UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-04892

Templeton Growth Fund, Inc.

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant's telephone number, including area code: (954) 527-7500_

Date of fiscal year end: _8/31__

Date of reporting period: 8/31/14__

Item 1. Reports to Stockholders.

Annual Report and Shareholder Letter

August 31, 2014

Templeton Growth Fund, Inc.

Sign up for electronic delivery at franklintempleton.com/edelivery

Franklin Templeton Investments

Gain From Our Perspective®

At Franklin Templeton Investments, we’re dedicated to one goal: delivering exceptional asset management for our clients. By bringing together multiple, world-class investment teams in a single firm, we’re able to offer specialized expertise across styles and asset classes, all supported by the strength and resources of one of the world’s largest asset managers. This has helped us to become a trusted partner to individual and institutional investors across the globe.

Focus on Investment Excellence

At the core of our firm, you’ll find multiple independent investment teams—each with a focused area of expertise—from traditional to alternative strategies and multi-asset solutions. And because our portfolio groups operate autonomously, their strategies can be combined to deliver true style and asset class diversification.

All of our investment teams share a common commitment to excellence grounded in rigorous, fundamental research and robust, disciplined risk management. Decade after decade, our consistent, research-driven processes have helped Franklin Templeton earn an impressive record of strong, long-term results.

Global Perspective Shaped by Local Expertise

In today’s complex and interconnected world, smart investing demands a global perspective. Franklin Templeton pioneered international investing over 60 years ago, and our expertise in emerging markets spans more than a quarter of a century. Today, our investment professionals are on the ground across the globe, spotting investment ideas and potential risks firsthand. These locally based teams bring in-depth understanding of local companies, economies and cultural nuances, and share their best thinking across our global research network.

Strength and Experience

Franklin Templeton is a global leader in asset management serving clients in over 150 countries.1 We run our business with the same prudence we apply to asset management, staying focused on delivering relevant investment solutions, strong long-term results and reliable, personal service. This approach, focused on putting clients first, has helped us to become one of the most trusted names in financial services.

1. As of 12/31/13. Clients are represented by the total number of shareholder accounts.

Not FDIC Insured | May Lose Value | No Bank Guarantee

| |

| Contents | |

| |

| Shareholder Letter | 1 |

| Annual Report | |

| Templeton Growth Fund, Inc. | 3 |

| Performance Summary | 9 |

| Your Fund’s Expenses | 14 |

| Financial Highlights and | |

| Statement of Investments | 16 |

| Financial Statements | 25 |

| Notes to Financial Statements | 29 |

| Report of Independent Registered | |

| Public Accounting Firm | 38 |

| Tax Information | 39 |

| Board Members and Officers | 40 |

| Shareholder Information | 45 |

Annual Report

Templeton Growth Fund, Inc.

This annual report for Templeton Growth Fund covers the fiscal year ended August 31, 2014.

Your Fund’s Goal and Main Investments

Templeton Growth Fund seeks long-term capital growth. Under normal market conditions, the Fund invests primarily in equity securities of companies located anywhere in the world, including emerging markets.

Performance Overview

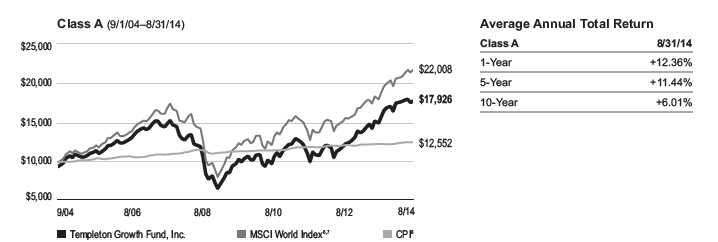

Templeton Growth Fund – Class A delivered a +19.22% cumulative total return for the 12 months under review. In comparison, the MSCI World Index, which measures stock performance in global developed markets, posted a +21.74% total return.1,2 The Fund’s long-term results are shown in the Performance Summary beginning on page 9. For the 10-year period ended August 31, 2014, Templeton Growth Fund –Class A generated a +90.17% cumulative total return, compared with the MSCI World Index’s +120.08% cumulative total return for the same period.1,2 Please note index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find more performance data in the Performance Summary.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

Economic and Market Overview

The global economy grew moderately during the 12 months under review as many developed markets continued to recover and many emerging markets continued to grow. Major developed market central banks reaffirmed their accommodative monetary policies in an effort to support the ongoing recovery. Some emerging market central banks cut interest rates to boost

economic growth, while others raised rates to control inflation and currency depreciation.

U.S. economic growth trends were generally encouraging during the period, despite a contraction in gross domestic product (GDP) in the first quarter of 2014. In January 2014, the U.S. Federal Reserve Board (Fed) began reducing its bond purchases $10 billion a month, based on largely positive economic and employment data in late 2013. Fed comments made in July and August 2014 indicated the central bank was committed to supporting the U.S. recovery, although policymakers were divided on when to raise key interest rates. Fed Chair Janet Yellen took the middle ground about the exact timing, saying rates could rise sooner than expected and at a brisker pace in the case of “faster convergence” toward the Fed’s labor and inflation goals, or rates could remain low if progress toward the Fed’s goals was slower than expected.

Outside the U.S., the U.K. economy grew relatively well, supported by the services and manufacturing sectors. In the second quarter of 2014, GDP registered expansion at pre-crisis levels. Although out of recession, the eurozone experienced deflation-ary risks and lackluster employment trends. Economic growth

1. Source: © 2014 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied

or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising

from any use of this information. As of 8/31/14, the Fund’s Class A 10-year average annual total return not including the maximum sales charge was +6.64%, compared with

the MSCI World Index’s 10-year average annual total return of +8.21%.

2. Source: MSCI.

The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 21.

franklintempleton.com Annual Report | 3

TEMPLETON GROWTH FUND, INC.

remained subdued and weaker than expected as concerns arose about the potential negative impacts to growth from the crisis in Ukraine and tension in the Middle East. In June 2014, the European Central Bank reduced its main interest rate and, for the first time, set a negative deposit rate. After recording strong growth in the first quarter of 2014, Japan’s economy weakened in the second quarter as consumption and investments plunged after a sales tax increase in April. The Bank of Japan (BOJ) kept its accommodative monetary policy unchanged as it maintained an upbeat inflation forecast and reiterated that the economy continued to recover moderately despite challenges resulting from the sales tax increase. In August, the BOJ hinted at rolling out additional stimulus if the economic situation worsened.

In several emerging markets, including China, growth remained solid though moderating as domestic demand and exports were relatively soft. Emerging market equities generally rose for the 12-month period despite volatility resulting from concerns about moderating economic growth, geopolitical tensions in certain regions and the potential impact of the Fed’s tapering its asset purchases. Many emerging market currencies depreciated against the U.S. dollar, leading central banks in several countries, including Brazil, India, Turkey and South Africa, to raise interest rates in an effort to curb inflation and support their currencies.

Stocks in developed markets advanced overall during the period amid a generally accommodative monetary policy environment, continued strength in corporate earnings and signs of an economic recovery. Global government and corporate bonds delivered solid performance as interest rates in many developed market countries remained low. Oil and gold prices were volatile and ended lower for the 12-month period. The U.S. dollar appreciated slightly compared to most currencies.

Investment Strategy

Our investment strategy employs a bottom-up, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. As we look worldwide, we consider specific companies, rather than sectors or countries, while doing in-depth research to construct a bargain list from which we buy. Before we make a purchase, we look at the company’s price/earnings ratio, price/cash flow ratio, profit margins and liquidation value.

Manager’s Discussion

The Fund underperformed the benchmark MSCI World Index during a period when global stocks overcame considerable headwinds to finish at record-high levels. As the 12-month period began, investor attention turned to the imminent tapering of U.S. quantitative easing programs, which led to a stock price correction in emerging markets that had benefited most from cheap U.S. dollar liquidity. A number of escalating geopolitical conflicts also threatened to derail the market rally, including Russia’s annexation of Crimea, renewed hostilities in Gaza and the emergence of a terrorist organization in Syria and Iraq. Other major global events included a sovereign default in Argentina, a military coup in Thailand, intensifying border disputes in the East China Sea and a severe Ebola outbreak in West Africa. Alongside such alarming headlines were more fundamental questions about the resiliency of the global economic recovery. Would Europe strike the right balance of stimulus and austerity to generate sustainable growth momentum? Could China rebalance its economy without popping asset bubbles? Would Abenomics deliver genuine structural reforms in Japan? Could U.S. companies sustain record-high profit margins in a moderate economic growth environment?

In 1958, Sir John Templeton observed, “The influences on stock prices are so numerous and so complex that no person has ever been able to predict the trend of stock prices with consistent success.” This was long before globalization, technology and the 24-hour news cycle overwhelmed investors with a volley of conflicting data points, opinions and analyses. It was also before the scars of the global financial crisis and the consequent pervasiveness of policymakers in the marketplace created a hyperawareness of short-term financial conditions among the general public. To make sense of today’s information overload, we need a framework for thinking about complex variables. At Templeton, this framework is long-term value. Amid the deluge of data points and short-term analyses, we believe long-term opportunities will continue to arise for investors with a disciplined value process and fundamental focus.

A long-term perspective can lead to different conclusions from those reached by the short-term consensus. For example, a longer term outlook could suggest that the recovery from the worst economic crisis of our lifetime was unfolding rather predictably. The U.S., which implemented the greatest amount of monetary stimulus and stabilized first, seemed to be the furthest along the road to recovery, while regions like Europe and

4 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Japan, where increased stimulus and reform came later, were still nursing their economies back to health. Emerging markets, which enjoyed a decade of outperformance buoyed by strong commodity prices, low unit labor costs and a massive influx of developed market liquidity, have lost a number of these supports and now must deal with the consequences. Admittedly, this is a simplistic analysis, and the outlook remains fraught with risk, but it still seems to us a more sensible context to current events than the knee-jerk confusion of the ticker tape. The other part of our framework is value, and the bottom-up valuation analysis that forms the basis of our process is broadly consistent with our assessment of long-term global economic trends. The U.S. market appeared to offer selective value at the stock level but, after staging the strongest rally, recently looked expensive on a headline basis. European stocks had begun to rebound, but ongoing concerns continued to pressure valuation multiples, and we believe significant scope for recovery remained in corporate earnings and economic growth. Emerging markets did not move in lockstep, but overall these markets pulled back from their 2007 all-time price highs, and we believe selective opportunities are arising.

| | |

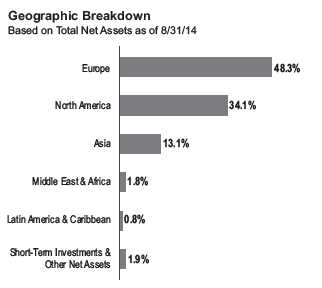

| Top 10 Countries | | |

| Based on Equity Securities | | |

| 8/31/14 | | |

| | % of Total | |

| | Net Assets | |

| U.S. | 32.6 | % |

| U.K. | 11.2 | % |

| France | 10.1 | % |

| Germany | 5.4 | % |

| Netherlands | 4.9 | % |

| South Korea | 4.7 | % |

| Switzerland | 4.5 | % |

| Italy | 2.7 | % |

| Singapore | 2.7 | % |

| Japan | 2.6 | % |

As global industry experts, we would normally begin any portfolio review with a discussion of sector performance. However, the strength of regional trends during the 12-month review period coupled with our contrarian regional weightings resulted in a high influence of geographic allocation on Fund returns. Notably, our long-standing overweighting in Europe relative to the benchmark index had a major impact, initially buoying returns during the first half of the period before significantly pressuring performance as new headwinds buffeted the region.

Although the tail risk of Russian aggression appeared to be materializing as sanctions from the European Union and the U.S. and retaliatory measures from Moscow took their toll on both sides, we nonetheless found continued reasons for optimism in Europe.

Consistent with our investment strategy, our long-term view is rooted in the findings of our bottom-up, fundamental security analysis. As of period-end, European stocks traded near their lowest levels on record relative to their U.S. peers based on cyclically adjusted price-to-earnings ratios (a normalized valuation metric that has historically been predictive of long-term returns). European companies also delivered much lower earnings than their U.S. peers, despite having higher operating leverage and more diversified global revenues, both of which could help amplify an eventual recovery in corporate profits on the continent. From a fiscal/economic standpoint, Europe’s sovereign debt crisis has stabilized, with the at-risk peripheral countries running current account surpluses and realizing mostly positive GDP growth while borrowing at lower rates than the U.S., in some instances. Furthermore, the European Central Bank has relied more on words than actions to boost regional confidence, and therefore can draw on a number of policy measures to promote growth and stability in the euro-zone financial system, if necessary. Still, concerns about deflation, Russian aggression and the recent torpor of regional growth engine Germany persisted and presented significant risks that must be taken into account. These concerns were also what kept valuations so attractive to us, and we believe that investors with a long-term view and open-minded value discipline can still find abundant bargains in the eurozone.

In terms of sectors, we were encouraged by the marked outperformance of our overweighted financials holdings, which included a substantial allocation to deep-value European lenders and insurers.3 For example, three European banks and one insurer finished among the Fund’s top 10 contributors during the review period. French lender Credit Agricole was among the sector’s best-performing stocks and was exemplary of the progress we witnessed in the European banking sector. The firm has done perhaps more than any of its peers to adjust to the post-financial crisis landscape, disposing of non-core operations to bolster capital and enhance focus on its core domestic banking business. Generally, European lenders have simplified their business structures to stabilize returns and increased capital to meet more stringent regulatory requirements. Loan growth has remained subdued in an environment of weak net interest margins, sluggish economic growth, and

3. The financials sector comprises banks, capital markets and insurance in the SOI.

franklintempleton.com

Annual Report

| 5

TEMPLETON GROWTH FUND, INC.

high provisioning for loan losses and regulatory judgments in the aftermath of the financial crisis. Yet, loan officer surveys indicated that lending activity was trending upward, and these adverse conditions could quickly become tailwinds once the credit cycle turns. For now, they mean that investors can buy shares of restructured, recapitalized European lenders at material discounts to tangible book value. Signs also pointed to a renewed focus on shareholder returns, which could improve yield opportunities while we wait for valuations and returns on equity to normalize across the European banking sector.

Another overweighted sector that outperformed during the period was telecommunication services.4 After years of disappointing returns attributable to regulatory headwinds, poor pricing discipline and fierce industry competition, signs of optimism emerged in the sector. A wave of merger and acquisition (M&A) activity during the period gave rise to hopes that profitability (and returns to shareholders) may improve in a more consolidated industry. We were somewhat circumspect about the ultimate impact of this theme and felt that ongoing structural challenges and regulatory unknowns still affected the degree of certainty with which we could forecast sector fundamentals. Although we continued to find some opportunities among select firms with emerging market operations and/or restructuring opportunities, we viewed value in the sector as somewhat limited, and our absolute allocation was modest. We also maintained limited exposure to materials, though here too our holdings outperformed the benchmark’s during the period.5 The Fund’s long-standing underweighting in metals and mining stocks was vindicated in the aftermath of the global financial crisis as the commodities supercycle (the decade-long rise in commodity prices fueled by unsustainable Chinese infrastructure investment) subsided. Poor capital discipline during the boom years left a legacy of overcapacity at a time when demand for industrial commodities flagged, negatively impacting returns across the industry. However, having largely stayed away from these stocks during the boom times (and focused our limited sector investments in building materials and chemicals firms that we believed managed capital and capacity more judiciously), we found isolated opportunities in beaten-down mining stocks, particularly in emerging markets.

Turning to sector laggards, the Fund’s underweighted information technology holdings overall delivered solid absolute returns but underperformed the index and finished as one of the period’s biggest relative detractors.6 At the stock level, South

| | |

| Top 10 Sectors/Industries | | |

| Based on Equity Securities | | |

| 8/31/14 | | |

| | % of Total | |

| | Net Assets | |

| Banks | 13.3 | % |

| Pharmaceuticals | 11.9 | % |

| Oil, Gas & Consumable Fuels | 11.6 | % |

| Insurance | 6.7 | % |

| Diversified Telecommunication Services | 4.4 | % |

| Media | 4.2 | % |

| Wireless Telecommunication Services | 3.1 | % |

| Capital Markets | 2.8 | % |

| Software | 2.7 | % |

| Energy Equipment & Services | 2.6 | % |

Korean semiconductor and consumer electronics manufacturer Samsung Electronics, which is not part of the index, was a major laggard, as it succumbed to concerns about slowing revenue growth and increasing competition in the high-margin smartphone space. Proving our long-term view, Samsung has gained nearly 600% since we added it to the bargain list in 2001. During this time, Samsung consolidated market share in its semiconductor division while expanding its lucrative consumer electronics division to become the world’s largest manufacturer of smartphones and flat-screen televisions. Company management’s stellar track record notwithstanding, concerns about margin sustainability in the company’s most profitable business segments continued to pressure Samsung’s share price. We believe that additional value could be unlocked should the firm continue its legacy of astute capital allocation, and we are closely monitoring the incoming chairman’s strategic plan for Samsung’s prodigious cash hoard. The outperformance of other key technology positions also warrants mention. Shares of Microsoft, the world’s largest software firm and a long-time Fund holding, reached their highest price levels since 2000 as the U.S. company continued its successful growth as a subscription-based provider of cloud services to enterprise customers. A position in the deeply underappreciated U.S. hardware and personal computer (PC) manufacturer Hewlett-Packard also climbed to multi-year price highs as an improving PC cycle, successful new product launches and ongoing cost efficiencies validated the firm’s restructuring efforts.

4. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in the SOI.

5. The materials sector comprises chemicals, construction materials, and metals and mining in the SOI.

6. The information technology sector comprises communications equipment; electronic equipment, instruments and components; semiconductors and semiconductor

equipment; software; and technology hardware, storage and peripherals in the SOI.

6 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Certain overweighted positions in energy and health care also detracted.7 Although our overall allocations to the sectors were favorable, stock-specific issues ultimately led to relative under-performance. One of the biggest laggards was Fugro, a Dutch oilfield surveyor, which declined in value after issuing a profit warning and writing down the value of impaired assets. At recent levels, shares looked oversold to us; we considered the effects of pessimism and the bad news on the stock price mostly short term. As new management improves communication and near-term headwinds abate, we expect sentiment to improve, creating a more favorable exit point. Elsewhere in the oilfield services sector, we continued to find opportunities we felt were attractive among firms with the technology and expertise to help multinational integrated oil companies (oil majors) and state-owned oil companies extract hydrocarbons from increasingly challenging locations. We also found opportunities among the oil majors themselves, which after years of aggressive spending have refocused on shareholder returns as legacy capital expenditures began to translate into production growth. Shares of these companies are among the market’s most attractively valued stocks, in our view, trading near multi-decade lows based on price-to-book values.

Energy investors today would be wise to study the performance of health care stocks over the past decade, which offers a potential roadmap for value recognition. Like the oil majors more recently, the big pharmaceutical companies in the 2000s came under pressure amid concerns about the elevated levels of research and development (R&D) spending required to maintain the pace of new drug development. Anticipated regulatory adversity (such as health care reform) and an industry-wide wave of patent expirations further compounded the challenges facing big pharmaceutical companies, resulting in very cheap valuations. At Templeton, we saw a number of bloated businesses with significant potential to cut costs and reorganize to enhance profitability and productivity. Our long-term outlook allowed us to see beyond the pending patent expirations and think about how earnings might recover over that secular horizon. In the period under review, the process of value recognition continued to unfold, led by a mix of specialty pharmaceutical firms such as Forest Laboratories (U.S.),8 whose share price more than doubled after the firm agreed to be acquired by a larger rival, and traditional pharmaceutical companies such as Merck & Co., whose share price rose to a 13-year high as successful restructuring efforts helped bolster profitability. As value recognition continued to develop among

| | |

| Top 10 Equity Holdings | | |

| 8/31/14 | | |

| Company | % of Total | |

| Sector/Industry, Country | Net Assets | |

| Microsoft Corp. | 2.6 | % |

| Software, U.S. | | |

| Samsung Electronics Co. Ltd. | 2.5 | % |

| Semiconductors & Semiconductor Equipment, South Korea | |

| Citigroup Inc. | 2.0 | % |

| Banks, U.S. | | |

| Comcast Corp., Special A | 1.9 | % |

| Media, U.S. | | |

| Roche Holding AG | 1.9 | % |

| Pharmaceuticals, Switzerland | | |

| Amgen Inc. | 1.8 | % |

| Biotechnology, U.S. | | |

| Teva Pharmaceutical Industries Ltd., ADR | 1.8 | % |

| Pharmaceuticals, Israel | | |

| Hewlett-Packard Co. | 1.8 | % |

| Technology Hardware, Storage & Peripherals, U.S. | | |

| Total SA, B | 1.7 | % |

| Oil, Gas & Consumable Fuels, France | | |

| Pfizer Inc. | 1.7 | % |

| Pharmaceuticals, U.S. | | |

our longer term pharmaceutical holdings, we also found newer opportunities in the biotechnology and medical technology industries. Despite the strong momentum and heavy M&A activity during the review period, we found select companies that were highly profitable and capable of self-funding R&D from the cash flows of currently approved products. In many cases, the market’s short-term focus resulted in the conservative valuation of these base businesses while assigning zero —or in some cases, negative — value to potentially lucrative new product pipelines.

We hope that the preceding discussion helped shed light on our portfolio operations during the review period. We also hope it helped highlight some of the opportunities for long-term value investors in an increasingly short-term, trend-driven market. As Sir John Templeton wrote in 1946, “Experience teaches us that one of the most common errors in selecting stocks for purchase, or for sale, is the tendency to emphasize only the most obvious factor, namely, the temporary outlook for sales and profits of the company.” As the crowd abandons a long-term view and seeks short-term gains, we think greater opportunities should arise for patient investors. Among those investors who have made a long-term commitment to equities, many have put their

7. The energy sector comprises energy equipment and services; and oil, gas and consumable fuels in the SOI. The health care sector comprises biotechnology, health care

equipment and supplies, life sciences tools and services, and pharmaceuticals in the SOI.

8. No longer held by period-end.

franklintempleton.com Annual Report | 7

TEMPLETON GROWTH FUND, INC.

capital in index funds — passive investments that do not reflect a view of corporate fundamentals. Instead, many of these funds are periodically rebalanced toward expensive issues and away from cheaper ones as the prices and market capitalizations of underlying stocks fluctuate. In November 1954, Sir John Templeton founded Templeton Growth Fund. A hypothetical $10,000 investment (after fees and without sales charges) in the Fund’s Class A shares at that time would be worth roughly $12,000,000 on August 31, 2014. A similar hypothetical investment in the “passive” MSCI World Index, the Fund’s benchmark, would be worth roughly $3,500,000.1,9 That investors today are being conditioned to invest passively does not alter the fact that our long-term, active approach to fundamental investing has yielded superior total returns over time. If our goal as investors is to maximize total returns over time, we firmly believe it still pays to think differently from the crowd.

Thank you for your continued participation in Templeton Growth Fund. We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of August 31, 2014, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

9. The inception date of the MSCI World Index is 1/1/70. Prior to that date, for comparative purposes, the index is assumed to have mirrored the Fund’s performance.

8 | Annual Report franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Performance Summary as of August 31, 2014

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | |

| Net Asset Value | | | | | | |

| Share Class (Symbol) | | 8/31/14 | | 8/31/13 | | Change |

| A (TEPLX) | $ | 26.05 | $ | 22.13 | +$ | 3.92 |

| C (TEGTX) | $ | 25.32 | $ | 21.53 | +$ | 3.79 |

| R (TEGRX) | $ | 25.78 | $ | 21.91 | +$ | 3.87 |

| R6 (FTGFX) | $ | 26.08 | $ | 22.16 | +$ | 3.92 |

| Advisor (TGADX) | $ | 26.13 | $ | 22.15 | +$ | 3.98 |

| |

| |

| Distributions (9/1/13–8/31/14) | | | | | | |

| Dividend |

| Share Class | | Income | | | | |

| A | $ | 0.3050 | | | | |

| C | $ | 0.1384 | | | | |

| R | $ | 0.2456 | | | | |

| R6 | $ | 0.3872 | | | | |

| Advisor | $ | 0.3206 | | | | |

franklintempleton.com

Annual Report

| 9

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Performance as of 8/31/14

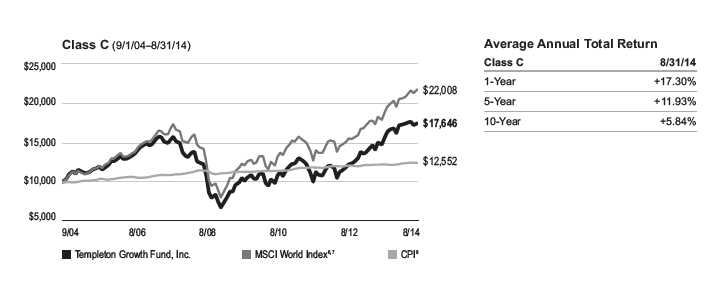

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Class R/R6/Advisor Class: no sales charges.

| | | | | | | | | | | | | |

| | | | | | | | | | | Average Annual | | | |

| | | Cumulative | | | Average Annual | | | Value of $10,000 | | Total Return | | Total Annual | |

| Share Class | | Total Return1 | | | Total Return2 | | | Investment3 | | (9/30/14 | )4 | Operating Expenses5 | |

| A | | | | | | | | | | | | 1.07 | % |

| 1-Year | + | 19.22 | % | + | 12.36 | % | $ | 11,236 | + | 2.79 | % | | |

| 5-Year | + | 82.38 | % | + | 11.44 | % | $ | 17,188 | + | 9.47 | % | | |

| 10-Year | + | 90.17 | % | + | 6.01 | % | $ | 17,926 | + | 5.39 | % | | |

| C | | | | | | | | | | | | 1.82 | % |

| 1-Year | + | 18.30 | % | + | 17.30 | % | $ | 11,730 | + | 7.30 | % | | |

| 5-Year | + | 75.65 | % | + | 11.93 | % | $ | 17,565 | + | 9.95 | % | | |

| 10-Year | + | 76.46 | % | + | 5.84 | % | $ | 17,646 | + | 5.23 | % | | |

| R | | | | | | | | | | | | 1.32 | % |

| 1-Year | + | 18.88 | % | + | 18.88 | % | $ | 11,888 | + | 8.82 | % | | |

| 5-Year | + | 80.06 | % | + | 12.48 | % | $ | 18,006 | + | 10.50 | % | | |

| 10-Year | + | 85.53 | % | + | 6.38 | % | $ | 18,553 | + | 5.76 | % | | |

| R6 | | | | | | | | | | | | 0.71 | % |

| 1-Year | + | 19.60 | % | + | 19.60 | % | $ | 11,960 | + | 9.48 | % | | |

| Since Inception (5/1/13) | + | 24.20 | % | + | 17.63 | % | $ | 12,420 | + | 13.77 | % | | |

| Advisor | | | | | | | | | | | | 0.82 | % |

| 1-Year | + | 19.55 | % | + | 19.55 | % | $ | 11,955 | + | 9.36 | % | | |

| 5-Year | + | 84.75 | % | + | 13.06 | % | $ | 18,475 | + | 11.05 | % | | |

| 10-Year | + | 95.02 | % | + | 6.91 | % | $ | 19,502 | + | 6.28 | % | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

10 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Total Return Index Comparison for a Hypothetical $10,000 Investment

Total return represents the change in value of an investment over the periods shown. It includes any applicable, maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged index includes reinvestment of any income or distributions. It differs from the Fund in composition and does not pay management fees or expenses. One cannot invest directly in an index.

franklintempleton.com Annual Report | 11

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

Total Return Index Comparison for a Hypothetical $10,000 Investment (continued)

12 | Annual Report franklintempleton.com

TEMPLETON GROWTH FUND, INC.

PERFORMANCE SUMMARY

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic

instability and political developments; investments in emerging markets involve heightened risks related to the same factors. In addition, smaller company stocks

have historically experienced more price volatility than larger company stocks, especially over the short term. To the extent the Fund focuses on particular coun-

tries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus

than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. The Fund is actively managed but there is no guarantee that

the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

Class C: These shares have higher annual fees and expenses than Class A shares.

Class R: Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees and expenses than Class A shares.

Class R6: Shares are available to certain eligible investors as described in the prospectus.

Advisor Class: Shares are available to certain eligible investors as described in the prospectus.

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated.

3. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

4. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

5. Figures are as stated in the Fund’s current prospectus. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to

become higher than the figures shown.

6. Source: © 2014 Morningstar. The MSCI World Index is a free float-adjusted, market capitalization-weighted index designed to measure equity market performance in

global developed markets.

7. Source: MSCI.

8. Source: Bureau of Labor Statistics, bls.gov/cpi. The Consumer Price Index (CPI) is a commonly used measure of the inflation rate.

franklintempleton.com Annual Report | 13

TEMPLETON GROWTH FUND, INC.

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribu- tion and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

14 | Annual Report

franklintempleton.com

| | | | | | |

| | | | | | | TEMPLETON GROWTH FUND, INC. |

| | | | | | | YOUR FUND’S EXPENSES |

| |

| |

| |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Share Class | | Value 3/1/14 | | Value 8/31/14 | | Period* 3/1/14–8/31/14 |

| A | | | | | | |

| Actual | $ | 1,000 | $ | 1,018.40 | $ | 5.14 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,020.11 | $ | 5.14 |

| C | | | | | | |

| Actual | $ | 1,000 | $ | 1,014.80 | $ | 8.94 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,016.33 | $ | 8.94 |

| R | | | | | | |

| Actual | $ | 1,000 | $ | 1,017.00 | $ | 6.41 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,018.85 | $ | 6.41 |

| R6 | | | | | | |

| Actual | $ | 1,000 | $ | 1,019.90 | $ | 3.56 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.68 | $ | 3.57 |

| Advisor | | | | | | |

| Actual | $ | 1,000 | $ | 1,019.90 | $ | 3.87 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,021.37 | $ | 3.87 |

*Expenses are calculated using the most recent six-month expense ratio, annualized for each class (A: 1.01%; C: 1.76%; R: 1.26%; R6: 0.70%;

and Advisor: 0.76%), multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period.

franklintempleton.com

Annual Report

| 15

TEMPLETON GROWTH FUND, INC.

| | | | | | | | | | | | | | | |

| Financial Highlights | | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| Class A | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 22.13 | | $ | 18.04 | | $ | 17.05 | | $ | 15.28 | | $ | 15.55 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.55 | c | | 0.30 | | | 0.35 | | | 0.31 | | | 0.24 | |

| Net realized and unrealized gains (losses) | | 3.68 | | | 4.15 | | | 1.01 | | | 1.74 | | | (0.25 | ) |

| Total from investment operations | | 4.23 | | | 4.45 | | | 1.36 | | | 2.05 | | | (0.01 | ) |

| Less distributions from net investment income | | (0.31 | ) | | (0.36 | ) | | (0.37 | ) | | (0.28 | ) | | (0.26 | ) |

| Net asset value, end of year | $ | 26.05 | | $ | 22.13 | | $ | 18.04 | | $ | 17.05 | | $ | 15.28 | |

| |

| Total returnd | | 19.22 | % | | 25.00 | % | | 8.17 | % | | 13.38 | % | | (0.21 | )% |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.03 | % | | 1.07 | %e | | 1.11 | %e | | 1.08 | %e | | 1.10 | %e,f |

| Net investment income | | 2.18 | %c | | 1.47 | % | | 2.03 | % | | 1.71 | % | | 1.50 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 14,138,298 | | $ | 12,970,707 | | $ | 11,582,174 | | $ | 11,865,049 | | $ | 11,954,334 | |

| Portfolio turnover rate | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %g | | 9.21 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.43%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

eBenefit of expense reduction rounds to less than 0.01%.

fBenefit of waiver and payments by affiliates rounds to less than 0.01%.

gExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

16 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

| | | | | | | | | | | | | | | |

| | | | | | TEMPLETON GROWTH FUND, INC. | |

| | | | | | | | | FINANCIAL HIGHLIGHTS | |

| |

| |

| |

| |

| | | | | | Year Ended August 31, | | | | |

| | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| Class C | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 21.53 | | $ | 17.56 | | $ | 16.58 | | $ | 14.87 | | $ | 15.14 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.35 | c | | 0.14 | | | 0.21 | | | 0.17 | | | 0.12 | |

| Net realized and unrealized gains (losses) | | 3.58 | | | 4.05 | | | 0.99 | | | 1.69 | | | (0.25 | ) |

| Total from investment operations | | 3.93 | | | 4.19 | | | 1.20 | | | 1.86 | | | (0.13 | ) |

| Less distributions from net investment income | | (0.14 | ) | | (0.22 | ) | | (0.22 | ) | | (0.15 | ) | | (0.14 | ) |

| Net asset value, end of year | $ | 25.32 | | $ | 21.53 | | $ | 17.56 | | $ | 16.58 | | $ | 14.87 | |

| |

| Total returnd | | 18.30 | % | | 24.07 | % | | 7.39 | % | | 12.47 | % | | (0.91 | )% |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.78 | % | | 1.82 | %e | | 1.86 | %e | | 1.83 | %e | | 1.85 | %e,f |

| Net investment income | | 1.43 | %c | | 0.72 | % | | 1.28 | % | | 0.96 | % | | 0.75 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 900,525 | | $ | 800,312 | | $ | 722,614 | | $ | 810,279 | | $ | 888,857 | |

| Portfolio turnover rate | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %g | | 9.21 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 0.68%.

dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

eBenefit of expense reduction rounds to less than 0.01%.

fBenefit of waiver and payments by affiliates rounds to less than 0.01%.

gExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 17

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| Class R | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 21.91 | | $ | 17.86 | | $ | 16.88 | | $ | 15.13 | | $ | 15.40 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.48 | c | | 0.25 | | | 0.30 | | | 0.26 | | | 0.20 | |

| Net realized and unrealized gains (losses) | | 3.64 | | | 4.12 | | | 1.00 | | | 1.73 | | | (0.25 | ) |

| Total from investment operations | | 4.12 | | | 4.37 | | | 1.30 | | | 1.99 | | | (0.05 | ) |

| Less distributions from net investment income | | (0.25 | ) | | (0.32 | ) | | (0.32 | ) | | (0.24 | ) | | (0.22 | ) |

| Net asset value, end of year | $ | 25.78 | | $ | 21.91 | | $ | 17.86 | | $ | 16.88 | | $ | 15.13 | |

| |

| Total return | | 18.88 | % | | 24.72 | % | | 7.87 | % | | 13.08 | % | | (0.44 | )% |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 1.28 | % | | 1.32 | %d | | 1.36 | %d | | 1.33 | %d | | 1.35 | %d,e |

| Net investment income | | 1.93 | %c | | 1.22 | % | | 1.78 | % | | 1.46 | % | | 1.25 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 155,334 | | $ | 146,530 | | $ | 136,909 | | $ | 150,841 | | $ | 163,865 | |

| Portfolio turnover rate | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %f | | 9.21 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.18%.

dBenefit of expense reduction rounds to less than 0.01%.

eBenefit of waiver and payments by affiliates rounds to less than 0.01%.

fExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

18 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | |

| | | Year Ended August 31, | |

| | | 2014 | | | 2013 | a |

| Class R6 | | | | | | |

| Per share operating performance | | | | | | |

| (for a share outstanding throughout the year) | | | | | | |

| Net asset value, beginning of year | $ | 22.16 | | $ | 21.34 | |

| Income from investment operationsb: | | | | | | |

| Net investment incomec | | 0.63 | d | | 0.17 | |

| Net realized and unrealized gains (losses) | | 3.68 | | | 0.65 | |

| Total from investment operations | | 4.31 | | | 0.82 | |

| Less distributions from net investment income | | (0.39 | ) | | — | |

| Net asset value, end of year | $ | 26.08 | | $ | 22.16 | |

| |

| Total returne | | 19.60 | % | | 3.84 | % |

| |

| Ratios to average net assetsf | | | | | | |

| Expenses | | 0.69 | % | | 0.71 | %g |

| Net investment income | | 2.52 | %d | | 1.83 | % |

| |

| Supplemental data | | | | | | |

| Net assets, end of year (000’s) | $ | 2,363,855 | | $ | 2,042,413 | |

| Portfolio turnover rate | | 17.17 | % | | 12.46 | % |

aFor the period May 1, 2013 (effective date) to August 31, 2013.

bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

cBased on average daily shares outstanding.

dNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.77%.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gBenefit of expense reduction rounds to less than 0.01%.

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 19

TEMPLETON GROWTH FUND, INC.

FINANCIAL HIGHLIGHTS

| | | | | | | | | | | | | | | |

| | | | | | Year Ended August 31, | | | | |

| | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| Advisor Class | | | | | | | | | | | | | | | |

| Per share operating performance | | | | | | | | | | | | | | | |

| (for a share outstanding throughout the year) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | $ | 22.15 | | $ | 18.06 | | $ | 17.07 | | $ | 15.30 | | $ | 15.56 | |

| Income from investment operationsa: | | | | | | | | | | | | | | | |

| Net investment incomeb | | 0.59 | c | | 0.31 | | | 0.38 | | | 0.35 | | | 0.28 | |

| Net realized and unrealized gains (losses) | | 3.71 | | | 4.19 | | | 1.02 | | | 1.75 | | | (0.25 | ) |

| Total from investment operations | | 4.30 | | | 4.50 | | | 1.40 | | | 2.10 | | | 0.03 | |

| Less distributions from net investment income | | (0.32 | ) | | (0.41 | ) | | (0.41 | ) | | (0.33 | ) | | (0.29 | ) |

| Net asset value, end of year | $ | 26.13 | | $ | 22.15 | | $ | 18.06 | | $ | 17.07 | | $ | 15.30 | |

| |

| Total return | | 19.55 | % | | 25.28 | % | | 8.47 | % | | 13.65 | % | | 0.07 | % |

| |

| Ratios to average net assets | | | | | | | | | | | | | | | |

| Expenses | | 0.78 | % | | 0.82 | %d | | 0.86 | %d | | 0.83 | %d | | 0.85 | %d,e |

| Net investment income | | 2.43 | %c | | 1.72 | % | | 2.28 | % | | 1.96 | % | | 1.75 | % |

| |

| Supplemental data | | | | | | | | | | | | | | | |

| Net assets, end of year (000’s) | $ | 429,080 | | $ | 425,222 | | $ | 2,355,806 | | $ | 2,589,977 | | $ | 2,851,417 | |

| Portfolio turnover rate | | 17.17 | % | | 12.46 | % | | 13.47 | % | | 21.60 | %f | | 9.21 | % |

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and

repurchases of the Fund shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.19 per share received in the form of special dividend paid in connection with certain Fund’s holdings.

Excluding these amounts, the ratio of net investment income to average net assets would have been 1.68%.

dBenefit of expense reduction rounds to less than 0.01%.

eBenefit of waiver and payments by affiliates rounds to less than 0.01%.

fExcludes the value of portfolio securities delivered as a result of a redemption in-kind.

20 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

| | | | |

| Statement of Investments, August 31, 2014 | | | |

| | Industry | Shares | | Value |

| Common Stocks 97.3% | | | | |

| Canada 1.5% | | | | |

| Talisman Energy Inc. | Oil, Gas & Consumable Fuels | 26,368,000 | $ | 265,062,301 |

| China 2.2% | | | | |

| China Mobile Ltd. | Wireless Telecommunication Services | 4,859,500 | | 60,351,465 |

| China Shenhua Energy Co. Ltd., H | Oil, Gas & Consumable Fuels | 45,284,500 | | 130,885,968 |

| China Telecom Corp. Ltd., ADR | Diversified Telecommunication Services | 735,230 | | 45,223,997 |

| aDongfang Electric Corp. Ltd., H | Electrical Equipment | 16,395,140 | | 27,374,419 |

| Kunlun Energy Co. Ltd. | Oil, Gas & Consumable Fuels | 80,062,000 | | 131,817,359 |

| | | | | 395,653,208 |

| Denmark 0.6% | | | | |

| aFLSmidth & Co. AS | Construction & Engineering | 2,095,190 | | 111,870,107 |

| France 10.1% | | | | |

| bAlstom SA | Electrical Equipment | 2,493,182 | | 88,230,095 |

| AXA SA | Insurance | 8,817,061 | | 218,363,970 |

| BNP Paribas SA | Banks | 3,558,980 | | 240,251,125 |

| Cie Generale des Etablissements Michelin, B | Auto Components | 2,311,009 | | 255,506,256 |

| Credit Agricole SA | Banks | 14,535,330 | | 215,512,389 |

| Orange SA | Diversified Telecommunication Services | 4,311,032 | | 65,249,848 |

| Sanofi | Pharmaceuticals | 2,691,517 | | 295,276,840 |

| Total SA, B | Oil, Gas & Consumable Fuels | 4,668,754 | | 307,867,588 |

| bVivendi SA | Diversified Telecommunication Services | 5,281,272 | | 137,353,529 |

| | | | | 1,823,611,640 |

| Germany 5.4% | | | | |

| bCommerzbank AG | Banks | 4,854,510 | | 73,475,688 |

| Deutsche Lufthansa AG | Airlines | 15,394,331 | | 266,475,463 |

| Merck KGaA | Pharmaceuticals | 1,987,384 | | 172,934,772 |

| bMetro AG | Food & Staples Retailing | 3,040,145 | | 106,767,491 |

| Muenchener Rueckversicherungs- | | | | |

| Gesellschaft AG | Insurance | 706,419 | | 141,632,424 |

| SAP SE | Software | 193,410 | | 15,043,414 |

| Siemens AG | Industrial Conglomerates | 1,596,669 | | 200,002,684 |

| | | | | 976,331,936 |

| India 0.6% | | | | |

| ICICI Bank Ltd., ADR | Banks | 2,184,200 | | 116,854,700 |

| Ireland 1.4% | | | | |

| CRH PLC | Construction Materials | 10,952,328 | | 252,971,208 |

| Israel 1.8% | | | | |

| Teva Pharmaceutical Industries Ltd., ADR | Pharmaceuticals | 6,159,610 | | 323,502,717 |

| Italy 2.7% | | | | |

| Eni SpA | Oil, Gas & Consumable Fuels | 6,671,477 | | 166,365,773 |

| bSaipem SpA | Energy Equipment & Services | 3,732,900 | | 88,574,740 |

| UniCredit SpA | Banks | 29,238,098 | | 226,261,256 |

| | | | | 481,201,769 |

| Japan 2.6% | | | | |

| Konica Minolta Inc. | Technology Hardware, Storage & Peripherals | 11,948,500 | | 131,249,200 |

| Nissan Motor Co. Ltd. | Automobiles | 20,118,600 | | 193,152,481 |

| Toyota Motor Corp. | Automobiles | 2,602,310 | | 148,253,267 |

| | | | | 472,654,948 |

| |

| |

| franklintempleton.com | | Annual Report | 21 |

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| Netherlands 4.9% | | | | |

| Akzo Nobel NV | Chemicals | 2,972,140 | $ | 210,047,051 |

| Fugro NV, IDR | Energy Equipment & Services | 2,787,285 | | 101,091,563 |

| bING Groep NV, IDR | Banks | 13,344,341 | | 183,477,218 |

| Koninklijke Philips NV | Industrial Conglomerates | 3,402,481 | | 103,667,408 |

| b,cNN Group NV, 144A | Insurance | 2,476,200 | | 72,338,356 |

| bQIAGEN NV | Life Sciences Tools & Services | 3,422,165 | | 82,865,177 |

| Randstad Holding NV | Professional Services | 1,341,726 | | 65,127,632 |

| TNT Express NV | Air Freight & Logistics | 5,279,489 | | 39,454,565 |

| cTNT Express NV, 144A | Air Freight & Logistics | 3,825,802 | | 28,590,902 |

| | | | | 886,659,872 |

| Portugal 1.3% | | | | |

| Galp Energia SGPS SA, B | Oil, Gas & Consumable Fuels | 12,900,340 | | 228,813,006 |

| Russia 2.3% | | | | |

| LUKOIL Holdings, ADR (London Stock | | | | |

| Exchange) | Oil, Gas & Consumable Fuels | 1,740,790 | | 97,049,043 |

| Mining and Metallurgical Co. Norilsk Nickel OJSC, | | | | |

| ADR | Metals & Mining | 9,487,292 | | 185,666,304 |

| Mobile TeleSystems, ADR | Wireless Telecommunication Services | 7,206,502 | | 132,959,962 |

| | | | | 415,675,309 |

| Singapore 2.7% | | | | |

| DBS Group Holdings Ltd. | Banks | 8,010,734 | | 114,929,229 |

| bFlextronics International Ltd. | Electronic Equipment, Instruments & Components | 11,802,010 | | 130,294,190 |

| Singapore Telecommunications Ltd. | Diversified Telecommunication Services | 74,861,000 | | 233,144,622 |

| | | | | 478,368,041 |

| South Korea 4.7% | | | | |

| KB Financial Group Inc. | Banks | 4,960,243 | | 203,232,518 |

| POSCO | Metals & Mining | 575,778 | | 189,635,985 |

| Samsung Electronics Co. Ltd. | Semiconductors & Semiconductor Equipment | 364,460 | | 443,490,425 |

| | | | | 836,358,928 |

| Spain 1.2% | | | | |

| Telefonica SA | Diversified Telecommunication Services | 13,999,911 | | 222,012,960 |

| Sweden 1.5% | | | | |

| Ericsson, B | Communications Equipment | 9,646,500 | | 120,261,278 |

| Getinge AB, B | Health Care Equipment & Supplies | 6,060,820 | | 158,401,243 |

| | | | | 278,662,521 |

| Switzerland 4.5% | | | | |

| Credit Suisse Group AG | Capital Markets | 8,543,380 | | 240,800,124 |

| Roche Holding AG | Pharmaceuticals | 1,174,578 | | 342,446,668 |

| Swiss Re AG | Insurance | 2,652,800 | | 217,407,101 |

| | | | | 800,653,893 |

| Thailand 0.3% | | | | |

| Bangkok Bank PCL, fgn. | Banks | 8,099,000 | | 51,957,284 |

| Turkey 1.2% | | | | |

| bTurkcell Iletisim Hizmetleri AS, ADR | Wireless Telecommunication Services | 14,355,442 | | 211,886,324 |

22 | Annual Report

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | |

| | Industry | Shares | | Value |

| Common Stocks (continued) | | | | |

| United Kingdom 11.2% | | | | |

| Aviva PLC | Insurance | 30,637,172 | $ | 264,920,772 |

| BAE Systems PLC | Aerospace & Defense | 14,860,062 | | 109,776,108 |

| BP PLC | Oil, Gas & Consumable Fuels | 22,801,450 | | 182,273,547 |

| British Sky Broadcasting Group PLC | Media | 1,765,770 | | 25,599,216 |

| GlaxoSmithKline PLC | Pharmaceuticals | 10,166,128 | | 248,788,307 |

| HSBC Holdings PLC | Banks | 22,977,340 | | 247,857,191 |

| bInternational Consolidated Airlines Group SA | Airlines | 25,665,651 | | 153,861,386 |

| Kingfisher PLC | Specialty Retail | 36,340,979 | | 183,177,036 |

| Royal Dutch Shell PLC, B | Oil, Gas & Consumable Fuels | 5,497,253 | | 232,246,105 |

| Serco Group PLC | Commercial Services & Supplies | 21,201,298 | | 109,222,918 |

| Tesco PLC | Food & Staples Retailing | 30,597,529 | | 116,774,867 |

| Vodafone Group PLC | Wireless Telecommunication Services | 38,800,571 | | 133,141,440 |

| | | | | 2,007,638,893 |

| United States 32.6% | | | | |

| bActavis PLC | Pharmaceuticals | 681,039 | | 154,582,232 |

| American International Group Inc. | Insurance | 5,094,260 | | 285,584,216 |

| Amgen Inc. | Biotechnology | 2,343,210 | | 326,596,610 |

| Baker Hughes Inc. | Energy Equipment & Services | 1,300,364 | | 89,907,167 |

| Best Buy Co. Inc. | Specialty Retail | 3,151,560 | | 100,503,248 |

| Chevron Corp. | Oil, Gas & Consumable Fuels | 1,528,510 | | 197,865,620 |

| Cisco Systems Inc. | Communications Equipment | 9,535,010 | | 238,279,900 |

| Citigroup Inc. | Banks | 6,890,580 | | 355,898,457 |

| Comcast Corp., Special A | Media | 6,353,820 | | 346,918,572 |

| CVS Caremark Corp. | Food & Staples Retailing | 2,275,920 | | 180,821,844 |

| FedEx Corp. | Air Freight & Logistics | 337,250 | | 49,872,530 |

| Hewlett-Packard Co. | Technology Hardware, Storage & Peripherals | 8,504,900 | | 323,186,200 |

| JPMorgan Chase & Co. | Banks | 3,542,510 | | 210,602,219 |

| Medtronic Inc. | Health Care Equipment & Supplies | 4,272,880 | | 272,823,388 |

| Merck & Co. Inc. | Pharmaceuticals | 5,009,330 | | 301,110,826 |

| Microsoft Corp. | Software | 10,439,430 | | 474,263,305 |

| Morgan Stanley | Capital Markets | 7,599,670 | | 260,744,678 |

| b,dNavistar International Corp. | Machinery | 5,754,190 | | 216,990,505 |

| bNews Corp., A | Media | 2,728,302 | | 48,086,323 |

| Noble Corp. PLC | Energy Equipment & Services | 6,111,990 | | 173,947,235 |

| bParagon Offshore PLC | Energy Equipment & Services | 2,037,330 | | 18,987,916 |

| Pfizer Inc. | Pharmaceuticals | 10,415,680 | | 306,116,835 |

| bSprint Corp. | Wireless Telecommunication Services | 4,088,454 | | 22,936,227 |

| SunTrust Banks Inc. | Banks | 4,098,280 | | 156,062,502 |

| Target Corp. | Multiline Retail | 1,822,100 | | 109,453,547 |

| Twenty-First Century Fox Inc., A | Media | 5,686,150 | | 201,403,433 |

| United Parcel Service Inc., B | Air Freight & Logistics | 2,154,350 | | 209,682,886 |

| Verizon Communications Inc. | Diversified Telecommunication Services | 1,870,841 | | 92,849,839 |

| The Walt Disney Co. | Media | 1,557,546 | | 139,992,234 |

| | | | | 5,866,070,494 |

| Total Common Stocks | | | | |

| (Cost $13,852,673,654) | | | | 17,504,472,059 |

franklintempleton.com

Annual Report

| 23

TEMPLETON GROWTH FUND, INC.

STATEMENT OF INVESTMENTS

| | | | | | |

| | | Industry | Shares | | Value | |

| Preferred Stocks (Cost $110,595,539) 0.8% | | | | | | |

| Brazil 0.8% | | | | | | |

| Petroleo Brasileiro SA, ADR, pfd. | | Oil, Gas & Consumable Fuels | 7,053,860 | $ | 146,790,827 | |

| Total Investments before Short Term | | | | | | |

| Investments (Cost $13,963,269,193) | | | | | 17,651,262,886 | |

| |

| | | | Principal | | | |

| | | | Amount* | | | |

| Short Term Investments 2.4% | | | | | | |

| Time Deposits 1.8% | | | | | | |

| Canada 1.3% | | | | | | |

| Bank of Montreal, 0.05%, 9/02/14 | | | 128,000,000 | | 128,000,000 | |

| Royal Bank of Canada, 0.05%, 9/02/14 | | | 110,000,000 | | 110,000,000 | |

| | | | | | 238,000,000 | |

| United States 0.5% | | | | | | |

| Scotia Capital Markets, 0.03%, 9/02/14 | | | 90,000,000 | | 90,000,000 | |

| Total Time Deposits | | | | | | |

| (Cost $328,000,000) | | | | | 328,000,000 | |

| Total Investments before Money | | | | | | |

| Market Funds | | | | | | |

| (Cost $14,291,269,193) | | | | | 17,979,262,886 | |

| |

| | | | Shares | | | |

| eInvestments from Cash Collateral | | | | | | |

| Received for Loaned Securities | | | | | | |

| (Cost $111,753,017) 0.6% | | | | | | |

| Money Market Funds 0.6% | | | | | | |

| United States 0.6% | | | | | | |

| fBNY Mellon Overnight Government Fund, | | | | | | |

| 0.053% | | | 111,753,017 | | 111,753,017 | |

| Total Investments | | | | | | |

| (Cost $14,403,022,210) 100.5% | | | | | 18,091,015,903 | |

| Other Assets, less Liabilities (0.5)% | | | | | (103,923,802 | ) |

| Net Assets 100.0% | | | | $ | 17,987,092,101 | |

See Abbreviations on page 37.

*The principal amount is stated in U.S. dollars unless otherwise indicated.

aA portion or all of the security is on loan at August 31, 2014. See Note 1(c).

bNon-income producing.

cSecurity was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers

or in a public offering registered under the Securities Act of 1933.These securities have been deemed liquid under guidelines approved by the Fund’s Board of Directors. At

August 31, 2014, the aggregate value of this security was $100,929,258, representing 0.56% of net assets.

dSee Note 8 regarding holdings of 5% voting securities.

eSee Note 1(c) regarding securities on loan.

fThe rate shown is the annualized seven-day yield at period end.

24 | Annual Report | The accompanying notes are an integral part of these financial statements. franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Financial Statements

Statement of Assets and Liabilities

August 31, 2014

| | | |

| Assets: | | | |

| Investments in securities: | | | |

| Cost - Unaffiliated issuers | $ | 14,223,327,030 | |

| Cost - Non-controlled affiliated issuers (Note 8) | | 179,695,180 | |

| Total cost of investments | $ | 14,403,022,210 | |

| Value - Unaffiliated issuers | $ | 17,874,025,398 | |

| Value - Non-controlled affiliated issuers (Note 8) | | 216,990,505 | |

| Total value of investments (includes securities loaned in the amount of $106,341,007) | | 18,091,015,903 | |

| Cash | | 344,632 | |

| Foreign currency, at value (cost $13,709,017) | | 13,709,017 | |

| Receivables: | | | |

| Investment securities sold | | 45,726,790 | |

| Capital shares sold | | 8,118,973 | |

| Dividends and interest | | 36,388,880 | |

| Other assets | | 5,954 | |

| Total assets | | 18,195,310,149 | |

| Liabilities: | | | |

| Payables: | | | |

| Investment securities purchased | | 25,666,016 | |

| Capital shares redeemed | | 53,667,828 | |

| Management fees | | 10,141,213 | |

| Distribution fees | | 3,791,232 | |

| Transfer agent fees | | 1,974,289 | |

| Payable upon return of securities loaned | | 111,753,017 | |

| Accrued expenses and other liabilities | | 1,224,453 | |

| Total liabilities | | 208,218,048 | |

| Net assets, at value | $ | 17,987,092,101 | |

| Net assets consist of: | | | |

| Paid-in capital | $ | 15,587,047,393 | |

| Undistributed net investment income | | 354,540,069 | |

| Net unrealized appreciation (depreciation) | | 3,687,765,506 | |

| Accumulated net realized gain (loss) | | (1,642,260,867 | ) |

| Net assets, at value | $ | 17,987,092,101 | |

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 25

| | |

| TEMPLETON GROWTH FUND, INC. | | |

| FINANCIAL STATEMENTS | | |

| |

| |

| Statement of Assets and Liabilities (continued) | | |

| August 31, 2014 | | |

| |

| Class A: | | |

| Net assets, at value | $ | 14,138,298,387 |

| Shares outstanding | | 542,756,672 |

| Net asset value per sharea | $ | 26.05 |

| Maximum offering price per share (net asset value per share ÷ 94.25%) | $ | 27.64 |

| Class C: | | |

| Net assets, at value | $ | 900,524,879 |

| Shares outstanding | | 35,565,346 |

| Net asset value and maximum offering price per sharea | $ | 25.32 |

| Class R: | | |

| Net assets, at value | $ | 155,333,895 |

| Shares outstanding | | 6,024,843 |

| Net asset value and maximum offering price per share | $ | 25.78 |

| Class R6: | | |

| Net assets, at value | $ | 2,363,854,578 |

| Shares outstanding | | 90,622,206 |

| Net asset value and maximum offering price per share | $ | 26.08 |

| Advisor Class: | | |

| Net assets, at value | $ | 429,080,362 |

| Shares outstanding | | 16,424,059 |

| Net asset value and maximum offering price per share | $ | 26.13 |

| |

| aRedemption price is equal to net asset value less contingent deferred sales charges, if applicable. | |

| 26 | Annual Report | The accompanying notes are an integral part of these financial statements. | franklintempleton.com |

TEMPLETON GROWTH FUND, INC.

FINANCIAL STATEMENTS

Statement of Operations

for the year ended August 31, 2014

| | | |

| Investment income: | | | |

| Dividends (net of foreign taxes of $35,319,810) | $ | 582,676,119 | |

| Interest | | 149,132 | |

| Income from securities loaned | | 534,008 | |

| Total investment income | | 583,359,259 | |

| Expenses: | | | |

| Management fees (Note 3a) | | 109,827,248 | |

| Administrative fees (Note 3b) | | 11,770,195 | |

| Distribution fees: (Note 3c) | | | |

| Class A | | 35,952,946 | |

| Class C | | 8,908,471 | |

| Class R | | 794,556 | |

| Transfer agent fees: (Note 3e) | | | |

| Class A | | 12,480,281 | |

| Class C | | 772,492 | |

| Class R | | 137,924 | |

| Class R6 | | 137 | |

| Advisor Class | | 363,659 | |

| Custodian fees (Note 4) | | 1,460,881 | |

| Reports to shareholders | | 1,612,532 | |

| Registration and filing fees | | 178,109 | |

| Professional fees | | 401,997 | |

| Directors’ fees and expenses | | 277,824 | |

| Other | | 346,370 | |

| Total expenses | | 185,285,622 | |

| Net investment income | | 398,073,637 | |

| Realized and unrealized gains (losses): | | | |

| Net realized gain (loss) from: | | | |

| Investments: | | | |

| Unaffiliated issuers | | 548,945,450 | |

| Controlled affiliated issuers (Note 8) | | 4,339,701 | |

| Non-controlled affiliated issuers (Note 8) | | 89,196,987 | |

| Foreign currency transactions | | (57,586 | ) |

| Net realized gain (loss) | | 642,424,552 | |

| Net change in unrealized appreciation (depreciation) on: | | | |

| Investments | | 2,062,313,423 | |

| Translation of other assets and liabilities denominated in foreign currencies | | (223,043 | ) |

| Net change in unrealized appreciation (depreciation) | | 2,062,090,380 | |

| Net realized and unrealized gain (loss) | | 2,704,514,932 | |

| Net increase (decrease) in net assets resulting from operations | $ | 3,102,588,569 | |

franklintempleton.com

The accompanying notes are an integral part of these financial statements. | Annual Report | 27

| | | | | | |

| TEMPLETON GROWTH FUND, INC. | | | | | | |

| FINANCIAL STATEMENTS | | | | | | |

| |

| |

| Statements of Changes in Net Assets | | | | | | |

| |

| |

| | | Year Ended August 31, | |

| | | 2014 | | | 2013 | |

| Increase (decrease) in net assets: | | | | | | |

| Operations: | | | | | | |

| Net investment income | $ | 398,073,637 | | $ | 235,578,766 | |

| Net realized gain (loss) from investments and foreign currency transactions | | 642,424,552 | | | 466,403,762 | |

| Net change in unrealized appreciation (depreciation) on investments and translation of other | | | | | | |

| assets and liabilities denominated in foreign currencies | | 2,062,090,380 | | | 2,813,829,931 | |

| Net increase (decrease) in net assets resulting from operations | | 3,102,588,569 | | | 3,515,812,459 | |

| Distributions to shareholders from: | | | | | | |

| Net investment income: | | | | | | |

| Class A | | (176,426,824 | ) | | (226,694,764 | ) |

| Class C | | (5,057,087 | ) | | (8,762,781 | ) |

| Class R | | (1,589,979 | ) | | (2,308,178 | ) |

| Class R6 | | (34,522,085 | ) | | — | |

| Advisor Class | | (5,705,937 | ) | | (49,914,616 | ) |

| Total distributions to shareholders | | (223,301,912 | ) | | (287,680,339 | ) |

| Capital share transactions: (Note 2) | | | | | | |

| Class A | | (1,115,879,967 | ) | | (1,150,663,450 | ) |

| Class B | | — | | | (22,692,424 | ) |

| Class C | | (39,445,476 | ) | | (78,078,548 | ) |

| Class R | | (16,570,744 | ) | | (19,582,566 | ) |

| Class R6 | | (38,783,301 | ) | | 1,961,343,561 | |

| Advisor Class | | (66,698,023 | ) | | (2,351,712,636 | ) |

| Total capital share transactions | | (1,277,377,511 | ) | | (1,661,386,063 | ) |

| Net increase (decrease) in net assets | | 1,601,909,146 | | | 1,566,746,057 | |

| Net assets: | | | | | | |

| Beginning of year | | 16,385,182,955 | | | 14,818,436,898 | |

| End of year | $ | 17,987,092,101 | | $ | 16,385,182,955 | |

| Undistributed net investment income included in net assets: | | | | | | |

| End of year | $ | 354,540,069 | | $ | 169,691,105 | |

28 | Annual Report | The accompanying notes are an integral part of these financial statements.

franklintempleton.com

TEMPLETON GROWTH FUND, INC.

Notes to Financial Statements

1. Organization and Significant Accounting Policies

Templeton Growth Fund, Inc. (Fund) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as an open-end management investment company. The Fund offers five classes of shares: Class A, Class C, Class R, Class R6, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, voting rights on matters affecting a single class, its exchange privilege and fees primarily due to differing arrangements for distribution and transfer agent fees.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. The Fund calculates the net asset value (NAV) per share at the close of the New York Stock Exchange (NYSE), generally at 4 p.m. Eastern time (NYSE close) on each day the NYSE is open for trading. Under compliance policies and procedures approved by the Fund’s Board of Directors (the Board), the Fund’s administrator has responsibility for oversight of valuation, including leading the cross-functional Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.