are managed by TAM. The Target Portfolio is sub-advised by Madison Asset Management, LLC (“Madison”) and the Destination Portfolio is sub-advised by J.P. Morgan Investment Management Inc. (“JPMorgan”). The Target Portfolio and Destination Portfolio have identical investment objectives, and similar principal investment strategies and policies, and related risks. The tables below provide a comparison of certain features of the Portfolios. In the tables below, if a row extends across the entire table, the information disclosed applies to both the Destination Portfolio and the Target Portfolio.

Comparison of Transamerica Madison Conservative Allocation VP

and Transamerica JPMorgan Asset Allocation—Conservative VP

| | | | | | |

| | | Target Portfolio | | Destination Portfolio |

| | | Transamerica Madison Conservative Allocation VP | | Transamerica JPMorgan Asset Allocation—Conservative VP |

| Investment Objective | | Seeks current income and preservation of capital |

| | |

| Principal investment strategies | | The portfolio’s sub-adviser, Madison (the “sub-adviser”), seeks to achieve the portfolio’s investment objective by investing its assets primarily in shares of underlying mutual funds advised by the sub-adviser and TAM-managed mutual funds (the “underlying portfolios”). Although actual allocations may vary, the portfolio’s asset allocation among asset classes is expected to be within the following ranges: | | The portfolio’s sub-adviser, JPMorgan (the “sub-adviser”), currently seeks to achieve the portfolio’s investment objective by primarily investing its assets in a broad mix of underlying Transamerica funds (“underlying portfolios”). The portfolio expects to allocate its assets among underlying portfolios with the goal of achieving exposure targets over time of approximately 35% of its net assets in equities, which may include stocks and real estate securities, and approximately 65% of its net assets in fixed income, which may include bonds, cash equivalents and other debt securities. The actual percentage allocations at any time may vary. The sub-adviser may increase equity exposure to approximately 50% of net assets or may decrease equity exposure to zero, and may increase fixed income exposure to approximately 100% of net assets or may decrease fixed income exposure to approximately 50% of net assets, subject to the portfolio’s multi-factor risk management framework. The risk management framework incorporates quantitative models and signals. Under this framework, the portfolio’s maximum equity exposure may be limited in response to individual asset class momentum signals and a portfolio level volatility signal. Notwithstanding the portfolio’s equity target and any maximum equity exposure limit imposed under the risk management framework, the sub-adviser may elect to allocate fewer |

| | 0% to 5% 39% to 90% 0% to 5% 10% to 46% 0% to 11% 0% to 5% | | money market funds; debt securities (e.g., bond funds and convertible bond funds); below-investment grade debt securities (e.g., high income funds); equity securities (e.g., U.S. stock funds); foreign securities (e.g., international stock and bond funds); and alternative asset classes (e.g., real estate investment trust funds, natural resources funds and precious metal funds). |

10

| | | | |

| | | Target Portfolio | | Destination Portfolio |

| | | Transamerica Madison Conservative Allocation VP | | Transamerica JPMorgan Asset Allocation—Conservative VP |

| | The portfolio’s allocation to high yield bonds will normally not exceed 5% of the portfolio’s assets. | | assets to equities and more assets to fixed income when it believes it is advisable to do so. The portfolio may not achieve its stated asset mix goal. |

| | The portfolio is subject to volatility constraints. Based on these constraints and the level of volatility of the equity markets, the sub-adviser may increase equity exposure to approximately 46% or may decrease equity exposure to approximately 10%. Notwithstanding the constraints, the sub-adviser may elect to allocate fewer assets to equity underlying portfolio when it believes it is advisable to do so. The constraints may result in the portfolio not achieving its stated asset mix goal. Each underlying portfolio has its own investment objective, principal investment strategies and investment risks. The sub-adviser for each underlying portfolio decides which securities to purchase and sell for that underlying portfolio. The portfolio’s ability to achieve its investment objective depends largely on the performance of the underlying portfolios in which it invests. The “Underlying Portfolios” section of the prospectus lists the underlying portfolios currently available for investment by the portfolio, provides a summary of their respective investment objectives and principal investment strategies, and identifies certain risks of the underlying portfolios. It is not possible to predict the extent to which the portfolio will be invested in a particular underlying portfolio at any time. The portfolio may be a significant shareholder in certain underlying portfolios. The sub-adviser may change the portfolio’s asset allocations and underlying portfolios at any time without notice to shareholders and without shareholder approval. The sub-adviser may invest up to 10% of the portfolio’s assets in ETFs to gain exposure to asset classes or sectors not otherwise accessible through the underlying mutual funds in which the portfolio otherwise invests. | | In seeking to achieve the investment objective of the portfolio, the sub-adviser employs an investment process consisting of four integrated components: strategic asset allocation, underlying strategy and portfolio selection, active asset allocation and the multifactor risk management framework. For the first three components, the sub-adviser’s portfolio management team draws on the analysis produced by dedicated research and strategy teams who support the investment process by generating qualitative and quantitative research and insights on the underlying portfolios TAM has designated as available for investment by the portfolio. For the fourth component, the portfolio management team draws on the output of its multi-factor risk management framework, which is a quantitative driven process that makes asset class allocation recommendations and may impose a maximum equity exposure limit and require equity exposure reductions based on a set of individual asset class momentum signals and a portfolio level volatility signal. As part of its investment process, the sub-adviser selects underlying equity and fixed income portfolios to invest in from the underlying portfolios TAM has designated as available for investment by the portfolio and rebalances the portfolio’s assets among the selected underlying portfolios. The underlying portfolios include portfolios sub-advised by the sub-adviser. Consistent with the portfolio’s objective and strategies, the sub-adviser is permitted to invest any portion of the portfolio’s assets in underlying portfolios which it sub-advises. When choosing among potential underlying portfolios the sub-adviser faces a conflict of interest, because it will receive additional fees when it selects underlying portfolios for which it also acts as sub-adviser. For more information on the sub-adviser’s conflicts of interest, see Appendix B – “Portfolio Managers” to the SAI. |

| | |

| | | | Exposure to high yield bonds (commonly known as “junk bonds”) and floating rate loans together generally will not exceed 10% of the portfolio’s net assets. Junk bonds are high-risk debt securities rated below investment grade (that is, securities rated below BBB by Standard & Poor’s or Fitch or below Baa by Moody’s or, if unrated, determined to be of comparable quality by the portfolio’s sub-adviser). Each underlying portfolio has its own investment objective, principal investment strategies and investment risks. The sub-adviser for each underlying portfolio decides which securities to purchase and sell for that underlying portfolio. The portfolio’s ability to achieve its investment objective depends largely on the performance of the underlying portfolios in which it invests. The “Underlying Portfolios” section of the prospectus lists the underlying portfolios currently available for investment by the portfolio, provides a summary of their respective investment objectives and principal investment strategies, and identifies certain risks of the underlying portfolios. It is not possible to predict the extent to which the portfolio will be invested in a particular underlying portfolio at any time. The portfolio may be a significant shareholder in certain underlying portfolios. The portfolio may have exposure to derivatives instruments, such as options, futures or forward contracts and swaps through its investments in the underlying portfolios. The portfolio also may, but is not required to, invest in derivative instruments such as futures contracts for a variety of purposes, including as a means to manage equity and fixed income exposure (including for purposes of complying with the risk management framework) without having to purchase or sell underlying portfolios and to increase the portfolio’s return as a non-hedging strategy that may be considered speculative. For example, when the level of market volatility is increasing, the sub-adviser may limit the portfolio’s equity exposure by shorting or selling long futures positions on an index. It is anticipated that any derivatives usage by the portfolio would primarily involve the use of exchange-traded equity index, U.S. |

11

| | | | |

| | | Target Portfolio | | Destination Portfolio |

| | | Transamerica Madison Conservative Allocation VP | | Transamerica JPMorgan Asset Allocation—Conservative VP |

| | |

| | | | Treasury and currency futures, but the portfolio also could utilize other types of derivatives. The use of derivatives may be deemed to involve the use of leverage because the portfolio is not required to invest the full market value of the contract upon entering into the contract but participates in gains and losses on the full contract price and because the portfolio’s use of derivative instruments may result in its exposure exceeding 100% of portfolio value. The portfolio may maintain a significant percentage of its assets in cash and cash equivalent instruments, some of which may serve as margin for the portfolio’s obligations under derivatives transactions. The portfolio may also invest in unaffiliated funds. The sub-adviser may change the portfolio’s asset allocations and underlying portfolios at any time without notice to shareholders and without shareholder approval. |

| Investment manager | | TAM |

| | |

| Sub–adviser | | Madison | | JPMorgan |

| | |

| Portfolio managers | | David S. Hottmann, CFA – Portfolio Manager since 2011 Patrick F. Ryan, CFA – Portfolio Manager since 2011 | | Michael Feser, CFA – Portfolio Manager since 2016 Jeff Geller, CFA – Portfolio Manager since 2016 Grace Koo – Portfolio Manager since 2016 |

| |

| | The Portfolios’ statement of additional information provides additional information about the portfolio manager(s)’ compensation, other accounts managed by the portfolio manager(s), and the portfolio manager(s)’ ownership of securities in the Portfolios. |

| Net assets (as of April 30, 2019) | | $63,647,967 | | $1,295,993,948 |

Classes of Shares, Fees and Expenses

| | | | |

| | | Target Portfolio | | Destination Portfolio |

| | | Transamerica Madison Conservative Allocation VP | | Transamerica JPMorgan Asset Allocation—Conservative VP |

| |

| Initial Class sales charges and fees | | Initial Class shares are offered without an initial sales charge and are not subject to a contingent deferred sales charge. Initial Class shares can have up to a maximum Rule 12b-1 fee equal to an annual rate of 0.15% (expressed as a percentage of average daily net assets of the Portfolio), but TST does not intend to pay any distribution fees for Initial Class shares through May 1, 2020. TST reserves the right to pay such fees after that date. |

| Service Class sales charges and fees | | Service Class shares are offered without an initial sales charge and are not subject to a contingent deferred sales charge. Service Class shares have a maximum Rule 12b–1 fee equal to an annual rate of 0.25% (expressed as a percentage of average daily net assets of the Portfolio), which is used to pay distribution and service fees for the sale and distribution of the Portfolio’s shares and to pay for non–distribution activities and services provided to shareholders. These services include compensation to financial intermediaries that sell Portfolio shares and/or service shareholder accounts. |

| Management fees | | TAM receives compensation, calculated daily and paid monthly, from the Target Portfolio at an annual rate (expressed as a specified percentage of the Portfolio’s average daily net assets) of 0.18. | | TAM receives compensation, calculated daily and paid monthly, from the Destination Portfolio at an annual rate (expressed as a specified percentage of the Portfolio’s average daily net assets) of 0.1225% of the first $10 billion; and 0.1025% in excess of $10 billion. |

| Fee waiver and expense limitations | | TAM has contractually undertaken through May 1, 2020 to pay expenses on behalf of the portfolio to the extent normal operating expenses (including investment advisory fees but excluding, as applicable, 12b-1 fees, acquired fund fees and expenses, interest, taxes, brokerage commissions, dividend and interest expenses on securities sold short, extraordinary expenses and other expenses not incurred in the ordinary course of the portfolio’s business) exceed, as a percentage of the portfolio’s average daily net assets, 0.35% for Initial Class shares and 0.60% for Service Class shares. TAM is entitled to reimbursement by the portfolio of fees waived or expenses reduced during any of the previous 36 months if on any day or month the estimated annualized portfolio operating expenses are less than the cap. | | TAM has contractually undertaken through May 1, 2020 to pay expenses on behalf of the portfolio to the extent normal operating expenses (including investment advisory fees but excluding, as applicable, 12b-1 fees, acquired fund fees and expenses, interest, taxes, brokerage commissions, dividend and interest expenses on securities sold short, extraordinary expenses and other expenses not incurred in the ordinary course of the portfolio’s business) exceed, as a percentage of the portfolio’s average daily net assets, 0.25% for Initial Class shares and 0.50% for Service Class shares. TAM is entitled to reimbursement by the portfolio of fees waived or expenses reduced during any of the previous 36 months if on any day or month the estimated annualized portfolio operating expenses are less than the cap. |

| |

| | For a comparison of the gross and net expenses of the Portfolios, please see the class fee tables in “The Portfolios’ Fees and Expenses” below. |

12

Comparison of Principal Risks of Investing in the Portfolios

Because the Portfolios have the same investment objectives and similar principal investment strategies and policies, they are subject to similar principal risks. Risk is inherent in all investing. The value of your investment in a Portfolio, as well as the amount of return you receive on your investment, may fluctuate significantly from day to day and over time. You may lose part or all of your investment in a Portfolio or your investment may not perform as well as other similar investments.

Your primary risk in investing in the Portfolios is you could lose money. You should carefully assess the risks associated with an investment in the Portfolios.

The following is a description of certain principal risks of investing in each Portfolio. Additional principal risks of the Portfolios are discussed later in this section.

| | • | | Market – The value of the portfolio’s securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates or currency rates, lack of liquidity in the markets or adverse investor sentiment. Adverse market conditions may be prolonged and may not have the same impact on all types of securities. The value of securities also may go down due to events or conditions that affect particular sectors, industries or issuers. If the value of the securities owned by the portfolio fall, the value of your investment will go down. The portfolio may experience a substantial or complete loss on any individual security. In the past decade, financial markets throughout the world have experienced increased volatility, depressed valuations, decreased liquidity and heightened uncertainty. Governmental and non-governmental issuers have defaulted on, or been forced to restructure, their debts. These market conditions may continue, worsen or spread. Events that have contributed to these market conditions include, but are not limited to, major cybersecurity events; geopolitical events (including wars and terror attacks); measures to address budget deficits; downgrading of sovereign debt; declines in oil and commodity prices; dramatic changes in currency exchange rates; and public sentiment. The European Union has experienced increasing stress for a variety of reasons, including economic downturns in various member countries. In June 2016, the United Kingdom voted to withdraw from the European Union, and additional members could do the same. The impact of these conditions and events is not yet known. |

There has been significant U.S. and non-U.S. government and central bank intervention in and support of financial markets during the past decade. The Federal Reserve has reduced and begun unwinding its market support activities and has begun raising interest rates. Certain foreign governments and central banks are implementing so-called negative interest rates (e.g., charging depositors who keep their cash at a bank) to spur economic growth. Further Federal Reserve or other U.S. or non-U.S. governmental or central bank actions, including interest rate increases, unwinding of quantitative easing, or contrary actions by different governments, may not work as intended, could negatively affect financial markets generally, increase market volatility, and reduce the value and liquidity of securities in which the portfolio invests.

Policy and legislative changes in the United States and in other countries are affecting many aspects of financial regulation, and may in some instances contribute to decreased liquidity and increased volatility in the financial markets. The impact of these changes on the markets, and the practical implications for market participants, may not be fully known for some time.

Economies and financial markets throughout the world are increasingly interconnected. Economic, financial or political events, trading and tariff arrangements, terrorism, natural disasters and other circumstances in one country or region could have profound impacts on global economies or markets. As a result, whether or not the portfolio invests in securities of issuers located in or with significant exposure to the countries directly affected, the value and liquidity of the portfolio’s investments may be negatively affected.

| | • | | Management – The portfolio is subject to the risk that the investment manager’s or sub-adviser’s judgments and decisions may be incorrect or otherwise may not produce the desired results, causing the value of your investment to go down. The portfolio may also suffer losses if there are imperfections, errors or limitations in the quantitative, analytic or other tools, resources, information and data used, investment techniques applied, or the analyses employed or relied on, by the investment manager or sub-adviser, if such tools, resources, information or data are used incorrectly or otherwise do not work as intended, or if the investment manager’s or sub-adviser’s investment style is out of favor or otherwise fails to produce the desired results. In addition, the portfolio’s investment strategies or policies may change from time to time. Those changes may not lead to the results intended by the investment manager or sub-adviser and could have an adverse effect on the value or performance of the portfolio. Any of these things could cause the portfolio to lose value or its results to lag relevant benchmarks or other funds with similar objectives. |

| | • | | Asset Allocation – The sub-adviser allocates the portfolio’s assets among various asset classes and underlying portfolios. These allocations may be unsuccessful in maximizing the portfolio’s return and/or avoiding investment losses, and may cause the portfolio to underperform. |

13

| | • | | Equity Securities – Equity securities represent an ownership interest in an issuer, rank junior in a company’s capital structure and consequently may entail greater risk of loss than debt securities. Equity securities include common and preferred stocks. Stock markets are volatile and the value of equity securities may go up or down sometimes rapidly and unpredictably. Equity securities may have greater price volatility than other asset classes, such as fixed income securities. The value of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions. If the market prices of the equity securities owned by the portfolio fall, the value of your investment in the portfolio will decline. If the portfolio holds equity securities in a company that becomes insolvent, the portfolio’s interests in the company will rank junior in priority to the interests of debtholders and general creditors of the company. |

| | • | | Fixed-Income Securities – The value of fixed-income securities may go up or down, sometimes rapidly and unpredictably, due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the bond markets or adverse investor sentiment. In addition, the value of a fixed-income security may decline if the issuer or other obligor of the security fails to pay principal and/or interest, otherwise defaults or has its credit rating downgraded or is perceived to be less creditworthy, or the credit quality or value of any underlying assets declines. If the value of fixed-income securities owned by the portfolio fall, the value of your investment will go down. The value of your investment will generally go down when interest rates rise. Interest rates have been at historically low levels in the U.S., so the portfolio faces a heightened risk that interest rates may rise. A general rise in interest rates may cause investors to move out of fixed-income securities on a large scale, which could adversely affect the price and liquidity of fixed-income securities. A rise in rates tends to have a greater impact on the prices of longer term or duration securities. |

| | • | | Foreign Investments – Investing in securities of foreign issuers or issuers with significant exposure to foreign markets involves additional risk. Foreign countries in which the portfolio may invest may have markets that are less liquid, less regulated, less transparent and more volatile than U.S. markets. The value of the portfolio’s investments may decline because of factors affecting the particular issuer as well as foreign markets and issuers generally, such as unfavorable or unsuccessful government actions, reduction of government or central bank support, political or financial instability or other adverse economic or political developments. Lack of information and weaker accounting standards also may affect the value of these securities. |

| | • | | Underlying Portfolios – Because the portfolio invests its assets in various underlying portfolios, its ability to achieve its investment objective depends largely on the performance of the underlying securities or assets held by those underlying portfolios. Each of the underlying portfolios in which the portfolio may invest has its own investment risks, and those risks can affect the value of the underlying portfolios’ shares and therefore the value of the portfolio’s investments. There can be no assurance that the investment objective of any underlying portfolio will be achieved. To the extent that the portfolio invests more of its assets in one underlying portfolio than in another, the portfolio will have greater exposure to the risks of that underlying portfolio. In addition, the portfolio will bear a pro rata portion of the operating expenses of the underlying portfolios in which it invests. The “List and Description of Underlying Portfolios” section of the portfolio’s prospectus identifies certain risks of each underlying portfolio. |

Each Portfolio is subject to the following additional principal risks (in alphabetical order):

| | • | | Active Trading – The portfolio may purchase and sell securities without regard to the length of time held. Active trading may have a negative impact on performance by increasing transaction costs. During periods of market volatility, active trading may be more pronounced. |

| | • | | Allocation Conflicts – The sub-adviser is subject to conflicts of interest in allocating the portfolio’s assets among underlying portfolios. The sub-adviser serves as sub-adviser to certain underlying portfolios in which the portfolio may invest. The sub-adviser will receive more revenue when it selects an underlying portfolio it sub-advises for inclusion in the portfolio. TAM has an incentive to include Transamerica funds, including funds sub-advised by an affiliate of TAM, as investment options for the portfolio. |

| | • | | Commodities and Commodity-Related Securities – To the extent the portfolio invests in commodities, instruments whose performance is linked to the price of an underlying commodity or commodity index or the securities of issuers in commodity-related businesses or industries, the portfolio will be subject to the risks of investing in commodities, including regulatory, economic and political developments, weather events and natural disasters and market disruptions. The portfolio’s investment exposure to the commodities markets may subject the portfolio to greater volatility. Commodities and commodity-linked investments may be less liquid than other investments. Commodity-linked investments are subject to the credit risks associated with the issuer, and their values may decline substantially if the issuer’s creditworthiness deteriorates. |

| | • | | Convertible Securities – Convertible securities are subject to risks associated with both fixed income and equity securities. When the underlying common stock falls in value, the market price of the convertible security may be more influenced by the security’s yield and fixed income characteristics. When the underlying common stock rises in value, the market price may be more influenced by the equity conversion features. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality. |

14

| | • | | Counterparty – The portfolio will be subject to credit risk with respect to counterparties to derivatives, repurchase agreements and other financial contracts entered into by the portfolio or held by special purpose or structured vehicles in which the portfolio invests. Adverse changes to counterparties (including derivatives exchanges and clearinghouses) may cause the value of financial contracts to go down. If a counterparty becomes bankrupt or otherwise fails to perform its obligations, the value of your investment in the portfolio may decline. |

| | • | | Credit – If an issuer or other obligor (such as a party providing insurance or other credit enhancement) of a security held by the portfolio or a counterparty to a financial contract with the portfolio defaults or is downgraded, or is perceived to be less creditworthy, or if the value of any underlying assets declines, the value of your investment will typically decline. A decline may be significant, particularly in certain market environments. Below investment grade, high-yield debt securities (commonly known as “junk” bonds) have a higher risk of default and are considered speculative. Subordinated securities are more likely to suffer a credit loss than non-subordinated securities of the same issuer and will be disproportionately affected by a default, downgrade or perceived decline in creditworthiness. |

| | • | | Currency – The value of investments in securities denominated in foreign currencies increases or decreases as the rates of exchange between those currencies and the U.S. dollar change. Currency conversion costs and currency fluctuations could reduce or eliminate investment gains or add to investment losses. Currency exchange rates can be volatile and may fluctuate significantly over short periods of time, and are affected by factors such as general economic conditions, the actions of the U.S. and foreign governments or central banks, the imposition of currency controls, and speculation. |

| | • | | Cybersecurity – Cybersecurity incidents may allow an unauthorized party to gain access to portfolio assets, shareholder data (including private shareholder information), and/or proprietary information, or cause the portfolio, TAM, a sub-adviser and/or the portfolio’s other service providers (including, but not limited to, fund accountants, custodians, sub-custodians, transfer agents and financial intermediaries) to suffer data breaches, data corruption or loss of operational functionality. A cybersecurity incident may disrupt the processing of shareholder transactions, impact the portfolio’s ability to calculate its net asset values, and prevent shareholders from redeeming their shares. |

| | • | | Derivatives – Using derivatives exposes the portfolio to additional or heightened risks and can increase portfolio losses and reduce opportunities for gains when market prices, interest rates, currencies, or the derivatives themselves, behave in a way not anticipated. Using derivatives may have a leveraging effect, increase portfolio volatility and not produce the result intended. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment. Even a small investment in derivatives can have a disproportionate impact on the portfolio. Derivatives may be difficult to sell, unwind or value, and the counterparty (including, if applicable, the portfolio’s clearing broker, the derivatives exchange or the clearinghouse) may default on its obligations to the portfolio. Derivatives are generally subject to the risks applicable to the assets, rates, indices or other indicators underlying the derivative. The value of a derivative may fluctuate more or less than, or otherwise not correlate well with, the underlying assets, rates, indices or other indicators to which it relates. The portfolio may be required to segregate or earmark liquid assets or otherwise cover its obligations under derivatives transactions and may have to liquidate positions before it is desirable in order to meet these segregation and coverage requirements. Use of derivatives may have different tax consequences for the portfolio than an investment in the underlying security, and those differences may affect the amount, timing and character of income distributed to shareholders. The U.S. government and foreign governments are in the process of adopting and implementing regulations governing derivatives markets, including mandatory clearing of certain derivatives, margin and reporting requirements. There may be additional regulation of the use of derivatives by registered investment companies, such as the portfolio, which could significantly affect their use. The ultimate impact of the regulations remains unclear. Additional regulation of derivatives may make derivatives more costly, limit their availability or utility, otherwise adversely affect their performance, limit portfolio investments in derivatives, or disrupt markets. For additional information regarding derivatives, see “More on Risks of Investing in the Portfolios—More on Principal Risks: Derivatives” in the prospectus. |

| | • | | Extension – When interest rates rise, repayments of fixed income securities, particularly asset- and mortgage-backed securities, may occur more slowly than anticipated, extending the effective duration of these fixed income securities at below market interest rates and causing their market prices to decline more than they would have declined due to the rise in interest rates alone. This may cause the portfolio’s share price to be more volatile or go down. |

| | • | | Growth Stocks – Returns on growth stocks may not move in tandem with returns on other categories of stocks or the market as a whole. Growth stocks typically are particularly sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations may not be met, the prices of growth securities typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market for a long period of time, for example, while the market favors “value” stocks. |

| | • | | High-Yield Debt Securities – High-yield debt securities, commonly referred to as “junk” bonds, are securities that are rated below “investment grade” or, if unrated, determined to be below investment grade by the sub-adviser. Changes in interest rates, the market’s perception of the issuers, the creditworthiness of the issuers and negative perceptions of the junk bond market generally may significantly affect the value of these bonds. Junk bonds are considered speculative, have a higher risk of default, tend to be less liquid and may be more difficult to value than higher grade securities. Junk bonds tend to be volatile and more susceptible to adverse events, credit downgrades and negative sentiments. |

15

| | • | | Interest Rate – Interest rates in the U.S. have been at historically low levels, so the portfolio faces a heightened risk that interest rates may rise. The value of fixed income securities generally goes down when interest rates rise, and therefore the value of your investment in the portfolio may also go down. Debt securities have varying levels of sensitivity to changes in interest rates. A rise in rates tends to have a greater impact on the prices of longer term or duration securities. A general rise in interest rates may cause investors to move out of fixed income securities on a large scale, which could adversely affect the price and liquidity of fixed income securities and could also result in increased redemptions from the portfolio. |

| | • | | Investments in Affiliated Portfolios – A substantial portion of the portfolio’s assets are invested in underlying Transamerica portfolios. The portfolio’s investment manager, TAM, is subject to conflicts of interest in connection with the allocation by the portfolio’s sub-adviser of the portfolio’s assets among the underlying portfolios. For example, TAM has an incentive for the sub-adviser to allocate the portfolio’s assets to those underlying portfolios paying the highest net management fees to TAM or to those underlying portfolios for which an affiliate of TAM serves as the sub-adviser. A further discussion of actual and potential conflicts of interest appears in “More on Risks of Investing in the Portfolios—More on Certain Additional Risks: Conflicts of Interest” in the prospectus and in the statement of additional information. |

| | • | | Legal and Regulatory – Legal and regulatory changes could occur that may adversely affect the portfolio, its investments, and its ability to pursue its investment strategies and/or increase the costs of implementing such strategies. New or revised laws or regulations may be imposed by the U.S. Securities and Exchange Commission, the U.S. Commodity Futures Trading Commission, the Internal Revenue Service, the U.S. Federal Reserve or other governmental regulatory authorities or self-regulatory organizations that could adversely affect the portfolio. The portfolio also may be adversely affected by changes in the enforcement or interpretation of existing statutes and rules by governmental regulatory authorities or self-regulatory organizations. |

| | • | | Leveraging – The value of your investment may be more volatile to the extent that the portfolio borrows or uses derivatives or other investments, such as ETFs, that have embedded leverage. Other risks also will be compounded because leverage generally magnifies the effect of a change in the value of an asset and creates a risk of loss of value on a larger pool of assets than the portfolio would otherwise have. The use of leverage is considered to be a speculative investment practice and may result in the loss of a substantial amount, and possibly all, of the portfolio’s assets. The portfolio also may have to sell assets at inopportune times to satisfy its obligations or meet segregation or coverage requirements. |

| | • | | Liquidity – The portfolio may make investments that are illiquid or that become illiquid after purchase. Investments may become illiquid due to the lack of an active market, a reduced number of traditional market participants, or reduced capacity of traditional market participants to make a market in securities. The liquidity and value of investments can deteriorate rapidly and those investments may be difficult or impossible for the portfolio to sell, particularly during times of market turmoil. Illiquid investments can be difficult to value, may trade at a discount from comparable, more liquid investments, and may be subject to wide fluctuations in value. As a general matter, dealers recently have been less willing to make markets for fixed income securities. If the portfolio is forced to sell an illiquid investment to meet redemption requests or other cash needs, the portfolio may be forced to sell at a loss. The portfolio may not receive its proceeds from the sale of certain securities for an extended period (for example, several weeks or even longer). |

| | • | | Model and Data – If quantitative models, algorithms or calculations (whether proprietary and developed by the sub-adviser or supplied by third parties) (“Models”) or information or data supplied by third parties (“Data”) prove to be incorrect or incomplete, any decisions made, in whole or part, in reliance thereon expose the portfolio to additional risks. Models can be predictive in nature. The use of predictive Models has inherent risks. The success of relying on or otherwise using Models depends on a number of factors, including the validity, accuracy and completeness of the Model’s development, implementation and maintenance, the Model’s assumptions, factors, algorithms and methodologies, and the accuracy and reliability of the supplied historical or other Data. Models rely on, among other things, correct and complete Data inputs. If incorrect Data is entered into even a well-founded Model, the resulting information will be incorrect. However, even if Data is input correctly, Model prices may differ substantially from market prices, especially for securities with complex characteristics. Investments selected with the use of Models may perform differently than expected as a result of the design of the Model, inputs into the Model or other factors. There also can be no assurance that the use of Models will result in effective investment decisions for the portfolio. |

| | • | | Prepayment or Call – Many issuers have a right to prepay their fixed income securities. Issuers may be more likely to prepay their securities if interest rates fall. If this happens, the portfolio will not benefit from the rise in the market price of the securities that normally accompanies a decline in interest rates and will be forced to reinvest prepayment proceeds at a time when yields on securities available in the market are lower than the yield on prepaid securities. The portfolio may also lose any premium it paid on prepaid securities. |

16

| | • | | Real Estate Securities – Investments in the real estate industry are subject to risks associated with direct investment in real estate. These risks include declines in the value of real estate, adverse general and local economic conditions, increased competition, overbuilding and changes in operating expenses, property taxes or interest rates. |

| | • | | REITs – Investing in real estate investment trusts (“REITs”) involves unique risks. When the portfolio invests in REITs, it is subject to risks generally associated with investing in real estate. A REIT’s performance depends on the types and locations of the properties it owns, how well it manages those properties and cash flow. REITs may have lower trading volumes and may be subject to more abrupt or erratic price movements than the overall securities markets. In addition to its own expenses, the portfolio will indirectly bear its proportionate share of any management and other expenses paid by REITs in which it invests. U.S. REITs are subject to a number of highly technical tax-related rules and requirements; and a U.S. REIT’s failure to qualify for the favorable U.S. federal income tax treatment generally available to U.S. REITs could result in corporate-level taxation, significantly reducing the return on an investment to the portfolio. |