UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman, Sachs & Co. | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: April 30, 2015

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | April 30, 2015 |

| | |

| | | | Multi-Asset Real Return Fund |

Goldman Sachs Multi-Asset Real Return Fund

| | | | |

TABLE OF CONTENTS | | | | |

| |

Principal Investment Strategies and Risks | | | 1 | |

| |

Investment Process | | | 2 | |

| |

Portfolio Management Discussions and Performance Summaries | | | 3 | |

| |

Schedule of Investments | | | 11 | |

| |

Financial Statements | | | 17 | |

| |

Financial Highlights | | | 20 | |

| |

Notes to the Financial Statements | | | 22 | |

| |

Other Information | | | 32 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Fund. For additional information concerning the risks applicable to the Fund, please see the Fund’s Prospectus.

The Goldman Sachs Multi-Asset Real Return Fund seeks long-term real return by investing in inflation sensitive assets (i.e., investments that, in the judgment of the Investment Adviser, are expected to perform favorably in rising or high inflationary environments). The Fund invests primarily in a portfolio of equity, fixed income and commodity asset classes (the “Underlying Asset Classes”), including derivatives that provide exposure to the Underlying Asset Classes. Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; risk of default by a counterparty; and liquidity risk. The Fund’s equity investments are subject to market risk, which means that the value of its investments may go up or down in response to the prospects of individual companies, particular industry sectors and/or general economic conditions. Investing in real estate investment trusts (REITs) involves certain unique risks in addition to those risks associated with investing in the real estate industry in general. REITs whose underlying properties are concentrated in a particular industry or geographic region are also subject to risks affecting such industries and regions. The securities of REITs involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements because of interest rate changes, economic conditions and other factors. The Fund may also invest in fixed income securities, which are subject to the risks associated with debt securities generally, including credit and interest rate risk. The Fund may invest in non-investment grade securities, which involve greater price volatility and present greater risks than higher rated fixed income securities. The value of the Fund’s treasury inflation protected securities (TIPS) generally fluctuates in response to inflationary concerns, and as inflationary concerns decrease, TIPS become less valuable. Any guarantee on U.S. government securities applies only to the underlying securities of the Fund if held to maturity and not to the value of the Fund’s shares. Foreign and emerging market investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic and political developments. Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. The Fund’s investments in pooled investment vehicles (including other investment companies, exchange-traded funds, master limited partnerships (MLPs) and publicly traded partnerships (PTPs)) subject it to additional expenses. Investments in MLPs are subject to certain risks, including risks related to limited control and limited rights to vote, potential conflicts of interest, cash flow risks, dilution risks, limited liquidity and risks related to the general partner’s right to force sales at undesirable times or prices. MLPs are also subject to risks relating to their complex tax structure, including the risk that a distribution received by the Fund from an MLP is treated as a return of capital, which may increase the Fund’s tax liability and require the Fund to restate the character of its distributions and amend shareholder tax reporting previously issued, and the risk that an MLP could lose its tax status as a partnership, resulting in a reduction in the value of the Fund’s investment in the MLP and lower income to the Fund. Risks of PTPs may include potential lack of liquidity and limitations on voting and distribution rights.

1

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

What Differentiates Goldman Sachs Multi-Asset Real Return Fund’s Investment Process?

The Goldman Sachs Multi-Asset Real Return Fund (the “Fund”) seeks to achieve long-term real return. The Fund invests primarily in a portfolio of equity, fixed income and commodity securities in an attempt to perform favorably in rising or high inflationary environments. The Fund seeks to provide exposure beyond traditional asset classes to protect against a broader set of inflation catalysts in various market environments.

| n | | Inflation-sensitive assets tend to move in the same direction as inflation which may preserve real portfolio returns. |

| n | | We seek to provide access to investments that have historically provided the necessary growth to protect purchasing power in periods of high or rising inflation. |

| n | | Traditional stocks and bonds may not be able to provide the necessary diversification to improve portfolio returns across changing market environments. |

| n | | The Fund invests in a diversified portfolio in an attempt to provide investors with lower volatility over the long-term. |

| n | | We utilize a comprehensive investment process that opportunistically shifts portfolio assets through long-term strategic allocation, tactical adjustments, underlying security selection and active risk management. |

| n | | The flexibility in our investment process helps us to respond to ever-changing markets and to balance the portfolio’s risk and potential return. |

| n | | We have a robust risk management framework, with multiple layers of oversight at the strategic allocation, security selection and firm levels. |

2

PORTFOLIO RESULTS

Goldman Sachs Multi-Asset Real Return Fund

Investment Objective

The Fund seeks to achieve long-term real return.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Portfolio Solutions Team discusses the Goldman Sachs Multi-Asset Real Return Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2015 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, IR and R Shares generated cumulative total returns, without sales charges, of -2.39%, -2.75%, -2.28%, -2.26% and -2.51%, respectively. These returns compare to the 0.60% cumulative total return of the Fund’s benchmark, the Barclays 1-10 Year U.S. TIPS Index (the “Barclays Index”), during the same time period. |

| Q | | What economic and market factors most influenced the Fund during the Reporting Period? |

| A | | Unfolding divergence in central bank monetary policy and in economic growth across countries and regions around the globe, particularly in developed markets, was a dominant theme impacting the various asset classes through most of the Reporting Period. More specifically, central bank action across the globe surprised the financial markets early in 2015, with 14 central banks announcing quantitative easing measures in January 2015 alone. Such actions brought risk assets into favor for a time. Meanwhile, in the U.S., the Federal Reserve (the “Fed”) had ended its quantitative easing program asset purchases on schedule at the end of October 2014, but March 2015’s Fed meeting surprised to the dovish side, as it lowered forecasts for interest rates and U.S. Gross Domestic Product (“GDP”). (A dovish economy would tend to indicate lower interest rates; a dovish action or event is one that is not strong or aggressive (opposite of hawkish).) This led the U.S. Treasury yield curve to flatten modestly, meaning the differential between longer-term and shorter-term yields narrowed. The momentum in global monetary and economic divergence slowed only slightly in April 2015 on the heels of global economic growth concerns, including a lackluster first quarter 2015 report for U.S. GDP. |

| | On the inflation front, falling energy prices and a weaker global economic growth outlook, coupled with a strengthening U.S. dollar, led to more muted U.S. inflation expectations. Core inflation remained range-bound during the Reporting Period between 1.6% and 1.8%, but the market saw a slight pick-up from the lower end of the range in 2015, with March 2015 marking the third consecutive month of increases against expectations of a moderate decline. Commodities underperformed during the Reporting Period, as oil prices remained depressed due to unbalanced supply/ demand dynamics, with supply outpacing demand. We believe the relative strength in oil prices seen toward the end of the Reporting Period is likely to prove transient in nature, and we expect plentiful supply to maintain downward price pressures. The Reporting Period saw the U.S. dollar strengthen against most major global currencies, supported by improving macroeconomic data, improving budget deficit and trade balances, and widespread monetary easing outside the U.S. Accommodative economic policy and a generally positive growth outlook in Europe contributed positively to equity performance across the Eurozone (as measured by the Dow Jones Euro Stoxx 50 Index), though European equities still lagged developed market equities broadly (as measured by the MSCI World Index) due to ongoing negotiations over the Greek debt situation toward the end of the Reporting Period. Economic conditions in China also remained comparatively weaker, but expectations of further easing by the People’s Bank of China (“PBOC”) and domestic demand helped offset the impact of slower growth amidst a controlled slowdown. |

| | The 12-month percent change of the U.S. Consumer Price Index (“CPI”) for April 2015 was -0.2%. The core CPI, which excludes food and energy, for the same time period rose 1.8%. The food index advanced 2.0% during the |

3

PORTFOLIO RESULTS

| | Reporting Period, and the energy index of the CPI actually declined 19.4% over the same time span. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | During the Reporting Period, the Fund posted negative absolute returns and underperformed the Barclays Index on a relative basis. U.S. Treasury inflation protected securities (“TIPS”) failed to keep pace with nominal, or non-inflation protected, U.S. Treasuries, as break-even inflation levels were negatively impacted by the drop in crude oil prices during the Reporting Period. (The break-even inflation rate is the difference between the nominal yield on a fixed-rate investment and the real yield on an inflation-linked investment of similar maturity and credit quality. If inflation averages more than the break-even, the inflation-linked investment will outperform the fixed-rate. Conversely, if inflation averages below the break-even, the fixed-rate will outperform the inflation-linked.) |

| | The Fund’s underperformance relative to the Barclays Index was primarily driven by strategic asset allocation, which reflects a longer-term perspective of diversifying and investing in inflation-sensitive asset classes beyond TIPS. These additional asset classes included equities, real estate securities, Master Limited Partnerships (“MLPs”), infrastructure, commodities and additional fixed income sectors. The Fund’s longer-term strategic asset allocation performance was partially offset by effective short-term tactical allocation positioning. Underlying security selection and implementation also contributed positively. |

| | More specifically, the Fund’s strategic asset allocation performance was driven most during the Reporting Period by its exposure to commodities and MLPs and, to a lesser extent, by its exposure to local emerging markets debt. Interest rate curve positioning, intended to protect against potential increases in real rates, was also a detractor. Conversely, the Fund’s exposure to global infrastructure equities, select equity sectors (i.e., health care, consumer staples, energy and materials) and U.S. real estate securities, via a variety of underlying investments, contributed positively to relative results. The Fund’s strategic asset allocation to an unconstrained multi-sector fixed income investment also boosted results. |

| | Tactical asset allocation overall contributed positively to the Fund’s relative results during the Reporting Period. As mentioned earlier, in seeking its objective to achieve long-term real return, the Fund invests in a diversified portfolio of inflation-sensitive equity, fixed income and commodity securities and exposures. The Fund’s portfolio managers allocate across these diversified exposures by addressing the multiple potential drivers of inflation in what we determine to be a balanced way. This sets the Fund’s strategic asset allocation. The Fund’s portfolio managers then adjust the relative sizing of these exposures based on a shorter investment horizon that reflects tactical market views. Relative to the strategic asset allocation set during the Reporting Period, the Fund was overweight equities and underweight fixed income. More specifically, within equities, the Fund favored U.S. large-cap equities broadly as well as non-U.S. equities, mainly through index exposure in Japan and Europe. The Fund had an underweighted allocation to inflation-sensitive U.S. equity sectors. Within fixed income, the Fund was underweight U.S. TIPS for the majority of the Reporting Period and was positioned for anticipated increases in U.S. rates. The Fund also had only modest exposure to local emerging markets debt. For the Reporting Period overall, the Fund’s allocation to equities and its local emerging markets debt positioning added value, partially offset by its fixed income exposure and interest rate curve positioning, which detracted. |

| | Underlying fund implementation and security selection overall contributed positively to the Fund’s results. Positive security selection in commodities, MLPs and U.S. real estate securities offset security selection in fixed income sectors, which detracted. |

| Q | | How was the Fund positioned during the Reporting Period? |

| A | | At the start of the Reporting Period, the Fund had approximately 13.4% of its total net assets invested in commodity-related investments; approximately 48.6% of its total net assets invested in equity-related investments; and 40.7% of its total net assets invested in fixed income-related investments. The strategic asset allocation of the Fund reflects a risk-based allocation approach to increase diversification across the portfolio. |

| Q | | How did you tactically manage the Fund’s allocations during the Reporting Period? |

| A | | During the Reporting Period, positioning within the Fund was adjusted to reflect what we considered to be modest signs of improvement in global economic growth sentiment. Tactically, this positioning translated into a positive view of risk assets, maintained through a broad tilt toward U.S. and |

4

PORTFOLIO RESULTS

| | other developed market equities, which was modulated based on regional and sector exposure views. |

| | Within the allocation to U.S. equity sectors, our team reduced the Fund’s allocation to energy-related equities during the Reporting Period, as we believed the sector would be negatively impacted by ongoing oil price volatility, uncertain supply/demand dynamics and geopolitical concerns. Instead, we favored the health care sector given what we viewed as a robust product pipeline and supportive reform environment. |

| | Our team also reduced the Fund’s allocation to commodities within the Fund during the Reporting Period. As inventory levels remained elevated and production had not significantly decelerated, we did not expect commodities to be a meaningful driver of rising inflation expectations. Similarly, the Fund maintained only a modest exposure to emerging markets debt denominated in local currencies. Such positioning proved prudent, as investors shied away from economies sensitive to plummeting commodity prices and currency depreciation relative to the U.S. dollar. |

| | Additionally, our team maintained a generally negative view on U.S. interest rates amidst the persistently low rate environment. The implementation of this view on U.S. interest rates was through a shorter duration stance than that of the Barclays Index. (Duration is a measure of sensitivity to changes in interest rates.) |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, the Fund used interest rate swaps and Eurodollar futures in seeking tactical interest rate curve shape positions. (Different positions may be taken within the Fund based on expectations of changes in interest rates and expectations of changes in the yield curve. Changes in the shape of the yield curve will change the relative price of bonds represented by the curve.) The Fund also used equity index futures during the Reporting Period to tactically adjust the amount of risk incurred from exposure to equities in four markets — the U.S., the U.K., Europe and Japan. In addition, some of the Fund’s underlying fund investments used derivatives during the Reporting Period to manage duration along the yield curve, to apply their active investment views with greater versatility, seeking greater risk management precision, and to gain exposure to equity, fixed income and commodity asset classes. As market conditions warranted during the Reporting Period, some of these underlying funds engaged in interest rate swaps, swaptions (or options on interest rate swap contracts) and futures. |

| Q | | How was the Fund positioned at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had approximately 10.8% of its total net assets invested in commodity-related investments; 44.0% of its total net assets invested in equity-related investments; and 44.1% of its total net assets invested in fixed income-related investments. We believe that, fundamentally, U.S. rates were too low at the end of the Reporting Period and that as U.S. monetary policy moves away from quantitative easing and stimulation, interest rate volatility may re-enter the market. The above sector breakout is inclusive of derivative exposure across all asset classes. |

| Q | | What is the Fund’s tactical asset allocation view and strategy for the months ahead? |

| A | | Despite global economic growth concerns and weak first quarter 2015 U.S. GDP data released in April 2015, we maintained our conviction at the end of the Reporting Period that global output may improve modestly in aggregate, but ongoing divergence in economic activity and monetary policy may drive market performance. Falling energy prices and a weaker global economic growth outlook, coupled with a stronger U.S. dollar, resulted in downward pressure on U.S. inflation expectations during the Reporting Period. While we acknowledge the potential for this trend to continue in the near term, massive economic stimulus from major central banks outside the U.S., including the Bank of Japan (“BoJ”) and European Central Bank (“ECB”), may have larger implications for inflation on a long-term basis. Should economic growth return, as we anticipate, we expect to see a rise in U.S. interest rates, and we thus intend to maintain the Fund’s shorter duration relative to that of the Barclays Index. Further, in our view, the macroeconomic environment was still supportive of risk assets at the end of the Reporting Period, and we anticipate continued divergence in performance across regions, particularly in developed markets. |

| | At the end of the Reporting Period, we did not see deflationary risks, but we maintain our view that U.S. inflation may remain below target, with expectations of an interest rate hike in mid-2015 at the earliest. After the initial rate hike by the Fed, we believe monetary policy tightening may proceed at a more accelerated pace than that implied by the market at the end of April 2015. Ultimately, we believe |

5

PORTFOLIO RESULTS

| | timing for the first rate hike will depend on the two conditions set by the Fed in March 2015 — improvement in the labor market and inflation moving to its 2% objective over medium term. A stronger U.S. dollar and a renewed fall in oil prices may continue to weigh on inflation, although the rise in oil prices seen in April 2015 may be seen as a reprieve, helping to firm up U.S. inflation prospects. Overall, however, we expect core inflation to remain quiescent, or subdued. We further expect faster wage gains and a gradual recovery in oil prices, combined with a slower pace of U.S. dollar appreciation, to push headline inflation toward the Fed’s 2% target. (Headline inflation is the raw inflation figure as reported through the Consumer Price Index (“CPI”) that is released monthly by the Bureau of Labor Statistics. The CPI calculates the cost to purchase a fixed basket of goods as a way of determining how much inflation is occurring in the broad economy. The headline inflation figure is not adjusted for seasonality or for the often volatile elements of food and energy prices, which are removed in the core CPI.) |

| | Given this view, we believe the Fund was well positioned at the end of the Reporting Period to perform well in a variety of inflationary environments. We continue to seek opportunities to incorporate our tactical market views on a shorter-term basis. |

6

FUND BASICS

Multi-Asset Real Return Fund

as of April 30, 2015

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2014–April 30, 2015 | | Fund Total Return

(based on NAV)1 | | | Barclays Index2 | |

| | Class A | | | -2.39 | % | | | 0.60 | % |

| | Class C | | | -2.75 | | | | 0.60 | |

| | Institutional | | | -2.28 | | | | 0.60 | |

| | Class IR | | | -2.26 | | | | 0.60 | |

| | | Class R | | | -2.51 | | | | 0.60 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Barclays 1-10 Year U.S. TIPS Index is an unmanaged index comprised of U.S. Treasury Inflation Protected securities having a maturity of at least 1 year and less than 10 years. It is not possible to invest in an unmanaged index. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 3/31/15 | | One Year | | | Since Inception | | | Inception Date |

| | Class A | | | -8.28 | % | | | -1.14 | % | | 8/30/2013 |

| | Class C | | | -4.64 | | | | 1.64 | | | 8/30/2013 |

| | Institutional | | | -2.56 | | | | 2.81 | | | 8/30/2013 |

| | Class IR | | | -2.70 | | | | 2.67 | | | 8/30/2013 |

| | | Class R | | | -3.19 | | | | 2.12 | | | 8/30/2013 |

| | 3 | | The Standardized Total Returns are cumulative total returns (only if performance is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.50% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class IR and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

7

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.28 | % | | | 3.51 | % |

| | Class C | | | 2.05 | | | | 4.62 | |

| | Institutional | | | 0.88 | | | | 3.45 | |

| | Class IR | | | 1.02 | | | | 3.59 | |

| | | Class R | | | 1.53 | | | | 4.10 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 29, 2016, and prior to such date the investment adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | |

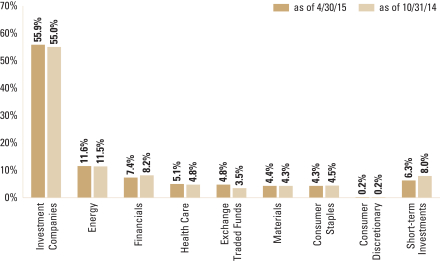

| | TOP TEN HOLDINGS AS OF 4/30/155 |

| | | Holding | | % of Net Assets | | | Line of Business |

| | Goldman Sachs Strategic Income Fund | | | 24.9 | % | | Investment Company |

| | Goldman Sachs Inflation Protected Securities Fund | | | 15.0 | | | Investment Company |

| | Goldman Sachs Commodity Strategy Fund | | | 10.9 | | | Investment Company |

| | iShares Global Infrastructure ETF | | | 4.7 | | | Exchange Traded Funds |

| | Goldman Sachs Local Emerging Markets Debt Fund | | | 4.6 | | | Investment Company |

| | Enterprise Products Partners LP | | | 0.9 | | | Oil, Gas & Consumable Fuels |

| | Simon Property Group, Inc. | | | 0.9 | | | Real Estate Investment Trusts |

| | Exxon Mobil Corp. | | | 0.8 | | | Oil, Gas & Consumable Fuels |

| | The Williams Cos., Inc. | | | 0.7 | | | Oil, Gas & Consumable Fuels |

| | | Plains All American Pipeline LP | | | 0.7 | | | Oil, Gas & Consumable Fuels |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

8

FUND BASICS

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of Exchange Traded Funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. Short-term investments represent repurchase agreements. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

9

FUND BASICS

Index Definitions

The Dow Jones Euro Stoxx 50 Index is a market capitalization-weighted stock index of 50 large, blue-chip European companies operating within Eurozone nations.

The MSCI World Index is a market capitalization-weighted benchmark index made up of equities from 23 developed market countries, including the United States.

10

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Schedule of Investments

April 30, 2015 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – 32.7% | |

| | Beverages – 0.9% | |

| | 41 | | | Brown-Forman Corp. Class B | | $ | 3,699 | |

| | 56 | | | Coca-Cola Enterprises, Inc. | | | 2,487 | |

| | 46 | | | Constellation Brands, Inc. Class A* | | | 5,333 | |

| | 51 | | | Dr. Pepper Snapple Group, Inc. | | | 3,804 | |

| | 46 | | | Molson Coors Brewing Co. Class B | | | 3,382 | |

| | 38 | | | Monster Beverage Corp.* | | | 5,210 | |

| | 377 | | | PepsiCo., Inc. | | | 35,860 | |

| | 3 | | | The Boston Beer Co., Inc. Class A* | | | 743 | |

| | 1,000 | | | The Coca-Cola Co. | | | 40,560 | |

| | | | | | | | |

| | | | | | | 101,078 | |

| | |

| | Biotechnology – 1.0% | |

| | 42 | | | Alexion Pharmaceuticals, Inc.* | | | 7,108 | |

| | 148 | | | Amgen, Inc. | | | 23,371 | |

| | 46 | | | Biogen, Inc.* | | | 17,201 | |

| | 157 | | | Celgene Corp.* | | | 16,965 | |

| | 289 | | | Gilead Sciences, Inc.* | | | 29,047 | |

| | 15 | | | Regeneron Pharmaceuticals, Inc.* | | | 6,862 | |

| | 9 | | | United Therapeutics Corp.* | | | 1,437 | |

| | 50 | | | Vertex Pharmaceuticals, Inc.* | | | 6,164 | |

| | | | | | | | |

| | | | | | | 108,155 | |

| | |

| | Chemicals – 2.9% | |

| | 23 | | | A. Schulman, Inc. | | | 976 | |

| | 124 | | | Air Products & Chemicals, Inc. | | | 17,785 | |

| | 45 | | | Airgas, Inc. | | | 4,558 | |

| | 70 | | | Albemarle Corp. | | | 4,179 | |

| | 40 | | | Ashland, Inc. | | | 5,054 | |

| | 26 | | | Balchem Corp. | | | 1,363 | |

| | 41 | | | Cabot Corp. | | | 1,752 | |

| | 56 | | | Calgon Carbon Corp. | | | 1,243 | |

| | 31 | | | CF Industries Holdings, Inc. | | | 8,912 | |

| | 52 | | | Cytec Industries, Inc. | | | 2,875 | |

| | 584 | | | E.I. du Pont de Nemours and Co. | | | 42,749 | |

| | 97 | | | Eastman Chemical Co. | | | 7,393 | |

| | 171 | | | Ecolab, Inc. | | | 19,149 | |

| | 33 | | | Flotek Industries, Inc.* | | | 472 | |

| | 87 | | | FMC Corp. | | | 5,160 | |

| | 42 | | | H.B. Fuller Co. | | | 1,754 | |

| | 22 | | | Innophos Holdings, Inc. | | | 1,162 | |

| | 48 | | | International Flavors & Fragrances, Inc. | | | 5,508 | |

| | 47 | | | Intrepid Potash, Inc.* | | | 589 | |

| | 12 | | | LSB Industries, Inc.* | | | 509 | |

| | 256 | | | LyondellBasell Industries NV Class A | | | 26,501 | |

| | 29 | | | Minerals Technologies, Inc. | | | 1,964 | |

| | 312 | | | Monsanto Co. | | | 35,555 | |

| | 8 | | | NewMarket Corp. | | | 3,575 | |

| | 52 | | | Olin Corp. | | | 1,536 | |

| | 34 | | | OM Group, Inc. | | | 1,021 | |

| | 73 | | | PolyOne Corp. | | | 2,851 | |

| | 87 | | | PPG Industries, Inc. | | | 19,276 | |

| | 181 | | | Praxair, Inc. | | | 22,069 | |

| | 12 | | | Quaker Chemical Corp. | | | 999 | |

| | 90 | | | RPM International, Inc. | | | 4,279 | |

| | 34 | | | Sensient Technologies Corp. | | | 2,222 | |

| | 74 | | | Sigma-Aldrich Corp. | | | 10,280 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Chemicals – (continued) | |

| | 704 | | | The Dow Chemical Co. | | $ | 35,904 | |

| | 204 | | | The Mosaic Co. | | | 8,976 | |

| | 31 | | | The Scotts Miracle-Gro Co. Class A | | | 2,000 | |

| | 51 | | | The Sherwin-Williams Co. | | | 14,178 | |

| | 46 | | | The Valspar Corp. | | | 3,731 | |

| | | | | | | | |

| | | | | | | 330,059 | |

| | |

| | Construction Materials – 0.1% | |

| | 32 | | | Eagle Materials, Inc. | | | 2,668 | |

| | 62 | | | Headwaters, Inc.* | | | 1,090 | |

| | 38 | | | Martin Marietta Materials, Inc. | | | 5,421 | |

| | 86 | | | Vulcan Materials Co. | | | 7,355 | |

| | | | | | | | |

| | | | | | | 16,534 | |

| | |

| | Containers & Packaging – 0.4% | |

| | 42 | | | AptarGroup, Inc. | | | 2,607 | |

| | 62 | | | Avery Dennison Corp. | | | 3,447 | |

| | 83 | | | Ball Corp. | | | 6,093 | |

| | 56 | | | Bemis Co., Inc. | | | 2,520 | |

| | 24 | | | Greif, Inc. Class A | | | 978 | |

| | 109 | | | MeadWestvaco Corp. | | | 5,319 | |

| | 111 | | | Owens-Illinois, Inc.* | | | 2,654 | |

| | 65 | | | Packaging Corp. of America | | | 4,497 | |

| | 94 | | | Rock-Tenn Co. Class A | | | 5,920 | |

| | 129 | | | Sealed Air Corp. | | | 5,883 | |

| | 29 | | | Silgan Holdings, Inc. | | | 1,562 | |

| | 68 | | | Sonoco Products Co. | | | 3,039 | |

| | | | | | | | |

| | | | | | | 44,519 | |

| | |

| | Energy Equipment & Services – 0.7% | |

| | 27 | | | Atwood Oceanics, Inc. | | | 901 | |

| | 104 | | | Baker Hughes, Inc. | | | 7,120 | |

| | 10 | | | Bristow Group, Inc. | | | 621 | |

| | 49 | | | Cameron International Corp.* | | | 2,686 | |

| | 23 | | | Diamond Offshore Drilling, Inc. | | | 770 | |

| | 15 | | | Dresser-Rand Group, Inc.* | | | 1,240 | |

| | 14 | | | Dril-Quip, Inc.* | | | 1,116 | |

| | 53 | | | Ensco PLC Class A | | | 1,446 | |

| | 14 | | | Exterran Holdings, Inc. | | | 519 | |

| | 62 | | | FMC Technologies, Inc.* | | | 2,734 | |

| | 203 | | | Halliburton Co. | | | 9,937 | |

| | 37 | | | Helix Energy Solutions Group, Inc.* | | | 610 | |

| | 23 | | | Helmerich & Payne, Inc. | | | 1,793 | |

| | 84 | | | Nabors Industries Ltd. | | | 1,403 | |

| | 97 | | | National Oilwell Varco, Inc. | | | 5,278 | |

| | 64 | | | Noble Corp. PLC | | | 1,108 | |

| | 30 | | | Oceaneering International, Inc. | | | 1,653 | |

| | 16 | | | Oil States International, Inc.* | | | 761 | |

| | 36 | | | Patterson-UTI Energy, Inc. | | | 805 | |

| | 47 | | | Rowan Cos. PLC Class A | | | 996 | |

| | 310 | | | Schlumberger Ltd. | | | 29,329 | |

| | 43 | | | Superior Energy Services, Inc. | | | 1,097 | |

| | 92 | | | Transocean Ltd. | | | 1,731 | |

| | 15 | | | Unit Corp.* | | | 523 | |

| | 17 | | | US Silica Holdings, Inc. | | | 635 | |

| | | | | | | | |

| | | | | | | 76,812 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 11 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Schedule of Investments (continued)

April 30, 2015 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Food & Staples Retailing – 1.0% | |

| | 16 | | | Casey’s General Stores, Inc. | | $ | 1,315 | |

| | 108 | | | Costco Wholesale Corp. | | | 15,449 | |

| | 289 | | | CVS Health Corp. | | | 28,695 | |

| | 73 | | | Safeway Casa Ley | | | 74 | |

| | 73 | | | Safeway PDC, LLC | | | 4 | |

| | 52 | | | SUPERVALU, Inc.* | | | 457 | |

| | 158 | | | Sysco Corp. | | | 5,851 | |

| | 121 | | | The Kroger Co. | | | 8,338 | |

| | 20 | | | United Natural Foods, Inc.* | | | 1,349 | |

| | 398 | | | Wal-Mart Stores, Inc. | | | 31,064 | |

| | 221 | | | Walgreens Boots Alliance, Inc. | | | 18,328 | |

| | 103 | | | Whole Foods Market, Inc. | | | 4,919 | |

| | | | | | | | |

| | | | | | | 115,843 | |

| | |

| | Food Products – 0.8% | |

| | 163 | | | Archer-Daniels-Midland Co. | | | 7,967 | |

| | 50 | | | Campbell Soup Co. | | | 2,235 | |

| | 105 | | | ConAgra Foods, Inc. | | | 3,796 | |

| | 35 | | | Darling Ingredients, Inc.* | | | 478 | |

| | 45 | | | Flowers Foods, Inc. | | | 1,005 | |

| | 147 | | | General Mills, Inc. | | | 8,135 | |

| | 48 | | | Hormel Foods Corp. | | | 2,609 | |

| | 24 | | | Ingredion, Inc. | | | 1,906 | |

| | 61 | | | Kellogg Co. | | | 3,863 | |

| | 29 | | | Keurig Green Mountain, Inc. | | | 3,375 | |

| | 149 | | | Kraft Foods Group, Inc. | | | 12,628 | |

| | 9 | | | Lancaster Colony Corp. | | | 807 | |

| | 46 | | | McCormick & Co., Inc. | | | 3,464 | |

| | 52 | | | Mead Johnson Nutrition Co. | | | 4,988 | |

| | 414 | | | Mondelez International, Inc. Class A | | | 15,885 | |

| | 14 | | | Post Holdings, Inc.* | | | 657 | |

| | 8 | | | Sanderson Farms, Inc. | | | 601 | |

| | 13 | | | Snyder’s-Lance, Inc. | | | 384 | |

| | 26 | | | The Hain Celestial Group, Inc.* | | | 1,566 | |

| | 37 | | | The Hershey Co. | | | 3,401 | |

| | 22 | | | The J.M. Smucker Co. | | | 2,550 | |

| | 15 | | | TreeHouse Foods, Inc.* | | | 1,219 | |

| | 72 | | | Tyson Foods, Inc. Class A | | | 2,844 | |

| | 42 | | | WhiteWave Foods Co. Class A* | | | 1,847 | |

| | | | | | | | |

| | | | | | | 88,210 | |

| | |

| | Health Care Equipment & Supplies – 0.8% | |

| | 294 | | | Abbott Laboratories | | | 13,647 | |

| | 8 | | | ABIOMED, Inc.* | | | 506 | |

| | 20 | | | Align Technology, Inc.* | | | 1,177 | |

| | 98 | | | Baxter International, Inc. | | | 6,736 | |

| | 42 | | | Becton Dickinson & Co. | | | 5,917 | |

| | 278 | | | Boston Scientific Corp.* | | | 4,954 | |

| | 19 | | | C.R. Bard, Inc. | | | 3,165 | |

| | 30 | | | DENTSPLY International, Inc. | | | 1,530 | |

| | 23 | | | Edwards Lifesciences Corp.* | | | 2,913 | |

| | 11 | | | Haemonetics Corp.* | | | 446 | |

| | 12 | | | Halyard Health, Inc.* | | | 582 | |

| | 13 | | | Hill-Rom Holdings, Inc. | | | 649 | |

| | 53 | | | Hologic, Inc.* | | | 1,788 | |

| | 10 | | | IDEXX Laboratories, Inc.* | | | 1,254 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Health Care Equipment & Supplies – (continued) | |

| | 7 | | | Intuitive Surgical, Inc.* | | $ | 3,472 | |

| | 289 | | | Medtronic PLC | | | 21,516 | |

| | 12 | | | NuVasive, Inc.* | | | 537 | |

| | 9 | | | Sirona Dental Systems, Inc.* | | | 835 | |

| | 64 | | | St. Jude Medical, Inc. | | | 4,483 | |

| | 16 | | | STERIS Corp. | | | 1,064 | |

| | 62 | | | Stryker Corp. | | | 5,719 | |

| | 8 | | | Teleflex, Inc. | | | 984 | |

| | 11 | | | The Cooper Cos., Inc. | | | 1,959 | |

| | 12 | | | Thoratec Corp.* | | | 481 | |

| | 24 | | | Varian Medical Systems, Inc.* | | | 2,132 | |

| | 22 | | | West Pharmaceutical Services, Inc. | | | 1,172 | |

| | 30 | | | Zimmer Holdings, Inc. | | | 3,295 | |

| | | | | | | | |

| | | | | | | 92,913 | |

| | |

| | Health Care Providers & Services – 1.0% | |

| | 70 | | | Aetna, Inc. | | | 7,481 | |

| | 38 | | | AmerisourceBergen Corp. | | | 4,343 | |

| | 13 | | | Amsurg Corp.* | | | 815 | |

| | 55 | | | Anthem, Inc. | | | 8,301 | |

| | 68 | | | Cardinal Health, Inc. | | | 5,735 | |

| | 20 | | | Centene Corp.* | | | 1,240 | |

| | 52 | | | CIGNA Corp. | | | 6,481 | |

| | 28 | | | Community Health Systems, Inc.* | | | 1,503 | |

| | 38 | | | DaVita HealthCare Partners, Inc.* | | | 3,082 | |

| | 141 | | | Express Scripts Holding Co.* | | | 12,182 | |

| | 58 | | | HCA Holdings, Inc.* | | | 4,293 | |

| | 17 | | | Health Net, Inc.* | | | 895 | |

| | 17 | | | Henry Schein, Inc.* | | | 2,331 | |

| | 30 | | | Humana, Inc. | | | 4,968 | |

| | 19 | | | Laboratory Corp. of America Holdings* | | | 2,272 | |

| | 10 | | | LifePoint Hospitals, Inc.* | | | 749 | |

| | 47 | | | McKesson Corp. | | | 10,500 | |

| | 22 | | | MEDNAX, Inc.* | | | 1,557 | |

| | 9 | | | Molina Healthcare, Inc.* | | | 533 | |

| | 14 | | | Omnicare, Inc. | | | 1,232 | |

| | 20 | | | Owens & Minor, Inc. | | | 674 | |

| | 18 | | | Patterson Cos., Inc. | | | 845 | |

| | 32 | | | Quest Diagnostics, Inc. | | | 2,286 | |

| | 24 | | | Tenet Healthcare Corp.* | | | 1,149 | |

| | 186 | | | UnitedHealth Group, Inc. | | | 20,720 | |

| | 18 | | | Universal Health Services, Inc. Class B | | | 2,105 | |

| | 20 | | | VCA, Inc.* | | | 1,019 | |

| | 11 | | | WellCare Health Plans, Inc.* | | | 852 | |

| | | | | | | | |

| | | | | | | 110,143 | |

| | |

| | Health Care Technology* – 0.1% | |

| | 49 | | | Allscripts Healthcare Solutions, Inc. | | | 651 | |

| | 59 | | | Cerner Corp. | | | 4,237 | |

| | 14 | | | Medidata Solutions, Inc. | | | 748 | |

| | | | | | | | |

| | | | | | | 5,636 | |

| | |

| | Hotels, Restaurants & Leisure* – 0.2% | |

| | 353 | | | Hyatt Hotels Corp. Class A | | | 20,492 | |

| | |

| | Household Durables* – 0.1% | |

| | 179 | | | Toll Brothers, Inc. | | | 6,362 | |

| | |

| | |

| 12 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

| | | | | | | | |

Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Household Products – 0.8% | |

| | 28 | | | Church & Dwight Co., Inc. | | $ | 2,273 | |

| | 215 | | | Colgate-Palmolive Co. | | | 14,465 | |

| | 19 | | | Energizer Holdings, Inc. | | | 2,596 | |

| | 88 | | | Kimberly-Clark Corp. | | | 9,652 | |

| | 41 | | | The Clorox Co. | | | 4,350 | |

| | 694 | | | The Procter & Gamble Co. | | | 55,180 | |

| | | | | | | | |

| | | | | | | 88,516 | |

| | |

| | Life Sciences Tools & Services – 0.2% | |

| | 75 | | | Agilent Technologies, Inc. | | | 3,103 | |

| | 7 | | | Bio-Techne Corp. | | | 672 | |

| | 11 | | | Charles River Laboratories International, Inc.* | | | 761 | |

| | 6 | | | Mettler-Toledo International, Inc.* | | | 1,902 | |

| | 16 | | | PAREXEL International Corp.* | | | 1,017 | |

| | 26 | | | PerkinElmer, Inc. | | | 1,333 | |

| | 79 | | | Thermo Fisher Scientific, Inc. | | | 9,928 | |

| | 16 | | | Waters Corp.* | | | 2,003 | |

| | | | | | | | |

| | | | | | | 20,719 | |

| | |

| | Metals & Mining – 0.6% | |

| | 122 | | | AK Steel Holding Corp.* | | | 620 | |

| | 772 | | | Alcoa, Inc. | | | 10,360 | |

| | 83 | | | Allegheny Technologies, Inc. | | | 2,821 | |

| | 33 | | | Carpenter Technology Corp. | | | 1,427 | |

| | 35 | | | Century Aluminum Co.* | | | 451 | |

| | 113 | | | Cliffs Natural Resources, Inc. | | | 671 | |

| | 102 | | | Commercial Metals Co. | | | 1,693 | |

| | 24 | | | Compass Minerals International, Inc. | | | 2,120 | |

| | 663 | | | Freeport-McMoRan, Inc. | | | 15,428 | |

| | 37 | | | Globe Specialty Metals, Inc. | | | 737 | |

| | 10 | | | Kaiser Aluminum Corp. | | | 804 | |

| | 12 | | | Materion Corp. | | | 480 | |

| | 318 | | | Newmont Mining Corp. | | | 8,424 | |

| | 193 | | | Nucor Corp. | | | 9,430 | |

| | 53 | | | Reliance Steel & Aluminum Co. | | | 3,430 | |

| | 46 | | | Royal Gold, Inc. | | | 2,969 | |

| | 17 | | | RTI International Metals, Inc.* | | | 640 | |

| | 165 | | | Steel Dynamics, Inc. | | | 3,652 | |

| | 92 | | | Stillwater Mining Co.* | | | 1,236 | |

| | 40 | | | SunCoke Energy, Inc. | | | 701 | |

| | 28 | | | TimkenSteel Corp. | | | 817 | |

| | 108 | | | United States Steel Corp. | | | 2,594 | |

| | 45 | | | Worthington Industries, Inc. | | | 1,216 | |

| | | | | | | | |

| | | | | | | 72,721 | |

| | |

| | Oil, Gas & Consumable Fuels – 10.8% | |

| | 119 | | | Anadarko Petroleum Corp. | | | 11,198 | |

| | 700 | | | Antero Midstream Partners LP | | | 17,500 | |

| | 91 | | | Apache Corp. | | | 6,224 | |

| | 650 | | | Buckeye Partners LP | | | 53,027 | |

| | 106 | | | Cabot Oil & Gas Corp. | | | 3,585 | |

| | 84 | | | California Resources Corp. | | | 781 | |

| | 14 | | | Carrizo Oil & Gas, Inc.* | | | 780 | |

| | 132 | | | Chesapeake Energy Corp. | | | 2,082 | |

| | 456 | | | Chevron Corp. | | | 50,643 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Oil, Gas & Consumable Fuels – (continued) | |

| | 20 | | | Cimarex Energy Co. | | $ | 2,488 | |

| | 400 | | | Columbia Pipeline Partners LP | | | 10,820 | |

| | 299 | | | ConocoPhillips | | | 20,308 | |

| | 62 | | | CONSOL Energy, Inc. | | | 2,014 | |

| | 800 | | | DCP Midstream Partners LP | | | 32,640 | |

| | 101 | | | Denbury Resources, Inc. | | | 890 | |

| | 96 | | | Devon Energy Corp. | | | 6,548 | |

| | 26 | | | Energen Corp. | | | 1,850 | |

| | 750 | | | Energy Transfer Equity LP | | | 49,995 | |

| | 2,900 | | | Enterprise Products Partners LP | | | 99,325 | |

| | 130 | | | EOG Resources, Inc. | | | 12,864 | |

| | 40 | | | EQT Corp. | | | 3,598 | |

| | 1,028 | | | Exxon Mobil Corp. | | | 89,816 | |

| | 950 | | | Genesis Energy LP | | | 47,224 | |

| | 20 | | | Gulfport Energy Corp.* | | | 979 | |

| | 64 | | | Hess Corp. | | | 4,922 | |

| | 54 | | | HollyFrontier Corp. | | | 2,094 | |

| | 410 | | | Kinder Morgan, Inc. | | | 17,610 | |

| | 800 | | | Magellan Midstream Partners LP | | | 66,800 | |

| | 161 | | | Marathon Oil Corp. | | | 5,007 | |

| | 63 | | | Marathon Petroleum Corp. | | | 6,210 | |

| | 325 | | | MarkWest Energy Partners LP | | | 21,925 | |

| | 350 | | | MPLX LP | | | 27,212 | |

| | 39 | | | Murphy Oil Corp. | | | 1,857 | |

| | 35 | | | Newfield Exploration Co.* | | | 1,373 | |

| | 91 | | | Noble Energy, Inc. | | | 4,616 | |

| | 184 | | | Occidental Petroleum Corp. | | | 14,738 | |

| | 750 | | | ONEOK Partners LP | | | 31,462 | |

| | 453 | | | ONEOK, Inc. | | | 21,789 | |

| | 13 | | | PDC Energy, Inc.* | | | 738 | |

| | 129 | | | Phillips 66 | | | 10,231 | |

| | 36 | | | Pioneer Natural Resources Co. | | | 6,220 | |

| | 1,491 | | | Plains All American Pipeline LP | | | 74,714 | |

| | 1,000 | | | Plains GP Holdings LP Class A | | | 29,400 | |

| | 60 | | | QEP Resources, Inc. | | | 1,350 | |

| | 41 | | | Range Resources Corp. | | | 2,606 | |

| | 30 | | | Rosetta Resources, Inc.* | | | 685 | |

| | 200 | | | SemGroup Corp. Class A | | | 16,838 | |

| | 22 | | | SM Energy Co. | | | 1,275 | |

| | 90 | | | Southwestern Energy Co.* | | | 2,523 | |

| | 852 | | | Spectra Energy Corp. | | | 31,737 | |

| | 1,300 | | | Sunoco Logistics Partners LP | | | 57,668 | |

| | 209 | | | Targa Resources Corp. | | | 21,939 | |

| | 600 | | | Targa Resources Partners LP | | | 27,264 | |

| | 500 | | | Teekay Offshore Partners LP | | | 11,730 | |

| | 28 | | | Tesoro Corp. | | | 2,403 | |

| | 550 | | | Tesoro Logistics LP | | | 30,816 | |

| | 1,460 | | | The Williams Cos., Inc. | | | 74,737 | |

| | 124 | | | Valero Energy Corp. | | | 7,056 | |

| | 17 | | | Western Refining, Inc. | | | 749 | |

| | 743 | | | Williams Partners LP | | | 36,704 | |

| | 24 | | | World Fuel Services Corp. | | | 1,332 | |

| | 66 | | | WPX Energy, Inc.* | | | 908 | |

| | | | | | | | |

| | | | | | | 1,206,417 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Schedule of Investments (continued)

April 30, 2015 (Unaudited)

| | | | | | | | |

Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Paper & Forest Products – 0.2% | |

| | 30 | | | Boise Cascade Co.* | | $ | 1,041 | |

| | 18 | | | Clearwater Paper Corp.* | | | 1,151 | |

| | 48 | | | Domtar Corp. | | | 2,075 | |

| | 274 | | | International Paper Co. | | | 14,719 | |

| | 58 | | | KapStone Paper and Packaging Corp. | | | 1,621 | |

| | 96 | | | Louisiana-Pacific Corp.* | | | 1,463 | |

| | 10 | | | Neenah Paper, Inc. | | | 605 | |

| | 41 | | | PH Glatfelter Co. | | | 1,017 | |

| | 24 | | | Schweitzer-Mauduit International, Inc. | | | 1,061 | |

| | | | | | | | |

| | | | | | | 24,753 | |

| | |

| | Personal Products – 0.1% | |

| | 122 | | | Avon Products, Inc. | | | 997 | |

| | 57 | | | The Estee Lauder Cos., Inc. Class A | | | 4,633 | |

| | | | | | | | |

| | | | | | | 5,630 | |

| | |

| | Pharmaceuticals – 2.0% | |

| | 310 | | | AbbVie, Inc. | | | 20,045 | |

| | 76 | | | Actavis PLC* | | | 21,497 | |

| | 16 | | | Akorn, Inc.* | | | 666 | |

| | 323 | | | Bristol-Myers Squibb Co. | | | 20,585 | |

| | 193 | | | Eli Lilly & Co. | | | 13,871 | |

| | 37 | | | Endo International PLC* | | | 3,110 | |

| | 34 | | | Hospira, Inc.* | | | 2,968 | |

| | 16 | | | Impax Laboratories, Inc.* | | | 724 | |

| | 532 | | | Johnson & Johnson | | | 52,774 | |

| | 7 | | | Lannett Co., Inc.* | | | 403 | |

| | 24 | | | Mallinckrodt PLC* | | | 2,716 | |

| | 547 | | | Merck & Co., Inc. | | | 32,579 | |

| | 78 | | | Mylan NV* | | | 5,636 | |

| | 27 | | | Perrigo Co. PLC | | | 4,949 | |

| | 1,179 | | | Pfizer, Inc. | | | 40,004 | |

| | 11 | | | Prestige Brands Holdings, Inc.* | | | 432 | |

| | 17 | | | The Medicines Co.* | | | 435 | |

| | 94 | | | Zoetis, Inc. | | | 4,176 | |

| | | | | | | | |

| | | | | | | 227,570 | |

| | |

| | Real Estate Investment Trusts – 7.3% | |

| | 683 | | | Acadia Realty Trust | | | 21,105 | |

| | 161 | | | Alexandria Real Estate Equities, Inc. | | | 14,873 | |

| | 171 | | | American Tower Corp. | | | 16,165 | |

| | 295 | | | AvalonBay Communities, Inc. | | | 48,480 | |

| | 321 | | | Blackstone Mortgage Trust, Inc. Class A | | | 9,864 | |

| | 368 | | | Boston Properties, Inc. | | | 48,690 | |

| | 1,191 | | | Brixmor Property Group, Inc. | | | 27,929 | |

| | 358 | | | CBL & Associates Properties, Inc. | | | 6,448 | |

| | 960 | | | Chesapeake Lodging Trust | | | 30,480 | |

| | 473 | | | CyrusOne, Inc. | | | 15,363 | |

| | 1,463 | | | DDR Corp. | | | 24,944 | |

| | 1,391 | | | Empire State Realty Trust, Inc. Class A | | | 25,038 | |

| | 238 | | | Equity Residential | | | 17,579 | |

| | 50 | | | Essex Property Trust, Inc. | | | 11,098 | |

| | 214 | | | HCP, Inc. | | | 8,622 | |

| | 160 | | | Health Care REIT, Inc. | | | 11,523 | |

| | 480 | | | Highwoods Properties, Inc. | | | 20,659 | |

| | 570 | | | Liberty Property Trust | | | 19,859 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Real Estate Investment Trusts – (continued) | |

| | 119 | | | Mack-Cali Realty Corp. | | $ | 2,136 | |

| | 425 | | | Mid-America Apartment Communities, Inc. | | | 31,709 | |

| | 260 | | | National Health Investors, Inc. | | | 17,347 | |

| | 1,241 | | | Parkway Properties, Inc. | | | 20,191 | |

| | 326 | | | Pebblebrook Hotel Trust | | | 13,998 | |

| | 551 | | | Physicians Realty Trust | | | 9,147 | |

| | 493 | | | Post Properties, Inc. | | | 28,185 | |

| | 885 | | | ProLogis, Inc. | | | 35,577 | |

| | 231 | | | PS Business Parks, Inc. | | | 17,637 | |

| | 257 | | | Public Storage | | | 48,293 | |

| | 791 | | | RLJ Lodging Trust | | | 23,469 | |

| | 542 | | | Simon Property Group, Inc. | | | 98,368 | |

| | 39 | | | SL Green Realty Corp. | | | 4,772 | |

| | 182 | | | Sovran Self Storage, Inc. | | | 15,896 | |

| | 78 | | | The Macerich Co. | | | 6,377 | |

| | 621 | | | Ventas, Inc. | | | 42,787 | |

| | 158 | | | Vornado Realty Trust | | | 16,351 | |

| | | | | | | | |

| | | | | | | 810,959 | |

| | |

| | Real Estate Management & Development – 0.1% | |

| | 212 | | | RE/MAX Holdings, Inc. Class A | | | 7,163 | |

| | |

| | Tobacco – 0.6% | |

| | 500 | | | Altria Group, Inc. | | | 25,025 | |

| | 91 | | | Lorillard, Inc. | | | 6,357 | |

| | 388 | | | Philip Morris International, Inc. | | | 32,386 | |

| | 89 | | | Reynolds American, Inc. | | | 6,524 | |

| | 15 | | | Universal Corp. | | | 706 | |

| | | | | | | | |

| | | | | | | 70,998 | |

| | |

| | TOTAL COMMON STOCKS | |

| | (Cost $3,212,631) | | $ | 3,652,202 | |

| | |

| | | | | | | | |

| | Exchange Traded Fund – 4.7% | |

| | 12,057 | | | iShares Global Infrastructure ETF | | | | |

| | (Cost $445,790) | | $ | 527,011 | |

| | |

| | | | | | | | |

| Shares | | | Rate | | Value | |

| | Investment Companies(a) – 55.3% | |

| Goldman Sachs Commodity Strategy Fund —

Institutional Shares |

|

| | 305,062 | | | 0.000% | | $ | 1,214,146 | |

| Goldman Sachs Inflation Protected Securities Fund —

Institutional Shares |

|

| | 158,508 | | | 0.000 | | | 1,672,259 | |

| Goldman Sachs Local Emerging Markets Debt Fund —

Institutional Shares |

|

| | 71,878 | | | 0.001 | | | 513,211 | |

| Goldman Sachs Strategic Income Fund — Institutional

Shares |

|

| | 276,466 | | | 0.001 | | | 2,778,485 | |

| | |

| | TOTAL INVESTMENT COMPANIES | |

| | (Cost $6,763,882) | | $ | 6,178,101 | |

| | |

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

| | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | Maturity

Date | | | Value | |

| | Short-term Investment(b) – 6.3% | | | | | |

| | Repurchase Agreement – 6.3% | | | | | |

| Joint Repurchase Agreement Account II | | | | | |

| $ | 700,000 | | | 0.127% | | | 05/01/15 | | | $ | 700,000 | |

| | (Cost $700,000) | | | | | | | | |

| | |

| | TOTAL INVESTMENTS – 99.0% | | | | | |

| | (Cost $11,122,303) | | | | | | $ | 11,057,314 | |

| | |

| OTHER ASSETS IN EXCESS OF

LIABILITIES – 1.0% |

| | | 115,036 | |

| | |

| | NET ASSETS – 100.0% | | | $ | 11,172,350 | |

| | |

| | |

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

* | | Non-income producing security. |

(a) | | Represents an Affiliated Fund. |

(b) | | Joint repurchase agreement was entered into on April 30, 2015. Additional information appears on Page 16. |

| | |

|

Investment Abbreviations: |

ETF | | —Exchange Traded Fund |

GP | | —General Partnership |

LLC | | —Limited Liability Company |

LP | | —Limited Partnership |

REIT | | —Real Estate Investment Trust |

|

|

| ADDITIONAL INVESTMENT INFORMATION |

FUTURES CONTRACTS — At April 30, 2015, the Fund had the following futures contracts:

| | | | | | | | | | | | | | |

| Type | | Number of

Contracts

Long (Short) | | | Expiration Date | | Current Value | | | Unrealized Gain (Loss) | |

Eurodollar | | | (12 | ) | | December 2017 | | $ | (2,941,350 | ) | | $ | (29,562 | ) |

Euro Stoxx 50 Index | | | 9 | | | June 2015 | | | 360,570 | | | | (2,877 | ) |

S&P 500 E-Mini Index | | | 2 | | | June 2015 | | | 207,890 | | | | 4,687 | |

Topix Index | | | 1 | | | June 2015 | | | 133,040 | | | | 5,650 | |

| TOTAL | | | | | | | | | | | | $ | (22,102 | ) |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Schedule of Investments (continued)

April 30, 2015 (Unaudited)

|

| ADDITIONAL INVESTMENT INFORMATION (continued) |

JOINT REPURCHASE AGREEMENT ACCOUNT II — At April 30, 2015, the Fund had undivided interests in the Joint Repurchase Agreement Account II, with a maturity date of May 1, 2015, as follows:

| | | | |

| Principal Amount | | Maturity Value | | Collateral Allocation Value |

$700,000 | | $700,002 | | $714,001 |

REPURCHASE AGREEMENTS — At April 30, 2015, the Principal Amount of the Fund’s interest in the Joint Repurchase Agreement Account II was as follows:

| | | | | | |

| Counterparty | | Interest

Rate | | | Principal

Amounts |

Citigroup Global Markets, Inc. | | | 0.130 | % | | $225,370 |

Merrill Lynch & Co., Inc. | | | 0.130 | | | 262,782 |

BNP Paribas Securities Co. | | | 0.120 | | | 211,848 |

| TOTAL | | | | | | $700,000 |

At April 30, 2015, the Joint Repurchase Agreement Account II was fully collateralized by:

| | | | | | | | |

| Issuer | | Interest Rates | | | Maturity Dates | |

Federal Home Loan Bank Discount Notes | | | 0.000 | % | | | 07/29/15 | |

Federal Home Loan Mortgage Corp. | | | 3.000 to 6.000 | | | | 07/01/34 to 03/01/45 | |

Federal National Mortgage Association | | | 3.000 to 7.000 | | | | 10/01/15 to 04/01/45 | |

Government National Mortgage Association | | | 2.500 to 7.500 | | | | 05/20/42 to 10/20/44 | |

United States Treasury Inflation Protected Securities | | | 2.000 | | | | 01/15/21 | |

U.S. Treasury Notes | | | 2.250 to 2.630 | | | | 03/31/21 to 11/15/20 | |

| | |

| 16 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Statement of Assets and Liabilities

April 30, 2015 (Unaudited)

| | | | | | |

| | | | | | |

| | Assets: | | | | |

| | Investments of unaffiliated issuers, at value (cost $4,358,421) | | $ | 4,879,213 | |

| | Investments of affiliated issuers, at value (cost $6,763,882) | | | 6,178,101 | |

| | Cash | | | 126,937 | |

| | Variation margin on certain derivative contracts | | | 44,294 | |

| | Receivables: | | | | |

| | Reimbursement from investment adviser | | | 32,569 | |

| | Dividends and interest | | | 17,748 | |

| | Other assets | | | 80 | |

| | Total assets | | | 11,278,942 | |

| | | | | | |

| | Liabilities: | | | | |

| | Payables: | | | | |

| | Investments purchased | | | 10,041 | |

| | Management fees | | | 4,093 | |

| | Distribution and service fees and transfer agent fees | | | 414 | |

| | Accrued expenses | | | 92,044 | |

| | Total liabilities | | | 106,592 | |

| | | | | | |

| | Net Assets: | | | | |

| | Paid-in capital | | | 11,093,227 | |

| | Undistributed net investment income | | | 87,046 | |

| | Accumulated net realized gain | | | 79,168 | |

| | Net unrealized loss | | | (87,091 | ) |

| | | NET ASSETS | | $ | 11,172,350 | |

| | | Net Assets: | | | | |

| | | Class A | | $ | 55,839 | |

| | | Class C | | | 10,402 | |

| | | Institutional | | | 11,048,375 | |

| | | Class IR | | | 31,516 | |

| | | Class R | | | 26,218 | |

| | | Total Net Assets | | $ | 11,172,350 | |

| | | Shares Outstanding $0.001 par value (unlimited number of shares authorized): | | | | |

| | | Class A | | | 5,523 | |

| | | Class C | | | 1,031 | |

| | | Institutional | | | 1,092,437 | |

| | | Class IR | | | 3,117 | |

| | | Class R | | | 2,595 | |

| | | Net asset value, offering and redemption price per share:(a) | | | | |

| | | Class A | | | $10.11 | |

| | | Class C | | | 10.09 | |

| | | Institutional | | | 10.11 | |

| | | Class IR | | | 10.11 | |

| | | Class R | | | 10.10 | |

| | (a) | | Maximum public offering price per share for Class A Shares of the fund is $10.70. At redemption, Class C shares may be subject to a contingent deferred sales charge assessed on the amount equal to the lesser of the current net asset value (“NAV”) or the original purchase price of the shares. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Statement of Operations

For the Six Months Ended April 30, 2015 (Unaudited)

| | | | | | |

| | | | | | |

| | Investment income: | | | | |

| | Dividends — unaffiliated issuers | | $ | 111,507 | |

| | Dividends — affiliated issuers | | | 17,473 | |

| | Interest | | | 424 | |

| | Total investment income | | | 129,404 | |

| | | | | | |

| | Expenses: | | | | |

| | Professional fees | | | 47,572 | |

| | Management fees | | | 38,588 | |

| | Custody, accounting and administrative services | | | 36,039 | |

| | Registration fees | | | 25,618 | |

| | Printing and mailing costs | | | 20,084 | |

| | Trustee fees | | | 13,252 | |

| | Transfer Agent fees(a) | | | 2,304 | |

| | Distribution and Service fees(a) | | | 199 | |

| | Other | | | 11,463 | |

| | Total expenses | | | 195,119 | |

| | Less — expense reductions | | | (164,071 | ) |

| | Net expenses | | | 31,048 | |

| | NET INVESTMENT INCOME | | | 98,356 | |

| | | | | | |

| | Realized and unrealized gain (loss): | | | | |

| | Net realized gain (loss) from: | | | | |

| | Investments — unaffiliated issuers | | | 151,493 | |

| | Investments — affiliated issuers | | | (166,033 | ) |

| | Futures contracts | | | 116,757 | |

| | Swap contracts | | | 537 | |

| | Net change in unrealized loss on: | | | | |

| | Investments — unaffiliated issuers | | | (138,016 | ) |

| | Investments — affiliated issuers | | | (296,041 | ) |

| | Futures contracts | | | (18,309 | ) |

| | Net realized and unrealized loss | | | (349,612 | ) |

| | NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (251,256 | ) |

| | (a) | | Class specific Distribution and Service, and Transfer Agent fees were as follows: |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Distribution and Service Fees | | | Transfer Agent Fees | |

Fund | | Class A | | | Class C | | | Class R | | | Class A | | | Class C | | | Institutional | | | Class IR | | | Class R | |

Multi-Asset Real Return | | $ | 83 | | | $ | 51 | | | $ | 65 | | | $ | 63 | | | $ | 9 | | | $ | 2,178 | | | $ | 29 | | | $ | 25 | |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Statement of Changes in Net Assets

| | | | | | | | | | |

| | | | | For the Six Months Ended April 30, 2015

(Unaudited) | | | For the Fiscal

Year Ended

October 31, 2014 | |

| | From operations: | | | | | | | | |

| | Net investment income | | $ | 98,356 | | | $ | 159,934 | |

| | Net realized gain | | | 102,754 | | | | 280,990 | |

| | Net change in unrealized gain (loss) | | | (452,366 | ) | | | 51,923 | |

| | Net increase (decrease) in net assets resulting from operations | | | (251,256 | ) | | | 492,847 | |

| | | | | | | | | | |

| | Distributions to shareholders: | | | | | | | | |

| | From net investment income | | | | | | | | |

| | Class A Shares | | | (319 | ) | | | (254 | ) |

| | Class C Shares | | | (14 | ) | | | (43 | ) |

| | Institutional Shares | | | (77,524 | ) | | | (162,202 | ) |

| | Class IR Shares | | | (199 | ) | | | (353 | ) |

| | Class R Shares | | | (100 | ) | | | (219 | ) |

| | From net realized gains | | | | | | | | |

| | Class A Shares | | | (1,311 | ) | | | (44 | ) |

| | Class C Shares | | | (219 | ) | | | (44 | ) |

| | Institutional Shares | | | (230,605 | ) | | | (44,596 | ) |

| | Class IR Shares | | | (660 | ) | | | (111 | ) |

| | Class R Shares | | | (551 | ) | | | (111 | ) |

| | Total distributions to shareholders | | | (311,502 | ) | | | (207,977 | ) |

| | | | | | | | | | |

| | From share transactions: | | | | | | | | |

| | Proceeds from sales of shares | | | 73,852 | | | | 407,789 | |

| | Reinvestment of distributions | | | 311,502 | | | | 207,977 | |

| | Cost of shares redeemed | | | (35,601 | ) | | | (1,048 | ) |

| | Net increase in net assets resulting from share transactions | | | 349,753 | | | | 614,718 | |

| | TOTAL INCREASE (DECREASE) | | | (213,005 | ) | | | 899,588 | |

| | | | | | | | | | |

| | Net assets: | | | | | | | | |

| | Beginning of period | | | 11,385,355 | | | | 10,485,767 | |

| | End of period | | $ | 11,172,350 | | | $ | 11,385,355 | |

| | Undistributed net investment income | | $ | 87,046 | | | $ | 66,846 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 19 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Financial Highlights

Selected Data for a Share Outstanding Throughout Each Period

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | Income (loss) from

investment operations | | | Distributions

to shareholders | |

| | | Year - Share Class | | Net asset

value,

beginning

of period | | | Net

investment

income(a) | | | Net realized

and unrealized

gain (loss) | | | Total from

investment

operations | | | From net

investment

income | | | From net

realized

gains | | | Total

distributions | |

| | FOR THE SIX MONTHS ENDED APRIL 30, (UNAUDITED) | |

| | 2015 - A | | $ | 10.63 | | | $ | 0.07 | (e) | | $ | (0.32 | ) | | $ | (0.25 | ) | | $ | (0.09 | ) | | $ | (0.18 | ) | | $ | (0.27 | ) |

| | 2015 - C | | | 10.61 | | | | 0.03 | (e) | | | (0.32 | ) | | | (0.29 | ) | | | (0.05 | ) | | | (0.18 | ) | | | (0.23 | ) |

| | 2015 - Institutional | | | 10.64 | | | | 0.09 | (e) | | | (0.33 | ) | | | (0.24 | ) | | | (0.11 | ) | | | (0.18 | ) | | | (0.29 | ) |

| | 2015 - IR | | | 10.63 | | | | 0.08 | (e) | | | (0.32 | ) | | | (0.24 | ) | | | (0.10 | ) | | | (0.18 | ) | | | (0.28 | ) |

| | 2015 - R | | | 10.62 | | | | 0.06 | (e) | | | (0.32 | ) | | | (0.26 | ) | | | (0.08 | ) | | | (0.18 | ) | | | (0.26 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | FOR THE FISCAL ENDED OCTOBER 31, | |

| | 2014 - A | | | 10.35 | | | | 0.11 | | | | 0.33 | | | | 0.44 | | | | (0.12 | ) | | | (0.04 | ) | | | (0.16 | ) |

| | 2014 - C | | | 10.34 | | �� | | 0.03 | | | | 0.33 | | | | 0.36 | | | | (0.05 | ) | | | (0.04 | ) | | | (0.09 | ) |

| | 2014 - Institutional | | | 10.35 | | | | 0.15 | | | | 0.34 | | | | 0.49 | | | | (0.16 | ) | | | (0.04 | ) | | | (0.20 | ) |

| | 2014 - IR | | | 10.35 | | | | 0.14 | | | | 0.32 | | | | 0.46 | | | | (0.14 | ) | | | (0.04 | ) | | | (0.18 | ) |

| | 2014 - R | | | 10.34 | | | | 0.08 | | | | 0.33 | | | | 0.41 | | | | (0.09 | ) | | | (0.04 | ) | | | (0.13 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | FOR THE PERIOD ENDED OCTOBER 31, | |

| | 2013 - A (Commenced August 30, 2013) | | | 10.00 | | | | 0.01 | | | | 0.34 | | | | 0.35 | | | | — | | | | — | | | | — | |

| | 2013 - C (Commenced August 30, 2013) | | | 10.00 | | | | — | (g) | | | 0.34 | | | | 0.34 | | | | — | | | | — | | | | — | |

| | 2013 - Institutional (Commenced August 30, 2013) | | | 10.00 | | | | 0.02 | | | | 0.33 | | | | 0.35 | | | | — | | | | — | | | | — | |

| | 2013 - IR (Commenced August 30, 2013) | | | 10.00 | | | | 0.02 | | | | 0.33 | | | | 0.35 | | | | — | | | | — | | | | — | |

| | 2013 - R (Commenced August 30, 2013) | | | 10.00 | | | | 0.01 | | | | 0.33 | | | | 0.34 | | | | — | | | | — | | | | — | |

| | (a) | | Calculated based on the average shares outstanding methodology. |

| | (b) | | Assumes investment at the net asset value at the beginning of the period, reinvestment of all dividends and distributions, a complete redemption of the investment at the net asset value at the end of the period and no sales or redemption charges. Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total returns for periods less than one full year are not annualized. |

| | (c) | | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (d) | | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | (e) | | Reflects income recognized from special dividends which amounted to $0.02 per share and 0.38% of average net assets. |

| | (g) | | Amount is less than $0.005 per share. |

| | |

| 20 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Net asset

value, end

of period | | | | | Total

return(b) | | | | | Net assets,

end of

period (in 000s) | | | | | Ratio of

net expenses

to average

net assets(c) | | | | | Ratio of

total expenses

to average

net assets(c) | | | | | Ratio of

net investment

income

to average net assets | | | | | Portfolio

turnover

rate(d) | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ | 10.11 | | | | | | (2.39 | )% | | | | $ | 56 | | | | | | 0.96 | %(f) | | | | | 3.92 | %(f) | | | | | 1.33 | %(e)(f) | | | | | 11 | % |

| | | 10.09 | | | | | | (2.75 | ) | | | | | 10 | | | | | | 1.69 | (f) | | | | | 4.67 | (f) | | | | | 0.66 | (e)(f) | | | | | 11 | |

| | | 10.11 | | | | | | (2.28 | ) | | | | | 11,048 | | | | | | 0.56 | (f) | | | | | 3.54 | (f) | | | | | 1.79 | (e)(f) | | | | | 11 | |

| | | 10.11 | | | | | | (2.26 | ) | | | | | 32 | | | | | | 0.71 | (f) | | | | | 3.69 | (f) | | | | | 1.64 | (e)(f) | | | | | 11 | |

| | | 10.10 | | | | | | (2.51 | ) | | | | | 26 | | | | | | 1.21 | (f) | | | | | 4.18 | (f) | | | | | 1.14 | (e)(f) | | | | | 11 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 10.63 | | | | | | 4.28 | | | | | | 49 | | | | | | 0.99 | | | | | | 4.75 | | | | | | 1.00 | | | | | | 34 | |

| | | 10.61 | | | | | | 3.47 | | | | | | 11 | | | | | | 1.76 | | | | | | 5.86 | | | | | | 0.28 | | | | | | 34 | |

| | | 10.64 | | | | | | 4.77 | | | | | | 11,272 | | | | | | 0.59 | | | | | | 4.69 | | | | | | 1.45 | | | | | | 34 | |

| | | 10.63 | | | | | | 4.51 | | | | | | 27 | | | | | | 0.73 | | | | | | 4.83 | | | | | | 1.31 | | | | | | 34 | |

| | | 10.62 | | | | | | 4.00 | | | | | | 27 | | | | | | 1.24 | | | | | | 5.34 | | | | | | 0.80 | | | | | | 34 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 10.35 | | | | | | 3.50 | | | | | | 10 | | | | | | 0.97 | (f) | | | | | 5.91 | (f) | | | | | 0.80 | (f) | | | | | 4 | |

| | | 10.34 | | | | | | 3.40 | | | | | | 10 | | | | | | 1.72 | (f) | | | | | 6.66 | (f) | | | | | 0.06 | (f) | | | | | 4 | |

| | | 10.35 | | | | | | 3.50 | | | | | | 10,413 | | | | | | 0.61 | (f) | | | | | 5.54 | (f) | | | | | 1.16 | (f) | | | | | 4 | |

| | | 10.35 | | | | | | 3.50 | | | | | | 26 | | | | | | 0.79 | (f) | | | | | 5.71 | (f) | | | | | 0.98 | (f) | | | | | 4 | |

| | | 10.34 | | | | | | 3.40 | | | | | | 26 | | | | | | 1.25 | (f) | | | | | 6.18 | (f) | | | | | 0.52 | (f) | | | | | 4 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 21 |

GOLDMAN SACHS MULTI-ASSET REAL RETURN FUND

Notes to Financial Statements

April 30, 2015 (Unaudited)

Goldman Sachs Trust (the “Trust”) is a Delaware statutory trust registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company. The Trust includes the Goldman Sachs Multi-Asset Real Return Fund (the “Fund”). The Fund is a diversified fund and currently offers five classes of shares: Class A, Class C, Class IR, Class R and Institutional Shares.

Class A Shares are sold with a front-end sales charge of up to 5.50%. Class C Shares are sold with a contingent deferred sales charge (“CDSC”) of 1.00%, which is imposed on redemptions made within 12 months of purchase. Institutional, Class IR and Class R Shares are not subject to a sales charge.

Goldman Sachs Asset Management, L.P. (“GSAM”), an affiliate of Goldman, Sachs & Co. (“Goldman Sachs”), serves as investment adviser to the Fund pursuant to a management agreement (the “Agreement”) with the Trust.

|

| 2. SIGNIFICANT ACCOUNTING POLICIES |

The financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and require management to make estimates and assumptions that may affect the reported amounts and disclosures. Actual results may differ from those estimates and assumptions.

A. Investment Valuation — The Fund’s valuation policy is to value investments at fair value.

B. Investment Income and Investments — Investment income includes interest income and dividend income, net of any foreign withholding taxes, less any amounts reclaimable. Interest income is accrued daily and adjusted for amortization of premiums and accretion of discounts. Dividend income is recognized on ex-dividend date or, for certain foreign securities, as soon as such information is obtained subsequent to the ex-dividend date. Investment transactions are reflected on trade date. Realized gains and losses are calculated using identified cost. Investment transactions are recorded on the following business day for daily net asset value (“NAV”) calculations. Any foreign capital gains tax is accrued daily based upon net unrealized gains, and is payable upon sale of such investments. Distributions received from the Fund’s investments in United States (“U.S.”) real estate investment trusts (“REITs”) may be characterized as ordinary income, net capital gain or a return of capital. A return of capital is recorded by the Fund as a reduction to the cost basis of the REIT.

Distributions from Master Limited Partnerships (“MLPs”) are generally recorded based on the characterization reported on the MLP’s tax return.

For derivative contracts, realized gains and losses are recorded upon settlement of the contract. Upfront payments are made or received upon entering into a swap agreement and are reflected in the Statement of Assets and Liabilities. Upfront payments are recognized over the contract’s term/event as realized gains or losses, with the exception of forward starting interest rate swaps whose realized gains or losses are recognized from the effective start date. For securities with paydown provisions, principal payments received are treated as a proportionate reduction to the cost basis of the securities, and excess or shortfall amounts are recorded as income. For treasury inflation protected securities (“TIPS”), adjustments to principal due to inflation/deflation are reflected as increases/decreases to interest income with a corresponding adjustment to cost.

C. Class Allocations and Expenses — Investment income, realized and unrealized gain (loss), and non-class specific expenses of the Fund are allocated daily based upon the proportion of net assets of each class. Class specific expenses, where applicable, are borne by the respective share classes and include Distribution and Service, Transfer Agent and Service and Shareholder Administration fees. Non-class specific expenses directly incurred by the Fund are charged to the Fund, while such expenses incurred by the Trust are allocated across the Fund on a straight-line and/or pro-rata basis depending upon the nature of the expenses.