Exhibit (17)(b)(i)

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy (Privacy Policy) with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer’s account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Privacy Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc. Our Privacy Policy applies only to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer’s account (i.e., fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser’s privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures. For more information about Eaton Vance’s Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the “SEC”) permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called “householding” and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise. If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser. Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio(s) (if applicable) will file a schedule of portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website at www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC’s website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC’s public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds’ and Portfolios’ Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC’s website at www.sec.gov.

Eaton Vance Municipal Income Funds a s o f J u l y 3 1 , 2 0 1 0

TABLE OF CONTENTS |

| |

| Management’s Discussion of Fund Performance | 2 |

| |

| Performance Information and Portfolio Composition | |

Arizona | 3 |

Colorado | 5 |

Connecticut | 7 |

Michigan | 9 |

Minnesota | 11 |

New Jersey | 13 |

Pennsylvania | 15 |

| |

| Fund Expenses | 17 |

| |

| Financial Statements | 21 |

| |

| Federal Tax Information | 89 |

| |

| Board of Trustees’ Contract Approval | 90 |

| |

| Management and Organization | 93 |

1

Eaton Vance Municipal Income Funds a s o f J u l y 3 1 , 2 0 1 0

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE |

Economic and Market Conditions

The U.S. economy remained generally stable, if still weak, during the year ending July 31, 2010, even as concerns about high unemployment and budget deficits provoked ongoing skittishness in the capital markets. The U.S. economy grew at an annualized rate of 3.7% in the first quarter of 2010, but slowed to 1.6% in the second quarter, according to the U.S. Department of Commerce. This followed annualized growth rates of 2.2% and 5.6% in the third and fourth quarters of 2009, respectively.

Municipal bond performance was positive for the period, in spite of ongoing negative media attention on the tax-exempt sector. The Barclays Capital Municipal Bond Index (the Index)1— an unmanaged index of municipal bonds traded in the U.S.—gained 9.15% for the period, reflecting continued demand for munis, supported in part by the limited supply of tax-exempt issues due to the success of the Build America Bond program. Demand began to taper off later in the period, however, likely as a result of low yields and concerns about the fiscal stress on many issuers.

Against this backdrop, munis with longer and intermediate maturities performed best during the year, with the 20-year segment of the Index returning 10.94% and the 7-year segment 7.59%. Shorter-maturity bonds in the 5-year segment of the Index returned 6.49%, trailing the broader municipal bond market.

Management Discussion

During the year ending July 31, 2010, the Funds’ performances at net asset value were generally in line with the Index and their Lipper peer group averages, with notable outperformance seen in Eaton Vance Colorado and New Jersey Municipal Income Funds, and underperformance in Eaton Vance Minnesota Municipal Income Fund. Given the significant price movement at the longer end of the municipal yield curve, management’s bias toward longer maturities was generally beneficial for relative performance during the period. Investing across the credit spectrum and making higher allocations to revenue bonds was helpful.

The Funds were modestly hedged using Treasury futures—an ongoing strategy that management has employed for many years and is designed to mitigate interest-rate risk. During the second half of the period, the volatile economic situation in Europe and increasing uncertainty about the global economic outlook bolstered the U.S. Treasury market, sending Treasury yields lower and causing the municipal/Treasury ratio to climb from 89% at the beginning of 2010 to 99.8% as of July 31, 2010. As a result, the Funds’ hedged Treasury positions detracted from their relative returns during the second half of the year. However, this strategy contributed positively during the first half.

Management employed leverage in some of the Funds, through which additional exposure to the municipal market was achieved. Leverage has the impact of magnifying a Fund’s exposure to its underlying investments in both up and down markets. During the period, the Funds’ leverage contributed positively to their relative performance.2

As we move ahead, we continue to focus on state and local government budget deficits, which likely peaked in 2010 or are expected to peak in early 2011. The decline in tax revenues appears to be reaching a bottom, with some municipalities realizing growth in tax receipts due to a combination of slim economic growth and an increase in actual tax rates. However, spending continues to grow faster than tax receipts despite deep spending cuts enacted by some government officials. We will continue to analyze any new developments and solutions that government leaders formulate to address their fiscal problems.

The Board of Trustees of the Eaton Vance Colorado Municipal Income Fund approved a proposal to reorganize the Fund into Eaton Vance National Municipal Income Fund, a series of Eaton Vance Municipals Trust, with substantially the same investment objective and policies as the Fund. Proxy materials describing the proposed reorganization commenced mailing on August 31, 2010, to the Fund’s record date shareholders. If approved by shareholders of the Fund, the reorganization is expected to be completed in the fourth quarter of 2010.

1 It is not possible to invest directly in an Index or a Lipper classification. The Index’s total return does not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. The Lipper total returns are the average total returns, at net asset value, of the funds that are in the same Lipper Classification as the Funds.

2 Certain Funds employ residual interest bond (RIB) financing. The leverage created by RIB investments provides an opportunity for increased income but, at the same time, creates special risks (including the likelihood of greater volatility of net asset value). See Note 1I to the financial statements for more information on RIB investments.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

The views expressed throughout this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund. Portfolio information provided in the report may not be representative of the Funds’ current or future investments and may change due to active management.

2

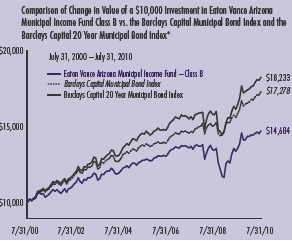

Eaton Vance Arizona Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: Craig R. Brandon, CFA

* Source: Lipper, Inc. Class B of the Fund commenced investment operations on 7/25/91.

A $10,000 hypothetical investment at net asset value in Class A on 7/31/00 and Class C on 12/16/05 (commencement of operations) would have been valued at $15,809 ($15,058 at the maximum offering price) and $11,482, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. 2 Source: Prospectus dated 12/1/09, as supplemented. Includes interest expense of 0.06% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with residual interest bond transactions by the Fund. The Fund also records offsetting interest income in an amount equal to this expense relating to the municipal obligations underlying such transactions, and as a result net asset value and performance have not been affected by this expense. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 37.95% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Arizona Municipal Debt Funds Classification contained 30, 23 and 23 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

3

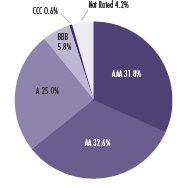

Eaton Vance Arizona Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PORTFOLIO COMPOSITION |

Rating Distribution*1

By total investments |

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund's financial statements. Absent such securities, the Fund's rating distribution as of 7/31/10 is as follows:

| | | |

| AAA | 31.4% | BBB | 5.9% |

| AA | 32.4% | CCC | 0.6% |

| A | 25.4% | Not Rated | 4.3% |

| Fund Statistics2 | |

|

| * Number of Issues: | 73 |

| * Average Maturity: | 17.4 years |

| * Average Effective Maturity: | 11.3 years |

| * Average Call Protection: | 8.1 years |

| * Average Dollar Price: | $100.25 |

| * RIB Leverage3 : | 1.8% |

1Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

2Fund holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

3See Note 1l to the Fund’s financial statements. RIB leverage represents the amount of Floating Rate Notes outstanding as of 7/31/10 as a percentage of the Fund’s net assets plus Floating Rate Notes.

4

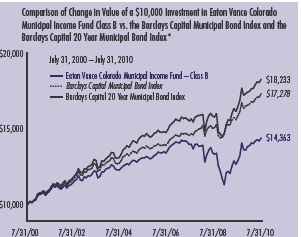

Eaton Vance Colorado Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: William H. Ahern, Jr., CFA

* Source: Lipper, Inc. Class B of the Fund commenced investment operations on 8/25/92.

A $10,000 hypothetical investment at net asset value in Class A on 7/31/00 and Class C on 10/8/07 (commencement of operations) would have been valued at $15,441 ($14,708 at the maximum offering price) and $10,295, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. 2 Source: Prospectus dated 12/1/09, as supplemented. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 38.01% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Colorado Municipal Debt Funds Classification contained 21, 18 and 18 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

5

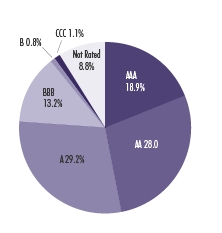

Eaton Vance Colorado Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PORTFOLIO COMPOSITION |

Rating Distribution1

By total investments |

| |

| * Number of Issues: | 58 |

| * Average Maturity: | 19.9 years |

| * Average Effective Maturity: | 11.6 years |

| * Average Call Protection: | 8.1 years |

| * Average Dollar Price: | $96.44 |

1 Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

6

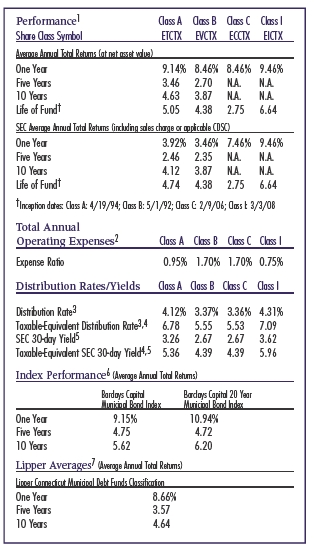

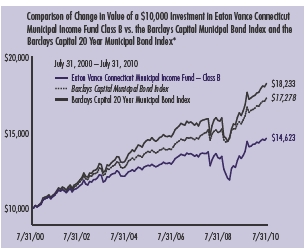

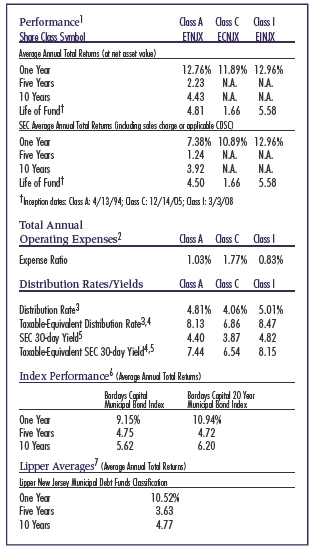

Eaton Vance Connecticut Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: William H. Ahern, Jr., CFA

* Source: Lipper, Inc. Class B of the Fund commenced investment operations on 5/1/92.

A $10,000 hypothetical investment at net asset value in Class A on 7/31/00, Class C on 2/9/06 (commencement of operations) and Class I on 3/3/08 (commencement of operations) would have been valued at $15,729 ($14,982 at the maximum offering price), $11,291 and $11,677, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. Class I shares are not subject to a sales charge. 2 Source: Prospectus dated 12/1/09, as supplemented. Includes interest expense of 0.15% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with residual interest bond transactions by the Fund. The Fund also records offsetting interest income in an amount equal to this expense relating to the municipal obligations underlying such transactions, and as a result net asset value and performance have not been affected by this expense. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 39.23% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Connecticut Municipal Debt Funds Classification contained 22, 16 and 16 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

7

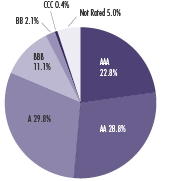

Eaton Vance Connecticut Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PORTFOLIO COMPOSITION |

Rating Distribution*1

By total investments |

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund's financial statements. Absent such securities, the Fund's rating distribution as of 7/31/10 is as follows:

| | | |

| AAA | 20.7% | BBB | 11.3% |

| AA | 29.1% | BB | 2.1% |

| A | 30.4% | CCC | 0.4% |

| | | Not Rated | 6.0% |

| |

| * Number of Issues: | 82 |

| * Average Maturity: | 16.5 years |

| * Average Effective Maturity: | 8.8 years |

| * Average Call Protection: | 7.2 years |

| * Average Dollar Price: | $106.80 |

| * RIB Leverage3 : | 5.2% |

1Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

2Fund holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

3See Note 1l to the Fund’s financial statements. RIB leverage represents the amount of Floating Rate Notes outstanding as of 7/31/10 as a percentage of the Fund’s net assets plus Floating Rate Notes.

8

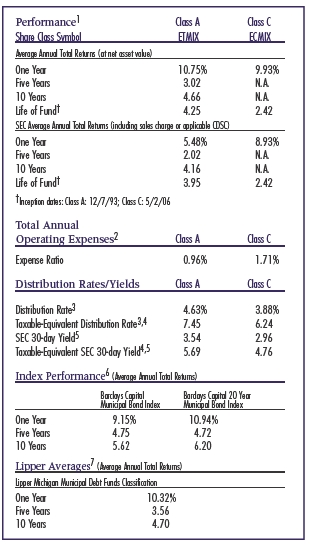

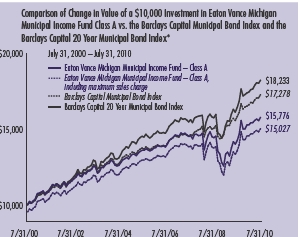

Eaton Vance Michigan Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class A of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class A, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. Class A total returns are presented at net asset value and maximum public offering price. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: William H. Ahern, Jr., CFA

* Source: Lipper, Inc. Class A of the Fund commenced investment operations on 12/7/93.

A $10,000 hypothetical investment at net asset value in Class C on 5/2/06 (commencement of operations) would have been valued at $11,069 on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charge (CDSC) for Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. 2 Source: Prospectus dated 12/1/09, as supplemented. Includes interest expense of 0.16% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with residual interest bond transactions by the Fund. The Fund also records offsetting interest income in an amount equal to this expense relating to the municipal obligations underlying such transactions, and as a result net asset value and performance have not been affected by this expense. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 37.83% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Michigan Municipal Debt Funds Classification contained 22, 15 and 15 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

9

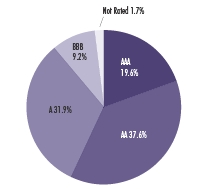

Eaton Vance Michigan Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

Rating Distribution*1

By total investments |

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund's financial statements. Absent such securities, the Fund's rating distribution as of 7/31/10 is as follows:

| | | |

| AAA | 18.9% | BBB | 9.4% |

| AA | 37.4% | Not Rated | 1.8% |

| A | 32.5% | | |

| |

| * Number of Issues: | 56 |

| * Average Maturity: | 19.8 years |

| * Average Effective Maturity: | 13.0 years |

| * Average Call Protection: | 7.5 years |

| * Average Dollar Price: | $96.90 |

| * RIB Leverage3 : | 1.9% |

1Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

2Fund holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

3See Note 1l to the Fund’s financial statements. RIB leverage represents the amount of Floating Rate Notes outstanding as of 7/31/10 as a percentage of the Fund’s net assets plus Floating Rate Notes.

10

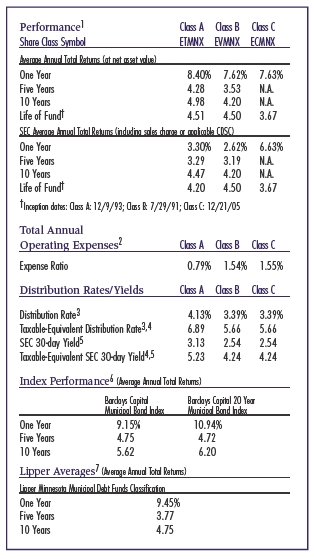

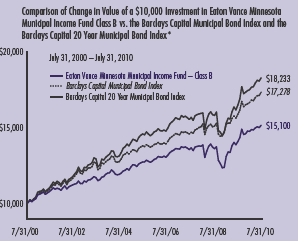

Eaton Vance Minnesota Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: Craig R. Brandon, CFA

* Source: Lipper, Inc. Class B of the Fund commenced investment operations on 7/29/91.

A $10,000 hypothetical investment at net asset value in Class A on 7/31/00 and Class C on 12/21/05 (commencement of operations) would have been valued at $16,259 ($15,486 at the maximum offering price) and $11,809, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. 2 Source: Prospectus dated 12/1/09, as supplemented. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 40.10% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Minnesota Municipal Debt Funds Classification contained 40, 33 and 32 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

11

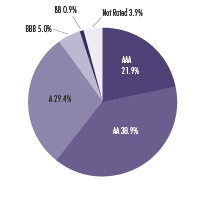

Eaton Vance Minnesota Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PORTFOLIO COMPOSITION |

Rating Distribution1

By total investments |

| |

| * Number of Issues: | 93 |

| * Average Maturity: | 19.9 years |

| * Average Effective Maturity: | 8.8 years |

| * Average Call Protection: | 6.7 years |

| * Average Dollar Price: | $100.46 |

1 Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

12

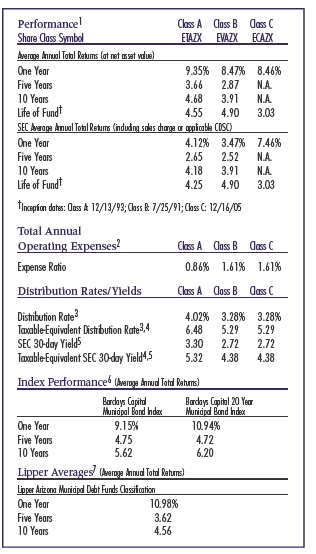

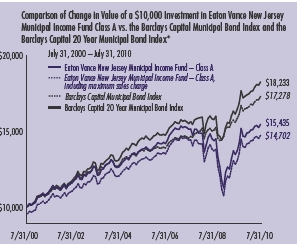

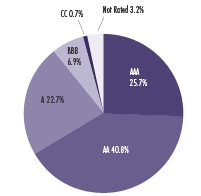

Eaton Vance New Jersey Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class A of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class A, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. Class A total returns are presented at net asset value and maximum public offering price. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: Adam A. Weigold, CFA

* Source: Lipper, Inc. Class A of the Fund commenced investment operations on 4/13/94.

A $10,000 hypothetical investment at net asset value in Class C on 12/14/05 (commencement of operations) and Class I on 3/3/08 (commencement of operations) would have been valued at $10,791 and $11,399, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charge (CDSC) for Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. Class I shares are not subject to a sales charge. 2 Source: Prospectus dated 12/1/09, as supplemented. Includes interest expense of 0.18% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with residual interest bond transactions by the Fund. The Fund also records offsetting interest income in an amount equal to this expense relating to the municipal obligations underlying such transactions, and as a result net asset value and performance have not been affected by this expense. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 40.83% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper New Jersey Municipal Debt Funds Classification contained 47, 34 and 31 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

13

Eaton Vance New Jersey Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PORTFOLIO COMPOSITION |

Rating Distribution*1

By total investments |

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund's financial statements. Absent such securities, the Fund's rating distribution as of 7/31/10 is as follows.

| | | |

| AAA | 12.7% | BBB | 25.4% |

| AA | 31.7% | BB | 0.3% |

| A | 24.0% | B | 1.0% |

| | | Not Rated | 4.9% |

| |

| * Number of Issues: | 91 |

| * Average Maturity: | 26.4 years |

| * Average Effective Maturity: | 13.1 years |

| * Average Call Protection: | 8.8 years |

| * Average Dollar Price: | $92.18 |

| * RIB Leverage3 : | 13.2% |

1Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

2Fund holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

3See Note 1l to the Fund’s financial statements. RIB leverage represents the amount of Floating Rate Notes outstanding as of 7/31/10 as a percentage of the Fund’s net assets plus Floating Rate Notes.

14

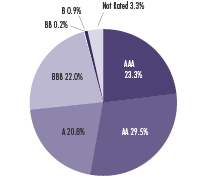

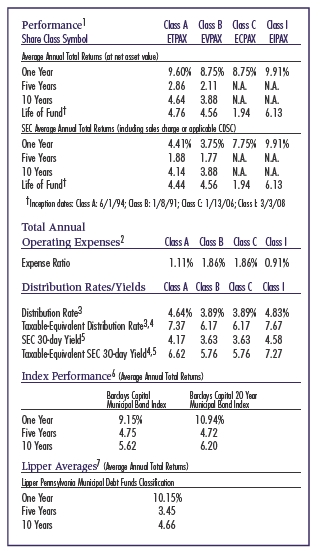

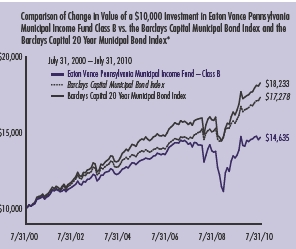

Eaton Vance Pennsylvania Municipal Income Fund as of J u l y 3 1 , 2 0 1 0

PERFORMANCE INFORMATION |

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Barclays Capital Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S., and the Barclays Capital 20 Year Municipal Bond Index, an unmanaged index of municipal bonds traded in the U.S. with maturities ranging from 17-22 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B, the Barclays Capital Municipal Bond Index and the Barclays Capital 20 Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

Portfolio Manager: Adam A. Weigold, CFA

* Source: Lipper, Inc. Class B of the Fund commenced investment operations on 1/8/91.

A $10,000 hypothetical investment at net asset value in Class A on 7/31/00, Class C on 1/13/06 (commencement of operations) and Class I on 3/3/08 (commencement of operations) would have been valued at $15,742 ($14,995 at the maximum offering price), $10,913 and $11,542, respectively, on 7/31/10. It is not possible to invest directly in an Index. The Indices’ total returns do not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. Fund performance during certain periods reflects the strong bond market performance and/or the strong performance of bonds held during those periods. This performance is not typical and may not be repeated. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average Annual Total Returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, the returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. Class I shares are not subject to a sales charge. 2 Source: Prospectus dated 12/1/09, as supplemented. Includes interest expense of 0.29% relating to the Fund’s liability with respect to floating rate notes held by third parties in conjunction with residual interest bond transactions by the Fund. The Fund also records offsetting interest income in an amount equal to this expense relating to the municipal obligations underlying such transactions, and as a result net asset value and performance have not been affected by this expense. 3 The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last regular distribution per share in the period (annualized) by the net asset value at the end of the period. 4 Taxable-equivalent figures assume a maximum 37.00% combined federal and state income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Indices’ total returns do not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Indices. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Pennsylvania Municipal Debt Funds Classification contained 60, 48 and 47 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

15

Eaton Vance Pennsylvania Municipal Income Fund as of J u l y 31, 2010

PORTFOLIO COMPOSITION |

Rating Distribution*1

By total investments |

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund's financial statements. Absent such securities, the Fund's rating distribution as of 7/31/10 is as follows.

| | | |

| AAA | 19.3% | BBB | 7.8% |

| AA | 43.3% | CC | 0.8 |

| A | 25.2% | Not Rated | 3.6% |

Fund Statistics2 | |

| * Number of Issues: | 134 |

| * Average Maturity: | 21.2 years |

| * Average Effective Maturity: | 12.4 years |

| * Average Call Protection: | 8.3 years |

| * Average Dollar Price: | $97.79 |

| * RIB Leverage3 : | 10.6% |

1Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. Ratings are based on Moody’s, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency’s investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. If securities are rated differently by the rating agencies, the higher rating is applied.

2Fund holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

3See Note 1l to the Fund’s financial statements. RIB leverage represents the amount of Floating Rate Notes outstanding as of 7/31/10 as a percentage of the Fund’s net assets plus Floating Rate Notes.

16

Eaton Vance Municipal Income Funds as of July 31, 2010

FUN D EXP ENSES |

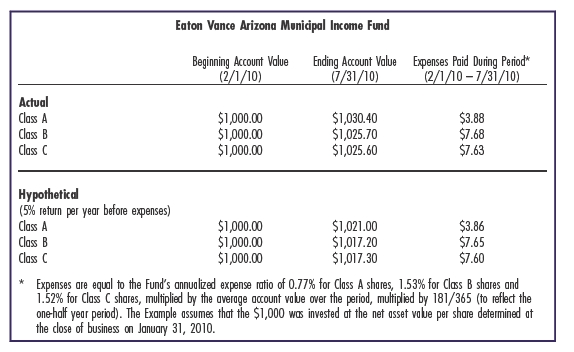

Example: As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (February 1, 2010 – July 31, 2010).

Actual Expenses: The first section of each table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of each table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in each table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of each table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would be higher.

17

Eaton Vance Municipal Income Funds as of July 31, 2010

FUN D EXP ENSES CONT’D |

| | | |

| | Eaton Vance Colorado Municipal Income Fund | |

| |

| | Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,040.80 | $3.74 |

| Class B | $1,000.00 | $1,036.50 | $7.57 |

| Class C | $1,000.00 | $1,036.50 | $7.47 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | | |

| Class A | $1,000.00 | $1,021.10 | $3.71 |

| Class B | $1,000.00 | $1,017.40 | $7.50 |

| Class C | $1,000.00 | $1,017.50 | $7.40 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.74% for Class A shares, 1.50% for Class B shares and |

| 1.48% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the |

| one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at |

| the close of business on January | 31, 2010. | | |

| | | |

| Eaton Vance Connecticut Municipal Income Fund |

| |

| | Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,030.90 | $4.08 |

| Class B | $1,000.00 | $1,027.20 | $7.84 |

| Class C | $1,000.00 | $1,027.20 | $7.84 |

| Class I | $1,000.00 | $1,031.90 | $3.07 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | |

| Class A | $1,000.00 | $1,020.80 | $4.06 |

| Class B | $1,000.00 | $1,017.10 | $7.80 |

| Class C | $1,000.00 | $1,017.10 | $7.80 |

| Class I | $1,000.00 | $1,021.80 | $3.06 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.81% for Class A shares, 1.56% for Class B shares, 1.56% |

| for Class C shares and 0.61% for Class I shares, multiplied by the average account value over the period, multiplied by |

| 181/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value |

| per share determined at the close of business on January 31, 2010. | |

18

Eaton Vance Municipal Income Funds as of July 31, 2010

FUN D EXP ENSES CONT’D |

| | | |

| | Eaton Vance Michigan Municipal Income Fund | |

| |

| | Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,032.50 | $3.88 |

| Class C | $1,000.00 | $1,028.70 | $7.65 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | | |

| Class A | $1,000.00 | $1,021.00 | $3.86 |

| Class C | $1,000.00 | $1,017.30 | $7.60 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.77% for Class A shares and 1.52% for Class C shares, |

| multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The |

| Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on |

| January 31, 2010. | | | |

| | | |

| | Eaton Vance Minnesota Municipal Income Fund | |

| |

| | Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,031.00 | $3.73 |

| Class B | $1,000.00 | $1,027.50 | $7.54 |

| Class C | $1,000.00 | $1,026.50 | $7.49 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | |

| Class A | $1,000.00 | $1,021.10 | $3.71 |

| Class B | $1,000.00 | $1,017.40 | $7.50 |

| Class C | $1,000.00 | $1,017.40 | $7.45 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.74% for Class A shares, 1.50% for Class B shares and |

| 1.49% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the |

| one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at |

| the close of business on January 31, 2010. | | |

19

Eaton Vance Municipal Income Funds as of July 31, 2010

FUN D EXP ENSES CONT’D |

| | | |

| Eaton Vance New Jersey Municipal Income Fund |

| |

| Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,036.50 | $4.65 |

| Class C | $1,000.00 | $1,033.40 | $8.42 |

| Class I | $1,000.00 | $1,037.50 | $3.59 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | | |

| Class A | $1,000.00 | $1,020.20 | $4.61 |

| Class C | $1,000.00 | $1,016.50 | $8.35 |

| Class I | $1,000.00 | $1,021.30 | $3.56 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.92% for Class A shares, 1.67% for Class C shares and |

| 0.71% for Class I shares, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the |

| one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at |

| the close of business on January 31, 2010. | | | |

| | | |

| Eaton Vance Pennsylvania Municipal Income Fund |

| |

| | Beginning Account Value | Ending Account Value | Expenses Paid During Period* |

| | (2/1/10) | (7/31/10) | (2/1/10 – 7/31/10) |

| |

| Actual | | | |

| Class A | $1,000.00 | $1,023.00 | $4.41 |

| Class B | $1,000.00 | $1,019.30 | $8.16 |

| Class C | $1,000.00 | $1,019.30 | $8.16 |

| Class I | $1,000.00 | $1,025.20 | $3.41 |

| |

| |

| Hypothetical | | | |

| (5% return per year before expenses) | | |

| Class A | $1,000.00 | $1,020.40 | $4.41 |

| Class B | $1,000.00 | $1,016.70 | $8.15 |

| Class C | $1,000.00 | $1,016.70 | $8.15 |

| Class I | $1,000.00 | $1,021.40 | $3.41 |

| |

| * Expenses are equal to the Fund’s annualized expense ratio of 0.88% for Class A shares, 1.63% for Class B shares, 1.63% |

| for Class C shares and 0.68% for Class I shares, multiplied by the average account value over the period, multiplied by |

| 181/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value |

| per share determined at the close of business on January 31, 2010. | |

20

Eaton Vance Arizona Municipal Income Fund as of July 31, 2010

PORTFOLIO OF INVESTMENTS |

| | |

| Tax-Exe m pt Inve stm e nts — 100. 4% | |

| |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Education — 3.3% | |

| $ 1,500 | Arizona Board of Regents, (University of Arizona), | |

| | 5.00%, 6/1/33 | $ 1,570,155 |

| 1,500 | Glendale Industrial Development Authority, | |

| | (Midwestern University), 5.00%, 5/15/25 | 1,534,815 |

| | | $ 3,104,970 |

| |

| Electric Utilities — 5.0% | |

| $ 500 | Maricopa County Pollution Control Corp., (Arizona Public | |

| | Service Co.), 6.00% to 5/1/14 (Put Date), 5/1/29 | $ 538,535 |

| 2,000 | Salt River Agricultural Improvements and Power District, | |

| | 5.00%, 1/1/33 | 2,126,280 |

| 2,000 | Salt River Agricultural Improvements and Power District, | |

| | 5.00%, 1/1/39 | 2,108,780 |

| | | $ 4,773,595 |

| |

| Escrowed / Prerefunded — 13.4% | |

| $ 7,500 | Maricopa County, SFMR, Escrowed to Maturity, | |

| | 0.00%, 2/1/16 | $ 6,683,025 |

| 6,500 | Phoenix Industrial Development Authority, SFMR, Escrowed | |

| | to Maturity, 0.00%, 12/1/14(1) | 6,092,190 |

| | | $12,775,215 |

| |

| General Obligations — 5.6% | |

| $ 1,200 | Maricopa County Community College District, | |

| | 3.00%, 7/1/23 | $ 1,187,916 |

| 1,125 | Puerto Rico, 0.00%, 7/1/18 | 773,302 |

| 1,385 | Tempe, 3.75%, 7/1/24 | 1,398,310 |

| 1,600 | Tempe, 5.375%, 7/1/21 | 1,935,792 |

| | | $ 5,295,320 |

| |

| Health Care-Miscellaneous — 1.0% | |

| $ 475 | Yavapai County Industrial Development Authority, | |

| | (West Yavapai Guidance Clinic), 6.25%, 12/1/36 | $ 434,216 |

| 500 | Yavapai County Industrial Development Authority, (West | |

| | Yavapai Guidance Clinic), 6.625%, 8/15/24 | 484,470 |

| | | $ 918,686 |

| |

| Hospital — 11.4% | |

| $ 2,000 | Arizona Health Facilities Authority, (Banner Health | |

| | System), 5.00%, 1/1/35 | $ 1,983,200 |

| 1,275 | Glendale Industrial Development Authority, (John C. Lincoln | |

| | Health Network), 5.00%, 12/1/28 | 1,223,171 |

| | |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Hospital (continued) | |

| $ 750 | Glendale Industrial Development Authority, (John C. Lincoln | |

| | Health Network), 5.00%, 12/1/32 | $ 700,230 |

| 200 | Glendale Industrial Development Authority, (John C. Lincoln | |

| | Health Network), 5.00%, 12/1/37 | 183,552 |

| 1,750 | Maricopa County Industrial Development Authority, | |

| | (Catholic Healthcare), 5.25%, 7/1/32 | 1,777,300 |

| 1,350 | Maricopa County Industrial Development Authority, | |

| | (Catholic Healthcare), 5.50%, 7/1/26 | 1,387,949 |

| 1,450 | Maricopa County Industrial Development Authority, (Mayo | |

| | Clinic), 5.00%, 11/15/36 | 1,474,679 |

| 1,500 | Scottsdale Industrial Development Authority, (Scottsdale | |

| | Healthcare), 5.25%, 9/1/30 | 1,494,390 |

| 630 | Winslow Industrial Development Authority, (Winslow | |

| | Memorial Hospital), 5.50%, 6/1/22 | 565,022 |

| | | $10,789,493 |

| |

| Industrial Development Revenue — 0.6% | |

| $ 650 | Phoenix Industrial Development Authority, (America West | |

| | Airlines, Inc.), (AMT), 6.25%, 6/1/19 | $ 544,102 |

| | | $ 544,102 |

| |

| Insured-Education — 1.1% | |

| $ 1,000 | North Campus Facilities LLC, (Northern Arizona University), | |

| | (AMBAC), 5.00%, 6/1/25 | $ 1,053,930 |

| | | $ 1,053,930 |

| |

| Insured-Electric Utilities — 4.2% | |

| $ 750 | Maricopa County Pollution Control Corp., | |

| | (El Paso Electric Co.), (FGIC), 4.80%, 8/1/40 | $ 676,327 |

| 1,000 | Mesa Utility System, (FGIC), (NPFG), 5.00%, 7/1/23 | 1,139,710 |

| 750 | Puerto Rico Electric Power Authority, (NPFG), | |

| | 5.25%, 7/1/29 | 785,415 |

| 1,200 | Puerto Rico Electric Power Authority, (NPFG), | |

| | 5.50%, 7/1/16 | 1,364,712 |

| | | $ 3,966,164 |

| |

| Insured-Escrowed / Prerefunded — 2.4% | |

| $ 1,000 | Maricopa County Industrial Development Authority, | |

| | (Samaritan Health Services), (NPFG), Escrowed to | |

| | Maturity, 7.00%, 12/1/16 | $ 1,220,680 |

| 1,000 | Pima County Industrial Development Authority, (Carondolet | |

| | Health Care Corp.), (NPFG), Escrowed to Maturity, | |

| | 5.25%, 7/1/11 | 1,046,130 |

| | | $ 2,266,810 |

S e e notes to financ ial statem ents

21

Eaton Vance Arizona Municipal Income Fund as of July 31, 2010

PORTFOLIO OF INVESTMENTS CONT’D |

| | |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Insured-General Obligations — 7.6% | |

| $ 400 | Flagstaff, (AMBAC), 3.25%, 7/1/23 | $ 401,172 |

| 810 | Goodyear, (AGM), 4.25%, 7/1/37 | 785,943 |

| 1,300 | Goodyear, (NPFG), 3.00%, 7/1/26 | 1,180,244 |

| 2,920 | Maricopa County Elementary School District No. 3, | |

| | (AGM), 5.00%, 7/1/25 | 3,493,430 |

| 1,200 | Pinal County Unified School District No. 43, Apache | |

| | Junction, (AGM), 5.00%, 7/1/24 | 1,386,912 |

| | | $ 7,247,701 |

| |

| Insured-Hospital — 3.5% | |

| $ 1,195 | Arizona Health Facilities Authority, (Arizona Healthcare | |

| | Systems), (FGIC), (NPFG), 5.50%, 6/1/15 | $ 1,318,372 |

| 2,000 | Maricopa County Industrial Development Authority, (Mayo | |

| | Clinic), (AMBAC), 5.25%, 11/15/37 | 2,000,900 |

| | | $ 3,319,272 |

| |

| Insured-Lease Revenue / Certificates of | |

| Participation — 2.6% | |

| $ 1,000 | Arizona State University, (Research Infrastructure Projects), | |

| | (AMBAC), 5.00%, 9/1/30 | $ 1,004,170 |

| 1,500 | Phoenix Civic Improvement Corp., (Civic Plaza), (FGIC), | |

| | (NPFG), 5.50%, (0.00% until 7/1/13), 7/1/41 | 1,351,860 |

| 130 | Prescott Municipal Property Corp., (NPFG), | |

| | 5.00%, 7/1/34 | 133,011 |

| | | $ 2,489,041 |

| |

| Insured-Special Tax Revenue — 10.4% | |

| $ 915 | Arizona Tourism and Sports Authority, (Multipurpose | |

| | Stadium Facility), (NPFG), 4.50%, 7/1/24 | $ 926,639 |

| 1,000 | Arizona Tourism and Sports Authority, (Multipurpose | |

| | Stadium Facility), (NPFG), 5.00%, 7/1/25 | 1,011,590 |

| 500 | Arizona Tourism and Sports Authority, (Multipurpose | |

| | Stadium Facility), (NPFG), 5.00%, 7/1/28 | 501,595 |

| 3,915 | Downtown Phoenix Hotel Corp., (FGIC), (NPFG), | |

| | 5.00%, 7/1/36 | 3,763,646 |

| 750 | Glendale Transportation, Excise Tax Revenue, (NPFG), | |

| | 4.50%, 7/1/32 | 753,075 |

| 3,370 | Puerto Rico Sales Tax Financing Corp., (AMBAC), | |

| | 0.00%, 8/1/54 | 210,456 |

| 680 | Puerto Rico Sales Tax Financing Corp., (NPFG), | |

| | 0.00%, 8/1/44 | 82,899 |

| 1,345 | Puerto Rico Sales Tax Financing Corp., (NPFG), | |

| | 0.00%, 8/1/45 | 152,819 |

| 1,080 | Puerto Rico Sales Tax Financing Corp., (NPFG), | |

| | 0.00%, 8/1/46 | 115,117 |

| 2,000 | Queen Creek, Excise Tax & State Shared Revenue, | |

| | (NPFG), 5.00%, 8/1/27 | 2,062,520 |

| | |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Insured-Special Tax Revenue (continued) | |

| $ 320 | Scottsdale, (Municipal Property Corp.), (AMBAC), | |

| | 4.50%, 7/1/35 | $ 321,891 |

| | | $ 9,902,247 |

| |

| Insured-Transportation — 6.8% | |

| $ 2,750 | Phoenix Civic Improvement Corp., Airport Revenue, (FGIC), | |

| | (NPFG), (AMT), 5.25%, 7/1/27 | $ 2,772,330 |

| 1,725 | Pima County, Street and Highway Revenue, (AMBAC), | |

| | 3.25%, 7/1/22 | 1,696,451 |

| 1,900 | Puerto Rico Highway and Transportation Authority, (AGC), | |

| | (CIFG), 5.25%, 7/1/41(2) | 1,981,966 |

| | | $ 6,450,747 |

| |

| Insured-Water and Sewer — 1.7% | |

| $ 500 | Cottonwood Property Corp., Water Revenue, (XLCA), | |

| | 5.00%, 7/1/29 | $ 473,055 |

| 1,135 | Phoenix Civic Improvement Corp., Wastewater System | |

| | Revenue, (AGM), (NPFG), 5.00%, 7/1/37 | 1,182,080 |

| | | $ 1,655,135 |

| |

| Lease Revenue / Certificates of Participation — 0.9% |

| $ 750 | Mohave County Industrial Development Authority, (Mohave | |

| | Prison LLC), 8.00%, 5/1/25 | $ 862,463 |

| | | $ 862,463 |

| |

| Other Revenue — 3.6% | |

| $ 1,750 | Arizona Health Facilities Authority, (Blood Systems, Inc.), | |

| | 4.75%, 4/1/25 | $ 1,759,537 |

| 16,505 | Children’s Trust Fund, PR, Tobacco Settlement, | |

| | 0.00%, 5/15/50 | 565,626 |

| 10,765 | Children’s Trust Fund, PR, Tobacco Settlement, | |

| | 0.00%, 5/15/55 | 194,847 |

| 1,000 | Salt Verde Financial Corp., Senior Gas Revenue, | |

| | 5.00%, 12/1/37 | 891,520 |

| | | $ 3,411,530 |

| |

| Senior Living / Life Care — 1.3% | |

| $ 1,800 | Arizona Health Facilities Authority, (Care Institute, Inc. - | |

| | Mesa), 7.625%, 1/1/26(3) | $ 1,204,074 |

| | | $ 1,204,074 |

S e e notes to financ ial statem ents

22

Eaton Vance Arizona Municipal Income Fund as of July 31, 2010

PORTFOLIO OF INVESTMENTS CONT’D |

| | |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Special Tax Revenue — 9.5% | |

| $ 1,000 | Gilbert Public Facilities Municipal Property Corp., | |

| | 5.50%, 7/1/27 | $ 1,093,120 |

| 1,000 | Glendale Western Loop, (101 Public Facilities Corp.), | |

| | Series A, 6.25%, 7/1/38 | 1,051,290 |

| 250 | Glendale Western Loop, (101 Public Facilities Corp.), | |

| | Series B, 6.25%, 7/1/38 | 262,823 |

| 270 | Guam, Limited Obligation Bonds, 5.625%, 12/1/29 | 278,281 |

| 295 | Guam, Limited Obligation Bonds, 5.75%, 12/1/34 | 303,885 |

| 1,000 | Puerto Rico Sales Tax Financing Corp., 5.25%, 8/1/57(2) | 1,009,560 |

| 2,500 | Scottsdale, (Municipal Property Corp.), 5.00%, 7/1/30 | 2,849,500 |

| 1,000 | Scottsdale, (Municipal Property Corp.), 5.00%, 7/1/34 | 1,120,450 |

| 1,000 | Tempe Transportation, Excise Tax Revenue, | |

| | 5.00%, 7/1/33 | 1,058,570 |

| | | $ 9,027,479 |

| |

| Transportation — 3.4% | |

| $ 3,000 | Arizona Transportation Board, Highway Revenue, | |

| | 5.00%, 7/1/32 | $ 3,190,290 |

| | | $ 3,190,290 |

| |

| Water and Sewer — 1.1% | |

| $ 1,000 | Arizona Water Infrastructure Finance Authority, | |

| | 5.00%, 10/1/30 | $ 1,092,000 |

| | | $ 1,092,000 |

| |

| Total Tax-Exempt Investments — 100.4% | |

| (identified cost $90,853,914) | $95,340,264 |

| |

| Other Assets, Less Liabilities — (0.4)% | $ (368,900) |

| |

| Net Assets — 100.0% | $94,971,364 |

The percentage shown for each investment category in the Portfolio of Investments is based on net assets.

AGC - Assured Guaranty Corp.

AGM - Assured Guaranty Municipal Corp.

AMBAC - AMBAC Financial Group, Inc.

AMT - Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax.

CIFG - CIFG Assurance North America, Inc.

FGIC - Financial Guaranty Insurance Company

NPFG - National Public Finance Guaranty Corp.

SFMR - Single Family Mortgage Revenue

XLCA - XL Capital Assurance, Inc.

The Fund invests primarily in debt securities issued by Arizona municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at July 31, 2010, 40.2% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution ranged from 0.5% to 24.0% of total investments.

(1) Security (or a portion thereof) has been pledged to cover margin requirements on open financial futures contracts.

(2) Security represents the underlying municipal bond of an inverse floater (see Note 1I).

(3) Security is in default with respect to scheduled principal payments.

S e e notes to financ ial statem ents

23

Eaton Vance Colorado Municipal Income Fund as of July 31, 2010

PORTFOLIO OF INVESTMENTS |

| | |

| Tax-Exe m pt Inve stm e nts — 97.3% | |

| |

| Principal Amount | | |

| (000’s omitted) | Security | Value |

| |

| Education — 7.9% | |

| $1,000 | Colorado Educational and Cultural Facilities Authority, | |

| | (Alexander Dawson School), 5.30%, 2/15/29 | $ 1,005,170 |

| 425 | Colorado Educational and Cultural Facilities Authority, (Kent | |

| | Denver School), 5.125%, 10/1/39 | 427,597 |

| 500 | Mesa State College, (Auxiliary Facilities System Enterprise | |

| | Revenue), 5.00%, 5/15/33 | 522,760 |

| 750 | University of Colorado, (Enterprise Revenue), | |

| | 5.125%, 6/1/29 | 814,980 |

| | | $ 2,770,507 |

| |

| Electric Utilities — 3.2% | |

| $1,000 | Platte River Power Authority, 5.00%, 6/1/27 | $ 1,106,310 |

| | | $ 1,106,310 |

| |

| Escrowed / Prerefunded — 9.2% | |

| $ 500 | Colorado Health Facilities Authority, (Portercare Adventist | |

| | Health), Prerefunded to 11/15/11, 6.50%, 11/15/31 | $ 544,090 |

| 3,000 | Dawson Ridge Metropolitan District No. 1, Escrowed to | |