UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4526

Name of Registrant: Vanguard Quantitative Funds

Address of Registrant:

P.O. Box 2600

Valley Forge, PA 19482

Name and address of agent for service:

Heidi Stam, Esquire

P.O. Box 876

Valley Forge, PA 19482

Registrant’s telephone number, including area code: (610) 669-1000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2007–September 30, 2008

Item 1: Reports to Shareholders |

> Over a turbulent 12 months, Vanguard Growth and Income Fund Investor Shares returned –23.3%.

> The fund’s return slightly lagged its benchmark index and the average return of its peer group.

> Relative to its benchmark, the fund’s health care, materials, and consumer staples stocks were its weakest performers.

Contents |

|

|

|

Your Fund’s Total Returns | 1 |

President’s Letter | 2 |

Advisor’s Report | 7 |

Fund Profile | 9 |

Performance Summary | 10 |

Financial Statements | 12 |

Your Fund’s After-Tax Returns | 24 |

About Your Fund’s Expenses | 25 |

Trustees Approve Advisory Agreement | 27 |

Glossary | 28 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this report. Of course, the risks of investing in your fund are spelled out in the prospectus.

Your Fund’s Total Returns

Fiscal Year Ended September 30, 2008 |

|

|

| Ticker | Total |

| Symbol | Returns |

Vanguard Growth and Income Fund |

|

|

Investor Shares | VQNPX | –23.3% |

Admiral™ Shares1 | VGIAX | –23.2 |

S&P 500 Index |

| –22.0 |

Average Large-Cap Core Fund2 |

| –22.0 |

Your Fund’s Performance at a Glance | ||||

September 30, 2007–September 30, 2008 | ||||

|

|

| Distributions Per Share | |

| Starting | Ending | Income | Capital |

| Share Price | Share Price | Dividends | Gains |

Vanguard Growth and Income Fund |

|

|

|

|

Investor Shares | $38.62 | $25.84 | $0.560 | $4.008 |

Admiral Shares | 63.08 | 42.20 | 0.985 | 6.545 |

1 A lower-cost class of shares available to many longtime shareholders and to those with significant investments in the fund.

2 Derived from data provided by Lipper Inc.

1

President’s Letter

Dear Shareholder,

During the fiscal year ended September 30, the Investor Shares of Vanguard Growth and Income Fund returned a disappointing –23.3%, while the lower-cost Admiral Shares returned –23.2%, slightly below the –22.0% return of the Standard & Poor’s 500 Index, the fund’s primary benchmark, and the average return of large-capitalization core mutual funds.

The tumultuous market during the past 12 months, particularly in September, was challenging for the Growth and Income Fund, an actively managed quantitative fund that seeks to outperform its benchmark index while matching the index’s risk characteristics. The fund fell short of this goal during the past year, largely because of subpar stock selections in the health care, materials, and consumer staples sectors that weighed on the fund’s overall performance.

If you own the Growth and Income Fund in a taxable account, see page 24 for a report on the fund’s after-tax returns for the 12 months ended September 30.

Credit-market turbulence weighed heavily on stock prices

Troubles simmering in the credit markets for much of the past year came to a boil at the end of the fiscal period, producing several high-profile bankruptcies and putting severe pressure on stock prices around the world. The broad U.S. stock market returned –21.2% for the 12 months

2

ended September 30. In September alone, stock prices fell more than –9%. International stock markets were similarly disappointing, returning –30.0% for the full 12 months.

Policymakers and elected officials, both in the United States and abroad, responded to the upheavals with dramatic new programs designed to help stabilize the credit markets. As participants struggled to make sense of the markets’ fast-changing dynamics, stock prices were exceptionally volatile, with daily ups and downs of 2 percentage points or more becoming commonplace.

U.S. Treasuries rallied in a nervous market

Nervousness in the stock market was echoed, and even amplified, in the bond market. For the 12 months, the broad U.S. bond market returned 3.7%, largely on the strength of Treasuries—investors’ security of choice in times of duress. Corporate bonds generally produced negative returns for the period, coming under heavy selling pressure during investors’ flight to safety. Even the municipal market, made up of generally high-quality securities issued by states and municipalities, recorded a negative 12-month return.

The U.S. Federal Reserve Board responded to the turmoil with a dramatic easing of monetary policy. Over the full 12 months, the Fed reduced its target for the federal

Market Barometer |

|

|

|

| Average Annual Total Returns | ||

| Periods Ended September 30, 2008 | ||

| One Year | Three Years | Five Years |

Stocks |

|

|

|

Russell 1000 Index (Large-caps) | –22.1% | 0.1% | 5.5% |

Russell 2000 Index (Small-caps) | –14.5 | 1.8 | 8.1 |

Dow Jones Wilshire 5000 Index (Entire market) | –21.2 | 0.6 | 6.0 |

MSCI All Country World Index ex USA (International) | –30.0 | 3.1 | 11.8 |

|

|

|

|

|

|

|

|

Bonds |

|

|

|

Lehman U.S. Aggregate Bond Index (Broad taxable market) | 3.7% | 4.2% | 3.8% |

Lehman Municipal Bond Index | –1.9 | 1.9 | 2.8 |

Citigroup 3-Month Treasury Bill Index | 2.6 | 4.0 | 3.1 |

|

|

|

|

|

|

|

|

CPI |

|

|

|

Consumer Price Index | 4.9% | 3.2% | 3.4% |

3

funds rate from 4.75% to 2.00%. On October 8, shortly after the close of the fiscal period, the Fed cut rates again, to 1.50%. The move was made in coordination with rate cuts by several other central banks.

Fund’s poor stock selection hurt performance

Vanguard Growth and Income Fund’s advisor, Franklin Portfolio Associates, LLC, seeks to outperform the S&P 500 Index by relying on stock-selection models that overweight and underweight individual stocks relative to the index while closely mirroring the index’s sector weightings.

In this challenging market environment, the fund fell short of this goal. The benchmark suffered a double-digit decline, and the fund finished the period a few steps behind. Although trailing the index overall, the fund outperformed it in some sectors. For example, in information technology, the fund’s selections finished 11 percentage points ahead of the index’s tech stocks. In financials, although both the fund and benchmark sustained steep losses, the advisor slightly moderated the decline by avoiding some of the hardest-hit companies, including Freddie Mac, Fannie Mae, and Lehman Brothers Holdings.

During the fiscal year, the Growth and Income Fund’s biggest challenges in seeking to outpace its benchmark lay in the health care, materials, and consumer staples sectors. In health care, the fund’s subpar stock picks left it underweighted in the few pharmaceutical and biotech stocks

Expense Ratios1 |

|

|

| |

Your Fund Compared With Its Peer Group |

|

|

| |

|

|

|

| Average |

|

| Investor | Admiral | Large-Cap |

|

| Shares | Shares | Core Fund |

Growth and Income Fund | 0.32% | 0.18% | 1.29% | |

1 The fund expense ratios shown are from the prospectus dated January 28, 2008. For the fiscal year ended September 30, 2008, the fund’s expense ratios were 0.31% for Investor Shares and 0.16% for Admiral Shares. The peer-group expense ratio is derived from data provided by Lipper Inc. and captures information through year-end 2007.

4

that posted gains during the period. The fund’s materials holdings suffered because of the weakness in metals and mining stocks. For example, the fund’s largest materials investment, Freeport-McMoRan Copper & Gold, a leading international mining company based in Arizona, registered one of the sector’s worst yearly returns (–45%). Lastly, the fund’s consumer staples holdings were overweighted in stocks that performed poorly, mainly beverage companies like Pepsi Bottling Group.

The fund has benefited long-term investors

Over the past ten years (a period that included two bear markets), the Growth and Income Fund has returned an annualized 3.4%, slightly higher than the results of the S&P 500 Index and almost a full percentage point more than the average return of large-cap core mutual funds.

The fund’s performance edge comes both from its advisor’s stock-selection skills and the fund’s low costs. The advisor seeks to outperform the index without taking on additional risk. When stocks struggle, as they have recently, the fund will struggle, too. Over time, however, the fund’s risk-controlled stock-selection strategies have enhanced performance, while the fund’s low expenses have helped ensure that investors keep more of their returns in both good and bad market conditions.

A long-term perspective is key in uncertain markets

The past year’s unsettled market has left many investors disappointed and uncertain about their investments.

Total Returns |

|

Ten Years Ended September 30, 2008 |

|

| Average |

| Annual Return |

Growth and Income Fund | 3.4% |

S&P 500 Index | 3.1 |

Average Large-Cap Core Fund1 | 2.4 |

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1 Derived from data provided by Lipper Inc.

5

The stock market’s volatility has been dramatic, but a long-term perspective suggests that the financial markets’ sudden, unpredictable movements are an unavoidable trade-off for the potential to earn long-term returns superior to those of lower-risk assets. In such uncertain times, seasoned investors understand that panic is not the answer.

The best response to uncertainty is diversification both within and across asset classes, which is why we counsel investors to hold a broadly diversified portfolio of stocks and fixed income investments in proportions consistent with their goals, risk tolerance, and time horizon.

During the past 12 months, of course, even balanced portfolios of stocks and bonds have faced tough times, although they've outperformed many all-stock portfolios. Everything that history has taught us about the markets, however, suggests that these principles can put you in the best position to achieve long-term investment success. Vanguard Growth and Income Fund can play a valuable role in such a portfolio.

Thank you for entrusting your assets to Vanguard.

Sincerely,

F. William McNabb III

President and Chief Executive Officer

October 15, 2008

6

Advisor’s Report

A turbulent market environment

During the 12 months ended September 30, 2008, the U.S. stock market declined significantly. Although early in the period investors had hopes that rising delinquency and default rates on subprime home mortgages would remain an isolated issue and that the Federal Reserve Board’s rate cuts, which began last September, would help to stimulate the economy, such optimism proved unfounded.

The slow-motion credit crisis actually began in summer 2007, but gained speed in March 2008 when Bear Stearns was taken over by JPMorgan Chase and the U.S. Treasury. Financial stocks suffered through the rest of the first half of 2008, but in the third quarter IndyMac, Fannie Mae, Freddie Mac, Lehman Brothers Holdings, Merrill Lynch, American International Group, Washington Mutual, and Wachovia all either failed or required rescues of one kind or another.

Remarkably, the rest of the financial sector rebounded in the third quarter in anticipation of U.S. government assistance. This resulted in the extraordinary outcome that, despite the headline-grabbing failures, financial services was the strongest sector in the Standard & Poor’s 500 Index—the Growth and Income Fund’s benchmark—for the three months; however, financials was the index’s poorest-performing group for the full fiscal year.

We do not foresee a quick recovery from the current credit crisis. Banks do not have adequate capital to substitute for the disappearance of so much of the “shadow” banking system (commercial paper and asset-backed debt issuance). Also, for many banks, capital has been impaired and needs to be rebuilt. The deleveraging of the economy—even if the immediate crisis were solved today—will continue to reverberate through the system as financial and corporate deleveraging makes its way down to individual deleveraging. The slowdown that nine months ago was being called a “recession without layoffs” is certain to become a more traditional recession before long. On the positive side, it could eventually be an opportunity for patient capital to acquire high-quality assets at depressed prices.

Positive contributions from technology stocks and sector tilts

Stock selection in the fund over the past 12 months was strongest in the information technology sector. Tech stocks that generated positive returns relative to their index groupings include the following companies: Apple, which saw strong iPhone, iPod, and Macintosh sales during the year; Applied Materials, which had a difficult year but benefited from investor optimism about growth in its solar power and display businesses; and QUALCOMM, which settled its long-running patent dispute with Nokia. In other sectors, property insurer Chubb and pharmacy benefits provider Express Scripts outperformed their peers and also contributed to the fund’s performance.

7

Although we deliberately minimize the fund’s sector tilts (measured as the difference between the portfolio weighting and the S&P 500 Index weighting in a particular sector), we do not force the tilts to zero. During the previous 12 months, the fund’s small overweighting in energy and small underweighting in financials and telecommunication services contributed positively to the portfolio’s relative return. In addition, the fund’s tilt toward stocks with less leverage helped performance.

Stock-ranking process underperformed

The fund underperformed the S&P 500 Index for the full fiscal year primarily owing to the portfolio’s poor performance in fourth-quarter 2007. Year-to-date, the fund outpaced the index despite the turbulent market environment. Our stock-ranking process emphasizes stocks with positive value and growth/momentum characteristics. Over the full fiscal year, including our weak start, these types of stocks underperformed their average historical rate of return.

Holdings that weakened results included several financial stocks that were hurt by the mortgage crisis, such as Citigroup and Fifth Third Bancorp. At the same time, the fund either didn’t own, or held less than the benchmark weighting of, several financial stocks that performed relatively better, including Wells Fargo and U.S. Bancorp. In other sectors, oil refiner Valero Energy declined due to falling margins, and Biogen Idec fell as a result of safety concerns about its multiple sclerosis drug Tysabri.

The fund’s positioning and risk controls

We remain focused on our investment discipline as it applies to stock selection, portfolio construction, and implementation, and we believe the Growth and Income Fund is well positioned to achieve its long-run goal of outperforming the S&P 500 Index. We have emphasized and will continue to emphasize stocks with strong momentum and reasonable prices—stocks that historically have represented the most desirable market segment. At the same time, we are focused on controlling non-stock-specific risks in the portfolio. While we always seek to minimize the impact on the fund of industry, sector, market-capitalization, and other top-down risk factors, we believe that the current environment of increased volatility calls for increased caution, and in some cases tighter bands for allowable risk exposure. For example, we are being particularly careful to avoid positive exposure to leverage, as firms find it increasingly difficult to renew credit lines. We continue to believe the Growth and Income Fund is an excellent choice for those seeking a diversified exposure to large-cap U.S. equities.

Oliver E. Buckley, Chief Investment Officer

and Chief Executive Officer

Franklin Portfolio Associates, LLC1

October 17, 2008

1 Franklin Portfolio Associates, LLC has announced that, effective January 1, 2009, it expects to merge with Mellon Capital Management Corp. Both firms are wholly owned subsidiaries of The Bank of New York Mellon Corp.

8

Fund Profile

As of September 30, 2008

Portfolio Characteristics |

|

| |

|

| Comparative | Broad |

| Fund | Index1 | Index2 |

Number of Stocks | 123 | 499 | 4,679 |

Median Market Cap | $36.8B | $43.8B | $29.6B |

Price/Earnings Ratio | 13.0x | 14.8x | 15.5x |

Price/Book Ratio | 2.2x | 2.3x | 2.2x |

Yield3 |

| 2.4% | 2.3% |

Investor Shares | 2.2% |

|

|

Admiral Shares | 2.3% |

|

|

Return on Equity | 20.3% | 21.3% | 20.0% |

Earnings Growth Rate | 21.5% | 17.8% | 17.7% |

Foreign Holdings | 0.0% | 0.0% | 0.0% |

Turnover Rate | 96% | — | — |

Expense Ratio |

|

|

|

(9/30/2007)4 |

| — | — |

Investor Shares | 0.32% |

|

|

Admiral Shares | 0.18% |

|

|

Short-Term Reserves | 0.1% | — | — |

Sector Diversification (% of equity exposure) | |||

|

| Comparative | Broad |

| Fund | Index1 | Index2 |

Consumer Discretionary | 8.1% | 8.5% | 9.2% |

Consumer Staples | 12.7 | 12.2 | 10.5 |

Energy | 13.7 | 13.4 | 12.6 |

Financials | 15.5 | 15.9 | 17.3 |

Health Care | 12.3 | 13.1 | 13.0 |

Industrials | 11.4 | 11.1 | 11.4 |

Information Technology | 15.6 | 15.7 | 15.7 |

Materials | 3.6 | 3.4 | 3.7 |

Telecommunication |

|

|

|

Services | 2.8 | 3.1 | 2.8 |

Utilities | 4.3 | 3.6 | 3.8 |

Volatility Measures5 |

| |

| Fund Versus | Fund Versus |

| Comparative Index1 | Broad Index2 |

R-Squared | 0.97 | 0.96 |

Beta | 1.00 | 0.96 |

Ten Largest Holdings6 (% of total net assets) | |||

|

|

|

|

ExxonMobil Corp. | integrated oil |

|

|

| and gas | 5.2% |

|

General Electric Co. | industrial |

|

|

| conglomerates | 3.7 |

|

The Procter & Gamble Co. | household products | 3.3 |

|

Wal-Mart Stores, Inc. | hypermarkets and |

|

|

| supercenters | 2.5 |

|

Bank of America Corp. | diversified |

|

|

| financial services | 2.5 |

|

ConocoPhillips Co. | integrated oil |

|

|

| and gas | 2.5 |

|

Hewlett-Packard Co. | computer hardware | 2.2 |

|

Intel Corp. | semiconductors | 2.0 |

|

International Business |

|

|

|

Machines Corp. | computer hardware | 1.8 |

|

Monsanto Co. | fertilizers and |

|

|

| agricultural chemicals | 1.6 |

|

Top Ten |

| 27.3% |

|

Investment Focus

1 S&P 500 Index.

2 Dow Jones Wilshire 5000 Index.

3 30-day SEC yield for the fund; annualized dividend yield for the indexes. See the Glossary.

4 The expense ratios shown are from the prospectus dated January 28, 2008. For the fiscal year ended September 30, 2008, expense ratios were 0.31% for Investor Shares and 0.16% for Admiral Shares.

5 For an explanation of R-squared, beta, and other terms used here, see the Glossary.

6 The holdings listed exclude any temporary cash investments and equity index products.

9

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at www.vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

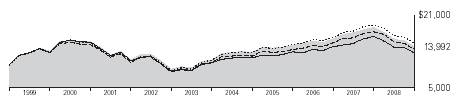

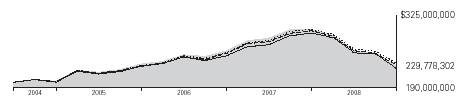

Cumulative Performance: September 30, 1998–September 30, 2008

Initial Investment of $10,000

| Average Annual Total Returns | Final Value | ||

| Periods Ended September 30, 2008 | of a $10,000 | ||

| One Year | Five Years | Ten Years | Investment |

Growth and Income Fund Investor Shares1 | –23.28% | 4.80% | 3.42% | $13,992 |

Dow Jones Wilshire 5000 Index | –21.20 | 6.04 | 4.00 | 14,801 |

S&P 500 Index | –21.98 | 5.17 | 3.06 | 13,520 |

Average Large-Cap Core Fund2 | –21.95 | 3.88 | 2.43 | 12,708 |

|

|

|

| Final Value |

|

|

| Since | of a $100,000 |

| One Year | Five Years | Inception3 | Investment |

Growth and Income Fund Admiral Shares | –23.19% | 4.96% | 0.92% | $107,016 |

Dow Jones Wilshire 5000 Index | –21.20 | 6.04 | 2.10 | 116,589 |

S&P 500 Index | –21.98 | 5.17 | 0.87 | 106,611 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Derived from data provided by Lipper Inc.

3 Performance for the fund’s Admiral Shares and comparative standards is calculated since the Admiral Shares’ inception: May 14, 2001.

10

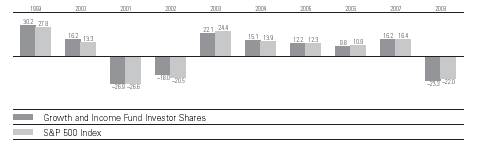

Fiscal-Year Total Returns (%): September 30, 1998–September 30, 2008

Note: See Financial Highlights tables for dividend and capital gains information.

11

Financial Statements

Statement of Net Assets

As of September 30, 2008

The fund provides a complete list of its holdings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at www.sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

|

|

| Market |

|

|

| Value• |

|

| Shares | ($000) |

Common Stocks (98.5%)1 |

|

| |

Consumer Discretionary (8.0%) |

|

| |

| The Walt Disney Co. | 2,420,285 | 74,279 |

| NIKE, Inc. Class B | 765,000 | 51,178 |

| Best Buy Co., Inc. | 1,202,900 | 45,109 |

| News Corp., Class A | 3,531,600 | 42,344 |

| H & R Block, Inc. | 1,412,900 | 31,861 |

| The Gap, Inc. | 1,591,400 | 28,295 |

* | Big Lots Inc. | 963,000 | 26,800 |

| Time Warner, Inc. | 1,816,200 | 23,810 |

* | GameStop Corp. Class A | 680,700 | 23,287 |

| Omnicom Group Inc. | 575,800 | 22,203 |

| Jones Apparel Group, Inc. | 1,059,600 | 19,613 |

| McDonald’s Corp. | 252,300 | 15,567 |

| Pulte Homes, Inc. | 1,110,300 | 15,511 |

| Tiffany & Co. | 395,200 | 14,037 |

| Hasbro, Inc. | 403,700 | 14,016 |

* | The Goodyear Tire & |

|

|

| Rubber Co. | 525,700 | 8,048 |

* | DIRECTV Group, Inc. | 299,900 | 7,848 |

|

|

| 463,806 |

Consumer Staples (12.5%) |

|

| |

| The Procter & Gamble Co. | 2,726,400 | 190,003 |

| Wal-Mart Stores, Inc. | 2,472,000 | 148,048 |

| Philip Morris |

|

|

| International Inc. | 1,715,300 | 82,506 |

| Sysco Corp. | 2,266,900 | 69,889 |

| Altria Group, Inc. | 2,169,400 | 43,041 |

| The Coca-Cola Co. | 683,800 | 36,159 |

| Coca-Cola Enterprises, Inc. | 1,946,600 | 32,644 |

| The Pepsi Bottling |

|

|

| Group, Inc. | 1,057,800 | 30,856 |

| Avon Products, Inc. | 453,400 | 18,848 |

| Archer-Daniels-Midland Co. | 818,900 | 17,942 |

| Reynolds American Inc. | 272,200 | 13,234 |

| Wm. Wrigley Jr. Co. | 162,500 | 12,902 |

| CVS/Caremark Corp. | 352,600 | 11,868 |

| Safeway, Inc. | 453,400 | 10,755 |

| PepsiCo, Inc. | 133,700 | 9,529 |

|

|

| 728,224 |

Energy (13.5%) |

|

| |

| ExxonMobil Corp. | 3,895,736 | 302,543 |

| ConocoPhillips Co. | 2,000,919 | 146,567 |

* | National Oilwell Varco Inc. | 1,508,400 | 75,767 |

| Williams Cos., Inc. | 2,643,000 | 62,507 |

| Chevron Corp. | 749,100 | 61,786 |

| Apache Corp. | 580,400 | 60,524 |

| BJ Services Co. | 1,410,600 | 26,985 |

| Baker Hughes, Inc. | 403,000 | 24,398 |

* | Southwestern Energy Co. | 605,500 | 18,492 |

| Massey Energy Co. | 148,700 | 5,304 |

|

|

| 784,873 |

Financials (15.2%) |

|

| |

| Bank of America Corp. | 4,191,599 | 146,706 |

| Northern Trust Corp. | 1,020,600 | 73,687 |

| Prudential Financial, Inc. | 1,007,500 | 72,540 |

| American Express Co. | 1,831,700 | 64,897 |

| AFLAC Inc. | 857,900 | 50,402 |

| State Street Corp. | 857,700 | 48,786 |

| Charles Schwab Corp. | 1,869,000 | 48,594 |

| The Goldman Sachs |

|

|

| Group, Inc. | 367,300 | 47,014 |

| ProLogis REIT | 1,016,400 | 41,947 |

| Hudson City Bancorp, Inc. | 2,069,000 | 38,173 |

| The Chubb Corp. | 638,800 | 35,070 |

| MetLife, Inc. | 551,700 | 30,895 |

| Wells Fargo & Co. | 755,700 | 28,361 |

| Apartment Investment |

|

|

| & Management Co. |

|

|

| Class A REIT | 755,600 | 26,461 |

| ^Zions Bancorp | 656,000 | 25,387 |

| ^BB&T Corp. | 655,800 | 24,789 |

| Marsh & |

|

|

| McLennan Cos., Inc. | 756,800 | 24,036 |

| Cincinnati Financial Corp. | 513,108 | 14,593 |

| NYSE Euronext | 324,200 | 12,702 |

* | IntercontinentalExchange Inc. | 150,800 | 12,167 |

| PNC Financial |

|

|

| Services Group | 151,200 | 11,295 |

| JPMorgan Chase & Co. | 180,400 | 8,425 |

|

|

| 886,927 |

12

|

|

| Market |

|

|

| Value• |

|

| Shares | ($000) |

Health Care (12.1%) |

|

| |

| Bristol-Myers Squibb Co. | 4,037,300 | 84,178 |

* | Express Scripts Inc. | 1,108,300 | 81,815 |

* | Biogen Idec Inc. | 1,513,700 | 76,124 |

| Stryker Corp. | 1,101,300 | 68,611 |

| Aetna Inc. | 1,817,400 | 65,626 |

| Pfizer Inc. | 3,529,227 | 65,079 |

| Merck & Co., Inc. | 1,816,200 | 57,319 |

* | Boston Scientific Corp. | 3,832,300 | 47,022 |

| Eli Lilly & Co. | 949,000 | 41,784 |

| CIGNA Corp. | 895,700 | 30,436 |

| Abbott Laboratories | 403,600 | 23,239 |

| Johnson & Johnson | 302,200 | 20,936 |

* | Watson Pharmaceuticals, Inc. | 602,500 | 17,171 |

| AmerisourceBergen Corp. | 302,200 | 11,378 |

* | Thermo Fisher Scientific, Inc. | 156,400 | 8,602 |

* | St. Jude Medical, Inc. | 185,300 | 8,059 |

|

|

| 707,379 |

Industrials (11.2%) |

|

| |

| General Electric Co. | 8,433,500 | 215,054 |

| Caterpillar, Inc. | 1,310,200 | 78,088 |

| Ingersoll-Rand Co. | 1,853,800 | 57,783 |

| CSX Corp. | 952,000 | 51,951 |

| General Dynamics Corp. | 654,900 | 48,214 |

| Northrop Grumman Corp. | 781,000 | 47,282 |

| Fluor Corp. | 622,700 | 34,684 |

| Union Pacific Corp. | 403,700 | 28,727 |

* | Allied Waste Industries, Inc. | 2,346,600 | 26,071 |

* | Jacobs Engineering |

|

|

| Group Inc. | 387,500 | 21,045 |

| L-3 Communications |

|

|

| Holdings, Inc. | 189,600 | 18,641 |

| The Manitowoc Co., Inc. | 921,200 | 14,325 |

| Deere & Co. | 176,400 | 8,732 |

| Goodrich Corp. | 118,700 | 4,938 |

|

|

| 655,535 |

Information Technology (15.3%) |

|

| |

| Hewlett-Packard Co. | 2,720,300 | 125,787 |

| Intel Corp. | 6,347,400 | 118,887 |

| International Business |

|

|

| Machines Corp. | 908,100 | 106,211 |

* | Oracle Corp. | 4,227,700 | 85,865 |

| Microsoft Corp. | 3,022,500 | 80,670 |

* | Apple Inc. | 706,300 | 80,278 |

* | Computer Sciences Corp. | 1,516,100 | 60,841 |

* | Google Inc. | 145,940 | 58,452 |

* | Cisco Systems, Inc. | 1,816,900 | 40,989 |

* | Juniper Networks, Inc. | 1,712,700 | 36,087 |

| Texas Instruments, Inc. | 1,410,400 | 30,324 |

* | Autodesk, Inc. | 745,000 | 24,995 |

* | Agilent Technologies, Inc. | 548,200 | 16,260 |

| Xilinx, Inc. | 503,800 | 11,814 |

| Corning, Inc. | 586,300 | 9,170 |

| Jabil Circuit, Inc. | 614,800 | 5,865 |

|

|

| 892,495 |

Materials (3.6%) |

|

| |

| Monsanto Co. | 959,700 | 94,991 |

| Freeport-McMoRan |

|

|

| Copper & Gold, Inc. |

|

|

| Class B | 807,996 | 45,935 |

| Nucor Corp. | 958,900 | 37,877 |

| Dow Chemical Co. | 723,400 | 22,990 |

| Alcoa Inc. | 335,000 | 7,564 |

|

|

| 209,357 |

Telecommunication Services (2.8%) |

|

| |

| AT&T Inc. | 3,375,100 | 94,233 |

| CenturyTel, Inc. | 1,882,800 | 69,005 |

|

|

| 163,238 |

Utilities (4.3%) |

|

| |

| Duke Energy Corp. | 4,685,000 | 81,660 |

| American Electric |

|

|

| Power Co., Inc. | 2,197,000 | 81,465 |

| Public Service Enterprise |

|

|

| Group, Inc. | 1,866,600 | 61,206 |

| Integrys Energy Group, Inc. | 201,800 | 10,078 |

* | AES Corp. | 805,500 | 9,416 |

| CenterPoint Energy Inc. | 403,400 | 5,878 |

|

|

| 249,703 |

Total Common Stocks |

|

| |

(Cost $6,083,548) |

| 5,741,537 | |

Temporary Cash Investments (2.0%)1 |

|

| |

Money Market Fund (1.9%) |

|

| |

2,3 | Vanguard Market |

|

|

| Liquidity Fund, 2.296% | 109,755,869 | 109,756 |

|

|

|

|

|

|

|

|

|

| Face |

|

|

| Amount |

|

|

| ($000) |

|

U.S. Government Obligation (0.1%) |

|

| |

| U.S. Treasury Bill |

|

|

4 | 1.252%, 11/6/08 | 6,200 | 6,194 |

Total Temporary Cash Investments |

|

| |

(Cost $115,950) |

| 115,950 | |

Total Investments (100.5%) |

|

| |

(Cost $6,199,498) |

| 5,857,487 | |

Other Assets and Liabilities (–0.5%) |

|

| |

Other Assets |

| 16,244 | |

Liabilities3 |

| (47,831) | |

|

|

| (31,587) |

Net Assets (100%) |

| 5,825,900 | |

13

At September 30, 2008, net assets consisted of: | |

| Amount |

| ($000) |

Paid-in Capital | 6,720,351 |

Undistributed Net Investment Income | 17,713 |

Accumulated Net Realized Losses | (569,252) |

Unrealized Appreciation (Depreciation) |

|

Investment Securities | (342,011) |

Futures Contracts | (901) |

Net Assets | 5,825,900 |

|

|

|

|

Investor Shares—Net Assets |

|

Applicable to 151,679,223 outstanding |

|

$.001 par value shares of beneficial |

|

interest (unlimited authorization) | 3,918,851 |

Net Asset Value Per Share— |

|

Investor Shares | $25.84 |

|

|

|

|

Admiral Shares—Net Assets |

|

Applicable to 45,191,727 outstanding |

|

$.001 par value shares of beneficial |

|

interest (unlimited authorization) | 1,907,049 |

Net Asset Value Per Share— |

|

Admiral Shares | $42.20 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Part of security position is on loan to broker-dealers.The total value of securities on loan is $20,509,000.

1 The fund invests a portion of its cash reserves in equity markets through the use of index futures contracts. After giving effect to futures investments, the fund’s effective common stock and temporary cash investment positions represent 100.0% and 0.5%, respectively, of net assets.

2 Affiliated money market fund available only to Vanguard funds and certain trusts and accounts managed by Vanguard. Rate shown is the 7-day yield.

3 Includes $21,178,000 of collateral received for securities on loan.

4 Securities with a value of $6,194,000 have been segregated as initial margin for open futures contracts.

REIT—Real Estate Investment Trust.

See accompanying Notes, which are an integral part of the Financial Statements.

14

Statement of Operations

| Year Ended |

| September 30, 2008 |

| ($000) |

Investment Income |

|

Income |

|

Dividends | 136,118 |

Interest1 | 3,293 |

Security Lending | 993 |

Total Income | 140,404 |

Expenses |

|

Investment Advisory Fees—Note B |

|

Basic Fee | 6,148 |

Performance Adjustment | (1,446) |

The Vanguard Group—Note C |

|

Management and Administrative—Investor Shares | 10,094 |

Management and Administrative—Admiral Shares | 1,771 |

Marketing and Distribution—Investor Shares | 965 |

Marketing and Distribution—Admiral Shares | 465 |

Custodian Fees | 53 |

Auditing Fees | 21 |

Shareholders’ Reports—Investor Shares | 136 |

Shareholders’ Reports—Admiral Shares | 12 |

Trustees’ Fees and Expenses | 11 |

Total Expenses | 18,230 |

Expenses Paid Indirectly | (1,556) |

Net Expenses | 16,674 |

Net Investment Income | 123,730 |

Realized Net Gain (Loss) |

|

Investment Securities Sold | (425,923) |

Futures Contracts | (20,593) |

Realized Net Gain (Loss) | (446,516) |

Change in Unrealized Appreciation (Depreciation) |

|

Investment Securities | (1,517,873) |

Futures Contracts | (2,975) |

Change in Unrealized Appreciation (Depreciation) | (1,520,848) |

Net Increase (Decrease) in Net Assets Resulting from Operations | (1,843,634) |

1 Interest income from an affiliated company of the fund was $3,200,000.

See accompanying Notes, which are an integral part of the Financial Statements.

15

Statement of Changes in Net Assets

| Year Ended September 30, | |

| 2008 | 2007 |

| ($000) | ($000) |

Increase (Decrease) in Net Assets |

|

|

Operations |

|

|

Net Investment Income | 123,730 | 132,725 |

Realized Net Gain (Loss) | (446,516) | 912,849 |

Change in Unrealized Appreciation (Depreciation) | (1,520,848) | 134,840 |

Net Increase (Decrease) in Net Assets Resulting from Operations | (1,843,634) | 1,180,414 |

Distributions |

|

|

Net Investment Income |

|

|

Investor Shares | (81,970) | (88,650) |

Admiral Shares | (43,850) | (46,594) |

Realized Capital Gain1 |

|

|

Investor Shares | (564,334) | — |

Admiral Shares | (284,167) | — |

Total Distributions | (974,321) | (135,244) |

Capital Share Transactions |

|

|

Investor Shares | 335,349 | (333,115) |

Admiral Shares | 50,006 | 138,269 |

Net Increase (Decrease) from Capital Share Transactions | 385,355 | (194,846) |

Total Increase (Decrease) | (2,432,600) | 850,324 |

Net Assets |

|

|

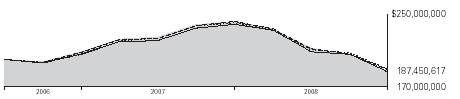

Beginning of Period | 8,258,500 | 7,408,176 |

End of Period2 | 5,825,900 | 8,258,500 |

1 Includes fiscal 2008 short-term gain distributions totaling $89,550,000. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed net investment income of $17,713,000 and $19,803,000. See accompanying Notes, which are an integral part of the Financial Statements.

16

Financial Highlights

Investor Shares |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

For a Share Outstanding | Year Ended September 30, | ||||

Throughout Each Period | 2008 | 2007 | 2006 | 2005 | 2004 |

Net Asset Value, Beginning of Period | $38.62 | $33.79 | $31.29 | $28.31 | $24.91 |

Investment Operations |

|

|

|

|

|

Net Investment Income | .546 | .600 | .550 | .460 | .370 |

Net Realized and Unrealized Gain (Loss) |

|

|

|

|

|

on Investments | (8.758) | 4.840 | 2.470 | 2.980 | 3.390 |

Total from Investment Operations | (8.212) | 5.440 | 3.020 | 3.440 | 3.760 |

Distributions |

|

|

|

|

|

Dividends from Net Investment Income | (.560) | (.610) | (.520) | (.460) | (.360) |

Distributions from Realized Capital Gains | (4.008) | — | — | — | — |

Total Distributions | (4.568) | (.610) | (.520) | (.460) | (.360) |

Net Asset Value, End of Period | $25.84 | $38.62 | $33.79 | $31.29 | $28.31 |

|

|

|

|

|

|

|

|

|

|

|

|

Total Return1 | –23.28% | 16.20% | 9.76% | 12.20% | 15.12% |

|

|

|

|

|

|

|

|

|

|

|

|

Ratios/Supplemental Data |

|

|

|

|

|

Net Assets, End of Period (Millions) | $3,919 | $5,465 | $5,088 | $5,202 | $5,780 |

Ratio of Total Expenses to |

|

|

|

|

|

Average Net Assets2 | 0.31% | 0.32% | 0.38% | 0.40% | 0.42% |

Ratio of Net Investment Income to |

|

|

|

|

|

Average Net Assets | 1.69% | 1.61% | 1.65% | 1.53% | 1.35% |

Portfolio Turnover Rate | 96% | 100% | 93% | 84% | 79%3 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

2 Includes performance-based investment advisory fee increases (decreases) of (0.02%), 0.00%, 0.01%, 0.01%, and 0.01%.

3 Excludes the value of portfolio securities received or delivered as a result of in-kind purchases or redemptions of the fund’s capital shares. See accompanying Notes, which are an integral part of the Financial Statements.

17

Admiral Shares |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

For a Share Outstanding | Year Ended September 30, | ||||

Throughout Each Period | 2008 | 2007 | 2006 | 2005 | 2004 |

Net Asset Value, Beginning of Period | $63.08 | $55.20 | $51.12 | $46.25 | $40.70 |

Investment Operations |

|

|

|

|

|

Net Investment Income | .963 | 1.070 | .997 | .849 | .683 |

Net Realized and Unrealized Gain (Loss) |

|

|

|

|

|

on Investments | (14.313) | 7.903 | 4.036 | 4.853 | 5.530 |

Total from Investment Operations | (13.350) | 8.973 | 5.033 | 5.702 | 6.213 |

Distributions |

|

|

|

|

|

Dividends from Net Investment Income | (.985) | (1.093) | (.953) | (.832) | (.663) |

Distributions from Realized Capital Gains | (6.545) | — | — | — | — |

Total Distributions | (7.530) | (1.093) | (.953) | (.832) | (.663) |

Net Asset Value, End of Period | $42.20 | $63.08 | $55.20 | $51.12 | $46.25 |

|

|

|

|

|

|

|

|

|

|

|

|

Total Return | –23.19% | 16.37% | 9.97% | 12.39% | 15.29% |

|

|

|

|

|

|

|

|

|

|

|

|

Ratios/Supplemental Data |

|

|

|

|

|

Net Assets, End of Period (Millions) | $1,907 | $2,794 | $2,321 | $2,039 | $843 |

Ratio of Total Expenses to |

|

|

|

|

|

Average Net Assets1 | 0.16% | 0.18% | 0.20% | 0.23% | 0.25% |

Ratio of Net Investment Income to |

|

|

|

|

|

Average Net Assets | 1.84% | 1.75% | 1.83% | 1.68% | 1.51% |

Portfolio Turnover Rate | 96% | 100% | 93% | 84% | 79%2 |

1 Includes performance-based investment advisory fee increases (decreases) of (0.02%), 0.00%, 0.01%, 0.01%, and 0.01%.

2 Excludes the value of portfolio securities received or delivered as a result of in-kind purchases or redemptions of the fund’s capital shares. See accompanying Notes, which are an integral part of the Financial Statements.

18

Notes to Financial Statements

Vanguard Growth and Income Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund. The fund offers two classes of shares, Investor Shares and Admiral Shares. Investor Shares are available to any investor who meets the fund’s minimum purchase requirements. Admiral Shares are designed for investors who meet certain administrative, service, tenure, and account-size criteria.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. mutual funds. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments are valued at amortized cost, which approximates market value.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued at their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken on federal income tax returns for all open tax years (tax years ended September 30, 2005–2008), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Security Lending: The fund may lend its securities to qualified institutional borrowers to earn additional income. Security loans are required to be secured at all times by collateral at least equal to the market value of securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability for the return of the collateral, during the period the securities are on loan. Security lending income represents the income earned on investing cash collateral, less expenses associated with the loan.

19

6. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

Each class of shares has equal rights as to assets and earnings, except that each class separately bears certain class-specific expenses related to maintenance of shareholder accounts (included in Management and Administrative expenses) and shareholder reporting. Marketing and distribution expenses are allocated to each class of shares based on a method approved by the board of trustees. Income, other non-class-specific expenses, and gains and losses on investments are allocated to each class of shares based on its relative net assets.

B. Franklin Portfolio Associates, LLC, provides investment advisory services to the fund for a fee calculated at an annual percentage rate of average net assets. The basic fee is subject to quarterly adjustments based on the fund’s performance for the preceding three years relative to the S&P 500 Index. For the year ended September 30, 2008, the investment advisory fee represented an effective annual basic rate of 0.09% of the fund’s average net assets before a decrease of $1,446,000 (0.02%) based on performance.

C. The Vanguard Group furnishes at cost corporate management, administrative, marketing, and distribution services. The costs of such services are allocated to the fund under methods approved by the board of trustees. The fund has committed to provide up to 0.40% of its net assets in capital contributions to Vanguard. At September 30, 2008, the fund had contributed capital of $555,000 to Vanguard (included in Other Assets), representing 0.01% of the fund’s net assets and 0.55% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and officers of Vanguard.

D. The fund has asked its investment advisor to direct certain security trades, subject to obtaining the best price and execution, to brokers who have agreed to rebate to the fund part of the commissions generated. Such rebates are used solely to reduce the fund’s management and administrative expenses. The fund’s custodian bank has also agreed to reduce its fees when the fund maintains cash on deposit in the non-interest-bearing custody account. For the year ended September 30, 2008, these arrangements reduced the fund’s management and administrative expenses by $1,555,000 and custodian fees by $1,000. The total expense reduction represented an effective annual rate of 0.02% of the fund’s average net assets.

E. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

For tax purposes, at September 30, 2008, the fund had $34,599,000 of ordinary income available for distribution. Tax-basis capital gains required to be distributed in December 2007 included net capital gains realized through October 31, 2007. Subsequently, the fund realized capital losses of $570,743,000, which are available to offset future net capital gains.

20

At September 30, 2008, the cost of investment securities for tax purposes was $6,199,498,000. Net unrealized depreciation of investment securities for tax purposes was $342,011,000, consisting of unrealized gains of $390,992,000 on securities that had risen in value since their purchase and $733,003,000 in unrealized losses on securities that had fallen in value since their purchase.

At September 30, 2008, the aggregate settlement value of open futures contracts expiring in December 2008 and the related unrealized appreciation (depreciation) were:

|

|

| ($000) |

| Number of | Aggregate | Unrealized |

| Long (Short) | Settlement | Appreciation |

Futures Contracts | Contracts | Value | (Depreciation) |

S&P 500 Index | 290 | 84,753 | (901) |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

F. During the year ended September 30, 2008, the fund purchased $6,696,223,000 of investment securities and sold $7,157,841,000 of investment securities, other than temporary cash investments.

G. Capital share transactions for each class of shares were:

| Year Ended September 30, | ||||

|

| 2008 |

|

| 2007 |

| Amount | Shares |

| Amount | Shares |

| ($000) | (000) |

| ($000) | (000) |

Investor Shares |

|

|

|

|

|

Issued | 550,897 | 17,490 |

| 581,626 | 15,817 |

Issued in Lieu of Cash Distributions | 622,470 | 19,829 |

| 84,713 | 2,312 |

Redeemed | (838,018) | (27,137) |

| (999,454) | (27,194) |

Net Increase (Decrease)—Investor Shares | 335,349 | 10,182 |

| (333,115) | (9,065) |

Admiral Shares |

|

|

|

|

|

Issued | 220,621 | 4,296 |

| 491,880 | 8,143 |

Issued in Lieu of Cash Distributions | 305,215 | 5,955 |

| 42,270 | 706 |

Redeemed | (475,830) | (9,345) |

| (395,881) | (6,600) |

Net Increase (Decrease)—Admiral Shares | 50,006 | 906 |

| 138,269 | 2,249 |

21

H. In September 2006, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 157 (“FAS 157”), “Fair Value Measurements.” FAS 157 establishes a framework for measuring fair value and expands disclosures about fair value measurements in financial statements.

The various inputs that may be used to determine the value of the fund’s investments are summarized in three broad levels. The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments).

The following table summarizes the fund's investments as of September 30, 2008, based on the inputs used to value them:

| Investments | Futures |

| in Securities | Contracts |

Valuation Inputs | ($000) | ($000) |

Level 1—Quoted prices | 5,851,293 | (901) |

Level 2—Other significant observable inputs | 6,194 | — |

Level 3—Significant unobservable inputs | — | — |

Total | 5,857,487 | (901) |

22

Report of Independent Registered

Public Accounting Firm

To the Trustees of Vanguard Quantitative Funds and the Shareholders of Vanguard Growth and Income Fund:

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard Growth and Income Fund (the “Fund”) at September 30, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at September 30, 2008 by correspondence with the custodian and broker, and by agreement to the underlying ownership records for Vanguard Market Liquidity Fund, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

November 19, 2008

Special 2008 tax information (unaudited) for Vanguard Growth and Income Fund

This information for the fiscal year ended September 30, 2008, is included pursuant to provisions of the Internal Revenue Code.

The fund distributed $759,528,000 as capital gain dividends (from net long-term capital gains) to shareholders during the fiscal year.

For non-resident alien shareholders, 100% of short-term capital gain dividends distributed by the fund are qualified short-term capital gains.

The fund distributed $135,688,000 of qualified dividend income to shareholders during the fiscal year.

For corporate shareholders, 96.8% of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

23

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2008. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

The table shows returns for Investor Shares only; returns for other share classes will differ. Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

Average Annual Total Returns: Growth and Income Fund Investor Shares1 |

|

| |

Periods Ended September 30, 2008 |

|

|

|

| One | Five | Ten |

| Year | Years | Years |

Returns Before Taxes | –23.28% | 4.80% | 3.42% |

Returns After Taxes on Distributions | –24.92 | 4.15 | 2.65 |

Returns After Taxes on Distributions and Sale of Fund Shares | –12.73 | 4.18 | 2.81 |

1 Total returns do not include the account service fee that may be applicable to certain accounts with balances below $10,000.

24

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the fund’s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading “Expenses Paid During Period.”

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund’s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Six Months Ended September 30, 2008 |

|

|

|

| Beginning | Ending | Expenses |

| Account Value | Account Value | Paid During |

Growth and Income Fund | 3/31/2008 | 9/30/2008 | Period1 |

Based on Actual Fund Return |

|

|

|

Investor Shares | $1,000.00 | $895.47 | $1.47 |

Admiral Shares | 1,000.00 | 896.06 | 0.76 |

Based on Hypothetical 5% Yearly Return |

|

|

|

Investor Shares | $1,000.00 | $1,023.51 | $1.57 |

Admiral Shares | 1,000.00 | 1,024.27 | 0.81 |

1 The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratios for that period are 0.31% for Investor Shares and 0.16% for Admiral Shares. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period.

25

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include the account service fee described in the prospectus. If such a fee were applied to your account, your costs would be higher. Your fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

26

Trustees Approve Advisory Agreement

The board of trustees of Vanguard Growth and Income Fund has renewed the fund’s investment advisory agreement with Franklin Portfolio Associates, LLC. The board determined that the retention of Franklin was in the best interests of the fund and its shareholders.

The board based its decision upon an evaluation of the advisor’s investment staff, portfolio management process, and performance. The trustees considered the factors discussed below, among others. However, no single factor determined whether the board approved the agreement. Rather, it was the totality of the circumstances that drove the board’s decision.

Nature, extent, and quality of services

The board considered the quality of investment management to the fund over both the short and long term, and took into account the organizational depth and stability of the advisor. The board noted that Franklin, founded in 1982, is known for quantitative equity management combining investment experience, financial databases, and computer modeling. The firm has advised the Growth and Income Fund since the fund’s inception in 1986. The investment team at Franklin employs a quantitative investment strategy that seeks to provide a total return greater than that of the S&P 500 Index by investing in U.S. large- and mid-capitalization stocks. Stock selection is driven by a series of more than 40 computer models covering a broad range of public data.

The board concluded that the advisor’s experience, stability, depth, and performance, among other factors, warranted continuation of the advisory agreement.

Investment performance

The board considered the short- and long-term performance of the fund, including any periods of outperformance or underperformance of a relevant benchmark and peer group. The board noted that the advisor has carried out the fund’s investment strategy in disciplined fashion, and that the results have been in line with expectations. Information about the fund’s most recent performance can be found in the Performance Summary section of this report.

Cost

The board concluded that the fund’s expense ratio was far below the average expense ratio charged by funds in its peer group. The board noted that the fund’s advisory fee rate was also well below the peer-group average. Information about the fund’s expense ratio appears in the About Your Fund’s Expenses section of this report as well as in the Financial Statements section, which also includes information about the advisory fee rate. The board did not consider profitability of Franklin in determining whether to approve the advisory fee, because Franklin is independent of Vanguard, and the advisory fee is the result of arm’s-length negotiations.

The benefit of economies of scale

The board concluded that the fund’s shareholders benefit from economies of scale because of breakpoints in the fund’s advisory fee schedule. The breakpoints reduce the effective rate of the fee as the fund’s assets increase.

The board will consider whether to renew the advisory agreement again after a one-year period.

27

Glossary

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. The percentage of a fund’s average net assets used to pay its annual administrative and advisory expenses. These expenses directly reduce returns to investors.

Foreign Holdings. The percentage of a fund represented by stocks or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share. For a fund, the weighted average price/book ratio of the stocks it holds.

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

28

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (in the case of bonds) or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

29

This page intentionally left blank.

This page intentionally left blank.

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals.

Our independent board members bring distinguished backgrounds in business, academia, and public service to their task of working with Vanguard officers to establish the policies and oversee the activities of the funds. Among board members’ responsibilities are selecting investment advisors for the funds; monitoring fund operations, performance, and costs; reviewing contracts; nominating and selecting new trustees/directors; and electing Vanguard officers.

Each trustee serves a fund until its termination; or until the trustee’s retirement, resignation, or death; or otherwise as specified in the fund’s organizational documents. Any trustee may be removed at a shareholders’ meeting by a vote representing two-thirds of the net asset value of all shares of the fund together with shares of other Vanguard funds organized within the same trust. The table on these two pages shows information for each trustee and executive officer of the fund. The mailing address of the trustees and officers is P.O. Box 876, Valley Forge, PA 19482.

Chairman of the Board and Trustee

John J. Brennan1

Born 1954 Principal Occupation(s) During the Past Five Years: Chairman of the Board and Director/ Trustee Since May 1987; Trustee of The Vanguard Group, Inc., and of each of the investment companies served Chairman of the Board by The Vanguard Group; Chief Executive Officer and President of The Vanguard Group 156 Vanguard Funds Overseen and of each of the investment companies served by The Vanguard Group (1996–2008).

Independent Trustees

Charles D. Ellis

Born 1937 Principal Occupation(s) During the Past Five Years: Applecore Partners (pro bono ventures Trustee Since January 2001 in education); Senior Advisor to Greenwich Associates (international business strategy 156 Vanguard Funds Overseen consulting); Successor Trustee of Yale University; Overseer of the Stern School of Business at New York University; Trustee of the Whitehead Institute for Biomedical Research.

Emerson U. Fullwood

Born 1948 Principal Occupation(s) During the Past Five Years: Executive Chief Staff and Marketing Trustee Since January 2008 Officer for North America since 2004 and Corporate Vice President of Xerox Corporation 156 Vanguard Funds Overseen (photocopiers and printers); Director of SPX Corporation (multi-industry manufacturing), of the United Way of Rochester, and of the Boy Scouts of America.

Rajiv L. Gupta

Born 1945 Principal Occupation(s) During the Past Five Years: Chairman, President, and Trustee Since December 20012 Chief Executive Officer of Rohm and Haas Co. (chemicals); Board Member of 156 Vanguard Funds Overseen the American Chemistry Council; Director of Tyco International, Ltd. (diversified manufacturing and services) since 2005.

Amy Gutmann

Born 1949 Principal Occupation(s) During the Past Five Years: President of the University of

Trustee Since June 2006 Pennsylvania since 2004; Professor in the School of Arts and Sciences, Annenberg School 156 Vanguard Funds Overseen for Communication, and Graduate School of Education of the University of Pennsylvania since 2004; Provost (2001–2004) and Laurance S. Rockefeller Professor of Politics and the University Center for Human Values (1990–2004), Princeton University; Director of Carnegie Corporation of New York since 2005 and of Schuylkill River Development Corporation and Greater Philadelphia Chamber of Commerce since 2004; Trustee of the National Constitution Center since 2007.

JoAnn Heffernan Heisen

Born 1950 Principal Occupation(s) During the Past Five Years: Corporate Vice President and Trustee Since July 1998 Chief Global Diversity Officer since 2006, Vice President and Chief Information 156 Vanguard Funds Overseen Officer (1997–2005), and Member of the Executive Committee of Johnson & Johnson (pharmaceuticals/consumer products); Director of the University Medical Center at Princeton and Women’s Research and Education Institute.

André F. Perold

Born 1952 Principal Occupation(s) During the Past Five Years: George Gund Professor of Finance Trustee Since December 2004 and Banking, Harvard Business School; Senior Associate Dean and Director of Faculty 156 Vanguard Funds Overseen Recruiting, Harvard Business School; Director and Chairman of UNX, Inc. (equities trading firm); Chair of the Investment Committee of HighVista Strategies LLC (private investment firm) since 2005.

Alfred M. Rankin, Jr.

Born 1941 Principal Occupation(s) During the Past Five Years: Chairman, President, Chief Executive Trustee Since January 1993 Officer, and Director of NACCO Industries, Inc. (forklift trucks/housewares/lignite); Director 156 Vanguard Funds Overseen of Goodrich Corporation (industrial products/aircraft systems and services).

J. Lawrence Wilson

Born 1936 Principal Occupation(s) During the Past Five Years: Retired Chairman and Chief Executive Trustee Since April 1985 Officer of Rohm and Haas Co. (chemicals); Director of Cummins Inc. (diesel engines) and 156 Vanguard Funds Overseen AmerisourceBergen Corp. (pharmaceutical distribution); Trustee of Vanderbilt University and of Culver Educational Foundation.

Executive Officers1

Thomas J. Higgins

Born 1957 Principal Occupation(s) During the Past Five Years: Principal of The Vanguard Group, Inc.; Chief Financial Officer Treasurer of each of the investment companies served by The Vanguard Group; Chief Since September 2008 Financial Officer of each of the investment companies served by The Vanguard Treasurer Since July 1998 Group since 2008. 156 Vanguard Funds Overseen

F. William McNabb III

Born 1957 Principal Occupation(s) During the Past Five Years: Chief Executive Officer, Director, Chief Executive Officer and President of The Vanguard Group, Inc., since 2008; Chief Executive Officer and Since August 31, 2008 President of each of the investment companies served by The Vanguard Group since President Since March 2008 2008; Director of Vanguard Marketing Corporation; Managing Director of The Vanguard 156 Vanguard Funds Overseen Group (1995–2008).

Heidi Stam

Born 1956 Principal Occupation(s) During the Past Five Years: Managing Director of The Vanguard Secretary Since July 2005 Group, Inc., since 2006; General Counsel of The Vanguard Group since 2005; Secretary of 156 Vanguard Funds Overseen The Vanguard Group and of each of the investment companies served by The Vanguard Group since 2005; Director and Senior Vice President of Vanguard Marketing Corporation since 2005; Principal of The Vanguard Group (1997–2006).

Vanguard Senior Management Team |

|

| |

|

|

|

|

R. Gregory Barton | Kathleen C. Gubanich | Michael S. Miller | Glenn W. Reed |

Mortimer J. Buckley | Paul A. Heller | Ralph K. Packard | George U. Sauter |

Founder

John C. Bogle

Chairman and Chief Executive Officer, 1974–1996

1 These individuals are “interested persons” as defined in the Investment Company Act of 1940.

2 December 2002 for Vanguard Equity Income Fund, Vanguard Growth Equity Fund, the Vanguard Municipal Bond Funds, and the Vanguard State Tax-Exempt Funds.

More information about the trustees is in the Statement of Additional Information, available from The Vanguard Group.

P.O. Box 2600

Valley Forge, PA 19482-2600

Connect with Vanguard® > www.vanguard.com

Fund Information > 800-662-7447 | All comparative mutual fund data are from Lipper Inc. |

| or Morningstar, Inc., unless otherwise noted. |

Direct Investor Account Services > 800-662-2739 |

|

| You can obtain a free copy of Vanguard’s proxy voting |

Institutional Investor Services > 800-523-1036 | guidelines by visiting our website, www.vanguard.com, |

| and searching for “proxy voting guidelines,” or by |

Text Telephone for People | calling Vanguard at 800-662-2739. The guidelines are |

With Hearing Impairment > 800-952-3335 | also available from the SEC’s website, www.sec.gov. |