UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04920

WASATCH FUNDS TRUST

(Exact name of registrant as specified in charter)

505 Wakara Way, 3rd Floor

Salt Lake City, UT 84108

(Address of principal executive offices) (Zip code)

| | | | | | |

| | (Name and Address of Agent for Service) | | Copy to: | | |

| | | |

| | | Eric S. Bergeson Wasatch Advisors, Inc. 505 Wakara Way, 3rd Floor Salt Lake City, UT 84108 | | Eric F. Fess, Esq. Chapman & Cutler LLP 320 S. Canal Street Chicago, IL 60606 | | |

Registrant’s telephone number, including area code: (801) 533-0777

Date of fiscal year end: September 30

Date of reporting period: March 31, 2023

Item 1. Report to Shareholders.

| (a) | A copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “1940 Act”) is filed herewith. |

WASATCHGLOBAL.COM MARCH 31, 2023 2023 Semi-Annual Report Fund Investor Institutional Fund Investor Institutional Name Class Class Name Class Class Wasatch Core Growth Fund WGROX WIGRX Wasatch International Opportunities Fund WAIOX WIIOX Wasatch Emerging India Fund WAINX WIINX Wasatch International Select Fund WAISX WGISX Wasatch Emerging Markets Select Fund WAESX WIESX Wasatch Long/Short Alpha Fund WALSX WGLSX Wasatch Emerging Markets Small Cap Fund WAEMX WIEMX Wasatch Micro Cap Fund WMICX WGICX Wasatch Frontier Emerging Small Wasatch Micro Cap Value Fund WAMVX WGMVX WAFMX WIFMX Countries Fund Wasatch Small Cap Growth Fund WAAEX WIAEX Wasatch Global Opportunities Fund WAGOX WIGOX Wasatch Small Cap Value Fund WMCVX WICVX Wasatch Global Select Fund WAGSX WGGSX Wasatch Ultra Growth Fund WAMCX WGMCX Wasatch Global Value Fund FMIEX WILCX Wasatch U.S. Select Fund WAUSX WGUSX Wasatch Greater China Fund WAGCX WGGCX Wasatch-Hoisington U.S. Treasury Fund WHOSX Ë‘ Wasatch International Growth Fund WAIGX WIIGX

Wasatch Funds

Salt Lake City, Utah

wasatchglobal.com

800.551.1700

This material must be accompanied or preceded by a prospectus.

Please read the prospectus carefully before you invest.

Wasatch Funds are distributed by ALPS Distributors, Inc.

1

| | |

Letter to Shareholders —While Stocks Have Been Volatile, High Quality is Back in Favor | | |

| | |

Mick Rasmussen, CFA Lead Portfolio Manager | | DEAR FELLOW SHAREHOLDERS: After a poor showing in 2022, high-quality growth stocks got off to a strong start in January 2023. Then, in February, stocks sold off based on concerns regarding overheated economic activity, stubbornly elevated inflation, and persistent interest-rate hikes by the U.S. Federal Reserve (Fed) and counterparts around the world. In March, a few well-publicized bank failures worsened market sentiment — causing stocks to slip further. Nevertheless, investor sentiment improved toward the end of March and U.S. small-cap growth stocks, as measured by the Russell 2000® Growth Index, finished the first quarter of 2023 in positive territory. Small-cap growth stocks also generally performed well internationally in both developed and emerging |

markets. Moreover, the Wasatch-specific approach to high-quality growth investing was generally favored.

In a broad sense, Wasatch defines high-quality growth companies as those having innovative products, services and business models, increasing market share, great management teams, significant returns on capital, relatively low debt and the ability to self-fund expansion. Another element of our approach to quality-oriented investing is that we often attempt to identify excellent companies before high quality is evident in their financial results. If we do this well, stock-price appreciation can be particularly strong.

PERSPECTIVE ON RECENT BANK FAILURES

While elevated inflation and interest-rate hikes have impacted markets for over a year, the failures of three U.S. banks in March sparked stock-price volatility around the world. In the span of less than a week, Silvergate Bank announced it would wind down operations due to losses suffered in its loan portfolio, Silicon Valley Bank (SVB) was placed under receivership of the Federal Deposit Insurance Corporation (FDIC) and regulators closed Signature Bank. The downfalls of SVB and Signature were the second- and third-largest bank failures in U.S. history.

None of the Wasatch funds owned any banks that failed in March. Furthermore, we believe the few banks that we do hold are structurally quite different from the banks that failed.

WHY OUR BANKS ARE DIFFERENT

The banks that failed had concentrated customer bases. Silvergate and Signature focused on the cryptocurrency industry, and the bulk of SVB’s customers were early-stage technology companies. Moreover, SVB and Silvergate had low loan-to-deposit ratios and depended on sizable long-term securities portfolios to support short-term deposits — which created a timing mismatch. These factors played large roles in the banks’ failures.

The banks held in the Wasatch funds are quite different, with reasonable loan-to-deposit ratios and relatively small securities portfolios. Additionally, our banks either focus on retail customers or serve a diversified group of commercial clients. So far, the management teams of the banks we own have reported that operations have remained normal or have actually improved.

BANKING’S EFFECTS ON THE TECHNOLOGY SPACE

Outside of banking, the failures will surely affect the technology space. Many technology companies hold cash and lines of credit at banks like SVB. The government’s decision to protect SVB’s depositors means businesses still have access to working capital in the near term. But we expect to see a somewhat more difficult environment for early-stage technology companies as they seek new banking relationships.

Regarding our own technology holdings, we don’t think we’ll see much friction. We have very few holdings that had any exposure to SVB. We tend to invest in companies that have control over their destinies because they’re self-funded through their ability to generate positive free cash flows.

SUMMARIZING INVESTMENT CONDITIONS DURING THE PAST THREE YEARS

For much of 2020 and 2021, the Covid-19 pandemic accelerated the digitalization of daily activities — working, banking, studying, shopping and accessing entertainment from home. In general, the stocks of companies tied to these themes performed well. For the most part, Wasatch benefited as investors extrapolated rapid rates of growth and market penetration far into the future. A backdrop of very low interest rates magnified the positive effects on Wasatch’s performance in areas like software as a service (SaaS), technology consulting, semiconductor chips, digital banking and e-commerce.

During most of 2022, by contrast, rising inflation and interest rates — and a shift in market leadership — proved quite hostile to Wasatch’s investing approach. Because the long-duration growth companies we favor generate cash flows further into the future, higher interest rates make the income streams of these companies less valuable in the present.

With fallout from the Omicron variant of Covid-19 less severe than initially expected, the stocks of companies tied to digitalization and other areas that had benefited from the pandemic and helped Wasatch’s performance in 2020 and 2021 tended to be hurt the most in 2022. Even so, we believe these themes are enduring and will continue to offer attractive opportunities for long-term investors.

2

| | |

| | | MARCH 31, 2023 (Unaudited) |

While inflation was already set to rise in 2022 due to pandemic-induced supply-chain challenges and increased consumer demand, the war in Ukraine exacerbated inflationary pressures. These pressures supported cyclical, value-oriented areas of the market such as energy and some segments of materials and utilities, where Wasatch was structurally underweighted. We believe these sectors are mostly comprised of capital-intensive and undifferentiated businesses that typically don’t fit well with our preference for dynamic, high-quality companies. Also, energy and materials firms tend to carry significant debt and are often highly cyclical — with success generally linked to a single commodity that’s beyond management’s control.

Worsening inflation also forced central banks to raise interest rates aggressively in 2022, posing stronger headwinds for our long-duration growth stocks. Late in the first quarter of 2023, however, these headwinds showed signs of reversing.

THOUGHTS AND POSITIONING FOR 2023 AND BEYOND

Before discussing our thoughts and positioning, we must first acknowledge that macro predictions are inherently unreliable. To understand why, investors may want to consider a few of the high-profile misjudgments over the past three years. Mainstream experts on Russia failed to foresee the invasion of Ukraine. The Fed incorrectly assumed that inflation was “transitory.” Banks loaded up on long-term bonds based on the wrongheaded belief that interest rates wouldn’t rise sharply in such a short period of time.

Regarding these macro issues, we admit that our early judgments may have been equally incorrect. However, we didn’t make major decisions based on these judgments. Instead, we try to invest in companies we think can perform well under a variety of scenarios. Over the long term, we think this approach will deliver attractive risk-adjusted returns.

Now we come to our thoughts and positioning for 2023 and beyond. As mentioned above, despite continued volatility, high-quality growth stocks reasserted their attractiveness and performed well during the first quarter. While we don’t know what’s in store for us in terms of geopolitics and market conditions, we like our companies regardless of the macro environment.

If the economy enters a significant recession and interest rates fall dramatically, we think we’ll be well-positioned with the likes of profitable technology companies, recession-resistant health-care providers and recurring-revenue businesses that can self-fund their expansion. Additionally, in a lower interest-rate environment, investors tend to prize high-quality growth companies.

But if the economy stays strong or gains momentum, we believe we’ll benefit from generally less expensive investments in the consumer-discretionary and industrials sectors. These sectors tend to be more sensitive to economic development. Having said that, our individual companies aren’t “make or break” economically cyclical businesses.

WE THINK OUR COMPANIES ARE ATTRACTIVELY PRICED

Across all of our investments, we��re paying particular attention to operating margins because companies are seeing rising input costs. By investing in companies with pricing power, we think we’re less vulnerable to margin pressures.

After 2022’s market selloff, which was especially hard on growth stocks, we think our companies are attractively priced for the next five years. And it’s evident that businesses are delivering increasingly normal results, which are being more appropriately reflected in the price of their stocks.

We’re particularly optimistic about our technology companies, whose management teams have realized that profitability must be a top priority. The mantra of “growth at all costs” from the past several years is no longer acceptable. We believe this greater fiscal discipline should lessen the risk and improve the consistency of returns in tech investing.

Still, other factors may increase general market volatility. These factors include a possible recession, rising costs of doing business, uncertainty surrounding interest rates and inflation, heightened geopolitical tensions and central banks balancing various — often conflicting — priorities.

With sincere thanks for your continuing investment and for your trust,

Mick Rasmussen, Lead Portfolio Manager, Wasatch Long/Short Alpha Fund

Information in this report regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this report. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

Wasatch Advisors LP, doing business as Wasatch Global Investors, is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

Definitions of financial terms and index descriptions and disclosures begin on page 44.

3

| | |

| Wasatch Core Growth Fund (WGROX / WIGRX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Core Growth Fund is managed by a team of Wasatch portfolio managers led by JB Taylor, Paul Lambert and Mike Valentine.

| | | | |

JB Taylor Lead Portfolio Manager | |

Paul Lambert Portfolio Manager | |

Mike Valentine Portfolio Manager |

OVERVIEW

The first quarter of 2023 was positive for stocks of small U.S. growth companies. The Wasatch Core Growth Fund —Investor Class returned 8.89%, outgaining the benchmark Russell 2000® Growth Index, which rose 6.07%. The broader Russell 2000 Index of small-cap stocks added 2.74%. Our companies posted strong operating results in 2022 and entered 2023 with their stocks trading at some of the most attractive valuations we’ve seen in several years.

Energy and banking, areas where the Fund is not heavily exposed, were the main laggards within the benchmark during the first quarter. The failures of three U.S. regional banks and the government-brokered sale of troubled Swiss firm Credit Suisse Group AG dragged down bank stocks and rattled investors.

The broad U.S. equity market weathered the turmoil well, with investors seemingly optimistic that the banking crisis was contained and that the events may push the Federal Reserve closer to the end of its tightening cycle.

DETAILS OF THE QUARTER

The consumer-discretionary sector was the Fund’s biggest source of outperformance relative to the benchmark in the quarter. Our retailers tend to have strong brand names and typically operate in well-established niches. We believe the Fund’s retail companies are positioned better than most of their peers to navigate inflationary and recessionary environments.

Other significant sources of outperformance included industrials, health care and the Fund’s lack of investments in energy. Information technology was the Fund’s primary source of weakness relative to the benchmark.

A top contributor to Fund performance during the quarter was Floor & Decor Holdings, Inc. A multi-channel specialty retailer of hard-surface flooring, Floor & Decor has become a “category killer” among big-box home centers. Because the company cuts out middlemen and buys in large quantities, it can offer customers a wider selection of flooring at lower prices than most competitors. Floor & Decor’s expanding retail footprint, strong cash flows and solid balance sheet provide what we consider a built-in engine for self-funded growth.

Focus Financial Partners, Inc. was also a contributor. Focus is a leading partnership of independent, fiduciary wealth-management firms. The company’s stock price jumped in February after Focus announced it was in talks to sell itself to a private-equity firm. Later that month, Focus entered into a definitive agreement to be acquired in an all-cash deal expected to close in the third quarter of 2023. We liquidated our position to lock in gains.

Banks were the Fund’s two biggest detractors during the quarter — Bank OZK and Webster Financial Corp., respectively. Although their stock prices declined in sympathy with other bank stocks during March, we believe the strong fundamentals of these two banks set them apart from the ones making headlines.

Bank OZK and Webster follow conventional banking models, with well-diversified customer bases, appropriate levels of loans and deposits and small securities portfolios. Despite liquidity pressures at a number of other banks, our research found no significant uptick in withdrawals at either Bank OZK or Webster. We believe these are well-managed banks serving geographical areas with healthy real-estate markets, favorable demographics and above-average economic growth.

OUTLOOK

According to an old English proverb, “It’s an ill wind that blows no one any good.” As dark clouds gathered over Silicon Valley Bank and the wind blew it down, it wasn’t clear what good might be blown our way. With the clouds now parted, we’re beginning to see some silver linings.

Silicon Valley Bank’s failure is likely to make it more difficult for small firms in biotechnology, software, and other tech-driven industries to get funding to launch and grow businesses. What does this mean for the companies owned in the Fund? Weaker competition and fewer rivals, mostly.

The Wasatch investment approach seeks high-quality companies with solid business models, strong cash flows and healthy balance sheets. Therefore, our companies are unlikely to run out of money when business conditions get tough. This is a key advantage in the current environment, with stock prices down and interest rates elevated. While their competitors scramble, our companies can use their cash to make acquisitions, hire talent, invest in their businesses and take market share. The long-term competitive advantages gained from these actions can be substantial.

In short, we think our focus on businesses with strong fundamentals may be as important now as ever. While no one wants to see bank runs, financial instability or economic turmoil, we believe the Fund’s portfolio of high-quality companies is well-positioned to weather potential storms.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

4

| | |

| Wasatch Core Growth Fund (WGROX / WIGRX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

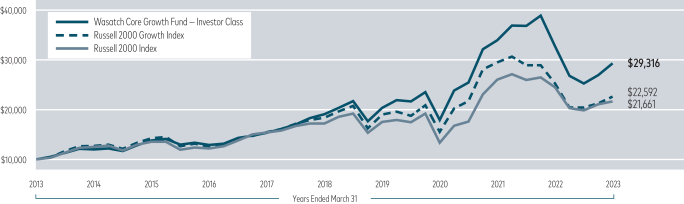

Core Growth (WGROX) — Investor | | | | 16.17% | | | | | -10.43% | | | | | 8.96% | | | | | 11.36% | |

| | | | |

Core Growth (WIGRX) — Institutional | | | | 16.24% | | | | | -10.30% | | | | | 9.10% | | | | | 11.49% | |

| | | | |

Russell 2000® Growth Index | | | | 10.46% | | | | | -10.60% | | | | | 4.26% | | | | | 8.49% | |

| | | | |

Russell 2000® Index | | | | 9.14% | | | | | -11.61% | | | | | 4.71% | | | | | 8.04% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Core Growth Fund are Investor Class: 1.19% / Institutional Class — Gross: 1.06%, Net: 1.05%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

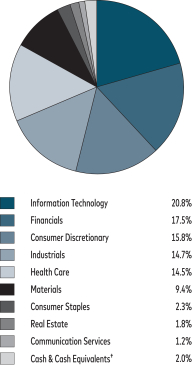

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

Ensign Group, Inc. | | | 3.4% | |

| |

Kadant, Inc. | | | 3.4% | |

| |

HealthEquity, Inc. | | | 3.2% | |

| |

RBC Bearings, Inc. | | | 3.1% | |

| |

Guidewire Software, Inc. | | | 3.1% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

Balchem Corp. | | | 3.0% | |

| |

Hamilton Lane, Inc., Class A | | | 2.9% | |

| |

Novanta, Inc. | | | 2.9% | |

| |

Trex Co., Inc. | | | 2.8% | |

| |

ICON PLC | | | 2.7% | |

| *As | of March 31, 2023, there were 53 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

| † | Also includes Other Assets & Liabilities. |

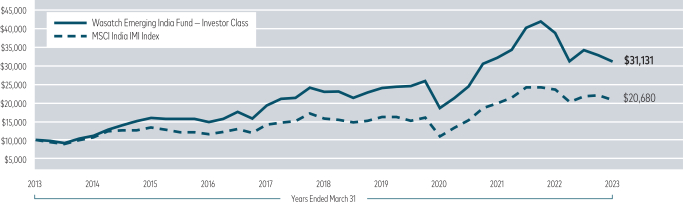

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

5

| | |

| Wasatch Emerging India Fund (WAINX / WIINX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Emerging India Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan and Matthew Dreith.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager | |

Matthew Dreith, CFA Portfolio Manager | | OVERVIEW During the first quarter of 2023, India’s major stock averages continued their slow retreat from all-time highs reached in December. The benchmark MSCI |

India Investable Market Index (IMI) was down -5.94% for the quarter. The Wasatch Emerging India Fund — Investor Class outperformed its benchmark with a smaller decline of -5.03%.

Rebounding from steeper losses during the quarter’s final trading sessions, Indian equities showed resilience amid a slew of negative headlines. A short-seller report attacking companies linked to Indian billionaire Gautam Adani shook investor confidence in January as worries about exposure to the sprawling Adani conglomerate sparked fears of contagion to the banking system.

Inflation and rising interest rates also created headwinds for stocks. Consumer prices in India rose faster than had been expected. Rising prices and higher borrowing costs have pinched household budgets and dented consumption, which accounts for about 60% of India’s gross domestic product (GDP).

DETAILS OF THE QUARTER

The benchmark’s worst-performing sector during the first quarter was utilities. Several Adani Group constituents detracted from performance among utilities. Because no utilities are owned in the Fund, this sector was the Fund’s biggest source of outperformance relative to the benchmark. Other outperforming sectors in the Fund included information technology (IT) and industrials. Holdings in the health-care, consumer-staples and financials sectors were the Fund’s primary sources of weakness against the benchmark.

The IT-services industry accounted for the two strongest contributors to Fund performance for the quarter: Persistent Systems Ltd. and LTIMindtree Ltd., respectively. Because these companies serve customers world-wide, their stock prices can at times be sensitive to global economic conditions. As a result, both stocks benefited from expectations that the U.S. Federal Reserve and other central banks were nearing the end of their interest-rate increases. Investors hoped looser monetary conditions might encourage corporations to free up spending on IT projects that have been placed on hold.

Persistent Systems provides outsourced software development to clients across a range of industries. In the company’s most recent quarter, after-tax profit rose 35% on

revenue growth of 45% compared to the same quarter a year ago. Bookings increased 20% in terms of total contract value, boosted by several large deals across industries and service lines.

LTIMindtree provides a wide array of IT services and solutions. The company reported a 25% year-over-year increase in quarterly revenues, but profit after tax was down -4.7%. Investors appeared to look past the earnings setback because it was largely attributable to costs and temporary inefficiencies stemming from the merger between L&T Infotech and Mindtree, which was completed in November 2022.

The greatest detractor from Fund performance during the quarter was Bajaj Finance Ltd. A non-bank financial company, Bajaj offers a broad spectrum of lending services. Shares of Bajaj declined in sympathy with other Indian equities as a selloff in the shares of Adani Group spilled over to the broader market and weighed especially heavily on the financials sector. The stock moved lower again in March when investors reacted negatively to reports that Bajaj was working on an offer to purchase a banking business in Indonesia in a deal potentially valued in the hundreds of millions of dollars.

Dr. Lal PathLabs Ltd. was also a detractor. The company operates one of the largest chains of diagnostic pathology labs in India. Robust demand for Covid-19 testing during previous phases of the pandemic had driven increased volumes and margin expansion at Dr. Lal’s. Those effects are now reversing, resulting in difficult year-over-year comparisons to early 2022 — the time of India’s peak in Omicron infections. We expect growth to normalize over the next quarter or two, and we believe Dr. Lal’s has the ultimate potential to become India’s dominant consumer brand in diagnostics as the company continues to consolidate and formalize the market.

OUTLOOK

IT-services firms like Persistent Systems and LTIMindtree have been mainstays of India’s services exports for decades. Now, global capability centers (GCCs) have moved up the value chain from providers of low-cost routine services to centers of excellence for automation, innovation, analytics and other functions. Around 40% of the world’s GCCs are currently based in India. We think this number is likely to increase going forward.

Although economic growth in India has come down in recent quarters, the country is expected to remain one of the world’s fastest-growing major economies. Recent upward revisions in India’s real GDP growth reflect increased capital expenditures in the budget released by the Modi government in February. With risks in the U.S. on the rise, we believe well-situated businesses in consumer-driven economies such as India’s offer potentially attractive opportunities for long-term investment.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

6

| | |

| Wasatch Emerging India Fund (WAINX / WIINX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

Emerging India (WAINX) — Investor | | | | -9.04% | | | | | -19.79% | | | | | 6.29% | | | | | 12.03% | |

| | | | |

Emerging India (WIINX) — Institutional | | | | -8.93% | | | | | -19.58% | | | | | 6.45% | | | | | 12.16% | |

| | | | |

MSCI India IMI Index | | | | -4.81% | | | | | -12.02% | | | | | 5.66% | | | | | 7.54% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging India Fund are Investor Class: 1.51% / Institutional Class: 1.38%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets and political and social instability, which are described in more detail in the prospectus. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

HDFC Bank Ltd. | | | 9.7% | |

| |

Bajaj Finance Ltd. | | | 9.5% | |

| |

Elgi Equipments Ltd. | | | 8.1% | |

| |

AU Small Finance Bank Ltd. | | | 7.6% | |

| |

Persistent Systems Ltd. | | | 5.4% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

LTIMindtree Ltd. | | | 5.3% | |

| |

Trent Ltd. | | | 5.1% | |

| |

L&T Technology Services Ltd. | | | 4.4% | |

| |

Avenue Supermarts Ltd. | | | 4.3% | |

| |

Dr. Lal PathLabs Ltd. | | | 4.2% | |

| *As | of March 31, 2023, there were 27 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

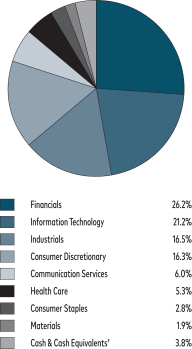

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

7

| | |

| Wasatch Emerging Markets Select Fund (WAESX / WIESX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Emerging Markets Select Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan, Neal Dihora, Scott Thomas and Matthew Dreith.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager

Scott Thomas, CFA Associate Portfolio

Manager | |

Neal Dihora, CFA Portfolio Manager

Matthew Dreith, CFA Associate Portfolio

Manager | | OVERVIEW Emerging-market equities pared early gains as worries about the health of financial companies stoked fears of global recession. Failures of three regional banks in the U.S. and the hastily arranged government-brokered sale of troubled Swiss firm Credit Suisse Group AG added complexity to an economic backdrop that was already uncertain, |

clouding the path forward for policymakers who now must also contend with risks to financial stability as they struggle to bring inflation under control.

The benchmark MSCI Emerging Markets Index rose 3.96% for the first quarter of 2023. Surpassing its benchmark, the Wasatch Emerging Markets Select Fund — Investor Class generated a total return of 9.19%.

DETAILS OF THE QUARTER

Taiwan and Mexico posted above-average returns relative to the benchmark during the quarter, driven by overweight positioning and outsized gains in our holdings. Early signs that the semiconductor cycle may be bottoming fueled a surge of foreign buying in Taiwan’s tech-heavy stock market. And in Mexico, the peso’s appreciation of more than 8% against the U.S. dollar boosted equity returns as the Bank of Mexico, the country’s central bank, raised its policy interest rate to 11.25%.

Driven largely by MercadoLibre, Inc., which we consider a Brazilian holding for portfolio-management purposes, Brazil was the Fund’s single-biggest source of outperformance relative to the benchmark. MercadoLibre provides e-commerce platforms and payment solutions in Latin America. The company’s stock price rose sharply in January after reports of accounting inconsistencies at rival firm Americanas SA, which later filed for bankruptcy. Already a dominant player in the markets it serves, MercadoLibre is expected to gain additional share as the woes of Americanas hinder its ability to borrow, grow and invest in its business. In February, MercadoLibre’s stock rose further after a solid financial report. For the recent quarter, the company posted greater

than 40% year-over-year revenue growth, helped by robust increases in total payment volume and gross merchandise volume.

Other top contributors to Fund performance during the quarter included ASPEED Technology, Inc. Headquartered in Taiwan, the company is a fabless designer of integrated circuits, specializing in areas that include server management and audio-visual extensions. An upswell of enthusiasm during February about artificial intelligence (AI) helped push ASPEED’s stock price higher. Investors reckoned that the massive data-processing requirements of AI’s large language models may lead to increased demand for the company’s chips.

The greatest detractor from Fund performance for the quarter was Bajaj Finance Ltd. A non-bank financial company, Bajaj offers a broad spectrum of lending services in India. Shares of Bajaj declined in sympathy with other Indian equities, as a selloff in the shares of Gautam Adani’s sprawling conglomerate spilled over to the broader market and weighed especially heavily on financials. The stock moved lower again in March when investors reacted negatively to reports that Bajaj was working on an offer to purchase a banking business in Indonesia in a deal potentially valued in the hundreds of millions of dollars.

Meituan was also a significant detractor from Fund performance. The company operates leading online platforms for consumer products and retail services in China. Stocks in China faced headwinds during the first quarter as optimism about the country’s reopening from zero-Covid gave way to doubts about the ability of consumers to spend. Worries about increased competition in Meituan’s business also impacted the company’s share price.

OUTLOOK

Although emerging markets felt the effects of turmoil at U.S. and European banks, recent stresses in the global financial system didn’t originate in developing nations. Instead, developed markets have been the source of this recent market volatility. Relative to developed countries, emerging markets may not be as risky as investors have been led to believe.

We think emerging markets continue to offer more appealing valuations and better growth prospects. For example, Moody’s Investors Service currently forecasts real gross domestic product growth in India of 5.5% in 2023, up from an earlier forecast of 5%. Growth in 2024 is expected to come in at 6.5%. Recent upward revisions for India reflect increased capital expenditures in the budget released by the Modi government in February. With risks in the U.S. on the rise, we believe well-situated businesses in consumer-driven economies such as India’s offer potentially attractive opportunities for long-term investment.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

8

| | |

| Wasatch Emerging Markets Select Fund (WAESX / WIESX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

Emerging Markets Select (WAESX) — Investor | | | | 14.92% | | | | | -18.24% | | | | | 6.50% | | | | | 4.05% | |

| | | | |

Emerging Markets Select (WIESX) — Institutional | | | | 15.01% | | | | | -18.05% | | | | | 6.72% | | | | | 4.33% | |

| | | | |

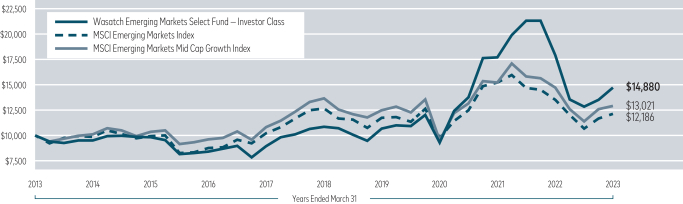

MSCI Emerging Markets Index | | | | 14.04% | | | | | -10.70% | | | | | -0.91% | | | | | 2.00% | |

| | | | |

MSCI Emerging Markets Mid Cap Growth Index | | | | 14.14% | | | | | -12.66% | | | | | -1.14% | | | | | 2.67% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Select Fund are Investor Class: 1.32% / Institutional Class: 1.14%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

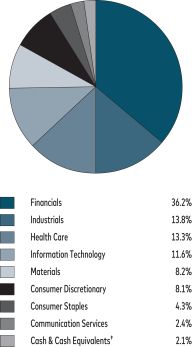

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

MercadoLibre, Inc. | | | 7.7% | |

| |

HDFC Bank Ltd. | | | 6.7% | |

| |

Voltronic Power Technology Corp. | | | 5.3% | |

| |

Bajaj Finance Ltd. | | | 4.9% | |

| |

Chailease Holding Co. Ltd. | | | 4.8% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

Lasertec Corp. | | | 4.5% | |

| |

Silergy Corp. | | | 4.4% | |

| |

WEG SA | | | 4.4% | |

| |

Globant SA | | | 4.2% | |

| |

Grupo Aeroportuario del Pacifico SAB de CV | | | 4.0% | |

| * | As of March 31, 2023, there were 36 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

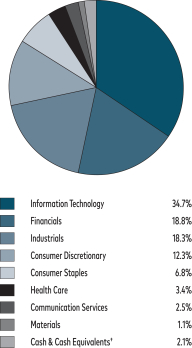

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

9

| | |

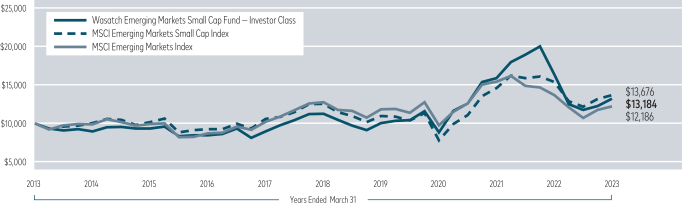

| Wasatch Emerging Markets Small Cap Fund (WAEMX / WIEMX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Emerging Markets Small Cap Fund is managed by a team of Wasatch portfolio managers led by Ajay Krishnan, Dan Chace, Scott Thomas, Kevin Unger and Anh Hoang.

| | | | |

Ajay Krishnan, CFA Lead Portfolio Manager

Kevin Unger, CFA Associate Portfolio Manager | |

Dan Chace, CFA Portfolio Manager

Anh Hoang, CFA Associate Portfolio Manager | |

Scott Thomas, CFA Portfolio Manager OVERVIEW During the first quarter of 2023, the Wasatch Emerging Markets Small Cap Fund �� Investor Class gained 7.60% and surpassed its benchmark, the |

|

MSCI Emerging Markets Small Cap Index, which rose 3.87%.

Growing optimism that central banks were nearing the end of their interest-rate increases evaporated in February after strong economic data challenged the consensus view that inflationary pressures had peaked. The sudden arrival of a crisis at several banks in the U.S. and one in Europe in March further clouded the path forward for policymakers. In India, stocks declined as a short-seller report attacking companies linked to billionaire Gautam Adani shook investor confidence. India’s economic growth slowed as rising borrowing costs weighed on manufacturing and consumption. Consumer prices exceeded the target of India’s central bank for a second straight month. As a result, the Reserve Bank of India may continue to raise interest rates to rein in stubbornly high inflation.

DETAILS OF THE QUARTER

Taiwan and Mexico were sources of outperformance relative to the benchmark, driven by overweight positioning and outsized gains in our holdings. Early signs that the semiconductor cycle may be bottoming fueled a surge of foreign buying in Taiwan’s tech-heavy stock market. And in Mexico, the peso’s appreciation against the U.S. dollar boosted equity returns as the Bank of Mexico, the country’s central bank, raised its policy interest rate to 11.25%.

China’s reopening from zero-Covid restrictions helped spark an upturn in sentiment throughout the region. Equities in Korea did well, but the Korean stocks in the Fund underperformed the Korean positions in the Index. As a result, Korea was the Fund’s primary source of weakness against the benchmark. In China, the benchmark’s positions posted a negative return. However, the Fund’s Chinese stocks logged a solid double-digit gain that helped performance.

The top contributor to Fund performance for the quarter was Taiwanese holding ASPEED Technology, Inc. The company is a fabless designer of integrated circuits, specializing in areas that include server management and audio-visual extensions. Enthusiasm about artificial intelligence (AI) helped push ASPEED’s stock price higher. Investors reckoned that the massive data-processing requirements of AI’s large language models may lead to increased demand for the company’s chips.

Another top contributor was Grupo Aeroportuario del Centro Norte SAB de CV. Often referred to as “OMA,” the company operates international airports in the northern and central regions of Mexico under contracts with the government. Pent-up demand for travel has raised passenger counts and boosted revenues at the company’s airports.

Although our Indian stocks declined less than the Indian positions in the Index, overweight positioning in India hurt the Fund’s relative performance. As the Fund’s most heavily weighted country, India accounted for the two biggest detractors in the first quarter: AU Small Finance Bank Ltd. and Dr. Lal PathLabs Ltd.

With consumer inflation in India coming in above the central bank’s target, the growing likelihood of additional rate hikes weighed on share prices in the financials sector, including those of AU Small Finance Bank, which primarily targets unbanked and underbanked low- and middle-income borrowers.

Dr. Lal’s operates one of the largest chains of diagnostic pathology labs in India. Robust demand for Covid-19 testing had driven increased volumes and margin expansion for the company. Those effects are now reversing, resulting in difficult year-over-year comparisons to early 2022 — the time of India’s peak in Omicron infections. We expect growth to normalize, and we believe Dr. Lal’s has the potential to become India’s dominant consumer brand in diagnostics.

OUTLOOK

Broadly speaking, we think recent developments could ultimately strengthen, not weaken, the case for investing in emerging markets. Over time, emerging markets may benefit if problems at U.S. banks result in lower global interest rates and a weaker U.S. dollar.

Moreover, we think emerging markets continue to offer more appealing valuations and have better growth prospects than developed markets. For example, India’s economic growth forecasts have recently been revised upward, reflecting increased capital expenditures in the budget released by the Modi government in February. With risks in the U.S. on the rise, we believe well-situated businesses in consumer-driven economies such as India’s offer potentially attractive opportunities for long-term investment.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

10

| | |

| Wasatch Emerging Markets Small Cap Fund (WAEMX / WIEMX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

Emerging Markets Small Cap (WAEMX) — Investor | | | | 12.39% | | | | | -19.30% | | | | | 3.23% | | | | | 2.80% | |

| | | | |

Emerging Markets Small Cap (WIEMX) — Institutional | | | | 12.24% | | | | | -19.37% | | | | | 3.35% | | | | | 2.90% | |

| | | | |

MSCI Emerging Markets Small Cap Index | | | | 12.38% | | | | | -10.99% | | | | | 1.80% | | | | | 3.18% | |

| | | | |

MSCI Emerging Markets Index | | | | 14.04% | | | | | -10.70% | | | | | -0.91% | | | | | 2.00% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Emerging Markets Small Cap Fund are Investor Class: 1.91% / Institutional Class: 1.78%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

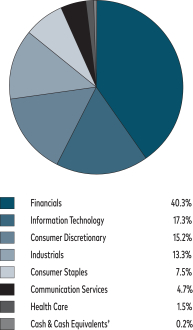

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

Voltronic Power Technology Corp. | | | 6.5% | |

| |

AU Small Finance Bank Ltd. | | | 5.0% | |

| |

Globant SA | | | 4.3% | |

| |

Grupo Aeroportuario del Centro Norte SAB de CV | | | 4.3% | |

| |

Silergy Corp. | | | 4.0% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

momo.com, Inc. | | | 3.6% | |

| |

LEENO Industrial, Inc. | | | 3.5% | |

| |

Persistent Systems Ltd. | | | 3.5% | |

| |

ASPEED Technology, Inc. | | | 3.4% | |

| |

LTIMindtree Ltd. | | | 3.2% | |

| * | As of March 31, 2023, there were 46 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

11

| | |

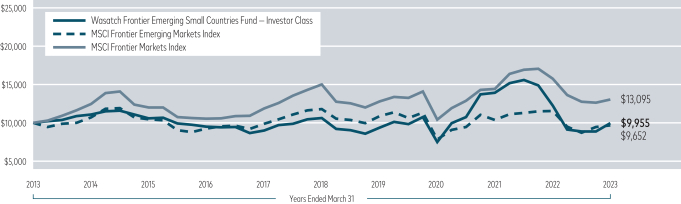

| Wasatch Frontier Emerging Small Countries Fund (WAFMX / WIFMX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Frontier Emerging Small Countries Fund is managed by a team of Wasatch portfolio managers led by Scott Thomas.

| | |

Scott Thomas, CFA Lead Portfolio Manager | | OVERVIEW During 2022, rising rates and inflation sapped investor enthusiasm for growth-oriented stocks. However, as many central banks seemed poised to slow or pause interest-rate increases in 2023, investors have begun to reward the strong results of many of our companies, leading to significant gains for many stocks in the portfolio. |

In this environment, the Wasatch Frontier Emerging Small Countries Fund — Investor Class returned 12.65% in the first quarter, outperforming the benchmark MSCI Frontier Emerging Markets Index, which returned 2.39%.

DETAILS OF THE QUARTER

MercadoLibre, Inc. was the Fund’s top contributor to performance during the quarter. The company operates an online e-commerce, payments, and credit system in 18 countries, and has been called “the Amazon of Latin America” due to its leadership in the region’s fast-growing online marketplace. MercadoLibre experienced considerable growth in 2022, with fourth-quarter revenue up 56.5% from the same period in 2021 and operating income jumping from $24 million to $349 million. MercadoLibre also benefited as an important rival in Brazil was engulfed in an accounting scandal that led to the departure of its CEO and CFO.

Mexico’s Qualitas Controladora SAB de CV was another top performer. The auto insurer is rebounding from a difficult period when mobility trends and accident frequency returned to pre-pandemic levels while inflation increased the cost of parts for vehicle repairs. As the company and industry raise prices and inflation settles down, we think profitability should recover on the back of improving underwriting results and the company’s investment portfolio benefiting from higher interest rates. We continue to like the company’s long-term growth potential and stability as the market leader in an underpenetrated Mexican insurance market. Qualitas is also expanding geographically and diversifying into the relatively nascent Mexican health-insurance business.

The largest detractor from Fund performance was Bajaj Finance Ltd. A non-bank financial company, Bajaj offers a broad spectrum of lending services in India. Shares of Bajaj declined in sympathy with other Indian equities as a selloff in the shares of Gautam Adani’s sprawling conglomerate spilled over to the broader market and weighed especially heavily on financials. The stock moved lower again in March, in part due to investors reacting negatively to reports that Bajaj was planning to purchase an Indonesian bank.

We continue to have confidence in Bajaj’s management team, which has an outstanding track record, and we see significant opportunities ahead for this non-bank lender. Bajaj is outpacing the stodgy traditional banks and their notoriously poor customer service by lending to affluent urban and semi-urban consumers and offering credit cards, mortgages and loans for durable goods. The company is a leader in employing sophisticated data analytics to identify opportunities and reduce credit risk, all while lowering its broader risk profile as it reinvests fee income from higher-risk products into lower-risk areas like mortgage lending.

VEF AB also detracted from performance. The Swedish firm invests in growth-stage financial-technology companies in frontier and emerging markets. The stock was down after a Brazilian company in its investment portfolio tabled its initial public offering and a Mexican holding ran into liquidity issues, raising concerns about whether VEF could sustain its growth. Some setbacks are inevitable with startups, but we continue to believe that VEF is investing in companies with savvy management teams that have structured their businesses to withstand challenges. Importantly, we think these companies represent the future of finance in their target markets.

OUTLOOK

Even as the global banking industry shudders in response to high-profile meltdowns at U.S. and Swiss banks, we continue to see a bright future for the innovative businesses we own within emerging and frontier markets.

To be sure, an extended banking crisis or recession in developed markets could create economic headwinds everywhere. We would note, however, that the worst of the rate-related tumult affecting the developed world has, in many cases, already passed in emerging and frontier markets. Interest rates in these markets remain very high, but some key central banks, including Brazil’s, have already stopped their increases.

Importantly, many of our holdings may not need the strongest economic backdrop to thrive because they’re tied to strong secular tailwinds. The Fund remains focused on companies at the forefront of the longer-term social and technological trends that are transforming the frontier and emerging markets in which they operate.

For example, some of our largest holdings include: IT companies enabling digital transformation for businesses and consumers; financial-service firms facilitating safer and frictionless digital transactions for a growing middle class; hospital chains improving quality of life within local markets; and retail companies and communication-services firms aligned to new purchasing and consumption trends. We believe these companies have a long runway for growth, and we look forward to watching these themes play out in 2023 and beyond.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

12

| | |

| Wasatch Frontier Emerging Small Countries Fund (WAFMX / WIFMX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

Frontier Emerging Small Countries (WAFMX) — Investor | | | | 12.65% | | | | | -19.06% | | | | | -1.31% | | | | | -0.04% | |

| | | | |

Frontier Emerging Small Countries (WIFMX) — Institutional | | | | 13.31% | | | | | -18.79% | | | | | -1.06% | | | | | 0.15% | |

| | | | |

MSCI Frontier Emerging Markets Index | | | | 11.76% | | | | | -16.63% | | | | | -3.99% | | | | | -0.35% | |

| | | | |

MSCI Frontier Markets Index | | | | 2.24% | | | | | -17.55% | | | | | -2.85% | | | | | 2.73% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Frontier Emerging Small Countries Fund are Investor Class — Gross: 2.29%, Net: 2.19% / Institutional Class — Gross: 2.08%, Net: 1.99%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

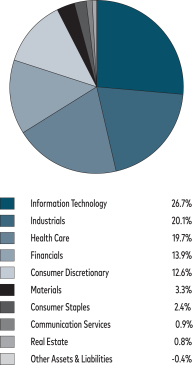

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

MercadoLibre, Inc. | | | 9.9% | |

| |

FPT Corp. | | | 8.2% | |

| |

Bajaj Finance Ltd. | | | 6.6% | |

| |

Bank for Foreign Trade of Vietnam JSC | | | 6.1% | |

| |

Qualitas Controladora SAB de CV | | | 5.2% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

WEG SA | | | 5.1% | |

| |

Discovery Ltd. | | | 4.9% | |

| |

Wilcon Depot, Inc. | | | 4.5% | |

| |

NU Holdings Ltd. | | | 4.4% | |

| |

Sea Ltd., ADR | | | 4.1% | |

| * | As of March 31, 2023, there were 34 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

| † | Also includes Other Assets & Liabilities. |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

13

| | |

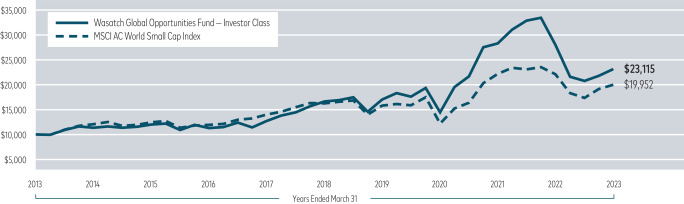

| Wasatch Global Opportunities Fund (WAGOX / WIGOX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Global Opportunities Fund is managed by a team of Wasatch portfolio managers led by JB Taylor, Ajay Krishnan, Ken Applegate and Paul Lambert.

| | | | |

JB Taylor Lead Portfolio Manager

Ken Applegate, CFA Portfolio Manager | |

Ajay Krishnan, CFA Lead Portfolio Manager

Paul Lambert Portfolio Manager | | OVERVIEW Global equities notched gains for the first quarter of 2023 but were volatile. Stocks started the year on an upswing, but signs of persistent inflation weighed on equity markets in February. Volatility continued in March after a few high-profile bank failures led to concerns about the banking industry. In this environment, the Wasatch Global |

|

Opportunities Fund — Investor Class gained 6.32%, outperforming its benchmark, the MSCI AC (All Country) World Small Cap Index, which was up 4.24%.

DETAILS OF THE QUARTER

The most significant contributor to the Fund’s performance during the first quarter was BayCurrent Consulting, Inc., a Japan-based business management and information-technology (IT) consultant. Demand for digital transformation projects, a key area of focus for BayCurrent, continues to be strong, which has helped lift the company’s stock in recent months. Recent results indicate that our thesis on the company continues to play out. Japan is behind many countries when it comes to digitalization. The pandemic and work-from-home environment underscored its need to catch up. As Japanese enterprises undertake large-scale digitalization projects, we believe domestic IT consultants such as BayCurrent have a strong home-country advantage relative to global consulting firms.

ASPEED Technology, Inc. was another top contributor. Headquartered in Taiwan, the company is a fabless designer of integrated circuits specializing in areas that include server management and audio-visual extensions. An upswell of enthusiasm during February about artificial intelligence (AI) helped push ASPEED’s stock price higher. Investors reckoned the massive data-processing requirements of AI’s large language models may lead to increased demand for the company’s chips.

Stock-market jitters in India and negative sentiment toward banks in March helped produce one of the Fund’s biggest detractors from performance during the quarter — AU Small Finance Bank Ltd. The company targets unbanked and

underbanked low- and middle-income borrowers in India. While the stocks of many banking companies were down in the first quarter, we think AU Small Finance’s risk profile is quite different from some of the banks that failed. Operating in an emerging market means its management team is used to navigating a volatile interest-rate environment. As such, the bank has an asset-liability management structure well-suited for fluctuating interest rates. Further, AU Small Finance withstood a severe liquidity crisis in India in 2018, which presented a different set of circumstances but was arguably a more challenging crisis than what developed-market banks face today.

Abcam PLC was another detractor. The stock of the British health-care company was down after it reported annual revenue that was below consensus expectations, due in part to the implementation of a new enterprise resource planning (ERP) system, which caused an order backlog. Despite these near-term setbacks, we don’t believe anything has structurally changed for the firm. Abcam provides biological reagents and tools that are essential to a wide range of fields, including drug discovery, diagnostics and basic research. We expect high demand for these products as health-care innovation pushes forward. In addition, we believe profit margins will expand after an extended period of investment for the firm.

OUTLOOK

So far, central banks have ring-fenced banking industry turmoil, limiting the damage to just a few troubled institutions. However, it’s hard to predict whether more bank failures will occur or how severe the fallout from those failures would be. Nevertheless, we feel good about the prospects of the banks we hold. Within our portfolio, we own just two banks, both of which have a risk profile we believe is quite different from the banks that failed.

While we feel good about our bank holdings, we continue to think about the knock-on effects of banking turmoil. Already, at least two things seem certain. First, trouble for banks will be another drag on economic growth. Second, the cost of capital for businesses is poised to increase.

We believe an environment of slower growth and rising capital costs should favor the types of high-quality companies in which Wasatch invests. Our investment process focuses on firms with strong balance sheets, low levels of debt and typically, a steady history of earnings growth and cash flow generation. These self-funded businesses can continue to carry out their growth plans at a time when rising capital costs may force weaker competitors to pare back. We believe this should set our firms up for better growth in the years to come.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

14

| | |

| Wasatch Global Opportunities Fund (WAGOX / WIGOX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | Six Months

(Not annualized) | | 1 Year | | 5 Years | | 10 Years |

| | | | |

Global Opportunities (WAGOX) — Investor | | | | 11.56% | | | | | -17.43% | | | | | 6.85% | | | | | 8.74% | |

| | | | |

Global Opportunities (WIGOX) — Institutional | | | | 11.75% | | | | | -17.28% | | | | | 7.06% | | | | | 8.87% | |

| | | | |

MSCI AC World Small Cap Index | | | | 15.14% | | | | | -9.57% | | | | | 4.19% | | | | | 7.15% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

As of the January 31, 2023 prospectus, the Total Annual Fund Operating Expenses for the Wasatch Global Opportunities Fund are Investor Class: 1.50% / Institutional Class — Gross: 1.38%, Net: 1.35%. The expense ratio shown elsewhere in this report may be different. Net expenses are based on Fund expenses, net of waivers and reimbursements. See the prospectus for additional information regarding Fund expenses.

Wasatch will deduct a 2.00% redemption fee on Fund shares held 60 days or less. Performance data do not reflect the deduction of fees, including sales charges, or the taxes you would pay on fund distributions or the redemption of fund shares. Fees and taxes, if reflected, would reduce the performance quoted. Wasatch does not charge any sales fees. For more complete information including charges, risks and expenses, read the prospectus carefully.

Performance for the Institutional Class prior to 2/1/2016 is based on the performance of the Investor Class. Performance of the Fund’s Institutional Class prior to 2/1/2016 uses the actual expenses of the Fund’s Investor Class without any adjustments. For any such period of time, the performance of the Fund’s Institutional Class would have been substantially similar to, yet higher than, the performance of the Fund’s Investor Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses.

Investing in small and micro cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus.

TOP 10 EQUITY HOLDINGS*

| | | | |

| |

| Company | | % of Net Assets | |

| |

BayCurrent Consulting, Inc. | | | 5.8% | |

| |

AU Small Finance Bank Ltd. | | | 3.9% | |

| |

Ensign Group, Inc. | | | 3.7% | |

| |

Five Below, Inc. | | | 3.1% | |

| |

HealthEquity, Inc. | | | 3.1% | |

| | | | |

| |

| Company | | % of Net Assets | |

| |

Globant SA | | | 2.9% | |

| |

Abcam PLC | | | 2.8% | |

| |

Voltronic Power Technology Corp. | | | 2.7% | |

| |

Silergy Corp. | | | 2.6% | |

| |

Saia, Inc. | | | 2.4% | |

| * | As of March 31, 2023, there were 64 holdings in the Fund. Foreign currency contracts, written options and repurchase agreements, if any, are not included in the number of holdings. Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk. |

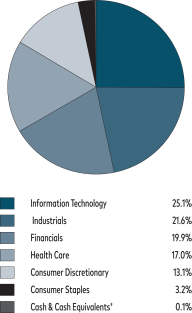

SECTOR BREAKDOWN**

| ** | Excludes securities sold short, if any. |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

Past performance does not predict future performance. The graph above does not reflect the deduction of fees, sales charges, or taxes that you would pay on fund distributions or the redemption of fund shares. Wasatch does not charge any sales fees.

15

| | |

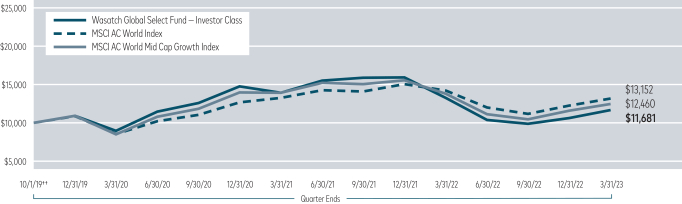

| Wasatch Global Select Fund (WAGSX / WGGSX) | | MARCH 31, 2023 (Unaudited) |

Management Discussion

The Wasatch Global Select Fund is managed by a team of Wasatch portfolio managers led by Ken Applegate, Paul Lambert, Linda Lasater and Mike Valentine.

| | | | |

Ken Applegate, CFA Portfolio Manager

Linda Lasater, CFA Portfolio Manager | |

Paul Lambert Portfolio Manager

Mike Valentine Portfolio Manager | | OVERVIEW Global equities notched gains for the quarter but were volatile. Stocks started the year on an upswing, but signs of persistent inflation weighed on equity markets in February. Volatility continued in March after a few high-profile bank failures led to concerns about the banking industry. |

In this environment, the Wasatch Global Select Fund — Investor Class gained 9.68%, outperforming the benchmark MSCI AC (All Country) World Index, which was up 7.31%.

DETAILS OF THE QUARTER

The most significant contributor to the Fund’s performance during the quarter was BayCurrent Consulting, Inc., a Japan-based business management and information-technology (IT) consultant. Demand for digital transformation projects, a key area of focus for BayCurrent, continues to be strong, which has helped lift the company’s stock in recent months. Recent results indicate that our thesis on the company continues to play out. Japan is behind many countries when it comes to digitalization. The pandemic and work-from-home environment underscored its need to catch up. As Japanese enterprises undertake large-scale digitalization projects, we believe domestic IT consultants such as BayCurrent have a strong home-country advantage relative to global consulting firms.

MercadoLibre, Inc. was another large contributor. The company operates an online e-commerce, payments, and credit system in 18 Latin American countries. It has been called “the Amazon of Latin America” due to its leadership in the region’s fast-growing online marketplace. MercadoLibre experienced considerable growth in 2022, with fourth-quarter revenue up 56.5% from the same period in 2021 and operating income jumping from $24 million to $349 million. MercadoLibre also benefited as an important rival in Brazil was engulfed in an accounting scandal that led to the departure of its CEO and CFO.

The largest detractor from Fund performance during the quarter was DiaSorin SpA, an Italian health-diagnostics company. The company benefited from heightened demand for its tests used to detect Covid-19. Now that the world is past the height of the pandemic, DiaSorin needs to offset the decline in Covid-19 tests with other diagnostics. This has weighed on the stock recently, but we still like DiaSorin’s long-term growth potential and recurring-revenue operating model. The company is a leader in specialty disease testing in Europe, and we believe an acquisition it made in 2021 positions DiaSorin to take share in the U.S. disease-testing market.

Abcam PLC was another detractor. The stock of the British health-care company was down after it reported annual revenue that was below consensus expectations, due in part to the implementation of a new enterprise resource planning (ERP) system, an undertaking that caused an order backlog in September and October. While these were near-term setbacks, we don’t believe anything has structurally changed for the firm. Abcam provides biological reagents and tools that are essential to a wide range of fields, including drug discovery, diagnostics and basic research. We expect high demand for these products as health-care innovation pushes forward. In addition, we believe profit margins will expand after an extended period of investment for the firm.

OUTLOOK

So far, central banks have ring-fenced banking industry turmoil, limiting the damage to just a few troubled institutions. However, it’s hard to predict whether more bank failures will occur or how severe the fallout from those failures would be. What we can say, however, is that we feel good about the prospects of the banks we do hold. Within our portfolio, we own just two banks, both of which have a risk profile we believe is quite different from the banks that failed.

While we feel good about our bank holdings, we continue to think about the knock-on effects of banking turmoil. Already, at least two things seem certain. First, trouble for banks will be another drag on economic growth. Second, the cost of capital for businesses is poised to increase.

We believe an environment of slower growth and rising capital costs should favor the types of high-quality companies in which Wasatch invests. Our investment process focuses on firms with strong balance sheets, low levels of debt and typically, a steady history of earnings growth and cash flow generation. These self-funded businesses can continue to carry out their growth plans at a time when rising capital costs may force weaker competitors to pare back. We believe this should set our firms up for better growth in the years to come.

Thank you for the opportunity to manage your assets.

Current and future holdings are subject to risk.

16

| | |

| Wasatch Global Select Fund (WAGSX / WGGSX) | | MARCH 31, 2023 (Unaudited) |

Portfolio Summary

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | | | | | | | | |

| | | |

| Name | | Six Months

(Not annualized) | | 1 Year | | Since Inception

10/1/2019 |

| | | |

Global Select (WAGSX) — Investor | | | | 18.37% | | | | | -11.73% | | | | | 4.54% | |

| | | |

Global Select (WGGSX) — Institutional | | | | 18.48% | | | | | -11.44% | | | | | 4.91% | |

| | | |

MSCI AC World Index | | | | 17.78% | | | | | -7.44% | | | | | 8.15% | |

| | | |

MSCI AC World Mid Cap Growth Index | | | | 18.92% | | | | | -9.49% | | | | | 6.49% | |

Data show past performance, which is not indicative of future performance. Current performance may be lower or higher than the performance quoted. To obtain the most recent month-end performance data available, please visit wasatchglobal.com. The Advisor may absorb certain Fund expenses, without which total returns would have been lower. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.