UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04892

Templeton Growth Fund, Inc.

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant's telephone number, including area code: (954) 527-7500_

Date of fiscal year end: _8/31__

Date of reporting period: 8/31/15__

Item 1. Reports to Stockholders.

Annual Report and Shareholder Letter

August 31, 2015

Templeton Growth Fund, Inc.

Franklin Templeton Investments

Gain From Our Perspective®

At Franklin Templeton Investments, we’re dedicated to one goal: delivering exceptional asset management for our clients. By bringing together multiple, world-class investment teams in a single firm, we’re able to offer specialized expertise across styles and asset classes, all supported by the strength and resources of one of the world’s largest asset managers. This has helped us to become a trusted partner to individual and institutional investors across the globe.

Focus on Investment Excellence

At the core of our firm, you’ll find multiple independent investment teams—each with a focused area of expertise—from traditional to alternative strategies and multi-asset solutions. And because our portfolio groups operate autonomously, their strategies can be combined to deliver true style and asset class diversification.

All of our investment teams share a common commitment to excellence grounded in rigorous, fundamental research and robust, disciplined risk management. Decade after decade, our consistent, research-driven processes have helped Franklin Templeton earn an impressive record of strong, long-term results.

Global Perspective Shaped by Local Expertise

In today’s complex and interconnected world, smart investing demands a global perspective. Franklin Templeton pioneered international investing over 60 years ago, and our expertise in emerging markets spans more than a quarter of a century. Today, our investment professionals are on the ground across the globe, spotting investment ideas and potential risks firsthand. These locally based teams bring in-depth understanding of local companies, economies and cultural nuances, and share their best thinking across our global research network.

Strength and Experience

Franklin Templeton is a global leader in asset management serving clients in over 150 countries.1 We run our business with the same prudence we apply to asset management, staying focused on delivering relevant investment solutions, strong long-term results and reliable, personal service. This approach, focused on putting clients first, has helped us to become one of the most trusted names in financial services.

1. As of 12/31/14. Clients are represented by the total number of shareholder accounts.

Not FDIC Insured | May Lose Value | No Bank Guarantee

| |

| Contents | |

| |

| Shareholder Letter | 1 |

| Annual Report | |

| Templeton Growth Fund, Inc. | 3 |

| Performance Summary | 9 |

| Your Fund’s Expenses | 14 |

| Financial Highlights and | |

| Statement of Investments | 16 |

| Financial Statements | 25 |

| Notes to Financial Statements | 29 |

| Report of Independent Registered | |

| Public Accounting Firm | 38 |

| Tax Information | 39 |

| Board Members and Officers | 40 |

| Shareholder Information | 45 |

franklintempleton.com Not part of the annual report | 1

Annual Report

Templeton Growth Fund, Inc.

This annual report for Templeton Growth Fund covers the fiscal year ended August 31, 2015.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests primarily in equity securities of companies located anywhere in the world, including developing markets.

Performance Overview

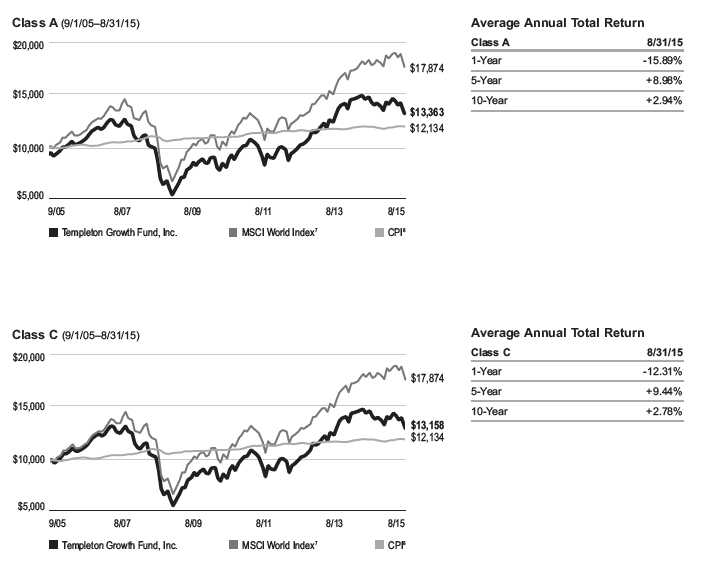

The Fund’s Class A shares had a -10.76% cumulative total return for the 12 months under review. In comparison, the MSCI World Index, which measures stock performance in global developed markets, had a -3.61% total return.1 The Fund’s long-term relative results are shown in the Performance Summary beginning on page 9. For the 10-year period ended August 31, 2015, the Fund’s Class A shares generated a +41.76% cumulative total return, compared with the MSCI World Index’s +78.74% cumulative total return for the same period.1 Please note index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find more performance data in the Performance Summary.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

Economic and Market Overview

The global economy expanded moderately during the 12 months under review despite slowing growth in some countries. As measured by the MSCI World Index, stocks in global developed markets overall declined during the period, although a generally accommodative monetary policy environment and signs of economic improvement in Europe provided some support. However, weighing on global stocks near period-end

was a rapid sell-off in China’s equity markets, despite the government’s monetary easing effort. Over the reporting period, oil prices declined sharply owing largely to strong global supply, and gold and other commodity prices also fell. The U.S. dollar appreciated against most currencies during the period, which reduced returns of many foreign assets in U.S. dollar terms.

U.S. economic growth was mixed during the 12 months under review. In 2014’s fourth quarter, growth expanded due to increased consumer spending, business investment, exports, and state and local government spending. Growth slowed in 2015’s first quarter as the U.S. dollar strengthened, energy prices fell, and a West Coast ports labor dispute led to decreased exports. However, growth rebounded in the second quarter due to increases in consumer spending, net exports, state and local government spending, and investments for businesses, homes and inventory. The U.S. Federal Reserve (Fed) ended its bond buying program in October 2014 and kept its target interest rate at 0%–0.25% while considering when to begin increasing it toward normal levels. During its July meeting, the Fed stated that although labor market and economic conditions had improved, committee members would like more confidence that inflation was moving toward their goal before raising the federal funds target rate. Furthermore, it regarded international

1. Source: Morningstar. As of 8/31/15, the Fund’s Class A 10-year average annual total return not including the maximum sales charge was +3.55%, compared with the

MSCI World Index’s 10-year average annual total return of +5.98%.

The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 21.

franklintempleton.com

Annual Report

| 3

TEMPLETON GROWTH FUND, INC.

developments, particularly moderating growth in China and other emerging markets and China’s unexpected currency devaluation, as well as a strengthening U.S. dollar, as potential risks to U.S. economic growth.

Outside the U.S., the U.K. economy grew in 2015’s second quarter supported by services and industrial production. Eurozone economic growth generally improved during the period. France’s economy stagnated due to lower consumer spending and business investment, which was partially offset by higher exports, while Italy expanded but at a slower pace. In contrast, Greece’s economy grew despite the country’s liquidity crisis. Germany’s economic growth rose slightly compared with the previous quarter largely due to strong exports, although at a lower-than-expected rate as weak inventories and investments weighed on the economy. The eurozone’s annual inflation rate rose beginning in May as services and food prices increased. In late 2014, the European Central Bank (ECB) reduced its interest rates, and in early 2015, it expanded asset purchases to avoid deflation and potentially boost the economy. Despite Greece’s debt issues and geopolitical tension in Ukraine, the region generally benefited from lower oil prices, a weaker euro that helped exports, the ECB’s accommodative policy and an improved 2015 eurozone growth forecast.

The Bank of Japan (BOJ) broadened its stimulus measures amid weak domestic demand and lower inflation. In December, Japan’s ruling coalition was reelected and announced a new stimulus package to revive economic growth. The country exited recession in the fourth quarter, supported largely by exports. Japan’s economy continued to grow in 2015’s first quarter, driven by increasing private demand as business investment and private consumption rose. However, growth contracted in the second quarter due to decreases in net exports, consumer spending and business investment. The BOJ lowered its economic growth and inflation forecasts twice during the period.

In emerging markets, economic growth generally moderated. In early 2015, a temporary solution to Greece’s dispute with the country’s international creditors and a Russia-Ukraine ceasefire agreement bolstered emerging market stocks. Later in the period, investors remained concerned about Greece’s economy, even though the country and its international creditors agreed on a third bailout package. In China, the government sought to cool domestic stock market speculation, but its intervention led to severe market volatility in June and July. Emerging market stocks, especially Chinese equities, slumped in August after China devalued the renminbi. This move sparked concerns among investors about China’s moderating economy and a possible currency war. Toward period-end,

China’s reluctance to implement widely anticipated monetary policy easing measures triggered a fresh sell-off in the domestic equity market, forcing China’s central bank to reduce the benchmark interest rate and the reserve ratio requirement.

In the recent global environment, emerging market stocks, as measured by the MSCI Emerging Markets Index, fell for the 12-month period.

Investment Strategy

Our investment strategy employs a bottom-up, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. As we look worldwide, we consider specific companies, rather than sectors or countries, while doing in-depth research to construct a bargain list from which we buy. Before we make a purchase, we look at the company’s price/earnings ratio, price/cash flow ratio, profit margins and liquidation value.

Manager’s Discussion

The 12 months under review brought renewed volatility to global equity markets and renewed headwinds for our patient, bottom-up value investment approach. The years since the onset of the global financial crisis have come to represent one of the most challenging periods of our investment career. The problem has not been absolute returns, as the Fund has generated significant gains since the depths of the global financial crisis. We believe the problem has been an unusually hostile market for value investors. In fact, value as a style is on track to underper-form growth for its ninth consecutive year, the longest stretch on record. Although the Fund has weathered deeper periods of underperformance in the past, this latest episode of relative weakness has been notable for being the longest on record.

In our opinion, recent performance was an anomaly. Historically, value-oriented stocks have outperformed the broader market more often than not. Over the past four decades, even taking into account recent weakness, the Fund has outperformed value, significantly bettering the excess return of the MSCI World Value Index over the MSCI World Index. Yet, this recent period has been different for a few reasons. First, global economic growth has been persistently low, affording a scarcity premium to companies that have been able to exhibit above-average revenue growth. Second, central bank policy rates have fallen to historical lows. As interest rates declined, so too did equity earnings yields. Because earnings yields are simply the inverse of price-to-earnings ratios, equity valuations tend to expand in falling rate environments, further improving the backdrop for growth stocks.

4 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Other aspects of this environment have been equally challenging. To begin with, this has not been a typical monetary loosening cycle. Central banks have not just lowered interest rates, they have acquired vast portfolios of debt securities in an effort to boost lending and stimulate the economy. As a result of such quantitative easing, the balance sheet of the U.S. Fed has quadrupled to nearly US$4.5 trillion, or around 25% of gross domestic product (GDP). Furthermore, the Bank of Japan’s balance sheet has ballooned to 65% of GDP. In Europe, the ECB and the Bank of England embarked on their own quantitative easing programs. The result of all this stimulus has been a wave of what we believe to be indiscriminate support for financial assets in general, and risk assets like equities in particular. Given the extent to which central bank actions have influenced financial markets, investors recently seemed to us more intently focused on analyzing economic and policy trends than on distinguishing fundamental values at the individual security level. This scenario has led to high degrees of correlation between individual equities, which have put at a disadvantage fundamentally oriented, bottom-up stock-pickers like us. Although such conditions have been frustrating, we nevertheless remain confident in the long-term value of our time-tested investment approach. We believe recent market trends cannot persist indefinitely; it has been our experience that price has eventually converged with value.

This convergence has certainly not yet occurred in the energy sector, a major Fund overweighting and a large detractor during the 12 months under review.2 Global energy stocks tumbled during the period, and the price of oil fell to a six-and-half-year low as modest economic growth raised concerns about energy demand and the Organization of the Petroleum Exporting Countries’ (OPEC’s) decision not to cut production compounded a global supply glut. Half of the Fund’s worst 10 detractors during the period were energy stocks, led by Brazilian oil major Petroleo Brasileiro (Petrobras).3 Petrobras remained a higher risk holding given ongoing uncertainty around legal issues, government interference and strategic execution. However, we believe many of these risks were discounted in the firm’s depressed share price, which seemed to us more reflective of the company’s ancillary problems than its core value proposition as owner of perhaps the world’s most promising long-term production portfolio.

More broadly, despite the near-term supply and demand imbalances currently depressing oil prices, we believed longer term

| | |

| Top 10 Sectors/Industries | | |

| 8/31/15 | | |

| | % of Total | |

| | Net Assets | |

| Banks | 14.1 | % |

| Pharmaceuticals | 11.9 | % |

| Oil, Gas & Consumable Fuels | 9.0 | % |

| Insurance | 5.6 | % |

| Technology Hardware, Storage & Peripherals | 5.0 | % |

| Media | 4.4 | % |

| Diversified Telecommunication Services | 3.4 | % |

| Wireless Telecommunication Services | 3.4 | % |

| Health Care Equipment & Supplies | 3.2 | % |

| Software | 3.2 | % |

conditions remained supportive of higher prices. The reserve life of U.S. shale deposits, a major source of recent supply growth, is a fraction of the life of traditional deposits, meaning shale deposits’ productive capacity should fade relatively quickly. In the meantime, low prices were beginning to have their expected effect as higher cost North American oil production began to decline. In fact, the International Energy Agency recently predicted that non-OPEC production will decrease the most in 20 years in 2016. In short, the shale boom is aging and does not appear to represent a permanent impediment to balanced oil markets. To us, a balanced market is one where price levels encourage the production of the all-important marginal barrel of supply, or the last barrel needed to satisfy demand. At period-end, the marginal cost of production in global oil markets was roughly US$70–US$80, and we believe prices are likely to recover to these levels over our investment horizon.

Stock selection in industrials also detracted from returns, with this cyclical sector subject to many of the same concerns about weak global demand that pressured energy stocks.4 Our stake in U.S. truck manufacturer Navistar International declined after a failed truck engine emissions strategy impaired sales.3 The firm came under new management with a chief executive officer who has been aggressively rebuilding the brand and helping Navistar gain market share in the profitable medium-duty truck segment. A prominent activist investor has also become the firm’s largest shareholder and has been agitating for further restructuring, and we expected continued operational improvements and an eventual share price recovery over our long-term investment horizon.

2. The energy sector comprises energy equipment and services; and oil, gas and consumable fuels in the SOI.

3. Not part of the index.

4. The industrials sector comprises aerospace and defense, air freight and logistics, airlines, commercial services and supplies, construction and engineering, electrical

equipment, industrial conglomerates and machinery in the SOI.

franklintempleton.com

Annual Report

| 5

TEMPLETON GROWTH FUND, INC.

| | |

| Top 10 Holdings | | |

| 8/31/15 | | |

| Company | % of Total | |

| Sector/Industry, Country | Net Assets | |

| Microsoft Corp. | 3.1 | % |

| Software, U.S. | | |

| Samsung Electronics Co. Ltd. | 2.9 | % |

| Technology Hardware, Storage & Peripherals, South Korea | |

| Citigroup Inc. | 2.5 | % |

| Banks, U.S. | | |

| Teva Pharmaceutical Industries Ltd. | 2.5 | % |

| Pharmaceuticals, Israel | | |

| Amgen Inc. | 2.1 | % |

| Biotechnology, U.S. | | |

| CRH PLC, ord. and 144A | 2.0 | % |

| Construction Materials, Ireland | | |

| Pfizer Inc. | 2.0 | % |

| Pharmaceuticals, U.S. | | |

| Comcast Corp. | 2.0 | % |

| Media, U.S. | | |

| Medtronic PLC | 2.0 | % |

| Health Care Equipment & Supplies, U.S. | | |

| Roche Holding AG | 2.0 | % |

| Pharmaceuticals, Switzerland | | |

Other notable sector-level detractors during the period included an underweighted allocation and stock selection in information technology and stock selection in telecommunication services.5 From the information technology sector, South Korean semiconductor and consumer electronics firm Samsung Electronics notably lagged.3 Samsung shares declined amid cyclical weakness in the firm’s memory division, slowing growth in its highly successful smartphone business, and disappointment in the company’s decision not to issue a special dividend this year. We think that Samsung, with a cash hoard equal to one-third of its market capitalization, and trading near all-time lows on a number of meaningful valuation metrics, can weather current weakness and enjoy continued appreciation over our long-term investment horizon. Even after its recent decline, the stock was up roughly 500% from when it was first recommended for our bargain list, and we see continued potential for price appreciation over the long term given our view of Samsung’s modest valuation and impressive market position across a range of lucrative technology products. From the telecommunication services sector, Russian mobile operator Mobile TeleSystems declined due to a weaker ruble and concerns surrounding corporate governance.3 Although the company’s core business

continued to perform well and meet our operational expectations, ancillary issues surrounding an investigation into the firm’s controlling shareholder and currency volatility stemming from economic sanctions largely undermined our fundamental investment thesis, and we exited the position during the year in review.

Despite the aforementioned challenges for value investors, the year in review did bring some encouraging results. Stock selection in the materials sector aided relative performance.6 Irish cement manufacturer CRH rose to an eight-year high as firmer demand in key markets like the U.S. and Europe improved the firm’s earnings outlook. We believed restructuring and cost-saving initiatives have been well executed thus far, and CRH also stood to potentially benefit from an acquisition of assets divested as a regulatory requirement of a merger between competitors. More broadly within the materials sector, we continued to find only selective values. In general, construction materials firms were highly sensitive to wider economic trends, and valuations began to reflect expected earnings improvements as major western property markets recovered. Elsewhere, chemical stocks looked generally expensive to us with margins near cyclical peaks and new capacity negatively affecting industry pricing. The mining industry also suffered from significant excess capacity following an unprecedented investment boom in China, and although some stocks were beginning to look attractively valued in our analysis, much depends on China’s economic trajectory as the country’s leadership seeks a more sustainable growth model. We believe a gradual transition away from investment toward consumption (which has been customary as an economy develops) may be manageable for the major miners. However, an abrupt shift to less commodity-intensive growth would likely deepen the industry’s painful adjustment process considering that China, which accounted for just 13% of global GDP, has in recent years been consuming 40%–70% of the world’s industrial metals.

Stock selection in the financials sector and an overweighted allocation in health care also contributed to relative performance as our value theses in both sectors continued to mature.7 We went into the global financial crisis underweighted in banking stocks but soon thereafter began increasing exposure as many stocks traded at what we considered significant discounts to tangible book value, historically an attractive entry

5. The information technology sector comprises communications equipment; electronic equipment, instruments and components; software; and technology hardware,

storage and peripherals in the SOI. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in

the SOI.

6. The materials sector comprises chemicals, construction materials, and metals and mining in the SOI.

7. The financials sector comprises banks, capital markets, consumer finance and insurance in the SOI. The health care sector comprises biotechnology, health care

equipment and supplies, life sciences tools and services, and pharmaceuticals in the SOI.

See www.franklintempletondatasources.com for additional data provider information.

6 | Annual Report franklintempleton.com

TEMPLETON GROWTH FUND, INC.

point for long-term investors. Six years later the industry has largely restructured, recapitalized and refocused on core earnings drivers. Dutch lender ING Groep, one of the Fund’s top contributors during the period, is an excellent example of the progress that has been made at the corporate level in the banking industry. After years of drastic restructuring following a state-sponsored bailout, ING has divested non-core businesses and repaid in full the Dutch government’s crisis-era rescue loan. The firm comfortably passed the ECB’s stress tests earlier this year and once again began to grow its loan book, subsequently generating higher profitability levels and a strong share price rally. In health care, we increased our allocation throughout the 2000s as consensus fears about an impending patent cliff and waning research and development productivity led to valuations we considered attractive. The industry largely survived the patent cliff, and companies implemented successful strategies designed to rein in bloated cost structures and refocus investment on new drug development. We found value across the sector, including in major pharmaceuticals companies like Pfizer (U.S.), innovative biotechnology companies like Amgen (U.S.), growth-oriented devices firms like Medtronic (U.S.), and specialty pharmaceuticals firms like Teva Pharmaceutical Industries (Israel), each of which finished among the Fund’s top 10 contributors during the year in review.

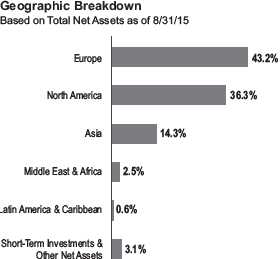

Turning to regions, relative weakness was primarily attributable to an overweighted position and stock selection in Europe as well as stock selection in Asia. In our analysis, European stocks at period-end traded at major discounts to their U.S. peers on most cycle-adjusted valuation metrics. We saw little justification for this discount; given the different stages of economic, earnings and policy cycles, we think European equities should trade at a premium. Corporate earnings have improved significantly since the spring, leading economic indicators have been encouraging, and improving credit conditions were helping to underpin a sustainable recovery. Overall, we believe Europe continued to manage its unique policy and political challenges well, and featured reasonably valued companies with strong operating leverage that were positioned to potentially benefit from an improving growth environment. Asian weakness was primarily attributable to investments in South Korea3 such as in the aforementioned Samsung. South Korean stocks encountered significant headwinds as the period progressed due to a strengthening won (which impinged export profitability), corporate governance concerns at some of the country’s bellwether conglomerates and a flu-like viral outbreak that dampened economic activity. However, in our opinion, valuations in the market remained unusually cheap, particularly for larger capitalization stocks, and we were

| | |

| Top 10 Countries | | |

| 8/31/15 | | |

| | % of Total | |

| | Net Assets | |

| U.S. | 36.2 | % |

| U.K. | 11.0 | % |

| France | 8.7 | % |

| South Korea | 6.2 | % |

| Switzerland | 5.1 | % |

| Germany | 4.6 | % |

| Netherlands | 3.3 | % |

| Japan | 3.3 | % |

| Singapore | 2.7 | % |

| Israel | 2.5 | % |

encouraged by recent government-sponsored corporate reform measures that we think should benefit minority shareholders over the long term. Elsewhere, the Fund’s underweighted allocation and stock selection in the U.S. detracted from relative performance given the country’s continued strong performance. However, the Fund’s allocation to the U.S. remained meaningful. Although we continued to find attractive values at the bottom-up level, the U.S. was still among the world’s most expensive markets and corporate profit margins remained near record levels, making it difficult for us to find sufficient bargains to even approach the global benchmark’s comparatively large U.S. allocation.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the 12 months ended August 31, 2015, the U.S. dollar rose in value relative to most currencies. As a result, the Fund’s performance was negatively affected by the portfolio’s substantial investment in securities with non-U.S. currency exposure.

During challenging times, we often turn for perspective to the words of our firm’s founder, Sir John Templeton. In 1995, he wrote, “In almost every activity of normal life people try to go where the outlook is best. ... You look for a job in an industry with a good future, or build a factory where the prospects are best. But my contention is if you’re selecting publicly traded investments, you have to do the opposite. You’re trying to buy

franklintempleton.com

Annual Report

| 7

TEMPLETON GROWTH FUND, INC.

a share at the lowest possible price in relation to what that corporation is worth. And there’s only one reason a share goes to a bargain price — because other people are selling. There is no other reason. To get a bargain price, you’ve got to look for where the public is most frightened and pessimistic.” As valuations have risen with equity markets since the recovery from the global financial crisis, we have continued to search pockets of fear and pessimism where we believe we can still find long-term value for our clients. Although the market has not favored this style of value investing in recent years, we have maintained our disciplined process and continue to believe it will pay off over the long term. Central banks cannot support global financial markets with extraordinary stimulus indefinitely. Historically, when policymakers have raised interest rates (as we believe the Fed is likely preparing to do), value investing has outperformed. As central banks begin the delicate process of withdrawing stimulus, and global economies find their footing in a market-based (as opposed to policy-driven) system, we believe the ensuing normalization of interest rate and economic conditions will support the process of value recognition at the individual stock level. We believe the Fund is well positioned to take advantage of this eventual normalization and add to its long-term performance.

Thank you for your continued participation in Templeton Growth Fund. We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of August 31, 2015, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

8 | Annual Report franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Performance Summary as of August 31, 2015

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | |

| Net Asset Value | | | | | | |

| Share Class (Symbol) | | 8/31/15 | | 8/31/14 | | Change |

| A (TEPLX) | $ | 22.60 | $ | 26.05 | -$ | 3.45 |

| C (TEGTX) | $ | 21.96 | $ | 25.32 | -$ | 3.36 |

| R (TEGRX) | $ | 22.37 | $ | 25.78 | -$ | 3.41 |

| R6 (FTGFX) | $ | 22.63 | $ | 26.08 | -$ | 3.45 |

| Advisor (TGADX) | $ | 22.66 | $ | 26.13 | -$ | 3.47 |

| |

| |

| Distributions1 (9/1/14–8/31/15) | | | | | | |

| Dividend |

| Share Class | | Income | | | | |

| A | $ | 0.6694 | | | | |

| C | $ | 0.4823 | | | | |

| R | $ | 0.6040 | | | | |

| R6 | $ | 0.7583 | | | | |

| Advisor | $ | 0.7383 | | | | |

franklintempleton.com

Annual Report

| 9

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Performance as of 8/31/15

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum

sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only;

Class R/R6/Advisor Class: no sales charges.

| | | | | | | | | | |

| | | | | | | | Average Annual | | | |

| | Cumulative | | Average Annual | | | Value of $10,000 | Total Return | | Total Annual | |

| Share Class | Total Return2 | | Total Return3 | | | Investment4 | (9/30/15 | )5 | Operating Expenses6 | |

| A | | | | | | | | | 1.03 | % |

| 1-Year | -10.76 | % | -15.89 | % | $ | 8,411 | -17.52 | % | | |

| 5-Year | +63.11 | % | +8.98 | % | $ | 15,375 | +5.78 | % | | |

| 10-Year | +41.76 | % | +2.94 | % | $ | 13,363 | +2.18 | % | | |

| C | | | | | | | | | 1.78 | % |

| 1-Year | -11.44 | % | -12.31 | % | $ | 8,769 | -14.02 | % | | |

| 5-Year | +56.99 | % | +9.44 | % | $ | 15,699 | +6.24 | % | | |

| 10-Year | +31.58 | % | +2.78 | % | $ | 13,158 | +2.03 | % | | |

| R | | | | | | | | | 1.28 | % |

| 1-Year | -10.97 | % | -10.97 | % | $ | 8,903 | -12.72 | % | | |

| 5-Year | +61.02 | % | +10.00 | % | $ | 16,102 | +6.76 | % | | |

| 10-Year | +38.29 | % | +3.30 | % | $ | 13,829 | +2.53 | % | | |

| R6 | | | | | | | | | 0.69 | % |

| 1-Year | -10.41 | % | -10.41 | % | $ | 8,959 | -12.19 | % | | |

| Since Inception (5/1/13) | +11.27 | % | +4.68 | % | $ | 11,127 | +2.21 | % | | |

| Advisor | | | | | | | | | 0.78 | % |

| 1-Year | -10.54 | % | -10.54 | % | $ | 8,946 | -12.25 | % | | |

| 5-Year | +65.16 | % | +10.56 | % | $ | 16,516 | +7.30 | % | | |

| 10-Year | +45.42 | % | +3.82 | % | $ | 14,542 | +3.05 | % | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value

will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown.

For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

10 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Total Return Index Comparison for a Hypothetical $10,000 Investment

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged index includes reinvestment of any income or distributions. It differs from the Fund in composition and does not pay management fees or expenses. One cannot invest directly in an index.

franklintempleton.com Annual Report | 11

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Total Return Index Comparison for a Hypothetical $10,000 Investment (continued)

12 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic

instability and political developments; investments in emerging markets involve heightened risks related to the same factors. In addition, smaller company

stocks have historically experienced more price volatility than larger company stocks, especially over the short term. To the extent the Fund focuses on particu-

lar countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of

focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. The Fund is actively managed but there is no guarantee

that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class C: These shares have higher annual fees and expenses than Class A shares.

Class R: Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares.

Class R6: Shares are available to certain eligible investors as described in the prospectus.

Advisor Class: Shares are available to certain eligible investors as described in the prospectus.

1. The distribution amount is the sum of the dividend payments to shareholders for the period shown and includes only estimated tax-basis net investment income.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated.

4. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

5. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

6. Figures are as stated in the Fund’s current prospectus. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses

to become higher than the figures shown.

7. Source: Morningstar. The MSCI World Index is a free float-adjusted, market capitalization-weighted index designed to measure equity market performance in global

developed markets.

8. Source: Bureau of Labor Statistics, bls.gov/cpi. The Consumer Price Index (CPI) is a commonly used measure of the inflation rate.

See www.franklintempletondatasources.com for additional data provider information.

franklintempleton.com Annual Report | 13

TEMPLETON GROWTH FUND, INC.

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribu- tion and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

14 | Annual Report

franklintempleton.com

| | | | | | |

| | | | | | | TEMPLETON GROWTH FUND, INC. |

| | | | | | | YOUR FUND’S EXPENSES |

| |

| |

| |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Share Class | | Value 3/1/15 | | Value 8/31/15 | | Period* 3/1/15–8/31/15 |

| A | | | | | | |

| Actual | $ | 1,000 | $ | 922.80 | $ | 5.09 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,019.91 | $ | 5.35 |

| C | | | | | | |

| Actual | $ | 1,000 | $ | 919.20 | $ | 8.71 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,016.13 | $ | 9.15 |

| R | | | | | | |

| Actual | $ | 1,000 | $ | 921.70 | $ | 6.30 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,018.65 | $ | 6.61 |

| R6 | | | | | | |

| Actual | $ | 1,000 | $ | 924.80 | $ | 3.35 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.73 | $ | 3.52 |

| Advisor | | | | | | |

| Actual | $ | 1,000 | $ | 924.10 | $ | 3.88 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.17 | $ | 4.08 |

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 1.05%; C: 1.80%; R: 1.30%; R6: 0.69%;

and Advisor: 0.80%), multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period.

franklintempleton.com

Annual Report

| 15

TEMPLETON GROWTH FUND, INC.

| | | | | | | | | | | | | | | |

| Financial Highlights | | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Class A | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 26.05 | | $ | 22.13 | | $ | 18.04 | | $ | 17.05 | | $ | 15.28 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.42 | | | 0.55 | c | | 0.30 | | | 0.35 | | | 0.31 | |

| Net realized and unrealized gains (losses) | | (3.20 | ) | | 3.68 | | | 4.15 | | | 1.01 | | | 1.74 | |

| Total from investment operations | | (2.78 | ) | | 4.23 | | | 4.45 | | | 1.36 | | | 2.05 | |

| Less distributions from net investment income | | (0.67 | ) | | (0.31 | ) | | (0.36 | ) | | (0.37 | ) | | (0.28 | ) |

| Net asset value, end of year | $ | 22.60 | | $ | 26.05 | | $ | 22.13 | | $ | 18.04 | | $ | 17.05 | |

| |

| Total returnd | | (10.76 | )% | | 19.22 | % | | 25.00 | % | | 8.17 | % | | 13.38 | % |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.05 | %e | | 1.03 | % | | 1.07 | %f | | 1.11 | %f | | 1.08 | %f |

| Net investment income | | 1.74 | % | | 2.18 | %c | | 1.47 | % | | 2.03 | % | | 1.71 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 11,506,800 | | $ | 14,138,298 | | $ | 12,970,707 | | $ | 11,582,174 | | $ | 11,865,049 | |

| Portfolio turnover rate | | 18.47 | % | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %g |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.43%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

eBenefit of waiver and payments by affiliates rounds to less than 0.01%.

fBenefit of expense reduction rounds to less than 0.01%.

gExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

16 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

| | | | | | | | | | | | | | | |

| | | | | | TEMPLETON GROWTH FUND, INC. | |

| | | | | | | | | FINANCIAL HIGHLIGHTS | |

| |

| |

| |

| |

| | | | | | Year Ended August 31, | | | | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Class C | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 25.32 | | $ | 21.53 | | $ | 17.56 | | $ | 16.58 | | $ | 14.87 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.23 | | | 0.35 | c | | 0.14 | | | 0.21 | | | 0.17 | |

| Net realized and unrealized gains (losses) | | (3.11 | ) | | 3.58 | | | 4.05 | | | 0.99 | | | 1.69 | |

| Total from investment operations | | (2.88 | ) | | 3.93 | | | 4.19 | | | 1.20 | | | 1.86 | |

| Less distributions from net investment income | | (0.48 | ) | | (0.14 | ) | | (0.22 | ) | | (0.22 | ) | | (0.15 | ) |

| Net asset value, end of year | $ | 21.96 | | $ | 25.32 | | $ | 21.53 | | $ | 17.56 | | $ | 16.58 | |

| |

| Total returnd | | (11.44 | )% | | 18.30 | % | | 24.07 | % | | 7.39 | % | | 12.47 | % |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.80 | %e | | 1.78 | % | | 1.82 | %f | | 1.86 | %f | | 1.83 | %f |

| Net investment income | | 0.99 | % | | 1.43 | %c | | 0.72 | % | | 1.28 | % | | 0.96 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 724,843 | | $ | 900,525 | | $ | 800,312 | | $ | 722,614 | | $ | 810,279 | |

| Portfolio turnover rate | | 18.47 | % | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %g |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 0.68%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

eBenefit of waiver and payments by affiliates rounds to less than 0.01%.

fBenefit of expense reduction rounds to less than 0.01%.

gExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 17

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Class R | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 25.78 | | $ | 21.91 | | $ | 17.86 | | $ | 16.88 | | $ | 15.13 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.36 | | | 0.48 | c | | 0.25 | | | 0.30 | | | 0.26 | |

| Net realized and unrealized gains (losses) | | (3.17 | ) | | 3.64 | | | 4.12 | | | 1.00 | | | 1.73 | |

| Total from investment operations | | (2.81 | ) | | 4.12 | | | 4.37 | | | 1.30 | | | 1.99 | |

| Less distributions from net investment income | | (0.60 | ) | | (0.25 | ) | | (0.32 | ) | | (0.32 | ) | | (0.24 | ) |

| Net asset value, end of year | $ | 22.37 | | $ | 25.78 | | $ | 21.91 | | $ | 17.86 | | $ | 16.88 | |

| |

| Total return | | (10.97 | )% | | 18.88 | % | | 24.72 | % | | 7.87 | % | | 13.08 | % |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.30 | %d | | 1.28 | % | | 1.32 | %e | | 1.36 | %e | | 1.33 | %e |

| Net investment income | | 1.49 | % | | 1.93 | %c | | 1.22 | % | | 1.78 | % | | 1.46 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 119,665 | | $ | 155,334 | | $ | 146,530 | | $ | 136,909 | | $ | 150,841 | |

| Portfolio turnover rate | | 18.47 | % | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %f |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.18%.

dBenefit of waiver and payments by affiliates rounds to less than 0.01%.

eBenefit of expense reduction rounds to less than 0.01%.

fExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

18 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | | | | |

| | | Year Ended August 31, | |

| | | 2015 | | | 2014 | | | 2013 | a |

| Class R6 | | | | | | | | | |

| Per share operating performance | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | |

| Net asset value, beginning of year | $ | 26.08 | | $ | 22.16 | | $ | 21.34 | |

| Income from investment operationsb: | | | | | | | | | |

| Net investment incomec | | 0.51 | | | 0.63 | d | | 0.17 | |

| Net realized and unrealized gains (losses) | | (3.20 | ) | | 3.68 | | | 0.65 | |

| Total from investment operations | | (2.69 | ) | | 4.31 | | | 0.82 | |

| Less distributions from net investment income | | (0.76 | ) | | (0.39 | ) | | — | |

| Net asset value, end of year | $ | 22.63 | | $ | 26.08 | | $ | 22.16 | |

| |

| Total returne | | (10.41 | )% | | 19.60 | % | | 3.84 | % |

| |

| Ratios to average net assetsf | | | | | | | | | |

| Expenses | | 0.70 | %g | | 0.69 | % | | 0.71 | %h |

| Net investment income | | 2.09 | % | | 2.52 | %d | | 1.83 | % |

| |

| Supplemental data | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 1,977,253 | $2,363,855 | $ | 2,042,413 | |

| Portfolio turnover rate | | 18.47 | % | | 17.17 | % | | 12.46 | % |

aFor the period May 1, 2013 (effective date) to August 31, 2013.

bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

cBased on average daily shares outstanding.

dNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.77%.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of waiver and payments by affiliates rounds to less than 0.01%.

hBenefit of expense reduction rounds to less than 0.01%.

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 19

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2015 | | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| Advisor Class | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 26.13 | | $ | 22.15 | | $ | 18.06 | | $ | 17.07 | | $ | 15.30 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.49 | | | 0.59 | c | | 0.31 | | | 0.38 | | | 0.35 | |

| Net realized and unrealized gains (losses) | | (3.22 | ) | | 3.71 | | | 4.19 | | | 1.02 | | | 1.75 | |

| Total from investment operations | | (2.73 | ) | | 4.30 | | | 4.50 | | | 1.40 | | | 2.10 | |

| Less distributions from net investment income | | (0.74 | ) | | (0.32 | ) | | (0.41 | ) | | (0.41 | ) | | (0.33 | ) |

| Net asset value, end of year | $ | 22.66 | | $ | 26.13 | | $ | 22.15 | | $ | 18.06 | | $ | 17.07 | |

| |

| Total return | | (10.54 | )% | | 19.55 | % | | 25.28 | % | | 8.47 | % | | 13.65 | % |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 0.80 | %d | | 0.78 | % | | 0.82 | %e | | 0.86 | %e | | 0.83 | %e |

| Net investment income | | 1.99 | % | | 2.43 | %c | | 1.72 | % | | 2.28 | % | | 1.96 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 396,094 | | $ | 429,080 | | $ | 425,222 | | $ | 2,355,806 | | $ | 2,589,977 | |

| Portfolio turnover rate | | 18.47 | % | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %f |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.68%.

dBenefit of waiver and payments by affiliates rounds to less than 0.01%.

eBenefit of expense reduction rounds to less than 0.01%.

fExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

20 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

| | | | |

| Statement of Investments, August 31, 2015 | | | |

| | Industry | Shares | | Value |

| Common Stocks 96.3% | | | | |

| Canada 0.1% | | | | |

| Suncor Energy Inc. | Oil, Gas & Consumable Fuels | 419,400 | $ | 11,882,176 |

| China 1.4% | | | | |

| China Mobile Ltd. | Wireless Telecommunication Services | 4,859,500 | | 59,912,932 |

| aChina Telecom Corp. Ltd., ADR | Diversified Telecommunication Services | 735,230 | | 38,305,483 |

| Kunlun Energy Co. Ltd. | Oil, Gas & Consumable Fuels | 154,862,700 | | 109,902,562 |

| | | | | 208,120,977 |

| Denmark 0.5% | | | | |

| aFLSmidth & Co. AS | Construction & Engineering | 2,095,190 | | 79,271,674 |

| France 8.7% | | | | |

| AXA SA | Insurance | 8,817,061 | | 222,240,292 |

| BNP Paribas SA | Banks | 3,558,980 | | 224,595,845 |

| Cie Generale des Etablissements Michelin, B | Auto Components | 1,558,399 | | 150,812,863 |

| Credit Agricole SA | Banks | 14,535,330 | | 197,002,077 |

| Sanofi | Pharmaceuticals | 2,157,097 | | 213,299,467 |

| Technip SA | Energy Equipment & Services | 1,228,000 | | 66,876,925 |

| Total SA, B | Oil, Gas & Consumable Fuels | 4,668,754 | | 213,655,279 |

| | | | | 1,288,482,748 |

| Germany 4.6% | | | | |

| bCommerzbank AG | Banks | 922,510 | | 10,337,672 |

| bDeutsche Lufthansa AG | Airlines | 15,394,331 | | 187,408,767 |

| Merck KGaA | Pharmaceuticals | 1,666,254 | | 159,344,370 |

| Metro AG | Food & Staples Retailing | 5,118,650 | | 149,426,924 |

| SAP SE | Software | 193,410 | | 13,012,389 |

| Siemens AG | Industrial Conglomerates | 1,596,669 | | 158,402,154 |

| | | | | 677,932,276 |

| India 0.4% | | | | |

| Hero Motocorp Ltd. | Automobiles | 1,450,303 | | 52,405,446 |

| Ireland 2.0% | | | | |

| CRH PLC | Construction Materials | 9,707,855 | | 290,583,606 |

| cCRH PLC, 144A | Construction Materials | 326,292 | | 9,766,844 |

| | | | | 300,350,450 |

| Israel 2.5% | | | | |

| Teva Pharmaceutical Industries Ltd., ADR | Pharmaceuticals | 5,603,827 | | 360,942,497 |

| Italy 2.0% | | | | |

| Eni SpA | Oil, Gas & Consumable Fuels | 6,671,477 | | 109,462,553 |

| UniCredit SpA | Banks | 29,238,098 | | 191,168,761 |

| | | | | 300,631,314 |

| Japan 3.3% | | | | |

| Konica Minolta Inc. | Technology Hardware, Storage & Peripherals | 11,948,500 | | 131,271,874 |

| Nissan Motor Co. Ltd. | Automobiles | 20,118,600 | | 182,036,491 |

| SoftBank Group Corp. | Wireless Telecommunication Services | 2,847,800 | | 165,902,437 |

| | | | | 479,210,802 |

franklintempleton.com

Annual Report

| 21

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| Netherlands 3.3% | | | | |

| Aegon NV | Insurance | 15,829,990 | $ | 97,394,784 |

| Akzo Nobel NV | Chemicals | 2,137,090 | | 144,619,672 |

| ING Groep NV, IDR | Banks | 10,137,371 | | 155,130,837 |

| bQIAGEN NV | Life Sciences Tools & Services | 3,422,165 | | 90,441,476 |

| | | | | 487,586,769 |

| Portugal 0.9% | | | | |

| Galp Energia SGPS SA, B | Oil, Gas & Consumable Fuels | 13,080,490 | | 137,851,817 |

| Russia 1.0% | | | | |

| Mining and Metallurgical Co. Norilsk Nickel OJSC, | | | | |

| ADR | Metals & Mining | 9,171,571 | | 145,231,827 |

| Singapore 2.7% | | | | |

| DBS Group Holdings Ltd. | Banks | 8,010,734 | | 100,836,796 |

| bFlextronics International Ltd. | Electronic Equipment, Instruments & Components | 11,802,010 | | 124,039,125 |

| Singapore Telecommunications Ltd. | Diversified Telecommunication Services | 63,658,000 | | 168,744,008 |

| | | | | 393,619,929 |

| South Korea 6.2% | | | | |

| Hyundai Motor Co. | Automobiles | 1,688,779 | | 212,782,498 |

| KB Financial Group Inc. | Banks | 4,960,243 | | 150,162,951 |

| POSCO | Metals & Mining | 797,666 | | 128,159,705 |

| Samsung Electronics Co. Ltd. | Technology Hardware, Storage & Peripherals | 458,402 | | 422,134,841 |

| | | | | 913,239,995 |

| Spain 1.4% | | | | |

| Telefonica SA | Diversified Telecommunication Services | 14,874,905 | | 210,028,961 |

| Sweden 1.7% | | | | |

| Ericsson, B | Communications Equipment | 8,281,470 | | 80,788,384 |

| Getinge AB, B | Health Care Equipment & Supplies | 7,932,270 | | 176,417,442 |

| | | | | 257,205,826 |

| Switzerland 5.1% | | | | |

| Credit Suisse Group AG | Capital Markets | 8,803,397 | | 236,305,303 |

| Roche Holding AG | Pharmaceuticals | 1,057,688 | | 288,833,341 |

| Swiss Re AG | Insurance | 2,652,800 | | 227,892,464 |

| | | | | 753,031,108 |

| Thailand 0.3% | | | | |

| Bangkok Bank PCL, fgn. | Banks | 8,099,000 | | 37,193,900 |

| Turkey 1.0% | | | | |

| Turkcell Iletisim Hizmetleri AS, ADR | Wireless Telecommunication Services | 14,409,442 | | 140,636,154 |

| United Kingdom 11.0% | | | | |

| BAE Systems PLC | Aerospace & Defense | 16,720,102 | | 116,024,725 |

| BP PLC | Oil, Gas & Consumable Fuels | 23,130,712 | | 127,960,326 |

| GlaxoSmithKline PLC | Pharmaceuticals | 11,344,568 | | 233,365,069 |

| HSBC Holdings PLC | Banks | 22,977,340 | | 181,743,348 |

| Kingfisher PLC | Specialty Retail | 43,265,874 | | 236,494,184 |

| Royal Dutch Shell PLC, A | Oil, Gas & Consumable Fuels | 82,766 | | 2,152,795 |

| Royal Dutch Shell PLC, B | Oil, Gas & Consumable Fuels | 5,497,253 | | 143,957,099 |

| Serco Group PLC | Commercial Services & Supplies | 42,875,357 | | 74,347,653 |

| Sky PLC | Media | 9,409,666 | | 150,605,068 |

| |

| |

| 22 | Annual Report | | | | franklintempleton.com |

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| United Kingdom (continued) | | | | |

| Standard Chartered PLC | Banks | 6,335,660 | $ | 74,376,265 |

| Tesco PLC | Food & Staples Retailing | 48,771,945 | | 143,212,066 |

| Vodafone Group PLC | Wireless Telecommunication Services | 38,800,571 | | 134,980,398 |

| | | | | 1,619,218,996 |

| United States 36.2% | | | | |

| bAllergan PLC | Pharmaceuticals | 412,179 | | 125,195,249 |

| American International Group Inc. | Insurance | 4,582,520 | | 276,509,257 |

| Amgen Inc. | Biotechnology | 1,993,750 | | 302,611,375 |

| Apache Corp. | Oil, Gas & Consumable Fuels | 3,199,650 | | 144,752,166 |

| Baker Hughes Inc. | Energy Equipment & Services | 2,727,884 | | 152,761,504 |

| Capital One Financial Corp. | Consumer Finance | 1,887,860 | | 146,781,115 |

| aChesapeake Energy Corp. | Oil, Gas & Consumable Fuels | 13,972,030 | | 109,121,554 |

| Chevron Corp. | Oil, Gas & Consumable Fuels | 1,528,510 | | 123,794,025 |

| Cisco Systems Inc. | Communications Equipment | 7,207,250 | | 186,523,630 |

| Citigroup Inc. | Banks | 6,890,580 | | 368,508,218 |

| Comcast Corp., Special A | Media | 5,203,480 | | 297,847,195 |

| CVS Health Corp. | Food & Staples Retailing | 855,670 | | 87,620,608 |

| Eli Lilly & Co. | Pharmaceuticals | 920,330 | | 75,789,176 |

| Gilead Sciences Inc. | Biotechnology | 579,290 | | 60,866,000 |

| bGoogle Inc., A | Internet Software & Services | 225,530 | | 146,102,845 |

| Halliburton Co. | Energy Equipment & Services | 2,711,580 | | 106,700,673 |

| Hewlett-Packard Co. | Technology Hardware, Storage & Peripherals | 6,415,070 | | 180,006,864 |

| JPMorgan Chase & Co. | Banks | 3,542,510 | | 227,074,891 |

| Medtronic PLC | Health Care Equipment & Supplies | 4,059,560 | | 293,465,592 |

| bMichael Kors Holdings Ltd. | Textiles, Apparel & Luxury Goods | 2,969,730 | | 129,064,466 |

| Microsoft Corp. | Software | 10,439,430 | | 454,323,994 |

| Morgan Stanley | Capital Markets | 6,286,700 | | 216,576,815 |

| b,dNavistar International Corp. | Machinery | 5,754,190 | | 102,654,750 |

| bNews Corp., A | Media | 2,728,302 | | 37,186,756 |

| Noble Corp. PLC | Energy Equipment & Services | 4,837,980 | | 62,990,500 |

| Pfizer Inc. | Pharmaceuticals | 9,262,540 | | 298,439,039 |

| SunTrust Banks Inc. | Banks | 4,098,280 | | 165,447,564 |

| Twenty-First Century Fox Inc., A | Media | 5,686,150 | | 155,743,649 |

| United Parcel Service Inc., B | Air Freight & Logistics | 2,154,350 | | 210,372,277 |

| Verizon Communications Inc. | Diversified Telecommunication Services | 1,870,841 | | 86,077,394 |

| | | | | 5,330,909,141 |

| Total Common Stocks | | | | |

| (Cost $12,943,973,655) | | | | 14,184,984,783 |

| Preferred Stocks | | | | |

| (Cost $200,646,430) 0.6% | | | | |

| Brazil 0.6% | | | | |

| bPetroleo Brasileiro SA, ADR, pfd. | Oil, Gas & Consumable Fuels | 17,262,556 | | 87,003,282 |

| Total Investments before Short Term | | | | |

| Investments (Cost $13,144,620,085) | | | | 14,271,988,065 |

franklintempleton.com

Annual Report

| 23

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | |

| | | Principal | | |

| | | Amount* | | Value |

| Short Term Investments 2.2% | | | | |

| Time Deposits 1.8% | | | | |

| United States 1.8% | | | | |

| Bank of Montreal, 0.05%, 9/01/15 | $ | 30,000,000 | $ | 30,000,000 |

| Royal Bank of Canada, 0.05%, 9/01/15 | | 240,200,000 | | 240,200,000 |

| Total Time Deposits | | | | |

| (Cost $270,200,000) | | | | 270,200,000 |

| Total Investments before Money | | | | |

| Market Funds | | | | |

| (Cost $13,414,820,085) | | | | 14,542,188,065 |

| | | Shares | | |

| eInvestments from Cash Collateral | | | | |

| Received for Loaned Securities | | | | |

| (Cost $53,424,958) 0.4% | | | | |

| Money Market Funds 0.4% | | | | |

| United States 0.4% | | | | |

| b,fInstitutional Fiduciary Trust Money Market | | | | |

| Portfolio | | 53,424,958 | | 53,424,958 |

| Total Investments | | | | |

| (Cost $13,468,245,043) 99.1% | | | | 14,595,613,023 |

| Other Assets, less Liabilities 0.9% | | | | 129,041,783 |

| Net Assets 100.0% | | | $ | 14,724,654,806 |

See Abbreviations on page 37.

*The principal amount is stated in U.S. dollars unless otherwise indicated.

aA portion or all of the security is on loan at August 31, 2015. See Note 1(c).

bNon-income producing.

cSecurity was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers

or in a public offering registered under the Securities Act of 1933. This security has been deemed liquid under guidelines approved by the Fund’s Board of Directors. At

August 31, 2015, the value of this security was $9,766,844, representing 0.07% of net assets.

dSee Note 8 regarding holdings of 5% voting securities.

eSee Note 1(c) regarding securities on loan.

fSee Note 3(f) regarding investments in Institutional Fiduciary Trust Money Market Portfolio.

24 | Annual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Financial Statements

Statement of Assets and Liabilities

August 31, 2015

| | | |

| Assets: | | | |

| Investments in securities: | | | |

| Cost - Unaffiliated issuers | $ | 13,235,124,905 | |

| Cost - Non-controlled affiliated issuers (Note 8) | | 179,695,180 | |

| Cost - Sweep Money Fund (Note 3f) | | 53,424,958 | |

| Total cost of investments | $ | 13,468,245,043 | |

| Value - Unaffiliated issuers | $ | 14,439,533,315 | |

| Value - Non-controlled affiliated issuers (Note 8) | | 102,654,750 | |

| Value - Sweep Money Fund (Note 3f) | | 53,424,958 | |

| Total value of investments (includes securities loaned in the amount of $51,548,697) | | 14,595,613,023 | |

| Cash | | 14,475,182 | |

| Foreign currency, at value (cost $5,735,780) | | 5,731,747 | |

| Receivables: | | | |

| Investment securities sold | | 129,446,664 | |

| Capital shares sold | | 6,283,028 | |

| Dividends and interest | | 38,155,410 | |

| Due from custodian | | 145,800 | |

| Other assets | | 15,739,823 | |

| Total assets | | 14,805,590,677 | |

| Liabilities: | | | |

| Payables: | | | |

| Capital shares redeemed | | 11,984,813 | |

| Management fees | | 8,829,582 | |

| Distribution fees | | 3,247,608 | |

| Transfer agent fees | | 2,175,823 | |

| Payable upon return of securities loaned | | 53,570,758 | |

| Accrued expenses and other liabilities | | 1,127,287 | |

| Total liabilities | | 80,935,871 | |

| Net assets, at value | $ | 14,724,654,806 | |

| Net assets consist of: | | | |

| Paid-in capital | $ | 14,618,826,347 | |

| Undistributed net investment income | | 189,371,778 | |

| Net unrealized appreciation (depreciation) | | 1,126,544,848 | |

| Accumulated net realized gain (loss) | | (1,210,088,167 | ) |

| Net assets, at value | $ | 14,724,654,806 | |

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 25

| | |

| TEMPLETON GROWTH FUND, INC. | | |

| FINANCIAL STATEMENTS | | |

| |

| |

| Statement of Assets and Liabilities (continued) | | |

| August 31, 2015 | | |

| |

| Class A: | | |

| Net assets, at value | $ | 11,506,799,608 |

| Shares outstanding | | 509,169,284 |

| Net asset value per sharea | $ | 22.60 |

| Maximum offering price per share (net asset value per share ÷ 94.25%) | $ | 23.98 |

| Class C: | | |

| Net assets, at value | $ | 724,842,950 |

| Shares outstanding | | 33,006,485 |

| Net asset value and maximum offering price per sharea | $ | 21.96 |

| Class R: | | |

| Net assets, at value | $ | 119,665,287 |

| Shares outstanding | | 5,350,149 |

| Net asset value and maximum offering price per share | $ | 22.37 |

| Class R6: | | |

| Net assets, at value | $ | 1,977,252,503 |

| Shares outstanding | | 87,382,446 |

| Net asset value and maximum offering price per share | $ | 22.63 |

| Advisor Class: | | |

| Net assets, at value | $ | 396,094,458 |

| Shares outstanding | | 17,480,928 |

| Net asset value and maximum offering price per share | $ | 22.66 |

aRedemption price is equal to net asset value less contingent deferred sales charges, if applicable.

26 | Annual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON GROWTH FUND, INC.

FINANCIAL STATEMENTS

Statement of Operations

for the year ended August 31, 2015

| | | |

| Investment income: | | | |

| Dividends (net of foreign taxes of $35,383,026) | $ | 436,339,819 | |

| Interest | | 379,933 | |

| Income from securities loaned | | 1,516,497 | |

| Other income (Note 1d) | | 21,230,201 | |

| Total investment income | | 459,466,450 | |

| Expenses: | | | |

| Management fees (Note 3a) | | 111,005,717 | |

| Distribution fees: (Note 3c) | | | |

| Class A | | 32,183,011 | |

| Class C | | 8,196,180 | |

| Class R | | 696,361 | |

| Transfer agent fees: (Note 3e) | | | |

| Class A | | 13,625,892 | |

| Class C | | 867,831 | |

| Class R | | 147,586 | |

| Class R6 | | 1,029 | |

| Advisor Class | | 444,277 | |

| Custodian fees (Note 4) | | 1,188,668 | |

| Reports to shareholders | | 1,068,435 | |

| Registration and filing fees | | 208,391 | |

| Professional fees | | 289,965 | |

| Directors’ fees and expenses | | 283,251 | |

| Other | | 444,545 | |

| Total expenses | | 170,651,139 | |

| Expenses waived/paid by affiliates (Note 3f) | | (69,647 | ) |

| Net expenses | | 170,581,492 | |

| Net investment income | | 288,884,958 | |

| Realized and unrealized gains (losses): | | | |

| Net realized gain (loss) from: | | | |

| Investments | | 432,158,604 | |

| Foreign currency transactions | | 42,778 | |

| Net realized gain (loss) | | 432,201,382 | |

| Net change in unrealized appreciation (depreciation) on: | | | |

| Investments | | (2,560,625,713 | ) |

| Translation of other assets and liabilities denominated in foreign currencies | | (594,945 | ) |

| Net change in unrealized appreciation (depreciation) | | (2,561,220,658 | ) |

| Net realized and unrealized gain (loss) | | (2,129,019,276 | ) |

| Net increase (decrease) in net assets resulting from operations | $ | (1,840,134,318 | ) |

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 27

| | | | | | |

| TEMPLETON GROWTH FUND, INC. | | | | | | |

| FINANCIAL STATEMENTS | | | | | | |

| |

| |

| Statements of Changes in Net Assets | | | | | | |

| |

| |

| | | Year Ended August 31, | |

| | | 2015 | | | 2014 | |

| Increase (decrease) in net assets: | | | | | | |

| Operations: | | | | | | |

| Net investment income | $ | 288,884,958 | | $ | 398,073,637 | |

| Net realized gain (loss) | | 432,201,382 | | | 642,424,552 | |

| Net change in unrealized appreciation (depreciation) | | (2,561,220,658 | ) | | 2,062,090,380 | |

| Net increase (decrease) in net assets resulting from operations | | (1,840,134,318 | ) | | 3,102,588,569 | |

| Distributions to shareholders from: | | | | | | |

| Net investment income: | | | | | | |

| Class A | | (353,064,451 | ) | | (176,426,824 | ) |

| Class C | | (16,734,300 | ) | | (5,057,087 | ) |

| Class R | | (3,533,174 | ) | | (1,589,979 | ) |

| Class R6 | | (68,333,640 | ) | | (34,522,085 | ) |

| Advisor Class | | (12,416,781 | ) | | (5,705,937 | ) |

| Total distributions to shareholders | | (454,082,346 | ) | | (223,301,912 | ) |

| Capital share transactions: (Note 2) | | | | | | |

| Class A | | (832,642,688 | ) | | (1,115,879,967 | ) |

| Class C | | (61,254,169 | ) | | (39,445,476 | ) |

| Class R | | (16,406,989 | ) | | (16,570,744 | ) |

| Class R6 | | (83,826,742 | ) | | (38,783,301 | ) |

| Advisor Class | | 25,909,957 | | | (66,698,023 | ) |

| Total capital share transactions | | (968,220,631 | ) | | (1,277,377,511 | ) |

| Net increase (decrease) in net assets | | (3,262,437,295 | ) | | 1,601,909,146 | |

| Net assets: | | | | | | |

| Beginning of year | | 17,987,092,101 | | | 16,385,182,955 | |

| End of year | $ | 14,724,654,806 | | $ | 17,987,092,101 | |

| Undistributed net investment income included in net assets: | | | | | | |

| End of year | $ | 189,371,778 | | $ | 354,540,069 | |

28 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Notes to Financial Statements

1. Organization and Significant Accounting Policies

Templeton Growth Fund, Inc. (Fund) is registered under the Investment Company Act of 1940 (1940 Act) as an open-end management investment company and applies the specialized accounting and reporting guidance in U.S. Generally Accepted Accounting Principles (U.S. GAAP). The Fund offers five classes of shares: Class A, Class C, Class R, Class R6, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, voting rights on matters affecting a single class, its exchange privilege and fees primarily due to differing arrangements for distribution and transfer agent fees.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. The Fund calculates the net asset value (NAV) per share at the close of the New York Stock Exchange (NYSE), generally at 4 p.m. Eastern time (NYSE close) on each day the NYSE is open for trading. Under compliance policies and procedures approved by the Fund’s Board of Directors (the Board), the Fund’s administrator has responsibility for oversight of valuation, including leading the cross-functional Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.