Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: 811-04920 | ||||

| ||||

| WASATCH FUNDS TRUST | ||||

| ||||

(Exact name of registrant as specified in charter)

505 Wakara Way, 3rd Floor

Salt Lake City, UT 84108

| ||||

(Address of principal executive offices)(Zip code)

| (Name and Address of Agent for Service) | Copy to: | |

Samuel S. Stewart, Jr. Wasatch Advisors, Inc. 505 Wakara Way, 3rd Floor Salt Lake City, UT 84108 | Eric F. Fess, Esq. Chapman & Cutler LLP 111 West Monroe Street Chicago, IL 60603 | |

Registrant’s telephone number, including area code: (801) 533-0777

Date of fiscal year end: September 30

Date of reporting period: March 31, 2016

Table of Contents

Item 1: Report to Shareholders.

Table of Contents

2016 SEMI-ANNUAL REPORT

AND QUARTERLY COMMENTARIES

March 31, 2016

2016

WASATCH

FUNDS

EQUITY FUNDS / Wasatch Core Growth Fund • Wasatch Emerging India Fund • Wasatch Emerging Markets Select Fund • Wasatch Emerging Markets Small Cap Fund • Wasatch Frontier Emerging Small Countries Fund • Wasatch Global Opportunities Fund • Wasatch International Growth Fund • Wasatch International Opportunities Fund • Wasatch Large Cap Value Fund • Wasatch Long/Short Fund • Wasatch Micro Cap Fund • Wasatch Micro Cap Value Fund • Wasatch Small Cap Growth Fund • Wasatch Small Cap Value Fund • Wasatch Strategic Income Fund • Wasatch Ultra Growth Fund • Wasatch World Innovators Fund BOND FUNDS / Wasatch-1st Source Income Fund • Wasatch-Hoisington U.S. Treasury Fund •

Table of Contents

Wasatch Funds

Salt Lake City, Utah

www.WasatchFunds.com

800.551.1700

Table of Contents

| TABLEOF CONTENTS | ||

| ||

| ||

| 2 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

Wasatch Emerging Markets Small Cap Fund® Management Discussion | 10 | |||

| 11 | ||||

Wasatch Frontier Emerging Small Countries Fund® Management Discussion | 12 | |||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

Wasatch International Opportunities Fund® Management Discussion | 18 | |||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 28 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

Wasatch-Hoisington U.S. Treasury Fund® Management Discussion | 40 | |||

| 41 | ||||

| 42 | ||||

| 44 | ||||

| 47 | ||||

| 92 | ||||

| 98 | ||||

| 104 | ||||

| 112 | ||||

| 118 | ||||

| 119 | ||||

| 138 | ||||

| 138 | ||||

| 139 | ||||

| 139 | ||||

| 139 | ||||

| 139 | ||||

| 148 | ||||

| 148 |

This material must be accompanied or preceded by a prospectus.

Please read the prospectus carefully before you invest.

Wasatch Funds are distributed by ALPS Distributors, Inc.

1

Table of Contents

| LETTERTO SHAREHOLDERS — 90% PSYCHOLOGICAL, 10% LOGICAL | ||||

|

| |||

|

| |||

Samuel S. Stewart, Jr. PhD, CFA President of | DEAR FELLOW SHAREHOLDERS:

As a portfolio manager, I’m periodically confronted by the market’s bouts of excessive fear and optimism. While company earnings tend to drive stock prices toward fair value over the long term, anything can happen in the short term. This is what Benjamin Graham meant when he characterized the market as a rational “weighing machine” that considers the facts over the long term, but also as a fickle “voting machine” that’s influenced by fads and fleeting popularity in the short term. Such short-term psychological mood swings were exactly what we saw during the first quarter of 2016. At the heart of the current situation is that the U.S. economy has plodded along at a tortoise-like pace since the end of the Global Financial Crisis (GFC) in 2009. But the stock market has mostly run at a hare’s pace, with a pause to rest in the last year. Because central banks around the world haven’t been satisfied with the global economy’s tortoise-like pace, ever since the GFC they have pursued unprecedented monetary policies — including massive bond purchases, low interest rates, zero interest rates and now even negative interest rates! |

Investors have been left to battle their emotions, waffling in their views as to whether the glass is half empty or half full. But for the economy as a whole, the level in the glass really hasn’t changed much. What does change is the tenor of the financial headlines, which can meaningfully influence investor psychology. I believe this is what accounted for the market reversal that began mid-quarter.

ECONOMY

As we consider economies around the world, the big concerns recently have been the slowdown in China and the decline in commodity prices. For years, economists have worried that China’s development has been grossly unbalanced — even as the country’s economy has grown to be the world’s second-largest. Now, with economic growth slowing, China’s government is finding it necessary to work on developing a more balanced economy — one that will rely more on Chinese consumption and less on manufacturing goods to export to the rest of the world.

As the economy shifts, the decline in production of goods exported from China gives economists a new worry — that the flattening use of commodities in Chinese manufacturing will trigger turmoil in countries and industries that are dependent on Chinese demand for petroleum and metals.

But I think China and other emerging markets are simply going through the normal phases of economic development that many other countries, including the United States, experienced in the past. Along with these phases, there may be further adjustments in the Chinese yuan now that it will be pegged to a basket of currencies, rather than just to the U.S. dollar. However, I don’t expect to see a global crisis as the yuan and other emerging-market currencies reach new equilibriums.

Declining prices for commodities — particularly oil — also have some beneficial impacts. Consumers are receiving what is, in effect, a tax cut. So despite the often apocalyptic headlines, the real story of weak energy prices is that the winners vastly outnumber the losers.

In addition to the constructive overall effects of lower commodity prices, there were other favorable economic conditions in the United States that continued during the quarter. These conditions included the spread of information-age businesses and high-tech industries, still positive gross domestic product (GDP) growth, falling unemployment, modest wage increases, and the progress consumers have made in repairing their balance sheets since the GFC.

MARKETS

As I’ve already discussed, the economic story hasn’t changed much in the last several years. And stock markets throughout most developed countries have generally performed remarkably well during this period. The past year was an exception. The majority of indices across countries, sectors and industries were down for the 12 months ended March 31, 2016.

Similarly, the first quarter of 2016 started with powerful declines across most stock markets. But later in the quarter, stocks staged encouraging rebounds as commodity prices firmed, the U.S. Federal Reserve (Fed) backed off its rhetoric regarding future interest-rate increases, and investors regained their optimism.

The large-cap S&P 500® Index rose 1.35% for the quarter. And the Russell 2000® Index of small caps fell only -1.52%, after having been down almost -16%. As for international stocks, the MSCI World Ex-U.S.A. Index declined -1.95% for the quarter — which was much improved from an interim loss of over -12%.

Meanwhile, high-quality bonds moved up nicely. The intermediate-term Barclays Capital U.S. Aggregate Bond Index returned 3.03%. Similarly, the long-term Barclays U.S. 20+ Year Treasury Bond Index gained 8.49% for the quarter.

For stocks, an important concern is the possibility that the declines in the past year and early in the first quarter indicate the type of vulnerability we may see going forward. This concern is heightened because the low-single-digit annual GDP growth over the last several years hasn’t remotely kept pace with stocks, many of which have had annual returns approaching or exceeding double digits. Market observers frequently attribute the high stock prices we have seen to the unorthodox experiments in monetary policy by central banks around the world.

The classic role of central banks is to ensure that adequate liquidity exists in times of panic so the panic doesn’t feed on itself. The first round of quantitative easing during the height of the GFC was a prime example of this classic role. Subsequent easings by the U.S. Fed and other central banks have essentially been experiments in trying to stimulate economies that haven’t been in a state of panic. But the lackluster growth rates of economies around the world suggest that the intended improvement hasn’t been achieved.

2

Table of Contents

| MARCH 31, 2016 (UNAUDITED) | ||

| ||

| ||

So here we are with very modest global economic growth, seemingly excessive gains in stocks over the past several years and potentially flawed monetary policies around the world. Although this may sound like a prescription for flat — or possibly even falling — stock prices, I continue to be the “nervous bull” that I’ve been for quite a few years. In hindsight, I should have been a “raging bull” for most of that time. But while I don’t feel comfortable abandoning my caution now given the challenges described above, I have taken note of several favorable conditions — including the availability of some stocks at fairly reasonable valuations, the recent tightening of credit spreads between high-quality and lower-quality bonds of the same maturity, and the prevalence of stock yields that exceed 30-year Treasury bond yields. This last condition is particularly noteworthy because when you buy a stock, the dividend can rise. But when you buy a Treasury bond, the yield is fixed until maturity.

WASATCH

As discussed, especially in the short term (which may last for several years), investment returns can be influenced by factors that are more psychological than logical. This means that investors who chase the performance of stocks that have done well in the past may be ignoring valuations and may be missing opportunities in areas of the markets where company fundamentals are strong and valuations are more reasonable.

At Wasatch Advisors, we believe one of the best examples of negative psychology creating attractive valuations is the recent situation in emerging markets — where, in stark contrast to developed markets, stock returns have generally been uninspiring over the past five years. We think this has largely been due to fears regarding the economic slowdown in China, negative sentiment surrounding the commodities rout that tainted the entire emerging-market category, and currency movements — namely, strength in the U.S. dollar and weakness in emerging-market currencies.

Our outlook is that these conditions won’t persist. We believe well-chosen emerging-market companies will stand on their own merits and will decouple from the problems in China and the commodities complex. Therefore, we believe the stock prices of these companies have the potential to rise. Moreover, many of the companies in our emerging-market portfolios pay significant dividends. And for U.S. dollar-based investors, we think there’s strong potential for appreciation from currency adjustments.

With sincere thanks for your continued investment and for your trust,

Sam Stewart

Information in this report regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this report. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

CFA® is a trademark owned by CFA Institute.

Wasatch Advisors is the investment advisor to Wasatch Funds.

Someone who is “bullish” or “a bull” is optimistic with regard to the stock market’s prospects.

The financial crisis of 2007-09, also known as the Global Financial Crisis (GFC) and 2008 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance, and is the market value of all final goods and services made within the borders of a country in a year.

A credit spread is the difference in yield between two bonds of similar maturity but different credit quality. For example, if the 10-year Treasury note is trading at a yield of 6% and a 10-year corporate bond is trading at a yield of 8%, the corporate bond is said to offer a spread over the Treasury of two percentage points.

Quantitative easing is a government monetary policy used to increase the money supply by buying government securities or other securities from the market. Quantitative easing increases the money supply by flooding financial institutions with capital in an effort to promote increased lending and liquidity.

Valuation is the process of determining the current worth of an asset or company.

The S&P 500 Index includes 500 of the United States’ largest stocks from a broad variety of industries. The Index is unmanaged, but is a commonly used measure of common stock total-return performance.

The MSCI World Ex-U.S.A. Index captures large and mid cap representation across 22 of 23 developed market countries — excluding the United States. With 1,004 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

The Russell 2000 Index is an unmanaged total-return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 is widely used in the industry to measure the performance of small-company stocks. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell indices. Russell® is a trademark of Russell Investment Group.

The Barclays Capital U.S. Aggregate Bond Index covers the U.S. investment grade fixed rate bond market, including government and corporate securities, agency mortgage pass-through securities, and asset-backed securities.

The Barclays U.S. 20+ Year Treasury Bond Index measures the performance of U.S. Treasury securities that have remaining maturities of 20 or more years.

You cannot invest directly in these or any indices.

3

Table of Contents

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Core Growth Fund is managed by a team of Wasatch portfolio managers led by JB Taylor and Paul Lambert.

JB Taylor Lead Portfolio Manager |

Paul Lambert Portfolio Manager | OVERVIEW

It was a volatile start to the quarter for small-cap stocks. Through the first week of February, the Russell 2000 Index and Russell 2000 Growth Index were down -16% and -19%, respectively. |

For small-cap investors, the January Effect was conspicuously missing. Perhaps it was delayed to February, as both indices posted strong rallies to finish the quarter and erased most of their losses. As for reasons for the pivot in the quarter, market commentators have pointed to the U.S. Federal Reserve backing off its rhetoric of steady interest-rate increases, a reversal in the strong U.S. dollar, and a bottoming of commodity prices. At quarter’s end, the Russell 2000 finished with a modest decline of -1.52% and the Russell 2000 Growth declined -4.68%. The Wasatch Core Growth Fund — Investor Class was down -3.19%.

When parsing the quarter’s results, the strongest theme to emerge was the market’s changing appetite for higher-growth stocks. This was most apparent when looking at the indices by industry. The fastest-growing industries of the economy — technology services, health technology and health services — delivered the worst stock returns during the first quarter of 2016. In 2015, these were a few of the only industries to contribute positively to Index performance. Conversely, stocks from the non-energy materials, utilities, process industries and producer-manufacturing industries, produced the best returns in the quarter after underperforming for all of 2015.

DETAILSOFTHE QUARTER

The Fund finished the quarter ahead of the Russell 2000 Growth but behind the Russell 2000. This is mostly explained by our large underweight in one high-growth industry, biotechnology, offset by our relatively large weight in another high-growth industry, technology services. Being underweight in biotech was positive for relative performance, especially versus the Russell 2000 Growth Index that had over two times our weight in biotechnology stocks.

Our decision to overweight technology-services stocks hurt us disproportionately in the quarter. Information-technology stocks were among our worst detractors in the first quarter. While biotech and technology services comprise companies with entirely different fundamental drivers, it appears technology stocks, and specifically the higher-growth companies within the sector, were thrown into the same basket as biotech stocks as the market appeared to have associated higher growth with higher risk.

The selloff in these higher-growth stocks isn’t surprising in that valuations were fairly expensive entering the quarter.

But it also seems that high-growth stocks have been painted with the same broad brush, irrespective of the underlying fundamentals or business-model differences.

We don’t see reasons to believe the recent rotation out of high-growth stocks will be long lived. To us, the shift appears to have been driven by changes in short-term sentiment, rather than by improving fundamentals for the average company. In contrast to the anemic growth provided by the broader economy, and revenue growth of just 3.7% for the average U.S. small cap company, our companies reported average revenue growth of 14.2% and average earnings growth of 20.9% during the quarter.

As of March 31st, high-growth companies were only about 20% of the Fund. We’re attracted to these companies because they stand out so sharply in a lower-growth economy. It’s in this group that we are currently seeing the most volatility but we are also seeing some of the greatest potential returns going forward.

The average return of the rest of the Fund, which is made up of our more stable, consistent growers was slightly positive for the quarter. Examples are companies that are steady compound growth stories like Waste Connections, Inc. and Copart, Inc. We have owned Waste Connections and Copart for over 12 and 19 years, respectively. Waste Connections grew revenues 1.5% in the quarter and Copart grew revenues 8.5%, but the stocks were up 15% and 7%, respectively, so there is evidence the Fund also benefited from the market’s pivot away from the highest-growth companies.

OUTLOOK

Through the market’s volatility, we remained steadfast in owning what we believe are the highest-quality growth businesses in the small-cap universe. In a macroeconomic environment where growth is scarce, we think outstanding growth will be disproportionately rewarded over the long term. Throughout our history, we have observed that the market occasionally goes through periods where it underestimates the ultimate earnings power of companies with high and sustainable earnings growth. Valuation resets like the one we saw during the quarter in biotechnology and technology create great opportunities for investors focused on the long term. When these high-growth companies are combined with a portfolio of our more stable growth companies, we believe the Core Growth Fund can continue to offer a portfolio that has better growth and quality metrics when compared to the indices, but with similar overall valuations.

Thank you for the opportunity to manage your very important assets.

| Current and future holdings are subject to risk. |

4

Table of Contents

| WASATCH CORE GROWTH FUND (WGROX / WIGRX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

| SIX MONTHS* | 1 YEAR | 5 YEARS | 10 YEARS | |||||||||||||||||

Core Growth (WGROX) — Investor | -0.34% | -6.24% | 10.29% | 6.25% | ||||||||||||||||

Core Growth (WIGRX) — Institutional | -0.28% | -6.17% | 10.36% | 6.28% | ||||||||||||||||

Russell 2000® Index | 2.02% | -9.76% | 7.20% | 5.26% | ||||||||||||||||

Russell 2000® Growth Index | -0.57% | -11.84% | 7.70% | 6.00% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Core Growth Fund are Investor Class: 1.17% / Institutional Class — Gross: 1.13%, Net: 1.05%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 1/31/2012 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 1/31/2012 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

| * | Not annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Cimpress N.V. | 3.4% | |||

| Waste Connections, Inc. | 3.3% | |||

| Spirit Airlines, Inc. | 3.0% | |||

| Allegiant Travel Co. | 2.9% | |||

| ICON plc (Ireland) | 2.8% | |||

| Company | % of Net Assets | |||

| Credit Acceptance Corp. | 2.6% | |||

| Copart, Inc. | 2.5% | |||

| MEDNAX, Inc. | 2.5% | |||

| Cornerstone OnDemand, Inc. | 2.4% | |||

| Ensign Group, Inc. (The) | 2.4% | |||

| ** | As of March 31, 2016, there were 67 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

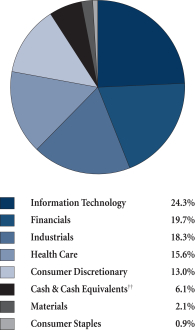

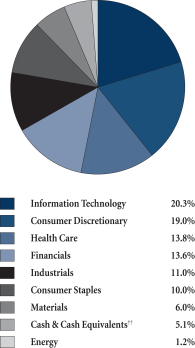

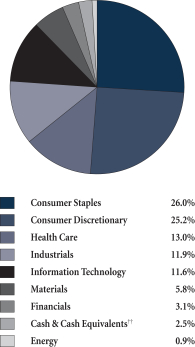

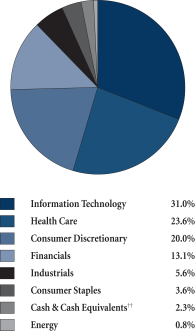

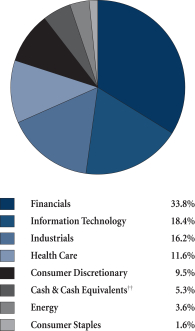

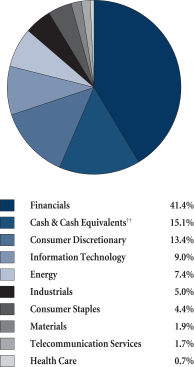

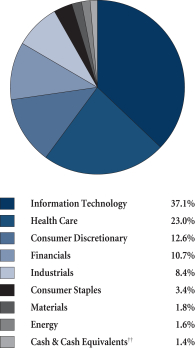

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

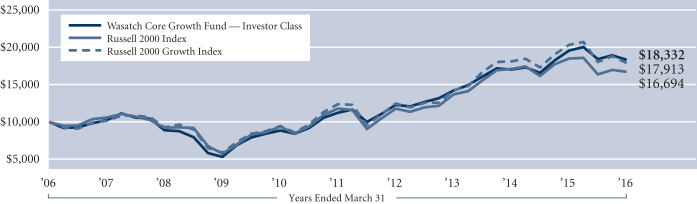

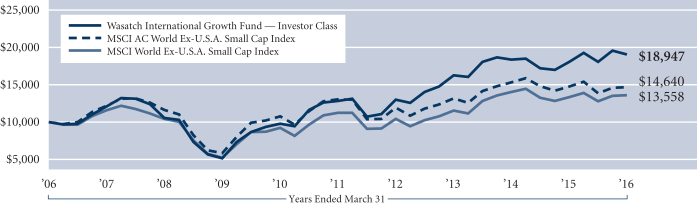

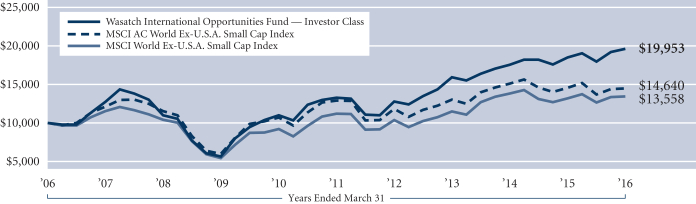

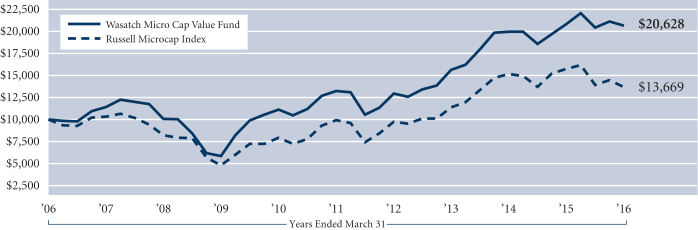

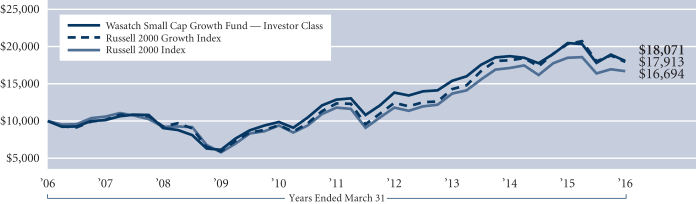

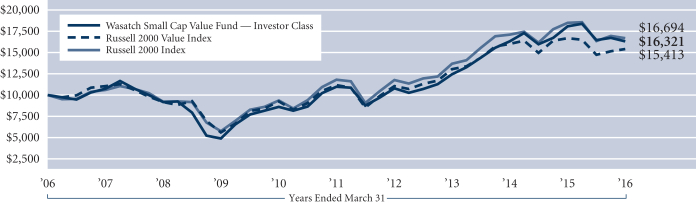

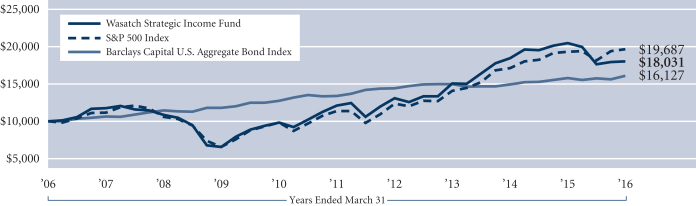

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 Index is widely regarded in the industry as accurately capturing the universe of small company stocks. The Russell 2000 Growth Index is an unmanaged total return index that measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. You cannot invest directly in these or any indices.

5

Table of Contents

| WASATCH EMERGING INDIA FUND (WAINX / WIINX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Emerging India Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan and Matthew Dreith.

Ajay Krishnan, CFA Lead Portfolio Manager |

Matthew Dreith, CFA Associate Portfolio Manager | OVERVIEW

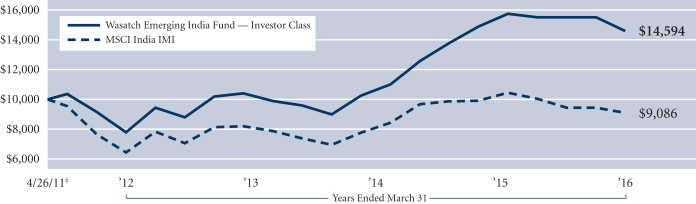

The Wasatch Emerging India Fund — Investor Class declined -5.94% in what was a difficult first quarter for Indian equities. The Fund underperformed its benchmark, the MSCI India |

Investable Market Index, which fell -3.73%.

Indian stocks declined during January and February, as concerns about the global economy and fears of higher U.S. interest rates weighed on emerging markets. Higher interest rates in the U.S. make the dollar more attractive to global investors, while lower rates increase the appeal of emerging-market currencies such as the Indian rupee. Although India’s stock market reversed course in March as the rupee firmed on signs that the U.S. Federal Reserve may hike rates more slowly than previously expected, major Indian averages ended the quarter in the red.

Stocks of large companies led the rebound in equities during the final month of the quarter. Top performers included India’s information-technology (IT) services companies that account for nearly 20% of the benchmark, but only around 5% of the Fund. The Fund’s underexposure to this top-performing industry group was a headwind to performance — as was our lack of investments in the energy sector, which also rose.

Besides IT and energy, the materials sector was the only other sector of the benchmark to finish the quarter with a gain. As improving investor sentiment lifted risk appetite, however, the materials stocks held in the Fund lagged the cyclical, more-speculative issues represented in the Index. Consequently, the materials sector was an additional source of underperformance for the Fund.

Increased scrutiny from U.S. and United Kingdom (U.K.) regulators in India negatively affected the health-care sector, which was the worst-performing sector of the Index and the Fund’s greatest source of underperformance in the first quarter. Likewise, stricter regulations from the Indian government with respect to non-performing loans sent Indian banking shares lower.

Considering the obstacles the Fund had to overcome, we think it performed reasonably well in what proved to be a weak and unusually volatile quarter for Indian stocks.

DETAILSOFTHE QUARTER

Our greatest contributor to Fund performance for the quarter was Dr. Lal PathLabs Ltd. A recent addition the Fund, Dr. Lal Path is one of the largest chains of diagnostic pathology labs in India. The company has been benefiting from its trusted brand reputation and increased demand for

diagnostic testing, which is one of the fastest-growing segments of the Indian health-care market. As it continues to formalize the market by gaining share from unorganized, standalone competitors, we think Dr. Lal Path has the potential to become the dominant consumer brand in diagnostics in India and one of the top health-care service companies in emerging markets.

Bajaj Finance Ltd. is the lending arm of the Bajaj Group, a well-regarded Indian industrial house founded in 1926. Bajaj Finance is a non-bank financial company offering a broad spectrum of lending services, including vehicle loans, mortgage loans, consumer loans and commercial loans. Its greater focus on the consumer enabled the company to avoid much of the first-quarter fallout from tighter regulation of the lending industry that affected stocks of other Indian financials. As a result, Bajaj Finance was the Fund’s second-best contributor to performance for the quarter.

The pharmaceutical industry accounted for our three worst detractors from performance for the quarter: Marksans Pharma Ltd., Natco Pharma Ltd. and Caplin Point Laboratories Ltd., respectively.

Marksans markets its branded prescription and over-the-counter drugs both in India and internationally, with the U.K. accounting for approximately 40% of revenues. The company’s stock price tumbled in January on news that its manufacturing plant in Goa had failed a good manufacturing practice (GMP) inspection by the U.K. Medicines & Healthcare products Regulatory Agency (MHRA). In mid-March, however, Marksans announced that it had received a “Restricted GMP Certificate” that will allow the company to continue manufacturing and selling the majority of its products into U.K. markets until the MHRA’s next inspection. Shares of Natco and Caplin Point also fell as the U.S. Food and Drug Administration stepped up its regulatory activity in India.

OUTLOOK

Although the Fund’s overweight position in health care relative to the benchmark hurt performance in the first quarter, we don’t plan to reduce exposure to this important sector. As a developing economy broadens its focus beyond such mainstays as commodity production and other basic industries, health care becomes one of the next logical areas for growth.

Regulatory scrutiny is not new to the pharmaceutical industry, and exists everywhere in the world that drugs are manufactured for the U.S. and other developed markets. However, the stringency with which minor infractions are enforced tends to be cyclical, and we believe the industry appears to be at or near the peak of regulatory intensity in India.

Longer term, we believe structural trends remain favorable for India’s pharmaceutical industry. In particular, we think Indian companies’ substantial cost advantages are likely to drive further market-share gains as the companies continue to supply low-cost, high-quality medicine to the world.

Thank you for the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

6

Table of Contents

| WASATCH EMERGING INDIA FUND (WAINX / WIINX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

SIX MONTHS* | 1 YEAR | 5 YEARS | SINCE INCEPTION 4/26/11 | |||||||||||||||||

Emerging India (WAINX) — Investor | -5.86% | -7.37% | N/A | 7.96% | ||||||||||||||||

Emerging India (WIINX) — Institutional | -5.86% | -7.37% | N/A | 7.96% | ||||||||||||||||

MSCI India IMI | -3.76% | -13.04% | N/A | -1.92% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging India Fund are Investor Class — Gross: 1.87%, Net: 1.75% / Institutional Class — Gross: 1.75%, Net: 1.50%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets and political and social instability, which are described in more detail in the prospectus.

| * | Not annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Dr. Lal PathLabs Ltd. (India) | 4.0% | |||

| Bajaj Finance Ltd. (India) | 4.0% | |||

| MakeMyTrip Ltd. (India) | 3.4% | |||

| Berger Paints India Ltd. (India) | 2.8% | |||

| Welspun India Ltd. (India) | 2.8% | |||

| Company | % of Net Assets | |||

| Natco Pharma Ltd. (India) | 2.6% | |||

| Glenmark Pharmaceuticals Ltd. (India) | 2.6% | |||

| UPL Ltd. (India) | 2.4% | |||

| Godrej Consumer Products Ltd. (India) | 2.3% | |||

| Somany Ceramics Ltd. (India) | 2.2% | |||

| ** | As of March 31, 2016, there were 64 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

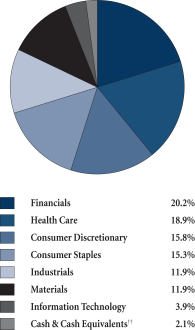

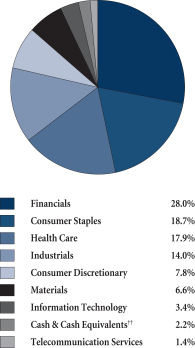

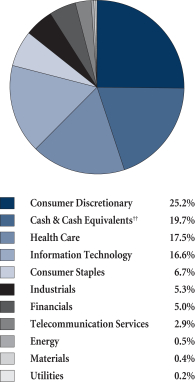

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: April 26, 2011. The MSCI India IMI (Investable Market Index) is designed to measure the performance of the large-, mid- and small-cap segments of the Indian market. The Index covers approximately 99% of the free-float adjusted market capitalization of the Indian equity universe. You cannot invest directly in this or any index.

7

Table of Contents

| WASATCH EMERGING MARKETS SELECT FUND (WAESX / WIESX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Emerging Markets Select Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan, Roger Edgley and Scott Thomas.

Ajay Krishnan, CFA Lead Portfolio Manager |

Roger Edgley, CFA Portfolio Manager |

Scott Thomas, CFA Associate Portfolio |

OVERVIEW

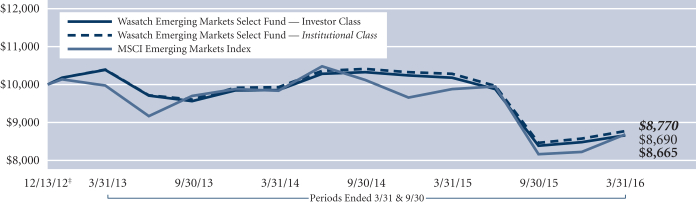

The Wasatch Emerging Markets Select Fund — Investor Class gained 2.13% in what was a positive first quarter for emerging-market equities. The Fund rose less than its benchmark, the MSCI Emerging Markets Index, which increased 5.71%.

After a weak start, investors’ appetite for risk returned during the latter part of the quarter on signs that the U.S. Federal Reserve may raise interest rates more slowly than previously expected. Lower interest rates in the U.S. enhance the appeal of emerging markets by making dollar-denominated investments less attractive to global investors.

As the rebound from early-quarter losses unfolded, investors appeared to seek exposure to the emerging-market asset class itself. Shares of the large companies held in exchange-traded funds and market indices led the advance, while mid-size and smaller companies lagged. Although the Fund invests in companies of all sizes, its holdings of lesser-known and less-widely followed companies generally hurt performance relative to the benchmark.

The energy and materials sectors were the quarter’s biggest gainers within the Index. Energy and materials companies tend to score poorly on our measures of financial quality because the capital-intensive nature of their businesses typically requires substantial amounts of debt. Consequently, in an environment in which energy and materials companies outperformed, our focus on companies with what we consider to be strong balance sheets and sustainable competitive advantages was an additional headwind for the Fund.

Of the significantly weighted countries in the Index, China declined the most, with India posting a somewhat smaller loss. Although our near-zero weighting in China provided a strong tailwind for the Fund, our significantly overweight position in India hurt. Considering the variety of obstacles the Fund had to overcome, we think it performed reasonably well in what was a volatile three months for world equity markets.

DETAILSOFTHE QUARTER

The Fund’s greatest contributor to performance for the quarter was Raia Drogasil S.A., a Brazilian drug-store chain. The company recently completed its acquisition of 4Bio, Brazil’s second-largest specialty pharmacy. It also launched a

proprietary pharmacy-benefits manager focused on capturing demand from corporations and health-care operators to drive volume to its stores.

Universal Robina Corp. was our second-largest contributor. Universal Robina is the leading branded convenience-food and beverage company in the Philippines and a major player throughout Southeast Asia and greater China. Although revenue growth in the company’s most-recently reported quarter was unimpressive, investors cheered as widening margins, better cost controls and a series of one-time items boosted profits.

The health-care sector accounted for the four greatest detractors from Fund performance for the quarter. South Korea-based Medytox, Inc. develops injectable neurotoxins for cosmetic applications and for the treatment of muscular disorders. In what we view as normal fluctuation, the company’s share price declined approximately 10% in apparent sympathy with the Chinese stock market. As the Fund’s largest holding, however, Medytox was its greatest detractor from performance.

Stock prices of Indian pharmaceutical manufacturers fell as the U.S. Food and Drug Administration stepped up its regulatory activity in India and spooked investors. This group included the Fund’s three other large detractors in the health-care sector: Divi’s Laboratories Ltd., Lupin Ltd. and Glenmark Pharmaceuticals Ltd. Although the declines in these holdings caused the Fund’s Indian stocks to underperform as a group, we observed no structural changes in their businesses.

OUTLOOK

While the benchmark largely sidestepped first-quarter weakness in the health-care sector, the Fund felt its full impact. The second-most heavily weighted sector of the Fund, health care traditionally has been the smallest sector of the benchmark. During the first quarter, for example, health-care stocks represented only about 2.8% of the Index on average. Although this difference in weightings hurt performance relative to the Index during the period, we have no plans to reduce our exposure to a sector whose outlook we believe is among the brightest in emerging markets.

The aerospace-and-defense industry is another non-traditional area in which a new class of innovative Korean companies has begun to make inroads — both in the domestic Korean market and throughout the region. With aerospace-and-defense companies currently accounting for less than 1% of the benchmark, we have begun exploring this industry as a potentially rewarding theme for future investment.

Despite recent gains against the dollar, a number of emerging-market currencies remain undervalued in our view. We believe low energy prices are likely to provide an additional boost to emerging economies that are net importers of oil. While we remain cautious toward countries tied to the production of oil and other natural resources, we continue to favor countries such as India, Mexico and the Philippines. Our view toward China also remains cautious on structural concerns.

Thank you for the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

8

Table of Contents

| WASATCH EMERGING MARKETS SELECT FUND (WAESX / WIESX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

| SIX MONTHS* | 1 YEAR | 5 YEARS | SINCE INCEPTION 12/13/12 | |||||||||||||||||

Emerging Markets Select (WAESX) — Investor | 3.47% | -14.89% | N/A | -4.25% | ||||||||||||||||

Emerging Markets Select (WIESX) — Institutional | 3.57% | -14.69% | N/A | -3.90% | ||||||||||||||||

MSCI Emerging Markets Index | 6.41% | -12.03% | N/A | -4.17% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Select Fund are Investor Class — Gross: 1.75%, Net: 1.51% / Institutional Class — Gross: 1.52%, Net: 1.21%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

| * | Not annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Promotora y Operadora de Infraestructura S.A.B. de C.V. (Mexico) | 4.5% | |||

| Gentera S.A.B. de C.V. (Mexico) | 4.5% | |||

| Medytox, Inc. (Korea) | 4.4% | |||

| Grupo Aeroportuario del Pacifico S.A.B. de C.V., Class B (Mexico) | 3.8% | |||

| Bajaj Finance Ltd. (India) | 3.7% | |||

| Company | % of Net Assets | |||

| Grupo Financiero Interacciones S.A. de C.V., Class O (Mexico) | 3.7% | |||

| Bangkok Dusit Medical Services Public Co. Ltd., Class F (Thailand) | 3.6% | |||

| GT Capital Holdings, Inc. (Philippines) | 3.6% | |||

| Universal Robina Corp. (Philippines) | 3.5% | |||

| MercadoLibre, Inc. (Brazil) | 3.4% | |||

| ** | As of March 31, 2016, there were 39 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

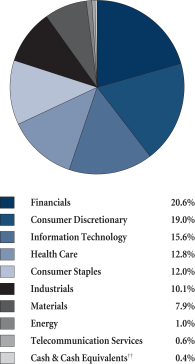

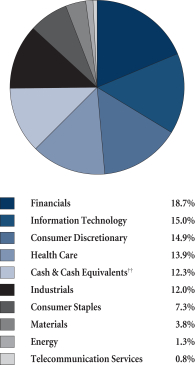

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: December 13, 2012. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure the equity market performance of emerging markets. You cannot invest directly in this or any index.

9

Table of Contents

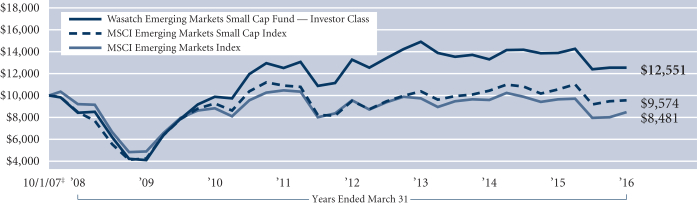

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX / WIEMX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Emerging Markets Small Cap Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Andrey Kutuzov and Scott Thomas.

Roger Edgley, CFA Lead Portfolio Manager |

Andrey Kutuzov, CFA Associate Portfolio |

Scott Thomas, CFA Associate Portfolio |

OVERVIEW

The Wasatch Emerging Markets Small Cap Fund ended the first quarter of 2016 with flat performance, while the benchmark, the MSCI Emerging Markets Small Cap Index, was up 0.97%.

From late 2015 into February 2016, the outlook for emerging markets was clouded by investor fears and short-term volatility. Stocks were hit hard globally, as concerns about China’s economy and its jittery currency multiplied.

During the quarter’s second half, signs that the U.S. Federal Reserve may raise interest rates more slowly than previously expected heartened investors. Lower interest rates in the U.S. enhance the appeal of emerging markets by making dollar-denominated investments less attractive to global investors who can invest elsewhere at higher rates.

In addition, we believe that most emerging-market currencies have seriously overshot in their weakness against the U.S. dollar. A reversal of this trend, which has lasted five years, may have already started. This would be positive for emerging-market investors because it would raise the value of their holdings when converted back into U.S. dollars.

DETAILSOFTHE QUARTER

Taiwan is one of the Fund’s largest market weightings, at approximately 20%. Lately, we have been finding interesting companies in health care, the auto supply chain for electric vehicles, automation and robotics. Although the Fund’s holdings in Taiwan slightly underperformed those in the benchmark during the quarter, we remain confident in the long-run story here. Two of the Fund’s top contributors were from Taiwan: Tung Thih Electronic Co. Ltd., a manufacturer of automobile electronic components and parts; and Silergy Corp., which designs and manufactures a broad range of analog integrated circuits.

India is also a large weighting in the Fund at roughly 20%. In late 2015 and February 2016, we visited 77 companies in and around Mumbai, New Delhi, Bangalore and Kolkata. While we saw no obvious groundswell of economic activity, we found pockets of strength and a number of interesting companies with attractive fundamentals, based on our metrics. During the quarter, stock prices of Indian pharmaceutical

manufacturers fell as the U.S. Food and Drug Administration stepped up its regulatory activity in India. Fund holdings Marksans Pharma Ltd., Natco Pharma Ltd. and Glenmark Pharmaceuticals Ltd. all suffered. Looking ahead, we believe India’s substantial cost advantage is likely to drive further market-share gains for its pharmaceutical industry as it continues to supply low-cost, high-quality medicine to the world.

The Fund’s weight in China remains substantially below that of the benchmark, which aided relative performance during the quarter, despite the Fund’s holdings being down more. We believe the economic and market trends in China are poor and we see a very difficult environment for equities to do well.

In contrast, Mexico has a strong, emerging middle class and a growing economy. An influx of manufacturing once done in China has expanded Mexico’s export base and created well-paying jobs. Strong export demand from the U.S. helped make Mexico a source of positive performance during the period.

Performance has stabilized and even rebounded in some areas of the Brazilian stock market. We see this as part of a broader phenomenon of stocks in several emerging markets bouncing back after having been oversold. In Brazil, the Fund holds only three companies that we see as high quality. One of these is Raia Drogasil S.A., a Brazilian drug-store chain that was a top contributor for the quarter. The company recently completed an acquisition and launched a proprietary pharmacy-benefits manager.

OUTLOOK

Manufacturing was the driver of emerging-market growth in the last up cycle when China and its demand for commodities played a big role. If emerging markets are now starting a new up cycle, we think manufacturing, innovation and political reform will likely be the drivers.

We strongly believe that the fundamental case for investing in emerging markets has not changed and remains attractive. We have seen the macroeconomic environment becoming more supportive for emerging-market stocks. Emerging-market equities have outperformed developed-market equities since January. Asset flows into emerging markets improved in February and March following a very difficult 2015. More specifically for the Fund, the valuations of quality growth companies appear more attractive after last year’s selloff in emerging markets.

Despite recent gains against the U.S. dollar, our view is that a number of emerging-market currencies remain undervalued. We believe low energy prices are likely to provide an additional boost to emerging economies that are net importers of oil. While we remain cautious toward countries tied to the production of oil and other natural resources, we continue to favor countries such as India, Taiwan, Mexico and the Philippines. Our view toward China remains cautious due to structural concerns.

Thank you for the opportunity to manage your assets.

| Current | and future holdings are subject to risk. |

10

Table of Contents

| WASATCH EMERGING MARKETS SMALL CAP FUND (WAEMX / WIEMX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

| SIX MONTHS* | 1 YEAR | 5 YEARS | SINCE INCEPTION 10/1/07 | |||||||||||||||||

Emerging Markets Small Cap (WAEMX) — Investor | 1.27% | -9.69% | 0.07% | 2.71% | ||||||||||||||||

Emerging Markets Small Cap (WIEMX) — Institutional | 1.27% | -9.69% | 0.07% | 2.71% | ||||||||||||||||

MSCI Emerging Markets Small Cap Index | 4.28% | -9.20% | -2.56% | -0.51% | ||||||||||||||||

MSCI Emerging Markets Index | 6.41% | -12.03% | -4.13% | -1.92% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Small Cap Fund are Investor Class: 1.91% / Institutional Class — Gross: 1.82%, Net: 1.80%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

| * | Not annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Grupo Aeroportuario del Centro Norte S.A.B. de C.V. (Mexico) | 2.0% | |||

| Silergy Corp. (Taiwan) | 1.9% | |||

| Raia Drogasil S.A. (Brazil) | 1.9% | |||

| Poya Co. Ltd. (Taiwan) | 1.9% | |||

| Voltronic Power Technology Corp. (Taiwan) | 1.9% | |||

| Company | % of Net Assets | |||

| Security Bank Corp. (Philippines) | 1.8% | |||

| Unifin Financiera SAPI de C.V. SOFOM (Mexico) | 1.8% | |||

| Medytox, Inc. (Korea) | 1.8% | |||

| Minor International Public Co. Ltd. (Thailand) | 1.7% | |||

| Tung Thih Electronic Co. Ltd. (Taiwan) | 1.7% | |||

| ** | As of March 31, 2016, there were 108 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

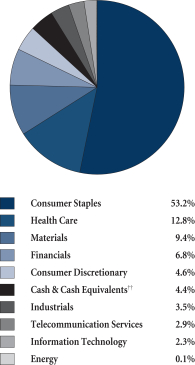

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: October 1, 2007. The MSCI Emerging Markets and Emerging Markets Small Cap indices are free float-adjusted market capitalization indices designed to measure the equity market performance of emerging markets. You cannot invest directly in these or any indices.

11

Table of Contents

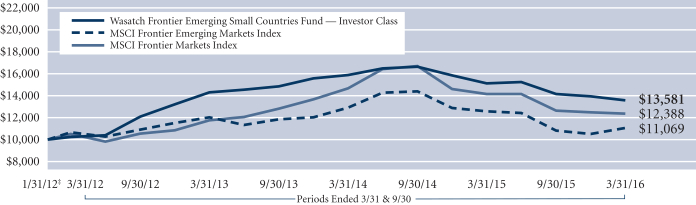

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX / WIFMX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Frontier Emerging Small Countries Fund is managed by a team of Wasatch portfolio managers led by Laura Geritz and Jared Whatcott.

Laura Geritz, CFA Lead Portfolio Manager |

Jared Whatcott, CFA Associate Portfolio Manager | OVERVIEW

The Wasatch Frontier Emerging Small Countries Fund — Investor Class fell -2.57% for the quarter ended March 31, 2016 and underperformed the MSCI Frontier Emerging Markets Index (Frontier |

Index), which gained 5.03%. Emerging markets experienced one of their best months on record in March, as evidenced by the 13.23% return of the MSCI Emerging Markets Index (Emerging Markets Index). In contrast, March was one of the worst months of performance for the Frontier Index relative to the Emerging Markets Index. Although heavyweights in the Frontier Index — Kuwait, Nigeria and Pakistan — managed small gains, what is more astonishing is that some of the stalwart countries — Argentina, Bangladesh and Sri Lanka — actually put up negative returns during what turned out to be a big rally.

Since the Fund is overweight in what we consider to be the real frontier countries (Vietnam, Bangladesh, Pakistan, Kenya and Sri Lanka) and substantially underweight in some of the emerging markets that rallied (the Philippines, Colombia and Peru), the performance discrepancy is pretty simple — we were sitting in the wrong countries during the rally and in some cases our stocks underperformed. While this was disappointing, it should not be startling — frontier markets usually lag emerging markets in rallies. If the rally continues, we would expect liquidity and fundamental improvement to support stocks in frontier markets. In essence, we would expect better days ahead for frontier markets relative to emerging markets.

DETAILSOFTHE QUARTER

Frontier and emerging markets began the year with sharp declines. By late January, however, global markets had started rebounding, which continued throughout the quarter. The rally was largely confined to energy and materials companies that benefited from strengthening commodity prices. We do not believe, however, that the higher property and infrastructure spending in China, presumably among the primary drivers of the rebound in commodity prices, is likely to prove sustainable. As such, we do not expect to change our view of countries like Peru and Colombia, where materials and energy names make up roughly 40% and 34% of each country’s benchmark, respectively. So while the Fund took what we believe is a short-term hit relative to its benchmark due to lack of exposure to, and the underperformance of our holdings in, these often volatile sectors, we remain confident that by focusing on companies with

long-term competitive advantages and sustainable earnings and cash flows, our process will provide the potential to generate healthy long-term returns for shareholders.

In addition to Peru and Colombia, where we mostly lacked exposure to the rebounds in their equity markets, the Fund also suffered from heavy weightings in poor-performing countries like Nigeria and Sri Lanka where we own what we consider to be a stable of strong consumer brand companies including global brands like Nestlé, Unilever and Guinness.

Vietnam continued to be a source of strength for the Fund. The country is one of Southeast Asia’s fastest-growing economies and is a signatory to the Trans-Pacific Partnership, which is expected to continue to boost foreign investment in the country. The Fund’s second-largest overall contributor was Vietnam Dairy Products. The company continues to grow both its top and bottom lines by double digits by maintaining its dominant market position in the country.

The Fund’s gain in the consumer-discretionary sector was more than double that of the benchmark. This was primarily due to Kuwait Foods Americana, a leading restaurant company operating in the Middle East and North Africa.

The sector of the Fund that detracted the most was consumer staples. Our weighting in consumer staples, which was nearly eight times that of the benchmark, hurt even though our stocks were not down as much. Within the sector, the Fund holds a number of what we consider to be high-quality African and South Asian companies, including food, breweries and consumer brand companies. Although many of these holdings detracted from performance in the quarter, we believe they are still very well positioned for long-term success.

OUTLOOK

Our view is that the stocks of companies with sustainable earnings growth, strong cash-flow generation, dominant market positions, strong competitive advantages and excellent management teams have the best potential to be rewarded in the long run.

In the first quarter of 2016, we were on the road again visiting companies in Malaysia, Thailand, Mexico, Indonesia, the Philippines, Vietnam, the United Arab Emirates and Pakistan. In each of these markets, we continued to find companies that we believe are positioned to flourish for years to come. In particular, we spent a combined six weeks in Southeast Asia scouring the markets for companies that meet our rigorous investment standards.

The turbulence witnessed this past quarter is part and parcel of investing in frontier and emerging markets. Yet market volatility often belies the underlying stability of the companies we own. While some markets are struggling for growth, others have pushed forward reforms and are taking steps that we believe could prove beneficial to investors.

We remain grateful for your continued trust with your investment.

| Current | and future holdings are subject to risk. |

12

Table of Contents

| WASATCH FRONTIER EMERGING SMALL COUNTRIES FUND (WAFMX / WIFMX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

| SIX MONTHS* | 1 YEAR | 5 YEARS | SINCE INCEPTION 1/31/12 | |||||||||||||||||

Frontier Emerging Small Countries (WAFMX) — Investor | -4.17% | -10.32% | N/A | 7.62% | ||||||||||||||||

Frontier Emerging Small Countries (WIFMX) — Institutional | -3.80% | -9.98% | N/A | 7.72% | ||||||||||||||||

MSCI Frontier Emerging Markets Index | 2.25% | -12.07% | N/A | 2.47% | ||||||||||||||||

MSCI Frontier Markets Index | -2.16% | -12.54% | N/A | 5.27% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Frontier Emerging Small Countries Fund are Investor Class — Gross: 2.28%, Net: 2.25% / Institutional Class — Gross: 2.09%, Net: 2.05%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

| *Not | annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Vietnam Dairy Products JSC (Vietnam) | 5.7% | |||

| Square Pharmaceuticals Ltd. (Bangladesh) | 3.8% | |||

| East African Breweries Ltd. (Kenya) | 3.2% | |||

| Tanzania Breweries Ltd. (Tanzania, United Republic of) | 3.2% | |||

| Nestlé Nigeria plc (Nigeria) | 2.3% | |||

| Company | % of Net Assets | |||

| Kuwait Foods Americana (Kuwait) | 2.2% | |||

| PriceSmart, Inc. (Costa Rica) | 2.0% | |||

| FPT Corp. (Vietnam) | 1.9% | |||

| Universal Robina Corp. (Philippines) | 1.8% | |||

| British American Tobacco Bangladesh Co. Ltd. (Bangladesh) | 1.8% | |||

| ** | As of March 31, 2016, there were 133 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

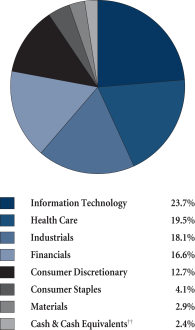

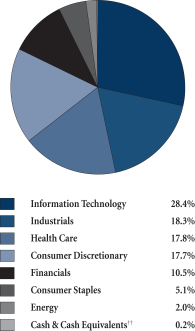

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: January 31, 2012. The MSCI Frontier Emerging Markets and MSCI Frontier Markets indices are free float-adjusted market capitalization indices designed to measure the equity market performance of the global frontier and emerging markets. You cannot invest directly in these or any indices.

13

Table of Contents

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX / WIGOX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch Global Opportunities Fund is managed by a team of Wasatch portfolio managers led by JB Taylor and Ajay Krishnan.

JB Taylor Lead Portfolio Manager

|

Ajay Krishnan, CFA Lead Portfolio Manager

| OVERVIEW

The Wasatch Global Opportunities Fund — Investor Class declined |

(AC) World Small Cap Index, which gained 0.70%.

In January, investors’ nervousness intensified sending most stocks sharply lower. The downward spiral continued until mid-February, when stocks began a dramatic recovery. As a result, the benchmark’s modest increase masks much more significant volatility during the quarter.

Unfortunately, the specific nature of the decline and recovery didn’t favor the Fund relative to the benchmark. During the beginning of the quarter, growth-oriented stocks tended to suffer disproportionately, reflecting investors’ fears of a slowdown in China and potentially in developed markets as well. Then, as the markets recovered, investors’ ongoing caution meant that some growth-oriented industries — such as biotech and software — didn’t fully participate in the broader rally. This was particularly true in the U.S., where many of the slowest-growing companies actually performed the best in the stock market. Therefore, the Fund’s holdings in areas with high potential for growth, but with less-established businesses, lost ground on a relative basis even as economic conditions supported continued optimism for their future prospects.

DETAILSOFTHE QUARTER

DIO Corp., based in South Korea, was the leading contributor to Fund performance during the quarter. DIO has developed a completely new procedure for dental implants that involves a 3-D scan of the patient’s jaw, relying more on technology than on the dentist’s skill. The procedure is a win-win for both dentists and patients. Dentists can see twice as many patients because of the procedure’s increased speed — while also charging 20% more. Patients benefit from much faster recovery times.

Another strong contributor to Fund performance was Seria Co. Ltd., which operates a chain of dollar stores (called 100-yen shops in Japan). The company continued to benefit from industry consolidation and a stronger yen, which has the effect of lowering the cost of many imported goods that are sold by Seria.

Additional contributors included a trio of U.S.-based industrials that were responsible for a substantial portion of our outperformance in the sector: Echo Global Logistics, Inc., Trex Co., Inc. and Spirit Airlines, Inc. In the case of Spirit, the airline had been taking advantage of sharply lower

fuel costs to improve margins and finance growth during the past two years. That growth orientation proved problematic, however, as customer complaints about reliability increased and other airlines, notably American, began competing aggressively on price to take share from Spirit. With a recent change in leadership at Spirit, the airline intends to pare growth to a more-manageable level of potentially 15% to 20% annually, while increasing expenditures to improve customer service. So far, investors have responded favorably.

Among detractors from the Fund’s performance, the most significant were several health-care companies including India’s Marksans Pharma Ltd. Based in Mumbai, Marksans markets its branded prescription and over-the-counter drugs in India and internationally, with the United Kingdom (U.K.) accounting for approximately 40% of revenues. The company’s stock tumbled in January on news that its manufacturing plant in Goa had failed a good manufacturing practice (GMP) inspection by the U.K. Medicines & Healthcare products Regulatory Agency (MHRA). In mid-March, the company announced that the U.K. regulator had issued a “Restricted GMP Certificate” that will allow Marksans to continue manufacturing and selling products considered critical for U.K. markets until the MHRA’s next inspection.

Two U.S.-based biotechs, Seattle Genetics, Inc. and Sangamo BioSciences, Inc., were also significant detractors. Both illustrate the general case of growth-oriented companies selling off during the beginning of the quarter and failing to fully participate in the recovery later in the quarter. We don’t see any company-specific problems, and we remain optimistic about future growth in these names and in the biotech industry.

OUTLOOK

During the first quarter, we trimmed our exposure to Japan — moving from a notable overweight to a near-neutral weight relative to the benchmark. In our view, corporate fundamentals for Japanese companies remain strong. However, we see the country’s risk profile as higher due to increased stock-price volatility and macroeconomic uncertainties.

Also, valuations have increased as other investors have come to recognize the opportunities in Japan. Based on how valuations have risen, we suspect we were early among institutional investors to opt for a substantially overweight position in Japan. Now, we think we’re in the first wave to reduce that exposure in favor of broad-based growth opportunities elsewhere. That said, we continue to hold key investments in Japanese companies.

As always, our analysis focuses heavily on firsthand research (including meetings with management teams), fundamental due diligence and attention to macroeconomic factors. Although the first quarter didn’t bring a significant rebound in the high-quality growth stocks favored by the Fund, we remain confident in our positioning for the future. In particular, we expect our companies’ quarter-end earnings results to be strong and have the potential to ultimately be reflected in their stock prices.

Thank you for the opportunity to manage your assets.

| Current and future holdings are subject to risk. |

14

Table of Contents

| WASATCH GLOBAL OPPORTUNITIES FUND (WAGOX / WIGOX) — Portfolio Summary | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

AVERAGE ANNUAL TOTAL RETURNS

| SIX MONTHS* | 1 YEAR | 5 YEARS | SINCE INCEPTION 11/17/08 | |||||||||||||||||

Global Opportunities (WAGOX) — Investor | 3.39% | -5.99% | 5.67% | 16.94% | ||||||||||||||||

Global Opportunities (WIGOX) — Institutional | 3.39% | -5.99% | 5.67% | 16.94% | ||||||||||||||||

MSCI AC World Small Cap Index | 4.87% | -4.50% | 5.39% | 14.99% | ||||||||||||||||

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit www.WasatchFunds.com. The Advisor may absorb certain Fund expenses, without which total return would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2016 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Global Opportunities Fund are Investor Class: 1.56% / Institutional Class — Gross: 1.46%, Net: 1.35%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information, including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small and micro cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

| * | Not annualized. |

TOP 10 EQUITY HOLDINGS**

| Company | % of Net Assets | |||

| Patrizia Immobilien AG (Germany) | 3.2% | |||

| Unifin Financiera SAPI de C.V. SOFOM (Mexico) | 2.3% | |||

| Cornerstone OnDemand, Inc. | 2.2% | |||

| Rightmove plc (United Kingdom) | 2.0% | |||

| Medytox, Inc. (Korea) | 2.0% | |||

| Allegiant Travel Co. | 2.0% | |||

| Company | % of Net Assets | |||

| Voltronic Power Technology Corp. (Taiwan) | 2.0% | |||

| Grupo Aeroportuario del Centro Norte S.A.B. de C.V. (Mexico) | 2.0% | |||

| Ultimate Software Group, Inc. | 1.9% | |||

| Frutarom Industries Ltd. (Israel) | 1.8% | |||

| ** | As of March 31, 2016, there were 96 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN†

| † | Excludes securities sold short and options written, if any. |

| †† | Also includes Other Assets & Liabilities. |

GROWTHOFA HYPOTHETICAL $10,000 INVESTMENT

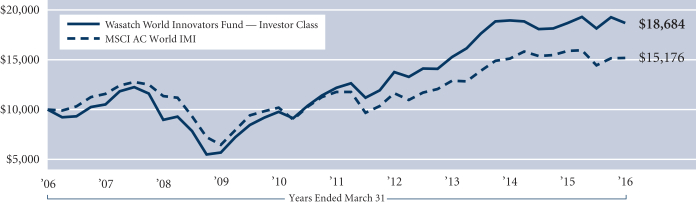

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees. ‡Inception: November 17, 2008. The MSCI AC (All Country) World Small Cap Index is a free float-adjusted market capitalization index designed to measure the performance of small capitalization securities in developed and emerging markets. You cannot invest directly in this or any index.

15

Table of Contents

| WASATCH INTERNATIONAL GROWTH FUND (WAIGX / WIIGX) — Management Discussion | MARCH 31, 2016 (UNAUDITED) | |

| ||

| ||

The Wasatch International Growth Fund is managed by a team of Wasatch portfolio managers led by Roger Edgley, Ken Applegate, Linda Lasater and Kabir Goyal.

Roger Edgley, CFA Lead Portfolio Manager |

Ken Applegate, CFA Portfolio Manager | OVERVIEW

Quality growth stocks did not have a strong start to 2016. Many stocks seemed to be reverting toward their historical average prices. For example, health care was the leading sector in the MSCI All Country (AC) World Ex-U.S.A. Small Cap Index in 2015, rising over 21%, and the performance of the Fund’s health-care stocks was even stronger. In the first quarter of 2016, health care was one of the worst-performing sectors in the Index, dropping | ||