UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04537

Liberty All-Star Growth Fund, Inc.

(exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Tane T. Tyler, General Counsel

ALPS Fund Services, Inc.

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: December 31

Date of reporting period: January 1 - December 31, 2011

Item 1. Reports to Stockholders.

A SINGLE INVESTMENT...

A DIVERSIFIED GROWTH PORTFOLIO

A single fund that offers:

| Ÿ | A diversified, multi-managed portfolio of small, mid- and large cap growth stocks |

| Ÿ | Exposure to many of the industries that make the U.S. economy one of the world’s most dynamic |

| Ÿ | Access to institutional quality investment managers |

| Ÿ | Objective and ongoing manager evaluation |

| Ÿ | Active portfolio rebalancing |

| Ÿ | A quarterly fixed distribution policy |

| Ÿ | Actively managed, exchange traded fund listed on the New York Stock Exchange (ticker symbol: ASG) |

LIBERTY ALL-STAR® GROWTH FUND, INC.

The views expressed in the President’s Letter, Unique Fund Attributes and Manager Roundtable reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions, and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for the Fund are based on numerous factors, may not be relied on as an indication of trading intent. References to specific company securities should not be construed as a recommendation or investment advice.

Contents

| LIBERTY ALL-STAR® GROWTH FUND | 1 | |||||

| PRESIDENT’S LETTER (UNAUDITED) | ||||||

| Fellow Shareholders: | February 2012 |

The stock market was essentially unchanged over the span of 12 months in 2011, but that doesn’t mean it was a smooth ride. Quite the contrary, the market fluctuated wildly during a year in which investors seemed to develop a split personality-optimistic one day, fearful the next. In an attempt to explain the volatility, the media even coined the term “risk-on/risk-off,” as if repeated changes in direction could be likened to the flip of a switch.

The greatest volatility came during the second half of the year. The S&P 500® Index moved up or down by 1 percent or more on 22 percent of the trading days during the first half of the year. That rate more than doubled in the second half, rising to 57 percent of trading days, approaching the 69 percent of trading days with similar moves in the first quarter of 2009. That period marked the capitulation phase of the market decline triggered by the most severe financial crisis since the Great Depression.

When the dust finally settled, the S&P 500® Index gained 2.11 percent for the year. The first and fourth quarters of the year were positive, as they returned 5.92 percent and 11.82 percent, respectively. However, the second quarter was flat (+0.10 percent) and the third quarter was very poor, as the index declined 13.87 percent. Among key growth benchmarks, the Russell 3000® Growth Index returned 2.18 percent for the year, while the NASDAQ Composite Index declined 0.51 percent.

Behind the uneven performance of the stock market and its extreme volatility was a mix of factors. On the positive side, corporate earnings were strong, balance sheets continued to recover nicely and managements did a good job of managing costs. The offsets to good corporate performance were an anemic housing and job market. But it was macro concerns on both sides of the Atlantic that created the turmoil as investors lost confidence in governments’ ability to deal with fiscal crises. In the U.S., concerns were driven by the size of the federal

budget deficit and the political infighting that prevented Washington from coming up with any meaningful solution. The federal debt, just $1 trillion in 1981, skyrocketed 15-fold by 2011. It didn’t help when Standard & Poor’s downgraded U.S. debt from AAA to AA+. It was the first-ever downgrade of U.S. debt. Sovereign debt woes plagued the European Union as well. Greece, a relatively small economy, was at the eye of the storm, but the real worry was that debt problems could result in defaults in Italy, Ireland, Spain or Portugal-and could even lead to the demise of the euro. Not even a core euro-zone economy like France was immune to the concerns. Like their counterparts in Washington, Europe’s leaders have proved ineffectual in dealing with the problem.

For the year, Liberty All-Star Growth Fund declined 1.59 percent with shares valued at net asset value (NAV), 1.04 percent with shares valued at NAV with dividends reinvested and 4.38 percent with shares valued at market price (with dividends reinvested). Fund returns were mixed compared to its primary benchmark, the Lipper Multi-Cap Growth Mutual Fund Average, which declined 3.62 percent for the year. Overall, the Fund’s NAV reinvested performance ranked it in the top one-third of the 506 funds in the Lipper Multi-Cap Growth universe. For the trailing three-year period the Fund ranks in the top half of funds in its peer group (45th percentile) and for the trailing five-year period the Fund is in the top one-third (31st percentile).

For most of the year, the discount at which Fund shares traded relative to their underlying NAV narrowed, although it widened in the fourth quarter. For the year, the discount ranged from 2.7 percent to 11.7 percent compared with 6.3 percent to 16.2 percent in 2010. Also, although the Fund’s expense ratio has declined, it was still negatively impacted by higher expenses associated with actions by dissident shareholders.

Fund distributions totaled $0.27 per share in 2011, up from $0.25 in 2010. The Fund’s distribution policy has

www.all-starfunds.com |

ASG |

| 2 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| PRESIDENT’S LETTER (UNAUDITED) | ||||||

been in place since 1997 and is a major component of the Fund’s total return. Since 1997, the Fund has paid distributions totaling $10.97 per share and we would emphasize that shareholders need to include these distributions when determining the return on their investment in the Fund.

Once again, in this annual report we offer a question and answer session with the Fund’s three growth style investment managers. We believe you will find the comments of these leading investors to be both interesting and insightful. As we have also done in recent annual reports, we once again offer a brief summary of the Fund’s attributes on pages 4 and 5. I urge you to revisit these attributes, as they help to make the Fund a unique and attractive vehicle for investment in quality growth stocks.

In closing, 2011 was a challenging year. While Fund performance was in line with relevant benchmarks, we are always hoping for better returns and are constructive about prospects for 2012. For certain, as its top third ranking within the Lipper peer group for the past five years attests, the Fund weathered the volatility of the greatest financial crisis since the Great Depression well. The Fund has continued to demonstrate its worth as a way to own predictable, sustainable quality growth companies of all sizes.

We thank you for your ongoing support of the Fund. Please remain assured that we at Liberty All-Star Growth Fund will continue to monitor markets and our managers closely, and will keep the best long-term interests of shareholders first and foremost in all that we do.

Sincerely,

William R. Parmentier, Jr.

President and Chief Executive Officer

Liberty All-Star Growth Fund, Inc.

|

| LIBERTY ALL-STAR® GROWTH FUND | 3 | |||||

| PRESIDENT’S LETTER (UNAUDITED) | ||||||

FUND STATISTICS AND SHORT-TERM PERFORMANCE PERIODS ENDING DECEMBER 31, 2011 | ||||

| FUND STATISTICS: | ||||

Net Asset Value (NAV) | $4.24 | |||

Market Price | $3.81 | |||

Discount | 10.1% | |||

| Quarter | 2011 | |||||||

Distributions | $0.07 | $0.27 | ||||||

Market Price Trading Range | $3.31 to $4.09 | $3.31 to $4.70 | ||||||

Discount Range | 8.6% to 11.7% | 2. 7% to 11.7% | ||||||

| PERFORMANCE: | ||||||||

Shares Valued at NAV | 9.11% | (1.59%) | ||||||

Shares Valued at NAV with Dividends Reinvested | 9.26% | (1.04%) | ||||||

Shares Valued at Market Price with Dividends Reinvested | 7.72% | (4.38%) | ||||||

NASDAQ Composite Index | 8.53% | (0.51%) | ||||||

Russell 3000® Growth Index | 10.94% | 2.18% | ||||||

S&P 500® Index | 11.82% | 2.11% | ||||||

Lipper Multi-Cap Growth Mutual Fund Average* | 8.91% | (3.62%) | ||||||

NAV Reinvested Percentile Rank (1 = best; 100 = worst) | 57th | 32nd | ||||||

Number of Funds in Category | 541 | 506 | ||||||

LONG-TERM PERFORMANCE SUMMARY AND DISTRIBUTIONS |

ANNUALIZED RATES OF RETURN | |||||||||||||||||

| PERIODS ENDING DECEMBER 31, 2011 | 3 YEARS | 5 YEARS | 10 YEARS | INCEPTION** | ||||||||||||||

| LIBERTY ALL-STAR® GROWTH FUND, INC. | ||||||||||||||||||

Distributions | $0.76 | $1.84 | $4.89 | $6.18 | ||||||||||||||

Shares Valued at NAV | 16.65% | 2.10% | 2.43% | (0.80%) | ||||||||||||||

Shares Valued at NAV with Dividends Reinvested | 17.49% | 2.77% | 2.86% | (0.30%) | ||||||||||||||

Shares Valued at Market Price with Dividends Reinvested | 22.00% | 1.77% | 1.74% | 0.99% | ||||||||||||||

NASDAQ Composite Index | 19.51% | 2.54% | 3.75% | (2.62%) | ||||||||||||||

Russell 3000® Growth Index | 18.09% | 2.46% | 2.74% | (1.86%) | ||||||||||||||

S&P 500® Index | 14.11% | (0.25%) | 2.92% | 0.63% | ||||||||||||||

Lipper Multi-Cap Growth Mutual Fund Average* | 16.84% | 1.27% | 3.25% | (0.93%) | ||||||||||||||

NAV Reinvested Percentile Rank (1 = best; 100 = worst) | 45th | 31st | 62nd | 47th | ||||||||||||||

Number of Funds in Category | 425 | 347 | 236 | 193 | ||||||||||||||

| * | Percentile ranks calculated using the Fund’s NAV Reinvested results within the Lipper Multi-Cap Growth Mutual Fund Universe. |

| ** | Since restructuring to a multi-cap growth fund on May 1, 2000. |

Figures shown for the Fund and the Lipper Multi-Cap Growth Mutual Fund Average are total returns, which include dividends, after deducting Fund expenses. The Fund’s performance is calculated assuming that a shareholder exercised all primary rights in the Fund’s rights offerings. Figures shown for the unmanaged NASDAQ Composite Index, the Russell 3000® Growth Index and the S&P 500® Index are total returns, including dividends. A description of the Lipper benchmark and the market indices can be found on page 35.

Past performance cannot predict future results. Performance will fluctuate with market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of the Fund. Therefore, the Fund cannot predict whether its shares will trade at, below or above net asset value.

www.all-starfunds.com |

ASG |

| 4 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| UNIQUE FUND ATTRIBUTES (UNAUDITED) | ||||||

| Multi-management for Individual Investors

| |||

Large institutional investors have traditionally employed multiple investment managers. With three investment managers investing across the full capitalization range of growth stocks, the Fund brings multi-management to individual investors. | ||||

| Real-time Trading and Liquidity

| |||

The Fund has a fixed number of shares that trade on the New York Stock Exchange and other exchanges. Share pricing is continuous—not just end-of-day, as it is with open-end mutual funds. In addition, Fund shares offer immediate liquidity and there are no annual sales fees. | ||||

|

| LIBERTY ALL-STAR® GROWTH FUND | 5 | |||||

| UNIQUE FUND ATTRIBUTES (UNAUDITED) | ||||||

| Access to Institutional Managers

| |||

The Fund’s investment managers invest primarily for pension funds, endowments, foundations and other institutions. Because institutional managers are closely monitored by their clients, they tend to be more disciplined and consistent in their investment process. | ||||

| Monitoring and Rebalancing

| |||

ALPS Advisors continuously monitors these investment managers to ensure that they are performing as expected and adhering to their style and strategy, and will replace the managers when warranted. Periodic rebalancing maintains the Fund’s structural integrity and is a well-recognized investment discipline. | ||||

| Alignment and Objectivity

| |||

Alignment with shareholders’ best interests and objective decision-making help to ensure that the Fund is managed openly and equitably. In addition, the Fund is governed by a Board of Directors that is elected by and responsible to shareholders. | ||||

| Distribution Policy

| |||

Since 1997, the Fund has followed a policy of paying annual distributions on its shares at a rate that approximates historical equity market returns. The current annual distribution rate is 6 percent of the Fund’s net asset value (paid quarterly at 1.5 percent per quarter), providing a systematic mechanism for distributing funds to shareholders. | ||||

www.all-starfunds.com |

ASG |

| 6 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| INVESTMENT MANAGERS/PORTFOLIO CHARACTERISTICS (UNAUDITED) | ||||||

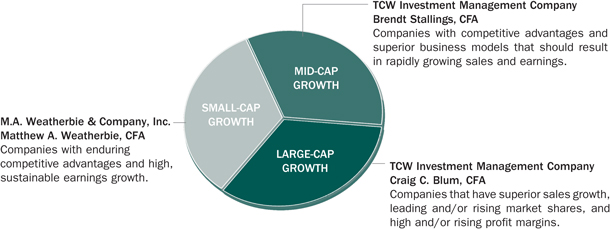

THE FUND’S THREE GROWTH INVESTMENT MANAGERS AND THE MARKET CAPITALIZATION ON WHICH EACH FOCUSES:

MANAGERS’ DIFFERING INVESTMENT STRATEGIES ARE REFLECTED IN PORTFOLIO CHARACTERISTICS

The portfolio characteristics table below is a regular feature of the Fund’s shareholder reports. It serves as a useful tool for understanding the value of the Fund’s multi-managed portfolio. The characteristics are different for each of the Fund’s three investment managers. These differences are a reflection of the fact that each has a different capitalization focus and investment strategy. The shaded column highlights the characteristics of the Fund as a whole, while the first three columns show portfolio characteristics for the Russell Smallcap, Midcap and Largecap Growth indices. See page 35 for a description of these indices.

| RUSSELL GROWTH: | ||||||||||||||

Smallcap Index | Midcap Index | Largecap Index | M .A. Weatherbie | TCW (Mid-Cap) | TCW (Large-Cap) | Total Fund | ||||||||

| Number of Holdings | 1162 | 466 | 588 | 62 | 51 | 31 | 128* | |||||||

| Weighted Average Market Capitalization (billions) | $1.4 | $7.9 | $97.1 | $2.5 | $8.2 | $68.3 | $26.2 | |||||||

| Average Five-Year Earnings Per Share Growth | 15% | 13% | 14% | 14% | 21% | 21% | 19% | |||||||

| Average Five-Year Sales Per Share Growth | 9% | 9% | 11% | 13% | 17% | 17% | 16% | |||||||

| Price/Earnings Ratio** | 19x | 18x | 16x | 23x | 25x | 23x | 23x | |||||||

| Price/Book Value Ratio | 4.0x | 4.5x | 4.9x | 4.8x | 6.0x | 4.9x | 5.2x | |||||||

* Certain holdings are held by more than one manager.

** Excludes negative earnings.

|

| LIBERTY ALL-STAR® GROWTH FUND | 7 | |||||

| MANAGER ROUNDTABLE (UNAUDITED) | ||||||

Investment Manager Roundtable

The Fund’s growth style investment managers summarize their strategy, look back at 2011 and identify stocks that exemplify their investment approach

Liberty All-Star Growth Fund’s investment managers bring long experience, deep knowledge, a proven track record and a firm commitment to growth style investing. Once again, therefore, we are grateful to be able to call upon this resource to provide Fund shareholders with commentary and insight. The Fund’s Investment Advisor, ALPS Advisors, Inc., serves as moderator of the roundtable. Participating investment management firms, the portfolio manager for each and their respective capitalization ranges are:

M. A. WEATHERBIE & CO., INC.

Portfolio Manager/Matthew A. Weatherbie, CFA

President and Founder

Capitalization Focus/Small-Cap Growth – M.A. Weatherbie practices a small capitalization growth investment style focusing on high quality companies that demonstrate superior earnings growth prospects, yet are reasonably priced relative to their intrinsic value. The firm seeks to provide superior returns relative to small capitalization growth indices over a full market cycle.

TCW INVESTMENT MANAGEMENT COMPANY

Portfolio Manager/Brendt Stallings, CFA

Managing Director

Capitalization Focus/Mid-Cap Growth – TCW seeks capital appreciation through investment in the securities of rapidly growing companies whose business prospects, in TCW’s view, are not properly perceived by consensus research.

TCW INVESTMENT MANAGEMENT COMPANY

Portfolio Manager/Craig C. Blum, CFA

Group Managing Director

Capitalization Focus/Large-Cap Growth – TCW seeks large-cap companies that have superior sales growth, leading and/or rising market shares, and high and/or rising profit margins. TCW’s concentrated growth equity strategy seeks companies with distinct advantages in their business model.

With all three managers contributing to the roundtable, it’s a good opportunity for shareholders to compare the various approaches to growth stock investing that each of you represent. Can you summarize your investment style, strategy and process, as well as any factors that are distinct to your firm? Let’s start with Matt Weatherbie and small-cap growth stocks and go up through the capitalization range.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): We invest in high quality smaller cap growth stocks on a bottom-up basis, employing stringent quality criteria. We do pay attention to valuation. We do company-specific research that includes management interviews and preparation of our own models of future earnings and cash flows. One distinct feature of our process is that we invest in what we call Foundation stocks, characterized by consistent growth, as well as Opportunity stocks, which are cyclical or re-emergent growth stocks.

Stallings (TCW – Mid-Cap Growth): Our mid-cap growth strategy is a stock-picking strategy – we seek to earn our performance by assembling a portfolio of 40-60 mid-size companies where we have an out-of-consensus opinion on each company’s three- to five- year free cash flow potential. The only way we can achieve this is by doing our own fundamental research, which we view as a key competitive advantage. For each of our investments, we perform our own primary research, interview management and develop our own proprietary financial forecasts. Wall Street expectations are consulted only as a benchmark. We develop a best, worst and base-case cash flow estimate, using these three estimates to produce best, worst and base-case stock price targets. These targets drive every buy and sell decision in the portfolio. When we assemble the portfolio, we pay close attention to sector diversification. It has been our experience that we can find promising growth companies across most, if not all, major sectors of the economy. We believe that it is possible to achieve our investment objective in the long term by focusing the scope of analysis on companies with businesses that demonstrate strong competitive advantages, clean balance sheets, proven management teams and large market opportunities.

Blum (TCW – Large-Cap Growth): We are a quality-focused, concentrated, large-cap growth manager. In our view, four attributes set the strategy apart from many others. First, our definition of quality is unique in that we focus squarely on large and attractive end markets that face each company and then combine that with research around business model advantage. Second, we own a concentrated portfolio of approximately 25 to 35 stocks, allowing us to focus our efforts strictly on our best ideas.

www.all-starfunds.com |

ASG |

| 8 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| MANAGER ROUNDTABLE (UNAUDITED) | ||||||

Third, we embrace a long-term orientation, which typically translates into a holding period of between three and five years. This enables the strategy to | ||

remain invested in the most attractive opportunities given our belief that the best businesses tend to repeat their successes for long time periods. Finally, we employ what we refer to as |

“The team’s investment process is a proprietary, fundamental, bottom-up approach designed to identify attractive opportunities and then move those names through an exhaustive, fundamental research process.”

Craig Blum (TCW – Large-Cap Growth) | |

a “light macro overlay” that aligns our current portfolio construction with our current macro view. The team’s investment process is a proprietary, fundamental, bottom-up approach designed to identify attractive opportunities and then move those names through an exhaustive, fundamental research process. Our focus is on evaluating and modeling industry dynamics, modeling company-specific fundamentals, conducting competitor analysis, identifying sustainable competitive advantages, meeting with and evaluating management, and performing all related valuation work. | ||

Please summarize what produced the best results for you in 2011 and what, in retrospect, didn’t play out the way you thought. Let’s reverse the order and ask Craig Blum to start.

Blum (TCW – Large-Cap Growth): From a portfolio attribution perspective, our information technology holdings contributed most to our results during the year. Solid fundamental developments continued to support names such as QUALCOMM and Apple, while Visa continued to execute well and post respectable growth following the poor sentiment that developed after the debit-interchange legislation of 2010. Intuitive Surgical, a leader in robotically-assisted minimally invasive surgery, was our single best performing name, with performance driven by procedure growth, profitability and innovation that continued to exceed expectations.

One of our disappointments was mainly isolated to poor sentiment and industry dynamics that continue to pressure C.H. Robinson. Third-party logistics provider C.H. Robinson struggled throughout the year with anemic growth in freight volumes combined with a reduced ability to raise prices. While it was a disappointment for the year, we still believe the company to be meaningfully underpriced longer term and we are maintaining our current exposure.

Stallings (TCW – Mid-Cap Growth): Our investments in the energy and technology sectors were our best performers in 2011. In energy, our focus on energy services firms served us well. With oil prices remaining high and the U.S. in the middle of an energy exploration boom due to the abundance of both shale oil and gas, energy services companies did well. We have a bias towards services companies with relatively differentiated, high-margin offerings. Additionally, the portfolio benefitted from M&A activity in the energy sector, with Brigham Exploration being acquired by StatOil. The technology sector remains very fertile ground for mid-cap growth investors. With the increasing ubiquity and speed of the Internet (especially wireless) and the proliferation of both devices (e.g., iPads) and applications (e.g., Facebook, software-as-a-service models), there is plenty of innovation to invest in. It is somewhat surprising, then, that the technology sector was one of the worst performing sectors within our benchmark. Owing to some good stock picking, especially in semiconductors and software, our investments did relatively well against the benchmark. In the consumer staples sector, Green Mountain helped performance for the year, despite the stock’s decline at year-end. We had a more difficult year in the consumer discretionary sector. Our investments in the for-profit educational industry dragged down performance, and we sold these from the portfolio. Conversely, we did not own enough of the traditional retailers, which hurt our relative performance. Healthcare was a challenge for us as new products launched more slowly than expected at some of our largest biotech companies in the portfolio. In several cases, we have added to these biotech positions.

Weatherbie (M.A. Weatherbie – Small-Cap Growth): Individual stock selection across several different indus-try sectors created our 2011 outperformance versus our benchmark. Notable positive contributors included LKQ Corp., the largest provider of recycled original equipment manufacturer (OEM) auto replacement parts; | ||

Bio-marin Pharmaceutical, a biotech company that develops therapeutic en-zyme-based drugs for rare diseases; and Ulta Salon Cosmetics, a fragrances retailer. Detractors to per-formance included |

“One distinct feature of our process is that we invest in what we call Foundation stocks, characterized by consistent growth, as well as opportunity stocks, which are cyclical or re-emergent growth stocks.”

Matt Weatherbie (M.A. Weatherbie –Small-Cap Growth) | |

Monster Worldwide, an online recruitment company, and Masimo Corporation, a healthcare company focused on blood tests. We continue to own both as we expect earnings growth to pick up while their shares are now undervalued. | ||

|

| LIBERTY ALL-STAR® GROWTH FUND | 9 | |||||

| MANAGER ROUNDTABLE (UNAUDITED)) | ||||||

What is a stock in the portion of the All-Star Growth Fund portfolio that you manage that is a long-term holding that reflects your strategy and process as summarized in the first question? And what is a recent addition to your portion of the portfolio about which you are optimistic, and why? Matt, please start off.

Weatherbie (M.A. Weatherbie – Small-Cap Growth):

Signature Bank (SBNY) is a metropolitan New York-based full-service commercial bank with proven management whose steadily growing private client offices serve the diverse financial needs of privately-owned businesses, their owners and senior managers. SBNY’s sophisticated services and one-stop shopping approach have filled a void created by the mergers of prior competitors into giant banks, whose unspecialized service is anathema to busy entrepreneurs. SBNY is “deposit-rich” and can grow for years, we believe, by prudently growing its loan portfolio.

Liquidity Services (LQDT), a recent purchase, is a leader in providing internet-based auctions that enable retailers, other businesses, and federal and state government agencies to dispose of surplus inventory, capital equipment, office furniture, scrap metal and other unwanted items. Among its many clients, LQDT is a trusted partner of Wal-Mart, Target and the U.S. Department of Defense. It enjoys a first-mover advantage and economies of scale versus its non-web-based competitors. We believe this market has significant longer-term growth potential.

Stallings (TCW – Mid-Cap Growth): A long-term holding that we would mention is F5 Networks. F5 designs and markets IT solutions that enable managers to optimize data center investments. Among other products, the company is a leading provider of application delivery controllers (ADCs). These are utilized to manage and accelerate data traffic into and out of data centers. We believe that the adoption of cloud-based services is in its infancy and that F5 will be a beneficiary of a very long adoption cycle. Consistent with our discipline, we took advantage of the stock’s weakness during the year to add to our position.

An example of recent addition is Arcos Dorados, which is McDonald’s largest franchisee, representing over 5 percent of McDonald’s 2010 sales. The company operates nearly 1,800 restaurants and has a master franchise agreement with McDonald’s covering Latin

America. Arcos Dorados provides us the opportunity to invest in a company experiencing both rapid unit growth and positive same-store sales in a region undergoing above-average economic growth.

Blum (TCW – Large-Cap Growth): Precision Castparts Corp. (PCP) remains a relatively long term holding for the portfolio. PCP manufactures specialized metal components and engineered composite products for the global aerospace, infrastructure and power markets. We | ||

believe a multi year cycle has developed, defined by increasing demand for lighter, stronger, cleaner and more energy efficient materials to be used across a wide variety of industrial end markets. PCP is thus benefiting from rising demand |

“We earn our performance by assembling a portfolio of 40-60 midsize companies where we have an out-of-consensus opinion... the only way we can achieve (our goal) is by doing our own fundamental research, which we view as a key competitive advantage.”

Brendt Stallings (TCW - Mid-Cap Growth) | |

strength-to-weight ratio products that are forged and cast with proprietary materials and technology. In particular, we believe the commercial aerospace market represents a significant long-term opportunity for the company as high-margin composite products continue to increase as a share of total aircraft content. Additionally, the company is nicely leveraged to emerging market infrastructure growth and is a best-of-breed operator with industry leading margins and returns on capital. | ||

A recent addition to the portfolio is VMware. VMware is the dominant provider of server virtualization software and virtualization-based cloud infrastructure solutions. We believe the financial and operational benefits of server virtualization will continue to drive penetration of workloads in the enterprise, with VMware being the primary beneficiary. Increased virtualization penetration is also driving an increased need for management and automation software, another significant opportunity that VMware is well positioned to exploit. The company has also amassed a portfolio of technologies, including desktop virtualization, cloud-based applications and cloud-related development platforms, that is expanding its addressable market. In our opinion, the current valuation does not adequately reflect these growth opportunities.

Great insights from experienced investment managers and we thank you all. It should be an interesting year ahead. We’ll check in again next year.

www.all-starfunds.com |

ASG |

| 10 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| TABLE OF DISTRIBUTIONS AND RIGHTS OFFERINGS (UNAUDITED) | ||||||

| RIGHTS OFFERINGS | ||||||||||||||

| YEAR | PER SHARE DISTRIBUTION | MONTH COMPLETED | SHARES NEEDED TO PURCHASE ONE ADDITIONAL SHARES | SUBSCRIPTION PRICE | ||||||||||

1997 | $1.24 | |||||||||||||

1998 | 1.35 | July | 10 | $12.41 | ||||||||||

1999 | 1.23 | |||||||||||||

2000 | 1.34 | |||||||||||||

2001 | 0.92 | September | 8 | 6.64 | ||||||||||

2002 | 0.67 | |||||||||||||

2003 | 0.58 | September | 8* | 5.72 | ||||||||||

2004 | 0.63 | |||||||||||||

2005 | 0.58 | |||||||||||||

2006 | 0.59 | |||||||||||||

2007 | 0.61 | |||||||||||||

2008 | 0.47 | |||||||||||||

2009** | 0.24 | |||||||||||||

2010 | 0.25 | |||||||||||||

2011 | 0.27 | |||||||||||||

Total | $10.97 | |||||||||||||

| * | The number of shares offered was increased by an additional 25% to cover a portion of the over-subscription requests. |

| ** | Effective with the second quarter distribution, the annual distribution rate was changed from 10 percent to 6 percent. |

DISTRIBUTION POLICY

Liberty All-Star® Growth Fund, Inc.’s current policy is to pay distributions on its shares totaling approximately 6 percent of its net asset value per year, payable in four quarterly installments of 1.5 percent of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. The fixed distributions are not related to the amount of the Fund’s net investment income or net realized capital gains or losses and may be taxed as ordinary income up to the amount of the Fund’s current and accumulated earnings and profits. If, for any calendar year, the total distributions made under the distribution policy exceed the Fund’s net investment income and net realized capital gains, the excess will generally be treated as a non-taxable return of capital, reducing the shareholder’s adjusted basis in his or her shares. If the Fund’s net investment income and net realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute net realized capital gains and pay income tax thereon to the extent of such excess.

|

| LIBERTY ALL-STAR® GROWTH FUND | 11 | |||||

| TOP 20 HOLDINGS AND ECONOMIC SECTORS (UNAUDITED) | ||||||

December 31, 2011 | ||||||

| TOP 20 HOLDINGS* | PERCENT OF NET ASSETS | |||||

Apple, Inc. | 2.34% | |||||

C.H. Robinson Worldwide, Inc. | 2.15 | |||||

FMC Technologies, Inc. | 2.04 | |||||

ACE Ltd. | 2.00 | |||||

IHS, Inc., Class A | 1.92 | |||||

QUALCOMM, Inc. | 1.90 | |||||

Intuitive Surgical, Inc. | 1.86 | |||||

Oceaneering International, Inc. | 1.85 | |||||

Core Laboratories N.V. | 1.78 | |||||

American Tower Corp., Class A | 1.74 | |||||

Salesforce.com, Inc. | 1.72 | |||||

ARM Holdings PLC | 1.69 | |||||

Google, Inc., Class A | 1.60 | |||||

Rockwell Automation, Inc. | 1.53 | |||||

LKQ Corp. | 1.47 | |||||

BioMarin Pharmaceutical, Inc. | 1.45 | |||||

Expeditors International of Washington, Inc. | 1.43 | |||||

VMware, Inc., Class A | 1.42 | |||||

Signature Bank | 1.37 | |||||

Occidental Petroleum Corp. | 1.36 | |||||

| 34.62% | ||||||

| ECONOMIC SECTORS* | PERCENT OF NET ASSETS | |||||

Information Technology | 28.31% | |||||

Industrials | 15.51 | |||||

Health Care | 13.12 | |||||

Consumer Discretionary | 12.27 | |||||

Energy | 10.16 | |||||

Financials | 9.63 | |||||

Materials | 2.97 | |||||

Consumer Staples | 2.63 | |||||

Telecommunication Services | 1.74 | |||||

Utilities | 0.69 | |||||

Other Net Assets | 2.97 | |||||

| 100.00% | ||||||

* Because the Fund is actively managed, there can be no guarantee that the Fund will continue to hold securities of the indicated issuers and sectors in the future. | ||||||

www.all-starfunds.com |

ASG |

| 12 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| MAJOR STOCK CHANGES IN THE QUARTER (UNAUDITED) | ||||||

December 31, 2011 | ||||||

The following are the major ($300,000 or more) stock changes - both purchases and sales - that were made in the Fund’s portfolio during the fourth quarter of 2011.

| 00000000000000 | 00000000000000 | |||

| SECURITY NAME | PURCHASES (SALES) | SHARES AS OF 12/31/11 | ||

| PURCHASES | ||||

Arcos Dorados Holdings, Inc., Class A | 32,300 | 32,300 | ||

Human Genome Sciences, Inc. | 33,500 | 88,888 | ||

Linkedln Corp., Class A | 6,200 | 6,200 | ||

Shutterfly, Inc. | 15,360 | 15,360 | ||

| SALES | ||||

Brigham Exploration Co. | (15,700) | 0 | ||

ICF International, Inc. | (14,139) | 0 | ||

Pharmasset Inc. | (4200) | 0 | ||

SuccessFactors, Inc. | (25,581) | 21,500 | ||

Urban Outfitters, Inc. | (25,100) | 0 | ||

Varian Medical Systems, Inc. | (5,900) | 16,700 | ||

|

| LIBERTY ALL-STAR® GROWTH FUND | 13 | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

| COMMON STOCKS (97.03%) | SHARES | MARKET VALUE | ||||||

u CONSUMER DISCRETIONARY (12.27%) | ||||||||

Auto Components (0.62%) | ||||||||

BorgWarner, lnc.(a) | 12,500 | $ | 796,750 | |||||

|

| |||||||

Automobiles (0.51%) | ||||||||

Thor Industries, Inc. | 23,752 | 651,517 | ||||||

|

| |||||||

Distributors (1.47%) | ||||||||

LKQ Corp.(a) | 62,490 | 1,879,699 | ||||||

|

| |||||||

Hotels, Restaurants & Leisure (1.49%) | ||||||||

Arcos Dorados Holdings, Inc., Class A | 32,300 | 663,119 | ||||||

BJ’s Restaurants, lnc.(a) | 14,588 | 661,128 | ||||||

Ctrip.com International Ltd.(a)(b) | 24,366 | 570,165 | ||||||

|

| |||||||

| 1,894,412 | ||||||||

|

| |||||||

Household Durables (0.20%) | ||||||||

Harman International Industries, Inc. | 6,667 | 253,613 | ||||||

|

| |||||||

Internet & Catalog Retail (2.50%) | ||||||||

Amazon.com, lnc.(a) | 6,465 | 1,119,091 | ||||||

priceline.com, lnc.(a) | 2,575 | 1,204,353 | ||||||

Shutter-fly, lnc.(a) | 15,360 | 349,594 | ||||||

TripAdvisor, lnc.(a) | 20,600 | 519,326 | ||||||

|

| |||||||

| 3,192,364 | ||||||||

|

| |||||||

Specialty Retail (3.77%) | ||||||||

CarMax, lnc.(a) | 32,100 | 978,408 | ||||||

Dick’s Sporting Goods, Inc. | 19,300 | 711,784 | ||||||

Francesca’s Holdings Corp.(a) | 17,803 | 307,992 | ||||||

Monro Muffler Brake, Inc. | 19,431 | 753,728 | ||||||

Rue21, lnc.(a) | 54,490 | 1,176,984 | ||||||

Teavana Holdings, lnc.(a) | 20,756 | 389,798 | ||||||

Ulta Salon, Cosmetics & Fragrance, lnc.(a) | 7,563 | 490,990 | ||||||

|

| |||||||

| 4,809,684 | ||||||||

|

| |||||||

Textiles, Apparel & Luxury Goods (1.71%) | ||||||||

Fossil, lnc.(a) | 10,200 | 809,472 | ||||||

Gildan Activewear, Inc. | 31,100 | 584,369 | ||||||

Michael Kors Holdings Ltd.(a) | 2,000 | 54,500 | ||||||

Under Armour, Inc., Class A(a) | 10,248 | 735,704 | ||||||

|

| |||||||

| 2,184,045 | ||||||||

|

| |||||||

u CONSUMER STAPLES (2.63%) | ||||||||

Food & Staples Retailing (0.91%) | ||||||||

Costco Wholesale Corp. | 11,750 | 979,010 | ||||||

The Fresh Market, lnc.(a) | 4,645 | 185,336 | ||||||

|

| |||||||

| 1,164,346 | ||||||||

|

| |||||||

Food Products (1.72%) | ||||||||

Green Mountain Coffee Roasters, lnc.(a) | 20,600 | 923,910 | ||||||

Mead Johnson Nutrition Co. | 18,500 | 1,271,505 | ||||||

|

| |||||||

| 2,195,415 | ||||||||

|

| |||||||

See Notes to Schedule of Investments and Financial Statements

| ||

www.all-starfunds.com |

ASG |

| 14 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

u ENERGY (10.16%) | ||||||||

Energy Equipment & Services (8.80%) | ||||||||

CARBO Ceramics, Inc. | 6,200 | $ | 764,646 | |||||

Core Laboratories N.V. | 19,909 | 2,268,631 | ||||||

Dril-Quip, lnc. (a) | 9,967 | 656,028 | ||||||

FMC Technologies, lnc. (a) | 49,800 | 2,601,054 | ||||||

Lufkin Industries, Inc. | 16,232 | 1,092,576 | ||||||

Oceaneering International, Inc. | 51,250 | 2,364,162 | ||||||

Schlumberger Ltd. | 21,795 | 1,488,816 | ||||||

|

| |||||||

| 11,235,913 | ||||||||

|

| |||||||

Oil, Gas & Consumable Fuels (1.36%) | ||||||||

Occidental Petroleum Corp. | 18,500 | 1,733,450 | ||||||

|

| |||||||

u FINANCIALS (9.63%) | ||||||||

Capital Markets (3.33%) | ||||||||

Affiliated Managers Group, lnc. (a) | 14,005 | 1,343,780 | ||||||

The Charles Schwab Corp. | 62,900 | 708,254 | ||||||

Financial Engines, lnc. (a) | 9,586 | 214,055 | ||||||

FXCM, Inc., Class A | 37,470 | 365,333 | ||||||

T. Rowe Price Group, Inc. | 16,700 | 951,065 | ||||||

Virtus Investment Partners, lnc. (a) | 8,718 | 662,655 | ||||||

|

| |||||||

| 4,245,142 | ||||||||

|

| |||||||

Commercial Banks (1.37%) | ||||||||

Signature Bank (a) | 29,148 | 1,748,589 | ||||||

|

| |||||||

Consumer Finance (0.58%) | ||||||||

Green Dot Corp., Class A (a) | 23,800 | 743,036 | ||||||

|

| |||||||

Diversified Financial Services (1.15%) | ||||||||

MSCI, Inc., Class A (a) | 21,867 | 720,080 | ||||||

Portfolio Recovery Associates, lnc. (a) | 11,006 | 743,125 | ||||||

|

| |||||||

| 1,463,205 | ||||||||

|

| |||||||

Insurance (2.55%) | ||||||||

ACE Ltd. | 36,400 | 2,552,368 | ||||||

Greenlight Capital Re Ltd., Class A (a) | 29,869 | 706,999 | ||||||

|

| |||||||

| 3,259,367 | ||||||||

|

| |||||||

Real Estate Management & Development (0.65%) | ||||||||

FirstService Corp. (a) | 31,154 | 825,269 | ||||||

|

| |||||||

u HEALTH CARE (13.12%) | ||||||||

Biotechnology (2.97%) | ||||||||

BioMarin Pharmaceutical, lnc. (a) | 53,670 | 1,845,175 | ||||||

Dendreon Corp. (a) | 55,200 | 419,520 | ||||||

Human Genome Sciences, lnc. (a) | 88,888 | 656,882 | ||||||

Ironwood Pharmaceuticals, lnc. (a) | 19,200 | 229,824 | ||||||

Vertex Pharmaceuticals, lnc. (a) | 19,300 | 640,953 | ||||||

|

| |||||||

| 3,792,354 | ||||||||

|

| |||||||

Health Care Equipment & Supplies (3.78%) | ||||||||

Accuray, lnc. (a) | 42,336 | 179,081 | ||||||

Intuitive Surgical, lnc. (a) | 5,125 | 2,372,926 | ||||||

Masimo Corp. (a) | 28,488 | 532,299 | ||||||

Varian Medical Systems, lnc. (a) | 16,700 | 1,121,071 | ||||||

Volcano Corp. (a) | 25,800 | 613,782 | ||||||

|

| |||||||

| 4,819,159 | ||||||||

|

| |||||||

| See Notes to Schedule of Investments and Financial Statements

| ||||

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 15 | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

Health Care Providers & Services (1.55%) | ||||||||

IPC The Hospitalist Co., lnc.(a) | 10,143 | $ | 463,738 | |||||

PSS World Medical, lnc.(a) | 34,151 | 826,112 | ||||||

VCA Antech, lnc.(a) | 34,665 | 684,634 | ||||||

|

| |||||||

| 1,974,484 | ||||||||

|

| |||||||

Health Care Technology (1.94%) | ||||||||

athena health, lnc.(a) | 15,683 | 770,349 | ||||||

Cerner Corp.(a) | 27,800 | 1,702,750 | ||||||

|

| |||||||

| 2,473,099 | ||||||||

|

| |||||||

Life Sciences Tools & Services (0.87%) | ||||||||

Life Technologies Corp.(a) | 28,650 | 1,114,772 | ||||||

|

| |||||||

Pharmaceuticals (2.01%) | ||||||||

Allergan, Inc. | 18,250 | 1,601,255 | ||||||

Mylan, lnc.(a) | 45,100 | 967,846 | ||||||

|

| |||||||

| 2,569,101 | ||||||||

|

| |||||||

u INDUSTRIALS (15.51%) | ||||||||

Aerospace & Defense (2.95%) | ||||||||

Aerovironment, lnc.(a) | 18,020 | 567,089 | ||||||

HEICO Corp. | 16,190 | 946,791 | ||||||

Precision Castparts Corp. | 8,400 | 1,384,236 | ||||||

TransDigm Group, lnc.(a) | 9,098 | 870,497 | ||||||

|

| |||||||

| 3,768,613 | ||||||||

|

| |||||||

Air Freight & Logistics (3.59%) | ||||||||

C.H. Robinson Worldwide, Inc. | 39,400 | 2,749,332 | ||||||

Expeditor International of Washington, Inc. | 44,700 | 1,830,912 | ||||||

|

| |||||||

| 4,580,244 | ||||||||

|

| |||||||

Commercial Services & Supplies (0.92%) | ||||||||

American Reprographics Co.(a) | 47,644 | 218,686 | ||||||

Waste Connections, Inc. | 28,864 | 956,553 | ||||||

|

| |||||||

| 1,175,239 | ||||||||

|

| |||||||

Electrical Equipment (1.96%) | ||||||||

II-VI, lnc.(a) | 29,769 | 546,559 | ||||||

Rockwell Automation, Inc. | 26,650 | 1,955,310 | ||||||

|

| |||||||

| 2,501,869 | ||||||||

|

| |||||||

Machinery (1.07%) | ||||||||

Graco, Inc. | 17,077 | 698,278 | ||||||

Middleby Corp.(a) | 7,072 | 665,051 | ||||||

|

| |||||||

| 1,363,329 | ||||||||

|

| |||||||

Professional Services (4.33%) | ||||||||

Huron Consulting Group, lnc.(a) | 21,472 | 831,825 | ||||||

IMS, Inc., Class A(a) | 28,499 | 2,455,474 | ||||||

Resources Connection, Inc. | 55,983 | 592,860 | ||||||

Robert Half International, Inc. | 37,400 | 1,064,404 | ||||||

Stantec, lnc.(a) | 21,250 | 575,875 | ||||||

|

| |||||||

| 5,520,438 | ||||||||

|

| |||||||

See Notes to Schedule of Investments and Financial Statements | ||

www.all-starfunds.com |

ASG |

| 16 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

Road & Rail (0.69%) | ||||||||

Landstar System, Inc. | 18,482 | $ | 885,658 | |||||

|

| |||||||

u INFORMATION TECHNOLOGY (28.31%) | ||||||||

Communications Equipment (4.23%) | ||||||||

Aruba Networks, lnc.(a) | 37,483 | 694,185 | ||||||

F5 Networks, Inc.(a) | 9,100 | 965,692 | ||||||

InterDigital, Inc. | 13,750 | 599,088 | ||||||

Polycom, lnc.(a) | 44,225 | 720,868 | ||||||

QUALCOMM, Inc. | 44,265 | 2,421,295 | ||||||

|

| |||||||

| 5,401,128 | ||||||||

|

| |||||||

Computers & Peripherals (2.82%) | ||||||||

Apple, lnc.(a) | 7,360 | 2,980,800 | ||||||

Fusion-io, lnc.(a) | 25,702 | 621,988 | ||||||

|

| |||||||

| 3,602,788 | ||||||||

|

| |||||||

Electronic Equipment & Instruments (1.76%) | ||||||||

FARO Technologies, lnc.(a) | 21,488 | 988,448 | ||||||

FLIR Systems, Inc. | 9,102 | 228,187 | ||||||

IPG Photonics Corp.(a) | 5,459 | 184,896 | ||||||

National Instruments Corp. | 24,024 | 623,423 | ||||||

Universal Display Corp.(a) | 5,900 | 216,471 | ||||||

|

| |||||||

| 2,241,425 | ||||||||

|

| |||||||

Internet Software & Services (5.49%) | ||||||||

Baidu, lnc.(a)(b) | 14,725 | 1,715,021 | ||||||

Google, Inc., Class A(a) | 3,160 | 2,041,044 | ||||||

Linkedln Corp., Class A(a) | 6,200 | 390,662 | ||||||

Liquidity Services, lnc.(a) | 27,491 | 1,014,418 | ||||||

Monster Worldwide, lnc.(a) | 59,017 | 468,005 | ||||||

SINA Corp.(a) | 5,400 | 280,800 | ||||||

VistaPrint Ltd.(a) | 19,431 | 594,588 | ||||||

Youku, lnc.(a)(b) | 31,864 | 499,309 | ||||||

|

| |||||||

| 7,003,847 | ||||||||

|

| |||||||

IT Services (3.29%) | ||||||||

Cognizant Technology Solutions Corp., Class A(a) | 19,150 | 1,231,536 | ||||||

FleetCor Technologies, lnc.(a) | 9,265 | 276,746 | ||||||

ServiceSource International, lnc.(a) | 35,930 | 563,742 | ||||||

VeriFone Systems, lnc.(a) | 27,162 | 964,794 | ||||||

Visa, Inc., Class A | 11,415 | 1,158,965 | ||||||

|

| |||||||

| 4,195,783 | ||||||||

|

| |||||||

Semiconductors & Semiconductor Equipment (2.73%) | ||||||||

ARM Holdings PLC(b) | 77,817 | 2,153,196 | ||||||

Cavium, lnc.(a) | 29,388 | 835,501 | ||||||

Hittite Microwave Corp.(a) | 9,932 | 490,442 | ||||||

|

| |||||||

| 3,479,139 | ||||||||

|

| |||||||

Software (7.99%) | ||||||||

ANSYS, lnc.(a) | 17,131 | 981,264 | ||||||

Concur Technologies, lnc.(a) | 15,873 | 806,190 | ||||||

QLIK Technologies, lnc.(a) | 36,577 | 885,163 | ||||||

RealPage, lnc.(a) | 29,925 | 756,205 | ||||||

Salesforce.com, lnc.(a) | 21,650 | 2,196,609 | ||||||

See Notes to Schedule of Investments and Financial Statements | ||||

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 17 | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

| COMMON STOCKS (continued) | SHARES | MARKET VALUE | ||||||

Software (continued) | ||||||||

Solera Holdings, Inc. | 24,143 | $ | 1,075,329 | |||||

SuccessFactors, lnc.(a) | 21,500 | 857,205 | ||||||

Ultimate Software Group, lnc.(a) | 12,713 | 827,871 | ||||||

VMware, Inc., Class A(a) | 21,750 | 1,809,382 | ||||||

|

| |||||||

| 10,195,218 | ||||||||

|

| |||||||

u MATERIALS (2.97%) | ||||||||

Chemicals (1.71%) | ||||||||

CF Industries Holdings, Inc. | 4,700 | 681,406 | ||||||

Praxair, Inc. | 13,975 | 1,493,928 | ||||||

|

| |||||||

| 2,175,334 | ||||||||

|

| |||||||

Metals & Mining (1.26%) | ||||||||

Allegheny Technologies, Inc. | 17,900 | 855,620 | ||||||

Silver Wheaton Corp. | 26,000 | 752,960 | ||||||

|

| |||||||

| 1,608,580 | ||||||||

|

| |||||||

u TELECOMMUNICATION SERVICES (1.74%) | ||||||||

Wireless Telecommunication Services (1.74%) | ||||||||

American Tower Corp., Class A | 36,900 | 2,214,369 | ||||||

|

| |||||||

u UTILITIES (0.69%) | ||||||||

Electric Utilities (0.69%) | ||||||||

ITC Holdings Corp. | 11,636 | 882,940 | ||||||

|

| |||||||

TOTAL COMMON STOCKS | ||||||||

(COST OF $107,089,109) | 123,814,726 | |||||||

|

| |||||||

| SHORT TERM INVESTMENTS (2.93%) | PAR VALUE | |||||||

u REPURCHASE AGREEMENT (2.93%) | ||||||||

Repurchase agreement with State Street Bank & Trust Co., dated 12/30/11, due 01/03/12 at 0.01%, collateralized by several Fannie Mae and Freddie Mac instruments with various maturity dates, market value of $3,825,774 (Repurchase proceeds of $3,743,004) (COST OF $3,743,000) | $ | 3,743,000 | 3,743,000 | |||||

|

| |||||||

TOTAL INVESTMENTS (99.96%) | ||||||||

(COST OF $110,832,109)(C) | 127,557,726 | |||||||

|

| |||||||

OTHER ASSETS IN EXCESS OF LIABILITIES (0.04%) | 44,671 | |||||||

|

| |||||||

NET ASSETS (100.00%) | $ | 127,602,397 | ||||||

|

| |||||||

NET ASSET VALUE PER SHARE | ||||||||

(30,080,350 SHARES OUTSTANDING) | $ | 4.24 | ||||||

|

| |||||||

Notes to Schedule of Investments:

| (a) | Non-income producing security. |

| (b) | American Depositary Receipt. |

| (c) | Cost of investments for federal income tax purposes is $111,121,709. |

See Notes to Financial Statements | ||

www.all-starfunds.com |

ASG |

| 18 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| SCHEDULE OF INVESTMENTS | ||||||

| as of December 31, 2011 | ||||||

Gross unrealized appreciation and depreciation at December 31, 2011 based on cost of investments for federal income tax purposes is as follows:

Gross unrealized appreciation | $ | 26,642,370 | ||

Gross unrealized depreciation | (10,206,353 | ) | ||

Net unrealized appreciation | $ | 16,436,017 | ||

See Notes to Financial Statements | ||||

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 19 | |||||

| STATEMENT OF ASSETS AND LIABILITIES | ||||||

| December 31, 2011 | ||||||

ASSETS: | ||||

Investments at market value (Cost $110,832,109) | $ | 127,557,726 | ||

Cash | 804 | |||

Receivable for investment securities sold | 2,814,870 | |||

Dividends and interest receivable | 40,193 | |||

Prepaid assets | 225 | |||

TOTAL ASSETS | 130,413,818 | |||

LIABILITIES: | ||||

Payable for investments purchased | 471,544 | |||

Distributions payable to shareholders | 2,105,625 | |||

Investment advisory fee payable | 87,871 | |||

Payable for administration, pricing and bookkeeping fees | 28,767 | |||

Accrued expenses | 117,614 | |||

TOTAL LIABILITIES | 2,811,421 | |||

NET ASSETS | $ | 127,602,397 | ||

NET ASSETS REPRESENTED BY: | ||||

Paid-in capital | $ | 111,166,380 | ||

Overdistributed net investment income | (26,710 | ) | ||

Accumulated net realized loss on investments | (262,890 | ) | ||

Net unrealized appreciation on investments | 16,725,617 | |||

NET ASSETS | $ | 127,602,397 | ||

Shares of common stock outstanding | 30,080,350 | |||

NET ASSET VALUE PER SHARE | $ | 4.24 | ||

See Notes to Financial Statements | ||

www.all-starfunds.com |

ASG |

| 20 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| STATEMENT OF OPERATIONS | ||||||

| Year Ended December 31, 2011 | ||||||

INVESTMENT INCOME: | ||||

Dividends (Net of foreign taxes withheld at source which amounted to $7,421) | $ | 659,288 | ||

Interest | 328 | |||

TOTAL INVESTMENT INCOME | 659,616 | |||

EXPENSES: | ||||

Investment advisory fee | 1,095,426 | |||

Administration fee | 273,856 | |||

Pricing and bookkeeping fees | 74,398 | |||

Audit fee | 32,881 | |||

Custodian fee | 48,971 | |||

Directors’ fees and expenses | 68,541 | |||

Insurance expense | 7,927 | |||

Legal fees | 320,936 | |||

NYSE fee | 27,975 | |||

Shareholder communication expenses | 71,088 | |||

Transfer agent fees | 54,828 | |||

Miscellaneous expenses | 5,891 | |||

TOTAL EXPENSES | 2,082,718 | |||

NET INVESTMENT LOSS | (1,423,102 | ) | ||

REALIZED AND UNREALIZED GAIN ON INVESTMENTS: | ||||

Net realized gain on investment transactions | 9,291,538 | |||

Net change in unrealized appreciation/(depreciation) on investments | (9,617,091 | ) | ||

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (325,553 | ) | ||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (1,748,655 | ) | |

See Notes to Financial Statements | ||||

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 21 | |||||

| STATEMENTS OF CHANGES IN NET ASSETS | ||||||

| Year Ended December 31, | ||||||||||

| 2011 | 2010 | |||||||||

FROM OPERATIONS: | ||||||||||

Net investment loss | $ | (1,423,102 | ) | $ | (1,175,567 | ) | ||||

Net realized gain on investment transactions | 9,291,538 | 5,137,175 | ||||||||

Net change in unrealized appreciation/(depreciation) on investments | (9,617,091 | ) | 20,620,701 | |||||||

Net Increase/(Decrease) in Net Assets From Operations | (1,748,655 | ) | 24,582,309 | |||||||

DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||

From net investment income | (1,994,479 | ) | (5,615,921 | ) | ||||||

From net realized gains | (6,127,216 | ) | — | |||||||

Tax return of capital | — | (1,904,168 | ) | |||||||

Total Distributions | (8,121,695 | ) | (7,520,089 | ) | ||||||

Total Increase/(Decrease) in Net Assets | (9,870,350 | ) | 17,062,220 | |||||||

NET ASSETS: | ||||||||||

Beginning of year | 137,472,747 | 120,410,527 | ||||||||

End of year (Includes overdistributed net investment income of $(26,710) and $(62,208), respectively) | $ | 127,602,397 | $ | 137,472,747 | ||||||

See Notes to Financial Statements

www.all-starfunds.com |

ASG |

| 22 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| FINANCIAL HIGHLIGHTS | ||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

|

| |||||||||||||||||||

PER SHARE OPERATING PERFORMANCE: | ||||||||||||||||||||

Net asset value at beginning of year | $ | 4.57 | $ | 4.00 | $ | 3.24 | $ | 6.03 | $ | 5.69 | ||||||||||

|

| |||||||||||||||||||

INCOME FROM INVESTMENT OPERATIONS: | ||||||||||||||||||||

Net investment loss(a) | (0.05 | ) | (0.04 | ) | (0.02 | ) | (0.03 | ) | (0.03 | ) | ||||||||||

Net realized and unrealized gain/loss) on investments | (0.01 | ) | 0.86 | 1.02 | (2.29 | ) | 0.98 | |||||||||||||

|

| |||||||||||||||||||

Total from Investment Operations | (0.06 | ) | 0.82 | 1.00 | (2.32 | ) | 0.95 | |||||||||||||

|

| |||||||||||||||||||

LESS DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||||||

Net investment income | (0.07 | ) | (0.19 | ) | — | — | — | |||||||||||||

Net realized gain on investments | (0.20 | ) | — | — | (0.02 | ) | (0.61 | ) | ||||||||||||

Tax return of capital | — | (0.06 | ) | (0.24 | ) | (0.45 | ) | — | ||||||||||||

|

| |||||||||||||||||||

Total Distributions | (0.27 | ) | (0.25 | ) | (0.24 | ) | (0.47 | ) | (0.61 | ) | ||||||||||

|

| |||||||||||||||||||

Net asset value at end of year | $ | 4.24 | $ | 4.57 | $ | 4.00 | $ | 3.24 | $ | 6.03 | ||||||||||

|

| |||||||||||||||||||

Market price at end of year | $ | 3.81 | $ | 4.25 | $ | 3.36 | $ | 2.60 | $ | 5.96 | ||||||||||

|

| |||||||||||||||||||

TOTAL INVESTMENT RETURN | ||||||||||||||||||||

FOR SHAREHOLDERS:(b) | ||||||||||||||||||||

Based on net asset value | (1.0 | %) | 21.8 | % | 34.6 | % | (40.0 | %) | 17.9 | % | ||||||||||

Based on market price | (4.4 | %) | 34.8 | % | 40.8 | % | (51.3 | %) | 23.5 | % | ||||||||||

RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||

Net assets at end of year (millions) | $ | 128 | $ | 137 | $ | 120 | $ | 96 | $ | 172 | ||||||||||

Ratio of expenses to average net assets | 1.52 | % | 1.79 | % | 1.44 | % | 1.46 | % | 1.28 | %(C) | ||||||||||

Ratio of net investment loss to average net assets | (1.04 | %) | (0.95 | %) | (0.58 | %) | (0.74 | %) | (0.51 | %)(C) | ||||||||||

Portfolio turnover rate | 32 | % | 80 | % | 135 | % | 97 | % | 60 | % | ||||||||||

| (a) | Calculated using average shares outstanding during the period. |

| (b) | Calculated assuming all distributions are reinvested at actual reinvestment prices. The net asset value and market price returns will differ depending upon the level of any discount from or premium to net asset value at which the Fund’s shares traded during the period. Past performance is not a guarantee of future results. |

| (c) | The benefits derived from custody credits and directed brokerage arrangements, if any, had an impact of less that 0.01%. |

See Notes to Financial Statements

|

| LIBERTY ALL-STAR® GROWTH FUND | 23 | |||||

| NOTES TO FINANCIAL STATEMENTS | ||||||

| December 31, 2011 | ||||||

NOTE 1. ORGANIZATION

Liberty All-Star® Growth Fund, Inc. (the “Fund”) is a Maryland corporation registered under the Investment Company Act of 1940 (the “Act”), as amended, as a diversified, closed-end management investment company.

Investment Goal

The Fund seeks long-term capital appreciation.

Fund Shares

The Fund may issue 60,000,000 shares of common stock at $0.10 par.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

Security Valuation

Equity securities including common stocks and exchange traded funds are valued at the last sale price at the close of the principal exchange on which they trade, except for securities listed on the National Association of Securities Dealers Automated Quotations (“NASDAQ”) exchange, which are valued at the NASDAQ official closing price. Unlisted securities or listed securities for which there were no sales during the day are valued at the closing bid price on such exchanges or over-the-counter markets.

Short-term debt obligations maturing in more than 60 days for which market quotations are readily available are valued at current market value. Short-term debt obligations maturing within 60 days are valued at amortized cost, which approximates market value.

Investments for which market quotations are not readily available are valued at fair value as determined in good faith under consistently applied procedures approved by and under the general supervision of the Fund’s Board of Directors.

Foreign Securities

The Fund may directly purchase securities of foreign issuers. Investing in securities of foreign issuers involves special risks not typically associated with investing in securities of U.S. issuers. The risks include possible reevaluation of currencies, the inability to repatriate foreign currency, less complete financial information about companies and possible future adverse political and economic developments. Moreover, securities of many foreign issuers and their markets may be less liquid and their prices more volatile than those of securities of com parable U.S. issuers. For the year ended December 31, 2011, the Fund only held American Depository Receipts and did not hold any securities denominated in foreign currencies.

Security Transactions

Security transactions are recorded on trade date. Cost is determined and gains/flosses) are based upon the specific identification method for both financial statement and federal income tax purposes.

Repurchase Agreements

The Fund engages in repurchase agreement transactions with institutions that the Fund’s investment advisor has determined are creditworthy. The Fund, through its custodian, receives delivery of underlying securities collateralizing a repurchase agreement. Collateral is at least equal, at all times, to the value of the repurchase obligation including interest. A repurchase agreement transaction involves certain risks in the event of default or insolvency of the counterparty. These risks include possible delays or restrictions upon a Fund’s ability to dispose of the underlying securities and a possible decline in the value of the underlying securities during the period while the Fund seeks to assert its rights.

Income Recognition

Interest income is recorded on the accrual basis. Corporate actions and dividend income are recorded on the ex-date.

Recent Accounting Pronouncements

In April 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (ASU) No. 2011-03 “Transfers and Servicing (Topic 860): Reconsideration of Effective Control for Repurchase Agreements.” The ASU 2011-03 is intended to improve financial reporting of repurchase agreements and other agreements that both entitle and obligate a transferor to repurchase or redeem the financial assets before their maturity. The ASU is effective for the first interim or annual period beginning on or after December 15, 2011. Management is currently evaluating the impact this ASU may have on the Fund’s financial statements.

In May 2011, the FASB issued ASU No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements” in U.S. GAAP and International Financial Reporting Standards (“IFRSs”). ASU 2011-04 includes common requirements for measurement of and disclosure about fair value between U.S. GAAP and IFRS. ASU 2011-04 will require reporting entities to disclose quantitative information about the unobservable inputs used in the fair value measurements categorized within Level 3 of the fair value hierarchy. In addition, ASU 2011-04 will require reporting entities to make disclosures about amounts and reasons for all transfers in and out of Level 1 and Level 2 fair value measurements. The new and revised disclosures are effective for interim and annual reporting periods beginning after December 15, 2011. Management is currently evaluating the impact this ASU may have on the Fund’s financial statements.

Fair Value Measurements

The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the

www.all-starfunds.com |

ASG |

| 24 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| NOTES TO FINANCIAL STATEMENTS | ||||||

| December 31, 2011 | ||||||

inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

Level 1 |

| – |

| Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that a Fund has the ability to access at the measurement date; | ||

Level 2 | – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and | ||||

Level 3 | – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. | ||||

The following is a summary of the inputs used to value the Fund’s investments as of December 31, 2011. The Fund recognizes transfers between the levels as of the beginning of the annual period in which the tranfer occurred.

| Valuation inputs | Investments in Securities at Value* | |||

Level 1 - Unadjusted Quoted Prices | $ | 123,814,726 | ||

Level 2 - Other Significant Observable Inputs | 3,743,000 | |||

Level 3 - Significant | – | |||

TOTAL | $ | 127,557,726 | ||

*See Schedule of Investments for industry classification.

For the year ended December 31, 2011, the Fund did not have any significant transfers between Level 1 and Level 2 securities. The Fund did not have any securities which used significant unobservable inputs (Level 3) in determining fair value.

Distributions to Shareholders

The Fund currently has a policy of paying distributions on its common shares totaling approximately 6% of its net asset value per year. The distributions are payable in four quarterly distributions of 1.5% of the Fund’s net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date. Distributions to shareholders are recorded on ex-date.

NOTE 3. FEDERAL TAX INFORMATION

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP. Reclassifications are made to the Fund’s capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations. If, for any calendar year, the total distributions made under the distribution policy exceed the Fund’s net investment income and net realized capital gains, the excess will generally be treated as a non-taxable return of capital, reducing the shareholder’s adjusted basis in his or her shares. If the Fund’s net investment income and net realized capital gains for any year exceed the amount distributed under the distribution policy, the Fund may, in its discretion, retain and not distribute net realized capital gains and pay income tax thereon to the extent of such excess.

For the year ended December 31, 2011, permanent book and tax basis differences resulting primarily from a net operating loss and excess distributions were identified and reclassified among the components of the Fund’s net assets as follows:

| Accumulated Net Investment Income | Accumulated Net Realized Loss | Paid-in Capital | ||

$3,453,079 | ($1,019,242) | ($2,433,837) |

Net investment loss and net realized gain, as disclosed on the Statement of Operations, and net assets were not affected by this reclassification.

Classification of Distributions to Shareholders

Net investment income/loss) and net realized gain/loss) may differ for financial statement and tax purposes. The character of distributions made during the year from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain was recorded by the Funds.

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 25 | |||||

| NOTES TO FINANCIAL STATEMENTS | ||||||

| December 31, 2011 | ||||||

The tax character of distributions paid during the years ended December 31, 2011, and December 31, 2010 was as follows:

| 12/31/11 | 12/31/10 | |||||||

Distributions paid from: | ||||||||

Ordinary income | $ | 1,994,479 | $ | 5,615,921 | ||||

Long-term capital gain | 6,127,216 | — | ||||||

Tax return of capital | — | 1,904,168 | ||||||

| $ | 8,121,695 | $ | 7,520,089 | |||||

The Fund used capital loss carry forwards of $1,800,878 to offset taxable capital gains during the period ended December 31, 2011.

Future realized gains offset by the loss carryforwards are not required to be distributed to shareholders. However, under the Fund’s distribution policy, such gains may be distributed to shareholders in the year the gains are realized. Any such gains distributed may be taxable to shareholders as ordinary income.

Under the Regulated Investment Company Modernization Act of 2010 (“the Modernization Act”), net capital losses recognized in tax years beginning after December 22, 2010 may be carried forward indefinitely, and the character of the losses is retained as short-term and/or long-term. Under the law in effect prior to the Modernization Act, net capital losses were carried forward for eight years and treated as short-term. As a transition rule, the Modernization Act requires that post-enactment net capital losses be used before pre-enactment net capital losses. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term losses rather than being considered all short-term as under previous law.

As of December 31, 2011, the components of distributable earnings on a tax basis were as follows:

Accumulated Capital Gains/Losses | Net Unrealized Appreciation | Undistributed Net Investment Income | ||

$0 | $16,436,017 | $0 |

The differences between book-basis and tax-basis are primarily due to adjustments related to passive foreign investment companies and deferral of losses from wash sales.

Federal Income Tax Status

For federal income tax purposes, the Fund currently qualifies, and intends to remain qualified, as a regulated investment company under the provisions of Subchapter M of the Internal Revenue Code by distributing substantially all of its investment company taxable net income including realized gain, not offset by capital loss carryforwards, if any, to its shareholders. Accordingly, no provision for federal income or excise taxes has been made.

Management has concluded that the Fund has taken no uncertain tax positions that require recognition in the fi-

nancial statements. The Fund files income tax returns in the U.S. federal jurisdiction and Colorado. For the years ended December 31, 2008, December 31, 2009, December 31, 2010, and December 31, 2011 the Fund’s returns are still open to examination by the appropriate taxing authorities.

NOTE 4. FEES AND COMPENSATION PAID TO AFFILIATES

Investment Advisory Fee

ALPS Advisors, Inc. (“AAI”) serves as the investment advisor to the Fund. AAI receives a monthly investment advisory fee based on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |

First $300 million | 0.80% | |

Over $300 million | 0.72% |

AAI retains multiple Portfolio Managers to manage the Fund’s investments in various asset classes. AAI pays each Portfolio Manager a portfolio management fee based on the assets of the investment portfolio that they manage. The portfolio management fee is paid from the investment advisory fees collected by AAI and is based on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |

First $300 million | 0.40% | |

Over $300 million | 0.36% |

Administration, Bookkeeping and Pricing Services Agreement

ALPS Fund Services, Inc. (“ALPS”) provides administrative and other services to the Fund for a monthly administration fee based on the Fund’s average daily net assets at the following annual rates:

Average Daily Net Assets | Annual Fee Rate | |

First $300 million | 0.20% | |

Over $300 million | 0.18% |

In addition, ALPS provides bookkeeping and pricing services to the Fund for an annual fee consisting of: (i) $38,000 paid monthly plus 0.015% on the average daily net assets for the month; and (ii) a multi-manager fee based on the number of portfolio managers; provided that during any 12-month period, the aggregate amount of (i) shall not exceed $140,000 (exclusive of out-of-pocket expenses and charges). The Fund also reimburses ALPS for out-of-pocket expenses and charges, including fees payable to third parties for pricing the Fund’s portfolio securities and direct internal costs incurred by ALPS in connection with providing fund accounting oversight and monitoring and certain other services.

Fees Paid to Officers

All officers of the Fund, including the Fund’s Chief Compliance Officer, are employees of AAI or its affiliates, and receive no compensation from the Fund. The Board of Directors has appointed a Chief Compliance Officer to the Fund in accordance with federal securities regulations.

www.all-starfunds.com |

ASG |

| 26 | LIBERTY ALL-STAR® GROWTH FUND | |||||

| NOTES TO FINANCIAL STATEMENTS | ||||||

| December 31, 2011 | ||||||

NOTE 5. PORTFOLIO INFORMATION

Purchases and Sales of Securities

For the year ended December 31, 2011, the cost of purchases and proceeds from sales of securities, excluding short-term obligations, were $42,567,605 and $52,892,885, respectively.

NOTE 6. INDEMNIFICATION

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims against the Fund. Also, under the Fund’s organizational documents and by contract, the Directors and Officers of the Fund are indemnified against certain liabilities that may arise out of their duties to the Fund. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be minimal.

NOTE 7. OTHER MATTERS

Maryland Statutes

By resolution of the Board of Directors, the Fund has opted into the Maryland Control Share Acquisition Act and the Maryland Business Combination Act. In general, the Maryland Control Share Acquisition Act provides that “control shares” of a Maryland corporation acquired in a control share acquisition may not be voted except to the extent approved by shareholders at a meeting by a vote of two-thirds of the votes entitled to be cast on the matter (excluding shares owned by the acquirer and by officers or directors who are employees of the corporation). “Control shares” are voting shares of stock which, if aggregated with all other shares of stock owned by the acquirer or in respect of which the acquirer is able to exercise or direct the exercise of voting power (except solely by virtue of a revocable proxy), would entitle the acquirer to exercise voting power in electing directors within certain statutorily defined ranges (one-tenth but less than one-third, one-third but less than a majority, and more than a majority of the voting power). In general, the Maryland Business Combination Act prohibits an interested shareholder (a shareholder that holds 10% or more of the voting power of the outstanding stock of the corporation) of a Maryland corporation from engaging in a business combination (generally defined to include a merger, consolidation, share exchange, sale of a substantial amount of assets, a transfer of the corporation’s securities and similar transactions to or with the interested shareholder or an entity affiliated with the interested shareholder) with the corporation for a period of five years after the most recent date on which the interested shareholder became an interested shareholder. At the time of adoption, March 19, 2009, the Board and the Fund were not aware, and currently are not aware, of any shareholder that held control shares or that was an interested shareholder under the statutes.

| | ||||

| LIBERTY ALL-STAR® GROWTH FUND | 27 | |||||

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | ||||||

TO THE BOARD OF DIRECTORS AND SHAREHOLDERS OF LIBERTY ALL-STAR® GROWTH FUND, INC.: