UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kathleen L. Prudhomme

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: October 31

Date of reporting period: October 31, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | |

| | |  |

| Mutual Funds | |

| | | | | | |

| | | | | | | Annual Report October 31, 2016 |

| | | | | | | | | | | | | | |

| | | | | | | Share Class / Ticker Symbol | | |

| | | Fund Name | | | | Class A | | Class C | | Class R3 | | Class I | | |

| | |

| | Nuveen Equity Index Fund | | | | FAEIX | | FCEIX | | FADSX | | FEIIX | | |

| | Nuveen Mid Cap Index Fund | | | | FDXAX | | FDXCX | | FMCYX | | FIMEX | | |

| | Nuveen Small Cap Index Fund | | | | FMDAX | | FPXCX | | ARSCX | | ASETX | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| | |

| | Life is Complex. | | |

| | |

| | Nuveen makes things e-simple. | | |

| | |

| | It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. | | |

| | | | |

| | | | | | Free e-Reports right to your e-mail! | | |

| | | |

| | | | | | www.investordelivery.com If you receive your Nuveen Fund distributions and statements from your

financial advisor or brokerage account. |

| | | | |

| | | | or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund distributions and statements directly from Nuveen. Must be preceded by or accompanied by a prospectus. NOT FDIC INSURED MAY LOSE VALUE

NO BANK GUARANTEE | | |

| | | | | | | | | | |

| | | | | | | | | | | | | |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

After a sluggish first half of 2016, the U.S. economy gained some momentum in the third quarter. In fact, it was the economy’s strongest quarterly acceleration in two years, propelled by healthy consumer spending, a temporary surge in exports and a turnaround in inventories. As the year winds down, 2016 looks on track to deliver the same steady-but-slow growth that has characterized the seven-year recovery.

A year ago, the U.S. Federal Reserve (Fed) took the first step toward policy “normalization” by raising its benchmark interest rate at its December 2015 meeting. Speculation about the Fed’s intentions since then has been a strong influence on the markets throughout 2016. After remaining on hold for a year, the Fed judged that the economy’s modest growth, the return to “full” employment and an uptick in inflation were sufficient to raise the target rate at the December 2016 meeting.

Global conditions continue to look subdued by comparison. Investors continue to adjust to the idea of a slower Chinese economy, which has helped commodity prices stabilize and lift global inflation expectations. The U.K.’s June 23rd “Brexit” vote to leave the European Union introduced a new set of economic and political uncertainties to the already fragile conditions across Europe. Moreover, there are growing concerns that global central banks’ unprecedented efforts to revive growth may be showing signs of fatigue. Interest rates are currently negative in Europe and Japan and near or at zero in the U.S., U.K. and elsewhere; nonetheless, growth has remained subdued.

Since the election, U.S. stocks have rallied strongly on expectations that the Republican controlled Congress and Trump administration will pursue more business friendly policies. But the details have yet to be seen. Given muted global growth, the risk of policy errors by central banks around the world, the unfolding Brexit process and an uncertain political outlook (not just in the U.S. but also in Europe), we anticipate that turbulence remains on the horizon for the time being. In this environment, Nuveen remains committed to both managing downside risks and seeking upside potential. If you’re concerned about how resilient your investment portfolio might be, we encourage you to talk to your financial advisor. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

December 22, 2016

Portfolio Managers’

Comments

Nuveen Equity Index Fund

Nuveen Mid Cap Index Fund

Nuveen Small Cap Index Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen Investments, Inc. During this reporting period, David A. Friar and Michael N. Lindh, CFA and CPA, were the portfolio managers for the Funds. David has managed the Nuveen Equity Index Fund since 2000 and the Nuveen Mid Cap Index Fund and the Nuveen Small Cap Index Fund since 2001. Michael was named co-manager of all three Funds in 2014.

The Nuveen Equity Index, the Nuveen Mid Cap Index and the Nuveen Small Cap Index Funds will be liquidated after the close of business on April 27, 2017.

On the following pages, the portfolio management teams for the Funds discuss economic and market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period ended October 31, 2016.

What factors affected the U.S. economy and the financial markets during the twelve-month reporting period ended October 31, 2016?

The restrained pace of growth that has defined the U.S. economic recovery since 2009 continued in the twelve-month reporting period. Growth over the previous four calendar quarters averaged below 2% (annualized), as measured by real gross domestic product (GDP), which is the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. For most of the reporting period, consumer spending remained healthy but was offset by the drag from the inventory cycle, lackluster business spending and weak net exports. As a result, GDP growth stayed below 1.5% from the fourth quarter of 2015 through the second quarter of 2016. However, decent consumer spending, an inventory turnaround and a short-term jump in exports contributed to a more robust gain of 3.2% in the third quarter, as reported by the “second” estimate of the Bureau of Economic Analysis.

Consumers, whose purchases comprise the largest component of the U.S. economy, benefited from employment growth and firming wages over the twelve-month reporting period. As reported by the Bureau of Labor Statistics, the unemployment rate was little changed at 4.9% in October 2016 from 5.0% in October 2015, and job gains averaged slightly above 200,000 per month for the past twelve months. Although consumer spending gains were rather muted in the latter half of 2015, spending surged in the second quarter of 2016. Although inflation began to accelerate slightly in the reporting period, the overall level remained low, which also contributed to consumers’ willingness to buy. The Consumer Price Index (CPI) rose 1.6% over the twelve-month reporting period ended October 2016 on a seasonally adjusted basis, as reported by the U.S. Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 2.1% during the same period, slightly above the Fed’s unofficial longer term inflation objective of 2.0%.

The housing market was another bright spot in the economy. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 5.5% annual gain in September 2016 (most recent data available at the time this report was prepared) (effective July 26, 2016, the S&P/Case-Shiller U.S. National Home Price Index was renamed the S&P CoreLogic Case-Shiller U.S. National Home Price Index). The 10-City and 20-City Composites reported year-over-year increases of 4.3% and 5.1%, respectively.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

However, business investment remained soft over the reporting period. Corporate earnings growth continued to be constrained by diminished demand expectations amid sluggish U.S. and global growth, the impact of falling commodity prices and a strong U.S. dollar. Additionally, a murky outlook kept capital spending muted. Concerns about financial market turbulence in early 2016, the U.K.’s “Brexit” vote to leave the European Union (EU) and the U.S. presidential election weighed on business sentiment throughout the reporting period.

The consistent growth of the economy prompted the U.S. Federal Reserve (Fed) to raise the Fed funds rate from the zero bound range to a range of 0.25% to 0.50% in December 2015. The widely anticipated move had little impact on the financial markets. Over the remainder of the reporting period, speculation on the timing of future rate hikes drove short-term swings in the markets, including falling bond yields, rallies in the U.S. dollar and bouts of volatility in stock prices. For most of 2016, the Fed kept this rate unchanged due to concerns ranging from low inflation in the U.S. to weakening growth prospects globally and the U.K.’s Brexit vote. However, the third quarter’s strong GDP report and an uptick in inflation boosted expectations that the Fed would likely increase the target rate at the December 2016 meeting. As anticipated, subsequent to the close of the reporting period, the Fed raised the rate to a range of 0.50% to 0.75%.

Other market-moving events during the reporting period included a spike in volatility in January and February 2016 triggered by deteriorating sentiment about China’s economy, another sharp downturn in oil prices and concerns about central bank policy both in the U.S. and around the world. The Brexit referendum on June 23 also caught investors off guard. In response, U.K. sterling fell to 30-year lows and global equities tumbled while perceived safe-haven assets such as gold, the U.S. dollar and government bonds saw large inflows. However, the markets stabilized fairly quickly post-Brexit vote, buoyed by reassurances from global central banks and a perception that the temporary price rout presented an attractive buying opportunity. Following a relatively calm July and August 2016, volatility resumed in the final months of the reporting period. Investors worried whether central banks were reaching the limits of their effectiveness as global growth continues to stagnate. The health of the European banking sector came into question, renewing concerns about the potential to trigger a wider crisis. Political uncertainty increased leading up to the November U.S. presidential election, and after the close of the reporting period, the unexpected win of Donald Trump contributed to an initial sell-off across global markets. However, after digesting the “shock”, U.S. equities rallied strongly and global developed market stocks pared their losses, while emerging markets, fixed income and gold remained lower.

Despite several bouts of significant volatility, the U.S. equity market ended the twelve-month reporting period with a gain of 4.51% as measured by the S&P 500® Index. Small-cap stocks in the U.S. recovered from last year’s significant underperformance with a 4.11% return according to the Russell 2000® Index. Mid-cap stocks were in the same range. Across the capitalization spectrum in the U.S., investors favored the relatively safer, more defensive areas of the market for much of the reporting period, leading value stocks to strongly outperform growth stocks. Emerging markets outpaced other developed markets overseas as investors returned to this asset class in the second half of the reporting period, largely due to commodity price stability and the ongoing search for yield and returns. The MSCI Emerging Markets Index advanced 9.67%. Meanwhile, in developed overseas markets, Europe struggled and turned in negative results, dragging down the overall return of the MSCI EAFE Index to -2.74% for the twelve-month reporting period.

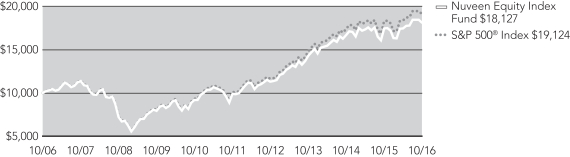

Nuveen Equity Index Fund

How did the Fund perform during the twelve-month reporting period ended October 31, 2016?

The tables in the Fund Performance and Expense Ratios section of this report provide total returns for the Fund for the one-year, five-year and ten-year periods ended October 31, 2016. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the Lipper S&P 500® Index Objective Funds Classification Average, but underperformed the S&P 500® Index during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund’s investment objective is to replicate the return of the S&P 500® Index as closely as possible, with consideration given to turnover costs and fees. S&P Dow Jones changes the index definition as often as weekly, deleting firms as they are acquired or when the membership committee determines that a firm is no longer representative of the index definition. Additionally, index weights are changed to reflect merger and acquisition activity or share issuance and repurchasing. These changes typically result in low turnover, well below 10% per year. We believe the Fund’s objective can best be achieved by investing in approximately 90% to 100% of the

issues included in the S&P 500® Index, depending on the size of the Fund. During the reporting period, we held essentially all of the issues found in the index. In addition, we aggressively tracked and implemented the occasional changes to index member names, as well as changes to the relative weights in the index.

The Fund underperformed the S&P 500® Index during the twelve-month reporting period. The index experienced a divergence of nearly 21% between the returns of its best and worst performing sectors. The utilities sector was the standout performer due to heightened investor interest in more defensive, yield generating stocks, returning approximately 17% in the S&P 500® Index during the reporting period. The information technology and telecommunication services sectors also produced double-digit returns in the index, with both segments gaining nearly 11%. Only two sectors in the index reported negative results, health care and consumer discretionary. Health care fell approximately 4% in the index mainly due to weak results from the biotechnology and pharmaceuticals industries, which suffered from continued fears regarding drug pricing controls. The consumer discretionary sector was down approximately 2% on the back of cautious consumer spending. The newly formed real estate investment trust (REIT) sector, which was officially broken out from the financial sector during the reporting period, also turned in fairly lackluster results of around 2%. Following stronger results earlier in the year, the REIT sector took a step back after investors began to price in a higher likelihood that the Fed would raise rates later in 2016.

We also continued to invest in S&P 500® Index futures to convert cash into the equivalent of an S&P 500® Index holding in order to manage cash flow activity and minimize tracking error to the Fund’s benchmark index. These contracts are used as a means to efficiently gain exposure to a broad base of equity securities. The Fund’s holdings of futures, which were matched to the level of cash, were helpful in keeping the Fund fully invested, neither overexposed nor underexposed to equities, despite cash flows. Due to the positive equity returns over the reporting period, these positions benefited the Fund’s performance.

Nuveen Mid Cap Index Fund

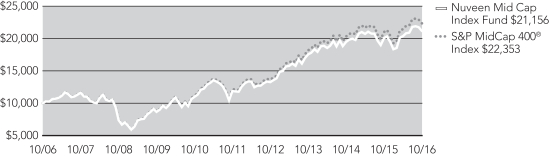

How did the Fund perform during the twelve-month reporting period ended October 31, 2016?

The tables in the Fund Performance and Expense Ratios section of this report provide total returns for the Fund for the one-year, five-year and ten-year periods ended October 31, 2016. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the Lipper Mid-Cap Core Funds Classification Average, but underperformed the S&P MidCap 400® Index for the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund’s investment objective is to replicate the return of the S&P MidCap 400® Index as closely as possible, with consideration given to turnover costs and fees. S&P Dow Jones changes the index definition as often as weekly, deleting firms as they are acquired or when the membership committee determines that a firm is no longer representative of the index definition. Additionally, index weights are changed to reflect merger and acquisition activity or share issuance and repurchasing. These changes typically result in low turnover, well below 20% per year. We believe the Fund’s objective can best be achieved by investing in approximately 90% to 100% of the issues included in the S&P MidCap 400® Index, depending on the size of the Fund. During the reporting period, we held essentially all of the issues found in the index. In addition, we aggressively tracked and implemented the occasional changes to index member names, as well as changes to the relative weights in the index.

The Fund underperformed the S&P MidCap 400® Index during the twelve-month reporting period. The index experienced a divergence of more than 52% between the returns of its best and worst performing sectors. The utilities sector was the standout performer due to heightened investor interest in more defensive, yield generating stocks, returning approximately 22% in the S&P MidCap 400® Index during the reporting period. The materials sector also produced a double-digit return in the index, gaining nearly 19%. The newly formed real estate investment trust (REIT) sector, which was officially broken out from the financial sector during the reporting period, was another area of strength in the mid-cap universe. The sector was up more than 13%, holding onto gains realized earlier in the reporting period. Energy was the most significant laggard in the mid-cap space, ending the reporting period down almost 31% as many mid-cap companies have not yet recovered from the significant oil price decline over the past year. Telecommunication services and consumer discretionary also ended in negative territory, down approximately 8% and 3%, respectively.

Portfolio Managers’ Comments (continued)

We also continued to invest in E-mini S&P MidCap 400® futures to convert cash into the equivalent of an S&P MidCap 400® Index holding in order to manage cash flow activity and minimize tracking error to the Fund’s benchmark index. These contracts are used as a means to efficiently gain exposure to a broad base of equity securities. The Fund’s holdings of futures, which were matched to the level of cash, were helpful in keeping the Fund fully invested, neither overexposed nor underexposed to equities, despite cash flows. Due to the positive equity returns over the reporting period, these positions benefited the Fund’s performance.

Nuveen Small Cap Index Fund

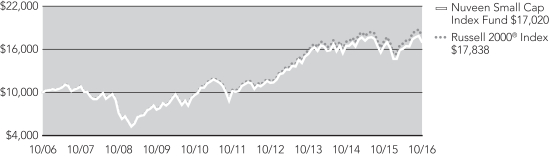

How did the Fund perform during the twelve-month reporting period ended October 31, 2016?

The tables in the Fund Performance and Expense Ratios section of this report provide total returns for the Fund for the one-year, five-year and ten-year periods ended October 31, 2016. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the Lipper Small-Cap Core Funds Classification Average, but underperformed the Russell 2000® Index for the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund’s investment objective is to replicate the return of the Russell 2000® Index as closely as possible, with consideration given to turnover costs and fees. Russell Investments reconstitutes this index near the end of June each year, generally selecting the stocks that are numbered 1001 through 3000 of the largest eligible U.S. companies. (To reduce turnover expenses, companies near the 1000 breakpoint remain in their prior category.) Throughout the remainder of the year, the number of stocks in the index will vary as appropriate IPOs are added quarterly and stocks are removed because of merger and acquisition activity or delisting. Share changes due to issuance and repurchasing are adjusted monthly. These changes typically result in low turnover, well below 20% per year. The majority of changes are from successful firms that move up to the Russell 1000® Index. We believe the Fund’s objective can best be achieved by investing in approximately 90% to 100% of the issues included in the Russell 2000® Index, depending on the size of the Fund. During the reporting period, we held essentially all of the issues found in the index. In addition, we aggressively tracked and implemented the occasional changes to index member names, as well as changes to the relative weights in the index.

The Fund underperformed the Russell 2000® Index during the reporting period. The index experienced a divergence of more than 33% between the returns of its best and worst performing sectors. The utilities sector was the standout performer due to heightened investor interest in more defensive, yield generating stocks, returning approximately 17% in the Russell 2000® Index during the reporting period. Four other sectors produced double-digit returns in the index, including materials, information technology, real estate investment trusts (REITs) and consumer staples, returning approximately 16%, 11%, 11% and 10%, respectively. The newly formed REIT sector was officially broken out from the financial sector during the reporting period. Energy was the most significant laggard in the small-cap space, ending the reporting period down more than 16% as many small-cap companies have not yet recovered from the significant oil price decline over the past year. Health care and consumer discretionary also ended in negative territory, down approximately 8% and 6%, respectively.

We also continued to invest in E-mini Russell 2000® futures to convert cash into the equivalent of a Russell 2000® Index holding in order to manage cash flow activity and minimize tracking error to the Fund’s benchmark index. These contracts are used as a means to efficiently gain exposure to a broad base of equity securities. The Fund’s holdings of futures, which were matched to the level of cash, were helpful in keeping the Fund fully invested, neither overexposed nor underexposed to equities, despite cash flows. Due to the positive equity returns over the reporting period, these positions benefited the Fund’s performance.

Risk Considerations

Nuveen Equity Index Fund

Nuveen Mid Cap Index Fund

Nuveen Small Cap Index Fund

Mutual fund investing involves risk; principal loss is possible. The Funds’ investments in common stocks involve the risk of decline due to adverse company or industry news or a general economic decline. The use of derivatives involves substantial financial risk and transaction costs. In addition, each Fund may fail to match index performance. Small- and mid-cap stocks are subject to greater price volatility and liquidity risks.

THIS PAGE INTENTIONALLY LEFT BLANK

Fund Performance

and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown within this section of the report.

Returns quoted represent past performance, which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Total returns for a period of less than one year are not annualized. Returns at net asset value (NAV) would be lower if the sales charge were included. Returns assume reinvestment of dividends and capital gains. For performance, current to the most recent month-end visit Nuveen.com or call (800) 257-8787.

Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect fee waivers and/or expense reimbursements by the investment adviser during the periods presented. If any such waivers and/or reimbursements had not been in place, returns would have been reduced. See Notes to Financial Statements, Note 7—Management Fees and Other Transactions with Affiliates for more information.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees, and assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for Class A Shares at NAV only.

The expense ratios shown reflect total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the most recent prospectus. The expense ratios include management fees and other fees and expenses.

Fund Performance and Expense Ratios (continued)

Nuveen Equity Index Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of October 31, 2016

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 3.91% | | | | 12.88% | | | | 6.13% | |

S&P 500® Index | | | 4.51% | | | | 13.57% | | | | 6.70% | |

Lipper S&P 500® Index Objective Funds Classification Average | | | 3.84% | | | | 12.93% | | | | 6.13% | |

| | | |

Class C Shares | | | 3.10% | | | | 12.04% | | | | 5.33% | |

Class R3 Shares | | | 3.65% | | | | 12.60% | | | | 5.87% | |

Class I Shares | | | 4.17% | | | | 13.17% | | | | 6.39% | |

Average Annual Total Returns as of September 30, 2016 (Most Recent Calendar Quarter)

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 14.74% | | | | 15.68% | | | | 6.66% | |

Class C Shares | | | 13.89% | | | | 14.81% | | | | 5.87% | |

Class R3 Shares | | | 14.45% | | | | 15.39% | | | | 6.40% | |

Class I Shares | | | 15.03% | | | | 15.97% | | | | 6.93% | |

Index and Lipper averages are not available for direct investment.

Class A Shares have no sales charge and are available only through fee-based programs and certain retirement plans. Class C Shares have a 1% contingent deferred sales charge (CDSC) for redemptions within less than twelve months of purchase, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Gross Expense Ratios | | | 0.71% | | | | 1.46% | | | | 0.96% | | | | 0.46% | |

Net Expense Ratios | | | 0.59% | | | | 1.34% | | | | 0.84% | | | | 0.34% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through February 28, 2018, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.34% of the average daily net assets of any class of Fund shares. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Board of Directors of the Fund.

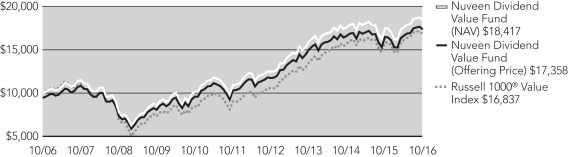

Growth of an Assumed $10,000 Investment as of October 31, 2016 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen Mid Cap Index Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of October 31, 2016

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 5.43% | | | | 12.18% | | | | 7.78% | |

S&P MidCap 400® Index | | | 6.26% | | | | 12.92% | | | | 8.38% | |

Lipper Mid-Cap Core Funds Classification Average | | | 2.79% | | | | 11.24% | | | | 6.39% | |

| | | |

Class C Shares | | | 4.67% | | | | 11.35% | | | | 6.97% | |

Class R3 Shares | | | 5.15% | | | | 11.89% | | | | 7.51% | |

Class I Shares | | | 5.76% | | | | 12.47% | | | | 8.04% | |

Average Annual Total Returns as of September 30, 2016 (Most Recent Calendar Quarter)

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 14.51% | | | | 15.74% | | | | 8.51% | |

Class C Shares | | | 13.68% | | | | 14.89% | | | | 7.71% | |

Class R3 Shares | | | 14.27% | | | | 15.45% | | | | 8.24% | |

Class I Shares | | | 14.82% | | | | 16.03% | | | | 8.79% | |

Index and Lipper averages are not available for direct investment.

Class A Shares have no sales charge and are available only through fee-based programs and certain retirement plans. Class C Shares have a 1% contingent deferred sales charge (CDSC) for redemptions within less than twelve months of purchase, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Gross Expense Ratios | | | 0.79% | | | | 1.54% | | | | 1.04% | | | | 0.54% | |

Net Expense Ratios | | | 0.64% | | | | 1.39% | | | | 0.89% | | | | 0.39% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through February 28, 2018, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.41% of the average daily net assets of any class of Fund shares. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Board of Directors of the Fund.

Growth of an Assumed $10,000 Investment as of October 31, 2016 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

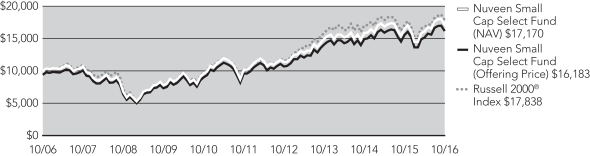

Nuveen Small Cap Index Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of October 31, 2016

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 3.58% | | | | 10.89% | | | | 5.46% | |

Russell 2000® Index | | | 4.11% | | | | 11.51% | | | | 5.96% | |

Lipper Small-Cap Core Funds Classification Average | | | 3.01% | | | | 10.67% | | | | 5.89% | |

| | | |

Class C Shares | | | 2.82% | | | | 10.05% | | | | 4.67% | |

Class R3 Shares | | | 3.31% | | | | 10.61% | | | | 5.20% | |

Class I Shares | | | 3.86% | | | | 11.17% | | | | 5.73% | |

Average Annual Total Returns as of September 30, 2016 (Most Recent Calendar Quarter)

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares | | | 14.85% | | | | 15.18% | | | | 6.57% | |

Class C Shares | | | 14.05% | | | | 14.32% | | | | 5.78% | |

Class R3 Shares | | | 14.65% | | | | 14.89% | | | | 6.30% | |

Class I Shares | | | 15.20% | | | | 15.46% | | | | 6.84% | |

Index and Lipper averages are not available for direct investment.

Class A Shares have no sales charge and are available only through fee-based programs and certain retirement plans. Class C Shares have a 1% contingent deferred sales charge (CDSC) for redemptions within less than twelve months of purchase, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Gross Expense Ratios | | | 1.00% | | | | 1.75% | | | | 1.25% | | | | 0.74% | |

Net Expense Ratios | | | 0.77% | | | | 1.52% | | | | 1.02% | | | | 0.52% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through February 28, 2018, so that total annual fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.54% of the average daily net assets of any class of Fund shares. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Board of Directors of the Fund.

Growth of an Assumed $10,000 Investment as of October 31, 2016 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Holding

Summaries as of October 31, 2016

This data relates to the securities held in each Fund’s portfolio of investments as of the end of this reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Nuveen Equity Index Fund

Fund Allocation

(% of net assets)

| | | | |

Common Stocks | | | 95.4% | |

Common Stock Rights | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 1.2% | |

Money Market Funds | | | 4.4% | |

U.S. Government and Agency Obligations | | | 0.4% | |

Other Assets Less Liabilities | | | (1.4)% | |

Net Assets | | | 100% | |

Portfolio Composition

(% of net assets)

| | | | |

Oil, Gas & Consumable Fuels | | | 5.8% | |

Banks | | | 5.5% | |

Pharmaceuticals | | | 5.1% | |

Internet Software & Services | | | 4.5% | |

Software | | | 4.3% | |

Technology Hardware, Storage & Peripherals | | | 3.7% | |

IT Services | | | 3.6% | |

Semiconductors & Semiconductor Equipment | | | 3.1% | |

Media | | | 2.8% | |

Equity Real Estate Investment Trusts | | | 2.8% | |

Biotechnology | | | 2.6% | |

Insurance | | | 2.6% | |

Health Care Equipment & Supplies | | | 2.5% | |

Capital Markets | | | 2.5% | |

Internet and Direct Marketing Retail | | | 2.4% | |

Industrial Conglomerates | | | 2.4% | |

Health Care Providers & Services | | | 2.4% | |

Diversified Telecommunication Services | | | 2.4% | |

Specialty Retail | | | 2.3% | |

Beverages | | | 2.1% | |

Aerospace & Defense | | | 2.1% | |

Food & Staples Retailing | | | 2.1% | |

Electric Utilities | | | 2.0% | |

Chemicals | | | 2.0% | |

Household Products | | | 1.9% | |

Other | | | 19.9% | |

Common Stock Rights | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 1.2% | |

Money Market Funds | | | 4.4% | |

U.S. Government and Agency Obligations | | | 0.4% | |

Other Assets Less Liabilities | | | (1.4)% | |

Net Assets | | | 100% | |

Top Five Common Stock Holdings

(% of net assets)

| | | | |

Apple, Inc. | | | 3.2% | |

Microsoft Corporation | | | 2.4% | |

Exxon Mobil Corporation | | | 1.8% | |

Johnson & Johnson | | | 1.6% | |

Amazon.com, Inc. | | | 1.6% | |

Nuveen Mid Cap Index Fund

Fund Allocation

(% of net assets)

| | | | |

Common Stocks | | | 97.4% | |

Common Stock Rights | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 5.6% | |

Money Market Funds | | | 2.3% | |

U.S. Government and Agency Obligations | | | 0.5% | |

Other Assets Less Liabilities | | | (5.8)% | |

Net Assets | | | 100% | |

Portfolio Composition

(% of net assets)

| | | | |

Equity Real Estate Investment Trusts | | | 11.0% | |

Banks | | | 5.8% | |

Insurance | | | 5.1% | |

Machinery | | | 4.7% | |

Software | | | 4.6% | |

Electronic Equipment, Instruments & Components | | | 4.0% | |

IT Services | | | 3.8% | |

Health Care Equipment & Supplies | | | 3.7% | |

Capital Markets | | | 3.4% | |

Chemicals | | | 2.9% | |

Food Products | | | 2.8% | |

Hotels, Restaurants & Leisure | | | 2.6% | |

Semiconductors & Semiconductor Equipment | | | 2.5% | |

Specialty Retail | | | 2.2% | |

Gas Utilities | | | 2.2% | |

Oil, Gas & Consumable Fuels | | | 2.1% | |

Aerospace & Defense | | | 2.0% | |

Electric Utilities | | | 1.9% | |

Metals & Mining | | | 1.9% | |

Health Care Providers & Services | | | 1.8% | |

Containers & Packaging | | | 1.7% | |

Household Durables | | | 1.5% | |

Communications Equipment | | | 1.5% | |

Energy, Equipment & Services | | | 1.4% | |

Media | | | 1.3% | |

Other | | | 19.0% | |

Common Stock Rights | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 5.6% | |

Money Market Funds | | | 2.3% | |

U.S. Government and Agency Obligations | | | 0.5% | |

Other Assets Less Liabilities | | | (5.8)% | |

Net Assets | | | 100% | |

Top Five Common Stock Holdings

(% of net assets)

| | | | |

Idexx Labs Inc. | | | 0.7% | |

WhiteWave Foods Company | | | 0.6% | |

Everest Reinsurance Group Ltd | | | 0.6% | |

Ingredion Inc. | | | 0.6% | |

Duke Realty Corporation | | | 0.6% | |

Holding Summaries as of October 31, 2016 (continued)

Nuveen Small Cap Index Fund

Fund Allocation

(% of net assets)

| | | | |

Common Stocks | | | 94.3% | |

Exchange-Traded Funds | | | 0.0% | |

Common Stock Rights | | | 0.0% | |

Warrants | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 9.3% | |

Money Market Funds | | | 5.5% | |

U.S. Government and Agency Obligations | | | 0.3% | |

Other Assets Less Liabilities | | | (9.4)% | |

Net Assets | | | 100% | |

Portfolio Composition

(% of net assets)

| | | | |

Banks | | | 9.8% | |

Equity Real Estate Investment Trusts | | | 7.2% | |

Biotechnology | | | 4.5% | |

Software | | | 4.1% | |

Semiconductors & Semiconductor Equipment | | | 3.6% | |

Machinery | | | 3.3% | |

Health Care Equipment & Supplies | | | 3.0% | |

Hotels, Restaurants & Leisure | | | 2.8% | |

Electronic Equipment, Instruments & Components | | | 2.7% | |

Internet Software & Services | | | 2.4% | |

Chemicals | | | 2.3% | |

Specialty Retail | | | 2.3% | |

Insurance | | | 2.2% | |

Commercial Services & Supplies | | | 2.2% | |

Thrifts & Mortgage Finance | | | 2.1% | |

Oil, Gas & Consumable Fuels | | | 2.1% | |

Health Care Providers & Services | | | 2.0% | |

IT Services | | | 2.0% | |

Pharmaceuticals | | | 1.7% | |

Communications Equipment | | | 1.7% | |

Aerospace & Defense | | | 1.5% | |

Media | | | 1.4% | |

Food Products | | | 1.4% | |

Capital Markets | | | 1.3% | |

Professional Services | | | 1.3% | |

Household Durables | | | 1.2% | |

Metals & Mining | | | 1.2% | |

Auto Components | | | 1.2% | |

Other | | | 19.8% | |

Exchange-Traded Funds | | | 0.0% | |

Common Stock Rights | | | 0.0% | |

Warrants | | | 0.0% | |

Investments Purchased with Collateral from Securities Lending | | | 9.3% | |

Money Market Funds | | | 5.5% | |

U.S. Government and Agency Obligations | | | 0.3% | |

Other Assets Less Liabilities | | | (9.4)% | |

Net Assets | | | 100% | |

Top Five Common Stock Holdings

(% of net assets)

| | | | |

Advanced Micro Devices, Inc. | | | 0.3% | |

Microsemi Corporation | | | 0.3% | |

Aspen Technology Inc. | | | 0.2% | |

Curtiss Wright Corporation | | | 0.2% | |

IDACORP, INC | | | 0.2% | |

Expense

Examples

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through the period ended October 31, 2016.

The beginning of the period is May 1, 2016.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Equity Index Fund

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Actual Performance | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,037.80 | | | $ | 1,033.50 | | | $ | 1,036.50 | | | $ | 1,039.10 | |

Expenses Incurred During Period | | $ | 3.07 | | | $ | 6.90 | | | $ | 4.35 | | | $ | 1.79 | |

Hypothetical Performance (5% annualized return before expenses) | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,022.12 | | | $ | 1,018.35 | | | $ | 1,020.86 | | | $ | 1,023.38 | |

Expenses Incurred During Period | | $ | 3.05 | | | $ | 6.85 | | | $ | 4.32 | | | $ | 1.78 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 0.60%, 1.35%, 0.85% and 0.35% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Expense Examples (continued)

Nuveen Mid Cap Index Fund

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Actual Performance | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,037.60 | | | $ | 1,033.70 | | | $ | 1,036.40 | | | $ | 1,039.30 | |

Expenses Incurred During Period | | $ | 3.43 | | | $ | 7.21 | | | $ | 4.66 | | | $ | 2.10 | |

Hypothetical Performance (5% annualized return before expenses) | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,021.77 | | | $ | 1,018.05 | | | $ | 1,020.56 | | | $ | 1,023.08 | |

Expenses Incurred During Period | | $ | 3.40 | | | $ | 7.15 | | | $ | 4.62 | | | $ | 2.08 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 0.67%, 1.41%, 0.91% and 0.41% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Nuveen Small Cap Index Fund

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Actual Performance | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,058.40 | | | $ | 1,054.30 | | | $ | 1,056.90 | | | $ | 1,059.80 | |

Expenses Incurred During Period | | $ | 4.09 | | | $ | 7.95 | | | $ | 5.38 | | | $ | 2.80 | |

Hypothetical Performance (5% annualized return before expenses) | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,021.17 | | | $ | 1,017.39 | | | $ | 1,019.91 | | | $ | 1,022.42 | |

Expenses Incurred During Period | | $ | 4.01 | | | $ | 7.81 | | | $ | 5.28 | | | $ | 2.75 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 0.79%, 1.54%, 1.04% and 0.54% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Report of

Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of

Nuveen Investment Funds, Inc.:

In our opinion, the accompanying statements of assets and liabilities, including the portfolios of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Nuveen Equity Index Fund, Nuveen Mid Cap Index Fund and Nuveen Small Cap Index Fund (each a series of the Nuveen Investment Funds, Inc., hereinafter referred to as the “Funds”) at October 31, 2016, the results of each of their operations for the year then ended, the changes in each of their net assets for each of the two years in the period then ended and the financial highlights for the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2016 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

As disclosed in Note 9 – Subsequent Events of the Notes to Financial Statements, after the close of business on April 27, 2017, the Funds will liquidate any remaining shareholder accounts and cease operations.

PricewaterhouseCoopers LLP

Chicago, IL

December 28, 2016

Nuveen Equity Index Fund

| | |

| Portfolio of Investments | | October 31, 2016 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | LONG-TERM INVESMTENTS – 95.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | COMMON STOCKS – 95.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Aerospace & Defense – 2.1% | | | | | | | | | | | | |

| | | | | |

| | 21,619 | | | Boeing Company | | | | | | | | | | | | | | $ | 3,079,194 | |

| | | | | |

| | 10,694 | | | General Dynamics Corporation | | | | | | | | | | | | | | | 1,612,014 | |

| | | | | |

| | 3,019 | | | L-3 Communications Holdings, Inc. | | | | | | | | | | | | | | | 413,422 | |

| | | | | |

| | 9,406 | | | Lockheed Martin Corporation | | | | | | | | | | | | | | | 2,317,450 | |

| | | | | |

| | 6,654 | | | Northrop Grumman Corporation | | | | | | | | | | | | | | | 1,523,766 | |

| | | | | |

| | 11,602 | | | Raytheon Company | | | | | | | | | | | | | | | 1,584,949 | |

| | | | | |

| | 4,888 | | | Rockwell Collins, Inc. | | | | | | | | | | | | | | | 412,156 | |

| | | | | |

| | 10,522 | | | Textron Inc. | | | | | | | | | | | | | | | 421,722 | |

| | | | | |

| | 1,242 | | | TransDigm Group Inc., (2) | | | | | | | | | | | | | | | 338,395 | |

| | | | | |

| | 30,186 | | | United Technologies Corporation | | | | | | | | | | | | | | | 3,085,009 | |

| | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 14,788,077 | |

| | | | | |

| | | | Air Freight & Logistics – 0.7% | | | | | | | | | | | | |

| | | | | |

| | 5,690 | | | C.H. Robinson Worldwide, Inc. | | | | | | | | | | | | | | | 387,603 | |

| | | | | |

| | 7,067 | | | Expeditors International of Washington, Inc. | | | | | | | | | | | | | | | 363,738 | |

| | | | | |

| | 9,103 | | | FedEx Corporation | | | | | | | | | | | | | | | 1,586,835 | |

| | | | | |

| | 25,760 | | | United Parcel Service, Inc., Class B | | | | | | | | | | | | | | | 2,775,898 | |

| | | | Total Air Freight & Logistics | | | | | | | | | | | | | | | 5,114,074 | |

| | | | | |

| | | | Airlines – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 782 | | | Alaska Air Group, Inc. | | | | | | | | | | | | | | | 56,476 | |

| | | | | |

| | 20,610 | | | American Airlines Group Inc. | | | | | | | | | | | | | | | 836,766 | |

| | | | | |

| | 29,128 | | | Delta Air Lines, Inc. | | | | | | | | | | | | | | | 1,216,677 | |

| | | | | |

| | 24,760 | | | Southwest Airlines Co. | | | | | | | | | | | | | | | 991,638 | |

| | | | | |

| | 13,038 | | | United Continental Holdings Inc., (2) | | | | | | | | | | | | | | | 733,127 | |

| | | | Total Airlines | | | | | | | | | | | | | | | 3,834,684 | |

| | | | | |

| | | | Auto Components – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 3,517 | | | Adient PLC, (2) | | | | | | | | | | | | | | | 160,084 | |

| | | | | |

| | 7,505 | | | BorgWarner Inc. | | | | | | | | | | | | | | | 268,979 | |

| | | | | |

| | 10,164 | | | Delphi Automotive PLC | | | | | | | | | | | | | | | 661,371 | |

| | | | | |

| | 10,363 | | | Goodyear Tire & Rubber Company | | | | | | | | | | | | | | | 300,838 | |

| | | | Total Auto Components | | | | | | | | | | | | | | | 1,391,272 | |

| | | | | |

| | | | Automobiles – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 145,417 | | | Ford Motor Company | | | | | | | | | | | | | | | 1,707,196 | |

| | | | | |

| | 51,842 | | | General Motors Company | | | | | | | | | | | | | | | 1,638,207 | |

| | | | | |

| | 6,663 | | | Harley-Davidson, Inc. | | | | | | | | | | | | | | | 379,924 | |

| | | | Total Automobiles | | | | | | | | | | | | | | | 3,725,327 | |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Banks – 5.5% | | | | | | | | | | | | |

| | | | | |

| | 380,265 | | | Bank of America Corporation | | | | | | | | | | | | | | $ | 6,274,373 | |

| | | | | |

| | 31,443 | | | BB&T Corporation | | | | | | | | | | | | | | | 1,232,566 | |

| | | | | |

| | 108,264 | | | Citigroup Inc. | | | | | | | | | | | | | | | 5,321,176 | |

| | | | | |

| | 8,058 | | | Citizens Financial Group Inc. | | | | | | | | | | | | | | | 212,248 | |

| | | | | |

| | 7,141 | | | Comerica Incorporated | | | | | | | | | | | | | | | 371,975 | |

| | | | | |

| | 34,253 | | | Fifth Third Bancorp. | | | | | | | | | | | | | | | 745,345 | |

| | | | | |

| | 32,229 | | | Huntington BancShares Inc. | | | | | | | | | | | | | | | 341,627 | |

| | | | | |

| | 134,595 | | | JP Morgan Chase & Co. | | | | | | | | | | | | | | | 9,322,050 | |

| | | | | |

| | 33,744 | | | KeyCorp. | | | | | | | | | | | | | | | 476,465 | |

| | | | | |

| | 5,767 | | | M&T Bank Corporation | | | | | | | | | | | | | | | 707,784 | |

| | | | | |

| | 12,440 | | | People’s United Financial, Inc. | | | | | | | | | | | | | | | 202,026 | |

| | | | | |

| | 18,312 | | | PNC Financial Services Group, Inc. | | | | | | | | | | | | | | | 1,750,627 | |

| | | | | |

| | 53,171 | | | Regions Financial Corporation | | | | | | | | | | | | | | | 569,461 | |

| | | | | |

| | 20,341 | | | SunTrust Banks, Inc. | | | | | | | | | | | | | | | 920,023 | |

| | | | | |

| | 59,951 | | | U.S. Bancorp | | | | | | | | | | | | | | | 2,683,407 | |

| | | | | |

| | 169,212 | | | Wells Fargo & Company | | | | | | | | | | | | | | | 7,785,444 | |

| | | | | |

| | 8,340 | | | Zions Bancorporation | | | | | | | | | | | | | | | 268,631 | |

| | | | Total Banks | | | | | | | | | | | | | | | 39,185,228 | |

| | | | | |

| | | | Beverages – 2.1% | | | | | | | | | | | | |

| | | | | |

| | 6,797 | | | Brown-Forman Corporation | | | | | | | | | | | | | | | 313,817 | |

| | | | | |

| | 141,956 | | | Coca-Cola Company | | | | | | | | | | | | | | | 6,018,934 | |

| | | | | |

| | 6,903 | | | Constellation Brands, Inc., Class A | | | | | | | | | | | | | | | 1,153,629 | |

| | | | | |

| | 7,661 | | | Dr. Pepper Snapple Group | | | | | | | | | | | | | | | 672,559 | |

| | | | | |

| | 7,172 | | | Molson Coors Brewing Company, Class B | | | | | | | | | | | | | | | 744,525 | |

| | | | | |

| | 5,037 | | | Monster Beverage Corporation, (2) | | | | | | | | | | | | | | | 727,041 | |

| | | | | |

| | 53,627 | | | PepsiCo, Inc. | | | | | | | | | | | | | | | 5,748,814 | |

| | | | Total Beverages | | | | | | | | | | | | | | | 15,379,319 | |

| | | | | |

| | | | Biotechnology – 2.6% | | | | | | | | | | | | |

| | | | | |

| | 60,686 | | | AbbVie Inc. | | | | | | | | | | | | | | | 3,385,065 | |

| | | | | |

| | 8,356 | | | Alexion Pharmaceuticals Inc., (2) | | | | | | | | | | | | | | | 1,090,458 | |

| | | | | |

| | 27,887 | | | Amgen Inc. | | | | | | | | | | | | | | | 3,936,529 | |

| | | | | |

| | 8,165 | | | Biogen Inc., (2) | | | | | | | | | | | | | | | 2,287,670 | |

| | | | | |

| | 28,884 | | | Celgene Corporation, (2) | | | | | | | | | | | | | | | 2,951,367 | |

| | | | | |

| | 49,174 | | | Gilead Sciences, Inc. | | | | | | | | | | | | | | | 3,620,682 | |

| | | | | |

| | 2,812 | | | Regeneron Pharmaceuticals, Inc., (2) | | | | | | | | | | | | | | | 970,196 | |

| | | | | |

| | 9,233 | | | Vertex Pharmaceuticals Inc., (2) | | | | | | | | | | | | | | | 700,415 | |

| | | | Total Biotechnology | | | | | | | | | | | | | | | 18,942,382 | |

| | | | | |

| | | | Building Products – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 3,729 | | | Allegion PLC | | | | | | | | | | | | | | | 238,059 | |

Nuveen Equity Index Fund (continued)

| | |

| Portfolio of Investments | | October 31, 2016 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Building Products (continued) | | | | | | | | | | | | |

| | | | | |

| | 2,840 | | | Fortune Brands Home & Security | | | | | | | | | | | | | | $ | 155,149 | |

| | | | | |

| | 35,175 | | | Johnson Controls International PLC | | | | | | | | | | | | | | | 1,418,256 | |

| | | | | |

| | 12,958 | | | Masco Corporation | | | | | | | | | | | | | | | 400,143 | |

| | | | Total Building Products | | | | | | | | | | | | | | | 2,211,607 | |

| | | | | |

| | | | Capital Markets – 2.5% | | | | | | | | | | | | |

| | | | | |

| | 2,007 | | | Affiliated Managers Group Inc., (2) | | | | | | | | | | | | | | | 266,249 | |

| | | | | |

| | 6,016 | | | Ameriprise Financial, Inc. | | | | | | | | | | | | | | | 531,754 | |

| | | | | |

| | 39,786 | | | Bank New York Mellon | | | | | | | | | | | | | | | 1,721,540 | |

| | | | | |

| | 4,547 | | | BlackRock Inc. | | | | | | | | | | | | | | | 1,551,618 | |

| | | | | |

| | 44,862 | | | Charles Schwab Corporation | | | | | | | | | | | | | | | 1,422,125 | |

| | | | | |

| | 12,627 | | | CME Group, Inc. | | | | | | | | | | | | | | | 1,263,963 | |

| | | | | |

| | 12,615 | | | E*Trade Group Inc., (2) | | | | | | | | | | | | | | | 355,238 | |

| | | | | |

| | 13,096 | | | Franklin Resources, Inc. | | | | | | | | | | | | | | | 440,811 | |

| | | | | |

| | 14,052 | | | Goldman Sachs Group, Inc. | | | | | | | | | | | | | | | 2,504,628 | |

| | | | | |

| | 4,435 | | | Intercontinental Exchange Group, Inc. | | | | | | | | | | | | | | | 1,199,180 | |

| | | | | |

| | 15,274 | | | Invesco LTD | | | | | | | | | | | | | | | 429,047 | |

| | | | | |

| | 3,436 | | | Legg Mason, Inc. | | | | | | | | | | | | | | | 98,682 | |

| | | | | |

| | 6,729 | | | Moody’s Corporation | | | | | | | | | | | | | | | 676,399 | |

| | | | | |

| | 54,855 | | | Morgan Stanley | | | | | | | | | | | | | | | 1,841,482 | |

| | | | | |

| | 5,009 | | | NASDAQ Stock Market, Inc. | | | | | | | | | | | | | | | 320,426 | |

| | | | | |

| | 7,936 | | | Northern Trust Corporation | | | | | | | | | | | | | | | 574,725 | |

| | | | | |

| | 10,295 | | | S&P Global, Inc. | | | | | | | | | | | | | | | 1,254,446 | |

| | | | | |

| | 13,661 | | | State Street Corporation | | | | | | | | | | | | | | | 959,139 | |

| | | | | |

| | 9,261 | | | T. Rowe Price Group Inc. | | | | | | | | | | | | | | | 592,797 | |

| | | | Total Capital Markets | | | | | | | | | | | | | | | 18,004,249 | |

| | | | | |

| | | | Chemicals – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 1 | | | AdvanSix, Inc. | | | | | | | | | | | | | | | 8 | |

| | | | | |

| | 7,532 | | | Air Products & Chemicals Inc. | | | | | | | | | | | | | | | 1,004,919 | |

| | | | | |

| | 4,343 | | | Albemarle Corporation | | | | | | | | | | | | | | | 362,858 | |

| | | | | |

| | 9,353 | | | CF Industries Holdings, Inc. | | | | | | | | | | | | | | | 224,566 | |

| | | | | |

| | 41,990 | | | Dow Chemical Company | | | | | | | | | | | | | | | 2,259,482 | |

| | | | | |

| | 32,581 | | | E.I. Du Pont de Nemours and Company | | | | | | | | | | | | | | | 2,241,247 | |

| | | | | |

| | 5,504 | | | Eastman Chemical Company | | | | | | | | | | | | | | | 395,793 | |

| | | | | |

| | 9,625 | | | Ecolab Inc. | | | | | | | | | | | | | | | 1,098,886 | |

| | | | | |

| | 5,363 | | | FMC Corporation | | | | | | | | | | | | | | | 251,471 | |

| | | | | |

| | 2,965 | | | International Flavors & Fragrances Inc. | | | | | | | | | | | | | | | 387,763 | |

| | | | | |

| | 12,702 | | | LyondellBasell Industries NV | | | | | | | | | | | | | | | 1,010,444 | |

| | | | | |

| | 16,306 | | | Monsanto Company | | | | | | | | | | | | | | | 1,643,156 | |

| | | | | |

| | 13,125 | | | Mosaic Company | | | | | | | | | | | | | | | 308,831 | |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Chemicals (continued) | | | | | | | | | | | | |

| | | | | |

| | 9,922 | | | PPG Industries, Inc. | | | | | | | | | | | | | | $ | 924,036 | |

| | | | | |

| | 10,741 | | | Praxair, Inc. | | | | | | | | | | | | | | | 1,257,341 | |

| | | | | |

| | 2,989 | | | Sherwin-Williams Company | | | | | | | | | | | | | | | 731,887 | |

| | | | Total Chemicals | | | | | | | | | | | | | | | 14,102,688 | |

| | | | | |

| | | | Commercial Services & Supplies – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 3,399 | | | Cintas Corporation | | | | | | | | | | | | | | | 362,571 | |

| | | | | |

| | 6,915 | | | Pitney Bowes Inc. | | | | | | | | | | | | | | | 123,364 | |

| | | | | |

| | 9,234 | | | Republic Services, Inc. | | | | | | | | | | | | | | | 485,985 | |

| | | | | |

| | 3,405 | | | Stericycle Inc., (2) | | | | | | | | | | | | | | | 272,706 | |

| | | | | |

| | 16,083 | | | Waste Management, Inc. | | | | | | | | | | | | | | | 1,056,010 | |

| | | | Total Commercial Services & Supplies | | | | | | | | | | | | | | | 2,300,636 | |

| | | | | |

| | | | Communications Equipment – 1.0% | | | | | | | | | | | | |

| | | | | |

| | 187,425 | | | Cisco Systems, Inc. | | | | | | | | | | | | | | | 5,750,199 | |

| | | | | |

| | 2,468 | | | F5 Networks, Inc., (2) | | | | | | | | | | | | | | | 341,102 | |

| | | | | |

| | 4,578 | | | Harris Corporation | | | | | | | | | | | | | | | 408,403 | |

| | | | | |

| | 14,194 | | | Juniper Networks Inc. | | | | | | | | | | | | | | | 373,870 | |

| | | | | |

| | 6,156 | | | Motorola Solutions Inc. | | | | | | | | | | | | | | | 446,802 | |

| | | | Total Communications Equipment | | | | | | | | | | | | | | | 7,320,376 | |

| | | | | |

| | | | Construction & Engineering – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 5,189 | | | Fluor Corporation | | | | | | | | | | | | | | | 269,776 | |

| | | | | |

| | 4,847 | | | Jacobs Engineering Group, Inc., (2) | | | | | | | | | | | | | | | 250,008 | |

| | | | | |

| | 6,535 | | | Quanta Services Incorporated, (2) | | | | | | | | | | | | | | | 187,881 | |

| | | | Total Construction & Engineering | | | | | | | | | | | | | | | 707,665 | |

| | | | | |

| | | | Construction Materials – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 2,285 | | | Martin Marietta Materials | | | | | | | | | | | | | | | 423,593 | |

| | | | | |

| | 5,082 | | | Vulcan Materials Company | | | | | | | | | | | | | | | 575,282 | |

| | | | Total Construction Materials | | | | | | | | | | | | | | | 998,875 | |

| | | | | |

| | | | Consumer Finance – 0.7% | | | | | | | | | | | | |

| | | | | |

| | 28,916 | | | American Express Company | | | | | | | | | | | | | | | 1,920,601 | |

| | | | | |

| | 18,858 | | | Capital One Financial Corporation | | | | | | | | | | | | | | | 1,396,246 | |

| | | | | |

| | 15,041 | | | Discover Financial Services | | | | | | | | | | | | | | | 847,260 | |

| | | | | |

| | 13,898 | | | Navient Corporation | | | | | | | | | | | | | | | 177,616 | |

| | | | | |

| | 23,362 | | | Synchrony Financial | | | | | | | | | | | | | | | 667,920 | |

| | | | Total Consumer Finance | | | | | | | | | | | | | | | 5,009,643 | |

| | | | | |

| | | | Containers & Packaging – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 3,670 | | | Avery Dennison Corporation | | | | | | | | | | | | | | | 256,129 | |

| | | | | |

| | 5,545 | | | Ball Corporation | | | | | | | | | | | | | | | 427,353 | |

| | | | | |

| | 15,955 | | | International Paper Company | | | | | | | | | | | | | | | 718,454 | |

| | | | | |

| | 6,135 | | | Owens-Illinois, Inc., (2) | | | | | | | | | | | | | | | 118,406 | |

Nuveen Equity Index Fund (continued)

| | |

| Portfolio of Investments | | October 31, 2016 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Containers & Packaging (continued) | | | | | | | | | | | | |

| | | | | |

| | 7,605 | | | Sealed Air Corporation | | | | | | | | | | | | | | $ | 347,016 | |

| | | | | |

| | 9,850 | | | WestRock Company | | | | | | | | | | | | | | | 454,972 | |

| | | | Total Containers & Packaging | | | | | | | | | | | | | | | 2,322,330 | |

| | | | | |

| | | | Distributors – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 5,550 | | | Genuine Parts Company | | | | | | | | | | | | | | | 502,775 | |

| | | | | |

| | 9,149 | | | LKQ Corporation, (2) | | | | | | | | | | | | | | | 295,330 | |

| | | | Total Distributors | | | | | | | | | | | | | | | 798,105 | |

| | | | | |

| | | | Diversified Consumer Services – 0.0% | | | | | | | | | | | | |

| | | | | |

| | 8,165 | | | H & R Block Inc. | | | | | | | | | | | | | | | 187,550 | |

| | | | | |

| | | | Diversified Financial Services – 1.5% | | | | | | | | | | | | |

| | | | | |

| | 70,751 | | | Berkshire Hathaway Inc., Class B, (2) | | | | | | | | | | | | | | | 10,209,369 | |

| | | | | |

| | 13,797 | | | Leucadia National Corporation | | | | | | | | | | | | | | | 257,590 | |

| | | | Total Diversified Financial Services | | | | | | | | | | | | | | | 10,466,959 | |

| | | | | |

| | | | Diversified Telecommunication Services – 2.4% | | | | | | | | | | | | |

| | | | | |

| | 229,244 | | | AT&T Inc. | | | | | | | | | | | | | | | 8,433,887 | |

| | | | | |

| | 20,345 | | | CenturyLink Inc. | | | | | | | | | | | | | | | 540,770 | |

| | | | | |

| | 44,316 | | | Frontier Communications Corporation, (3) | | | | | | | | | | | | | | | 178,150 | |

| | | | | |

| | 11,570 | | | Level 3 Communications Inc., (2) | | | | | | | | | | | | | | | 649,656 | |

| | | | | |

| | 151,885 | | | Verizon Communications Inc. | | | | | | | | | | | | | | | 7,305,670 | |

| | | | Total Diversified Telecommunication Services | | | | | | | | | | | | | | | 17,108,133 | |

| | | | | |

| | | | Electric Utilities – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 6,028 | | | Alliant Energy Corporation | | | | | | | | | | | | | | | 229,365 | |

| | | | | |

| | 18,323 | | | American Electric Power Company, Inc. | | | | | | | | | | | | | | | 1,188,063 | |

| | | | | |

| | 25,673 | | | Duke Energy Corporation | | | | | | | | | | | | | | | 2,054,353 | |

| | | | | |

| | 12,444 | | | Edison International | | | | | | | | | | | | | | | 914,385 | |

| | | | | |

| | 6,670 | | | Entergy Corporation | | | | | | | | | | | | | | | 491,446 | |

| | | | | |

| | 11,820 | | | Eversource Energy | | | | | | | | | | | | | | | 650,809 | |

| | | | | |

| | 34,389 | | | Exelon Corporation | | | | | | | | | | | | | | | 1,171,633 | |

| | | | | |

| | 15,844 | | | FirstEnergy Corp. | | | | | | | | | | | | | | | 543,291 | |

| | | | | |

| | 17,405 | | | NextEra Energy Inc. | | | | | | | | | | | | | | | 2,227,840 | |

| | | | | |

| | 18,576 | | | PG&E Corporation | | | | | | | | | | | | | | | 1,153,941 | |

| | | | | |

| | 4,447 | | | Pinnacle West Capital Corporation | | | | | | | | | | | | | | | 338,550 | |

| | | | | |

| | 25,268 | | | PPL Corporation | | | | | | | | | | | | | | | 867,703 | |

| | | | | |

| | 35,423 | | | Southern Company | | | | | | | | | | | | | | | 1,826,764 | |

| | | | | |

| | 19,695 | | | Xcel Energy, Inc., (3) | | | | | | | | | | | | | | | 818,327 | |

| | | | Total Electric Utilities | | | | | | | | | | | | | | | 14,476,470 | |

| | | | | |

| | | | Electrical Equipment – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 958 | | | Acuity Brands Inc. | | | | | | | | | | | | | | | 214,180 | |

| | | | | |

| | 9,141 | | | Ametek Inc. | | | | | | | | | | | | | | | 403,118 | |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Electrical Equipment (continued) | | | | | | | | | | | | |

| | | | | |

| | 17,289 | | | Eaton PLC | | | | | | | | | | | | | | $ | 1,102,520 | |

| | | | | |

| | 23,981 | | | Emerson Electric Company | | | | | | | | | | | | | | | 1,215,357 | |

| | | | | |

| | 5,381 | | | Rockwell Automation, Inc. | | | | | | | | | | | | | | | 644,213 | |

| | | | Total Electrical Equipment | | | | | | | | | | | | | | | 3,579,388 | |

| | | | | |

| | | | Electronic Equipment, Instruments & Components – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 11,505 | | | Amphenol Corporation, Class A | | | | | | | | | | | | | | | 758,525 | |

| | | | | |

| | 43,185 | | | Corning Incorporated | | | | | | | | | | | | | | | 980,731 | |

| | | | | |

| | 5,115 | | | FLIR Systems Inc. | | | | | | | | | | | | | | | 168,386 | |

| | | | | |

| | 13,250 | | | TE Connectivity Limited | | | | | | | | | | | | | | | 833,028 | |

| | | | Total Electronic Equipment, Instruments & Components | | | | | | | | | | | | | | | 2,740,670 | |

| | | | | |

| | | | Energy Equipment & Services – 1.0% | | | | | | | | | | | | |

| | | | | |

| | 15,946 | | | Baker Hughes Incorporated | | | | | | | | | | | | | | | 883,408 | |

| | | | | |

| | 8,408 | | | FMC Technologies Inc., (2) | | | | | | | | | | | | | | | 271,326 | |

| | | | | |

| | 32,088 | | | Halliburton Company | | | | | | | | | | | | | | | 1,476,048 | |

| | | | | |

| | 3,941 | | | Helmerich & Payne Inc. | | | | | | | | | | | | | | | 248,717 | |

| | | | | |

| | 14,071 | | | National-Oilwell Varco Inc. | | | | | | | | | | | | | | | 451,679 | |

| | | | | |

| | 51,822 | | | Schlumberger Limited | | | | | | | | | | | | | | | 4,054,035 | |

| | | | | |

| | 12,798 | | | Transocean Inc., (3) | | | | | | | | | | | | | | | 122,989 | |

| | | | Total Energy Equipment & Services | | | | | | | | | | | | | | | 7,508,202 | |

| | | | | |

| | | | Equity Real Estate Investment Trust – 2.8% | | | | | | | | | | | | |

| | | | | |

| | 15,855 | | | American Tower Corporation | | | | | | | | | | | | | | | 1,858,047 | |

| | | | | |

| | 6,271 | | | Apartment Investment & Management Company, Class A | | | | | | | | | | | | | | | 276,363 | |

| | | | | |

| | 5,116 | | | AvalonBay Communities, Inc. | | | | | | | | | | | | | | | 875,757 | |

| | | | | |

| | 5,727 | | | Boston Properties, Inc., (3) | | | | | | | | | | | | | | | 689,989 | |

| | | | | |

| | 12,579 | | | Crown Castle International Corporation | | | | | | | | | | | | | | | 1,144,563 | |

| | | | | |

| | 5,712 | | | Digital Realty Trust Inc., (3) | | | | | | | | | | | | | | | 533,672 | |

| | | | | |

| | 2,734 | | | Equinix Inc. | | | | | | | | | | | | | | | 976,804 | |

| | | | | |

| | 13,621 | | | Equity Residential | | | | | | | | | | | | | | | 841,097 | |

| | | | | |

| | 1,855 | | | Essex Property Trust Inc. | | | | | | | | | | | | | | | 397,137 | |

| | | | | |

| | 4,688 | | | Extra Space Storage Inc. | | | | | | | | | | | | | | | 342,927 | |

| | | | | |

| | 2,643 | | | Federal Realty Investment Trust | | | | | | | | | | | | | | | 383,843 | |

| | | | | |

| | 21,759 | | | General Growth Properties Inc. | | | | | | | | | | | | | | | 542,887 | |

| | | | | |

| | 17,424 | | | Health Care Property Investors Inc. | | | | | | | | | | | | | | | 596,772 | |

| | | | | |

| | 27,667 | | | Host Hotels & Resorts Inc. | | | | | | | | | | | | | | | 428,285 | |

| | | | | |

| | 7,699 | | | Iron Mountain Inc. | | | | | | | | | | | | | | | 259,687 | |

| | | | | |

| | 15,652 | | | Kimco Realty Corporation | | | | | | | | | | | | | | | 416,500 | |

| | | | | |

| | 4,495 | | | Macerich Company | | | | | | | | | | | | | | | 318,156 | |

| | | | | |

| | 19,635 | | | Prologis Inc. | | | | | | | | | | | | | | | 1,024,162 | |

| | | | | |

| | 5,556 | | | Public Storage, Inc. | | | | | | | | | | | | | | | 1,187,428 | |

Nuveen Equity Index Fund (continued)

| | |

| Portfolio of Investments | | October 31, 2016 |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | | |

| | | | Equity Real Estate Investment Trust (continued) | | | | | | | | | | | | |

| | | | | |

| | 9,834 | | | Realty Income Corporation | | | | | | | | | | | | | | $ | 582,566 | |

| | | | | |

| | 11,709 | | | Simon Property Group, Inc. | | | | | | | | | | | | | | | 2,177,406 | |

| | | | | |

| | 4,109 | | | SL Green Realty Corporation | | | | | | | | | | | | | | | 403,586 | |

| | | | | |

| | 9,911 | | | UDR Inc. | | | | | | | | | | | | | | | 346,588 | |

| | | | | |

| | 13,092 | | | Ventas Inc. | | | | | | | | | | | | | | | 886,983 | |

| | | | | |

| | 6,403 | | | Vornado Realty Trust | | | | | | | | | | | | | | | 594,070 | |

| | | | | |

| | 13,338 | | | Welltower Inc. | | | | | | | | | | | | | | | 914,053 | |

| | | | | |

| | 27,900 | | | Weyerhaeuser Company | | | | | | | | | | | | | | | 835,047 | |