UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-01716

AB CAP FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)221-5672

Date of fiscal year end: November 30, 2018

Date of reporting period: November 30, 2018

ITEM 1. REPORTS TO STOCKHOLDERS.

NOV 11.30.18

ANNUAL REPORT

AB ALL CHINA EQUITY PORTFOLIO

Beginning January 1, 2021, as permitted by new regulations adopted by the Securities and Exchange Commission, the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website address to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling the Fund at (800) 221 5672.

You may elect to receive all future reports in paper form free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports; if you invest directly with the Fund, you can call the Fund at (800) 221 5672. Your election to receive reports in paper form will apply to all funds held in your account with your financial intermediary or, if you invest directly, to all AB Mutual Funds you hold.

A discussion of the Fund’s investment performance is not included in this report. AllianceBernstein L.P. would like to thank you for your interest in the Fund.

| | |

| |

| Investment Products Offered | | • Are Not FDIC Insured• May Lose Value• Are Not Bank Guaranteed |

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.abfunds.com or contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year. The Fund’s portfolio holdings reports are available on the Commission’s website at www.sec.gov. The Fund’s portfolio holdings reports may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC 0330. AB publishes full portfolio holdings for the Fund monthly at www.abfunds.com.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

EXPENSE EXAMPLE

(unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 1 |

EXPENSE EXAMPLE(continued)

| | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

7/25/2018+ | | | Ending

Account Value

11/30/2018 | | | Expenses Paid

During Period* | | | Annualized

Expense Ratio* | |

| Class A | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 837.00 | | | $ | 4.83 | | | | 1.50 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,017.55 | | | $ | 7.59 | | | | 1.50 | % |

| Advisor Class | | | | | | | | | | | | | | | | |

Actual | | $ | 1,000 | | | $ | 838.00 | | | $ | 4.03 | | | | 1.25 | % |

Hypothetical** | | $ | 1,000 | | | $ | 1,018.80 | | | $ | 6.33 | | | | 1.25 | % |

| + | Commencement of operations. |

| * | Actual expenses paid are based on the period from July 25, 2018 (commencement of operations) and are equal to the Portfolio’s annualized expense ratio, multiplied by the average account value over the period multiplied by 128/365 (to reflect since the inception period). Hypothetical expenses are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

| ** | Assumes 5% annual return before expenses. |

| | |

| |

| 2 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

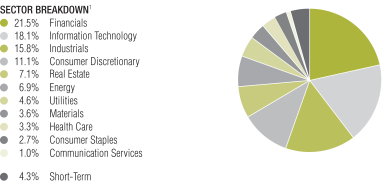

PORTFOLIO SUMMARY

November 30, 2018(unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $36.8

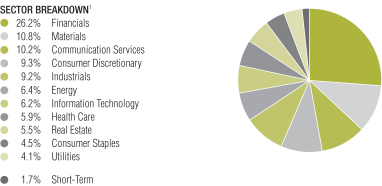

| 1 | All data are as of November 30, 2018. The Fund’s sector and country breakdowns are expressed as a percentage of total investments and may vary over time. |

Please note: The sector classifications presented herein are based on the Global Industry Classification Standard (GICS) which was developed by Morgan Stanley Capital International and Standard & Poor’s. The components are divided into sector, industry group, and industrysub-indices as classified by the GICS for each of the market capitalization indices in the broad market. These sector classifications are broadly defined. The “Portfolio of Investments” section of the report reflects more specific industry information and is consistent with the investment restrictions discussed in the Update Fund’s prospectus.

| | |

| |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 3 |

PORTFOLIO SUMMARY(continued)

November 30, 2018(unaudited)

TEN LARGEST HOLDINGS1

| | | | | | | | |

| Company | | U.S. $ Value | | | Percent of

Net Assets | |

| Tencent Holdings Ltd. | | $ | 2,824,491 | | | | 7.7 | % |

| Ping An Insurance Group Co. of China Ltd. – Class A | | | 2,608,699 | | | | 7.1 | |

| Alibaba Group Holding Ltd. (Sponsored ADR) | | | 2,421,747 | | | | 6.6 | |

| China Construction Bank Corp. – Class H | | | 2,254,899 | | | | 6.1 | |

| Huaxin Cement Co., Ltd. | | | 1,303,544 | | | | 3.5 | |

| China Petroleum & Chemical Corp. – Class H | | | 1,188,131 | | | | 3.2 | |

| PetroChina Co., Ltd. – Class H | | | 1,162,236 | | | | 3.2 | |

| Anhui Conch Cement Co., Ltd. – Class A | | | 1,110,251 | | | | 3.0 | |

| CITIC Securities Co., Ltd. | | | 988,532 | | | | 2.7 | |

| Shanghai Pharmaceuticals Holding Co., Ltd. – Class H | | | 935,174 | | | | 2.5 | |

| | $ | 16,797,704 | | | | 45.6 | % |

| | |

| 4 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

PORTFOLIO OF INVESTMENTS

November 30, 2018

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| |

| | | | | | | | |

COMMON STOCKS – 97.9% | | | | | | | | |

Financials – 26.1% | | | | | | | | |

Banks – 13.7% | | | | | | | | |

Bank of Hangzhou Co., Ltd. – Class A | | | 340,140 | | | $ | 379,331 | |

Bank of Nanjing Co., Ltd. | | | 405,700 | | | | 409,194 | |

BOC Hong Kong Holdings Ltd. | | | 45,500 | | | | 178,152 | |

China CITIC Bank Corp., Ltd. – Class H | | | 1,182,000 | | | | 752,865 | |

China Construction Bank Corp. – Class H | | | 2,641,000 | | | | 2,254,899 | |

China Minsheng Banking Corp., Ltd. – Class H | | | 747,000 | | | | 553,212 | |

Industrial Bank Co., Ltd. – Class A | | | 230,100 | | | | 530,596 | |

| | | | | | | | |

| | | | | | | 5,058,249 | |

| | | | | | | | |

Capital Markets – 3.6% | | | | | | | | |

CITIC Securities Co., Ltd. | | | 405,200 | | | | 988,532 | |

Haitong Securities Co., Ltd. – Class H | | | 330,800 | | | | 344,902 | |

| | | | | | | | |

| | | | | | | 1,333,434 | |

| | | | | | | | |

Insurance – 8.8% | | | | | | | | |

China Taiping Insurance Holdings Co., Ltd. | | | 100,400 | | | | 334,825 | |

PICC Property & Casualty Co., Ltd. – Class H | | | 276,000 | | | | 284,703 | |

Ping An Insurance Group Co. of China Ltd. – Class A | | | 282,600 | | | | 2,608,699 | |

| | | | | | | | |

| | | | | | | 3,228,227 | |

| | | | | | | | |

| | | | | | | 9,619,910 | |

| | | | | | | | |

Materials – 10.8% | | | | | | | | |

Chemicals – 3.2% | | | | | | | | |

Luxi Chemical Group Co., Ltd. – Class A | | | 207,500 | | | | 330,617 | |

Shandong Hualu Hengsheng Chemical Co., Ltd. | | | 213,200 | | | | 391,308 | |

Zhejiang Longsheng Group Co., Ltd. – Class A | | | 346,090 | | | | 454,583 | |

| | | | | | | | |

| | | | | | | 1,176,508 | |

| | | | | | | | |

Construction Materials – 7.6% | | | | | | | | |

Anhui Conch Cement Co., Ltd. – Class A | | | 240,600 | | | | 1,110,251 | |

Huaxin Cement Co., Ltd. | | | 692,480 | | | | 1,303,544 | |

West China Cement Ltd. | | | 2,348,000 | | | | 370,593 | |

| | | | | | | | |

| | | | | | | 2,784,388 | |

| | | | | | | | |

| | | | | | | 3,960,896 | |

| | | | | | | | |

Communication Services – 10.2% | | | | | | | | |

Diversified Telecommunication Services – 1.6% | | | | | | | | |

China Unicom Hong Kong Ltd. | | | 506,000 | | | | 590,921 | |

| | | | | | | | |

| | |

Interactive Media & Services – 8.6% | | | | | | | | |

Baidu, Inc. (Sponsored ADR)(a) | | | 1,709 | | | | 321,771 | |

Tencent Holdings Ltd. | | | 70,650 | | | | 2,824,491 | |

| | | | | | | | |

| | | | | | | 3,146,262 | |

| | | | | | | | |

| | | | | | | 3,737,183 | |

| | | | | | | | |

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 5 |

PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| |

| | | | | | | | |

Consumer Discretionary – 9.2% | | | | | | | | |

Hotels, Restaurants & Leisure – 0.9% | | | | | | | | |

China International Travel Service Corp., Ltd. – Class A | | | 41,500 | | | $ | 332,057 | |

| | | | | | | | |

| | |

Household Durables – 0.8% | | | | | | | | |

Hisense Home Appliances Group Co., Ltd. – Class H | | | 391,000 | | | | 304,118 | |

| | | | | | | | |

| | |

Internet & Direct Marketing Retail – 6.6% | | | | | | | | |

Alibaba Group Holding Ltd. (Sponsored ADR)(a) | | | 15,055 | | | | 2,421,747 | |

| | | | | | | | |

| | |

Textiles, Apparel & Luxury Goods – 0.9% | | | | | | | | |

Li Ning Co., Ltd.(a) | | | 322,500 | | | | 347,022 | |

| | | | | | | | |

| | | | | | | 3,404,944 | |

| | | | | | | | |

Industrials – 9.2% | | | | | | | | |

Construction & Engineering – 2.1% | | | | | | | | |

China Railway Construction Corp., Ltd. – Class H | | | 276,000 | | | | 354,525 | |

China State Construction Engineering Corp., Ltd. | | | 492,300 | | | | 410,439 | |

| | | | | | | | |

| | | | | | | 764,964 | |

| | | | | | | | |

Machinery – 4.1% | | | | | | | | |

Guangxi Liugong Machinery Co., Ltd. – Class A | | | 584,780 | | | | 563,124 | |

Sany Heavy Industry Co., Ltd. | | | 489,500 | | | | 569,433 | |

Weichai Power Co., Ltd. – Class A | | | 344,796 | | | | 375,305 | |

| | | | | | | | |

| | | | | | | 1,507,862 | |

| | | | | | | | |

Road & Rail – 1.0% | | | | | | | | |

Daqin Railway Co., Ltd. – Class A | | | 327,300 | | | | 364,457 | |

| | | | | | | | |

| | |

Trading Companies & Distributors – 1.1% | | | | | | | | |

BOC Aviation Ltd.(b) | | | 53,300 | | | | 411,786 | |

| | | | | | | | |

| | |

Transportation Infrastructure – 0.9% | | | | | | | | |

Yuexiu Transport Infrastructure Ltd. | | | 458,000 | | | | 343,767 | |

| | | | | | | | |

| | | | | | | 3,392,836 | |

| | | | | | | | |

Energy – 6.4% | | | | | | | | |

Oil, Gas & Consumable Fuels – 6.4% | | | | | | | | |

China Petroleum & Chemical Corp. – Class H | | | 1,388,000 | | | | 1,188,131 | |

PetroChina Co., Ltd. – Class H | | | 1,664,000 | | | | 1,162,236 | |

| | | | | | | | |

| | | | | | | 2,350,367 | |

| | | | | | | | |

Information Technology – 6.1% | | | | | | | | |

Electronic Equipment, Instruments & Components – 0.7% | | | | | | | | |

Universal Scientific Industrial Shanghai Co., Ltd. – Class A | | | 194,700 | | | | 256,876 | |

| | | | | | | | |

| | |

| 6 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| |

| | | | | | | | |

IT Services – 0.8% | | | | | | | | |

Wonders Information Co., Ltd. – Class A | | | 155,600 | | | $ | 279,135 | |

| | | | | | | | |

| | |

Semiconductors & Semiconductor Equipment – 1.6% | | | | | | | | |

Hua Hong Semiconductor Ltd.(b) | | | 278,000 | | | | 593,945 | |

| | | | | | | | |

| | |

Software – 1.1% | | | | | | | | |

Beijing Jetsen Technology Co., Ltd. – Class A | | | 234,199 | | | | 163,148 | |

Shanghai 2345 Network Holding Group Co., Ltd. – Class A | | | 465,800 | | | | 260,599 | |

| | | | | | | | |

| | | | | | | 423,747 | |

| | | | | | | | |

Technology Hardware, Storage & Peripherals – 1.9% | | | | | | | | |

Lenovo Group Ltd. | | | 968,000 | | | | 702,427 | |

| | | | | | | | |

| | | | | | | 2,256,130 | |

| | | | | | | | |

Health Care – 5.9% | | | | | | | | |

Health Care Providers & Services – 2.5% | | | | | | | | |

Shanghai Pharmaceuticals Holding Co., Ltd. – Class H | | | 377,800 | | | | 935,174 | |

| | | | | | | | |

| | |

Pharmaceuticals – 3.4% | | | | | | | | |

CSPC Pharmaceutical Group Ltd. | | | 166,000 | | | | 337,593 | |

Jiangsu Hengrui Medicine Co., Ltd. | | | 65,690 | | | | 622,729 | |

Sichuan Kelun Pharmaceutical Co., Ltd. – Class A | | | 79,600 | | | | 278,027 | |

| | | | | | | | |

| | | | | | | 1,238,349 | |

| | | | | | | | |

| | | | | | | 2,173,523 | |

| | | | | | | | |

Real Estate – 5.4% | | | | | | | | |

Real Estate Management & Development – 5.4% | | | | | | | | |

China Resources Land Ltd. | | | 138,000 | | | | 513,707 | |

CIFI Holdings Group Co., Ltd. | | | 736,000 | | | | 371,761 | |

Future Holdings Co., Ltd. – Class A | | | 100,800 | | | | 400,264 | |

RiseSun Real Estate Development Co., Ltd. | | | 219,200 | | | | 265,895 | |

Times China Holdings Ltd. | | | 484,000 | | | | 453,891 | |

| | | | | | | | |

| | | | | | | 2,005,518 | |

| | | | | | | | |

Consumer Staples – 4.5% | | | | | | | | |

Beverages – 2.7% | | | | | | | | |

Beijing Shunxin Agriculture Co., Ltd. – Class A | | | 87,700 | | | | 440,980 | |

Wuliangye Yibin Co., Ltd. – Class A | | | 73,100 | | | | 555,213 | |

| | | | | | | | |

| | | | | | | 996,193 | |

| | | | | | | | |

Food Products – 1.8% | | | | | | | | |

Fujian Sunner Development Co., Ltd. – Class A(a) | | | 145,162 | | | | 363,713 | |

Heilongjiang Agriculture Co., Ltd. | | | 226,200 | | | | 287,246 | |

| | | | | | | | |

| | | | | | | 650,959 | |

| | | | | | | | |

| | | | | | | 1,647,152 | |

| | | | | | | | |

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 7 |

PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Company | | Shares | | | U.S. $ Value | |

| |

| | | | | | | | |

Utilities – 4.1% | | | | | | | | |

Gas Utilities – 2.1% | | | | | | | | |

China Resources Gas Group Ltd. | | | 92,000 | | | $ | 372,829 | |

ENN Energy Holdings Ltd. | | | 46,000 | | | | 413,924 | |

| | | | | | | | |

| | | | | | | 786,753 | |

| | | | | | | | |

Independent Power and Renewable Electricity Producers – 2.0% | | | | | | | | |

Huadian Power International Corp., Ltd. – Class H | | | 876,000 | | | | 376,710 | |

SDIC Power Holdings Co., Ltd. – Class A | | | 338,800 | | | | 356,771 | |

| | | | | | | | |

| | | | | | | 733,481 | |

| | | | | | | | |

| | | | | | | 1,520,234 | |

| | | | | | | | |

Total Common Stocks

(cost $36,920,240) | | | | | | | 36,068,693 | |

| | | | | | | | |

| | | | | | | | |

SHORT-TERM INVESTMENTS – 1.7% | | | | | | | | |

Investment Companies – 1.7% | | | | | | | | |

AB Fixed Income Shares, Inc. – Government Money Market Portfolio – Class AB, 2.13%(c)(d)(e)

(cost $607,265) | | | 607,265 | | | | 607,265 | |

| | | | | | | | |

| | |

Total Investments – 99.6%

(cost $37,527,505) | | | | | | | 36,675,958 | |

Other assets less liabilities – 0.4% | | | | | | | 154,052 | |

| | | | | | | | |

| | |

Net Assets – 100.0% | | | | | | $ | 36,830,010 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (b) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities are considered restricted, but liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers. At November 30, 2018, the aggregate market value of these securities amounted to $1,005,731 or 2.7% of net assets. |

| (c) | To obtain a copy of the fund’s shareholder report, please go to the Securities and Exchange Commission’s website at www.sec.gov, or call

AB at (800)227-4618. |

| (d) | Affiliated investments. |

| (e) | The rate shown represents the7-day yield as of period end. |

Glossary:

ADR – American Depositary Receipt

See notes to financial statements.

| | |

| 8 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

STATEMENT OF ASSETS & LIABILITIES

November 30, 2018

| | | | |

| Assets | | | | |

Investments in securities, at value | | | | |

Unaffiliated issuers (cost $36,920,240) | | $ | 36,068,693 | |

Affiliated issuers (cost $607,265) | | | 607,265 | |

Foreign currencies, at value (cost $217,547) | | | 217,021 | |

Receivable for capital stock sold | | | 318,384 | |

Deferred offering cost | | | 82,710 | |

Receivable from Adviser | | | 72,592 | |

Affiliated dividends receivable | | | 2,431 | |

| | | | |

Total assets | | | 37,369,096 | |

| | | | |

| Liabilities | | | | |

Payable for investment securities purchased and foreign currency transactions | | | 367,755 | |

Custody fee payable | | | 81,713 | |

Audit and tax fee payable | | | 41,940 | |

Transfer Agent fee payable | | | 1,500 | |

Distribution fee payable | | | 139 | |

Due to Custodian | | | 23 | |

Accrued expenses and other liabilities | | | 46,016 | |

| | | | |

Total liabilities | | | 539,086 | |

| | | | |

Net Assets | | $ | 36,830,010 | |

| | | | |

| Composition of Net Assets | | | | |

Capital stock, at par | | $ | 440 | |

Additional paid-in capital | | | 38,749,502 | |

Accumulated loss | | | (1,919,932 | ) |

| | | | |

| | $ | 36,830,010 | |

| | | | |

Net Asset Value Per Share—11 billion shares of capital stock authorized, $.0001 par value

| | | | | | | | | | | | |

| Class | | Net Assets | | | Shares Outstanding | | | Net Asset Value | |

| |

| A | | $ | 685,173 | | | | 81,858 | | | $ | 8.37 | * |

| |

| Advisor | | $ | 36,144,837 | | | | 4,314,443 | | | $ | 8.38 | |

| |

| * | The maximum offering price per share for Class A shares was $8.74 which reflects a sales charge of 4.25%. |

See notes to financial statements.

| | |

| |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 9 |

STATEMENT OF OPERATIONS

Period from July 25, 2018(a) to November 30, 2018

| | | | | | | | |

| Investment Income | | | | | | | | |

Dividends | | | | | | | | |

Unaffiliated issuers (net of foreign taxes withheld of $2,879) | | $ | 49,478 | | | | | |

Affiliated issuers | | | 5,357 | | | $ | 54,835 | |

| | | | | | | | |

| Expenses | | | | | | | | |

Advisory fee (see Note B) | | | 58,473 | | | | | |

Transfer agency—Class A | | | 140 | | | | | |

Transfer agency—Advisor Class | | | 7,026 | | | | | |

Distribution fee—Class A | | | 455 | | | | | |

Custodian | | | 86,038 | | | | | |

Audit and tax | | | 41,940 | | | | | |

Amortization of offering expenses | | | 35,574 | | | | | |

Administrative | | | 18,856 | | | | | |

Legal | | | 18,134 | | | | | |

Registration fees | | | 14,028 | | | | | |

Directors’ fees | | | 12,425 | | | | | |

Printing | | | 4,100 | | | | | |

Miscellaneous | | | 17,961 | | | | | |

| | | | | | | | |

Total expenses | | | 315,150 | | | | | |

Less: expenses waived and reimbursed by the Adviser (see Note B) | | | (237,812 | ) | | | | |

| | | | | | | | |

Net expenses | | | | | | | 77,338 | |

| | | | | | | | |

Net investment loss | | | | | | | (22,503 | ) |

| | | | | | | | |

| Realized and Unrealized Gain (Loss) on Investment and Foreign Currency Transactions | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | |

Investment transactions | | | | | | | (1,031,394 | ) |

Futures | | | | | | | (31,576 | ) |

Foreign currency transactions | | | | | | | 2,862 | |

Net change in unrealized appreciation/depreciation on: | | | | | | | | |

Investments | | | | | | | (851,547 | ) |

Foreign currency denominated assets and liabilities | | | | | | | (761 | ) |

| | | | | | | | |

Net loss on investment and foreign currency transactions | | | | | | | (1,912,416 | ) |

| | | | | | | | |

Net Decrease in Net Assets from Operations | | | | | | $ | (1,934,919 | ) |

| | | | | | | | |

| (a) | Commencement of operations. |

See notes to financial statements.

| | |

| 10 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

STATEMENT OF CHANGES IN NET ASSETS

| | | | |

| | | July 25, 2018(a)

to

November 30, 2018 | |

| Increase (Decrease) in Net Assets from Operations | | | | |

Net investment loss | | $ | (22,503 | ) |

Net realized loss on investment and foreign currency transactions | | | (1,060,108 | ) |

Net change in unrealized appreciation/depreciation on investments and foreign currency denominated assets and liabilities | | | (852,308 | ) |

| | | | |

Net decrease in net assets from operations | | | (1,934,919 | ) |

| Capital Stock Transactions | | | | |

Net increase | | | 38,764,929 | |

| | | | |

Total increase | | | 36,830,010 | |

| Net Assets | | | | |

Beginning of period | | | – 0 | – |

| | | | |

End of period | | $ | 36,830,010 | |

| | | | |

| (a) | Commencement of operations. |

See notes to financial statements.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 11 |

NOTES TO FINANCIAL STATEMENTS

November 30, 2018

NOTE A

Significant Accounting Policies

AB Cap Fund, Inc. (the “Company”), which is a Maryland corporation, is registered under the Investment Company Act of 1940 as an open-end management investment company. The Company operates as a series company comprised of 29 portfolios currently in operation. Each portfolio is considered to be a separate entity for financial reporting and tax purposes. This report relates only to the AB All China Equity Portfolio (the “Fund”), a non-diversified portfolio. The Fund commenced operations on July 25, 2018. The Fund has authorized the issuance of Class A, Class B, Class C, Advisor Class, Class R, Class K, Class I, Class Z, Class T, Class 1 and Class 2 shares. Class B, Class C, Class R, Class K, Class I, Class Z, Class T, Class 1 and Class 2 shares are not currently being offered. Class A shares are sold with a front-end sales charge of up to 4.25% for purchases not exceeding $1,000,000. With respect to purchases of $1,000,000 or more, Class A shares redeemed within one year of purchase may be subject to a contingent deferred sales charge of 1%. Advisor Class shares are sold without an initial or contingent deferred sales charge and are not subject to ongoing distribution expenses. All eleven classes of shares have identical voting, dividend, liquidation and other rights, except that the classes bear different distribution and transfer agency expenses. Each class has exclusive voting rights with respect to its distribution plan. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”), which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The Fund is an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies. The following is a summary of significant accounting policies followed by the Fund.

1. Security Valuation

Portfolio securities are valued at their current market value determined on the basis of market quotations or, if market quotations are not readily available or are deemed unreliable, at “fair value” as determined in accordance with procedures established by and under the general supervision of the Company’s Board of Directors (the “Board”).

In general, the market values of securities which are readily available and deemed reliable are determined as follows: securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities

| | |

| 12 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

exchange. If there has been no sale on such day, the securities are valued at the last traded price from the previous day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed or over the counter (“OTC”) market put or call options are valued at the mid level between the current bid and ask prices. If either a current bid or current ask price is unavailable, AllianceBernstein L.P. (the “Adviser”) will have discretion to determine the best valuation (e.g., last trade price in the case of listed options); open futures are valued using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used; U.S. Government securities and any other debt instruments having 60 days or less remaining until maturity are generally valued at market by an independent pricing vendor, if a market price is available. If a market price is not available, the securities are valued at amortized cost. This methodology is commonly used for short term securities that have an original maturity of 60 days or less, as well as short term securities that had an original term to maturity that exceeded 60 days. In instances when amortized cost is utilized, the Valuation Committee (the “Committee”) must reasonably conclude that the utilization of amortized cost is approximately the same as the fair value of the security. Such factors the Committee will consider include, but are not limited to, an impairment of the creditworthiness of the issuer or material changes in interest rates. Fixed-income securities, including mortgage-backed and asset-backed securities, may be valued on the basis of prices provided by a pricing service or at a price obtained from one or more of the major broker-dealers. In cases where broker/dealer quotes are obtained, the Adviser may establish procedures whereby changes in market yields or spreads are used to adjust, on a daily basis, a recently obtained quoted price on a security; swaps and other derivatives are valued daily, primarily using independent pricing services, independent pricing models using market inputs, as well as third party broker-dealers or counterparties. Open end mutual funds are valued at the closing net asset value per share, while exchange traded funds are valued at the closing market price per share.

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value as deemed appropriate by the Adviser. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Fund may use fair value pricing for securities primarily traded innon-U.S. markets because most foreign markets close well before the Fund values its securities at 4:00 p.m., Eastern Time. The earlier close of these foreign markets gives rise to the

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 13 |

NOTES TO FINANCIAL STATEMENTS(continued)

possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities. To account for this, the Fund generally values many of its foreign equity securities using fair value prices based on third party vendor modeling tools to the extent available.

2. Fair Value Measurements

In accordance with U.S. GAAP regarding fair value measurements, fair value is defined as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. U.S. GAAP establishes a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability (including those valued based on their market values as described in Note A.1 above). Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions that market participants would use in pricing the asset or liability based on the best information available in the circumstances. Each investment is assigned a level based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| | • | | Level 1—quoted prices in active markets for identical investments |

| | • | | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| | • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

Where readily available market prices or relevant bid prices are not available for certain equity investments, such investments may be valued based on similar publicly traded investments, movements in relevant indices since last available prices or based upon underlying company fundamentals and comparable company data (such as multiples to earnings or other multiples to equity). Where an investment is valued using an observable input such as another publicly traded security, the investment will be classified as Level 2. If management determines that an adjustment is appropriate based on restrictions on resale, illiquidity or uncertainty, and such adjustment is a significant component of the valuation, the investment will be classified as Level 3. An investment will also be classified as Level 3 where management uses company fundamentals and other significant inputs to determine the valuation.

| | |

| 14 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

The following table summarizes the valuation of the Fund’s investments by the above fair value hierarchy levels as of November 30, 2018:

| | | | | | | | | | | | | | | | |

Investments in Securities | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets: | |

Common Stocks: | | | | | | | | | | | | | | | | |

Financials | | $ | – 0 | – | | $ | 9,619,910 | | | $ | – 0 | – | | $ | 9,619,910 | |

Materials | | | – 0 | – | | | 3,960,896 | | | | – 0 | – | | | 3,960,896 | |

Communication Services | | | 321,771 | | | | 3,415,412 | | | | – 0 | – | | | 3,737,183 | |

Consumer Discretionary | | | 2,421,747 | | | | 983,197 | | | | – 0 | – | | | 3,404,944 | |

Industrials | | | – 0 | – | | | 3,392,836 | | | | – 0 | – | | | 3,392,836 | |

Energy | | | – 0 | – | | | 2,350,367 | | | | – 0 | – | | | 2,350,367 | |

Information Technology | | | – 0 | – | | | 2,256,130 | | | | – 0 | – | | | 2,256,130 | |

Health Care | | | – 0 | – | | | 2,173,523 | | | | – 0 | – | | | 2,173,523 | |

Real Estate | | | – 0 | – | | | 2,005,518 | | | | – 0 | – | | | 2,005,518 | |

Consumer Staples | | | – 0 | – | | | 1,647,152 | | | | – 0 | – | | | 1,647,152 | |

Utilities | | | – 0 | – | | | 1,520,234 | | | | – 0 | – | | | 1,520,234 | |

Short-Term Investments: | | | | | | | | | | | | | | | | |

Investment Companies | | | 607,265 | | | | – 0 | – | | | – 0 | – | | | 607,265 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | | 3,350,783 | | | | 33,325,175 | † | | | – 0 | – | | | 36,675,958 | |

Other Financial Instruments*: | | | – 0 | – | | | – 0 | – | | | – 0 | – | | | – 0 | – |

| | | | | | | | | | | | | | | | |

Total | | $ | 3,350,783 | | | $ | 33,325,175 | | | $ | – 0 | – | | $ | 36,675,958 | |

| | | | | | | | | | | | | | | | |

| † | A significant portion of the Fund’s foreign equity investments are categorized as Level 2 investments since they are valued using fair value prices based on third party vendor modeling tools to the extent available, see Note A.1. |

| * | Other financial instruments are derivative instruments, such as futures, forwards and swaps, which are valued at the unrealized appreciation/(depreciation) on the instrument. Other financial instruments may also include swaps with upfront premiums, options written and swaptions written which are valued at market value. |

The Fund recognizes all transfers between levels of the fair value hierarchy assuming the financial instrument was transferred at the beginning of the reporting period.

The Adviser established the Committee to oversee the pricing and valuation of all securities held in the Fund. The Committee operates under pricing and valuation policies and procedures established by the Adviser and approved by the Board, including pricing policies which set forth the mechanisms and processes to be employed on a daily basis to implement these policies and procedures. In particular, the pricing policies describe how to determine market quotations for securities and other instruments. The Committee’s responsibilities include: 1) fair value and liquidity determinations (and oversight of any third parties to whom any responsibility for fair value and liquidity determinations is delegated), and 2) regular monitoring of the Adviser’s pricing and valuation policies and procedures and modification or enhancement of these policies and procedures (or recommendation of the modification of these policies and procedures) as the Committee believes appropriate.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 15 |

NOTES TO FINANCIAL STATEMENTS(continued)

The Committee is also responsible for monitoring the implementation of the pricing policies by the Adviser’s Pricing Group (the “Pricing Group”) and any third party which performs certain pricing functions in accordance with the pricing policies. The Pricing Group is responsible for the oversight of the third party on aday-to-day basis. The Committee and the Pricing Group perform a series of activities to provide reasonable assurance of the accuracy of prices including: 1) periodic vendor due diligence meetings, review of methodologies, new developments and process at vendors, 2) daily comparison of security valuation versus prior day for all securities that exceeded established thresholds, and 3) daily review of unpriced, stale, and variance reports with exceptions reviewed by senior management and the Committee.

In addition, several processes outside of the pricing process are used to monitor valuation issues including: 1) performance and performance attribution reports are monitored for anomalous impacts based upon benchmark performance, and 2) portfolio managers review all portfolios for performance and analytics (which are generated using the Adviser’s prices).

3. Currency Translation

Assets and liabilities denominated in foreign currencies and commitments under forward currency exchange contracts are translated into U.S. dollars at the mean of the quoted bid and ask prices of such currencies against the U.S. dollar. Purchases and sales of portfolio securities are translated into U.S. dollars at the rates of exchange prevailing when such securities were acquired or sold. Income and expenses are translated into U.S. dollars at rates of exchange prevailing when accrued.

Net realized gain or loss on foreign currency transactions represents foreign exchange gains and losses from sales and maturities of foreign fixed income investments, holding of foreign currencies, currency gains or losses realized between the trade and settlement dates on foreign investment transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains and losses from valuing foreign currency denominated assets and liabilities at period end exchange rates are reflected as a component of net unrealized appreciation and depreciation of foreign currency denominated assets and liabilities.

4. Taxes

It is the Fund’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to

| | |

| 16 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

shareholders. Therefore, no provisions for federal income or excise taxes are required. The Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income and/or capital gains earned or repatriated. Taxes are accrued and applied to net investment income, net realized gains and net unrealized appreciation/depreciation as such income and/or gains are earned.

In accordance with U.S. GAAP requirements regarding accounting for uncertainties in income taxes, management has analyzed the Fund’s tax positions taken or expected to be taken on federal and state income tax returns for all open tax years (all years since inception of the Fund) and has concluded that no provision for income tax is required in the Fund’s financial statements.

5. Investment Income and Investment Transactions

Dividend income is recorded on theex-dividend date or as soon as the Fund is informed of the dividend. Interest income is accrued daily. Investment transactions are accounted for on the date securities are purchased or sold. Investment gains and losses are determined on the identified cost basis. The Fund amortizes premiums and accretes discounts as adjustments to interest income.

6. Class Allocations

All income earned and expenses incurred by the Fund are borne on apro-rata basis by each outstanding class of shares, based on the proportionate interest in the Fund represented by the net assets of such class, except for class specific expenses which are allocated to the respective class. Expenses of the Company are charged proportionately to each portfolio or based on other appropriate methods. Realized and unrealized gains and losses are allocated among the various share classes based on their respective net assets.

7. Dividends and Distributions

Dividends and distributions to shareholders, if any, are recorded on theex-dividend date. Income dividends and capital gains distributions are determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. GAAP. To the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

8. Offering Expenses

Offering expenses of $118,284 were deferred and amortized on a straight line basis over a one year period starting from July 25, 2018 (commencement of operations).

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 17 |

NOTES TO FINANCIAL STATEMENTS(continued)

NOTE B

Advisory Fee and Other Transactions with Affiliates

Under the terms of the investment advisory agreement, the Fund pays the Adviser an advisory fee at an annual rate of .95% of Fund’s average daily net assets. The fee is accrued daily and paid monthly. The Adviser has agreed to reimburse its fees and bear certain expenses to the extent necessary to limit total operating (excluding acquired fund fees and expenses other than the advisory fees of any AB mutual funds in which the Fund may invest, interest expense, taxes, extraordinary expenses, and brokerage commissions and other transaction costs), on an annual basis (the “Expense Caps”) to 1.50% and 1.25% of the daily average net assets for Class A and Advisor Class, respectively. For the period ended November 30, 2018, such reimbursement waivers amounted to $218,709. The Expense Caps may not be terminated by the Adviser before July 25, 2019. Any fees waived and expenses borne by the Adviser through July 25, 2019 are subject to repayment by the Fund until the end of the third fiscal year after the fiscal period in which the fee was waived or the expense was borne; such waiver that is subject to repayment amounted to $218,709 for the fiscal period ended November 30, 2018. In any case, no repayment will be made that would cause the Fund’s total annual operating expenses to exceed the Expense Caps’ net fee percentages set forth above.

During 2017, AXA S.A. (“AXA”), a French holding company for the AXA Group, a worldwide leader in life, property and casualty and health insurance and asset management, announced its intention to pursue the sale of a minority stake in its subsidiary, AXA Equitable Holdings, Inc. (“AXA Equitable”), the holding company for a diversified financial services organization, through an initial public offering (“IPO”). AXA Equitable is the holding company for a diverse group of financial services companies, including AllianceBernstein L.P., the investment adviser to the Funds (“the Adviser”). During the second quarter of 2018, AXA Equitable completed the IPO, and, as a result, AXA held approximately 72.2% of the outstanding common stock of AXA Equitable as of September 30, 2018. Contemporaneously with the IPO, AXA sold $862.5 million aggregate principal amount of its 7.25% mandatorily exchangeable notes (the “MxB Notes”) due May 15, 2021 and exchangeable into up to 43,125,000 shares of common stock (or approximately 7% of the outstanding shares of common stock of AXA Equitable). AXA retains ownership (including voting rights) of such shares of common stock until the MxB Notes are exchanged, which may be on a date that is earlier than the maturity date at AXA’s option upon the occurrence of certain events.

In March 2018, AXA announced its intention to sell its entire interest in AXA Equitable over time, subject to market conditions and other factors (the

| | |

| 18 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

“Plan”). It is anticipated that one or more of the transactions contemplated by the Plan may ultimately result in the indirect transfer of a “controlling block” of voting securities of the Adviser (a “Change of Control Event”) and therefore may be deemed an “assignment” causing a termination of each Fund’s current investment advisory agreement. In order to ensure that the existing investment advisory services could continue uninterrupted, at meetings held in late July through early August 2018, the Boards of Directors/Trustees (each a “Board” and collectively, the “Boards”) approved new investment advisory agreements with the Adviser, in connection with the Plan. The Boards also agreed to call and hold a joint meeting of shareholders on October 11, 2018 for shareholders of each Fund to (1) approve the new investment advisory agreement with the Adviser that would be effective after the first Change of Control Event and (2) approve any future advisory agreement approved by the Board and that has terms not materially different from the current agreement, in the event there are subsequent Change of Control Events arising from completion of the Plan that terminate the advisory agreement after the first Change of Control Event. Approval of a future advisory agreement means that shareholders may not have another opportunity to vote on a new agreement with the Adviser even upon a change of control, as long as no single person or group of persons acting together gains “control” (as defined in the 1940 Act) of AXA Equitable.

At the October 11, 2018 meeting, shareholders approved the new and future investment advisory agreements.

On November 20, 2018 AXA completed a public offering of 60,000,000 shares of AXA Equitable’s common stock and simultaneously sold 30,000,000 of such shares to AXA Equitable pursuant to a separate agreement with it. As a result AXA currently owns approximately 59.2% of the shares of common stock of AXA Equitable.

Pursuant to the investment advisory agreement, the Fund may reimburse the Adviser for certain legal and accounting services provided to the Fund by the Adviser. For the period ended November 30, 2018, the Adviser voluntarily agreed to waive such fees in the amount to $18,856.

The Fund compensates AllianceBernstein Investor Services, Inc. (“ABIS”), a wholly-owned subsidiary of the Adviser, under a Transfer Agency Agreement for providing personnel and facilities to perform transfer agency services for the Fund. ABIS may make payments to intermediaries that provide omnibus account services,sub-accounting services and/or networking services. Such compensation retained by ABIS amounted to $6,027 for the period ended November 30, 2018.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 19 |

NOTES TO FINANCIAL STATEMENTS(continued)

AllianceBernstein Investments, Inc. (the “Distributor”), a wholly-owned subsidiary of the Adviser, serves as the distributor of the Fund’s shares. The Distributor has advised the Fund that it has retained nofront-end sales charges from the sale of Class A shares and received no contingent deferred sales charges imposed upon redemptions by shareholders of Class A for the period ended November 30, 2018.

The Fund may invest in AB Government Money Market Portfolio (the “Government Money Market Portfolio”) which has a contractual annual advisory fee rate of .20% of the portfolio’s average daily net assets and bears its own expenses. Effective August 1, 2018, the Adviser has contractually agreed to waive .10% of the advisory fee of Government Money Market Portfolio until August 31, 2019. In connection with the investment by the Fund in the Government Money Market Portfolio, the Adviser has contractually agreed to waive its advisory fee from the Fund in an amount equal to the Fund’s pro rata share of the effective advisory fees of Government Money Market Portfolio, as borne indirectly by the Fund as an acquired fund fee and expense. For the period ended November 30, 2018, such waiver amounted to $247.

A summary of the Fund’s transactions in AB mutual funds for the period ended November 30, 2018 is as follows:

| | | | | | | | | | | | | | | | | | | | |

Fund | | Market Value

7/25/18*

(000) | | | Purchases

at Cost

(000) | | | Sales

Proceeds

(000) | | | Market Value

11/30/18

(000) | | | Dividend

Income

(000) | |

Government Money Market Portfolio | | $ | – 0 | – | | $ | 13,275 | | | $ | 12,668 | | | $ | 607 | | | $ | 5 | |

| * | Commencement of operations. |

Brokerage commissions paid on investment transactions for the period ended November 30, 2018 amounted to $33,075, of which $0 and $0, respectively, was paid to Sanford C. Bernstein & Co., LLC and Sanford C. Bernstein Limited, affiliates of the Adviser.

NOTE C

Distribution Services Agreement

The Fund has adopted a Distribution Services Agreement (the “Agreement”) pursuant to Rule12b-1 under the Investment Company Act of 1940. Under the Agreement, the Fund pays distribution and servicing fees to the Distributor at an annual rate of up to .25% of the Fund’s average daily net assets attributable to Class A shares. There are no distribution and servicing fees on the Advisor Class. The fees are accrued daily and paid monthly. The Agreement provides that the Distributor will

| | |

| 20 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

use such payments in their entirety for distribution assistance and promotional activities. In accordance with the Agreement, there is no provision for recovery of unreimbursed distribution costs incurred by the Distributor beyond the current fiscal year for Class A shares. The Agreement also provides that the Adviser may use its own resources to finance the distribution of the Fund’s shares.

NOTE D

Investment Transactions

Purchases and sales of investment securities (excluding short-term investments) for the period ended November 30, 2018 were as follows:

| | | | | | | | |

| | | Purchases | | | Sales | |

Investment securities (excluding U.S. government securities) | | $ | 43,702,510 | | | $ | 5,750,998 | |

U.S. government securities | | | – 0 | – | | | – 0 | – |

The cost of investments for federal income tax purposes, gross unrealized appreciation and unrealized depreciation (excluding foreign currency contracts) are as follows:

| | | | |

Cost | | $ | 37,883,779 | |

| | | | |

Gross unrealized appreciation | | $ | 479,115 | |

Gross unrealized depreciation | | | (1,686,936 | ) |

| | | | |

Net unrealized depreciation | | $ | (1,207,821 | ) |

| | | | |

1. Derivative Financial Instruments

The Fund may use derivatives in an effort to earn income and enhance returns, to replace more traditional direct investments, to obtain exposure to otherwise inaccessible markets (collectively, “investment purposes”), or to hedge or adjust the risk profile of its portfolio.

The principal types of derivatives utilized by the Fund, as well as the methods in which they may be used are:

The Fund may buy or sell futures for investment purposes or for the purpose of hedging its portfolio against adverse effects of potential movements in the market. The Fund bears the market risk that arises from changes in the value of these instruments and the imperfect correlation between movements in the price of the futures and they are designed to track. Among other things, the Fund may purchase or sell futures for foreign currencies or options thereon fornon-hedging purposes as a means of making direct investment in foreign currencies, as described below under “Currency Transactions”.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 21 |

NOTES TO FINANCIAL STATEMENTS(continued)

At the time the Fund enters into futures, the Fund deposits and maintains as collateral an initial margin with the broker, as required by the exchange on which the transaction is effected. Such amount is shown as cash collateral due from broker on the statement of assets and liabilities. Pursuant to the contract, the Fund agrees to receive from or pay to the broker an amount of cash equal to the daily fluctuation in the value of the contract. Such receipts or payments are known as variation margin and are recorded by the Fund as unrealized gains or losses. Risks may arise from the potential inability of a counter party to meet the terms of the contract. The credit/counterparty risk for exchange-traded futures contracts is generally less than privately negotiated futures contracts, since the clearinghouse, which is the issuer or counterparty to each exchange-traded future, has robust risk mitigation standards, including the requirement to provide initial and variation margin. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the time it was closed.

Use of long futures subjects the Fund to risk of loss in excess of the amounts shown on the statement of assets and liabilities, up to the notional value of the futures. Use of short futures subjects the Fund to unlimited risk of loss. Under some circumstances, futures exchanges may establish daily limits on the amount that the price of a future can vary from the previous day’s settlement price, which could effectively prevent liquidation of unfavorable positions.

During period ended November 30, 2018, the Fund held futures for hedging purposes.

During the period ended November 30, 2018 the Fund had entered into the following derivatives:

| | | | | | | | | | |

Derivative Type | | Location of Gain

or (Loss) on Derivatives

Within Statement of

Operations | | Realized Gain

or (Loss) on

Derivatives | | | Change in

Unrealized

Appreciation or

(Depreciation) | |

Equity contracts | | Net realized gain/(loss) on futures; Net change in unrealized appreciation/ depreciation on futures | | $ | (31,576 | ) | | $ | – 0 – | |

| | | | | | | | | | |

Total | | | | $ | (31,576 | ) | | $ | – 0 – | |

| | | | | | | | | | |

The following table represents the average monthly volume of the Fund’s derivative transactions during the period ended November 30, 2018:

| | | | |

Futures: | | | | |

Average original value of buy contracts | | $ | 945,193 | (a) |

| (a) | Positions were open for less than one month during the period. |

| | |

| 22 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

2. Currency Transactions

The Fund may invest innon-U.S. Dollar-denominated securities on a currency hedged or unhedged basis. The Fund may seek investment opportunities by taking long or short positions in currencies through the use of currency-related derivatives, including forward currency exchange contracts, futures and options on futures, swaps, and other options. The Fund may enter into transactions for investment opportunities when it anticipates that a foreign currency will appreciate or depreciate in value but securities denominated in that currency are not held by the Fund and do not present attractive investment opportunities. Such transactions may also be used when the Adviser believes that it may be more efficient than a direct investment in a foreign currency-denominated security. The Fund may also conduct currency exchange contracts on a spot basis (i.e., for cash at the spot rate prevailing in the currency exchange market for buying or selling currencies).

NOTE E

Capital Stock

Each class consists of 1,000,000,000 authorized shares. Transactions in capital shares for each class were as follows:

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | Shares | | | | | | Amount | | | | |

| | | July 25, 2018* to

November 30,

2018 | | | | | | July 25, 2018* to

November 30,

2018 | | | | |

| | | | | | | | |

| Class A | | | | | | | | | | | | | | | | |

Shares sold | | | 81,858 | | | | | | | $ | 774,914 | | | | | |

| | | | | |

Shares redeemed | | | 0 | (a) | | | | | | | (1 | ) | | | | |

| | | | | |

Net increase | | | 81,858 | | | | | | | $ | 774,913 | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | |

| Advisor Class | | | | | | | | | | | | | | | | |

Shares sold | | | 4,325,262 | | | | | | | $ | 38,080,012 | | | | | |

| | | | | |

Shares redeemed | | | (10,819 | ) | | | | | | | (89,996 | ) | | | | |

| | | | | |

Net increase | | | 4,314,443 | | | | | | | $ | 37,990,016 | | | | | |

| | | | | |

| * | Commencement of operations. |

NOTE F

Risks Involved in Investing in the Fund

Foreign(Non-U.S.) Risk—Investments in securities ofnon-U.S. issuers may involve more risk than those of U.S. issuers. These securities may fluctuate more widely in price and may be less liquid due to adverse market, economic, political, regulatory or other factors. Investments in emerging market countries such as China may involve more risk than investments in developed countries because the markets in emerging market countries are less developed and less liquid and are subject to

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 23 |

NOTES TO FINANCIAL STATEMENTS(continued)

increased economic, political, regulatory, or other uncertainties. In addition, the value of the Fund’s investments may decline because of factors such as unfavorable or unsuccessful government actions and reduction in government or central bank support.

China/Single Country Risk—Investments in issuers located in a particular country or geographic region may have more risk because of particular market factors affecting that country or region, including political instability or unpredictable economic conditions. Risks of investments in securities of companies in China include the volatility of the Chinese stock market, heavy dependence on exports, which may be affected adversely by trade barriers or disputes or may decrease, sometimes significantly, when the world economy weakens, and the continuing importance of the role of the Chinese Government, which may take actions that affect economic and market practices. While the Chinese economy has grown rapidly in recent years, there is no guarantee that this growth rate will be maintained. Investments in China A shares are subject to quotas that may restrict daily trading and generally are less liquid than shares of companies in developed markets. Risks of investments in companies based in Hong Kong include heavy reliance on the U.S. economy and regional economies, particularly the Chinese economy, which makes these investments vulnerable to changes in these economies.

Currency Risk—Fluctuations in currency exchange rates may negatively affect the value of the Fund’s investments in equity securities denominated in foreign currencies or reduce the Fund’s returns. Emerging market currencies may be more volatile and less liquid, and subject to significantly greater risk of currency controls and convertibility restrictions, than currencies of developed countries.

Depositary Receipts Risk—Investing in depositary receipts involves risks that are similar to the risks of direct investments in foreign securities. For example, investing in depositary receipts may involve risks relating to political, economic or regulatory conditions in foreign countries. In addition, the issuers of the securities underlying certain depositary receipts may be under no obligation to distribute shareholder communications or pass through any voting rights with respect to the deposited securities to the holders of such receipts.

Liquidity Risk—Liquidity risk exists when particular investments are difficult to purchase or sell, possibly preventing the Fund from selling out of these illiquid securities at an advantageous price. Derivatives and securities involving substantial market and credit risk tend to involve greater liquidity risk.

| | |

| 24 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

NOTES TO FINANCIAL STATEMENTS(continued)

Non-Diversification Risk—The Fund may have more risk because it is“non-diversified”, meaning that it can invest more of its assets in a smaller number of issuers. Accordingly, changes in the value of a single security may have a more significant effect, either negative or positive, on the Fund’s net asset value, or NAV.

Indemnification Risk—In the ordinary course of business, the Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these indemnification provisions and expects the risk of loss thereunder to be remote. Therefore, the Fund has not accrued any liability in connection with these indemnification provisions.

NOTE H

Distributions to Shareholders

The tax character of distributions paid during the period ended November 30, 2018 was as follows:

| | | | |

Distributions paid from: | | | | |

Ordinary income | | $ | – 0 | – |

| | | | |

Total distributions paid | | $ | – 0 | – |

| | | | |

As of November 30, 2018, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| | | | |

Accumulated capital and other losses | | $ | (706,696 | )(a) |

Unrealized appreciation/(depreciation) | | | (1,208,582 | )(b) |

| | | | |

Total accumulated earnings/(deficit) | | $ | (1,915,278 | )(c) |

| | | | |

| (a) | As of November 30, 2018, the Fund had a net capital loss carryforward of $706,696. |

| (b) | The difference between book-basis and tax-basis unrealized appreciation/(depreciation) is attributable primarily to the tax deferral of losses on wash sales. |

| (c) | The difference between book-basis and tax-basis components of accumulated earnings/(deficit) is attributable primarily to the amortization of offering costs. |

For tax purposes, net realized capital losses may be carried over to offset future capital gains, if any. Funds are permitted to carry forward capital losses for an indefinite period, and such losses will retain their character as eithershort-term orlong-term capital losses. As of November 30, 2018, the Fund had a netshort-term capital loss carryforward of $706,696, which may be carried forward for an indefinite period.

During the current fiscal period, permanent differences primarily due to the disallowance of a net operating loss resulted in a net decrease in accumulated loss and a net decrease in additionalpaid-in capital. This reclassification had no effect on net assets.

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 25 |

NOTES TO FINANCIAL STATEMENTS(continued)

NOTE I

Recent Accounting Pronouncements

In August 2018, the Financial Accounting Standards Board issued an Accounting Standards Update, ASU2018-13, Fair Value Measurement (Topic 820), Disclosure Framework-Changes to the Disclosure Requirements for Fair Value Measurement which removes, modifies and adds disclosures to Topic 820. The amendments in this ASU2018-13 apply to all entities that are required, under existing U.S. GAAP, to make disclosures about recurring or nonrecurring fair value measurements. The amendments in this ASU2018-13 are effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019. At this time, management is evaluating the implications of these changes on the financial statements.

In October 2018, the U.S. Securities and Exchange Commission adopted amendments to certain disclosure requirements that had become “redundant, duplicative, overlapping, outdated or superseded, in light of the other Commission disclosure requirements, GAAP or changes in the information environment.” The compliance date for the amendments to RegulationS-X was November 5, 2018 (for reporting period end dates of September 30, 2018 or after). Management has adopted the amendments which simplified certain disclosure requirements on the financial statements.

NOTE J

Subsequent Events

Management has evaluated subsequent events for possible recognition or disclosure in the financial statements through the date the financial statements are issued. Management has determined that there are no material events that would require disclosure in the Fund’s financial statements through this date.

| | |

| 26 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

FINANCIAL HIGHLIGHTS

Selected Data For A Share Of Capital Stock Outstanding Throughout Each Period

| | | | |

| | | Class A | |

| | | July 25,

2018(a) to

November 30,

2018 | |

| | | | |

| | | | |

Net asset value, beginning of period | | | $ 10.00 | |

| | | | |

Income From Investment Operations | | | | |

| |

Net investment loss(b)(c) | | | (.01 | ) |

| |

Net realized and unrealized loss on investment and foreign currency transactions | | | (1.62 | ) |

| | | | |

Net decrease in net asset value from operations | | | (1.63 | ) |

| | | | |

Net asset value, end of period | | | $ 8.37 | |

| | | | |

| |

Total Return | | | | |

| |

Total investment return based on net asset value(d) | | | (16.30 | )% |

| |

Ratios/Supplemental Data | | | | |

| |

Net assets, end of period (000’s omitted) | | | $685 | |

| |

Ratio to average net assets of: | | | | |

| |

Expenses, net of waivers/reimbursements(e) | | | 1.50 | % |

| |

Expenses, before waivers/reimbursements(e) | | | 4.81 | % |

| |

Net investment loss(c)(e) | | | (.33 | )% |

| |

Portfolio turnover rate | | | 38 | % |

See footnote summary on page 28.

| | |

| |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 27 |

FINANCIAL HIGHLIGHTS(continued)

Selected Data For A Share Of Capital Stock Outstanding Throughout Each Period

| | | | |

| | | Advisor Class | |

| | | July 25,

2018(a) to

November 30,

2018 | |

| | | | |

| | | | |

Net asset value, beginning of period | | | $ 10.00 | |

| | | | |

Income From Investment Operations | | | | |

| |

Net investment loss(b)(c) | | | (.01 | ) |

| |

Net realized and unrealized loss on investment and foreign currency transactions | | | (1.61 | ) |

| | | | |

Net decrease in net asset value from operations | | | (1.62 | ) |

| | | | |

Net asset value, end of period | | | $ 8.38 | |

| | | | |

| |

Total Return | | | | |

| |

Total investment return based on net asset value(d) | | | (16.20 | )% |

| |

Ratios/Supplemental Data | | | | |

| |

Net assets, end of period (000’s omitted) | | | $36,145 | |

| |

Ratio to average net assets of: | | | | |

| |

Expenses, net of waivers/reimbursements(e) | | | 1.25 | % |

| |

Expenses, before waivers/reimbursements(e) | | | 5.13 | % |

| |

Net investment loss(c)(e) | | | (.37 | )% |

| |

Portfolio turnover rate | | | 38 | % |

| (a) | Commencement of operations. |

| (b) | Based on average shares outstanding. |

| (c) | Net of fees and expenses waived/reimbursed by the Adviser. |

| (d) | Total investment return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption on the last day of the period. Initial sales charge or contingent deferred sales charge is not reflected in the calculation of total investment return. Total investment return does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Total investment return for a period of less than one year is not annualized. |

See notes to financial statements.

| | |

| |

| 28 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Directors of

AB All China Equity Portfolio

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of AB All China Equity Portfolio (the “Fund”) (one of the funds constituting AB Cap Fund, Inc. (the “Company”)), including the portfolio of investments, as of November 30, 2018, and the related statements of operations and changes in net assets and the financial highlights for the period from July 25, 2018 (commencement of operations) through November 30, 2018 and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (one of the funds constituting AB Cap Fund, Inc.) at November 30, 2018, and the results of its operations, the changes in its net assets and its financial highlights for the period from July 25, 2018 (commencement of operations) through November 30, 2018, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of the Company’s internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation

| | |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 29 |

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM(continued)

of securities owned as of November 30, 2018, by correspondence with the custodian and others or by other appropriate auditing procedures where replies from others were not received. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

We have served as the auditor of one or more of the AB investment companies since 1968.

New York, New York

January 25, 2019

| | |

| 30 | AB ALL CHINA EQUITY PORTFOLIO | | abfunds.com |

RESULTS OF STOCKHOLDER MEETING

(unaudited)

A Special Meeting of Stockholders of the AB Cap Fund, Inc. (the “Company”)—AB All China Equity Portfolio (the “Fund”) was held on October 11, 2018. A description of the proposals and number of shares voted at the Meeting are as follows (the proposal number shown below corresponds to the proposal number in the Fund’s proxy statement):

| 1. | To approve and vote upon the election of Directors for the Company, each such Director to serve for a term of indefinite duration and until his or her successor is duly elected and qualifies. |

| | | | | | | | |

Director: | | Voted

For: | | | Authority

Withheld: | |

Michael J. Downey | | | 153,531,217 | | | | 1,117,868 | |

William H. Foulk, Jr. | | | 153,385,034 | | | | 1,264,050 | |

Nancy P. Jacklin | | | 153,607,746 | | | | 1,041,339 | |

Robert M. Keith | | | 153,546,025 | | | | 1,103,060 | |

Carol C. McMullin | | | 153,649,415 | | | | 999,670 | |

Gary L. Moody | | | 153,545,113 | | | | 1,103,972 | |

Marshall C. Turner, Jr. | | | 153,507,495 | | | | 1,141,590 | |

Earl D. Weiner | | | 153,514,727 | | | | 1,134,358 | |

| 2. | To vote upon the approval of new advisory agreements for the Fund with AllianceBernstein L.P. |

| | | | | | |

Voted

For: | | Voted

Against: | | Abstain: | | Broker

Non-Votes: |

| 200,000 | | – 0 – | | – 0 – | | – 0 – |

| | |

| |

| abfunds.com | | AB ALL CHINA EQUITY PORTFOLIO | 31 |

BOARD OF DIRECTORS

| | |

Marshall C. Turner, Jr.(1),Chairman Michael J. Downey(1) Nancy P. Jacklin(1) Robert M. Keith,President and Chief Executive Officer | | Carol C. McMullin(1) Garry L. Moody(1) Earl D. Weiner(1) |

OFFICERS

| | |

John Lin(2),Vice President Stuart Rae(2),Vice President Emilie D. Wrapp,Secretary Michael B. Reyes,Senior Analyst | | Joseph J. Mantineo,Treasurer and Chief Financial Officer Vincent S. Noto,Chief Compliance Officer Phyllis J. Clarke,Controller |

| | |

Custodian and Accounting Agent Brown Brothers Harriman & Co. 50 Post Office Square Boston, MA 02110 Principal Underwriter AllianceBernstein Investments, Inc. 1345 Avenue of the Americas New York, NY 10105 Legal Counsel Seward & Kissel LLP One Battery Park Plaza New York, NY 10004 | | Independent Registered Public Accounting Firm Ernst & Young LLP 5 Times Square New York, NY 10036 Transfer Agent AllianceBernstein Investor Services, Inc. P.O. Box 786003 San Antonio, TX 78278-6003 Toll-Free (800)221-5672 |

| 1 | Member of the Audit Committee, the Governance and Nominating Committee and the Independent Directors Committee. |

| 2 | Theday-to-day management of, and investment decisions for, the Fund’s portfolio are made by China Equity Team. Messrs. Lin and Rae are the investment professionals with the most significant responsibility for theday-to-day management of the Fund’s portfolio. |

| | |