UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kathleen L. Prudhomme

Vice President and Secretary

901 Marquette Avenue

Minneapolis, Minnesota 55402

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | |

| | |  |

| Mutual Funds | |

| | | | | | |

| | | | | | | Annual Report June 30, 2017 |

| | | | | | | | | | | | | | | | | | |

| | | | | | | Share Class / Ticker Symbol | | |

| | | Fund Name | | | | Class A | | Class C | | Class R3 | | Class R6 | | Class I | | Class T | | |

| | |

| | Nuveen Core Bond Fund | | | | FAIIX | | NTIBX | | — | | NTIFX | | FINIX | | FIDTX | | |

| | Nuveen Core Plus Bond Fund | | | | FAFIX | | FFAIX | | FFISX | | FPCFX | | FFIIX | | FFITX | | |

| | Nuveen High Income Bond Fund | | | | FJSIX | | FCSIX | | FANSX | | — | | FJSYX | | FCPTX | | |

| | Nuveen Inflation Protected Securities Fund | | | | FAIPX | | FCIPX | | FRIPX | | FISFX | | FYIPX | | FIFTX | | |

| | Nuveen Intermediate Government Bond Fund | | | | FIGAX | | FYGCX | | FYGRX | | — | | FYGYX | | FYGTX | | |

| | Nuveen Short Term Bond Fund | | | | FALTX | | FBSCX | | NSSRX | | NSSFX | | FLTIX | | NSATX | | |

| | Nuveen Strategic Income Fund | | | | FCDDX | | FCBCX | | FABSX | | FSFRX | | FCBYX | | FSFTX | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| | |

| | Life is Complex. | | |

| | |

| | Nuveen makes things e-simple. | | |

| | |

| | It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. | | |

| | | | |

| | | | | | Free e-Reports right to your e-mail! | | |

| | | |

| | | | | | www.investordelivery.com If you receive your Nuveen Fund distributions and statements from your

financial advisor or brokerage account. |

| | | | |

| | | | or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund distributions and statements directly from Nuveen. Must be preceded by or accompanied by a prospectus. NOT FDIC INSURED MAY LOSE VALUE

NO BANK GUARANTEE | | |

| | | | | | | | | | |

| | | | | | | | | | | | | |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

Some of the key assumptions driving the markets higher at the beginning of 2017 have recently come into question. Following the collapse of the health care reform bill in the Senate, progress on the rest of the White House’s pro-growth fiscal agenda, including tax reform and large infrastructure projects, is expected to be delayed. Economic growth projections, in turn, have been lowered, and with inflation recently waning, the markets are expecting fewer rate hikes from the Federal Reserve (Fed) than the Fed itself had predicted. Yet, asset prices continued to rise.

Investors have largely looked beyond policy disappointments and focused instead on the healthy profits reported by U.S. companies during the first two quarters of 2017. U.S. growth has remained slow and steady, European growth has surprised to the upside and concern that China would decelerate too rapidly has eased, further contributing to an optimistic tone in the markets. Additionally, political risk in Europe has moderated, with the election of mainstream candidates in the Dutch and French elections earlier this year.

The remainder of the year could bring challenges to this benign macro environment. The debt ceiling looms, with a vote needed from Congress to raise or suspend the nation’s borrowing limit before the Treasury is unable to pay its bills in full or on time (likely in early October). The mechanics of the U.K.’s separation from the European Union remain to be seen, as “Brexit” negotiations develop. A tightening of financial conditions in China or a more aggressive-than-expected policy action from the Fed, European Central Bank or Bank of Japan could also turn into headwinds.

Market volatility readings have been remarkably low lately, but conditions can change quickly. As market conditions evolve, Nuveen remains committed to rigorously assessing opportunities and risks. If you’re concerned about how resilient your investment portfolio might be, we encourage you to talk to your financial advisor. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

August 23, 2017

Portfolio Managers’

Comments

Nuveen Core Bond Fund

Nuveen Core Plus Bond Fund

Nuveen High Income Bond Fund

Nuveen Inflation Protected Securities Fund

Nuveen Intermediate Government Bond Fund

Nuveen Short Term Bond Fund

Nuveen Strategic Income Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen, LLC. In this report, the various portfolio management teams for the Funds discuss the economy and financial markets, key investment strategies and the Funds’ performance for the twelve-month reporting period ended June 30, 2017.

Effective, August 4, 2017 (subsequent to the close of this reporting period), investment policy changes were approved for the Nuveen High Income Bond Fund: Investments in preferred securities and contingent capital securities (CoCos) will be a principal investment strategy of the Fund. Because the fund must invest 80% of its assets in bonds, investments in preferred securities and CoCos, in the aggregate, will be limited to 20% of net assets (assuming no other securities are in the 20% bucket); Nuveen Core-Plus Bond Fund: Investments in preferred securities and CoCos will be a principal investment strategy of the Fund. Investments in preferred securities and CoCos, in the aggregate, will be limited to 15% of net assets; and the Nuveen Strategic Income Fund: The policy requiring the Fund to invest at least 80% of its assets in debt securities will be revised to require the Fund to invest at least 80% of its assets in income producing securities, and preferred securities and CoCos will be added to the list of securities comprising the 80% bucket and investments in preferred securities and CoCos, in the aggregate, will be limited to 20% of net assets.

These management teams include:

Nuveen Core Bond Fund

Jeffrey J. Ebert, Wan-Chong Kung, CFA, Chris J. Neuharth and Jason J. O’Brien, CFA, have been part of the management team for the Fund since 2000, 2002, 2012 and 2016, respectively.

Nuveen Core Plus Bond Fund

Timothy A. Palmer, CFA, has managed the Fund since 2003. Wan-Chong Kung, CFA, Jeffrey J. Ebert and Chris J. Neuharth joined the Fund as portfolio managers in 2001, 2005 and 2006, respectively. Douglas M. Baker, CFA, joined the Fund as portfolio manager in 2016.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives or circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

Nuveen High Income Bond Fund

John T. Fruit, CFA, has managed the Fund since 2006. Jeffrey T. Schmitz, CFA, has been part of the management team for the Fund since 2008

Nuveen Inflation Protected Securities Fund

Wan-Chong Kung, CFA, has managed the Fund since its inception in 2004 and Chad W. Kemper joined the Fund as a portfolio manager in 2010.

Nuveen Intermediate Government Bond Fund

Wan-Chong Kung, CFA, has managed the Fund since 2002. Chris J. Neuharth and Jason J. O’Brien, CFA, have been on the Fund’s management team since 2009.

Nuveen Short Term Bond Fund

Chris J. Neuharth and Peter L. Agrimson, CFA, have been on the management team since 2004 and 2011, respectively. Jason J. O’Brien, CFA, and Mackenzie S. Meyer joined the Fund in 2016.

Nuveen Strategic Income Fund

Timothy A. Palmer, CFA, has managed the Fund since 2005. Jeffrey J. Ebert, Marie A. Newcome, CFA, and Douglas M. Baker, CFA, joined the Fund as co-portfolio managers in 2000, 2011 and 2016, respectively.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended June 30, 2017?

During the twelve-month reporting period, the U.S. economy continued to grow moderately, now ranking the current expansion as the third-longest since World War II, according to the National Bureau of Economic Research. The second half of 2016 saw a short-term boost in economic activity, driven by a one-time jump in exports during the third quarter, but the economy resumed a below-trend pace thereafter. The Bureau of Economic Analysis reported an annual growth rate of 2.6% for the U.S. economy in the second quarter of 2017, as measured by the “advance” estimate of real gross domestic product (GDP), which is the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. By comparison, the annual GDP growth rate in the first quarter of 2017 was 1.2%.

Despite the slowdown in early 2017, other data pointed to positive momentum as the labor market continued to tighten, manufacturing improved and consumer and business confidence surveys reflected optimism about the economy’s prospects. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 4.4% in June 2017 from 4.9% in June 2016 and job gains averaged around 181,000 per month for the past twelve months. The Consumer Price Index (CPI) increased 1.6% over the twelve-month reporting period ended June 30, 2017 on a seasonally adjusted basis, as reported by the Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 1.7% during the same period, slightly below the Federal Reserve’s (Fed) unofficial longer term inflation objective of 2.0%. The housing market also continued to improve, with historically low mortgage rates and low inventory driving home prices higher. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 5.6% annual gain in May 2017 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 4.9% and 5.7%, respectively.

The U.S. economic outlook struck a more optimistic tone, prompting the Fed’s policy making committee to raise its main benchmark interest rate in December 2016, March 2017 and June 2017. These moves were widely expected by the markets and, while the Fed acknowledged in its June 2017 statement that inflation has remained unexpectedly low, an additional increase is anticipated later in 2017 as the Fed seeks to gradually “normalize” interest rates. Also after the June 2017 meeting, the Fed revealed its plan to begin shrinking its balance sheets by allowing a small amount of maturing Treasury and mortgage securities to roll off without reinvestment. The timing of this is less certain, however, as it depends on whether the economy performs in line with the Fed’s expectations.

Politics also dominated the headlines in this reporting period with two major electoral surprises: the U.K.’s vote to leave the European Union and Donald Trump’s win in the U.S. presidential race. Market volatility increased as markets digested the initial shocks,

but generally recovered and, in the case of the “Trump rally,” U.S. equities experienced significant gains. Investors also closely watched elections across Europe. To the markets’ relief, more mainstream candidates were elected in the Dutch and French elections in the spring of 2017. However, Britain’s June 2017 snap election unexpectedly overturned the Conservative Party’s majority in Parliament, which increased uncertainties about the Brexit negotiation process. Additionally, in the U.S., legislative delays with health care reform made President Trump’s plans for tax cuts and other fiscal stimulus look less likely to happen this year.

What strategies were used to manage the Funds during the twelve-month reporting period and how did these strategies influence performance?

All of the Funds continued to employ the same fundamental investment strategies and tactics used previously, although implementation of those strategies depended on the individual characteristics of the portfolios, as well as market conditions. The Funds’ management teams use a highly collaborative, research-driven approach that we believe offers the best opportunity to achieve consistent, superior long-term performance on a risk-adjusted basis across the full range of market environments. During the reporting period, the Funds were generally positioned for an environment of continued moderate economic growth. Nonetheless, during the reporting period we made smaller scaled shifts on an ongoing basis that were geared toward improving each Fund’s profile in response to changing conditions and valuations. These strategic moves are discussed in more detail within each Fund’s section of this report.

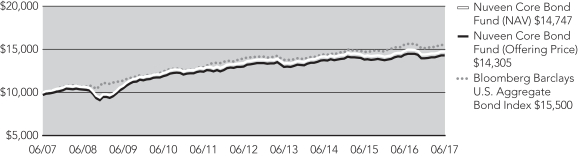

Nuveen Core Bond Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Bloomberg Barclays U.S. Aggregate Bond Index and the Lipper Core Bond Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. However, in the final months of the reporting period, three consecutive months of weaker-than-expected inflation readings were the catalyst for yields to move lower at the long end of the Treasury yield curve. Ten-year Treasury rates rose by more than 115 basis points through mid-March 2017, before falling approximately 30 basis points to end the reporting period about 85 basis points higher.

Around the rest of the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with the improved economic outlook, strong fundamentals and low market volatility, led investment grade corporate bonds to outperform during the reporting period. The segment generated strong excess returns over Treasuries and outperformed all other investment grade sectors despite heavy supply as issuers took advantage of favorable financing conditions and possible shifts in tax policy.

In the securitized sectors, agency mortgage-backed securities (MBS) performed well earlier in the reporting period due to continued bank and foreign purchases of the securities, the range-bound rate environment and lower levels of volatility. However, the sharp rise in interest rates and volatility, as well as relatively large net supply midway through the reporting period, proved to be a difficult environment for these securities. These factors, combined with increased rhetoric and the Fed’s eventual June 2017 announcement regarding plans to end its MBS reinvestments, weighed on agency MBS performance later in the reporting period. Over the full reporting period, agency MBS posted slight excess returns versus duration-matched Treasuries. Despite elevated levels of issuance in the first half of the reporting period, the commercial mortgage-backed securities (CMBS) sector finished the reporting period with a positive excess return over Treasuries. The segment benefited from the risk-on environment, steady demand, investors’ favorable reaction to the new risk retention rules and the associated lower CMBS issuance. However, toward the end of the reporting period, negative headlines surrounding retail loans in the CMBS segment mitigated most of the positive performance, especially for lower rated securities. Consumer related asset-backed securities (ABS) outpaced both the MBS and CMBS sectors, as well as duration-matched Treasuries. Demand for short-duration, high quality yield overshadowed ongoing headlines warning of weaker consumers and auto lending risks.

Sharply rising interest rates were a headwind for the Fund’s performance relative to its benchmark and peers in the first half of the reporting period. More specifically, we had the Fund positioned to benefit from a flatter Treasury yield curve at the time of the

Portfolio Managers’ Comments (continued)

November 2016 election. We did this by overweighting securities in the 10-year and 30-year portions of the yield curve, while underweighting securities with maturities of five years and under. However, the election’s surprising results sparked a sharp increase in rates and a dramatic steepening of the curve, with intermediate and long-term rates rising more than short-term rates. Although we shifted the Fund to a bias for a steeper yield curve as we neared the end of 2016, we did not make the move quickly enough. As a result, our yield curve positioning in the first half of the reporting period detracted the most from the Fund’s results. We also maintained a strategically short duration, or interest rate sensitivity, versus the benchmark during much of the reporting period, while tactically trading rates throughout. In aggregate, these duration moves detracted modestly from the Fund’s performance.

Conversely, our sector positioning had a positive impact on the Fund’s relative returns versus the benchmark. Given our longer-term outlook for moderate economic growth and a stable economy, we maintained the Fund’s approximately 10% overweight versus the benchmark in investment grade credit for much of the reporting period, which boosted results. Toward the end of the reporting period, we increased this overweight even further. Within corporates, our overweight to BBB rated credit was particularly beneficial due to the segment’s excess returns versus higher rated segments of the investment grade market. Also, our overweight positions in financials and industrials within investment grade credit generated excess returns.

In aggregate, our exposures in securitized sectors had little impact on the Fund’s results. On the positive side, the Fund’s performance benefited from our overweight exposure to high quality, short maturity ABS, which we increased slightly as the reporting period progressed. These securities benefited from strong demand for yield at the front end of the yield curve and the sector outperformed despite a relatively heavy new issuance calendar. The Fund’s overweight exposure to the CMBS sector was also modestly beneficial, especially our bias toward securities rated below AAA because these securities outperformed. On the other hand, the Fund’s underweight to agency MBS in the first half of the reporting period was a slight drag on performance because the sector produced excess returns. Also, within the MBS segment, the Fund’s overweight to 30-year MBS detracted because longer maturity MBS underperformed the rest of the segment toward the end of 2016.

We maintained essentially the same overarching investment themes during the reporting period. We maintained a portfolio duration that is modestly shorter than the benchmark and an underweight to the front end of the Treasury yield curve. As of the end of the reporting period, we had the Fund positioned to benefit from a flatter yield curve with a modest overweight in intermediate to longer maturity securities. This positioning was in response to weaker inflation numbers and the lack of any meaningful progress on various initiatives in Washington.

We also maintained the Fund’s focus on generating above market income by investing primarily in securities from the investment grade corporate and securitized sectors, with an emphasis on individual security selection. We believe the macro-economic backdrop remains constructive for these spread sectors because credit fundamentals are steady and investors’ continued quest for yield should keep spreads firm. However, valuations in the corporate market have meaningfully richened. While we don’t see a catalyst for significant spread widening in the near term, valuations at these levels warrant a strong focus on bottom-up fundamental research. We have maintained the Fund’s overweight position in investment grade credit with a bias toward securities in the financial and industrial sectors. Within investment grade, we are also maintaining an overweight in BBB rated credit versus the benchmark. In the MBS sector, we are positioned with a modest underweight to the sector because we expect to see some weakness after the Fed’s schedule to begin unwinding its balance sheet becomes more concrete. We are also maintaining overweight exposure in short maturity ABS versus the benchmark. We believe the short end of the ABS curve still offers value to investors versus positions in short maturity Treasuries. We continue to overweight the CMBS sector in the Fund’s portfolio.

In addition, we continued to use various derivative instruments in the Fund during the reporting period. We used U.S. Treasury note and bond futures as part of an overall construction strategy to manage the Fund’s duration and yield curve exposure. The effect of these activities during the reporting period was negative.

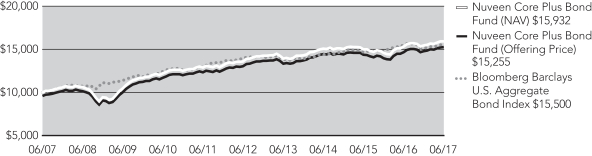

Nuveen Core Plus Bond Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed both the Bloomberg Barclays U.S. Aggregate Bond Index and the Lipper Core Plus Bond Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of

reduced accommodation by global central banks. However, in the final months of the reporting period, three consecutive months of weaker-than-expected inflation readings were the catalyst for yields to move lower at the long end of the Treasury yield curve. Ten-year Treasury rates rose by more than 115 basis points through mid-March, before falling approximately 30 basis points to end the reporting period about 85 basis points higher.

Around the rest of the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with the improved economic outlook, strong fundamentals and low market volatility, led high yield and investment grade corporate bonds to outperform during the reporting period, despite record issuance. High yield bonds enjoyed very strong performance helped along by continued accommodative Fed policy, which in turn drove more inflows into the market. The high yield market did reprice noticeably in March after a record-setting eight-day streak of outflows from exchange-traded funds (ETFs), and in June, the energy segment of the market saw spreads widen due to oil price pressures. However, toward the end of the reporting period, high yield spreads versus Treasuries had tightened to levels not seen since mid-2014. Investment grade corporate bonds generated strong excess returns over Treasuries and outperformed all other investment grade sectors despite heavy supply as issuers took advantage of favorable financing conditions and possible shifts in tax policy. International credit also performed well with European and U.K. credit rallying early in the reporting period as Brexit uncertainty faded and later in the reporting period due to the positive French election outcome and continued Eurozone economic strength.

In the securitized sectors, agency MBS performed well earlier in the reporting period due to continued bank and foreign purchases of the securities, the range-bound rate environment and lower levels of volatility. However, the sharp rise in interest rates and volatility, as well as relatively large net supply midway through the reporting period, proved to be a difficult environment for these securities. These factors, combined with increased rhetoric and the Fed’s eventual June 2017 announcement regarding plans to end its MBS reinvestments, weighed on agency MBS performance later in the reporting period. Over the full reporting period, agency MBS posted excess returns versus duration-matched Treasuries. Despite elevated levels of issuance in the first half of the reporting period, the commercial mortgage-backed securities (CMBS) sector finished the reporting period with a positive excess return over Treasuries. The segment benefited from the risk-on environment, steady demand, investors’ favorable reaction to the new risk retention rules and the associated lower CMBS issuance. However, toward the end of the reporting period, negative headlines surrounding retail loans in the CMBS segment mitigated most of the positive performance, especially for lower rated securities. Consumer related asset-backed securities (ABS) outpaced both the MBS and CMBS sectors, as well as duration-matched Treasuries. Demand for short-duration, high quality yield overshadowed ongoing headlines warning of weaker consumers and auto lending risks.

Emerging market (EM) bonds posted solid returns, supported by a larger scale global growth recovery, firming risk sentiment, easy financial conditions and strong inflows into EM assets in search of yield. Business sentiment and manufacturing trade improved as developed market activity supported EM economies through trade. Later in the reporting period, investors maintained their appetite for risk despite tighter credit and regulatory conditions in China and lower commodity prices. EM currencies declined in the broad-based dollar rally in the first half of the reporting period, with U.S. trade and protectionist pressures hitting the Mexican peso and ongoing domestic pressures hindering the Turkish lira. However, in the second half of the reporting period, the U.S. dollar reversed its post-election gains and most EM currencies benefited, especially Eastern European EM currencies. Russia and Colombia underperformed into the end of the reporting period following oil price declines.

Global rates remained low for much of the first half of the reporting period, until sprinting higher on the heels of the U.S. election. Throughout the reporting period, global yields remained sensitive to shifting growth conditions and changing fiscal and monetary policy expectations. Early in the reporting period, low inflation, continued stimulus from major central banks, and the surprise Brexit vote all exerted downward pressure on global yields. Then, the U.S. election drove a sudden shift toward increased expectations for fiscal stimulus and business spending, which combined with better economic data in developed and emerging markets to push rates up by approximately 80 basis points. The prospect for additional Fed rate hikes and an eventual reduction in extraordinary monetary stimulus globally also added to rate pressures as more central banks moderated their dovish outlooks. European rates were influenced during the reporting period by uncertainty surrounding April’s French election and questions regarding the future path of quantitative easing by the European Central Bank.

During the reporting period, non-U.S. markets outperformed Treasuries as global spreads moved in their favor, with the spread between Treasuries and German Bunds reaching a new historical wide, until late in the reporting period when broadening global

Portfolio Managers’ Comments (continued)

growth led several key central banks to question the need for continued aggressive stimulus. The U.S. dollar strengthened by 3-6% versus most major currencies in the first half of the reporting period due to higher growth, the policy outlook and interest rate differentials. However, in the second half of the reporting period, the dollar fell broadly versus most currencies except for the Japanese yen after U.S. fiscal policy optimism faded, trade fears receded and other central bankers shifted tone. In the final months of the reporting period, the euro rose more than 7% versus the dollar. Over the entire reporting period, the South African rand and European currencies were among the top performers, while the Turkish lira and Japanese yen lagged.

Broadly speaking, the Fund’s outperformance versus its benchmarks was driven by the continued improvement in global economic conditions and a strong improvement in market risk sentiment, accompanied by flows into bonds. More specifically, the Fund benefited from the demand for and continued outperformance of corporate credit sectors, through both the tightening of credit spreads and the Fund’s yield advantage versus the benchmark. Investment grade was the largest contributor to the Fund’s outperformance during the reporting period. A significant overweight to the sector relative to the benchmark, including an overweight to BBB rated securities, was the largest contributor to return. The BBB segment topped investment grade returns as quality spreads contracted amid ongoing improvement in the outlook for credit fundamentals, optimism about the strengthening economy and investors’ unrelenting demand for yield. Issue selection within the investment grade corporate sector was also a meaningful contributor to return. Exposure to cyclical credits and a significant overweight to the financial sector, including bank preferred securities, were advantageous.

High yield corporates were also a source of relative outperformance, both through an overweight to the sector and from issue selection. During the first part of the reporting period, the Fund was positioned near the top end of its high yield allocation range and benefited from tightening credit spreads and the sector’s higher income. Our credit selection within high yield also added to returns, particularly our overweight to more cyclical industries such as paper and chemicals, as well as our exposure to EM credit. As the reporting period progressed, we reduced the Fund’s high yield weighting and hedged part of the exposure; however, performance continued to benefit from our issue selection and positioning in the sector.

Our relatively small sovereign bond and currency positioning had a minimal net impact on the Fund’s performance. Overall interest rate positioning detracted modestly. Small gains from our defensive duration stance were more than offset by shifts in the yield curve since bonds with 10-year maturities underperformed in late 2016.

Our strategy during the reporting period remained biased toward earning income from credit sectors against the backdrop of supportive economics and financial conditions. We continued to overweight corporates with a focus on bottom-up, issue-specific credit selection and careful attention to risk management following the tightening of valuations throughout the reporting period. Due to the strong performance and substantial spread tightening in high yield credit, we significantly reduced exposure to this segment, including taking gains on targeted cyclical credits that had performed well and met targets. We also hedged a portion of our remaining high yield exposure, which allowed the portfolio to potentially benefit from credit selection and earn incremental yield, while seeking to dampen the impact of overall moves in high yield. We largely redeployed the sale proceeds into ABS, CMBS and higher quality investment grade corporates. We also used market opportunities to add to bank preferred securities; the Fund’s portfolio remained significantly overweight in financials. The portfolio was positioned with an overweight in BBB rated companies, but we also reduced this exposure as the reporting period progressed due to the strong outperformance of lower rated investment grade credits. Although we remained constructive on investment grade and high yield corporates as the reporting period ended, we took the opportunity after recent strength to reduce the overall risk profile of the Fund due to narrower risk premiums providing less compensation for ongoing policy and geopolitical risks.

Away from these sectors, we continued to find opportunities in securitized sectors such as ABS and CMBS, as well as in select foreign markets. Non-U.S. positions remained relatively low and tactical in nature during the reporting period, owing to shifting fundamentals and episodic market volatility. Other portfolio activity focused on individual credit selection and relative value opportunities. We continued to hold a large underweight in Treasuries, given our constructive economic view and the relatively unattractive duration and yield profile of the sector.

Interest rate positioning was marginally defensive for most of the reporting period, with adjustments based on valuations and risk management. At the end of the reporting period, the Fund’s duration remained moderately shorter than the benchmark index, given our bias for higher yields this year. Although the potential for volatility continues, particularly associated with central bank balance

sheet and policy transition, we expect the current rate cycle to be drawn out and the upside move in rates to be contained by macro factors. As a result, we do not believe that an aggressive positioning in interest rates is a beneficial strategy from a risk/reward perspective. Our strategic focus on diversified income and managing credit risk will be the important value drivers.

During the reporting period, we also continued to use various derivative instruments. We used Treasury note and bond futures as part of an overall construction strategy to manage the Fund’s duration and yield curve exposure. These derivative positions had a positive impact on performance during the reporting period. We also used interest rate swaps to manage portfolio duration and overall portfolio yield curve exposure. These positions had a negligible impact on performance and these positions were terminated prior to the end of the reporting period.

We used forward foreign currency exchange contracts to manage the Fund’s foreign currency exposure. For example, the Fund may reduce unwanted currency exposure from the Fund’s bond portfolio, or may take long forward positions in select currencies in an attempt to benefit from the potential price appreciation. These positions had a negative impact on performance during the reporting period.

The Fund also entered into credit default swaps to hedge credit risk. The effect of these activities on performance was negligible during the reporting period.

The Fund purchased currency put options which were used as part of an overall portfolio construction strategy to manage foreign currency exposure. These put options had a negligible impact on performance during the reporting period.

The Fund also purchased a small amount of currency call options as part of its overwrite strategy and purchased a small amount of call options on futures during the period. The call options had a negligible impact on performance during the reporting period.

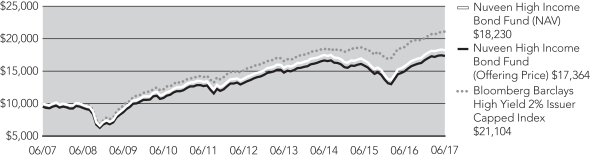

Nuveen High Income Bond Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed both the Bloomberg Barclays High Yield 2% Issuer Capped Index and the Lipper High Yield Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. However, in the final months of the reporting period, three consecutive months of weaker-than-expected inflation readings were the catalyst for yields to move lower at the long end of the Treasury yield curve. Ten-year Treasury rates rose by more than 115 basis points through mid-March, before falling approximately 30 basis points to end the reporting period about 85 basis points higher.

Around the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with a pickup in economic activity around the world, solid corporate earnings, strong fundamentals and low market volatility, led high yield corporate bonds to significantly outperform all other fixed income asset classes over the reporting period, despite record M&A-driven issuance at the end of 2016 and the first few months of 2017. High yield bonds were also helped along by continued accommodative Fed policy, which in turn drove more inflows into the market over much of the reporting period. Also, year-over-year revenue growth for high yield companies improved for five consecutive quarters. In March 2017, the high yield market did reprice noticeably after a record-setting eight-day streak of outflows from exchange-traded funds (ETFs), and in June, the energy segment of the market saw spreads widen due to oil price pressures. However, toward the end of the reporting period, high yield spreads versus Treasuries had tightened to levels not seen since mid-2014. As the reporting period ended, inflows into the market subsided as investors grew concerned about policy risk surrounding the Trump administration, geopolitical tensions, the decline in oil, lofty valuations and heightened risks heading into September with European Central Bank and Fed meetings.

Oil prices fell in the second half of the reporting period to below $43 per barrel by late June 2017, due to rising crude inventories in the United States. While the fall in oil and its relation to the health of the high yield market has become topical once again, we don’t believe it is yet a cause for credit loss concerns among energy producers, or for the broader high yield market. However, we acknowledge that the situation surrounding oil prices is still fluid, and the market is closer to a point (sub-$40 per barrel oil) where

Portfolio Managers’ Comments (continued)

this narrative could begin to change. Changes in the credit market’s structure have materially impacted the future sensitivity of corporate credit markets to oil prices. Easy access to debt and equity capital markets has allowed most energy firms to shore up their near-term liquidity and extend maturity profiles. As a result, the number of those credits rated B and below on negative outlook and most at risk of default has declined by 35-40%. To that point, some of the weakest credits from two years ago have undergone restructuring or defaulted and are no longer in high yield indices. However, energy does remain a large concentration in U.S. high yield indices, directly accounting for $178 billion in debt (13%), down from 15-20% at peak levels.

Over the reporting period, lower quality bonds significantly outperformed higher quality bonds as investors added risk to their portfolios due to the strong high yield market conditions. We witnessed a fair amount of spread compression between CCC rated securities and their higher quality single B and BB counterparts as the credit cycle was extended and friendly central bank policy and other factors helped to dampen corporate default rates. By June 2017, Moody’s global speculative grade default rate had fallen to 3.2%, down from its August 2016 high of 4.8% for this cycle. The uptick in global default rates due to the spike in defaults among energy and commodity companies over the past two years has run its course. Higher risk, CCC rated bonds gained 20.77% during the reporting period, compared to a return of 9.83% for BB rated bonds. Although in the final months of the reporting period, investors did favor the higher quality BB rated segment of high yield due to oil-driven risk aversion and renewed interest in Treasuries.

The leading sectors within high yield continued to be basic materials and energy for the reporting period. Within those sectors, the top performing industries were refining, metals and mining, chemicals and oilfield services, which benefited along with other cyclical sectors from a snap back after the oil price collapse in 2014 and 2015. Chemicals were strong because of developing tailwinds from what appeared to be the bottoming of certain commodity prices, while many companies within the index were also in deleveraging mode. The less cyclical telecommunications area of the market also showed strong results. Laggards during the reporting period included the secularly challenged retail sector and more defensive areas of the market such as supermarkets.

The Fund’s outperformance during the reporting period was mainly driven by the better environment for risk appetites that led to a substantial improvement in market liquidity and the outperformance of lower quality credit. We had positioned the Fund with an overweight in CCC rated debt, which was a significant driver of its favorable results. The increase in risk appetites also buoyed the previously lagging growth-sensitive areas of the market, specifically basic materials and energy. We saw particular strength among many distressed coal, energy and various other commodity-related bonds. The risk-on environment also led to strength in some of the Fund’s smaller-cap and small-issue size credits that had previously suffered simply because of illiquid market conditions.

In terms of sector allocations, the Fund benefited from overweight positions in chemicals, metals and mining, oilfield services, paper and financials. Underweights to retailers and consumer non-cyclical also proved helpful. While the Fund maintained close to a market weight in energy, it benefited from a down-in-quality bias within the exploration and production (E&P) sector because the stabilization in energy prices worked to lift many of the marginal producers. Similarly, within the mining sector, an uptick in natural gas prices helped to improve the relative attractiveness of coal, and by extension the performance of coal credits, which had been severely oversold on the heels of multiple industry bankruptcies. Therefore, the Fund’s overweight to coal within metals and mining was a net benefactor to performance. The Fund’s overweights to chemicals and paper were helpful since both sectors are cyclically exposed and had suffered disproportionately during 2015 and the beginning of 2016 when global growth scares were pervasive. Modest detractors to performance included underweights to health care, technology, cable/satellite and wireless communications.

The Fund also had modest exposure to Brazilian corporates, which were negatively affected by the country’s latest political scandal later in the reporting period. We accepted modest losses in a large agribusiness company that was at the forefront of the latest bribery scandal, while maintaining the Fund’s exposure to Petrobras, the large quasi-sovereign oil company that has proven rather resilient.

Elsewhere, the Fund’s holdings in European credit, particularly in the financial sector, performed well. European banks were increasingly in a much better situation with excess capital positions, while earnings were generally solid with few negative surprises. Regulators have mandated higher capital ratios, and an improving economy has benefited asset quality. Yields continue to look compelling when compared to large parts of the European high yield market, creating a large technical bid to the market.

As we neared the end of the reporting period, we reduced the Fund’s overweight to CCC rated debt, ending the reporting period with a modest overweight relative to the benchmark. We still believe that credit risk can continue to do well, but following the strong

performance of lower rated credit over the past two years, valuations are simply not as compelling as they had been for the lower tiers of corporate credit. With valuations near their tightest levels, it is important to assess the risks that potentially lie ahead. As central banks move to becoming less accommodative, monetary policy uncertainty will remain at the forefront of investor concerns. Continued oil and commodity volatility also remains a concern, even though we believe the sensitivity of credit spreads to oil prices should be lower than the in the recent past. Despite these issues, we continue to find attractive sources of yield in the CCC space on a selected basis. Also, we want to keep a modest overweight in CCCs because we believe lower quality securities will likely outperform higher quality paper if the interest rate threat facing the market over the next three to six months come to fruition.

Within energy, we maintained close to a neutral weighting versus that of the benchmark, but with a small emphasis toward higher beta within the energy E&P industry and a small overweight to oilfield services. Both of those sectors underperformed the market with the retreat of oil prices from the low $50s to the low $40s in the second half of the reporting period. Spreads within the energy E&P sector widened out by 75-100 basis points in the final two months of the reporting period and are at one-year highs, arguably offering value within a market that has seen spreads on broader BB rated securities reach historically tight levels. As noted above, we believe the changes in composition to the sector have reduced high yield’s sensitivity to oil, and that a decrease in production costs and a stronger cohort of surviving companies are all reasons not to abandon the sector. While we plan to take a cautious approach to energy investments given the uncertain path of oil prices and the inherent volatility, we do believe there are attractive opportunities to add portfolio yield. While fundamentally attractive, we continue to underweight health care, cable/satellite communications and technology based on valuation considerations, although we do find select opportunities in those sectors. In the case of health care, there are still many unknowns regarding the administration’s repeal and replace legislation.

We maintained the Fund’s emerging market (EM) exposure at slightly less than 5%. We are seeing pervasive evidence of a broad-based improvement in the industrial economy, not just in the U.S., but also in several emerging markets like China and Brazil. The medium-term drivers for these markets remain constructive because we believe the worst of the fundamental downturn has passed. The Fund owned modest weightings in preferred securities, split between $25-par preferred securities and hybrid capital European bank preferred securities, and contingent capital securities (CoCos). We also maintained small weights in various closed-end funds that invest in leveraged loans, high yield bonds and EM debt, as well as a small allocation to equities.

The Fund’s average duration (interest rate sensitivity) was 3.73 years at the end of the reporting period, essentially the same as the benchmark’s duration. Despite the spread narrowing in lower quality market segments, we continue to believe that high yield offers more protection from interest rate moves than other fixed income asset classes. The asset class has naturally low duration, while its incremental yield helps mitigate price movements in a rising rate environment.

During the reporting period, we also continued to use various derivative instruments. We used U.S. Treasury note and bond futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. The effect of these activities during the period was negative.

We used foreign currency exchange contracts to manage the Fund’s foreign currency exposures. During the reporting period, these instruments were used primarily for hedging purposes to reduce unwanted currency exposure from the Fund’s bond portfolio. These positions had a positive impact on performance during the reporting period.

The Fund also entered into credit default swaps to take on credit risk and earn a commensurate credit spread. The effect of these activities on performance was negligible and these positions were terminated prior to the end of the reporting period.

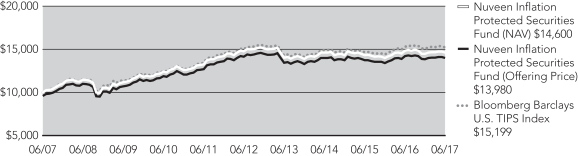

Nuveen Inflation Protected Securities Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Bloomberg Barclays U.S. TIPS Index and the Lipper Inflation-Protected Bond Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve during the reporting period as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. In the Treasury inflation-protected securities (TIPS) market, the asset class saw strong inflows

Portfolio Managers’ Comments (continued)

during the first half of the reporting period, reflecting increased investor interest in inflation protection after implied inflation expectations reached 2% by the end of 2016. Inflows continued in the second half of the reporting period, but at a slower pace. Strong

seasonal Consumer Price Index (CPI) prints at the beginning of 2017 and investor optimism about reflationary fiscal policies by the new Trump administration faded as the reporting period progressed. In the final months of the reporting period, three consecutive months of weaker-than-expected CPI prints were the catalyst for yields to move lower at the long end of the nominal Treasury curve and caused breakeven rates to narrow. (The breakeven rate measures the difference between the yields of nominal Treasuries versus TIPS with the same maturity.)

TIPS yields were higher, and therefore prices were lower, across the board during the reporting period. However, yields for shorter maturity TIPS rose much more than longer maturities because the falling price of oil caused shorter securities to struggle. The yield on five-year TIPS moved out of deeply negative territory at the beginning of the reporting period, jumping 63 basis points to end the reporting period at 0.22%. (Because the yield on a TIPS bond is equal to the corresponding Treasury bond yield minus the expected rate of inflation, it falls into negative territory if the inflation rate is higher than the current Treasury yield.) Meanwhile, the 10-year TIPS yield increased 53 basis points to end the reporting period at 0.57%, while 30-year TIPS yields rose 31 basis points to end at 0.99%. As a result, the TIPS yield curve flattened over the reporting period since short rates rose significantly more than longer rates. Meanwhile, the TIPS breakeven rate rose sharply at the end of 2016, indicating investor expectations of increased inflation risk, before reversing somewhat during the second quarter of 2017, but still ending the reporting period higher. The TIPS sector ended the reporting period in negative territory with a return of -0.63% for the Bloomberg Barclays U.S. TIPS Index, but still outperformed nominal Treasury securities.

Around the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with the improved economic outlook, strong fundamentals and low market volatility, led high yield and investment grade corporate bonds to outperform during the reporting period, despite record issuance. High yield bonds enjoyed very strong performance helped along by continued accommodative Fed policy, which in turn drove more inflows into the market. The high yield market did reprice noticeably in March after a record-setting eight-day streak of outflows from exchange-traded funds (ETFs), and in June, the energy segment of the market saw spreads widen due to oil price pressures. However, toward the end of the reporting period, high yield spreads versus Treasuries had tightened to levels not seen since mid-2014. Investment grade corporate bonds generated strong excess returns over Treasuries and outperformed all other investment grade sectors despite heavy supply as issuers took advantage of favorable financing conditions and possible shifts in tax policy.

In the securitized sectors, agency mortgage-backed securities (MBS) performed well earlier in the reporting period due to continued bank and foreign purchases of the securities, the range-bound rate environment and lower levels of volatility. However, the sharp rise in interest rates and volatility, as well as relatively large net supply midway through the reporting period, proved to be a difficult environment for these securities. These factors, combined with increased rhetoric and the Fed’s eventual June 2017 announcement regarding plans to end its MBS reinvestments, weighed on agency MBS performance later in the reporting period. Over the full reporting period, agency MBS posted slightly positive excess returns versus duration-matched Treasuries. Despite elevated levels of issuance in the first half of the reporting period, the commercial mortgage-backed securities (CMBS) sector finished the reporting period with a positive excess return over Treasuries. The segment benefited from the risk-on environment, steady demand, investors’ favorable reaction to the new risk retention rules and the associated lower CMBS issuance. However, toward the end of the reporting period, negative headlines surrounding retail loans in the CMBS segment mitigated most of the positive performance, especially for lower rated securities. Consumer related asset-backed securities (ABS) outpaced duration-matched Treasuries as well. Demand for short-duration, high quality yield overshadowed ongoing headlines warning of weaker consumers and auto lending risks.

The Fund held an overweight in nominal Treasuries versus the benchmark, which is comprised of 100% TIPS, to take advantage of changing inflation expectations along the TIPS yield curve. Although we shifted the Fund’s TIPS exposure from a low of approximately 81% of the Fund’s assets to about 88% of the portfolio by year-end 2016, our position still represented an underweight versus the index’s TIPS exposure with a bias to remain overweight to spread sectors. This positioning was a detractor through year-end 2016 as breakeven rates performed well following the November 2016 election.

Volatile real rates, especially at the end of 2016, were also a headwind for the Fund’s performance relative to its benchmark. Our yield curve positioning was a drag on results with most of the negative impact occurring in the first two months of the reporting period. The Fund was positioned with an underweight to securities at the long end of the yield curve, which flattened through August 2016 before reversing in September 2016.

On the positive side, the Fund’s approximately 10-12% weight among spread sectors, including ABS, CMBS, high yield credit and investment grade credit, benefited performance. As noted above, spread sectors, especially high yield corporates, produced strong excess returns during the reporting period. In addition, we positioned the Fund with a duration that was modestly shorter than the benchmark throughout the reporting period, which provided a modest boost to performance.

Toward the end of the reporting period, we slightly lowered the Fund’s TIPS exposure and invested the proceeds into nominal Treasuries. Despite attractive breakeven levels and a positive technical backdrop, soft inflation projections are weighing on the TIPS asset class. This increased the Fund’s weight in nominal Treasuries and agency debentures to approximately 3% of its portfolio. We also continued to favor modest exposure to several out-of-index spread sectors, including ABS, CMBS, high yield corporate bonds and investment grade corporate bonds, which represented a little more than 10% of the portfolio. We believe the macro-economic backdrop remains constructive for these spread sectors because credit fundamentals are steady and investors’ continued quest for yield should keep spreads firm. However, valuations in the corporate market have meaningfully richened. While we don’t see a catalyst for significant spread widening in the near term, valuations at these levels warrant a strong focus on bottom-up fundamental research. As noted, the Fund’s duration was kept modestly shorter than the benchmark, given our bias for rates to move slowly higher through the rest of the 2017.

We also used U.S. Treasury note and bond futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. These derivative positions had a negative impact on performance during the reporting period.

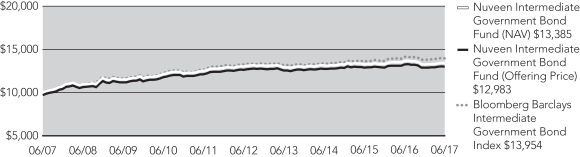

Nuveen Intermediate Government Bond Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Bloomberg Barclays Intermediate Government Bond Index and the Lipper Intermediate U.S. Government Funds Classification Average for the twelve-month reporting period.

Treasury rates rose fairly dramatically across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. At the front end of the Treasury yield curve, rates reflected Fed tightening with yields rising throughout the reporting period for maturities of three years and under. For example, the one-year Treasury yield was up approximately 80 basis points during the reporting period. In the more intermediate range of the Treasury yield curve, rates for five-year Treasuries increased by approximately 90 basis points. Meanwhile, rates for longer-term Treasuries rose significantly through mid-March 2016; however, in the final months, three consecutive inflation readings that were weaker than expected contributed to lower yields at the long end of the Treasury yield curve. Rates for 10-year Treasuries rose by more than 115 basis points, before falling approximately 30 basis points to end the reporting period about 85 basis points higher. Around the rest of the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income.

In the securitized sectors, mortgage-backed securities (MBS) issued by government agencies such as Fannie Mae (FNMA), Ginnie Mae (GNMA) and Freddie Mac (FHLMC) performed well earlier in the reporting period due to continued bank and foreign purchases of the securities, the range-bound rate environment and lower levels of volatility. However, the sharp rise in interest rates and volatility, as well as relatively large net supply midway through the reporting period, proved to be a difficult environment for these securities. These factors, combined with increased rhetoric and the Fed’s eventual June announcement regarding plans to end its MBS reinvestments, weighed on agency MBS performance later in the reporting period. The GNMA segment underperformed because lower all-in yields kept those buyers on the sidelines, while conventional FNMA and FHLMC MBS outperformed. The agency MBS sector as a whole posted slight excess returns versus duration-matched Treasuries. Despite high levels of issuance in late 2016, the commercial mortgage-backed securities (CMBS) sector performed well in the risk-on environment following the election. The segment benefited from the recovery in the broader markets, strong demand for high quality, non-government securities and the lower level of CMBS issuance in the second half of the reporting period. However, toward the end of the reporting period, negative headlines surrounding retail loans in the CMBS segment mitigated most of the positive performance, especially for lower rated securities.

Portfolio Managers’ Comments (continued)

Overall, CMBS finished the reporting period with positive excess returns over Treasuries. Consumer related asset-backed securities (ABS) outpaced duration-matched Treasuries on the back of strong consumer health and low volatility. Demand for short-duration, high quality yield overshadowed headlines warning of weaker consumers and auto lending risks as the reporting period progressed.

Sharply rising interest rates were a headwind for the Fund’s performance relative to its benchmark and peers during the reporting period. More specifically, we had the Fund positioned to benefit from a flatter Treasury yield curve at the time of the election. We did this by overweighting securities in the 10-year portion of the yield curve, while underweighting securities with maturities of five years and under. However, the election’s surprising results sparked a sharp increase in rates and a dramatic steepening of the curve, with intermediate and long-term rates rising more than short-term rates. Although we shifted to a bias for a steeper yield curve and reduced the Fund’s exposure to 10-year securities as we neared the end of 2016, the move was made after the rapid repricing of the curve post-election. As a result, our yield curve positioning detracted from the Fund’s results, mostly in the first half of the reporting period. In the second half of the reporting period, however, the Treasury yield curve was meaningfully flatter after the two Fed rate hikes pushed short rates higher, while longer term rates fell due to lower inflation readings. During the final months of the reporting period, our yield curve positioning proved beneficial, but it was not enough to offset the earlier shortfall. We also tactically traded the Fund’s duration, or interest rate sensitivity, throughout the reporting period. In aggregate, these duration moves slightly detracted from the Fund’s performance.

On the positive side, the Fund benefited from its sector weights, including overweight positions in securitized sectors of the market and a corresponding underweight to U.S. Treasuries. More specifically, the Fund benefited from overweights to ABS and CMBS. Demand remained strong for high quality, liquid paper and spreads tightened versus Treasuries for both ABS and CMBS throughout reporting period, but particularly after the election. However, the Fund experienced a slight drag on performance from a heavier overweight to longer maturity MBS, which underperformed during the interest rate volatility in late 2016.

While inflation came in consistently below the Fed’s target later in the reporting period, policymakers described this as transitory in nature and continued to signal their intent to normalize monetary policy. In addition, the Fed indicated its intent to begin shrinking the balance sheet in the second half of 2017. With this expectation, we preferred to maintain a defensive duration strategy for the Fund. We targeted a portfolio duration, or interest rate sensitivity, that was shorter than the benchmark at approximately 3.65 years as the reporting period came to a close. We are maintaining the Fund’s overweight to the intermediate to 10-year part of the curve because we expect yields on the shortest securities will rise more quickly as the Fed continues to increase the fed funds rate. While we typically do not make major changes to the Fund’s overall sector weightings, we made some minor adjustments. Over the reporting period, we modestly reduced the Fund’s floating rate MBS positions because they had reached our spread targets and invested part of the proceeds in the ABS sector through bottom-up security selection. We also slightly increased the Fund’s agency debenture and municipal bond weights.

In addition, we used U.S. Treasury note and bond futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. These derivative positions had a negative impact on performance during the reporting period.

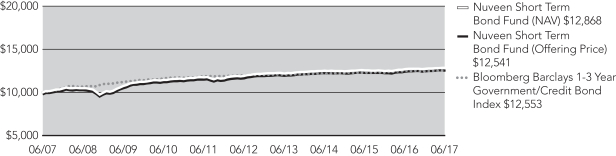

Nuveen Short Term Bond Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed the Bloomberg Barclays 1-3 Year Government/Credit Bond Index and underperformed the Lipper Short Investment Grade Debt Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. At the front end of the Treasury yield curve, rates reflected Fed tightening with yields rising throughout the reporting period for maturities of three years and under. For Treasury securities in the two-to-five-year range, rates increased by between 80 and 90 basis points over the reporting period. Rates for longer-term Treasuries rose during the first half of the reporting period; however, in the final months of the reporting period, three consecutive months of weaker-than-expected inflation readings and tighter Fed policy were the catalyst for yields to move lower at the long end of the Treasury yield curve.

Around the rest of the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with the

improved economic outlook, strong fundamentals and low market volatility, led shorter duration investment grade U.S. corporate bonds and, to an even greater degree, high yield U.S. corporates to perform well. Credit fundamentals remained stable as strong earnings growth helped to support corporate leverage levels. These segments generated substantial excess returns over Treasuries despite heavy issuance as issuers took advantage of favorable financing conditions and possible shifts in tax policy. By the end of the reporting period, credit spreads had tightened to levels not seen since mid-2014. Financials posted strong returns based on the potential for a more favorable regulatory environment under the new administration, while the energy and basic material sectors outperformed, mostly in the first half of the reporting period, on the back of higher commodity prices.

In the securitized sectors, consumer-related asset-backed securities (ABS) outpaced duration-matched Treasuries on the back of strong consumer health and low volatility. Demand for short-duration, high quality yield overshadowed headlines warning of weaker consumers and auto lending risks as the reporting period progressed. Despite elevated levels of issuance in late 2016, the commercial mortgage-backed securities (CMBS) sector performed well in the risk-on environment following the election. The segment benefited from a recovery in the broader markets, strong demand for high quality non-government securities and the lower level of CMBS issuance in the second half of the reporting period. Overall, CMBS finished the reporting period with positive excess returns over Treasuries. Short maturity residential MBS performed well supported by lower levels of volatility, continued strong fundamentals and investor demand. Mortgage delinquencies continued to decline and home price appreciation continued at a modest pace given historically low levels of supply and positive affordability metrics. As the reporting period progressed, residential MBS continued to benefit from strong fundamentals and low supply and posted excess returns versus duration-matched Treasuries.

The most substantial driver of the Fund’s outperformance relative to the benchmarks was its broad overweight to the corporate and securitized sectors and corresponding underweight to Treasuries. The Fund’s exposure to short duration high yield credit was a significant contributor to returns relative to the benchmark, given the spread tightening that took place in that segment. We maintained between 3%-6% of the Fund’s portfolio in bonds rated BB and single-B in the two-year to four-year portion of the yield curve during the reporting period. The Fund’s approximately 5-7% overweight in investment grade corporate bonds also added incremental return during the reporting period, particularly from our overweight to industrials and financials. We maintained a weighting of around 40% in investment grade corporates, with an emphasis on BBB rated paper. At the same time, we positioned approximately 40% of the Fund’s portfolio in securitized product, broadly diversified across the ABS, CMBS and residential MBS sectors. The Fund benefited from short duration ABS and CMBS because demand remained strong for high quality, liquid paper and spreads tightened versus Treasuries throughout the reporting period. Certain segments of the non-agency MBS sector also performed well.

In aggregate, the Fund also benefited modestly from our interest rate strategy. Throughout the reporting period, we positioned the Fund defensively to limit its sensitivity to rising rates with a duration between 0.30 and 0.50 years shorter than the benchmark, which produced a gain. Yields at the front end of the Treasury curve rose to their highest level since 2008 based on constructive domestic economic data and continued moves by the Fed to normalize monetary policy. On the other hand, our yield curve positioning didn’t have a noticeable impact on performance during the reporting period.

We believe short rates will continue to trend higher, with the market pricing in one more rate hike during 2017. While inflation came in consistently below the Fed’s target later in the reporting period, policymakers described this as transitory in nature and continued to signal their intent to normalize monetary policy. In addition, the Fed indicated its intent to begin shrinking the balance sheet in the second half of 2017. With this expectation, we maintained a defensive duration strategy for the Fund. As of the end of the reporting period, we were targeting a portfolio duration, or interest rate sensitivity, between 0.25-0.50 years shorter than the benchmark.

We also continued to focus our efforts on generating an attractive level of income by maintaining the Fund’s modest overweight to the non-government sectors of the bond market. The Fund’s portfolio was positioned with approximately a 5-7% overweight in the investment grade corporate sector during the reporting period. We reduced high yield exposure to around 3% of the portfolio and reinvested the proceeds into investment grade credit after the spread between the two areas narrowed to levels not seen since mid-2014. Within investment grade, we rotated up in quality from BBB rated to A rated companies toward the end of the reporting period, while also increasing the Fund’s overweight to financials due to the Fed’s expected tightening path.

We maintained the Fund’s weightings in the securitized sectors at approximately 40-45% of its portfolio. However, toward the end of the reporting period, we made a modest shift out of CMBS because of tight spreads and rotated into the ABS sector. Also, because

Portfolio Managers’ Comments (continued)

commercial real estate is further along in the credit cycle, we will continue to closely monitor fundamentals in the CMBS sector. We will likely continue to target higher quality bonds, while adding more risk opportunistically. Fundamentals in the ABS segment are supportive because consumer balance sheets remain healthy. We expect returns in the ABS segment to be income driven due to tight spreads, but continue to expect low volatility because of the high quality nature of the sector. We maintained the Fund’s weight in residential MBS because we believe the sector offers attractive income and shorter duration. Low levels of inventory and rising borrower income continue to provide a tailwind to appreciation in home prices. The residential MBS sector remains an area that provides incremental income to the portfolio, but with a low correlation to broader markets. Across the securitized sectors, we are maintaining ample liquidity to take advantage of bottom-up, relative-value opportunities. We also kept 5% to 10% of the Fund’s assets invested in Treasury and agency securities as a liquidity and volatility buffer.

In addition, we used U.S. Treasury note futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. These derivative positions had a negative impact on performance during the reporting period.

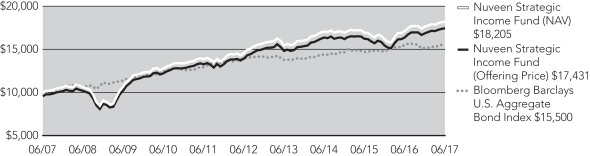

Nuveen Strategic Income Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed both the Bloomberg Barclays U.S. Aggregate Bond Index and the Lipper Multi-Sector Income Funds Classification Average for the twelve-month reporting period.

Treasury rates rose sharply across the yield curve, particularly in the first half of the reporting period, as investors braced for strong fiscal stimulus and factored in a higher risk of inflation following the U.S. election, while remaining concerned about the possibility of reduced accommodation by global central banks. However, in the final months of the reporting period, three consecutive months of weaker-than-expected inflation readings were the catalyst for yields to move lower at the long end of the Treasury yield curve. Ten-year Treasury rates rose by more than 115 basis points through mid-March, before falling approximately 30 basis points to end the reporting period about 85 basis points higher.

Around the rest of the world, global rates remained at exceptionally low levels due to accommodative central banks, resulting in strong demand from overseas investors for U.S. securities with incremental income. That technical underpinning, combined with the improved economic outlook, strong fundamentals and low market volatility, led high yield and investment grade corporate bonds to outperform during the reporting period, despite record issuance. High yield bonds enjoyed very strong performance helped along by continued accommodative Fed policy, which in turn drove more inflows into the market. The high yield market did reprice noticeably in March after a record-setting eight-day streak of outflows from exchange-traded funds (ETFs), and in June, the energy segment of the market saw spreads widen due to oil price pressures. However, toward the end of the reporting period, high yield spreads versus Treasuries had tightened to levels not seen since mid-2014. Investment grade corporate bonds generated strong excess returns over Treasuries and outperformed all other investment grade sectors despite heavy supply as issuers took advantage of favorable financing conditions and possible shifts in tax policy. International credit also performed well with European and U.K. credit rallying early in the reporting period as Brexit uncertainty faded and later in the reporting period due to the positive French election outcome and continued Eurozone economic strength.