UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4526

Name of Registrant: Vanguard Quantitative Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2008 – September 30, 2009

Item 1: Reports to Shareholders

| Vanguard Growth and Income Fund |

| Annual Report |

| September 30, 2009 |

|

> Vanguard Growth and Income Fund returned about –11% in a difficult 12 months for quantitative equity strategies.

> The fund trailed both the return of its benchmark index and the average return of peer funds.

> Consumer discretionary, health care, and financial stocks were the fund’s weakest sectors compared with the index.

| Contents | |

| Your Fund’s Total Returns | 1 |

| President’s Letter | 2 |

| Advisor’s Report | 7 |

| Results of Proxy Voting | 9 |

| Fund Profile | 10 |

| Performance Summary | 11 |

| Financial Statements | 13 |

| Your Fund’s After-Tax Returns | 25 |

| About Your Fund’s Expenses | 26 |

| Trustees Approve Advisory Agreement | 28 |

| Glossary | 29 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

Cover photograph: Veronica Coia.

Your Fund’s Total Returns

| Fiscal Year Ended September 30, 2009 | ||

| Ticker | Total | |

| Symbol | Returns | |

| Vanguard Growth and Income Fund | ||

| Investor Shares | VQNPX | –11.29% |

| Admiral™ Shares1 | VGIAX | –11.15 |

| S&P 500 Index | –6.91 | |

| Large-Cap Core Funds Average2 | –5.85 |

| Your Fund’s Performance at a Glance | ||||

| September 30, 2008–September 30, 2009 | ||||

| Distributions Per Share | ||||

| Starting | Ending | Income | Capital | |

| Share Price | Share Price | Dividends | Gains | |

| Vanguard Growth and Income Fund | ||||

| Investor Shares | $25.84 | $22.34 | $0.494 | $0.000 |

| Admiral Shares | 42.20 | 36.48 | 0.857 | 0.000 |

1 A lower-cost class of shares available to many longtime shareholders and to those with significant investments in the fund.

2 Derived from data provided by Lipper Inc.

1

President’s Letter

Dear Shareholder,

Vanguard Growth and Income Fund returned about –11% for the fiscal year ended September 30. This disappointing result was below both the return of the Standard & Poor’s 500 Index, the fund’s market benchmark, and the average return of large-cap core funds.

The fiscal year is best viewed as two distinct periods. For the year’s first half, the fund returned about –33% as the global financial crisis deepened and investors lost their tolerance for risk. Midway through March, however, the stock market began to recover as government stimulus programs took hold, the economy showed signs of improving, and investors’ taste for risk returned. With the rally continuing through the summer, the fund advanced about 32% during the year’s second half. Compared with its benchmark, however, the fund fell a bit farther during the descent and didn’t rise quite as high during the ascent.

Quantitative equity strategies, which attempt to outperform their benchmark indexes with superior stock selection, have faced a particularly difficult environment, as the stocks typically favored by these approaches trailed the market’s more speculative stocks for the year. For the Growth and Income Fund, poorly performing stock selections in the consumer discretionary, health care, and financial sectors were a further barrier to reaching the fund’s goals.

2

If you hold shares of the fund in a taxable account, you may wish to review information on the fund’s after-tax returns that appears later in this report.

After a precipitous fall, stock markets rebound

In recent months, the financial markets have performed so strongly that it’s almost hard to remember that less than a year ago the global financial system stood on the brink of collapse. Since then, markets have pulled back from the abyss. Although unemployment remains near generational highs, and the prospects of a robust recovery seem dim, the global economy has begun to grind into gear.

Reminders of the markets’ dark days are nevertheless apparent in the index returns for both the past 12 months and the past three years. Over both periods, U.S. stocks recorded negative returns. Global stocks did better over the past 12 months, recouping their late-2008 losses thanks to general strength in developed economies and a powerful rally in emerging markets. Over the past three years, however, international stocks posted a modestly negative return.

The bond market’s turnabout has been equally dramatic

The stock market’s collapse and recovery echo even more dramatic developments in the bond market. At the end of 2008, as the credit markets nearly ceased to

| Market Barometer | |||

| Average Annual Total Returns | |||

| Periods Ended September 30, 2009 | |||

| One Year | Three Years | Five Years | |

| Stocks | |||

| Russell 1000 Index (Large-caps) | –6.14% | –5.10% | 1.49% |

| Russell 2000 Index (Small-caps) | –9.55 | –4.57 | 2.41 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | –4.58 | 1.93 |

| MSCI All Country World Index ex USA (International) | 6.43 | –0.78 | 8.59 |

| Bonds | |||

| Barclays Capital U.S. Aggregate Bond Index | |||

| (Broad taxable market) | 10.56% | 6.41% | 5.13% |

| Barclays Capital Municipal Bond Index | 14.85 | 5.13 | 4.78 |

| Citigroup 3-Month Treasury Bill Index | 0.39 | 2.63 | 2.96 |

| CPI | |||

| Consumer Price Index | –1.29% | 2.10% | 2.61% |

3

function, the difference between the yields of corporate bonds and Treasury bonds spiked to levels last seen during the Great Depression.

The Federal Reserve and its central bank counterparts around the world responded with aggressive monetary stimulus efforts, while global governments opened the fiscal taps. Investors first tiptoed, then stampeded, back into the market, boosting bond prices and bringing down yields. Over the past 12 months, taxable U.S. bonds returned more than 10%; municipal securities did even better, returning almost 15%, as measured by the Barclays Capital Municipal Bond Index.

The Fed’s rescue campaign has imposed a heavy price on short-term savings vehicles such as money market funds. In December 2008, the Fed reduced its target for the federal funds rate, a benchmark for the interest rates paid by money market instruments and other very short-term securities, to between 0% and 0.25%. The Fed has said it expects to maintain its target at this level “for an extended period.”

High-quality stocks were not rewarded

The Growth and Income Fund’s advisor, Mellon Capital Management (formerly known as Franklin Portfolio Associates, LLC), aims to beat its benchmark by using computer models to select the market’s better-performing stocks––and to do so without taking on more risk than the benchmark. The stocks it selects are mostly high-quality dividend-payers that are relatively undervalued by the market and have potential for growth.

| Expense Ratios1 | |||

| Your Fund Compared With Its Peer Group | |||

| Large-Cap | |||

| Investor | Admiral | Core Funds | |

| Shares | Shares | Average | |

| Growth and Income Fund | 0.37% | 0.23% | 1.26% |

1 The fund expense ratios shown are from the prospectus dated January 23, 2009, and represent estimated costs for the current fiscal year based on the fund’s net assets as of the prospectus date. For the fiscal year ended September 30, 2009, the fund’s expense ratios were 0.35% for Investor Shares and 0.21% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2008.

4

Investors following quantitative programs were not in the best position to participate in the stock market rally during the fiscal year’s second half. Indeed, the market comeback was largely led by lower-quality, highly leveraged companies that surged after being trampled in the financial crisis.

While the fund’s sector weightings hovered near those in the benchmark––true to the fund’s strategy––the advisor’s selections within those sectors did not perform as well. Relative to the index, the weakest performers were in the consumer discretionary, financial, and health care sectors.

The advisor’s choices among large diversified financial firms, commercial banks, insurance companies, and real estate investment trusts all contributed to the financial sector’s subpar performance. Apparel, fast food, entertainment, and education services companies all had a hand in dragging down the consumer discretionary sector. Within health care, the fund was overexposed to several weak stocks and did not own shares of a major pharmaceutical company that rose after its acquisition was announced.

In contrast, the fund performed better than its benchmark in the information technology, utilities, and energy sectors. Stock selection was especially strong in the tech sector, most notably among computer hardware and software companies. Both businesses and consumers began to spend again on technology after budget-paring during the depths of the financial crisis.

| Total Returns | |

| Ten Years Ended September 30, 2009 | |

| Average | |

| Annual Return | |

| Growth and Income Fund | –0.48% |

| S&P 500 Index | –0.15 |

| Large-Cap Core Funds Average1 | –1.21 |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1 Derived from data provided by Lipper Inc.

5

Expertise and low expenses have characterized the fund

It’s prudent to evaluate the Growth and Income Fund in comparison with its benchmark and peer group––and within the context of its times. The fund has returned an average of –0.48% annually over the past ten years, a period that includes two of the most severe bear markets in history. This performance slightly lags that of its benchmark and is a bit better than the average return for large-cap core funds.

Although the fund is actively managed, the advisor keeps its investment characteristics very similar to those of the S&P 500 Index, while seeking to choose stocks with prospects for higher return. Mellon Capital Management’s expertise and the fund’s low expense ratio offer investors the potential (though clearly not the guarantee) to do a bit better than the benchmark without assuming extra risk.

Counter market uncertainty with a well-designed plan

After five straight years of gains, from 2003 through 2007, the broad U.S. stock market began the type of bumpy and circuitous trip for which it is periodically known. Of course, the recent path was harsher and harder than any since the 1930s. From its all-time highs in October 2007, the broad market fell about 55% through March 9 of this year. From there, it abruptly changed course and rose about 60% through September 30. The market, however, is still down more than 30% from its peak, and the only thing certain about its near-term future is uncertainty.

Although the markets often follow an uncharted route, investors don’t have to do the same. After evaluating their risk tolerance, goals, and time horizon, investors are encouraged to maintain a diversified portfolio of stocks and fixed income investments. A well-diversified portfolio can��t shield you from extreme market volatility, but it can provide a cushion and potentially curb some of the risk.

Complemented by international funds and small-cap funds within the stock asset class, and balanced by bond funds and money market funds to limit risk, the large-cap Vanguard Growth and Income Fund can serve an important role in your plan.

Thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

October 14, 2009

6

Advisor’s Report

Market decline and rebound

We’ve come a long way since the financial system meltdown started by the bankruptcy of Lehman Brothers one year ago in September. During the fourth quarter of 2008, markets fell precipitously as it became increasingly clear that the credit crisis would result in an extended global recession. After rebounding briefly on hopes spurred by massive government intervention, the markets continued to decline in the first quarter of 2009, hitting bottom in early March.

A sharp reversal led by the lowest-quality, most highly leveraged stocks ensued, as leading indicators suggested the economy might return to growth sooner than expected. Investors’ relief propelled the markets upward: The second and third quarters brought the strongest quarterly gains since the fourth quarter of 1998. Still, as our fiscal year ended on September 30, the markets remained approximately a third below their October 2007 high.

If the worst is over, the current recession will not have been substantially different in output decline or unemployment than the severe recessions of 1973–1975 and 1981–1983. Data for the second half of 2009 are expected to show that gross domestic product (GDP) is growing again, particularly in the sectors that have received stimulus from the federal government. On a more cautionary note, some economists believe that these sectors may again struggle as the stimulus programs wind down. Unemployment is expected to remain high for a time as spare capacity is utilized and as workers come back into the labor pool looking for work. In the most recent two recessions (1990–1991 and 2001), it took more than a year after the recession’s end for unemployment to peak.

Our stock ranking process underperformed the index

Our ranking process emphasizes stocks with attractive valuation and momentum characteristics, and also considers factors such as corporate share activity and earnings-quality metrics. The review period was highly volatile, with frequent shifts in market leadership and in the drivers underlying market direction. This environment proved to be challenging for our investment process, and the fund underperformed the S&P 500 Index for the full fiscal year. In particular, the part of our model that emphasizes earnings and price momentum subtracted value.

Total returns in the financial sector were significantly lower than elsewhere, with the sector’s very weak performance in the fourth quarter of 2008 dominating its sharp rebound starting in March. Overall, the portfolio benefited from a slight underweighting in financials, but our stock picks in the sector lagged the S&P 500. Although we did not own some of the sector’s weakest performers, such as Citigroup and Merrill Lynch, we were on average overweighted in several financial stocks with lower returns than their peers,

7

including Bank of America and the equity REIT ProLogis. On average, we were underweighted in JPMorgan Chase, one of the better-performing financial stocks.

The portfolio also lagged the benchmark in the health care sector. We held some strong performers, including Bristol-Myers Squibb and Watson Pharmaceuticals. However, the portfolio was hurt by the weak returns of several holdings, such as Eli Lilly. We also did not own Schering-Plough, which rose approximately 50% on news of its acquisition by Merck.

Stock selection was notably stronger in the technology sector, particularly among computer hardware and software firms. For example, throughout the year we owned Apple, which performed extremely well as analysts continued to recommend the stock, expecting the company to see continued growth. These beliefs are driven by the success of Apple’s iPhone and the increases in market share of its Macintosh computers.

The fund also held Oracle over the full fiscal year. Despite a decline in new contracts during the downturn, the enterprise-software maker maintained profitability through cost-cutting and reliance on its stable revenue from recurring software maintenance. Oracle is expected to benefit from a return of business investment as the economy improves.

Keeping a watchful eye on the fund’s risk controls

The recent period was characterized by higher-than-usual volatility, and as a result we have been particularly careful in the implementation of our risk controls. Even relatively small residual tilts had the potential to result in outsized impacts, and we therefore maintained tight control over industry, sector, capitalization, and other top-down differences between the portfolio and the index.

Although we have begun to return to more normal levels of risk control, we remain watchful of our exposures in the most volatile sectors, such as financials, materials, and energy. As always, we are maintaining our focus on stocks that exhibit both attractive value and improving fundamentals. We believe that as markets begin to reward fundamentals once more, the fund will be well positioned to benefit.

Oliver E. Buckley, Executive Vice President and Head of Active Equity Strategies

Mellon Capital Management Corp.

October 20, 2009

8

Results of Proxy Voting

At a special meeting of shareholders on July 2, 2009, fund shareholders approved the following two proposals:

Proposal 1—Elect trustees for each fund.*

The individuals listed in the table below were elected as trustees for each fund. All trustees with the exception of Messrs. McNabb and Volanakis (both of whom already served as directors of The Vanguard Group, Inc.) served as trustees to the funds prior to the shareholder meeting.

| Percentage | |||

| Trustee | For | Withheld | For |

| John J. Brennan | 159,956,902 | 5,954,687 | 96.4% |

| Charles D. Ellis | 157,719,476 | 8,192,112 | 95.1% |

| Emerson U. Fullwood | 158,422,350 | 7,489,238 | 95.5% |

| Rajiv L. Gupta | 159,601,353 | 6,310,235 | 96.2% |

| Amy Gutmann | 159,929,264 | 5,982,324 | 96.4% |

| JoAnn Heffernan Heisen | 159,793,652 | 6,117,936 | 96.3% |

| F. William McNabb III | 159,924,396 | 5,987,192 | 96.4% |

| André F. Perold | 158,350,070 | 7,561,519 | 95.4% |

| Alfred M. Rankin, Jr. | 159,681,434 | 6,230,154 | 96.2% |

| Peter F. Volanakis | 159,820,426 | 6,091,162 | 96.3% |

| * Results are for all funds within the same trust. |

Proposal 2—Update and standardize the funds’ fundamental policies regarding:

(a) Purchasing and selling real estate.

(b) Issuing senior securities.

(c) Borrowing money.

(d) Making loans.

(e) Purchasing and selling commodities.

(f) Concentrating investments in a particular industry or group of industries.

(g) Eliminating outdated fundamental investment policies not required by law.

The revised fundamental policies are clearly stated and simple, yet comprehensive, making oversight and compliance more efficient than under the former policies. The revised fundamental policies will allow the funds to respond more quickly to regulatory and market changes, while avoiding the costs and delays associated with successive shareholder meetings.

| Broker | Percentage | ||||

| Vanguard Fund | For | Abstain | Against | Non-Votes | For |

| Growth and Income Fund | |||||

| 2a | 120,275,455 | 5,052,367 | 3,888,353 | 11,043,547 | 85.8% |

| 2b | 119,217,826 | 5,486,179 | 4,512,168 | 11,043,547 | 85.0% |

| 2c | 117,327,673 | 5,535,781 | 6,352,718 | 11,043,550 | 83.7% |

| 2d | 117,649,708 | 5,481,093 | 6,085,371 | 11,043,549 | 83.9% |

| 2e | 118,074,549 | 5,288,964 | 5,852,661 | 11,043,548 | 84.2% |

| 2f | 119,377,554 | 5,379,922 | 4,458,696 | 11,043,549 | 85.1% |

| 2g | 119,997,396 | 5,324,485 | 3,894,293 | 11,043,546 | 85.6% |

9

Growth and Income Fund

Fund Profile

As of September 30, 2009

| Portfolio Characteristics | |||

| Comparative | Broad | ||

| Fund | Index1 | Index2 | |

| Number of Stocks | 139 | 500 | 4,324 |

| Median Market Cap | $41.2B | $41.5B | $29.0B |

| Price/Earnings Ratio | 17.4x | 23.5x | 27.9x |

| Price/Book Ratio | 2.0x | 2.2x | 2.1x |

| Yield3 | 2.0% | 1.9% | |

| Investor Shares | 1.8% | ||

| Admiral Shares | 2.0% | ||

| Return on Equity | 20.1% | 20.6% | 19.1% |

| Earnings Growth Rate | 12.5% | 9.8% | 9.6% |

| Foreign Holdings | 0.0% | 0.0% | 0.0% |

| Turnover Rate | 83% | — | — |

| Expense Ratio4 | — | — | |

| Investor Shares | 0.37% | ||

| Admiral Shares | 0.23% | ||

| Short-Term Reserves | 0.1% | — | — |

| Sector Diversification (% of equity exposure) | |||

| Comparative | Broad | ||

| Fund | Index1 | Index2 | |

| Consumer Discretionary | 7.9% | 9.1% | 10.1% |

| Consumer Staples | 11.7 | 11.5 | 9.9 |

| Energy | 11.3 | 11.7 | 11.0 |

| Financials | 15.0 | 15.2 | 16.7 |

| Health Care | 13.9 | 13.1 | 12.9 |

| Industrials | 10.1 | 10.3 | 10.6 |

| Information Technology | 20.1 | 18.7 | 18.2 |

| Materials | 2.8 | 3.5 | 3.9 |

| Telecommunication | |||

| Services | 4.1 | 3.2 | 2.9 |

| Utilities | 3.1 | 3.7 | 3.8 |

| Volatility Measures5 | ||

| Fund Versus | Fund Versus | |

| Comparative Index1 | Broad Index2 | |

| R-Squared | 0.99 | 0.98 |

| Beta | 1.02 | 0.99 |

| Ten Largest Holdings6 (% of total net assets) | ||

| Exxon Mobil Corp. | integrated oil | |

| and gas | 3.8% | |

| General Electric Co. | industrial | |

| conglomerates | 2.8 | |

| AT&T Inc. | integrated | |

| telecommunication | ||

| services | 2.7 | |

| Johnson & Johnson | pharmaceuticals | 2.6 |

| International Business | ||

| Machines Corp. | computer hardware | 2.6 |

| Apple Inc. | computer hardware | 2.4 |

| Wells Fargo & Co. | diversified banks | 2.2 |

| Procter & Gamble Co. | household products | 2.2 |

| Pfizer Inc. | pharmaceuticals | 2.1 |

| Goldman Sachs | investment banking | |

| Group Inc. | and brokerage | 1.7 |

| Top Ten | 25.1% | |

Investment Focus

1 S&P 500 Index.

2 Dow Jones U.S. Total Stock Market Index.

3 30-day SEC yield for the fund; annualized dividend yield for the indexes. See the Glossary.

4 The expense ratios shown are from the prospectus dated January 23, 2009, and represent estimated costs for the current fiscal year based on the fund’s net assets as of the prospectus date. For the fiscal year ended September 30, 2009, the fund’s expense ratios were 0.35% for Investor Shares and 0.21% for Admiral Shares.

5 For an explanation of R-squared, beta, and other terms used here, see the Glossary.

6 The holdings listed exclude any temporary cash investments and equity index products.

10

Growth and Income Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

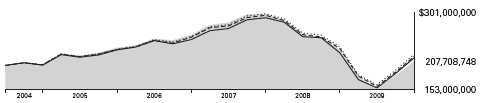

Cumulative Performance: September 30, 1999–September 30, 2009

Initial Investment of $10,000

| Average Annual Total Returns | Final Value | |||

| Periods Ended September 30, 2009 | of a $10,000 | |||

| One Year | Five Years | Ten Years | Investment | |

| Growth and Income Fund Investor Shares1 | –11.29% | –0.53% | –0.48% | $9,531 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | 1.93 | 0.94 | 10,978 |

| S&P 500 Index | –6.91 | 1.02 | –0.15 | 9,848 |

| Large-Cap Core Funds Average2 | –5.85 | 0.47 | –1.21 | 8,852 |

| Final Value | ||||

| Since | of a $100,000 | |||

| One Year | Five Years | Inception3 | Investment | |

| Growth and Income Fund Admiral Shares | –11.15% | –0.37% | –0.60% | $95,079 |

| Dow Jones U.S. Total Stock Market Index | –5.83 | 1.93 | 1.12 | 109,788 |

| S&P 500 Index | –6.91 | 1.02 | –0.09 | 99,247 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000. 2 Derived from data provided by Lipper Inc.

3 Performance for the fund’s Admiral Shares and comparative standards is calculated since the Admiral Shares’ inception: May 14, 2001.

11

Growth and Income Fund

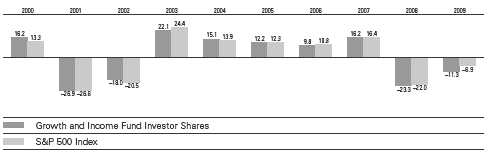

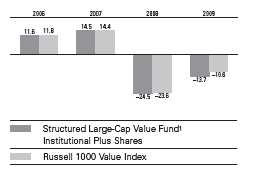

Fiscal-Year Total Returns (%): September 30, 1999–September 30, 2009

Note: See Financial Highlights tables for dividend and capital gains information.

12

Growth and Income Fund

Financial Statements

Statement of Net Assets

As of September 30, 2009

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Common Stocks (98.4%)1 | |||

| Consumer Discretionary (7.8%) | |||

| Comcast Corp. Class A | 4,136,200 | 69,860 | |

| McDonald’s Corp. | 925,100 | 52,795 | |

| Genuine Parts Co. | 943,500 | 35,910 | |

| * | Apollo Group Inc. Class A | 314,700 | 23,184 |

| Sherwin-Williams Co. | 323,400 | 19,456 | |

| Family Dollar Stores Inc. | 588,600 | 15,539 | |

| *,^ | Sears Holdings Corp. | 231,700 | 15,132 |

| Time Warner Inc. | 524,100 | 15,083 | |

| Pulte Homes Inc. | 1,345,200 | 14,784 | |

| * | Big Lots Inc. | 519,530 | 12,999 |

| Time Warner Cable Inc. | 276,766 | 11,926 | |

| Polo Ralph Lauren Corp. | |||

| Class A | 152,300 | 11,669 | |

| Coach Inc. | 328,500 | 10,814 | |

| RadioShack Corp. | 619,000 | 10,257 | |

| * | AutoNation Inc. | 530,400 | 9,590 |

| Wyndham Worldwide Corp. | 541,600 | 8,839 | |

| * | AutoZone Inc. | 56,900 | 8,320 |

| McGraw-Hill Cos. Inc. | 311,900 | 7,841 | |

| * | Starbucks Corp. | 352,800 | 7,285 |

| Target Corp. | 105,700 | 4,934 | |

| 366,217 | |||

| Consumer Staples (11.6%) | |||

| Procter & Gamble Co. | 1,745,900 | 101,123 | |

| Wal-Mart Stores Inc. | 1,416,000 | 69,511 | |

| Philip Morris | |||

| International Inc. | 1,299,700 | 63,347 | |

| Sysco Corp. | 2,074,800 | 51,559 | |

| PepsiCo Inc. | 769,100 | 45,115 | |

| Archer-Daniels-Midland Co. | 1,451,000 | 42,398 | |

| Kraft Foods Inc. | 1,471,800 | 38,664 | |

| Walgreen Co. | 1,012,300 | 37,931 | |

| Tyson Foods Inc. Class A | 2,527,600 | 31,924 | |

| Kimberly-Clark Corp. | 331,900 | 19,576 | |

| Coca-Cola Enterprises Inc. | 814,000 | 17,428 | |

| Safeway Inc. | 588,800 | 11,611 | |

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Hershey Co. | 170,900 | 6,641 | |

| Molson Coors Brewing Co. | |||

| Class B | 118,200 | 5,754 | |

| 542,582 | |||

| Energy (11.1%) | |||

| Exxon Mobil Corp. | 2,580,636 | 177,057 | |

| XTO Energy Inc. | 1,586,000 | 65,534 | |

| Chevron Corp. | 925,900 | 65,211 | |

| * | National Oilwell Varco Inc. | 1,123,400 | 48,452 |

| * | Cameron | ||

| International Corp. | 1,039,100 | 39,299 | |

| Tesoro Corp. | 1,660,400 | 24,873 | |

| Marathon Oil Corp. | 725,700 | 23,150 | |

| Peabody Energy Corp. | 619,600 | 23,062 | |

| Pioneer Natural | |||

| Resources Co. | 512,600 | 18,602 | |

| Williams Cos. Inc. | 696,800 | 12,452 | |

| Murphy Oil Corp. | 162,500 | 9,355 | |

| ConocoPhillips | 166,219 | 7,506 | |

| EOG Resources Inc. | 75,800 | 6,330 | |

| 520,883 | |||

| Financials (14.7%) | |||

| Wells Fargo & Co. | 3,624,300 | 102,133 | |

| Goldman Sachs Group Inc. | 421,900 | 77,777 | |

| JPMorgan Chase & Co. | 1,759,000 | 77,079 | |

| Bank of America Corp. | 3,381,399 | 57,213 | |

| Ameriprise Financial Inc. | 1,268,600 | 46,088 | |

| Morgan Stanley | 1,178,500 | 36,392 | |

| Hudson City Bancorp Inc. | 2,729,500 | 35,893 | |

| Northern Trust Corp. | 601,100 | 34,960 | |

| Prudential Financial Inc. | 547,200 | 27,311 | |

| Travelers Cos. Inc. | 532,200 | 26,200 | |

| Unum Group | 1,200,700 | 25,743 | |

| Equity Residential | 781,200 | 23,983 | |

| Cincinnati Financial Corp. | 783,008 | 20,350 | |

| Chubb Corp. | 375,600 | 18,934 | |

| Loews Corp. | 548,200 | 18,776 | |

| * | NASDAQ OMX Group Inc. | 778,600 | 16,390 |

13

| Growth and Income Fund | |||

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| Principal Financial | |||

| Group Inc. | 433,900 | 11,885 | |

| Aflac Inc. | 272,900 | 11,664 | |

| HCP Inc. | 229,800 | 6,604 | |

| Public Storage | 80,500 | 6,057 | |

| CME Group Inc. | 18,700 | 5,763 | |

| State Street Corp. | 86,400 | 4,545 | |

| 691,740 | |||

| Health Care (13.7%) | |||

| Johnson & Johnson | 2,031,300 | 123,686 | |

| Pfizer Inc. | 5,862,127 | 97,018 | |

| * | Amgen Inc. | 1,015,300 | 61,152 |

| Eli Lilly & Co. | 1,480,400 | 48,898 | |

| Abbott Laboratories | 945,300 | 46,764 | |

| Stryker Corp. | 918,900 | 41,746 | |

| * | Biogen Idec Inc. | 721,800 | 36,465 |

| Aetna Inc. | 1,243,800 | 34,615 | |

| Bristol-Myers Squibb Co. | 1,403,300 | 31,602 | |

| UnitedHealth Group Inc. | 875,300 | 21,917 | |

| Cardinal Health Inc. | 756,200 | 20,266 | |

| * | Humana Inc. | 438,500 | 16,356 |

| * | Zimmer Holdings Inc. | 302,300 | 16,158 |

| * | Forest Laboratories Inc. | 513,400 | 15,114 |

| Wyeth | 253,700 | 12,325 | |

| Medtronic Inc. | 261,000 | 9,605 | |

| * | Millipore Corp. | 75,600 | 5,317 |

| * | Gilead Sciences Inc. | 94,900 | 4,420 |

| 643,424 | |||

| Industrials (9.9%) | |||

| General Electric Co. | 8,092,400 | 132,877 | |

| General Dynamics Corp. | 1,075,900 | 69,503 | |

| Raytheon Co. | 812,000 | 38,952 | |

| CSX Corp. | 874,600 | 36,611 | |

| L-3 Communications | |||

| Holdings Inc. | 454,000 | 36,465 | |

| United Parcel Service Inc. | |||

| Class B | 510,100 | 28,805 | |

| CH Robinson | |||

| Worldwide Inc. | 377,200 | 21,783 | |

| Northrop Grumman Corp. | 406,600 | 21,042 | |

| * | Jacobs Engineering | ||

| Group Inc. | 404,200 | 18,573 | |

| Flowserve Corp. | 170,800 | 16,831 | |

| Expeditors International of | |||

| Washington Inc. | 358,300 | 12,594 | |

| Honeywell International Inc. | 327,400 | 12,163 | |

| WW Grainger Inc. | 86,300 | 7,712 | |

| Pitney Bowes Inc. | 291,300 | 7,239 | |

| Snap-On Inc. | 178,000 | 6,187 | |

| 467,337 | |||

| Information Technology (19.7%) | |||

| International Business | |||

| Machines Corp. | 1,016,600 | 121,596 | |

| * | Apple Inc. | 604,900 | 112,130 |

| Market | |||

| Value• | |||

| Shares | ($000) | ||

| * | Cisco Systems Inc. | 3,238,100 | 76,225 |

| * | Google Inc. Class A | 152,940 | 75,835 |

| Microsoft Corp. | 2,716,500 | 70,330 | |

| * | Computer Sciences Corp. | 1,167,300 | 61,528 |

| QUALCOMM Inc. | 1,329,800 | 59,814 | |

| Oracle Corp. | 2,086,000 | 43,472 | |

| Intel Corp. | 2,009,400 | 39,324 | |

| CA Inc. | 1,502,300 | 33,036 | |

| Xilinx Inc. | 1,399,300 | 32,772 | |

| * | Broadcom Corp. Class A | 1,020,600 | 31,322 |

| * | Intuit Inc. | 1,051,700 | 29,974 |

| Harris Corp. | 735,900 | 27,670 | |

| * | eBay Inc. | 1,101,700 | 26,011 |

| * | BMC Software Inc. | 640,500 | 24,038 |

| Fidelity National | |||

| Information Services Inc. | 924,900 | 23,594 | |

| * | Akamai Technologies Inc. | 1,182,500 | 23,272 |

| * | Novellus Systems Inc. | 373,600 | 7,838 |

| * | Teradata Corp. | 212,900 | 5,859 |

| 925,640 | |||

| Materials (2.7%) | |||

| Bemis Co. Inc. | 1,199,600 | 31,082 | |

| Airgas Inc. | 482,200 | 23,324 | |

| Ecolab Inc. | 429,100 | 19,837 | |

| * | Pactiv Corp. | 607,200 | 15,818 |

| Newmont Mining Corp. | 312,500 | 13,756 | |

| Allegheny Technologies Inc. | 377,900 | 13,223 | |

| Titanium Metals Corp. | 1,216,500 | 11,666 | |

| 128,706 | |||

| Telecommunication Services (4.1%) | |||

| AT&T Inc. | 4,694,700 | 126,804 | |

| Verizon | |||

| Communications Inc. | 1,193,500 | 36,127 | |

| CenturyTel Inc. | 861,100 | 28,933 | |

| 191,864 | |||

| Utilities (3.1%) | |||

| FPL Group Inc. | 923,700 | 51,016 | |

| Exelon Corp. | 981,100 | 48,682 | |

| Sempra Energy | 265,400 | 13,220 | |

| Questar Corp. | 337,400 | 12,673 | |

| Dominion | |||

| Resources Inc. | 248,700 | 8,580 | |

| Public Service Enterprise | |||

| Group Inc. | 167,900 | 5,279 | |

| Ameren Corp. | 164,500 | 4,158 | |

| 143,608 | |||

| Total Common Stocks | |||

| (Cost $4,419,370) | 4,622,001 | ||

14

| Growth and Income Fund | ||

| Market | ||

| Value• | ||

| Shares | ($000) | |

| Temporary Cash Investments (1.9%)1 | ||

| Money Market Fund (1.7%) | ||

| 2,3 Vanguard Market | ||

| Liquidity Fund, | ||

| 0.267% | 81,072,347 | 81,072 |

| Face | ||

| Amount | ||

| ($000) | ||

| U.S. Government and Agency Obligations (0.2%) | ||

| 4 United States | ||

| Treasury Bill, | ||

| 0.080%, 12/17/09 | 7,450 | 7,449 |

| Total Temporary Cash Investments | ||

| (Cost $88,521) | 88,521 | |

| Total Investments (100.3%) | ||

| (Cost $4,507,891) | 4,710,522 | |

| Other Assets and Liabilities (–0.3%) | ||

| Other Assets | 187,148 | |

| Liabilities3 | (203,494) | |

| (16,346) | ||

| Net Assets (100%) | 4,694,176 | |

| At September 30, 2009, net assets consisted of: | |

| Amount | |

| ($000) | |

| Paid-in Capital | 6,425,614 |

| Undistributed Net Investment Income | 6,443 |

| Accumulated Net Realized Losses | (1,940,672) |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 202,631 |

| Futures Contracts | 160 |

| Net Assets | 4,694,176 |

| Investor Shares—Net Assets | |

| Applicable to 145,586,165 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 3,252,737 |

| Net Asset Value Per Share— | |

| Investor Shares | $22.34 |

| Admiral Shares—Net Assets | |

| Applicable to 39,507,988 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 1,441,439 |

| Net Asset Value Per Share— | |

| Admiral Shares | $36.48 |

• See Note A in Notes to Financial Statements. * Non-income-producing security.

^ Part of security position is on loan to broker-dealers. The total value of securities on loan is $14,375,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 100.0% and 0.3%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $14,967,000 of collateral received for securities on loan.

4 Securities with a value of $7,449,000 have been segregated as initial margin for open futures contracts.

See accompanying Notes, which are an integral part of the Financial Statements.

15

| Growth and Income Fund | |

| Statement of Operations | |

| Year Ended | |

| September 30, 2009 | |

| ($000) | |

| Investment Income | |

| Income | |

| Dividends | 109,267 |

| Interest1 | 643 |

| Security Lending | 724 |

| Total Income | 110,634 |

| Expenses | |

| Investment Advisory Fees—Note B | |

| Basic Fee | 4,283 |

| Performance Adjustment | (1,791) |

| The Vanguard Group—Note C | |

| Management and Administrative—Investor Shares | 7,001 |

| Management and Administrative—Admiral Shares | 1,551 |

| Marketing and Distribution—Investor Shares | 832 |

| Marketing and Distribution—Admiral Shares | 379 |

| Custodian Fees | 46 |

| Auditing Fees | 23 |

| Shareholders’ Reports and Proxies—Investor Shares | 394 |

| Shareholders’ Reports and Proxies—Admiral Shares | 18 |

| Trustees’ Fees and Expenses | 10 |

| Total Expenses | 12,746 |

| Expenses Paid Indirectly | (446) |

| Net Expenses | 12,300 |

| Net Investment Income | 98,334 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold | (1,362,837) |

| Futures Contracts | (8,583) |

| Realized Net Gain (Loss) | (1,371,420) |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities | 544,642 |

| Futures Contracts | 1,061 |

| Change in Unrealized Appreciation (Depreciation) | 545,703 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (727,383) |

| 1 Interest income from an affiliated company of the fund was $625,000. | |

See accompanying Notes, which are an integral part of the Financial Statements.

16

| Growth and Income Fund | ||

| Statement of Changes in Net Assets | ||

| Year Ended September 30, | ||

| 2009 | 2008 | |

| ($000) | ($000) | |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net Investment Income | 98,334 | 123,730 |

| Realized Net Gain (Loss) | (1,371,420) | (446,516) |

| Change in Unrealized Appreciation (Depreciation) | 545,703 | (1,520,848) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | (727,383) | (1,843,634) |

| Distributions | ||

| Net Investment Income | ||

| Investor Shares | (73,186) | (81,970) |

| Admiral Shares | (36,418) | (43,850) |

| Realized Capital Gain1 | ||

| Investor Shares | — | (564,334) |

| Admiral Shares | — | (284,167) |

| Total Distributions | (109,604) | (974,321) |

| Capital Share Transactions | ||

| Investor Shares | (120,422) | 335,349 |

| Admiral Shares | (174,315) | 50,006 |

| Net Increase (Decrease) from Capital Share Transactions | (294,737) | 385,355 |

| Total Increase (Decrease) | (1,131,724) | (2,432,600) |

| Net Assets | ||

| Beginning of Period | 5,825,900 | 8,258,500 |

| End of Period2 | 4,694,176 | 5,825,900 |

1 Includes fiscal 2008 short-term gain distributions totaling $89,550,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed net investment income of $6,443,000 and $17,713,000.

See accompanying Notes, which are an integral part of the Financial Statements.

17

| Growth and Income Fund | |||||

| Financial Highlights | |||||

| Investor Shares | |||||

| For a Share Outstanding | Year Ended September 30, | ||||

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $25.84 | $38.62 | $33.79 | $31.29 | $28.31 |

| Investment Operations | |||||

| Net Investment Income | .447 | .546 | .600 | .550 | .460 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (3.453) | (8.758) | 4.840 | 2.470 | 2.980 |

| Total from Investment Operations | (3.006) | (8.212) | 5.440 | 3.020 | 3.440 |

| Distributions | |||||

| Dividends from Net Investment Income | (.494) | (.560) | (.610) | (.520) | (.460) |

| Distributions from Realized Capital Gains | — | (4.008) | — | — | — |

| Total Distributions | (.494) | (4.568) | (.610) | (.520) | (.460) |

| Net Asset Value, End of Period | $22.34 | $25.84 | $38.62 | $33.79 | $31.29 |

| Total Return1 | –11.29% | –23.28% | 16.20% | 9.76% | 12.20% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $3,253 | $3,919 | $5,465 | $5,088 | $5,202 |

| Ratio of Total Expenses to | |||||

| Average Net Assets2 | 0.35% | 0.31% | 0.32% | 0.38% | 0.40% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 2.28% | 1.69% | 1.61% | 1.65% | 1.53% |

| Portfolio Turnover Rate | 83% | 96% | 100% | 93% | 84% |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Includes performance-based investment advisory fee increases (decreases) of (0.04%), (0.02%), 0.00%, 0.01% and 0.01%.

See accompanying Notes, which are an integral part of the Financial Statements.

18

| Growth and Income Fund | |||||

| Financial Highlights | |||||

| Admiral Shares | |||||

| For a Share Outstanding | Year Ended September 30, | ||||

| Throughout Each Period | 2009 | 2008 | 2007 | 2006 | 2005 |

| Net Asset Value, Beginning of Period | $42.20 | $63.08 | $55.20 | $51.12 | $46.25 |

| Investment Operations | |||||

| Net Investment Income | .775 | .963 | 1.070 | .997 | .849 |

| Net Realized and Unrealized Gain (Loss) | |||||

| on Investments | (5.638) | (14.313) | 7.903 | 4.036 | 4.853 |

| Total from Investment Operations | (4.863) | (13.350) | 8.973 | 5.033 | 5.702 |

| Distributions | |||||

| Dividends from Net Investment Income | (.857) | (.985) | (1.093) | (.953) | (.832) |

| Distributions from Realized Capital Gains | — | (6.545) | — | — | — |

| Total Distributions | (.857) | (7.530) | (1.093) | (.953) | (.832) |

| Net Asset Value, End of Period | $36.48 | $42.20 | $63.08 | $55.20 | $51.12 |

| Total Return | –11.15% | –23.19% | 16.37% | 9.97% | 12.39% |

| Ratios/Supplemental Data | |||||

| Net Assets, End of Period (Millions) | $1,441 | $1,907 | $2,794 | $2,321 | $2,039 |

| Ratio of Total Expenses to | |||||

| Average Net Assets1 | 0.21% | 0.16% | 0.18% | 0.20% | 0.23% |

| Ratio of Net Investment Income to | |||||

| Average Net Assets | 2.42% | 1.84% | 1.75% | 1.83% | 1.68% |

| Portfolio Turnover Rate | 83% | 96% | 100% | 93% | 84% |

| 1 Includes performance-based investment advisory fee increases (decreases) of (0.04%), (0.02%), 0.00%, 0.01% and 0.01%. | |||||

See accompanying Notes, which are an integral part of the Financial Statements.

19

Growth and Income Fund

Notes to Financial Statements

Vanguard Growth and Income Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares: Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, tenure, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (September 30, 2006–2009), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

20

Growth and Income Fund

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses), shareholder reporting, and proxies. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Mellon Capital Management Corporation provides investment advisory services to the fund for a fee calculated at an annual percentage rate of average net assets. The basic fee is subject to quarterly adjustments based on the fund’s performance for the preceding three years relative to the S&P 500 Index. For the year ended September 30, 2009, the investment advisory fee represented an effective annual basic rate of 0.10% of the fund’s average net assets before a decrease of $1,791,000 (0.04%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At September 30, 2009, the fund had contributed capital of $974,000 to Vanguard (included in Other Assets), representing 0.02% of the fund’s net assets and 0.39% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisor to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. For the year ended September 30, 2009, these arrangements reduced the fund’s expenses by $446,000 (an annual rate of 0.01% of average net assets).

E. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

21

Growth and Income Fund

The following table summarizes the fund’s investments as of September 30, 2009, based on the inputs used to value them:

| Level 1 | Level 2 | Level 3 | |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 4,622,001 | — | — |

| Temporary Cash Investments | 81,072 | 7,449 | — |

| Futures Contracts—Liabilities1 | (128) | — | — |

| Total | 4,702,945 | 7,449 | — |

| 1 Represents variation margin on the last day of the reporting period. |

F. At September 30, 2009, the aggregate settlement value of open futures contracts and the related unrealized appreciation (depreciation) were:

| ($000) | ||||

| Number of | Aggregate | Unrealized | ||

| Long (Short) | Settlement | Appreciation | ||

| Futures Contracts | Expiration | Contracts | Value | (Depreciation) |

| S&P 500 Index | December 2009 | 270 | 71,071 | 160 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

G. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

For tax purposes, at September 30, 2009, the fund had $22,522,000 of ordinary income available for distribution. The fund had available capital loss carryforwards totaling $845,748,000 to offset future net capital gains through September 30, 2017. In addition, the fund realized losses of $1,093,871,000 during the period from November 1, 2008, through September 30, 2009, which are deferred and will be treated as realized for tax purposes in fiscal 2010.

At September 30, 2009, the cost of investment securities for tax purposes was $4,509,373,000. Net unrealized appreciation of investment securities for tax purposes was $201,149,000, consisting of unrealized gains of $533,428,000 on securities that had risen in value since their purchase and $332,279,000 in unrealized losses on securities that had fallen in value since their purchase.

H. During the year ended September 30, 2009, the fund purchased $3,511,095,000 of investment securities and sold $3,799,385,000 of investment securities, other than temporary cash investments.

22

Growth and Income Fund

| I. Capital share transactions for each class of shares were: | ||||

| Year Ended September 30, | ||||

| 2009 | 2008 | |||

| Amount | Shares | Amount | Shares | |

| ($000) | (000) | ($000) | (000) | |

| Investor Shares | ||||

| Issued | 342,754 | 17,955 | 550,897 | 17,490 |

| Issued in Lieu of Cash Distributions | 70,600 | 3,711 | 622,470 | 19,829 |

| Redeemed | (533,776) | (27,759) | (838,018) | (27,137) |

| Net Increase (Decrease)—Investor Shares | (120,422) | (6,093) | 335,349 | 10,182 |

| Admiral Shares | ||||

| Issued | 152,599 | 4,878 | 220,621 | 4,296 |

| Issued in Lieu of Cash Distributions | 32,886 | 1,059 | 305,215 | 5,955 |

| Redeemed | (359,800) | (11,621) | (475,830) | (9,345) |

| Net Increase (Decrease)—Admiral Shares | (174,315) | (5,684) | 50,006 | 906 |

J. In preparing the financial statements as of September 30, 2009, management considered the impact of subsequent events occurring through November 10, 2009, for potential recognition or disclosure in these financial statements.

23

Report of Independent Registered Public Accounting Firm

To the Trustees of Vanguard Quantitative Funds and the Shareholders of Vanguard Growth and Income Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Growth and Income Fund (the “Fund”) at September 30, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accor dance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at September 30, 2009 by correspondence with the custodian and broker, and by agreement to the underlying ownership records for Vanguard Market Liquidity Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

November 10, 2009

| Special 2009 tax information (unaudited) for Vanguard Growth and Income Fund |

This information for the fiscal year ended September 30, 2009, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $109,604,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 100.0% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

24

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2009. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

The table shows returns for Investor Shares only; returns for other share classes will differ. Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| Average Annual Total Returns: Growth and Income Fund Investor Shares1 | |||

| Periods Ended September 30, 2009 | |||

| One | Five | Ten | |

| Year | Years | Years | |

| Returns Before Taxes | –11.29% | –0.53% | –0.48% |

| Returns After Taxes on Distributions | –11.63 | –1.17 | –1.17 |

| Returns After Taxes on Distributions and Sale of Fund Shares | –6.99 | –0.36 | –0.51 |

1 Total returns figures do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

25

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading “Expenses Paid During Period.”

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund’s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

| Six Months Ended September 30, 2009 | |||

| Beginning | Ending | Expenses | |

| Account Value | Account Value | Paid During | |

| Growth and Income Fund | 3/31/2009 | 9/30/2009 | Period1 |

| Based on Actual Fund Return | |||

| Investor Shares | $1,000.00 | $1,317.69 | $1.98 |

| Admiral Shares | 1,000.00 | 1,319.04 | 1.16 |

| Based on Hypothetical 5% Yearly Return | |||

| Investor Shares | $1,000.00 | $1,023.36 | $1.72 |

| Admiral Shares | 1,000.00 | 1,024.07 | 1.01 |

1 The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.34% for Investor Shares and 0.20% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

26

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include the account service fee described in the prospectus. If such a fee were applied to your account, your costs would be higher. Your fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

27

Trustees Approve Advisory Agreement

The board of trustees of Vanguard Growth and Income Fund has renewed the fund’s investment advisory agreement with Mellon Capital Management Corporation. The board determined that the retention of the advisor was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of the advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the agreement. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of the fund’s investment management over both the short and long term, and took into account the organizational depth and stability of the advisor. The board noted that Mellon Capital was founded in 1983. The firm is a leader in asset allocation and quantitative investment strategies. The firm, through its predecessor, Franklin Portfolio Associates, has advised the fund since 1986. The investment team at Mellon Capital employs a quantitative investment strategy that seeks to provide a total return greater than that of the S&P 500 Index by investing in U.S. large- and mid-capitalization stocks. Stock selection is driven by a series of more than 40 computer models covering a broad range of public data. The board concluded that the advisor’s experience, stability, depth, and performance, among other factors, warranted continuation of the advisory agreement.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance of a relevant benchmark and peer group. The board noted that the advisor has carried out the fund’s investment strategy in disciplined fashion, and the results have been mixed—with periods of outperformance and periods of underperformance versus the fund’s benchmark and peer group. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was well below the average expense ratio charged by funds in its peer group and that the fund’s advisory fee rate was also well below its peer-group average. Information about the fund’s expense ratio appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the fund’s advisory fee rate.

The board did not consider profitability of Mellon Capital in determining whether to approve the advisory fee, because Mellon Capital is independent of Vanguard, and the advisory fee is the result of arm’s-length negotiations.

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the advisory fee schedule. The breakpoints reduce the effective rate of the fee as the fund’s assets increase.

The board will consider whether to renew the advisory agreement after a one-year period.

28

Glossary

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by stocks or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

29

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

30

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 156 Vanguard funds.

The following table provides information for each trustee and executive officer of the fund. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at www.vanguard.com.

| Interested Trustees | Emerson U. Fullwood |

| Born 1948. Trustee Since January 2008. Principal | |

| John J. Brennan1 | Occupation(s) During the Past Five Years: Executive |

| Born 1954. Trustee Since May 1987. Chairman of | Chief Staff and Marketing Officer for North America |

| the Board. Principal Occupation(s) During the Past | and Corporate Vice President (retired 2008) of Xerox |

| Five Years: Chairman of the Board and Director/Trustee | Corporation (photocopiers and printers); Director of |

| of The Vanguard Group, Inc., and of each of the | SPX Corporation (multi-industry manufacturing), the |

| investment companies served by The Vanguard Group; | United Way of Rochester, the Boy Scouts of America, |

| Chief Executive Officer (1996–2008) and President | Amerigroup Corporation (direct health and medical |

| (1989–2008) of The Vanguard Group and of each of the | insurance carriers), and Monroe Community College |

| investment companies served by The Vanguard Group; | Foundation. |

| Chairman of the Financial Accounting Foundation; | |

| Governor of the Financial Industry Regulatory Authority | Rajiv L. Gupta |

| (FINRA); Director of United Way of Southeastern | Born 1945. Trustee Since December 2001.2 Principal |

| Pennsylvania. | Occupation(s) During the Past Five Years: Chairman |

| and Chief Executive Officer (retired 2009) and President | |

| F. William McNabb III1 | (2006–2008) of Rohm and Haas Co. (chemicals); Board |

| Born 1957. Trustee Since July 2009. Principal | Member of American Chemistry Council; Director of |

| Occupation(s) During the Past Five Years: Director of | Tyco International, Ltd. (diversified manufacturing and |

| The Vanguard Group, Inc., since 2008; Chief Executive | services) and Hewlett-Packard Co. (electronic computer |

| Officer and President of The Vanguard Group and of | manufacturing); Trustee of The Conference Board. |

| each of the investment companies served by The | |

| Vanguard Group since 2008; Director of Vanguard | Amy Gutmann |

| Marketing Corporation; Managing Director of The | Born 1949. Trustee Since June 2006. Principal |

| Vanguard Group (1995–2008). | Occupation(s) During the Past Five Years: President of |

| the University of Pennsylvania; Christopher H. Browne | |

| Distinguished Professor of Political Science in the School | |

| Independent Trustees | of Arts and Sciences with secondary appointments |

| at the Annenberg School for Communication and the | |

| Charles D. Ellis | Graduate School of Education of the University of |

| Born 1937. Trustee Since January 2001. Principal | Pennsylvania; Director of Carnegie Corporation of |

| Occupation(s) During the Past Five Years: Applecore | New York, Schuylkill River Development Corporation, |

| Partners (pro bono ventures in education); Senior | and Greater Philadelphia Chamber of Commerce; |

| Advisor to Greenwich Associates (international business | Trustee of the National Constitution Center. |

| strategy consulting); Successor Trustee of Yale University; | |

| Overseer of the Stern School of Business at New York | |

| University; Trustee of the Whitehead Institute for | |

| Biomedical Research. |

| JoAnn Heffernan Heisen | Executive Officers | |

| Born 1950. Trustee Since July 1998. Principal | ||

| Occupation(s) During the Past Five Years: Corporate | Thomas J. Higgins1 | |

| Vice President and Chief Global Diversity Officer since | Born 1957. Chief Financial Officer Since September | |

| 2006 (retired 2008) and Member of the Executive | 2008. Principal Occupation(s) During the Past Five | |

| Committee (retired 2008) of Johnson & Johnson | Years: Principal of The Vanguard Group, Inc.; Chief | |

| (pharmaceuticals/consumer products); Vice President | Financial Officer of each of the investment companies | |

| and Chief Information Officer of Johnson & Johnson | served by The Vanguard Group since 2008; Treasurer | |

| (1997–2005); Director of the University Medical Center | of each of the investment companies served by The | |

| at Princeton and Women’s Research and Education | Vanguard Group (1998–2008). | |

| Institute. | ||

| Kathryn J. Hyatt1 | ||

| André F. Perold | Born 1955. Treasurer Since November 2008. Principal | |

| Born 1952. Trustee Since December 2004. Principal | Occupation(s) During the Past Five Years: Principal of | |

| Occupation(s) During the Past Five Years: George Gund | The Vanguard Group, Inc.; Treasurer of each of the | |

| Professor of Finance and Banking, Harvard Business | investment companies served by The Vanguard | |

| School; Chairman of UNX, Inc. (equities trading firm); | Group since 2008; Assistant Treasurer of each of the | |

| Chair of the Investment Committee of HighVista | investment companies served by The Vanguard Group | |

| Strategies LLC (private investment firm). | (1988–2008). | |

| Alfred M. Rankin, Jr. | Heidi Stam1 | |

| Born 1941. Trustee Since January 1993. Principal | Born 1956. Secretary Since July 2005. Principal | |

| Occupation(s) During the Past Five Years: Chairman, | Occupation(s) During the Past Five Years: Managing | |

| President, and Chief Executive Officer of NACCO | Director of The Vanguard Group, Inc., since 2006; | |

| Industries, Inc. (forklift trucks/housewares/lignite); | General Counsel of The Vanguard Group since 2005; | |

| Director of Goodrich Corporation (industrial products/ | Secretary of The Vanguard Group and of each of the | |

| aircraft systems and services); Deputy Chairman of | investment companies served by The Vanguard Group | |