UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file Number _811- 04471

Value Line Core Bond Fund

(Exact name of registrant as specified in charter)

7 Times Square, New York, N.Y. 10036

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: 212-907-1900

Date of fiscal year end: December 31, 2013

Date of reporting period: December 31, 2013

Item I Reports to Stockholders

A copy of the Annual Report to Stockholders for the period ended 12/31/13 is included with this Form.

Annual Report

December 31, 2013

| |

| Value Line Premier Growth Fund, Inc. |

| (VALSX) |

| |

| The Value Line Fund, Inc. |

(VLIFX) |

| |

| Value Line Income and Growth Fund, Inc. |

| (VALIX) |

| |

| Value Line Larger Companies Fund, Inc. |

| (VALLX) |

| |

| Value Line Core Bond Fund |

| (VAGIX) |

| |

This audited report is issued for information to shareholders. It is not authorized for distribution to prospective investors unless preceded or accompanied by a currently effective prospectus of the Fund (obtainable from the Distributor).

#00110946

Table of Contents | |

| | |

| President’s Letter with Economic, and Market Commentary | 3 |

| | |

| Value Line Premier Growth Fund, Inc.: | |

| Manager Discussion of Fund Performance | 6 |

| Portfolio Highlights | 8 |

| Schedule of Investments | 10 |

| | |

| The Value Line Fund, Inc.: | |

| Manager Discussion of Fund Performance | 13 |

| Portfolio Highlights | 15 |

| Schedule of Investments | 17 |

| | |

| Value Line Income and Growth Fund, Inc.: | |

| Manager Discussion of Fund Performance | 19 |

| Portfolio Highlights | 22 |

| Schedule of Investments | 24 |

| | |

| Value Line Larger Companies Fund, Inc.: | |

| Manager Discussion of Fund Performance | 30 |

| Portfolio Highlights | 32 |

| Schedule of Investments | 34 |

| | |

| Value Line Core Bond Fund: | |

| Manager Discussion of Fund Performance | 36 |

| Portfolio Highlights | 38 |

| Schedule of Investments | 40 |

| | |

| Statements of Assets and Liabilities | 46 |

| | |

| Statements of Operations | 47 |

| | |

| Statements of Changes in Net Assets | 48 |

| | |

| Financial Highlights | 52 |

| | |

| Notes to Financial Statements | 54 |

| | |

| Report of Independent Registered Public Accounting Firm | 65 |

| | |

| Fund Expenses | 66 |

| | |

| Federal Tax Notice | 67 |

| | |

| Management of the Funds | 68 |

| President’s Letter (unaudited) |

| |

Dear Fellow Shareholders:

We are pleased to present you with this annual report for Value Line Premier Growth Fund, Inc., The Value Line Fund, Inc., Value Line Income and Growth Fund, Inc., Value Line Larger Companies Fund, Inc. and Value Line Core Bond Fund (individually, a “Fund” and collectively, the “Funds”) for the 12 months ended December 31, 2013. We are especially excited to present this annual report in its new format, revised to be more informative, more useful and more reader-friendly.

The 12 months ended December 31, 2013 were rewarding ones for the equity and hybrid Value Line Funds but challenging ones for the fixed income Value Line Funds, as investors generally focused on the economic recovery despite persistent volatility. At the same time, the annual period was highlighted by several of the Funds being recognized for their long-term performance.

| ● | Value Line Premier Growth Fund, Inc. outpaced its peers for the three-, five- and ten-year periods ended December 31, 2013, as noted by leading independent mutual fund advisory service Lipper Inc.1 (multi-cap growth category). Lipper also awarded its top Lipper Leader rating of 5 to the Fund for Preservationi versus its peers as of December 31, 2013. Additionally, the Fund earned an Overall four-star rating from Morningstar2 in the mid-cap growth category among 638 funds as of December 31, 2013 based on risk-adjusted returns. Morningstar gave the Fund a Risk rating of Below Average.ii |

| | |

| ● | The Value Line Fund, Inc. was named a Lipper Leader1 for overall Preservation versus its peers as of December 2013.iii |

| | |

| ● | Value Line Income and Growth Fund, Inc. outpaced its peers for the three-, five- and ten-year periods ended December 31, 2013, as noted by Lipper Inc.1 (mixed-asset target allocation moderate category). The Fund also earned an Overall four- star rating from Morningstar2 in the moderate allocation category among 739 funds as of December 31, 2013 based on risk- adjusted returns.iv The Fund, along with Value Line Premier Growth Fund, Inc., was featured in various national publications for its consistent performance over multiple time periods. |

Also a highlight of the annual period was Value Line Core Bond Fund transitioning to a new, more efficient strategy. Value Line Core Bond Fund, having changed its strategy to be a broad-based intermediate-term investment grade bond fund in December 2012, enjoyed significantly increased assets with the merger of the Value Line U.S. Government Securities Fund, Inc. into the Fund in March 2013. The Fund has already begun to realize the benefits of a larger, more efficiently managed fund, and the investment adviser, EULAV Asset Management (the “Adviser”) permanently reduced the management fee in February 2013.

On the following pages, the Funds’ portfolio managers discuss the management of their respective Funds over the annual period. The discussions highlight key factors influencing recent performance of the Funds. You will also find a schedule of investments and financial statements for each of the Funds.

Before reviewing the performance of your individual mutual fund investment, we encourage you to take a brief look at the major factors affecting the financial markets over the 12 months ended December 31, 2013, especially given the newsworthy events of the year. With the exciting developments and performance results of the Funds during 2013, we also invite you to take this time to consider a broader diversification strategy by including additional Value Line Funds, which you can read about on the following pages, in your investment portfolio.

Economic Review

U.S. real Gross Domestic Product (GDP) was lackluster with growth in the first half of 2013 at less than 2% in the first and second calendar quarters. The U.S. economy faced strong headwinds, including increases in the payroll tax and disruptions from the sequester budget cuts. Third quarter GDP, however, turned sharply upward, coming in at 4.1%, as boosted by higher consumer spending, increased business investment and rising inventories. Estimates for fourth quarter GDP suggest the U.S. economy may have ended the year with more momentum than had been anticipated.

Despite the growing economy, inflation remained modest. Consumer prices stayed in check, with the Consumer Price Index (CPI) rising just 1.5% before seasonal adjustment. Limited wage growth and declining energy prices contributed to the relatively benign inflation scenario. The U.S. also saw moderate job growth, as reflected in a drop in unemployment from 7.8% at the close of 2012 to 6.7% at the close of 2013. The makeup of job growth, however, was somewhat disappointing, with hiring generally concentrated in sectors representative of low-wage jobs.

In recognition of the improving U.S. economy, the Federal Reserve (the “Fed”) had ongoing—and well-publicized—discussions throughout the year about the possibility of reducing its monthly bond-buying program. Speculation about the timing and magnitude of the tapering had a great impact on both the equity and fixed income markets. Ultimately, Fed Chair Ben Bernanke kept the focus on key market data as the basis for the decision on tapering. As unemployment dropped close to the Fed’s stated target of 6.5%, the Fed finally announced in December 2013 that it would modestly reduce its monthly bond purchases—from $85 billion to $75 billion—beginning in January 2014. At the same time, the Fed reaffirmed its commitment to maintaining low short-term interest rates, with the targeted federal funds rate not likely to exceed 0.25%. At the end of the annual period, the appointment of Janet Yellen as new Fed Chair was seen by the financial markets as likely to not steer the Fed too far off the course set by Ben Bernanke.

Equity Market Review

U.S. equities, as measured by the S&P 500® Index3, posted robust double-digit gains for 2013, supported by a significantly stronger real estate market, steady growth in manufacturing and a modest drop in the national unemployment rate.

Stocks began the year strong upon the announcement of a partial bi-partisan deal regarding the federal budget, debt ceiling and government shutdown—which drove a generally steady climb through May 2013. The S&P 500® Index subsequently dropped between the end of May and the end of June, as fears of over-bought conditions, an imminent end to the quantitative easing program by the Fed and worries over second quarter corporate earnings arose. The U.S. equity market snapped back to post solid gains after reasonably good earnings reports and what were perceived as dovish words by Fed members that eased investors’ concerns. A notable acceleration in market appreciation occurred in early October in response to the Fed’s surprise announcement in September that it would not yet begin tapering its asset purchases. This announcement combined with improving employment reports to drive the S&P 500® Index higher between early October and the end of December. Also boosting the U.S. equity market’s gain at the end of the annual period was the Fed’s announcement, ending seven months of speculation, that it would finally but gradually begin to taper its asset purchases in January 2014. A particularly notable catalyst for the U.S. equity market during the annual period was the expansion of the price/earnings multiple investors were willing to pay, as the price/earnings multiple of the S&P 500® Index expanded from 14x to 17x by the end of December 2013. The S&P 500® Index posted 45 new all-time closing highs in 2013, including a new closing high on the final day of trading. The last time the Index closed the year with a new high was in 1999.

All ten sectors of the S&P 500® Index posted positive double-digit absolute performance for the year, with the consumer discretionary, health care and industrials sectors leading the way. Telecommunication services and utilities, both traditionally considered defensive sectors, were the weakest sectors during the annual period.

Fixed Income Market Review

The broad U.S. fixed income market, as measured by the Barclays U.S. Aggregate Bond Index4, posted negative returns during the annual period. The U.S. fixed income market faced several headwinds, including speculation of the Fed tapering its bond-buying program and Congressional discord resulting in protracted budget disputes and a partial U.S. government shutdown for 16 days. Economic indicators, while mixed, were generally improving during the year.

Against this backdrop, interest rates rose across the spectrum of maturities, but most dramatically in the intermediate segment of the yield curve. The rise in interest rates helped propel investor demand for investment grade and high yield corporate bonds at the expense of owning U.S. Treasuries. In turn, spread, or non-U.S. Treasury, sectors of the U.S. fixed income market were the best performers in the Barclays U.S. Aggregate Bond Index during the annual period. Generally speaking, lower quality bonds outpaced higher quality bonds, as investors sought yield amidst the underlying support of a growing economy. U.S. Treasuries posted negative returns overall.

* * *

We thank you for trusting us to be a part of your long-term, comprehensive investment strategy. We appreciate your confidence in the Value Line Funds and look forward to serving your investment needs in the years ahead just as we have been helping to secure generations’ financial futures for more than 60 years—based on solid fundamentals, sound investment principles and the power of disciplined and rigorous analytics. If you have any questions or would like additional information on these or other Value Line Funds, we invite you to contact your investment representative or visit us at www.vlfunds.com.

| Sincerely, |

| |

| /s/ Mitchell Appel | |

| Mitchell Appel |

| President of the Value Line Funds |

Past performance does not guarantee future results. Investment return and principal value of an investment can fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost; and that current performance may be lower or higher than the performance data quoted. Investors should carefully consider the investment objective, risks, charges and expense of a fund. This and other important information about a fund is contained in the fund’s prospectus. A copy of our funds’ prospectuses can be obtained free of charge by going to our website at www.vlfunds.com or calling 800.243.2729.

| 1 | Lipper Leader ratings are derived from highly sophisticated formulas that analyze funds against clearly defined criteria. Funds are compared to similar funds, and only those that trust stand out are awarded Lipper Leader status. Funds are ranked against their peers on each of four measures: Total Return, Consistent Return, Preservation and Expense. A fifth measure, Tax Efficiency, applies in the United States. Scores are subject to change every month and are calculated for the following periods: 3-year, 5-year, 10-year and overall. The overall calculation is based on an equal-weighted average of percentile ranks for each measure over 3-year, 5-year and 10-year periods (if applicable). For each measure, the highest 20% of funds in each peer group are named Lipper Leaders. The next 20% receive a rating of 4: the middle 20% are rated 3: the next 20% are rated 2; and the lowest 20% are rated 1. |

| | |

| | i | For Value Line Premier Growth Fund, Inc.: Preservation 5 rating for 3-year (10,671 funds); 5-year (9,050 funds) and overall (10,671 funds) periods ended December 31, 2013; 4 rating for 10-year (5,264 funds) period ended December 31, 2013. |

| | |

| | iii | For The Value Line Fund, Inc.: overall Preservation (10,671 funds); 3-year 5 rating (10,671 funds); 5-year 5 rating (9,050 funds) and 10-year 3 rating (5,264 funds) periods ended December 31, 2013. |

| | |

| 2 | The Morningstar RatingTM for funds methodology rates funds based on an enhanced Morningstar Risk-Adjusted Return measure, which also accounts for the effects of all sales charges, loads, or redemption fees. Funds are ranked by their Morningstar Risk-Adjusted Return scores and stars are assigned using the following scale: 5 stars for top 10%; 4 starts next 22.5%; 3 stars next 35%; 2 stars next 22.5%; 1 star for bottom 10%. Funds are rated for up to three periods: the trailing three-, five- and 10-years. For a fund that does not change categories during the evaluation period, the overall rating is calculated using the following weights: At least 3 years, but less than 5 years uses 100% three-year rating. At least 5 years but less than 10 years uses 60% five-year ratings/40% three-year rating. At least 10 years uses 50% ten-year rating/30% five-year rating/20% three-year rating. |

| | |

| | ii | For Value Line Premier Growth Fund, Inc.: Four-star rating for 3-year (638 funds), 10-year (416 funds) and Overall (638 funds) periods ended December 31, 2013; 5-year period ended December 31, 2013 3 stars/548 funds). Morningstar Risk: Below Average for the 5-year, 10-year and Overall periods ended December 31, 2013; Low for the 3- year period ended December 31, 2013. |

| | |

| | iv | For Value Line Income and Growth Fund, Inc.: Overall four-star rating (739 funds); 3-year 3 stars (739 funds), 5-year 3 stars (674 funds), 10-year 5 stars (422 funds) for periods ended December 31, 2013. All in the moderate allocation category. |

| | |

| 3 | The S&P 500® Index consists of 500 stocks that are traded on the New York Stock Exchange, American Stock Exchange and the NASDAQ national Market System and is representative of the broad stock market. This is an unmanaged index and does not reflect charges, expenses or taxes, and it is not possible to directly invest in this index. |

| | |

| 4 | The Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar- denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS. This is an unmanaged index and does reflect charges, expenses or taxes, which are deducted from the Fund’s return. It is not possible to directly invest in this index. |

| VALUE LINE PREMIER GROWTH FUND, INC. |

| |

INVESTMENT OBJECTIVE AND STRATEGY

The Fund primarily seeks long-term growth of capital.

To achieve the Fund’s goal, the Fund’s investment adviser invests at least 80% of the Fund’s net assets in a diversified portfolio of U.S. equity securities with favorable growth prospects. In selecting securities for purchase or sale, the Adviser generally analyzes the issuer of a security using fundamental factors such as growth potential and earnings estimates and quantitative factors such as historical earnings, earnings momentum and price momentum. The Fund may invest in small, mid or large capitalization companies, including foreign companies. There are no set limitations of investments according to a company’s size, or to a sector weighting.

Manager Discussion of Fund Performance

Below, Value Line Premier Growth Fund, Inc. portfolio manager Stephen E. Grant discusses the Fund’s performance and positioning for the 12 months ended December 31, 2013.

How did the Fund perform during the annual period?

The Fund generated a total return of 26.56% during the 12 months ended December 31, 2013. This compares to the 32.39% return of the Fund’s benchmark, the S&P 500® Index, during the same period.

What key factors were responsible for the Fund’s performance during the 12-month reporting period?

While the Fund generated robust double-digit absolute gains, its underperformance of the S&P 500® Index during the 12-month reporting period can be attributed primarily to stock selection. Sector allocation overall was effective.

Which equity market sectors most significantly affected Fund performance?

Stock selection in the financials, health care, consumer staples and consumer discretionary sectors detracted from the Fund’s performance most during the annual period. In financials, an underweighted exposure to the strongly performing insurance industry hurt most. In health care, a lesser exposure than the S&P 500® Index to the strongly performing biotechnology industry particularly dampened results. In consumer staples, holdings of select foreign companies, via American Depositary Receipts (ADRs), proved disappointing. In consumer discretionary, we missed the rallies in select stocks that performed well. (An ADR is a negotiable certificate issued by a U.S. bank representing a specified number of shares in a foreign stock that is traded on a U.S. exchange.) Holding an average 3% position in cash during a period when the U.S. equity market rallied also hurt.

Partially offsetting these detractors were the positive contributions made by effective stock selection in the information technology sector, having an overweighted allocation in the strongly performing industrials sector, and both stock selection in and having an underweighted allocation to the lagging energy sector.

Which stocks detracted significantly from the Fund’s performance during the annual period?

During the annual period, among the stocks that detracted most from the Fund’s relative performance were several foreign banks, including Colombia’s Bancolombia, India’s HDFC Bank, Brazil’s Itau Unibanco Holding and Chile’s Banco de Chile. In health care, overweighted positions in laggards such as cardiovascular device manufacturer Edwards Lifesciences, pharmacy benefits management services provider Catamaran and surgical systems manufacturer Intuitive Surgical detracted. In consumer discretionary, we missed the rallies in online retailer Amazon.com, online travel company priceline.com, entertainment subscription company Netflix and entertainment giant The Walt Disney Company, and thus these positions detracted on a relative basis.

What were some of the Fund’s best-performing individual stocks?

Among the individual stocks that contributed most to the Fund’s relative results were two sizable positions in the information technology sector—namely, Alliance Data Systems, which provides data-driven and transaction-based marketing and customer loyalty solutions, and MasterCard, which is a global payment solutions company that provides a variety of services in support of the credit, debt and related payment programs of financial institutions. Avoiding several laggards in the information technology sector, such as Apple, IBM and Oracle, also boosted the Fund’s results.

Several Fund positions in the industrials sector added value. Top contributors in the sector were human resources firm Towers Watson, rail transportation equipment manufacturer Wabtec, inland tank barge fleet operator Kirby and renewable energy equipment manufacturer EnerSys.

In the energy sector, a position in Core Laboratories was an outstanding performer. Core Laboratories provides reservoir description, production enhancement and reservoir management services for oil and gas producers.

How did the Fund use derivatives and similar instruments during the reporting period?

The Fund did not use derivatives during the reporting period.

Did the Fund make any significant purchases or sales during the fiscal year?

During the fiscal year, we initiated a Fund position in Chevron. Whereas this large integrated oil company had inconsistent results prior to 2003, over the past decade it has demonstrated the ability to consistently grow its earnings and stock price. We added to the Fund’s long-time position in supplemental insurance company Aflac because it came through the 2008-09 world financial crisis in good shape and because we believe the company is now back on track to add to its long-term record of consistent growth in its earnings and stock price. In each case, we purchased shares as a dip in their respective share prices offered what we believed to be an attractive entry point.

A Fund position in Warnaco Group was eliminated because the company was acquired by PVH, combining to form one of the largest global branded lifestyle apparel companies in the world, with a diversified portfolio of brands, including Calvin Klein, Tommy Hilfiger, Van Heusen, IZOD, ARROW, Bass, Speedo, Olga and Warner’s. We sold the Fund’s position in food retailer Harris Teeter Supermarkets after its stock rose in response to a takeover bid by competitor Kroger.

Were there any notable changes in the Fund’s weightings during the 12-month period?

There were no material changes in the Fund’s sector weightings during the 12-month period ended December 31, 2013.

How was the Fund positioned relative to its benchmark index at the end of December 2013?

As of December 31, 2013, the Fund was overweighted relative to the S&P 500® Index in the industrials and materials sectors. The Fund was underweighted relative to the S&P 500® Index in the energy, financials and information technology sectors and rather neutrally weighted relative to the Index in the consumer discretionary, consumer staples, health care, utilities, telecommunication services sectors on the same date.

What is your tactical view and strategy for the months ahead?

Calendar year 2013 saw lower quality stocks outperform higher quality stocks, as investors became more bold and more confident in the economy and the financial system. Speculative stocks, such as those of biotechnology companies, and Initial Public Offerings, such as those of Facebook and Twitter, outperformed the broad U.S. equity market, along with the more cyclical, economically-sensitive stocks. Lagging were the more consistent, “steady-eddy,” long-term growth stocks in which we traditionally invest, i.e., those companies that have established strongholds in their market or market niche through proprietary products or services, which, in our view, gives them greater control of their own destiny and makes them less subject to ups and downs of the economy. We consider the Fund’s underperformance of the S&P 500® Index in 2013 as part of the natural ebb and flow of the market, as the lower quality stocks that performed poorly in 2011 and 2012 regained some ground. We do not know whether the trends of 2013 will continue into the new year, but, regardless of market trends and conditions, we do not intend to vary from our strategy of investing in high quality securities with a long-term perspective. Our portfolio turnover and trading costs have remained lower than many of our peers, as we have patience with a consistent grower until a change in the company’s strategy or its earnings and stock performance give solid reason to sell.

As always, we intend to stay true to our time-tested investment discipline going forward.

| Value Line Premier Growth Fund, Inc. |

| Portfolio Highlights at December 31, 2013 (unaudited) |

| Ten Largest Holdings | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | Percentage of |

| Issue | | Shares | | | Value | | | Net Assets |

| MasterCard, Inc. Class A | | | 8,600 | | | $ | 7,184,956 | | | | 1.8 | % |

| ANSYS, Inc. | | | 60,000 | | | | 5,232,000 | | | | 1.3 | % |

| Alliance Data Systems Corp. | | | 19,400 | | | | 5,100,842 | | | | 1.3 | % |

| AMETEK, Inc. | | | 96,750 | | | | 5,095,822 | | | | 1.3 | % |

| Alexion Pharmaceuticals, Inc. | | | 37,800 | | | | 5,029,668 | | | | 1.3 | % |

| Roper Industries, Inc. | | | 36,000 | | | | 4,992,480 | | | | 1.2 | % |

| Precision Castparts Corp. | | | 17,800 | | | | 4,793,540 | | | | 1.2 | % |

| AMBEV S.A. ADR | | | 650,000 | | | | 4,777,500 | | | | 1.2 | % |

| Danaher Corp. | | | 61,000 | | | | 4,709,200 | | | | 1.2 | % |

| Affiliated Managers Group, Inc. | | | 21,000 | | | | 4,554,480 | | | | 1.1 | % |

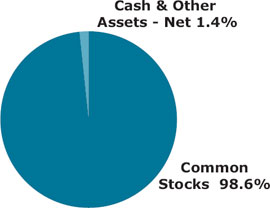

| Asset Allocation – Percentage of Net Assets |

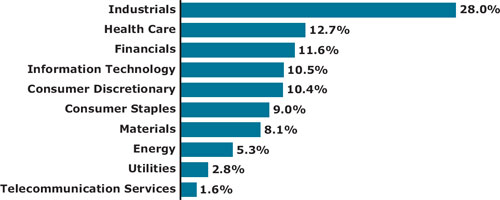

| Sector Weightings – Percentage of Total Investment Securities* |

*Sector weightings exclude short-term investments.

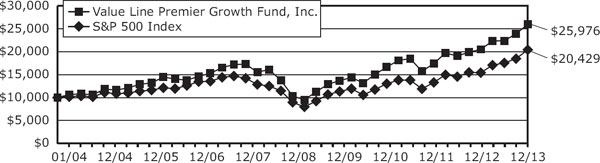

The following graph compares the performance of the Value Line Premier Growth Fund, Inc. to that of the S&P 500 Index (the “Index”). The Value Line Premier Growth Fund, Inc. is a professionally managed mutual fund, while the Index is not available for investment and is unmanaged. The returns for the Index do not reflect charges, expenses or taxes but do include the reinvestment of dividends. The comparison is shown for illustrative purposes only.

Comparison of a Change in Value of a $10,000 Investment in the Value Line Premier Growth Fund, Inc. and the S&P 500 Index*

| | | Average Annual | | Growth of an Assumed | |

| | | Total Return | | Investment of $10,000 | |

| 1 year ended 12/31/13 | | | 26.56 | % | | $12,656 | |

| 5 years ended 12/31/13 | | | 20.20 | % | | $25,096 | |

| 10 years ended 12/31/13 | | | 10.02 | % | | $25,976 | |

| * | The Standard and Poor’s 500 Index is an unmanaged index that is representative of the larger-capitalization stocks traded in the United States. |

| ** | The performance data quoted represent past performance and are no guarantee of future performance. The average annual total returns and growth of an assumed investment of $10,000 include dividends reinvested and capital gains distributions accepted in shares. The investment return and principal value of an investment will fluctuate so that an investment, when redeemed, may be worth more or less than its original cost. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

Value Line Premier Growth Fund, Inc. Schedule of Investments |

| | | | | | | |

| Shares | | | | | Value | |

COMMON STOCKS (98.6%) | | | | |

| | | CONSUMER DISCRETIONARY (10.3%) | | | | |

| 8,400 | | AutoZone, Inc. * | | $ | 4,014,696 | |

| 56,000 | | BorgWarner, Inc. | | | 3,130,960 | |

| 40,000 | | Brinker International, Inc. | | | 1,853,600 | |

| 10,500 | | Buckle, Inc. (The) (1) | | | 551,880 | |

| 36,000 | | Dick’s Sporting Goods, Inc. | | | 2,091,600 | |

| 23,800 | | Domino’s Pizza, Inc. | | | 1,657,670 | |

| 23,000 | | Genuine Parts Co. | | | 1,913,370 | |

| 15,200 | | Gildan Activewear, Inc. (1) | | | 810,312 | |

| 27,000 | | Johnson Controls, Inc. | | | 1,385,100 | |

| 112,000 | | LKQ Corp. * | | | 3,684,800 | |

| 24,000 | | McDonald’s Corp. | | | 2,328,720 | |

| 27,000 | | NIKE, Inc. Class B | | | 2,123,280 | |

| 18,000 | | O’Reilly Automotive, Inc. * | | | 2,316,780 | |

| 13,000 | | Penn National Gaming, Inc. * | | | 186,290 | |

| 40,000 | | Starbucks Corp. | | | 3,135,600 | |

| 68,600 | | TJX Companies, Inc. (The) | | | 4,371,878 | |

| 21,600 | | VF Corp. | | | 1,346,544 | |

| 33,600 | | Wolverine World Wide, Inc. | | | 1,141,056 | |

| 44,000 | | Yum! Brands, Inc. | | | 3,326,840 | |

| | | | | | 41,370,976 | |

| | | | | | | |

| | | CONSUMER STAPLES (8.9%) | | | | |

| 650,000 | | AMBEV S.A. ADR | | | 4,777,500 | |

| 71,000 | | BRF S.A. ADR (1) | | | 1,481,770 | |

| 17,000 | | British American Tobacco PLC ADR | | | 1,826,140 | |

| 21,300 | | Brown-Forman Corp. Class B | | | 1,609,641 | |

| 24,000 | | Bunge Ltd. | | | 1,970,640 | |

| 48,400 | | Church & Dwight Co., Inc. | | | 3,207,952 | |

| 16,800 | | Coca-Cola Femsa, S.A.B. de C.V. ADR (1) | | | 2,045,736 | |

| 14,000 | | Costco Wholesale Corp. | | | 1,666,140 | |

| 23,400 | | Energizer Holdings, Inc. | | | 2,532,816 | |

| 89,812 | | Flowers Foods, Inc. | | | 1,928,264 | |

| 20,000 | | Fomento Economico Mexicano S.A.B. de C.V. ADR | | | 1,957,400 | |

| 64,000 | | General Mills, Inc. | | | 3,194,240 | |

| 43,000 | | Hormel Foods Corp. | | | 1,942,310 | |

| 3,000 | | McCormick & Co., Inc. | | | 206,760 | |

| 29,000 | | PepsiCo, Inc. | | | 2,405,260 | |

| 22,000 | | Reynolds American, Inc. | | | 1,099,780 | |

| 32,000 | | Whole Foods Market, Inc. | | | 1,850,560 | |

| | | | | | 35,702,909 | |

| | | | | | | |

| | | ENERGY (5.3%) | | | | |

| 18,000 | | Chevron Corp. | | | 2,248,380 | |

| 8,600 | | CNOOC Ltd. ADR | | | 1,613,876 | |

| 14,600 | | Core Laboratories N.V. | | | 2,787,870 | |

| 17,000 | | Enbridge, Inc. | | | 742,560 | |

| 28,000 | | EQT Corp. | | | 2,513,840 | |

| 70,000 | | EMC Technologies, Inc. * | | | 3,654,700 | |

| 51,400 | | Noble Energy, Inc. | | | 3,500,854 | |

| Shares | | | | | Value | |

| 9,000 | | Oceaneering International, Inc. | | $ | 709,920 | |

| 5,000 | | Oil States International, Inc. * | | | 508,600 | |

| 5,346 | | Pioneer Natural Resources Co. | | | 984,038 | |

| 26,000 | | TransCanada Corp. (1) | | | 1,187,160 | |

| 25,600 | | Ultrapar Participacoes S.A. ADR | | | 605,440 | |

| | | | | | 21,057,238 | |

| | | | | | | |

| | | FINANCIALS (11.4%) | | | | |

| 8,000 | | ACE Ltd. | | | 828,240 | |

| 21,000 | | Affiliated Managers Group, Inc. * | | | 4,554,480 | |

| 52,600 | | AFLAC, Inc. | | | 3,513,680 | |

| 3,000 | | Alleghany Corp. * | | | 1,199,880 | |

| 36,000 | | American Tower Corp. REIT | | | 2,873,520 | |

| 45,000 | | Arch Capital Group Ltd. * | | | 2,686,050 | |

| 8,316 | | Banco de Chile ADR (1) | | | 730,145 | |

| 13,300 | | Bank of Montreal | | | 886,578 | |

| 22,100 | | Bank of Nova Scotia | | | 1,382,355 | |

| 7,700 | | BlackRock, Inc. | | | 2,436,819 | |

| 16,000 | | BRE Properties, Inc. REIT | | | 875,360 | |

| 9,400 | | Brown & Brown, Inc. | | | 295,066 | |

| 9,400 | | Camden Property Trust REIT | | | 534,672 | |

| 3,200 | | Canadian Imperial Bank of Commerce | | | 273,312 | |

| 18,000 | | Digital Realty Trust, Inc. (1) | | | 884,160 | |

| 23,200 | | Equity Lifestyle Properties, Inc. REIT | | | 840,536 | |

| 9,400 | | Essex Property Trust, Inc. REIT (1) | | | 1,348,994 | |

| 2,600 | | Everest Re Group Ltd. | | | 405,262 | |

| 13,000 | | Gaming and Leisure Properties, Inc. REIT * | | | 660,530 | |

| 75,500 | | HDFC Bank Ltd. ADR | | | 2,600,220 | |

| 22,000 | | M&T Bank Corp. (1) | | | 2,561,240 | |

| 15,000 | | MetLife, Inc. | | | 808,800 | |

| 10,000 | | PartnerRe Ltd. | | | 1,054,300 | |

| 27,000 | | Portfolio Recovery Associates, Inc. * | | | 1,426,680 | |

| 5,000 | | Principal Financial Group, Inc. | | | 246,550 | |

| 30,000 | | ProAssurance Corp. | | | 1,454,400 | |

| 21,500 | | Prudential Financial, Inc. | | | 1,982,730 | |

| 26,000 | | Royal Bank of Canada | | | 1,747,980 | |

| 17,000 | | Stifel Financial Corp. * | | | 814,640 | |

| 17,000 | | T. Rowe Price Group, Inc. | | | 1,424,090 | |

| 8,000 | | Taubman Centers, Inc. REIT | | | 511,360 | |

| 7,400 | | Toronto-Dominion Bank (The) | | | 697,376 | |

| 30,000 | | Wells Fargo & Co. | | | 1,362,000 | |

| | | | | | 45,902,005 | |

| | | | | | | |

| | | HEALTH CARE (12.5%) | | | | |

| 37,800 | | Alexion Pharmaceuticals, Inc. * | | | 5,029,668 | |

| 17,200 | | Allergan, Inc. | | | 1,910,576 | |

| 15,200 | | Bayer AG ADR | | | 2,158,400 | |

| 14,500 | | Becton, Dickinson & Co. | | | 1,602,105 | |

| Shares | | | | | Value | |

| 2,000 | | Bio-Rad Laboratories, Inc. Class A * | | $ | 247,220 | |

| 14,800 | | Bio-Reference Laboratories, Inc. * (1) | | | 377,992 | |

| 17,000 | | C.R. Bard, Inc. | | | 2,276,980 | |

| 56,000 | | Catamaran Corp. * | | | 2,658,880 | |

| 63,000 | | Cerner Corp. * | | | 3,511,620 | |

| 6,200 | | Cooper Cos., Inc. (The) | | | 767,808 | |

| 6,000 | | DaVita HealthCare Partners, Inc. * | | | 380,220 | |

| 10,000 | | DENTSPLY International, Inc. | | | 484,800 | |

| 26,000 | | Edwards Lifesciences Corp. * | | | 1,709,760 | |

| 46,000 | | Express Scripts Holding Co. * | | | 3,231,040 | |

| 38,800 | | Henry Schein, Inc. * | | | 4,433,288 | |

| 24,000 | | IDEXX Laboratories, Inc. * | | | 2,552,880 | |

| 15,000 | | McKesson Corp. | | | 2,421,000 | |

| 14,000 | | Mednax, Inc. * | | | 747,320 | |

| 14,700 | | Mettler-Toledo International, Inc. * | | | 3,566,073 | |

| 6,500 | | MWI Veterinary Supply, Inc. * | | | 1,108,835 | |

| 17,800 | | Novo Nordisk A/S ADR | | | 3,288,728 | |

| 4,000 | | ResMed, Inc. (1) | | | 188,320 | |

| 23,000 | | Teva Pharmaceutical Industries Ltd. ADR | | | 921,840 | |

| 29,000 | | Thermo Fisher Scientific, Inc. | | | 3,229,150 | |

| 11,000 | | Universal Health Services, Inc. Class B | | | 893,860 | |

| 7,000 | | WellPoint, Inc. | | | 646,730 | |

| | | | | | 50,345,093 | |

| | | | | | | |

| | | INDUSTRIALS (27.6%) | | | | |

| 85,000 | | ABB Ltd. ADR * | | | 2,257,600 | |

| 25,300 | | Acuity Brands, Inc. | | | 2,765,796 | |

| 96,750 | | AMETEK, Inc. | | | 5,095,822 | |

| 39,200 | | AZZ, Inc. | | | 1,915,312 | |

| 59,800 | | Canadian National Railway Co. | | | 3,409,796 | |

| 31,000 | | Chicago Bridge & Iron Co. N.V. | | | 2,577,340 | |

| 35,000 | | CLARCOR, Inc. | | | 2,252,250 | |

| 10,000 | | Clean Harbors, Inc. * | | | 599,600 | |

| 61,000 | | Danaher Corp. | | | 4,709,200 | |

| 56,000 | | Donaldson Co., Inc. | | | 2,433,760 | |

| 26,000 | | EnerSys | | | 1,822,340 | |

| 14,800 | | Equifax, Inc. | | | 1,022,532 | |

| 18,000 | | Esterline Technologies Corp. * | | | 1,835,280 | |

| 30,000 | | Fastenal Co. | | | 1,425,300 | |

| 15,000 | | FedEx Corp. | | | 2,156,550 | |

| 12,000 | | Flowserve Corp. | | | 945,960 | |

| 16,000 | | General Dynamics Corp. | | | 1,528,800 | |

| 6,000 | | Graco, Inc. | | | 468,720 | |

| 29,062 | | HEICO Corp. | | | 1,684,143 | |

| 47,850 | | IDEX Corp. | | | 3,533,722 | |

| 12,600 | | IHS, Inc. Class A * | | | 1,508,220 | |

| 31,776 | | Iron Mountain, Inc. | | | 964,402 | |

| 9,000 | | ITT Corp. | | | 390,780 | |

See Notes to Financial Statements. |

| 10 |

| Shares | | | | | Value | |

| 33,000 | | J.B. Hunt Transport Services, Inc. | | $ | 2,550,900 | |

| 21,000 | | Kansas City Southern | | | 2,600,430 | |

| 38,000 | | Kirby Corp. * | | | 3,771,500 | |

| 5,000 | | L-3 Communications Holdings, Inc. | | | 534,300 | |

| 26,000 | | Lincoln Electric Holdings, Inc. | | | 1,854,840 | |

| 12,000 | | Oshkosh Corp. | | | 604,560 | |

| 33,000 | | Parker Hannifin Corp. | | | 4,245,120 | |

| 17,800 | | Precision Castparts Corp. | | | 4,793,540 | |

| 66,500 | | Republic Services, Inc. | | | 2,207,800 | |

| 9,000 | | Rockwell Automation, Inc. | | | 1,063,440 | |

| 54,000 | | Rollins, Inc. | | | 1,635,660 | |

| 36,000 | | Roper Industries, Inc. | | | 4,992,480 | |

| 50,700 | | Rush Enterprises, Inc. Class A * | | | 1,503,255 | |

| 1,000 | | Snap-on, Inc. | | | 109,520 | |

| 37,600 | | Stericycle, Inc. * | | | 4,367,992 | |

| 23,000 | | Teledyne Technologies, Inc. * | | | 2,112,780 | |

| 66,000 | | Toro Co. (The) | | | 4,197,600 | |

| 14,700 | | Towers Watson & Co. Class A | | | 1,875,867 | |

| 20,000 | | Union Pacific Corp. | | | 3,360,000 | |

| 31,000 | | United Technologies Corp. | | | 3,527,800 | |

| 15,700 | | Valmont Industries, Inc. (1) | | | 2,341,184 | |

| 12,600 | | W.W. Grainger, Inc. | | | 3,218,292 | |

| 42,800 | | Wabtec Corp. | | | 3,178,756 | |

| 67,600 | | Waste Connections, Inc. | | | 2,949,388 | |

| | | | | | 110,900,229 | |

| | | | | | | |

| | | INFORMATION TECHNOLOGY (10.3%) | | | | |

| 25,000 | | Accenture PLC Class A | | | 2,055,500 | |

| 19,400 | | Alliance Data Systems Corp. * | | | 5,100,842 | |

| 30,800 | | Amphenol Corp. Class A | | | 2,746,744 | |

| 9,700 | | Anixter International Inc. | | | 871,448 | |

| 60,000 | | ANSYS, Inc. * | | | 5,232,000 | |

| 17,000 | | Automatic Data Processing, Inc. | | | 1,373,770 | |

| 42,000 | | Cognizant Technology Solutions Corp. Class A * | | | 4,241,160 | |

| 14,600 | | Equinix, Inc. * | | | 2,590,770 | |

| 16,400 | | Fiserv, Inc. * | | | 968,420 | |

| 8,600 | | MasterCard, Inc. Class A | | | 7,184,956 | |

| 11,200 | | MICROS Systems, Inc. * | | | 642,544 | |

| 75,000 | | Salesforce.com, Inc. * | | | 4,139,250 | |

| 51,000 | | Trimble Navigation Ltd. * | | | 1,769,700 | |

| 3,800 | | Ultimate Software Group, Inc. (The) * | | | 582,236 | |

| 20,300 | | WEX, Inc. * | | | 2,010,309 | |

| | | | | | 41,509,649 | |

| Shares | | | | | Value | |

| | | MATERIALS (8.0%) | | | | |

| 15,000 | | Air Products & Chemicals, Inc. | | $ | 1,676,700 | |

| 8,000 | | Airgas, Inc. | | | 894,800 | |

| 3,600 | | Albemarle Corp. | | | 228,204 | |

| 30,700 | | AptarGroup, Inc. | | | 2,081,767 | |

| 20,000 | | Ball Corp. | | | 1,033,200 | |

| 11,800 | | BASF SE ADR (1) | | | 1,271,922 | |

| 4,000 | | Compass Minerals International, Inc. | | | 320,200 | |

| 29,000 | | Crown Holdings, Inc. * | | | 1,292,530 | |

| 1,200 | | Cytec Industries, Inc. | | | 111,792 | |

| 43,000 | | Ecolab, Inc. | | | 4,483,610 | |

| 40,000 | | FMC Corp. | | | 3,018,400 | |

| 6,600 | | NewMarket Corp. (1) | | | 2,205,390 | |

| 31,000 | | Praxair, Inc. | | | 4,030,930 | |

| 24,000 | | Rockwood Holdings, Inc. | | | 1,726,080 | |

| 20,200 | | Scotts Miracle-Gro Co. (The) Class A | | | 1,256,844 | |

| 30,000 | | Sigma-Aldrich Corp. | | | 2,820,300 | |

| 12,800 | | Syngenta AG ADR | | | 1,023,232 | |

| 39,000 | | Valspar Corp. (The) | | | 2,780,310 | |

| | | | | | 32,256,211 | |

| | | | | | | |

| | | TELECOMMUNICATION SERVICES (1.6%) | | | | |

| 36,000 | | Crown Castle International Corp. * | | | 2,643,480 | |

| 43,000 | | SBA Communications Corp. Class A * | | | 3,863,120 | |

| | | | | | 6,506,600 | |

| | | | | | | |

| | | UTILITIES (2.7%) | | | | |

| 165,600 | | Cia de Saneamento Basico do Estado de Sao Paulo ADR (1) | | | 1,877,904 | |

| 20,000 | | ITC Holdings Corp. | | | 1,916,400 | |

| 17,400 | | MDU Resources Group, Inc. | | | 531,570 | |

| 13,000 | | NextEra Energy, Inc. | | | 1,113,060 | |

| 32,000 | | ONEOK, Inc. | | | 1,989,760 | |

| 52,000 | | Questar Corp. | | | 1,195,480 | |

| 14,000 | | Sempra Energy | | | 1,256,640 | |

| 26,800 | | Wisconsin Energy Corp. | | | 1,107,912 | |

| | | | | | 10,988,726 | |

| | | | | | | |

| | | TOTAL COMMON STOCKS (Cost $188,819,815) (98.6%) | | | 396,539,636 | |

| Principal | | | | | | |

| Amount | | | | | Value | |

SHORT-TERM INVESTMENTS (4.7%) | | | | |

| | | | | | | | |

| | | | REPURCHASE AGREEMENTS (1.1%) | | | | |

| $ | 4,100,000 | | With Morgan Stanley, 0.01%, dated 12/31/13, due 01/02/14, delivery value $4,100,002 (collateralized by $4,175,000 U.S.Treasury Notes 1.000% due 03/31/17, with a value of $4,195,567) | | $ | 4,100,000 | |

| | | | JOINT REPURCHASE AGREEMENTS (INVESTMENTS OF CASH COLLATERAL FOR SECURITIES ON LOAN) (3.6%) | | | | |

| | 5,347,820 | | Joint Repurchase Agreement with Morgan Stanley, 0.02%, dated 12/31/13, due 01/02/14, delivery value $5,347,826 (collateralized by $5,454,778 U.S. Treasury Bonds 4.250% - 8.000% due 11/15/21 - 11/15/40 and U.S. Treasury Notes 2.625% - 2.750% due 11/15/20 - 11/15/23, with a value of $5,427,020) | | | 5,347,820 | |

| | 7,894,401 | | Joint Repurchase Agreement with Barclays, 0.01%, dated 12/31/13, due 01/02/14, delivery value $7,894,405 (collateralized by $8,052,300 U.S. Treasury Inflation Indexed Notes 1.250% - 1.875% due 04/15/14 - 07/15/15, with a value of $7,991,429) | | | 7,894,401 | |

| See Notes to Financial Statements. |

| 11 |

Schedule of Investments (continued) |

| Principal | | | | | | |

| Amount | | | | | Value | |

| $ | 1,273,290 | | Joint Repurchase Agreement with Citigroup, 0.01%, dated 12/31/13, due 01/02/14, delivery value $1,273,291 (collateralized by $1,298,770 U.S. Treasury Bills 0.000% due 02/20/14, with a value of $1,298,770) | | $ | 1,273,290 | |

| | | | | | | 14,515,511 | |

| | | | TOTAL SHORT-TERM INVESTMENTS

(Cost $18,615,511) (4.7%) | | | 18,615,511 | |

| Principal | | | | | | |

| Amount | | | | | Value | |

| | | | TOTAL INVESTMENT SECURITIES (103.3%) (Cost $207,435,326) | | $ | 415,155,147 | |

| | | | | |

| EXCESS OF LIABILITIES OVER CASH AND OTHER ASSETS (-3.3%) | | | (13,082,195 | ) |

| NET ASSETS (100%) | | $ | 402,072,952 | |

| | | | | |

| NET ASSET VALUE OFFERING AND REDEMPTION PRICE, PER OUTSTANDING SHARE ($402,072,952 ÷ 11,828,557 shares outstanding) | | $ | 33.99 | |

| * | Non-income producing. |

| (1) | A portion or all of the security was held on loan. As of December 31, 2013, the market value of the securities on loan was $15,893,168. |

| ADR | American Depositary Receipt. |

| REIT | Real Estate Investment Trust. |

The following table summarizes the inputs used to value the Fund’s investments in securities as of December 31, 2013 (See Note 1B):

| Value Line Premier Growth Fund, Inc. | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | |

| Common Stocks | | $ | 396,539,636 | | | $ | — | | | $ | — | | | $ | 396,539,636 | |

| Short-Term Investment | | | — | | | | 18,615,511 | | | | — | | | | 18,615,511 | |

| Total | | $ | 396,539,636 | | | $ | 18,615,511 | | | $ | — | | | $ | 415,155,147 | |

See Notes to Financial Statements. |

| 12 |

| THE VALUE LINE FUND, INC. |

| |

| |

| INVESTMENT OBJECTIVE AND STRATEGY |

The Fund’s primary investment objective is long-term growth of capital. Current income is a secondary investment objective.

To achieve the Fund’s investment objectives the Advisor invests substantially all of the Fund’s net assets in common stocks. While the Fund is actively managed by the Adviser, the Adviser relies primarily on the rankings of companies by the Value Line Timeliness™ Ranking System (the “Ranking System”) in selecting securities for purchase or sale. The Fund’s investments principally are selected from common stocks ranked 1, 2 or 3 by the Ranking System at the time of purchase. The Adviser will determine the percentage of the Fund’s assets invested in each stock based on the stock’s relative attractiveness.

Manager Discussion of Fund Performance

Below, The Value Line Fund, Inc. portfolio manager Stephen E. Grant discusses the Fund’s performance and positioning for the 12 months ended December 31, 2013.

How did the Fund perform during the annual period?

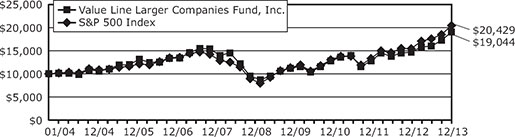

The Fund generated a total return of 30.86% during the 12 months ended December 31, 2013. This compares to the 32.39% return of the Fund’s benchmark, the S&P 500® Index, during the same period.

What key factors were responsible for the Fund’s performance during the 12-month reporting period?

While the Fund generated robust double-digit absolute gains, its underperformance of the S&P 500® Index during the 12-month reporting period can be attributed primarily to holding a position in cash during a strong rally in the U.S. equity market. Stock selection and sector allocation overall provided mixed results.

Which equity market sectors most significantly affected Fund performance?

Stock selection in the health care sector detracted from the Fund’s performance during the annual period. A lesser exposure than the S&P 500® Index to the strongly performing biotechnology industry particularly dampened results. Having an underweighted allocation to the financials sector, which outpaced the S&P 500® Index during the annual period, and an overweighted position in the materials sector, which lagged the S&P 500® Index during the annual period, also detracted. Perhaps most significantly, holding an average 2% position in cash during a period when the U.S. equity market rallied hurt.

Offsetting these detractors were the positive contributions made by effective stock selection in the information technology, consumer staples and energy sectors, having an overweighted allocation in the strongly performing industrials sector, and having an underweighted allocation to the lagging energy sector.

Which stocks detracted significantly from the Fund’s performance during the annual period?

During the annual period, among the stocks that detracted most from the Fund’s relative performance were overweighted positions in several health care laggards. These included positions in cardiovascular device manufacturer Edwards Lifesciences, pharmacy benefits management services provider Catamaran and surgical systems manufacturer Intuitive Surgical.

What were some of the Fund’s best-performing individual stocks?

Among the individual stocks that contributed most to the Fund’s relative results were three sizable positions in the information technology sector—namely, Alliance Data Systems, which provides data-driven and transaction-based marketing and customer loyalty solutions; MasterCard, which is a global payment solutions company that provides a variety of services in support of the credit, debt and related payment programs of financial institutions; and Open Text, which provides intranet, extranet and corporate portal solutions to organizations. Avoiding several laggards in the information technology sector, such as Apple, IBM and Oracle, boosted the Fund’s results as well.

Several Fund positions in the industrials sector added value. Top contributors in the sector were inland tank barge fleet operator Kirby, construction and engineering services firm Chicago Bridge & Iron, flow control equipment manufacturer IDEX, food preparation equipment manufacturer Middleby and aerospace and defense company HEICO.

In the consumer staples sector, positions in brewer The Boston Beer Company, food products manufacturer Hormel Foods and bakery foods producer Flowers Foods were outstanding performers. We also successfully avoided positions in several giant-capitalization laggards during the annual period, including The Coca-Cola Company, Altria Group, The Wal-Mart Stores and Procter & Gamble.

How did the Fund use derivatives and similar instruments during the reporting period?

The Fund did not use derivatives during the reporting period.

Did the Fund make any significant purchases or sales during the fiscal year?

In our view, the Fund was under-represented in the energy sector, so to enhance diversification, we were glad to identify two stocks that we believed well deserved to be in the portfolio—Chevron, one of the world’s largest integrated oil companies, and EQT, an integrated energy company with emphasis on Appalachian area natural gas supply, transmission and distribution. Both companies had inconsistent results prior to 2003, but over the past decade have demonstrated the ability to consistently grow their earnings and stock price. In each case, we purchased shares as a dip in their respective share prices offered what we believed to be an attractive entry point.

We initiated a Fund position in insurance company Prudential because, in our view, its earnings and stock price appeared to be back on a good growth track after struggling in the wake of the country’s financial crisis.

We reduced the Fund’s position in rail freight transportation company Union Pacific, taking profits after a strong run. We eliminated the Fund’s position in leather goods retailer Coach, as the company reported worse than expected earnings results. We sold the Fund’s position in food retailer Harris Teeter Supermarkets after its stock rose in response to a takeover bid by competitor Kroger.

Were there any notable changes in the Fund’s weightings during the 12-month period?

There were no material changes in the Fund’s sector weightings during the 12-month period ended December 31, 2013.

How was the Fund positioned relative to its benchmark index at the end of December 2013?

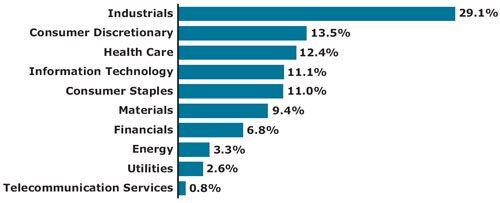

As of December 31, 2013, the Fund was overweighted relative to the S&P 500® Index in the industrials, consumer discretionary and materials sectors. The Fund was underweighted relative to the S&P 500® Index in the energy, financials and information technology sectors and rather neutrally weighted relative to the Index in the health care, consumer staples, utilities and telecommunication services sectors on the same date.

What is your tactical view and strategy for the months ahead?

Calendar year 2013 saw lower quality stocks outperform higher quality stocks, as investors became more bold and more confident in the economy and the financial system. Speculative stocks, such as those of biotechnology companies, and Initial Public Offerings, such as those of Facebook and Twitter, outperformed the broad U.S. equity market, along with the more cyclical, economically-sensitive stocks. Lagging were the more consistent, “steady-eddy,” long-term growth stocks in which we traditionally invest, i.e., those companies that have established strongholds in their market or market niche through proprietary products or services, which, in our view, gives them greater control of their own destiny and makes them less subject to ups and downs of the economy. We consider the Fund’s underperformance of the S&P 500® Index in 2013 as part of the natural ebb and flow of the market, as the lower quality stocks that performed poorly in 2011 and 2012 regained some ground. We do not know whether the trends of 2013 will continue into the new year, but, regardless of market trends and conditions, we do not intend to vary from our strategy of investing in high quality securities with a long-term perspective. Our portfolio turnover and trading costs have remained lower than many of our peers, as we have patience with a consistent grower until a change in the company’s strategy or its earnings and stock performance give solid reason to sell.

As always, we intend to stay true to our time-tested investment discipline going forward.

| The Value Line Fund, Inc. |

| Portfolio Highlights at December 31, 2013 (unaudited) |

Ten Largest Holdings

| | | | | | | | | | | | | |

| | | | | | | | | | | Percentage of |

| Issue | | Shares | | | Value | | | Net Assets |

| Rollins, Inc. | | | 75,600 | | | $ | 2,289,924 | | | | 1.8 | % |

| Alliance Data Systems Corp. | | | 8,300 | | | | 2,182,319 | | | | 1.7 | % |

| TJX Companies, Inc. (The) | | | 32,000 | | | | 2,039,360 | | | | 1.6 | % |

| AMETEK, Inc. | | | 36,750 | | | | 1,935,622 | | | | 1.5 | % |

| MasterCard, Inc. Class A | | | 2,300 | | | | 1,921,558 | | | | 1.5 | % |

| AutoZone, Inc. | | | 4,000 | | | | 1,911,760 | | | | 1.5 | % |

| Yum! Brands, Inc. | | | 24,800 | | | | 1,875,128 | | | | 1.5 | % |

| Affiliated Managers Group, Inc. | | | 8,000 | | | | 1,735,040 | | | | 1.4 | % |

| Church & Dwight Co., Inc. | | | 26,000 | | | | 1,723,280 | | | | 1.4 | % |

| Roper Industries, Inc. | | | 12,400 | | | | 1,719,632 | | | | 1.4 | % |

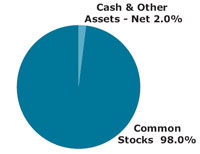

Asset Allocation – Percentage of Net Assets

| Sector Weightings – Percentage of Total Investment Securities* |

*Sector weightings exclude short-term investments.

The following graph compares the performance of The Value Line Fund, Inc. to that of the S&P 500 Index (the “Index”). The Value Line Fund, Inc. is a professionally managed mutual fund, while the Index is not available for investment and is unmanaged. The returns for the Index do not reflect charges, expenses or taxes, but do include the reinvestment of dividends. The comparison is shown for illustrative purposes only.

| |

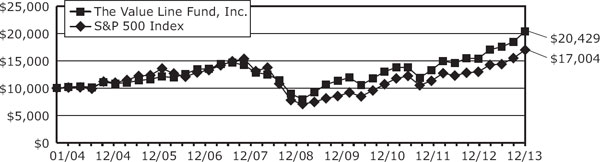

| Comparison of a Change in Value of a $10,000 Investment in The Value Line Fund, Inc. and the S&P 500 Index* |

| |

|

| | | | | | | | |

| Performance Data: ** | | | | | | | |

| | | | | | | | |

| | | Average Annual | | | Growth of an Assumed | |

| | | Total Return | | | Investment of $10,000 | |

| 1 year ended 12/31/13 | | 30.86 | % | | | $13,086 | |

| 5 years ended 12/31/13 | | 16.87 | % | | | $21,800 | |

| 10 years ended 12/31/13 | | 5.45 | % | | | $17,004 | |

| * | The Standard and Poor’s 500 Stock Index is an unmanaged index that is representative of the larger-capitalization stocks traded in the United States. |

| ** | The performance data quoted represent past performance and are no guarantee of future performance. The average annual total returns and growth of an assumed investment of $10,000 include dividends reinvested and capital gains distributions accepted in shares. The investment return and principal value of an investment will fluctuate so that an investment, when redeemed, may be worth more or less than its original cost. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| The Value Line Fund, Inc. | |

| Schedule of Investments | December 31, 2013 |

| | | | | | | |

| Shares | | | | | Value | |

| COMMON STOCKS (98.0%) | | | | |

| | | | | | | |

| | | CONSUMER DISCRETIONARY (13.2%) | | | | |

| 4,000 | | AutoZone, Inc. * | | $ | 1,911,760 | |

| 13,600 | | BorgWarner, Inc. | | | 760,376 | |

| 22,400 | | Brinker International, Inc. | | | 1,038,016 | |

| 6,000 | | Buckle, Inc. (The) (1) | | | 315,360 | |

| 7,600 | | Buffalo Wild Wings, Inc. * | | | 1,118,720 | |

| 12,300 | | Dick’s Sporting Goods, Inc. | | | 714,630 | |

| 7,000 | | Domino’s Pizza, Inc. | | | 487,550 | |

| 8,700 | | Gildan Activewear, Inc. | | | 463,797 | |

| 33,000 | | LKQ Corp. * | | | 1,085,700 | |

| 15,300 | | McDonald’s Corp. | | | 1,484,559 | |

| 10,000 | | NIKE, Inc. Class B | | | 786,400 | |

| 3,200 | | O’Reilly Automotive, Inc. * | | | 411,872 | |

| 10,400 | | Penn National Gaming, Inc. * | | | 149,032 | |

| 9,300 | | Starbucks Corp. | | | 729,027 | |

| 32,000 | | TJX Companies, Inc. (The) | | | 2,039,360 | |

| 10,400 | | VF Corp. | | | 648,336 | |

| 16,800 | | Wolverine World Wide, Inc. | | | 570,528 | |

| 24,800 | | Yum! Brands, Inc. | | | 1,875,128 | |

| | | | | | 16,590,151 | |

| | | | | | | |

| | | CONSUMER STAPLES (10.8%) | | | | |

| 3,100 | | Boston Beer Co., Inc. (The) Class A * | | | 749,549 | |

| 4,900 | | British American Tobacco PLC ADR | | | 526,358 | |

| 4,000 | | Bunge Ltd. | | | 328,440 | |

| 11,400 | | Casey’s General Stores, Inc. | | | 800,850 | |

| 26,000 | | Church & Dwight Co., Inc. | | | 1,723,280 | |

| 7,000 | | Costco Wholesale Corp. | | | 833,070 | |

| 7,500 | | Energizer Holdings, Inc. | | | 811,800 | |

| 40,500 | | Flowers Foods, Inc. | | | 869,535 | |

| 19,000 | | General Mills, Inc. | | | 948,290 | |

| 33,000 | | Hormel Foods Corp. | | | 1,490,610 | |

| 15,700 | | Ingredion, Inc. | | | 1,074,822 | |

| 18,100 | | J&J Snack Foods Corp. | | | 1,603,479 | |

| 9,000 | | PepsiCo, Inc. | | | 746,460 | |

| 6,000 | | Reynolds American, Inc. | | | 299,940 | |

| 12,000 | | Whole Foods Market, Inc. | | | 693,960 | |

| | | | | | 13,500,443 | |

| | | ENERGY (3.2%) | | | | |

| 6,000 | | Chevron Corp. | | | 749,460 | |

| 2,000 | | Core Laboratories N.V. | | | 381,900 | |

| 14,000 | | Enbridge, Inc. | | | 611,520 | |

| 10,000 | | EQT Corp. | | | 897,800 | |

| 5,600 | | FMC Technologies, Inc. * | | | 292,376 | |

| 13,400 | | Noble Energy, Inc. | | | 912,674 | |

| 2,600 | | Oceaneering International, Inc. | | | 205,088 | |

| | | | | | 4,050,818 | |

| | | | | | | |

| | | FINANCIALS (6.6%) | | | | |

| 8,000 | | Affiliated Managers Group, Inc. * | | | 1,735,040 | |

| 20,000 | | AFLAC, Inc. | | | 1,336,000 | |

| | | | | | | |

| Shares | | | | | Value | |

| 9,000 | | American Tower Corp. REIT | | $ | 718,380 | |

| 3,000 | | BlackRock, Inc. | | | 949,410 | |

| 500 | | Everest Re Group Ltd. | | | 77,935 | |

| 10,400 | | Gaming and Leisure Properties, Inc. REIT * | | | 528,424 | |

| 6,300 | | M&T Bank Corp. (1) | | | 733,446 | |

| 4,400 | | MetLife, Inc. | | | 237,248 | |

| 2,000 | | PartnerRe Ltd. | | | 210,860 | |

| 5,000 | | Prudential Financial, Inc. | | | 461,100 | |

| 8,000 | | Royal Bank of Canada | | | 537,840 | |

| 4,900 | | Stifel Financial Corp. * | | | 234,808 | |

| 6,600 | | T. Rowe Price Group, Inc. | | | 552,882 | |

| | | | | | 8,313,373 | |

| | | | | | | |

| | | HEALTH CARE (12.1%) | | | | |

| 11,600 | | Alexion Pharmaceuticals, Inc. * | | | 1,543,496 | |

| 9,600 | | Allergan, Inc. | | | 1,066,368 | |

| 5,800 | | C.R. Bard, Inc. | | | 776,852 | |

| 13,740 | | Catamaran Corp. * | | | 652,375 | |

| 20,400 | | Cerner Corp. * | | | 1,137,096 | |

| 800 | | Cooper Cos., Inc. (The) | | | 99,072 | |

| 1,500 | | DaVita HealthCare Partners, Inc. * | | | 95,055 | |

| 3,900 | | DENTSPLY International, Inc. | | | 189,072 | |

| 6,000 | | Edwards Lifesciences Corp. * | | | 394,560 | |

| 15,340 | | Express Scripts Holding Co * | | | 1,077,482 | |

| 12,700 | | Henry Schein, Inc. * | | | 1,451,102 | |

| 5,400 | | IDEXX Laboratories, Inc. * | | | 574,398 | |

| 4,800 | | McKesson Corp. | | | 774,720 | |

| 16,800 | | Mednax, Inc. * | | | 896,784 | |

| 4,700 | | Mettler-Toledo International, Inc. * | | | 1,140,173 | |

| 9,100 | | Novo Nordisk A/S ADR | | | 1,681,316 | |

| 10,000 | | Teva Pharmaceutical Industries Ltd. ADR | | | 400,800 | |

| 10,200 | | Thermo Fisher Scientific, Inc. | | | 1,135,770 | |

| 1,400 | | Universal Health Services, Inc. Class B | | | 113,764 | |

| | | | | | 15,200,255 | |

| | | | | | | |

| | | INDUSTRIALS (28.5%) | | | | |

| 7,800 | | Acuity Brands, Inc. | | | 852,696 | |

| 36,750 | | AMETEK, Inc. | | | 1,935,622 | |

| 22,200 | | Canadian National Railway Co. | | | 1,265,844 | |

| 800 | | Canadian Pacific Railway Ltd. | | | 121,056 | |

| 10,000 | | Chicago Bridge & Iron Co. N.V. | | | 831,400 | |

| 15,000 | | CLARCOR, Inc. | | | 965,250 | |

| 6,000 | | Clean Harbors, Inc. * | | | 359,760 | |

| 20,700 | | Danaher Corp. | | | 1,598,040 | |

| 31,000 | | Donaldson Co., Inc. | | | 1,347,260 | |

| 4,800 | | Equifax, Inc. | | | 331,632 | |

| 2,400 | | Esterline Technologies Corp. * | | | 244,704 | |

| 8,000 | | Fastenal Co. | | | 380,080 | |

| 7,000 | | FedEx Corp. | | | 1,006,390 | |

| | | | | | | |

| Shares | | | | | Value | |

| 7,900 | | General Dynamics Corp. | | $ | 754,845 | |

| 7,300 | | Graco, Inc. | | | 570,276 | |

| 13,983 | | HEICO Corp. | | | 810,315 | |

| 15,000 | | IDEX Corp. | | | 1,107,750 | |

| 3,500 | | IHS, Inc. Class A * | | | 418,950 | |

| 5,850 | | ITT Corp. | | | 254,007 | |

| 6,800 | | J.B. Hunt Transport Services, Inc. | | | 525,640 | |

| 8,200 | | Kansas City Southern | | | 1,015,406 | |

| 14,700 | | Kirby Corp. * | | | 1,458,975 | |

| 5,400 | | L-3 Communications Holdings, Inc. | | | 577,044 | |

| 2,000 | | Lincoln Electric Holdings, Inc. | | | 142,680 | |

| 2,300 | | Middleby Corp. (The) * | | | 551,931 | |

| 2,500 | | Oshkosh Corp. | | | 125,950 | |

| 9,200 | | Parker Hannifin Corp. | | | 1,183,488 | |

| 5,700 | | Precision Castparts Corp. | | | 1,535,010 | |

| 19,000 | | Republic Services, Inc. | | | 630,800 | |

| 2,800 | | Rockwell Automation, Inc. | | | 330,848 | |

| 75,600 | | Rollins, Inc. | | | 2,289,924 | |

| 12,400 | | Roper Industries, Inc. | | | 1,719,632 | |

| 12,000 | | Stericycle, Inc. * | | | 1,394,040 | |

| 15,600 | | Toro Co. (The) | | | 992,160 | |

| 4,800 | | Union Pacific Corp. | | | 806,400 | |

| 11,400 | | United Technologies Corp. | | | 1,297,320 | |

| 5,600 | | Valmont Industries, Inc. | | | 835,072 | |

| 4,900 | | W.W. Grainger, Inc. | | | 1,251,558 | |

| 10,500 | | Wabtec Corp. | | | 779,835 | |

| 25,300 | | Waste Connections, Inc. | | | 1,103,839 | |

| | | | | | 35,703,429 | |

| | | | | | | |

| | | INFORMATION TECHNOLOGY (10.9%) | | | | |

| 17,800 | | Accenture PLC Class A | | | 1,463,516 | |

| 8,300 | | Alliance Data Systems Corp. * | | | 2,182,319 | |

| 7,000 | | Amphenol Corp. Class A | | | 624,260 | |

| 3,700 | | Anixter International, Inc. | | | 332,408 | |

| 13,500 | | ANSYS, Inc. * | | | 1,177,200 | |

| 6,500 | | Automatic Data Processing, Inc. | | | 525,265 | |

| 16,000 | | Cognizant Technology Solutions Corp. Class A * | | | 1,615,680 | |

| 3,500 | | Equinix, Inc. * | | | 621,075 | |

| 5,400 | | Fiserv, Inc. * | | | 318,870 | |

| 2,300 | | MasterCard, Inc. Class A | | | 1,921,558 | |

| 2,800 | | MICROS Systems, Inc. * | | | 160,636 | |

| 8,800 | | Open Text Corp. | | | 809,248 | |

| 24,000 | | Salesforce.com, Inc. * | | | 1,324,560 | |

| 6,100 | | WEX, Inc. * | | | 604,083 | |

| | | | | | 13,680,678 | |

| | | | | | | |

| | | MATERIALS (9.3%) | | | | |

| 3,000 | | Airgas, Inc. | | | 335,550 | |

| 12,000 | | Ball Corp. | | | 619,920 | |

| 25,600 | | Crown Holdings, Inc. * | | | 1,140,992 | |

| 12,000 | | Ecolab, Inc. | | | 1,251,240 | |

| 22,400 | | FMC Corp. | | | 1,690,304 | |

| 2,000 | | NewMarket Corp. | | | 668,300 | |

| 10,000 | | Packaging Corp. of America | | | 632,800 | |

| 10,300 | | Praxair, Inc. | | | 1,339,309 | |

See Notes to Financial Statements. |

| 17 |

| Schedule of Investments (continued) |

| | | | | | | |

| Shares | | | | | Value | |

| 12,000 | | Scotts Miracle-Gro Co. (The) Class A | | $ | 746,640 | |

| 11,400 | | Sigma-Aldrich Corp. | | | 1,071,714 | |

| 25,900 | | Silgan Holdings, Inc. | | | 1,243,718 | |

| 12,400 | | Valspar Corp. (The) | | | 883,996 | |

| | | | | | 11,624,483 | |

| | | | | | | |

| | | TELECOMMUNICATION SERVICES (0.8%) | | | | |

| 13,000 | | Crown Castle International Corp. * | | | 954,590 | |

| | | | | | | |

| | | UTILITIES (2.6%) | | | | |

| 10,000 | | ITC Holdings Corp. | | | 958,200 | |

| 4,000 | | NextEra Energy, Inc. | | | 342,480 | |

| 15,000 | | ONEOK, Inc. | | | 932,700 | |

| 23,000 | | Questar Corp. | | | 528,770 | |

| 10,900 | | Wisconsin Energy Corp. | | | 450,606 | |

| | | | | | 3,212,756 | |

| | | | | | | |

| | | TOTAL COMMON STOCKS

(Cost $65,914,055) (98.0%) | | | 122,830,976 | |

| | | | | | | | |

| Principal | | | | | | |

| Amount | | | | | Value | |

| SHORT-TERM INVESTMENTS (2.0%) | | | | |

| | | | | | | | |

| | | | REPURCHASE AGREEMENTS (1.2%) | | | | |

| $ | 1,500,000 | | With Morgan Stanley, 0.01%, dated 12/31/13, due 01/02/14, delivery value $1,500,001 (collateralized by $1,530,000 U.S. Treasury Notes 1.000% due 03/31/17, with a value of $1,537,537) | | $ | 1,500,000 | |

| | | | | | | | |

| Principal | | | | | | |

| Amount | | | | | Value | |

| | | | JOINT REPURCHASE AGREEMENTS (INVESTMENTS OF CASH COLLATERAL FOR SECURITIES ON LOAN) (0.8%) | | | | |

| $ | 352,513 | | Joint Repurchase Agreement with Morgan Stanley, 0.02%, dated 12/31/13, due 01/02/14, delivery value $352,514 (collateralized by $359,564 U.S. Treasury Bonds 4.250% - 8.000% due 11/15/21 - 11/15/40 and U.S. Treasury Notes 2.625% - 2.750% due 11/15/20 - 11/15/23, with a value of $357,734) | | $ | 352,513 | |

| | 520,377 | | Joint Repurchase Agreement with Barclays, 0.01%, dated 12/31/13, due 01/02/14, delivery value $520,377 (collateralized by $530,785 U.S. Treasury Inflation Indexed Notes 1.250% - 1.875% due 04/15/14 - 07/15/15, with a value of $526,773) | | | 520,377 | |

| | | | | | | | |

| Principal | | | | |

| Amount | | | Value | |

| $ | 83,932 | | Joint Repurchase Agreement with Citigroup, 0.01%, dated 12/31/13, due 01/02/14, delivery value $83,932 (collateralized by $85,611 U.S. Treasury Bills 0.000% due 02/20/14, with a value of $85,611) | | $ | 83,932 | |

| | | | | | | 956,822 | |

| | | | | | | | |

| | | | TOTAL SHORT-TERM INVESTMENTS (Cost $2,456,822) (2.0%) | | | 2,456,822 | |

| | | | | | | | |

| | | | TOTAL INVESTMENT SECURITIES (100.0%) (Cost $68,370,877) | | $ | 125,287,798 | |

| | | | | |

EXCESS OF LIABILITIES OVER CASH AND OTHER ASSETS (0.0%) | | | (19,763 | ) |

| | $ | 125,268,035 | |

| | | | | | | | |

NET ASSET VALUE OFFERING AND REDEMPTION PRICE, PER OUTSTANDING SHARE ($125,268,035 ÷ 9,278,231 shares outstanding) | | $ | 13.50 | |

| | |

| * | Non-income producing. |

| (1) | A portion or all of the security was held on loan. As of December 31, 2013, the market value of the securities on loan was $1,048,806. |

| ADR | American Depositary Receipt. |

| REIT | Real Estate Investment Trust. |

The following table summarizes the inputs used to value the Fund’s investments in securities as of December 31, 2013 (See Note 1B):

| | | | | | | | | | | | | |

| The Value Line Fund, Inc. | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | |

| Common Stocks | | $ | 122,830,976 | | | $ | — | | | $ | — | | | $ | 122,830,976 | |

| Short-Term Investments | | | — | | | | 2,456,822 | | | | — | | | | 2,456,822 | |

| Total | | $ | 122,830,976 | | | $ | 2,456,822 | | | $ | — | | | $ | 125,287,798 | |

See Notes to Financial Statements. |

| 18 |

| VALUE LINE INCOME AND GROWTH FUND, INC. |

| |

| |

| INVESTMENT OBJECTIVE AND STRATEGY |

The Fund’s primary investment objective is income, as high and dependable as is consistent with reasonable risk. Capital growth to increase total return is a secondary objective.

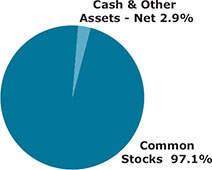

To achieve the Fund’s goals, the Adviser invests not less than 50% of the Fund’s net assets in common or preferred stocks or securities convertible into common stock which may or may not pay dividends. The balance of the Fund’s net assets are primarily invested in U.S. government securities, money market securities and investment grade debt securities rated at the time of purchase from the highest (AAA) to medium (BBB) quality. Although the Fund can invest in companies of any size, it generally invests in U.S. securities issued by larger, more established companies (those with a market capitalization of more than $5 billion).

| |

Manager Discussion of Fund Performance |

Below, Value Line Income and Growth Fund, Inc. portfolio managers Mark T. Spellman and Liane Rosenberg discuss the Fund’s performance and positioning for the 12 months ended December 31, 2013.

How did the Fund perform during the annual period?

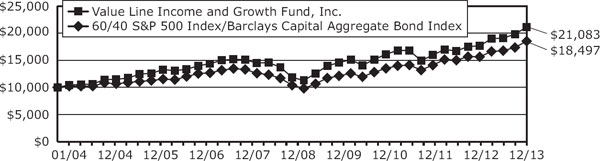

The Fund generated a total return of 19.55% during the 12 months ended December 31, 2013. This compares to the 18.62% return of the Fund’s blended benchmark, comprised 60% of the S&P 500® Index and 40% of the Barclays U.S. Aggregate Bond Index (the “Barclays Index”), during the same period.

What key factors were responsible for the Fund’s performance during the 12-month reporting period?

The Fund benefited most from effective asset allocation. Throughout the 12-month reporting period, the Fund was underweighted fixed income and overweighted equities. With U.S. equities, as measured by the S&P 500® Index, up 32.39% during the annual period, and bonds, as measured by the Barclays Index, posting a return of -2.02%, this asset allocation clearly added value. Stock selection overall within the equity portion of the Fund also proved beneficial.

Which equity market sectors most significantly affected Fund performance?

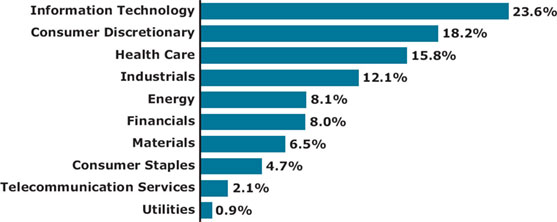

Stock selection in the information technology, industrials, utilities and health care sectors contributed most positively to the Fund’s results. The Fund also benefited from having underweighted allocations to the information technology and energy sectors, which each lagged the S&P 500® Index during the annual period, and from having an overweighted allocation to the industrials sector, which outpaced the S&P 500® Index during the annual period.

Only partially offsetting these positive contributors was stock selection in the consumer discretionary and energy sectors, which detracted. Having an overweighted allocation to utilities, which lagged the S&P 500® Index during the annual period, and having underweighted exposures to the consumer discretionary and health care sectors, which outpaced the broad U.S. equity market during the annual period, also hurt.

What were some of the Fund’s best-performing individual stocks?

Contributing most to the Fund’s relative results were retail food and drug chain operator Safeway, financial services provider Charles Schwab and construction and engineering services firm Chicago Bridge & Iron. Safeway performed well, as its restructuring program added value and its store performance improved. Shares of Charles Schwab rose, as its fee revenue and market share increased with the stock market’s rally. Chicago Bridge & Iron’s shares rose significantly, as its bookings for new construction projects rose and as its acquisition of a competitor positively impacted its results.

Which stocks detracted significantly from the Fund’s performance during the annual period?

During the annual period, the stocks that detracted most from the Fund’s performance were Canadian gold producer Yamana Gold, data storage center real estate investment trust (REIT) Digital Realty Trust and offshore oil and gas drilling contractor Diamond Offshore Drilling. Shares of Yamana Gold fell significantly reflecting the precipitous decline in the price of gold bullion. Digital Realty Trust performed poorly along with the broad REIT industry. The company also posted less than expected operating results. Diamond Offshore Drilling saw its shares decline due to poor fundamentals in offshore drilling as well as company-specific shortfalls.

Did the equity portion of the Fund make any significant purchases or sales?

During the fiscal year, we initiated positions in semiconductor device manufacturer Qualcomm, specialty pharmaceuticals company Allergan and Canadian telecommunications carrier BCE. We established a position in Qualcomm when the stock declined after an earnings disappointment, and we considered it an attractive entry point based on a longer-term perspective. We purchased Allergan after a dip in its share price, as we felt the fundamental outlook for the company was positive and the market had overreacted to news that it was delaying final studies for drugs to treat age-related macular degeneration and baldness. We initiated a position in BCE, as we believe its dividend yield is attractive and its shares, at the time of purchase, undervalued.

We sold the Fund’s position in integrated utilities company The Southern Company, as we became increasingly bearish on the outlook for this stock and on electric utilities in general. We exited the Fund’s position in clinical laboratory test provider Laboratory Corporation of America, after it hit the price target we had established for the company.

Were there any notable changes in the equity portion of the Fund’s weightings during the 12-month period?

During the annual period, we decreased weightings in the utilities sector and in the REITs industry, and we increased positions in the information technology and financials sectors.

How was the equity portion of the Fund positioned relative to its benchmark index at the end of December 2013?

As of December 31, 2013, the Fund was overweighted relative to the S&P 500® Index in the industrials, utilities, financials, telecommunication services and consumer staples sectors. The Fund was underweighted relative to the S&P 500® Index in the consumer discretionary, materials, information technology, energy and health care sectors on the same date.

What was the duration strategy of the fixed income portion of the Fund?

We kept the fixed income portion of the Fund’s duration short relative to that of the Barclays Index. As interest rates rose, this duration positioning contributed positively to relative results.

Which fixed income market segments most significantly affected Fund performance?

Overall, the fixed income portion of the Fund underperformed its benchmark, the Barclays Index. Detracting most from relative results was security selection within the securitized sector. Within the securitized sector, we held an overweighted allocation to seven-year to 10-year maturities. The flattening yield curve benefited shorter-term and longer-term maturities, where the Fund was underweight, but hurt the intermediate segment of the yield curve.

Conversely, having an underweighted allocation to U.S. Treasuries, the worst performing sector in the Barclays Index during the annual period, contributed most positively to the fixed income portion of the Fund’s performance. An overweighted allocation to corporate bonds also added value, as this sector experienced steady spread tightening throughout the year. Within the Fund’s corporate bond allocation, a heavier weighting in bonds of financial institutions proved beneficial.

Were there any notable changes in the fixed income portion of the Fund’s weightings during the 12-month period?

The most significant sector shifts in the fixed income portion of the Fund were a reduction in U.S. Treasuries and an increase in corporate bonds, both investment grade and high yield.

How was the fixed income portion of the Fund positioned relative to its benchmark index at the end of December 2013?

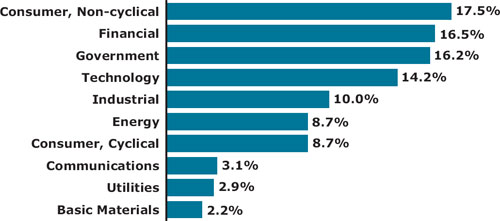

As of December 31, 2013, the fixed income portion of the Fund was overweight relative to the Barclays Index in corporate bonds. The Fund was underweight relative to the Barclays Index in U.S. Treasuries and government-related securities and was rather neutrally weighted to the benchmark index in the securitized sector on the same date.

How did the Fund’s overall asset allocation shift from beginning to end of the annual period?

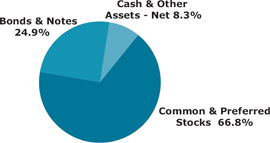

At the end of December 2012, the Fund had a weighting of 63% in stocks, 4% in bonds convertible into common stocks, 28% in fixed income securities and 3% in cash equivalents. By mid-year 2013, cash levels began to rise due to net sales in the equity portion of the Fund, as stock-specific price targets were hit and shares sold to take profits. Due primarily to market appreciation and depreciation, at the end of December 2013, the Fund had a weighting of 66% in stocks, 4% in bonds convertible into common stocks, 22% in fixed income securities and 8% in cash equivalents.

How did the Fund use derivatives and similar instruments during the reporting period?

During the reporting period, the Fund made limited use of covered equity call writing as a method of generating additional income for the Fund. Covered equity call writing is an options strategy whereby an investor holds a long position in an asset and writes, or sells, call options on that same asset in an attempt to generate increased income from the asset.