UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-04692

Emerging Markets Growth Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

6455 Irvine Center Drive

Irvine, California 92618

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (949) 975-5000

Date of fiscal year end: June 30

Date of reporting period: June 30, 2019

Gregory F. Niland

Emerging Markets Growth Fund, Inc.

5300 Robin Hood Road

Norfolk, Virginia 23513

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

| Emerging Markets Growth FundSM | |

| Annual report for the year ended June 30, 2019 |

Beginning January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, we intend to no longer mail paper copies of the fund’s shareholder reports, unless specifically requested from the fund or your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the fund’s website (capitalgroup.com/us/investments/emerging-markets-growth-fund.html); you will be notified by mail and provided with a website link to access the report each time a report is posted.

You may elect to receive paper copies of all future reports free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the fund, you may inform the fund that you wish to continue receiving paper copies of your shareholder reports by contacting us at (800) 421 4225. Your election to receive paper reports will apply to all funds held with the fund’s transfer agent or through your financial intermediary.

Emerging Markets Growth Fund seeks long-term growth of capital and invests primarily in common stock and other equity securities of issuers in developing countries.

Fund results shown in this report are for past periods and are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, please call (800) 421-4989.

Investing in developing markets may be subject to risks, such as significant currency and price fluctuations, political instability, differing securities regulations and periods of illiquidity, which are detailed in the fund’s prospectus. Investments in developing markets have been more volatile than investments in developed markets, reflecting the greater uncertainties of investing in less established economies. Individuals investing in developing markets should have a long-term perspective and be able to tolerate potentially sharp declines in the value of their investments.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Contents

| 1 | Letter to investors | |

| 2 | 20 largest equity holdings | |

| 6 | The value of a long-term investment | |

| 7 | Investment portfolio | |

| 13 | Financial statements | |

| 16 | Notes to financial statements |

Emerging markets stocks fluctuated over the fund’s fiscal year, largely due to bouts of volatility tied to U.S.-China trade talks and concerns over China’s slowing economy. Shifts in global monetary policies and the uncertainty of election outcomes in several developing countries also impacted sentiment at times.

In this environment, the fund outpaced its benchmark by a wide margin. The value of Emerging Markets Growth Fund increased 4.71% with distributions reinvested for the 12 months ended June 30, 2019, while its benchmark, the unmanaged MSCI Emerging Markets Investable Market Index (IMI), gained 0.47%.*

Market review

Developing-country stocks experienced sharp swings during the 12-month period. Equities sold off during the last six months of 2018, hit by trade tariffs, slowing global growth and U.S. interest rate hikes. However, stocks largely rebounded in 2019. U.S. and China called a truce on additional trade tariffs, market-friendly reformers were re-elected in India and Indonesia, and central bankers in the U.S. and Europe signaled intentions to maintain low interest rates.

Chinese stocks were volatile as the trade clash with the U.S. intensified and China’s economy decelerated. With its economy slowing and trade relationships

| * | Unless otherwise noted, country and sector returns are based on MSCI EM IMI indices, expressed in U.S. dollars, and assume the reinvestment of dividends. Results reflect dividends net of withholding taxes. |

Results at a glance

For periods ended June 30, 2019, with distributions reinvested

| Cumulative total returns | Average annual total returns | |||||||||||||||||||||||

| 6 months | 1 year | 3 years | 5 years | 10 years | Lifetime1 | |||||||||||||||||||

| Emerging Markets Growth Fund (Class M shares) | 14.33 | % | 4.71 | % | 12.50 | % | 2.93 | % | 4.93 | % | 12.89 | % | ||||||||||||

| MSCI Emerging Markets IMI2,3 | 10.14 | 0.47 | 10.01 | 2.25 | 5.83 | 9.96 | 4 | |||||||||||||||||

| MSCI Emerging Markets Index3,5 | 10.58 | 1.21 | 10.66 | 2.49 | 5.81 | 9.93 | 4 | |||||||||||||||||

| 1 | Since May 30, 1986. |

| 2 | Returns for the MSCI Emerging Markets Investable Market Index (IMI) were calculated using the MSCI Emerging Markets Index with dividends gross of withholding taxes from December 31, 1987, to December 31, 2000, and with dividends net of withholding taxes from January 1, 2001, to November 30, 2007, and using the MSCI Emerging Markets IMI with dividends net of withholding taxes thereafter. |

| 3 | The indices are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. Source: MSCI. |

| 4 | The MSCI Emerging Markets Index did not start until December 31, 1987. As a result, the International Finance Corporation (IFC) Global Composite Index was used in lieu of the MSCI Emerging Markets Index from May 30, 1986, to December 31, 1987. |

| 5 | Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

The total annual fund operating expense ratio is 0.84% for Class M shares as of the most recent fiscal year-end, and is 0.88% including “acquired fund” fees and expenses.

| Emerging Markets Growth Fund | 1 |

in flux, Chinese officials rolled out targeted stimulus measures to stabilize growth and improve market confidence. They loosened credit for infrastructure projects, lowered reserve requirements for banks and cut taxes for businesses and individuals. Overall, the MSCI China IMI fell 7.09%. Health care and consumer discretionary stocks fell the most, while the real estate and communication services sectors produced the largest gains.

Indian equities rose 5.11%, overcoming concerns about the pace of economic growth, credit quality issues among nonbank lenders and richer stock valuations compared with other developing markets. Prime Minister Narendra Modi won a decisive re-election in May, giving him a strong mandate to push for additional reforms to improve India’s business climate and modernize the economy.

Elsewhere in Asia, Indonesian equities surged 16.18%. President Joko Widodo won a second term in May and hopes to attract more foreign investment into Indonesia. He aims to grow the country’s digital economy through tax incentives, develop more infrastructure and cut the corporate tax rate. The MSCI Korea IMI fell 10.51% while the MSCI Taiwan IMI gained 0.22%. The export-driven economies of South Korea and Taiwan were affected at varying levels by the U.S.-China trade dispute.

In Latin America, Brazilian stocks surged 39.77% on hopes President Jair Bolsonaro can overhaul Brazil’s pension system and implement other reforms to revive economic growth. Bolsonaro took office January 1 after defeating a leftist candidate in October’s runoff election. Pension reform is a key building block of his pro-market business agenda and is seen as vital to shoring up Brazil’s fiscal policy.

| Percent of net assets as of 6/30/19 | Price change for the 12 months ended 6/30/19* | |||||||

| Samsung Electronics | 3.9 | % | –2.7 | % | ||||

| AIA Group | 3.7 | 23.4 | ||||||

| Taiwan Semiconductor Manufacturing | 3.7 | 8.4 | ||||||

| Tencent Holdings | 3.4 | –10.1 | ||||||

| Ctrip.com International | 3.1 | –22.5 | ||||||

| Jiangsu Hengrui Medicine | 2.9 | 0.8 | ||||||

| China Overseas Land & Investment | 2.8 | 11.9 | ||||||

| HDFC Bank | 2.5 | 15.0 | ||||||

| Longfor Properties | 2.4 | 39.9 | ||||||

| Galaxy Entertainment Group | 2.1 | –13.0 | ||||||

| Huazhu Group | 2.1 | –13.7 | ||||||

| Ping An Insurance Group | 2.0 | 30.5 | ||||||

| China Resources Land | 2.0 | 30.6 | ||||||

| Sberbank of Russia | 2.0 | 7.0 | ||||||

| BeiGene | 1.8 | N/A | † | |||||

| ICICI Bank | 1.7 | 57.2 | ||||||

| Alibaba Group Holding | 1.3 | –8.7 | ||||||

| Noah Holdings | 1.3 | –18.4 | ||||||

| Bank Central Asia | 1.3 | 41.6 | ||||||

| Hangzhou Tigermed Consulting | 1.3 | N/A | † | |||||

| Total | 47.3 | % | ||||||

| * | The percent change is reflected in U.S. dollars. The actual gain or loss on the total position in the fund may differ from the percentage shown. |

| † | Acquired during the reporting period. |

Portfolio review

Stock selection in China boosted returns on a relative basis, helped by holdings in several real estate companies that have very little presence in the benchmark index. Chinese property developer Longfor Group was the portfolio’s top contributor. Its shares rose on strong sales and profit growth in 2018 despite stricter home-buying rules and government-imposed price controls in major cities. China Resources Land and China Overseas Land & Investment also contributed to returns.

Stock selection within financials helped boost returns. Shares of Hong Kong–listed insurer AIA Group gained on increasing business from customers in China, Hong Kong and Singapore. AIA also hiked its dividend following steady profit growth over the past year.

| 2 | Emerging Markets Growth Fund |

Where the fund’s assets were invested

| Percent of net assets | MSCI EM IMI1 | Value of holdings 6/30/19 | ||||||||||||||||||||||

| 6/30/17 | 6/30/18 | 12/31/18 | 6/30/19 | 6/30/19 | (in thousands) | |||||||||||||||||||

| Asia-Pacific | ||||||||||||||||||||||||

| China | 24.3 | % | 25.9 | % | 27.2 | % | 32.3 | % | 29.2 | % | $ | 727,057 | ||||||||||||

| Hong Kong | 6.5 | 8.1 | 7.7 | 9.2 | — | 208,608 | ||||||||||||||||||

| India | 11.2 | 11.6 | 12.8 | 10.8 | 9.7 | 243,133 | ||||||||||||||||||

| Indonesia | 6.0 | 5.0 | 6.5 | 6.7 | 2.2 | 151,065 | ||||||||||||||||||

| Malaysia | .6 | .1 | — | — | 2.2 | — | ||||||||||||||||||

| Pakistan | — | — | — | — | .1 | — | ||||||||||||||||||

| Philippines | 1.7 | 2.4 | 3.1 | 2.2 | 1.1 | 49,783 | ||||||||||||||||||

| Singapore | 1.0 | .7 | .7 | .7 | — | 15,274 | ||||||||||||||||||

| South Korea | 5.6 | 5.1 | 4.9 | 4.8 | 12.7 | 107,803 | ||||||||||||||||||

| Taiwan | 7.9 | 5.9 | 6.0 | 5.2 | 11.7 | 116,464 | ||||||||||||||||||

| Thailand | 1.0 | .3 | — | .2 | 3.2 | 5,785 | ||||||||||||||||||

| Vietnam | — | 1.3 | 1.7 | 1.3 | — | 29,856 | ||||||||||||||||||

| 65.8 | 66.4 | 70.6 | 73.4 | 72.1 | 1,654,828 | |||||||||||||||||||

| Latin America | ||||||||||||||||||||||||

| Argentina | — | 2 | .3 | .6 | .5 | .4 | 10,855 | |||||||||||||||||

| Brazil | 4.9 | 5.9 | 6.4 | 5.7 | 7.7 | 127,352 | ||||||||||||||||||

| Chile | 1.1 | 1.1 | .7 | .1 | 1.0 | 2,946 | ||||||||||||||||||

| Colombia | — | — | — | — | .4 | — | ||||||||||||||||||

| Mexico | 3.7 | 2.2 | 2.1 | 1.2 | 2.6 | 28,252 | ||||||||||||||||||

| Peru | 1.3 | 1.2 | 1.3 | 1.1 | .4 | 23,790 | ||||||||||||||||||

| 11.0 | 10.7 | 11.1 | 8.6 | 12.5 | 193,195 | |||||||||||||||||||

| Eastern Europe and Middle East | ||||||||||||||||||||||||

| Czech Republic | — | — | — | — | .1 | — | ||||||||||||||||||

| Greece | — | — | — | — | .4 | — | ||||||||||||||||||

| Hungary | — | .2 | .2 | .2 | .3 | 4,629 | ||||||||||||||||||

| Kingdom of Saudi Arabia | 1.3 | .9 | .1 | .1 | 1.4 | 3,221 | ||||||||||||||||||

| Oman | .1 | — | — | — | — | — | ||||||||||||||||||

| Poland | — | — | — | — | 1.1 | — | ||||||||||||||||||

| Qatar | — | — | — | — | 1.0 | — | ||||||||||||||||||

| Romania | — | — | .1 | .2 | — | 3,469 | ||||||||||||||||||

| Russian Federation | 5.6 | 6.4 | 5.5 | 5.5 | 3.7 | 124,386 | ||||||||||||||||||

| Slovenia | — | — | .5 | .4 | — | 9,006 | ||||||||||||||||||

| Turkey | .6 | .5 | 1.1 | 1.2 | .6 | 27,867 | ||||||||||||||||||

| United Arab Emirates | .4 | .5 | .5 | .4 | .7 | 8,428 | ||||||||||||||||||

| 8.0 | 8.5 | 8.0 | 8.0 | 9.3 | 181,006 | |||||||||||||||||||

| Africa | ||||||||||||||||||||||||

| Egypt | — | — | — | — | .2 | — | ||||||||||||||||||

| Federal Republic of Nigeria | — | — | — | .1 | — | 3,053 | ||||||||||||||||||

| South Africa | 6.4 | 4.9 | 4.4 | 3.4 | 5.9 | 77,104 | ||||||||||||||||||

| 6.4 | 4.9 | 4.4 | 3.5 | 6.1 | 80,157 | |||||||||||||||||||

| Other markets3 | ||||||||||||||||||||||||

| Australia | — | 2 | .2 | .2 | .2 | 3,336 | ||||||||||||||||||

| Belgium | — | — | — | .1 | 1,235 | |||||||||||||||||||

| Canada | .2 | — | — | — | — | |||||||||||||||||||

| Denmark | 1.2 | 1.5 | 1.5 | .6 | 13,354 | |||||||||||||||||||

| France | — | 2 | — | 2 | — | 2 | .2 | 3,601 | ||||||||||||||||

| Italy | .2 | .2 | — | — | — | |||||||||||||||||||

| Netherlands | — | — | 2 | — | — | — | ||||||||||||||||||

| Norway | — | .1 | .1 | — | — | |||||||||||||||||||

| Portugal | — | — | — | .1 | 2,570 | |||||||||||||||||||

| Switzerland | .4 | — | — | — | — | |||||||||||||||||||

| United Kingdom | .8 | .7 | .4 | .9 | 20,079 | |||||||||||||||||||

| United States | 2.3 | 3.0 | 1.7 | 1.0 | 23,523 | |||||||||||||||||||

| 5.1 | 5.7 | 3.9 | 3.1 | 67,698 | ||||||||||||||||||||

| Multinational | — | 2 | — | — | — | — | ||||||||||||||||||

| Short-term securities and other assets less liabilities | 3.7 | 3.8 | 2.0 | 3.4 | 77,674 | |||||||||||||||||||

| Total net assets | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | $ | 2,254,558 | ||||||||||||||

| 1 | A dash indicates that the market is not included in the index. Source: MSCI. |

| 2 | Amount less than .1%. |

| 3 | Includes investments in companies incorporated in the region that have significant operations in emerging markets. |

| Emerging Markets Growth Fund | 3 |

Certain private sector banks in India helped returns. HDFC Bank shares rose on increasing profits, strong loan growth and credit quality; it continues to take market share from state-run banks that have been hamstrung by nonperforming loans. Shares of ICICI Bank gained on improving earnings and hopes a new CEO can shore up its asset quality.

MercadoLibre, an e-commerce company focused on Latin America, lifted portfolio returns. Its shares climbed to record highs as the company posted strong revenue growth and gained traction in expanding its network platform for processing online and offline payments. It also raised $1.85 billion in a secondary stock sale that involved a strategic investment from U.S.-based PayPal.

In contrast, Shanghai Fosun Pharmaceutical was the largest detractor to returns. Chinese health care stocks broadly sold off as regulators took aim at high drug prices and sped up approvals for foreign firms to sell in China. Shanghai Fosun reported solid revenue growth in 2018 but the company is incurring significantly higher expenses as it expands its R&D pipeline.

Investments in Hong Kong–listed casino operators Wynn Macau and Galaxy Entertainment detracted from results. Shares of both companies fell as investors tried to gauge the impact of the slowdown in China’s economy on spending at Macau casinos. New railways and bridges have improved access to Macau and may help drive more visitors from China to the gaming hub.

The investment in IndusInd Bank also weighed on returns, hurt by exposure to some troubled loans to nonbank finance companies. The company acquired microfinance lender Bharat Financial, a deal anticipated to boost IndusInd’s presence in rural areas.

Outlook

Our investment team focuses on companies in developing countries that are growing faster than their global peers as well as those that are trading at a discount based on our projections. We particularly emphasize small- and mid-sized companies, as we believe our global network of more than 40 investment analysts and macroeconomic professionals on three continents gives us unique insights in this part of the market.

As of this writing, the pace of global growth and any resolution to the U.S.-China trade conflict remain uncertain. Portfolio managers have conducted extensive planning around some potential winners and losers in a wide range of scenarios that may result from shifts in trade and the resulting effect on the global economy.

| 12 months ended 6/30/19 | 6 months ended 6/30/19 | |||||||||||||||

| Percent change in key markets* | Expressed in U.S. dollars | Expressed in local currency | Expressed in U.S. dollars | Expressed in local currency | ||||||||||||

| Asia-Pacific | ||||||||||||||||

| China IMI | –7.09 | % | –7.34 | % | 12.73 | % | 12.56 | % | ||||||||

| India IMI | 5.11 | 5.90 | 6.43 | 5.23 | ||||||||||||

| Indonesia IMI | 16.18 | 14.54 | 6.88 | 5.01 | ||||||||||||

| Korea IMI | –10.51 | –7.28 | 2.29 | 5.85 | ||||||||||||

| Malaysia IMI | –0.77 | 1.51 | 3.40 | 3.40 | ||||||||||||

| Pakistan IMI | –37.80 | –18.18 | –17.67 | –5.24 | ||||||||||||

| Philippines IMI | 19.05 | 14.29 | 12.72 | 9.82 | ||||||||||||

| Taiwan IMI | 0.22 | 2.10 | 10.34 | 11.50 | ||||||||||||

| Thailand IMI | 19.65 | 10.75 | 18.26 | 11.38 | ||||||||||||

| Latin America | ||||||||||||||||

| Argentina IMI | 11.74 | 11.74 | † | 23.63 | 23.63 | † | ||||||||||

| Brazil IMI | 39.77 | 39.23 | 16.39 | 15.10 | ||||||||||||

| Chile IMI | –10.31 | –6.47 | –0.49 | –2.65 | ||||||||||||

| Colombia IMI | –4.89 | 3.85 | 23.01 | 21.48 | ||||||||||||

| Mexico IMI | –6.46 | –8.57 | 7.57 | 4.94 | ||||||||||||

| Peru IMI | 2.39 | 2.44 | 7.97 | 7.94 | ||||||||||||

| Eastern Europe and Middle East | ||||||||||||||||

| Czech Republic IMI | 1.12 | 1.40 | 7.59 | 6.77 | ||||||||||||

| Greece IMI | 6.53 | 9.22 | 43.17 | 43.71 | ||||||||||||

| Hungary IMI | 11.82 | 12.43 | 1.55 | 2.56 | ||||||||||||

| Poland IMI | 10.17 | 9.73 | 3.78 | 3.02 | ||||||||||||

| Qatar IMI | 18.70 | 18.71 | –1.14 | –1.14 | ||||||||||||

| Russia IMI | 25.96 | 26.61 | 30.70 | 20.43 | ||||||||||||

| Saudi Arabia IMI | 9.87 | 9.87 | 15.34 | 15.30 | ||||||||||||

| Turkey IMI | –18.24 | 3.22 | –0.09 | 8.63 | ||||||||||||

| United Arab Emirates IMI | 0.58 | 0.58 | 4.32 | 4.32 | ||||||||||||

| Africa | ||||||||||||||||

| Egypt IMI | –2.60 | –9.10 | 20.59 | 12.35 | ||||||||||||

| South Africa IMI | –1.24 | 1.61 | 10.43 | 8.25 | ||||||||||||

| MSCI Emerging Markets IMI | 0.47 | % | 10.14 | % | ||||||||||||

| Emerging Markets Growth Fund | 4.71 | % | 14.33 | % | ||||||||||||

| * | The market indices, compiled by MSCI, reflect dividends net of withholding taxes. Source: MSCI. The indices are unmanaged and, therefore, have no expenses. Investors cannot invest directly in the indices. |

| † | During the reporting period, all securities in the Argentina IMI were American Depositary Receipts (ADRs) denominated in U.S. dollars. |

| 4 | Emerging Markets Growth Fund |

While markets are likely to experience some volatility in the months ahead, we are identifying companies that are more closely tied to longer term secular growth trends in developing countries and those less affected by near-term trade tensions and risks to global growth.

In this environment, we are interested in businesses with stronger balance sheets and company-specific catalysts that can potentially drive future revenue and earnings growth regardless of macro uncertainty. Specific investment areas include growth of mobile services on internet-connected devices, widening demand for specialty semiconductors and an expanding Asian consumer class.

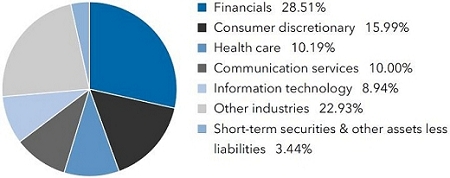

By sector, more than 28% of the fund’s net assets are invested in financials. Managers are focused on insurance providers targeting high-net-worth individuals in China and banks that can potentially benefit from specific regional factors, mostly in India, Russia and Southeast Asia. Holdings in consumer discretionary companies — including businesses involved in gaming, travel and online services — make up close to 16% of the portfolio.

Several large Chinese property developers are among the fund’s top holdings. Managers believe these companies have strong balance sheets and can readily access credit to fund new projects. They also trade at reasonable valuations based on our earnings growth projections. China has been loosening monetary policy and relaxing rules in the real estate market as part of a broader plan to sustain growth, and we believe these companies should benefit from these moves.

We also are looking closely at opportunities in Southeast Asia. Many global manufacturers are seeking to diversify capacity out of China, which could boost already solid domestic growth rates in several Southeast Asian countries.

We thank you for the trust you have placed in us and for your continued investment in the fund, and look forward to reporting to you again in six months.

Cordially,

Victor D. Kohn

President

August 19, 2019

About the fund and its adviser

Emerging Markets Growth Fund was organized in 1986 by the International Finance Corporation (IFC), an affiliate of the World Bank, as a vehicle for investing in the securities of companies based in developing countries. The premise behind the formation of the fund was that rapid growth in these countries could create very attractive investment opportunities. It also was felt that the availability of equity capital would stimulate the development of capital markets and encourage countries to liberalize their investment regulations.

Capital International, Inc., the fund’s investment adviser, is part of The Capital Group Companies,SMInc., one of the world’s most experienced investment advisory organizations, with roots dating back to 1931. The fund has been managed by Capital International or an affiliate since 1986. Capital Group employs a research-driven approach to investing and has a global investment research network spanning three continents. This network of analysts and portfolio managers travels the world, scrutinizing thousands of companies and keeping a close watch on industry trends and government actions.

Capital Group has devoted substantial resources to the task of evaluating and managing investments in developing countries. It is an intensive effort that combines company and industry analysis with broader political and macroeconomic views. We believe that our extensive worldwide research capabilities and integrated global investment process continue to provide Emerging Markets Growth Fund with a competitive edge.

| Emerging Markets Growth Fund | 5 |

The value of a long-term investment

How a $10,000 investment has grown (for the period December 31, 1987, to June 30, 2019, with distributions reinvested)

This chart shows how a $10,000 investment in Emerging Markets Growth Fund (EMGF) grew from December 31, 1987 — the inception of the MSCI Emerging Markets IMI — through June 30, 2019, the end of the fund’s latest fiscal year.

| Total returns | ||||||||

| (with all distributions reinvested for periods ended June 30, 2019) | Cumulative total returns | Average annual total returns | ||||||

| 1 year | 4.71 | % | 4.71 | % | ||||

| 5 years | 15.52 | 2.93 | ||||||

| 10 years | 61.77 | 4.93 | ||||||

Results are for past periods and are not predictive of results for future periods. The results shown are before taxes on fund distributions and sale of fund shares. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, please call (800) 421-4989.

| * | Returns for the MSCI Emerging Markets Index were calculated using the MSCI Emerging Markets Index with gross dividends from December 31, 1987, to December 31, 2000, and with net dividends from January 1, 2001, to November 30, 2007, and using the MSCI EM IMI with net dividends thereafter. The indices are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. Source: MSCI. |

| † | For the period December 31, 1987 (inception of the MSCI Emerging Markets Index), through June 30, 1988. EMGF began operations on May 30, 1986. |

| 6 | Emerging Markets Growth Fund |

Investment portfolio June 30, 2019

| Industry sector diversification | Percent of net assets |

| Common stocks 95.08% | Shares | Value (000) | ||||||

| Asia-Pacific 73.27% | ||||||||

| China 32.12% | ||||||||

| Alibaba Group Holding Ltd. (ADR)1 | 178,721 | $ | 30,284 | |||||

| BOC Aviation Ltd. | 722,600 | 6,068 | ||||||

| Cansino Biologics Inc., Class H1 | 867,400 | 3,698 | ||||||

| China Gas Holdings Ltd. | 1,743,400 | 6,483 | ||||||

| China Merchants Bank Co., Ltd., Class H | 5,584,000 | 27,842 | ||||||

| China Oilfield Services Ltd., Class H | 10,043,339 | 9,938 | ||||||

| China Overseas Land & Investment Ltd. | 17,129,950 | 63,154 | ||||||

| China Overseas Property Holdings Ltd. | 4,281,000 | 2,230 | ||||||

| China Resources Land Ltd. | 10,284,787 | 45,291 | ||||||

| China Tower Corp. Ltd., Class H | 37,280,000 | 9,783 | ||||||

| CNOOC Ltd. (ADR) | 19,400 | 3,305 | ||||||

| Ctrip.com International, Ltd. (ADR)1 | 1,886,317 | 69,624 | ||||||

| ENN Energy Holdings Ltd. | 388,800 | 3,783 | ||||||

| Gree Electric Appliances, Inc. of Zhuhai, Class A | 904,556 | 7,244 | ||||||

| Hangzhou Tigermed Consulting Co., Ltd., Class A1 | 2,537,863 | 28,489 | ||||||

| Huazhu Group Ltd. (ADR) | 1,295,800 | 46,973 | ||||||

| Hutchison China MediTech Ltd. | 28,180 | 129 | ||||||

| Hutchison China MediTech Ltd. (ADR)1 | 1,101,967 | 24,243 | ||||||

| HUYA, Inc. (ADR)1 | 472,000 | 11,663 | ||||||

| IMAX China Holding, Inc. | 1,680,929 | 4,119 | ||||||

| Jiangsu Hengrui Medicine Co., Ltd., Class A | 6,707,406 | 64,454 | ||||||

| Kweichow Moutai Co., Ltd., Class A | 80,058 | 11,470 | ||||||

| Longfor Group Holdings Ltd. | 14,496,113 | 54,650 | ||||||

| Midea Group Co., Ltd., Class A | 857,316 | 6,473 | ||||||

| Noah Holdings Ltd., Class A (ADR)1 | 710,709 | 30,241 | ||||||

| Ping An Insurance (Group) Co. of China, Ltd., Class H | 3,832,700 | 46,022 | ||||||

| Shanghai Fosun Pharmaceutical (Group) Co., Ltd. Class H | 7,075,594 | 21,421 | ||||||

| Shanghai Pharmaceutical (Group) Co., Ltd., Class H | 1,940,423 | 3,815 | ||||||

| Sun Art Retail Group Ltd. | 1,863,000 | 1,765 | ||||||

| Tencent Holdings Ltd. | 1,693,300 | 76,431 | ||||||

| Yunnan Energy New Material Co., Ltd., Class A | 439,749 | 2,993 | ||||||

| 724,078 | ||||||||

| Hong Kong 9.25% | ||||||||

| AIA Group Ltd. | 7,748,000 | 83,562 | ||||||

| BeiGene, Ltd. (ADR)1 | 320,200 | 39,689 | ||||||

| Galaxy Entertainment Group Ltd. | 7,015,000 | 47,280 | ||||||

| Hong Kong Exchanges and Clearing Ltd. | 469,700 | 16,583 | ||||||

| Jardine Matheson Holdings Ltd. | 19,700 | 1,242 | ||||||

| MicroPort Scientific Corp. | 1,958,000 | 1,454 | ||||||

| NagaCorp Ltd. | 1,660,000 | 2,042 | ||||||

| Wynn Macau, Ltd. | 7,479,429 | 16,756 | ||||||

| 208,608 | ||||||||

| Emerging Markets Growth Fund | 7 |

| Common stocks (continued) | Shares | Value (000) | ||||||

| Asia-Pacific (continued) | ||||||||

| India 10.78% | ||||||||

| Axis Bank Ltd.1 | 95,792 | $ | 1,122 | |||||

| Bharti Airtel Ltd. | 4,323,742 | 21,713 | ||||||

| City Union Bank Ltd. | 2,273,376 | 7,181 | ||||||

| Colgate-Palmolive Ltd. | 143,916 | 2,351 | ||||||

| Godrej Consumer Products Ltd. | 266,758 | 2,563 | ||||||

| HDFC Bank Ltd. | 937,472 | 33,189 | ||||||

| HDFC Bank Ltd. (ADR) | 172,900 | 22,484 | ||||||

| Housing Development Finance Corp. Ltd. | 758,723 | 24,095 | ||||||

| ICICI Bank Ltd. | 2,506,601 | 15,872 | ||||||

| ICICI Bank Ltd. (ADR) | 1,817,470 | 22,882 | ||||||

| IndusInd Bank Ltd. | 930,745 | 19,019 | ||||||

| Info Edge (India) Ltd. | 289,350 | 9,420 | ||||||

| ITC Ltd. | 631,861 | 2,507 | ||||||

| Kotak Mahindra Bank Ltd. | 947,178 | 20,268 | ||||||

| Maruti Suzuki India Ltd. | 85,154 | 8,061 | ||||||

| Nestlé India Ltd. | 14,844 | 2,562 | ||||||

| TeamLease Services Ltd. | 384,017 | 16,388 | ||||||

| United Spirits Ltd.1 | 1,128,661 | 9,564 | ||||||

| Varun Beverages Ltd. | 137,932 | 1,892 | ||||||

| 243,133 | ||||||||

| Indonesia 6.70% | ||||||||

| Astra International Tbk PT | 52,832,600 | 27,861 | ||||||

| Bank Central Asia Tbk PT | 14,202,500 | 30,134 | ||||||

| Bank Mandiri (Persero) Tbk PT, Series B | 18,293,708 | 10,392 | ||||||

| Bank Rakyat Indonesia (Persero) Tbk PT | 50,856,000 | 15,695 | ||||||

| Elang Mahkota Teknologi Tbk PT | 44,370,000 | 24,183 | ||||||

| Indocement Tunggal Prakarsa Tbk PT | 1,231,100 | 1,743 | ||||||

| Matahari Department Store Tbk PT | 22,043,700 | 5,383 | ||||||

| PT Bank Tabungan Pensiunan Nasional Syariah Tbk1 | 76,979,200 | 18,799 | ||||||

| PT Surya Citra Media Tbk | 98,449,600 | 11,219 | ||||||

| Semen Indonesia (Persero) Tbk PT | 6,903,500 | 5,656 | ||||||

| 151,065 | ||||||||

| Philippines 2.21% | ||||||||

| Ayala Corp. | 599,340 | 10,458 | ||||||

| Bloomberry Resorts Corp. | 87,473,900 | 19,292 | ||||||

| International Container Terminal Services, Inc. | 7,010,776 | 20,033 | ||||||

| 49,783 | ||||||||

| Singapore 0.68% | ||||||||

| Yoma Strategic Holdings Ltd. | 53,677,805 | 15,274 | ||||||

| South Korea 4.78% | ||||||||

| Hugel, Inc.1 | 24,093 | 8,756 | ||||||

| Hyundai Motor Co. | 65,296 | 7,917 | ||||||

| NAVER Corp. | 34,970 | 3,453 | ||||||

| Samsung Electronics Co., Ltd. | 1,816,690 | 73,948 | ||||||

| Samsung Electronics Co., Ltd. (GDR)2 | 12,721 | 12,937 | ||||||

| SK hynix, Inc. | 13,159 | 792 | ||||||

| 107,803 | ||||||||

| Taiwan 5.17% | ||||||||

| CTCI Corp. | 527,100 | 785 | ||||||

| Delta Electronics, Inc. | 518,521 | 2,629 | ||||||

| Gourmet Master Co. Ltd.1 | 344,000 | 1,922 | ||||||

| MediaTek Inc. | 2,427,042 | 24,536 | ||||||

| Taiwan Semiconductor Manufacturing Co., Ltd. | 10,747,094 | 82,698 | ||||||

| Vanguard International Semiconductor Corp. | 1,855,000 | 3,894 | ||||||

| 116,464 | ||||||||

| Thailand 0.26% | ||||||||

| TISCO Financial Group PCL, foreign registered | 1,897,500 | 5,785 | ||||||

| 8 | Emerging Markets Growth Fund |

| Shares | Value (000) | |||||||

| Vietnam 1.32% | ||||||||

| Masan Group Corp.1 | 3,918,770 | $ | 13,957 | |||||

| Vinhomes JSC1 | 4,672,475 | 15,899 | ||||||

| 29,856 | ||||||||

| Total Asia-Pacific | 1,651,849 | |||||||

| Eastern Europe and Middle East 8.03% | ||||||||

| Hungary 0.21% | ||||||||

| Wizz Air Holdings PLC1 | 106,929 | 4,629 | ||||||

| Kingdom of Saudi Arabia 0.14% | ||||||||

| Al Rajhi Banking and Investment Corp., non-registered shares | 173,562 | 3,221 | ||||||

| Romania 0.15% | ||||||||

| OMV Petrom SA | 36,484,776 | 3,469 | ||||||

| Russian Federation 5.52% | ||||||||

| Aeroflot - Russian Airlines PJSC | 598,000 | 962 | ||||||

| Alrosa PJSC | 12,838,882 | 17,469 | ||||||

| Baring Vostok Capital Fund IV Supplemental Fund, LP1,3,4,5,6,7 | 42,979,418 | 14,948 | ||||||

| Baring Vostok Private Equity Fund IV, LP1,3,4,5,6,7 | 23,522,779 | 9,593 | ||||||

| Detsky Mir PJSC | 1,317,840 | 1,788 | ||||||

| Moscow Exchange MICEX-RTS PJSC | 2,555,209 | 3,643 | ||||||

| New Century Capital Partners, LP1,3,4,5,7 | 5,247,900 | 339 | ||||||

| Rosneft Oil Co. PJSC (GDR) | 1,351,500 | 8,852 | ||||||

| Sberbank of Russia PJSC | 2,419,579 | 9,128 | ||||||

| Sberbank of Russia PJSC (ADR) | 2,305,200 | 35,454 | ||||||

| TCS Group Holding PLC (GDR)2 | 89,723 | 1,759 | ||||||

| TCS Group Holding PLC (GDR) | 149,003 | 2,920 | ||||||

| Yandex NV, Class A1 | 461,335 | 17,531 | ||||||

| 124,386 | ||||||||

| Slovenia 0.40% | ||||||||

| Nova Ljubljanska banka dd (GDR) | 682,794 | 9,006 | ||||||

| Turkey 1.24% | ||||||||

| Akbank TAS1 | 23,730,163 | 27,867 | ||||||

| Aktas Elektrik Ticaret AS1,3,4 | 4,273 | — | 8 | |||||

| 27,867 | ||||||||

| United Arab Emirates 0.37% | ||||||||

| DP World PLC | 286,297 | 4,552 | ||||||

| First Abu Dhabi Bank PJSC, non-registered shares | 957,925 | 3,876 | ||||||

| 8,428 | ||||||||

| Total Eastern Europe and Middle East | 181,006 | |||||||

| Latin America 7.23% | ||||||||

| Argentina 0.48% | ||||||||

| Loma Negra Compania Industrial Argentina SA (ADR)1 | 927,779 | 10,855 | ||||||

| Brazil 4.31% | ||||||||

| BR Malls Participacoes SA, ordinary nominative | 277,800 | 1,037 | ||||||

| CCR SA, ordinary nominative | 5,322,589 | 18,934 | ||||||

| Centro de Imagem Diagnosticos SA | 2,395,348 | 8,995 | ||||||

| Cyrela Brazil Realty SA, ordinary nominative | 1,904,372 | 10,316 | ||||||

| ENGIE Brasil Energia SA, ordinary nominative (ADR) | 6 | — | 8 | |||||

| Estre Ambiental Inc.2,3 | 739,920 | 615 | ||||||

| Gerdau SA (ADR) | 923,500 | 3,592 | ||||||

| Hypera SA, ordinary nominative | 2,641,017 | 20,626 | ||||||

| Lojas Americanas SA, ordinary nominative | 1,320,377 | 4,532 | ||||||

| Nexa Resources SA | 766,900 | 7,355 | ||||||

| OdontoPrev SA, ordinary nominative | 850,700 | 4,045 | ||||||

| Omega Geracao SA1 | 813,500 | 5,063 | ||||||

| Emerging Markets Growth Fund | 9 |

| Common stocks (continued) | Shares | Value (000) | ||||||

| Latin America (continued) | ||||||||

| Brazil(continued) | ||||||||

| Petróleo Brasileiro SA (Petrobras), ordinary nominative (ADR) | 246,500 | $ | 3,838 | |||||

| Vale SA, ordinary nominative | 406,127 | 5,481 | ||||||

| Vale SA, ordinary nominative (ADR) | 198,623 | 2,670 | ||||||

| 97,099 | ||||||||

| Chile 0.13% | ||||||||

| Enel Américas SA | 385,191 | 68 | ||||||

| Enel Américas SA (ADR) | 324,275 | 2,876 | ||||||

| 2,944 | ||||||||

| Mexico 1.25% | ||||||||

| América Móvil, SAB de CV, Series L (ADR) | 1,707,046 | 24,855 | ||||||

| Fomento Económico Mexicano, SAB de CV | 350,600 | 3,397 | ||||||

| 28,252 | ||||||||

| Peru 1.06% | ||||||||

| Credicorp Ltd. | 103,928 | 23,790 | ||||||

| Total Latin America | 162,940 | |||||||

| Africa 3.55% | ||||||||

| Federal Republic of Nigeria 0.13% | ||||||||

| Guaranty Trust Bank PLC | 33,454,673 | 3,053 | ||||||

| South Africa 3.42% | ||||||||

| AngloGold Ashanti Ltd. | 177,884 | 3,208 | ||||||

| Dis-Chem Pharmacies Ltd. | 3,362,906 | 6,031 | ||||||

| Discovery Ltd. | 1,695,897 | 17,954 | ||||||

| JSE Ltd. | 1,462,835 | 14,540 | ||||||

| Mr Price Group Ltd. | 114,359 | 1,612 | ||||||

| Naspers Ltd., Class N | 76,355 | 18,537 | ||||||

| Shoprite Holdings Ltd. | 1,167,795 | 13,072 | ||||||

| Telkom SA SOC Ltd.1 | 328,519 | 2,150 | ||||||

| 77,104 | ||||||||

| Total Africa | 80,157 | |||||||

| Other markets 3.00% | ||||||||

| Australia 0.15% | ||||||||

| Oil Search Ltd. | 672,048 | 3,336 | ||||||

| Belgium 0.05% | ||||||||

| Anheuser-Busch InBev SA/NV | 13,957 | 1,235 | ||||||

| Denmark 0.59% | ||||||||

| Carlsberg A/S, Class B | 100,737 | 13,354 | ||||||

| France 0.16% | ||||||||

| Edenred SA | 70,590 | 3,601 | ||||||

| Portugal 0.12% | ||||||||

| Galp Energia, SGPS, SA, Class B | 167,130 | 2,570 | ||||||

| United Kingdom 0.89% | ||||||||

| Airtel Africa PLC1,9 | 10,346,700 | 8,909 | ||||||

| British American Tobacco PLC | 117,700 | 4,109 | ||||||

| PZ Cussons PLC | 1,258,120 | 3,419 | ||||||

| Sedibelo Platinum Mines Ltd.1,3,4 | 17,665,800 | 3,642 | ||||||

| 20,079 | ||||||||

| 10 | Emerging Markets Growth Fund |

| Shares | Value (000) | |||||||

| United States 1.04% | ||||||||

| Capital International Private Equity Fund IV, LP1,3,4,5,6,7,10 | 50,842,740 | $ | 107 | |||||

| MercadoLibre, Inc.1 | 33,458 | 20,469 | ||||||

| Samsonite International SA | 1,284,765 | 2,947 | ||||||

| 23,523 | ||||||||

| Total Other markets | 67,698 | |||||||

| Total common stocks (cost: $1,616,391,000) | 2,143,650 | |||||||

| Preferred securities 1.34% | ||||||||

| Latin America 1.34% | ||||||||

| Brazil 1.34% | ||||||||

| Azul SA, preference shares (ADR)1 | 48,100 | 1,608 | ||||||

| Cia. Energética de Minas Gerais - CEMIG, preferred nominative | 800,590 | 3,096 | ||||||

| GOL Linhas Aéreas Inteligentes SA, preferred nominative1 | 79,000 | 671 | ||||||

| GOL Linhas Aéreas Inteligentes SA, preferred nominative (ADR) | 714,800 | 12,066 | ||||||

| Lojas Americanas SA, preferred nominative | 722,600 | 3,099 | ||||||

| Petróleo Brasileiro SA (Petrobras), preferred nominative | 1,008,100 | 7,196 | ||||||

| Petróleo Brasileiro SA (Petrobras), preferred nominative (ADR) | 177,220 | 2,517 | ||||||

| 30,253 | ||||||||

| Total preferred securities (cost: $21,695,000) | 30,253 | |||||||

| Rights & warrants 0.14% | ||||||||

| Asia-Pacific 0.14% | ||||||||

| China 0.14% | ||||||||

| Fujian Kuncai Material Technology Co., Ltd., Class A, warrants, expire 20213 | 1,392,732 | 2,979 | ||||||

| Latin America 0.00% | ||||||||

| Chile 0.00% | ||||||||

| Enel Américas SA, rights, expire 2019 | 125,573 | 2 | ||||||

| Total rights & warrants (cost: $3,069,000) | 2,981 | |||||||

| Convertible bonds 0.00% | Principal amount (000) | |||||||

| Asia-Pacific 0.00% | ||||||||

| China 0.00% | ||||||||

| Fu Ji Food and Catering Services Holdings Ltd., convertible notes, 0% 20203,4,11 | CNY | 97,700 | — | 8 | ||||

| Total convertible bonds (cost: $0) | — | 8 | ||||||

| Short-term securities 2.93% | Shares | |||||||

| Money market investments 2.93% | ||||||||

| Capital Group Central Cash Fund | 661,408 | 66,134 | ||||||

| Total short-term securities (cost: $66,137,000) | 66,134 | |||||||

| Total investment securities 99.49 % (cost: $1,707,292,000) | 2,243,018 | |||||||

| Other assets less liabilities 0.51% | 11,540 | |||||||

| Net assets 100.00% | 2,254,558 | |||||||

| Emerging Markets Growth Fund | 11 |

Investments in affiliates

A company is an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings represent 5% or more of the outstanding voting shares of that company. In addition, Capital International Private Equity Fund IV, LP is considered an affiliate since this issuer has the same investment adviser as the fund. Further details on these holdings and related transactions during the year ended June 30, 2019, appear below.

| Beginning shares | Additions | Reductions | Ending shares | Net realized loss (000) | Net unrealized appreciation (depreciation) (000) | Dividend income (000) | Value of affiliates at 6/30/2019 (000) | |||||||||||||||||||||||||

| Common stocks 0.00% | ||||||||||||||||||||||||||||||||

| Other markets 0.00% | ||||||||||||||||||||||||||||||||

| Netherlands 0.00% | ||||||||||||||||||||||||||||||||

| International Hospital Corp. Holding NV, Class A1,12 | 609,873 | — | 609,873 | — | $ | (7,281 | ) | $ | 7,608 | $ | — | $ | — | |||||||||||||||||||

| United States 0.00% | ||||||||||||||||||||||||||||||||

| Capital International Private Equity Fund IV, LP1,3,4,5,6,7 | 50,842,740 | — | — | 50,842,740 | — | (81 | ) | — | 107 | |||||||||||||||||||||||

| 107 | ||||||||||||||||||||||||||||||||

| Convertible stocks 0.00% | ||||||||||||||||||||||||||||||||

| Other markets 0.00% | ||||||||||||||||||||||||||||||||

| Netherlands 0.00% | ||||||||||||||||||||||||||||||||

| International Hospital Corp. Holding NV, Series B, cumulative convertible preferred1,12 | 622,354 | — | 622,354 | — | (2,759 | ) | 3,093 | — | — | |||||||||||||||||||||||

| Total 0.00% | $ | (10,040 | ) | $ | 10,620 | $ | — | $ | 107 | |||||||||||||||||||||||

| 1 | Security did not produce income during the last 12 months. |

| 2 | Acquired in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities was $15,311,000, which represented .68% of the net assets of the fund. |

| 3 | Valued under fair value procedures adopted by authority of the board of directors. The total value of all such securities was $32,223,000, which represented 1.43% of the net assets of the fund. |

| 4 | Value determined using significant unobservable inputs. |

| 5 | Cost and market value do not include prior distributions to the fund from income or proceeds realized from securities held by the private equity fund. Therefore, the cost and market value may not be indicative of the private equity fund’s performance. For private equity funds structured as limited partnerships, shares are not applicable and therefore the fund’s interest in the partnership is reported. |

| 6 | Excludes an unfunded capital commitment representing an agreement which obligates the fund to meet capital calls in the future. Capital calls can only be made if and when certain requirements have been fulfilled; thus, the timing and the amount of such capital calls cannot readily be determined. |

| 7 | Acquired through a private placement transaction exempt from registration under the Securities Act of 1933. May be subject to legal or contractual restrictions on resale. Further details on these holdings appear below. |

| 8 | Amount less than one thousand. |

| 9 | Security has been authorized but has not yet been issued. |

| 10 | Represents an affiliated company as defined under the Investment Company Act of 1940. Capital International Private Equity Fund IV, LP is also considered an affiliate since this issuer has the same investment adviser as the fund. |

| 11 | Scheduled interest and/or principal payment was not received. |

| 12 | Unaffiliated issuer at 6/30/2019. |

| Private placement securities | Acquisition date(s) | Cost (000) | Value (000) | Percent of net assets | ||||||||||

| Baring Vostok Capital Fund IV Supplemental Fund, LP | 10/8/2007-1/8/2019 | $ | 35,988 | $ | 14,948 | .66 | % | |||||||

| Baring Vostok Private Equity Fund IV, LP | 4/25/2007-6/27/2019 | 17,760 | 9,593 | .43 | ||||||||||

| New Century Capital Partners, LP | 12/7/1995 | — | 339 | .02 | ||||||||||

| Capital International Private Equity Fund IV, LP | 3/29/2005 | 7,098 | 107 | .00 | ||||||||||

| Total private placement securities | 60,846 | 24,987 | 1.11 | % | ||||||||||

Key to abbreviations

ADR = American Depositary Receipts

CNY = Chinese yuan renminbi

GDR = Global Depositary Receipts

See notes to financial statements.

| 12 | Emerging Markets Growth Fund |

| Financial statements | |

| Statement of assets and liabilities | |

| at June 30, 2019 | (dollars in thousands) |

| Assets: | ||||||||

| Investment securities, at value: | ||||||||

| Unaffiliated issuers (cost: $1,700,194) | $ | 2,242,911 | ||||||

| Affiliated issuers (cost: $7,098) | 107 | $ | 2,243,018 | |||||

| Cash | 1,610 | |||||||

| Cash denominated in currencies other than U.S. dollars (cost: $23,990) | 24,088 | |||||||

| Receivables for: | ||||||||

| Sales of investments | 5,197 | |||||||

| Sales of fund’s shares | 30 | |||||||

| Dividends | 12,821 | |||||||

| Other | 10 | 18,058 | ||||||

| 2,286,774 | ||||||||

| Liabilities: | ||||||||

| Payables for: | ||||||||

| Purchases of investments | 26,843 | |||||||

| Repurchases of fund’s shares | 516 | |||||||

| Investment advisory services | 1,365 | |||||||

| Services provided by related parties | 2 | |||||||

| Directors’ deferred compensation | 1,623 | |||||||

| Non-U.S. taxes | 1,518 | |||||||

| Other | 349 | 32,216 | ||||||

| Net assets at June 30, 2019 | $ | 2,254,558 | ||||||

| Net assets consist of: | ||||||||

| Capital paid in on shares of capital stock | $ | 1,654,379 | ||||||

| Total distributable earnings | 600,179 | |||||||

| Net assets at June 30, 2019 | $ | 2,254,558 |

| (dollars and shares in thousands, except per-share amounts) |

| Total authorized capital stock — 2,000,000 shares, $.01 par value (280,250 total shares outstanding) |

| Net assets | Shares outstanding | Net asset value per share | ||||||||||

| Class M | $ | 2,205,593 | 274,157 | $ | 8.06 | |||||||

| Class F-3 | 44,247 | 5,506 | 8.05 | |||||||||

| Class R-6 | 4,718 | 587 | 8.05 | |||||||||

See notes to financial statements.

| Emerging Markets Growth Fund | 13 |

| Statement of operations | |

| for the year ended June 30, 2019 | (dollars in thousands) |

| Investment income: | ||||||||

| Income: | ||||||||

| Dividends (net of non-U.S. taxes of $4,307) | $ | 44,533 | ||||||

| Interest (net of non-U.S. taxes of $108) | 2,429 | $ | 46,962 | |||||

| Fees and expenses*: | ||||||||

| Investment advisory services | 17,009 | |||||||

| Transfer agent services | 5 | |||||||

| Administrative services | 10 | |||||||

| Reports to shareholders | 16 | |||||||

| Registration statement and prospectus | 76 | |||||||

| Directors’ compensation | 35 | |||||||

| Auditing and legal | 368 | |||||||

| Custodian | 1,148 | |||||||

| State and local taxes | — | † | ||||||

| Other | 182 | 18,849 | ||||||

| Net investment income | 28,113 | |||||||

| Net realized gain and unrealized depreciation: | ||||||||

| Net realized gain (loss) on: | ||||||||

| Investments (net of non-U.S. tax of $1,643): | ||||||||

| Unaffiliated issuers | 110,984 | |||||||

| Affiliated issuers | (10,040 | ) | ||||||

| Forward currency contracts | (2,510 | ) | ||||||

| Currency transactions | (585 | ) | 97,849 | |||||

| Net unrealized (depreciation) appreciation on: | ||||||||

| Investments (net of non-U.S. taxes of $401): | ||||||||

| Unaffiliated issuers | (46,627 | ) | ||||||

| Affiliated issuers | 10,620 | |||||||

| Currency translations | 1,936 | (34,071 | ) | |||||

| Net realized gain and unrealized depreciation | 63,778 | |||||||

| Net increase in net assets resulting from operations | $ | 91,891 |

| * | Additional information related to class-specific fees and expenses is included in the notes to financial statements. |

| † | Amount less than one thousand. |

See notes to financial statements.

| 14 | Emerging Markets Growth Fund |

| Statements of changes in net assets |

| (dollars in thousands) |

| Year ended June 30 | ||||||||

| 2019 | 2018 | |||||||

| Operations: | ||||||||

| Net investment income | $ | 28,113 | $ | 28,269 | ||||

| Net realized gain | 97,849 | 289,278 | ||||||

| Net unrealized depreciation | (34,071 | ) | (98,347 | ) | ||||

| Net increase in net assets resulting from operations | 91,891 | 219,200 | ||||||

| Distributions paid to shareholders | (47,816 | ) | (30,240 | ) | ||||

| Net capital share transactions | (282,868 | ) | (240,936 | ) | ||||

| Total decrease in net assets | (238,793 | ) | (51,976 | ) | ||||

| Net assets: | ||||||||

| Beginning of year | 2,493,351 | 2,545,327 | ||||||

| End of year | $ | 2,254,558 | $ | 2,493,351 | ||||

See notes to financial statements.

| Emerging Markets Growth Fund | 15 |

1. Organization

Emerging Markets Growth Fund, Inc. (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital and invests primarily in common stock and other equity securities of issuers in developing countries.

The fund has three share classes consisting of two retail share classes (Classes M and F-3), and one retirement plan share class (Class R-6). The retirement plan share class is generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described further in the following table:

| Share class | Initial sales charge | Contingent deferred sales charge upon redemption | Conversion feature | ||||

| Classes M* and F-3 | None | None | None | ||||

| Class R-6 | None | None | None |

| * | Class M shares of the fund are not available for purchase. |

Holders of all share classes have equal pro rata rights to the assets, dividends and liquidation proceeds of the fund. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, transfer agent and administrative services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the fund’s investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Subsequent events, if any, have been evaluated through the date of issuance in the preparation of the financial statements. The fund follows the significant accounting policies described in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income— Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations— Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, transfer agent and administrative services, are charged directly to the respective share class.

Distributions paid to shareholders— Income dividends and capital gain distributions are recorded on the ex-dividend date.

Currency translation— Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments in the fund’s statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

Shares redeemed— The fund normally redeems shares in cash; however, under certain conditions and circumstances, payment of the redemption price wholly or partly with portfolio securities or other fund assets may be permitted. A redemption of shares in-kind is based upon the closing value of the shares being redeemed as of the trade date. Realized gains/losses resulting from redemptions of shares in-kind are reflected separately in the statement of operations.

| 16 | Emerging Markets Growth Fund |

3. Valuation

Capital International, Inc. (“CIInc”), the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs— The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs | |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) | |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer | |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or deemed to be not representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. The Capital Group Central Cash Fund (“CCF”) is valued based upon a floating net asset value, which fluctuates with changes in the value of CCF’s portfolio securities. The underlying securities are valued based on the policies and procedures in CCF’s statement of additional information. Forward currency contracts are valued at the mean of representative quoted bid and ask prices, generally based on prices supplied by one or more pricing vendors.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of directors as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure— The fund’s board of directors has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment

| Emerging Markets Growth Fund | 17 |

adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of directors. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications— The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following table presents the fund’s valuation levels as of June 30, 2019 (dollars in thousands):

| Investment securities | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: | ||||||||||||||||

| Common stocks: | ||||||||||||||||

| Asia-Pacific | $ | 1,651,849 | $ | — | $ | — | $ | 1,651,849 | ||||||||

| Eastern Europe and Middle East | 157,361 | — | 24,880 | 182,241 | ||||||||||||

| Latin America | 162,325 | 615 | — | 162,940 | ||||||||||||

| Africa | 80,157 | — | — | 80,157 | ||||||||||||

| Other markets | 62,714 | — | 3,749 | 66,463 | ||||||||||||

| Preferred securities | 30,253 | — | — | 30,253 | ||||||||||||

| Rights & warrants | 2 | 2,979 | — | 2,981 | ||||||||||||

| Convertible bonds | — | — | — | 1 | — | 1 | ||||||||||

| Short-term securities | 66,134 | — | — | 66,134 | ||||||||||||

| Total | $ | 2,210,795 | $ | 3,594 | $ | 28,629 | $ | 2,243,018 | ||||||||

| 1 | Amount less than one thousand. |

The following table reconciles the valuation of the fund’s Level 3 investment securities and related transactions for the year ended June 30, 2019 (dollars in thousands):

| Beginning value at 1/1/2019 | Transfers into Level 32 | Purchases | Sales | Net realized loss3 | Unrealized depreciation3 | Transfers out of Level 32 | Ending value at 6/30/2019 | |||||||||||||||||||||||||

| Private equity funds | $ | 32,620 | $ | — | $ | 4,888 | $ | — | $ | — | $ | (12,521 | ) | $ | — | $ | 24,987 | |||||||||||||||

| Other securities | 12,348 | 13,782 | 1,252 | (1,474 | ) | (10,040 | ) | (2,948 | ) | (9,278 | ) | 3,642 | ||||||||||||||||||||

| Total | $ | 44,968 | $ | 13,782 | $ | 6,140 | $ | (1,474 | ) | $ | (10,040 | ) | $ | (15,469 | ) | $ | (9,278 | ) | $ | 28,629 | ||||||||||||

| Net unrealized depreciation during the period on Level 3 investment securities held at June 30, 2019 | $ | (9,712 | ) | |||||||||||||||||||||||||||||

| 2 | Transfers into or out of Level 3 are based on the beginning market value of the quarter in which they occurred. |

| 3 | Net realized loss and unrealized depreciation are included in the related amounts on investments in the statement of operations. |

Unobservable inputs— Valuation of the fund’s Level 3 securities is based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The fund owns an interest in multiple private equity funds, which are considered alternative investments and are classified as Level 3 investment securities. The private equity funds are fair valued using the net asset value based on the fund’s financial statements adjusted for known company or market events, updated market pricing for underlying securities, and/or fund transactions (i.e., drawdowns and distributions) and may include other unobservable inputs.

| 18 | Emerging Markets Growth Fund |

The other unobservable inputs used in the fair value measurements of the fund’s private equity investments are directional adjustments based on relevant market data (such as significant movement of a country-specific exchange-traded fund or index after the financial statement date of the private equity fund). Significant increases (decreases) of these inputs could result in significantly higher (lower) fair valuation. There were no other unobservable inputs as of June 30, 2019.

The following table provides additional information used by the fund’s investment adviser to fair value the fund’s Level 3 securities (dollars in thousands):

| Investment strategy | Fair Value | Unfunded commitment* | Remaining life† | Redemption terms | Unobservable input | Range | |||||||||||||

| Private equity funds | Primarily private sector equity investments (i.e., expansion capital, buyouts) in emerging markets | $ | 24,987 | $ | 2,310 | ≤ 0 to 2 years | Redemptions are not permitted. These funds distribute proceeds from the liquidation of underlying assets of the funds. | Market index adjustment | 0 to 15% | ||||||||||

| * | Unfunded capital commitments represent agreements which obligate the fund to meet capital calls in the future. Payment would be made when a capital call is requested. Capital calls can only be made if and when certain requirements have been fulfilled; thus, the timing of such capital calls cannot readily be determined. |

| † | Represents the remaining life of the fund term or the estimated period of liquidation. |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions— The prices of, and the income generated by, the common stocks and other securities held by the fund may decline –sometimes rapidly or unpredictably – due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental, governmental agency or central bank responses to economic conditions; and currency exchange rate, interest rate and commodity price fluctuations.

Issuer risks— The prices of, and the income generated by, securities held by the fund may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance, major litigation related to the issuer, changes in government regulations affecting the issuer or its competitive environment and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiatives.

Investing in growth-oriented stocks— Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments. These risks may be even greater in the case of smaller capitalization stocks.

Investing outside the U.S.— Securities of issuers domiciled outside the U.S., or with significant operations or revenues outside the U.S., may lose value because of adverse political, social, economic or market developments (including social instability, regional conflicts, terrorism and war) in the countries or regions in which the issuers operate or generate revenue. These securities may also lose value due to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Issuers of these securities may be more susceptible to actions of foreign governments, such as nationalization, currency blockage or the imposition of price controls or punitive taxes, each of which could adversely impact the value of these securities. Securities markets in certain countries may be more volatile and/or less liquid than those in the U.S. Investments outside the U.S. may also be subject to different accounting practices and different regulatory, legal and reporting standards and practices, and may be more difficult to value, than those in the U.S. In addition, the value of investments outside the U.S. may be reduced by foreign taxes, including foreign withholding taxes on interest and dividends. Further, there may be increased risks of delayed settlement of securities purchased or sold by the fund. The risks of investing outside the U.S. may be heightened in connection with investments in developing countries.

Investing in developing countries— Investing in countries with developing economies and/or markets may involve risks in addition to and greater than those generally associated with investing in the securities markets of developed countries. For instance, emerging market countries may have less developed legal and accounting systems than those in developed countries. The governments of these countries may be less stable and more likely to impose capital controls, nationalize a company or industry, place restrictions on foreign ownership and on withdrawing sale proceeds of securities from the country, and/or impose punitive taxes that could adversely affect the prices of securities. In addition, the economies of these countries may be dependent on relatively few industries that are more susceptible to local and global changes. Securities markets in these countries can also be relatively small and have substantially lower trading volumes. As a result, securities issued in these countries may be more volatile and less liquid, and may be more difficult to value, than securities issued

| Emerging Markets Growth Fund | 19 |

in countries with more developed economies and/or markets. Less certainty with respect to security valuations may lead to additional challenges and risks in calculating the fund’s net asset value. Additionally, emerging markets are more likely to experience problems with the clearing and settling of trades and the holding of securities by banks, agents and depositories that are less established than those in developed countries.

Investing in small companies— Investing in smaller companies may pose additional risks. For example, it is often more difficult to value or dispose of small company stocks and more difficult to obtain information about smaller companies than about larger companies. Furthermore, smaller companies often have limited product lines, operating histories, markets and/or financial resources, may be dependent on one or a few key persons for management, and can be more susceptible to losses. Moreover, the prices of their stocks may be more volatile than stocks of larger, more established companies, particularly during times of market turmoil.

Management— The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses, including models, tools and data, employed by the investment adviser in this process may be flawed or incorrect and may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

5. Certain investment techniques

Forward currency contracts— The fund has entered into forward currency contracts, which represent agreements to exchange currencies on specific future dates at predetermined rates. The fund’s investment adviser uses forward currency contracts to manage the fund’s exposure to changes in exchange rates. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from possible movements in exchange rates.

On a daily basis, the fund’s investment adviser values forward currency contracts and records unrealized appreciation or depreciation for open forward currency contracts in the fund’s statement of assets and liabilities. Realized gains or losses are recorded at the time the forward currency contract is closed or offset by another contract with the same broker for the same settlement date and currency.

Closed forward currency contracts that have not reached their settlement date are included in the respective receivables or payables for closed forward currency contracts in the fund’s statement of assets and liabilities. Net realized gains or losses from closed forward currency contracts and net unrealized appreciation or depreciation from open forward currency contracts are recorded in the fund’s statement of operations. As of June 30, 2019, the fund did not have any open forward currency contracts. The average month-end notional amount of open forward currency contracts while held was $152,181,000.

The following table identifies the effect on the fund’s statement of operations resulting from the fund’s use of forward currency contracts for the year ended, June 30, 2019 (dollars in thousands):

| Net realized loss | Net unrealized appreciation | |||||||||||||

| Contracts | Risk type | Location on statement of operations | Value | Location on statement of operations | Value | |||||||||

| Forward currency | Currency | Net realized loss on forward currency contracts | $ | (2,510 | ) | Net unrealized appreciation on forward currency contracts | $ | — | ||||||

6. Taxation and distributions

Federal income taxation— The fund complies with the requirements under Subchapter M of the Internal Revenue Code applicable to mutual funds and intends to distribute substantially all of its net taxable income and net capital gains each year. The fund is not subject to income taxes to the extent such distributions are made. Therefore, no federal income tax provision is required.

As of and during the period ended June 30, 2019, the fund did not have a liability for any unrecognized tax benefits. The fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the fund did not incur any significant interest or penalties.

The fund’s tax returns are not subject to examination by federal, state and, if applicable, non-U.S. tax authorities after the expiration of each jurisdiction’s statute of limitations, which is generally three years after the date of filing but can be extended in certain jurisdictions.

Non-U.S. taxation— Dividend and interest income are recorded net of non-U.S. taxes paid. The fund may file withholding tax reclaims in certain jurisdictions to recover a portion of amounts previously withheld. As a result of rulings from European courts, the fund filed for

| 20 | Emerging Markets Growth Fund |

additional reclaims related to prior years. These reclaims are recorded when the amount is known and there are no significant uncertainties on collectability. Gains realized by the fund on the sale of securities in certain countries, if any, may be subject to non-U.S. taxes. If applicable, the fund records an estimated deferred tax liability based on unrealized gains to provide for potential non-U.S. taxes payable upon the sale of these securities.

Distributions— Distributions paid to shareholders are based on net investment income and net realized gains determined on a tax basis, which may differ from net investment income and net realized gains for financial reporting purposes. These differences are due primarily to different treatment for items such as currency gains and losses; short-term capital gains and losses; capital losses related to sales of certain securities within 30 days of purchase; unrealized appreciation of certain investments in securities outside the U.S.; deferred expenses; cost of investments sold; net capital losses; non-U.S. taxes on capital gains and income on certain investments. The fiscal year in which amounts are distributed may differ from the year in which the net investment income and net realized gains are recorded by the fund for financial reporting purposes. The fund may also designate a portion of the amount paid to redeeming shareholders as a distribution for tax purposes.

During the year ended June 30, 2019, the fund reclassified $1,778,000 from total distributable earnings to capital paid in on shares of beneficial interest to align financial reporting with tax reporting. The fund also utilized capital loss carryforward of $20,101,000.

As of June 30, 2019, the tax basis components of distributable earnings, unrealized appreciation (depreciation) and cost of investments were as follows (dollars in thousands):

| Undistributed ordinary income | $ | 13,749 | ||

| Undistributed long-term capital gains | 58,165 | |||

| Gross unrealized appreciation on investments | 662,966 | |||

| Gross unrealized depreciation on investments | (132,784 | ) | ||

| Net unrealized appreciation on investments | 530,182 | |||

| Cost of investments | 1,712,836 |

Distributions paid were characterized for tax purposes as follows (dollars in thousands):

| Year ended June 30, 2019 | Year ended June 30, 2018 | |||||||||||||||||||||||

| Share class | Ordinary income | Long-term capital gains | Total distributions paid | Ordinary income | Long-term capital gains | Total distributions paid | ||||||||||||||||||

| Class M | $ | 27,966 | $ | 19,452 | $ | 47,418 | $ | 30,206 | $ | — | $ | 30,206 | ||||||||||||

| Class F-3* | 233 | 165 | 398 | 34 | — | 34 | ||||||||||||||||||

| Class R-6* | — | † | — | † | — | † | — | † | — | — | † | |||||||||||||

| Total | $ | 28,199 | $ | 19,617 | $ | 47,816 | $ | 30,240 | $ | — | $ | 30,240 | ||||||||||||

| * | Class F-3 and R-6 shares began investment operations on September 1, 2017. |

| † | Amount less than one thousand. |

7. Fees and transactions with related parties