| OMB APPROVAL |

OMB Number: 3235-0570 Expires: August 31, 2020 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-04750 | |

| Fenimore Asset Management Trust |

| (Exact name of registrant as specified in charter) |

| 384 North Grand Street, P.O. Box 399 Cobleskill, New York | 12043 |

| (Address of principal executive offices) | (Zip code) |

Thomas O. Putnam

| Fenimore Asset Management Trust 384 North Grand Street, P.O. Box 399 Cobleskill, New York, 12043 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | 1-800-453-4392 | |

| Date of fiscal year end: | December 31 | |

| | | |

| Date of reporting period: | December 31, 2018 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting the Funds at 1-800-932-3271 or, if you own these shares through a financial intermediary, by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at 1-800-932-3271. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the fund complex or at your financial intermediary.

Table of Contents

Chairman’s Commentary | 1 |

FAM Value Fund | |

Letter to Shareholders | 4 |

Performance Summary | 10 |

Portfolio Data | 13 |

Schedule of Investments | 14 |

FAM Equity-Income Fund | |

Letter to Shareholders | 18 |

Performance Summary | 24 |

Portfolio Data | 27 |

Schedule of Investments | 28 |

FAM Small Cap Fund | |

Letter to Shareholders | 31 |

Performance Summary | 37 |

Portfolio Data | 40 |

Schedule of Investments | 41 |

Statements of Assets and Liabilities | 44 |

Statements of Operations | 45 |

Statements of Changes in Net Assets | 46 |

Notes to Financial Statements | 49 |

Report of Independent Registered Public Accounting Firm | 65 |

Board Consideration of the Continuation of the Investment Advisory Agreements for the Funds | 67 |

Information About Trustees and Officers | 72 |

Expense Data | 75 |

Supplemental Information | 77 |

Privacy Policy | 79 |

FAM Funds has adopted a Code of Ethics that applies to its principal

executive and principal financial officers. You may obtain a copy of this Code

without charge, by calling FAM Funds at (800) 932-3271.

Chairman’s Commentary

December 31, 2018

Dear Fellow Shareholder,

We began last year’s annual letter by recounting a Wall Street Journal article that described 2017 as “the year pretty much everything went up.” The opposite was true this year – 2018 could aptly be described as “the year pretty much everything went down.” 2017’s celebration of coordinated global growth turned to fears of a global slowdown. Safe-haven assets such as U.S. Treasuries were among the few winners. The total return of U.S. stocks as measured by the S&P 500, an index of the 500 largest corporations, was -4.38%. Smaller companies, as measured by the Russell 2000 Index, fared worse returning -11.01%.1

Within this context, we believe that FAM Funds performed well (please see individual fund letters for details). A standout was the FAM Equity-Income Fund, which outperformed most funds and indices during the year. A down year such as 2018 is not a surprise given the strength of equity markets in all but one of the last six years. And, for us, it is not disheartening either. As we had written a year ago, price-earnings multiples coming into 2018 were becoming stretched and opportunities were few. Today, the opposite is true. Valuations are becoming reasonable and opportunities plentiful. While there may be more fear in the markets, we at FAM Funds are becoming more excited.

Volatility  Opportunity

Opportunity

If investors were asked to describe the domestic stock markets in 2018 using only one word, many might say “volatile” (partially because you could not escape this word in the financial press). The placid 2017 market carried over into a very strong January of 2018. Then fears of inflation and rising interest rates caused investors to reassess the earnings growth and valuations of businesses, creating a surge in volatility through May. Things calmed down over the summer as the S&P 500 climbed to new highs on September 20. Along the way, on August 22, it was crowned the longest bull market in history at 3,453 days. No sooner had the coronation celebration ended when investors became fearful of a global slowdown and escalating trade wars. By the end of December, the longest running bull market threatened to give way to a bear market.

Opportunity  Activity

Activity

Long-term shareholders and those who have read our literature know that while downside volatility is not fun, FAM Funds embraces it rather than fears it. How? One insight crucial to embracing turbulent markets is that price does not equal value. The stock prices of many wonderful companies fell 30% or more in 2018, but we estimate that in most of these cases their value did not. This created an opportunity for long-term investors such as

1

Chairman’s Commentary

us. Similar to the shoppers who get excited when prices of ultra-high-definition television sets are marked down 30% on Black Friday, we get excited when market leading, highly profitable, growing, well-capitalized businesses trade 30% cheaper.

Our team used this environment of improving opportunities to enhance, in our opinion, the collective quality and expected return of our funds. Between the three funds, we took ownership stakes in 11 new businesses ranging from dental/medical distributors and label makers to faucet manufacturers and the company responsible for your neon orange fingers after eating a bag of CHEETOS®. We believe these are good firms and have long admired them, but we estimated that they were too expensive to offer us an adequate margin of safety. As volatility picked up through the year, more of these long admired and perennially expensive “wish list” companies began approaching attractive valuations. We hope to buy shares of more of these in 2019! Additionally, we added to many existing positions.

Preparation  Opportunity

Opportunity

Warren Buffett’s business partner Charlie Munger, paraphrasing Louis Pasteur, said, “Opportunity comes to the prepared mind.” We agree. The seven members of your investment research team spent countless hours on the road in 2018 visiting the management teams of companies we are either already invested in or assessing for future ownership. In addition, our analysts talked to hundreds of management teams over the phone. All these conversations, more than 275 in all, become tiles in the mosaic of opportunities and threats on the investment landscape. We get a better picture of the prospects for each enterprise, their competitors, and businesses in associated industries. Each interaction adds to the mosaic and helps us refine our investment opportunity set and outlook.

From company managements, we heard recurring concerns about tariffs and inflation in 2018. However, we heard much optimism about the ability to grow revenue (organically and by acquisition), improve profitability, invest in future growth, and return capital to us – the owners. Indeed, the median 2019 estimated revenue growth rate for all our fund holdings is approximately 5%, on top of nearly 7% in 2018. Median earnings per share growth in 2019 is expected to be more than 8%, after 20% tax-reform-infused growth in 2018.2 These are healthy numbers that reflect the optimism heard from many management teams. Some could certainly fall short of these expectations because growth is not as easy to achieve as in years past. But many could, in our opinion, continue to grow their earnings power and drive increases in per share value.

2

Chairman’s Commentary

Outlook

Though the FAM Funds team is optimistic, we do not have our heads in the sand. Your team is monitoring the trade issue and ability of our holdings to protect profit margins if the trade war intensifies or lingers on while watching for signs of a protracted downturn in China. We are also paying close attention to inflationary pressures on wages, raw materials, and other operating expenses such as transportation. Most of our holdings’ leaders have thus far been able to reduce the effects of these dynamics by a combination of raising prices, making operational improvements, and rerouting supply chains. Though optimistic, we are on the lookout for signs of a significant economic slowdown. If one occurs, investing in market leading, conservatively capitalized, and well-run businesses should serve us well as it has since we first opened our doors.

Please call us at 800-932-3271 if you have questions or need some reassurance. We also welcome you to visit us in our Albany or Cobleskill offices. Thank you for the ongoing trust and confidence that you place in us.

Thomas O. Putnam, Chairman

Research Team

Andrew F. Boord

John D. Fox, CFA

Kevin D. Gioia,CFA

Paul C. Hogan, CFA

William W. Preston, CFA

Drew P. Wilson, CFA

The opinions expressed herein are those of the portfolio managers as of the date of the report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

3

FAM Value Fund

December 31, 2018

Dear Fellow Value Fund Shareholder,

In 2018, most investments declined with U.S. stocks, international stocks, real estate, and some bonds providing a negative return for the year. It was the opposite of 2017 when these asset classes produced positive returns overall.1 In this difficult environment, the FAM Value Fund declined -6.18% for the year. This was a little better than the Fund’s primary benchmark, the Russell Midcap Index, which declined -9.06%.1 As 2018 was the FAM Value Fund’s 32nd year, we have experience in many different market environments. During this time, the Fund has declined nine of those years, a little less than one-third of the time. The table below shows the calendar years and the amount of the annual decline.

Year | Annual Return | Year | Annual Return | Year | Annual Return |

1987 | -17.2% | 2002 | -5.3% | 2011 | -0.4% |

1990 | -5.4% | 2007 | -0.8% | 2015 | -1.7% |

1999 | -4.8% | 2008 | -28.7% | 2018 | -6.2% |

Of course, every decline is a little different and the bear market of 2018 came on suddenly after stock prices hit a number of all-time highs during the year. It may be hard to remember that the Dow Jones Industrial Average closed at more than 25,000 for the first time in January.1 Given the speed of the decline, we are being asked the question, “What’s happening in the market?” Our thought is that the combination of slowing worldwide eco- nomic growth and high stock valuations has contributed to a fall in prices. The point about high valuations is important. We have been concerned about valuations for a couple years. The sentences below were written two years ago in the 2016 FAM Value Fund Annual Letter:

“The net result of these trends could be a record year for corporate earnings. We should point out that the stock market has already anticipated this good news. The price to earnings ratio on the S&P 500 Index is the highest in more than a decade and many individual stocks that we look at are trading at, or above, our estimate of fair value.”

When we wrote these words, the U.S. stock market, defined as the S&P 500 Index, was trading at 18.8 times trailing earnings compared to a long-term average of 17.7 times. By the end of calendar year 2017, the multiple of earnings was even higher at 20 times.1 In short, investors were willing to pay a high multiple for corporate earnings due to low interest rates and expectations of strong future growth. Using the weather as an analogy, many investors were expecting blue skies forever. Now, with some storm clouds brewing, they are likely re-

4

FAM Value Fund

evaluating their outlook. These clouds include slower economic growth in China and Europe, political uncertainty around the world, and concerns about the future level of interest rates in the United States. If there is a silver lining in these clouds, it is the fact that stocks are a much better value today and we are finding more investment opportunities.

To illustrate this point, in the first nine months of the year we made only one significant investment, a purchase in Henry Schein (HSIC). In addition, we made small purchases in three existing holdings. During this time, the portfolio’s cash balance drifted up to nearly 10% of the Fund’s assets. Since September 30, we have invested more than $85 million in two new stocks and several existing holdings (please see the Portfolio Activity section for details).

When we tell people that our investment team has been fairly active in the market the immediate question is usually, “Well what are you buying?” The answer to that question is consistent over time. While the company names change in any particular year, we continue to execute our investment philosophy and process. Our philosophy can be summed up in the idea of intrinsic value. We believe that every asset – be it a bond, a piece of real estate, or a company – has a value that is “intrinsic” to that asset. A share of stock represents a fractional ownership in a business. The value of that business comes from the amount of cash it produces and the rate of growth in that cash flow into the future. If you know those two variables, it is fairly easy to figure out what a firm is worth. Of course, making accurate projections about the future is difficult. As a result, we build some guardrails into our investment process to protect us if our forecasts are wrong.

Our process revolves around four core criteria that we seek:

| | 1. | A good business that is growing and protected by some competitive advantage |

| | 2. | A strong financial position with low debt, high profit margins, cash profits, and high returns on capital |

| | 3. | An excellent management team that exhibits both honesty and the ability to allocate capital |

| | 4. | A purchase price that is below what we think the stock is worth |

Once we purchase a stock, we follow it closely and try to meet with the management team face-to-face at least once a year. We also monitor the price to value relationship over time. As long as the stock does not become significantly overvalued, we tend to hold onto our stocks for many years. This long-term view is reflected in the Fund’s low turnover ratio which is significantly lower than the mutual fund industry average. One benefit of a long holding period is that when we do sell a stock and realize a capital gain, it is usually a long-term gain which is taxed at a lower rate than a short-term gain.

5

FAM Value Fund

Portfolio Activity

Purchases

During the first nine months of the year, we purchased one new position and added a small amount to three existing holdings: Air Products & Chemicals (APD), Dollar General Corp. (DG), and Mohawk Industries (MHK).

As mentioned above, the new holding from early 2018 is Henry Schein (HSIC). Schein is a distributor of dental, medical, and veterinary products to office-based practices. The main product categories are consumables, equipment, and software. It is a global enterprise with one-third of their sales outside of the United States. We have long admired Schein and their management. The corporation has a long track record of success with a 10-year sales growth rate of almost 8% per year and eight consecutive years of earnings per share growth.2 This strong performance has been reflected in the valuation of Schein’s stock. Over the last 10 years, the stock has had an average price-earnings ratio of nearly 19 times earnings and has regularly traded above 20 times earnings.3 Given uncertainty in the distribution industry, we were able to purchase the stock in the first quarter at less than 17 times earnings.

Since our purchase, the company has reported solid earnings with positive organic sales growth in all six of their segments. In addition, management is taking steps to unlock shareholder value through the creation of a software joint venture and the spin out of their veterinary business into a separate firm. While there are questions about the role of distributors in the dental industry going forward, we believe Schein’s lead over the other players and the proactive moves by management could result in a higher stock price.

In the fourth quarter, we were very active adding to 13 existing holdings and purchasing one significant new position, Avery Dennison Corp. (AVY). The existing buys covered a number of industries including banking, energy, and industrials. In each case we believe the stock was selling at a price that was below the true intrinsic value of the company. With several purchases in the last quarter, the Fund’s cash is down to 5.49% of assets. We believe the future returns on these purchases should be much higher than the returns on cash over the long term.

Based on sales and market share, Avery Dennison is the leader in manufacturing pressure-sensitive labels. These labels are used on thousands of products from bottles to automotive tires. Avery’s size and 40% market share give them an advantage over their competitors in product pricing and delivery.4 Management has done an excellent job in growing the operation and profit margins over time. We estimate that the return on invested capital is above 15% and that Avery generates significantly more cash than is needed to grow the business. We purchased the stock after it declined more than 25% from its high price.

2 | Henry Schein 2017 Annual Report |

4 | Avery Dennison 2017 Annual Report |

6

FAM Value Fund

Sales

There were three significant sales during the year.

When the market was roaring in January, we sold our entire position in Loews Corp. (L) after a 40% increase in the stock price over the last two years. Loews is a holding company in New York City managed by the Tisch family. The enterprise has five primary assets and a liquid investment portfolio, so it is fairly simple to add up the value of the pieces and determine a per share value. The challenge has been that the public stock price has typically traded at a significant discount to the sum of the parts. We believed this was due to management’s poor capital allocation decisions. After observing management’s choices over a few years, we determined the value of the business was growing at only a modest rate and that it was unlikely that the discount to fair value would close.

Our longtime real estate investment, Forest City Realty Trust (FCE.A), was acquired by another one of our holdings for $25.35 in cash. We valued Forest City at $25 a share and made a substantial purchase in 2016 at below $19 a share. Our value was confirmed this summer when one of our holdings, Brookfield Asset Management, offered $25.35 to acquire it. The acquisition closed in December and we were able to redeploy the cash proceeds into other investments.

Finally, we sold the majority of our shares in the advertising agency Interpublic Group of Companies (IPG). We originally purchased the stock in April of 2012 when IPG was the operating laggard among the four, global advertising holding companies. These firms are in the flow of most advertising dollars spent around the world helping organizations with creative ideas, purchasing advertising time, and developing campaigns. Historically, these were great businesses as agencies earned a commission on every dollar spent by advertisers to promote their products. IPG was the laggard, but we thought the problems were solvable by a new management team. We were right. The new team fixed the balance sheet and increased profit margins over the last six years. The stock price doubled over this time. In the last few years, we have been questioning the ad agency business model given the amount of new competition and disruption in the industry. The emergence of new competitors such as Google and Facebook may have changed the game for the traditional advertising model. In addition to our concerns about competition, IPG made a large acquisition funded in part by increased debt. This added to our concern and we sold almost all of our shares.

Closing Thoughts

After a very quiet 2017, stock prices swung wildly in 2018’s fourth quarter. Given the recent twists and turns in stock prices, it seems more perilous than usual to make a prediction about 2019. With all the normal caveats about predicting the future, this is what we are seeing today. Corporate news and economic data released the first week of January indicate

7

FAM Value Fund

that the global economy is slowing and expectations about earnings for 2019 may be too high. We should learn much more in the third week of January when companies begin to report their financial results.

In the meantime, the Fund’s holdings are generating considerable cash profits that can be used for investment, acquisitions, dividends, or stock buybacks. We think we have invested in management teams that can use these cash profits wisely and create value per share. The recent decline in stock prices has created more opportunities to purchase shares in well-run operations at a discount to what we think they are worth. After a few years of writing about fair to high valuations and limited opportunities, we see good opportunities to invest in what we believe to be great businesses at attractive prices.

Thank you for investing with us in the FAM Value Fund.

Best & Worst Performers for 2018

Best Performers | Worst Performers |

CDW Corp. | 0.95% | Mohawk Industries | -2.13% |

AutoZone | 0.67% | Illinois Tool Works | -0.85% |

Interpublic Group of Companies | 0.46% | MEDNAX | -0.69% |

Brown & Brown | 0.36% | South State Corp. | -0.64% |

Henry Schein | 0.30% | EOG Resources | -0.63% |

This reflects the FAM Value Fund’s best and worst performers, in descending order, based on individual stock performance. Past performance does not indicate future results.

8

FAM Value Fund

Performance (as of 12/31/18)

| | 1-Year | 3-Year | 5-Year | 10-Year | Since Inception 1/2/1987 |

FAM Value Fund Investor Shares | -6.18% | 8.26% | 7.18% | 11.55% | 10.08% |

Russell Midcap Index | -9.06% | 7.04% | 6.26% | 14.03% | 11.04% |

S&P 500 Index | -4.38% | 9.26% | 8.49% | 13.12% | 10.02% |

Past performance does not indicate future results.

|

|  |

John D. Fox, CFA

Co-Manager | Thomas O. Putnam

Co-Manager | Drew P. Wilson, CFA

Co-Manager |

The opinions expressed herein are those of the portfolio managers as of the date of the report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

9

FAM Value Fund — Performance Summary (Unaudited)

Annual Total Investment Returns:

January 2, 1987 to December 31, 2018 |

| | FAM VALUE FUND | RUSSELL MIDCAP INDEX | S&P 500 INDEX |

FISCAL YEAR | TOTAL RETURN* | TOTAL RETURN | TOTAL RETURN |

1987 | -17.40% | 0.23% | 5.25% |

1988 | 35.50% | 19.80% | 16.61% |

1989 | 20.32% | 26.27% | 31.69% |

1990 | -5.36% | -11.50% | -3.11% |

1991 | 47.63% | 41.51% | 30.47% |

1992 | 25.08% | 16.34% | 7.60% |

1993 | 0.21% | 14.30% | 10.06% |

1994 | 6.82% | -2.09% | 1.31% |

1995 | 19.71% | 34.45% | 37.53% |

1996 | 11.23% | 19.00% | 22.95% |

1997 | 39.06% | 29.01% | 33.35% |

1998 | 6.19% | 10.09% | 28.58% |

1999 | -4.84% | 18.23% | 21.04% |

2000 | 19.21% | 8.25% | -9.10% |

2001 | 15.07% | -5.62% | -11.88% |

2002 | -5.33% | -16.19% | -22.09% |

2003 | 24.98% | 40.06% | 28.67% |

2004 | 16.86% | 20.22% | 10.88% |

2005 | 5.56% | 12.65% | 4.91% |

2006 | 8.73% | 15.26% | 15.79% |

2007 | -0.79% | 5.60% | 5.49% |

2008 | -28.68% | -41.46% | -37.00% |

2009 | 22.18% | 40.48% | 26.46% |

2010 | 17.02% | 25.48% | 14.76% |

2011 | -0.41% | -1.55% | 2.11% |

2012 | 11.39% | 17.28% | 16.00% |

2013 | 32.96% | 34.76% | 32.44% |

2014 | 13.41% | 13.22% | 13.69% |

2015 | -1.74% | -2.44% | 1.38% |

2016 | 15.60% | 13.80% | 11.96% |

2017 | 17.00% | 18.52% | 21.83% |

2018 | -6.18% | -9.06% | -4.38% |

| * | The performance results shown are for the Investor Shares of the Fund. The Fund also offers Institutional Shares, which commenced operations on January 3, 2017, and therefore have a limited performance history. Because of differences in the level of fees paid by the Investor Shares and the Institutional Shares, performance results for each share class will differ. |

10

FAM Value Fund — Performance Summary (Unaudited)

The chart below depicts the change in value of a $10,000 investment in the Investor Shares of the FAM Value Fund since inception on January 2, 1987, as compared with the growth of the Russell Midcap Index, the Fund’s primary benchmark index, and the Standard & Poor’s 500 Index, an additional comparative index, during the same period. The information assumes reinvestment of dividends and capital gain distributions. The Russell Midcap Index is an unmanaged index generally representative of the market for the stocks of mid-size U.S. companies. The Standard & Poor’s 500 Index is an unmanaged index generally representative of the market for the stocks of large size U.S. companies. Investors cannot invest directly in an index.

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN FAM VALUE FUND,

THE RUSSELL MIDCAP INDEX AND THE S&P 500 INDEX

This information represents past performance of the FAM Value Fund and is not indicative of future results. The investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

11

FAM Value Fund — Performance Summary (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2018

The performance data quoted represents past performance.

| | 1 YEAR | 3 YEAR | 5 YEAR | 10 YEAR | SINCE INCEPTION | TOTAL FUND OPERATING EXPENSES* |

FAM VALUE FUND Investor Shares (1/2/87) | -6.18% | 8.26% | 7.18% | 11.55% | 10.08% | 1.20%* |

Institutional Shares

(1/3/17) | -6.00% | N/A | N/A | N/A | 4.96% | 1.01%* |

Russell Midcap Index | -9.06% | 7.04% | 6.26% | 14.03% | 11.04% | N/A |

S&P 500 Index | -4.38% | 9.26% | 8.49% | 13.12% | 10.02% | N/A |

* | Disclosure: The total annual operating expense ratio as stated in the fee table of the Fund’s most recent prospectus is 1.20% after fee waivers of (0.01)% for the Investor Class. The Fund’s total annual operating expense ratio as stated in the fee table of the Fund’s most recent prospectus is 1.01% after fee waivers of (0.18)% for the Institutional Class. The total annual operating expense as reported in the Fund’s audited financial statements is 1.18% as of 12/31/2017 after a fee waiver of (0.01%) for the Investor Class. The Advisor has contractually agreed, untl May 1, 2019, to waive fees and/or reimburse the Fund certain expenses (excluding interest, taxes, brokerage costs, Acquired Fund Fees and Expenses, dividend expense and extraordinary expenses) to the extent necessary to maintain Net Fund Operating Expenses for Investor Shares at 1.18% and Institutional Shares at 0.99%. |

| Past performance is not indicative of future results, current performance may be lower or higher than the performance date quoted. Investment returns may fluctuate; the value of your investment upon redemption may be more or less than the initial amount invested. |

| Please consider a fund’s investment objectives, risks, charges and expenses carefully before investing. The FAM Funds prospectus or summary prospectus contains this and other important information about the FAM Value Fund and should be read carefully before you invest or send money. The principal risks of investing in the Funds are: stock market risk (stocks fluctuate in response to the activities of individual companies and to general stock market and economic conditions), stock selection risk (Fenimore utilizes a value approach to stock selection and there is risk that the stocks selected may not realize their intrinsic value, or their price may go down over time), and small-cap risk (prices of small-cap companies can fluctuate more than the stocks of larger companies and may not correspond to changes in the stock market in general). |

| To obtain a prospectus or summary prospectus and performance data that is current to the most recent month-end for each fund as well as other information on the FAM Value Fund, please go to famfunds.com or call (800) 932-3271. |

| This presentation was prepared by Fenimore Asset Management, Inc. (“Fenimore”). Neither this presentation nor any of its contents may be distributed or used for any other purpose without the prior written consent of Fenimore. |

| In part, the purpose of this presentation is to provide investors with an update on financial market conditions. The description of certain aspects of the market herein is a condensed summary only. This summary does not purport to be complete and no obligation to update or otherwise revise such information is being assumed. These materials are provided for informational purposes only and are not otherwise intended as an offer to sell, or the solicitation of an offer to purchase, any security or other financial instrument. This summary is not advice, a recommendation or an offer to enter into any transaction with Fenimore or any of their affiliated funds |

| This presentation may contain statements based on the current beliefs and expectations of Fenimore’s management and are subject to significant risks and uncertainties. Actual results may differ from those set forth in the forward-looking statements. |

| Any references herein to any of Fenimore’s past or present investments, portfolio characteristics, or performance, have been provided for illustrative purposes only. It should not be assumed that these investments were or will be profitable or that any future investments will be profitable or will equal the performance of these investments. There can be no guarantee that the investment objectives of Fenimore will be achieved. Any investment entails a risk of loss. Unless otherwise noted, information included herein is presented as of the date indicated on the cover page and may change at any time without notice. |

12

FAM Value Fund — Portfolio Data (Unaudited)

December 31, 2018

TOP TEN EQUITY HOLDINGS |

(% of Net Assets) | |

CDW Corp. | 6.1% |

Ross Stores | 5.9% |

IDEX Corp. | 5.3% |

Markel Corp. | 5.1% |

Brown & Brown | 4.7% |

Berkshire Hathaway, Inc. - Class A | 4.4% |

Brookfield Asset Management Inc. - Class A | 3.7% |

CarMax, Inc. | 3.4% |

AutoZone | 3.4% |

Illinois Tool Works, Inc. | 3.2% |

TOTAL NET ASSETS | $1,132,404,096 |

COMPOSITION OF NET ASSETS |

Machinery | 15.7% |

Specialty Retail | 12.7% |

Insurance | 10.8% |

Electronic Equipment, Instruments & Components | 9.2% |

Capital Markets | 6.5% |

Diversified Financial Services | 4.4% |

Banks | 4.3% |

Health Care Providers & Services | 3.5% |

Hotels, Restaurants & Leisure | 3.1% |

Life Sciences Tools & Services | 2.9% |

Oil, Gas & Consumable Fuels | 2.9% |

Health Care Equipment & Supplies | 2.6% |

Household Durables | 2.5% |

Chemicals | 2.5% |

Air Freight & Logistics | 1.9% |

Multi-Line Retail | 1.9% |

Road & Rail | 1.7% |

IT Services | 1.6% |

Containers & Packaging | 1.5% |

Semiconductors & Semiconductor Equipment | 1.3% |

Media | 0.5% |

Building Products | 0.5% |

Money Market Funds | 5.5% |

Statement Regarding Availability of Quarterly Portfolio Schedule. Please note that (i) the Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission as of the end of the first and third quarters of each fiscal year on Form N-Q; (ii) the Fund’s Forms N-Q are available on the Commission’s website at http://www.sec.gov; and (iii) the Fund makes the information on Form N-Q available to shareholders, upon request, by calling FAM Funds at 1-800-932-3271.

13

FAM Value Fund — Schedule of Investments

December 31, 2018

| | Shares | | | Value | |

COMMON STOCKS — 94.5% | | | | | | | | |

Air Freight & Logistics — 1.9% | | | | | | | | |

Forward Air Corporation | | | 389,233 | | | $ | 21,349,430 | |

Banks — 4.3% | | | | | | | | |

M&T Bank Corporation | | | 179,000 | | | | 25,620,270 | |

South State Corporation | | | 388,110 | | | | 23,267,194 | |

| | | | | | | | 48,887,464 | |

Building Products — 0.5% | | | | | | | | |

Fortune Brands Home & Security, Inc. | | | 147,000 | | | | 5,584,530 | |

Capital Markets — 6.5% | | | | | | | | |

Brookfield Asset Management, Inc. - Class A | | | 1,102,500 | | | | 42,280,875 | |

Franklin Resources, Inc. | | | 290,000 | | | | 8,601,400 | |

T. Rowe Price Group, Inc. | | | 239,500 | | | | 22,110,640 | |

| | | | | | | | 72,992,915 | |

Chemicals — 2.5% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 175,500 | | | | 28,088,775 | |

Containers & Packaging — 1.5% | | | | | | | | |

Avery Dennison Corporation | | | 187,000 | | | | 16,798,210 | |

Diversified Financial Services — 4.4% | | | | | | | | |

Berkshire Hathaway, Inc. - Class A (a) | | | 163 | | | | 49,878,000 | |

Electronic Equipment, Instruments & Components — 9.2% | | | | | | | | |

CDW Corporation | | | 858,000 | | | | 69,540,900 | |

FLIR Systems, Inc. | | | 794,728 | | | | 34,602,457 | |

| | | | | | | | 104,143,357 | |

Health Care Equipment & Supplies — 2.6% | | | | | | | | |

Stryker Corporation | | | 191,000 | | | | 29,939,250 | |

See Notes to Financial Statements

14

FAM Value Fund — Schedule of Investments (continued)

December 31, 2018

| | SHARES | | | VALUE | |

COMMON STOCKS — 94.5% (continued) | | | | | | | | |

Health Care Providers & Services — 3.5% | | | | | | | | |

Henry Schein, Inc. (a) | | | 350,000 | | | $ | 27,482,000 | |

MEDNAX, Inc. (a) | | | 381,400 | | | | 12,586,200 | |

| | | | | | | | 40,068,200 | |

Hotels, Restaurants & Leisure — 3.1% | | | | | | | | |

Marriott International, Inc. - Class A | | | 113,800 | | | | 12,354,128 | |

Yum! Brands, Inc. | | | 245,600 | | | | 22,575,552 | |

| | | | | | | | 34,929,680 | |

Household Durables — 2.5% | | | | | | | | |

Mohawk Industries, Inc. (a) | | | 241,100 | | | | 28,199,056 | |

Insurance — 10.8% | | | | | | | | |

Brown & Brown, Inc. | | | 1,919,392 | | | | 52,898,443 | |

Markel Corporation (a) | | | 55,850 | | | | 57,975,092 | |

White Mountains Insurance Group Ltd. | | | 13,233 | | | | 11,349,812 | |

| | | | | | | | 122,223,347 | |

IT Services — 1.6% | | | | | | | | |

Black Knight, Inc. (a) | | | 406,711 | | | | 18,326,398 | |

Life Sciences Tools & Services — 2.9% | | | | | | | | |

Waters Corporation (a) | | | 171,702 | | | | 32,391,583 | |

Machinery — 15.7% | | | | | | | | |

Donaldson Company, Inc. | | | 755,400 | | | | 32,776,806 | |

Graco, Inc. | | | 716,650 | | | | 29,991,803 | |

IDEX Corporation | | | 476,750 | | | | 60,194,455 | |

Illinois Tool Works, Inc. | | | 289,950 | | | | 36,733,765 | |

Snap-on, Inc. | | | 127,000 | | | | 18,451,830 | |

| | | | | | | | 178,148,659 | |

See Notes to Financial Statements

15

FAM Value Fund — Schedule of Investments (continued)

December 31, 2018

| | SHARES | | | VALUE | |

COMMON STOCKS — 94.5% (continued) | | | | | | | | |

Media — 0.5% | | | | | | | | |

Interpublic Group of Companies, Inc. (The) | | | 300,000 | | | $ | 6,189,000 | |

Multi-Line Retail — 1.9% | | | | | | | | |

Dollar General Corporation | | | 196,300 | | | | 21,216,104 | |

Oil, Gas & Consumable Fuels — 2.9% | | | | | | | | |

EOG Resources, Inc. | | | 370,000 | | | | 32,267,700 | |

Road & Rail — 1.7% | | | | | | | | |

Landstar System, Inc. | | | 204,221 | | | | 19,537,823 | |

Semiconductors & Semiconductor Equipment — 1.3% | | | | | | | | |

Microchip Technology, Inc. | | | 203,000 | | | | 14,599,760 | |

Specialty Retail — 12.7% | | | | | | | | |

AutoZone, Inc. (a) | | | 45,700 | | | | 38,312,138 | |

CarMax, Inc. (a) | | | 615,000 | | | | 38,578,950 | |

Ross Stores, Inc. | | | 810,688 | | | | 67,449,242 | |

| | | | | | | | 144,340,330 | |

| | | | | | | | | |

Total Common Stocks (Cost $455,887,840) | | | | | | $ | 1,070,099,571 | |

See Notes to Financial Statements

16

FAM Value Fund — Schedule of Investments (continued)

December 31, 2018

| | SHARES | | | VALUE | |

MONEY MARKET FUND — 5.5% | | | | | | | | |

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 2.30% (b) (Cost $62,181,640) | | | 62,181,640 | | | $ | 62,181,640 | |

| | | | | | | | | |

Investments in Securities at Value — 100.0% (Cost $518,069,480) | | | | | | $ | 1,132,281,211 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.0% (c) | | | | | | | 122,885 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 1,132,404,096 | |

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of December 31, 2018. |

(c) | Percentage rounds to less than 0.1%. |

See Notes to Financial Statements

17

FAM Equity-Income Fund

December 31, 2018

Dear Fellow Equity-Income Fund Shareholder,

The Fund performed well in a turbulent market posting a slightly positive return of +0.06%. This result was considerably ahead of our benchmark the Russell Midcap Index, which fell -9.06% for the year. The Fund also performed better than the S&P 500 Index which declined -4.38% for the year.1 According to Morningstar, an industry-rating firm, 94% of all U.S. Equity Midcap funds posted negative returns for the year while only 6% earned returns above zero. We are pleased to be part of that 6%.2

We attribute the outperformance of the Fund relative to the Russell Midcap Index to three factors. Firstly, over the last few years, we exited positions that were disappointments rather than waiting for them to work out their problems in the hope of generating a higher return. This process of quickly getting out of poor performers and weaker holdings allowed us to concentrate more assets in names that had demonstrated the ability to compound capital. The result of this strategy was that more than 45% of the Fund’s holdings posted a positive return in the down market. Our batting average was even better for the largest holdings with seven out of the Top 10 Holdings posting positive results. This was due to the strength of the businesses in the portfolio and their ability to compound capital over time.

The second reason the Fund beat the benchmark, in our opinion, is our strategy of letting the “compounders” compound. This simply means resisting the temptation of trimming names in the portfolio when they perform well and grow to larger weightings in order to recycle the capital into names that may not be performing as well. In our minds, this is like cutting the flowers and watering the weeds. In theory, this sounds like a good strategy, but, in practice, our team believes it diminishes long-term returns. We define compounders as companies that have consistently performed well and have a long runway for growth. They also tend to earn high returns on invested capital.

Thirdly, two companies in the portfolio were acquired at significant premiums and the transactions closed in December. These acquisitions immediately added to performance, but also had the effect of insulating a small portion of the portfolio to the fourth quarter’s market gyrations.

The overarching strategy of the Fund is to invest in companies that pay a dividend and consistently increase that dividend over time. Every Fund holding pays a dividend and the majority grow that dividend every year. In fact, on average, the companies in the Fund have increased their dividends more than 10.6% compounded over the last five years (as of 12/31/18).3 We believe dividend growth is important because companies that are growing

2 | Morningstar.com, 12/31/18 |

3 | FactSet & Bloomberg, 12/31/18 |

18

FAM Equity-Income Fund

their cash flow are potentially able to consistently grow their dividends. We favor investing in businesses that are growing their dividends quickly because it usually means the underlying company is expanding. It also means that they are generating more cash than needed to reinvest back into the operation. These growing dividends contribute to the total return of the investment.

Portfolio Activity

There was considerable activity in the portfolio during the past year. The focus was on selling a few underperforming names that were disappointments where our team could not make the investment case that holding the names would be better than reinvesting that capital into higher quality names. We also replaced two companies that were acquired late in the year. Overall, it is our belief that the new portfolio holdings are of much higher quality than the positions we exited.

Purchases

We bought shares in Avery Dennison (AVY). Based on sales and market share, they are the leader in manufacturing pressure-sensitive labels. We were attracted to Avery because of their ability to grow over the business cycle and their remarkable consistency. During our due diligence, we learned how strong their competitive position is with 40% market share and how they can pass on higher prices to customers.4 This dynamic is rare. We were also impressed with the management team. We first started buying shares in the second quarter and added to the position throughout the year as the price fell.

Broadridge Financial Solutions (BR) was invested in during the fourth quarter after the price declined significantly from its peak. Broadridge offers a broad array of products serving financial services firms and public companies. Their flagship product is Proxy Edge which aggregates shareholder and voting information. The company has a long history of growth augmented by acquisition. It also has a significant base of recurring revenue. According to our estimates, Broadridge earns close to a 20% return on invested capital, has more than doubled their dividend over the last five years, and regularly buys back stock. We expect that financial firms could increasingly outsource many of their functions to companies such as Broadridge as complexity grows and the cost to maintain in-house systems increases.

We initiated a position in Forest City Realty Trust (FCE.A) in the first quarter after the stock sold off. The board concluded their strategic review process and decided that shareholder value would be better enhanced on a standalone basis rather than pursuing the sale of Forest at the price of received offers. Our valuation work indicated a significantly higher value than the price we paid for the initial position. A few months later, this proved correct as Forest accepted a higher acquisition price.

4 | Avery Dennison 2017 Annual Report |

19

FAM Equity-Income Fund

Our team also bought an initial position in International Flavors & Fragrances (IFF). IFF is a global manufacturer and supplier of flavor and fragrance ingredients that are used in a wide variety of consumer products. Their broad geographic footprint, defensive end markets, and diversified customer base support consistent financial results and a growing dividend. International Flavors recently completed the acquisition of Israeli-based competitor Frutarom, which led to a sell-off in their stock price as concerns emerged over the price of the transaction and the use of debt to partially fund the deal. We believe the acquisition better aligns International Flavors with changing consumer trends and the balance sheet concerns are very manageable. The sell-off presented us with an opportunity to start our initial position.

We bought shares in Watsco (WSO) – the largest HVAC distribution company in the U.S. They represent 1,000 manufacturers, serve their customer base of 80,000 contractors through 568 stores in 37 states, and carry more than 300,000 SKUs.5 Watsco’s locations are primarily in the Sun Belt states with the highest concentration of stores in Florida and Texas. We believe this is an attractive industry because every air conditioning unit the firm sells will ultimately break or wear out and need to be replaced. When units break, they are typically replaced immediately and customers are less price sensitive. The replacement cycle of Watsco’s growing installed base increases the profitability of each store and their operation is driven primarily by replacement of existing units. In fact, replacement sales make up 85% of industry revenue.

We took a small position in Marriott International (MAR) after the company disclosed a data breach that sent the stock lower to nearly 25% below its 52-week high. Marriott has more than doubled their dividend over the last five years.6 We believe this hotel chain is a premier lodging franchise and expect to build a larger position over time.

In addition to new holdings, our team put capital to work by adding to existing names including Digital Realty Trust (DLR), Ingersoll Rand (IR), M&T Bank (MTB), Snap-on (SNA), Versum Materials (VSM), Ross Stores (ROST), Robert Half International (RHI), and US Ecology (ECOL). The sell-off in the market at year-end gave us a good opportunity to buy shares in these companies at what we estimated to be attractive prices.

Sales

Interpublic Group of Companies (IPG) was sold from the portfolio because we believe the advertising market is shifting more in favor of online firms such as Google and Facebook. This puts Interpublic Group at a disadvantage that could increase over time. We were able to get a good price for our shares before the market turned down.

5 | Watsco 2017 Annual Report |

6 | FactSet & Bloomberg, 12/31/18 |

20

FAM Equity-Income Fund

We exited a long-term holding, Flowers Foods (FLO), at a price approximately 49% above the low set in September of 2016. This was a case where we wanted to move on from the holding 18 months earlier, but estimated we could get a higher price for our shares by just waiting. The return from the low point was double the market return. The moral of the story, in this case, is that patience pays.

Fast food restaurant company, Sonic Corp. (SONC), is no longer held in the portfolio after it was acquired for cash. Sonic was sold at a 21% premium over the previous 30-day trading range.7 The transaction closed on December 6.

Forest City Realty Trust (FCE.A) was also acquired for cash by Brookfield Asset Management. We only held this position for a few months before the transaction was announced and the price represented a premium of 26% over the previous closing price.7

We sold our position in Patterson Companies (PDCO) after a long string of missteps by management. Patterson was one of the premier companies in the distribution of dental products, but poor management allowed their strong position to be competed away. The business struggled as the market slowed and price inflation disappeared. This meant that pricing pressure could have a more pronounced impact on earnings growth.

Macquarie Infrastructure (MIC) was sold from the portfolio as well. When we initially invested in Macquarie, we liked the assets they held – petrochemical storage tanks, general aviation operations, power generation, and a gas utility – and believed management had a growing track record of creating value through additional acquisitions. However, Macquarie announced a softening in their storage tank business in February 2018 and we had viewed this as their most stable segment. In our view, the fundamental deterioration was swift and, given the immediate capital needs this created, it led them to substantially cut their dividend.8 Our team determined the financial profile no longer fit FAM Funds’ criteria and exited the entire position.

In addition to exiting positions, we trimmed US Ecology (ECOL) due to its strong performance over the last 12 months and high valuation. Their business tends to be lumpy, so we expect to be able to buy those shares back at a lower price in the future. We also trimmed Franklin Resources (BEN) because we believed it was an inferior holding.

Closing Thoughts

Our team is optimistic over the long term and believes the Fund’s holdings should be able to continue their growth leading to higher dividends to shareholders. In short, the “compounders” should continue to compound. In the near term, however, the picture is murkier and the market could exhibit more turbulence. While this may be uncomfortable for

8 | FactSet & Bloomberg, 12/31/18 |

21

FAM Equity-Income Fund

many investors, it has historically provided the Fund with great purchasing opportunities. We have cash at the ready to potentially invest in more great companies or add to existing holdings when opportunities arise.

As always, we will continue to work diligently on your behalf. Thank you for investing with us in the FAM Equity Income Fund.

Best & Worst Performers for 2018

Best Performers | Worst Performers |

CDW Corp. | 1.13% | South State Corp. | -0.85% |

Sonic Corp. | 1.12% | Patterson Companies | -0.74% |

Xilinx | 0.96% | Microchip Technology | -0.69% |

Arthur J. Gallagher & Co. | 0.92% | Macquarie Infrastructure | -0.65% |

US Ecology | 0.78% | EOG Resources | -0.65% |

This reflects the FAM Value Fund’s best and worst performers, in descending order, based on individual stock performance. Past performance does not indicate future results.

Performance (as of 12/31/18)

| | 1-Year | 3-Year | 5-Year | 10-Year | Since Inception 4/1/1996 |

FAM Equity-Income Fund | 0.06% | 11.07% | 7.97% | 12.41% | 8.59% |

Russell Midcap Index | -9.06% | 7.04% | 6.26% | 14.03% | 9.63% |

S&P 500 Index | -4.38% | 9.26% | 8.49% | 13.12% | 8.17% |

Past performance does not indicate future results.

|  |

Paul Hogan, CFA

Co-Manager | Thomas O. Putnam

Co-Manager |

The opinions expressed herein are those of the portfolio managers as of the date of the report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

22

FAM Equity-Income Fund

Performance data quoted above is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

23

FAM Equity-Income Fund — Performance Summary (Unaudited)

Annual Total Investment Returns:

APRIL 1, 1996 TO DECEMBER 31, 2018 |

| | FAM EQUITY-INCOME FUND | RUSSELL MIDCAP INDEX | S&P 500 INDEX |

FISCAL YEAR | TOTAL RETURN | TOTAL RETURN | TOTAL RETURN |

4/1/96-12/31/96 | 11.84% | 12.00% | 15.20% |

1997 | 26.90% | 29.01% | 33.35% |

1998 | 4.67% | 10.09% | 28.58% |

1999 | -6.98% | 18.23% | 21.04% |

2000 | 17.18% | 8.25% | -9.10% |

2001 | 20.79% | -5.62% | -11.88% |

2002 | -2.25% | -16.19% | -22.09% |

2003 | 20.30% | 40.06% | 28.67% |

2004 | 14.04% | 20.22% | 10.88% |

2005 | 5.75% | 12.65% | 4.91% |

2006 | 6.57% | 15.26% | 15.79% |

2007 | -3.64% | 5.60% | 5.49% |

2008 | -29.04% | -41.46% | -37.00% |

2009 | 21.43% | 40.48% | 26.46% |

2010 | 17.47% | 25.48% | 14.76% |

2011 | 6.79% | -1.55% | 2.11% |

2012 | 11.02% | 17.28% | 16.00% |

2013 | 29.79% | 34.76% | 32.44% |

2014 | 7.85% | 13.22% | 13.69% |

2015 | -0.73% | -2.44% | 1.38% |

2016 | 21.59% | 13.80% | 11.96% |

2017 | 12.64% | 18.52% | 21.83% |

2018 | 0.06% | -9.06% | -4.38% |

24

FAM Equity-Income Fund — Performance Summary (Unaudited)

The chart below depicts the change in value of a $10,000 investment in the FAM Equity-Income Fund since inception on April 1, 1996, as compared with the growth of the Russell Midcap Index, the Fund’s primary benchmark index, and the Standard and Poor’s 500 Index, an additional comparative index, during the same period. The information assumes reinvestment of dividends and capital gain distributions. The Russell Midcap Index is an unmanaged index generally representative of the market for the stocks of mid-size U.S. companies. The Standard and Poor’s 500 Index is an unmanaged index generally representative of the market for the stocks of large size U.S. companies. Investors cannot invest directly in an index.

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN FAM EQUITY-INCOME FUND,

THE RUSSELL MIDCAP INDEX AND THE S&P 500 INDEX

This information represents past performance of the FAM Equity-Income Fund and is not indicative of future results. The investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost.

25

FAM Equity-Income Fund — Performance Summary (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2018

The performance data quoted represents past performance.

| | 1 YEAR | 3 YEAR | 5 YEAR | 10 YEAR | SINCE INCEPTION | TOTAL FUND OPERATING EXPENSES* |

FAM Equity-Income Fund (4/1/96) | 0.06% | 11.07% | 7.97% | 12.41% | 8.59% | 1.26%* |

Russell Midcap Index | -9.06% | 7.04% | 6.26% | 14.03% | 9.63% | N/A |

S&P 500 Index | -4.38% | 9.26% | 8.49% | 13.12% | 8.17% | N/A |

* | Disclosure: The Fund’s total annual operating expense ratio as stated in the fee table of the Fund’s most recent prospectus is 1.26%. The total operating expense as reported in the FAM Equity-Income Fund’s audited financial statements as of 12/31/17 is 1.25%. The Advisor has contractually agreed, until May 1, 2019, to waive fees and/or reimburse the Fund certain expenses (excluding interest, taxes, brokerage costs, Acquired Fund Fees and Expenses, dividend expense and extraordinary expenses) to the extent necessary to maintain Net Fund Operating Expenses for Investor Shares at 1.26%. |

| Past performance is not indicative of future results, current performance may be lower or higher than the performance date quoted. Investment returns may fluctuate; the value of your investment upon redemption may be more or less than the initial amount invested. |

| Please consider a fund’s investment objectives, risks, charges and expenses carefully before investing. The FAM Funds prospectus or summary prospectus contains this and other important information about the FAM Equity-Income Fund and should be read carefully before you invest or send money. The principal risks of investing in the Funds are: stock market risk (stocks fluctuate in response to the activities of individual companies and to general stock market and economic conditions), stock selection risk (Fenimore utilizes a value approach to stock selection and there is risk that the stocks selected may not realize their intrinsic value, or their price may go down over time), and small-cap risk (prices of small-cap companies can fluctuate more than the stocks of larger companies and may not correspond to changes in the stock market in general). |

| To obtain a prospectus or summary prospectus and performance data that is current to the most recent month-end for each fund as well as other information on the FAM Equity-Income Fund, please go to famfunds.com or call (800) 932-3271. |

| This presentation was prepared by Fenimore Asset Management, Inc. (“Fenimore”). Neither this presentation nor any of its contents may be distributed or used for any other purpose without the prior written consent of Fenimore. |

| In part, the purpose of this presentation is to provide investors with an update on financial market conditions. The description of certain aspects of the market herein is a condensed summary only. This summary does not purport to be complete and no obligation to update or otherwise revise such information is being assumed. These materials are provided for informational purposes only and are not otherwise intended as an offer to sell, or the solicitation of an offer to purchase, any security or other financial instrument. This summary is not advice, a recommendation or an offer to enter into any transaction with Fenimore or any of their affiliated funds |

| This presentation may contain statements based on the current beliefs and expectations of Fenimore’s management and are subject to significant risks and uncertainties. Actual results may differ from those set forth in the forward-looking statements. |

| Any references herein to any of Fenimore’s past or present investments, portfolio characteristics, or performance, have been provided for illustrative purposes only. It should not be assumed that these investments were or will be profitable or that any future investments will be profitable or will equal the performance of these investments. There can be no guarantee that the investment objectives of Fenimore will be achieved. Any investment entails a risk of loss. Unless otherwise noted, information included herein is presented as of the date indicated on the cover page and may change at any time without notice. |

26

FAM Equity-Income Fund — Portfolio Data (Unaudited)

December 31, 2018

TOP TEN EQUITY HOLDINGS |

(% of Net Assets) | |

CDW Corp. | 7.3% |

Air Products & Chemicals | 5.8% |

Arthur J. Gallagher & Co. | 5.6% |

Stryker Corp. | 5.6% |

Ross Stores | 5.1% |

Ingersoll Rand | 4.3% |

Xilinx, Inc. | 4.3% |

AveryDennison Corp. | 4.0% |

Digital Realty Trust | 3.9% |

Microchip Technology | 3.5% |

TOTAL NET ASSETS | $240,545,373 |

COMPOSITION OF NET ASSETS |

Machinery | 11.3% |

Semiconductors & Semiconductor Equipment | 9.7% |

Electronic Equipment, Instruments & Components | 9.6% |

Specialty Retail | 9.0% |

Money Market Funds | 8.6% |

Chemicals | 7.5% |

Banks | 6.0% |

Insurance | 5.6% |

Health Care Equipment & Supplies | 5.6% |

Containers & Packaging | 4.0% |

Equity Real Estate Investment Trusts (REITs) | 3.9% |

Oil, Gas & Consumable Fuels | 2.8% |

Water Utilities | 2.7% |

Professional Services | 2.6% |

IT Services | 2.4% |

Capital Markets | 2.3% |

Commercial Services & Supplies | 1.9% |

Food Products | 1.5% |

Trading Companies & Distributors | 1.4% |

Hotels, Restaurants & Leisure | 1.0% |

Other | 0.6% |

Statement Regarding Availability of Quarterly Portfolio Schedule. Please note that (i) the Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission as of the end of the first and third quarters of each fiscal year on Form N-Q; (ii) the Fund’s Forms N-Q are available on the Commission’s website at http://www.sec.gov; and (iii) the Fund makes the information on Form N-Q available to shareholders, upon request, by calling FAM Funds at 1-800-932-3271.

27

FAM Equity-Income Fund — Schedule of Investments

December 31, 2018

| | SHARES | | | VALUE | |

COMMON STOCKS — 90.8% | | | | | | | | |

Banks — 6.0% | | | | | | | | |

M&T Bank Corporation | | | 47,000 | | | $ | 6,727,110 | |

South State Corporation | | | 88,000 | | | | 5,275,600 | |

Stock Yards Bancorp, Inc. | | | 70,664 | | | | 2,317,779 | |

| | | | | | | | 14,320,489 | |

Capital Markets — 2.3% | | | | | | | | |

Franklin Resources, Inc. | | | 33,900 | | | | 1,005,474 | |

T. Rowe Price Group, Inc. | | | 48,000 | | | | 4,431,360 | |

| | | | | | | | 5,436,834 | |

Chemicals — 7.5% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 87,000 | | | | 13,924,350 | |

International Flavors & Fragrances, Inc. | | | 30,000 | | | | 4,028,100 | |

| | | | | | | | 17,952,450 | |

Commercial Services & Supplies — 1.9% | | | | | | | | |

US Ecology, Inc. | | | 71,647 | | | | 4,512,328 | |

Containers & Packaging — 4.0% | | | | | | | | |

Avery Dennison Corporation | | | 108,000 | | | | 9,701,640 | |

Electronic Equipment, Instruments & Components — 9.6% | | | | | | | | |

CDW Corporation | | | 217,000 | | | | 17,587,850 | |

National Instruments Corporation | | | 122,000 | | | | 5,536,360 | |

| | | | | | | | 23,124,210 | |

Equity Real Estate Investment Trusts (REITs) - 3.9% | | | | | | | | |

Digital Realty Trust, Inc. | | | 89,000 | | | | 9,482,950 | |

Food Products — 1.5% | | | | | | | | |

McCormick & Company, Inc. | | | 26,000 | | | | 3,620,240 | |

Health Care Equipment & Supplies — 5.6% | | | | | | | | |

Stryker Corporation | | | 85,500 | | | | 13,402,125 | |

See Notes to Financial Statements

28

FAM Equity-Income Fund — Schedule of Investments (continued)

December 31, 2018

| | SHARES | | | VALUE | |

COMMON STOCKS — 90.8% (continued) | | | | | | | | |

Hotels, Restaurants & Leisure — 1.0% | | | | | | | | |

Marriott International, Inc. - Class A | | | 22,000 | | | $ | 2,388,320 | |

Insurance — 5.6% | | | | | | | | |

Arthur J. Gallagher & Company | | | 183,920 | | | | 13,554,904 | |

IT Services — 2.4% | | | | | | | | |

Broadridge Financial Solutions, Inc. | | | 60,000 | | | | 5,775,000 | |

Machinery — 11.3% | | | | | | | | |

Donaldson Company, Inc. | | | 91,600 | | | | 3,974,524 | |

IDEX Corporation | | | 62,984 | | | | 7,952,360 | |

Ingersoll-Rand plc | | | 114,000 | | | | 10,400,220 | |

Snap-on, Inc. | | | 33,700 | | | | 4,896,273 | |

| | | | | | | | 27,223,377 | |

Oil, Gas & Consumable Fuels — 2.8% | | | | | | | | |

EOG Resources, Inc. | | | 78,000 | | | | 6,802,380 | |

Professional Services — 2.6% | | | | | | | | |

Robert Half International, Inc. | | | 110,000 | | | | 6,292,000 | |

Semiconductors & Semiconductor Equipment — 9.7% | | | | | | | | |

Microchip Technology, Inc. | | | 117,000 | | | | 8,414,640 | |

Versum Materials, Inc. | | | 165,710 | | | | 4,593,481 | |

Xilinx, Inc. | | | 120,414 | | | | 10,255,661 | |

| | | | | | | | 23,263,782 | |

See Notes to Financial Statements

29

FAM Equity-Income Fund — Schedule of Investments (continued)

December 31, 2018

| | SHARES | | | VALUE | |

COMMON STOCKS — 90.8% (continued) | | | | | | | | |

Specialty Retail — 9.0% | | | | | | | | |

Monro, Inc. | | | 96,000 | | | $ | 6,600,000 | |

Penske Automotive Group, Inc. | | | 70,000 | | | | 2,822,400 | |

Ross Stores, Inc. | | | 147,686 | | | | 12,287,475 | |

| | | | | | | | 21,709,875 | |

Trading Companies & Distributors — 1.4% | | | | | | | | |

Watsco, Inc. | | | 24,000 | | | | 3,339,360 | |

Water Utilities — 2.7% | | | | | | | | |

Aqua America, Inc. | | | 190,750 | | | | 6,521,742 | |

| | | | | | | | | |

Total Common Stocks (Cost $128,015,087) | | | | | | $ | 218,424,006 | |

MONEY MARKET FUND — 8.6% | | | | | | | | |

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 2.30% (a) (Cost $20,727,438) | | | 20,727,438 | | | | 20,727,438 | |

| | | | | | | | | |

Investments in Securities at Value — 99.4% (Cost $148,742,525) | | | | | | | 239,151,444 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.6% | | | | | | | 1,393,929 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 240,545,373 | |

(a) | The rate shown is the 7-day effective yield as of December 31, 2018. |

See Notes to Financial Statements

30

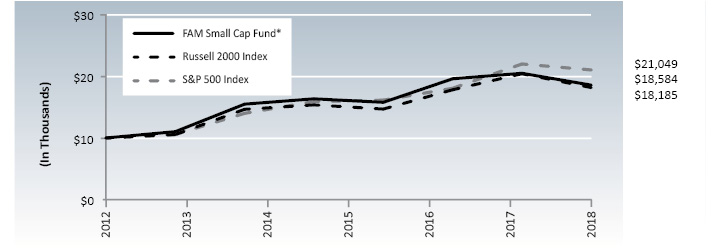

FAM Small Cap Fund

December 31, 2018

Dear Fellow Small Cap Fund Shareholder,

Clearly, the past few months have been volatile with concern about a slowing economy spreading among many investors. As investors turned from optimism to pessimism, the Russell 2000 Index (the primary index for small, publicly traded U.S. companies) at its August 31 peak was up 14.3% year-to-date before falling to end the year down -11.01%.1 We are studying various economic and political concerns, especially the setting of new trade rules and tariffs, inflation (both labor and materials), and falling optimism (which potentially creates a self-fulfilling prophecy). Our team is also assessing the risk that the Federal Reserve may accidentally raise interest rates too high, thus stemming growth rates. So far, our conclusion is that while these issues are quite real – we see many companies reporting slower growth and thinner profit margins – it remains unclear if they are severe enough to trigger a recession, as some may fear, or justify the 25.31% drop in small-cap stock prices.2

The impact of these issues differs at every business our team follows. At one extreme, a firm might rely on a Chinese-centered supply chain now facing tariffs, suffer through higher trucking costs, and face a step up in government mandated minimum wage rates while having little ability to raise prices. At the other extreme, some businesses do not encounter many of these issues. For example, consider enterprises that hire experts and resell their advice, such as in real estate brokerage or accounting services. While they too would be impacted by a recession if it occurs, they do not import goods, use trucks to move anything, or hire many minimum-wage employees. Plus, they have some ability to raise prices to reflect their higher costs. Much of our time is devoted to studying various industries and companies to better ascertain the impact of these new realities.

Meanwhile, there are reasons to be optimistic. Many of the problems facing us will likely be resolved. For instance, the U.S. and China may eventually strike a trade agreement with lower tariffs. Furthermore, the longer this uncertainty goes on, the more firms move sourcing to places such as Mexico, India, or Vietnam to avoid the China tariffs. Additionally, the Federal Reserve may decide that conditions no longer warrant further interest rate increases. It is quite possible that a year from now many of these issues may have passed. Humans certainly have their shortcomings, but they excel at adaptation.

In volatile days such as these, it is worth reiterating what our investment research analysts are striving to accomplish. Most of our shareholders have longer-term goals they wish to achieve – saving for retirement, funding college educations, providing for the care of a disabled child, or the like. However, it is a virtual certainty that while saving for these big

2 | Bloomberg, 12/31/18: from the intra-day high on 8/31/18 to the 12/31/18 close |

31

FAM Small Cap Fund

goals in life, we will see a tremendous variety of macro environments and swings in investor sentiment. Additionally, the shifts from extremes are essentially unpredictable; however, this is nothing new.

In just the past 20 years, we have seen: the devaluation of several emerging market currencies in 1998 (and a debt default by Russia); a massive bubble in technology stocks in the late 1990s; a recession in 2001; the horrific events of 9/11; a slew of accounting scandals in the early 2000s; a rash of hurricanes including Katrina; a housing bubble; the Great Recession of 2008-2009; unemployment touching 10% in October 2009 and frustratingly slow growth in the years after; struggles in Greece (and Portugal, Spain, Italy, etc.) so severe the European Union almost unwound; and a collection of various epidemics and government shutdowns – and this is only a partial list.3 Despite all these events, the Russell 2000 Index compounded at 7.40% per annum in the past 20 years as of December 31, 2018. What this means is that $100 invested 20 years ago is now worth approximately $417 (this assumes all dividends and capital gains were reinvested).4

Our goal for your capital and ours, as we too are investors in the Fund, is to find about 25 to 30 of what we deem to be the best businesses possible. Enterprises that have some advantage over competitors which, when combined with strong management, should allow them to be much larger in 5 to 10 years. This may involve grinding through challenging economic or political climates along the way.

Not only that, we wish to buy our shares “on the cheap” – at a discount to what a rational competitor or private equity firm would pay for the entire company. This is where the swings in investor sentiment pay off. When investors are overly optimistic, seeing nothing but opportunity on the horizon, prices tend to be so expensive as to make future returns unimpressive. However, good times are difficult to sustain. Eventually, conditions change and anxiety typically returns. When most investors are fearful, this is the time for value investors such as us to scoop up bargains. Sooner or later, the skies clear and optimism reappears – and the never-ending cycle continues. While our team tends to benefit from knowing companies well, our true advantage is the ability to be less emotional than the average investor.

In the short term, stock prices are unquestionably driven by emotions, but over the long term they are typically more rational and driven primarily by earnings growth. Specifically, in our small-cap universe, if a profitable, growing enterprise is ignored by investors for too long, then a larger competitor or private investor often buys the entire operation. This is one of the underpinnings of our long-term enthusiasm for investing in smaller companies.

3 | Wikipedia, 12/31/18 (our predecessors faced the same reality with 24 recessions in the 19th century) |

4 | Cumulative performance of a hypothetical $100 investment in the Russell 2000 Index. The returns do not reflect the payment of any brokerage commissions or brokerage costs incurred as a result of buying or selling Russell 2000 Index fund shares or trading shares on an exchange and do not reflect the deduction of taxes to which an investor would be subject as a result of owning or selling shares of a fund. If they did, the returns would be lower than those shown. |

32

FAM Small Cap Fund

We have successfully assembled a collection of high-quality businesses from our viewpoint. Each seems to have the potential and necessary leadership to grow profits considerably over time under our most reasonable assumptions. Perhaps more importantly, after several years of struggle to find attractively priced opportunities, today’s bargains are more prevalent. In our opinion, many of the Fund’s holdings trade at a considerable discount to the price a knowledgeable, private, cash buyer would offer for the whole company.

Portfolio Activity

Earlier this year, we struggled to find interesting investment opportunities, but as prices declined our team put quite a bit of capital to work. This is demonstrated in our cash balances, which are essentially a residual of our efforts to find interesting opportunities. The Fund entered the year with only 5.3% in cash, but as prices rose bargains were difficult to find. Cash reached 11.5% by September 30. However, with the recent price declines, we found additional attractive investments. The cash balance declined to 2.4% by year-end. During 2018, we initiated four new positions and exited six.

Three of our purchases and sales were really “swaps” where, in our opinion, our team sold admirable, well-run companies only because we found an even more attractive opportunity in a similar business. In the first case, we sold our shares in Evolution Petroleum (EPM) after concluding that Matador Resources (MTDR) was an even better investment opportunity. Similarly, we sold real estate owner Consolidated-Tomoka Land Co. (CTO) and invested in real estate service provider/broker Colliers International Group (CIGI). Finally, we sold our shares in value manager Westwood Holdings Group (WHG) while adding to our existing position in Diamond Hill Investment Group (DHIL).

Purchases

Matador Resources (MTDR) is a domestic energy firm, primarily focused on finding oil in southeast New Mexico and West Texas. Two things separate Matador from the dozens of other small-cap energy businesses, in our opinion. Firstly, they are good operators, routinely drilling good wells at solid economics. Secondly, although harder to define but definitely important, their culture is excellent in our view. This shows up several ways, but is best highlighted by their contrarian approach to capital allocation. Management has a long history of smart moves such as buying reserves when prices are low, selling most of their natural gas operations when prices were near a peak, and leveraging their own oil assets to develop a valuable pipeline serving themselves and neighboring competitors.

Colliers International Group (CIGI) is a global real estate services company offering everything from building management and lease negotiations to valuation services and brokering the sales of buildings. While the business could undoubtedly remain cyclical, it is a growing, profitable corporation in a prosperous industry where all the major players tend to do well. What makes Colliers particularly interesting, from our viewpoint, is its sharp leadership that allows for both organic growth and smart bolt-on acquisitions of smaller peers at attractive returns on capital.

33

FAM Small Cap Fund

Natus Medical (BABY) was added to the portfolio in the second quarter. Natus is a medical instrument/device firm with impressive franchises in newborn care (e.g., newborn hearing), neurology (e.g., sleep diagnostics), and audiology (e.g., hearing aid tuning). However, Natus stumbled recently, the largest factor being unexpected difficulty integrating an acquisition. We believe these challenges should abate, leading to a rebound in profitability. Some of our best purchases have come from a good business faltering temporarily and we believe Natus falls into this category.