UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04537

Liberty All-Star Growth Fund, Inc.

(exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Tane T. Tyler, General Counsel

ALPS Fund Services, Inc.

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

| Date of fiscal year end: | December 31 | |||

| Date of reporting period: | January 1 - December 31, 2010 | |||

Item 1. Reports to Stockholders.

| LIBERTY ALL-STAR® GROWTH FUND | 1 | |||||

PRESIDENT’S LETTER (UNAUDITED) |

Fellow Shareholders:

Equity investors generally enjoyed a rewarding year in 2010, as stocks built on 2009’s momentum, posting gains in three out of four quarters and finishing the year with a strong December.

For the year, the S&P 500 Index rose 15.06 percent on top of the 26.46 percent advance in 2009. The S&P 500 Index gained 10.76 percent in the final quarter and headed into 2011 on the strength of a 6.68 percent return in December. The technology-oriented NASDAQ Composite Index and the Russell 3000® Growth Index rose 18.02 percent and 17.64 percent, respectively, in 2010. Reinforcing the patience and long-term commitment that is often required of investors—especially as they suffered through the financial crisis of 2008 and early 2009—the S&P 500 Index returned 93.08 percent from its low in March 2009 through year-end 2010. The NASDAQ Composite Index has returned 109.11 percent since early March 2009 and the Russell 3000® Growth has increased 97.00 percent.

The stock market performed well in 2010 in spite of a lack of enthusiasm, periodic bouts of doubt, continued problems with employment and housing on the home front, and nervousness over sovereign debt abroad. Many economists gave little credence to the durability of the recovery even as it made progress through the year, and some high profile strategists continued to believe that the economy was vulnerable to a double dip recession. Given the depths to which the economy had plunged, however, a slow but steady recovery was acceptable, even if not warmly embraced. Despite the lackluster economy, the major source of strength for the stock market has been the strong rebound in corporate profits. Profitability was driven by surging productivity and a reasonable pickup in demand. During the recession, companies lowered their break even points by shuttering inefficient plants, reducing capacity and lowering unit labor costs—setting up a scenario in which even a modest rebound in economic activity would produce a strong recovery in corporate profitability.

February 2011

As it turned out, the only negative period was the second quarter, when the S&P 500 Index retreated 11.43 percent and the Russell 3000® Growth Index declined 11.55 percent. Many factors contributed to the retracement: chief among them were the previously mentioned sovereign debt problems, and one unnerving event, the so-called “flash crash” on May 6, when the Dow Jones Industrial Average briefly and inexplicably fell 1,000 points. Stocks continued to drift lower through June before rallying in July, only to weaken again in August. On August 26, however, Federal Reserve Chairman Ben Bernanke opened the door for another round of bond purchases to boost the economy. From that point, the trajectory was higher through the end of the year, with the November 3 announcement of another round of quantitative easing.

For the year, Liberty All-Star® Growth Fund returned 21.47 percent with shares valued at net asset value (“NAV”), 21.79 percent with shares valued at NAV with dividends reinvested and 34.84 percent with shares valued at market price with dividends reinvested. These returns were strong on both an absolute and a relative basis, as all three measures topped the Russell 3000® Growth Index (+17.64 percent), the NASDAQ Composite Index (+18.02 percent) and the S&P 500 Index (+15.06 percent). Similarly, they also topped the Fund’s primary benchmark, the Lipper Multi-Cap Growth Mutual Fund Average, which advanced 18.62 percent. The Fund’s NAV reinvested return ranked in the 29th percentile of all funds in that universe for 2010. Longer term, off the March 2009 low, the Fund’s NAV with dividends reinvested advanced 99.40 percent by year-end 2010, while Fund shares valued at market price with dividends reinvested gained 145.66 percent over the same period.

Over the course of the year, the discount at which Fund shares traded relative to their underlying NAV ranged from 6.3 percent to 16.2 percent versus a range of 13.9 percent to 24.6 percent in 2009. We are pleased that the discount narrowed over the year, even though it remains above the Fund’s historical average. We believe

www.all-starfunds.com | ASG |

| 2 | LIBERTY ALL-STAR® GROWTH FUND | |||||

PRESIDENT’S LETTER (UNAUDITED) |

that the discount range of closed-end domestic equity funds remains relatively wide as investors have favored bond and international equities, particularly emerging markets. We believe those investment flows may be in the process of reversing and if the current direction holds we should see discounts continue to narrow.

Once again, in this annual report we offer a question and answer session with the Fund’s three growth style investment managers. We believe you will find the comments of these leading investment managers to be both interesting and insightful. As we have also done in recent annual reports, we once again offer a brief summary of the Fund’s attributes (on pages 4 and 5). I urge you to revisit these attributes, as they help to make the Fund a unique and attractive investment vehicle.

One of those attributes is the Fund’s distribution policy. This policy is a major component of the Fund’s total return. Often, however, these distributions—either in cash or reinvested in additional Fund shares—are overlooked. As you will see in the table on the facing page, these distributions add up over time—a total of $5.54 per share over the past 10 years. We would emphasize that shareholders need to include these distributions when determining the return on their investment in the Fund.

We are pleased that the Fund demonstrated its value as a high quality, growth equity holding by allowing shareholders to fully participate in the stock market’s rebound since the March 2009 low. We would also point out that the Fund’s NAV reinvested return ranks in the top third of its primary benchmark for the trailing three years, which includes the worst financial crisis since the 1930s. This is testament to the quality of the Fund’s three growth style investment managers. For our part, we at Liberty All-Star® Growth Fund will continue to diligently manage the Fund with the best long-term interests of shareholders first and foremost.

Sincerely,

William R. Parmentier, Jr.

President and Chief Executive Officer

Liberty All-Star® Growth Fund, Inc.

ANNUAL REPORT |

DECEMBER 31, 2010

DECEMBER 31, 2010| LIBERTY ALL-STAR® GROWTH FUND | 3 | |||||

PRESIDENT’S LETTER (UNAUDITED) |

FUND STATISTICS AND SHORT-TERM PERFORMANCE PERIODS ENDING DECEMBER 31, 2010 |

| |||||||||||||

FUND STATISTICS: | ||||||||||||||

Net Asset Value (NAV) | $4.57 | |||||||||||||

Market Price | $4.25 | |||||||||||||

Discount | 7.0% | |||||||||||||

| Quarter | 2010 | |||||||||||||

Distributions | $0.07 | $0.25 | ||||||||||||

Market Price Trading Range | $3.75 to $4.33 | $2.95 to $4.33 | ||||||||||||

Discount Range | 6.3% to 9.6% | 6.3% to 16.2% | ||||||||||||

PERFORMANCE: | ||||||||||||||

Shares Valued at NAV | 11.00% | 21.47% | ||||||||||||

Shares Valued at NAV with Dividends Reinvested | 11.10% | 21.79% | ||||||||||||

Shares Valued at Market Price with Dividends Reinvested | 13.35% | 34.84% | ||||||||||||

NASDAQ Composite Index | 12.32% | 18.02% | ||||||||||||

Russell 3000® Growth Index | 12.26% | 17.64% | ||||||||||||

S&P 500 Index | 10.76% | 15.06% | ||||||||||||

Lipper Multi-Cap Growth Mutual Fund Average* | 11.97% | 18.62% | ||||||||||||

NAV Reinvested Percentile Rank (1 = best; 100 = worst) | 67th | 29th | ||||||||||||

Number of Funds in Category | 467 | 433 | ||||||||||||

LONG-TERM PERFORMANCE SUMMARY AND DISTRIBUTIONS | ANNUALIZED RATES OF RETURN | |||||||||||||

PERIODS ENDING DECEMBER 31, 2010 | 3 YEARS | 5 YEARS | 10 YEARS | |||||||||||

LIBERTY ALL-STAR® GROWTH FUND, INC. | ||||||||||||||

Distributions | $0.96 | $2.16 | $5.54 | |||||||||||

Shares Valued at NAV | (1.35%) | 3.56% | 1.01% | |||||||||||

Shares Valued at NAV with Dividends Reinvested | (0.59%) | 4.27% | 1.46% | |||||||||||

Shares Valued at Market Price with Dividends Reinvested | (2.59%) | 4.70% | 2.15% | |||||||||||

NASDAQ Composite Index | 0.98% | 4.69% | 1.41% | |||||||||||

Russell 3000® Growth Index | (0.26%) | 3.88% | 0.30% | |||||||||||

S&P 500 Index | (2.86%) | 2.29% | 1.41% | |||||||||||

Lipper Multi-Cap Growth Mutual Fund Average* | (1.92%) | 3.46% | 1.20% | |||||||||||

NAV Reinvested Percentile Rank (1 = best; 100 = worst) | 33rd | 38th | 53rd | |||||||||||

Number of Funds in Category | 359 | 298 | 202 | |||||||||||

* Percentile ranks calculated using the Fund’s NAV Reinvested results within the Lipper Multi-Cap Growth Open-end Mutual Fund Universe.

Figures shown for the Fund and the Lipper Multi-Cap Growth Mutual Fund Average are total returns, which include dividends, after deducting Fund expenses. The Fund’s performance is calculated assuming that a shareholder exercised all primary rights in the Fund’s rights offerings. Figures shown for the unmanaged NASDAQ Composite Index, the Russell 3000®Growth Index and the S&P 500 Index are total returns, including dividends. A description of the Lipper benchmark and the market indices can be found on page 35.

Past performance cannot predict future results. Performance will fluctuate with market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of the Fund. Therefore, the Fund cannot predict whether its shares will trade at, below or above net asset value.

www.all-starfunds.com | ASG |

| 4 | LIBERTY ALL-STAR® GROWTH FUND | |||||

UNIQUE FUND ATTRIBUTES (UNAUDITED) |

| Multi-management for Individual Investors

| |||

Large institutional investors have traditionally employed multiple investment managers. With three investment managers investing across the full capitalization range of growth stocks, the Fund brings multi-management to individual investors. | ||||

| Real-time Trading and Liquidity

| |||

The Fund has a fixed number of shares that trade on the New York Stock Exchange and other exchanges. Share pricing is continuous—not just end-of-day, as it is with open-end mutual funds. In addition, Fund shares offer immediate liquidity and there are no annual sales fees. | ||||

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 5 | |||||

UNIQUE FUND ATTRIBUTES (UNAUDITED) |

| Access to Institutional Managers

| |||

The Fund’s investment managers invest primarily for pension funds, endowments, foundations and other institutions. Because institutional managers are closely monitored by their clients, they tend to be more disciplined and consistent in their investment process. | ||||

| Monitoring and Rebalancing

| |||

ALPS Advisors continuously monitors these investment managers to ensure that they are performing as expected and adhering to their style and strategy, and will replace the managers when warranted. Periodic rebalancing maintains the Fund’s structural integrity and is a well-recognized investment discipline. | ||||

| Alignment and Objectivity

| |||

Alignment with shareholders’ best interests and objective decision-making help to ensure that the Fund is managed openly and equitably. In addition, the Fund is governed by a Board of Directors that is elected by and responsible to shareholders. | ||||

| Distribution Policy

| |||

Since 1997, the Fund has followed a policy of paying annual distributions on its shares at a rate that approximates historical equity market returns. The current annual distribution rate is 6 percent of the Fund’s net asset value (paid quarterly at 1.5 percent per quarter), providing a systematic mechanism for distributing funds to shareholders.

| ||||

www.all-starfunds.com | ASG |

| 6 | LIBERTY ALL-STAR® GROWTH FUND | |||||

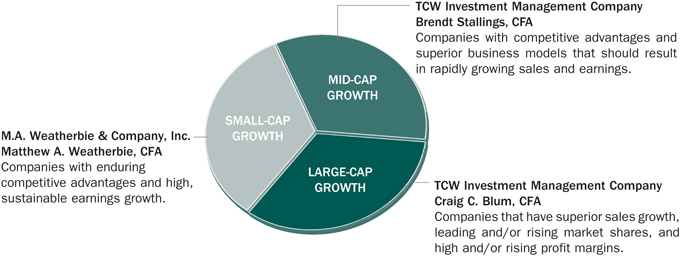

INVESTMENT MANAGERS/PORTFOLIO CHARACTERISTICS (UNAUDITED) | ||||||

THE FUND’S THREE GROWTH INVESTMENT MANAGERS AND THE MARKET CAPITALIZATION ON WHICH EACH FOCUSES: |

| |||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||

MANAGERS’ DIFFERING INVESTMENT STRATEGIES ARE REFLECTED IN PORTFOLIO CHARACTERISTICS |

| |||||||||||||||||||||||||||||

The portfolio characteristics table below is a regular feature of the Fund’s shareholder reports. It serves as a useful tool for understanding the value of the Fund’s multi-managed portfolio. The characteristics are different for each of the Fund’s three investment managers. These differences are a reflection of the fact that each has a different capitalization focus and investment strategy. The shaded column highlights the characteristics of the Fund as a whole, while the first three columns show portfolio characteristics for the Russell Smallcap, Midcap and Largecap Growth indices. See page 35 for a description of these indices.

|

| |||||||||||||||||||||||||||||

| MARKET CAPITALIZATION SPECTRUM | ||||||||||||||||||||||||||||||

PORTFOLIO CHARACTERISTICS | SMALL | LARGE | ||||||||||||||||||||||||||||

AS OF DECEMBER 31, 2010 |  | |||||||||||||||||||||||||||||

RUSSELL GROWTH: | ||||||||||||||||||

| Smallcap Index | Midcap Index | Largecap Index | M.A. Weatherbie | TCW (Mid-Cap) | TCW (Large-Cap) | Total Fund | ||||||||||||

Number of Holdings | 1269 | 493 | 627 | 60 | 55 | 32 | 131* | |||||||||||

| Weighted Average Market Capitalization (billions) | $1.4 | $8.1 | $83.9 | $2.6 | $6.7 | $60.4 | $22.7 | |||||||||||

| Average Five-Year Earnings Per Share Growth | 10% | 11% | 11% | 9% | 16% | 23% | 16% | |||||||||||

| Dividend Yield | 0.5% | 0.9% | 1.4% | 0.3% | 0.4% | 0.7% | 0.4% | |||||||||||

| Price/Earnings Ratio** | 22x | 22x | 18x | 25x | 28x | 24x | 26x | |||||||||||

| Price/Book Value Ratio | 4.4x | 5.0x | 4.8x | 5.0x | 7.0x | 5.4x | 5.8x | |||||||||||

* Certain holdings are held by more than one manager.

** Excludes negative earnings.

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 7 | |||||

MANAGER ROUNDTABLE (UNAUDITED) |

Investment Manager Roundtable

The Fund’s growth style investment managers look at markets in 2010 and at what they expect in 2011 through the lens of their capitalization focus

Liberty All-Star® Growth Fund’s investment managers bring long experience, deep knowledge, a proven track record and a firm commitment to growth style investing. Once again, therefore, we are grateful to be able to call upon this resource to provide Fund shareholders with commentary and insight. The Fund’s Investment Advisor, ALPS Advisors, serves as moderator of the roundtable. Participating investment management firms, the portfolio manager for each and their respective capitalization ranges are:

M. A. WEATHERBIE & CO., INC.

Portfolio Manager/Matthew A. Weatherbie, CFA

President and Founder

Capitalization Focus/Small-Cap Growth – M.A. Weatherbie practices a small capitalization growth investment style focusing on high quality companies that demonstrate superior earnings growth prospects, yet are reasonably priced relative to their intrinsic value. The firm seeks to provide superior returns relative to small capitalization growth indices over a full market cycle.

TCW INVESTMENT MANAGEMENT COMPANY

Portfolio Manager/Brendt Stallings, CFA

Managing Director

Capitalization Focus/Mid-Cap Growth – TCW seeks capital appreciation through investment in the securities of rapidly growing companies whose business prospects, in TCW’s view, are not properly perceived by consensus research.

TCW Investment Management Company

Portfolio Manager/Craig C. Blum, CFA

Group Managing Director

Capitalization Focus/Large-Cap Growth – TCW seeks large-cap companies that have superior sales growth, leading and/or rising market shares, and high and/or rising profit margins. TCW’s concentrated growth equity strategy seeks companies with distinct advantages in their business model.

Thank you for your participation in this year’s roundtable. To start, a question related to growth style investing: Across the capitalization spectrum—and especially in the small and mid-cap space—growth outperformed value in 2010. Reflecting your own capitalization focus, to what do you attribute this? Do you believe growth is poised to lead again in 2011 and why? Let’s start with Matt Weatherbie and small-cap growth stocks and go up through the capitalization range.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): In small caps over the past decade, there have been two distinct cycles. The first was from March 2000, which was the peak of the dotcom/telecom mania, to June 2007 and it was a period when value trounced growth. Note that this was a seven-plus-year time period. The second cycle began in June 2007; since then growth has outperformed value. In the current subpar economic recovery, we believe growth companies will show stronger relative earnings growth because they control their destiny to a greater extent. Thus, we expect growth to continue to lead in 2011.

Stallings (TCW – Mid-Cap Growth): In 2009, market values rebounded from crisis levels, as it became clear the economy was not falling into a depression. In 2010, with the economy in a slow, grinding recovery, investors turned their attention to finding companies where the underlying growth of the business—even in a slow-growth environment—would support further stock price appreciation, even absent expansion of earnings multiples. This naturally plays to the advantage of growth stocks, as does investors’ increased risk appetite. We are actually surprised that the performance gap between growth and value was not bigger in 2010, and are hopeful that growth will again outperform in 2011.

Blum (TCW – Large-Cap Growth): Market returns in 2009 were heavily driven by multiple expansion, setting up 2010 to be a proving ground for earnings. While earnings were generally more than supportive of the expectations being priced in during the latter part of 2009, the market began to differentiate between companies generating top line growth versus those merely cutting costs. Many growth companies, therefore, saw additional multiple expansion in addition to better-than-expected earnings in 2010. In 2011, we believe the market will continue to reward

companies producing attractive top line growth amid a less-than-robust recovery, leading to continued outperformance of growth stocks. | ‘If you can keep your head when all about you are losing theirs... yours is the Earth and everything that’s in it.’

—Craig Blum (TCW – Large-Cap Growth... with a bow to Rudyard Kipling) |

www.all-starfunds.com | ASG |

| 8 | LIBERTY ALL-STAR® GROWTH FUND | |||||

MANAGER ROUNDTABLE (UNAUDITED) |

Good thoughts, thank you. Again from the perspective of your capitalization focus, please summarize what produced the best results for you in 2010 and what, in retrospect, didn’t play out the way you thought. Let’s reverse the order and ask Craig Blum to start.

Blum (TCW – Large-Cap Growth): Strong secular tailwinds in combination with leverage to a recovering economy in a host of key holdings drove the outperformance of our portfolio in 2010. Our holdings in technology—including Internet names—energy and industrials were particularly strong. Our outperformance was tempered, however, by the defensive growth portion of our portfolio that we continue to hold in light of our structural concerns. Specifically, we note the unusually weak recovery in U.S. employment, even after accounting for historical lags, supports a modest exposure to extremely resilient businesses. Although the caution represented in the construction of the portfolio held back our performance last year, we continue to believe it makes for a more robust portfolio that should outperform in a variety of macro environments.

Stallings (TCW – Mid-Cap Growth): Our best stock-picking in 2010 was in the technology sector. With the economy showing improvement, corporations were more willing to invest back into their businesses. Given that technology is roughly half of capital spending—and it often provides the most immediate return on investment—this environment favored technology revenues. Our biggest winners were companies with leading market shares in areas experiencing rapid secular growth, such as server virtualization and cloud computing. Our poorest performance was in the consumer sector. We underestimated the degree to which retailers would grow revenues in 2010, and as a result were underexposed to the best performing sector of our benchmark.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): We are bottom-up stock pickers, not thematic investors. As a result, 2010’s strong returns were driven by individual security selection. Our biggest winners included top 10 holdings Verifone, Signature Bank, IHS, Monster World-wide and Solera Holdings. They are all in

very different businesses and each is a leader in its field. Our poorest performers included for-profit education stocks Capella and Strayer Education, which encountered unanticipated negative government proposals impacting their future |

‘Dollar cost averaging was one of the first truisms I learned about investing and I continue to believe it is one of the best.’

—Matt Weatherbie (M.A. Weatherbie – Small-Cap Growth) |

enrollment, and tech stock FormFactor, whose revenue recovery following the recession did not materialize as its memory chip customers postponed their transition to new FormFactor products.

What will you be focused on going into 2011, once again, from your own perspective, and what is a stock in the portion of the All-Star portfolio that you manage that reflects your point of view? Let’s stay with Matt Weatherbie.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): In 2011, we will remain focused on investing in companies that we believe can show strong earnings growth even in an economic recovery that remains weak by historic standards. One recent purchase is Under Armour, the technical clothing company, whose growth will be propelled by the expansion of its product line in the U.S. to include footwear as well as continued rapid growth in the European technical clothing market, where the company is rapidly gaining share.

Stallings (TCW – Mid-Cap Growth): Aruba Networks provides enterprise-class wireless local area networks, enabling companies to migrate from existing wired networks to wireless networks. A stronger economy will certainly help Aruba’s revenues, but the company grew revenues even at the depths of the “great recession” owing

to the strength of its products—and the resulting market share—as well as the secular shift to wireless data. | ‘In investing, as in driving, it’s best to not spend too much time peering in the rear-view mirror.’

—Brendt Stallings (TCW – Mid-Cap Growth) |

Blum (TCW – Large-Cap Growth): We continue to be cyclically bullish but structurally have our eyes wide open. As a result, we are maintaining a barbell approach to our portfolio construction. Two-thirds of the portfolio is in more aggressive growth names that have strong secular tailwinds, such as Salesforce.com, while one-third of the portfolio is in more defensive growth names, like American Tower, which enjoys huge competitive barriers, long-term contracts with price escalators and secular tailwinds around wireless data, giving it superior revenue and cash flow visibility.

Lacking confidence, many individual investors have shunned stocks and missed two good years. What’s a piece of advice that you received at some point in your career that you’d pass along to individual investors? This time we’ll ask Brendt Stallings to lead off, followed by Craig Blum and Matt Weatherbie.

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 9 | |||||

MANAGER ROUNDTABLE (UNAUDITED) |

Stallings (TCW – Mid-Cap Growth): In investing, as in driving, it’s best to not spend too much time peering in the rear-view mirror. Even with a good two years, equities have had one of their worst decades ever, just as bonds have had one of their best. With our human propensity to anchor on recent events, it is little wonder investors continue to shun equities in favor of bonds. But performance moves in long cycles, and equities still provide one of the best long-term opportunities for benefiting from the power of compounding—in this case by owning real companies, with real assets and products, and the potential to grow cash flows.

Blum (TCW – Large-Cap Growth): To quote Rudyard Kipling, “If you can keep your head when all about you are losing theirs … yours is the Earth and everything that’s in it.” Markets cycle through pessimism and euphoria but rarely are things as bad as they seem during the dark days nor as good as they seem during the booms. And opportunity rarely comes in nice packaging.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): I have learned that it is important to invest for the long term. Timing investments is always tricky and 2010 was admittedly a good year for smaller cap growth stocks. By dollar cost averaging an investment—investing the same amount periodically so as to buy more shares at lower prices—you can ease into the market in a disciplined way. Dollar cost averaging was one of the first truisms I learned about investing and I continue to believe it is one of the best.

Sound thinking from experienced, knowledgeable investment managers and we thank you all. Let’s hope that a year from now we can look back on a good 2011.

www.all-starfunds.com | ASG |

| 10 | LIBERTY ALL-STAR® GROWTH FUND | |||||

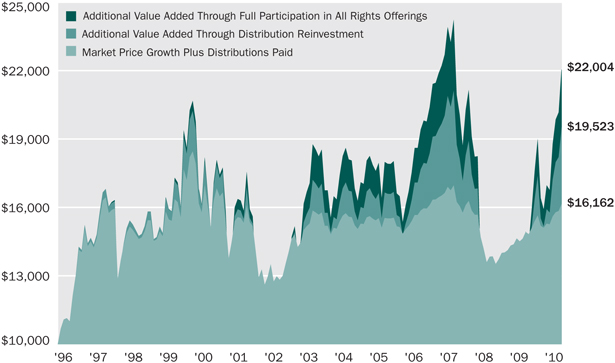

INVESTMENT GROWTH (UNAUDITED) | ||||||

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT | ||

The graph below illustrates the growth of a hypothetical $10,000 investment assuming the purchase of shares of common stock at the closing market price (NYSE: ASG) of $9.25 on December 31, 1996, and tracking its progress through December 31, 2010. For certain information, it also assumes that a shareholder exercised all primary rights in the Fund’s rights offerings (see below). This graph covers the period since the Fund commenced its 10 percent distribution policy in 1997. Effective with the 2009 second quarter distribution, the annual distribution rate was changed from 10 percent to 6 percent. | ||

| ||

| The growth of the investment assuming all distributions were received in cash and not reinvested back into the Fund. The value of the investment under this scenario grew to $16,162 (including the December 31, 2010 value of the original investment of $4,595, plus distributions during the period of $11,567). | |

| The additional value realized through reinvestment of all distributions. The value of the investment under this scenario grew to $19,523. | |

| The additional value realized by exercising all primary rights in the Fund’s rights offerings. The value of the investment under this scenario grew to $22,004 excluding the cost to exercise all primary rights in the rights offerings which was $5,299. | |

Past performance cannot predict future results. Performance will fluctuate with changes in market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal. | ||

ANNUAL REPORT |

LIBERTY ALL-STAR® GROWTH FUND | 11 | |||||

TABLE OF DISTRIBUTIONS AND RIGHTS OFFERINGS (UNAUDITED) |

RIGHTS OFFERINGS | ||||||||||||||||||

YEAR | PER SHARE DISTRIBUTIONS | MONTH COMPLETED | SHARES NEEDED TO PURCHASE | SUBSCRIPTION PRICE | ||||||||||||||

1997 | $1.24 | |||||||||||||||||

1998 | 1.35 | July | 10 | $12.41 | ||||||||||||||

1999 | 1.23 | |||||||||||||||||

2000 | 1.34 | |||||||||||||||||

2001 | 0.92 | September | 8 | 6.64 | ||||||||||||||

2002 | 0.67 | |||||||||||||||||

2003 | 0.58 | September | 8* | 5.72 | ||||||||||||||

2004 | 0.63 | |||||||||||||||||

2005 | 0.58 | |||||||||||||||||

2006 | 0.59 | |||||||||||||||||

2007 | 0.61 | |||||||||||||||||

2008 | 0.47 | |||||||||||||||||

2009** | 0.24 | |||||||||||||||||

2010 | 0.25 | |||||||||||||||||

* The number of shares offered was increased by an additional 25% to cover a portion of the over-subscription requests.

** Effective with the second quarter distribution, the annual distribution rate was changed from 10 percent to 6 percent.

DISTRIBUTION POLICY

Liberty All-Star® Growth Fund, Inc.’s current policy is to pay distributions on its shares totaling approximately 6 percent of its net asset value per year, payable in four quarterly installments of 1.5 percent of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. The fixed distributions are not related to the amount of the Fund’s net investment income or net realized capital gains or losses and may be taxed as ordinary income up to the amount of the Fund’s current and accumulated earnings and profits. If, for any calendar year, the total distributions made under the distribution policy exceed the Fund’s net investment income and net realized capital gains, the excess will generally be treated as a non-taxable return of capital, reducing the shareholder’s adjusted basis in his or her shares. If the Fund’s net investment income and net realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute net realized capital gains and pay income tax thereon to the extent of such excess.

www.all-starfunds.com | ASG |

| 12 | LIBERTY ALL-STAR® GROWTH FUND | |||||

TOP 20 HOLDINGS AND ECONOMIC SECTORS (UNAUDITED) | ||||||

December 31, 2010 |

| TOP 20 HOLDINGS* | PERCENT OF NET ASSETS | |

C.H. Robinson Worldwide, Inc. | 2.39% | |

Salesforce.com, Inc. | 2.13 | |

Apple, Inc. | 2.13 | |

Expeditors International of Washington, Inc. | 1.72 | |

QUALCOMM, Inc. | 1.72 | |

Rockwell Automation, Inc. | 1.70 | |

Core Laboratories N.V. | 1.60 | |

Google, Inc., Class A | 1.59 | |

FMC Technologies, Inc. | 1.47 | |

Oceaneering International, Inc. | 1.46 | |

ACE Ltd. | 1.45 | |

IHS, Inc., Class A | 1.43 | |

Resources Connection, Inc. | 1.42 | |

Rue21, Inc. | 1.41 | |

Intuitive Surgical, Inc. | 1.37 | |

MSCI, Inc., Class A | 1.36 | |

Amazon.com, Inc. | 1.34 | |

VeriFone Systems, Inc. | 1.30 | |

Cognizant Technology Solutions Corp., Class A | 1.23 | |

Varian Medical Systems, Inc. | 1.16 | |

| 31.38% | ||

ECONOMIC SECTORS* | PERCENT OF NET ASSETS | |

Information Technology | 25.21% | |

Industrials | 17.66 | |

Health Care | 15.02 | |

Financials | 12.24 | |

Consumer Discretionary | 11.92 | |

Energy | 9.36 | |

Consumer Staples | 3.23 | |

Materials | 1.55 | |

Telecommunication Services | 1.01 | |

Utilities | 0.61 | |

Other Net Assets | 2.19 | |

| 100.00% | ||

| * | Because the Fund is actively managed, there can be no guarantee that the Fund will continue to hold securities of the indicated issuers and sectors in the future. |

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 13 | |||||

MAJOR STOCK CHANGES IN THE QUARTER (UNAUDITED) | ||||||

December 31, 2010 |

The following are the major ($500,000 or more) stock changes - both purchases and sales - that were made in the Fund’s portfolio during the fourth quarter of 2010.

|

| |||||||

| SECURITY NAME | PURCHASES (SALES) | SHARES AS OF 12/31/10 | ||||||

PURCHASES | ||||||||

athenahealth, Inc. | 22,983 | 22,983 | ||||||

Brigham Exploration Co. | 30,200 | 30,200 | ||||||

E-Commerce China Dangdang, Inc. | 29,673 | 29,673 | ||||||

Gildan Activewear, Inc. | 23,800 | 23,800 | ||||||

Green Dot Corp., Class A | 13,311 | 15,500 | ||||||

Green Mountain Coffee Roasters, Inc. | 28,307 | 28,307 | ||||||

Harman International Industries, Inc. | 20,004 | 20,004 | ||||||

Precision Castparts Corp. | 6,400 | 6,400 | ||||||

QLIK Technologies, Inc. | 31,872 | 31,872 | ||||||

Rue21, Inc. | 19,360 | 66,277 | ||||||

Under Armour, Inc., Class A | 13,050 | 13,050 | ||||||

Youku.com, Inc. | 20,964 | 20,964 | ||||||

SALES | ||||||||

Clean Harbors, Inc. | (8,900) | 0 | ||||||

Contango Oil & Gas Co. | (15,800) | 0 | ||||||

Flowserve Corp. | (8,200) | 0 | ||||||

Martek Biosciences Corp. | (28,579) | 0 | ||||||

Marvell Technology Group Ltd. | (49,600) | 0 | ||||||

Quanta Services, Inc. | (39,000) | 0 | ||||||

Spirit Aerosystems Holdings, Inc., | (35,100) | 0 | ||||||

Venoco, Inc. | (32,411) | 0 | ||||||

www.all-starfunds.com | ASG |

| 14 | LIBERTY ALL-STAR® GROWTH FUND | |||||

SCHEDULE OF INVESTMENTS

| ||||||

as of December 31, 2010 |

| COMMON STOCKS (97.81%) | SHARES | MARKET VALUE | ||||||

u CONSUMER DISCRETIONARY (11.92%) | ||||||||

Automobiles (0.51%) | ||||||||

Thor Industries, Inc. | 20,704 | $ | 703,108 | |||||

Distributors (1.16%) | ||||||||

LKQ Corp.(a) | 70,194 | 1,594,808 | ||||||

Diversified Consumer Services (2.10%) | ||||||||

Capella Education Co.(a) | 17,638 | 1,174,338 | ||||||

Global Education & Technology Group Ltd.(a)(b) | 44,918 | 424,924 | ||||||

Strayer Education, Inc. | 6,500 | 989,430 | ||||||

Xueda Education Group(a)(b) | 26,254 | 295,883 | ||||||

| 2,884,575 | ||||||||

Hotels, Restaurants & Leisure (1.02%) | ||||||||

BJ’s Restaurants, Inc.(a) | 21,050 | 745,801 | ||||||

Ctrip.com International Ltd.(a)(b) | 16,066 | 649,870 | ||||||

| 1,395,671 | ||||||||

Household Durables (0.67%) | ||||||||

Harman International Industries, Inc.(a) | 20,004 | 926,185 | ||||||

Internet & Catalog Retail (2.71%) | ||||||||

Amazon.com, Inc.(a) | 10,240 | 1,843,200 | ||||||

E-Commerce China Dangdang, Inc.(a)(b) | 29,673 | 803,248 | ||||||

priceline. com, Inc.(a) | 2,700 | 1,078,785 | ||||||

| 3,725,233 | ||||||||

Specialty Retail (2.74%) | ||||||||

CarMax, Inc.(a) | 29,600 | 943,648 | ||||||

Monro Muffler Brake, Inc. | 10,635 | 367,847 | ||||||

Rue21, Inc.(a) | 66,277 | 1,942,579 | ||||||

Ulta Salon, Cosmetics & Fragrance, Inc.(a) | 14,884 | 506,056 | ||||||

| 3,760,130 | ||||||||

Textiles, Apparel & Luxury Goods (1.01%) | ||||||||

Gildan Activewear, Inc.(a) | 23,800 | 678,062 | ||||||

Under Armour, Inc., Class A(a) | 13,050 | 715,662 | ||||||

| 1,393,724 | ||||||||

u CONSUMER STAPLES (3.23%) | ||||||||

Food & Staples Retailing (1.36%) | ||||||||

Costco Wholesale Corp. | 12,700 | 917,067 | ||||||

CVS Caremark Corp. | 27,300 | 949,221 | ||||||

| 1,866,288 | ||||||||

Food Products (1.32%) | ||||||||

Green Mountain Coffee Roasters, Inc.(a) | 28,307 | 930,168 | ||||||

Mead Johnson Nutrition Co. | 14,200 | 883,950 | ||||||

| 1,814,118 | ||||||||

Household Products (0.55%) | ||||||||

The Procter & Gamble Co. | 11,870 | 763,597 | ||||||

See Notes to Schedule of Investments and Financial Statements

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 15 | |||||

SCHEDULE OF INVESTMENTS |

as of December 31, 2010

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

u ENERGY (9.36%) | ||||||||

Energy Equipment & Services (6.21%) | ||||||||

Core Laboratories N.V. | 24,646 | $ | 2,194,726 | |||||

Dril-Quip, Inc.(a) | 10,973 | 852,822 | ||||||

FMC Technologies, Inc.(a) | 22,800 | 2,027,148 | ||||||

Oceaneering International, Inc.(a) | 27,200 | 2,002,736 | ||||||

Schlumberger Ltd. | 17,495 | 1,460,832 | ||||||

| 8,538,264 | ||||||||

Oil, Gas & Consumable Fuels (3.15%) | ||||||||

Brigham Exploration Co.(a) | 30,200 | 822,648 | ||||||

Occidental Petroleum Corp. | 15,900 | 1,559,790 | ||||||

Plains Exploration & Production Co.(a) | 37,100 | 1,192,394 | ||||||

Ultra Petroleum Corp.(a) | 15,900 | 759,543 | ||||||

| 4,334,375 | ||||||||

u FINANCIALS (12.24%) | ||||||||

Banks (0.05%) | ||||||||

First Republic Bank(a) | 2,300 | 66,976 | ||||||

Capital Markets (4.65%) | ||||||||

Affiliated Managers Group, Inc.(a) | 14,457 | 1,434,424 | ||||||

The Charles Schwab Corp. | 50,100 | 857,211 | ||||||

Duff & Phelps Corp., Class A | 23,325 | 393,259 | ||||||

FXCM, Inc., Class A(a) | 16,628 | 220,321 | ||||||

Janus Capital Group, Inc. | 77,700 | 1,007,769 | ||||||

LPL Investment Holdings, Inc.(a) | 1,700 | 61,829 | ||||||

optionsXpress Holdings, Inc. | 23,220 | 363,857 | ||||||

SEI Investments Co. | 40,600 | 965,874 | ||||||

T. Rowe Price Group, Inc. | 16,800 | 1,084,272 | ||||||

| 6,388,816 | ||||||||

Commercial Banks (1.11%) | ||||||||

SignatureBank(a) | 30,521 | 1,526,050 | ||||||

Consumer Finance (0.64%) | ||||||||

Green Dot Corp., Class A(a) | 15,500 | 879,470 | ||||||

Diversified Financial Services (2.82%) | ||||||||

IntercontinentalExchange, Inc.(a) | 5,000 | 595,750 | ||||||

MSCI, Inc., Class A(a) | 48,103 | 1,874,093 | ||||||

Portfolio Recovery Associates, Inc.(a) | 18,726 | 1,408,195 | ||||||

| 3,878,038 | ||||||||

Insurance (2.07%) | ||||||||

ACE Ltd. | 32,100 | 1,998,225 | ||||||

Greenlight Capital Re Ltd., Class A(a) | 31,484 | 844,086 | ||||||

| 2,842,311 | ||||||||

Real Estate Management & Development (0.90%) | ||||||||

China Real Estate Information Corp.(a)(b) | 53,969 | 518,103 | ||||||

FirstService Corp.(a) | 24,022 | 727,386 | ||||||

| 1,245,489 | ||||||||

See Notes to Schedule of Investments and Financial Statements

www.all-starfunds.com | ASG |

| 16 | LIBERTY ALL-STAR® GROWTH FUND | |||||

SCHEDULE OF INVESTMENTS

| ||||||

as of December 31, 2010 |

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

u HEALTH CARE (15.02%) | ||||||||

Biotechnology (2.97%) | ||||||||

BioMarin Pharmaceutical, Inc.(a) | 48,522 | $ | 1,306,698 | |||||

Dendreon Corp.(a) | 18,800 | 656,496 | ||||||

Genzyme Corp.(a) | 11,500 | 818,800 | ||||||

Human Genome Sciences, Inc.(a) | 21,088 | 503,792 | ||||||

Ironwood Pharmaceuticals, Inc.(a) | 20,300 | 210,105 | ||||||

Vertex Pharmaceuticals, Inc.(a) | 16,800 | 588,504 | ||||||

| 4,084,395 | ||||||||

Health Care Equipment & Supplies (5.05%) | ||||||||

Accuray, Inc.(a) | 57,082 | 385,304 | ||||||

Intuitive Surgical, Inc.(a) | 7,300 | 1,881,575 | ||||||

Masimo Corp. | 54,992 | 1,598,617 | ||||||

ResMed, Inc.(a) | 21,300 | 737,832 | ||||||

Varian Medical Systems, Inc.(a) | 23,100 | 1,600,368 | ||||||

Volcano Corp.(a) | 27,100 | 740,101 | ||||||

| 6,943,797 | ||||||||

Health Care Providers & Services (1.80%) | ||||||||

IPC The Hospitalist Co., Inc.(a) | 6,483 | 252,902 | ||||||

Lincare Holdings, Inc. | 26,825 | 719,715 | ||||||

PSS World Medical, Inc.(a) | 32,547 | 735,562 | ||||||

VCA Antech, Inc.(a) | 32,967 | 767,801 | ||||||

| 2,475,980 | ||||||||

Health Care Technology (1.74%) | ||||||||

athenahealth, Inc.(a) | 22,983 | 941,844 | ||||||

Cerner Corp.(a) | 15,300 | 1,449,522 | ||||||

| 2,391,366 | ||||||||

Life Sciences Tools & Services (1.06%) | ||||||||

Life Technologies Corp.(a) | 26,100 | 1,448,550 | ||||||

Pharmaceuticals (2.40%) | ||||||||

Allergan, Inc. | 18,300 | 1,256,661 | ||||||

Mylan, Inc.(a) | 39,500 | 834,635 | ||||||

Teva Pharmaceutical Industries Ltd.(b) | 23,210 | 1,209,937 | ||||||

| 3,301,233 | ||||||||

u INDUSTRIALS (17.66%) | ||||||||

Aerospace & Defense (2.41%) | ||||||||

Aerovironment, Inc.(a) | 27,700 | 743,191 | ||||||

HEICO Corp. | 16,155 | 824,389 | ||||||

Precision Castparts Corp. | 6,400 | 890,944 | ||||||

TransDigm Group, Inc.(a) | 11,979 | 862,608 | ||||||

| 3,321,132 | ||||||||

Air Freight & Logistics (4.11%) | ||||||||

C.H. Robinson Worldwide, Inc. | 41,000 | 3,287,790 | ||||||

Expeditors International of Washington, Inc. | 43,300 | 2,364,180 | ||||||

| 5,651,970 | ||||||||

See Notes to Schedule of Investments and Financial Statements | ||||||||

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 17 | |||||

SCHEDULE OF INVESTMENTS

| ||||||

| as of December 31, 2010 |

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

Commercial Services & Supplies (2.17%) | ||||||||

American Reprographics Co.(a) | 67,082 | $ | 509,152 | |||||

Ritchie Bros. Auctioneers, Inc. | 17,140 | 395,077 | ||||||

Stericycle, Inc.(a) | 14,654 | 1,185,802 | ||||||

Waste Connections, Inc. | 32,318 | 889,715 | ||||||

| 2,979,746 | ||||||||

Electrical Equipment (2.20%) | ||||||||

II-VI, Inc.(a) | 14,960 | 693,546 | ||||||

Rockwell Automation, Inc. | 32,500 | 2,330,575 | ||||||

| 3,024,121 | ||||||||

Machinery (0.81%) | ||||||||

Graco, Inc. | 21,287 | 839,772 | ||||||

Watts Water Technologies, Inc., Class A | 7,367 | 269,559 | ||||||

| 1,109,331 | ||||||||

Professional Services (4.97%) | ||||||||

Huron Consulting Group, Inc.(a) | 29,883 | 790,405 | ||||||

ICF International, Inc.(a) | 17,970 | 462,188 | ||||||

IHS, Inc., Class A(a) | 24,537 | 1,972,530 | ||||||

Resources Connection, Inc. | 105,312 | 1,957,750 | ||||||

Robert Half International, Inc. | 33,100 | 1,012,860 | ||||||

Stantec, Inc.(a) | 22,616 | 632,570 | ||||||

| 6,828,303 | ||||||||

Road & Rail (0.99%) | ||||||||

Knight Transportation, Inc. | 27,402 | 520,638 | ||||||

Landstar System, Inc. | 20,507 | 839,556 | ||||||

| 1,360,194 | ||||||||

| u INFORMATION TECHNOLOGY (25.21%) | ||||||||

Communications Equipment (3.76%) | ||||||||

Aruba Networks, Inc.(a) | 31,800 | 663,984 | ||||||

Cisco Systems, Inc.(a) | 59,405 | 1,201,763 | ||||||

Polycom, Inc.(a) | 24,198 | 943,238 | ||||||

QUALCOMM, Inc. | 47,665 | 2,358,941 | ||||||

| 5,167,926 | ||||||||

Computers & Peripherals (2.13%) | ||||||||

Apple, Inc.(a) | 9,060 | 2,922,393 | ||||||

Electronic Equipment & Instruments (0.99%) | ||||||||

FARO Technologies, Inc.(a) | 2,460 | 80,786 | ||||||

FLIR Systems, Inc.(a) | 20,202 | 601,010 | ||||||

National Instruments Corp. | 18,030 | 678,649 | ||||||

| 1,360,445 | ||||||||

See Notes to Schedule of Investments and Financial Statements

www.all-starfunds.com | ASG |

| 18 | LIBERTY ALL-STAR® GROWTH FUND | |||||

SCHEDULE OF INVESTMENTS

| ||||||

as of December 31, 2010 |

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

Internet Software & Services (5.05%) | ||||||||

Akamai Technologies, Inc.(a) | 16,200 | $ | 762,210 | |||||

Baidu, Inc.(a)(b) | 9,100 | 878,423 | ||||||

comScore, Inc.(a) | 16,655 | 371,573 | ||||||

Google, Inc., Class A(a) | 3,675 | 2,182,840 | ||||||

Monster Worldwide, Inc.(a) | 52,488 | 1,240,291 | ||||||

VistaPrint Ltd.(a) | 16,759 | 770,914 | ||||||

Youku.com, Inc.(a)(b) | 20,964 | 733,950 | ||||||

| 6,940,201 | ||||||||

IT Services (4.09%) | ||||||||

Alliance Data Systems Corp.(a) | 13,400 | 951,802 | ||||||

Cognizant Technology Solutions Corp., Class A(a) | 23,100 | 1,692,999 | ||||||

FleetCor Technologies, Inc.(a) | 9,310 | 287,865 | ||||||

VeriFone Systems, Inc.(a) | 46,366 | 1,787,873 | ||||||

Visa, Inc., Class A | 12,915 | 908,958 | ||||||

| 5,629,497 | ||||||||

Semiconductors & Semiconductor Equipment (2.25%) | ||||||||

ARM Holdings Plc(b) | 54,200 | 1,124,650 | ||||||

Cavium Networks, Inc.(a) | 26,388 | 994,300 | ||||||

Hittite Microwave Corp.(a) | 16,024 | 978,105 | ||||||

| 3,097,055 | ||||||||

Software (6.94%) | ||||||||

ANSYS, Inc.(a) | 23,333 | 1,214,949 | ||||||

Concur Technologies, Inc.(a) | 12,992 | 674,675 | ||||||

QLIK Technologies, Inc.(a) | 31,872 | 822,616 | ||||||

RealPage, Inc.(a) | 13,925 | 430,700 | ||||||

Salesforce. com, Inc.(a) | 22,200 | 2,930,400 | ||||||

SMART Technologies, Inc., Class A(a) | 77,200 | 728,768 | ||||||

Solera Holdings, Inc. | 23,763 | 1,219,517 | ||||||

VMware, Inc., Class A(a) | 17,160 | 1,525,696 | ||||||

| 9,547,321 | ||||||||

u MATERIALS (1.55%) | ||||||||

Chemicals (1.55%) | ||||||||

CF Industries Holdings, Inc. | 6,400 | 864,960 | ||||||

Praxair, Inc. | 13,300 | 1,269,751 | ||||||

| 2,134,711 | ||||||||

Mining (0.00%)* | ||||||||

Contango ORE, Inc.(a) | 47 | 494 | ||||||

| u TELECOMMUNICATION SERVICES (1.01%) | ||||||||

Wireless Telecommunication Services (1.01%) | ||||||||

American TowerCorp., Class A(a) | 26,800 | 1,383,952 | ||||||

| u UTILITIES (0.61%) | ||||||||

Electric Utilities (0.61%) | ||||||||

ITC Holdings Corp. | 13,493 | 836,296 | ||||||

| TOTAL COMMON STOCKS | ||||||||

(COST OF $108,124,927) | 134,467,635 | |||||||

See Notes to Schedule of Investments and Financial Statements | ||||||||

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 19 | |||||

SCHEDULE OF INVESTMENTS | ||||||

as of December 31, 2010 |

| SHORT TERM INVESTMENT (2.33%) | PAR VALUE | MARKET VALUE | ||||||

u REPURCHASE AGREEMENT (2.33%) | ||||||||

Repurchase agreement with State Street Bank & Trust Co., dated 12/31/10, due 01/03/11 at 0.010%, collateralized by several Fannie Mae and Freddie Mac instruments with various maturity dates, market value of $3,265,421 (Repurchase proceeds of $3,196,003) (COST OF $3,196,000) | $ | 3,196,000 | $ | 3,196,000 | ||||

TOTAL INVESTMENTS (100.14%) | ||||||||

(COST OF $111,320,927)(c) | 137,663,635 | |||||||

LIABILITIES IN EXCESS OF OTHER ASSETS (-0.14%) | (190,888) | |||||||

NET ASSETS (100.00%) | $ | 137,472,747 | ||||||

NET ASSET VALUE PER SHARE | ||||||||

(30,080,350 SHARES OUTSTANDING) | $ | 4.57 | ||||||

Notes to Schedule of Investments:

| * | Less than 0.005% of net assets. |

| (a) | Non-income producing security. |

| (b) | American Depositary Receipt. |

| (c) | Cost of investments for federal income tax purposes is $111,710,194. |

Gross unrealized appreciation and depreciation at December 31, 2010 based on cost of investments for federal income tax purposes is as follows:

Gross unrealized appreciation | $ | 30,353,004 | ||||||

Gross unrealized depreciation | (4,399,563 | ) | ||||||

Net unrealized appreciation | $ | 25,953,441 | ||||||

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are unaudited.

| See Notes to Financial Statements | ||

www.all-starfunds.com | ASG |

| 20 | LIBERTY ALL-STAR® GROWTH FUND | |||||

STATEMENT OF ASSETS AND LIABILITIES | ||||||

December 31, 2010 |

ASSETS: | ||||

Investments at market value (Cost $111,320,927) | $ | 137,663,635 | ||

Cash | 612 | |||

Receivable for investment securities sold | 2,659,062 | |||

Dividends and interest receivable | 42,316 | |||

Prepaid and other assets | 31 | |||

TOTAL ASSETS | 140,365,656 | |||

LIABILITIES: | ||||

Payable for investments purchased | 564,202 | |||

Distributions payable to shareholders | 2,105,625 | |||

Investment advisory fee payable | 93,437 | |||

Payable for administration, pricing and bookkeeping fees | 29,725 | |||

Accrued expenses | 99,920 | |||

TOTAL LIABILITIES | 2,892,909 | |||

NET ASSETS | $ | 137,472,747 | ||

NET ASSETS REPRESENTED BY: | ||||

Paid-in capital | $ | 113,600,217 | ||

Overdistributed net investment income | (62,208) | |||

Accumulated net realized loss on investments | (2,407,970) | |||

Net unrealized appreciation on investments | 26,342,708 | |||

NET ASSETS | $ | 137,472,747 | ||

Shares of common stock outstanding | ||||

(authorized 60,000,000 shares at $0.10 par) | 30,080,350 | |||

NET ASSET VALUE PER SHARE | $ | 4.57 | ||

See Notes to Financial Statements | ||||

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 21 | |||||

STATEMENT OF OPERATIONS | ||||||

For the Year Ended December 31, 2010 |

INVESTMENT INCOME: | ||||

Dividends (Net of foreign taxes withheld at source which amounted to $8,526) | $ | 1,050,010 | ||

Interest | 271 | |||

TOTAL INVESTMENT INCOME | 1,050,281 | |||

EXPENSES: | ||||

Investment advisory fee | 993,074 | |||

Administration fee | 248,268 | |||

Pricing and bookkeeping fees | 70,995 | |||

Custodian fee | 46,360 | |||

Directors’ fees and expenses | 74,493 | |||

Insurance expense | 8,909 | |||

Legal fees | 138,816 | |||

Proxy solicitation and related legal expenses(a) | 468,113 | |||

NYSE fee | 24,472 | |||

Shareholder communication expenses | 79,633 | |||

Transfer agent fees | 37,608 | |||

Miscellaneous expenses | 35,107 | |||

TOTAL EXPENSES | 2,225,848 | |||

NET INVESTMENT LOSS | (1,175,567) | |||

REALIZED AND UNREALIZED GAIN ON INVESTMENTS: | ||||

Net realized gain on investment transactions | 5,137,175 | |||

Net unrealized appreciation on investments: | ||||

Beginning of year | 5,722,007 | |||

End of year | 26,342,708 | |||

Net change in unrealized appreciation | 20,620,701 | |||

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 25,757,876 | |||

NET INCREASE IN NET ASSETS FROM OPERATIONS | $ | 24,582,309 | ||

| (a) | See Note 8 to Financial Statements |

| See Notes to Financial Statements | ||

www.all-starfunds.com | ASG |

| 22 | LIBERTY ALL-STAR® GROWTH FUND | |||||

STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended December 31, | ||||||||||

| 2010 | 2009 | |||||||||

FROM OPERATIONS: | ||||||||||

Net investment loss | $ | (1,175,567) | $ | (601,322) | ||||||

Net realized gain/(loss) on investment transactions | 5,137,175 | (1,607,219) | ||||||||

Net change in unrealized appreciation/(depreciation) | 20,620,701 | 32,715,240 | ||||||||

Net Increase in Net Assets From Operations | 24,582,309 | 30,506,699 | ||||||||

DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||

From net investment income | (5,615,921) | – | ||||||||

Tax return of capital | (1,904,168) | (7,157,268) | ||||||||

Total Distributions | (7,520,089) | (7,157,268) | ||||||||

CAPITAL SHARE TRANSACTIONS: | ||||||||||

Dividend reinvestments | – | 1,531,661 | ||||||||

Net Increase in net assets from capital share transactions | – | 1,531,661 | ||||||||

Total Increase in Net Assets | 17,062,220 | 24,881,092 | ||||||||

NET ASSETS: | ||||||||||

Beginning of period | 120,410,527 | 95,529,435 | ||||||||

End of period (includes overdistributed net investment income of $(62,208) and $0, respectively) | $ | 137,472,747 | $ | 120,410,527 | ||||||

See Notes to Financial Statements

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 23 | |||||

FINANCIAL HIGHLIGHTS |

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||

PER SHARE OPERATING PERFORMANCE: | ||||||||||||||||||||||||

Net asset value at beginning of year | $ | 4.00 | $ | 3.24 | $ | 6.03 | $ | 5.69 | $ | 5.97 | ||||||||||||||

INCOME FROM INVESTMENT OPERATIONS: | ||||||||||||||||||||||||

Net investment loss(a) | (0.04 | ) | (0.02 | ) | (0.03 | ) | (0.03 | ) | (0.04 | ) | ||||||||||||||

Net realized and unrealized gain/(loss) | 0.86 | 1.02 | (2.29 | ) | 0.98 | 0.35 | ||||||||||||||||||

Total from Investment Operations | 0.82 | 1.00 | (2.32 | ) | 0.95 | 0.31 | ||||||||||||||||||

LESS DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||||||||||

Net investment income | (0.19 | ) | – | – | – | – | ||||||||||||||||||

Net realized gain on investments | – | – | (0.02 | ) | (0.61 | ) | (0.47 | ) | ||||||||||||||||

Tax return of capital | (0.06 | ) | (0.24 | ) | (0.45 | ) | – | (0.12 | ) | |||||||||||||||

Total Distributions | (0.25 | ) | (0.24 | ) | (0.47 | ) | (0.61 | ) | (0.59 | ) | ||||||||||||||

Net asset value at end of year | $ | 4. 57 | $ | 4.00 | $ | 3.24 | $ | 6.03 | $ | 5.69 | ||||||||||||||

Market price at end of year | $ | 4. 25 | $ | 3.36 | $ | 2.60 | $ | 5.96 | $ | 5.37 | ||||||||||||||

TOTAL INVESTMENT RETURN FOR SHAREHOLDERS:(b) | ||||||||||||||||||||||||

Based on net asset value | 21.8 | % | 34.6 | % | (40.0 | %) | 17.9 | % | 6.4 | % | ||||||||||||||

Based on market price | 34.8 | % | 40.8 | % | (51.3 | %) | 23.5 | % | 10.2 | % | ||||||||||||||

RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

Net assets at end of year (millions) | $ | 137 | $ | 120 | $ | 96 | $ | 172 | 157 | |||||||||||||||

Ratio of expenses to average net assets | 1.79 | % | 1.44 | % | 1.46 | % | 1.28 | %(c) | 1.40 | %(c) | ||||||||||||||

Ratio of net investment loss to average net assets | (0.95 | %) | (0.58 | %) | (0.74 | %) | (0.51 | %)(c) | (0.73 | %)(c) | ||||||||||||||

Portfolio turnover rate | 80 | % | 135 | % | 97 | % | 60 | % | 52 | % | ||||||||||||||

| (a) | Calculated using average shares outstanding during the year. |

| (b) | Calculated assuming all distributions are reinvested at actual reinvestment prices. The net asset value and market price returns will differ depending upon the level of any discount from or premium to net asset value at which the Fund’s shares traded during the period. Past performance is not a guarantee of future results. |

| (c) | The benefits derived from custody credits and directed brokerage arrangements, if any, had an impact of less than 0.01%. |

| See Notes to Financial Statements | ||

www.all-starfunds.com | ASG |

| 24 | LIBERTY ALL-STAR® GROWTH FUND | |||||

NOTES TO FINANCIAL STATEMENTS | ||||||

December 31, 2010 |

NOTE 1. ORGANIZATION

Liberty All-Star® Growth Fund, Inc. (the “Fund”) is a Maryland corporation registered under the Investment Company Act of 1940 (the “Act”), as amended, as a diversified, closed-end management investment company.

Investment Goal

The Fund seeks long-term capital appreciation.

Fund Shares

The Fund may issue 60,000,000 shares of common stock at $0.10 par.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

Security Valuation

Equity securities including common stocks and exchange traded funds are valued at the last sale price at the close of the principal exchange on which they trade, except for securities listed on the National Association of Securities Dealers Automated Quotations (“NASDAQ”) exchange, which are valued at the NASDAQ official closing price. Unlisted securities or listed securities for which there were no sales during the day are valued at the closing bid price on such exchanges or over-the-counter markets.

Short-term debt obligations maturing in more than 60 days for which market quotations are readily available are valued at current market value. Short-term debt obligations maturing within 60 days are valued at amortized cost, which approximates market value.

Investments for which market quotations are not readily available are valued at fair value as determined in good faith under consistently applied procedures approved by and under the general supervision of the Fund’s Board of Directors.

Foreign Securities

The Fund invests in foreign securities including American Depositary Receipts, which may involve a number of risk factors and special considerations not present with investments in securities of U.S. corporations.

Security Transactions

Security transactions are recorded on trade date. Cost is determined and gains/(losses) are based upon the specific identification method for both financial statement and federal income tax purposes.

Repurchase Agreements

The Fund may engage in repurchase agreement transactions with institutions that the Fund’s investment advisor has determined are creditworthy. The Fund, through its custodian, receives delivery of underlying securities collateralizing a repurchase agreement. Collateral is at least equal, at all times, to the value of the repurchase obligation including interest. A repurchase agreement transaction involves certain risks in the event of default or insolvency of the counterparty. These risks include possible delays or restrictions upon a Fund’s ability to dispose of the underlying securities and a possible decline in the value of the underlying securities during the period while the Fund seeks to assert its rights.

Income Recognition

Interest income is recorded on the accrual basis. Corporate actions and dividend income are recorded on the ex-date.

New Accounting Pronouncements

In January 2010, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update No. 2010-06, “Improving Disclosures About Fair Value Measurements” (“ASU”). The ASU requires enhanced disclosures about (1) transfers into and out of Levels 1 and 2; and (2) purchases, sales, issuances, and settlements on a gross basis relating to Level 3 measurements. Certain disclosures were effective for the first reporting period (including interim periods) beginning after December 15, 2009, and the second disclosure will be effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years.

Fair Value Measurements

The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 25 | |||||

NOTES TO FINANCIAL STATEMENTS | ||||||

December 31, 2010 |

Level 1 | – | Unadjusted quoted prices in active markets for identical investments | ||

Level 2 | – | Other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) | ||

Level 3 | – | Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) | ||

The following is a summary of the inputs used to value the Fund’s investments as of December 31, 2010:

| Valuation inputs | Investments in Securities at Value* | |||

Level 1 - Unadjusted Quoted Prices Common Stocks | $ | 134,467,635 | ||

Level 2 - Other Significant Observable Inputs Short Term Investment | 3,196,000 | |||

Level 3 - Significant Unobservable Inputs | – | |||

Total | $ | 137,663,635 | ||

*See Schedule of Investments for industry classification.

For the year ended December 31, 2010, the Fund did not have any significant transfers between Level 1 and Level 2 securities. The Fund did not have any securities which used significant unobservable inputs (Level 3) in determining fair value.

Distributions to Shareholders

The Fund currently has a policy of paying distributions on its common shares totaling approximately 6% of its net asset value per year. The distributions are payable in four quarterly distributions of 1.5% of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. Distributions to shareholders are recorded on ex-date.

NOTE 3. FEDERAL TAX INFORMATION

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. Reclassifications are made to the Fund’s capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations. If, for any calendar year, the total distributions made under the distribution policy exceed the Fund’s net investment income and net realized capital gains, the excess will generally be treated as a non-taxable return of capital, reducing the shareholder’s adjusted basis in his or her shares. If the Fund’s net investment income and net

realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute net

realized capital gains and pay income tax thereon to the extent of such excess.

For the year ended December 31, 2010, permanent book and tax basis differences resulting primarily from excess distributions were identified and reclassified among the components of the Fund’s net assets as follows:

Accumulated Net Investment Income | Accumulated Net Realized Gain | Paid-In Capital | ||

$6,729,280 | $41,416 | ($6,770,696) |

Net investment income and net realized gains/(losses), as disclosed on the Statement of Operations, and net assets were not affected by this reclassification.

Included in the amount reclassified was a net operating loss offset to Paid-In Capital of $1,154,775.

Classification of Distributions to Shareholders

Net investment income/(loss) and net realized gain/(loss) may differ for financial statement and tax purposes. The character of distributions made during the year from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain was recorded by the Funds.

The tax character of distributions paid during the years ended December 31, 2010, and December 31, 2009 was as follows:

| 12/31/10 | 12/31/09 | |||||||

Distributions paid from: | ||||||||

Ordinary income | $ | 5,615,921 | $ | – | ||||

Tax return of capital | 1,904,168 | 7,708,298 | ||||||

| $ | 7,520,089 | $ | 7,708,298 | |||||

The following capital loss carryforwards are available to reduce taxable income arising from future net realized gains on investments, if any to the extent permitted by the Internal Revenue Code:

Year of Expiration | Capital Loss Carryforward | |

2017 | $1,769,353 |

The Fund used capital loss carry forwards of $5,615,921 to offset taxable capital gains during the period ended December 31, 2010.

Future realized gains offset by the loss carryforwards are not required to be distributed to shareholders. However, under the Fund’s distribution policy, such gains may be distributed to shareholders in the year the gains are realized. Any such gains distributed may be taxable to shareholders as ordinary income.

www.all-starfunds.com | ASG |

| 26 | LIBERTY ALL-STAR® GROWTH FUND | |||||

NOTES TO FINANCIAL STATEMENTS | ||||||

December 31, 2010 |

As of December 31, 2010, the components of distributable earnings on a tax basis were as follows:

Accumulated Capital Losses | Net Unrealized Appreciation | Other Cumulative Effect of Timing Differences | ||||

($2,080,911) | $ | 25,953,441 | 0 | |||

The differences between book-basis and tax-basis are primarily due to adjustments related to partnerships, passive foreign investment companies, and deferral of losses from wash sales.

Under current tax regulations, capital losses on securities transactions realized after October 31 may be deferred and treated as occurring on the first day of the following fiscal year.

As of December 31, 2010, for federal income tax purposes, the Fund elected to defer post-October losses of $311,558 to December 31, 2011.

Federal Income Tax Status

For federal income tax purposes, the Fund currently qualifies, and intends to remain qualified, as a regulated investment company under the provisions of Subchapter M of the Internal Revenue Code by distributing substantially all of its investment company taxable net income including realized gain, not offset by capital loss carryforwards, if any, to its shareholders. Accordingly, no provision for federal income or excise taxes has been made.

Management has concluded that the Fund has taken no uncertain tax positions that require recognition in the financial statements. The Fund files income tax returns in the U.S. federal jurisdiction and Colorado. For the years ended December 31, 2007, December 31, 2008, December 31, 2009, and December 31, 2010 the Fund’s returns are still open to examination by the appropriate taxing authorities.

NOTE 4. FEES AND COMPENSATION PAID TO AFFILIATES

Investment Advisory Fee

ALPS Advisors, Inc. (“AAI”) serves as the investment advisor to the Fund. AAI receives a monthly investment advisory fee based on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |||||

First $300 million | 0.80% | |||||

Over $300 million | 0.72% |

AAI retains multiple Portfolio Managers to manage the Fund’s investments in various asset classes. AAI pays each Portfolio Manager a portfolio management fee based on the assets of the investment portfolio that they manage. The portfolio management fee is paid from the investment advisory fees collected by AAI and is based

on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |||||

First $300 million | 0.40 | |||||

Over $300 million | 0.36% |

Administration, Bookkeeping and Pricing

Services Agreement

ALPS Fund Services, Inc. (“ALPS”) provides administrative and other services to the Fund for a monthly administration fee based on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |||||

First $300 million | 0.20% | |||||

Over $300 million | 0.18% |

In addition, ALPS provides bookkeeping and pricing services to the Fund for an annual fee consisting of: (i) $38,000 paid monthly plus 0.015% on the average daily net assets for the month; and (ii) a multi-manager fee based on the number of portfolio managers; provided that during any 12-month period, the aggregate amount of (i) shall not exceed $140,000 (exclusive of out-of-pocket expenses and charges). The Fund also reimburses ALPS for out-of-pocket expenses and charges, including fees payable to third parties for pricing the Fund’s portfolio securities and direct internal costs incurred by ALPS in connection with providing fund accounting oversight and monitoring and certain other services.

Fees Paid to Officers

All officers of the Fund, including the Fund’s Chief Compliance Officer, are employees of AAI or its affiliates, and receive no compensation from the Fund. The Board of Directors has appointed a Chief Compliance Officer to the Fund in accordance with federal securities regulations.

NOTE 5. PORTFOLIO INFORMATION

Purchases and Sales of Securities

For the year ended December 31, 2010, the cost of purchases and proceeds from sales of securities, excluding short-term obligations, were $97,180,419 and $106,672,993, respectively.

NOTE 6. CAPITAL TRANSACTIONS

During the year ended December 31, 2009, distributions in the amount of $1,531,661 were paid in newly issued shares valued at market value or net asset value, but not less than 95% of market value. Such distributions resulted in the issuance of 632,213 shares.

Under the Fund’s Automatic Dividend Reinvestment and Direct Purchase Plan (the “Plan”), shareholders automatically participate and have all their Fund dividends

ANNUAL REPORT |

| LIBERTY ALL-STAR® GROWTH FUND | 27 | |||||

NOTES TO FINANCIAL STATEMENTS | ||||||

December 31, 2010 |

and distributions reinvested. Under the Plan, all dividends and distributions will be reinvested in additional shares of the Fund. Distributions declared payable in cash will be reinvested for the accounts of participants in the Plan in additional shares purchased by the Plan Agent on the open market at prevailing market prices, subject to certain limitations as described more fully in the Plan. Distributions declared payable in shares are paid to participants in the Plan entirely in newly issued full and fractional shares valued at the lower of market value or net asset value per share on the valuation date for the distribution (but not at a discount of more than 5 percent from market price). Dividends and distributions are subject to taxation, whether received in cash or in shares.

NOTE 7. INDEMNIFICATION

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also, under the Fund’s organizational documents and by contract, the Directors and Officers of the Fund are indemnified against certain liabilities that may arise out of their duties to the Fund. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be minimal.

NOTE 8. OTHER MATTERS

Maryland Statutes

By resolution of the Board of Directors, the Fund has opted into the Maryland Control Share Acquisition Act and the Maryland Business Combination Act. In general, the Maryland Control Share Acquisition Act provides that “control shares” of a Maryland corporation acquired in a control share acquisition may not be voted except to the extent approved by shareholders at a meeting by a vote of two-thirds of the votes entitled to be cast on the matter (excluding shares owned by the acquiror and by officers or directors who are employees of the corporation). “Control shares” are voting shares of stock which, if aggregated with all other shares of stock owned by the acquiror or in respect of which the acquiror is able to exercise or direct the exercise of voting power (except solely by virtue of a revocable proxy), would entitle the acquiror to exercise voting power in electing directors within certain statutorily defined ranges (one-tenth but less than one-third, one-third but less than a majority, and more than a majority of the voting power). In general, the Maryland Business Combination Act prohibits an interested shareholder (a shareholder that holds 10% or more of the voting power of the outstanding stock of the corporation) of a Maryland corporation from engaging in a business combination (generally defined to include a merger, consolidation, share exchange, sale of a substantial amount of assets, a transfer of the corporation’s securities and similar transactions to or with the interested shareholder or an entity affiliated with the interested shareholder) with

the corporation for a period of five years after the most recent date on which the interested shareholder became an interested shareholder. At the time of adoption, March 19, 2009, the Board and the Fund were not aware, and currently are not aware, of any shareholder that held control shares or that was an interested shareholder under the statutes.

Expense Disclosure

Proxy solicitation and related legal expenses include additional expenses as a result of the proxy solicitation by dissident shareholders.

www.all-starfunds.com | ASG |

| 28 | LIBERTY ALL-STAR® GROWTH FUND | |||||

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

TO THE BOARD OF DIRECTORS AND SHAREHOLDERS OF LIBERTY ALL-STAR®GROWTH FUND, INC.:

We have audited the accompanying statement of assets and liabilities of Liberty All-Star® Growth Fund, Inc. (the “Fund”), including the schedule of investments, as of December 31, 2010, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights of the Fund for the year ended December 31, 2006 were audited by other auditors whose report, dated February 20, 2007, expressed an unqualified opinion on the financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2010, by correspondence with the custodian and brokers where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Liberty All-Star® Growth Fund, Inc., as of December 31, 2010, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

DELOITTE & TOUCHE LLP

Denver, Colorado

February 17, 2011

ANNUAL REPORT |

LIBERTY ALL-STAR® GROWTH FUND | 29 | |||||

AUTOMATIC DIVIDEND REINVESTMENT AND DIRECT PURCHASE PLAN (UNAUDITED) |