UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05387

Franklin Mutual Series Funds

(Exact name of registrant as specified in charter)

101 John F. Kennedy Parkway, Short Hills, NJ 07078-2705

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant’s telephone number, including area code: (210) 912-2100

Date of fiscal year end: 12/31

Date of reporting period: 6/30/17

| Item 1. | Reports to Stockholders. |

| Semiannual Report and Shareholder Letter June 30, 2017 |

Franklin Mutual Beacon Fund

A SERIES OF FRANKLIN MUTUAL SERIES FUNDS

Sign up for electronic delivery at franklintempleton.com/edelivery

Franklin Templeton Investments

Gain From Our Perspective®

At Franklin Templeton Investments, we’re dedicated to one goal: delivering exceptional asset management for our clients. By bringing together multiple, world-class investment teams in a single firm, we’re able to offer specialized expertise across styles and asset classes, all supported by the strength and resources of one of the world’s largest asset managers. This has helped us to become a trusted partner to individual and institutional investors across the globe.

Dear Franklin Mutual Beacon Fund Shareholder:

The first half of 2017 saw most equity markets continue their long move upwards. The Standard & Poor’s 500® Index (S&P 500®) posted a +9.34% total return and the MSCI World Index delivered a +11.02% total return.1

The political uncertainty and unpredictability of recent years has continued in 2017. In the U.S., President Trump has continued his unconventional governance approach, while Congress has remained relentlessly partisan, leading to significant uncertainty about policies and legislation. The financial markets expected “business friendly” moves, but specific legislative progress on issues such as health care, tax reform and infrastructure did not come to fruition. In the U.K., a surprise election was called in April when the Conservative Party held a huge polling lead, but at the June election the Tories lost their majority in Parliament. Recent elections in France went according to expectations, lending some much appreciated stability there.

Despite these generally unsettling events, the global economy continued its slow expansion since the Great Recession. Unemployment also continued to decline in most developed markets. Wage growth showed signs of acceleration and in the U.S. interest rates began to rise, perhaps signaling the first steps toward monetary normalization.

Equity markets appreciated as economic fundamentals improved. Valuation is, of course, a critical factor in our analysis and we always ask ourselves if current and potential investments represent an attractive balance of risk and reward. As some equity markets reached all-time highs, we maintained our focus on individual investments and the prospects for each

1. Source: Morningstar.

See www.franklintempletondatasources.com for additional data provider information.

business in the context of its valuation and the backdrop of potential political and economic risks.

In many equity markets, growth stocks outperformed value stocks during the period. For example, the S&P 500 Growth Index returned +13.33%, while the S&P 500 Value Index returned +4.85%.1 The difference in performance was driven in part by a significant rally in Internet and software stocks, which dominated the S&P 500 Growth Index. We do not know how long these trends will continue, but historically, periods of strong performance by growth stocks have eventually been followed by relatively weaker performance. In addition, the S&P 500 Value Index has components that we believe are facing disruption from new technology (e.g., the rapid market share shift to online retailing from traditional bricks and mortar dominated retailers that are often labeled as value stocks). Exacerbating the disruption is the reality that many new technology companies are able to innovate without the need to show immediate profits.

Amid dynamic markets and evolving economic conditions, we believe active, professional investment management serves investors well. We also recognize the important role of financial advisors in today’s markets and encourage investors to continue to seek their advice. Amid changing markets and economic conditions, we are confident investors with a well-diversified portfolio and a patient, long-term outlook will be well positioned for the years ahead.

On the following pages, the Fund’s portfolio management team discusses the economic environment during the first six months of 2017 and reviews investment decisions made during this

| Not FDIC Insured | | | May Lose Value | | | No Bank Guarantee |

franklintempleton.com |

Not part of the semiannual report |

|

1 |

|

period. Please remember all securities markets fluctuate, as do mutual fund share prices.

We thank you for investing with Franklin Templeton, welcome your questions and comments, and look forward to continuing to serve your investment needs in the years ahead.

Sincerely,

Peter A. Langerman

Chairman, President and Chief Executive Officer

Franklin Mutual Advisers, LLC

This letter reflects our analysis and opinions as of June 30, 2017, unless otherwise indicated. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

Semiannual Report

| Franklin Mutual Beacon Fund | 3 | |||

| Performance Summary | 10 | |||

| Your Fund’s Expenses | 12 | |||

| Financial Highlights and Statement of Investments | 13 | |||

| Financial Statements | 24 | |||

| Notes to Financial Statements | 28 | |||

|

| 40

|

| |

Visit franklintempleton.com for fund updates, to access your account, or to find helpful financial planning tools.

2 |

Not part of the semiannual report |

franklintempleton.com |

Semiannual Report

This semiannual report for Franklin Mutual Beacon Fund covers the period ended June 30, 2017.

Your Fund’s Goal and Main Investments

The Fund seeks capital appreciation, which may occasionally be short term, with income as a secondary goal. The Fund focuses mainly on what the investment manager believes are undervalued mid- and large-cap equity securities with a significant portion of its assets in foreign securities and, to a lesser extent, in the securities of distressed companies and merger arbitrage securities. The Fund may invest a substantial portion, potentially up to 100% of its assets in foreign securities, which may include sovereign debt and participations in foreign government debt.

Performance Overview

The Fund’s Class Z shares delivered a +8.76% cumulative total return for the six months ended June 30, 2017. In comparison, the Fund’s benchmark, the MSCI World Index, which tracks stock performance in global developed markets, generated a +11.02% total return.1 You can find more of the Fund’s performance data in the Performance Summary beginning on page 10.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

Economic and Market Overview

The global economy generally expanded during the period under review. In this environment, global developed and emerging market stocks, as measured by the MSCI All Country World Index, generated a total return of +11.82%. Global markets were aided by improved industrial commodity prices at certain points during the period, generally upbeat economic data across regions, investor optimism about pro-growth and pro-business policies in the U.S., hopes of tax reforms under

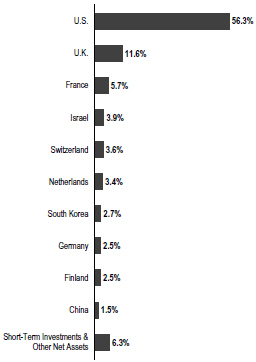

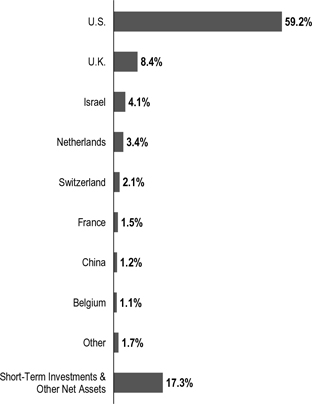

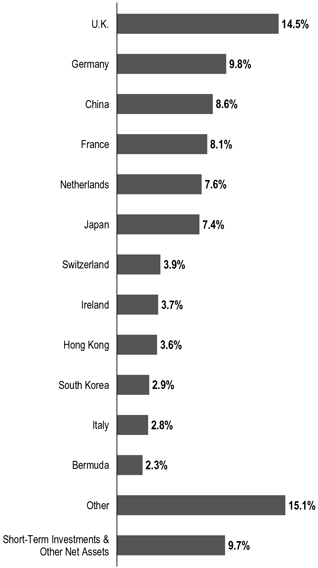

Geographic Composition*

Based on Total Net Assets as of 6/30/17

*Figures are stated as a percentage of total and may not equal 100% or may be negative due to rounding, use of any derivatives, unsettled trades or other factors.The Fund held 37.4% of total net assets in foreign securities.

the Trump administration, Emmanuel Macron’s election as France’s president and encouraging corporate earnings reports.

However, global markets reflected investor concerns about the timing and economic effects of the U.K.’s exit from the European Union (also known as “Brexit”). Other headwinds included the health of European banks, concerns about political uncertainty in the U.S. and European Union, geopolitical tensions in certain regions, worries about global oversupply in oil production despite a pact to extend cuts, and comments

1. Source: Morningstar.

The indexes are unmanaged and include reinvestment of any income or distributions. They do not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 18.

franklintempleton.com |

Semiannual Report |

|

3 |

|

F R A N K L I N M U T U A L B E A C O N F U N D

toward period-end from key central bankers around the world about potentially raising interest rates.

U.S. economic growth decelerated in 2017’s first quarter, largely due to slower growth in consumer spending and declines in private inventory investment and government spending. However, growth accelerated in the second quarter due to increases in consumer spending, business investment and federal government spending. The unemployment rate decreased from 4.7% in December 2016 to 4.4% at period-end.2 Annual inflation, as measured by the Consumer Price Index, decreased from 2.1% to 1.6% during the period. After increasing its benchmark interest rate in March, the U.S. Federal Reserve (Fed), at its June meeting, made the widely anticipated increase to its target range for the federal funds rate from 0.75%–1.00% to 1.00%–1.25%, amid signs of a growing U.S. economy, a strengthening labor market and an improvement in business spending.

In Europe, the U.K.’s economy grew at a slower rate in 2017’s first quarter over the previous quarter, largely due to slower growth in household spending. The eurozone’s growth increased in the first quarter over the previous quarter. The bloc’s annual inflation rate fluctuated during the reporting period and ended slightly higher from where it began. During the period, the European Central Bank kept its key policy rates unchanged.

In Asia, Japan’s quarterly gross domestic product (GDP) remained unchanged in 2017’s first quarter compared to 2016’s fourth quarter. In April 2017, the Bank of Japan (BOJ) slightly increased its GDP forecasts for the 2017–2018 fiscal year. However, the BOJ lowered its inflation forecast.

In emerging markets, Brazil’s quarterly GDP grew for the first time in two years, as its first-quarter 2017 GDP grew compared to the previous quarter. The country’s central bank cut its benchmark interest rate four times between January and June 2017 to spur economic growth. Russia’s GDP grew in 2017’s first quarter compared to the prior-year period. The Bank of Russia reduced its key interest rate in March, April and June 2017 to try to revive its economy. China’s economy grew faster in the first half of 2017 compared to the first half of 2016, driven by solid growth in industrial production, services, fixed-asset investment, retail sales, and imports and exports. The People’s Bank of China left its benchmark interest rate unchanged during the period. Overall, emerging market stocks,

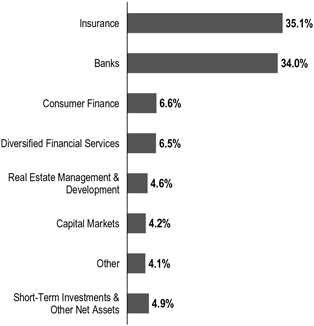

| Top 10 Sectors/Industries | ||||

| Based on Equity Securities as of 6/30/17 | ||||

| % of Total Net Assets | ||||

| Pharmaceuticals | 12.0% | |||

| Banks | 10.0% | |||

| Software | 8.7% | |||

| Media | 7.7% | |||

| Oil, Gas & Consumable Fuels | 5.7% | |||

| Health Care Equipment & Supplies | 5.1% | |||

| Communications Equipment | 4.3% | |||

| Diversified Telecommunication Services | 3.4% | |||

| Electrical Equipment | 3.2% | |||

| Tobacco | 3.1% | |||

as measured by the MSCI Emerging Markets Index, rose during the period.

Investment Strategy

At Franklin Mutual Series, we are committed to our distinctive value approach to investing, which we believe can generate above-average risk-adjusted returns over time for our shareholders. Our major investment strategy is investing in undervalued stocks. When selecting undervalued equities, we are attracted to what we believe are fundamentally strong companies with healthy balance sheets, high-quality assets, substantial free cash flow and shareholder-oriented management teams and whose stocks are trading at discounts to our assessment of the companies’ intrinsic or business value. We also look for asset-rich companies whose shares may be trading at depressed levels due to concerns over short-term earnings disappointments, litigation, management strategy or other perceived negatives. This strict value approach is not only intended to improve the likelihood of upside potential, but also reduces the risk of substantial declines, in our opinion. While the vast majority of our undervalued equity investments are made in publicly traded companies globally, we may invest occasionally in privately held companies as well.

We complement this more traditional investment strategy with two others. One is distressed investing, a highly specialized field that has proven quite profitable during certain periods over the years. Distressed investing is complex and can take many forms. The most common distressed investment the Fund undertakes is the purchase of financially troubled or bankrupt companies’ debt at a substantial discount to face value. After the financially distressed company is reorganized, often in

2. Source: Bureau of Labor Statistics.

4 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

bankruptcy court, the old debt is typically replaced with new securities issued by the financially stronger company.

The other piece of our investment strategy is participating in arbitrage situations, another highly specialized field. When companies announce proposed mergers or takeovers, commonly referred to as “deals,” the target company may trade at a discount to the bid it ultimately accepts. One form of arbitrage involves purchasing the target company’s stock when it is trading below the value we believe it would receive in a deal. In keeping with our commitment to a relatively conservative investment approach, we typically focus our arbitrage efforts on announced deals, and avoid rumored deals or other situations we consider relatively risky.

In addition, it is our practice to hedge the Fund’s currency exposure when we deem it advantageous for our shareholders.

What is meant by “hedge”?

To hedge an investment is to take a position intended to offset potential losses/gains that may be incurred by a companion financial instrument.

Manager’s Discussion

Many equity markets posted meaningful gains in 2017’s first half, across most regions and with minimal volatility. Global markets were aided by generally upbeat economic data, improved corporate earnings in the U.S., Europe and Japan, as well as improved industrial commodity prices at certain points during the period. However, those largely positive headline conditions overshadowed a fair amount of turbulence and uncertainty.

In the U.S., markets began 2017 rallying as investors hoped that a Republican sweep of U.S. elections in November 2016 would lead to a general loosening in regulations and tax reform, including lower corporate tax rates. However, political gridlock took hold. The political drama in Washington, D.C., tempered the rally in U.S. markets overall. Many stocks that led the way in the post-election rally subsequently gave back some or all of their outperformance, particularly value stocks dominated by companies in cyclical sectors most likely to benefit from acceleration in economic growth. In an environment of modest economic growth and low interest rates, investors continued to favor growth stocks. During the period, the Russell 1000® Growth Index generated a total return of +13.99%, while the

Russell 1000® Value Index posted a total return of +4.66%.1 Within the Russell 1000® Growth Index, stocks with the largest weights were technology firms that dominated the headlines: Apple,3 Alphabet (a.k.a. Google),3 Microsoft, Amazon.com3 and Facebook.3

European equity markets started 2017 slowly, but political events combined with upbeat economic news sparked strong performance during the period, with the notable exception of the U.K. Elections in Europe produced generally positive outcomes, with voters in the Netherlands and France rejecting extremist candidates. Political stability in the European Union (EU) helped to support equity markets on the belief that it would help facilitate the ongoing economic recovery. In the U.K., however, a snap election resulting in no party having a majority in Parliament appeared to make a “hard Brexit,” in which the U.K. leaves the EU in March 2019 without a negotiated deal, even more likely than before.

As value investors, we managed to benefit from steady economic growth despite underlying market turbulence. In all market environments, we seek to invest prudently in securities that we believe represent good value, and then we adjust our views as the world around us changes.

The energy sector has been a significant area of investment for the Fund.4 Following an extended period of high prices, crude oil and natural gas prices have been significantly lower during the past few years. The benchmark oil price declined from more than $100 a barrel to below $30, and has more recently stayed between $40 and $60 during the first half of 2017. The impact on the sector, and the securities of companies in the sector, has been unsurprisingly quite dramatic. Although many uncertainties exist, we continue to expect demand for oil and gas to rise for a number of years, which we believe will require continued investment by the sector, not only to meet that growth but also to replace declining production in mature fields around the world. Accordingly, we expect some combination of higher prices or lower costs over time to provide the sufficient returns needed to justify the required investment.

After an initial period of distress, most companies within the energy sector appear to have made considerable progress in resizing their cost structures and strengthening their balance sheets. In aggregate, capital spending has been cut massively, and cash flow breakeven levels suggest an ability to fund a base level of investment activity given crude oil and gas prices as of

3. Not a Fund holding.

4. The energy sector comprises oil, gas and consumable fuels in the SOI.

franklintempleton.com |

Semiannual Report |

|

5 |

|

F R A N K L I N M U T U A L B E A C O N F U N D

period-end. From an investment standpoint, in many cases we are finding securities with reasonable prospects at current commodity prices, and substantively greater upside potential should our longer term price-versus-cost outlook come to pass. We expect continued commodity price volatility, but would look to use that to our advantage when seeking to buy or sell energy sector securities.

Our energy sector investment process has focused on finding situations where commodity price upside is not necessary to generate attractive security returns. One such area is within the infrastructure space. Companies such as Kinder Morgan3 and Williams provide critical pipelines, processing facilities, ports, and other assets used to bring vital commodities to market. Investors shunned these companies due to a combination of counterparty risk related to exploration and production companies, their own balance sheet concerns and dividend levels. As our analysis about the criticality of their assets and the flexibility of their funding options has, in our view, been proven, the securities of infrastructure companies have recovered significantly from their lows. Moreover, if expectations of an oil and gas supply glut from greater North American production hold true, more infrastructure investment should be needed to move this product to export markets.

Royal Dutch Shell, a leading integrated oil and gas company, is another investment held by the Fund for which fears about the impact of low commodity prices were overblown, in our view. The company used the initial phase of the crude oil price downturn to acquire BG Group, a major exploration and production company with significant positions and strength in liquefied natural gas and a great oil asset in the pre-salt Santos Basin in Brazil. The assets were highly complementary to Shell’s existing positions, allowing the post-merger company to prune other areas of its portfolio and still show considerable growth. Management, under the leadership of relatively new chief executive officer Ben van Beurden, has been focused on reducing costs so that the company can still grow, while funding all required capital expenditures and its dividend, at an oil price below $50 per barrel. As Shell shows continued progress in its efforts and demonstrates the resilience of its portfolio and balance sheet, we expect the shares to continue to benefit.

Merger and acquisition activity has remained healthy, with the number of deals remaining high, although the average size of deals fell. Very large deals may have been affected negatively by ongoing political and regulatory uncertainty. Although

many mega-deals were rumored, the largest deal actually announced during the period was Becton, Dickinson and Company’s3 takeover of C.R. Bard.3 Meanwhile, many large deals initiated in 2016 await regulatory approval, including Bayer’s3 acquisition of Monsanto, AT&T’s3 acquisition of Time Warner, and 21st Century Fox’s3 offer for Sky. Several key regulatory agencies remain short of members, including the Federal Communication Commission and the Federal Trade Commission, and these openings may be affecting regulatory approvals.

Credit spreads narrowed in 2016 and continued that trend in the first half of 2017 for higher quality credit, with the exception of a brief period of volatility in March and April. High yield credit spreads have remained at levels seen at the start of 2017. The spread compression provided the Fund with the opportunity to exit many of the opportunities that presented themselves in early 2016, including several “hung deals,” as prices improved, spreads shrank, and the risk-adjusted returns were no longer mispriced. As the year progressed and investors became more willing buyers of credit, mispriced risk became more difficult to find, in our opinion. However, we found what we viewed as value in some unloved industries like specialty pharmaceuticals, hospitals, media/broadcasting and telecommunications5 that faced increasing political or secular challenges. In sorting through these less-favored industries, we sought out securities that we believed could benefit most from liquidity-enhancing events like asset sales, the ability within existing agreements to issue secured debt, and free cash flow that could create a long enough runway to weather the storm and/or provide enough current recovery to create the enterprise at a significant discount to our assessment of its intrinsic value. In times when the credit markets fluctuate and value is difficult to easily identify, we believe our industry specific expertise, deep fundamental analysis with a focus on cash flow, and intensive credit and covenant review combine seamlessly and provide us with unique ways of looking at the same ideas others may disregard.

Turning to Fund performance, top positive contributors included South Korea-based Samsung Electronics, U.S.-based medical device maker Medtronic and Finland-based global communications and information technology company Nokia.

Samsung Electronics is a low cost provider of commodity memory products (e.g., dynamic random-access memory and flash memory), which have seen very strong pricing recently. Samsung also produces smartphones, consumer electronics and

5. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in the SOI.

6 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

| Top 10 Equity Holdings | ||||

| 6/30/17 | ||||

Company Sector/Industry, Country | % of Total Net Assets | |||

Medtronic PLC | 3.6% | |||

| Health Care Equipment & Supplies, U.S. | ||||

Novartis AG | 3.6% | |||

| Pharmaceuticals, Switzerland | ||||

Time Warner Inc. | 3.4% | |||

| Media, U.S. | ||||

Koninklijke KPN NV | 3.4% | |||

| Diversified Telecommunication Services, Netherlands | ||||

Sensata Technologies Holding NV | 3.2% | |||

| Electrical Equipment, U.S. | ||||

British American Tobacco PLC | 3.1% | |||

| Tobacco, U.K. | ||||

Societe Generale SA | 3.0% | |||

| Banks, France | ||||

JPMorgan Chase & Co. | 3.0% | |||

| Banks, U.S. | ||||

Vodafone Group PLC | 2.9% | |||

| Wireless Telecommunication Services, U.K. | ||||

KLX Inc. | 2.9% | |||

| Aerospace & Defense, U.S. | ||||

other goods. In February, shares retreated as Samsung chief Jay Y. Lee was arrested for bribery as part of a wider government influence-peddling scandal that led to the impeachment of then president Park Geun-hye. However, the stock price rallied as investors turned their focus to Samsung’s better-than-expected earnings results announced in April. Samsung reported strong sales in its core businesses, including memory chips and OLED (organic light-emitting diode) displays. Despite adverse publicity surrounding its Note 7 smartphone in the fall of 2016, sales of its newest generation of smartphones have been running ahead of market expectations. Management also pleasantly surprised investors in April by announcing a plan to cancel existing treasury shares held by the company.

Investors responded positively to quarterly results issued by Medtronic in February and May. On both occasions, earnings exceeded consensus expectations, driven by solid revenues and successful cost control efforts, which led to better operating profitability. The positive results led to improved investor confidence in Medtronic’s ability to deliver on future growth goals, especially given concerns following tough quarterly results issued in November 2016. Medtronic’s agreement in April to sell its medical supplies business to Cardinal Health3 provided additional support to Medtronic’s stock price. Medtronic obtained the medical supplies business as part of its 2014 acquisition of Covidien. The medical supplies business, in our view, was not core to Medtronic’s operations and had less

attractive profitability and future growth prospects. In addition, Medtronic intends to use the after-tax proceeds for additional share buybacks and to pay down debt.

In April, Nokia reported an upbeat set of quarterly results that included strong margins in its networks business and solid sales in its wireless business. The positive results appear to reflect some improvement in market conditions for wireless network equipment. Nokia also earned more revenue from its patents, while management reaffirmed its earnings guidance for 2017. We believe the trend of declining revenues is on the path to stabilizing and that further synergies from Nokia’s acquisition of Alcatel-Lucent, completed in mid-2016, are likely to support earnings improvement. Shares of Nokia also reacted positively to the announcement in May that the company reached a settlement on unresolved patent litigation and signed a business collaboration agreement with Apple.3 In our view, Nokia likely saved a meaningful amount in litigation costs and gained a potential source of growth for its Internet protocol routing business.

During the period under review, Fund investments that detracted from performance included U.S.-based drugstore chain Rite Aid, U.S.-based oil and gas exploration and production company Marathon Oil and U.S. bank Capital One Financial.

Shares of Rite Aid declined as a deal to be acquired by Walgreens Boots Alliance fell apart. The transaction was mired in antitrust review by the Federal Trade Commission (FTC) during much of the period as the FTC questioned whether Walgreens’ proposed divestitures were sufficient to maintain competition. In late June, Walgreens announced the immediate termination of the merger agreement. Instead, Rite Aid agreed to sell numerous stores and related distribution assets to Walgreens. The new agreement is also subject to antitrust review, but we believe FTC approval is likely.

Shares of Marathon Oil generally followed the path of declining oil prices. During the first half of 2017, oil prices retreated as U.S. crude oil production increased and data showed that worldwide supply had not yet begun to decline. The supply and price trends for crude oil prices overshadowed some moves by Marathon that we believe were positive. As part of its portfolio transformation effort, in March Marathon announced agreements to exit a Canadian oil sands asset, and two transactions to acquire acreage in the northern Delaware basin of New Mexico. Although we regard the price received for the oil sands asset to be merely adequate, we look favorably upon the continuing expansion of the company’s resource portfolio and increasing focus on predictable, higher return

franklintempleton.com |

Semiannual Report |

|

7 |

|

F R A N K L I N M U T U A L B E A C O N F U N D

onshore assets. Additionally, the three transactions led to a further improvement in Marathon’s balance sheet. These favorable changes were nonetheless overshadowed by an oil market which remains both volatile and challenging.

Capital One Financial is the seventh largest bank in the U.S. Financials stocks were negatively impacted in March by a combination of a decline in the 10-year U.S. Treasury yield and increased doubts among investors that the current U.S. administration and Congress would quickly enact their economic agenda.6 Also in March, weaker-than-expected U.S. consumer credit data drove investors to anticipate lower future earnings as a result of higher reserves. Additionally, Capital One withdrew its late 2016 agreement to acquire the credit card portfolio of retailer Cabela’s3 due to complications related to a 2015 consent order with the U.S. Office of the Comptroller of the Currency. The Cabela deal was subsequently revived as Capital One partnered with financial company Synovus.3 In late April, shares of Capital One slipped further after the company announced quarterly results that fell short of consensus expectations. The miss in earnings was largely driven by a higher-than-expected increase in reserves as Capital One raised its expected rate of net charge-offs (the amount of bad debt written off minus any subsequent amount recovered) for 2017. In our view, however, the update was more of a hit to confidence than a meaningful negative for Capital One’s financial performance.

During the period, the Fund held currency forwards and futures seeking to hedge most of the currency risk of the portfolio’s non-U.S. dollar investments. The currency forwards had a negative impact on the Fund’s performance because of the depreciation of the U.S. dollar versus the hedged currencies, while currency futures had a negligible impact.

What is a currency forward?

A currency forward is an agreement between the Fund and a counterparty to buy or sell a foreign currency in exchange for another currency at a specific exchange rate on a future date.

What is a future?

A future is an agreement between the Fund and a counterparty made through a U.S. or foreign futures exchange to buy or sell an underlying instrument or asset at a specific price on a future date.

Thank you for your participation in Franklin Mutual Beacon Fund. We look forward to continuing to serve your investment needs.

|

Christian Correa, CFA Co-Portfolio Manager | |

|

Mandana Hormozi Co-Portfolio Manager | |

|

Aman Gupta, CFA Assistant Portfolio Manager | |

The foregoing information reflects our analysis, opinions and portfolio holdings as of June 30, 2017, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

CFA® is a trademark owned by CFA Institute.

6. The financials sector comprises banks, consumer finance and insurance in the SOI.

See www.franklintempletondatasources.com for additional data provider information.

8 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

Christian Correa has been portfolio manager for Franklin Mutual Beacon Fund since 2007 and a co-portfolio manager since December 2010. He joined Franklin Templeton Investments in 2003 and serves as Director of Research for Franklin Mutual Advisers. Previously, he covered merger arbitrage and special situations at Lehman Brothers Holdings Inc.

Mandana Hormozi has been a co-portfolio manager for Franklin Mutual Beacon Fund since 2010 and was assistant portfolio manager for the Fund since 2009. Before that, she was assistant portfolio manager for Franklin Mutual Global Discovery Fund since 2007. She has been an analyst for Franklin Mutual Advisers since 2003, when she joined Franklin Templeton Investments. Previously, she was a senior vice president in the equity research department at Lazard Freres. Also, she was an economic research analyst at Mitsubishi Bank.

Aman Gupta has been assistant portfolio manager for Franklin Mutual Beacon Fund since December 2013 and has been an analyst for Franklin Mutual Advisers since 2010. Previously, Mr. Gupta was a senior equity analyst and director at Evergreen Investments, where he covered the health care industry with additional responsibilities in the consumer and industrials sectors.

franklintempleton.com |

Semiannual Report |

|

9 |

|

F R A N K L I N M U T U A L B E A C O N F U N D

Performance Summary as of June 30, 2017

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 6/30/17

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Sales charges will vary depending on the size of the investment and the class of share purchased. The maximum is 5.75% and the minimum is 0%. Class A: 5.75% maximum initial sales charge. For other share classes, visit franklintempleton.com.

| Share Class | | Cumulative Total Return1 | | | Average Annual Total Return2 | | ||

Z | ||||||||

6-Month | +8.76% | +8.76% | ||||||

1-Year | +20.87% | +20.87% | ||||||

5-Year | +81.36% | +12.64% | ||||||

10-Year | +53.77% | +4.40% | ||||||

A | ||||||||

6-Month | +8.63% | +2.36% | ||||||

1-Year | +20.53% | +13.63% | ||||||

5-Year | +78.83% | +11.00% | ||||||

10-Year | +49.33% | +3.48% | ||||||

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

See page 11 for Performance Summary footnotes.

10 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

P E R F O R M A N C E S U M M A R Y

Total Annual Operating Expenses3

| Share Class | ||||

Z | 0.80% | |||

A | 1.05% | |||

Each class of shares is available to certain eligible investors and has different annual fees and expenses, as described in the prospectus.

All investments involve risks, including possible loss of principal. Value securities may not increase in price as anticipated or may decline further in value. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Smaller company stocks have exhibited greater price volatility than larger company stocks, particularly over the short term. The Fund’s investments in companies engaged in mergers, reorganizations or liquidations also involve special risks as pending deals may not be completed on time or on favorable terms. The Fund may invest in lower rated bonds, which entail higher credit risk. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

3. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

franklintempleton.com |

Semiannual Report |

11 |

F R A N K L IN M U T U A L B E A C O N F U N D

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions; and (2) ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value” for each class of shares. You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

Actual (actual return after expenses) | Hypothetical (5% annual return before expenses) | |||||||||||||||||

Share Class | Beginning Account Value 1/1/17 | Ending Account Value 6/30/17 | Expenses Paid During 1/1/17–6/30/171,2 | Ending Value 6/30/17 | Expenses Paid During 1/1/17–6/30/171,2 | Net Annualized Expense Ratio2 | ||||||||||||

| Z | $1,000 | $1,087.60 | $4.04 | $1,020.93 | $3.91 | 0.78% | ||||||||||||

| A | $1,000 | $1,086.30 | $5.33 | $1,019.69 | $5.16 | 1.03% | ||||||||||||

| C | $1,000 | $1,082.30 | $9.19 | $1,015.97 | $8.90 | 1.78% | ||||||||||||

| R | $1,000 | $1,084.60 | $6.62 | $1,018.45 | $6.41 | 1.28% | ||||||||||||

| R6 | $1,000 | $1,088.20 | $3.68 | $1,021.27 | $3.56 | 0.71% | ||||||||||||

1. Expenses are equal to the annualized expense ratio for the six-month period as indicated above–in the far right column–multiplied by the simple average account value over the period indicated, and then multiplied by 181/365 to reflect the one-half year period.

2. Reflects expenses after fee waivers and expense reimbursements. Does not include acquired fund fees and expenses.

12 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

Six Months Ended

June 30, 2017 |

Year Ended December 31,

| |||||||||||||||||||||||||

(unaudited)

|

2016

|

2015

|

2014

|

2013

|

2012

| |||||||||||||||||||||

Class Z | ||||||||||||||||||||||||||

| Per share operating performance | ||||||||||||||||||||||||||

(for a share outstanding throughout the period) | ||||||||||||||||||||||||||

Net asset value, beginning of period | $15.30

| $14.30 |

| $16.59

|

|

| $16.91

|

|

| $13.36

|

|

| $11.68

|

| ||||||||||||

Income from investment operationsa: | ||||||||||||||||||||||||||

Net investment incomeb | 0.17

|

| 0.37c

|

|

| 0.29

|

|

| 0.54d

|

|

| 0.31

|

|

| 0.24

|

| ||||||||||

Net realized and unrealized gains (losses) | 1.17

|

| 1.93

|

|

| (0.99)

|

|

| 0.62

|

|

| 3.56

|

|

| 1.68

|

| ||||||||||

Total from investment operations |

1.34

|

| 2.30

|

|

|

(0.70)

|

|

|

1.16

|

|

|

3.87

|

|

|

1.92

|

| ||||||||||

Less distributions from: | ||||||||||||||||||||||||||

Net investment income | —

|

| (0.37)

|

|

| (0.37)

|

|

| (0.69)

|

|

| (0.32)

|

|

| (0.24)

|

| ||||||||||

Net realized gains | —

|

| (0.93)

|

|

| (1.22)

|

|

| (0.79)

|

|

| —

|

|

| —

|

| ||||||||||

Total distributions |

—

|

|

(1.30)

|

|

|

(1.59)

|

|

|

(1.48)

|

|

|

(0.32)

|

|

|

(0.24)

|

| ||||||||||

Net asset value, end of period |

$16.64

|

|

$15.30

|

|

|

$14.30

|

|

|

$16.59

|

|

|

$16.91

|

|

|

$13.36

|

| ||||||||||

Total returne | 8.76%

|

| 16.11%

|

|

| (4.14)%

|

|

| 6.82%

|

|

| 29.11%

|

|

| 16.44%

|

| ||||||||||

Ratios to average net assetsf | ||||||||||||||||||||||||||

Expensesg | 0.78%h

|

| 0.80%h

|

|

| 0.84%h,i

|

|

| 0.83%h

|

|

| 0.80%h

|

|

| 0.84%

|

| ||||||||||

Expenses incurred in connection with securities sold short | —%

|

| 0.01%

|

|

| 0.04%

|

|

| 0.04%

|

|

| —%j

|

|

| 0.01%

|

| ||||||||||

Net investment income | 2.11%

|

| 2.48%c

|

|

| 1.73%

|

|

| 3.14%d

|

|

| 2.02%

|

|

| 1.87%

|

| ||||||||||

| Supplemental data | ||||||||||||||||||||||||||

Net assets, end of period (000’s) | $2,772,594

|

| $2,564,120

|

|

| $2,420,165

|

|

| $2,774,929

|

|

| $2,876,322

|

|

| $2,450,546

|

| ||||||||||

Portfolio turnover rate | 10.39%

|

| 30.94%

|

|

| 35.80%

|

|

| 40.06%

|

|

| 32.95%

|

|

| 43.23%

|

| ||||||||||

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.81%.

dNet investment income per share includes approximately $0.24 per share related to income received in the form of a special dividend in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.74%.

eTotal return is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gIncludes dividend and/or interest expense on securities sold short and security borrowing fees, if any. See below for the ratios of such expenses to average net assets for the periods presented. See Note 1(d).

hBenefit of expense reduction rounds to less than 0.01%.

iBenefit of waiver and payments by affiliates rounds to less than 0.01%.

jRounds to less than 0.01%.

franklintempleton.com |

The accompanying notes are an integral part of these financial statements. |

Semiannual Report |

13 |

F R A N K L I N M U T U A L B E A C O N F U N D

F I N A N C I A L H I G H L I G H T S

Six Months Ended (unaudited) | Year Ended December 31, | |||||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||||||

| ||||||||||||||||||||||||

| Class A | ||||||||||||||||||||||||

| Per share operating performance | ||||||||||||||||||||||||

(for a share outstanding throughout the period) | ||||||||||||||||||||||||

Net asset value, beginning of period | $15.18 | $14.20 | $16.47 | $16.80 | $13.28 | $11.61 | ||||||||||||||||||

|

| |||||||||||||||||||||||

Income from investment operationsa: | ||||||||||||||||||||||||

Net investment incomeb | 0.15 | 0.33c | 0.24 | 0.49d | 0.26 | 0.20 | ||||||||||||||||||

Net realized and unrealized gains (losses) | 1.16 | 1.91 | (0.97) | 0.60 | 3.54 | 1.67 | ||||||||||||||||||

|

| |||||||||||||||||||||||

Total from investment operations | 1.31 | 2.24 | (0.73) | 1.09 | 3.80 | 1.87 | ||||||||||||||||||

|

| |||||||||||||||||||||||

Less distributions from: | ||||||||||||||||||||||||

Net investment income | — | (0.33) | (0.32) | (0.63) | (0.28) | (0.20) | ||||||||||||||||||

Net realized gains | — | (0.93) | (1.22) | (0.79) | — | — | ||||||||||||||||||

|

| |||||||||||||||||||||||

Total distributions | — | (1.26) | (1.54) | (1.42) | (0.28) | (0.20) | ||||||||||||||||||

|

| |||||||||||||||||||||||

Net asset value, end of period | $16.49 | $15.18 | $14.20 | $16.47 | $16.80 | $13.28 | ||||||||||||||||||

|

| |||||||||||||||||||||||

Total returne | 8.63% | 15.80% | (4.33)% | 6.48% | 28.70% | 16.10% | ||||||||||||||||||

| Ratios to average net assetsf | ||||||||||||||||||||||||

Expensesg | 1.03%h | 1.05%h | 1.12%h,i | 1.13%h | 1.10%h | 1.14% | ||||||||||||||||||

Expenses incurred in connection with securities sold short | —% | 0.01% | 0.04% | 0.04% | —%j | 0.01% | ||||||||||||||||||

Net investment income | 1.86% | 2.23%c | 1.45% | 2.84%d | 1.72% | 1.57% | ||||||||||||||||||

| Supplemental data | ||||||||||||||||||||||||

Net assets, end of period (000’s) | $1,000,642 | $992,306 | $1,019,568 | $1,101,706 | $1,148,409 | $983,981 | ||||||||||||||||||

Portfolio turnover rate | 10.39% | 30.94% | 35.80% | 40.06% | 32.95% | 43.23% | ||||||||||||||||||

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.56%.

d Net investment income per share includes approximately $0.24 per share related to income received in the form of a special dividend in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.44%.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gIncludes dividend and/or interest expense on securities sold short and security borrowing fees, if any. See below for the ratios of such expenses to average net assets for the periods presented. See Note 1(d).

hBenefit of expense reduction rounds to less than 0.01%.

iBenefit of waiver and payments by affiliates rounds to less than 0.01%.

jRounds to less than 0.01%.

14 |

Semiannual Report |

The accompanying notes are an integral part of these financial statements. |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

DF I N A N C I A L H I G H L I G H T S

Six Months Ended

June 30, 2017 | Year Ended December 31, | |||||||||||||||||||||||||||

| (unaudited) | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||||||||||

Class C | ||||||||||||||||||||||||||||

| Per share operating performance | ||||||||||||||||||||||||||||

(for a share outstanding throughout the period) | ||||||||||||||||||||||||||||

Net asset value, beginning of period | $15.06 | $14.10 | $16.36 | $16.70 | $13.21 | $11.54 | ||||||||||||||||||||||

Income from investment operationsa: | ||||||||||||||||||||||||||||

Net investment incomeb | 0.09 | 0.22c | 0.12 | 0.37d | 0.15 | 0.11 | ||||||||||||||||||||||

Net realized and unrealized gains (losses) | 1.15 | 1.88 | (0.96) | 0.59 | 3.51 | 1.66 | ||||||||||||||||||||||

Total from investment operations | 1.24 | 2.10 | (0.84) | 0.96 | 3.66 | 1.77 | ||||||||||||||||||||||

Less distributions from: | ||||||||||||||||||||||||||||

Net investment income | — | (0.21) | (0.20) | (0.51) | (0.17) | (0.10) | ||||||||||||||||||||||

Net realized gains | — | (0.93) | (1.22) | (0.79) | — | — | ||||||||||||||||||||||

Total distributions | — | (1.14) | (1.42) | (1.30) | (0.17) | (0.10) | ||||||||||||||||||||||

Net asset value, end of period | $16.30 | $15.06 | $14.10 | $16.36 | $16.70 | $13.21 | ||||||||||||||||||||||

Total returne | 8.23% | 14.94% | (5.06)% | 5.78% | 27.79% | 15.29% | ||||||||||||||||||||||

Ratios to average net assetsf | ||||||||||||||||||||||||||||

Expensesg | 1.78%h | 1.80%h | 1.84%h,i | 1.83%h | 1.80%h | 1.84% | ||||||||||||||||||||||

Expenses incurred in connection with securities sold short | —% | 0.01% | 0.04% | 0.04% | —%j | 0.01% | ||||||||||||||||||||||

Net investment income | 1.11% | 1.48%c | 0.73% | 2.14%d | 1.02% | 0.87% | ||||||||||||||||||||||

| Supplemental data | ||||||||||||||||||||||||||||

Net assets, end of period (000’s) | $271,283 | $275,138 | $285,333 | $320,832 | $336,222 | $295,958 | ||||||||||||||||||||||

Portfolio turnover rate | 10.39% | 30.94% | 35.80% | 40.06% | 32.95% | 43.23% | ||||||||||||||||||||||

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.81%.

dNet investment income per share includes approximately $0.24 per share related to income received in the form of a special dividend in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.74%.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year.

fRatios are annualized for periods less than one year.

gIncludes dividend and/or interest expense on securities sold short and security borrowing fees, if any. See below for the ratios of such expenses to average net assets for the periods presented. See Note 1(d).

hBenefit of expense reduction rounds to less than 0.01%.

iBenefit of waiver and payments by affiliates rounds to less than 0.01%.

jRounds to less than 0.01%.

franklintempleton.com |

The accompanying notes are an integral part of these financial statements. | |

Semiannual Report |

15 |

F R A N K L I N M U T U A L B E A C O N F U N D

F I N A N C I A L H I G H L I G H T S

| Six Months Ended June 30, 2017 | Year Ended December 31, | |||||||||||||||||||||||||||

| (unaudited) | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||||||||||

Class R | ||||||||||||||||||||||||||||

| Per share operating performance | ||||||||||||||||||||||||||||

(for a share outstanding throughout the period) | ||||||||||||||||||||||||||||

Net asset value, beginning of period | $15.01 | $14.05 | $16.33 | $16.68 | $13.19 | $11.52 | ||||||||||||||||||||||

Income from investment operationsa: | ||||||||||||||||||||||||||||

Net investment incomeb | 0.13 | 0.30c | 0.20 | 0.44d | 0.23 | 0.18 | ||||||||||||||||||||||

Net realized and unrealized gains (losses) | 1.14 | 1.89 | (0.97) | 0.61 | 3.50 | 1.66 | ||||||||||||||||||||||

Total from investment operations | 1.27 | 2.19 | (0.77) | 1.05 | 3.73 | 1.84 | ||||||||||||||||||||||

Less distributions from: | ||||||||||||||||||||||||||||

Net investment income | — | (0.30) | (0.29) | (0.61) | (0.24) | (0.17) | ||||||||||||||||||||||

Net realized gains | — | (0.93) | (1.22) | (0.79) | — | — | ||||||||||||||||||||||

Total distributions | — | (1.23) | (1.51) | (1.40) | (0.24) | (0.17) | ||||||||||||||||||||||

Net asset value, end of period | $16.28 | $15.01 | $14.05 | $16.33 | $16.68 | $13.19 | ||||||||||||||||||||||

Total returne | 8.46% | 15.58% | (4.61)% | 6.31% | 28.34% | 15.95% | ||||||||||||||||||||||

Ratios to average net assetsf | ||||||||||||||||||||||||||||

Expensesg | 1.28%h | 1.30%h | 1.34%h,i | 1.33%h | 1.30%h | 1.34% | ||||||||||||||||||||||

Expenses incurred in connection with securities sold short | —% | 0.01% | 0.04% | 0.04% | —%j | 0.01% | ||||||||||||||||||||||

Net investment income | 1.61% | 1.98%c | 1.23% | 2.64%d | 1.52% | 1.37% | ||||||||||||||||||||||

| Supplemental data | ||||||||||||||||||||||||||||

Net assets, end of period (000’s) | $2,162 | $2,035 | $2,343 | $2,246 | $1,956 | $1,905 | ||||||||||||||||||||||

Portfolio turnover rate | 10.39% | 30.94% | 35.80% | 40.06% | 32.95% | 43.23% | ||||||||||||||||||||||

s The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

b Based on average daily shares outstanding.

c Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.31%.

d Net investment income per share includes approximately $0.24 per share related to income received in the form of a special dividend in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.24%.

e Total return is not annualized for periods less than one year.

f Ratios are annualized for periods less than one year.

g Includes dividend and/or interest expense on securities sold short and security borrowing fees, if any. See below for the ratios of such expenses to average net assets for the periods presented. See Note 1(d).

h Benefit of expense reduction rounds to less than 0.01%.

i Benefit of waiver and payments by affiliates rounds to less than 0.01%.

j Rounds to less than 0.01%.

16 |

Semiannual Report |

The accompanying notes are an integral part of these financial statements. |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

F I N A N C I A L H I G H L I G H T S

| Six Months Ended June 30, 2017 | Year Ended December 31, | |||||||||||||||||||

| (unaudited) | 2016 | 2015 | 2014 | 2013a | ||||||||||||||||

Class R6 | ||||||||||||||||||||

| Per share operating performance | ||||||||||||||||||||

(for a share outstanding throughout the period) | ||||||||||||||||||||

Net asset value, beginning of period | $15.30 | $14.30 | $16.58 | $16.88 | $14.77 | |||||||||||||||

Income from investment operationsb: | ||||||||||||||||||||

Net investment incomec | 0.10 | 0.38d | 0.30 | 0.56e | 0.24 | |||||||||||||||

Net realized and unrealized gains (losses) | 1.25 | 1.93 | (0.98) | 0.63 | 2.21 | |||||||||||||||

Total from investment operations | 1.35 | 2.31 | (0.68) | 1.19 | 2.45 | |||||||||||||||

Less distributions from: | ||||||||||||||||||||

Net investment income | — | (0.38) | (0.38) | (0.70) | (0.34) | |||||||||||||||

Net realized gains | — | (0.93) | (1.22) | (0.79) | — | |||||||||||||||

Total distributions | — | (1.31) | (1.60) | (1.49) | (0.34) | |||||||||||||||

Net asset value, end of period | $16.65 | $15.30 | $14.30 | $16.58 | $16.88 | |||||||||||||||

Total returnf | 8.82% | 16.20% | (3.98)% | 6.91% | 16.83% | |||||||||||||||

Ratios to average net assetsg | ||||||||||||||||||||

Expenses before waiver and payments by affiliates and expense reductionh | 0.73% | 0.71% | 0.74% | 0.74% | 2.10% | |||||||||||||||

Expenses net of waiver and payments by affiliates and expense reductionh,i | 0.71% | 0.71% | 0.74%j | 0.74% | 0.71% | |||||||||||||||

Expenses incurred in connection with securities sold short | —% | 0.01% | 0.04% | 0.04% | —%k | |||||||||||||||

Net investment income | 2.18% | 2.57%d | 1.83% | 3.23%e | 2.11% | |||||||||||||||

Supplemental data | ||||||||||||||||||||

Net assets, end of period (000’s) | $741 | $604 | $48,844 | $50,868 | $6 | |||||||||||||||

Portfolio turnover rate | 10.39% | 30.94% | 35.80% | 40.06% | 32.95% | |||||||||||||||

a For the period May 1, 2013 (effective date) to December 31, 2013.

b The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

c Based on average daily shares outstanding.

d Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.90%.

e Net investment income per share includes approximately $0.24 per share related to income received in the form of a special dividend in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.83%.

f Total return is not annualized for periods less than one year.

g Ratios are annualized for periods less than one year.

h Includes dividend and/or interest expense on securities sold short and security borrowing fees, if any. See below for the ratios of such expenses to average net assets for the periods presented. See Note 1(d).

i Benefit of expense reduction rounds to less than 0.01%.

j Benefit of waiver and payments by affiliates rounds to less than 0.01%.

k Rounds to less than 0.01%.

franklintempleton.com |

The accompanying notes are an integral part of these financial statements. | |

Semiannual Report |

17 |

F R A N K L I N M U T U A L B E A C O N F U N D

Statement of Investments, June 30, 2017 (unaudited)

| Country | Shares | Value | ||||||||||||||

|

| |||||||||||||||

Common Stocks and Other Equity Interests 84.9% | ||||||||||||||||

Aerospace & Defense 2.9% | ||||||||||||||||

| a | KLX Inc. | United States | 2,360,689 | $ | 118,034,450 | |||||||||||

|

| |||||||||||||||

Auto Components 0.4% | ||||||||||||||||

| a,b | International Automotive Components Group Brazil LLC | Brazil | 2,846,329 | 69,618 | ||||||||||||

| a,b,c | International Automotive Components Group North America LLC | United States | 22,836,904 | 14,056,480 | ||||||||||||

|

| |||||||||||||||

| 14,126,098 | ||||||||||||||||

|

| |||||||||||||||

Banks 10.0% | ||||||||||||||||

JPMorgan Chase & Co. | United States | 1,337,400 | 122,238,360 | |||||||||||||

Societe Generale SA | France | 2,284,180 | 122,914,917 | |||||||||||||

| a | Standard Chartered PLC | United Kingdom | 4,695,355 | 47,533,047 | ||||||||||||

Wells Fargo & Co. | United States | 2,016,650 | 111,742,576 | |||||||||||||

|

| |||||||||||||||

| 404,428,900 | ||||||||||||||||

|

| |||||||||||||||

Chemicals 1.2% | ||||||||||||||||

| a, | d,e | Dow Corning Corp., Contingent Distribution | United States | 12,598,548 | — | |||||||||||

Monsanto Co. | United States | 409,620 | 48,482,623 | |||||||||||||

|

| |||||||||||||||

| 48,482,623 | ||||||||||||||||

|

| |||||||||||||||

Communications Equipment 4.3% | ||||||||||||||||

Cisco Systems Inc. | United States | 2,338,442 | 73,193,235 | |||||||||||||

Nokia OYJ, ADR | Finland | 16,607,263 | 102,300,740 | |||||||||||||

|

| |||||||||||||||

| 175,493,975 | ||||||||||||||||

|

| |||||||||||||||

Consumer Finance 2.9% | ||||||||||||||||

Capital One Financial Corp. | United States | 1,419,398 | 117,270,663 | |||||||||||||

|

| |||||||||||||||

Diversified Telecommunication Services 3.4% | ||||||||||||||||

Koninklijke KPN NV | Netherlands | 42,357,350 | 135,519,894 | |||||||||||||

|

| |||||||||||||||

Electrical Equipment 3.2% | ||||||||||||||||

| a | Sensata Technologies Holding NV | United States | 3,037,386 | 129,757,130 | ||||||||||||

|

| |||||||||||||||

Food & Staples Retailing 2.8% | ||||||||||||||||

| a | Rite Aid Corp. | United States | 6,467,611 | 19,079,452 | ||||||||||||

Walgreens Boots Alliance Inc. | United States | 1,177,451 | 92,206,188 | |||||||||||||

|

| |||||||||||||||

| 111,285,640 | ||||||||||||||||

|

| |||||||||||||||

Health Care Equipment & Supplies 5.1% | ||||||||||||||||

Medtronic PLC | United States | 1,649,990 | 146,436,613 | |||||||||||||

Stryker Corp. | United States | 435,540 | 60,444,241 | |||||||||||||

|

| |||||||||||||||

| 206,880,854 | ||||||||||||||||

|

| |||||||||||||||

Hotels, Restaurants & Leisure 2.7% | ||||||||||||||||

Accor SA | France | 2,335,910 | 109,515,989 | |||||||||||||

|

| |||||||||||||||

Independent Power & Renewable Electricity Producers 0.5% | ||||||||||||||||

Vistra Energy Corp. | United States | 1,256,451 | 21,095,812 | |||||||||||||

|

| |||||||||||||||

Insurance 1.4% | ||||||||||||||||

White Mountains Insurance Group Ltd | United States | 65,148 | 56,589,507 | |||||||||||||

|

| |||||||||||||||

Internet Software & Services 1.5% | ||||||||||||||||

| a | Baidu Inc., ADR. | China | 344,487 | 61,614,945 | ||||||||||||

|

| |||||||||||||||

IT Services 2.4% | ||||||||||||||||

Cognizant Technology Solutions Corp., A | United States | 1,437,830 | 95,471,912 | |||||||||||||

|

| |||||||||||||||

Media 7.7% | ||||||||||||||||

| a | Charter Communications Inc., A | United States | 239,187 | 80,570,141 | ||||||||||||

| a | DISH Network Corp., A | United States | 709,941 | 44,555,897 | ||||||||||||

Sky PLC | United Kingdom | 4,052,422 | 52,468,117 | |||||||||||||

18 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

S T A T E M E N T O F I N V E S T M E N T S (U N A U D I T E D)

| Country | Shares | Value | ||||||||||||

| ||||||||||||||

Common Stocks and Other Equity Interests (continued) | ||||||||||||||

Media (continued) | ||||||||||||||

Time Warner Inc. | United States | 1,351,872 | $ | 135,741,468 | ||||||||||

|

| |||||||||||||

| 313,335,623 | ||||||||||||||

|

| |||||||||||||

Metals & Mining 0.1% | ||||||||||||||

b,c | Warrior Met Coal Inc. | United States | 301,445 | 4,931,343 | ||||||||||

|

| |||||||||||||

Oil, Gas & Consumable Fuels 5.7% | ||||||||||||||

Marathon Oil Corp. | United States | 5,097,161 | 60,401,358 | |||||||||||

Royal Dutch Shell PLC, B | United Kingdom | 2,384,850 | 64,069,223 | |||||||||||

The Williams Cos. Inc. | United States | 3,549,332 | 107,473,773 | |||||||||||

|

| |||||||||||||

| 231,944,354 | ||||||||||||||

|

| |||||||||||||

Pharmaceuticals 12.0% | ||||||||||||||

Eli Lilly & Co. | United States | 1,203,639 | 99,059,490 | |||||||||||

GlaxoSmithKline PLC | United Kingdom | 2,900,817 | 61,796,704 | |||||||||||

Merck & Co. Inc. | United States | 1,764,077 | 113,059,695 | |||||||||||

Novartis AG, ADR | Switzerland | 1,728,690 | 144,293,754 | |||||||||||

Teva Pharmaceutical Industries Ltd., ADR | Israel | 2,022,480 | 67,186,785 | |||||||||||

|

| |||||||||||||

| 485,396,428 | ||||||||||||||

|

| |||||||||||||

Software 8.7% | ||||||||||||||

CA Inc. | United States | 1,812,066 | 62,461,915 | |||||||||||

a | Check Point Software Technologies Ltd. | Israel | 816,412 | 89,054,221 | ||||||||||

Microsoft Corp. | United States | 1,303,159 | 89,826,750 | |||||||||||

Symantec Corp. | United States | 3,943,254 | 111,396,925 | |||||||||||

|

| |||||||||||||

| 352,739,811 | ||||||||||||||

|

| |||||||||||||

Tobacco 3.1% | ||||||||||||||

British American Tobacco PLC | United Kingdom | 1,808,426 | 123,290,295 | |||||||||||

|

| |||||||||||||

Wireless Telecommunication Services 2.9% | ||||||||||||||

Vodafone Group PLC | United Kingdom | 41,827,469 | 118,635,367 | |||||||||||

|

| |||||||||||||

Total Common Stocks and Other Equity Interests (Cost $2,645,410,135) | 3,435,841,613 | |||||||||||||

|

| |||||||||||||

Preferred Stocks 5.2% | ||||||||||||||

Automobiles 2.5% | ||||||||||||||

f | Porsche Automobil Holding SE, 2.053%, pfd | Germany | 1,831,012 | 102,879,578 | ||||||||||

|

| |||||||||||||

Technology Hardware, Storage & Peripherals 2.7% | ||||||||||||||

f | Samsung Electronics Co. Ltd., 1.909%, pfd | South Korea | 66,285 | 107,799,315 | ||||||||||

|

| |||||||||||||

Total Preferred Stocks (Cost $147,563,120) | 210,678,893 | |||||||||||||

|

| |||||||||||||

| Principal Amount | ||||||||||||||

Corporate Notes and Senior Floating Rate Interests 1.8% | ||||||||||||||

g,h | Cumulus Media Holdings Inc., Term Loans, 4.48%, 12/23/20 | United States | $ | 15,063,918 | 12,182,943 | |||||||||

Frontier Communications Corp., | ||||||||||||||

senior note, 10.50%, 9/15/22 | United States | 2,650,000 | 2,534,062 | |||||||||||

senior note, 11.00%, 9/15/25 | United States | 23,907,000 | 22,143,859 | |||||||||||

iHeartCommunications Inc., | ||||||||||||||

senior secured note, first lien, 9.00%, 12/15/19 | United States | 18,873,000 | 14,886,079 | |||||||||||

g,h Tranche D Term Loan, 7.976%, 1/30/19 | United States | 15,813,483 | 12,967,056 | |||||||||||

g,h Tranche E Term Loan, 8.726%, 7/30/19 | United States | 5,080,935 | 4,166,367 | |||||||||||

franklintempleton.com |

Semiannual Report |

19 |

F R A N K L I N M U T U A L B E A C O N F U N D

S T A T E M E N T O F I N V E S T M E N T S ( U N A U D I T E D )

| Country | Principal Amount | Value | ||||||||||

| ||||||||||||

Corporate Notes and Senior Floating Rate Interests (continued) | ||||||||||||

iVeritas U.S. Inc./Veritas Bermuda Ltd., senior note, 144A, 7.50%, 2/01/23 | United States | $ | 2,112,000 | $ | 2,275,680 | |||||||

|

| |||||||||||

Total Corporate Notes and Senior Floating Rate Interests | 71,156,046 | |||||||||||

|

| |||||||||||

Corporate Notes and Senior Floating Rate Interests in | ||||||||||||

b,jBroadband Ventures III LLC, secured promissory note, 5.00%, 2/01/12 | United States | 10,848 | — | |||||||||

g,h,jCaesars Entertainment Operating Co. Inc., | ||||||||||||

Term B-5-B Loans, 1.50%, 3/01/17 | United States | 7,504,361 | 8,733,200 | |||||||||

Term B-6-B Loans, 1.50%, 3/01/17 | United States | 31,654,839 | 37,708,827 | |||||||||

Term B-7 Loans, 1.50%, 3/01/17 | United States | 10,119,494 | 12,611,420 | |||||||||

|

| |||||||||||

Total Corporate Notes and Senior Floating Rate Interests in | 59,053,447 | |||||||||||

|

| |||||||||||

| Shares | ||||||||||||

Companies in Liquidation 0.1% | ||||||||||||

aAdelphia Recovery Trust | United States | 48,268,724 | 31,375 | |||||||||

a,dAdelphia Recovery Trust, Arahova Contingent Value Vehicle, Contingent Distribution | United States | 6,161,087 | 616 | |||||||||

a,b,c,kCB FIM Coinvestors LLC | United States | 15,831,950 | — | |||||||||

a,d,eCentury Communications Corp., Contingent Distribution | United States | 16,986,000 | — | |||||||||

a,bFIM Coinvestor Holdings I, LLC | United States | 19,805,560 | — | |||||||||

a,lLehman Brothers Holdings Inc., Bankruptcy Claim | United States | 163,140,446 | 3,621,718 | |||||||||

a,d,eTribune Media, Litigation Trust, Contingent Distribution | United States | 497,438 | — | |||||||||

a,eVistra Energy Corp., Litigation Trust | United States | 74,588,735 | 865,230 | |||||||||

aVistra Energy Corp., Litigation Trust, TRA | United States | 1,256,451 | 1,350,684 | |||||||||

|

| |||||||||||

Total Companies in Liquidation (Cost $21,511,636) | 5,869,623 | |||||||||||

|

| |||||||||||

| Principal Amount | ||||||||||||

Municipal Bonds in Reorganization (Cost $14,893,535) 0.2% | ||||||||||||

j Puerto Rico Commonwealth GO, Refunding, Series A, 8.00%, 7/01/35 | United States | $ | 17,038,000 | 10,393,180 | ||||||||

|

| |||||||||||

Total Investments before Short Term Investments | 3,792,992,802 | |||||||||||

|

| |||||||||||

Short Term Investments 6.7% | ||||||||||||

U.S. Government and Agency Securities 6.7% | ||||||||||||

mFHLB, | ||||||||||||

7/03/17 | United States | 66,100,000 | 66,100,000 | |||||||||

7/05/17 | United States | 12,000,000 | 11,999,340 | |||||||||

mU.S. Treasury Bill, | ||||||||||||

n 8/31/17 - 9/07/17 | United States | 30,000,000 | 29,952,590 | |||||||||

7/20/17 - 12/21/17 | United States | 163,000,000 | 162,593,419 | |||||||||

|

| |||||||||||

Total U.S. Government and Agency Securities | 270,645,349 | |||||||||||

|

| |||||||||||

Total Investments (Cost $3,223,731,838) 100.4% | 4,063,638,151 | |||||||||||

Other Assets, less Liabilities (0.4)% | (16,217,571 | ) | ||||||||||

|

| |||||||||||

Net Assets 100.0% | $ | 4,047,420,580 | ||||||||||

|

| |||||||||||

20 |

Semiannual Report |

franklintempleton.com |

F R A N K L I N M U T U A L B E A C O N F U N D

S T A T E M E N T O F I N V E S T M E N T S ( U N A U D I T E D )

aNon-income producing.

bSee Note 10 regarding restricted securities.

cAt June 30, 2017, pursuant to the Fund’s policies and the requirements of applicable securities law, the Fund is restricted from trading these securities at period end.

dContingent distributions represent the right to receive additional distributions, if any, during the reorganization of the underlying company. Shares represent total underlying principal of debt securities.

eSecurity has been deemed illiquid because it may not be able to be sold within seven days. At June 30, 2017, the aggregate value of these securities was $865,230, representing less than 0.1% of net assets.

fVariable rate security. The rate shown represents the yield at period end.

gThe coupon rate shown represents the rate at period end.

hSee Note 1(e) regarding senior floating rate interests.

iSecurity was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers or in a public offering registered under the Securities Act of 1933. This security has been deemed liquid under guidelines approved by the Trust’s Board of Trustees. At June 30, 2017, the value of this security was $2,275,680, representing 0.1% of net assets.

jSee Note 8 regarding credit risk and defaulted securities.

kSee Note 12 regarding holdings of 5% voting securities.

lBankruptcy claims represent the right to receive distributions, if any, during the liquidation of the underlying pool of assets. Shares represent amount of allowed unsecured claims.

mThe security was issued on a discount basis with no stated coupon rate.

nA portion or all of the security has been segregated as collateral for open forward contracts. At June 30, 2017, the aggregate value of these securities and/or cash pledged amounted to $25,024,031, representing 0.6% of net assets.

franklintempleton.com |

Semiannual Report |

21 |

F R A N K L I N M U T U A L B E A C O N F U N D

S T A T E M E N T O F I N V E S T M E N T S ( U N A U D I T E D )

At June 30, 2017, the Fund had the following futures contracts outstanding. See Note 1(c).

Futures Contracts

| Description | Type | Number of Contracts | Notional Value | Expiration Date | Unrealized Appreciation | Unrealized Depreciation | ||||||||||||||||||

| ||||||||||||||||||||||||

| Currency Contracts | ||||||||||||||||||||||||

EUR/USD | Short | 1,210 | $ | 173,438,375 | 9/18/17 | $ — | $ | (3,035,891 | ) | |||||||||||||||

GBP/USD | Short | 1,648 | 134,363,500 | 9/18/17 | — | (2,736,471 | ) | |||||||||||||||||

|

| |||||||||||||||||||||||

Total Futures Contracts | $ — | $ | (5,772,362 | ) | ||||||||||||||||||||

|

| |||||||||||||||||||||||