UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04443 |

|

Eaton Vance Investment Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner

The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | March 31 | |

|

Date of reporting period: | March 31, 2006 | |

| | | | | | | | |

Item 1. Reports to Stockholders

Annual Report March 31, 2006

EATON VANCE

NATIONAL

LIMITED

MATURITY

MUNICIPALS

FUND

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about

its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e. fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and it's underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to portfolio securities during the 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

Eaton Vance National Limited Maturity Municipals Fund (the “Fund”) is designed to provide current income exempt from regular federal income tax and limited principal fluctuation. The Fund invests primarily in investment-grade municipal obligations.

Economic and Market Conditions

The economy expanded at a 4.8% pace in the first quarter of 2006, an increase from the 1.7% rate in the fourth quarter. Even with a cooling housing market, the economy generated respectable growth in 2005 and early 2006. Despite high energy prices, rising mortgage rates and a persistent tightening by the Federal Reserve (the “Fed”), the economy continued to create jobs – 211,000 in March 2006. The economy appeared to be sustaining growth in both the manufacturing and service sectors, with moderate signs of inflationary pressures.

Investor sentiment regarding the Fed’s monetary policy appears to have stabilized in recent months as investors have begun to anticipate the end of the Fed’s series of interest rate hikes (which began in June 2004). The Fed has raised rates at all of the last 15 Open Market Committee meetings, with the current Federal Funds rate standing at 4.75%.

Boosted by lower-than-anticipated long-term interest rates, the municipal market saw record supply in 2005, more than $400 billion in new issuance. However, supply has lagged thus far in 2006, contributing to municipal bond outperformance. At March 31, 2006, long-term AAA-rated insured municipal bonds yielded 93% of U.S. Treasury bonds with similar maturities.*

For the year ended March 31, 2006, the Lehman Brothers 7-Year Municipal Bond Index† (the “Index”), a broad-based, unmanaged index of investment-grade municipal debt securities with an average maturity of 7 years, posted a modest gain of 2.63%. For information about the Fund’s performance and the performance of funds in the same Lipper Classification†, see the Performance Information and Portfolio Composition pages that follow.

Management Discussion

The Fund currently invests primarily in bonds with maturities between five and sixteen years. Shorter maturity bonds usually provide somewhat less tax-exempt income than longer ones but also usually exhibit lower price volatility. Given the flattening of the yield curve for fixed-income securities over the past eighteen months, the intermediate part of the curve has become an attractive area.

During the year ended March 31, 2006, the Fed raised short-term interest rates at regular intervals, and commodities prices rose significantly. However, the economy grew at a solid pace, with moderate inflation. In this climate, Fund management continued to maintain a somewhat cautious outlook on interest rates and positioned the Fund’s duration accordingly. Duration measures a bond fund’s sensitivity to changes in interest rates.

During the past year, management invested in bonds with attractive coupons and long call protection. These strategies contributed positively to the Fund’s performance over the 12-month period. Management also took advantage of narrow credit spreads in an effort to lower the Fund’s exposure to credit risk, where possible.

Management continued to focus on finding relative value within the marketplace — in issuer names, coupons, maturities and sectors. We believe that relative value trading, which seeks to capitalize on undervalued securities, has enhanced the Fund’s returns during the year. Finally, management continued to monitor closely call protection in the Fund. Call protection remains an important strategic consideration for municipal bond investors, especially because refinancing activity has increased over the past year.

* Source: Bloomberg L.P. Yields are a compilation of a representative variety of general obligations and are not necessarily representative of the Fund’s yield.

† It is not possible to invest directly in an Index or Lipper Classification. The Index’s total return does not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

Past performance is no guarantee of future results.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

The views expressed throughout this report are those of the portfolio manager and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

2

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PERFORMANCE INFORMATION AND PORTFOLIO COMPOSITION

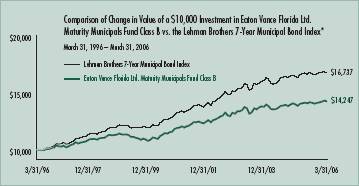

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Lehman Brothers 7-Year Municipal Bond Index, a broad-based, unmanaged market index of investment-grade municipal debt securities with an average maturity of 7 years. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B and in the Lehman Brothers 7-Year Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on Fund distributions or redemptions of Fund shares.

Portfolio Manager: William H. Ahern, CFA

Performance(1) | | Class A | | Class B | | Class C | |

| | | | | | | |

Average Annual Total Returns (at net asset value) | | | | | | | |

One Year | | 4.88 | % | 3.99 | % | 3.93 | % |

Five Years | | 5.01 | | 4.21 | | 4.20 | |

Ten Years | | N.A. | | 4.15 | | 4.03 | |

Life of Fund† | | 5.07 | | 4.44 | | 3.70 | |

| | | | | | | |

SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | | | | |

One Year | | 2.47 | % | 0.99 | % | 2.93 | % |

Five Years | | 4.53 | | 4.21 | | 4.20 | |

Ten Years | | N.A. | | 4.15 | | 4.03 | |

Life of Fund† | | 4.82 | | 4.44 | | 3.70 | |

† Inception Dates – Class A: 6/27/96; Class B: 5/22/92; Class C: 12/8/93

(1) Average annual total returns do not include the 2.25% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, returns would be lower. SEC average annual total returns for Class A reflect the maximum 2.25% sales charge. SEC returns for Class B reflect the applicable CDSC based on the following schedule: 3% - 1st year; 2.5% - 2nd year; 2% - 3rd year; 1% - 4th year. SEC returns for Class C reflect a 1% CDSC for the first year.

Index Performance(2)

Lehman Brothers 7-Year Municipal Bond Index – Average Annual Total Returns

One Year | | 2.63 | % |

Five Years | | 4.57 | |

Ten Years | | 5.28 | |

Lipper Averages(3)

Lipper Intermediate Municipal Debt Funds Classification – Average Annual Total Returns

One Year | | 2.45 | % |

Five Years | | 3.86 | |

Ten Years | | 4.66 | |

Distribution Rates/Yields | | Class A | | Class B | | Class C | |

| | | | | | | |

Distribution Rate(4) | | 3.97 | % | 3.23 | % | 3.23 | % |

Taxable-Equivalent Distribution Rate(4),(5) | | 6.11 | | 4.97 | | 4.97 | |

SEC 30-day Yield(6) | | 3.55 | | 2.88 | | 2.88 | |

Taxable-Equivalent SEC 30-day Yield(5),(6) | | 5.46 | | 4.43 | | 4.43 | |

*Sources: Thomson Financial; Lipper, Inc. Class B of the Fund commenced operations on 5/22/92.

A $10,000 hypothetical investment at net asset value in Class A and Class C on 6/27/96 (commencement of operations) and 3/31/96, respectively, would have been valued at $16,196 ($15,833 at the maximum offering price) and $14,850, respectively, on 3/31/06. It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

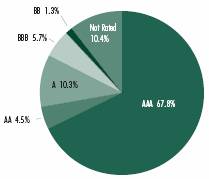

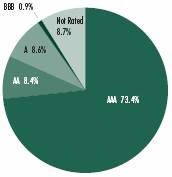

Rating Distribution(7),(8)

By total investments

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(2) It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only.

(3) The Lipper Averages are the average total returns of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper Intermediate Municipal Debt Funds Classification contained 150, 104 and 70 funds for the 1-year, 5-year and 10-year time periods, respectively. Lipper Averages are available as of month end only.

(4) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share in the period (annualized) by the net asset value at the end of the period.

(5) Taxable-equivalent figure assumes a maximum 35.00% federal income tax rate. A lower tax rate would result in lower tax-equivalent figures.

(6) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result.

(7) As of 3/31/06. Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund.

(8) Portfolio information may not be representative of the Fund’s current or future investments and may change due to active management.

3

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

FUND EXPENSES

Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2005 – March 31, 2006).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Eaton Vance National Limited Maturity Municipals Fund

| | Beginning Account Value | | Ending Account Value | | Expenses Paid During Period* | |

| | (10/1/05) | | (3/31/06) | | (10/1/05 - 3/31/06) | |

| | | | | | | |

Actual | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,021.90 | | $ | 3.93 | |

Class B | | $ | 1,000.00 | | $ | 1,017.10 | | $ | 7.69 | |

Class C | | $ | 1,000.00 | | $ | 1,017.20 | | $ | 7.69 | |

| | | | | | | |

Hypothetical | | | | | | | |

(5% return per year before expenses) | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,021.00 | | $ | 3.93 | |

Class B | | $ | 1,000.00 | | $ | 1,017.30 | | $ | 7.70 | |

Class C | | $ | 1,000.00 | | $ | 1,017.30 | | $ | 7.70 | |

* Expenses are equal to the Fund’s annualized expense ratio of 0.78% for Class A shares, 1.53% for Class B shares and 1.53% for Class C shares, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on September 30, 2005.

4

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PORTFOLIO OF INVESTMENTS

| Tax-Exempt Investments — 99.4% | | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Cogeneration — 1.8% | | | |

| $ | 3,095 | | | Carbon County, PA, IDA, (Panther Creek Partners), (AMT),

6.65%, 5/1/10 | | $ | 3,266,061 | | |

| | 985 | | | Ohio Water Development Authority, Solid Waste Disposal,

(Bay Shore Power), (AMT), 6.625%, 9/1/20 | | | 1,019,918 | | |

| | 675 | | | Pennsylvania EDA, (Resource Recovery-Colver), (AMT),

5.125%, 12/1/15 | | | 670,336 | | |

| | | | | | | $ | 4,956,315 | | |

| Education — 3.4% | | | |

| $ | 2,000 | | | Illinois Educational Facility Authority, (Art Institute of

Chicago), 4.45%, 3/1/34 | | $ | 1,999,640 | | |

| | 420 | | | Maryland Industrial Development Financing Authority,

(Our Lady of Good Counsel High School),

5.50%, 5/1/20 | | | 438,749 | | |

| | 2,815 | | | Missouri Health and Educational Facilities Authority,

(St. Louis University), 5.50%, 10/1/16 | | | 3,126,930 | | |

| | 850 | | | New Hampshire HEFA, (Colby-Sawyer College),

7.20%, 6/1/12 | | | 870,340 | | |

| | 1,235 | | | New Jersey Educational Facilities Authority,

(Steven's Institute of Technology), 5.00%, 7/1/12 | | | 1,288,389 | | |

| | 1,700 | | | University of Illinois, 0.00%, 4/1/15 | | | 1,147,517 | | |

| | 1,000 | | | University of Illinois, 0.00%, 4/1/16 | | | 640,500 | | |

| | | | | | | $ | 9,512,065 | | |

| Electric Utilities — 7.7% | | | |

| $ | 1,000 | | | Brazos River Authority, TX, (Reliant Energy, Inc.),

7.75%, 12/1/18 | | $ | 1,087,990 | | |

| | 3,000 | | | Energy Northwest Washington Electric, (Columbia

Generating), 5.50%, 7/1/15 | | | 3,307,050 | | |

| | 1,000 | | | Illinois Development Finance Authority PCR, (AMT),

5.00%, 6/1/28 | | | 1,004,170 | | |

| | 2,500 | | | New Hampshire Business Finance Authority Pollution

Control, (Central Maine Power Co.), 5.375%, 5/1/14 | | | 2,615,375 | | |

| | 3,050 | | | New York Energy Research and Development Authority

Facility, (AMT), Variable Rate, 4.70%, 6/1/36 | | | 3,050,793 | | |

| | 4,000 | | | North Carolina Municipal Power Agency, (Catawba),

5.50%, 1/1/13 | | | 4,286,840 | | |

| | 1,000 | | | North Carolina Municipal Power Agency, (Catawba),

6.375%, 1/1/13 | | | 1,082,310 | | |

| | 1,250 | | | Sam Rayburn, TX, Municipal Power Agency, Power

Supply System, 6.00%, 10/1/16 | | | 1,328,975 | | |

| | 1,000 | | | San Antonio, TX, Electric and Natural Gas,

4.50%, 2/1/21 | | | 1,002,190 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Electric Utilities (continued) | | | |

| $ | 2,500 | | | Wake County, NC, Industrial Facilities and Pollution

Control Financing Authority, (Carolina Power and

Light Co.), 5.375%, 2/1/17 | | $ | 2,638,700 | | |

| | | | | | | $ | 21,404,393 | | |

| Escrowed / Prerefunded — 7.3% | | | |

| $ | 1,000 | | | Arkansas State Student Loan Authority, (AMT),

Prerefunded to 6/1/06, 6.25%, 6/1/10 | | $ | 1,003,850 | | |

| | 1,500 | | | California Department of Water Resource Power Supply,

Prerefunded to 5/1/12, 5.125%, 5/1/18 | | | 1,626,420 | | |

| | 1,650 | | | Capital Trust Agency, FL, (Seminole Tribe Convention),

Prerefunded to 10/1/12, 8.95%, 10/1/33 | | | 2,056,840 | | |

| | 220 | | | Florence, KY, Housing Facilities, (Bluegrass Housing),

Escrowed to Maturity, 7.25%, 5/1/07 | | | 220,350 | | |

| | 360 | | | Forsyth County, GA, Hospital Authority, (Georgia Baptist

Health Care System), Escrowed to Maturity,

6.00%, 10/1/08 | | | 371,218 | | |

| | 500 | | | Kershaw County, SC, School District, Prerefunded to

2/1/10, 5.00%, 2/1/18 | | | 523,280 | | |

| | 3,500 | | | Maricopa County, AZ, IDA, Multifamily,

Escrowed to Maturity, 6.45%, 1/1/17 | | | 3,677,765 | | |

| | 495 | | | Maricopa County, AZ, IDA, Multifamily,

Escrowed to Maturity, 7.875%, 1/1/11 | | | 536,045 | | |

| | 3,000 | | | Massachusetts Turnpike Authority,

Escrowed to Maturity, 5.00%, 1/1/20 | | | 3,222,240 | | |

| | 230 | | | Mesquite, TX, Health Facilities Development,

(Christian Care Centers), Escrowed to Maturity,

7.00%, 2/15/10 | | | 245,803 | | |

| | 2,000 | | | New Jersey Transportation Trust Fund Authority,

(Transportation System), Prerefunded to 6/15/13,

5.50%, 6/15/14 | | | 2,205,140 | | |

| | 1,195 | | | North Carolina Eastern Municipal Power Agency,

Escrowed to Maturity, 4.00%, 1/1/18 | | | 1,181,138 | | |

| | 1,000 | | | Northwest Arkansas Regional Airport Authority, (AMT),

Prerefunded to 2/1/08, 7.625%, 2/1/27 | | | 1,085,620 | | |

| | 2,000 | | | Orange County, FL, Health Facilities Authority,

(Adventist Health System), Prerefunded to 11/15/10,

6.375%, 11/15/20 | | | 2,238,100 | | |

| | 5 | | | Pennsylvania EDA, (Resource Recovery- Northampton),

(AMT), Escrowed to Maturity, 6.75%, 1/1/07 | | | 5,033 | | |

| | | | | | | $ | 20,198,842 | | |

| General Obligations — 1.5% | | | |

| $ | 1,000 | | | Keller, TX, Independent School District, 0.00%, 8/15/11 | | $ | 811,120 | | |

| | 1,650 | | | McAllen, TX, Independent School District, (PSF),

4.50%, 2/15/18 | | | 1,655,659 | | |

| | 1,500 | | | New York City, NY, 5.625%, 12/1/13 | | | 1,615,155 | | |

| | | | | | | $ | 4,081,934 | | |

See notes to financial statements

5

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Health Care-Miscellaneous — 0.2% | | | |

| $ | 85 | | | Pittsfield Township, MI, EDC, (Arbor Hospice),

7.875%, 8/15/27 | | $ | 87,860 | | |

| | 502 | | | Tax Revenue Exempt Securities Trust, Community Health

Provider, (Pooled Loan Program Various States Trust

Certificates), 6.00%, 12/1/36 | | | 524,921 | | |

| | | | | | | $ | 612,781 | | |

| Hospital — 6.8% | | | |

| $ | 550 | | | Colorado Health Facilities Authority, (Parkview Episcopal

Medical Center), 5.75%, 9/1/09 | | $ | 578,600 | | |

| | 2,500 | | | Cuyahoga County, OH, (Cleveland Clinic Health System),

6.00%, 1/1/17 | | | 2,794,300 | | |

| | 100 | | | Michigan Hospital Finance Authority, (Central Michigan

Community Hospital), 6.10%, 10/1/06 | | | 100,760 | | |

| | 225 | | | Michigan Hospital Finance Authority, (Central Michigan

Community Hospital), 6.20%, 10/1/07 | | | 229,736 | | |

| | 370 | | | Michigan Hospital Finance Authority, (Gratiot

Community Hospital), 6.10%, 10/1/07 | | | 379,857 | | |

| | 2,000 | | | Michigan Hospital Finance Authority, (Henry Ford

Health System), 5.50%, 3/1/14 | | | 2,132,600 | | |

| | 1,000 | | | Michigan Hospital Finance Authority, (Memorial

Healthcare Center), 5.875%, 11/15/21 | | | 1,046,940 | | |

| | 2,490 | | | Michigan Hospital Finance Authority, Variable Rate,

8.155%, 11/1/12(1)(2) | | | 2,856,677 | | |

| | 200 | | | New Hampshire HEFA, (Littleton Hospital Association),

5.45%, 5/1/08 | | | 202,224 | | |

| | 2,000 | | | Orange County, FL, Health Facilities Authority,

(Adventist Health System), 5.25%, 11/15/18 | | | 2,113,760 | | |

| | 1,130 | | | Orange County, FL, Health Facilities Authority,

(Nemours Foundation), 5.00%, 1/1/18 | | | 1,195,133 | | |

| | 1,740 | | | Saginaw, MI, Hospital Finance Authority,

5.125%, 7/1/22 | | | 1,794,166 | | |

| | 775 | | | Salina, KS, Hospital Revenue, Salina Regional Health,

5.00%, 10/1/18(3) | | | 807,705 | | |

| | 2,000 | | | South Carolina Jobs-Economic Development Authority,

(Palmetto Health Alliance), 6.00%, 8/1/12 | | | 2,195,560 | | |

| | 500 | | | Washington County, AR, (Washington Regional

Medical Center), 5.00%, 2/1/16 | | | 511,910 | | |

| | | | | | | $ | 18,939,928 | | |

| Housing — 1.4% | | | |

| $ | 600 | | | Georgia Private Colleges and Universities Authority,

Student Housing Revenue, (Mercer Housing Corp.),

6.00%, 6/1/31 | | $ | 621,000 | | |

| | 670 | | | Sandoval County, NM, Multifamily, 6.00%, 5/1/32 | | | 667,769 | | |

| | 95 | | | Texas Student Housing Corp., (University of

Northern Texas), 9.375%, 7/1/06(4) | | | 84,740 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Housing (continued) | | | |

| $ | 2,400 | | | Vancouver, WA, Housing Authority, 4.20%, 3/1/08 | | $ | 2,397,336 | | |

| | | | | | | $ | 3,770,845 | | |

| Industrial Development Revenue — 9.5% | | | |

| $ | 220 | | | Austin, TX, (Cargoport Development LLC), (AMT),

7.50%, 10/1/07 | | $ | 224,352 | | |

| | 425 | | | Austin, TX, (Cargoport Development LLC), (AMT),

8.30%, 10/1/21 | | | 459,412 | | |

| | 1,500 | | | Dallas-Fort Worth, TX, International Airport Facilities

Improvement Corp., (AMT), 9.00%, 5/1/29 | | | 1,628,640 | | |

| | 1,320 | | | Denver, CO, City and County Special Facilities,

(United Airlines), (AMT), 6.875%, 10/1/32(4) | | | 1,344,750 | | |

| | 1,630 | | | Houston, TX, Industrial Development Corp., (AMT),

6.375%, 1/1/23 | | | 1,746,170 | | |

| | 5,000 | | | Liberty, NY, Development Corp., (Goldman Sachs

Group, Inc.), 5.25%, 10/1/35 | | | 5,508,900 | | |

| | 1,000 | | | Michigan Strategic Fund, (Waste Management, Inc.),

(AMT), 4.50%, 12/1/13 | | | 1,004,130 | | |

| | 1,435 | | | Mississippi Business Finance Corp., (Air Cargo), (AMT),

7.25%, 7/1/34 | | | 1,478,724 | | |

| | 1,440 | | | New Jersey EDA, (Continental Airlines), (AMT),

6.25%, 9/15/19 | | | 1,438,646 | | |

| | 1,000 | | | New Jersey EDA, (Holt Hauling), (AMT),

7.90%, 3/1/27(4) | | | 966,000 | | |

| | 3,000 | | | New York, NY, Industrial Development Agency,

(American Airlines), (AMT), 7.50%, 8/1/16 | | | 3,301,170 | | |

| | 2,750 | | | New York, NY, Industrial Development Agency,

(Terminal One Group), (AMT), 5.50%, 1/1/14 | | | 2,930,840 | | |

| | 1,500 | | | Nez Perce County, ID, PCR, (Potlatch Corp.),

6.125%, 12/1/07 | | | 1,527,840 | | |

| | 2,825 | | | Toledo Lucas County, OH, Port Authority, (Cargill, Inc.),

4.50%, 12/1/15 | | | 2,846,442 | | |

| | | | | | | $ | 26,406,016 | | |

| Insured-Cogeneration — 0.6% | | | |

| $ | 1,600 | | | Pennsylvania EDA, (Resource Recovery-Colver),

(AMBAC), (AMT), 4.625%, 12/1/18 | | $ | 1,595,200 | | |

| | | | | | | $ | 1,595,200 | | |

| Insured-Education — 1.7% | | | |

| $ | 2,025 | | | New York Dormitory Authority, (Educational

Housing Services), (AMBAC), 5.25%, 7/1/21 | | $ | 2,225,272 | | |

| | 2,000 | | | New York Dormitory Authority, (SUNY, NY), (XLCA),

5.25%, 7/1/32 | | | 2,161,740 | | |

| | 500 | | | Southern Illinois University, Housing and Auxiliary

Facilities, (MBIA), 0.00%, 4/1/17 | | | 306,000 | | |

| | | | | | | $ | 4,693,012 | | |

See notes to financial statements

6

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Insured-Electric Utilities — 4.1% | | | |

| $ | 750 | | | California Pollution Control Financing Authority, PCR,

(Pacific Gas and Electric), (MBIA), (AMT),

5.35%, 12/1/16 | | $ | 797,392 | | |

| | 2,000 | | | Forsyth, MT, PCR, (Avista Corp.), (AMBAC),

5.00%, 10/1/32(5) | | | 2,053,300 | | |

| | 1,600 | | | Long Island Power Authority, NY, (FGIC), Variable Rate,

8.39%, 12/1/19(1)(2) | | | 1,896,448 | | |

| | 400 | | | Piedmont, SC, Municipal Power Agency, (MBIA),

5.00%, 1/1/15 | | | 409,344 | | |

| | 1,000 | | | Puerto Rico Electric Power Authority, (XLCA),

5.375%, 7/1/18 | | | 1,106,000 | | |

| | 5,000 | | | Sacramento, CA, Municipal Utility District, (Consumnes),

(MBIA), 4.75%, 7/1/23 | | | 5,120,000 | | |

| | | | | | | $ | 11,382,484 | | |

| Insured-Escrowed / Prerefunded — 3.6% | | | |

| $ | 1,000 | | | Laredo, TX, Certificates of Obligation, (MBIA),

Prerefunded to 2/15/08, 4.50%, 2/15/17 | | $ | 1,015,390 | | |

| | 1,000 | | | Metropolitan Transportation Authority, NY, Commuter

Facilities, (AMBAC), Escrowed to Maturity,

5.00%, 7/1/20 | | | 1,035,970 | | |

| | 1,000 | | | Metropolitan Transportation Authority, NY, Transit

Facilities, (FGIC), Prerefunded to 10/1/15,

4.50%, 4/1/18 | | | 1,039,760 | | |

| | 500 | | | Metropolitan Transportation Authority, NY, Transit

Facilities, (MBIA), Escrowed to Maturity,

5.00%, 7/1/17 | | | 518,110 | | |

| | 1,000 | | | Montgomery, AL, BMC Special Care Facilities Financing

Authority, (Baptist Health Montgomery), (MBIA),

Prerefunded to 11/15/14, 0.00%, 11/15/22 | | | 975,370 | | |

| | 3,000 | | | Montgomery, AL, BMC Special Care Facilities Financing

Authority, (Baptist Health Montgomery), (MBIA),

Prerefunded to 11/15/14, 0.00%, 11/15/17 | | | 2,926,110 | | |

| | 2,000 | | | Montogmery, AL, BMC Special Care Facilities Financing

Authority, (Baptist Health Montgomery), (MBIA),

Prerefunded to 11/15/14, 0.00%, 11/15/18(6) | | | 1,950,740 | | |

| | 625 | | | Reno, NV, Capital Improvements, (FGIC),

Prerefunded to 6/1/12, 5.625%, 6/1/14 | | | 686,500 | | |

| | | | | | | $ | 10,147,950 | | |

| Insured-General Obligations — 10.2% | | | |

| $ | 1,000 | | | Clackamas County, OR, (School District No. 7J

Lake Oswego), (FSA), 5.25%, 6/1/21 | | $ | 1,110,300 | | |

| | 1,000 | | | Hillsborough Township, NJ, School District, (FSA),

5.375%, 10/1/18 | | | 1,124,260 | | |

| | 1,055 | | | Linn County, OR, Community School District No. 9,

(Lebanon), (FGIC), 5.25%, 6/15/21 | | | 1,171,577 | | |

| | 1,175 | | | Linn County, OR, Community School District No. 9,

(Lebanon), (FGIC), 5.25%, 6/15/22 | | | 1,306,424 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Insured-General Obligations (continued) | | | |

| $ | 5,580 | | | New Orleans, LA, (MBIA), 5.25%, 12/1/15 | | $ | 5,999,002 | | |

| | 5,000 | | | New York City, NY, (MBIA), 5.00%, 8/1/18 | | | 5,308,900 | | |

| | 1,815 | | | Pima County, AZ, (FSA), 3.50%, 7/1/20 | | | 1,633,500 | | |

| | 5,000 | | | Puerto Rico Public Buildings Authority, (CIFG),

5.25%, 7/1/21 | | | 5,500,400 | | |

| | 3,150 | | | Springfield, OH, City School District, Clark County,

(AMBAC), 4.30%, 12/1/14 | | | 3,165,687 | | |

| | 1,400 | | | Springfield, OH, City School District, Clark County,

(FGIC), 5.00%, 12/1/17 | | | 1,480,682 | | |

| | 1,000 | | | St. Louis, MO, Board of Education, (FSA),

0.00%, 4/1/16 | | | 647,430 | | |

| | | | | | | $ | 28,448,162 | | |

| Insured-Hospital — 0.7% | | | |

| $ | 2,000 | | | El Paso County, TX, Hospital District, (MBIA),

0.00%, 8/15/06 | | $ | 1,974,240 | | |

| | | | | | | $ | 1,974,240 | | |

Insured-Lease Revenue / Certificates of

Participation — 0.9% | | | |

| $ | 1,380 | | | Anaheim, CA, Public Financing Authority, (Public

Improvements), (FSA), 0.00%, 9/1/19 | | $ | 747,919 | | |

| | 2,100 | | | Texas Public Finance Authority, (MBIA),

0.00%, 2/1/12 | | | 1,666,140 | | |

| | | | | | | $ | 2,414,059 | | |

| Insured-Miscellaneous — 0.4% | | | |

| $ | 1,000 | | | Missouri Development Finance Board Cultural Facility,

(Nelson Gallery Foundation), (MBIA), 5.25%, 12/1/14 | | $ | 1,066,370 | | |

| | | | | | | $ | 1,066,370 | | |

| Insured-Solid Waste — 0.5% | | | |

| $ | 1,175 | | | Massachusetts Development Finance Agency,

(Semass System), (MBIA), 5.625%, 1/1/12 | | $ | 1,272,443 | | |

| | | | | | | $ | 1,272,443 | | |

| Insured-Special Tax Revenue — 1.6% | | | |

| $ | 3,000 | | | Arlington, TX, (Dallas Cowboys), (MBIA),

5.00%, 8/15/34 | | $ | 3,152,880 | | |

| | 1,000 | | | Julington Creek Plantation, FL, Community Development

District, (MBIA), 4.75%, 5/1/19 | | | 1,023,820 | | |

| | 375 | | | Reno, NV, Capital Improvements, (FGIC),

5.625%, 6/1/12 | | | 409,552 | | |

| | | | | | | $ | 4,586,252 | | |

See notes to financial statements

7

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Insured-Transportation — 12.2% | | | |

| $ | 2,295 | | | Chicago, IL, O'Hare International Airport, (MBIA),

(AMT), 5.75%, 1/1/17 | | $ | 2,470,636 | | |

| | 1,000 | | | Denver, CO, City and County Airport, (FSA), (AMT),

5.00%, 11/15/11 | | | 1,045,910 | | |

| | 1,000 | | | Houston, TX, Airport System, (FGIC), (AMT),

5.50%, 7/1/12 | | | 1,066,520 | | |

| | 2,000 | | | Kenton County, KY, Airport, (Cincinnati/Northern Kentucky),

(MBIA), (AMT), 5.625%, 3/1/13 | | | 2,145,160 | | |

| | 2,500 | | | Massachusetts Port Authority, (Delta Airlines), (AMBAC),

(AMT), 5.50%, 1/1/15 | | | 2,623,300 | | |

| | 1,000 | | | Miami-Dade County, FL, Aviation, (Miami International

Airport), (FGIC), (AMT), 5.50%, 10/1/13 | | | 1,074,460 | | |

| | 2,000 | | | Minneapolis and St. Paul, MN, Metropolitan Airport

Commission, (FGIC), (AMT), 5.25%, 1/1/11 | | | 2,111,920 | | |

| | 1,430 | | | Minneapolis and St. Paul, MN, Metropolitan Airports

Commission Airport, (FGIC), (AMT), 6.00%, 1/1/11 | | | 1,539,095 | | |

| | 5,000 | | | New Jersey Transportation Trust Fund Authority, (FGIC),

5.50%, 12/15/20(7) | | | 5,657,350 | | |

| | 1,000 | | | Ohio Turnpike Commission, (FGIC), 5.50%, 2/15/18 | | | 1,122,990 | | |

| | 5,000 | | | Port Authority New York and New Jersey, (FGIC), (AMT),

4.50%, 10/1/20 | | | 4,944,900 | | |

| | 1,000 | | | Port Seattle, WA, (MBIA), (AMT), 6.00%, 2/1/11 | | | 1,086,590 | | |

| | 4,450 | | | Puerto Rico Commonwealth Highway and Transportation

Authority, (FSA), 5.50%, 7/1/19 | | | 5,016,040 | | |

| | 2,000 | | | Wayne Charter County, MI, Metropolitan Airport, (FGIC),

(AMT), 5.50%, 12/1/15 | | | 2,143,100 | | |

| | | | | | | $ | 34,047,971 | | |

| Insured-Water and Sewer — 0.6% | | | |

| $ | 2,000 | | | Honolulu, HI, Wastewater System, (FGIC),

0.00%, 7/1/11 | | $ | 1,630,400 | | |

| | | | | | | $ | 1,630,400 | | |

| Lease Revenue / Certificates of Participation — 4.3% | | | |

| $ | 7,870 | | | California Public Works Board, (Department Health

Services), 5.00%, 11/1/19 | | $ | 8,232,571 | | |

| | 3,385 | | | New Jersey EDA, (School Facilities Construction),

5.50%, 9/1/19 | | | 3,768,250 | | |

| | | | | | | $ | 12,000,821 | | |

| Nursing Home — 0.5% | | | |

| $ | 810 | | | Clovis, NM, IDR, (Retirement Ranches, Inc.),

7.75%, 4/1/19 | | $ | 847,098 | | |

| | 485 | | | Wisconsin HEFA, (Wisconsin Illinois Senior Housing),

7.00%, 8/1/29 | | | 498,886 | | |

| | | | | | | $ | 1,345,984 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Other Revenue — 2.3% | | | |

| $ | 1,000 | | | Arizona Health Facilities Authority, (Blood Systems, Inc.),

5.00%, 4/1/21 | | $ | 1,022,830 | | |

| | 890 | | | Barona, CA, (Band of Mission Indians), 8.25%, 1/1/20 | | | 926,339 | | |

| | 1,960 | | | California Statewide Communities Development Authority,

(East Valley Tourist Development Authority),

8.25%, 10/1/14 | | | 2,111,077 | | |

| | 1,220 | | | Central Falls, RI, Detention Facility Revenue,

7.25%, 7/15/35 | | | 1,340,085 | | |

| | 1,000 | | | Mohegan Tribe, CT, Gaming Authority,

5.375%, 1/1/11 | | | 1,048,520 | | |

| | | | | | | $ | 6,448,851 | | |

| Pooled Loans — 1.4% | | | |

| $ | 1,900 | | | Arizona Educational Loan Marketing Corp., (AMT),

6.25%, 6/1/06 | | $ | 1,904,655 | | |

| | 1,300 | | | Ohio Economic Development, (Ohio Enterprise Bond

Fund), (AMT), 4.60%, 6/1/20 | | | 1,322,412 | | |

| | 790 | | | Ohio Economic Development, (Ohio Enterprise Bond

Fund), (AMT), 5.25%, 12/1/15 | | | 807,878 | | |

| | | | | | | $ | 4,034,945 | | |

| Senior Living / Life Care — 1.2% | | | |

| $ | 760 | | | Albuquerque, NM, Retirement Facilities, (La Vida Liena

Retirement Center), 6.60%, 12/15/28 | | $ | 784,913 | | |

| | 1,105 | | | Arizona Health Facilities Authority,

(Care Institute, Inc.-Mesa), 7.625%, 1/1/06(4) | | | 977,616 | | |

| | 500 | | | Kansas City, MO, IDR, (Kingswood Manor),

5.80%, 11/15/17 | | | 482,365 | | |

| | 240 | | | Massachusetts IFA, (Forge Hill), (AMT),

6.75%, 4/1/30 | | | 242,251 | | |

| | 480 | | | North Miami, FL, Health Facilities Authority,

(Imperial Club), 6.75%, 1/1/33 | | | 466,637 | | |

| | 460 | | | St. Joseph County, IN, Holy Cross Village,

5.55%, 5/15/19 | | | 464,025 | | |

| | | | | | | $ | 3,417,807 | | |

| Solid Waste — 1.1% | | | |

| $ | 3,000 | | | Niagara County, NY, IDA, (American Ref-Fuel Co. LLC),

(AMT), 5.55%, 11/15/24 | | $ | 3,152,220 | | |

| | | | | | | $ | 3,152,220 | | |

| Special Tax Revenue — 9.6% | | | |

| $ | 1,450 | | | Brentwood, CA, Infrastructure Financing Authority,

6.375%, 9/2/33 | | $ | 1,495,399 | | |

| | 2,500 | | | Bridgeville, DE, (Heritage Shores Special

Development District), 5.125%, 7/1/35 | | | 2,508,925 | | |

See notes to financial statements

8

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

PORTFOLIO OF INVESTMENTS CONT'D

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Special Tax Revenue (continued) | | | |

| $ | 3,000 | | | California State Economic Recovery,

5.25%, 7/1/13 | | $ | 3,252,450 | | |

| | 555 | | | Concorde Estates Community Development District, FL,

Capital Improvements, 5.00%, 5/1/11 | | | 558,563 | | |

| | 500 | | | Cottonwood, CO, Water and Sanitation District,

7.75%, 12/1/20 | | | 515,735 | | |

| | 300 | | | Covington Park Community Development District, FL,

Capital Improvements, 5.00%, 5/1/21 | | | 299,829 | | |

| | 2,000 | | | Detroit, MI, Downtown Development Authority

Tax Increment, 0.00%, 7/1/21 | | | 914,180 | | |

| | 1,400 | | | Dupree Lakes Community Development District, FL,

5.00%, 11/1/10 | | | 1,404,774 | | |

| | 50 | | | Fishhawk, FL, Community Development District,

5.00%, 11/1/07 | | | 50,231 | | |

| | 1,820 | | | Fishhawk, FL, Community Development District II,

5.125%, 11/1/09 | | | 1,841,385 | | |

| | 250 | | | Frederick County, MD, Urbana Community Development

Authority, 6.625%, 7/1/25 | | | 261,048 | | |

| | 265 | | | Gateway, FL, Services Community Development District,

(Stoneybrook), 5.50%, 7/1/08 | | | 266,852 | | |

| | 1,610 | | | Heritage Harbour, FL, South Community Development

District, Capital Improvements, 5.25%, 11/1/08 | | | 1,620,385 | | |

| | 1,105 | | | Jurupa, CA, Community Services District,

5.00%, 9/1/21 | | | 1,117,785 | | |

| | 785 | | | Jurupa, CA, Community Services District,

5.00%, 9/1/25 | | | 787,135 | | |

| | 95 | | | Longleaf, FL, Community Development District,

6.20%, 5/1/09 | | | 95,286 | | |

| | 3,000 | | | New Jersey EDA, (Cigarette Tax), 5.50%, 6/15/16 | | | 3,234,210 | | |

| | 1,000 | | | New York Local Government Assistance Corp.,

5.25%, 4/1/16 | | | 1,085,020 | | |

| | 1,750 | | | Sterling Hill Community Development District, FL,

Capital Improvements, 5.50%, 11/1/10 | | | 1,763,213 | | |

| | 2,900 | | | Tisons Landing Community Development District, FL,

5.00%, 11/1/11 | | | 2,920,648 | | |

| | 850 | | | Tiverton, RI, Obligation Tax Increment, (Mount Hope

Bay Village), 6.00%, 5/1/09 | | | 864,620 | | |

| | | | | | | $ | 26,857,673 | | |

| Transportation — 1.4% | | | |

| $ | 100 | | | Eagle County, CO, Airport Terminal Corp.,

(American Airlines), (AMT), 6.75%, 5/1/06 | | $ | 100,097 | | |

| | 2,500 | | | Louisiana Offshore Terminal Authority, Deepwater Port

Revenue, (Loop, LLC), 5.25%, 9/1/15 | | | 2,608,700 | | |

| | 1,000 | | | Port Authority of New York and New Jersey,

5.375%, 3/1/28 | | | 1,124,830 | | |

| | | | | | | $ | 3,833,627 | | |

Principal Amount

(000's omitted) | |

Security | |

Value | |

| Water and Sewer — 0.9% | |

| $ | 2,500 | | | New Orleans, LA, Sewer Service Revenue,

3.00%, 7/26/06 | | $ | 2,453,969 | | |

| | | | | $ | 2,453,969 | | |

Total Tax-Exempt Investments — 99.4%

(identified cost $269,502,246) | | | | $ | 276,687,559 | | |

| Other Assets, Less Liabilities — 0.6% | | | | $ | 1,702,995 | | |

| Net Assets — 100.0% | | | | $ | 278,390,554 | | |

AMBAC - AMBAC Financial Group, Inc.

AMT - Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax.

CIFG - CDC IXIS Financial Guaranty North America, Inc.

FGIC - Financial Guaranty Insurance Company

FSA - Financial Security Assurance, Inc.

MBIA - Municipal Bond Insurance Association

XLCA - XL Capital Assurance, Inc.

At March 31, 2006, the concentration of the Fund's investments in the various states, determined as a percentage of net assets, is as follows:

| New York | | | 14.7 | % | |

| Others, representing less than 10% individually | | | 84.7 | % | |

The Fund invests primarily in debt securities issued by municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at March 31, 2006, 37.3% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution ranged from 1.2% to 14.9% of total investments.

(1) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At March 31, 2006, the aggregate value of the securities is $4,753,125 or 1.7% of the Fund's net assets.

(2) Security has been issued as a leveraged inverse floater bond. The stated interest rate represents the rate in effect at March 31, 2006.

(3) When-issued security.

(4) Defaulted bond.

(5) Security (or a portion thereof) has been segregated to cover margin requirements on open financial futures contracts.

(6) Step bond.

(7) Security (or a portion thereof) has been segregated to cover when-issued securities.

See notes to financial statements

9

National Limited Maturity Municipals Fund as of March 31, 2006

FINANCIAL STATEMENTS

Statement of Assets and Liabilities

As of March 31, 2006

| Assets | |

Investments, at value

(identified cost, $269,502,246) | | $ | 276,687,559 | | |

| Cash | | | 88,823 | | |

| Receivable for investments sold | | | 67,701 | | |

| Receivable for Fund shares sold | | | 1,007,612 | | |

| Interest receivable | | | 4,180,426 | | |

| Prepaid expenses | | | 8,433 | | |

| Total assets | | $ | 282,040,554 | | |

| Liabilities | |

| Payable for Fund shares redeemed | | $ | 1,029,826 | | |

| Demand note payable | | | 1,000,000 | | |

| Payable for when-issued securities | | | 810,960 | | |

| Dividends payable | | | 451,087 | | |

| Payable to affiliate for distribution and service fees | | | 146,372 | | |

| Payable to affiliate for investment advisory fees | | | 106,346 | | |

| Payable for daily variation margin on open financial futures contracts | | | 5,392 | | |

| Accrued expenses | | | 100,017 | | |

| Total liabilities | | $ | 3,650,000 | | |

| Net Assets | | $ | 278,390,554 | | |

| Sources of Net Assets | |

| Paid-in capital | | $ | 274,374,849 | | |

| Accumulated net realized loss (computed on the basis of identified cost) | | | (4,400,316 | ) | |

| Accumulated distributions in excess of net investment income | | | (98,345 | ) | |

| Net unrealized appreciation (computed on the basis of identified cost) | | | 8,514,366 | | |

| Total | | $ | 278,390,554 | | |

| Class A Shares | |

| Net Assets | | $ | 180,401,150 | | |

| Shares Outstanding | | | 17,537,012 | | |

Net Asset Value and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 10.29 | | |

Maximum Offering Price Per Share

(100 ÷ 97.75 of $10.29) | | $ | 10.53 | | |

| Class B Shares | |

| Net Assets | | $ | 20,609,997 | | |

| Shares Outstanding | | | 2,002,147 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 10.29 | | |

| Class C Shares | |

| Net Assets | | $ | 77,379,407 | | |

| Shares Outstanding | | | 8,022,873 | | |

Net Asset Value, Offering Price and Redemption Price Per Share

(net assets ÷ shares of beneficial interest outstanding) | | $ | 9.64 | | |

| On sales of $100,000 or more, the offering price of Class A shares is reduced. | �� |

Statement of Operations

For the Year Ended

March 31, 2006

| Investment Income | |

| Interest | | $ | 12,916,520 | | |

| Total investment income | | $ | 12,916,520 | | |

| Expenses | |

| Investment adviser fee | | $ | 1,202,204 | | |

| Trustees' fees and expenses | | | 16,609 | | |

| Distribution and service fees | |

| Class A | | | 249,971 | | |

| Class B | | | 222,274 | | |

| Class C | | | 715,306 | | |

| Custodian fee | | | 172,935 | | |

| Transfer and dividend disbursing agent fees | | | 123,657 | | |

| Registration fees | | | 74,719 | | |

| Legal and accounting services | | | 56,454 | | |

| Printing and postage | | | 31,625 | | |

| Miscellaneous | | | 54,094 | | |

| Total expenses | | $ | 2,919,848 | | |

Deduct —

Reduction of custodian fee | | $ | 38,125 | | |

| Total expense reductions | | $ | 38,125 | | |

| Net expenses | | $ | 2,881,723 | | |

| Net investment income | | $ | 10,034,797 | | |

| Realized and Unrealized Gain (Loss) | |

Net realized gain (loss) —

Investment transactions (identified cost basis) | | $ | 537,358 | | |

| Financial futures contracts | | | (102,238 | ) | |

| Net realized gain | | $ | 435,120 | | |

Change in unrealized appreciation (depreciation) —

Investments (identified cost basis) | | $ | 289,105 | | |

| Financial futures contracts | | | 995,842 | | |

| Net change in unrealized appreciation (depreciation) | | $ | 1,284,947 | | |

| Net realized and unrealized gain | | $ | 1,720,067 | | |

| Net increase in net assets from operations | | $ | 11,754,864 | | |

See notes to financial statements

10

National Limited Maturity Municipals Fund as of March 31, 2006

FINANCIAL STATEMENTS CONT'D

Statements of Changes in Net Assets

Increase (Decrease)

in Net Assets | | Year Ended

March 31, 2006 | | Year Ended

March 31, 2005 | |

From operations —

Net investment income | | $ | 10,034,797 | | | $ | 8,972,540 | | |

Net realized gain (loss) from investment

transactions and financial

futures contracts | | | 435,120 | | | | (265,297 | ) | |

Net change in unrealized appreciation

(depreciation) from investments and

financial futures contracts | | | 1,284,947 | | | | (4,315,100 | ) | |

| Net increase in net assets from operations | | $ | 11,754,864 | | | $ | 4,392,143 | | |

Distributions to shareholders —

From net investment income

Class A | | $ | (6,615,915 | ) | | $ | (5,454,047 | ) | |

| Class B | | | (798,175 | ) | | | (1,048,876 | ) | |

| Class C | | | (2,566,759 | ) | | | (2,470,667 | ) | |

| Total distributions to shareholders | | $ | (9,980,849 | ) | | $ | (8,973,590 | ) | |

Transactions in shares of beneficial interest —

Proceeds from sale of shares

Class A | | $ | 73,645,825 | | | $ | 64,046,619 | | |

| Class B | | | 2,975,642 | | | | 7,250,045 | | |

| Class C | | | 19,330,607 | | | | 25,915,496 | | |

Net asset value of shares issued to

shareholders in payment of

distributions declared

Class A | | | 3,903,927 | | | | 3,133,855 | | |

| Class B | | | 470,142 | | | | 558,191 | | |

| Class C | | | 1,154,523 | | | | 1,076,697 | | |

Cost of shares redeemed

Class A | | | (54,759,567 | ) | | | (50,093,129 | ) | |

| Class B | | | (5,719,091 | ) | | | (6,533,382 | ) | |

| Class C | | | (20,978,060 | ) | | | (15,450,266 | ) | |

Net asset value of shares exchanged

Class A | | | 4,473,296 | | | | 7,265,517 | | |

| Class B | | | (4,473,296 | ) | | | (7,265,517 | ) | |

Net increase in net assets from

Fund share transactions | | $ | 20,023,948 | | | $ | 29,904,126 | | |

| Net increase in net assets | | $ | 21,797,963 | | | $ | 25,322,679 | | |

| Net Assets | |

| At beginning of year | | $ | 256,592,591 | | | $ | 231,269,912 | | |

| At end of year | | $ | 278,390,554 | | | $ | 256,592,591 | | |

Accumulated distributions

in excess of net investment

income included in net assets | |

| At end of year | | $ | (98,345 | ) | | $ | (206,375 | ) | |

See notes to financial statements

11

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class A | |

| | | Year Ended March 31, | |

| | | 2006(1) | | 2005(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | |

| Net asset value — Beginning of year | | $ | 10.210 | | | $ | 10.400 | | | $ | 10.250 | | | $ | 9.860 | | | $ | 10.040 | | |

| Income (loss) from operations | |

| Net investment income | | $ | 0.411 | | | $ | 0.422 | | | $ | 0.437 | | | $ | 0.461 | | | $ | 0.485 | | |

| Net realized and unrealized gain (loss) | | | 0.078 | | | | (0.187 | ) | | | 0.138 | | | | 0.395 | | | | (0.152 | ) | |

| Total income from operations | | $ | 0.489 | | | $ | 0.235 | | | $ | 0.575 | | | $ | 0.856 | | | $ | 0.333 | | |

| Less distributions | |

| From net investment income | | $ | (0.409 | ) | | $ | (0.425 | ) | | $ | (0.425 | ) | | $ | (0.466 | ) | | $ | (0.513 | ) | |

| Total distributions | | $ | (0.409 | ) | | $ | (0.425 | ) | | $ | (0.425 | ) | | $ | (0.466 | ) | | $ | (0.513 | ) | |

| Net asset value — End of year | | $ | 10.290 | | | $ | 10.210 | | | $ | 10.400 | | | $ | 10.250 | | | $ | 9.860 | | |

| Total Return(3) | | | 4.88 | % | | | 2.29 | % | | | 5.70 | % | | | 8.90 | % | | | 3.39 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of year (000's omitted) | | $ | 180,401 | | | $ | 152,111 | | | $ | 130,466 | | | $ | 119,619 | | | $ | 83,647 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses | | | 0.79 | % | | | 0.80 | %†(4) | | | 0.80 | %(4) | | | 0.82 | %(4) | | | 0.91 | %(4) | |

| Expenses after custodian fee reduction | | | 0.78 | % | | | 0.79 | %†(4) | | | 0.80 | %(4) | | | 0.81 | %(4) | | | 0.88 | %(4) | |

| Net investment income | | | 3.99 | % | | | 4.09 | %† | | | 4.22 | % | | | 4.54 | % | | | 4.85 | % | |

| Portfolio Turnover of the Portfolio | | | — | | | | 14 | %(5) | | | 27 | %(5) | | | 24 | %(5) | | | 12 | %(5) | |

| Portfolio Turnover of the Fund | | | 48 | % | | | 19 | % | | | — | | | | — | | | | — | | |

† The operating expenses of the Fund reflect a reduction of the investment advisor fee. Had such actions not been taken, the ratios would have been the same.

(1) Net investment income per share was computed using the average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accouting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended March 31, 2002 was to increase net investment income per share by $0.002, and increase net realized and unrealized losses per share by $0.002, and increase the ratio of net investment income to average net assets from 4.83% to 4.85%.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(5) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

12

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class B | |

| | | Year Ended March 31, | |

| | | 2006(1) | | 2005(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | |

| Net asset value — Beginning of year | | $ | 10.220 | | | $ | 10.410 | | | $ | 10.260 | | | $ | 9.860 | | | $ | 10.040 | | |

| Income (loss) from operations | |

| Net investment income | | $ | 0.335 | | | $ | 0.346 | | | $ | 0.360 | | | $ | 0.381 | | | $ | 0.409 | | |

| Net realized and unrealized gain (loss) | | | 0.068 | | | | (0.191 | ) | | | 0.142 | | | | 0.405 | | | | (0.155 | ) | |

| Total income from operations | | $ | 0.403 | | | $ | 0.155 | | | $ | 0.502 | | | $ | 0.786 | | | $ | 0.254 | | |

| Less distributions | |

| From net investment income | | $ | (0.333 | ) | | $ | (0.345 | ) | | $ | (0.352 | ) | | $ | (0.386 | ) | | $ | (0.434 | ) | |

| Total distributions | | $ | (0.333 | ) | | $ | (0.345 | ) | | $ | (0.352 | ) | | $ | (0.386 | ) | | $ | (0.434 | ) | |

| Net asset value — End of year | | $ | 10.290 | | | $ | 10.220 | | | $ | 10.410 | | | $ | 10.260 | | | $ | 9.860 | | |

| Total Return(3) | | | 3.99 | % | | | 1.51 | % | | | 4.94 | % | | | 8.15 | % | | | 2.58 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of year (000's omitted) | | $ | 20,610 | | | $ | 27,157 | | | $ | 33,731 | | | $ | 32,517 | | | $ | 10,638 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses | | | 1.54 | % | | | 1.55 | %†(4) | | | 1.55 | %(4) | | | 1.57 | %(4) | | | 1.66 | %(4) | |

| Expenses after custodian fee reduction | | | 1.53 | % | | | 1.54 | %†(4) | | | 1.55 | %(4) | | | 1.56 | %(4) | | | 1.63 | %(4) | |

| Net investment income | | | 3.25 | % | | | 3.36 | %† | | | 3.48 | % | | | 3.75 | % | | | 4.09 | % | |

| Portfolio Turnover of the Portfolio | | | — | | | | 14 | %(5) | | | 27 | %(5) | | | 24 | %(5) | | | 12 | %(5) | |

| Portfolio Turnover of the Fund | | | 48 | % | | | 19 | % | | | — | | | | — | | | | — | | |

† The operating expenses of the Fund reflect a reduction of the investment advisor fee. Had such actions not been taken, the ratios would have been the same.

(1) Net investment income per share was computed using the average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accouting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended March 31, 2002 was to increase net investment income per share by $0.002, and increase net realized and unrealized losses per share by $0.002, and increase the ratio of net investment income to average net assets from 4.07% to 4.09%.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(5) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

13

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Class C | |

| | | Year Ended March 31, | |

| | | 2006(1) | | 2005(1) | | 2004(1) | | 2003(1) | | 2002(1)(2) | |

| Net asset value — Beginning of year | | $ | 9.580 | | | $ | 9.750 | | | $ | 9.610 | | | $ | 9.240 | | | $ | 9.400 | | |

| Income (loss) from operations | |

| Net investment income | | $ | 0.313 | | | $ | 0.324 | | | $ | 0.335 | | | $ | 0.357 | | | $ | 0.379 | | |

| Net realized and unrealized gain (loss) | | | 0.059 | | | | (0.171 | ) | | | 0.133 | | | | 0.379 | | | | (0.138 | ) | |

| Total income from operations | | $ | 0.372 | | | $ | 0.153 | | | $ | 0.468 | | | $ | 0.736 | | | $ | 0.241 | | |

| Less distributions | |

| From net investment income | | $ | (0.312 | ) | | $ | (0.323 | ) | | $ | (0.328 | ) | | $ | (0.366 | ) | | $ | (0.401 | ) | |

| Total distributions | | $ | (0.312 | ) | | $ | (0.323 | ) | | $ | (0.328 | ) | | $ | (0.366 | ) | | $ | (0.401 | ) | |

| Net asset value — End of year | | $ | 9.640 | | | $ | 9.580 | | | $ | 9.750 | | | $ | 9.610 | | | $ | 9.240 | | |

| Total Return(3) | | | 3.93 | % | | | 1.51 | %(4) | | | 4.93 | % | | | 8.12 | % | | | 2.58 | % | |

| Ratios/Supplemental Data | |

| Net assets, end of year (000's omitted) | | $ | 77,379 | | | $ | 77,325 | | | $ | 67,073 | | | $ | 46,629 | | | $ | 19,488 | | |

| Ratios (As a percentage of average daily net assets): | |

| Expenses | | | 1.54 | % | | | 1.55 | %†(5) | | | 1.55 | %(5) | | | 1.57 | %(5) | | | 1.66 | %(5) | |

| Expenses after custodian fee reduction | | | 1.53 | % | | | 1.54 | %†(5) | | | 1.55 | %(5) | | | 1.56 | %(5) | | | 1.63 | %(5) | |

| Net investment income | | | 3.25 | % | | | 3.35 | %† | | | 3.45 | % | | | 3.75 | % | | | 4.05 | % | |

| Portfolio Turnover of the Portfolio | | | — | | | | 14 | %(6) | | | 27 | %(6) | | | 24 | %(6) | | | 12 | %(6) | |

| Portfolio Turnover of the Fund | | | 48 | % | | | 19 | % | | | — | | | | — | | | | — | | |

† The operating expenses of the Fund reflect a reduction of the investment advisor fee. Had such actions not been taken, the ratios would have been the same.

(1) Net investment income per share was computed using the average shares outstanding.

(2) The Fund, through its investment in the Portfolio, has adopted the provisions of the revised AICPA Audit and Accouting Guide for Investment Companies and began using the interest method to amortize premiums on fixed-income securities. The effect of this change for the year ended March 31, 2002 was to increase net investment income per share by $0.002, and increase net realized and unrealized losses per share by $0.002, and increase the ratio of net investment income to average net assets from 4.03% to 4.05%.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Total return reflects a decrease of 0.07% due to a change in the timing of the payment and reinvestment of distributions.

(5) Includes the Fund's share of the Portfolio's allocated expenses while the Fund was making investments directly into the Portfolio.

(6) Portfolio turnover represents the rate of portfolio activity for the period while the Fund was making investments directly into the Portfolio.

See notes to financial statements

14

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

NOTES TO FINANCIAL STATEMENTS

1 Significant Accounting Policies

Eaton Vance National Limited Maturity Municipals Fund (the Fund) is a diversified series of Eaton Vance Investment Trust (the Trust). The Trust is an entity of the type commonly known as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund seeks to achieve current income exempt from regular federal income tax and particular state or local income or other taxes by investing primarily in investment grade municipal obligations. The Fund offers three classes of shares: Class A, Class B and Class C shares. Class A shares are generally sold subject to a sales charge imposed at time of purchase. Class B and Class C shares are sold at net asset value and are subject to a contingent deferred sales charge (see Note 6). Class B shares held longer than (i) four years or (ii) the time at which the contingent deferred sales charge applicab le to such shares expires will automatically convert to Class A shares. In addition, Class B shares acquired through the reinvestment of distributions will also convert to Class A shares in proportion to shares not acquired through reinvestment. Each class represents a pro rata interest in the Fund, but votes separately on class-specific matters and (as noted below) is subject to different expenses. Realized and unrealized gains or losses are allocated daily to each class of shares based on the relative net assets of each class to the total net assets of the Fund. Net investment income, other than class specific expenses, is allocated daily to each class of shares based upon the ratio of the value of paid shares of each class to the total value of all paid shares. Each class of shares differs in its distribution plan and certain other class specific expenses.

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America.

A Investment Valuation — Municipal bonds and taxable obligations, if any, are normally valued on the basis of valuations furnished by a pricing service. Financial futures contracts and options on financial future contracts listed on the commodity exchanges are valued at closing settlement prices. Over-the-counter options on futures contracts are normally valued at the mean between the latest bid and asked price. Interest rate swaps are normally valued on the basis of valuations furnished by a pricing service. Short-term obligations, maturing in sixty days or less, are valued at amortized cost, which approximates value. Investments for which valuations or market quotations are not readily available, an d investments for which the price of the security is not believed to represent its fair market value, are valued at fair value using methods determined in good faith by or at the direction of the Trustees.

B Income — Interest income is determined on the basis of interest accrued, adjusted for amortization of premium or accretion of discount.

C Expenses — The majority of expenses of the Trust are directly identifiable to an individual fund. Expenses which are not readily identifiable to a specific fund are allocated taking into consideration, among other things, the nature and type of expense and the relative size of the funds.

D Federal Taxes — The Fund's policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year all of its taxable income, if any, and tax-exempt income, including any net realized gain on investments. Accordingly, no provision for federal income or excise tax is necessary. At March 31, 2006, the Fund, for federal income tax purposes, had a capital loss carryover of $3,239,908 which will reduce the taxable income arising from future net realized gain on investments, if any, to the extent permitted by the Internal Revenue Code and thus will reduce the amount of distributions to shareholders which would otherwise be necessary to relieve the Fund of any liability for federal income tax . Such capital loss carryover will expire as follows on: March 31, 2011, $1,047,498, March 31, 2012, $779,785, March 31, 2013, $1,412,625. Dividends paid by the Fund from net interest on tax-exempt municipal bonds are not includable by shareholders as gross income for federal income tax purposes because the Fund intends to meet certain requirements of the Internal Revenue Code applicable to regulated Investment companies which will enable the Fund to pay exempt-interest dividends. The portion of such interest, if any, earned on private activity bonds issued after August 7, 1986, may be considered a tax preference item to shareholders.

E Financial Futures Contracts — Upon the entering of a financial futures contract, the Fund is required to deposit (initial margin) either in cash or securities an amount equal to a certain percentage of the purchase price indicated in the financial futures contract. Subsequent payments are made or received by the Fund (margin maintenance) each day, dependent on the daily fluctuations in the value of the underlying security, and are recorded for book purposes as unrealized gains or losses by the Fund. The Fund's investment in financial futures contracts is designed for both hedging against anticipated

15

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D

future changes in interest rates and investment purposes. Should interest rates move unexpectedly, the Fund may not achieve the anticipated benefits of the financial futures contracts and may realize a loss.

F Legal Fees — Legal fees and other related expenses incurred as part of negotiations of the terms and requirements of capital infusions, or that are expected to result in the restructuring of or a plan of reorganization for an investment are recorded as realized losses. Ongoing expenditures to protect or enhance an investment are treated as operating expenses.

G Options on Financial Futures Contracts — Upon the purchase of a put option on a financial futures contract by the Fund, the premium paid is recorded as an investment, the value of which is marked-to-market daily. When a purchased option expires, the Fund will realize a loss in the amount of the cost of the option. When the Fund enters into a closing sale transaction, the Fund will realize a gain or loss depending on whether the sales proceeds from the closing sale transaction are greater or less than the cost of the option. When the Fund exercises a put option, settlement is made in cash. The risk associated with purchasing put options is limited to the premium originally paid.

H When-issued and Delayed Transactions — The Fund may engage in when-issued and delayed delivery transactions. The Fund records when-issued securities on trade date and maintains security positions such that sufficient liquid assets will be available to make payments for the securities purchased. Securities purchased on a when-issued or delayed delivery basis are marked-to-market daily and begin earning interest on settlement date.

I Expense Reduction — Investors Bank & Trust Company (IBT) serves as custodian of the Fund. Pursuant to the custodian agreement, IBT receives a fee reduced by credits which are determined based on the average daily cash balance the Fund maintains with IBT. All credit balances used to reduce the Fund's custodian fees are reported as a reduction of total expenses on the Statement of Operations.

J Use of Estimates — The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.

K Indemnifications — Under the Trust's organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund and shareholders are indemnified against personal liability for obligations of the Trust. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund's maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

L Other — Investment transactions are accounted for on a trade-date basis. Realized gains and losses are computed on the specific identification of securities sold.

2 Distributions to Shareholders

The net income of the Fund is determined daily and substantially all of the net income so determined is declared as a dividend to shareholders of record at the time of declaration. Dividends are declared separately for each class of shares. Distributions are paid monthly. Distributions of allocated realized capital gains, if any, are made at least annually. Shareholders may reinvest income and capital gain distributions in additional shares of the same class of the Fund at the net asset value as of the reinvestment date. Distributions are paid in the form of additional shares of the same class or, at the election of the shareholder, in cash. The Fund distinguishes between distributions on a tax basis and a financial reporting basis. Accounting principles generally accepted in the United States of America require that only distributions in excess of tax basis earnings and profits be reported in the financial statements as a retur n of capital. Permanent differences between book and tax accounting relating to distributions are reclassified to paid-in capital. The tax treatment of distributions for the calendar year will be reported to shareholders prior to February 1, 2007 and will be based on tax accounting methods which may differ from amounts determined for financial statement purposes.

The tax character of distributions paid for the years ended March 31, 2006 and March 31, 2005 was as follows:

| | | Year Ended March 31, | |

| | | 2006 | | 2005 | |

| Distributions declared from: | |

| Tax-exempt income | | $ | 9,845,126 | | | $ | 8,956,195 | | |

| Ordinary income | | $ | 135,723 | | | $ | 17,395 | | |

16

Eaton Vance National Limited Maturity Municipals Fund as of March 31, 2006

NOTES TO FINANCIAL STATEMENTS CONT'D

During the year ended March 31, 2006, accumulated distributions in excess of net investment income was decreased by $54,082, and accumulated net realized loss was increased by $54,082 primarily due to differences between book and tax policies and capital loss carryovers. This change had no effect on the net assets or the net asset value per share.

As of March 31, 2006, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

| Undistributed income | | $ | 352,742 | | |

| Capital loss carryforwards | | $ | (3,239,908 | ) | |

| Unrealized appreciation | | $ | 8,683,011 | | |

| Other temporary differences | | $ | (1,780,140 | ) | |

3 Shares of Beneficial Interest

The Fund's Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest (without par value). Such shares may be issued in a number of different series (such as the Fund) and classes. Transactions in Fund shares were as follows:

| | | Year Ended March 31, | |

| Class A | | 2006 | | 2005 | |

| Sales | | | 7,156,285 | | | | 6,206,100 | | |

Issued to shareholders electing to

receive payments of distributions

in Fund shares | | | 379,472 | | | | 304,029 | | |

| Redemptions | | | (5,327,434 | ) | | | (4,862,281 | ) | |

| Exchange from Class B shares | | | 434,033 | | | | 706,919 | | |

| Net increase | | | 2,642,356 | | | | 2,354,767 | | |

| | | Year Ended March 31, | |

| Class B | | 2006 | | 2005 | |

| Sales | | | 288,651 | | | | 704,599 | | |

Issued to shareholders electing to

receive payments of distributions

in Fund shares | | | 45,652 | | | | 54,163 | | |

| Redemptions | | | (556,574 | ) | | | (635,881 | ) | |

| Exchange to Class A shares | | | (432,572 | ) | | | (706,414 | ) | |

| Net decrease | | | (654,843 | ) | | | (583,533 | ) | |

| | | Year Ended March 31, | |

| Class C | | 2006 | | 2005 | |

| Sales | | | 2,002,769 | | | | 2,689,404 | | |

Issued to shareholders electing to

receive payments of distributions

in Fund shares | | | 119,690 | | | | 111,362 | | |

| Redemptions | | | (2,174,339 | ) | | | (1,603,822 | ) | |

| Net increase (decrease) | | | (51,880 | ) | | | 1,196,944 | | |

4 Investment Adviser Fee and Other Transactions with Affiliates

The investment adviser fee is earned by Boston Management and Research (BMR), a wholly-owned subsidiary of Eaton Vance Management (EVM), as compensation for management and investment advisory services rendered to the Fund. The fee is based upon a percentage of average daily net assets plus a percentage of gross income (i.e., income other than gains from the sale of securities). For the year ended March 31, 2006 the advisory fee amounted to $1,202,204 representing 0.44% of the Fund's average daily net assets.

EVM serves as the sub-transfer agent of the Fund and receives from the transfer agent an aggregate fee based upon the actual expenses incurred by EVM in the performance of those activities. For the year ended March 31, 2006, EVM earned $7,491 in sub-transfer agent fees.