| | | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| | |

| Investment Company Act file number: (811-04616) | |

| |

| Exact name of registrant as specified in charter: | Putnam High Yield Advantage Fund |

| |

| Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | | Beth S. Mazor, Vice President |

| | | One Post Office Square |

| | | Boston, Massachusetts 02109 |

| | | |

| Copy to: | | John W. Gerstmayr, Esq. |

| | | Ropes & Gray LLP |

| | | One International Place |

| | | Boston, Massachusetts 02110 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | | |

| Date of fiscal year end: November 30, 2009 | | |

| |

| Date of reporting period: December 1, 2008 — May 31, 2009 |

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Since 1937, when George Putnam created a prudent mix of stocks and bonds in a single, professionally managed portfolio, we have championed the wisdom of the balanced approach. Today, we offer a world of equity, fixed-income, multi-asset, and absolute-return portfolios so investors can pursue a range of financial goals. Our seasoned portfolio managers seek superior results over time, backed by original, fundamental research on a global scale. We believe in service excellence, in the value of experienced financial advice, and in putting clients first in everything we do.

In 1830, Massachusetts Supreme Judicial Court Justice Samuel Putnam established The Prudent Man Rule, a legal foundation for responsible money management.

THE PRUDENT MAN RULE

All that can be required of a trustee to invest is that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

Putnam

High Yield

Advantage Fund

Semiannual Report

5 | 31 | 09

| | |

| Message from the Trustees | 2 | |

| |

| About the fund | 4 | |

| |

| Performance snapshot | 6 | |

| |

| Interview with your fund’s Portfolio Manager | 7 | |

| |

| Performance in depth | 11 | |

| |

| Expenses | 13 | |

| |

| Portfolio turnover | 15 | |

| |

| Your fund’s management | 16 | |

| |

| Terms and definitions | 17 | |

| |

| Trustee approval of management contract | 18 | |

| |

| Other information for shareholders | 23 | |

| |

| Financial statements | 24 | |

| |

Message from the Trustees

Dear Fellow Shareholder:

Following many months of painful losses, the stock market finally reversed course this spring and posted solid gains. Returns in the fixed-income area have been more mixed, with Treasuries losing ground but corporate and high-yield debt rebounding. We are pleased to report that, in many instances, Putnam mutual fund performance has also been strong in recent months, demonstrating the power of active portfolio management and the substantial efforts of an investment team infused with new talent and a singular focus.

Putnam Investments and the Board of Trustees continue to evolve during this exciting time of renewal. After several years of steady leadership, Charles E. “Ed” Haldeman, Jr. has stepped down as President of the Putnam Funds and as a member of the Board of Trustees of the Funds. Effective July 1, 2009, Robert L. Reynolds, President and Chief Executive Officer of Putnam Investments and a Trustee of the Putnam Funds, replaced Mr. Haldeman as President of the Putnam Funds.

In other developments at Putnam, Walter C. Donovan, a 25-year investment industry veteran, has joined the firm as Chief Investment Officer. Mr. Donovan will oversee a reinvigorated investment organization strengthened by the recent arrival of several industry-leading senior portfolio managers, research analysts, and traders.

Ravi Akhoury has been elected to the Board of Trustees of the Putnam Funds and W. Thomas Stephens has rejoined the Board. From 1992 to 2007, Mr. Akhoury was Chairman and CEO of MacKay Shields, a multi-product investment management

2

firm with more than $40 billion in assets under management. Mr. Stephens retired in December 2008 as Chairman and Chief Executive Officer of Boise Cascade, L.L.C., a paper, forest products, and timberland assets company.

We would like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam.

About the fund

Seeking a high level of current income for investors since 1986

Unlike most types of fixed-income investments, high-yield bond performance is more dependent on the performance of the companies that issue the bonds than on interest rates. For this reason, distinguishing between opportunities and potential pitfalls requires a rigorous investment process that includes analyzing companies. With Putnam High Yield Advantage Fund, this process is highlighted by intensive research, investment diversification, and carefully timed portfolio adjustments.

Because of the risks of high-yield bond investing, in-depth credit research is essential. The fund’s research team — which includes analysts who specialize by industry — visits with the management of issuing companies and analyzes each company’s prospects. The team then compares this information to the bond’s upside or downside potential before deciding whether it is an appropriate investment for the fund.

The fund’s portfolio typically consists of bonds from a broad range of industries and companies. Holdings are diversified across industry sectors and among bonds with differing credit ratings. While the fund invests primarily in the bonds of U.S. companies, its diversified approach allows it to include foreign bonds as well. Among these securities, investments in emerging-market bonds may be used to enhance the fund’s appreciation potential. Although diversification does not ensure a profit or protect against a loss and it is possible to lose money in a diversified portfolio, the fund’s diversification can help reduce the volatility that typically comes with higher-risk investments.

As the bond markets shift over time, the fund’s managers look for ways to capitalize on developments that affect fixed-income securities in general and high-yield bonds in particular. For example, when credit spreads are wide and are expected to tighten, the fund may pursue the higher income potential offered by lower-quality issues. On the other hand, when credit spreads are narrow — that is, when the difference in yield between higher- and lower-rated bonds of comparable maturities is small — the fund may shift its emphasis to higher-quality high-yield bonds.

Lower-rated bonds may offer higher yields in return for more risk. The use of derivatives involves special risks and may result in losses. Mutual funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

What makes a bond

“high yield”?

High-yield bonds are fixed-income investments typically issued by companies that lack an established earnings track record or a solid credit history. In general, high-yield bonds offer higher interest rates than investment-grade bonds to compensate for their increased risk. Because of this added risk, these bonds are typically rated below investment grade by an independent rating agency (for example, the lowest Moody’s Investors Service rating of investment-grade bonds is Baa). The lower the rating, the greater the possibility that a bond’s issuer will be unable to make interest payments or repay the principal.

Bond ratings

| | |

| Moody’s | Grade | |

| |

| Aaa | Investment | |

| |

| Aa, A | Investment | |

| |

| Baa | Investment | |

| |

| Ba, B | High yield | |

| |

| Caa/Ca | High yield | |

| |

| C | High yield | |

| |

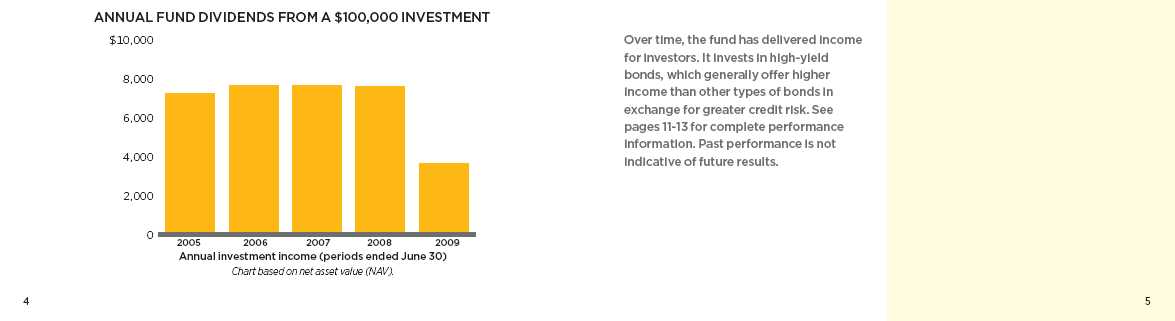

High-yield bonds can offer greater income potential than other types

of bonds.

Performance

snapshot

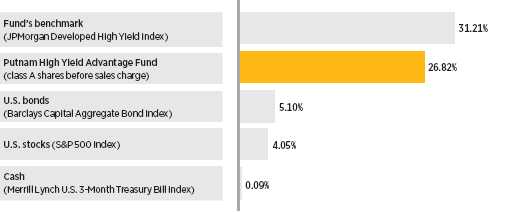

Average annual total return (%) comparison as of 5/31/09

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 7 and 11–13 for additional performance information. For a portion of the periods, this fund may have limited expenses, withoutwhich returns would have been lower. Due to market volatility, current performance may be higher or lower than performance shown. A 1% short-term trading fee may apply. To obtain the most recent month-end performance, visit putnam.com.

* Returns for the six-month period are not annualized, but cumulative.

† The fund’s benchmark, the JPMorgan Developed High Yield Index, was introduced on 12/31/94, which postdates the 3/25/86 date of the fund’s class A shares.

6

Interview with your

fund’s Portfolio Manager

Paul Scanlon

Paul, how did the fund perform during the six months ended May 31, 2009?

The fund benefited from a strong rally in the high-yield market and posted a very strong absolute return of 26.82% during the period. This beat the 24.55% average registered by the fund’s Lipper peer group, High Current Yield Funds, but underperformed its benchmark, the JPMorgan Developed High Yield Index, which rose 31.21%.

What factors helped the high-yield market post such strong returns over the past six months?

It’s important to look back over the last year to help frame 2009’s strong performance. A sharp decline in the high yield market due to the deterioration of the U.S. economy, a downturn in corporate business fundamentals, and very negative market technicals had characterized 2008. In this environment, high-yield spreads rose to a historically wide level of 1,900 basis points in mid-December. This spread widening resulted from massive market dislocations and illiquidity that hampered all asset classes, and arose despite relatively low default rates. From that peak through the end of the period, yield spreads narrowed by about 800 basis points as the trajectory of the economy became clearer and investors reentered the asset class. This spread tightening, which has been the most dramatic move I’ve seen in my career, led to very strong performance for high-yield bonds. The market

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 5/31/09. See page 6 and pages 11–13 for additional fund performance information. Index descriptions can be found on page 17.

7

recovery resulted from more positive investor sentiment amid signs of stabilization in the U.S. economy, with the more economically sensitive and riskier segments of high yield performing best.

Why did the fund underperform its benchmark during the period?

The fund had been defensively positioned over the last 18 months. While this helped relative performance as the market sold off in 2008, the bias toward higher-quality bonds hurt relative performance as the high-yield market rallied dramatically and lower-quality and distressed segments within high yield performed best. From a sector perspective, an underweight to financials, many of which are fallen angels, hurt relative performance. In addition, underweighting housing and services — two economically sensitive areas that outperformed as the market rallied —detracted further. Conversely, overweighting the energy, health-care, cable TV, and wireless telecommunications sectors helped the fund’s relative performance. Finally, our allocation to floating-rate bank loans issued on behalf of high-yield companies also bolstered returns, as loans as an asset class outperformed bonds during the period.

What strategy did you pursue during the six-month period?

We remained overweight in the upper credit-quality tiers of the high-yield market. We are skeptical about lower-rated issues because, like many market participants, we believe that defaults are poised to further increase and feel that recovery values — what an investor can expect to get back in the event of a bankruptcy — are going to test record lows. We also maintained a significant stake in bank loans, which we had purchased at very attractive valuations when they tumbled in 2007 and 2008. At this point in the credit cycle, the loans offered the additional benefit of being higher in a company’s capital structure and by being secured by the assets of the company. Both of these attributes help

Top 10 holdings

This table shows the fund’s top 10 holdings and the percentage of the fund’s net assets that each represented as of 5/31/09. Holdings will vary over time.

| | |

| Coupon (%) and | |

| HOLDING (percentage of fund’s net assets) | maturity date | Sector/industry |

|

| NRG Energy, Inc. (1.0%) | 7 3/8%, 2016 | Utilities and power/Power producers |

| Freeport-McMoRan Copper & | 8 3/8%, 2017 | Basic materials/Metals |

| Gold, Inc. (0.8%) | | |

| HCA, Inc. (0.8%) | 9 1/4%, 2016 | Health care/Health care |

| Intelsat Bermuda, Ltd. (Bermuda) (0.8%) | 11 1/4%, 2016 | Communication services/ |

| | | Telecommunications |

| Energy Future Holdings Corp. (0.6%) | 3 7/8%, 2014 | Utilities and power/Electric utilities |

| Peabody Energy Corp. (0.6%) | 7 3/8%, 2016 | Energy/Coal |

| Arch Western Finance, LLC (0.6%) | 6 3/4%, 2013 | Energy/Coal |

| Qwest Corp. (0.6%) | 8 7/8%, 2012 | Communication services/Regional Bells |

| EchoStar DBS Corp. (0.6%) | 6 3/8%, 2011 | Consumer cyclicals/Broadcasting |

| Chesapeake Energy Corp. (0.6%) | 7 1/2%, 2013 | Energy/Oil and gas |

8

an investor recoup a higher recovery value than high-yield bonds, which are lower in the issuer’s capital structure, in the event of a default. At the sector level, we were overweight in issuers in less economically cyclical sectors, such as energy, health care, cable TV, and wireless. Underweights were held in financials, housing, and services.

Which holdings detracted from performance relative to the benchmark?

We underweighted real estate finance company Residential Capital [ResCap] because of our concerns that the housing market would continue to struggle going forward. However, the company is a subsidiary of General Motors Acceptance Corp. [GMAC], the financing arm of General Motors. During the period, GMAC received a significant capital infusion from the U.S. Treasury, making it much less likely that ResCap would default, and these expectations buoyed results. Our underweight to the bond constrained relative performance, and we sold the holding prior to the end of the period. Another holding that underper-formed was magazine and supermarket tabloid publisher American Media, which encountered problems due to declining advertising and circulation trends. As a result, the firm went through an out-of-court restructuring, causing its bonds to fall in price. However, we believe that the issue still has good relative value, and we continue to hold the bonds.

Which investments contributed to returns?

We believe that the role of the high-yield manager is not only to decide which issues to own, but also to choose which part of the issuer’s capital structure to invest in. For example, cable TV company Charter Communications restructured its debt by converting some of its bonds into equity shares during the period. Our investments in Charter were in a part of its capital structure that benefited performance, as the bonds we held had a greater equity cushion due to restructuring, which

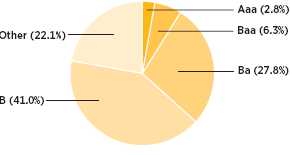

Credit quality overview

Credit qualities shown as a percentage of portfolio value as of 5/31/09. A bond rated Baa or higher (MIG3/VMIG3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds not rated by Moody’s but considered by Putnam Management to be of comparable quality. Ratings will vary over time.

9

caused the price of the issues to rise. An overweight allocation to GMAC also buoyed performance. As I mentioned earlier, at the end of December, GMAC received significant capital from the federal government, a move that made default less likely and caused the issue’s price to rise dramatically.

Paul, what’s your outlook?

I believe the economy will remain weak, but the worst part of the economic contraction is likely behind us and there have been recent signs of slowing in the pace of decline and some stabilization. Despite the plunge in economic activity that began last fall, first-quarter corporate earnings, though still weak, surprised to the upside of greatly diminished expectations. We expect the default rate to rise more, although we believe that we are now closer to the peak in the current default cycle. Although high-yield bond prices have rallied year-to-date, valuations still remain very attractive on a historical basis, especially in the highest-quality tier of the high-yield market. Market technicals — that is, issues of supply and demand — have improved markedly, as new issuance has resumed at the same time that additional funds have been flowing into the asset class.

Against this varied backdrop, we believe the higher-quality tiers of our market offer the most value, particularly as the credit cycle turns and defaults increase. From a sector perspective, we anticipate remaining overweight in groups offering stable businesses and valuable physical assets, including energy, cable TV, health care, wireless telecom, and utilities. At the same time, we’ll look to underweight economically sensitive areas, such as chemicals, financials, housing, forest products, technology, retail, and services.

Thanks for taking the time to speak with us today, Paul.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

IN THE NEWS

Citigroup and General Motors Corp. were removed from the Dow Jones Industrial Average (DJIA) on June 1, 2009. Citigroup was dropped due to its substantial restructuring process, and General Motors because of its bankruptcy, an automatic disqualifier for DJIA membership. Dow Jones & Company, which manages the average, announced that the two companies were replaced by Travelers Companies and Cisco Systems. The DJIA, which consists of 30 stocks, is a widely cited measure of U.S. stock market performance. When the index was introduced 113 years ago, it included just 12 industrial companies. In 1928, it expanded to 30 stocks, and a divisor was introduced to adjust for the effects of stock splits, stock distributions, and stock substitutions. Index components change on a regular basis for varying reasons; the most recent modification occurred in September 2008, when Kraft Foods repla ced American International Group. General Electric is the only stock in the current DJIA that was part of the original index in 1896.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

10

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended May 31, 2009, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represents past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section of putnam.com or call Put nam at 1-800-225-1581. Class Y shares are generally only available to corporate and institutional clients and clients in other approved programs. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 5/31/09

| | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| (inception dates) | (3/25/86) | (5/16/94) | (3/30/07) | (12/1/94) | (3/30/07) | (12/31/98) |

|

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV |

|

| Annual average | | | | | | | | | | |

| (life of fund) | 6.82% | 6.63% | 5.92% | 5.92% | 6.02% | 6.02% | 6.53% | 6.38% | 6.56% | 6.99% |

|

| 10 years | 46.75 | 40.92 | 35.75 | 35.75 | 36.22 | 36.22 | 43.97 | 39.21 | 43.65 | 52.06 |

| Annual average | 3.91 | 3.49 | 3.10 | 3.10 | 3.14 | 3.14 | 3.71 | 3.36 | 3.69 | 4.28 |

|

| 5 years | 22.18 | 17.35 | 17.83 | 16.16 | 17.66 | 17.66 | 20.86 | 16.86 | 21.04 | 23.82 |

| Annual average | 4.09 | 3.25 | 3.34 | 3.04 | 3.31 | 3.31 | 3.86 | 3.17 | 3.89 | 4.37 |

|

| 3 years | 3.08 | –1.04 | 0.92 | –1.51 | 0.85 | 0.85 | 2.40 | –0.89 | 2.67 | 3.85 |

| Annual average | 1.02 | –0.35 | 0.31 | –0.51 | 0.28 | 0.28 | 0.79 | –0.30 | 0.88 | 1.27 |

|

| 1 year | –9.32 | –13.01 | –9.96 | –14.09 | –9.95 | –10.77 | –9.53 | –12.49 | –9.46 | –9.20 |

|

| 6 months | 26.82 | 21.71 | 26.54 | 21.54 | 26.66 | 25.66 | 26.90 | 22.66 | 26.96 | 27.07 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns (public offering price, or POP) for class A and M shares reflect a maximum 4.00% and 3.25% load, respectively. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC for the first year that is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and, except for class Y shares, the higher operating expenses for such shares.

For a portion of the periods, this fund may have limited expenses, without which returns would have been lower.

Due to market volatility, current performance may be higher or lower than performance shown. A 1% short-term trading fee may be applied to shares exchanged or sold within 90 days of purchase.

11

Comparative index returns For periods ended 5/31/09

| | |

| | | Lipper High Current Yield Funds |

| | JPMorgan Developed High Yield Index | category average* |

|

| Annual average (life of fund) | —† | 6.07% |

|

| 10 years | 53.36% | 32.94 |

| Annual average | 4.37 | 2.49 |

|

| 5 years | 18.65 | 11.12 |

| Annual average | 3.48 | 1.81 |

|

| 3 years | 0.88 | –4.27 |

| Annual average | 0.29 | –1.80 |

|

| 1 year | –9.75 | –12.32 |

|

| 6 months | 31.21 | 24.55 |

|

Index and Lipper results should be compared to fund performance at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 5/31/09, there were 475, 460, 389, 335, 205, and 27 funds, respectively, in this Lipper category.

† This index began operations on 12/31/94.

Fund price and distribution information For the six-month period ended 5/31/09

| | | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Number | 6 | 6 | 6 | 6 | 6 | 6 |

|

| Income | $0.230 | $0.215 | $0.217 | $0.224 | $0.226 | $0.236 |

|

| Capital gains | — | — | — | — | — | — |

|

| Total | $0.230 | $0.215 | $0.217 | $0.224 | $0.226 | $0.236 |

|

| Share value | NAV | POP | NAV | NAV | NAV | POP | NAV | NAV |

|

| 11/30/08 | $4.05 | $4.22 | $3.99 | $3.98 | $4.05 | $4.19 | $4.05 | $4.15 |

|

| 5/31/09 | 4.87 | 5.07 | 4.80 | 4.79 | 4.88 | 5.04 | 4.88 | 5.00 |

|

| Current yield (end of period) | NAV | POP | NAV | NAV | NAV | POP | NAV | NAV |

|

| Current dividend rate 1 | 8.62% | 8.28% | 8.00% | 8.02% | 8.36% | 8.10% | 8.36% | 8.64% |

|

| Current 30-day SEC yield 2,3 | | | | | | | | |

| (with expense limitation) | N/A | 8.94 | 8.51 | 8.43 | N/A | 8.81 | 9.05 | 9.55 |

|

| Current 30-day SEC yield 3 | | | | | | | | |

| (without expense limitation) | N/A | 8.92 | 8.48 | 8.40 | N/A | 8.78 | 9.02 | 9.52 |

|

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

1 Most recent distribution, excluding capital gains, annualized and divided by NAV or POP at end of period.

2 For a portion of the period, this fund may have limited expenses, without which yields would have been lower.

3 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

12

Fund performance as of most recent calendar quarter

Total return for periods ended 6/30/09

| | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

| (inception dates) | (3/25/86) | (5/16/94) | (3/30/07) | (12/1/94) | (3/30/07) | (12/31/98) |

|

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV |

|

| Annual average | | | | | | | | | | |

| (life of fund) | 6.94% | 6.75% | 6.03% | 6.03% | 6.13% | 6.13% | 6.64% | 6.49% | 6.67% | 7.10% |

|

| 10 years | 51.18 | 45.12 | 39.63 | 39.63 | 40.15 | 40.15 | 47.99 | 43.24 | 47.61 | 56.51 |

| Annual average | 4.22 | 3.79 | 3.39 | 3.39 | 3.43 | 3.43 | 4.00 | 3.66 | 3.97 | 4.58 |

|

| 5 years | 24.42 | 19.54 | 19.79 | 18.10 | 19.78 | 19.78 | 22.82 | 18.79 | 22.99 | 26.02 |

| Annual average | 4.47 | 3.63 | 3.68 | 3.38 | 3.68 | 3.68 | 4.20 | 3.50 | 4.23 | 4.73 |

|

| 3 years | 5.75 | 1.53 | 3.38 | 0.89 | 3.25 | 3.25 | 4.85 | 1.47 | 5.10 | 6.48 |

| Annual average | 1.88 | 0.51 | 1.11 | 0.30 | 1.07 | 1.07 | 1.59 | 0.49 | 1.67 | 2.11 |

|

| 1 year | –4.39 | –8.23 | –5.19 | –9.52 | –5.16 | –6.03 | –4.82 | –7.86 | –4.76 | –4.23 |

|

| 6 months | 25.35 | 20.44 | 25.09 | 20.09 | 24.90 | 23.90 | 25.18 | 21.11 | 25.24 | 25.62 |

|

Fund’s annual operating expenses For the fiscal year ended 11/30/08

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Net expenses* | 1.11% | 1.86% | 1.86% | 1.36% | 1.36% | 0.86% |

|

| Total annual fund operating expenses | 1.13 | 1.88 | 1.88 | 1.38 | 1.38 | 0.88 |

|

* Reflects Putnam Management’s decision to contractually limit expenses through 11/30/09.

Expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown in the next section and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund limited these expenses; had it not done so, expenses would have been higher. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Review your fund’s expenses

The following table shows the expenses you would have paid on a $1,000 investment in Putnam High Yield Advantage Fund from December 1, 2008, to May 31, 2009. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000* | $6.45 | $10.67 | $10.68 | $7.86 | $7.87 | $5.04 |

|

| Ending value (after expenses) | $1,268.20 | $1,265.40 | $1,266.60 | $1,269.00 | $1,269.60 | $1,270.70 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 5/31/09. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended May 31, 2009, use the following calculation method. To find the value of your investment on December 1, 2008, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000* | $5.74 | $9.50 | $9.50 | $6.99 | $6.99 | $4.48 |

|

| Ending value (after expenses) | $1,019.25 | $1,015.51 | $1,015.51 | $1,018.00 | $1,018.00 | $1,020.49 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 5/31/09. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

14

Compare expenses using industry averages

You can also compare your fund’s expenses with the average of its peer group, as defined by Lipper, an independent fund-rating agency that ranks funds relative to others that Lipper considers to have similar investment styles or objectives. The expense ratio for each share class shown indicates how much of your fund’s average net assets have been used to pay ongoing expenses during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Your fund’s annualized | | | | | | |

| expense ratio | 1.14% | 1.89% | 1.89% | 1.39% | 1.39% | 0.89% |

|

| Average annualized expense | | | | | | |

| ratio for Lipper peer group* | 1.15% | 1.90% | 1.90% | 1.40% | 1.40% | 0.90% |

|

* Putnam keeps fund expenses below the Lipper peer group average expense ratio by limiting our fund expenses if they exceed the Lipper average. The Lipper average is a simple average of front-end load funds in the peer group that excludes 12b-1 fees as well as any expense offset and brokerage/service arrangements that may reduce fund expenses. To facilitate the comparison in this presentation, Putnam has adjusted the Lipper average to reflect 12b-1 fees. Investors should note that the other funds in the peer group may be significantly smaller or larger than the fund, and that an asset-weighted average would likely be lower than the simple average. Also, the fund and Lipper report expense data at different times; the fund’s expense ratio shown here is annualized data for the most recent six-month period, while the quarterly updated Lipper average is based on the most recent fiscal year-end data available for the peer group funds as of 3/31/09.

Your fund’s portfolio turnover

Putnam funds are actively managed by experts who buy and sell securities based on intensive analysis of companies, industries, economies, and markets. Portfolio turnover is a measure of how often a fund’s managers buy and sell securities for your fund. A portfolio turnover of 100%, for example, means that the managers sold and replaced securities valued at 100% of a fund’s average portfolio value within a given period. Funds with high turnover may be more likely to generate capital gains that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance.

Funds that invest in bonds or other fixed-income instruments may have higher turnover than funds that invest only in stocks. Short-term bond funds tend to have higher turnover than longer-term bond funds, because shorter-term bonds will mature or be sold more frequently than longer-term bonds. You can use the following table to compare your fund’s turnover with the average turnover for funds in its Lipper category.

Turnover comparisons Percentage of holdings that change every year

| | | | | |

| | 2008 | 2007 | 2006 | 2005 | 2004 |

|

| Putnam High Yield Advantage Fund | 34% | 48% | 46% | 33% | 53% |

|

| Lipper High Current Yield Fund | | | | | |

| category average | 81% | 83% | 83% | 73% | 95% |

|

Turnover data for the fund is calculated based on the fund's fiscal-year period, which ends on November 30. Turnover data for the fund's Lipper category is calculated based on the average of the turnover of each fund in the category for its fiscal year ended during the indicated year. Fiscal years vary across funds in the Lipper category, which may limit the comparability of the fund's portfolio turnover rate to the Lipper average. Comparative data for 2008 is based on information available as of 12/31/08.

15

Your fund’s management

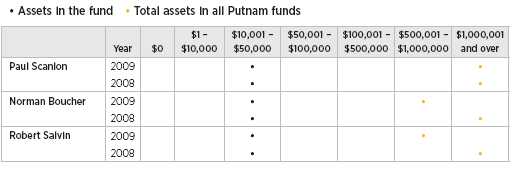

In addition to Paul Scanlon, your fund’s Portfolio Managers are Norman Boucher and Robert Salvin.

Portfolio management fund ownership

The following table shows how much the fund’s current Portfolio Managers have invested in the fund and in all Putnam mutual funds (in dollar ranges). Information shown is as of May 31, 2009, and May 31, 2008.

Trustee and Putnam employee fund ownership

As of May 31, 2009, all of the Trustees of the Putnam funds owned fund shares. The following table shows the approximate value of investments in the fund and all Putnam funds as of that date by the Trustees and Putnam employees. These amounts include investments by the Trustees’ and employees’ immediate family members and investments through retirement and deferred compensation plans.

| | |

| | Assets in the fund | Total assets in all Putnam funds |

|

| Trustees | $216,000 | $36,000,000 |

|

| Putnam employees | $2,594,000 | $357,000,000 |

|

Other Putnam funds managed by the Portfolio Managers

Paul Scanlon is also a Portfolio Manager of Putnam Absolute Return 100 Fund, Putnam Absolute Return 300 Fund, Putnam Diversified Income Trust, Putnam Floating Rate Income Fund, Putnam High Yield Trust, Putnam Master Intermediate Income Trust, and Putnam Premier Income Trust.

Norman Boucher is also a Portfolio Manager of Putnam Floating Rate Income Fund and Putnam High Yield Trust.

Robert Salvin is also a Portfolio Manager of Putnam Convertible Income-Growth Trust, Putnam Floating Rate Income Fund, Putnam High Income Securities Fund, and Putnam High Yield Trust.

Paul Scanlon, Norman Boucher, and Robert Salvin may also manage other accounts and variable trust funds advised by Putnam Management or an affiliate.

16

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Barclays Capital Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

JPMorgan Developed High Yield Index is an unmanaged index of high-yield fixed-income securities issued in developed countries.

Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

17

Trustee approval of management contract

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management (“Putnam Management”) and the sub-management contract, in respect of your fund, between Putnam Management’s affiliate, Putnam Investments Limited (“PIL”), and Putnam Management. In this regard, the Board of Trustees, with the assistance of its Contract Committee consisting solely of Trustees who are not “interested persons” (as such term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (the “Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances. Over the course of several months ending in June 2008, the Contract Committee met several times to consider the information provided by Putnam Management an d other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of this information with all of the Independent Trustees. The Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s management and sub-management contracts, effective July 1, 2008. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees have not evaluated PIL as a separate entity, and all subsequent references to Putnam Management below should be deemed to include reference to PIL as necessary or appropriate in the context.)

The Independent Trustees’ approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds and the costs incurred by Putnam Management in providing such services, and

• That this fee schedule represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees, were subject to the continued application of certain expense reductions and waivers and other considerations noted below, and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the fee arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that certain aspects of such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements in prior years.

Management fee schedules and

categories; total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints, and the assignment of funds to particular fee categories. In reviewing fees and expenses,

18

the Trustees generally focused their attention on material changes in circumstances — for example, changes in a fund’s size or investment style, changes in Putnam Management’s operating costs or responsibilities, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund, which had been carefully developed over the years, re-examined on many occasions and adjusted where appropriate. In this regard, the Trustees also noted that shareholders of your fund voted in 2007 to approve new management contracts containing an identical fee structure. The Trustees focused on two areas of particular interest, as discussed further below:

• Competitiveness. The Trustees reviewed comparative fee and expense information for competitive funds, which indicated that, in a custom peer group of competitive funds selected by Lipper Inc., your fund ranked in the 79th percentile in management fees and in the 41st percentile in total expenses (less any applicable 12b-1 fees) as of December 31, 2007 (the first percentile being the least expensive funds and the 100th percentile being the most expensive funds). (Because the fund’s custom peer group is smaller than the fund’s broad Lipper Inc. peer group, this expense information may differ from the Lipper peer expense information found elsewhere in this report.) The Trustees noted that expense ratios for a number of Putnam funds, which show the percentage of fund assets used to pay for management and administrative services, distribution (12b-1) fees and other expenses, h ad been increasing recently as a result of declining net assets and the natural operation of fee breakpoints.

The Trustees noted that the expense ratio increases described above were currently being controlled by expense limitations initially implemented in January 2004. The Trustees have received a commitment from Putnam Management and its parent company to continue this program through at least June 30, 2009. These expense limitations give effect to a commitment by Putnam Management that the expense ratio of each open-end fund would be no higher than the average expense ratio of the competitive funds included in the fund’s relevant Lipper universe (exclusive of any applicable 12b-1 charges in each case). The Trustees observed that this commitment to limit fund expenses has served shareholders well since its inception.

In order to ensure that the expenses of the Putnam funds continue to meet evolving competitive standards, the Trustees requested, and Putnam Management agreed, to extend for the twelve months beginning July 1, 2008, an additional expense limitation for certain funds at an amount equal to the average expense ratio (exclusive of 12b-1 charges) of a custom peer group of competitive funds selected by Lipper to correspond to the size of the fund. This additional expense limitation will be applied to those open-end funds that had above-average expense ratios (exclusive of 12b-1 charges) based on the custom peer group data for the period ended December 31, 2007. This additional expense limitation will not be applied to your fund because it had a below-average expense ratio relative to its custom peer group.

In addition, the Trustees devoted particular attention to analyzing the Putnam funds’ fees and expenses relative to those of competitors in fund complexes of comparable size and with a comparable mix of asset categories. The Trustees concluded that this analysis did not reveal any matters requiring further attention at the current time.

• Economies of scale. Your fund currently has the benefit of breakpoints in its management fee that provide shareholders with significant

19

economies of scale, which means that the effective management fee rate of the fund (as a percentage of fund assets) declines as the fund grows in size and crosses specified asset thresholds. Conversely, if the fund shrinks in size — as has been the case for many Putnam funds in recent years — these breakpoints result in increasing fee levels. In recent years, the Trustees have examined the operation of the existing breakpoint structure during periods of both growth and decline in asset levels. The Trustees concluded that the fee schedule in effect for your fund represented an appropriate sharing of economies of scale at current asset levels.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services to be provided and profits to be realized by Putnam Management and its affiliates from the relationship with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability with respect to the funds’ management contracts, allocated on a fund-by-fund basis.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the Investment Oversight Coordinating Committee of the Trustees and the Investment Oversight Committees of the Trustees, which had met on a regular monthly basis with the funds’ portfolio teams throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — as measured by the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to such personnel, and in general the ability of Putnam Management to attract and retain high-quality personnel — but also recogn ized that this does not guarantee favorable investment results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time periods and considered information comparing each fund’s performance with various benchmarks and with the performance of competitive funds.

While the Trustees noted the satisfactory investment performance of certain Putnam funds, they considered the disappointing investment performance of many funds in recent periods, particularly over periods in 2007 and 2008. They discussed with senior management of Putnam Management the factors contributing to such underperformance and actions being taken to improve performance. The Trustees recognized that, in recent years, Putnam Management has taken steps to strengthen its investment personnel and processes to address areas of underperformance, including recent efforts to further centralize Putnam Management’s equity research function. In this regard, the Trustees took into consideration efforts by Putnam Management to improve its ability to assess and mitigate investment risk in individual funds, across asset classes, and across the complex as a whole. The Trustees indicated their intention to continue to monitor performance trends to assess the effectivenes s of these efforts and to evaluate whether additional changes to address areas of underperformance are warranted.

In the case of your fund, the Trustees considered that your fund’s class A share cumulative total return performance at net asset value was in the following percentiles of its Lipper Inc. peer group (Lipper High Current Yield Funds) for

20

the one-year, three-year and five-year periods ended December 31, 2007 (the first percentile being the best-performing funds and the 100th percentile being the worst-performing funds):

| | |

| One-year period | 11th | |

| |

| Three-year period | 8th | |

| |

| Five-year period | 15th | |

| |

(Because of the passage of time, these performance results may differ from the performance results for more recent periods shown elsewhere in this report.) Over the one-year, three-year and five-year periods ended December 31, 2007, there were 455, 388, and 334 funds, respectively, in your fund’s Lipper peer group.* Past performance is no guarantee of future returns.

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance problems. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on the responsiveness of Putnam Management in the recent past to Trustee concerns about investment performance, the Trustees concluded that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of engaging a new investment adviser for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations;

other benefits

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage and soft-dollar allocations, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that may be useful to Putnam Management in managing the assets of the fund and of other clients. The Trustees considered changes made in 2008, at Putnam Management’s request, to the Putnam funds’ brokerage allocation policy, which expanded the permitted categories of brokerage and research services payable with soft dollars and increased the permitted soft dollar allocation to third-party services over what had been authorized in previous years. The Trustees indicated their continued intent to monitor the potential benefits associated with the allocation of fund brokerage and trends in industry practice to ensure that the principle of seeking “best price and execution” remains paramount in the portfolio trading process.

The Trustees’ annual review of your fund’s management contract arrangements also included the review of its distributor’s contract and distribution plan with Putnam Retail Management Limited Partnership and the investor servicing agreement with Putnam Fiduciary Trust Company (“PFTC”), each of which provides benefits to affiliates of Putnam Management. In the case of the investor servicing agreement, the Trustees considered that certain shareholder servicing functions

* The percentile rankings for your fund’s class A share annualized total return performance in the Lipper High Current Yield Funds category for the one-year, five-year, and ten-year periods ended June 30, 2009, were 33%, 9%, and 25%, respectively. Over the one-year, five-year, and ten-year periods ended June 30, 2009, your fund ranked 150th out of 462, 28th out of 333, and 49th out of 202 funds, respectively. Note that this more recent information was not available when the Trustees approved the continuance of your fund’s management contract.

21

were shifted to a third-party service provider by PFTC in 2007.

Comparison of retail and institutional

fee schedules

The information examined by the Trustees as part of their annual contract review has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, etc. This information included comparisons of such fees with fees charged to the funds, as well as a detailed assessment of the differences in the services provided to these two types of clients. The Trustees observed, in this regard, that the differences in fee rates between institutional clients and mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients reflect to a substantial degree historical competitive forces operating in separate market places. The Trustees considered the fact that fee rates across different asset classes are typicall y higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to institutional clients of the firm, but did not rely on such comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

22

Other information for shareholders

Important notice regarding delivery

of shareholder documents

In accordance with SEC regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2008, are available in the Individual Investors section of putnam.com, and on the SEC’s Web site, www.sec.gov. If you have questions about finding forms on the SEC’s Web site, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s Web site at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s Web site or the operation of the Public Reference Room.

23

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and noninvestment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlight table also includes the current reporting period.

24

| | | |

| The fund’s portfolio 5/31/09 (Unaudited) | | | |

| |

| |

| CORPORATE BONDS AND NOTES (80.0%)* | Principal amount | Value |

|

| Advertising and marketing services (0.2%) | | | |

| Lamar Media Corp. company guaranty 7 1/4s, 2013 | | $1,230,000 | $1,125,450 |

|

| Lamar Media Corp. 144A sr. notes 9 3/4s, 2014 | | 280,000 | 288,400 |

|

| Vertis, Inc. company guaranty sr. sec. notes Ser. A, | | | |

| zero %, 2012 ‡‡ | | 542,138 | 41,338 |

|

| | | | 1,455,188 |

| Automotive (2.5%) | | | |

| Dana Corp. escrow sr. notes 5.85s, 2015 (In default) † | | 2,135,000 | 214 |

|

| Ford Motor Credit Co., LLC notes 7 7/8s, 2010 | | 3,200,000 | 3,045,862 |

|

| Ford Motor Credit Co., LLC sr. notes 9 7/8s, 2011 | | 3,695,000 | 3,380,925 |

|

| Ford Motor Credit Co., LLC sr. unsec. notes 9 3/4s, 2010 | | 2,790,000 | 2,664,450 |

|

| Ford Motor Credit Co., LLC unsec. notes 7 3/8s, 2009 | | 1,345,000 | 1,311,827 |

|

| Ford Motor Credit Corp. sr. notes 7 1/4s, 2011 | | 205,000 | 176,909 |

|

| Tenneco Automotive, Inc. sec. notes Ser. B, 10 1/4s, 2013 | | 2,135,000 | 1,974,875 |

|

| Tenneco, Inc. sr. unsec. notes company guaranty 8 1/8s, 2015 | | 775,000 | 569,625 |

|

| TRW Automotive, Inc. company guaranty sr. unsec. unsub. | | | |

| notes Ser. REGS, 6 3/8s, 2014 | EUR | 125,000 | 90,092 |

|

| TRW Automotive, Inc. 144A company guaranty sr. notes | | | |

| 7 1/4s, 2017 | | $2,095,000 | 1,466,500 |

|

| TRW Automotive, Inc. 144A company guaranty sr. unsec. unsub. | | | |

| notes 7s, 2014 | | 550,000 | 404,250 |

|

| | | | 15,085,529 |

| Basic materials (8.0%) | | | |

| Airgas, Inc. 144A company | | | |

| guaranty sr. sub. notes 7 1/8s, 2018 | | 2,345,000 | 2,186,713 |

|

| AK Steel Corp. company guaranty sr. unsec. notes 7 3/4s, 2012 | | 1,270,000 | 1,193,800 |

|

| Aleris International, Inc. company guaranty sr. unsec. notes 9s, | | | |

| 2014 (In default) † ‡‡ | | 1,905,000 | 7,144 |

|

| Aleris International, Inc. company guaranty sr. unsec. sub. notes | | | |

| 10s, 2016 (In default) † | | 1,090,000 | 4,088 |

|

| Builders FirstSource, Inc. company guaranty sr. notes FRN | | | |

| 5.133s, 2012 | | 1,675,000 | 741,188 |

|

| Clondalkin Acquisition BV 144A company guaranty sr. notes | | | |

| FRN 3.32s, 2013 (Netherlands) | | 1,165,000 | 768,900 |

|

| Compass Minerals International, Inc. 144A sr. notes 8s, 2019 | | 1,385,000 | 1,371,150 |

|

| Dow Chemical Co. (The) sr. unsec. notes 7.6s, 2014 | | 995,000 | 1,007,143 |

|

| Freeport-McMoRan Copper & Gold, Inc. sr. unsec. notes | | | |

| 8 3/8s, 2017 | | 5,150,000 | 5,137,125 |

|

| Freeport-McMoRan Copper & Gold, Inc. sr. unsec. notes | | | |

| 8 1/4s, 2015 | | 2,030,000 | 2,035,075 |

|

| Georgia-Pacific Corp. sr. unsec. unsub. notes 9 1/2s, 2011 | | 1,900,000 | 1,952,250 |

|

| Gerdau Ameristeel Corp. sr. notes 10 3/8s, 2011 (Canada) | | 2,007,000 | 2,057,175 |

|

| Graphic Packaging International Corp sr. notes 8 1/2s, 2011 | | 1,770,000 | 1,752,300 |

|

| Hexion U.S. Finance Corp./Hexion Nova Scotia Finance, | | | |

| ULC company guaranty 9 3/4s, 2014 | | 875,000 | 376,250 |

|

| Huntsman International, LLC company guaranty sr. unsec. | | | |

| sub. notes Ser. Regs 6 7/8s, 2013 | EUR | 1,060,000 | 936,245 |

|

| Huntsman International, LLC company guaranty sr. unsec. sub. | | | |

| notes 7 7/8s, 2014 | | $660,000 | 452,100 |

|

| International Paper Co. sr. unsec. notes 9 3/8s, 2019 | | 770,000 | 758,450 |

|

| International Paper Co. sr. unsec. notes 7.4s, 2014 | | 2,085,000 | 2,056,807 |

|

25

| | | |

| CORPORATE BONDS AND NOTES (80.0%)* cont. | Principal amount | Value |

|

| Basic materials cont. | | | |

| Jefferson Smurfit Corp. company guaranty 8 1/4s, 2012 | | $540,000 | $170,100 |

|

| Metals USA, Inc. sec. notes 11 1/8s, 2015 | | 1,645,000 | 1,237,863 |

|

| Momentive Performance Materials, Inc. company guaranty | | | |

| sr. unsec. notes 9 3/4s, 2014 | | 1,875,000 | 712,500 |

|

| Mosaic Co. (The) 144A sr. unsec. unsub. notes 7 5/8s, 2016 | | 2,235,000 | 2,223,825 |

|

| Mosaic Co. (The) 144A sr. unsec. unsub. notes 7 3/8s, 2014 | | 670,000 | 680,137 |

|

| Nalco Co. 144A sr. notes 8 1/4s, 2017 | | 365,000 | 366,825 |

|

| NewPage Holding Corp. sr. unsec. unsub. notes FRN | | | |

| 8.579s, 2013 ‡‡ | | 625,796 | 68,838 |

|

| Norske Skog Canada, Ltd. company guaranty Ser. D, 8 5/8s, | | | |

| 2011 (Canada) | | 2,031,000 | 1,183,058 |

|

| Novelis, Inc. company guaranty 7 1/4s, 2015 | | 1,995,000 | 1,311,713 |

|

| Rio Tinto Finance USA LTD company guaranty sr. unsec. notes | | | |

| 8.95s, 2014 (United Kingdom) | | 555,000 | 596,464 |

|

| Rockwood Specialties Group, Inc. company guaranty | | | |

| 7 5/8s, 2014 | EUR | 470,000 | 611,068 |

|

| Smurfit Kappa Funding PLC sr. unsec. sub. notes 7 3/4s, | | | |

| 2015 (Ireland) | | $2,287,000 | 1,555,160 |

|

| Steel Dynamics, Inc. company guaranty sr. unsec. unsub. notes | | | |

| 7 3/8s, 2012 | | 310,000 | 285,200 |

|

| Steel Dynamics, Inc. company guaranty sr. unsec. unsub. notes | | | |

| 6 3/4s, 2015 | | 2,900,000 | 2,472,250 |

|

| Steel Dynamics, Inc. 144A sr. notes 7 3/4s, 2016 | | 1,085,000 | 924,963 |

|

| Stone Container Corp. sr. notes 8 3/8s, 2012 | | 1,960,000 | 617,400 |

|

| Teck Resources, Ltd. sr. unsec. notes 6 1/8s, 2035 (Canada) | | 820,000 | 534,320 |

|

| Teck Resources, Ltd. 144A sr. sec. notes 10 3/4s, 2019 (Canada) | | 1,265,000 | 1,301,369 |

|

| Teck Resources, Ltd. 144A sr. sec. notes 10 1/4s, 2016 (Canada) | | 1,905,000 | 1,928,813 |

|

| Teck Resources, Ltd. 144A sr. sec. notes 9 3/4s, 2014 (Canada) | | 1,585,000 | 1,577,075 |

|

| Tube City IMS Corp. company guaranty sr. unsec. sub. notes | | | |

| 9 3/4s, 2015 | | 1,530,000 | 872,100 |

|

| Verso Paper Holdings, LLC./Verso Paper, Inc. 144A sr. sec. notes | | | |

| 11 1/2s, 2014 | | 635,000 | 590,550 |

|

| Verso Paper Holdings, LLC/Verso Paper, Inc. company guaranty | | | |

| 11 3/8s, 2016 | | 855,000 | 350,550 |

|

| Verso Paper Holdings, LLC/Verso Paper, Inc. company guaranty | | | |

| sr. sec. notes FRN Ser. B, 4.778s, 2014 | | 860,000 | 464,400 |

|

| Verso Paper Holdings, LLC/Verso Paper, Inc. sec. notes | | | |

| 9 1/8s, 2014 | | 2,430,000 | 1,445,850 |

|

| | | | 48,876,294 |

| Broadcasting (1.6%) | | | |

| Clear Channel Communications, Inc. sr. unsec. notes 7.65s, 2010 | | 610,000 | 268,400 |

|

| Clear Channel Communications, Inc. sr. unsec. notes 5 1/2s, 2014 | | 285,000 | 44,175 |

|

| DIRECTV Holdings, LLC company guaranty sr. unsec. notes | | | |

| 7 5/8s, 2016 | | 1,315,000 | 1,272,263 |

|

| DIRECTV Holdings, LLC company guaranty sr. unsec. notes | | | |

| 6 3/8s, 2015 | | 3,145,000 | 2,861,950 |

|

| EchoStar DBS Corp. sr. notes 6 3/8s, 2011 | | 3,700,000 | 3,575,125 |

|

| Univision Communications, Inc. 144A company guaranty unsec. | | | |

| notes zero %, 2015 ‡‡ | | 1,460,000 | 452,600 |

|

| XM Satellite Radio, Inc. 144A company guaranty sr. unsec. notes | | | |

| 13s, 2013 | | 2,105,000 | 1,515,600 |

|

26

| | | |

| CORPORATE BONDS AND NOTES (80.0%)* cont. | Principal amount | Value |

|

| Broadcasting cont. | | | |

| Young Broadcasting, Inc. company guaranty sr. sub. notes 8 3/4s, | | | |

| 2014 (In default) † | | $395,000 | $1,481 |

|

| Young Broadcasting, Inc. company guaranty sr. unsec. sub. notes | | | |

| 10s, 2011 (In default) † | | 1,142,000 | 8,565 |

|

| | | | 10,000,159 |

| Building materials (1.2%) | | | |

| Associated Materials, Inc. company guaranty 9 3/4s, 2012 | | 2,970,000 | 2,509,650 |

|

| Masco Corp. sr. unsec. unsub. notes 6 1/8s, 2016 | | 1,185,000 | 967,820 |

|

| NTK Holdings, Inc. sr. unsec. disc. notes stepped-coupon zero % | | | |

| (10 3/4s, 9/1/09), 2014 †† | | 1,765,000 | 174,294 |

|

| Owens Corning, Inc. company guaranty sr. unsec. notes | | | |

| 6 1/2s, 2016 | | 1,655,000 | 1,439,951 |

|

| Texas Industries, Inc. sr. unsec. notes 7 1/4s, 2013 | | 715,000 | 614,900 |

|

| Texas Industries, Inc. 144A company guaranty sr. unsec. notes | | | |

| 7 1/4s, 2013 | | 360,000 | 309,600 |

|

| THL Buildco, Inc. (Nortek Holdings, Inc.) sr. sec. notes 10s, 2013 | | 345,000 | 223,388 |

|

| THL Buildco, Inc. (Nortek Holdings, Inc.) sr. sub. notes | | | |

| 8 1/2s, 2014 | | 3,495,000 | 926,175 |

|

| | | | 7,165,778 |

| Cable television (1.9%) | | | |

| Atlantic Broadband Finance, LLC company guaranty | | | |

| 9 3/8s, 2014 | | 710,000 | 599,950 |

|

| Cablevision Systems Corp. sr. unsec. notes Ser. B, 8s, 2012 | | 2,010,000 | 1,974,825 |

|

| CCH I Holdings, LLC company guaranty sr. unsec. unsub. notes | | | |

| 12 1/8s, 2015 (In default) † | | 25,000 | 250 |

|

| CCH I, LLC sec. notes 11s, 2015 (In default) † | | 2,792,000 | 321,080 |

|

| CCH II, LLC sr. unsec. notes 10 1/4s, 2010 (In default) † | | 290,000 | 287,100 |

|

| CCH II, LLC sr. unsec. notes Ser. B, 10 1/4s, 2010 (In default) † | | 3,205,000 | 3,140,900 |

|

| CCO Holdings LLC/CCO Holdings Capital Corp. sr. unsec. notes | | | |

| 8 3/4s, 2013 (In default) † | | 1,075,000 | 983,625 |

|

| CSC Holdings, Inc. sr. notes 6 3/4s, 2012 | | 2,145,000 | 2,069,925 |

|

| CSC Holdings, Inc. 144A sr. unsec. notes 8 1/2s, 2014 | | 405,000 | 402,975 |

|

| Rainbow National Services, LLC 144A sr. notes 8 3/4s, 2012 | | 1,730,000 | 1,749,463 |

|

| | | | 11,530,093 |

| Capital goods (5.0%) | | | |

| Alliant Techsystems, Inc. sr. sub. notes 6 3/4s, 2016 | | 2,810,000 | 2,606,275 |

|

| Allied Waste North America, Inc. company guaranty sr. unsub. | | | |

| sec. notes 7 7/8s, 2013 | | 355,000 | 361,213 |

|

| Baldor Electric Co. company guaranty 8 5/8s, 2017 | | 1,670,000 | 1,528,050 |

|

| BE Aerospace, Inc. sr. unsec. unsub. notes 8 1/2s, 2018 | | 2,970,000 | 2,806,650 |

|

| Berry Plastics Corp. company guaranty sr. notes FRN | | | |

| 5.881s, 2015 | | 1,745,000 | 1,494,156 |

|

| Bombardier, Inc. 144A sr. unsec. notes FRN 4.406s, | | | |

| 2013 (Canada) | EUR | 870,000 | 1,023,545 |

|

| Bombardier, Inc. 144A unsec. notes 6 3/4s, 2012 (Canada) | | $1,530,000 | 1,407,600 |

|

| Crown Americas, LLC/Crown Americas Capital Corp. sr. notes | | | |

| 7 5/8s, 2013 | | 1,960,000 | 1,911,000 |

|

| General Cable Corp. company guaranty sr. unsec. notes FRN | | | |

| 3.583s, 2015 | | 1,900,000 | 1,539,000 |

|

| Hawker Beechcraft Acquisition Co., LLC sr. sub. notes | | | |

| 9 3/4s, 2017 | | 1,770,000 | 548,700 |

|

27

| | | |

| CORPORATE BONDS AND NOTES (80.0%)* cont. | Principal amount | Value |

|

| Capital goods cont. | | | |

| Hawker Beechcraft Acquisition Co., LLC sr. unsec. notes | | | |

| 8 1/2s, 2015 | | $200,000 | $84,000 |

|

| Hexcel Corp. sr. sub. notes 6 3/4s, 2015 | | 1,720,000 | 1,556,600 |

|

| L-3 Communications Corp. company guaranty Ser. B, | | | |

| 6 3/8s, 2015 | | 2,985,000 | 2,716,350 |

|

| L-3 Communications Corp. company guaranty sr. unsec. sub. | | | |

| notes 6 1/8s, 2014 | | 725,000 | 667,000 |

|

| L-3 Communications Corp. company guaranty sr. unsec. sub. | | | |

| notes 5 7/8s, 2015 | | 575,000 | 511,750 |

|

| Legrand SA unsec. unsub. debs. 8 1/2s, 2025 (France) | | 3,185,000 | 2,737,762 |

|

| Owens-Brockway Glass Container, Inc. company guaranty | | | |

| 6 3/4s, 2014 | EUR | 695,000 | 913,422 |

|

| Ryerson Tull, Inc. company guaranty sr. sec. notes 12 1/4s, 2015 | | $1,635,000 | 1,103,625 |

|

| TD Funding Corp. company guaranty 7 3/4s, 2014 | | 1,780,000 | 1,717,700 |

|

| Terex Corp. company guaranty 7 3/8s, 2014 | | 1,750,000 | 1,605,625 |

|

| Titan International, Inc. company guaranty 8s, 2012 | | 2,150,000 | 1,849,000 |

|

| | | | 30,689,023 |

| Coal (1.2%) | | | |

| Arch Western Finance, LLC company guaranty sr. sec. notes | | | |

| 6 3/4s, 2013 | | 4,165,000 | 3,790,150 |

|

| Peabody Energy Corp. company guaranty 7 3/8s, 2016 | | 4,020,000 | 3,829,050 |

|

| | | | 7,619,200 |

| Commercial and consumer services (1.6%) | | | |

| Aramark Corp. company guaranty 8 1/2s, 2015 | | 3,210,000 | 3,061,538 |

|

| Corrections Corporation of America company guaranty sr. notes | | | |

| 7 3/4s, 2017 | | 1,820,000 | 1,779,050 |

|

| Expedia, Inc. sr. unsec. notes company guaranty 7.456s, 2018 | | 550,000 | 528,000 |

|

| Expedia, Inc. 144A company guaranty sr. notes 8 1/2s, 2016 | | 1,430,000 | 1,337,050 |

|

| Lender Processing Services, Inc. company guaranty sr. unsec. | | | |

| unsub. notes 8 1/8s, 2016 | | 1,985,000 | 1,955,225 |

|

| Travelport LLC company guaranty 11 7/8s, 2016 | | 390,000 | 202,800 |

|

| Travelport LLC company guaranty 9 7/8s, 2014 | | 1,125,000 | 708,750 |

|

| | | | 9,572,413 |

| Conglomerates (0.2%) | | | |

| SPX Corp. sr. unsec. notes 7 5/8s, 2014 (acquired 11/3/08, | | | |

| cost $1,283,500) ‡ | | 1,510,000 | 1,464,700 |

|

| | | | 1,464,700 |

| Consumer (0.6%) | | | |

| Jostens IH Corp. company guaranty 7 5/8s, 2012 | | 2,040,000 | 2,009,400 |

|

| Yankee Acquisition Corp. company guaranty Ser. B, 8 1/2s, 2015 | | 2,680,000 | 2,023,400 |

|

| | | | 4,032,800 |

| Consumer staples (5.1%) | | | |

| Archibald Candy Corp. company guaranty 10s,2009 (In default) † F�� | | 415,457 | 6,416 |

|

| Avis Budget Car Rental, LLC company guaranty sr. unsec. unsub. | | | |

| notes 7 3/4s, 2016 | | 1,475,000 | 1,054,625 |

|

| Avis Budget Car Rental, LLC company guaranty sr. unsec. unsub. | | | |

| notes 7 5/8s, 2014 | | 965,000 | 689,975 |

|

| Chiquita Brands International, Inc. sr. notes 7 1/2s, 2014 | | 2,060,000 | 1,709,800 |

|

| Chiquita Brands International, Inc. sr. unsec. unsub. notes | | | |

| 8 7/8s, 2015 | | 290,000 | 246,500 |

|

| Claire’s Stores, Inc. 144A company guaranty sr. unsec. notes | | | |

| 9 5/8s, 2015 (In default) † ‡‡ | | 57,853 | 15,620 |

|

28

| | |

| CORPORATE BONDS AND NOTES (80.0%)* cont. | Principal amount | Value |

|

| Consumer staples cont. | | |

| Constellation Brands, Inc. company guaranty sr. unsec. notes | | |

| 7 1/4s, 2017 | $275,000 | $256,438 |

|

| Constellation Brands, Inc. company guaranty sr. unsec. unsub. | | |

| notes 7 1/4s, 2016 | 2,715,000 | 2,531,738 |

|

| Del Monte Corp. sr. sub. notes 8 5/8s, 2012 | 2,625,000 | 2,638,125 |

|

| Dole Food Co. 144A sr. unsec. notes 13 7/8s, 2014 | 1,965,000 | 2,102,550 |

|

| Elizabeth Arden, Inc. company guaranty 7 3/4s, 2014 | 2,645,000 | 2,221,800 |

|

| Hertz Corp. company guaranty 8 7/8s, 2014 | 2,310,000 | 2,102,100 |

|

| Jarden Corp. company guaranty 7 1/2s, 2017 | 3,185,000 | 2,755,025 |

|

| Jarden Corp. sr. unsec. 8s, 2016 | 605,000 | 585,338 |

|

| Pinnacle Foods Finance LLC sr. notes 9 1/4s, 2015 | 655,000 | 584,588 |

|

| Prestige Brands, Inc. sr. sub. notes 9 1/4s, 2012 | 2,178,000 | 2,134,440 |

|

| Rite Aid Corp. company guaranty 9 1/2s, 2017 | 1,885,000 | 1,225,250 |

|

| Rite Aid Corp. sec. notes 7 1/2s, 2017 | 180,000 | 141,300 |

|

| Sealy Mattress Co. sr. sub. notes 8 1/4s, 2014 | 945,000 | 746,550 |

|

| Sealy Mattress Co. 144A sr. sec. notes 10 7/8s, 2016 | 1,400,000 | 1,435,000 |

|

| Smithfield Foods, Inc. sr. unsec. notes 7s, 2011 | 410,000 | 352,600 |

|