UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05407

Trust for Credit Unions

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street, 3rd Floor

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Jay E. Johnson

Callahan Financial Services, Inc.

1001 Connecticut Avenue NW, Suite 1001

Washington, DC 20036

(Name and address of agent for service)

With Copies To:

Andrew E. Seaberg

Faegre Drinker Biddle & Reath LLP

One Logan Square, Suite 2000

Philadelphia, PA 19103

Registrant's telephone number, including area code: 1-800-342-5828

Date of fiscal year end: August 31

Date of reporting period: August 31, 2022

Item 1. Reports to Stockholders.

| (a) |

Ultra-Short Duration Portfolio

Short Duration Portfolio

Annual Report

August 31, 2022

The reports concerning the Trust for Credit Unions (“TCU” or the “Trust”) Ultra-Short Duration Portfolio and Short Duration Portfolio (each a “Portfolio” and together the “Portfolios”) included in this shareholder report may contain certain forward-looking statements about the factors that may affect the performance of the Portfolios in the future. These statements are based on Portfolio management’s predictions and expectations concerning certain future events and their expected impact on the Portfolios, such as performance of the economy as a whole and of specific industry sectors, changes in the levels of interest rates, the impact of developing world events, and other factors that may influence the future performance of the Portfolios. Management believes these forward-looking statements to be reasonable, although they are inherently uncertain and difficult to predict. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed.

TCU files the complete schedule of portfolio holdings of each Portfolio with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-PORT. The Portfolios’ Forms N-PORT are available on the SEC’s website at http://www.sec.gov.

Information regarding how the Portfolios voted proxies relating to portfolio securities, if any, during the most recent 12-month period ended June 30 is available by August 31 of the relevant year: (i) without charge, upon request, by calling the Trust at 1-800-342-5828; and (ii) on the SEC’s website at http://www.sec.gov.

An investment in a TCU Portfolio is not a credit union deposit and is not insured or guaranteed by the National Credit Union Share Insurance Fund, the National Credit Union Administration, or any other government agency.

The TCU Ultra-Short Duration Portfolio and the TCU Short Duration Portfolio are not money market funds. Investors in these Portfolios should understand that the net asset values of the Portfolios will fluctuate, which may result in a loss of the principal amount invested. The Portfolios’ net asset values and yields are not guaranteed by the U.S. government or by its agencies, instrumentalities or sponsored enterprises. Investments in fixed income securities are subject to the risks associated with debt securities including credit and interest rate risk. The guarantee on U.S. government securities applies only to the underlying securities of the Portfolios if held to maturity and not to the value of the Portfolios’ shares. The Portfolios’ investments in mortgage-backed securities are subject to prepayment risks. These risks may result in greater share price volatility.

Holdings and allocations shown may not be representative of current or future investments. Portfolio holdings should not be relied on in making investment decisions and should not be construed as research or investment advice regarding particular securities.

This material is not authorized for distribution unless preceded or accompanied by a current Prospectus. Investors should consider a Portfolio’s objectives, risks, and charges and expenses, and read the Prospectus carefully before investing or sending money. The Prospectus contains this and other information about the Portfolios.

Callahan Financial Services, Inc. is the distributor of the TCU Portfolios.

This report is for the information of the shareholders of the Trust.

Its use in connection with any offering of shares of the Trust is

authorized only in the case of a concurrent or prior delivery of

the Trust’s current Prospectus.

Dear Credit Union Shareholders,

The difference in the economic environment and credit union performance dynamics at August 31, 2022 versus a year ago is striking. Inflation is the headline issue in 2022, and the Federal Reserve shifted significantly from their position a year ago that inflation was “transitory” by implementing interest rate increases at the fastest pace since the 1980s. Inflation as measured by the consumer price index might have peaked in June at 9.0% but the 12-month increase of 8.2% as of September remains well above the Fed’s target level of 2.0%. As a result, the rate increases are not finished, with the Fed projecting another 1.25 percentage point increase by year-end and more increases projected in 2023.

Similar to the change in the interest rate environment, credit union balance sheet growth dynamics have flipped in 2022 as compared to the prior year. Share growth was the story a year ago but the annual growth rate of 8.1% as of June 2022 is almost half of the 15% rate posted in June 2021. Loan growth has now taken the lead, with a 16.1% annual growth rate as of June that is not only more than triple the 4.9% rate posted a year ago, but the highest in decades. As a result, the industry’s loan-to-share ratio recorded the highest quarterly increase ever in the second quarter, jumping 4.5 percentage points to 74.7% as of June 30th.

Although the industry’s loan-to-share ratio is moving up, the current level would not typically indicate any liquidity concerns. However, the rapid increase in interest rates has resulted in a significant rise in unrealized losses in credit unions’ investment portfolios. Since credit unions prefer to hold investments until maturity, most of these losses will never be realized. The situation does constrain Chief Financial Officers though, who would rather tap into other sources of liquidity before selling securities and having to recognize a loss.

In this environment, the ability of investors in the Trust for Credit Unions (“TCU”) portfolios to access funds on a next-day basis is a significant value. Over the past few years, the TCU funds have demonstrated their value to credit unions by serving the exact purpose they are designed for – a source of returns when liquidity is high, as it was during the deposit surge tied to stimulus inflows and slower consumer spending in 2020 and 2021, and a source of liquid funds when lending picks up and share growth slows, as has happened over the past year.

As a result of credit unions’ need for liquidity to fund loan demand, combined balances in the Ultra-Short Duration and Short Duration portfolios declined over the past fiscal year from $4.8 billion to $1.0 billion. This is a reversal of the trends recorded in the fiscal year ended August 31st 2021 when balances rose 95%, underscoring TCU’s role as conditions in credit unions change.

The rapid rise in interest rates resulted in negative returns in most fixed income securities, as reflected in TCU’s performance results. For the twelve-month period ended August 31, 2022, the cumulative total return of the TCU share class of the Ultra-Short Duration Portfolio (TCU Shares) was -1.93% versus a cumulative total return of the Portfolio’s benchmark, the ICE BofAML Three-Month U.S. Treasury Bill Index, of 0.38%. Over the same period, the TCU share class of the Short Duration Portfolio (TCU Shares) was -5.40% versus a -4.09% cumulative total return for the ICE BofAML Two-Year U.S. Treasury Note Index (Including Transaction Costs). The Investment Adviser’s Discussion and Analysis in this report provides perspective from ALM First on the positioning of the TCU portfolios. Please refer to their discussion for more information.

In an environment that continues to shift, ensuring investors have the most current information available is one of the key value components of TCU. Please visit our website, www.TrustCU.com, for the most current information on the Portfolios, including performance and portfolio holdings. We also regularly host webinars in which ALM First discusses the current market environment and provides an update on TCU portfolio performance and positioning. Please check the website for the next scheduled date. Of course, we are also available to connect with by calling 800-237-5678.

TCU is a unique operation, led by and for credit unions. The credit unions in the Callahan Credit Union Financial Services LLLP partnership continue to provide important support of and market perspective to TCU. Our business partners, including ALM First, U.S. Bank Global Fund Services, Callahan Financial Services and Eascorp, work together to ensure our investors receive outstanding service. The TCU Board of Trustees provide oversight and guidance for this collaboration. They each are important contributors to TCU’s success over the past 35 years.

Thank you, our credit union shareholders, for your interest in and support of TCU. If you have any questions or suggestions, please reach out to our team.

Sincerely,

Jay E. Johnson

President and Treasurer

Trust for Credit Unions

1

INVESTMENT ADVISER’S DISCUSSION AND ANALYSIS

TCU ULTRA-SHORT DURATION PORTFOLIO

Investment Objective

The TCU Ultra-Short Duration Portfolio (“USDP” or the “Portfolio”) seeks to achieve a high level of current income, consistent with low volatility of principal, by investing in obligations authorized under the Federal Credit Union Act. Under normal circumstances, substantially all of the assets (and at least 80%, measured at the time of purchase) of USDP will be invested in fixed-income securities consisting of the following: (1) securities issued or guaranteed as to principal and interest by the U.S. government or by its agencies, instrumentalities or sponsored enterprises and related custodial receipts; (2) repurchase agreements secured with obligations authorized by the Federal Credit Union Act; and (3) U.S. dollar denominated bank notes issued or guaranteed by banks with total assets exceeding $1 billion with weighted average maturities of less than 5 years, but only to the extent permitted under the Federal Credit Union Act and the rules and regulations thereunder. The Portfolio expects that a substantial portion of these securities will be mortgage-related securities. The Portfolio may also invest in non-U.S. government related securities, including bank notes and repurchase agreements secured by non-U.S. government related collateral. While there will be fluctuations in the net asset value (“NAV”) of the USDP, the Portfolio is expected to have less interest rate risk and asset value fluctuation than funds investing primarily in longer-term mortgage-backed securities paying a fixed rate of interest. An investment in the Portfolio is neither insured nor guaranteed by the U.S. government. USDP invests in obligations authorized under the Federal Credit Union Act with a maximum portfolio duration not to exceed that of a One-Year U.S. Treasury Security and a target duration equal to that of its benchmark, the ICE BofAML Three-Month U.S. Treasury Note Index.

Portfolio Management Discussion and Analysis

Below, ALM First discusses the Portfolio’s performance and positioning for the Reporting Period.

Q. How did the Portfolio perform during the Reporting Period?

For the twelve-month period ended August 31, 2022, the cumulative total return of USDP TCU Shares was -1.93% versus a 0.38% cumulative total return of the Portfolio’s benchmark, the ICE BofAML Three-Month U.S. Treasury Bill Index (the “Index”). The Portfolio’s net asset value (“NAV”) per share at the end of the Reporting Period was $9.21, versus $9.40 on February 28, 2022.

Q. What key factors were responsible for the Portfolio’s performance during the Reporting Period?

2022 has seen high credit quality fixed income spreads widen substantially, and floating-rate securities were no exception. Floating-rate Agency Commercial-Backed Securities (“ACMBS”) and Home Equity Conversion Mortgages (“HECMs”) have seen their spreads hit the wide end of their respective historical ranges. These securities exhibit little interest rate risk but are sensitive to changes in spreads which has led to underperformance relative to the index.

Q. Which fixed income market sectors most significantly affected Portfolio performance?

As discussed above spreads on floating-rate ACMBS, HECMs, and Collateralized Mortgage Obligations (“CMOs”) widened over the period and led to the Portfolio underperforming relative to its benchmark as increasing spreads led to a larger price decline than can be attributed to the change in rates alone.

Q. Did the Portfolio’s duration and yield curve positioning strategy help or hurt its results during the Reporting Period?

Since ALM First keeps the duration of the Portfolio aligned with that of the Index to avoid taking a position on the direction of interest rates, the Portfolio’s duration neither helped nor hurt its performance.

Q. Were there any notable changes in the Portfolio’s weightings during the Reporting Period?

The allocation to short-term Treasury securities increased from zero to 20% of portfolio assets over the period. The allocation to repurchase agreements declined significantly as the period progressed amid heavier redemption activity.

Q. How was the Portfolio positioned relative to its benchmark index at the end of August 2022?

At the end of the Reporting Period, the Portfolio’s largest allocations were in Agency Mortgage-Related Securities, which the Index has no allocation to since the Index is made up only of U.S. Treasury securities.

Past performance does not guarantee future results, which may vary.

There is no guarantee that these objectives will be met.

Portfolio holdings and/or allocations shown above are as of the date indicated and may not be representative of future investments. The holdings and/or allocations shown may not represent all of the Portfolio’s investments. Future investments may or may not be profitable.

2

THIS PAGE LEFT INTENTIONALLY BLANK

3

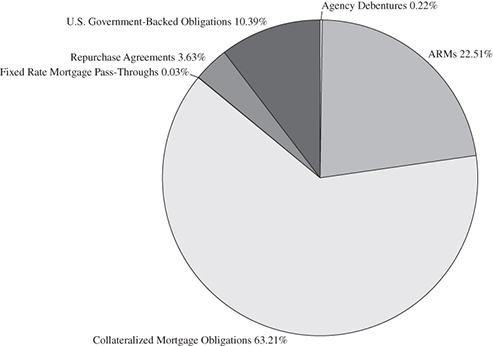

PORTFOLIO COMPOSITION—SECTOR ALLOCATION

TCU ULTRA-SHORT DURATION PORTFOLIO (Unaudited)

August 31, 2022*

August 31, 2021*

4

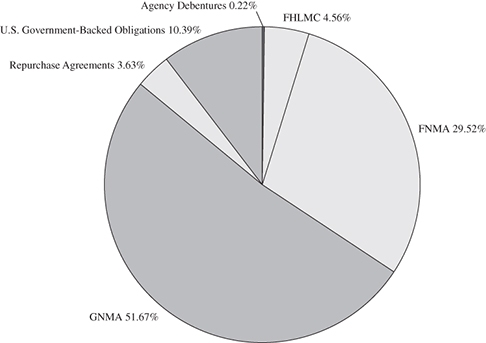

PORTFOLIO COMPOSITION—ISSUER ALLOCATION

TCU ULTRA-SHORT DURATION PORTFOLIO (Unaudited)

August 31, 2022*

August 31, 2021*

| * | These percentages reflect Portfolio holdings as a percentage of net assets. Figures in the above charts may not sum to 100% due to the exclusion of other assets and liabilities, including cash. Holdings and allocations may not be representative of current or future investments. Holdings and allocations may not include the Portfolio’s entire investment portfolio, which may change at any time. Portfolio holdings should not be relied on in making investment decisions and should not be construed as research or investment advice regarding particular securities. |

5

INVESTMENT ADVISER’S DISCUSSION AND ANALYSIS

TCU SHORT DURATION PORTFOLIO

Investment Objective

The TCU Short Duration Portfolio (“SDP” or the “Portfolio”) seeks to achieve a high level of current income, consistent with relatively low volatility of principal, by investing in obligations authorized under the Federal Credit Union Act. During normal market conditions, SDP intends to invest a substantial portion of its assets in mortgage-related securities, which include mortgage-related securities issued or guaranteed by the U.S. government, its agencies, instrumentalities or sponsored enterprises. Mortgage-related securities held by SDP may include adjustable rate and fixed rate mortgage pass-through securities, collateralized mortgage obligations and other multi-class mortgage-related securities, as well as other securities that are collateralized by or represent direct or indirect interests in mortgage-related securities or mortgage loans. An investment in the Portfolio is neither insured nor guaranteed by the U.S. government. SDP invests in obligations authorized under the Federal Credit Union Act with a target duration that is equal to that of the ICE BofAML Two-Year U.S. Treasury Note Index and its maximum duration is that of a Three-Year U.S. Treasury Security.

Portfolio Management Discussion and Analysis

Below, ALM First discusses the Portfolio’s performance and positioning for the Reporting Period.

Q. How did the Portfolio perform during the Reporting Period?

The Portfolio’s cumulative total return for the twelve-month period ended August 31, 2022 was -5.40% for the TCU shares, versus a -4.09% cumulative total return for the ICE BofAML Two-Year U.S. Treasury Note Index (Including Transaction Costs) (the “Index”). The Portfolio’s net asset value per share closed the Reporting Period at $9.22, versus $9.62 on February 28, 2022.

Q. What key factors were responsible for the Portfolio’s performance during the Reporting Period?

During the twelve-month period ended August 31, 2022 the yield curve flattened by 140 basis points, with the spread between the 2-year and 10-year Treasuries decreasing to -30 basis points from 110 basis points. Additionally, the yield curve shifted higher, the 2-year yield increased by 328 basis points while the 10-year yield ended the period 188 basis points higher.

Wider spreads and higher levels of interest rate volatility also impacted the portfolio. Agency Mortgage-Backed Securities (“MBS”), Agency Commercial Backed Securities (“ACMBS”) both experienced spread widening over the period. Additionally, higher levels of interest rate volatility had a negative impact on the price of securities with embedded options such as MBS.

Q. Which fixed income market sectors most significantly affected Portfolio performance?

Wider spreads on MBS and ACMBS had a negative impact on the Portfolio’s performance relative to its benchmark. Additionally, higher levels of interest rate volatility put downward pressure on MBS valuations due to the options embedded within those securities.

Q. Did the Portfolio’s duration and yield curve positioning strategy help or hurt its results during the Reporting Period?

Since ALM First keeps the duration of the Portfolio aligned with that of the Index to avoid taking a position on the direction of interest rates, the Portfolio’s duration neither helped nor hurt its performance. Unlike the benchmark which is sensitive only to changes in 2-year rates, the Portfolio has exposure to the entire yield curve and with long-end rates increasing less than the 2-year, the Portfolio was able to avoid some of that impact.

Q. Were there any notable changes in the Portfolio’s weightings during the Reporting Period?

No.

Q. How was the Portfolio positioned at the end of August 2022?

At the end of the Reporting Period, the Portfolio’s largest allocations were in Agency MBS securities, which the Index has no allocation to since the index is made up only of US Treasury securities.

Past performance does not guarantee future results, which may vary.

There is no guarantee that these objectives will be met.

Portfolio holdings and/or allocations shown above are as of the date indicated and may not be representative of future investments. The holdings and/or allocations shown may not represent all of the Portfolio’s investments. Future investments may or may not be profitable.

6

THIS PAGE LEFT INTENTIONALLY BLANK

7

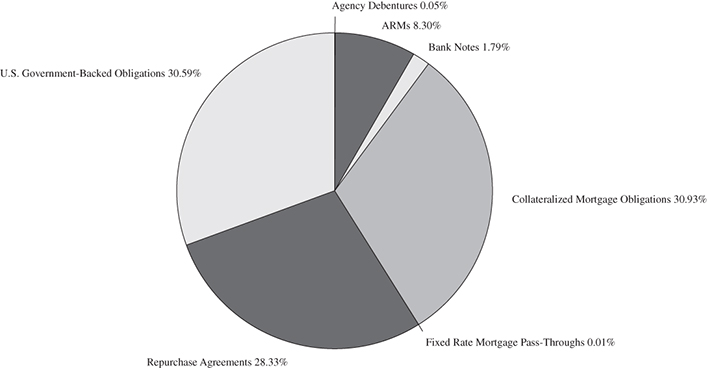

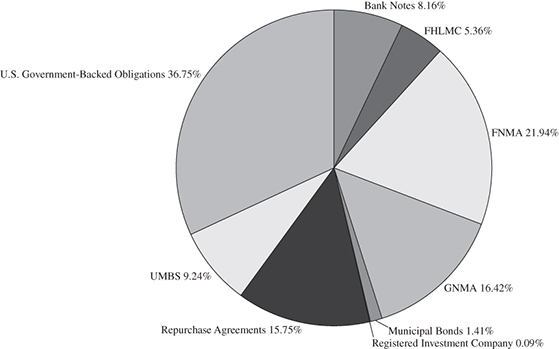

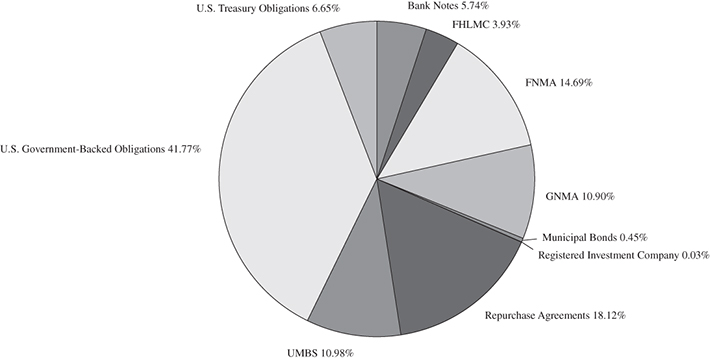

PORTFOLIO COMPOSITION—SECTOR ALLOCATION

TCU SHORT DURATION PORTFOLIO (Unaudited)

August 31, 2022*

August 31, 2021*

8

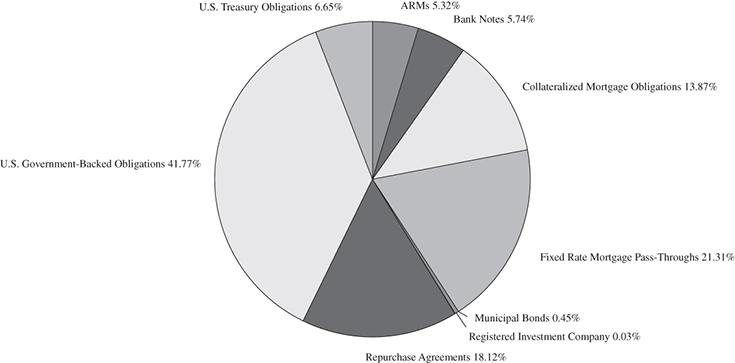

PORTFOLIO COMPOSITION—ISSUER ALLOCATION

TCU SHORT DURATION PORTFOLIO (Unaudited)

August 31, 2022*

August 31, 2021*

| * | These percentages reflect Portfolio holdings as a percentage of net assets. Figures in the above charts may not sum to 100% due to the exclusion of other assets and liabilities, including cash. Holdings and allocations may not be representative of current or future investments. Holdings and allocations may not include the Portfolio’s entire investment portfolio, which may change at any time. Portfolio holdings should not be relied on in making investment decisions and should not be construed as research or investment advice regarding particular securities. |

9

PORTFOLIO COMPARISON

TCU ULTRA-SHORT DURATION PORTFOLIO (Unaudited)

In accordance with the requirements of the Securities and Exchange Commission, the following data for the Ultra-Short Duration Portfolio is supplied for the period ended August 31, 2022. The Portfolio is compared to its benchmarks assuming the following initial investment:

| Initial | ||

Portfolio | Investment | Compare to: |

| Ultra-Short Duration (“USDP”) | $10,000 | ICE BofAML 3-Month U.S. Treasury Bill Index (“3-Month T-Bill”); |

| ICE BofAML 6-Month U.S. Treasury Bill Index (“6-Month T-Bill”). |

Ultra-Short Duration Portfolio’s(1) TCU Shares 10 Year Performance

Average Annual Total Return(a) | ||||

| One Year | Five Year | Ten Year | Since Inception | |

| TCU Shares | -1.93% | 0.71% | 0.46% | 2.43%(b) |

| Investor Shares | -1.96% | 0.68% | — | 0.43%(c) |

| 3-Month T-Bill (Performance since August 1, 1991) | 0.38% | 1.12% | 0.66% | 2.47% |

(1) | The Portfolio changed its investment strategy effective December 31, 2018. Information for periods prior to December 31, 2018 does not reflect the current investment strategy. |

(a) | ALM First began serving as investment adviser on April 16, 2017. Prior to that date, the Portfolio was advised by a different investment adviser. Performance of the Portfolio for periods prior to April 16, 2017 reflect management of the Portfolio by the previous investment adviser. |

(b) | The Portfolio’s TCU Shares commenced operations on July 10, 1991. |

(c) | The Portfolio’s Investor Shares commenced operations on November 30, 2012. |

The ICE BofAML Three-Month U.S. Treasury Bill Index and the ICE BofAML Six-Month U.S. Treasury Bill Index do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The TCU Ultra-Short Duration Portfolio is not a money market fund. Investors in this Portfolio should understand that the net asset value of the Portfolio will fluctuate, which may result in a loss of the principal amount invested. The Portfolio’s net asset value and yield are not guaranteed by the U.S. government, the National Credit Union Administration, or any other U.S. government agency, instrumentality or sponsored enterprise. Investments in fixed income securities are subject to the risks associated with debt securities including credit and interest rate risk. The guarantee on U.S. government securities applies only to the underlying securities of the Portfolio if held to maturity and not to the value of the Portfolio’s shares. The Portfolio’s investments in mortgage-backed securities are subject to prepayment risks. These risks may result in greater share price volatility.

All performance data shown represents past performance and should not be considered indicative of future performance, which will fluctuate as market conditions change. The investment return and principal value of an investment will fluctuate with changes in market conditions so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The chart and table above assume reinvestment of dividends and distributions. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. In addition to the investment adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect portfolio performance. These factors include, but are not limited to, portfolio operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting a portfolio. Please call 1-800-342-5828 or 1-800-CFS-5678 for the most recent month-end returns.

10

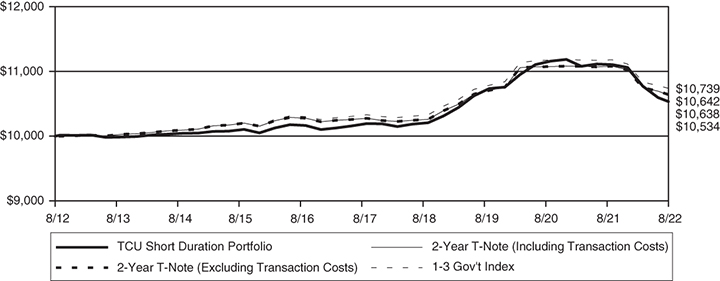

PORTFOLIO COMPARISON

TCU SHORT DURATION PORTFOLIO (Unaudited)

In accordance with the requirements of the Securities and Exchange Commission, the following data for the Short Duration Portfolio is supplied for the period ended August 31, 2022. The Portfolio is compared to its benchmarks assuming the following initial investment:

| Initial | ||

Portfolio | Investment | Compare to: |

| Short Duration (“SDP”) | $10,000 | ICE BofAML 2-Year U.S. Treasury Note Index (Including Transaction Costs) (“2-Year T-Note”); |

| ICE BofAML 2-Year U.S. Treasury Note Index (Excluding Transaction Costs) (“2-Year T-Note”); | ||

| Bloomberg Barclays Mutual Fund Short (1-3 Year) Government Index (“1-3 Gov’t Index”). |

Short Duration Portfolio’s TCU Shares 10 Year Performance

Average Annual Total Return(a) | ||||

| One Year | Five Year | Ten Year | Since Inception | |

| TCU Shares | -5.40% | 0.62% | 0.52% | 2.92%(b) |

| Investor Shares | -5.42% | 0.61% | — | 0.50%(c) |

| 2-Year T-Note (Including Transaction Costs) | ||||

(Performance since October 9, 1992)(d) | -4.09% | 0.66% | 0.62% | 3.08%(d) |

| 2-Year T-Note (Excluding Transaction Costs) | ||||

(Performance since October 9, 1992)(e) | -4.06% | 0.67% | 0.62% | 3.08%(d) |

(a) | ALM First began serving as investment adviser on April 16, 2017. Prior to that date, the Portfolio was advised by a different investment adviser. Performance of the Portfolio for periods prior to April 16, 2017 reflect management of the Portfolio by the previous investment adviser. |

(b) | The Portfolio’s TCU Shares commenced operations on October 9, 1992. |

(c) | The Portfolio’s Investor Shares commenced operations on November 30, 2012. |

(d) | The 2-Year T-Note (Including Transaction Costs) became the Portfolio’s primary benchmark effective October 7, 2022. |

(e) | Prior to October 7, 2022, the Portfolio’s primary benchmark was the 2-Year T-Note (Excluding Transaction Costs). |

The Bloomberg Barclays Mutual Fund Short (1-3 Year) Government Index and the ICE BofAML Two-Year U.S. Treasury Note Index (Excluding Transaction Costs) does not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The TCU Short Duration Portfolio is not a money market fund. Investors in this Portfolio should understand that the net asset value of the Portfolio will fluctuate, which may result in a loss of the principal amount invested. The Portfolio’s net asset value and yield are not guaranteed by the U.S. government, the National Credit Union Administration, or any other U.S. government agency, instrumentality or sponsored enterprise. Investments in fixed income securities are subject to the risks associated with debt securities including credit and interest rate risk. The guarantee on U.S. government securities applies only to the underlying securities of the Portfolio if held to maturity and not to the value of the Portfolio’s shares. The Portfolio’s investments in mortgage-backed securities are subject to prepayment risks. These risks may result in greater share price volatility.

All performance data shown represents past performance and should not be considered indicative of future performance, which will fluctuate as market conditions change. The investment return and principal value of an investment will fluctuate with changes in market conditions so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The chart and table above assume reinvestment of dividends and distributions. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. In addition to the investment adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect portfolio performance. These factors include, but are not limited to, portfolio operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting a portfolio. Please call 1-800-342-5828 or 1-800-CFS-5678 for the most recent month-end returns.

11

TRUST FOR CREDIT UNIONS

Ultra-Short Duration Portfolio

Portfolio of Investments – August 31, 2022

| Par Value | Value | ||||||

| ASSET BACKED SECURITIES* – 0.06% | |||||||

| Federal National Mortgage | |||||||

| Association REMIC – 0.06% | |||||||

| $ | 31,341 | Series 2001-W4, Class AV1 | |||||

| 1 Month LIBOR USD + 0.140% | |||||||

| 2.539%, 02/25/32 (a) | $ | 31,099 | |||||

| 48,227 | Series 2002-W2, Class AV1 | ||||||

| 1 Month LIBOR USD + 0.130% | |||||||

| 2.519%, 06/25/32 (a) | 47,015 | ||||||

| 251,207 | Series 2002-T7, Class A1 | ||||||

| 1 Month LIBOR USD + 0.220% | |||||||

| 2.664%, 07/25/32 (a) | 247,107 | ||||||

| Total Asset Backed Securities | 325,221 | ||||||

| (Cost $330,774) | |||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS – 63.21% | |||||||

| Federal Home Loan Mortgage | |||||||

| Corporation REMIC – 4.53% | |||||||

| 153 | Series 1448, Class F | ||||||

| 1 Month LIBOR USD + 1.400% | |||||||

| 3.791%, 12/15/22 (a)(b) | 153 | ||||||

| 172,637 | Series 2977, Class M | ||||||

| 5.000%, 05/15/25 (c) | 173,089 | ||||||

| 879,197 | Series 3702, Class FG | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.841%, 08/15/32 (a)(d) | 878,850 | ||||||

| 918,552 | Series 3346, Class FT | ||||||

| 1 Month LIBOR USD + 0.350% | |||||||

| 2.741%, 10/15/33 (a)(c)(d) | 914,593 | ||||||

| 662,065 | Series 3208, Class FH | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.791%, 08/15/36 (a) | 659,807 | ||||||

| 52,400 | Series 3231, Class FB | ||||||

| 1 Month LIBOR USD + 0.350% | |||||||

| 2.741%, 10/15/36 (a) | 52,089 | ||||||

| 32,483 | Series 3314, Class FC | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.791%, 12/15/36 (a) | 32,361 | ||||||

| 517,448 | Series 4248, Class QF | ||||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.891%, 06/15/39 (a)(d) | 517,284 | ||||||

| 104,823 | Series 3545, Class FA | ||||||

| 1 Month LIBOR USD + 0.850% | |||||||

| 3.241%, 06/15/39 (a) | 106,530 | ||||||

| 196,258 | Series 3827, Class KF | ||||||

| 1 Month LIBOR USD + 0.370% | |||||||

| 2.761%, 03/15/41 (a) | 195,725 | ||||||

| 30,831 | Series 3868, Class FA | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.791%, 05/15/41 (a) | 30,700 | ||||||

| 51,606 | Series 4109, Class EC | ||||||

| 2.000%, 12/15/41 (b)(d) | 40,408 | ||||||

| 1,637,369 | Series 4566, Class FA | ||||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.891%, 04/15/46 (a) | 1,638,204 | ||||||

| 2,159,063 | Series 4748, Class DF | ||||||

| 1 Month LIBOR USD + 0.300% | |||||||

| 2.691%, 08/15/47 (a)(c) | 2,133,347 | ||||||

| 2,329,817 | Series 4735, Class FB | ||||||

| 1 Month LIBOR USD + 0.350% | |||||||

| 2.741%, 12/15/47 (a) | 2,309,929 | ||||||

| 2,508,593 | Series 4875, Class F | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.841%, 04/15/49 (a)(c) | 2,501,508 | ||||||

| 6,087,372 | Series 4980, Class FP | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 07/25/49 (a) | 6,046,240 | ||||||

| 3,315,730 | Series 4906, Class QF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 09/25/49 (a) | 3,302,904 | ||||||

| 3,291,576 | Series 4982, Class F | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 06/25/50 (a)(c) | 3,302,543 | ||||||

| 1,072,264 | Series 4981, Class GF | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 06/25/50 (a) | 1,058,028 | ||||||

| 25,894,292 | |||||||

| Federal National Mortgage | |||||||

| Association REMIC – 8.33% | |||||||

| 2,695 | Series 1993-27, Class F | ||||||

| 1 Month LIBOR USD + 1.150% | |||||||

| 3.594%, 02/25/23 (a)(e) | 2,701 | ||||||

| 6,485 | Series 1998-21, Class F | ||||||

H15T1Y + 0.350% 2.776%, 03/25/28 (a) | |||||||

| 6,459 | |||||||

| 68,196 | Series 2000-16, Class ZG | ||||||

| 8.500%, 06/25/30 (b) | 76,292 | ||||||

| 64,669 | Series 2000-32, Class Z | ||||||

| 7.500%, 10/18/30 | 70,436 | ||||||

| 89,982 | Series 2006-45, Class TF | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 06/25/36 (a) | 89,704 | ||||||

| 127,240 | Series 2006-79, Class PF | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 08/25/36 (a)(c) | 126,839 | ||||||

| 131,655 | Series 2006-76, Class QF | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 08/25/36 (a)(c) | 131,255 | ||||||

| 288,349 | Series 2006-111, Class FA | ||||||

| 1 Month LIBOR USD + 0.380% | |||||||

| 2.824%, 11/25/36 (a) | 287,102 | ||||||

| 118,943 | Series 2007-75, Class VF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 08/25/37 (a) | 118,844 | ||||||

See accompanying notes to financial statements.

12

TRUST FOR CREDIT UNIONS

Ultra-Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| Federal Home Loan Mortgage | |||||||

| Association REMIC – (continued) | |||||||

| $ | 281,215 | Series 2007-85, Class FC | |||||

| 1 Month LIBOR USD + 0.540% | |||||||

| 2.984%, 09/25/37 (a) | $ | 281,996 | |||||

| 119,003 | Series 2007-86, Class FC | ||||||

| 1 Month LIBOR USD + 0.570% | |||||||

| 3.014%, 09/25/37 (a) | 119,482 | ||||||

| 110,559 | Series 2007-92, Class OF | ||||||

| 1 Month LIBOR USD + 0.570% | |||||||

| 3.014%, 09/25/37 (a) | 110,914 | ||||||

| 155,208 | Series 2007-99, Class FD | ||||||

| 1 Month LIBOR USD + 0.600% | |||||||

| 3.044%, 10/25/37 (a) | 155,879 | ||||||

| 14,596 | Series 2009-84, Class WF | ||||||

| 1 Month LIBOR USD + 1.100% | |||||||

| 3.544%, 10/25/39 (a) | 14,997 | ||||||

| 270,085 | Series 2010-123B, Class FL | ||||||

| 1 Month LIBOR USD + 0.430% | |||||||

| 2.874%, 11/25/40 (a)(c) | 269,841 | ||||||

| 516,843 | Series 2011-110, Class FE | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 04/25/41 (a)(c) | 516,203 | ||||||

| 267,118 | Series 2011-63, Class FG | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 07/25/41 (a) | 266,621 | ||||||

| 291,346 | Series 2012-38, Class JE | ||||||

| 3.250%, 04/25/42 (c) | 275,678 | ||||||

| 1,686,138 | Series 2013-92, Class FA | ||||||

| 1 Month LIBOR USD + 0.550% | |||||||

| 2.994%, 09/25/43 (a) | 1,689,073 | ||||||

| 652,830 | Series 2013-118, Class FB | ||||||

| 1 Month LIBOR USD + 0.520% | |||||||

| 2.964%, 12/25/43 (a) | 653,926 | ||||||

| 1,070,047 | Series 2015-30, Class AB | ||||||

| 3.000%, 05/25/45 | 1,030,242 | ||||||

| 1,746,202 | Series 2017-39, Class FT | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 05/25/47 (a) | 1,733,561 | ||||||

| 2,322,295 | Series 2017-112, Class FC | ||||||

| 1 Month LIBOR USD + 0.350% | |||||||

| 2.794%, 01/25/48 (a) | 2,297,600 | ||||||

| 738,045 | Series 2008-22, Class FD | ||||||

| 1 Month LIBOR USD + 0.840% | |||||||

| 3.284%, 04/25/48 (a)(d) | 751,369 | ||||||

| 4,322,396 | Series 2019-25, Class PF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 06/25/49 (a)(c) | 4,309,592 | ||||||

| 1,143,362 | Series 2019-35, Class EF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 07/25/49 (a) | 1,138,485 | ||||||

| 4,315,965 | Series 2019-33, Class CF | ||||||

| 1 Month LIBOR USD + 0.470% | |||||||

| 2.914%, 07/25/49 (a) | 4,300,763 | ||||||

| 4,882,477 | Series 2019-50, Class CF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 09/25/49 (a)(c) | 4,863,584 | ||||||

| 3,359,794 | Series 2019-61, Class F | ||||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.944%, 11/25/49 (a)(c) | 3,353,906 | ||||||

| 2,237,377 | Series 2020-17, Class PF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 03/25/50 (a)(c) | 2,226,209 | ||||||

| 6,055,673 | Series 2020-26, Class GF | ||||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.944%, 05/25/50 (a)(c) | 6,050,001 | ||||||

| 7,252,037 | Series 2020-38, Class NF | ||||||

| 1 Month LIBOR USD + 0.450% | |||||||

| 2.894%, 06/25/50 (a) | 7,221,136 | ||||||

| 3,089,055 | Series 2017-96, Class FA | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.844%, 12/25/57 (a) | 3,069,258 | ||||||

| 47,609,948 | |||||||

| Government National | |||||||

| Mortgage Association – 50.35% | |||||||

| 3,643,551 | Series 2019-054, Class HF | ||||||

| 1 Month SOFR + 0.400% | |||||||

| 1.786%, 04/20/44 (a) | 3,574,521 | ||||||

| 5,588,372 | Series 2017-H11, Class FV | ||||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.298%, 05/20/67 (a) | 5,541,290 | ||||||

| 2,899,217 | Series 2018-H01, Class FC | ||||||

| 1 Month LIBOR USD + 0.400% | |||||||

| 2.198%, 01/20/68 (a) | 2,866,827 | ||||||

| 2,407,652 | Series 2019-H04, Class FB | ||||||

| 1 Month LIBOR USD + 0.550% | |||||||

| 2.205%, 03/20/69 (a) | 2,357,313 | ||||||

| 2,374,884 | Series 2019-H15, Class NF | ||||||

| 1 Month LIBOR USD + 0.630% | |||||||

| 2.428%, 05/20/69 (a) | 2,340,815 | ||||||

| 2,840,562 | Series 2019-H15, Class EF | ||||||

| 1 Month LIBOR USD + 0.630% | |||||||

| 2.257%, 09/20/69 (a) | 2,797,927 | ||||||

| 3,116,076 | Series 2019-H16, Class FA | ||||||

| 1 Month LIBOR USD + 0.700% | |||||||

| 1.601%, 10/20/69 (a) | 3,073,260 | ||||||

| 3,190,989 | Series 2019-H19, Class FC | ||||||

| 1 Month LIBOR USD + 0.750% | |||||||

| 2.021%, 10/20/69 (a) | 3,164,111 | ||||||

| 5,794,443 | Series 2019-H20, Class AF | ||||||

| 1 Month LIBOR USD + 0.650% | |||||||

| 2.448%, 11/20/69 (a) | 5,695,573 | ||||||

| 33,168,921 | Series 2021-H03, Class FA | ||||||

| 30-Day Average SOFR + 0.380% | |||||||

| 2.438%, 04/20/70 (a) | 33,011,086 | ||||||

See accompanying notes to financial statements.

13

TRUST FOR CREDIT UNIONS

Ultra-Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| Government National | |||||||

| Mortgage Association – (continued) | |||||||

| $ | 4,235,413 | Series 2020-H13, Class FK | |||||

| 1 Month LIBOR USD + 0.500% | |||||||

| 2.298%, 07/20/70 (a) | $ | 4,194,949 | |||||

| 2,725,899 | Series 2020-H16, Class LF | ||||||

| 1 Month LIBOR USD + 1.050% | |||||||

| 2.482%, 09/20/70 (a) | 2,746,362 | ||||||

| 9,144,222 | Series 2020-H22, Class HF | ||||||

| 3.257%, 10/20/70 (a) | 9,689,222 | ||||||

| 17,437,635 | Series 2021-H11, Class FA | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 2.455%, 12/20/70 (a) | 17,637,606 | ||||||

| 18,728,218 | Series 2021-H04, Class FD | ||||||

| 30-Day Average SOFR + 1.150% | |||||||

| 2.417%, 12/20/70 (a) | 18,634,655 | ||||||

| 11,681,330 | Series 2021-H03, Class JF | ||||||

| 30-Day Average SOFR + 1.250% | |||||||

| 3.308%, 01/20/71 (a) | 11,771,474 | ||||||

| 12,313,575 | Series 2021-H04, Class FA | ||||||

| 30-Day Average SOFR + 1.250% | |||||||

| 3.308%, 02/20/71 (a) | 12,405,742 | ||||||

| 16,734,350 | Series 2021-H04, Class FB | ||||||

| 30-Day Average SOFR + 1.200% | |||||||

| 3.258%, 02/20/71 (a) | 16,820,460 | ||||||

| 14,991,302 | Series 2021-H03, Class FJ | ||||||

| 30-Day Average SOFR + 1.150% | |||||||

| 2.537%, 02/20/71 (a) | 14,904,012 | ||||||

| 22,169,028 | Series 2021-H06, Class LF | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 3.558%, 03/20/71 (a) | 22,629,306 | ||||||

| 20,782,282 | Series 2021-H06, Class PF | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 3.558%, 04/20/71 (a) | 21,219,172 | ||||||

| 21,788,338 | Series 2021-H08, Class NF | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 3.558%, 04/20/71 (a) | 22,236,426 | ||||||

| 23,035,969 | Series 2021-H10, Class FB | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 3.558%, 06/20/71 (a) | 23,521,784 | ||||||

| 24,523,736 | Series 2021-H11, Class FM | ||||||

| 30-Day Average SOFR + 1.500% | |||||||

| 3.558%, 07/20/71 (a) | 25,020,400 | ||||||

| 287,854,293 | |||||||

| Total Collateralized | |||||||

| Mortgage Obligations | 361,358,533 | ||||||

| (Cost $372,032,232) | |||||||

| MORTGAGE-BACKED OBLIGATIONS – 22.48% | |||||||

| Federal Home Loan | |||||||

| Mortgage Corporation – 0.03% | |||||||

| 189 | 6 Month LIBOR USD + 1.625% | ||||||

| 2.375%, 11/01/22 (a) | 188 | ||||||

| 425 | 6 Month LIBOR USD + 1.095% | ||||||

| 2.254%, 11/01/22 (a) | 423 | ||||||

| 3,762 | 6 Month LIBOR USD + 2.232% | ||||||

| 2.974%, 10/01/24 (a) | 3,719 | ||||||

| 135,613 | H15T3Y + 2.537% 2.900%, 08/01/28 (a) | ||||||

| 134,675 | |||||||

| 25,508 | H15T1Y + 1.920% 3.690%, 05/01/31 (a) | ||||||

| 25,243 | |||||||

| 164,248 | |||||||

| Federal Home Loan Mortgage | |||||||

| Corporation Gold – 0.00% | |||||||

| 92 | 3.500%, 10/01/22 | 92 | |||||

| 41 | 4.500%, 07/01/23 | 42 | |||||

| 134 | |||||||

| Federal National | |||||||

| Mortgage Association – 21.13% | |||||||

| 24,095 | 5.000%, 03/01/27 | 24,660 | |||||

| 10,329 | 11th District COFI Institutional | ||||||

| Replacement Index + 1.254% | |||||||

| 2.358%, 07/01/27 (a) | 10,169 | ||||||

| 28,937 | 11th District COFI Institutional | ||||||

| Replacement Index + 1.504% | |||||||

| 4.685%, 01/01/29 (a) | 29,482 | ||||||

| 4,531 | 11th District COFI Institutional | ||||||

| Replacement Index + 1.504% | |||||||

| 4.671%, 02/01/29 (a) | 4,616 | ||||||

| 5,000,000 | 1 Month LIBOR USD + 0.520% | ||||||

| 2.882%, 05/01/29 (a) | 4,999,743 | ||||||

| 5,000,000 | 1 Month LIBOR USD + 0.580% | ||||||

| 2.942%, 06/01/29 (a) | 4,999,850 | ||||||

| 5,546 | 11th District COFI Institutional | ||||||

| Replacement Index + 1.695% | |||||||

| 2.188%, 08/01/29 (a) | 5,471 | ||||||

| 31,131,000 | 30-Day Average SOFR + 0.390% | ||||||

| 1.945%, 12/01/30 (a) | 31,134,449 | ||||||

| 30,870,000 | 30-Day Average SOFR + 0.350% | ||||||

| 1.905%, 01/01/31 (a) | 30,872,908 | ||||||

| 3,675,000 | 30-Day Average SOFR + 0.380% | ||||||

| 1.935%, 01/01/31 (a) | 3,675,529 | ||||||

| 21,122,124 | 30-Day Average SOFR + 0.390% | ||||||

| 1.945%, 01/01/31 (a) | 21,125,422 | ||||||

| 20,100,000 | 30-Day Average SOFR + 0.250% | ||||||

| 1.805%, 04/01/31 (a) | 20,099,100 | ||||||

| 37,580 | 12 Month LIBOR USD + 1.755% | ||||||

| 4.005%, 07/01/32 (a) | 37,275 | ||||||

| 7,233 | 6.000%, 08/01/32 | 7,495 | |||||

| 143,621 | H15T1Y + 2.625% | ||||||

| 3.703%, 09/01/32 (a) | 142,215 | ||||||

| 7,170 | 12 Month LIBOR USD + 1.225% | ||||||

| 1.475%, 01/01/33 (a) | 7,087 | ||||||

| 9,775 | H15T1Y + 2.181% | ||||||

| 3.180%, 06/01/33 (a) | 9,986 | ||||||

See accompanying notes to financial statements.

14

TRUST FOR CREDIT UNIONS

Ultra-Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| Federal National | |||||||

| Mortgage Association – (continued) | |||||||

| $ | 192,930 | 11th District COFI Institutional | |||||

| Replacement Index + 1.254% | |||||||

| 4.592%, 08/01/33 (a) | $ | 196,041 | |||||

| 673 | 6.000%, 11/01/33 | 699 | |||||

| 94,530 | H15T1Y + 2.003% 3.003%, 04/01/34 (a) | ||||||

| 96,864 | |||||||

| 347,618 | 12 Month US Treasury Average + 1.144% | ||||||

| 1.788%, 08/01/34 (a) | 346,870 | ||||||

| 25,556 | 6.000%, 09/01/34 | 26,485 | |||||

| 119,322 | 12 Month LIBOR USD + 1.713% | ||||||

| 3.298%, 07/01/37 (a) | 122,191 | ||||||

| 53,833 | 6.500%, 11/01/37 | 54,111 | |||||

| 13,703 | 6.000%, 06/01/38 | 14,190 | |||||

| 17,334 | 6.000%, 09/01/38 | 18,013 | |||||

| 6,969 | 6.000%, 09/01/38 | 7,423 | |||||

| 5,716 | 6.000%, 11/01/38 | 5,914 | |||||

| 855 | 6.000%, 10/01/39 | 884 | |||||

| 824,259 | 12 Month LIBOR USD + 1.714% | ||||||

| 2.727%, 07/01/40 (a) | 836,512 | ||||||

| 1,371,072 | 12 Month LIBOR USD + 1.755% | ||||||

| 2.926%, 02/01/42 (a) | 1,403,872 | ||||||

| 204,550 | 12 Month LIBOR USD + 1.749% | ||||||

| 2.949%, 05/01/42 (a) | 207,990 | ||||||

| 290,438 | 12 Month US Treasury Average + 1.153% | ||||||

| 1.797%, 08/01/44 (a) | 289,984 | ||||||

| 120,813,500 | |||||||

| Government National | |||||||

| Mortgage Association – 1.32% | |||||||

| 4,811 | 7.000%, 04/15/26 | 4,903 | |||||

| 68,941 | H15T1Y + 2.000% 3.375%, 04/20/34 (a) | ||||||

| 68,658 | |||||||

| 229,663 | H15T1Y + 1.500% 2.875%, 06/20/34 (a) | ||||||

| 228,200 | |||||||

| 349,609 | H15T1Y + 1.500% 1.625%, 08/20/34 (a) | ||||||

| 343,580 | |||||||

| 14,554 | H15T1Y + 1.500% 2.875%, 05/20/42 (a) | ||||||

| 14,535 | |||||||

| 12,199 | H15T1Y + 1.500% 2.875%, 06/20/42 (a) | ||||||

| 12,183 | |||||||

| 71,555 | H15T1Y + 1.500% 1.625%, 07/20/42 (a) | ||||||

| 70,646 | |||||||

| 7,005 | H15T1Y + 1.500% 1.750%, 10/20/42 (a) | ||||||

| 6,895 | |||||||

| 14,005 | H15T1Y + 1.500% 1.750%, 12/20/42 (a) | ||||||

| 13,784 | |||||||

| 1,337,798 | 12 Month LIBOR USD + 1.695% 1.982%, 11/20/68 (a) | ||||||

| 1,362,100 | |||||||

| 2,702,910 | 12 Month LIBOR USD + 1.903% 3.206%, 06/20/69 (a) | ||||||

| 2,796,655 | |||||||

| 2,568,725 | 12 Month LIBOR USD + 1.511% 2.806%, 09/20/69 (a) | ||||||

| 2,612,516 | |||||||

| 7,534,655 | |||||||

| Total Mortgage-Backed Obligations | 128,512,537 | ||||||

| (Cost $128,604,560) | |||||||

| AGENCY DEBENTURES – 0.22% | |||||||

| Other Agency Debentures – 0.22% | |||||||

| 1,250,000 | Sri Lanka Government AID Bond | ||||||

3 Month LIBOR USD + 0.300% 1.635%, 11/01/24 (a)(f)(g) | |||||||

| 1,250,000 | |||||||

| Total Agency Debentures | 1,250,000 | ||||||

| (Cost $1,250,000) | |||||||

| U.S. GOVERNMENT-BACKED OBLIGATIONS – 10.39% | |||||||

| FHLMC, Multifamily Structured | |||||||

| Pass Through Certificates | |||||||

| 414,447 | Series K-F29, Class A | ||||||

1 Month LIBOR USD + 0.360% 2.722%, 02/25/24 (a)(d) | |||||||

| 414,093 | |||||||

| 251,087 | Series K-BF1, Class A | ||||||

1 Month LIBOR USD + 0.390% 2.752%, 07/25/24 (a)(d) | |||||||

| 250,723 | |||||||

| 2,208,589 | Series K-F49, Class A | ||||||

1 Month LIBOR USD + 0.340% 2.702%, 06/25/25 (a)(d) | |||||||

| 2,202,143 | |||||||

| 5,996,644 | Series K-F55, Class A | ||||||

1 Month LIBOR USD + 0.510% 2.872%, 11/25/25 (a)(d) | |||||||

| 5,996,638 | |||||||

| 152,072 | Series K-F30, Class A | ||||||

1 Month LIBOR USD + 0.370% 2.732%, 03/25/27 (a)(d) | |||||||

| 150,352 | |||||||

| 3,906,240 | Series K-F81, Class AL | ||||||

1 Month LIBOR USD + 0.360% 2.722%, 06/25/27 (a)(d) | |||||||

| 3,876,978 | |||||||

| 676,379 | Series K-F86, Class AS | ||||||

30-Day Average SOFR + 0.320% 1.875%, 08/25/27 (a)(d) | |||||||

| 674,059 | |||||||

| 985,500 | Series K-F50, Class A | ||||||

1 Month LIBOR USD + 0.400% 2.762%, 07/25/28 (a)(d) | |||||||

| 983,522 | |||||||

| 15,000,000 | Series K-L06, Class AFL | ||||||

1 Month LIBOR USD + 0.370% 2.732%, 12/25/29 (a)(d) | |||||||

| 14,931,909 | |||||||

| 14,701,060 | Series K-F87, Class AL | ||||||

1 Month LIBOR USD + 0.350% 2.712%, 08/26/30 (a) | |||||||

| 14,591,931 | |||||||

| 15,356,877 | Series K-F92, Class AL | ||||||

1 Month LIBOR USD + 0.330% 2.692%, 10/25/30 (a)(d) | |||||||

| 15,312,700 | |||||||

| Total U.S. Government-Backed | |||||||

| Obligations | 59,385,048 | ||||||

| (Cost $59,649,380) | |||||||

See accompanying notes to financial statements.

15

TRUST FOR CREDIT UNIONS

Ultra-Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| REPURCHASE AGREEMENTS – 3.63% | |||||||

| $ | 20,750,000 | INTL FCStone Financial, Inc., 2.410%, | |||||

| Dated 08/31/2022, matures 09/01/2022, | |||||||

| repurchase price $20,751,389 (collateralized | |||||||

| by $22,280,230 par amount of GNMA, | |||||||

| FNMA, and FHLMC securities of 3.180% to | |||||||

| 5.000% due 03/01/28 to 08/20/52, | |||||||

| total market value $21,122,243) | $ | 20,750,000 | |||||

| Total Repurchase Agreements | 20,750,000 | ||||||

| (Cost $20,750,000) | |||||||

| Total Investments – 99.99% | 571,581,339 | ||||||

| (Cost $582,616,946) | |||||||

| Net Other Assets | |||||||

| and Liabilities – 0.01% | 77,220 | ||||||

| Net Assets – 100.00% | $ | 571,658,559 | |||||

| * | See Note A. |

| (a) | Variable rate securities. Interest rates disclosed are those which are in effect at August 31, 2022. Maturity date shown is the date of the next coupon rate reset or actual maturity. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description. For those variable rate securities which are based on published reference and spread, the reference rate and spread are indicated in the description in the Portfolio of Investments. See also, Explanation of Abbreviations and Acronyms below. |

| (b) | The security has Sequential collateral. |

| (c) | The security has PAC (Planned Amortization Class) collateral. |

| (d) | The security has Structured collateral. |

| (e) | The security has Support collateral. |

| (f) | Security has been valued at fair market value as determined in good faith by or under the direction of the Board of Trustees of the Trust. As of August 31, 2022, this security amounted to $1,250,000 or 0.22% of net assets. Investment categorized as a significant unobservable input (Level 3). |

| (g) | Illiquid security. The total market value of this security was $1,250,000, representing 0.22% of net assets. |

Explanation of Abbreviations and Acronyms:

| COFI | Cost of Funds Indices |

| FHLMC | Federal Home Loan Mortgage Corporation |

| FNMA | Federal National Mortgage Association |

| GNMA | Government National Mortgage Association |

| H15T1Y | 1 Year US Treasury Yield Curve Constant Maturity Rate |

| H15T3Y | 3 Year US Treasury Yield Curve Constant Maturity Rate |

| LIBOR | London Interbank Offered Rate |

| REMIC | Real Estate Mortgage Investment Conduit |

| SOFR | Secured Overnight Financing Rate |

| USD | U.S. Dollar |

See accompanying notes to financial statements.

16

TRUST FOR CREDIT UNIONS

Short Duration Portfolio

Portfolio of Investments – August 31, 2022

| Par Value | Value | ||||||

| BANK NOTES – 8.16% | |||||||

| Financials – 8.16% | |||||||

| $ | 6,308,000 | Citizens Bank NA, | |||||

| 2.250%, 04/28/25 | $ | 5,980,299 | |||||

| 10,000,000 | Discover Bank, | ||||||

| 2.450%, 09/12/24 | 9,607,930 | ||||||

| 20,562,000 | First-Citizens Bank & Trust Co., | ||||||

3 Month SOFR + 1.715% 2.969%, 09/27/25 (a) | |||||||

| 19,644,311 | |||||||

| Total Bank Notes | 35,232,540 | ||||||

| (Cost $37,774,164) | |||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS – 23.02% | |||||||

| Federal Home Loan Mortgage | |||||||

| Corporation REMIC – 2.04% | |||||||

| 358 | Series 1448, Class F | ||||||

1 Month LIBOR USD + 1.400% 3.791%, 12/15/22 (a)(b) | |||||||

| 358 | |||||||

| 35,338 | Series 2868, Class AV | ||||||

| 5.000%, 08/15/24 (b)(c) | 35,422 | ||||||

| 51,820 | Series 1980, Class Z | ||||||

| 7.000%, 07/15/27 (b) | 54,006 | ||||||

| 762,066 | Series 3346, Class FT | ||||||

1 Month LIBOR USD + 0.350% 2.741%, 10/15/33 (a)(c)(d) | |||||||

| 758,781 | |||||||

| 595,511 | Series 3471, Class FB | ||||||

1 Month LIBOR USD + 1.000% 3.391%, 08/15/35 (a) | |||||||

| 599,798 | |||||||

| 997,086 | Series 3208, Class FA | ||||||

1 Month LIBOR USD + 0.400% 2.791%, 08/15/36 (a) | |||||||

| 993,686 | |||||||

| 335,021 | Series 3208, Class FH | ||||||

1 Month LIBOR USD + 0.400% 2.791%, 08/15/36 (a) | |||||||

| 333,878 | |||||||

| 231,911 | Series 3367, Class YF | ||||||

1 Month LIBOR USD + 0.550% 2.941%, 09/15/37 (a) | |||||||

| 232,649 | |||||||

| 805,775 | Series 3371, Class FA | ||||||

1 Month LIBOR USD + 0.600% 2.991%, 09/15/37 (a) | |||||||

| 810,331 | |||||||

| 324,764 | Series 4248, Class QF | ||||||

1 Month LIBOR USD + 0.500% 2.891%, 06/15/39 (a)(c) | |||||||

| 324,661 | |||||||

| 123,142 | Series 3827, Class KF | ||||||

1 Month LIBOR USD + 0.370% 2.761%, 03/15/41 (a) | |||||||

| 122,808 | |||||||

| 41,120 | Series 4109, Class EC | ||||||

| 2.000%, 12/15/41 (b)(c) | 32,197 | ||||||

| 668,414 | Series 4272, Class FD | ||||||

1 Month LIBOR USD + 0.350% 2.741%, 11/15/43 (a) | |||||||

| 665,296 | |||||||

| 1,020,714 | Series 4606, Class FL | ||||||

1 Month LIBOR USD + 0.500% 2.891%, 12/15/44 (a)(c) | |||||||

| 1,017,176 | |||||||

| 447,794 | Series 4784, Class PK | ||||||

| 3.500%, 06/15/45 (d) | 442,273 | ||||||

| 2,096,369 | Series 4968, Class NP | ||||||

| 6.500%, 04/25/50 (d) | 2,402,674 | ||||||

| 8,825,994 | |||||||

| Federal National Mortgage | |||||||

| Association REMIC – 5.20% | |||||||

| 1,567,714 | Series 2013-57, Class DK | ||||||

| 3.500%, 06/25/33 | 1,547,351 | ||||||

| 130,238 | Series 2006-45, Class TF | ||||||

1 Month LIBOR USD + 0.400% 2.844%, 06/25/36 (a) | |||||||

| 129,834 | |||||||

| 155,773 | Series 2006-76, Class QF | ||||||

1 Month LIBOR USD + 0.400% 2.844%, 08/25/36 (a)(d) | |||||||

| 155,299 | |||||||

| 89,207 | Series 2007-75, Class VF | ||||||

1 Month LIBOR USD + 0.450% 2.894%, 08/25/37 (a) | |||||||

| 89,133 | |||||||

| 106,735 | Series 2010-123, Class FL | ||||||

1 Month LIBOR USD + 0.430% 2.874%, 11/25/40 (a)(d) | |||||||

| 106,638 | |||||||

| 169,211 | Series 2011-110, Class FE | ||||||

1 Month LIBOR USD + 0.400% 2.844%, 04/25/41 (a)(d) | |||||||

| 169,002 | |||||||

| 225,605 | Series 2015-92, Class PA | ||||||

| 2.500%, 12/25/41 (c)(d) | 213,613 | ||||||

| 233,687 | Series 2012-38, Class JE | ||||||

| 3.250%, 04/25/42 (d) | 221,120 | ||||||

| 579,874 | Series 2012-71, Class FL | ||||||

1 Month LIBOR USD + 0.500% 2.944%, 07/25/42 (a) | |||||||

| 579,884 | |||||||

| 1,613,215 | Series 2013-101, Class FE | ||||||

1 Month LIBOR USD + 0.600% 3.044%, 10/25/43 (a) | |||||||

| 1,621,003 | |||||||

| 2,323,276 | Series 2013-101, Class CF | ||||||

1 Month LIBOR USD + 0.600% 3.044%, 10/25/43 (a) | |||||||

| 2,334,391 | |||||||

| 2,828,382 | Series 2016-62, Class FH | ||||||

1 Month LIBOR USD + 0.400% 2.844%, 09/25/46 (a) | |||||||

| 2,817,519 | |||||||

| 3,094,390 | Series 2016-83, Class FK | ||||||

1 Month LIBOR USD + 0.500% 2.944%, 11/25/46 (a) | |||||||

| 3,095,382 | |||||||

| 1,746,202 | Series 2017-39, Class FT | ||||||

1 Month LIBOR USD + 0.400% 2.844%, 05/25/47 (a) | |||||||

| 1,733,561 | |||||||

| 1,939,648 | Series 2017-112, Class FC | ||||||

1 Month LIBOR USD + 0.350% 2.794%, 01/25/48 | |||||||

| 1,919,022 | |||||||

| 572,951 | Series 2008-22, Class FD | ||||||

1 Month LIBOR USD + 0.840% 3.284%, 04/25/48 (a)(c) | |||||||

| 583,295 | |||||||

See accompanying notes to financial statements.

17

TRUST FOR CREDIT UNIONS

Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| Federal National Mortgage | |||||||

| Association REMIC – (continued) | |||||||

| $ | 4,488,637 | Series 2020-18, Class KD | |||||

| 6.500%, 03/25/50 | $ | 5,113,784 | |||||

| 22,429,831 | |||||||

| Government National | |||||||

| Mortgage Association – 15.78% | |||||||

| 2,899,217 | Series 2018-H01, Class FC | ||||||

1 Month LIBOR USD + 0.400% 2.198%, 01/20/68 (a) | |||||||

| 2,866,828 | |||||||

| 4,756,345 | Series 2018-H09, Class FC | ||||||

12 Month LIBOR USD + 0.150% 2.779%, 06/20/68 (a) | |||||||

| 4,633,479 | |||||||

| 5,563,700 | Series 2018-H11, Class FJ | ||||||

12 Month LIBOR USD + 0.080% 2.855%, 06/20/68 (a) | |||||||

| 5,438,848 | |||||||

| 16,584,460 | Series 2021-H03, Class FA | ||||||

30-Day Average SOFR + 0.380% 2.438%, 04/20/70 (a) | |||||||

| 16,505,543 | |||||||

| 3,292,237 | Series 2020-H09, Class DF | ||||||

1 Month LIBOR USD + 0.640% 2.438%, 05/20/70 (a) | |||||||

| 3,252,501 | |||||||

| 18,338,368 | Series 2021-H10, Class FB | ||||||

30-Day Average SOFR + 1.500% 3.558%, 06/20/71 (a) | |||||||

| 18,725,113 | |||||||

| 6,199,842 | Series 2021-H11, Class FM | ||||||

30-Day Average SOFR + 1.500% 3.558%, 07/20/71 (a) | |||||||

| 6,325,403 | |||||||

| 10,087,800 | Series 2020-176, Class MT | ||||||

| 5.000%, 11/20/50 | 10,402,023 | ||||||

| 68,149,738 | |||||||

| Total Collateralized | |||||||

| Mortgage Obligations | 99,405,563 | ||||||

| (Cost $101,726,517) | |||||||

| MORTGAGE-BACKED OBLIGATIONS – 29.94% | |||||||

| Federal Home Loan | |||||||

| Mortgage Corporation – 0.94% | |||||||

| 47,465 | 12 Month LIBOR USD + 1.840% 2.692%, 11/01/34 (a) | ||||||

| 47,205 | |||||||

| 1,266,302 | 3.000%, 11/01/34 | 1,231,195 | |||||

| 88,216 | H15T1Y + 2.250% 2.864%, 08/01/35 (a) | ||||||

| 90,189 | |||||||

| 112,433 | 12 Month LIBOR USD + 1.767% 2.332%, 05/01/36 | ||||||

| 113,757 | |||||||

| 60,911 | 12 Month LIBOR USD + 1.890% 2626%, 03/01/42 | ||||||

| 61,563 | |||||||

| 2,634,589 | 3.000%, 02/01/47 | 2,494,058 | |||||

| 4,037,967 | |||||||

| Federal Home Loan Mortgage | |||||||

| Corporation Gold – 2.38% | |||||||

| 76 | 3.500%, 10/01/22 | 76 | |||||

| 3,290,659 | 2.000%, 12/01/31 | 3,086,582 | |||||

| 35,332 | 5.000%, 08/01/35 | 36,955 | |||||

| 6,198 | 5.000%, 12/01/35 | 6,481 | |||||

| 1,435,285 | 3.000%, 01/01/37 | 1,380,535 | |||||

| 1,615,937 | 3.000%, 02/01/37 | 1,559,154 | |||||

| 2,045,854 | 3.500%, 02/01/37 | 2,022,324 | |||||

| 52,573 | 5.000%, 03/01/37 | 54,991 | |||||

| 1,713,081 | 3.500%, 03/01/37 | 1,693,379 | |||||

| 112,408 | 5.000%, 05/01/37 | 117,578 | |||||

| 77,586 | 5.000%, 02/01/38 | 80,687 | |||||

| 40,479 | 5.000%, 03/01/38 | 42,286 | |||||

| 25,920 | 5.000%, 09/01/38 | 27,105 | |||||

| 88,719 | 5.000%, 12/01/38 | 92,780 | |||||

| 59,962 | 5.000%, 01/01/39 | 62,709 | |||||

| 10,263,622 | |||||||

| Federal National | |||||||

| Mortgage Association – 16.74% | |||||||

| 19,276 | 5.000%, 03/01/27 | 19,728 | |||||

| 23,887 | 7.000%, 08/01/28 | 23,884 | |||||

| 19,349 | 7.000%, 08/01/28 | 19,346 | |||||

| 33,186 | 7.000%, 11/01/28 | 33,427 | |||||

| 5,233,000 | 1 Month LIBOR USD + 0.520% 2.882%, 05/01/29 (a) | ||||||

| 5,232,732 | |||||||

| 49,128 | 2.500%, 02/01/32 | 47,141 | |||||

| 6,859 | 7.000%, 02/01/32 | 7,093 | |||||

| 55,041 | 7.000%, 05/01/32 | 56,809 | |||||

| 147,490 | H15T1Y + 2.625% 3.703%, 09/01/32 (a) | ||||||

| 146,046 | |||||||

| 2,825,154 | 4.000%, 04/01/33 | 2,834,171 | |||||

| 146,587 | H15T1Y + 2.215% 4.105%, 07/01/33 (a) | ||||||

| 151,571 | |||||||

| 120,304 | 12 Month LIBOR USD + 1.537% 1.787%, 11/01/33 (a) | ||||||

| 119,175 | |||||||

| 159,141 | H15T1Y + 2.215% 2.340%, 12/01/33 (a) | ||||||

| 157,261 | |||||||

| 856,176 | 4.500%, 01/01/34 | 872,967 | |||||

| 442,916 | 4.500%, 01/01/34 | 450,926 | |||||

| 149,041 | 12 Month LIBOR USD + 1.533% 2.699%, 04/01/34 (a) | ||||||

| 148,027 | |||||||

| 55,944 | H15T1Y + 2.185% | ||||||

| 3.537%, 08/01/34 (a) | 55,785 | ||||||

| 329 | 6.000%, 09/01/34 | 343 | |||||

| 69,541 | 12 Month LIBOR USD + 1.679% 1.929%, 10/01/34 (a) | ||||||

| 70,975 | |||||||

| 2,769,783 | 3.000%, 01/01/35 | 2,692,986 | |||||

| 2,465,431 | 3.500%, 01/01/35 | 2,428,070 | |||||

| 2,266,244 | 2.500%, 03/01/35 | 2,160,134 | |||||

| 22,294 | 12 Month LIBOR USD + 1.671% 2.296%, 03/01/35 (a) | ||||||

| 22,153 | |||||||

| 40,620 | 12 Month LIBOR USD + 1.720% 3.095%, 04/01/35 (a) | ||||||

| 40,491 | |||||||

| 1,578,078 | 3.000%, 04/01/35 | 1,532,916 | |||||

See accompanying notes to financial statements.

18

TRUST FOR CREDIT UNIONS

Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| Federal National | |||||||

| Mortgage Association – (continued) | |||||||

| $ | 95,478 | 12 Month LIBOR USD + 1.413% 2.225%, 05/01/35 (a) | |||||

| $ | 96,992 | ||||||

| 115,665 | H15T1Y + 2.313% 3.284%, 05/01/35 (a) | ||||||

| 119,221 | |||||||

| 51,551 | 6 Month LIBOR USD + 1.412% 2.193%, 06/01/35 (a) | ||||||

| 50,945 | |||||||

| 1,407,654 | 4.000%, 06/01/35 | 1,393,137 | |||||

| 153,759 | 12 Month LIBOR USD + 1.750% 4.000%, 08/01/35 (a) | ||||||

| 158,817 | |||||||

| 62,092 | 6 Month LIBOR USD + 1.498% 2.587%, 08/01/35 (a) | ||||||

| 61,831 | |||||||

| 35,578 | 12 Month LIBOR USD + 2.435% 3.742%, 09/01/35 (a) | ||||||

| 35,576 | |||||||

| 74,001 | H15T1Y + 2.085% 2.085%, 10/01/35 (a) | ||||||

| 73,433 | |||||||

| 277,123 | 12 Month LIBOR USD + 1.557% 2.315%, 11/01/35 (a) | ||||||

| 274,513 | |||||||

| 12,156,528 | 3.000%, 01/01/36 | 11,820,541 | |||||

| 77,053 | 12 Month LIBOR USD + 1.737% 2.487%, 03/01/36 (a) | ||||||

| 76,532 | |||||||

| 6,693,860 | 2.000%, 03/01/36 | 6,186,791 | |||||

| 95,019 | 12 Month US Treasury Average + 2.245% 2.917%, 04/01/36 (a) | ||||||

| 99,888 | |||||||

| 856,866 | 4.500%, 12/01/38 | 868,605 | |||||

| 3,270,970 | 4.000%, 09/01/39 | 3,248,447 | |||||

| 29,333 | 5.000%, 10/01/39 | 30,378 | |||||

| 262,993 | 12 Month LIBOR USD + 1.749% 2.949%, 05/01/42 (a) | ||||||

| 267,416 | |||||||

| 83,616 | 12 Month LIBOR USD + 1.700% 3.450%, 06/01/42 (a) | ||||||

| 85,867 | |||||||

| 131,687 | 12 Month LIBOR USD + 1.684% 1.934%, 10/01/42 (a) | ||||||

| 133,158 | |||||||

| 213,164 | 12 Month LIBOR USD + 1.597% 3.108%, 12/01/44 (a) | ||||||

| 215,900 | |||||||

| 744,154 | 12 Month LIBOR USD + 1.610% 3.138%, 04/01/47 (a) | ||||||

| 728,445 | |||||||

| 627,082 | 12 Month LIBOR USD + 1.609% 3.141%, 09/01/47 (a) | ||||||

| 612,849 | |||||||

| 549,964 | 3.500%, 04/01/49 | 529,890 | |||||

| 704,151 | 4.000%, 05/01/49 | 694,189 | |||||

| 12,500,000 | 4.500%, 09/01/52 | 12,462,694 | |||||

| 12,500,000 | 5.000%, 09/01/52 | 12,639,476 | |||||

| 72,289,688 | |||||||

| Government National | |||||||

| Mortgage Association – 0.64% | |||||||

| 16,027 | H15T1Y + 1.500% 2.875%, 05/20/42 (a) | ||||||

| 16,007 | |||||||

| 13,881 | H15T1Y + 1.500% 2.875%, 06/20/42 (a) | ||||||

| 13,864 | |||||||

| 79,250 | H15T1Y + 1.500% 1.625%, 07/20/42 (a) | ||||||

| 78,243 | |||||||

| 7,971 | H15T1Y + 1.500% 1.750%, 10/20/42 (a) | ||||||

| 7,846 | |||||||

| 15,667 | H15T1Y + 1.500% 1.750%, 12/20/42 (a) | ||||||

| 15,420 | |||||||

| 2,606,109 | 12 Month LIBOR USD + 1.511% 2.431%, 09/20/69 (a) | ||||||

| 2,650,538 | |||||||

| 2,781,918 | |||||||

| Uniform Mortgage | |||||||

| Backed Securities – 9.24% | |||||||

| 40,000,000 | 4.000%, 09/15/29 (e) | 39,901,103 | |||||

| 39,901,103 | |||||||

| Total Mortgage-Backed Obligations | 129,274,298 | ||||||

| (Cost $132,206,962) | |||||||

| MUNICIPAL BONDS – 1.41% | |||||||

| City of New Orleans LA | |||||||

| Sewerage Service Revenue – 0.30% | |||||||

| 400,000 | 0.589%, 06/01/24 | 375,871 | |||||

| 500,000 | 0.808%, 06/01/25 | 455,493 | |||||

| 500,000 | 0.958%, 06/01/26 | 441,697 | |||||

| 1,273,061 | |||||||

| City of New Orleans LA | |||||||

| Water System Revenue – 0.28% | |||||||

| 500,000 | 0.465%, 12/01/23 | 478,195 | |||||

| 500,000 | 0.858%, 12/01/25 | 448,925 | |||||

| 315,000 | 1.008%, 12/01/26 | 274,340 | |||||

| 1,201,460 | |||||||

| City of New York NY – 0.83% | |||||||

| 4,000,000 | 1.216%, 08/01/26 | 3,603,569 | |||||

| Total Municipal Bonds | 6,078,090 | ||||||

| (Cost $6,764,671) | |||||||

| U.S. GOVERNMENT-BACKED OBLIGATIONS – 36.75% | |||||||

| FHLMC, Multifamily Structured | |||||||

| Pass Through Certificates | |||||||

| 414,447 | Series K-F29, Class A | ||||||

1 Month LIBOR USD + 0.360% 2.722%, 02/25/24 (a)(c) | |||||||

| 414,093 | |||||||

| 33,063 | Series K-J27, Class A1 | ||||||

| 2.092%, 07/25/24 (b)(c) | 32,850 | ||||||

| 1,192,883 | Series K-F49, Class A | ||||||

1 Month LIBOR USD + 0.340% 2.702%, 06/25/25 (a)(c) | |||||||

| 1,189,402 | |||||||

| 7,783,855 | Series K-S10, Class A10 | ||||||

1 Month LIBOR USD + 0.610% 2.972%, 10/25/28 (a)(c) | |||||||

| 7,771,098 | |||||||

| 876,806 | Series K-091, Class A1 | ||||||

| 3.339%, 10/25/28 (b)(c) | 869,802 | ||||||

| 21,791,372 | Series K-F125, Class AS | ||||||

30-Day Average SOFR + 0.220% 1.775%, 10/25/28 (a)(c) | |||||||

| 21,509,488 | |||||||

| 3,040,200 | Series K-F59, Class A | ||||||

1 Month LIBOR USD + 0.540% 2.902%, 02/25/29 (a)(c) | |||||||

| 3,028,023 | |||||||

See accompanying notes to financial statements.

19

TRUST FOR CREDIT UNIONS

Short Duration Portfolio

Portfolio of Investments (continued) – August 31, 2022

| Par Value | Value | ||||||

| U.S. GOVERNMENT-BACKED OBLIGATIONS – (continued) | |||||||

| FHLMC, Multifamily Structured | |||||||

| Pass Through Certificates (continued) | |||||||

| $ | 5,000,000 | Series K-S13, Class A | |||||

1 Month LIBOR USD + 0.660% 3.022%, 09/25/29 (a)(c) | |||||||

| $ | 4,993,811 | ||||||

| 15,356,877 | Series K-F92, Class AL | ||||||

1 Month LIBOR USD + 0.330% 2.692%, 10/25/30 (a)(c) | |||||||

| 15,312,700 | |||||||

| 18,506,220 | Series K-103, Class AS | ||||||

30-Day Average SOFR + 0.240% 1.795%, 01/27/31 (a)(c) | |||||||

| 18,177,507 | |||||||

| FNMA | |||||||

| 820,104 | Series 2013-M6, Class 2A | ||||||

| 2.672%, 03/25/23 (a) | 813,157 | ||||||

| GNMA | |||||||

| 22,074,505 | Series 2021-051, Class AC | ||||||

| 1.500%, 05/16/55 (d) | 19,418,399 | ||||||

| 22,986,671 | Series 2021-040, Class AD | ||||||

| 1.500%, 05/16/61 (d) | 20,083,006 | ||||||

| 20,396,382 | Series 2021-052, Class A | ||||||

| 1.500%, 05/16/61 (d) | 17,914,717 | ||||||

| 13,357,881 | Series 2021-068, Class AB | ||||||

| 1.500%, 12/16/61 (d) | 11,714,312 | ||||||

| 17,250,192 | Series 2020-132, Class AD | ||||||

| 2.200%, 09/16/62 (a) | 15,434,126 | ||||||

| Total U.S. Government-Backed | |||||||

| Obligations | 158,676,491 | ||||||

| (Cost $172,392,757) | |||||||

| REPURCHASE AGREEMENTS – 15.75% | |||||||

| 68,000,000 | INT FCStone Financial, Inc., 2.410%, Dated 08/31/2022, matures 09/01/2022, | ||||||

| repurchase price $68,004,552 (collateralized | |||||||

| by $305,218,322 par amount of | |||||||

| GNMA, FNMA, and FHLMC | |||||||

| securities of 1.000% to 9.500% | |||||||

| due 09/25/22 to 08/20/66, | |||||||

| total market value $69,541,725) | 68,000,000 | ||||||

| Total Repurchase Agreements | 68,000,000 | ||||||

| (Cost $68,000,000) | |||||||

| REGISTERED INVESTMENT COMPANY – 0.09% | |||||||

| 399,879 | First American Government | ||||||

| Obligations Fund – Class X | |||||||

| 2.039%, 12/01/31 (f) | 399,879 | ||||||

| Total Registered | |||||||

| Investment Company | 399,879 | ||||||

| (Cost $399,879) | |||||||

| Total Investments – 115.12% | 497,066,861 | ||||||

| (Cost $519,264,950) | |||||||

| Net Other Assets | |||||||

| and Liabilities – (15.12)% | (65,295,350 | ) | |||||

| Net Assets – 100.00% | $ | 431,771,511 | |||||

| (a) | Variable rate securities. Interest rates disclosed are those which are in effect at August 31, 2022. Maturity date shown is the date of the next coupon rate reset or actual maturity. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description. For those variable rate securities which are based on published reference and spread, the reference rate and spread are indicated in the description in the Portfolio of Investments. See also, Explanation of Abbreviations and Acronyms below. |

| (b) | The security has Sequential collateral. |

| (c) | The security has Structured collateral. |

| (d) | The security has PAC (Planned Amortization Class) collateral. |

| (e) | Represents or includes a TBA (To Be Announced) transaction. See Note 2.J. |

| (f) | Seven day yield as of August 31, 2022. |

Explanation of Abbreviations and Acronyms:

| FHLMC | Federal Home Loan Mortgage Corp. |

| FNMA | Federal National Mortgage Association |

| GNMA | Government National Mortgage Association |

| H15T1Y | 1 Year US Treasury Yield Curve Constant Maturity Rate |

| LIBOR | London Interbank Offered Rate |

| REMIC | Real Estate Mortgage Investment Conduit |

| SOFR | Secured Overnight Financing Rate |

| USD | U.S. Dollar |

See accompanying notes to financial statements.

20

TRUST FOR CREDIT UNIONS

Statements of Assets and Liabilities

August 31, 2022

| Ultra-Short | Short | |||||||

| Duration | Duration | |||||||

| Portfolio | Portfolio | |||||||

| ASSETS: | ||||||||

| INVESTMENTS: | ||||||||

| Investments and repurchase agreements at cost | $ | 582,616,946 | $ | 519,264,950 | ||||

| Investments at value | $ | 550,831,339 | $ | 429,066,861 | ||||

| Repurchase agreements at value | 20,750,000 | 68,000,000 | ||||||

| Total investments and repurchase agreements at value | 571,581,339 | 497,066,861 | ||||||

| Cash | 265,178 | — | ||||||

| RECEIVABLES: | ||||||||

| Interest | 603,788 | 1,053,736 | ||||||

| Investment securities sold | 3,817 | 14,441 | ||||||

| TBA investment securities sold | — | 35,423,733 | ||||||

| Other assets | 57,706 | 27,759 | ||||||

| Total Assets | 572,511,828 | 533,586,530 | ||||||

| LIABILITIES: | ||||||||

| PAYABLES: | ||||||||

| Dividends | 637,221 | 440,352 | ||||||

| Investment securities purchased | — | 25,156,163 | ||||||

| TBA investment securities purchased | — | 76,059,201 | ||||||

| Advisory fees | 61,719 | 49,586 | ||||||

| Administration fees | 25,304 | 18,891 | ||||||

| Distribution fees | 2,684 | 1,940 | ||||||

| Trustees’ fees | 8 | 5 | ||||||

| Accrued expenses | 126,333 | 88,881 | ||||||

| Total Liabilities | 853,269 | 101,815,019 | ||||||

| NET ASSETS | $ | 571,658,559 | $ | 431,771,511 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid-in capital | $ | 609,942,503 | $ | 493,173,190 | ||||

| Accumulated deficit | (38,283,944 | ) | (61,401,679 | ) | ||||

| NET ASSETS | $ | 571,658,559 | $ | 431,771,511 | ||||

| TCU Shares: | ||||||||

| Net assets | $ | 466,894,047 | $ | 356,187,421 | ||||

| Total shares outstanding, $0.001 par value (unlimited number of shares authorized) | 50,693,943 | 38,612,956 | ||||||

| Net asset value, offering price and redemption | ||||||||

| price per share (net assets/shares outstanding) | $ | 9.21 | $ | 9.22 | ||||

| Investor Shares: | ||||||||

| Net assets | $ | 104,764,512 | $ | 75,584,090 | ||||

| Total shares outstanding, $0.001 par value (unlimited number of shares authorized) | 11,378,470 | 8,189,457 | ||||||

| Net asset value, offering price and redemption | ||||||||

| price per share (net assets/shares outstanding) | $ | 9.21 | $ | 9.23 | ||||

See accompanying notes to financial statements.

21

TRUST FOR CREDIT UNIONS

Statements of Operations

For the Year Ended August 31, 2022

| Ultra-Short | Short | |||||||

| Duration | Duration | |||||||

| Portfolio | Portfolio | |||||||

| INVESTMENT INCOME: | ||||||||

| Interest | $ | 5,272,051 | $ | 7,694,570 | ||||

| EXPENSES: | ||||||||

| Advisory fees | 1,737,921 | 1,050,560 | ||||||

| Administration fees | 1,080,835 | 524,353 | ||||||

| Accounting fees | 550,220 | 293,091 | ||||||

| Distribution and Service (12b-1) Fees on Investor Shares | 315,398 | 108,193 | ||||||

| Legal fees | 210,712 | 103,924 | ||||||

| Trustees' fees | 200,233 | 98,417 | ||||||

| Transfer agent fees | 152,570 | 84,398 | ||||||

| Compliance fees | 123,303 | 63,023 | ||||||

| Custody fees | 94,603 | 51,050 | ||||||

| Interest expense | 76,151 | 37,995 | ||||||

| Audit and tax fees | 24,991 | 24,991 | ||||||

| Registration fees | 22,511 | 21,331 | ||||||

| Printing fees | 5,224 | 3,378 | ||||||

| Other expenses | 135,929 | 64,180 | ||||||

| Net operating expenses | 4,730,601 | 2,528,884 | ||||||

| Net Investment Income | 541,450 | 5,165,686 | ||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | ||||||||

| Net realized loss on investment transactions | (9,669,436 | ) | (29,890,222 | ) | ||||

| Net change in unrealized appreciation (depreciation) of: | ||||||||

| Investments | (17,006,407 | ) | (29,506,643 | ) | ||||

| Net Realized and Unrealized Loss on Investments | (26,675,843 | ) | (59,396,865 | ) | ||||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS: | $ | (26,134,393 | ) | $ | (54,231,179 | ) | ||

See accompanying notes to financial statements.

22

TRUST FOR CREDIT UNIONS

Statements of Changes in Net Assets

| Ultra-Short Duration Portfolio | Short Duration Portfolio | |||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | |||||||||||||

| August 31, 2022 | August 31, 2021 | August 31, 2022 | August 31, 2021 | |||||||||||||

| Investment Activities: | ||||||||||||||||

| Operations: | ||||||||||||||||

| Net investment income | $ | 541,450 | $ | 6,492,631 | $ | 5,165,686 | $ | 3,819,874 | ||||||||

| Net realized gain (loss) | ||||||||||||||||

| on investment transactions | (9,669,436 | ) | 352,841 | (29,890,222 | ) | 3,265,308 | ||||||||||

| Net change in unrealized appreciation | ||||||||||||||||

| (depreciation) of investments | (17,006,407 | ) | 1,329,797 | (29,506,643 | ) | (7,824,812 | ) | |||||||||

| Net increase (decrease) in net assets | ||||||||||||||||

| resulting from operations | (26,134,393 | ) | 8,175,269 | (54,231,179 | ) | (739,630 | ) | |||||||||

| Distributions to Shareholders: | ||||||||||||||||

| Dividends and distributions to shareholders | ||||||||||||||||

| TCU Shares | (3,643,894 | ) | (3,487,534 | ) | (5,244,302 | ) | (4,920,730 | ) | ||||||||

| Investor Shares | (2,478,607 | ) | (4,416,618 | ) | (2,080,511 | ) | (2,730,824 | ) | ||||||||

| Total Distributions | (6,122,501 | ) | (7,904,152 | ) | (7,324,813 | ) | (7,651,554 | ) | ||||||||

| From Shares Transactions: | ||||||||||||||||

| TCU Shares: | ||||||||||||||||

| Proceeds from sale of shares | 35,500,000 | 824,617,066 | 283,849,220 | 259,000,000 | ||||||||||||

| Reinvestment of dividends and distributions | 1,769,335 | 2,233,087 | 2,436,377 | 2,266,877 | ||||||||||||

| Cost of shares repurchased | (1,031,267,632 | ) | (95,042,735 | ) | (691,021,045 | ) | (43,688,555 | ) | ||||||||