UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman Sachs & Co. LLC | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code:(312) 655-4400

Date of fiscal year end: August 31

Date of reporting period: February 28, 2019

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | February 28, 2019 |

| | |

| | | | Financial Square FundsSM |

| | | | Federal Instruments |

| | | | Government |

| | | | Money Market |

| | | | Prime Obligations |

| | | | Treasury Instruments |

| | | | Treasury Obligations |

| | | | Treasury Solutions |

It is our intention that beginning on January 1, 2021, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from a Fund or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and certain communications from a Fund electronically by calling the applicable toll-free number below or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. If you hold shares of a Fund directly with the Fund’s transfer agent, you can inform the transfer agent that you wish to receive paper copies of reports by calling toll-free800-621-2550 for Institutional/Class I, Administration, Capital, Cash Management, Preferred, Premier, Resource, Service, Class R6 and Select shareholders or800-526-7384 for Class A and Class C shareholders. If you hold shares of a Fund through a financial intermediary, please contact your financial intermediary to make this election. Your election to receive reports in paper will apply to all Goldman Sachs Funds held in your account if you invest through your financial intermediary or all Goldman Sachs Funds held with the Funds’ transfer agent if you invest directly with the transfer agent.

Goldman Sachs Financial Square Funds

| ∎ | | FEDERAL INSTRUMENTS FUND |

| ∎ | | TREASURY INSTRUMENTS FUND |

| ∎ | | TREASURY OBLIGATIONS FUND |

| ∎ | | TREASURY SOLUTIONS FUND |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

PORTFOLIO RESULTS

Goldman Sachs Financial Square Funds

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Money Market Portfolio Management Team discusses the Goldman Sachs Financial Square Funds’ (the “Funds”) performance and positioning for the six-month period ended February 28, 2019 (the “Reporting Period”).

| Q | | What economic and market factors most influenced the money markets as a whole during the Reporting Period? |

| A | | During the Reporting Period, money market yields remained low but continued to move higher as the Federal Reserve (“Fed”) tightened monetary policy. Fed officials raised the targeted federal funds rate twice — in September and December 2018 — such that at the end of the Reporting Period, it was in a range of between 2.25% and 2.50%. Other influences on the money markets during the Reporting Period were the continuation of the Fed’s balance sheet normalization and the dovish stance of most developed markets central banks. (Balance sheet normalization refers to the steps the Fed is taking to reverse quantitative easing and remove the substantial monetary accommodation it has provided to the economy since the financial crisis began in 2007. Dovish tends to imply lower interest rates; opposite of hawkish.) |

| | | When the Reporting Period started in September 2018, U.S. economic growth was robust, though some major economies, including those of the Eurozone, the U.K. and China, exhibited a gradual weakening trend. The Fed raised the targeted federal funds rate by 25 basis points, citing ongoing strength in the labor market and a pickup in household spending and business fixed investment. (A basis point is 1/100th of a percentage point.) The Fed’s dot plot pointed to another increase by the end of 2018 and three more during 2019. (The “dot plot” shows rate projections of the members of the Fed’s Open Market Committee.) Fed Chair Jerome Powell delivered an upbeat assessment of the U.S. economy, which supported market expectations for these additional Fed rate hikes in 2019. During the fourth quarter of 2018, investor concerns about slowing global economic growth momentum as well as tighter financial conditions weighed on financial markets. Global interest rates, which had risen for most of the calendar year, fell, as investors grew fearful about the possible end of the global economic cycle and as their expectations for Fed rate hikes diminished. In December 2018, Fed policymakers raised short-term interest rates by an additional 25 basis points, much as the market had expected, but lowered their projection for 2019 monetary policy tightening from three rate hikes to two. In January 2019, the Fed left monetary policy unchanged and also eliminated language about “further gradual increases in rates,” cementing investor expectations for a near-term pause in rate hikes. Fed Chair Powell emphasized that the U.S. central bank would be largely guided by inflation indicators as well as by the global economic growth backdrop and the potential for financial market volatility. During February 2019, the release of minutes from the Fed’s January meeting confirmed policymakers’ dovish tilt. |

| Q | | What key factors were responsible for the performance of the Funds during the Reporting Period? |

| A | | The Funds’ yields rose during the Reporting Period, driven by the increase in money market yields, which occurred primarily because of the economic and market factors discussed above. The money market yield curve flattened, meaning yields on shorter-term maturities rose more than those on longer-term maturities. (Yield curve is a spectrum of interest rates based on maturities of varying lengths.) |

| Q | | How did you manage the Funds during the Reporting Period? |

| A | | Collectively, the Funds had investments in commercial paper, asset-backed commercial paper, U.S. Treasury securities, government agency securities, time deposits, certificates of deposit, floating rate securities, repurchase agreements (“repo”), government guaranteed paper, municipal securities and variable rate demand notes during the Reporting Period. |

| | | In our commercial paper strategies (i.e., the Goldman Sachs Financial Square Money Market Fund and the Goldman Sachs Financial Square Prime Obligations Fund), we maintained somewhat short weighted average maturities of between 34 and 40 days during the first four months of the Reporting Period in response to rather consistent clarity from the Fed around potential interest rate hikes in September and December 2018. For the same reason, during the first half of the Reporting Period, we maintained relatively short |

1

PORTFOLIO RESULTS

| | weighted average maturities of between 16 and 37 days in our government repo strategies (i.e., the Goldman Sachs Financial Square Government Fund, the Goldman Sachs Financial Square Treasury Obligations Fund and the Goldman Sachs Financial Square Treasury Solutions Fund) and between 27 days and 50 days in our government non-repo strategies (i.e., the Goldman Sachs Financial Square Federal Instruments Fund and the Goldman Sachs Financial Square Treasury Instruments Fund). The Funds’ purchases were focused on floating rate securities, asset-backed commercial paper and government agency securities, all of which helped us to manage duration. (Duration is a measure of the Funds’ sensitivity to changes in interest rates). |

| | | After the December 2018 rate hike, the Fed’s path became less clear to us. As a result, we lengthened the weighted average maturities of the commercial paper, government repo and government non-repo strategies. Within our commercial paper strategies, we extended weighted average maturities to between 49 and 52 days during the last two months of the Reporting Period. In our government and government non-repo strategies, we extended weighted average maturities to between 42 and 50 days during December 2018. Then, in January 2019, we shortened the weighted average maturities of our government repo strategies to between 32 and 40 days and the weighted average maturities of our government non-repo strategies to between 39 and 49 days. We continued to shorten the weighted average maturities of the government repo and government non-repo strategies during February, ending the Reporting Period with weighted average maturities of between 21 and 39 days and between 37 and 47 days, respectively. Purchases were focused overall on fixed-rate securities as we sought to manage the Funds’ duration. |

| | | The weighted average maturity of a money market fund is a measure of its price sensitivity to changes in interest rates. Also known as effective maturity, weighted average maturity measures the weighted average of the maturity date of bonds held by the Funds, taking into consideration any available maturity shortening features. |

| Q | | How did you manage the Funds’ weighted average life during the Reporting Period? |

| A | | During the Reporting Period, we managed the weighted average life of the Funds below 120 days. In our commercial paper strategies, we managed the Funds’ weighted average life in a range between approximately 75 days and approximately 101 days. In our government repo and government non-repo strategies, we managed the Funds’ weighted average life in a range between approximately 84 days and approximately 118 days. The weighted average life of a money market fund is a measure of a money market fund’s price sensitivity to changes in liquidity and/or credit risk. |

| | | Under amendments to SEC Rule 2a-7 that became effective in May 2010, the maximum allowable weighted average life of a money market fund is 120 days. While one of the goals of the SEC’s money market fund rule is to reinforce conservative investment practices across the money market fund industry, our security selection process has long emphasized conservative investment choices. |

| Q | | Did you make any changes to the Funds’ portfolios during the Reporting Period? |

| A | | During the Reporting Period, we made adjustments to the Funds’ weighted average maturities and their allocations to specific investments based on then-current market conditions, our near-term view and anticipated and actual Fed monetary policy statements. |

| Q | | What is the Funds’ tactical view and strategy for the months ahead? |

| A | | At the end of the Reporting Period, we expected the elongated U.S. economic expansion to continue and considered market concerns around a near-term recession premature. However, we believed global economic growth was likely to moderate in 2019. More than 60% of the 32 economies for which we track manufacturing data closed 2018 with a lower reading than where they commenced the year. This contrasts with 2017 when almost 80% of these economies ended the year with higher readings. However, manufacturing activity remained in expansionary territory for 70% of these countries, in our view. |

| | | Regarding inflation, the moderation in crude oil prices in October 2018 is likely, we believe, to feed through to lower headline inflation in key economies in the short term. Meanwhile, we think cyclical improvements — namely, a decline in unemployment rates and improving wage growth — could result in firmer core inflation in key developed economies. Potential downside inflation risks include slower than consensus anticipated economic growth and, therefore, stalling or declining labor market improvements, while potential upside risks include continued labor market improvements that lead to inflation or an increase in tariffs. |

| | | As for monetary policy, at the end of the Reporting Period, we had scaled back our expectations for 2019 Fed action |

2

PORTFOLIO RESULTS

| | from three interest rate hikes to one. We also anticipated a near-term pause in the Fed’s rate increases. Regarding other central banks, we expected the European Central Bank to start lifting its policy rates out of negative territory toward the end of 2019, though we thought low interest rates would continue for a prolonged period due to the subdued inflation outlook for the region. We also saw scope for monetary policy normalization in several other developed markets countries, including the U.K. once uncertainty about the country’s exit from the European Union subsides. |

| | | Overall, the Funds continue to be flexibly guided by shifting market conditions, and we have positioned them to seek to take advantage of anticipated interest rate movements. As always, we intend to continue to use our actively managed approach to seek the best possible return within the framework of our Funds’ investment guidelines and objectives. In addition, we will continue to manage interest, liquidity and credit risk daily. We will also continue to closely monitor economic data, Fed policy and any shifts in the money market yield curve, as we strive to navigate the interest rate environment. |

3

PORTFOLIO RESULTS

GOVERNMENT MONEY MARKET FUNDS

| | ∎ | | Federal Instruments Fund |

| | ∎ | | Treasury Instruments Fund |

| | ∎ | | Treasury Obligations Fund |

| | ∎ | | Treasury Solutions Fund |

You could lose money by investing in the Fund. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

INSTITUTIONAL MONEY MARKET FUNDS

You could lose money by investing in the Fund. Because the share price of the Fund will fluctuate, when you sell your shares they may be worth more or less than what you originally paid for them. The Fund may impose a fee upon sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

4

FUND BASICS

Financial Square Funds

as of February 28, 2019

| | | | | | | | | | |

| | PERFORMANCE REVIEW1,2 | |

| | | |

| | | September 1, 2018–

February 28, 2019 | | Fund Total Return (based on NAV)4 Institutional Shares | | | iMoneyNet Institutional

Average5 | |

| | | |

| | Federal Instruments3 | | | 1.05 | % | | | 1.95 | %6 |

| | Government | | | 1.07 | | | | 1.95 | 6 |

| | Money Market3 | | | 1.23 | | | | 2.19 | 7 |

| | Prime Obligations3 | | | 1.23 | | | | 2.19 | 7 |

| | Treasury Instruments | | | 1.04 | | | | 1.92 | 8 |

| | Treasury Obligations | | | 1.06 | | | | 1.95 | 9 |

| | | Treasury Solutions | | | 1.05 | | | | 1.95 | 9 |

The returns represent past performance. Past performance does not guarantee future results. The Funds’ investment returns will fluctuate. Current performance may be lower or higher than the performance quoted above. Please visit our Web site at www.GSAMFUNDS.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| | 1 | | Each of the Prime Obligations, Treasury Obligations, Money Market, Treasury Instruments and Treasury Solutions Funds offers nine separate classes of shares (Institutional, Select, Preferred, Capital, Administration, Service, Cash Management, Premier and Resource), the Federal Instruments Fund offers eight separate classes of shares (Institutional, Select, Preferred, Capital, Administration, Service, Cash Management and Premier), and the Government Fund offers twelve separate classes of shares (Institutional, Select, Preferred, Capital, Administration, Service, Cash Management, Premier, Resource, Class R6, Class A and Class C), each of which is subject to different fees and expenses that affect performance and entitles shareholders to different services. The Institutional and Class R6 Shares do not have distribution and/or service(12b-1) or administration and/or service(non-12b-1) fees. The Select, Preferred, Capital, Administration, Service, Cash Management, Premier, Resource, Class A and Class C Shares offer financial institutions the opportunity to receive fees for providing certain distribution, administrative support and/or shareholder services (as applicable). As an annualized percentage of average daily net assets, these share classes pay combined distribution and/or service(12b-1), administration and/ or service(non-12b-1) fees (as applicable) at the following contractual rates: the Select Shares pay 0.03%, Preferred Shares pay 0.10%, Capital Shares pay 0.15%, Administration Shares pay 0.25%, Service Shares pay 0.50%, Cash Management Shares pay 0.80%, Premier Shares pay 0.35%, Resource Shares pay 0.65%, Class A Shares pay 0.25% and Class C Shares pay 1.00%. If these fees were reflected in the above performance, performance would have been reduced. In addition, the Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The investment adviser may contractually agree to waive or reimburse certain fees and expenses until a specified date. The investment adviser may also voluntarily waive certain fees and expenses, and such voluntary waivers may be discontinued or modified at any time without notice. The performance shown above reflects any waivers or reimbursements that were in effect for all or a portion of the periods shown. When waivers or reimbursements are in place, the Fund’s operating expenses are reduced and the Fund’s yield and total returns to the shareholder are increased. |

| | 3 | | From the beginning of the reporting period through September 30, 2018, the investment adviser implemented a voluntary temporary fee waiver equal annually to 0.08% of the average daily net assets of the Financial Square Prime Obligations Fund and Financial Square Money Market Fund. On October 1, 2018, the investment adviser reduced the voluntary temporary fee waiver to a percentage rate equal annually to 0.06% of the average daily net assets for both funds. On February 28, 2019, the investment adviser has reduced the voluntary temporary fee waiver to a percentage rate equal annually to 0.05% of the average daily net assets for both funds. In addition, on December 28, 2018, GSAM implemented a management fee waiver equal to 0.02% of the average daily net assets for the Financial Square Federal Instruments Fund. |

| | 4 | | The net asset value (NAV) represents the net assets of the class of the Fund(ex-dividend) divided by the total number of shares of the class outstanding. A Fund’s total return reflects the reinvestment of dividends and other distributions. |

| | 5 | | Source: iMoneyNet, Inc. February 2019. |

| | 6 | | Government & Agencies Institutional–Category includes the most broadly based of the government institutional funds. These funds may generally invest in U.S. treasuries, U.S. agencies, repurchase agreements, or government-backed floating rate notes. |

| | 7 | | First Tier Institutional–Category includes onlynon-government institutional funds that also are not holding any second tier securities. Portfolio holdings of First Tier funds include U.S. Treasury, U.S. other, repurchase agreements, time deposits, domestic bank obligations, foreign bank obligations, first tier commercial paper, floating rate notes, and asset-backed commercial paper. |

| | 8 | | Treasury Institutional–Category includes only institutional government funds that hold 100 percent in U.S. Treasuries. |

| | 9 | | Treasury & Repo Institutional–Category includes only institutional government funds that hold U.S. Treasuries and repurchase agreements backed by the U.S. Treasury. |

5

FUND BASICS

| | | | | | | | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS1,2,10 |

| | | | | | | |

| | | For the period ended

December 31, 2018 | | SEC

7-Day

Current Yield11 | | | One Year | | | Five Years | | | Ten Years | | | Since

Inception | | | Inception Date |

| | | | | | | |

| | Federal Instruments | | | 2.23 | % | | | 1.71 | % | | | N/A | | | | N/A | | | | 0.85 | % | | 10/30/15 |

| | Government | | | 2.34 | | | | 1.74 | | | | 0.56 | % | | | 0.33 | % | | | 2.59 | | | 4/6/93 |

| | Money Market | | | 2.57 | | | | 2.07 | | | | 0.75 | | | | 0.47 | | | | 2.67 | | | 5/18/94 |

| | Prime Obligations | | | 2.56 | | | | 2.06 | | | | 0.73 | | | | 0.44 | | | | 3.00 | | | 3/8/90 |

| | Treasury Instruments | | | 2.22 | | | | 1.71 | | | | 0.53 | | | | 0.27 | | | | 1.97 | | | 3/3/97 |

| | Treasury Obligations | | | 2.33 | | | | 1.73 | | | | 0.54 | | | | 0.29 | | | | 2.79 | | | 4/25/90 |

| | | Treasury Solutions | | | 2.23 | | | | 1.72 | | | | 0.53 | | | | 0.30 | | | | 2.16 | | | 2/28/97 |

| 10 | | The Standardized Total Returns are average annual or cumulative total returns (only if the performance period is one year or less) of Institutional Shares as of the most recent calendarquarter-end. They assume reinvestment of all distributions at NAV. The SEC7-Day Current Yield is not a Standardized Total Return. |

| | | Because Institutional Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

| | | The yields and returns represent past performance. Past performance does not guarantee future results. The Funds’ investment yields and returns will fluctuate as market conditions change. Current performance may be lower or higher than the performance quoted above.Please visit our Web site at www.GSAMFUNDS.com to obtain the most recentmonth-end yields and returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| 11 | | The SEC7-Day Current Yield figures are as of December 31, 2018 and are calculated in accordance with securities industry regulations and do not include net capital gains. SEC7-Day Current Yield may differ slightly from the actual distribution rate of a given Fund because of the exclusion of distributed capital gains, which arenon-recurring.The SEC7-Day Current Yield more closely reflects a Fund’s current earnings than do the Standardized Total Return figures. |

6

YIELD SUMMARY

| | | | | | | | | | | | | | | | | | | | | | |

| | SUMMARY OF THE INSTITUTIONAL SHARES1,2 AS OF 2/28/19 | |

| | | | | | |

| | | Funds | | 7-Day Dist. Yield12 | | | SEC 7-Day Effective Yield13 | | | 30-Day Average Yield14 | | | Weighted Avg. Maturity (days)15 | | | Weighted Avg. Life (days)16 | |

| | | | | | |

| | Federal Instruments | | | 2.28 | % | | | 2.30 | % | | | 2.27 | % | | | 47 | | | | 88 | |

| | Government | | | 2.32 | | | | 2.34 | | | | 2.31 | | | | 22 | | | | 84 | |

| | Money Market | | | 2.62 | | | | 2.63 | | | | 2.61 | | | | 52 | | | | 85 | |

| | Prime Obligations | | | 2.60 | | | | 2.63 | | | | 2.60 | | | | 49 | | | | 75 | |

| | Treasury Instruments | | | 2.26 | | | | 2.27 | | | | 2.24 | | | | 37 | | | | 95 | |

| | Treasury Obligations | | | 2.29 | | | | 2.30 | | | | 2.28 | | | | 21 | | | | 87 | |

| | | Treasury Solutions | | | 2.26 | | | | 2.27 | | | | 2.25 | | | | 39 | | | | 89 | |

| | | The Yields represent past performance. Past performance does not guarantee future results. Current performance may be lower or higher than the performance quoted above. |

| | | Yields reflect fee waivers and expense limitations in effect and will fluctuate as market conditions change. The yield quotations more closely reflect the current earnings of the Fund. Please visit our Web site at www.GSAMFUNDS.com to obtain the most recentmonth-end performance. |

| 12 | | The7-Day Distribution Yield is an annualized measure of a Fund’s dividends per share, divided by the price per share. This yield can include capital gain/loss distribution, if any. This is not an SEC Yield. |

| 13 | | The SEC7-Day Effective Yield of a Fund is calculated in accordance with securities industry regulations and does not include net capital gains. The SEC7-Day Effective Yield assumes reinvestment of dividends for one year. |

| 14 | | The30-Day Average Yield is a net annualized yield of 30 days back from the current date listed. This yield includes capital gain/loss distribution. |

| 15 | | A Fund’s weighted average maturity (WAM) is an average of the effective maturities of all securities held in the portfolio, weighted by each security’s percentage of net assets. This must not exceed 60 days as calculated under SEC Rule2a-7. |

| 16 | | A Fund’s weighted average life (WAL) is an average of the final maturities of all securities held in the portfolio, weighted by each security’s percentage of net assets. This must not exceed 120 days as calculated under SEC Rule2a-7. |

7

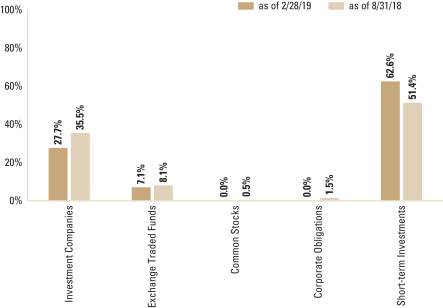

SECTOR ALLOCATIONS

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | SECTOR ALLOCATIONS17 | |

| | | | | | | |

| | | As of February 28, 2019 | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | Security Type

(Percentage of Net Assets) | | Federal Instruments | | | Government | | | Money

Market | | | Prime

Obligations | | | Treasury

Instruments | | | Treasury

Obligations | | | Treasury

Solutions | |

| | | | | | | | |

| | Certificates of Deposit | | | — | | | | — | | | | 0.5 | % | | | 0.5 | % | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Certificates of Deposit - Eurodollar | | | | | | | | | | | 7.8 | | | | — | | | | | | | | | | | | | |

| | | | | | | | |

| | Certificates of Deposit - Yankeedollar | | | — | | | | — | | | | 2.9 | | | | 3.4 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Commercial Paper & Corporate Obligations | | | — | | | | — | | | | 28.7 | | | | 30.8 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Fixed Rate Municipal Debt Obligations | | | — | | | | — | | | | 2.4 | | | | 3.4 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Repurchase Agreements | | | — | | | | 60.1 | % | | | 31.9 | | | | 30.2 | | | | — | | | | 61.6 | % | | | — | |

| | | | | | | | |

| | Time Deposits | | | — | | | | — | | | | 3.3 | | | | 6.0 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Government Agency Obligations | | | 75.2 | % | | | 18.1 | | | | — | | | | 0.2 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Treasury Obligations | | | 45.9 | | | | 23.3 | | | | — | | | | — | | | | 111.4 | % | | | 38.5 | | | | 115.1 | % |

| | | | | | | | |

| | Variable Rate Municipal Debt Obligations | | | — | | | | — | | | | 2.0 | | | | 2.7 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | | Variable Rate Obligations | | | — | | | | — | | | | 23.0 | | | | 24.5 | | | | — | | | | — | | | | — | |

| 17 | | Each Fund is actively managed and, as such, its portfolio composition may differ over time. The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the above table may not sum to 100% due to the exclusion of other assets and liabilities. |

8

SECTOR ALLOCATIONS

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | SECTOR ALLOCATIONS18 | |

| | | | | | | |

| | | As of August 31, 2018 | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| | | Security Type (Percentage of Net Assets) | | Federal

Instruments | | | Government | | | Money

Market | | | Prime

Obligations | | | Treasury

Instruments | | | Treasury

Obligations | | | Treasury

Solutions | |

| | | | | | | | |

| | Certificates of Deposit - Eurodollar | | | — | | | | — | | | | 3.2 | % | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Certificates of Deposit - Yankeedollar | | | — | | | | — | | | | 4.1 | | | | 4.9 | % | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Commercial Paper & Corporate Obligations | | | — | | | | — | | | | 30.4 | | | | 31.9 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Master Demand Notes | | | — | | | | — | | | | | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Fixed Rate Municipal Debt Obligations | | | — | | | | — | | | | 1.4 | | | | 1.1 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | Repurchase Agreements | | | — | | | | 48.9 | % | | | 30.1 | | | | 25.3 | | | | — | | | | 59.0 | % | | | — | |

| | | | | | | | |

| | Time Deposits | | | — | | | | — | | | | 1.3 | | | | 1.3 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Government Agency Obligations | | | 32.6 | % | | | 25.7 | | | | — | | | | 0.2 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Government Guarantee Notes | | | — | | | | — | | | | | | | | | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Government Guarantee Variable Rate Obligations | | | — | | | | — | | | | | | | | | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | U.S. Treasury Obligations | | | 67.9 | | | | 25.6 | | | | 8.3 | | | | 9.5 | | | | 100.5 | % | | | 41.3 | | | | 100.6 | % |

| | | | | | | | |

| | Variable Rate Municipal Debt Obligations | | | — | | | | — | | | | 1.7 | | | | 2.8 | | | | — | | | | — | | | | — | |

| | | | | | | | |

| | | Variable Rate Obligations | | | — | | | | — | | | | 20.4 | | | | 24.5 | | | | — | | | | — | | | | — | |

| 18 | | Each Fund is actively managed and, as such, its portfolio composition may differ over time. The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the above table may not sum to 100% due to the exclusion of other assets and liabilities. |

9

FINANCIAL SQUARE FEDERAL INSTRUMENTS FUND

Schedule of Investments

February 28, 2019 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| U.S. Government Agency Obligations – 75.2% | |

| | Federal Farm Credit Bank (1 Mo. LIBOR – 0.09%) | |

| $ | 1,000,000 | | | | 2.402 | %(a) | | | 03/28/19 | | | $ | 1,000,000 | |

| | Federal Farm Credit Bank (3 Mo. LIBOR – 0.14%) | |

| | 1,800,000 | | | | 2.663 | (a) | | | 09/30/19 | | | | 1,799,947 | |

| | Federal Farm Credit Bank (3 Mo. LIBOR – 0.26%) | |

| | 250,000 | | | | 2.523 | (a) | | | 07/10/19 | | | | 250,000 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.07%)(a) | |

| | 850,000 | | | | 2.485 | | | | 11/29/19 | | | | 850,000 | |

| | 650,000 | | | | 2.490 | | | | 02/18/20 | | | | 650,000 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.08%)(a) | |

| | 700,000 | | | | 2.495 | | | | 10/18/19 | | | | 699,987 | |

| | 750,000 | | | | 2.495 | | | | 12/26/19 | | | | 749,976 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.09%) | |

| | 900,000 | | | | 2.505 | (a) | | | 07/05/19 | | | | 899,994 | |

| | Federal Farm Credit Bank (FEDL01 + 0.11%) | |

| | 800,000 | | | | 2.510 | (a) | | | 08/13/20 | | | | 799,884 | |

| | Federal Farm Credit Bank (Prime Rate – 2.88%) | |

| | 1,000,000 | | | | 2.620 | (a) | | | 05/07/20 | | | | 999,906 | |

| | Federal Farm Credit Bank (Prime Rate – 2.90%) | |

| | 600,000 | | | | 2.600 | (a) | | | 01/30/20 | | | | 600,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.93%) | |

| | 1,200,000 | | | | 2.570 | (a) | | | 11/06/20 | | | | 1,200,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.96%) | |

| | 200,000 | | | | 2.540 | (a) | | | 03/13/20 | | | | 199,845 | |

| | Federal Farm Credit Bank (Prime Rate – 2.98%) | |

| | 300,000 | | | | 2.520 | (a) | | | 11/12/20 | | | | 299,747 | |

| | Federal Farm Credit Bank (Prime Rate – 3.08%)(a) | |

| | 250,000 | | | | 2.420 | | | | 06/27/19 | | | | 249,996 | |

| | 1,600,000 | | | | 2.420 | | | | 07/17/19 | | | | 1,599,939 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.05%) | |

| | 6,000,000 | | | | 2.462 | (a) | | | 10/07/19 | | | | 6,000,000 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.08%) | |

| | 14,000,000 | | | | 2.401 | (a) | | | 03/19/19 | | | | 14,000,000 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.10%) | |

| | 5,900,000 | | | | 2.386 | (a) | | | 04/18/19 | | | | 5,900,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.16%) | |

| | 5,000,000 | | | | 2.591 | (a) | | | 08/04/20 | | | | 5,000,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.26%)(a) | |

| | 25,000,000 | | | | 2.542 | | | | 07/09/19 | | | | 25,000,000 | |

| | 10,000,000 | | | | 2.544 | | | | 07/11/19 | | | | 10,000,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.31%)(a) | |

| | 7,200,000 | | | | 2.466 | | | | 03/12/19 | | | | 7,200,000 | |

| | 4,200,000 | | | | 2.469 | | | | 03/13/19 | | | | 4,200,000 | |

| | 7,200,000 | | | | 2.478 | | | | 03/15/19 | | | | 7,200,000 | |

| | 1,800,000 | | | | 2.514 | | | | 03/22/19 | | | | 1,800,000 | |

| | 750,000 | | | | 2.512 | | | | 03/25/19 | | | | 750,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.32%)(a) | |

| | 3,600,000 | | | | 2.470 | | | | 03/21/19 | | | | 3,600,000 | |

| | 7,300,000 | | | | 2.502 | | | | 03/25/19 | | | | 7,300,000 | |

| | 7,000,000 | | | | 2.502 | | | | 03/27/19 | | | | 7,000,000 | |

| | Federal Home Loan Bank (3 Mo. U.S. T-Bill + 0.07%) | |

| | 10,100,000 | | | | 2.530 | (a) | | | 01/30/20 | | | | 10,101,392 | |

| | Federal Home Loan Bank (Prime Rate – 2.94%) | |

| | 900,000 | | | | 2.560 | (a) | | | 02/26/21 | | | | 900,000 | |

| | Federal Home Loan Bank Discount Notes | |

| | 166,300,000 | | | | 2.428 | | | | 03/01/19 | | | | 166,300,000 | |

| | 2,000,000 | | | | 2.394 | | | | 03/06/19 | | | | 1,999,344 | |

| | |

|

| U.S. Government Agency Obligations – (continued) | |

| | Federal Home Loan Bank Discount Notes – (continued) | |

| 10,000,000 | | | | 2.402 | % | | | 03/06/19 | | | | 9,996,715 | |

| | 35,000,000 | | | | 2.364 | | | | 03/08/19 | | | | 34,983,939 | |

| | 1,800,000 | | | | 2.417 | | | | 03/15/19 | | | | 1,798,334 | |

| | 60,000,000 | | | | 2.423 | | | | 03/22/19 | | | | 59,916,525 | |

| | 10,000,000 | | | | 2.458 | | | | 03/22/19 | | | | 9,985,942 | |

| | 175,000,000 | | | | 2.418 | | | | 03/27/19 | | | | 174,699,195 | |

| | 1,200,000 | | | | 2.500 | | | | 05/17/19 | | | | 1,199,888 | |

| | 30,000,000 | | | | 2.498 | | | | 07/12/19 | | | | 29,729,567 | |

| | 50,000,000 | | | | 2.508 | | | | 08/02/19 | | | | 49,477,470 | |

| | |

| TOTAL U.S. GOVERNMENT

AGENCY OBLIGATIONS |

| | $ | 668,887,532 | |

| | |

| | |

|

| U.S. Treasury Obligations – 45.9% | |

| | United States Treasury Bills | |

| $ | 3,000,000 | | | | 2.383 | % | | | 03/05/19 | | | $ | 2,999,217 | |

| | 600,000 | | | | 2.406 | | | | 03/05/19 | | | | 599,842 | |

| | 500,000 | | | | 2.430 | | | | 03/05/19 | | | | 499,867 | |

| | 900,000 | | | | 2.412 | | | | 03/12/19 | | | | 899,347 | |

| | 7,200,000 | | | | 2.418 | | | | 03/12/19 | | | | 7,194,764 | |

| | 100,000 | | | | 2.422 | | | | 03/12/19 | | | | 99,927 | |

| | 200,000 | | | | 2.423 | | | | 03/12/19 | | | | 199,854 | |

| | 300,000 | | | | 2.428 | | | | 03/12/19 | | | | 299,781 | |

| | 200,000 | | | | 2.342 | (b) | | | 03/14/19 | | | | 199,831 | |

| | 5,300,000 | | | | 2.413 | | | | 03/19/19 | | | | 5,293,706 | |

| | 1,200,000 | | | | 2.418 | | | | 03/19/19 | | | | 1,198,572 | |

| | 5,500,000 | | | | 2.417 | | | | 03/26/19 | | | | 5,490,910 | |

| | 700,000 | | | | 2.422 | | | | 03/26/19 | | | | 698,841 | |

| | 200,000 | | | | 2.423 | | | | 03/26/19 | | | | 199,669 | |

| | 400,000 | | | | 2.402 | | | | 04/02/19 | | | | 399,161 | |

| | 400,000 | | | | 2.406 | | | | 04/02/19 | | | | 399,159 | |

| | 1,700,000 | | | | 2.410 | | | | 04/02/19 | | | | 1,696,419 | |

| | 3,600,000 | | | | 2.411 | | | | 04/02/19 | | | | 3,592,416 | |

| | 100,000 | | | | 2.415 | | | | 04/02/19 | | | | 99,789 | |

| | 3,200,000 | | | | 2.417 | | | | 04/02/19 | | | | 3,193,244 | |

| | 23,100,000 | | | | 2.448 | (b) | | | 04/02/19 | | | | 23,056,700 | |

| | 166,300,000 | | | | 2.440 | (b) | | | 04/11/19 | | | | 165,845,447 | |

| | 1,900,000 | | | | 2.546 | | | | 06/13/19 | | | | 1,886,388 | |

| | 3,170,000 | | | | 2.552 | | | | 06/20/19 | | | | 3,145,711 | |

| | 31,630,000 | | | | 2.546 | | | | 06/27/19 | | | | 31,372,883 | |

| | 4,500,000 | | | | 2.573 | | | | 07/05/19 | | | | 4,460,546 | |

| | 500,000 | | | | 2.469 | | | | 07/25/19 | | | | 495,113 | |

| | 500,000 | | | | 2.472 | | | | 07/25/19 | | | | 495,113 | |

| | 11,100,000 | | | | 2.515 | | | | 08/01/19 | | | | 10,984,421 | |

| | 500,000 | | | | 2.487 | | | | 08/08/19 | | | | 494,611 | |

| | 300,000 | | | | 2.492 | | | | 08/08/19 | | | | 296,760 | |

| | 1,700,000 | | | | 2.494 | | | | 08/08/19 | | | | 1,681,640 | |

| | 3,900,000 | | | | 2.500 | | | | 08/08/19 | | | | 3,857,793 | |

| | 700,000 | | | | 2.501 | | | | 08/08/19 | | | | 692,421 | |

| | 700,000 | | | | 2.502 | | | | 08/08/19 | | | | 692,417 | |

| | 9,800,000 | | | | 2.505 | | | | 08/08/19 | | | | 9,693,724 | |

| | 1,000,000 | | | | 2.510 | | | | 08/22/19 | | | | 988,182 | |

| | 900,000 | | | | 2.515 | | | | 08/22/19 | | | | 889,343 | |

| | 3,000,000 | | | | 2.520 | | | | 08/22/19 | | | | 2,964,403 | |

| | |

| | |

| 10 | | The accompanying notes are an integral part of these financial statements. |

FINANCIAL SQUARE FEDERAL INSTRUMENTS FUND

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| U.S. Treasury Obligations – (continued) | |

| United States Treasury Floating Rate Note (3 Mo. U.S. T-Bill

MMY – 0.00%) |

|

| $ | 15,900,000 | | | | 2.420 | %(a) | | | 01/31/20 | | | $ | 15,903,295 | |

| United States Treasury Floating Rate Note (3 Mo. U.S. T-Bill

MMY + 0.03%) |

|

| | 1,200,000 | | | | 2.453 | (a) | | | 04/30/20 | | | | 1,200,382 | |

| United States Treasury Floating Rate Notes (3 Mo. U.S. T-Bill

MMY + 0.05%)(a) |

|

| | 16,300,000 | | | | 2.468 | | | | 10/31/19 | | | | 16,308,555 | |

| | 10,450,000 | | | | 2.465 | | | | 10/31/20 | | | | 10,450,000 | |

| United States Treasury Floating Rate Note (3 Mo. U.S. T-Bill

MMY + 0.06%) |

|

| | 31,200,000 | | | | 2.480 | (a) | | | 07/31/19 | | | | 31,214,549 | |

| United States Treasury Floating Rate Note (3 Mo. U.S. T-Bill

MMY + 0.07%) |

|

| | 21,200,000 | | | | 2.490 | (a) | | | 04/30/19 | | | | 21,204,273 | |

| | United States Treasury Notes | |

| | 300,000 | | | | 1.000 | | | | 03/15/19 | | | | 299,836 | |

| | 1,800,000 | | | | 1.625 | | | | 03/31/19 | | | | 1,798,710 | |

| | 2,400,000 | | | | 1.250 | | | | 06/30/19 | | | | 2,389,375 | |

| | 3,100,000 | | | | 1.625 | | | | 06/30/19 | | | | 3,090,094 | |

| | 200,000 | | | | 0.750 | | | | 07/15/19 | | | | 198,630 | |

| | 600,000 | | | | 0.875 | | | | 07/31/19 | | | | 596,015 | |

| | 500,000 | | | | 0.750 | | | | 08/15/19 | | | | 495,753 | |

| | 2,400,000 | | | | 3.625 | | | | 08/15/19 | | | | 2,411,243 | |

| | 800,000 | | | | 8.125 | | | | 08/15/19 | | | | 820,282 | |

| | 600,000 | | | | 1.750 | | | | 09/30/19 | | | | 596,768 | |

| | |

| TOTAL U.S. TREASURY

OBLIGATIONS |

| | $ | 408,225,692 | |

| �� | |

| | TOTAL INVESTMENTS – 121.1% | | | $ | 1,077,113,224 | |

| | |

| LIABILITIES IN EXCESS OF

OTHER ASSETS – (21.1)% |

| | | (187,769,625 | ) |

| | |

| | NET ASSETS – 100.0% | | | $ | 889,343,599 | |

| | |

| | |

|

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

| |

(a) | | Variable or floating rate security. Except for floating rate notes (for which final maturity is disclosed), maturity date disclosed is the next interest reset date. Interest rate disclosed is that which is in effect on February 28, 2019. |

| |

(b) | | All or a portion represents a forward commitment. |

Interest rates represent either the stated coupon rate, annualized yield on date of purchase for discounted securities, or, for floating rate securities, the current reset rate, which is based upon current interest rate indices.

Maturity dates represent either the final legal maturity date on the security, the demand date for puttable securities, the date of the next interest rate reset for variable rate securities, or the prerefunded date for those types of securities.

| | |

|

Investment Abbreviations: |

FEDL01 | | —US Federal Funds Effective Rate |

LIBOR | | —London Interbank Offered Rates |

MMY | | —Money Market Yield |

Prime | | —Federal Reserve Bank Prime Loan Rate US |

T-Bill | | —Treasury Bill |

|

| | |

| The accompanying notes are an integral part of these financial statements. | | 11 |

FINANCIAL SQUARE GOVERNMENT FUND

Schedule of Investments

February 28, 2019 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| U.S. Government Agency Obligations – 18.1% | |

| | Federal Farm Credit Bank (1 Mo. LIBOR – 0.09%) | |

| $ | 148,000,000 | | | | 2.402 | %(a) | | | 03/28/19 | | | $ | 148,000,000 | |

| | Federal Farm Credit Bank (3 Mo. LIBOR – 0.14%) | |

| | 246,500,000 | | | | 2.663 | (a) | | | 09/30/19 | | | | 246,492,804 | |

| | Federal Farm Credit Bank (3 Mo. LIBOR – 0.26%) | |

| | 24,500,000 | | | | 2.523 | (a) | | | 07/10/19 | | | | 24,500,000 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.07%)(a) | |

| | 198,700,000 | | | | 2.485 | | | | 11/20/19 | | | | 198,695,707 | |

| | 98,500,000 | | | | 2.485 | | | | 11/29/19 | | | | 98,500,000 | |

| | 98,700,000 | | | | 2.490 | | | | 02/18/20 | | | | 98,700,000 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.08%)(a) | |

| | 120,500,000 | | | | 2.495 | | | | 10/18/19 | | | | 120,497,712 | |

| | 98,600,000 | | | | 2.495 | | | | 12/26/19 | | | | 98,596,781 | |

| | Federal Farm Credit Bank (3 Mo. U.S. T-Bill MMY + 0.09%) | |

| | 118,700,000 | | | | 2.505 | (a) | | | 07/05/19 | | | | 118,699,179 | |

| | Federal Farm Credit Bank (FEDL01 + 0.11%) | |

| | 123,400,000 | | | | 2.510 | (a) | | | 08/13/20 | | | | 123,382,156 | |

| | Federal Farm Credit Bank (Prime Rate – 2.88%) | |

| | 148,000,000 | | | | 2.620 | (a) | | | 05/07/20 | | | | 147,986,061 | |

| | Federal Farm Credit Bank (Prime Rate – 2.90%) | |

| | 88,800,000 | | | | 2.600 | (a) | | | 01/30/20 | | | | 88,800,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.93%) | |

| | 197,600,000 | | | | 2.570 | (a) | | | 11/06/20 | | | | 197,600,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.94%) | |

| | 244,900,000 | | | | 2.565 | (a) | | | 10/30/20 | | | | 244,900,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.95%) | |

| | 24,300,000 | | | | 2.550 | (a) | | | 04/30/20 | | | | 24,300,000 | |

| | Federal Farm Credit Bank (Prime Rate – 2.96%) | |

| | 24,600,000 | | | | 2.540 | (a) | | | 03/13/20 | | | | 24,580,932 | |

| | Federal Farm Credit Bank (Prime Rate – 2.98%) | |

| | 54,000,000 | | | | 2.520 | (a) | | | 11/12/20 | | | | 53,954,514 | |

| | Federal Farm Credit Bank (Prime Rate – 3.08%)(a) | |

| | 36,500,000 | | | | 2.420 | | | | 06/27/19 | | | | 36,499,399 | |

| | 216,800,000 | | | | 2.420 | | | | 07/17/19 | | | | 216,791,787 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.05%) | |

| | 988,000,000 | | | | 2.462 | (a) | | | 10/07/19 | | | | 988,000,000 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.08%) | |

| | 1,900,000,000 | | | | 2.401 | (a) | | | 03/19/19 | | | | 1,900,000,000 | |

| | Federal Home Loan Bank (1 Mo. LIBOR – 0.10%) | |

| | 903,750,000 | | | | 2.386 | (a) | | | 04/18/19 | | | | 903,750,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.16%) | |

| | 477,700,000 | | | | 2.591 | (a) | | | 08/04/20 | | | | 477,700,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.26%)(a) | |

| | 745,000,000 | | | | 2.549 | | | | 06/27/19 | | | | 745,000,000 | |

| | 495,000,000 | | | | 2.542 | | | | 07/09/19 | | | | 495,000,000 | |

| | 496,000,000 | | | | 2.544 | | | | 07/11/19 | | | | 496,000,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.31%)(a) | |

| | 566,900,000 | | | | 2.469 | | | | 03/13/19 | | | | 566,900,000 | |

| | 949,300,000 | | | | 2.478 | | | | 03/15/19 | | | | 949,300,000 | |

| | 224,000,000 | | | | 2.514 | | | | 03/22/19 | | | | 224,000,000 | |

| | 98,500,000 | | | | 2.512 | | | | 03/25/19 | | | | 98,500,000 | |

| | Federal Home Loan Bank (3 Mo. LIBOR – 0.32%)(a) | |

| | 493,500,000 | | | | 2.470 | | | | 03/21/19 | | | | 493,500,000 | |

| | 986,800,000 | | | | 2.502 | | | | 03/25/19 | | | | 986,800,000 | |

| | 987,000,000 | | | | 2.502 | | | | 03/27/19 | | | | 987,000,000 | |

| | Federal Home Loan Bank (3 Mo. U.S. T-Bill + 0.07%) | |

| | 1,755,000,000 | | | | 2.530 | (a) | | | 01/30/20 | | | | 1,755,241,963 | |

| | |

|

| U.S. Government Agency Obligations – (continued) | |

| | Federal Home Loan Bank (Prime Rate – 2.94%) | |

| 98,300,000 | | | | 2.560 | %(a) | | | 02/26/21 | | | | 98,300,000 | |

| | Federal Home Loan Bank Discount Notes | |

| | 200,000,000 | | | | 2.281 | | | | 03/01/19 | | | | 200,000,000 | |

| | 229,500,000 | | | | 2.526 | | | | 05/08/19 | | | | 228,429,255 | |

| | 217,500,000 | | | | 2.532 | | | | 05/14/19 | | | | 216,393,469 | |

| | 182,600,000 | | | | 2.500 | | | | 05/17/19 | | | | 182,582,920 | |

| | 496,700,000 | | | | 2.539 | | | | 05/21/19 | | | | 493,928,414 | |

| | 496,000,000 | | | | 2.498 | | | | 07/12/19 | | | | 491,528,836 | |

| | Federal National Mortgage Association (SOFR + 0.12%) | |

| | 994,000,000 | | | | 2.490 | (a) | | | 07/30/19 | | | | 994,000,000 | |

| | Federal National Mortgage Association (SOFR + 0.16%) | |

| | 124,250,000 | | | | 2.530 | (a) | | | 01/30/20 | | | | 124,250,000 | |

| | Overseas Private Investment Corp. (3 Mo. U.S. T-Bill + 0.00%)(a) | |

| | 102,234,956 | | | | 2.420 | | | | 03/07/19 | | | | 102,234,957 | |

| | 646,873,699 | | | | 2.440 | | | | 03/07/19 | | | | 646,873,699 | |

| | |

| TOTAL U.S. GOVERNMENT

AGENCY OBLIGATIONS |

| | $ | 18,156,690,545 | |

| | |

| | | | | | | | | | | | | | |

|

| U.S. Treasury Obligations – 23.3% | |

| | United States Treasury Bills | |

| $ | 100,000 | | | | 2.422 | % | | | 03/26/19 | | | $ | 99,834 | |

| | 428,300,000 | | | | 2.443 | (b) | | | 04/02/19 | | | | 427,498,841 | |

| | 2,710,000,000 | | | | 2.440 | (b) | | | 04/11/19 | | | | 2,702,592,676 | |

| | 443,400,000 | | | | 2.546 | | | | 06/13/19 | | | | 440,223,285 | |

| | 697,470,000 | | | | 2.552 | | | | 06/20/19 | | | | 692,125,925 | |

| | 518,730,000 | | | | 2.546 | | | | 06/27/19 | | | | 514,513,301 | |

| | 2,854,800,000 | | | | 2.573 | | | | 07/05/19 | | | | 2,829,770,541 | |

| | 159,700,000 | | | | 2.536 | | | | 07/11/19 | | | | 158,253,650 | |

| | 1,276,300,000 | | | | 2.515 | | | | 08/01/19 | | | | 1,263,010,527 | |

| | 56,100,000 | | | | 2.487 | | | | 08/08/19 | | | | 55,495,367 | |

| | 33,200,000 | | | | 2.492 | | | | 08/08/19 | | | | 32,841,440 | |

| | 238,600,000 | | | | 2.494 | | | | 08/08/19 | | | | 236,023,120 | |

| | 531,700,000 | | | | 2.500 | | | | 08/08/19 | | | | 525,945,824 | |

| | 101,300,000 | | | | 2.501 | | | | 08/08/19 | | | | 100,203,259 | |

| | 101,300,000 | | | | 2.502 | | | | 08/08/19 | | | | 100,202,583 | |

| | 1,096,750,000 | | | | 2.505 | | | | 08/08/19 | | | | 1,084,856,353 | |

| | 116,900,000 | | | | 2.510 | | | | 08/22/19 | | | | 115,518,534 | |

| | 121,250,000 | | | | 2.515 | | | | 08/22/19 | | | | 119,814,198 | |

| | 350,100,000 | | | | 2.520 | | | | 08/22/19 | | | | 345,945,772 | |

| United States Treasury Floating Rate Note (3 Mo. U.S. T-Bill

MMY + 0.04%) |

|

| | 3,000,000,500 | | | | 2.46 | (a) | | | 07/31/20 | | | | 2,999,688,879 | |

| United States Treasury Floating Rate Notes (3 Mo. U.S. T-Bill

MMY + 0.05%)(a) |

|

| | 4,854,100,000 | | | | 2.468 | | | | 10/31/19 | | | | 4,854,429,673 | |

| | 2,003,000,000 | | | | 2.465 | | | | 10/31/20 | | | | 2,003,000,000 | |

| | United States Treasury Notes | |

| | 51,300,000 | | | | 1.125 | | | | 05/31/19 | | | | 51,118,717 | |

| | 384,600,000 | | | | 1.250 | | | | 06/30/19 | | | | 382,897,461 | |

| | 506,300,000 | | | | 1.625 | | | | 06/30/19 | | | | 504,682,032 | |

| | 34,400,000 | | | | 0.750 | | | | 07/15/19 | | | | 34,164,401 | |

| | 69,900,000 | | | | 0.875 | | | | 07/31/19 | | | | 69,435,728 | |

| | 80,600,000 | | | | 0.750 | | | | 08/15/19 | | | | 79,915,404 | |

| | 370,000,000 | | | | 3.625 | | | | 08/15/19 | | | | 371,738,061 | |

| | |

| | |

| 12 | | The accompanying notes are an integral part of these financial statements. |

FINANCIAL SQUARE GOVERNMENT FUND

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| U.S. Treasury Obligations – (continued) | |

| | United States Treasury Notes – (continued) | |

| $ | 117,000,000 | | | | 8.125 | % | | | 08/15/19 | | | $ | 119,966,270 | |

| | 91,800,000 | | | | 1.750 | | | | 09/30/19 | | | | 91,305,457 | |

| | |

| TOTAL U.S. TREASURY

OBLIGATIONS |

| | $ | 23,307,277,113 | |

| | |

| TOTAL INVESTMENTS BEFORE

REPURCHASE AGREEMENTS |

| | $ | 41,463,967,658 | |

| | |

| | | | | | | | | | | | | | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – 59.5% | |

| | Bank of Montreal | |

| $ | 20,000,000 | | | | 2.600 | % | | | 03/01/19 | | | $ | 20,000,000 | |

| | Maturity Value: $20,001,444 | |

| Collateralized by Federal National Mortgage Association, 4.000%

to 4.500%, due 01/01/49 to 03/01/49, Government National

Mortgage Association, 4.500%, due 01/20/49, U.S. Treasury

Bonds, 2.500% to 3.000%, due 02/15/46 to 02/15/47 and a U.S.

Treasury Note, 2.250%, due 11/15/27. The aggregate market

value of the collateral, including accrued interest, was

$20,599,869. |

|

| | 500,000,000 | | | | 2.480 | (d) | | | 03/07/19 | | | | 500,000,000 | |

| | Maturity Value: $501,928,889 | |

| | Settlement Date: 02/13/19 | |

| Collateralized by Federal Home Loan Bank, 3.500%, due

06/09/28, Federal Home Loan Mortgage Corp., 3.000% to

4.000%, due 10/01/29 to 11/01/48, Federal National Mortgage

Association, 3.000% to 5.000%, due 03/01/28 to 03/01/49 and

Government National Mortgage Association, 3.000% to

4.500%, due 01/20/46 to 01/20/49. The aggregate market value

of the collateral, including accrued interest, was $514,979,563. |

|

| | |

| | Bank of Nova Scotia (The) | |

| | 200,000,000 | | | | 2.620 | | | | 03/01/19 | | | | 200,000,000 | |

| | Maturity Value: $200,014,556 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.500% to

6.000%, due 11/01/20 to 12/01/48, Federal National Mortgage

Association, 1.750% to 7.125%, due 09/12/19 to 02/01/49 and

Government National Mortgage Association, 4.000% to

5.000%, due 01/20/46 to 02/20/49. The aggregate market value

of the collateral, including accrued interest, was $205,880,107. |

|

| | |

| | BNP Paribas | |

| | 500,000,000 | | | | 2.600 | | | | 03/01/19 | | | | 500,000,000 | |

| | Maturity Value: $500,036,111 | |

| Collateralized by a U.S. Treasury Note, 3.625%, due 08/15/19.

The market value of the collateral, including accrued interest,

was $510,000,000. |

|

| | 1,000,000,000 | | | | 2.600 | | | | 03/01/19 | | | | 1,000,000,000 | |

| | Maturity Value: $1,000,072,222 | |

| Collateralized by a U.S. Treasury Note, 2.875%, due 07/31/25.

The market value of the collateral, including accrued interest,

was $1,020,000,000. |

|

| | 1,000,000,000 | | | | 2.600 | | | | 03/01/19 | | | | 1,000,000,000 | |

| | Maturity Value: $1,000,072,222 | |

| Collateralized by a U.S. Treasury Note, 2.500%, due 06/30/20.

The market value of the collateral, including accrued interest,

was $1,020,000,000. |

|

| | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | BNP Paribas – (continued) | |

| 475,000,000 | | | | 2.480 | %(d) | | | 03/07/19 | | | | 475,000,000 | |

| | Maturity Value: $480,890,001 | |

| | Settlement Date: 02/27/19 | |

| Collateralized by U.S. Treasury Bonds, 2.500% to 2.750%, due

08/15/42 to 02/15/45, U.S. Treasury Inflation-Indexed Bonds,

2.125% to 3.875%, due 04/15/29 to 02/15/41, U.S. Treasury

Interest-Only Stripped Securities, 0.000%, due 05/15/21 to

11/15/45, U.S. Treasury Notes, 1.750% to 3.500%, due

05/15/20 to 01/31/23 and U.S. Treasury Principal-Only

Stripped Securities, 0.000%, due 08/15/28 to 05/15/46. The

aggregate market value of the collateral, including accrued

interest, was $484,499,997. |

|

| | 1,490,000,000 | | | | 2.480 | (d) | | | 03/07/19 | | | | 1,490,000,000 | |

| | Maturity Value: $1,499,443,290 | |

| | Settlement Date: 12/20/18 | |

| Collateralized by Federal Farm Credit Bank, 1.375% to 4.080%,

due 06/12/19 to 09/20/38, Federal Home Loan Mortgage Corp.,

3.000% to 7.500%, due 03/01/19 to 03/01/49, Federal National

Mortgage Association, 2.500% to 7.500%, due 04/01/19 to

06/01/51, Federal National Mortgage Association Stripped

Security, 0.000%, due 11/15/30, Government National

Mortgage Association, 2.000% to 6.000%, due 02/15/33 to

02/20/49, U.S. Treasury Bills, 0.000%, due 07/05/19 to

08/08/19, U.S. Treasury Bonds, 2.750% to 8.125%, due

08/15/19 to 08/15/45, U.S. Treasury Inflation-Indexed Bonds,

0.750% to 3.875%, due 01/15/29 to 02/15/45, U.S. Treasury

Interest-Only Stripped Securities, 0.000%, due 05/15/37 to

08/15/37 and U.S. Treasury Notes, 1.000% to 2.750%, due

09/30/19 to 12/31/23. The aggregate market value of the

collateral, including accrued interest, was $1,529,098,824. |

|

| | 250,000,000 | | | | 2.500 | (d) | | | 03/07/19 | | | | 250,000,000 | |

| | Maturity Value: $253,142,359 | |

| | Settlement Date: 01/08/19 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000% to

4.500%, due 04/01/46 to 09/01/48, Federal National Mortgage

Association, 3.000% to 5.000%, due 10/01/30 to 07/01/48,

Government National Mortgage Association, 2.500% to

4.500%, due 12/15/26 to 12/20/48, a U.S. Treasury Bill,

0.000%, due 03/28/19, a U.S. Treasury Bond, 4.375%, due

11/15/39, a U.S. Treasury Inflation-Indexed Bond, 3.375%, due

04/15/32, U.S. Treasury Interest-Only Stripped Securities,

0.000%, due 05/15/19 to 02/15/33, U.S. Treasury Notes,

1.375% to 2.625%, due 03/31/20 to 02/28/26 and a U.S.

Treasury Principal-Only Stripped Security, 0.000%, due

05/15/39. The aggregate market value of the collateral,

including accrued interest, was $256,992,319. |

|

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

FINANCIAL SQUARE GOVERNMENT FUND

Schedule of Investments(continued)

February 28, 2019 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | BNP Paribas – (continued) | |

| $ | 870,000,000 | | | | 2.500 | %(d) | | | 03/07/19 | | | $ | 870,000,000 | |

| | Maturity Value: $880,874,993 | |

| | Settlement Date: 02/27/19 | |

| Collateralized by Federal Farm Credit Bank, 3.420%, due

09/11/37, Federal Home Loan Mortgage Corp., 2.000% to

7.000%, due 03/01/19 to 12/01/48, Federal National Mortgage

Association, 2.500% to 6.500%, due 04/01/19 to 01/01/57,

Government National Mortgage Association, 3.000% to

7.000%, due 12/15/25 to 02/20/49, a U.S. Treasury Bill,

0.000%, due 04/23/19, a U.S. Treasury Bond, 2.500%, due

02/15/45, U.S. Treasury Inflation-Indexed Notes, 0.500% to

1.125%, due 01/15/21 to 01/15/28, U.S. Treasury Interest-Only

Stripped Securities, 0.000%, due 02/15/33 to 08/15/47 and U.S.

Treasury Notes, 1.500% to 2.625%, due 08/15/20 to 02/28/23.

The aggregate market value of the collateral, including accrued

interest, was $895,836,763. |

|

| | 2,000,000,000 | | | | 2.500 | (d) | | | 03/07/19 | | | | 2,000,000,000 | |

| | Maturity Value: $2,024,999,984 | |

| | Settlement Date: 01/04/19 | |

| Collateralized by Federal Farm Credit Bank, 1.375% to 3.540%,

due 06/12/19 to 01/25/38, Federal Home Loan Bank, 0.875%,

due 08/05/19, Federal Home Loan Mortgage Corp., 3.000%,

due 01/01/47, Federal National Mortgage Association, 1.200%

to 5.500%, due 08/16/19 to 11/01/48, Federal National

Mortgage Association Stripped Security, 0.000%, due

11/15/30, Government National Mortgage Association,

3.645%, due 01/20/43, U.S. Treasury Bills, 0.000%, due

03/26/19 to 07/11/19, U.S. Treasury Bonds, 2.500% to 7.250%,

due 08/15/22 to 08/15/48, a U.S. Treasury Inflation-Indexed

Bond, 0.875%, due 02/15/47, U.S. Treasury Inflation-Indexed

Notes, 0.375% to 1.875%, due 07/15/19 to 07/15/27, U.S.

Treasury Interest-Only Stripped Securities, 0.000%, due

05/15/19 to 05/15/48, U.S. Treasury Notes, 1.125% to 2.875%,

due 01/31/20 to 02/15/29 and U.S. Treasury Principal-Only

Stripped Securities, 0.000%, due 11/15/22 to 02/15/23. The

aggregate market value of the collateral, including accrued

interest, was $2,040,181,870. |

|

| | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | BNP Paribas (Overnight MBS + 0.02%) | |

| 500,000,000 | | | | 2.630 | %(a)(d) | | | 03/01/19 | | | | 500,000,000 | |

| | Maturity Value: $540,765,025 | |

| | Settlement Date: 02/23/16 | |

| Collateralized by Federal Farm Credit Bank, 3.130% to 4.150%,

due 06/27/33 to 06/02/36, Federal Home Loan Bank, 4.200%,

due 06/01/33, Federal Home Loan Mortgage Corp., 0.000% to

8.000%, due 04/01/19 to 10/01/48, Federal National Mortgage

Association, 1.200% to 7.000%, due 08/16/19 to 11/01/48,

Federal National Mortgage Association Stripped Securities,

0.000%, due 05/15/22 to 05/15/29, Government National

Mortgage Association, 2.500% to 6.450%, due 12/15/26 to

12/20/48, U.S. Treasury Bills, 0.000%, due 03/28/19 to

06/20/19, U.S. Treasury Bonds, 2.750% to 6.625%, due

02/15/27 to 08/15/44, a U.S. Treasury Inflation-Indexed Note,

1.125%, due 01/15/21, U.S. Treasury Interest-Only Stripped

Securities, 0.000%, due 05/15/21 to 02/15/33 and U.S.

Treasury Notes, 1.375% to 2.750%, due 06/30/20 to 08/15/21.

The aggregate market value of the collateral, including accrued

interest, was $514,149,208. |

|

| | 550,000,000 | | | | 2.630 | (a)(d) | | | 03/01/19 | | | | 550,000,000 | |

| | Maturity Value: $594,560,263 | |

| | Settlement Date: 02/23/16 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000% to

7.500%, due 03/01/19 to 11/01/48, Federal National Mortgage

Association, 3.000% to 9.000%, due 04/01/19 to 11/01/48,

Government National Mortgage Association, 2.500% to

9.500%, due 06/15/21 to 11/20/48, a U.S. Treasury Bill,

0.000%, due 06/20/19, a U.S. Treasury Bond, 2.875%, due

05/15/43 and U.S. Treasury Notes, 1.250% to 2.375%, due

04/30/20 to 02/29/24. The aggregate market value of the

collateral, including accrued interest, was $566,310,755. |

|

| | |

| | CIBC Wood Gundy Securities | |

| | 100,000,000 | | | | 2.460 | (d) | | | 03/07/19 | | | | 100,000,000 | |

| | Maturity Value: $100,410,000 | |

| | Settlement Date: 02/11/19 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000%,

due 10/01/33, Federal National Mortgage Association, 3.500%

to 4.000%, due 11/01/48 to 03/01/49, Government National

Mortgage Association, 4.500%, due 10/20/48 to 01/20/49 and a

U.S. Treasury Note, 2.750%, due 09/15/21. The aggregate

market value of the collateral, including accrued interest, was

$102,999,091. |

|

| | 300,000,000 | | | | 2.460 | (d) | | | 03/07/19 | | | | 300,000,000 | |

| | Maturity Value: $301,926,999 | |

| | Settlement Date: 01/18/19 | |

| Collateralized by U.S. Treasury Bonds, 3.125%, due 02/15/43 to

05/15/48, U.S. Treasury Inflation-Indexed Notes, 0.625% to

0.750%, due 01/15/26 to 07/15/28 and U.S. Treasury Notes,

1.875% to 3.125%, due 09/30/20 to 11/15/28. The aggregate

market value of the collateral, including accrued interest, was

$306,000,020. |

|

| | |

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

FINANCIAL SQUARE GOVERNMENT FUND

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | CIBC Wood Gundy Securities – (continued) | |

| $ | 500,000,000 | | | | 2.460 | %(d) | | | 03/07/19 | | | $ | 500,000,000 | |

| | Maturity Value: $502,049,999 | |

| | Settlement Date: 02/11/19 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000% to

4.000%, due 04/01/44 to 02/01/48, Federal National Mortgage

Association, 3.500% to 4.500%, due 05/01/42 to 10/01/48,

Government National Mortgage Association, 4.500%, due

10/20/48 to 01/20/49 and a U.S. Treasury Note, 2.750%, due

09/15/21. The aggregate market value of the collateral,

including accrued interest, was $514,992,421. |

|

| | 300,000,000 | | | | 2.480 | (d) | | | 03/07/19 | | | | 300,000,000 | |

| | Maturity Value: $301,798,000 | |

| | Settlement Date: 01/14/19 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000% to

3.500%, due 12/01/47 to 02/01/48, Federal National Mortgage

Association, 3.500% to 5.000%, due 04/01/46 to 02/01/49,

Government National Mortgage Association, 4.000% to

5.000%, due 10/20/44 to 01/20/49 and a U.S. Treasury Note,

2.750%, due 09/15/21. The aggregate market value of the

collateral, including accrued interest, was $308,995,449. |

|

| | 550,000,000 | | | | 2.480 | (d) | | | 03/07/19 | | | | 550,000,000 | |

| | Maturity Value: $553,410,001 | |

| | Settlement Date: 01/18/19 | |

| Collateralized by Federal Home Loan Mortgage Corp., 3.000% to

4.500%, due 01/01/48 to 03/01/49, Federal National Mortgage

Association, 3.500% to 4.500%, due 11/01/30 to 03/01/49,

Government National Mortgage Association, 4.500%, due

10/20/48 to 01/20/49, a U.S. Treasury Bond, 3.125%, due

05/15/48 and a U.S. Treasury Note, 2.000%, due 11/15/26. The

aggregate market value of the collateral, including accrued

interest, was $566,494,286. |

|

| | |

| | Citibank N.A. (Overnight MBS + 0.01%) | |

| | 1,000,000,000 | | | | 2.630 | (a) | | | 03/07/19 | | | | 1,000,000,000 | |

| | Maturity Value: $1,009,570,284 | |

| | Settlement Date: 11/01/18 | |

| Collateralized by Federal Farm Credit Bank, 2.430% to 2.779%,

due 03/23/20 to 07/19/27, Federal Home Loan Bank, 2.484% to

5.500%, due 02/25/20 to 07/15/36, Federal Home Loan

Mortgage Corp., 0.875% to 11.000%, due 03/01/19 to

07/01/48, Federal National Mortgage Association, 0.000% to

8.500%, due 03/01/19 to 03/01/49, Government National

Mortgage Association, 2.500% to 8.500%, due 05/15/24 to

01/20/49, Tennessee Valley Authority, 2.875% to 3.500%, due

09/15/24 to 12/15/42, U.S. Treasury Bills, 0.000%, due

03/19/19 to 01/30/20, U.S. Treasury Bonds, 2.250% to 8.125%,

due 08/15/19 to 05/15/47, a U.S. Treasury Floating Rate Note,

2.535%, due 01/31/21, U.S. Treasury Inflation-Indexed Bonds,

0.625% to 3.875%, due 04/15/28 to 02/15/47, U.S. Treasury

Inflation-Indexed Notes, 0.125% to 1.875%, due 04/15/19 to

01/15/29 and U.S. Treasury Notes, 0.875% to 3.625%, due

04/30/19 to 02/15/27. The aggregate market value of the

collateral, including accrued interest, was $1,020,000,175. |

|

| | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | Credit Agricole Corporate and Investment Bank | |

| 3,200,000 | | | | 2.350 | % | | | 03/01/19 | | | | 3,200,000 | |

| | Maturity Value: $3,200,209 | |

| Collateralized by U.S. Treasury Bills, 0.000%, due 06/06/19 to

02/27/20, U.S. Treasury Bonds, 4.625% to 7.250%, due

08/15/22 to 02/15/40, a U.S. Treasury Inflation-Indexed Note,

0.125%, due 04/15/19 and U.S. Treasury Notes, 2.000% to

2.125%, due 01/31/21 to 02/28/21. The aggregate market value

of the collateral, including accrued interest, was $3,264,073. |

|

| | 300,000,000 | | | | 2.350 | | | | 03/01/19 | | | | 300,000,000 | |

| | Maturity Value: $300,019,583 | |

| Collateralized by U.S. Treasury Inflation-Indexed Notes, 0.125%

to 0.250%, due 04/15/20 to 07/15/26 and U.S. Treasury Notes,

2.250% to 2.750%, due 02/28/23 to 11/15/24. The aggregate

market value of the collateral, including accrued interest, was

$306,000,059. |

|

| | 150,000,000 | | | | 2.530 | | | | 03/01/19 | | | | 150,000,000 | |

| | Maturity Value: $150,010,542 | |

| Collateralized by U.S. Treasury Bills, 0.000%, due 03/26/19 to

02/27/20, a U.S. Treasury Floating Rate Note, 2.480%, due

07/31/19, U.S. Treasury Inflation-Indexed Notes, 0.125% to

0.375%, due 04/15/19 to 07/15/27 and U.S. Treasury Notes,

1.125% to 2.625%, due 01/31/20 to 03/31/22. The aggregate

market value of the collateral, including accrued interest, was

$153,000,024. |

|

| | |

| | Daiwa Capital Markets America, Inc. | |

| | 95,220,588 | | | | 2.580 | | | | 03/01/19 | | | | 95,220,588 | |

| | Maturity Value: $95,227,412 | |

| Collateralized by a U.S. Treasury Note, 2.250%, due 08/15/27.

The market value of the collateral, including accrued interest,

was $97,125,000. |

|

| | 95,656,715 | | | | 2.580 | | | | 03/01/19 | | | | 95,656,715 | |

| | Maturity Value: $95,663,570 | |

| Collateralized by a U.S. Treasury Note, 2.125%, due 09/30/24.

The market value of the collateral, including accrued interest,

was $97,569,849. |

|

| | 97,274,582 | | | | 2.580 | | | | 03/01/19 | | | | 97,274,582 | |

| | Maturity Value: $97,281,553 | |

| Collateralized by a U.S. Treasury Note, 2.125%, due 05/15/25.

The market value of the collateral, including accrued interest,

was $99,220,074. |

|

| | 109,460,782 | | | | 2.580 | | | | 03/01/19 | | | | 109,460,782 | |

| | Maturity Value: $109,468,627 | |

| Collateralized by a U.S. Treasury Note, 2.750%, due 06/30/25.

The market value of the collateral, including accrued interest,

was $111,649,998. |

|

| | 135,816,175 | | | | 2.580 | | | | 03/01/19 | | | | 135,816,175 | |

| | Maturity Value: $135,825,908 | |

| Collateralized by a U.S. Treasury Note, 2.000%, due 04/30/24.

The market value of the collateral, including accrued interest,

was $138,532,498. |

|

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

FINANCIAL SQUARE GOVERNMENT FUND

Schedule of Investments(continued)

February 28, 2019 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | Daiwa Capital Markets America, Inc. – (continued) | |

| $ | 144,176,285 | | | | 2.580 | % | | | 03/01/19 | | | $ | 144,176,285 | |

| | Maturity Value: $144,186,618 | |

| Collateralized by a U.S. Treasury Note, 2.875%, due 09/30/23.

The market value of the collateral, including accrued interest,

was $147,059,811. |

|

| | 144,485,292 | | | | 2.580 | | | | 03/01/19 | | | | 144,485,292 | |

| | Maturity Value: $144,495,647 | |

| Collateralized by a U.S. Treasury Note, 2.000%, due 02/15/23.

The market value of the collateral, including accrued interest,

was $147,374,998. |

|

| | 147,564,828 | | | | 2.580 | | | | 03/01/19 | | | | 147,564,828 | |

| | Maturity Value: $147,575,403 | |

| Collateralized by a U.S. Treasury Bond, 2.875%, due 05/15/28.

The market value of the collateral, including accrued interest,

was $150,516,125. |

|

| | 160,858,889 | | | | 2.580 | | | | 03/01/19 | | | | 160,858,889 | |

| | Maturity Value: $160,870,417 | |

| Collateralized by a U.S. Treasury Note, 2.875%, due 10/15/21.

The market value of the collateral, including accrued interest,

was $164,076,067. |

|

| | 175,794,117 | | | | 2.580 | | | | 03/01/19 | | | | 175,794,117 | |

| | Maturity Value: $175,806,716 | |

| Collateralized by a U.S. Treasury Bond, 6.500%, due 11/15/26.

The market value of the collateral, including accrued interest,

was $179,309,999. |

|

| | 250,839,091 | | | | 2.580 | | | | 03/01/19 | | | | 250,839,091 | |

| | Maturity Value: $250,857,068 | |

| Collateralized by a U.S. Treasury Note, 2.500%, due 01/15/22.

The market value of the collateral, including accrued interest,

was $255,855,873. |

|

| | 252,064,965 | | | | 2.580 | | | | 03/01/19 | | | | 252,064,965 | |

| | Maturity Value: $252,083,030 | |

| Collateralized by a U.S. Treasury Note, 2.750%, due 08/31/23.

The market value of the collateral, including accrued interest,

was $257,106,264. |

|

| | 282,103,042 | | | | 2.580 | | | | 03/01/19 | | | | 282,103,042 | |

| | Maturity Value: $282,123,259 | |

| Collateralized by a U.S. Treasury Note, 2.875%, due 10/31/23.

The market value of the collateral, including accrued interest,

was $287,745,103. |

|

| | 342,766,763 | | | | 2.580 | | | | 03/01/19 | | | | 342,766,763 | |

| | Maturity Value: $342,791,328 | |

| Collateralized by a U.S. Treasury Note, 2.375%, due 02/29/24.

The market value of the collateral, including accrued interest,

was $349,622,098. |

|

| | 370,172,000 | | | | 2.580 | | | | 03/01/19 | | | | 370,172,000 | |

| | Maturity Value: $370,198,529 | |

| Collateralized by a U.S. Treasury Bond, 2.750%, due 04/30/23.

The market value of the collateral, including accrued interest,

was $377,575,440. |

|

| | 385,467,518 | | | | 2.580 | | | | 03/01/19 | | | | 385,467,518 | |

| | Maturity Value: $385,495,143 | |

| Collateralized by a U.S. Treasury Note, 2.625%, due 12/31/25.

The market value of the collateral, including accrued interest,

was $393,176,868. |

|

| | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | Daiwa Capital Markets America, Inc. – (continued) | |

| 389,044,112 | | | | 2.580 | | | | 03/01/19 | | | | 389,044,112 | |

| | Maturity Value: $389,071,993 | |

| Collateralized by a U.S. Treasury Note, 2.250%, due 11/15/27.

The market value of the collateral, including accrued interest,

was $396,824,994. |

|

| | 439,647,051 | | | | 2.580 | | | | 03/01/19 | | | | 439,647,051 | |

| | Maturity Value: $439,678,559 | |

| Collateralized by a U.S. Treasury Note, 2.625%, due 12/15/21.

The market value of the collateral, including accrued interest,

was $448,439,992. |

|

| | 481,587,205 | | | | 2.580 | | | | 03/01/19 | | | | 481,587,205 | |

| | Maturity Value: $481,621,719 | |

| Collateralized by a U.S. Treasury Note, 2.875%, due 11/30/23.

The market value of the collateral, including accrued interest,

was $491,218,949. |

|

| | |

| | Deutsche Bank Securities, Inc. | |

| | 400,000,000 | | | | 2.620 | | | | 03/01/19 | | | | 400,000,000 | |

| | Maturity Value: $400,029,111 | |

| Collateralized by Federal Home Loan Mortgage Corp., 2.500% to

5.000%, due 01/01/27 to 02/01/49 and U.S. Treasury Notes,

2.250% to 2.625%, due 03/31/21 to 02/15/29. The aggregate

market value of the collateral, including accrued interest, was

$409,132,378. |

|

| | |

| | Federal Reserve Bank of New York | |

| | 350,000,000 | | | | 2.250 | | | | 03/01/19 | | | | 350,000,000 | |

| | Maturity Value: $350,021,875 | |

| Collateralized by U.S. Treasury Notes, 2.000% to 2.750%, due

11/30/22 to 08/31/25. The aggregate market value of the

collateral, including accrued interest, was $350,021,884. |

|

| | |

| | Fixed Income Clearing Corp. | |

| | 115,000,000 | | | | 2.360 | | | | 03/01/19 | | | | 115,000,000 | |

| | Maturity Value: $115,007,539 | |

| Collateralized by a U.S. Treasury Bill, 0.000%, due 02/27/20 and

a U.S. Treasury Note, 1.375%, due 01/31/21. The aggregate

market value of the collateral, including accrued interest, was

$117,300,072. |

|

| | 500,000,000 | | | | 2.400 | | | | 03/01/19 | | | | 500,000,000 | |

| | Maturity Value: $500,033,333 | |

| Collateralized by a U.S. Treasury Bill, 0.000%, due 02/27/20. The

market value of the collateral, including accrued interest, was

$510,000,009. |

|

| | 9,500,000,000 | | | | 2.550 | | | | 03/01/19 | | | | 9,500,000,000 | |

| | Maturity Value: $9,500,672,917 | |

| Collateralized by U.S. Treasury Bonds, 3.125% to 3.750%, due

11/15/43 to 08/15/44 and U.S. Treasury Notes, 2.750% to

3.375%, due 11/15/19 to 07/31/25. The aggregate market value

of the collateral, including accrued interest, was

$9,690,000,058. |

|

| | |

| | |

| 16 | | The accompanying notes are an integral part of these financial statements. |

FINANCIAL SQUARE GOVERNMENT FUND

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Amortized

Cost | |

|

| Repurchase Agreements-Unaffiliated Issuers(c) – (continued) | |

| | HSBC Bank PLC | |

| $ | 2,100,000,000 | | | | 2.570 | % | | | 03/01/19 | | | $ | 2,100,000,000 | |

| | Maturity Value: $2,100,149,917 | |

| Collateralized by U.S. Treasury Bonds, 0.750% to 8.000%, due

11/15/21 to 05/15/47 and U.S. Treasury Notes, 1.125% to

3.625%, due 04/30/19 to 08/15/27. The aggregate market value

of the collateral, including accrued interest, was

$2,142,000,006. |

|