UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman, Sachs & Co. | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: August 31

Date of reporting period: February 28, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | February 28, 2014 |

| | |

| | | | Global Tax-Aware Equity Portfolios |

| | | | Enhanced Dividend Global Equity Portfolio |

| | | | Tax-Advantaged Global Equity Portfolio |

Goldman Sachs Global Tax-Aware Equity Portfolios

| n | | ENHANCED DIVIDEND GLOBAL EQUITY PORTFOLIO |

| n | | TAX-ADVANTAGED GLOBAL EQUITY PORTFOLIO |

| | | | |

TABLE OF CONTENTS | | | | |

| |

Principal Investment Strategies and Risks | | | 1 | |

| |

Market Review | | | 2 | |

| |

Portfolio Management Discussion and Performance Summaries | | | 5 | |

| |

Schedules of Investments | | | 17 | |

| |

Financial Statements | | | 21 | |

| |

Financial Highlights | | | 24 | |

| |

Notes to Financial Statements | | | 28 | |

| |

Other Information | | | 43 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS GLOBAL TAX-AWARE EQUITY PORTFOLIOS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Portfolios. For additional information concerning the risks applicable to the Portfolios, please see the Portfolios’ Prospectus.

The Goldman Sachs Enhanced Dividend Global Equity Portfolio invests primarily in affiliated domestic and international equity and fixed income funds (“underlying funds”). The Portfolio will also invest directly in other securities, including exchange-traded funds, which may be denominated in currencies other than the U.S. dollar. The Portfolio is intended for investors who want current income. The Portfolio expects to invest primarily in underlying equity funds and equity securities with a blend of domestic large cap, small cap and international exposure, and expects to invest a relatively significant percentage of this equity allocation in the Goldman Sachs U.S. Equity Dividend and Premium and Goldman Sachs International Equity Dividend and Premium Funds, which have an emphasis on dividend paying stocks. In addition, the Portfolio will have a small strategic allocation in U.S. investment grade bonds, which may consist of an investment in the Goldman Sachs Core Fixed Income Fund or other fixed income securities. The Portfolio may also buy and sell among various underlying funds as part of a tactical allocation. The Portfolio may also engage in short selling. A short sale transaction involves the sale of a borrowed security to a third party, with the understanding that the security must later be returned to the lender. Short sales involve the risk of an unlimited increase in the market value of the security sold short, which could result in a theoretically unlimited loss.

The Portfolio is subject to the risk factors of each underlying fund and the securities that it holds directly, which include prepayment, credit, liquidity and interest rate risk; the price fluctuations of U.S. government securities in response to changes in interest rates and inflation; the volatility of investments in the markets; and political, economic and currency risks of non-U.S. investments. Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; the risk of default by a counterparty; and liquidity risk. From time to time, the underlying funds in which the Portfolio invests may change. Because the Portfolio is subject to the underlying fund expenses as well as its own expenses, the cost of investing in the Portfolio may be higher than investing in a mutual fund that only invests in stocks and bonds.

The Goldman Sachs Tax-Advantaged Global Equity Portfolio invests primarily in affiliated domestic and international equity and fixed income funds (“underlying funds”). The Portfolio will also invest directly in other securities, including exchange-traded funds, which may be denominated in currencies other than the U.S. dollar. The Portfolio is intended for investors who wish to minimize short-term gains and defer long-term gains. The Portfolio expects to invest primarily in underlying equity funds and equity securities with a blend of domestic large cap, small cap and international exposure, and expects to invest a relatively significant percentage of this equity allocation in the Goldman Sachs Structured Tax-Managed Equity and Goldman Sachs Structured International Tax-Managed Equity Funds. In addition, the Portfolio will have a small strategic allocation in U.S. investment grade bonds, which may consist of an investment in the Goldman Sachs Core Fixed Income Fund or other fixed income securities. The Portfolio may also buy and sell among various underlying funds as part of a tactical allocation. The Portfolio may also engage in short selling. A short sale transaction involves the sale of a borrowed security to a third party, with the understanding that the security must later be returned to the lender. Short sales involve the risk of an unlimited increase in the market value of the security sold short, which could result in a theoretically unlimited loss. The Portfolio strives to achieve returns primarily in the form of price appreciation and may use different strategies in seeking tax efficiency. No assurance can be offered that the Portfolio’s tax-managed strategies will reduce the amount of taxable income and capital gains distributed by the Portfolio to shareholders.

The Portfolio is subject to the risk factors of each underlying fund and the securities that it holds directly, which include prepayment, credit, liquidity and interest rate risk; the price fluctuations of U.S. government securities in response to changes in interest rates and inflation; the volatility of investments in the markets; and political, economic and currency risks of non-U.S. investments. Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; the risk of default by a counterparty; and liquidity risk. From time to time, the underlying funds in which the Portfolio invests may change. Because the Portfolio is subject to the underlying fund expenses as well as its own expenses, the cost of investing in the Portfolio may be higher than investing in a mutual fund that only invests directly in stocks and bonds.

1

MARKET REVIEW

Goldman Sachs Global Tax-Aware Equity Portfolios

|

| |

| Investment Strategy |

| |

| The Portfolios invest in a strategic mix of Underlying Funds and other securities with the goal of achieving long-term growth of capital (both Portfolios) and current income (Enhanced Dividend Global Equity Portfolio only). Under normal conditions, at least 80% of the Portfolios’ total assets measured at the time of purchase will be allocated among the Underlying Funds that currently exist or that may become available for investment in the future for which Goldman Sachs Asset Management (“GSAM”) or an affiliate, now or in the future, acts as investment adviser or principal underwriter. Some of the Underlying Funds invest primarily in fixed income or money market instruments and other Underlying Funds invest primarily in equity securities. The Portfolios may also invest directly in other securities or instruments, including unaffiliated exchange-traded funds, and can use these investments for implementing tactical tilts. Under normal circumstances, each of the Portfolios also has a small strategic allocation to U.S. investment grade bonds. |

Market Review

Economic conditions and monetary policies of global central banks drove the performance of the global equity and fixed income markets during the six months ended February 28, 2014 (“the Reporting Period”).

Equity Markets

The U.S. and international equity markets enjoyed four consecutive months of gains from September through December 2013. The S&P 500 Index made record highs in December 2013, as the U.S. Federal Reserve (the “Fed”) ended seven months of speculation and announced it would finally begin tapering its asset purchases, signaling confidence in the U.S. economy. Days later, the U.S. revised upward its Gross Domestic Product (“GDP”) growth estimate for the third quarter of 2013 to an annualized pace of 4.1%, the fastest rate in two years. Importantly, stronger consumption accounted for most of the upward revision. Stock markets in Japan and Europe reached new highs in December 2013 as well. Japan’s Nikkei 225 closed 2013 at a six-year high, as the market reflected optimism about Prime Minister Shinzo Abe’s bold reforms and big stimulus. Encouragingly, Japan’s consumer price index (“CPI”) steadily increased through the fourth quarter of 2013, boosting confidence that the Japanese economy is on a path to achieve its government’s inflation target of 2%. Germany’s Xetra Dax also reached a new high in December, as European markets continued to benefit from the European Central Bank’s (“ECB”) commitment to easy monetary policy and as economic growth returned to the region.

U.S. equities, along with global developed market equities broadly, stumbled in January 2014 on renewed concerns about a variety of issues in the growth and emerging markets, including lower manufacturing activity in China. Such concerns weighed even more heavily on Asian markets, excluding Japan. In February 2014, developed market equities, including those of the

2

MARKET REVIEW

U.S., snapped back. Indeed, the S&P 500 Index reached a new high in February 2014, as merger and acquisition activity picked up and corporate earnings announcements reflected top-line growth, even though overall management guidance for 2014 was less optimistic than the consensus view. Underlying U.S. economic activity during February 2014 was not as strong as it had been at the end of 2013, with disappointing payroll and retail sales reports, though it was unclear how much severe winter weather across most of the U.S. was to blame. Furthermore, a downward revision of fourth quarter 2013 U.S. GDP to an annualized rate of 2.4% from 3.2% indicated the American consumer was resilient but not quite as strong as previously thought.

In other developed markets, economic data was mixed. The Eurozone economy appeared to improve, growing at a stronger than expected annualized rate of 0.5% in the fourth quarter of 2013, and the European Commission raised its estimates for GDP growth to 1.2% in 2014 and 1.8% in 2015. However, other data releases in February 2014, including the Eurozone flash purchasing managers’ indices (“PMIs”), retail sales and industrial production, were not particularly strong. Disinflation also remained an immediate concern. In addition, many corporate earnings reports as well as conservative guidance from company management prompted downward revisions to earnings estimates. In Japan, inflation climbed higher, but the country’s fourth quarter 2013 GDP growth, at an annualized rate of 1.0%, was well below expectations, and the Bank of Japan did not provide additional stimulus ahead of the consumption tax hike scheduled for April 2014.

Fixed Income Markets

Market volatility drove global bond yields higher early in the Reporting Period on continued uncertainty over Fed policy, including speculation about who would replace Fed Chair Bernanke, and the risk of a military intervention in Syria. Interest rates rose and spread (or non-U.S. Treasury) sectors rallied on the Fed’s surprise decision at its September 2013 meeting to not yet start reducing asset purchases. The central bank cited insufficient economic conditions and concerns about fiscal tightening. Global economic growth momentum showed improvement, the Eurozone emerged from recession, and China’s economy stabilized on increased investment.

At the beginning of October 2013, a political stalemate over U.S. federal government funding led to a 16-day partial federal government shutdown. On October 16th, lawmakers reached a last-minute deal to extend the government’s borrowing authority and the U.S. narrowly avoided a default. Also in October, Janet Yellen, a relatively dovish choice, was nominated to succeed Bernanke as Fed Chair in 2014. Global bond yields increased in the fourth calendar quarter overall on improving economic data and, in December 2013, on the Fed’s decision to begin trimming its asset purchases. The Fed announced that starting in January 2014, it would reduce its monthly purchases of U.S. Treasury securities and mortgage-backed securities by $5 billion each, cutting its total monthly asset purchases from $85 billion to $75 billion.

3

MARKET REVIEW

In January 2014, spread sectors grew volatile on concerns about economic growth in the emerging markets and the condition of China’s banking system as well as on unusually cold weather and disappointing economic data in the U.S. Meanwhile, U.S. Treasury yields declined following softer U.S. economic news, including a sharp drop in the national PMI and weaker than expected payrolls data. In line with market expectations, the Fed announced in January that it would reduce its monthly asset purchases by an additional $10 billion in February 2014.

Benchmark yields in core government markets remained in a tight range during February 2014. In the U.S., economic data showed improvement, suggesting that previous weakness may have been influenced by temporary factors such as poor winter weather and a reduction in inventories. In the Eurozone, data continued to paint a picture of gently improving economic growth alongside subdued inflation, easing pressure on the ECB to offer more stimulus. Russia’s military presence in the Ukraine and tensions over Crimea’s possible secession weighed heavily on that region’s markets. Russian assets took the brunt of the selloff, and the Russian central bank hiked interest rates to curb further currency depreciation.

Looking Ahead

In our opinion, U.S. economic growth is likely to rebound near term, and we believe housing construction can be a key source of strength during 2014. The economy should also benefit, in our view, from strong private sector balance sheets, including both household wealth and a corporate cash surplus. We believe improving economic growth should put pressure on the Fed to raise interest rates sooner than the market was anticipating at the end of the Reporting Period.

Outside the U.S., we expect China’s unsustainable credit growth and rising schedule of maturing trust products to create tighter financial conditions, but the Chinese government may offset this with more fiscal spending, thereby keeping the country’s economic growth near 7.5% . Meanwhile, Europe is mired in a low economic growth, low inflation environment. Recent improvements have been driven by disinflationary factors (e.g., falling labor costs and improved competitiveness as well as lower imports in peripheral nations) rather than inflationary factors (e.g., consumer spending in Germany remains stagnant). We expect additional ECB easing in support of Eurozone economies. In Japan, we believe economic growth is likely to slow in the second half of 2014. Government reforms have benefited corporations, but wage growth is modest. As a result, we believe that the upcoming consumption tax hike is likely to weigh on Japan’s economic growth, and the markets may be overestimating the Bank of Japan’s willingness to respond. In the emerging markets, recent volatility may provide attractive opportunities given the divergence in country-specific fundamentals and policy.

The economic and market forecasts presented herein are for informational purposes as of the date of this report. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this report.

4

PORTFOLIO RESULTS

Goldman Sachs Enhanced Dividend Global Equity Portfolio

Effective May 1, 2013, the components of the Goldman Sachs Enhanced Dividend Global Equity Portfolio’s (the “Portfolio”) performance benchmark, the Enhanced Dividend Global Equity Composite Index (“EDGE Composite Index”), changed from the Russell 3000® Index (60%), the MSCI All Country World Index (ACWI), ex North America® (30%) and the Barclays U.S. Aggregate Bond Index (10%) to the MSCI All Country World Index Investable Market Index® (“MSCI ACWI IMI”) (90%) and the Barclays U.S. Aggregate Bond Index (10%). Goldman Sachs Asset Management believes these changes better reflect the strategic and tactical underlying allocations of the Portfolio and therefore provide more appropriate benchmarks against which to measure the Portfolio’s performance.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Portfolio’s performance and positioning for the six-month period ended February 28, 2014 (the “Reporting Period”).

| Q | | How did the Portfolio perform during the Reporting Period? |

| A | | During the Reporting Period, the Portfolio’s Class A and Institutional Shares generated cumulative total returns, without sales charges, of 11.22% and 11.38%, respectively. These returns compare to the 12.99% cumulative total return of the Portfolio’s new blended benchmark, the EDGE Composite Index, over the same time period. The Portfolio’s former blended benchmark generated a 13.76% cumulative total return for the same period. |

| | | The components of the Portfolio’s new blended benchmark generated cumulative total returns of 2.84% and 13.24% for the Barclays U.S. Aggregate Bond Index and the MSCI All Country World Index (ACWI) Investable Market Index® (“MSCI ACWI IMI”), respectively, during the Reporting Period. The components of the Portfolio’s former blended benchmark generated cumulative total returns of 2.84%, 13.57% and 15.83% for the Barclays U.S. Aggregate Bond Index, the MSCI ACWI, ex North America® and the Russell 3000® Index, respectively, during the same period. |

| Q | | What key factors affected the Portfolio’s performance during the Reporting Period? |

| A | | Though the Portfolio benefited from its tactical asset allocation decisions, it underperformed the EDGE Composite Index during the Reporting Period largely because of the performance of its Underlying Funds. The impact of the Portfolio’s strategic weightings was relatively neutral. |

| Q | | How did Global Tactical Asset Allocation decisions affect the Portfolio’s performance during the Reporting Period? |

| A | | The implementation of our tactical views contributed positively to performance. The Portfolio was overweight U.S. large-cap bank stocks through an exchange traded fund (“ETF”), which appreciated in value during the Reporting Period. In our opinion, the valuations of U.S. large-cap bank stocks were attractive relative to their historical performance and to the broad U.S. equity market. More specifically, the price-to-book ratio of large-cap bank stocks was particularly attractive. (The price-to-book ratio is used to compare a stock’s market value to its book value.) In addition, banks have a strong connection to the ongoing housing recovery because the majority of their balance sheets are backed by U.S. real estate. |

| | | The Portfolio was overweight U.S. technology stocks through an ETF, which appreciated in value. During the Reporting Period, the technology sector offered a free cash flow yield that was 200 basis points higher than the overall equity market. (A basis point is 1/100th of a percentage point.) In our view, this gave the sector an attractive risk/return profile. We also believe information technology companies have the potential for superior earnings growth and could increase their dividends and stock buybacks compared to other companies in the broad stock market. |

| | | The Portfolio was overweight European equities during the Reporting Period. Despite the rally in the European stock market since we initiated this tactical tilt in December 2011, European stock valuations, as represented by the Euro Stoxx 50® Index (covering 50 blue chip stocks from 12 Eurozone |

5

PORTFOLIO RESULTS

| | | countries), have remained depressed. If their price multiples revert to their 10-year average during the next five years, European equities could, in our view, post higher annual gains. Combined with moderate earnings growth and an attractive dividend yield, we believe European stocks could potentially generate higher annual total returns during the same timeframe. In addition, during the Reporting Period, the Portfolio was overweight Spanish equities. We believe Spain has made much-needed progress in reforming its economy and expect progress to continue. At the end of the Reporting Period, the Spanish government was committed to reform and had a stable majority in parliament. Also, the Portfolio was overweight Japanese equities. The Tokyo Stock Exchange’s Tokyo Stock Price Index (“TOPIX”) gained ground during the Reporting Period, breaking out of a narrow trading range and, in our opinion, is poised to continue its upward trend. We believe the Bank of Japan is increasingly likely to announce additional quantitative easing in April 2014, which may serve as a catalyst for Japanese equities to move higher. In addition, we believe Japan’s Government Pension Investment Fund is likely to increase its allocation to equities. Such a move could motivate other domestic Japanese institutions to do the same. The Portfolio’s weightings in the European and Spanish equity markets were implemented through investments in stock futures. (A stock future, which is traded on an exchange, is a contract that obligates a buyer to purchase stock at a predetermined future date and price.) The Portfolio’s overweight position in the Japanese equity market was implemented through an index call option. |

| | | The Portfolio was underweight U.S. investment grade bonds. It was overweight U.S. high yield corporate bonds through an investment in the Goldman Sachs High Yield Fund. During the Reporting Period, high yield corporate spreads (or yield differentials to U.S. Treasuries) remained more than 100 basis points higher than their previous lows and were consistent with spread levels during other periods of low defaults. In addition, we believe high yield corporate bonds could be a better interest rate hedge than many investors expect. Historically, when interest rates rise quickly, high yield corporate bonds generate positive returns approximately 73% of the time. |

| | | The Portfolio was overweight high yield bank loans — through an investment in the Goldman Sachs High Yield Floating Rate Fund — because they offered what we |

| | | The economic and market forecasts presented herein are for informational purposes as of the date of this report. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this report. |

| | believed to be an attractive yield. Furthermore, we think high yield bank loans are well-suited to the rising rate environment. Because of their rather short duration, high yield bank loans allow investors to act quickly — and potentially benefit — when interest rates rise. |

| Q | | How did the Portfolio’s Underlying Funds perform relative to their respective benchmark indices during the Reporting Period? |

| A | | We use seven Underlying Funds to implement our strategic asset allocation. Because of our tactical trading, the Portfolio was invested in six of these Underlying Funds during the Reporting Period. Four of those six Underlying Funds underperformed their respective benchmark indices and two outperformed their respective benchmark indices during the Reporting Period. (The Portfolio did not have an allocation to the Goldman Sachs Core Fixed Income Fund during the Reporting Period.) |

| | | Two of the Underlying Funds that underperformed in relative terms — the Goldman Sachs U.S. Equity Dividend and Premium Fund and the Goldman Sachs International Equity Dividend Fund — were those in which the Portfolio invested a significant percentage of its equity allocation. The Goldman Sachs U.S. Equity Dividend and Premium Fund underperformed its benchmark, the S&P 500® Index (with dividends reinvested), during the Reporting Period. The Goldman Sachs International Equity Dividend and Premium Fund also underperformed its benchmark, the MSCI Europe, Australasia, Far East (“EAFE”) Index. The Goldman Sachs Small Cap Equity Insights Fund and the Goldman Sachs Emerging Equity Insights Fund also underperformed their respective benchmark indices during the Reporting Period.1 |

| | | On the positive side, the Goldman Sachs International Small Cap Insights Fund2 and the Goldman Sachs MLP Energy Infrastructure Fund3 outperformed their respective benchmark indices during the Reporting Period. |

| 1 | | Effective after the close of business on May 3, 2013, the Goldman Sachs Structured Small Cap Equity Fund was renamed the Goldman Sachs Small Cap Equity Insights Fund and the Goldman Sachs Structured Emerging Markets Equity Fund was renamed the Goldman Sachs Emerging Markets Equity Insights Fund. |

| 2 | | Effective after the close of business on May 3, 2013, the Goldman Sachs Structured International Small Cap Equity Fund was renamed the Goldman Sachs International Small Cap Insights Fund. |

| 3 | | The Goldman Sachs MLP Energy Infrastructure Fund, which provides exposure to energy infrastructure master limited partnership (“MLP”) investments, was introduced as an Underlying Fund after the close of business on March 26, 2013. |

6

PORTFOLIO RESULTS

| Q | | How did call writing affect performance? |

| A | | As mentioned above, the Portfolio’s two largest allocations were to the Goldman Sachs U.S. Equity Dividend and Premium Fund and the Goldman Sachs International Equity Dividend and Premium Fund, which earn premiums through an equity index call writing strategy. When equity markets are down, flat or only modestly positive, these Underlying Funds tend to outperform their respective benchmark indices because of the premiums they earn from call writing. When equity markets rally strongly, these two Underlying Funds are likely to trail their respective benchmark indices. Although the Underlying Funds keep the premiums they earn from call writing, they can underperform when the call options are exercised. |

| | | The U.S. and international equity markets appreciated during the Reporting Period, and the call writing strategy of both Underlying Funds detracted from performance as call options were exercised. |

| Q | | How did the Portfolio use derivatives and similar instruments during the Reporting Period? |

| A | | The Portfolio used equity index futures and equity index options during the Reporting Period to implement our views on the European, Spanish and Japanese stock markets. In addition, some of the Portfolio’s Underlying Funds used derivatives during the Reporting Period to apply their active investment views with greater versatility and to afford greater risk management precision. As market conditions warranted during the Reporting Period, some of these Underlying Funds engaged in forward foreign currency exchange contracts, financial futures contracts, options and swap contracts to enhance portfolio return and for hedging purposes. |

| Q | | What changes did you make during the Reporting Period within both the equity and fixed income portions of the Portfolio? |

| A | | During September 2013, we hedged the Portfolio’s weight in U.S. equities by purchasing December 2013 S&P® 500 Index put options at a strike price of 1700. (For put options, the strike price is the price at which shares can be sold.) We funded the position by reducing the Portfolio’s allocation to investment grade fixed income. On September 30, 2013, the Portfolio’s position in September 2013 S&P® 500 Index put options, which had been purchased in May 2013 at a strike price of 1625, expired. |

| | | During November 2013, we increased the Portfolio’s overweight in high yield bank loans through an investment in the Goldman Sachs High Yield Floating Rate Fund. Also in November, we hedged the Fund’s weight in U.S. equities by purchasing December 2013 S&P® 500 Index put options at a strike price of 1750. In addition, we added to the Portfolio’s overweight in Japanese equities by purchasing TOPIX Index call options at a strike price of 1300. (For call options, the strike price is the price at which shares can be purchased.) These three positions were funded by reducing the Portfolio’s allocation to investment grade fixed income. |

| | | In January 2014, we decreased the Portfolio’s overweight in high yield corporate bonds and its overweight in large-cap U.S. bank stocks. We reallocated the proceeds to high yield bank loans through an investment in the Goldman Sachs High Yield Floating Rate Fund. |

| | | During February 2014, we increased the Portfolio’s overweight in large-cap U.S. bank stocks by adding to its investment in a SPDR® S&P® Bank ETF. We funded the position by reducing the Portfolio’s exposure to U.S. large-cap equities. |

| Q | | What was the Portfolio’s tactical view and strategy at the end of the Reporting Period? |

| A | | As of February 28, 2014, the Portfolio — through its holdings in equity index futures and equity index options — was overweight the European, Spanish and Japanese stock markets. It was overweight large-cap U.S. bank stocks and U.S. technology stocks through investments in ETFs, which were both funded out of investment grade fixed income and, in the case of large-cap U.S. bank stocks, out of U.S. equities. In fixed income, through allocations to the Underlying Funds, the Portfolio held overweighted positions in high yield corporate bonds and high yield bank loans and an underweighted position in investment grade securities. |

7

FUND BASICS

Enhanced Dividend Global Equity Portfolio

as of February 28, 2014

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | September 1, 2013–

February 28, 2014 | | Portfolio

Total Return

(based on NAV)1 | | | EDGE

Composite

Index2 | | | EDGE

Composite

Index

(prior to

5/1/13) | | | Barclays

U.S.

Aggregate

Bond

Index | | | MSCI

ACWI

IMI

Index | | | Russell

3000

Index | | | MSCI

ACWI Ex

NA | |

| | Class A | | | 11.22 | % | | | 12.99 | % | | | 13.76 | % | | | 2.84 | % | | | 13.24 | % | | | 15.83 | % | | | 13.57 | % |

| | | Institutional | | | 11.38 | | | | 12.99 | | | | 13.76 | | | | 2.84 | | | | 13.24 | | | | 15.83 | | | | 13.57 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Portfolio (ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance reflects the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The EDGE Composite Index (“EDGE Composite”) is a composite representation prepared by the investment adviser of the performance of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. Prior to May 1, 2013, the EDGE Composite was comprised of the Russell 3000® Index (60%), the MSCI All Country World Index (ACWI), ex-North America® (30%) and the Barclays U.S. Aggregate Box Index (10%). The EDGE Composite figures do not reflect any deduction for fees, expenses or taxes. |

Effective as of May 1, 2013, the EDGE Composite Index (Current) (“Current EDGE Composite”) is comprised of the Morgan Stanley Capital International All Country World Index IM I (Investable Market Index) (“MSCI ACWI IMI”) (90%) and the Barclays U.S. Aggregate Bond Index (10%). The MSCI is a broad and investable global equity benchmark. MSCI ACWI IMI covers over 9,000 securities across large, mid and small cap size segments and across style and sector segments in developed and emerging markets. The Current EDGE Composite figures do not reflect any deduction for fees, expenses or taxes.

The Russell 3000® Index is an unmanaged index that measures the performance of the 3,000 largest U.S. companies based on total market capitalization which represents approximately 98% of the investable U.S. equity market. The MSCI All Country World Index, Investable Market Indices, ex- North America represents an unmanaged, diversified portfolio of developed and emerging countries with the exception of the United States and Canada. The Barclay’s U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment grade corporate bonds, and mortgage-backed and asset-backed securities. The Index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 12/31/13 | | One Year | | | Five Years | | Since Inception | | Inception Date |

| | Class A | | | 13.87 | % | | 13.08% | | 4.61% | | 4/30/08 |

| | | Institutional | | | 20.93 | | | 14.81 | | 6.09 | | 4/30/08 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares. Because Institutional Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

8

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.36 | % | | | 1.44 | % |

| | | Institutional | | | 0.96 | | | | 1.05 | |

| | 4 | | The expense ratios of the Portfolio, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations), are as set forth above according to the most recent publicly available Prospectus for the Portfolio and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Portfolio’s waivers and/or expense limitations, if any, will remain in place through at least December 29, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Portfolio’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | STANDARDIZED AFTER-TAX PERFORMANCE AS OF 12/31/135 |

| | | Class A Shares | | One Year | | | Five Years | | Since Inception

(4/30/08) |

| | Returns before taxes6 | | | 13.87 | % | | 13.08% | | 4.61% |

| | Returns after taxes on distributions7 | | | 12.32 | | | 12.33 | | 3.94 |

| | | Returns after taxes on distributions8

and sale of Portfolio shares | | | 9.15 | | | 10.52 | | 3.63 |

| | 5 | | The after-tax returns are calculated using the historically highest individual federal marginal income tax rates at the time of distributions (currently 15% for qualifying ordinary income dividends and long-term capital gain distributions and 35% for non-qualifying ordinary income dividends) and do not reflect state and local taxes. Actual after-tax returns will be calculated at calendar year-end and depend on an investor’s tax situation and may differ from those shown. In addition, the after-tax returns shown are not relevant to investors who hold Portfolio shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Under certain circumstances, the addition of the tax benefits from capital losses resulting from redemptions may cause the Returns After Taxes on Distributions and Sale of Portfolio Shares to be greater than the Returns After Taxes on Distributions or even Returns Before Taxes. Standardized after-tax returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.5% for Class A Shares. |

| | 6 | | Returns Before Taxes do not reflect taxes on distributions on the Portfolio’s Class A Shares nor do they show how performance can be impacted by taxes when shares are redeemed. |

| | 7 | | Returns After Taxes on Distributions assume that taxes are paid on distributions on the Portfolio’s Class A Shares (i.e., dividends and capital gains) but do not reflect taxes that may be incurred upon redemption of the Class A Shares at the end of the performance period. |

| | 8 | | Returns After Taxes on Distributions and Sale of Portfolio Shares reflect taxes paid on distributions on the Portfolio’s Class A Shares and taxes applicable when the shares are redeemed. |

9

FUND BASICS

|

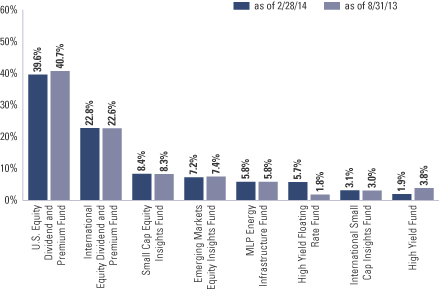

| OVERALL UNDERLYING FUND WEIGHTINGS9 |

| Percentage of Net Assets |

| | 9 | | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each Underlying Fund reflects the value of that underlying fund as a percentage of net assets of the Portfolio. Figures in the graph above may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. Underlying sector allocations of ETFs held by the Portfolio are not reflected in the graph above. The above graph depicts the Portfolio’s investments but may not represent the Portfolio’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

10

PORTFOLIO RESULTS

Goldman Sachs Tax-Advantaged

Global Equity Portfolio

Effective May 1, 2013, the components of the Goldman Sachs Tax-Advantaged Global Equity Portfolio’s (the “Portfolio”) performance benchmark, the Tax-Advantaged Global Equity Composite Index (“TAG Composite Index”), changed from the Russell 3000® Index (60%), the MSCI All Country World Index (ACWI), ex North America® (30%) and the Barclays U.S. Aggregate Bond Index (10%) to the MSCI All Country World Index Investable Market Index® (“MSCI ACWI IMI”) (90%) and the Barclays U.S. Aggregate Bond Index (10%). Goldman Sachs Asset Management believes these changes better reflect the strategic and tactical underlying allocations of the Portfolio and therefore provide more appropriate benchmarks against which to measure the Portfolio’s performance.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Portfolio’s performance and positioning for the six-month period ended February 28, 2014 (the “Reporting Period”).

| Q | | How did the Portfolio perform during the Reporting Period? |

| A | | During the Reporting Period, the Portfolio’s Class A and Institutional Shares generated cumulative total returns, without sales charges, of 15.75% and 16.02%, respectively. These returns compare to the 12.99% cumulative total return of the Portfolio’s new blended benchmark, the TAG Composite Index, over the same time period. The Portfolio’s former blended benchmark generated a 13.76% cumulative total return during the same period. |

| | The components of the Portfolio’s new blended benchmark generated cumulative total returns of 2.84% and 13.24% for the Barclays U.S. Aggregate Bond Index and the MSCI All Country World Index (ACWI) Investable Market Index® (“MSCI ACWI IMI”), respectively, during the Reporting Period. The components of the Portfolio’s former blended benchmark generated cumulative total returns of 2.84%, 13.57% and 15.83% for the Barclays U.S. Aggregate Bond Index, the MSCI ACWI, ex North America® and the Russell 3000® Index, respectively, during the same period. |

| Q | | What key factors affected the Portfolio’s performance during the Reporting Period? |

| A | | The Portfolio outperformed the TAG Composite Index during the Reporting Period, benefiting from our tactical asset allocation decisions. Security selection within the Underlying Funds overall also added to relative returns. The impact of the Portfolio’s strategic weightings was relatively neutral during the Reporting Period. |

| Q | | How did Global Tactical Asset Allocation decisions affect the Portfolio’s performance during the Reporting Period? |

| A | | The implementation of our tactical views contributed positively to performance. The Portfolio was overweight U.S. large-cap bank stocks through an exchange traded fund (“ETF”), which appreciated in value during the Reporting Period. In our opinion, the valuations of U.S. large-cap bank stocks were attractive relative to their historical performance and to the broad U.S. equity market. More specifically, the price-to-book ratio of large-cap bank stocks was particularly attractive. (The price-to-book ratio is used to compare a stock’s market value to its book value.) In addition, banks have a strong connection to the ongoing housing recovery because the majority of their balance sheets are backed by U.S. real estate. |

| | The Portfolio was overweight U.S. technology stocks through an ETF, which appreciated in value. During the Reporting Period, the technology sector offered a free cash flow yield that was 200 basis points higher than the overall equity market. (A basis point is 1/100th of a percentage point.) In our view, this gives the sector an attractive risk/return profile. We also believe information technology companies have the potential for superior earnings growth and could increase their dividends and stock buybacks compared to other companies in the broad stock market. |

| | | The economic and market forecasts presented herein are for informational purposes as of the date of this report. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this report. |

11

PORTFOLIO RESULTS

| | The Portfolio was overweight European equities during the Reporting Period. Despite the rally in the European stock market since we initiated this tactical tilt in December 2011, European stock valuations, as represented by the Euro Stoxx 50® Index (covering 50 blue chip stocks from 12 Eurozone countries), have remained depressed. If their price multiples revert to their 10-year average during the next five years, European equities could, in our view, post higher annual gains. Combined with moderate earnings growth and an attractive dividend yield, we believe European stocks could potentially generate higher annual total returns during the same timeframe. In addition, during the Reporting Period, the Portfolio was overweight Spanish equities. We believe Spain has made much-needed progress in reforming its economy and expect progress to continue. At the end of the Reporting Period, the Spanish government was committed to reform and had a stable majority in parliament. Also, the Portfolio was overweight Japanese equities. The Tokyo Stock Exchange’s Tokyo Stock Price Index (“TOPIX”) gained ground during the Reporting Period, breaking out of a narrow trading range and, in our opinion, is poised to continue its upward trend. We believe the Bank of Japan is increasingly likely to announce additional quantitative easing in April 2014, which may serve as a catalyst for Japanese equities to move higher. In addition, we believe Japan’s Government Pension Investment Fund is likely to increase its allocation to equities. Such a move could motivate other domestic Japanese institutions to do the same. The Portfolio’s weightings in the European and Spanish equity markets were implemented through investments in stock futures. (A stock future, which is traded on an exchange, is a contract that obligates a buyer to purchase stock at a predetermined future date and price.) The Portfolio’s overweight position in the Japanese equity market was implemented through an index call option. |

| | The Portfolio was underweight U.S. investment grade bonds. It was overweight U.S. high yield corporate bonds through an investment in the Goldman Sachs High Yield Fund. During the Reporting Period, high yield corporate spreads (or yield differentials to U.S. Treasuries) remained more than 100 basis points higher than their previous lows and were consistent with spread levels during other periods of low defaults. In addition, we believe high yield corporate bonds could be a better interest rate hedge than many investors expect. Historically, when interest rates rise quickly, high yield corporate bonds generate positive returns approximately 73% of the time. |

| | The Portfolio was overweight high yield bank loans —through an investment in the Goldman Sachs High Yield Floating Rate Fund — because they offered what we believed to be an attractive yield. Furthermore, we think high yield bank loans are well-suited to the rising rate environment. Because of their rather short duration, high yield bank loans allow investors to act quickly — and potentially benefit — when interest rates rise. |

| Q | | How did the Portfolio’s Underlying Funds perform relative to their respective benchmark indices during the Reporting Period? |

| A | | We use six Underlying Funds to implement our strategic allocation decisions within the Portfolio. Because of our tactical trading, the Portfolio was invested in five of these Underlying Funds during the Reporting Period. Four of those five Underlying Funds outperformed their respective benchmark indices and one underperformed its benchmark index. (The Portfolio did not have an allocation to the Goldman Sachs Core Fixed Income Fund during the Reporting Period.) The Underlying Funds that outperformed their respective benchmark indices were the Goldman Sachs Structured Tax-Managed Equity Fund, the Goldman Sachs Structured International Tax-Managed Equity Fund, the Goldman Sachs International Small Cap Insights Fund1 and the Goldman Sachs MLP Energy Infrastructure Fund.2 The Goldman Sachs Emerging Markets Equity Insights Fund3 underperformed its benchmark index. |

| | Of the Underlying Funds in which the Portfolio held its greatest weightings, the Goldman Sachs Structured Tax-Managed Equity Fund outperformed its benchmark, the Russell 3000® Index, and the Goldman Sachs Structured International Tax-Managed Equity Fund also outperformed its benchmark, the MSCI Europe, Australasia, Far East (“EAFE”) Index during the Reporting Period. |

| 1 | | Effective after the close of business on May 3, 2013, the Goldman Sachs International Small Cap Equity Fund was renamed the Goldman Sachs International Small Cap Insights Fund. |

| 2 | | The Goldman Sachs MLP Energy Infrastructure Fund, which provides exposure to energy infrastructure master limited partnership (“MLP”) investments, was introduced as an Underlying Fund after the close of business on March 26, 2013. |

| 3 | | Effective after the close of business on May 3, 2013, the Goldman Sachs Structured Emerging Markets Equity Fund was renamed the Goldman Sachs Emerging Markets Equity Insights Fund. |

12

PORTFOLIO RESULTS

| Q | | How did the Portfolio use derivatives and similar instruments during the Reporting Period? |

| A | | The Portfolio used equity index futures and equity index options during the Reporting Period to implement our views on the European, Spanish and Japanese stock markets. In addition, some of the Portfolio’s Underlying Funds used derivatives during the Reporting Period to apply their active investment views with greater versatility and to afford greater risk management precision. As market conditions warranted during the Reporting Period, some of these Underlying Funds engaged in forward foreign currency exchange contracts, financial futures contracts, options and swap contracts to enhance portfolio return and for hedging purposes. |

| Q | | What changes did you make during the Reporting Period within both the equity and fixed income portions of the Portfolio? |

| A | | During September 2013, we hedged the Portfolio’s weight in U.S. equities by purchasing December 2013 S&P® 500 Index put options at a strike price of 1700. (For put options, the strike price is the price at which shares can be sold.) We funded the position by reducing the Portfolio’s allocation to investment grade fixed income. On September 30, 2013, the Portfolio’s position in September 2013 S&P® 500 Index put options, which had been purchased in May 2013 at a strike price of 1625, expired. |

| | During November 2013, we hedged the Portfolio’s weight in high yield corporate bonds through an investment in the Goldman Sachs High Yield Floating Rate Fund. Also in November, we increased the Fund’s overweight in U.S. equities by purchasing December 2013 S&P® 500 Index put options at a strike price of 1750. In addition, we added to the Portfolio’s overweight in Japanese equities by purchasing TOPIX Index call options at a strike price of 1300. (For call options, the strike price is the price at which shares can be purchased.) These three positions were funded by reducing the Portfolio’s allocation to investment grade fixed income. |

| | In January 2014, we decreased the Portfolio’s overweight in high yield corporate bonds and its overweight in large-cap U.S. bank stocks. We reallocated the proceeds to high yield bank loans through an investment in the Goldman Sachs High Yield Floating Rate Fund. |

| | During February 2014, we increased the Portfolio’s overweight in large-cap U.S. bank stocks by adding to its investment in a SPDR® S&P® Bank ETF. We funded the position by reducing the Portfolio’s exposure to U.S. large-cap equities. |

| Q | | What was the Portfolio’s tactical view and strategy at the end of the Reporting Period? |

| A | | As of February 28, 2014, the Portfolio — through its holdings in equity index futures and equity index options —was overweight the European, Spanish and Japanese stock markets. It was overweight large-cap U.S. bank stocks and U.S. technology stocks through investments in ETFs, which were both funded out of investment grade fixed income and, in the case of large-cap U.S. bank stocks, out of U.S. equities. In fixed income, through allocations to the Underlying Funds, the Portfolio held overweighted positions in high yield corporate bonds and high yield bank loans and an underweighted position in investment grade securities. |

13

FUND BASICS

Tax-Advantaged Global Equity Portfolio

as of February 28, 2014

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | September 1, 2013–

February 28, 2014 | | Portfolio

Total Return

(based on NAV)1 | | | TAG

Composite

Index2 | | | TAG

Composite

Index

(prior to

5/1/13) | | | Barclays

U.S.

Aggregate

Bond

Index | | | MSCI

ACWI

IMI

Index | | | Russell

3000

Index | | | MSCI

ACWI Ex

NA | |

| | Class A | | | 15.75 | % | | | 12.99 | % | | | 13.76 | % | | | 2.84 | % | | | 13.24 | % | | | 15.83 | % | | | 13.57 | % |

| | | Institutional | | | 16.02 | | | | 12.99 | | | | 13.76 | | | | 2.84 | | | | 13.24 | | | | 15.83 | | | | 13.57 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Portfolio (ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance reflects the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The TAG Composite Index (“TAG Composite”) is a composite representation prepared by the investment adviser of the performance of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. Prior to May 1, 2013, the TAG Composite was comprised of the Russell 3000® Index (60%), the MSCI All Country World Index (ACWI), ex-North America® (30%) and the Barclays U.S. Aggregate Box Index (10%). The TAG Composite figures do not reflect any deduction for fees, expenses or taxes. |

Effective as of May 1, 2013, the TAG Composite Index (Current) (“Current TAG Composite”) is comprised of the Morgan Stanley Capital International All Country World Index IM I (Investable Market Index) (“MSCI ACWI IMI”) (90%) and the Barclays U.S. Aggregate Bond Index (10%). The MSCI is a broad and investable global equity benchmark. MSCI ACWI IMI covers over 9,000 securities across large, mid and small cap size segments and across style and sector segments in developed and emerging markets. The Current TAG Composite figures do not reflect any deduction for fees, expenses or taxes.

The Russell 3000® Index is an unmanaged index that measures the performance of the 3,000 largest U.S. companies based on total market capitalization which represents approximately 98% of the investable U.S. equity market. The MSCI All Country World Index, Investable Market Indices, ex- North America represents an unmanaged, diversified portfolio of developed and emerging countries with the exception of the United States and Canada. The Barclay’s U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment grade corporate bonds, and mortgage-backed and asset-backed securities. The Index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 12/31/13 | | One Year | | | Five Years | | Since Inception | | Inception Date |

| | Class A | | | 20.54 | % | | 14.27% | | 5.12% | | 4/30/08 |

| | | Institutional | | | 28.06 | | | 16.04 | | 6.60 | | 4/30/08 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares. Because Institutional Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

14

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.42 | % | | | 1.46 | % |

| | | Institutional | | | 1.02 | | | | 1.06 | |

| | 4 | | The expense ratios of the Portfolio, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Portfolio and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Portfolio’s waivers and/or expense limitations will remain in place through at least December 29, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Portfolio’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | STANDARDIZED AFTER-TAX PERFORMANCE AS OF 12/31/135 |

| | | Class A Shares | | One Year | | | Five Years | | Since Inception

(4/30/08) |

| | Returns before taxes6 | | | 20.54 | % | | 14.27% | | 5.12% |

| | Returns after taxes on distributions7 | | | 19.75 | | | 13.84 | | 4.72 |

| | | Returns after taxes on distributions8

and sale of Portfolio shares | | | 12.13 | | | 11.45 | | 3.96 |

| | 5 | | The after-tax returns are calculated using the historically highest individual federal marginal income tax rates at the time of distributions (currently 15% for qualifying ordinary income dividends and long-term capital gain distributions and 35% for non-qualifying ordinary income dividends) and do not reflect state and local taxes. Actual after-tax returns will be calculated at calendar year-end and depend on an investor’s tax situation and may differ from those shown. In addition, the after-tax returns shown are not relevant to investors who hold Portfolio shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. Under certain circumstances, the addition of the tax benefits from capital losses resulting from redemptions may cause the Returns After Taxes on Distributions and Sale of Portfolio Shares to be greater than the Returns After Taxes on Distributions or even Returns Before Taxes. Standardized after-tax returns assume reinvestment of all distributions at NAV and reflect a maximum initial sales charge of 5.5% for Class A Shares. |

| | 6 | | Returns Before Taxes do not reflect taxes on distributions on the Portfolio’s Class A Shares nor do they show how performance can be impacted by taxes when shares are redeemed. |

| | 7 | | Returns After Taxes on Distributions assume that taxes are paid on distributions on the Portfolio’s Class A Shares (i.e., dividends and capital gains) but do not reflect taxes that may be incurred upon redemption of the Class A Shares at the end of the performance period. |

| | 8 | | Returns After Taxes on Distributions and Sale of Portfolio Shares reflect taxes paid on distributions on the Portfolio’s Class A Shares and taxes applicable when the shares are redeemed. |

15

FUND BASICS

|

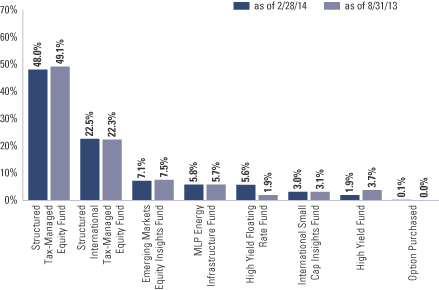

| OVERALL UNDERLYING FUND WEIGHTINGS9 |

| Percentage of Net Assets |

| | 9 | | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each Underlying Fund reflects the value of that underlying fund as a percentage of net assets of the Portfolio. Figures in the graph above may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. Underlying sector allocations of ETFs held by the Portfolio are not reflected in the graph above. The above graph depicts the Portfolio’s investments but may not represent the Portfolio’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

16

GOLDMAN SACHS ENHANCED DIVIDEND GLOBAL EQUITY PORTFOLIO

Schedule of Investments

February 28, 2014 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | Underlying Funds (Institutional Shares)(a) – 94.5% | |

| | Equity – 86.9% | |

| | 11,885,586 | | | Goldman Sachs U.S. Equity Dividend and Premium Fund | | $ | 133,593,982 | |

| | 9,520,962 | | | Goldman Sachs International Equity Dividend and Premium Fund | | | 76,834,165 | |

| | 1,548,449 | | | Goldman Sachs Small Cap Equity Insights Fund | | | 28,522,426 | |

| | 2,927,994 | | | Goldman Sachs Emerging Markets Equity Insights Fund | | | 24,185,232 | |

| | 1,696,089 | | | Goldman Sachs MLP Energy Infrastructure Fund | | | 19,521,984 | |

| | 961,377 | | | Goldman Sachs International Small Cap Insights Fund | | | 10,450,166 | |

| | | | | | | | |

| | | | | | | 293,107,955 | |

| | |

| | Fixed Income – 7.6% | |

| | 1,889,793 | | | Goldman Sachs High Yield Floating Rate Fund | | | 19,086,910 | |

| | 902,371 | | | Goldman Sachs High Yield Fund | | | 6,560,239 | |

| | 552 | | | Goldman Sachs Core Fixed Income Fund | | | 5,763 | |

| | | | | | | | |

| | | | | | | 25,652,912 | |

| | |

| TOTAL UNDERLYING FUNDS

(INSTITUTIONAL SHARES) – 94.5% | | | | |

| | (Cost $264,754,630) | | $ | 318,760,867 | |

| | |

| | | | | | | | |

Shares | | | Description | | Value | |

| | Exchange Traded Funds – 3.8% | |

| | 197,509 | | | SPDR S&P Bank Fund | | $ | 6,517,797 | |

| | 168,941 | | | Technology Select Sector SPDR Fund | | | 6,141,005 | |

| | |

| | TOTAL EXCHANGE TRADED FUNDS | | | | |

| | (Cost $10,777,908) | | $ | 12,658,802 | |

| | |

| | | | | | | | | | | | |

| Contracts | | | Strike

Price | | Expiration

Date | | | Value | |

| | Option Purchased – 0.0% | |

| TSE TOPIX Index Call Option | |

| | 49 | | | $1,300 | | | 06/13/14 | | | $ | 135,777 | |

| | (Cost $281,514) | |

| | |

| | TOTAL INVESTMENTS – 98.3% | |

| | (Cost $275,814,052) | | | $ | 331,555,446 | |

| | |

| OTHER ASSETS IN EXCESS OF

LIABILITIES – 1.7% |

| | | 5,707,291 | |

| | |

| | NET ASSETS – 100.0% | | | $ | 337,262,737 | |

| | |

| | |

| The percentage shown for each investment and investment category reflects the value of the respective investment or category as a percentage of net assets. |

(a) | | Represents Affiliated Funds. |

| | |

|

Investment Abbreviation: |

SPDR | | —Standard and Poor’s Depositary Receipts |

|

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS ENHANCED DIVIDEND GLOBAL EQUITY PORTFOLIO

Schedule of Investments (continued)

February 28, 2014 (Unaudited)

|

| ADDITIONAL INVESTMENT INFORMATION |

FUTURES CONTRACTS — At February 28, 2014, the Portfolio had the following futures contracts:

| | | | | | | | | | | | | | |

| Type | | Number of

Contracts

Long (Short) | | | Expiration

Date | | Current

Value | | | Unrealized

Gain (Loss) | |

EURO STOXX 50 Index | | | 145 | | | March 2014 | | $ | 6,284,506 | | | $ | 396,440 | |

IBEX 35 Index | | | 24 | | | March 2014 | | | 3,338,659 | | | | 9,933 | |

| TOTAL | | | | | | | | | | | | $ | 406,373 | |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS TAX-ADVANTAGED GLOBAL EQUITY PORTFOLIO

Schedule of Investments

February 28, 2014 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | | | | | | | |

| | Underlying Funds (Institutional Shares)(a) – 93.9% | |

| | Equity – 86.4% | |

| | 29,853,688 | | | Goldman Sachs Structured Tax-Managed Equity Fund | | $ | 478,256,076 | |

| | 24,059,679 | | | Goldman Sachs Structured International Tax-Managed Equity Fund | | | 224,236,207 | |

| | 8,541,767 | | | Goldman Sachs Emerging Markets Equity Insights Fund | | | 70,554,993 | |

| | 4,999,378 | | | Goldman Sachs MLP Energy Infrastructure Fund | | | 57,542,839 | |

| | 2,788,159 | | | Goldman Sachs International Small Cap Insights Fund | | | 30,307,289 | |

| | | | | | | | |

| | | | | | | 860,897,404 | |

| | |

| | Fixed Income – 7.5% | |

| | 5,504,571 | | | Goldman Sachs High Yield Floating Rate Fund | | | 55,596,165 | |

| | 2,630,165 | | | Goldman Sachs High Yield Fund | | | 19,121,297 | |

| | 2,215 | | | Goldman Sachs Core Fixed Income Fund | | | 23,127 | |

| | | | | | | | |

| | | | | | | 74,740,589 | |

| | |

| TOTAL UNDERLYING FUNDS

(INSTITUTIONAL SHARES) – 93.9% |

|

| | (Cost $699,454,841) | | $ | 935,637,993 | |

| | |

| | | | | | | | |

| | Exchange Traded Funds – 3.7% | |

| | 580,061 | | | SPDR S&P Bank Fund | | $ | 19,142,013 | |

| | 489,927 | | | Technology Select Sector SPDR Fund | | | 17,808,846 | |

| | |

| | TOTAL EXCHANGE TRADED FUNDS | | | | |

| | (Cost $31,936,533) | | $ | 36,950,859 | |

| | |

| | | | | | | | | | | | |

| Contracts | | Strike

Price | | | Expiration

Date | | | Value | |

| Option Purchased – 0.1% | |

TSE TOPIX Index Call Option | |

| 132 | | $ | 1,300 | | | | 06/13/14 | | | $ | 365,766 | |

| (Cost $758,365) | |

| |

| TOTAL INVESTMENTS – 97.7% | |

| (Cost $732,149,739) | | | $ | 972,954,618 | |

| |

| OTHER ASSETS IN EXCESS OF LIABILITIES – 2.3% | | | | 23,383,402 | |

| |

| NET ASSETS – 100.0% | | | $ | 996,338,020 | |

| |

| | |

| The percentage shown for each investment and investment category reflects the value of the respective investment or category as a percentage of net assets. |

(a) | | Represents Affiliated Funds. |

| | |

|

Investment Abbreviation: |

SPDR | | —Standard and Poor’s Depositary Receipts |

|

| | |

| The accompanying notes are an integral part of these financial statements. | | 19 |

GOLDMAN SACHS TAX-ADVANTAGED GLOBAL EQUITY PORTFOLIO

Schedule of Investments (continued)

February 28, 2014 (Unaudited)

|

| ADDITIONAL INVESTMENT INFORMATION |

FUTURES CONTRACTS — At February 28, 2014, the Portfolio had the following futures contracts:

| | | | | | | | | | | | | | |

| Type | | Number of

Contracts

Long (Short) | | | Expiration

Date | | Current

Value | | | Unrealized

Gain (Loss) | |

EURO STOXX 50 Index | | | 410 | | | March 2014 | | $ | 17,769,982 | | | $ | 1,062,869 | |

IBEX 35 Index | | | 63 | | | March 2014 | | | 8,763,979 | | | | 25,460 | |

| TOTAL | | | | | | | | | | | | $ | 1,088,329 | |

| | |

| 20 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS GLOBAL TAX-AWARE EQUITY PORTFOLIOS

Statements of Assets and Liabilities

February 28, 2014 (Unaudited)

| | | | | | | | | | |

| | | | | Enhanced Dividend

Global Equity

Portfolio | | | Tax-Advantaged

Global Equity

Portfolio | |

| | Assets: | |

| | Investments in Affiliated Underlying Funds, at value (cost $264,754,630 and $699,454,841) | | $ | 318,760,867 | | | $ | 935,637,993 | |

| | Investments, at value (cost $11,059,422 and $32,694,898) | | | 12,794,579 | | | | 37,316,625 | |

| | Cash | | | 3,378,869 | | | | 18,029,039 | |

| | Foreign currencies, at value (cost $2,034 and $5,762) | | | 2,020 | | | | 5,724 | |

| | Receivables: | | | | | | | | |

| | Portfolio shares sold | | | 1,197,803 | | | | 5,951,433 | |

| | Collateral on certain derivative contracts(a) | | | 1,080,000 | | | | 2,585,000 | |

| | Investments sold | | | 272,074 | | | | — | |

| | Reimbursement from investment adviser | | | 7,787 | | | | 11,103 | |

| | Other assets | | | 4,138 | | | | 5,349 | |

| | Total assets | | | 337,498,137 | | | | 999,542,266 | |

| | | | | | | | | | |

| | Liabilities: | |

| | Payables: | | | | | | | | |

| | Portfolio shares redeemed | | | 94,600 | | | | 1,177,000 | |

| | Amounts owed to affiliates | | | 47,804 | | | | 139,503 | |

| | Variation margin on certain derivative contracts | | | 21,670 | | | | 55,914 | |

| | Investments purchased | | | — | | | | 1,740,206 | |

| | Accrued expenses | | | 71,326 | | | | 91,623 | |

| | Total liabilities | | | 235,400 | | | | 3,204,246 | |

| | | | | | | | | | |

| | Net Assets: | |

| | Paid-in capital | | | 283,667,520 | | | | 749,845,334 | |

| | Undistributed (distributions in excess of) net investment income | | | (980,438 | ) | | | 2,007,259 | |

| | Accumulated net realized gain (loss) | | | (1,585,502 | ) | | | 2,553,111 | |

| | Net unrealized gain | | | 56,161,157 | | | | 241,932,316 | |

| | | NET ASSETS | | $ | 337,262,737 | | | $ | 996,338,020 | |

| | | Net Assets: | | | | | | | | |

| | | Class A | | $ | 212,171 | | | $ | 602,571 | |

| | | Institutional | | | 337,050,566 | | | | 995,735,449 | |

| | | Total Net Assets | | $ | 337,262,737 | | | $ | 996,338,020 | |

| | | Shares outstanding $0.001 par value (unlimited shares authorized): | | | | | | | | |

| | | Class A | | | 18,875 | | | | 47,223 | |

| | | Institutional | | | 29,845,916 | | | | 78,352,840 | |

| | | Net asset value, offering and redemption price per share:(b) | | | | | | | | |

| | | Class A | | | $11.24 | | | | $12.76 | |

| | | Institutional | | | 11.29 | | | | 12.71 | |

| | (a) | | Represents segregated cash relating to collateral on futures transactions. |

| | (b) | | Maximum public offering price per share for Class A shares of the Enhanced Dividend Global Equity and Tax-Advantaged Global Equity Portfolios is $11.89 and $13.50, respectively. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 21 |

GOLDMAN SACHS GLOBAL TAX-AWARE EQUITY PORTFOLIOS

Statements of Operations

For the Six Months Ended February 28, 2014 (Unaudited)

| | | | | | | | | | |

| | | | | Enhanced Dividend

Global Equity

Portfolio | | | Tax-Advantaged

Global Equity

Portfolio | |

| | Investment income: | |

| | Dividends from Affiliated Underlying Funds | | $ | 3,792,733 | | | $ | 12,582,252 | |

| | Dividends from Unaffiliated Funds | | | 98,564 | | | | 249,334 | |

| | Total investment income | | | 3,891,297 | | | | 12,831,586 | |

| | | | | | | | | | |

| | Expenses: | |

| | Management fees | | | 233,804 | | | | 646,560 | |

| | Transfer Agent fees(a) | | | 62,468 | | | | 172,931 | |

| | Professional fees | | | 35,725 | | | | 36,020 | |

| | Custody, accounting and administrative services | | | 26,078 | | | | 33,969 | |

| | Printing and mailing costs | | | 25,650 | | | | 40,962 | |

| | Registration fees | | | 14,986 | | | | 16,387 | |

| | Trustee fees | | | 10,832 | | | | 14,119 | |

| | Distribution and Service fees — Class A Shares | | | 200 | | | | 857 | |

| | Other | | | 9,799 | | | | 11,850 | |

| | Total expenses | | | 419,542 | | | | 973,655 | |

| | Less — expense reductions | | | (99,518 | ) | | | (95,074 | ) |

| | Net expenses | | | 320,024 | | | | 878,581 | |

| | NET INVESTMENT INCOME | | | 3,571,273 | | | | 11,953,005 | |

| | | | | | | | | | |

| | Realized and unrealized gain: | |

| | Net realized gain from: | | | | | | | | |

| | Investments in Affiliated Underlying Funds | | | 2,710,343 | | | | 15,885,607 | |

| | Investments | | | 605,498 | | | | 1,068,076 | |

| | Futures contracts | | | 1,203,913 | | | | 3,123,289 | |

| | Foreign currency transactions | | | 26,033 | | | | 64,408 | |

| | Capital gain distributions from Affiliated Underlying Funds | | | 7,910,646 | | | | 6,459,002 | |

| | Net change in unrealized gain on: | | | | | | | | |

| | Investments in Affiliated Underlying Funds | | | 16,456,149 | | | | 84,080,340 | |

| | Investments | | | 436,142 | | | | 1,623,495 | |

| | Futures contracts | | | 257,406 | | | | 714,175 | |

| | Foreign currency translation | | | 1,946 | | | | 10,474 | |

| | Net realized and unrealized gain | | | 29,608,076 | | | | 113,028,866 | |

| | NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 33,179,349 | | | $ | 124,981,871 | |

| | (a) | | Class specific Transfer Agent fees were as follows: |

| | | | | | | | |

| | | Transfer Agent Fees | |

Portfolio | | Class A | | | Institutional | |

Enhanced Dividend Global Equity | | $ | 152 | | | $ | 62,316 | |

Tax-Advantaged Global Equity | | | 651 | | | | 172,280 | |

| | |

| 22 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS GLOBAL TAX-AWARE EQUITY PORTFOLIOS

Statements of Changes in Net Assets

| | | | | | | | | | | | | | | | | | | | |

| | | | | Enhanced Dividend Global Equity

Portfolio | | | | | Tax-Advantaged Global Equity

Portfolio | |

| | | | | For the

Six Months Ended

February 28, 2014

(Unaudited) | | | For the

Fiscal Year Ended

August 31, 2013

| | | | | For the

Six Months Ended

February 28, 2014

(Unaudited) | | | For the

Fiscal Year Ended

August 31, 2013

| |

| | From operations: | |

| | Net investment income | | $ | 3,571,273 | | | $ | 5,787,590 | | | | | $ | 11,953,005 | | | $ | 10,381,242 | |

| | Net realized gain | | | 12,456,433 | | | | 11,892,680 | | | | | | 26,600,382 | | | | 18,768,814 | |

| | Net change in unrealized gain | | | 17,151,643 | | | | 12,269,346 | | | | | | 86,428,484 | | | | 63,456,041 | |

| | Net increase in net assets resulting from operations | | | 33,179,349 | | | | 29,949,616 | | | | | | 124,981,871 | | | | 92,606,097 | |

| | | | | | | | | | | | | | | | | | | | |

| | Distributions to shareholders: | |

| | From net investment income | | | | | | | | | | | | | | | | | | |

| | Class A Shares | | | (2,162 | ) | | | (2,275,656 | ) | | | | | — | | | | (4,171,091 | ) |

| | Institutional Shares | | | (4,881,333 | ) | | | (4,471,259 | ) | | | | | (11,583,396 | ) | | | (5,177,323 | ) |

| | From net realized gains | | | | | | | | | | | | | | | | | | |

| | Class A Shares | | | (5,994 | ) | | | (1,476,537 | ) | | | | | (17,701 | ) | | | (793,567 | ) |

| | Institutional Shares | | | (11,673,301 | ) | | | (941,687 | ) | | | | | (21,947,805 | ) | | | (745,537 | ) |

| | Total distributions to shareholders | | | (16,562,790 | ) | | | (9,165,139 | ) | | | | | (33,548,902 | ) | | | (10,887,518 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | From share transactions: | |

| | Proceeds from sales of shares | | | 39,347,023 | | | | 218,439,663 | | | | | | 179,088,861 | | | | 536,957,240 | |

| | Reinvestment of distributions | | | 16,205,596 | | | | 8,601,324 | | | | | | 32,487,429 | | | | 9,635,536 | |

| | Cost of shares redeemed | | | (19,578,059 | ) | | | (166,179,709 | ) | | | | | (47,166,178 | ) | | | (338,811,455 | ) |

| | Net increase in net assets resulting from share transactions | | | 35,974,560 | | | | 60,861,278 | | | | | | 164,410,112 | | | | 207,781,321 | |

| | TOTAL INCREASE | | | 52,591,119 | | | | 81,645,755 | | | | | | 255,843,081 | | | | 289,499,900 | |

| | | | | | | | | | | | | | | | | | | | |

| | Net assets: | |

| | Beginning of period | | | 284,671,618 | | | | 203,025,863 | | | | | | 740,494,939 | | | | 450,995,039 | |

| | End of period | | $ | 337,262,737 | | | $ | 284,671,618 | | | | | $ | 996,338,020 | | | $ | 740,494,939 | |

| | Undistributed (distributions in excess of) net

investment income | | $ | (980,438 | ) | | $ | 331,784 | | | | | $ | 2,007,259 | | | $ | 1,637,650 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 23 |

GOLDMAN SACHS ENHANCED DIVIDEND GLOBAL EQUITY PORTFOLIO

Financial Highlights

Selected Data for a Share Outstanding Throughout Each Period

��

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | Income (loss) from

investment operations | | | Distributions

to shareholders | |

| | | Year - Share Class | | Net asset

value,

beginning

of period | | | Net

investment

income(a)(b) | | | Net realized

and unrealized

gain (loss) | | | Total from

investment

operations | | | From net

investment

income | | | From net

realized

gains | | | Total

distributions | |

| | FOR THE SIX MONTHS ENDED FEBRUARY 28, (UNAUDITED) | |

| | 2014 - A | | $ | 10.64 | | | $ | 0.10 | | | $ | 1.07 | | | $ | 1.17 | | | $ | (0.15 | ) | | $ | (0.42 | ) | | $ | (0.57 | ) |

| | 2014 - Institutional | | | 10.69 | | | | 0.13 | | | | 1.06 | | | | 1.19 | | | | (0.17 | ) | | | (0.42 | ) | | | (0.59 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | FOR THE FISCAL YEARS ENDED AUGUST 31, | |

| | 2013 - A | | | 9.73 | | | | 0.21 | | | | 1.08 | | | | 1.29 | | | | (0.27 | ) | | | (0.11 | ) | | | (0.38 | ) |

| | 2013 - Institutional | | | 9.76 | | | | 0.26 | | | | 1.09 | | | | 1.35 | | | | (0.31 | ) | | | (0.11 | ) | | | (0.42 | ) |