UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04526

Name of Registrant: Vanguard Quantitative Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2011 – September 30, 2012

Item 1: Reports to Shareholders

|

| Annual Report | September 30, 2012 |

| Vanguard Growth and Income Fund |

|

> Vanguard Growth and Income Fund returned about 31% for the fiscal year ended September 30, 2012.

> For the 12-month period, the fund outpaced both its benchmark, the S&P 500 Index, and its large-capitalization core fund peers.

> Stocks in the information technology, financial, and consumer discretionary sectors helped fuel the fund’s advance.

| Contents | |

| Your Fund’s Total Returns. | 1 |

| Chairman’s Letter. | 2 |

| Advisors’ Report. | 8 |

| Fund Profile. | 13 |

| Performance Summary. | 14 |

| Financial Statements. | 16 |

| Your Fund’s After-Tax Returns. | 36 |

| About Your Fund’s Expenses. | 37 |

| Trustees Approve Advisory Arrangements. | 39 |

| Glossary. | 41 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Our cover photograph shows rigging on the HMSSurprise, a replica of an 18th-century Royal Navy frigate. It was featured in the 2003 movie Master and Commander: The Far Side of the World, which was based on Patrick O’Brian’s sea novels, set amid the Napoleonic Wars. Vanguard was named for another ship of that era, the HMSVanguard, which was the flagship of British Admiral Horatio Nelson at the Battle of the Nile.

Your Fund’s Total Returns

| Fiscal Year Ended September 30, 2012 | |

| Total | |

| Returns | |

| Vanguard Growth and Income Fund | |

| Investor Shares | 31.27% |

| Admiral™ Shares | 31.40 |

| S&P 500 Index | 30.20 |

| Large-Cap Core Funds Average | 27.34 |

Large-Cap Core Funds Average: Derived from data provided by Lipper Inc.

Admiral Shares carry lower expenses and are available to investors who meet certain account-balance requirements.

| Your Fund’s Performance at a Glance | ||||

| September 30, 2011, Through September 30, 2012 | ||||

| Distributions Per Share | ||||

| Starting | Ending | Income | Capital | |

| Share Price | Share Price | Dividends | Gains | |

| Vanguard Growth and Income Fund | ||||

| Investor Shares | $23.86 | $30.73 | $0.525 | $0.000 |

| Admiral Shares | 38.97 | 50.18 | 0.910 | 0.000 |

1

Chairman’s Letter

Dear Shareholder,

Global stock markets began the fiscal year strongly and, despite volatility in the middle of the period, finished on a high note with four straight monthly gains. In this robust environment, Vanguard Growth and Income Fund returned about 31% for both Investor and Admiral Shares. The fund’s returns exceeded the return of its benchmark, the Standard & Poor’s 500 Index, as well as the average return for its large-capitalization core fund peers.

The fund posted double-digit results in all ten market sectors for the 12-month period. Stocks in the information technology, financial, and consumer discretionary sectors were among the strongest performers.

Note: If you hold shares in a taxable account, you may wish to review the table and discussion of after-tax returns for the fiscal year, based on the highest tax braket, later in this report.

Stocks notched a powerful rally, with help from central bankers

U.S. stocks surged 30% in the 12 months ended September 30, 2012, outpacing the gains of their international counterparts. The rally came amid moves by U.S. and European central bankers to quiet—at least temporarily—investors’ concerns about the U.S. economy and the finances of European governments and banks.

2

Although U.S. stocks were the standouts, European and emerging markets stocks also posted double-digit results. The developed markets of the Pacific region were the weakest performers but still recorded a modest advance.

In July, the president of the European Central Bank declared that policymakers would do whatever was needed to preserve the euro common currency.

That pronouncement was encouraging to investors, but Europe’s financial troubles are by no means resolved. Vanguard economists believe the most likely scenario is that the Eurozone will “muddle through” for several years, with occasional spikes in market volatility, as fiscal tightening continues in the face of weak economic growth.

| Market Barometer | |||

| Average Annual Total Returns | |||

| Periods Ended September 30, 2012 | |||

| One | Three | Five | |

| Year | Years | Years | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | 30.06% | 13.27% | 1.22% |

| Russell 2000 Index (Small-caps) | 31.91 | 12.99 | 2.21 |

| Dow Jones U.S. Total Stock Market Index | 30.00 | 13.29 | 1.53 |

| MSCI All Country World Index ex USA (International) | 14.48 | 3.17 | -4.12 |

| Bonds | |||

| Barclays U.S. Aggregate Bond Index (Broad taxable market) | 5.16% | 6.19% | 6.53% |

| Barclays Municipal Bond Index (Broad tax-exempt market) | 8.32 | 5.99 | 6.06 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.05 | 0.08 | 0.63 |

| CPI | |||

| Consumer Price Index | 1.99% | 2.33% | 2.11% |

3

Bonds produced solid returns; future results may be more muted

Bonds once again advanced; the broad U.S. taxable market returned about 5% for the 12 months. Among U.S. Treasuries, long-term bonds were particularly strong as they benefited from the Federal Reserve’s bond-buying program.

As bond prices rose, the yield of the 10-year U.S. Treasury note fell to a record low in July, closing below 1.5%. (Bond yields and prices move in opposite directions.) By the end of the period, the yield had climbed, but it still remained low by historical standards.

Bondholders have enjoyed years of strong returns. But as Tim Buckley, our incoming chief investment officer, has noted, investors shouldn’t be surprised if future results are much more modest. As yields tumble, the scope for further declines—and price increases—diminishes.

The Federal Reserve announced on September 13 that it would continue to hold its target for short-term interest rates between 0% and 0.25% at least through mid-2015. The exceptionally low rates, in place since late 2008, kept a tight lid on returns from money market funds and savings accounts.

| Expense Ratios | |||

| Your Fund Compared With Its Peer Group | |||

| Investor | Admiral | Peer Group | |

| Shares | Shares | Average | |

| Growth and Income Fund | 0.34% | 0.23% | 1.19% |

The fund expense ratios shown are from the prospectus dated January 26, 2012, and represent estimated costs for the current fiscal year. For the fiscal year ended September 30, 2012, the fund’s expense ratios were 0.36% for Investor Shares and 0.25% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2011.

Peer group: Large-Cap Core Funds.

4

Strong stock selection boosted the fund’s returns

Vanguard Growth and Income Fund seeks to outperform the Standard & Poor’s 500 Index. The fund’s quantitative investment approach results in risk and sector profiles that are similar to those of its benchmark index, while providing broad exposure to a diverse group of large- and mid-cap U.S. companies.

During the past 12 months, the fund met its objective of outpacing the S&P 500 Index while maintaining sector weightings and other portfolio characteristics similar to those of the index. Information technology stocks—which constituted about 20% of the fund’s holdings, on average, during the period—contributed to the advance, adding more than 6 percentage points to total returns. The advisors’ strong stock selection in computer companies—especially those that have capitalized on the high demand for smartphones and tablets—also boosted the fund’s results relative to the benchmark.

Financial and consumer discretionary stocks also added significantly to total returns. Consumer finance stocks and REITs were among the top contributors to the fund’s strong overall showing in financials. The fund’s holdings among insurance firms and diversified financial services companies tempered results somewhat.

| Total Returns | |

| Ten Years Ended September 30, 2012 | |

| Average | |

| Annual Return | |

| Growth and Income Fund Investor Shares | 7.11% |

| S&P 500 Index | 8.01 |

| Large-Cap Core Funds Average | 6.30 |

| Large-Cap Core Funds Average: Derived from data provided by Lipper Inc. |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

5

Within the consumer discretionary category, the shares of retailers, including internet retailers, helped elevate returns. The fund also benefited from its holdings in energy and consumer staples stocks.

An approach designed for competitive performance

For the ten-year period ended September 30, 2012, Investor Shares of Vanguard Growth and Income Fund returned an average of 7.11% a year, trailing the 8.01% average annual return of the fund’s benchmark index. The fund outperformed the 6.30% average annual return of large-cap core funds.

Last year, the fund restructured its advisory arrangement, moving from a single manager to a multimanager approach. The early results have been consistent with our expectation that the fund is well-positioned to deliver competitive long-term returns. The fund’s three talented advisory teams are aided in their efforts by its low costs.

The lessons of the financial crisis remain relevant four years later

In September, the end of your fund’s fiscal year, we marked the fourth anniversary of Lehman Brothers’ collapse, the start of the 2008–2009 financial crisis. When the Lehman news broke, I was speaking to institutional clients at an event in Washington, D.C., all of three weeks into my new role as Vanguard’s CEO.

In the ensuing months, I was struck both by how fortunate I was to work with a great team of Vanguard “crew” and by the remarkable steadiness demonstrated by our clients. Many clients experienced significant losses, but signs of panic were few. On balance, they remained committed to their long-term investment programs and managed to benefit from the financial markets’ subsequent recovery.

As the crisis recedes further in time, it’s important not to lose sight of the lessons that it illuminated about investing and sound financial practices generally. First among those lessons is that diversification does work. Diversification didn’t immunize investors from the market’s decline, but it certainly helped to insulate them from the worst of it.

Second, saving money and living within your means are critical. Investors are acting on this lesson as they pay off debt, which is a form of saving, and increase their savings rates from the dangerously low levels that prevailed before the crisis.

6

Third, having the courage to stick with a sound investment plan—as so many of our clients did—is important during volatile, uncertain times. Investors who resisted the urge to bail out of stocks at the depths of the crisis have largely been rewarded in the succeeding years.

I am very optimistic that, if investors embrace these lessons, they can give themselves a better chance of reaching their long-term goals.

As always, thank you for investing with Vanguard.

Sincerely,

F. William McNabb III

Chairman and Chief Executive Officer

October 11, 2012

7

Advisors’ Report

Vanguard Growth and Income Fund’s Investor Shares returned 31.27% for the 12 months ended September 30, 2012. The Admiral Shares returned 31.40%. The benchmark S&P 500 Index returned 30.20%, while the average return of large-cap core funds was 27.34%.

Your fund is managed by three independent advisors, a strategy that enhances the fund’s diversification by providing exposure to distinct, yet complementary, investment approaches. It is not uncommon for different advisors

to have different views about individual securities or the broader investment environment.

The advisors, the percentage of fund assets each manages, and brief descriptions of their investment strategies are presented in the table below. The advisors have also prepared a discussion of the investment environment that existed during the fiscal year and of how the portfolio’s positioning reflects this assessment. These comments were prepared on October 17, 2012.

| Vanguard Growth and Income Fund Investment Advisors | |||

| Fund Assets Managed | |||

| Investment Advisor | % | $ Million | Investment Strategy |

| Vanguard Equity Investment | 33 | 1,446 | Employs a quantitative, fundamental management |

| Group | approach, using models that assess valuation, growth | ||

| prospects, management decisions, market sentiment, | |||

| and earnings quality of companies versus their peers. | |||

| D. E. Shaw Investment | 33 | 1,442 | Employs quantitative models that seek to capture |

| Management, L.L.C. | predominantly “bottom up” stock-specific return | ||

| opportunities while aiming to keep the portfolio’s | |||

| sector weights, size, and style characteristics similar to | |||

| the benchmark. | |||

| Los Angeles Capital | 33 | 1,432 | Employs a quantitative model that emphasizes stocks |

| with characteristics investors are currently seeking and | |||

| underweights stocks with characteristics investors are | |||

| currently avoiding. The portfolio’s sector weights, size, | |||

| and style characteristics may differ modestly from the | |||

| benchmark in a risk-controlled manner. | |||

| Cash Investments | 1 | 69 | These short-term reserves are invested by Vanguard in |

| equity index products to simulate investments in | |||

| stocks. Each advisor also may maintain a modest cash | |||

| position. | |||

8

D. E. Shaw Investment Management, L.L.C.

Portfolio Manager:

Anthony Foley, Managing Director and Chief Investment Officer

Macroeconomic pressures such as Europe’s sovereign-debt crisis and concerns about slowing growth, particularly in the United States, significantly affected U.S. equity markets during the fiscal year. The European crisis dominated perceptions of equity valuations in the early part of the fourth quarter of 2011. However, positive news suggesting that the U.S. economy was recovering, albeit slowly, began to outweigh negative news from Europe toward the end of the fourth quarter. This appeared to help drive equity markets higher, and that trend continued through the first quarter of 2012 amid signs that the U.S. economy was gaining strength.

The start of the second quarter saw investor sentiment shift as markets pulled back from the “risk-on” trade that dominated the first quarter. Those macro headwinds abated to some extent in the third quarter when the European Central Bank unveiled new policy initiatives to address the Eurozone crisis, the U.S. Federal Reserve announced another round of quantitative easing, and considerable speculation swirled that China would relax monetary policy to reinvigorate economic growth.

We generally attribute portfolio performance to three major sources: bottom-up stock selection; exposure to common risk factors such as value, growth, and market capitalization; and exposure to industry groups. Based on our analysis, the vast majority of our portfolio’s performance was attributable to stock selection. Among the biggest contributors to the portfolio’s excess return over the period were overweight positions in Apple, Marathon Petroleum, and priceline.com. The three largest single-stock detractors from excess return were overweights in Marvell Technology Group, International Flavors & Fragrances, and Occidental Petroleum.

Common risk factors had a modest positive net impact on the portfolio’s relative performance. The largest single positive contribution was a modest tilt toward stocks with high earnings estimates, and the largest detractor was a tilt toward higher-volatility stocks. Industry and sector exposures modestly influenced excess return. The net impact of sector and industry deviations from benchmark weights on portfolio returns over the fiscal year was modestly positive. The largest positive contributor to excess return was the building supplies industry; the largest detractor was the drug research, biotechnology, and therapeutics industry.

9

We believe that substantial disappointment about prospects for economic growth in the United States and globally in general or a resurgence of concerns about Europe’s debt crisis—or both—remain clear risks. Furthermore, absent a concrete plan by the U.S. government to address the federal deficit, the consequences of the so-called fiscal cliff—that is, reduced government outlays and the expiration of certain tax cuts—could play an increasingly important role in the deliberations of market participants in coming quarters.

Los Angeles Capital

Portfolio Managers:

Thomas D. Stevens, CFA, Chairman and Principal

Hal W. Reynolds, CFA,

Chief Investment Officer and Principal

The S&P 500 Index gained 30.20% for the fiscal year ended September 30, 2012, generating significant gains in three out of four quarters. Market participation was broad, with all sectors except utilities generating returns exceeding 20%. With downward revisions in global growth rates, the European Central Bank and the Federal Reserve have taken aggressive steps to ward off deflationary risks. Over the past 18 months, long-term U.S. Treasury yields fell from 4.51% to 2.83%, with real yields falling from 1.88% to only 0.43%. Despite lower growth rates and an expectation of negative earnings growth for S&P 500 constituents for the trailing year, the surge in prices suggests that investors think the Fed will ultimately succeed in stimulating growth without introducing unwanted inflation.

An analysis of equity factors over this period shows that size, momentum, and earnings quality contributed positively to return. The largest companies with strong balance sheets, higher-quality earnings, and positive estimate revisions generally performed the best. The banking industry benefited most directly from the Fed’s aggressive steps, rising 48%. Although riskier, more volatile securities rebounded in anticipation of monetary easing, it is interesting to note that the market again turned cautious one day after the Fed’s September 13 announcement of the third round of easing, suggesting that the Fed’s influence in supporting asset prices may be nearing an end.

Equity risk as measured by the Chicago Board Options Exchange Volatility Index fell from 38.8% one year ago to 15.7% at the end of September, a level close to the index’s long-term average. Although falling volatilities suggest that investors’ financial concerns have for the moment subsided, investors must further recognize that three significant risks are on the horizon. First, how will fiscal deleveraging affect growth rates? Second, how will central banks control inflation when growth rates pick up? And finally, how will increased regulation in the financial and health care sectors affect productivity?

Over the 12-month period, the portfolio maintained its bias toward higher-quality, lower-beta securities. Portfolio attribution shows that an underweighting in four large banks—JP Morgan Chase, Wells Fargo, Bank of America, and Citigroup—detracted from returns. Adding value was positive stock selection in technology, consumer

10

staples, consumer discretionary, and utilities, where we favored larger-cap companies with high earnings quality.

Despite strong equity returns over the past year, our models remain defensive. We continue to favor larger companies with strong balance sheets and high earnings quality and above-average payout ratios. We remain underweighted in riskier, more speculative companies. Our largest sector overweight is in finance, and our largest underweights are in energy and technology.

Vanguard Equity Investment Group

Portfolio Managers:

James D. Troyer, CFA, Principal

James P. Stetler, Principal

Michael R. Roach, CFA

For the 12-month period ended September 30, 2012, the Growth and Income Fund’s Investor Shares returned 31.27%, outperforming the fund’s benchmark’s gain of 30.20%. The full fiscal year presented two very different halves. For the first six months, large-cap stocks, the focus of your investment in the fund, rose sharply, gaining almost 26%. By the second half, however, the market’s momentum slowed dramatically, moving ahead by 3%. Although all ten sector groups generated positive returns within the benchmark, results were best in consumer discretionary, telecommunications, and financial companies. Utilities and consumer staples results were the laggards within the large-cap stock universe.

Equity markets have staged quite a rally since last fall, but investor concerns and economic uncertainty are still prominent. The United States faces a “fiscal cliff” scenario that could send us into recession if not resolved, and investors have renewed worries over the Eurozone crisis and slowing growth in China. Add to that stagnant employment, election-year uncertainty, and a lack of clarity on corporate profits, and it’s easy to see why investors’ appetite for riskier assets may be put on hold for a while. Market volatility, though it declined substantially during this period, is likely to persist amid our unresolved budget, deficit, and employment problems and anemic world economic growth.

Although it’s important to understand how these macro factors affect overall portfolio performance, our approach to investing focuses on specific stock fundamentals and employs five components:

• Valuation, which measures the price we pay for earnings and cash flows.

• Growth, which considers the growth of earnings as a factor in how much we pay for them.

• Management decisions, which assesses the actions taken by company management that signal its informed opinions regarding a firm’s prospects and earnings.

• Market sentiment, which captures how investors reflect their opinions of a company through their activity in the market.

11

• Quality, which measures balance-sheet strength and the sustainability of earnings.

Our risk-control process then neutralizes our exposure to market capitalization, volatility, and industry risks relative to our benchmark. In our view, the rewards available do not justify such risk exposures.

The results from our stock selection model continued the trend from the first six months of the year. Our quality and management decisions indicators were effective in distinguishing the outperformers from the underperformers, whereas our valuation indicator was ineffective and detracted from our results. The portfolio experienced modest gains from our growth and market sentiment signals.

The model’s effectiveness across sectors was strong, as we produced positive stock selection results in seven of the ten sectors in the benchmark. The materials, consumer discretionary, and energy sectors in the portfolio performed the best. Utilities, health care, and consumer staples underperformed.

At the individual stock level, the largest contributors came from overweight positions in Marathon Petroleum, CF Industries, and Constellation Brands. In addition, when comparing the portfolio’s performance to that of its benchmark, we benefited from underweighting or avoiding poor-performing stocks such as Hewlett-Packard, Electronic Arts, and Unum Group.

Unfortunately, we could not avoid all poor performers. Overweight positions in Helmerich & Payne and Goodyear Tire & Rubber directly lowered performance. Underweighting companies such as Walt Disney, Google, and Visa that our model’s fundamentals did not positively identify hurt our overall outperformance relative to our benchmark.

Although we cannot predict how broader political or economic events will affect the markets, we are confident that the stock market will provide worthwhile returns for long-term investors. With that in mind, we believe that equity exposure will continue to play an important part in a diversified investment plan.

We thank you for your investment and look forward to the new fiscal year.

12

Growth and Income Fund

Fund Profile

As of September 30, 2012

| Share-Class Characteristics | ||

| Investor | Admiral | |

| Shares | Shares | |

| Ticker Symbol | VQNPX | VGIAX |

| Expense Ratio1 | 0.34% | 0.23% |

| 30-Day SEC Yield | 1.93% | 2.04% |

| Portfolio Characteristics | |||

| DJ | |||

| U.S. Total | |||

| S&P 500 | Market | ||

| Fund | Index | Index | |

| Number of Stocks | 841 | 500 | 3,638 |

| Median Market Cap | $65.4B | $57.5B | $35.6B |

| Price/Earnings Ratio | 15.4x | 16.1x | 17.0x |

| Price/Book Ratio | 2.2x | 2.2x | 2.2x |

| Return on Equity | 18.5% | 19.3% | 18.0% |

| Earnings Growth Rate | 10.8% | 10.6% | 10.4% |

| Dividend Yield | 2.3% | 2.1% | 2.0% |

| Foreign Holdings | 0.1% | 0.0% | 0.0% |

| Turnover Rate | 102% | — | — |

| Short-Term Reserves | 0.4% | — | — |

| Sector Diversification (% of equity exposure) | |||

| DJ | |||

| U.S. Total | |||

| S&P 500 | Market | ||

| Fund | Index | Index | |

| Consumer Discretionary | 11.6% | 11.0% | 12.0% |

| Consumer Staples | 10.5 | 10.9 | 9.5 |

| Energy | 10.8 | 11.3 | 10.4 |

| Financials | 16.1 | 14.6 | 16.0 |

| Health Care | 11.5 | 12.0 | 11.9 |

| Industrials | 9.6 | 9.8 | 10.6 |

| Information Technology | 20.2 | 20.1 | 19.2 |

| Materials | 3.0 | 3.5 | 3.9 |

| Telecommunication | |||

| Services | 3.3 | 3.3 | 2.9 |

| Utilities | 3.4 | 3.5 | 3.6 |

| Volatility Measures | ||

| DJ | ||

| U.S. Total | ||

| S&P 500 | Market | |

| Index | Index | |

| R-Squared | 0.99 | 0.99 |

| Beta | 1.01 | 0.96 |

These measures show the degree and timing of the fund’s fluctuations compared with the indexes over 36 months.

| Ten Largest Holdings (% of total net assets) | ||

| Apple Inc. | Computer Hardware | 4.9% |

| Exxon Mobil Corp. | Integrated Oil & Gas | 3.4 |

| General Electric Co. | Industrial | |

| Conglomerates | 2.3 | |

| AT&T Inc. | Integrated | |

| Telecommunication | ||

| Services | 2.1 | |

| Pfizer Inc. | Pharmaceuticals | 2.0 |

| International Business | IT Consulting & | |

| Machines Corp. | Other Services | 2.0 |

| Chevron Corp. | Integrated Oil & Gas | 1.9 |

| Microsoft Corp. | Systems Software | 1.9 |

| Philip Morris | ||

| International Inc. | Tobacco | 1.8 |

| Wells Fargo & Co. | Diversified Banks | 1.7 |

| Top Ten | 24.0% | |

The holdings listed exclude any temporary cash investments and equity index products.

Investment Focus

1 The expense ratios shown are from the prospectus dated January 26, 2012, and represent estimated costs for the current fiscal year. For the fiscal year ended September 30, 2012, the expense ratios were 0.36% for Investor Shares and 0.25% for Admiral Shares.

13

Growth and Income Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

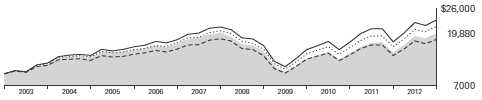

Cumulative Performance: September 30, 2002, Through September 30, 2012

Initial Investment of $10,000

| Average Annual Total Returns | |||||

| Periods Ended September 30, 2012 | |||||

| Final Value | |||||

| One | Five | Ten | of a $10,000 | ||

| Year | Years | Years | Investment | ||

| Growth and Income Fund Investor | |||||

| Shares | 31.27% | -0.23% | 7.11% | $19,880 | |

| •••••••• | S&P 500 Index | 30.20 | 1.05 | 8.01 | 21,615 |

| – – – – | Large-Cap Core Funds Average | 27.34 | -0.19 | 6.30 | 18,427 |

| Dow Jones U.S. Total Stock Market | |||||

| Index | 30.00 | 1.53 | 8.77 | 23,184 | |

| Large-Cap Core Funds Average: Derived from data provided by Lipper Inc. | |||||

| Final Value | ||||

| One | Five | Ten | of a $50,000 | |

| Year | Years | Years | Investment | |

| Growth and Income Fund Admiral Shares | 31.40% | -0.11% | 7.26% | $100,811 |

| S&P 500 Index | 30.20 | 1.05 | 8.01 | 108,075 |

| Dow Jones U.S. Total Stock Market Index | 30.00 | 1.53 | 8.77 | 115,920 |

See Financial Highlights for dividend and capital gains information.

14

Growth and Income Fund

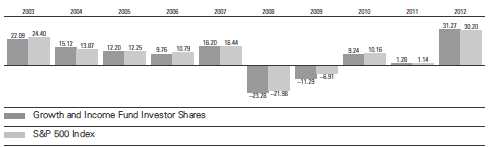

Fiscal-Year Total Returns (%): September 30, 2002, Through September 30, 2012

15

Growth and Income Fund

Financial Statements

Statement of Net Assets

As of September 30, 2012

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Common Stocks (98.2%)1 | |||

| Consumer Discretionary (11.4%) | |||

| Home Depot Inc. | 700,632 | 42,297 | |

| Comcast Corp. Class A | 1,096,508 | 39,222 | |

| Wyndham Worldwide | |||

| Corp. | 519,234 | 27,249 | |

| McDonald’s Corp. | 270,524 | 24,821 | |

| * | DIRECTV | 426,957 | 22,398 |

| * | O’Reilly Automotive Inc. | 252,746 | 21,135 |

| * | Amazon.com Inc. | 79,430 | 20,201 |

| Viacom Inc. Class B | 354,210 | 18,982 | |

| TJX Cos. Inc. | 408,947 | 18,317 | |

| Walt Disney Co. | 321,125 | 16,788 | |

| Gap Inc. | 424,116 | 15,175 | |

| Macy’s Inc. | 363,300 | 13,667 | |

| * | priceline.com Inc. | 21,643 | 13,391 |

| Lowe’s Cos. Inc. | 437,100 | 13,218 | |

| Time Warner Cable Inc. | 136,300 | 12,957 | |

| CBS Corp. Class B | 314,504 | 11,426 | |

| Time Warner Inc. | 242,545 | 10,995 | |

| * | Goodyear Tire & Rubber | ||

| Co. | 658,395 | 8,026 | |

| News Corp. Class A | 323,518 | 7,936 | |

| Newell Rubbermaid Inc. | 414,200 | 7,907 | |

| Expedia Inc. | 136,340 | 7,886 | |

| * | AutoZone Inc. | 20,024 | 7,402 |

| Coach Inc. | 131,610 | 7,373 | |

| Harley-Davidson Inc. | 172,800 | 7,322 | |

| NIKE Inc. Class B | 69,960 | 6,640 | |

| Target Corp. | 91,694 | 5,820 | |

| Whirlpool Corp. | 67,300 | 5,580 | |

| Cablevision Systems Corp. | |||

| Class A | 342,074 | 5,422 | |

| H&R Block Inc. | 294,200 | 5,098 | |

| Ford Motor Co. | 472,400 | 4,658 | |

| * | TripAdvisor Inc. | 136,436 | 4,493 |

| Limited Brands Inc. | 86,810 | 4,276 | |

| Starbucks Corp. | 83,717 | 4,249 | |

| Ralph Lauren Corp. Class A | 27,733 | 4,194 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Genuine Parts Co. | 65,966 | 4,026 | |

| Washington Post Co. | |||

| Class B | 10,800 | 3,921 | |

| Best Buy Co. Inc. | 136,100 | 2,340 | |

| Ross Stores Inc. | 35,580 | 2,298 | |

| * | NVR Inc. | 2,700 | 2,280 |

| Nordstrom Inc. | 41,222 | 2,275 | |

| Family Dollar Stores Inc. | 33,771 | 2,239 | |

| Marriott International Inc. | |||

| Class A | 49,800 | 1,947 | |

| * | AutoNation Inc. | 44,140 | 1,928 |

| Gannett Co. Inc. | 98,914 | 1,756 | |

| * | Dollar Tree Inc. | 36,280 | 1,751 |

| * | Discovery | ||

| Communications Inc. | 28,300 | 1,586 | |

| Kohl’s Corp. | 28,400 | 1,455 | |

| Yum! Brands Inc. | 20,300 | 1,347 | |

| * | Bed Bath & Beyond Inc. | 20,900 | 1,317 |

| Harman International | |||

| Industries Inc. | 28,500 | 1,316 | |

| Starwood Hotels & | |||

| Resorts Worldwide Inc. | 22,000 | 1,275 | |

| * | Fossil Inc. | 14,000 | 1,186 |

| * | Sears Holdings Corp. | 20,700 | 1,149 |

| Omnicom Group Inc. | 20,700 | 1,067 | |

| Ameristar Casinos Inc. | 57,480 | 1,023 | |

| * | Chipotle Mexican Grill Inc. | ||

| Class A | 3,140 | 997 | |

| Hasbro Inc. | 22,807 | 871 | |

| Domino’s Pizza Inc. | 20,200 | 762 | |

| Six Flags Entertainment | |||

| Corp. | 11,346 | 667 | |

| * | Fifth & Pacific Cos. Inc. | 49,600 | 634 |

| Wynn Resorts Ltd. | 5,475 | 632 | |

| * | Penn National Gaming Inc. | 14,300 | 616 |

| * | Imax Corp. | 25,674 | 511 |

| * | Live Nation Entertainment | ||

| Inc. | 54,080 | 466 | |

| * | Orbitz Worldwide Inc. | 180,221 | 460 |

16

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| International Game | |||

| Technology | 32,700 | 428 | |

| * | Charter Communications Inc. | ||

| Class A | 5,600 | 420 | |

| * | Boyd Gaming Corp. | 57,700 | 407 |

| * | Big Lots Inc. | 13,168 | 390 |

| Movado Group Inc. | 11,100 | 374 | |

| * | Apollo Group Inc. Class A | 9,800 | 285 |

| * | Biglari Holdings Inc. | 746 | 272 |

| * | Liberty Media Corp. - | ||

| Liberty Capital Class A | 2,200 | 229 | |

| Signet Jewelers Ltd. | 4,300 | 210 | |

| Interpublic Group of | |||

| Cos. Inc. | 18,535 | 206 | |

| Churchill Downs Inc. | 2,800 | 176 | |

| * | Netflix Inc. | 3,200 | 174 |

| * | Beazer Homes USA Inc. | 48,500 | 172 |

| McGraw-Hill Cos. Inc. | 2,965 | 162 | |

| * | Sally Beauty Holdings Inc. | 5,300 | 133 |

| * | Barnes & Noble Inc. | 10,200 | 130 |

| * | Liberty Global Inc. | 2,200 | 124 |

| Scripps Networks | |||

| Interactive Inc. Class A | 1,900 | 116 | |

| * | Discovery Communications | ||

| Inc. Class A | 1,950 | 116 | |

| Abercrombie & Fitch Co. | 3,400 | 115 | |

| * | Liberty Global Inc. Class A | 1,812 | 110 |

| Ethan Allen Interiors Inc. | 4,300 | 94 | |

| * | Office Depot Inc. | 26,100 | 67 |

| * | Pinnacle Entertainment Inc. | 4,880 | 60 |

| * | American Apparel Inc. | 38,397 | 59 |

| * | Sears Hometown and | ||

| Outlet Stores Inc. | |||

| Rights Exp. 10/3/12 | 21,600 | 59 | |

| * | Carter’s Inc. | 1,091 | 59 |

| Blyth Inc. | 2,200 | 57 | |

| Christopher & Banks Corp. | 16,200 | 57 | |

| * | Bloomin’ Brands Inc. | 3,300 | 54 |

| GameStop Corp. Class A | 2,400 | 50 | |

| * | LodgeNet Interactive Corp. | 75,900 | 49 |

| Lear Corp. | 1,300 | 49 | |

| * | Capella Education Co. | 1,200 | 42 |

| * | Overstock.com Inc. | 4,000 | 41 |

| RadioShack Corp. | 16,700 | 40 | |

| * | New York & Co. Inc. | 9,565 | 36 |

| * | Pandora Media Inc. | 3,200 | 35 |

| Hooker Furniture Corp. | 2,584 | 34 | |

| * | Cumulus Media Inc. Class A | 12,198 | 33 |

| * | Career Education Corp. | 7,649 | 29 |

| Ambassadors Group Inc. | 5,104 | 28 | |

| * | Exide Technologies | 8,800 | 27 |

| * | Isle of Capri Casinos Inc. | 3,462 | 24 |

| * | Carmike Cinemas Inc. | 1,875 | 21 |

| * | Lee Enterprises Inc. | 14,075 | 21 |

| * | Build-A-Bear Workshop Inc. | 3,780 | 15 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | American Public Education | ||

| Inc. | 400 | 15 | |

| * | G-III Apparel Group Ltd. | 400 | 14 |

| AH Belo Corp. Class A | 2,937 | 14 | |

| Universal Technical | |||

| Institute Inc. | 889 | 12 | |

| * | Ascena Retail Group Inc. | 500 | 11 |

| * | Kirkland’s Inc. | 950 | 9 |

| * | Pacific Sunwear of | ||

| California Inc. | 3,700 | 9 | |

| * | Meritage Homes Corp. | 200 | 8 |

| * | Coldwater Creek Inc. | 9,000 | 7 |

| * | Blue Nile Inc. | 199 | 7 |

| * | Chuy’s Holdings Inc. | 300 | 7 |

| Lennar Corp. Class A | 197 | 7 | |

| Nutrisystem Inc. | 617 | 6 | |

| * | Furniture Brands | ||

| International Inc. | 4,200 | 6 | |

| * | Valuevision Media | ||

| Inc. Class A | 2,463 | 6 | |

| Standard Motor Products Inc. | 295 | 5 | |

| * | Five Below Inc. | 136 | 5 |

| * | School Specialty Inc. | 2,200 | 5 |

| American Greetings Corp. | |||

| Class A | 300 | 5 | |

| * | Corinthian Colleges Inc. | 2,000 | 5 |

| * | Reading International Inc. | ||

| Class A | 800 | 5 | |

| * | Education Management Corp. | 1,300 | 4 |

| * | rue21 inc | 120 | 4 |

| * | Body Central Corp. | 300 | 3 |

| * | Express Inc. | 200 | 3 |

| * | Vitacost.com Inc. | 317 | 2 |

| * | MTR Gaming Group Inc. | 500 | 2 |

| Fred’s Inc. Class A | 100 | 1 | |

| * | Summer Infant Inc. | 500 | 1 |

| 498,696 | |||

| Consumer Staples (10.3%) | |||

| Philip Morris | |||

| International Inc. | 860,881 | 77,428 | |

| Procter & Gamble Co. | 901,360 | 62,518 | |

| Wal-Mart Stores Inc. | 588,019 | 43,396 | |

| Coca-Cola Co. | 1,137,734 | 43,154 | |

| CVS Caremark Corp. | 640,540 | 31,015 | |

| Kraft Foods Inc. | 681,310 | 28,172 | |

| Altria Group Inc. | 736,048 | 24,577 | |

| PepsiCo Inc. | 325,851 | 23,060 | |

| Kroger Co. | 713,492 | 16,796 | |

| Kimberly-Clark Corp. | 160,431 | 13,762 | |

| Costco Wholesale Corp. | 131,370 | 13,153 | |

| Reynolds American Inc. | 237,542 | 10,295 | |

| Walgreen Co. | 251,100 | 9,150 | |

| * | Dean Foods Co. | 553,630 | 9,052 |

| Colgate-Palmolive Co. | 73,932 | 7,927 | |

17

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Constellation Brands Inc. | ||

| Class A | 190,900 | 6,176 | |

| Lorillard Inc. | 42,439 | 4,942 | |

| Dr Pepper Snapple Group | |||

| Inc. | 92,301 | 4,110 | |

| Mead Johnson Nutrition Co. | 48,385 | 3,546 | |

| General Mills Inc. | 86,350 | 3,441 | |

| Sysco Corp. | 102,599 | 3,208 | |

| HJ Heinz Co. | 38,890 | 2,176 | |

| Estee Lauder Cos. Inc. | |||

| Class A | 35,221 | 2,169 | |

| Beam Inc. | 29,400 | 1,692 | |

| Hormel Foods Corp. | 43,700 | 1,278 | |

| Clorox Co. | 16,440 | 1,185 | |

| Campbell Soup Co. | 19,700 | 686 | |

| ConAgra Foods Inc. | 21,403 | 591 | |

| ^ | SUPERVALU Inc. | 164,000 | 395 |

| Avon Products Inc. | 21,500 | 343 | |

| Tyson Foods Inc. Class A | 17,100 | 274 | |

| * | Smart Balance Inc. | 10,913 | 132 |

| Hershey Co. | 1,807 | 128 | |

| Kellogg Co. | 1,607 | 83 | |

| * | Monster Beverage Corp. | 1,400 | 76 |

| * | Cott Corp. | 6,100 | 48 |

| B&G Foods Inc. Class A | 1,000 | 30 | |

| Energizer Holdings Inc. | 300 | 22 | |

| * | Post Holdings Inc. | 700 | 21 |

| * | Dole Food Co. Inc. | 800 | 11 |

| * | Natural Grocers by Vitamin | ||

| Cottage Inc. | 467 | 10 | |

| Safeway Inc. | 400 | 6 | |

| Archer-Daniels-Midland Co. | 200 | 5 | |

| * | Synutra International Inc. | 800 | 4 |

| 450,243 | |||

| Energy (10.6%) | |||

| Exxon Mobil Corp. | 1,610,014 | 147,236 | |

| Chevron Corp. | 719,642 | 83,881 | |

| ConocoPhillips | 661,894 | 37,847 | |

| Occidental Petroleum Corp. | 363,295 | 31,265 | |

| Marathon Petroleum Corp. | 476,300 | 26,001 | |

| Schlumberger Ltd. | 347,419 | 25,129 | |

| Phillips 66 | 472,102 | 21,891 | |

| National Oilwell Varco Inc. | 168,775 | 13,521 | |

| Anadarko Petroleum Corp. | 180,096 | 12,592 | |

| EOG Resources Inc. | 100,900 | 11,306 | |

| Williams Cos. Inc. | 284,900 | 9,963 | |

| Spectra Energy Corp. | 261,830 | 7,687 | |

| Marathon Oil Corp. | 241,600 | 7,144 | |

| Devon Energy Corp. | 98,891 | 5,983 | |

| Tesoro Corp. | 86,750 | 3,635 | |

| Kinder Morgan Inc. | 93,480 | 3,320 | |

| Valero Energy Corp. | 81,300 | 2,576 | |

| Halliburton Co. | 73,895 | 2,490 | |

| Murphy Oil Corp. | 37,840 | 2,032 | |

| * | Nabors Industries Ltd. | 133,900 | 1,879 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Denbury Resources Inc. | 94,300 | 1,524 |

| Nexen Inc. | 55,100 | 1,396 | |

| * | Cameron International Corp. | 15,600 | 875 |

| Hess Corp. | 12,900 | 693 | |

| * | WPX Energy Inc. | 32,599 | 541 |

| Diamond Offshore | |||

| Drilling Inc. | 7,700 | 507 | |

| Baker Hughes Inc. | 6,829 | 309 | |

| * | Hercules Offshore Inc. | 50,300 | 245 |

| * | SemGroup Corp. Class A | 6,600 | 243 |

| SandRidge Mississippian | |||

| Trust II | 11,500 | 234 | |

| Peabody Energy Corp. | 7,296 | 163 | |

| W&T Offshore Inc. | 8,600 | 161 | |

| * | Cheniere Energy Inc. | 10,200 | 159 |

| * | Ocean Rig UDW Inc. | 9,458 | 154 |

| * | Renewable Energy Group | ||

| Inc. | 11,100 | 74 | |

| * | Lone Pine Resources Inc. | 33,028 | 52 |

| * | Halcon Resources Corp. | 5,100 | 37 |

| * | Willbros Group Inc. | 4,900 | 26 |

| * | Cal Dive International Inc. | 13,600 | 21 |

| * | Kosmos Energy Ltd. | 1,400 | 16 |

| Noble Energy Inc. | 169 | 16 | |

| * | Uranium Resources Inc. | 29,100 | 15 |

| Noble Corp. | 400 | 14 | |

| * | McDermott International Inc. | 1,000 | 12 |

| * | EPL Oil & Gas Inc. | 600 | 12 |

| * | Amyris Inc. | 3,400 | 12 |

| * | Oil States International Inc. | 100 | 8 |

| * | ZaZa Energy Corp. | 2,464 | 7 |

| * | Endeavour International Corp. | 700 | 7 |

| QEP Resources Inc. | 200 | 6 | |

| * | Newfield Exploration Co. | 200 | 6 |

| * | Rentech Inc. | 2,500 | 6 |

| CONSOL Energy Inc. | 200 | 6 | |

| * | Harvest Natural Resources | ||

| Inc. | 600 | 5 | |

| * | Alpha Natural Resources Inc. | 814 | 5 |

| * | Gevo Inc. | 1,200 | 3 |

| DHT Holdings Inc. | 300 | 2 | |

| * | Houston American Energy | ||

| Corp. | 1,404 | 1 | |

| 464,951 | |||

| Exchange-Traded Fund (0.1%) | |||

| SPDR S&P 500 ETF Trust | 45,400 | 6,534 | |

| Financials (15.8%) | |||

| Wells Fargo & Co. | 2,144,180 | 74,039 | |

| JPMorgan Chase & Co. | 1,471,411 | 59,563 | |

| * | American International | ||

| Group Inc. | 1,189,390 | 39,000 | |

| * | Berkshire Hathaway Inc. | ||

| Class B | 404,924 | 35,714 | |

| US Bancorp | 1,041,024 | 35,707 | |

18

Growth and Income Fund

| Market | ||

| Value | ||

| Shares | ($000) | |

| Bank of America Corp. | 3,996,930 | 35,293 |

| American Express Co. | 516,585 | 29,373 |

| Citigroup Inc. | 720,900 | 23,588 |

| Goldman Sachs Group Inc. | 174,050 | 19,786 |

| CME Group Inc. | 286,290 | 16,404 |

| Discover Financial Services | 389,370 | 15,470 |

| Torchmark Corp. | 280,900 | 14,424 |

| Simon Property Group Inc. | 94,600 | 14,361 |

| Equity Residential | 248,855 | 14,317 |

| Fifth Third Bancorp | 859,100 | 13,325 |

| Marsh & McLennan Cos. | ||

| Inc. | 380,475 | 12,910 |

| Invesco Ltd. | 485,255 | 12,127 |

| State Street Corp. | 287,881 | 12,080 |

| SLM Corp. | 681,956 | 10,720 |

| Allstate Corp. | 250,100 | 9,906 |

| HCP Inc. | 221,345 | 9,845 |

| Assurant Inc. | 215,500 | 8,038 |

| American Tower | ||

| Corporation | 112,455 | 8,028 |

| Public Storage | 51,839 | 7,214 |

| Health Care REIT Inc. | 116,000 | 6,699 |

| Kimco Realty Corp. | 327,320 | 6,635 |

| NASDAQ OMX Group Inc. | 278,642 | 6,491 |

| MetLife Inc. | 185,100 | 6,379 |

| Prudential Financial Inc. | 112,900 | 6,154 |

| Prologis Inc. | 175,300 | 6,141 |

| BB&T Corp. | 183,800 | 6,095 |

| AvalonBay Communities | ||

| Inc. | 43,291 | 5,887 |

| Ameriprise Financial Inc. | 100,884 | 5,719 |

| Progressive Corp. | 267,833 | 5,555 |

| BlackRock Inc. | 30,920 | 5,513 |

| Capital One Financial Corp. | 92,634 | 5,281 |

| Aon plc | 99,800 | 5,219 |

| Host Hotels & Resorts Inc. | 311,400 | 4,998 |

| Legg Mason Inc. | 191,992 | 4,738 |

| T. Rowe Price Group Inc. | 74,701 | 4,729 |

| Travelers Cos. Inc. | 68,216 | 4,656 |

| NYSE Euronext | 175,400 | 4,324 |

| SunTrust Banks Inc. | 138,300 | 3,910 |

| Ventas Inc. | 61,200 | 3,810 |

| Bank of New York Mellon | ||

| Corp. | 167,213 | 3,782 |

| Federated Investors Inc. | ||

| Class B | 173,339 | 3,586 |

| M&T Bank Corp. | 36,689 | 3,491 |

| Plum Creek Timber Co. Inc. | 78,386 | 3,436 |

| Chubb Corp. | 38,409 | 2,930 |

| Hudson City Bancorp Inc. | 331,800 | 2,641 |

| PNC Financial Services | ||

| Group Inc. | 41,439 | 2,615 |

| Unum Group | 134,700 | 2,589 |

| Apartment Investment & | ||

| Management Co. Class A | 90,756 | 2,359 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Loews Corp. | 52,800 | 2,179 | |

| People’s United | |||

| Financial Inc. | 178,492 | 2,167 | |

| Granite Real Estate Inc. | 58,970 | 2,117 | |

| Equity Lifestyle | |||

| Properties Inc. | 30,871 | 2,103 | |

| Morgan Stanley | 91,200 | 1,527 | |

| Erie Indemnity Co. Class A | 22,889 | 1,471 | |

| * | IntercontinentalExchange | ||

| Inc. | 10,500 | 1,401 | |

| * | Genworth Financial Inc. | ||

| Class A | 244,070 | 1,277 | |

| Aflac Inc. | 25,387 | 1,216 | |

| Vornado Realty Trust | 12,300 | 997 | |

| Newcastle Investment | |||

| Corp. | 122,300 | 921 | |

| Huntington Bancshares Inc. | 96,200 | 664 | |

| Northern Trust Corp. | 12,993 | 603 | |

| XL Group plc Class A | 24,467 | 588 | |

| Lincoln National Corp. | 20,039 | 485 | |

| CNO Financial Group Inc. | 47,500 | 458 | |

| Symetra Financial Corp. | 34,800 | 428 | |

| ACE Ltd. | 5,400 | 408 | |

| Prospect Capital Corp. | 30,500 | 351 | |

| * | Alleghany Corp. | 1,000 | 345 |

| Starwood Property Trust Inc. | 13,700 | 319 | |

| American Assets Trust Inc. | 10,853 | 291 | |

| * | NewStar Financial Inc. | 23,000 | 276 |

| * | Popular Inc. | 15,300 | 267 |

| * | First Industrial Realty | ||

| Trust Inc. | 17,800 | 234 | |

| RLI Corp. | 3,200 | 213 | |

| KeyCorp | 22,200 | 194 | |

| Taubman Centers Inc. | 2,300 | 176 | |

| * | eHealth Inc. | 8,950 | 168 |

| * | Central Pacific Financial Corp. | 11,300 | 162 |

| White Mountains | |||

| Insurance Group Ltd. | 300 | 154 | |

| * | First BanCorp | 32,200 | 142 |

| Retail Properties of | |||

| America Inc. | 12,400 | 140 | |

| MarketAxess Holdings Inc. | 4,397 | 139 | |

| Potlatch Corp. | 3,500 | 131 | |

| Endurance Specialty | |||

| Holdings Ltd. | 2,900 | 112 | |

| Washington REIT | 3,500 | 94 | |

| Cash America | |||

| International Inc. | 1,700 | 66 | |

| Medley Capital Corp. | 3,100 | 44 | |

| EverBank Financial Corp. | 2,864 | 39 | |

| United Fire Group Inc. | 1,453 | 37 | |

| * | Ezcorp Inc. Class A | 1,500 | 34 |

| Sterling Financial Corp. | 1,500 | 33 | |

| * | Hilltop Holdings Inc. | 2,400 | 31 |

19

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Healthcare Trust of | |||

| America Inc. | 3,100 | 30 | |

| * | FelCor Lodging Trust Inc. | 5,300 | 25 |

| SeaBright Holdings Inc. | 2,200 | 24 | |

| Kilroy Realty Corp. | 500 | 22 | |

| * | Southwest Bancorp Inc. | 2,042 | 22 |

| RLJ Lodging Trust | 1,100 | 21 | |

| First Financial Bankshares Inc. | 500 | 18 | |

| * | Sunstone Hotel Investors Inc. | 1,600 | 18 |

| * | HomeTrust Bancshares Inc. | 1,300 | 17 |

| Rouse Properties Inc. | 1,200 | 17 | |

| Terreno Realty Corp. | 1,054 | 17 | |

| Willis Group Holdings plc | 400 | 15 | |

| Post Properties Inc. | 300 | 14 | |

| Primerica Inc. | 500 | 14 | |

| Piedmont Office Realty | |||

| Trust Inc. Class A | 800 | 14 | |

| Principal Financial Group Inc. | 507 | 14 | |

| Extra Space Storage Inc. | 400 | 13 | |

| * | Strategic Hotels & | ||

| Resorts Inc. | 1,900 | 11 | |

| Western Asset | |||

| Mortgage Capital Corp. | 500 | 11 | |

| Getty Realty Corp. | 569 | 10 | |

| * | HFF Inc. Class A | 600 | 9 |

| Old Republic International | |||

| Corp. | 900 | 8 | |

| Winthrop Realty Trust | 700 | 8 | |

| Acadia Realty Trust | 299 | 7 | |

| * | Phoenix Cos. Inc. | 226 | 7 |

| * | FBR & Co. | 2,060 | 6 |

| STAG Industrial Inc. | 335 | 5 | |

| Old National Bancorp | 300 | 4 | |

| Provident New York Bancorp | 400 | 4 | |

| FBL Financial Group Inc. | |||

| Class A | 101 | 3 | |

| AmREIT Inc. Class B | 200 | 3 | |

| * | Preferred Bank | 196 | 3 |

| Heritage Financial Group Inc. | 209 | 3 | |

| * | Virginia Commerce | ||

| Bancorp Inc. | 300 | 3 | |

| Investors Real Estate Trust | 300 | 2 | |

| Parkway Properties Inc. | 176 | 2 | |

| NGP Capital Resources Co. | 300 | 2 | |

| * | Global Indemnity plc | 100 | 2 |

| * | Netspend Holdings Inc. | 211 | 2 |

| * | Citizens Republic Bancorp | ||

| Inc. | 100 | 2 | |

| SI Financial Group Inc. | 100 | 1 | |

| MidSouth Bancorp Inc. | 6 | — | |

| 693,229 | |||

| Health Care (11.3%) | |||

| Pfizer Inc. | 3,606,279 | 89,616 | |

| Johnson & Johnson | 861,193 | 59,345 | |

| Merck & Co. Inc. | 1,219,666 | 55,007 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Abbott Laboratories | 468,649 | 32,131 | |

| UnitedHealth Group Inc. | 547,998 | 30,365 | |

| Eli Lilly & Co. | 534,792 | 25,354 | |

| Bristol-Myers Squibb Co. | 611,132 | 20,626 | |

| Amgen Inc. | 184,826 | 15,585 | |

| McKesson Corp. | 170,970 | 14,709 | |

| Baxter International Inc. | 184,868 | 11,140 | |

| Aetna Inc. | 250,320 | 9,913 | |

| WellPoint Inc. | 168,912 | 9,799 | |

| * | Biogen Idec Inc. | 62,949 | 9,394 |

| Covidien plc | 151,900 | 9,026 | |

| * | Celgene Corp. | 115,660 | 8,836 |

| Cardinal Health Inc. | 211,610 | 8,246 | |

| Zimmer Holdings Inc. | 118,300 | 7,999 | |

| * | Mylan Inc. | 312,900 | 7,635 |

| * | DaVita Inc. | 64,300 | 6,662 |

| Thermo Fisher Scientific | |||

| Inc. | 112,711 | 6,631 | |

| Allergan Inc. | 63,300 | 5,797 | |

| * | Gilead Sciences Inc. | 78,800 | 5,227 |

| * | Tenet Healthcare Corp. | 764,185 | 4,791 |

| Medtronic Inc. | 106,410 | 4,588 | |

| Becton Dickinson and Co. | 54,002 | 4,242 | |

| * | Life Technologies Corp. | 86,700 | 4,238 |

| AmerisourceBergen Corp. | |||

| Class A | 102,810 | 3,980 | |

| * | Forest Laboratories Inc. | 109,447 | 3,897 |

| Humana Inc. | 47,716 | 3,347 | |

| * | Alexion Pharmaceuticals | ||

| Inc. | 28,900 | 3,306 | |

| Stryker Corp. | 41,110 | 2,288 | |

| * | XenoPort Inc. | 123,600 | 1,416 |

| * | Intuitive Surgical Inc. | 2,822 | 1,399 |

| * | Boston Scientific Corp. | 212,800 | 1,221 |

| * | CareFusion Corp. | 34,899 | 991 |

| * | Illumina Inc. | 20,100 | 969 |

| * | Allscripts Healthcare | ||

| Solutions Inc. | 50,388 | 626 | |

| HCA Holdings Inc. | 12,502 | 416 | |

| Patterson Cos. Inc. | 11,252 | 385 | |

| * | Medivation Inc. | 6,400 | 361 |

| * | Watson Pharmaceuticals | ||

| Inc. | 4,000 | 341 | |

| Teleflex Inc. | 4,900 | 337 | |

| PerkinElmer Inc. | 9,280 | 273 | |

| * | PharMerica Corp. | 21,100 | 267 |

| * | Emergent Biosolutions Inc. | 17,100 | 243 |

| * | Furiex Pharmaceuticals Inc. | 11,800 | 225 |

| * | Pain Therapeutics Inc. | 41,997 | 212 |

| * | Sequenom Inc. | 59,100 | 209 |

| * | Questcor | ||

| Pharmaceuticals Inc. | 8,400 | 155 | |

| *,^ | StemCells Inc. | 70,751 | 146 |

| * | ViroPharma Inc. | 4,500 | 136 |

| * | Theravance Inc. | 5,200 | 135 |

20

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Threshold | ||

| Pharmaceuticals Inc. | 17,300 | 125 | |

| * | MEDNAX Inc. | 1,600 | 119 |

| * | Idenix Pharmaceuticals Inc. | 19,500 | 89 |

| * | Health Net Inc. | 3,900 | 88 |

| * | Array BioPharma Inc. | 14,451 | 85 |

| * | LCA-Vision Inc. | 20,797 | 84 |

| * | Synta Pharmaceuticals Corp. | 10,172 | 77 |

| * | MedAssets Inc. | 4,076 | 73 |

| * | AMAG Pharmaceuticals Inc. | 4,016 | 71 |

| * | Omeros Corp. | 6,371 | 60 |

| * | Sunesis Pharmaceuticals Inc. | 8,785 | 50 |

| * | HealthSouth Corp. | 2,000 | 48 |

| * | AngioDynamics Inc. | 3,942 | 48 |

| * | Exelixis Inc. | 9,600 | 46 |

| * | Neuralstem Inc. | 34,069 | 43 |

| * | BioDelivery Sciences | ||

| International Inc. | 5,700 | 36 | |

| * | Keryx Biopharmaceuticals | ||

| Inc. | 11,800 | 33 | |

| * | Nanosphere Inc. | 9,700 | 32 |

| * | Optimer Pharmaceuticals | ||

| Inc. | 2,247 | 32 | |

| * | Cambrex Corp. | 2,700 | 32 |

| * | Santarus Inc. | 3,300 | 29 |

| * | TranS1 Inc. | 10,180 | 27 |

| Invacare Corp. | 1,869 | 26 | |

| * | ACADIA Pharmaceuticals | ||

| Inc. | 10,415 | 26 | |

| * | Globus Medical Inc. | 1,400 | 25 |

| * | Achillion Pharmaceuticals Inc. | 2,100 | 22 |

| * | Nymox Pharmaceutical Corp. | 2,800 | 19 |

| * | SIGA Technologies Inc. | 5,900 | 19 |

| * | Infinity Pharmaceuticals Inc. | 800 | 19 |

| * | GTx Inc. | 3,100 | 14 |

| * | Arqule Inc. | 2,647 | 13 |

| * | Staar Surgical Co. | 1,400 | 11 |

| * | Enzon Pharmaceuticals Inc. | 1,520 | 11 |

| �� | Hill-Rom Holdings Inc. | 300 | 9 |

| * | Biosante Pharmaceuticals Inc. | 4,189 | 8 |

| * | Neurocrine Biosciences Inc. | 900 | 7 |

| * | Discovery Laboratories Inc. | 2,100 | 7 |

| * | Hospira Inc. | 200 | 7 |

| * | Alnylam Pharmaceuticals Inc. | 300 | 6 |

| * | Hologic Inc. | 227 | 5 |

| * | Biolase Inc. | 2,350 | 4 |

| * | Myrexis Inc. | 1,550 | 4 |

| * | Pacific Biosciences of | ||

| California Inc. | 2,000 | 4 | |

| * | Repligen Corp. | 612 | 4 |

| * | Rigel Pharmaceuticals Inc. | 300 | 3 |

| * | Anika Therapeutics Inc. | 200 | 3 |

| * | Masimo Corp. | 116 | 3 |

| * | Pozen Inc. | 300 | 2 |

| * | SurModics Inc. | 89 | 2 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Ventrus Biosciences Inc. | 400 | 1 |

| * | Gentiva Health Services Inc. | 101 | 1 |

| * | Accretive Health Inc. | 100 | 1 |

| * | Alimera Sciences Inc. | 400 | 1 |

| 495,797 | |||

| Industrials (9.4%) | |||

| General Electric Co. | 4,425,774 | 100,509 | |

| Union Pacific Corp. | 219,588 | 26,065 | |

| General Dynamics Corp. | 384,481 | 25,422 | |

| United Parcel Service Inc. | |||

| Class B | 296,393 | 21,213 | |

| Lockheed Martin Corp. | 205,574 | 19,197 | |

| Northrop Grumman Corp. | 286,692 | 19,045 | |

| Caterpillar Inc. | 214,821 | 18,483 | |

| Tyco International Ltd. | 326,980 | 18,396 | |

| Raytheon Co. | 314,049 | 17,951 | |

| Boeing Co. | 212,250 | 14,777 | |

| Ingersoll-Rand plc | 249,400 | 11,178 | |

| United Technologies Corp. | 129,350 | 10,127 | |

| Parker Hannifin Corp. | 116,720 | 9,755 | |

| L-3 Communications | |||

| Holdings Inc. | 120,964 | 8,674 | |

| CSX Corp. | 409,686 | 8,501 | |

| Equifax Inc. | 180,000 | 8,384 | |

| Textron Inc. | 306,900 | 8,032 | |

| Emerson Electric Co. | 117,529 | 5,673 | |

| Honeywell International Inc. | 94,169 | 5,627 | |

| 3M Co. | 59,180 | 5,469 | |

| Republic Services Inc. | |||

| Class A | 189,900 | 5,224 | |

| Precision Castparts Corp. | 31,037 | 5,070 | |

| Norfolk Southern Corp. | 61,802 | 3,932 | |

| Southwest Airlines Co. | 443,600 | 3,890 | |

| Xylem Inc. | 119,271 | 3,000 | |

| Cintas Corp. | 67,600 | 2,802 | |

| Covanta Holding Corp. | 136,800 | 2,347 | |

| Cummins Inc. | 25,197 | 2,323 | |

| Waste Management Inc. | 69,500 | 2,230 | |

| Illinois Tool Works Inc. | 36,650 | 2,180 | |

| Pentair Inc. | 42,500 | 1,892 | |

| * | Sensata Technologies | ||

| Holding NV | 51,900 | 1,545 | |

| * | Verisk Analytics Inc. Class A | 30,700 | 1,462 |

| Rockwell Automation Inc. | 18,937 | 1,317 | |

| C.H. Robinson | |||

| Worldwide Inc. | 20,500 | 1,200 | |

| Iron Mountain Inc. | 28,300 | 965 | |

| WW Grainger Inc. | 4,266 | 889 | |

| Fluor Corp. | 14,918 | 840 | |

| Avery Dennison Corp. | 26,100 | 831 | |

| * | Nielsen Holdings NV | 20,200 | 606 |

| Expeditors International | |||

| of Washington Inc. | 16,400 | 596 | |

| AAR Corp. | 32,274 | 530 | |

| * | EnerNOC Inc. | 40,000 | 519 |

21

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Ryder System Inc. | 11,631 | 454 | |

| * | Old Dominion Freight | ||

| Line Inc. | 14,500 | 437 | |

| Robert Half International Inc. | 16,200 | 431 | |

| Dun & Bradstreet Corp. | 5,300 | 422 | |

| * | Genesee & Wyoming Inc. | ||

| Class A | 5,500 | 368 | |

| Pitney Bowes Inc. | 22,300 | 308 | |

| Towers Watson & Co. | |||

| Class A | 5,300 | 281 | |

| * | Babcock & Wilcox Co. | 11,000 | 280 |

| * | Swift Transportation Co. | 32,240 | 278 |

| * | Engility Holdings Inc. | 14,297 | 264 |

| * | Shaw Group Inc. | 6,000 | 262 |

| Stanley Black & Decker Inc. | 3,000 | 229 | |

| * | DigitalGlobe Inc. | 9,309 | 190 |

| * | FuelCell Energy Inc. | 188,700 | 166 |

| Roper Industries Inc. | 1,500 | 165 | |

| Cooper Industries plc | 1,740 | 131 | |

| * | Spirit Aerosystems | ||

| Holdings Inc. Class A | 4,700 | 104 | |

| * | Huntington Ingalls | ||

| Industries Inc. | 2,200 | 93 | |

| US Ecology Inc. | 4,259 | 92 | |

| * | Odyssey Marine | ||

| Exploration Inc. | 26,700 | 84 | |

| * | Fuel Tech Inc. | 20,100 | 84 |

| Costamare Inc. | 4,900 | 75 | |

| * | AerCap Holdings NV | 5,900 | 74 |

| Rollins Inc. | 3,141 | 73 | |

| * | Nortek Inc. | 1,304 | 71 |

| Quad/Graphics Inc. | 4,000 | 68 | |

| Brink’s Co. | 2,200 | 57 | |

| Albany International Corp. | 2,200 | 48 | |

| American Science & | |||

| Engineering Inc. | 682 | 45 | |

| * | Sykes Enterprises Inc. | 3,075 | 41 |

| * | Rexnord Corp. | 2,100 | 38 |

| * | Teledyne Technologies Inc. | 400 | 25 |

| Crane Co. | 600 | 24 | |

| * | Esterline Technologies Corp. | 400 | 22 |

| * | Pendrell Corp. | 18,600 | 21 |

| H&E Equipment | |||

| Services Inc. | 1,400 | 17 | |

| Apogee Enterprises Inc. | 850 | 17 | |

| Star Bulk Carriers Corp. | 27,146 | 16 | |

| * | Federal Signal Corp. | 2,574 | 16 |

| * | American Reprographics Co. | 3,710 | 16 |

| * | CRA International Inc. | 900 | 16 |

| * | Xerium Technologies Inc. | 4,427 | 16 |

| Heartland Express Inc. | 1,100 | 15 | |

| Harsco Corp. | 700 | 14 | |

| Safe Bulkers Inc. | 2,300 | 13 | |

| Mueller Water Products Inc. | |||

| Class A | 2,700 | 13 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | WABCO Holdings Inc. | 200 | 12 |

| Alliant Techsystems Inc. | 200 | 10 | |

| * | NCI Building Systems Inc. | 900 | 9 |

| * | Jacobs Engineering | ||

| Group Inc. | 200 | 8 | |

| * | Pacer International Inc. | 1,949 | 8 |

| Fastenal Co. | 170 | 7 | |

| * | Zipcar Inc. | 900 | 7 |

| Encore Wire Corp. | 233 | 7 | |

| * | Quality Distribution Inc. | 600 | 6 |

| * | GeoEye Inc. | 200 | 5 |

| Kaman Corp. | 135 | 5 | |

| Aceto Corp. | 482 | 5 | |

| * | AECOM Technology Corp. | 200 | 4 |

| Briggs & Stratton Corp. | 216 | 4 | |

| * | MYR Group Inc. | 200 | 4 |

| * | Performant Financial Corp. | 361 | 4 |

| John Bean Technologies | |||

| Corp. | 200 | 3 | |

| * | CPI Aerostructures Inc. | 300 | 3 |

| * | Tecumseh Products Co. | ||

| Class A | 568 | 3 | |

| Acorn Energy Inc. | 300 | 3 | |

| * | ACCO Brands Corp. | 400 | 3 |

| 414,762 | |||

| Information Technology (19.8%) | |||

| Apple Inc. | 321,883 | 214,780 | |

| International Business | |||

| Machines Corp. | 431,259 | 89,465 | |

| Microsoft Corp. | 2,770,074 | 82,493 | |

| * | Google Inc. Class A | 74,679 | 56,345 |

| Cisco Systems Inc. | 2,178,997 | 41,597 | |

| QUALCOMM Inc. | 641,166 | 40,066 | |

| Intel Corp. | 1,582,959 | 35,901 | |

| Oracle Corp. | 1,114,625 | 35,100 | |

| Visa Inc. Class A | 242,558 | 32,571 | |

| Mastercard Inc. Class A | 47,620 | 21,499 | |

| Accenture plc Class A | 268,200 | 18,782 | |

| * | eBay Inc. | 297,866 | 14,420 |

| Motorola Solutions Inc. | 259,387 | 13,112 | |

| Seagate Technology plc | 346,810 | 10,751 | |

| Western Digital Corp. | 251,500 | 9,741 | |

| KLA-Tencor Corp. | 201,905 | 9,632 | |

| * | LSI Corp. | 1,225,300 | 8,467 |

| Hewlett-Packard Co. | 478,228 | 8,159 | |

| * | Citrix Systems Inc. | 103,523 | 7,927 |

| CA Inc. | 303,640 | 7,823 | |

| * | EMC Corp. | 282,400 | 7,701 |

| * | Symantec Corp. | 420,600 | 7,571 |

| Total System Services Inc. | 315,700 | 7,482 | |

| Intuit Inc. | 121,600 | 7,160 | |

| Jabil Circuit Inc. | 315,100 | 5,899 | |

| * | Yahoo! Inc. | 352,374 | 5,629 |

| * | VeriSign Inc. | 91,500 | 4,455 |

| * | F5 Networks Inc. | 41,410 | 4,336 |

22

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Marvell Technology | |||

| Group Ltd. | 367,200 | 3,360 | |

| Texas Instruments Inc. | 112,102 | 3,088 | |

| Fidelity National | |||

| Information Services Inc. | 96,090 | 3,000 | |

| * | Juniper Networks Inc. | 174,024 | 2,978 |

| * | AOL Inc. | 84,000 | 2,959 |

| * | Zebra Technologies Corp. | 73,600 | 2,763 |

| * | Autodesk Inc. | 82,300 | 2,746 |

| * | Advanced Micro | ||

| Devices Inc. | 793,500 | 2,674 | |

| Analog Devices Inc. | 66,284 | 2,598 | |

| * | Red Hat Inc. | 44,600 | 2,540 |

| * | Lam Research Corp. | 75,300 | 2,393 |

| * | NetApp Inc. | 71,200 | 2,341 |

| * | NVIDIA Corp. | 173,900 | 2,320 |

| TE Connectivity Ltd. | 67,898 | 2,309 | |

| * | BMC Software Inc. | 51,400 | 2,133 |

| Applied Materials Inc. | 155,025 | 1,731 | |

| Xerox Corp. | 198,400 | 1,456 | |

| Automatic Data | |||

| Processing Inc. | 24,400 | 1,431 | |

| * | Teradata Corp. | 18,800 | 1,418 |

| * | Fiserv Inc. | 17,600 | 1,303 |

| Paychex Inc. | 37,400 | 1,245 | |

| Linear Technology Corp. | 27,101 | 863 | |

| * | First Solar Inc. | 36,000 | 797 |

| * | CoreLogic Inc. | 29,600 | 785 |

| Dell Inc. | 71,816 | 708 | |

| Harris Corp. | 12,600 | 645 | |

| Computer Sciences Corp. | 16,500 | 531 | |

| Microchip Technology Inc. | 16,178 | 530 | |

| Molex Inc. | 15,100 | 397 | |

| * | Silicon Image Inc. | 84,700 | 389 |

| * | Electronic Arts Inc. | 29,088 | 369 |

| * | Vocus Inc. | 16,600 | 333 |

| * | NCR Corp. | 12,600 | 294 |

| InterDigital Inc. | 6,000 | 224 | |

| FLIR Systems Inc. | 10,630 | 212 | |

| Altera Corp. | 6,000 | 204 | |

| Avago Technologies Ltd. | 5,700 | 199 | |

| * | Agilysys Inc. | 21,400 | 184 |

| * | Brocade Communications | ||

| Systems Inc. | 27,100 | 160 | |

| Loral Space & | |||

| Communications Inc. | 2,100 | 149 | |

| * | Acxiom Corp. | 7,638 | 140 |

| * | Progress Software Corp. | 6,100 | 130 |

| * | VistaPrint NV | 3,740 | 128 |

| * | Travelzoo Inc. | 5,024 | 118 |

| * | Quest Software Inc. | 2,700 | 76 |

| * | ShoreTel Inc. | 17,150 | 70 |

| Tessera Technologies Inc. | 4,704 | 64 | |

| * | Sonus Networks Inc. | 27,500 | 52 |

| * | Ancestry.com Inc. | 1,300 | 39 |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Aspen Technology Inc. | 1,500 | 39 |

| IAC/InterActiveCorp | 700 | 36 | |

| * | TeleCommunication | ||

| Systems Inc. Class A | 16,706 | 36 | |

| * | Peregrine | ||

| Semiconductor Corp. | 2,123 | 36 | |

| * | MoneyGram International | ||

| Inc. | 2,400 | 36 | |

| *,^ | Ubiquiti Networks Inc. | 2,500 | 30 |

| * | Mattson Technology Inc. | 29,900 | 29 |

| * | Cognizant Technology | ||

| Solutions Corp. Class A | 400 | 28 | |

| * | Maxwell Technologies Inc. | 3,200 | 26 |

| Black Box Corp. | 1,000 | 25 | |

| * | AsiaInfo-Linkage Inc. | 2,000 | 23 |

| * | International Rectifier Corp. | 1,400 | 23 |

| * | IntraLinks Holdings Inc. | 3,400 | 22 |

| * | Riverbed Technology Inc. | 900 | 21 |

| * | AVG Technologies NV | 2,000 | 19 |

| Micrel Inc. | 1,500 | 16 | |

| * | Dolby Laboratories Inc. | ||

| Class A | 400 | 13 | |

| * | Quantum Corp. | 8,033 | 13 |

| * | Calix Inc. | 2,000 | 13 |

| Xilinx Inc. | 314 | 10 | |

| * | Powerwave Technologies | ||

| Inc. | 15,776 | 10 | |

| Western Union Co. | 485 | 9 | |

| * | Integrated Device | ||

| Technology Inc. | 1,500 | 9 | |

| * | Netscout Systems Inc. | 312 | 8 |

| * | Anaren Inc. | 387 | 8 |

| * | UTStarcom Holdings Corp. | 7,200 | 7 |

| * | MaxLinear Inc. | 1,108 | 7 |

| * | NXP Semiconductor NV | 284 | 7 |

| * | Arrow Electronics Inc. | 200 | 7 |

| Corning Inc. | 478 | 6 | |

| * | TNS Inc. | 400 | 6 |

| Amphenol Corp. Class A | 100 | 6 | |

| * | SunPower Corp. Class A | 1,300 | 6 |

| * | NCI Inc. Class A | 700 | 5 |

| * | Tech Data Corp. | 100 | 5 |

| Digimarc Corp. | 200 | 4 | |

| * | Imation Corp. | 794 | 4 |

| * | Rovi Corp. | 300 | 4 |

| * | Global Cash Access | ||

| Holdings Inc. | 525 | 4 | |

| * | WebMD Health Corp. | 294 | 4 |

| * | Acme Packet Inc. | 229 | 4 |

| * | Demand Media Inc. | 357 | 4 |

| * | EPAM Systems Inc. | 200 | 4 |

| * | Dice Holdings Inc. | 400 | 3 |

| * | TeleTech Holdings Inc. | 171 | 3 |

| * | Seachange International Inc. | 358 | 3 |

| * | Dynamics Research Corp. | 300 | 2 |

23

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| * | Amtech Systems Inc. | 500 | 2 |

| * | Smith Micro Software Inc. | 969 | 2 |

| * | FriendFinder Networks Inc. | 1,250 | 1 |

| * | Monster Worldwide Inc. | 100 | 1 |

| 867,089 | |||

| Materials (2.9%) | |||

| Monsanto Co. | 342,300 | 31,156 | |

| Freeport-McMoRan | |||

| Copper & Gold Inc. | 395,493 | 15,654 | |

| Dow Chemical Co. | 380,863 | 11,030 | |

| PPG Industries Inc. | 95,430 | 10,959 | |

| EI du Pont de Nemours | |||

| & Co. | 213,452 | 10,730 | |

| CF Industries Holdings Inc. | 45,164 | 10,037 | |

| Praxair Inc. | 64,540 | 6,704 | |

| Ball Corp. | 146,640 | 6,204 | |

| Sherwin-Williams Co. | 25,200 | 3,753 | |

| LyondellBasell | |||

| Industries NV Class A | 46,600 | 2,407 | |

| Air Products & Chemicals | |||

| Inc. | 22,400 | 1,853 | |

| Ecolab Inc. | 23,440 | 1,519 | |

| Newmont Mining Corp. | 25,461 | 1,426 | |

| International Flavors | |||

| & Fragrances Inc. | 23,151 | 1,379 | |

| Georgia Gulf Corp. | 37,900 | 1,373 | |

| * | Owens-Illinois Inc. | 66,700 | 1,251 |

| Titanium Metals Corp. | 88,795 | 1,139 | |

| Airgas Inc. | 11,740 | 966 | |

| Cliffs Natural Resources Inc. | 23,900 | 935 | |

| Nucor Corp. | 23,860 | 913 | |

| United States Steel Corp. | 46,550 | 888 | |

| Eastman Chemical Co. | 12,380 | 706 | |

| American Vanguard Corp. | 15,618 | 544 | |

| * | Headwaters Inc. | 70,889 | 466 |

| * | Louisiana-Pacific Corp. | 36,400 | 455 |

| Eagle Materials Inc. | 8,800 | 407 | |

| Teck Resources Ltd. | |||

| Class B | 13,500 | 398 | |

| * | Mercer International Inc. | 50,341 | 376 |

| Bemis Co. Inc. | 11,800 | 371 | |

| Schweitzer-Mauduit | |||

| International Inc. | 9,571 | 316 | |

| Valspar Corp. | 5,500 | 309 | |

| *,^ | Rare Element | ||

| Resources Ltd. | 58,464 | 288 | |

| * | Clearwater Paper Corp. | 5,200 | 215 |

| FMC Corp. | 3,323 | 184 | |

| * | SunCoke Energy Inc. | 11,239 | 181 |

| Sealed Air Corp. | 11,100 | 172 | |

| * | Resolute Forest Products | 12,726 | 165 |

| Rockwood Holdings Inc. | 3,100 | 144 | |

| PH Glatfelter Co. | 5,737 | 102 | |

| MeadWestvaco Corp. | 2,900 | 89 | |

| Barrick Gold Corp. | 2,100 | 88 | |

| Market | |||

| Value | |||

| Shares | ($000) | ||

| Commercial Metals Co. | 4,200 | 55 | |

| Noranda Aluminum | |||

| Holding Corp. | 8,075 | 54 | |

| * | US Silica Holdings Inc. | 3,500 | 47 |

| Wausau Paper Corp. | 4,200 | 39 | |

| * | General Moly Inc. | 8,000 | 25 |

| Myers Industries Inc. | 1,600 | 25 | |

| * | New Gold Inc. | 1,400 | 17 |

| Alcoa Inc. | 1,907 | 17 | |

| * | Northern Dynasty | ||

| Minerals Ltd. | 3,300 | 15 | |

| * | GSE Holding Inc. | 1,768 | 14 |

| Cabot Corp. | 300 | 11 | |

| Goldcorp Inc. | 200 | 9 | |

| Allegheny Technologies Inc. | 223 | 7 | |

| Pan American Silver Corp. | 291 | 6 | |

| * | WR Grace & Co. | 100 | 6 |

| Hecla Mining Co. | 883 | 6 | |

| * | Tahoe Resources Inc. | 100 | 2 |

| Boise Inc. | 200 | 2 | |

| * | Penford Corp. | 100 | 1 |

| 128,610 | |||

| Telecommunication Services (3.2%) | |||

| AT&T Inc. | 2,430,538 | 91,631 | |

| Verizon Communications | |||

| Inc. | 868,806 | 39,591 | |

| CenturyLink Inc. | 117,010 | 4,727 | |

| * | Sprint Nextel Corp. | 584,700 | 3,228 |

| * | Crown Castle | ||

| International Corp. | 22,540 | 1,445 | |

| Frontier Communications | |||

| Corp. | 90,600 | 444 | |

| * | Leap Wireless | ||

| International Inc. | 55,696 | 380 | |

| Windstream Corp. | 18,500 | 187 | |

| Cellcom Israel Ltd. | 5,000 | 43 | |

| * | Vonage Holdings Corp. | 5,347 | 12 |

| * | MetroPCS | ||

| Communications Inc. | 591 | 7 | |

| USA Mobility Inc. | 67 | 1 | |

| 141,696 | |||

| Utilities (3.4%) | |||

| American Electric Power | |||

| Co. Inc. | 285,820 | 12,559 | |

| PG&E Corp. | 256,696 | 10,953 | |

| DTE Energy Co. | 159,680 | 9,571 | |

| Pinnacle West Capital Corp. | 157,911 | 8,338 | |

| Entergy Corp. | 119,400 | 8,274 | |

| Public Service | |||

| Enterprise Group Inc. | 247,927 | 7,978 | |

| Ameren Corp. | 238,800 | 7,802 | |

| Dominion Resources Inc. | 146,027 | 7,731 | |

| FirstEnergy Corp. | 146,800 | 6,474 | |

| CenterPoint Energy Inc. | 295,850 | 6,302 | |

24

Growth and Income Fund

| Market | |||

| Value | |||

| Shares | ($000) | ||

| NextEra Energy Inc. | 84,890 | 5,970 | |

| ONEOK Inc. | 116,650 | 5,635 | |

| Northeast Utilities | 139,549 | 5,335 | |

| Southern Co. | 112,659 | 5,193 | |

| Duke Energy Corp. | 71,620 | 4,641 | |

| Consolidated Edison Inc. | 70,597 | 4,228 | |

| CMS Energy Corp. | 178,703 | 4,209 | |

| * | AES Corp. | 380,600 | 4,175 |

| Exelon Corp. | 107,410 | 3,822 | |

| PPL Corp. | 77,400 | 2,249 | |

| NiSource Inc. | 79,167 | 2,017 | |

| Integrys Energy Group Inc. | 38,277 | 1,998 | |

| Xcel Energy Inc. | 69,910 | 1,937 | |

| Sempra Energy | 28,196 | 1,818 | |

| NRG Energy Inc. | 79,300 | 1,696 | |

| Wisconsin Energy Corp. | 36,540 | 1,377 | |

| Pepco Holdings Inc. | 55,600 | 1,051 | |

| AGL Resources Inc. | 23,402 | 957 | |

| TECO Energy Inc. | 49,100 | 871 | |

| SCANA Corp. | 13,000 | 628 | |

| ITC Holdings Corp. | 5,069 | 383 | |

| IDACORP Inc. | 7,288 | 315 | |

| NorthWestern Corp. | 6,200 | 225 | |

| MGE Energy Inc. | 1,800 | 95 | |

| * | Calpine Corp. | 4,900 | 85 |

| Southwest Gas Corp. | 1,800 | 80 | |

| WGL Holdings Inc. | 1,800 | 72 | |

| Chesapeake Utilities Corp. | 1,107 | 52 | |

| Great Plains Energy Inc. | 800 | 18 | |

| Alliant Energy Corp. | 400 | 17 | |

| Vectren Corp. | 500 | 14 | |

| UNS Energy Corp. | 240 | 10 | |

| 147,155 | |||

| Total Common Stocks (Cost $3,722,691) | 4,308,762 | ||

| Temporary Cash Investments (2.0%)1 | |||

| Money Market Fund (1.8%) | |||

| 2,3 | Vanguard Market | ||

| Liquidity Fund, | |||

| 0.163% | 82,107,393 | 82,107 | |

| Face | Market | ||

| Amount | Value | ||

| ($000) | ($000) | ||

| U.S. Government and Agency Obligations (0.2%) | |||

| 4,5 | Fannie Mae | ||

| Discount Notes, | |||

| 0.135%, 12/12/12 | 8,000 | 7,998 | |

| 5,6 | Federal Home Loan | ||

| Bank Discount Notes, | |||

| 0.130%, 10/19/12 | 100 | 100 | |

| 4,5 | Freddie Mac | ||

| Discount Notes, | |||

| 0.160%, 10/16/12 | 100 | 100 | |

| 8,198 | |||

| Total Temporary Cash Investments | |||

| (Cost $90,305) | 90,305 | ||

| Total Investments (100.2%) | |||

| (Cost $3,812,996) | 4,399,067 | ||

| Other Assets and Liabilities (-0.2%) | |||

| Other Assets | 35,003 | ||

| Liabilities3 | (45,190) | ||

| (10,187) | |||

| Net Assets (100%) | 4,388,880 | ||

25

Growth and Income Fund

| At September 30, 2012, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 4,730,391 |

| Undistributed Net Investment Income | 9,985 |

| Accumulated Net Realized Losses | (936,553) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 586,071 |

| Futures Contracts | (1,014) |

| Net Assets | 4,388,880 |

| Investor Shares—Net Assets | |

| Applicable to 91,049,524 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 2,797,855 |

| Net Asset Value Per Share— | |

| Investor Shares | $30.73 |

| Admiral Shares—Net Assets | |

| Applicable to 31,705,945 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 1,591,025 |

| Net Asset Value Per Share— | |

| Admiral Shares | $50.18 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $595,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 99.8% and 0.4%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.