UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05426

AIM Investment Funds (Invesco Investment Funds)

(Exact name of registrant as specified in charter)

11 Greenway Plaza, Suite 1000 Houston, Texas 77046

(Address of principal executive offices) (Zip code)

Sheri Morris 11 Greenway Plaza, Suite 1000 Houston, Texas 77046

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713)626-1919

Date of fiscal year end: 10/31

Date of reporting period: 10/31/19

The Registrant is filing this amendment to its FormN-CSR for the period ended October 31, 2019, originally filed with the Securities and Exchange Commission on January 3, 2020 (AccessionNo. 0001193125-20-001332). The sole purpose of this amendment is to amend the date of the Report of Independent Registered Public Accounting Firm in the “Item 1 ‘Report to Stockholders’” for Invesco Multi-Asset Income Fund. Except for such change, this amendment does not amend, update or change any other items or disclosures found in the original FormN-CSR filing nor does it reflect events occurring after the filing of the original FormN-CSR.

Items 1 (amended further herein) through 13(a)(1), and Item 13(a)(4) to this FormN-CSR are incorporated by reference to the FormN-CSR filed with the Securities and Exchange Commission on January 3, 2020 (AccessionNo. 0001193125-20-001332).”

| Item 1. | Reports to Stockholders. |

| | | | |

| | |

| | Annual Report to Shareholders | | October 31, 2019 |

| | |

| | Invesco Multi-Asset Income Fund Nasdaq: A: PIAFX∎ C: PICFX∎ R: PIRFX∎ Y: PIYFX∎ R5: IPNFX∎ R6: PIFFX |

Letters to Shareholders

| | |

Andrew Schlossberg | | Dear Shareholders: This annual report includes information about your Fund, including performance data and a complete list of its investments as of the close of the reporting period. Inside is a discussion of how your Fund was managed and the factors that affected its performance during the reporting period. Despite marked market volatility along the way, most global equity markets produced solid gains for the reporting period. As the reporting period unfolded in the final months of 2018, global equities were reeling from a sharpsell-off. The catalyst for thesell-off was a combination of ongoing trade concerns between the US and China, fears of a global economic slowdown and lower oil prices from a supply glut. Gains posted earlier in 2018 for global equities were erased, while US Treasury bonds, along with government and municipal bonds, rallied as investors fled to “safe haven” assets. |

At the start of 2019, global equity markets rebounded strongly buoyed by more policy from central banks and optimism about a potentialUS-China trade deal. In May,US-China trade concerns and slowing global growth led to a global equitysell-off and rally in US Treasuries. Despite the Maysell-off, domestic equity markets rallied in June in anticipation of a US Federal Reserve (the Fed) interest rate cut and closed the second quarter with modest gains. ContinuedUS-China trade worries and signs of slowing global economic growth left global equity markets largely flat for the third quarter. As the reporting period came to a close in October 2019, a raft of upbeat positive corporate earnings results and a US interest rate cut buoyed domestic equity results with some domestic indices recording record highs.

The Fed, in fact, both raised and lowered the federal funds rate during the reporting period. Given signs of a strong economy, the Fed raised rates in December 2018. In 2019, however, the Fed altered its outlook on further rate hikes leaving rates unchanged for the first half of the year. In July, the Fed lowered interest rates for the first time in 11 years. It again lowered rates in September and once again in October. As the year continues to unfold, we’ll see how the interplay of interest rates, economic data, geopolitics and a host of other factors affect US and overseas equity and fixed income markets.

Investor uncertainty and market volatility, such as we witnessed during the reporting period, are unfortunate facts of life when it comes to investing. That’s why Invesco encourages investors to work with a professional financial adviser who can stress the importance of starting to save and invest early and the importance of adhering to a disciplined investment plan. A financial adviser who knows your unique financial situation, investment goals and risk tolerance can be an invaluable partner as you seek to achieve your financial goals. He or she can offer a long-term perspective when markets are volatile and timetested advice and guidance when your financial situation or investment goals change.

Visit our website for more information on your investments

Our website, invesco.com/us, offers a wide range of market insights and investment perspectives. On the website, you’ll find detailed information about our funds, including performance, holdings and portfolio manager commentaries. You can access information about your account by completing a simple, secure online registration. To do so, select “Log In” on the right side of the homepage, and then select “Register for Individual Account Access.”

In addition to the resources accessible on our website and through our mobile app, you can obtain timely updates to help you stay informed about the markets and the economy by connecting with Invesco on Twitter, LinkedIn or Facebook. You can access our blog at blog.invesco.us.com. Our goal is to provide you the information you want, when and where you want it.

Finally, I’m pleased to share with you Invesco’s commitment to both the Principles for Responsible Investment and to considering environmental, social and governance issues in our robust investment process. I invite you to learn more at invesco.com/esg.

Have questions?

For questions about your account, contact an Invesco client services representative at 800 959 4246.

All of us at Invesco look forward to serving your investment management needs. Thank you for investing with us.

Sincerely,

Andrew Schlossberg

Head of the Americas,

Senior Managing Director, Invesco Ltd.

|

| 2 Invesco Multi-Asset Income Fund |

| | |

Bruce Crockett | | Dear Shareholders: Among the many important lessons I’ve learned in more than 40 years in a variety of business endeavors is the value of a trusted advocate. As independent chair of the Invesco Funds Board, I can assure you that the members of the Board are strong advocates for the interests of investors in Invesco’s mutual funds. We work hard to represent your interests through oversight of the quality of the investment management services your funds receive and other matters important to your investment, including but not limited to: ∎ Ensuring that Invesco offers a diverse lineup of mutual funds that your financial adviser can use to strive to meet your financial needs as your investment goals change over time. ∎ Monitoring how the portfolio management teams of the Invesco funds are performing in light of changing economic and market conditions. |

∎ Assessing each portfolio management team’s investment performance within the context of the investment strategy described in the fund’s prospectus.

∎ Monitoring for potential conflicts of interests that may impact the nature of the services that your funds receive.

We believe one of the most important services we provide our fund shareholders is the annual review of the funds’ advisory andsub-advisory contracts with Invesco Advisers and its affiliates. This review is required by the Investment Company Act of 1940 and focuses on the nature and quality of the services Invesco provides as the adviser to the Invesco funds and the reasonableness of the fees that it charges for those services. Each year, we spend months carefully reviewing information received from Invesco and a variety of independent sources, such as performance and fee data prepared by Lipper, Inc. (a subsidiary of Broadridge Financial Solutions, Inc.), an independent, third-party firm widely recognized as a leader in its field. We also meet with our independent legal counsel and other independent advisers to review and help us assess the information that we have received. Our goal is to assure that you receive quality investment management services for a reasonable fee.

I trust the measures outlined above provide assurance that you have a worthy advocate when it comes to choosing the Invesco Funds.

On behalf of the Board, we look forward to continuing to represent your interests and serving your needs.

Sincerely,

Bruce L. Crockett

Independent Chair

Invesco Funds Board of Trustees

|

| 3 Invesco Multi-Asset Income Fund |

Management’s Discussion of Fund Performance

| | | | | |

Performance summary | |

For the fiscal year ended October 31, 2019, Class A shares of Invesco Multi-Asset Income Fund (the Fund), at net asset value (NAV), underperformed the Custom Invesco Multi-Asset Income Index, the Fund’s style-specific benchmark. Your Fund’s long-term performance appears later in this report. | |

Fund vs. Indexes | |

Total returns, October 31, 2018 to October 31, 2019, at net asset value (NAV). Performance shown does not include applicable contingent deferred sales charges (CDSC) orfront-end sales charges, which would have reduced performance. | |

| |

Class A Shares | | | | 13.18% | |

Class C Shares | | | | 12.35 | |

Class R Shares | | | | 12.90 | |

Class Y Shares | | | | 13.47 | |

Class R5 Shares | | | | 13.46 | |

Class R6 Shares | | | | 13.47 | |

Bloomberg Barclays U.S. Aggregate Bond Index▼(Broad Market Index) | | | | 11.51 | |

Custom Invesco Multi-Asset Income Index⬛(Style-Specific Index) | | | | 13.23 | |

Lipper Mixed-Asset Target Allocation Conservative Funds Index◆(Peer Group Index) | | | | 8.95 | |

|

Source(s):▼RIMES Technologies Corp.;⬛Invesco, RIMES Technologies Corp.;◆Lipper Inc. | |

Market conditions and your Fund

The fiscal year ended October 31, 2019, provided a strong environment for Invesco Multi-Asset Income Fund as it reported positive absolute performance with all seven strategic asset classes in which the Fund invests posting positive returns. The fiscal year began with a general deterioration in US and international economic sentiment, inciting the US Federal Reserve (the Fed) to take a more accommodative monetary stance in the first quarter of 2019. This resulted in a decline in US Treasury yields and fueled the largest quarterly equity market rally since 2009.1 The decrease in interest rates was the primary driver of performance for each of the Fund’s strategic asset classes for the fiscal year. Results were led by US preferred equity securities, emerging market debt, US high yield debt and US Treasuries. There were no detractors from the Fund’s performance

for the fiscal year, as the tactical overlay also contributed to performance.

Exposure to US preferred equity securities was the top contributor to the Fund’s performance for the fiscal year. The asset class started the fiscal year off strong, rebounding from losses in the previous months that had resulted from increases in the federal funds rate. The Fed raised interest rates in December 2018, then held steady before changing course and issuing a rate cut in July 2019.2 Two more rate cuts followed in September and October2, benefiting asset classes that are sensitive to interest rate changes. US Treasuries also contributed to the Fund’s performance for the fiscal year, having been positively impacted by lower rates.

During the fiscal year, emerging market debt exposure also contributed to the Fund’s performance. The asset class recovered from losses in the previous fiscal

year as low to negative yields across developed markets drove investors into riskier assets. Asset class performance is correlated to the strength of the US dollar, as a strengthening US dollar makes it more expensive for foreign governments to service US dollar-denominated debt. The lowering of interest rates helped cap further strengthening of the dollar. The asset class was challenged in the middle of the fiscal year, as results from the Argentinian elections suggested a return to a populist government, spooking investors. However, the gains outweighed the losses during the fiscal year.

Exposure to high yield securities also contributed to the Fund’s results for the fiscal year, largely due to yield spreads between high yield and US Treasuries widening from the Fed lowering interest rates. The asset class started the fiscal year on weak footing following a period of tightening financial conditions and global growth fears. It then bounced back at the beginning of 2019, following reports of strong corporate earnings, a rebound of the equity markets and oil prices, and easing China and US trade tensions. Positive performance in the asset class continued through the fiscal year as the Fed pivoted toward easier monetary policy.

Exposure to interest rate-sensitive US real estate investment trusts (REITs) – both mortgage and equity REITs – contributed to the Fund’s performance after beginning the fiscal year significantly lower. The fiscal year was plagued by trade uncertainty, slowing economic growth and geopolitical volatility coupled with a shift to an accommodative monetary policy. These conditions supported the performance of many income-oriented US REIT sectors over recent months and generally led US REITs to

| | |

Portfolio Composition |

By security type, based on Net Assets as of October 31, 2019 | | |

| |

U.S. Dollar Denominated Bonds & Notes | | 56.25% |

| Preferred Stocks | | 20.58 |

| Common Stocks & Other Equity Interests | | 7.23 |

| U.S. Treasury Securities | | 6.31 |

| Exchange-Traded Notes | | 1.79 |

| Exchange-Traded Funds | | 1.74 |

Security Types Each Less Than 1% of Portfolio | | 0.50 |

Money Market Funds Plus Other Assets Less Liabilities | | 5.60 |

| | |

Top Five Debt Issuers* |

| % of total net assets |

| |

1. U.S. Treasury | | 6.3% |

| |

2. GS Finance Corp. | | 4.0 |

| |

3. Royal Bank of Canada | | 3.8 |

| |

4. JPMorgan Chase Bank NA | | 2.4 |

| |

5. UBS AG | | 2.0 |

| | | | | |

Total Net Assets | | | $ | 769.5 million | |

| |

Total Number of Holdings* | | | | 753 | |

The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security.

The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security.

*Excluding money market fund holdings, if any.

Data presented here are as of October 31, 2019.

|

| 4 Invesco Multi-Asset Income Fund |

positive returns, broadly reflecting investor appetite for adding exposure to more defensive income-focused investments. Master Limited Partnerships (MLPs) also contributed to the Fund’s performance for the fiscal year due to rising energy prices and increased production coming out of the Permian basin.

The Fund’s tactical overlay, obtained through the use of futures, also contributed to results for the fiscal year. Overweight exposure to equities proved timely and outweighed gains from tactical bond exposure in aggregate during the fiscal year. The tactical overlay is designed to allow the Fund to adapt to short-term market dynamics by shifting the Fund’s sensitivity to equity (beta) or fixed income (duration) markets. The tactical process is implemented by buying or selling futures on six global equity markets (Europe, Hong Kong, UK, USlarge-cap and USsmall-cap) and three global government bond markets (UK, Germany and the US), which serve as proxies for equity and fixed income risk metrics, beta and duration. The benefit of a tactical overlay is that the Fund can adjust the beta and duration of the portfolio without adjusting the seven strategic assets and disrupting the income stream.

The landscape at the close of the fiscal year placed the upcoming Brexit deadline, geopolitical tensions in the Middle East, turmoil in Hong Kong and the lack of resolution to the US and China trade dispute at the forefront of catalysts for potential market volatility. Meanwhile, it is our view that shift in monetary policy during the fiscal year could lead to an expansion in total size of assets by central banks. The question that arises is whether these actions are going to achieve the intended effect of stimulating inflation, and if not, will fiscal stimulus be deployed.

Please note that our strategy utilizes derivative instruments that include futures and total return swaps. Therefore, some of the performance of the strategy, both positive and negative, can be attributed to these instruments. Derivatives can be a cost-effective way to gain exposure to asset classes. However, derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities.

Thank you for your continued investment in Invesco Multi-Asset Income Fund.

1 Source: US Department of the Treasury

2 Source: US Federal Reserve

Portfolio Managers:

Mark Ahnrud

Chris Devine

Scott Hixon

Peter Hubbard

Christian Ulrich

Scott Wolle - Lead

The views and opinions expressed in management’s discussion of Fund performance are those of Invesco Advisers, Inc. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

See important Fund and, if applicable, index disclosures later in this report.

|

| 5 Invesco Multi-Asset Income Fund |

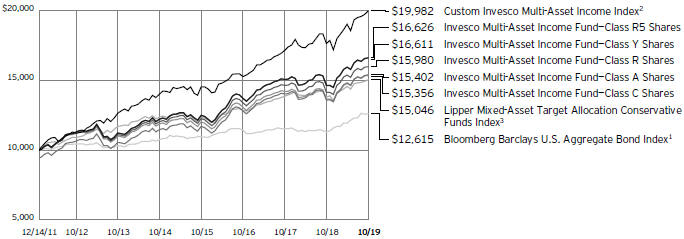

Your Fund’s Long-Term Performance

Results of a $10,000 Investment – Oldest Share Class(es) since Inception

Fund and index data from 12/14/11

1 Source: RIMES Technologies Corp.

2 Sources: Invesco, RIMES Technologies Corp.

3 Source: Lipper Inc.

Past performance cannot guarantee comparable future results.

The data shown in the chart include reinvested distributions, applicable sales charges and Fund expenses including

management fees. Index results include reinvested dividends, but they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses and management fees; performance

of a market index does not. Performance shown in the chart does not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares.

|

| 6 Invesco Multi-Asset Income Fund |

| | | | | |

Average Annual Total Returns | |

As of 10/31/19, including maximum applicable sales charges | |

| |

Class A Shares | | | | | |

Inception (12/14/11) | | | | 5.63 | % |

5 Years | | | | 4.88 | |

1 Year | | | | 6.92 | |

| |

Class C Shares | | | | | |

Inception (12/14/11) | | | | 5.59 | % |

5 Years | | | | 5.27 | |

1 Year | | | | 11.35 | |

| |

Class R Shares | | | | | |

Inception (12/14/11) | | | | 6.13 | % |

5 Years | | | | 5.82 | |

1 Year | | | | 12.90 | |

| |

Class Y Shares | | | | | |

Inception (12/14/11) | | | | 6.65 | % |

5 Years | | | | 6.33 | |

1 Year | | | | 13.47 | |

| |

Class R5 Shares | | | | | |

Inception (12/14/11) | | | | 6.66 | % |

5 Years | | | | 6.35 | |

1 Year | | | | 13.46 | |

| |

Class R6 Shares | | | | | |

Inception | | | | 6.63 | % |

5 Years | | | | 6.33 | |

1 Year | | | | 13.47 | |

| | | | | |

Average Annual Total Returns | |

As of 9/30/19, the most recent calendar quarter end, including maximum applicable sales charges | |

| |

Class A Shares | | | | | |

Inception (12/14/11) | | | | 5.67 | % |

5 Years | | | | 5.11 | |

1 Year | | | | 1.87 | |

| |

Class C Shares | | | | | |

Inception (12/14/11) | | | | 5.63 | % |

5 Years | | | | 5.51 | |

1 Year | | | | 6.03 | |

| |

Class R Shares | | | | | |

Inception (12/14/11) | | | | 6.17 | % |

5 Years | | | | 6.06 | |

1 Year | | | | 7.56 | |

| |

Class Y Shares | | | | | |

Inception (12/14/11) | | | | 6.69 | % |

5 Years | | | | 6.58 | |

1 Year | | | | 8.10 | |

| |

Class R5 Shares | | | | | |

Inception (12/14/11) | | | | 6.70 | % |

5 Years | | | | 6.60 | |

1 Year | | | | 8.10 | |

| |

Class R6 Shares | | | | | |

Inception | | | | 6.67 | % |

5 Years | | | | 6.58 | |

1 Year | | | | 8.00 | |

Class R6 shares incepted on September 24, 2012. Performance shown prior to that date is that of Class A shares and includes the12b-1 fees applicable to Class A shares.

The performance data quoted represent past performance and cannot guarantee comparable future results; current performance may be lower or higher. Please visit invesco.com/ performance for the most recentmonth-end performance. Performance figures reflect reinvested distributions, changes in net asset value and the effect of the maximum sales charge unless otherwise stated. Performance figures do not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares.

The net annual Fund operating expense ratio set forth in the most recent Fund prospectus as of the date of this report for Class A, Class C, Class R, Class Y, Class R5 and Class R6 shares was 0.85%, 1.60%, 1.10%, 0.60%, 0.60% and 0.60%, respectively.1 The total annual Fund operating expense ratio set forth in the

most recent Fund prospectus as of the date of this report for Class A, Class C, Class R, Class Y, Class R5 and Class R6 shares was 1.01%, 1.76%, 1.26%, 0.76%, 0.70% and 0.64%, respectively. The expense ratios presented above may vary from the expense ratios presented in other sections of this report that are based on expenses incurred during the period covered by this report.

Class A share performance reflects the maximum 5.50% sales charge, and Class C share performance reflects the applicable contingent deferred sales charge (CDSC) for the period involved. The CDSC on Class C shares is 1% for the first year after purchase. Class R, Class Y, Class R5 and Class R6 shares do not have afront-end sales charge or a CDSC; therefore, performance is at net asset value.

The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses.

Fund performance reflects any applicable fee waivers and/or expense reimbursements. Had the adviser not waived fees and/or reimbursed expenses currently or in the past, returns

would have been lower. See current prospectus for more information.

| 1 | Total annual Fund operating expenses after any contractual fee waivers and/or expense reimbursements by the adviser in effect through at least February 28, 2021. See current prospectus for more information. |

|

| 7 Invesco Multi-Asset Income Fund |

Invesco Multi-Asset Income Fund’s investment objective is to provide current income.

| ∎ | | Unless otherwise stated, information presented in this report is as of October 31, 2019, and is based on total net assets. |

| ∎ | | Unless otherwise noted, all data provided by Invesco. |

| ∎ | | To access your Fund’s reports/prospectus, visit invesco.com/fundreports. |

About share classes

| ∎ | | Class R sharesare generally available only to employer sponsored retirement and benefit plans. Please see the prospectus for more information. |

| ∎ | | Class Y sharesare available only to certain investors. Please see the prospectus for more information. |

| ∎ | | Class R5 sharesandClass R6 sharesare available for use by retirement plans that meet certain standards and for institutional investors. Class R6 shares are also available through intermediaries that have established an agreement with Invesco Distributors, Inc. to make such shares available for use in retail omnibus accounts. Please see the prospectus for more information. |

Principal risks of investing in the Fund

| ∎ | | Bank loan risk.There are a number of risks associated with an investment in bank loans including credit risk, interest rate risk, liquidity risk and prepayment risk. Lack of an active trading market, restrictions on resale, irregular trading activity, wide bid/ask spreads and extended trade settlement periods may impair the Fund’s ability to sell bank loans within its desired time frame or at an acceptable price and its ability to accurately value existing and prospective investments. Extended trade settlement periods may result in cash not being immediately available to the Fund. As a result, the Fund may have to sell other investments or engage in borrowing transactions to raise cash to meet its obligations. The risk of holding bank loans is also directly tied to the risk of insolvency or bankruptcy of the issuing banks. These risks could cause the Fund to lose income or principal on a particular investment, which in turn could affect the Fund’s returns. The value of bank loans can be affected by and sensitive to changes in government regulation and to economic downturns in the United States and |

| | | abroad. Bank loans generally are floating rate loans, which are subject to interest rate risk as the interest paid on the floating rate loans adjusts periodically based on changes in widely accepted reference rates. |

| ∎ | | Changing fixed income market conditions risk.The current low interest rate environment was created in part by the Federal Reserve Board (FRB) and certain foreign central banks keeping the federal funds and equivalent foreign rates near historical lows. Increases in the federal funds and equivalent foreign rates may expose fixed income markets to heightened volatility and reduced liquidity for certain fixed income investments, particularly those with longer maturities. In addition, decreases in fixed income dealer market-making capacity may also potentially lead to heightened volatility and reduced liquidity in the fixed income markets. As a result, the value of the Fund’s investments and share price may decline. Changes in central bank policies could also result in higher than normal shareholder redemptions, which could potentially increase portfolio turnover and the Fund’s transaction costs. |

| ∎ | | Commodities tax risk.The tax treatment of commodity-linked derivative instruments may be adversely affected by changes in legislation, regulations or other legally binding authority. If, as a result of any such adverse action, the income of the Fund from certain commodity-linked derivatives was treated asnon-qualifying income, the Fund might fail to qualify as a regulated investment company and be subject to federal income tax at the Fund level. As a result of an announcement by the Internal Revenue Service (IRS), the Fund intends to invest in commodity-linked notes: (a) directly, relying on an opinion of counsel confirming that income from such investments should be qualifying income because such commodity-linked notes constitute securities under section 2(a)(36) of the 1940 Act or (b) |

|

This report must be accompanied or preceded by a currently effective Fund prospectus, which contains more complete information, including sales charges and expenses. Investors should read it carefully before investing. |

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| | indirectly through the Subsidiary. Should the IRS issue further guidance, or Congress enact legislation, that adversely affects the tax treatment of the Fund’s use of commodity-linked notes or the Subsidiary (which guidance might be applied to the Fund retroactively), it could, among other consequences, limit the Fund’s ability to pursue its investment strategy. |

| ∎ | | Commodity risk.The Fund may have investment exposure to the commodities markets and/or a particular sector of the commodities markets, which may subject the Fund to greater volatility than investments in traditional securities, such as stocks and bonds. Volatility in the commodities markets may be caused by changes in overall market movements, domestic and foreign political and economic events and policies, war, acts of terrorism, changes in domestic or foreign interest rates and/or investor expectations concerning interest rates, domestic and foreign inflation rates, investment and trading activities of mutual funds, hedge funds and commodities funds, and factors such as drought, floods, weather, livestock disease, embargoes, tariffs and other regulatory developments or supply and demand disruptions. Because the Fund’s performance may be linked to the performance of volatile commodities, investors should be willing to assume the risks of potentially significant fluctuations in the value of the Fund’s shares. |

| ∎ | | Credit linked notes risk.Risks of credit linked notes include those risks associated with the underlying reference obligation including but not limited to market risk, interest rate risk, credit risk, default risk and, in some cases, foreign currency risk. An investor in a credit linked note bears counterparty risk or the risk that the issuer of the credit linked note will default or become bankrupt and not make timely payment of principal and interest of the structured security. Credit linked notes may be less liquid than other |

|

| 8 Invesco Multi-Asset Income Fund |

| | investments and therefore harder to dispose of at the desired time and price. In addition, credit linked notes may be leveraged and, as a result, small changes in the value of the underlying reference obligation may produce disproportionate losses to the Fund. |

| ∎ | | Debt securities risk.The prices of debt securities held by the Fund will be affected by changes in interest rates, the creditworthiness of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing debt securities to fall and often has a greater impact on longer-duration debt securities and higher quality debt securities. Falling interest rates will cause the Fund to reinvest the proceeds of debt securities that have been repaid by the issuer at lower interest rates. Falling interest rates may also reduce the Fund’s distributable income because interest payments on floating rate debt instruments held by the Fund will decline. The Fund could lose money on investments in debt securities if the issuer or borrower fails to meet its obligations to make interest payments and/or to repay principal in a timely manner. Changes in an issuer’s financial strength, the market’s perception of such strength or in the credit rating of the issuer or the security may affect the value of debt securities. The Adviser’s credit analysis may fail to anticipate such changes, which could result in buying a debt security at an inopportune time or failing to sell a debt security in advance of a price decline or other credit event. |

| ∎ | | Derivatives risk.The value of a derivative instrument depends largely on (and is derived from) the value of an underlying security, currency, commodity, interest rate, index or other asset (each referred to as an underlying asset). In addition to risks relating to the underlying assets, the use of derivatives may include other, possibly greater, risks, including counterparty, leverage and liquidity risks. Counterparty risk is the risk that the counterparty to the derivative contract will default on its obligation to pay the Fund the amount owed or otherwise perform under the derivative contract. Derivatives create leverage risk because they do not require payment up front equal to the economic exposure created by holding a position in the derivative. As a result, an adverse change in the value of the |

| | underlying asset could result in the Fund sustaining a loss that is substantially greater than the amount invested in the derivative or the anticipated value of the underlying asset, which may make the Fund’s returns more volatile and increase the risk of loss. Derivative instruments may also be less liquid than more traditional investments and the Fund may be unable to sell or close out its derivative positions at a desirable time or price. This risk may be more acute under adverse market conditions, during which the Fund may be most in need of liquidating its derivative positions. Derivatives may also be harder to value, less tax efficient and subject to changing government regulation that could impact the Fund’s ability to use certain derivatives or their cost. Derivatives strategies may not always be successful. For example, derivatives used for hedging or to gain or limit exposure to a particular market segment may not provide the expected benefits, particularly during adverse market conditions. These risks are greater for the Fund than mutual funds that do not use derivative instruments or that use derivative instruments to a lesser extent than the Fund to implement their investment strategies. |

| ∎ | | Dividend paying security risk.Securities that pay high dividends as a group can fall out of favor with the market, causing such companies to underperform companies that do not pay high dividends. Also, changes in the dividend policies of such companies and the capital resources available for such companies’ dividend payments may affect the Fund. |

| ∎ | | Emerging markets securities risk.Emerging markets (also referred to as developing markets) are generally subject to greater market volatility, political, social and economic instability, uncertain trading markets and more governmental limitations on foreign investment than more developed markets. In addition, companies operating in emerging markets may be subject to lower trading volume and greater price fluctuations than companies in more developed markets. Securities law and the enforcement of systems of taxation in many emerging market countries may change quickly and unpredictably. In addition, investments in emerging markets securities |

| | may be subject to additional transaction costs, delays in settlement procedures, and lack of timely information. |

| ∎ | | Equity linked notes risk.ELNs may not perform as anticipated and could cause the Fund to realize significant losses including its entire principal investment. Other risks include those of underlying securities, as well as counterparty risk, liquidity risk and imperfect correlation between ELNs and the underlying securities. |

| ∎ | | Exchange-traded funds risk.In addition to the risks associated with the underlying assets held by the exchange-traded fund, investments in exchange-traded funds are subject to the following additional risks: (1) an exchange-traded fund’s shares may trade above or below its net asset value; (2) an active trading market for the exchange-traded fund’s shares may not develop or be maintained; (3) trading an exchange-traded fund’s shares may be halted by the listing exchange; (4) a passively managed exchange-traded fund may not track the performance of the reference asset; and (5) a passively managed exchange-traded fund may hold troubled securities. Investment in exchange-traded funds may involve duplication of management fees and certain other expenses, as the Fund indirectly bears its proportionate share of any expenses paid by the exchange-traded funds in which it invests. Further, certain exchange-traded funds in which the Fund may invest are leveraged, which may result in economic leverage, permitting the Fund to gain exposure that is greater than would be the case in anun-levered instrument and potentially resulting in greater volatility. |

| ∎ | | Exchange-traded notes risk.Exchange-traded notes are subject to credit risk, counterparty risk, and the risk that the value of the exchange-traded note may drop due to a downgrade in the issuer’s credit rating. The value of an exchange-traded note may also be influenced by time to maturity, level of supply and demand for the exchange-traded note, volatility and lack of liquidity in the underlying market, changes in the applicable interest rates, and economic, legal, political, or geographic events that affect the referenced underlying market or assets. The Fund will bear its proportionate share of any fees and expenses borne by an exchange-traded note in which it invests. For certain exchange-traded |

|

| 9 Invesco Multi-Asset Income Fund |

| | notes, there may be restrictions on the Fund’s right to redeem its investment, which is meant to be held until maturity. |

| ∎ | | Financial services sector risk.The Fund may be susceptible to adverse economic or regulatory occurrences affecting the financial services sector. Financial services companies are subject to extensive government regulation and are disproportionately affected by unstable interest rates, each of which could adversely affect the profitability of such companies. Financial services companies may also have concentrated portfolios, which makes them especially vulnerable to unstable economic conditions. |

| ∎ | | Foreign currency tax risk. If the US Treasury Department were to exercise its authority to issue regulations that exclude from the definition of “qualifying income” foreign currency gains not directly related to the Fund’s business of investing in securities, the Fund may be unable to qualify as a regulated investment company for one or more years. In this event, the Fund’s Board of Trustees may authorize a significant change in investment strategy or other action. |

| ∎ | | Foreign government debt risk.Investments in foreign government debt securities (sometimes referred to as sovereign debt securities) involve certain risks in addition to those relating to foreign securities or debt securities generally. The issuer of the debt or the governmental authorities that control the repayment of the debt may be unable or unwilling to repay principal or interest when due in accordance with the terms of such debt, and the Fund may have limited recourse in the event of a default against the defaulting government. Without the approval of debt holders, some governmental debtors have in the past been able to reschedule or restructure their debt payments or declare moratoria on payments. |

| ∎ | | Foreign securities risk.The Fund’s foreign investments may be adversely affected by political and social instability, changes in economic or taxation policies, difficulty in enforcing obligations, decreased liquidity or increased volatility. Foreign investments also involve the risk of the possible seizure, nationalization or expropriation of the issuer or foreign deposits (in which the Fund could lose its entire investments in a certain market) and the possible adoption of foreign |

| | | governmental restrictions such as exchange controls. Unless the Fund has hedged its foreign securities risk, foreign securities risk also involves the risk of negative foreign currency rate fluctuations, which may cause the value of securities denominated in such foreign currency (or other instruments through which the Fund has exposure to foreign currencies) to decline in value. Currency exchange rates may fluctuate significantly over short periods of time. Currency hedging strategies, if used, are not always successful. |

| ∎ | | High yield debt securities (junk bond) risk.Investments in high yield debt securities (“junk bonds”) and other lower-rated securities will subject the Fund to substantial risk of loss. These securities are considered to be speculative with respect to the issuer’s ability to pay interest and principal when due, are more susceptible to default or decline in market value and are less liquid than investment grade debt securities. Prices of high yield debt securities tend to be very volatile. |

| ∎ | | Indexing risk.Certain portions of the Fund’s assets are managed pursuant to an indexing approach (Indexed Assets) and, therefore, the adverse performance of a particular security necessarily will not result in the elimination of the security from the Indexed Assets. Ordinarily, the Fund will not sell portfolio securities of the Indexed Assets except to reflect additions or deletions of the securities that comprise the index the Fund seeks to track with respect to the Indexed Assets (Underlying Index), or as may be necessary to raise cash to pay Fund shareholders who sell Fund shares. As such, the Indexed Assets, and therefore the Fund, will be negatively affected by declines in the securities represented by the Underlying Index. Also, there is no guarantee that the Fund will be able to correlate the performance of the Indexed Assets with that of the Underlying Index. |

| ∎ | | Investment companies risk.Investing in other investment companies could result in the duplication of certain fees, including management and administrative fees, and may expose the Fund to the risks of owning the underlying investments that the other investment company holds. |

| ∎ | | Liquidity risk.The Fund may be unable to sell illiquid investments at the time or price it desires and, as a result, could lose its entire investment in |

| | | such investments. Liquid securities can become illiquid during periods of market stress. If a significant amount of the Fund’s securities become illiquid, the Fund may not be able to timely pay redemption proceeds and may need to sell securities at significantly reduced prices. |

| ∎ | | Management risk.Certain portions of the Fund’s assets are actively managed and depend heavily on the Adviser’s judgment about markets, interest rates or the attractiveness, relative values, liquidity, or potential appreciation of particular investments made for the Fund’s portfolio. The Fund could experience losses if these judgments prove to be incorrect. Because the Fund’s investment process relies heavily on its asset allocation process, market movements that are counter to the portfolio managers’ expectations may have a significant adverse effect on the Fund’s net asset value. Additionally, legislative, regulatory, or tax developments may adversely affect management of the Fund and, therefore, the ability of the Fund to achieve its investment objective. |

| ∎ | | Market risk.The market values of the Fund’s investments, and therefore the value of the Fund’s shares, will go up and down, sometimes rapidly or unpredictably. Market risk may affect a single issuer, industry or section of the economy, or it may affect the market as a whole. Individual stock prices tend to go up and down more dramatically than those of certain other types of investments, such as bonds. During a general downturn in the financial markets, multiple asset classes may decline in value. When markets perform well, there can be no assurance that specific investments held by the Fund will rise in value. |

| ∎ | | MLP risk.The Fund invests in securities of MLPs, which are subject to the following risks: |

| | - | Limited partner risk. An MLP is a public limited partnership or limited liability company taxed as a partnership under the Internal Revenue Code of 1986, as amended (the Code). Although the characteristics of MLPs closely resemble a traditional limited partnership, a major difference is that MLPs may trade on a public exchange or in theover-the-counter market. The risks of investing in an MLP are similar to those of investing in a partnership, including more flexible governance |

|

| 10 Invesco Multi-Asset Income Fund |

| | structures, which could result in less protection for investors than investments in a corporation. Investors in an MLP normally would not be liable for the debts of the MLP beyond the amount that the investor has contributed but investors may not be shielded to the same extent that a shareholder of a corporation would be. In certain circumstances, creditors of an MLP would have the right to seek return of capital distributed to a limited partner, which right would continue after an investor sold its investment in the MLP. In addition, MLP distributions may be reduced by fees and other expenses incurred by the MLP. |

| | - | Liquidity risk.The ability to trade on a public exchange or in theover-the-counter market provides a certain amount of liquidity not found in many limited partnership investments. However, MLP interests may be less liquid than conventional publicly traded securities and, therefore, more difficult to trade at desirable times and/or prices. |

| | - | Interest rate risk.MLPs generally are considered interest-rate sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns. |

| | - | General partner risk.The holder of the general partner or managing member interest can be liable in certain circumstances for amounts greater than the amount of the holder’s investment in the general partner or managing member. |

Additionally, if the Fund were to invest more than 25% of its total assets in MLPs that are taxed as partnerships this could cause the Fund to lose its status as regulated investment company under Subchapter M of the Code.

| ∎ | | MLP tax risk.MLPs taxed as partnerships do not pay US federal income tax at the partnership level, subject to the application of certain partnership audit rules. A change in current tax law, or a change in the underlying business mix of a given MLP, however, could result in an MLP being classified as a corporation for US federal income tax purposes, which would have the effect of reducing the amount of cash available for distribution by the MLP and, as a result, could result in a reduction of the value of the Fund’s investment, and consequently your investment in the Fund |

| | | and lower income. Each year, the Fund will send you an annual tax statement (Form 1099) to assist you in completing your federal, state and local tax returns. If an MLP in which the Fund invests amends its partnership tax return, the Fund will, when necessary, send you a corrected Form 1099, which could, in turn, require you to amend your federal, state or local tax returns. |

| ∎ | | Mortgage- and asset-backed securities risk.Mortgage- and asset-backed securities, including collateralized debt obligations and collateralized mortgage obligations, are subject to prepayment or call risk, which is the risk that a borrower’s payments may be received earlier or later than expected due to changes in prepayment rates on underlying loans. This could result in the Fund reinvesting these early payments at lower interest rates, thereby reducing the Fund’s income. Mortgage- and asset-backed securities also are subject to extension risk, which is the risk that an unexpected rise in interest rates could reduce the rate of prepayments, causing the price of the mortgage- and asset-backed securities and the Fund’s share price to fall. An unexpectedly high rate of defaults on the mortgages held by a mortgage pool may adversely affect the value of mortgage-backed securities and could result in losses to the Fund. Privately-issued mortgage-backed securities and asset-backed securities may be less liquid than other types of securities and the Fund may be unable to sell these securities at the time or price it desires. During periods of market stress or high redemptions, the Fund may be forced to sell these securities at significantly reduced prices, resulting in losses. Liquid privately-issued mortgaged-backed securities and asset-backed securities can become illiquid during periods of market stress. The Fund may invest in mortgage pools that include subprime mortgages, which are loans made to borrowers with weakened credit histories or with lower capacity to make timely payments on their mortgages. Liquidity risk is even greater for mortgage pools that include subprime mortgages. Privately issued mortgage-related securities are not subject to the same underwriting requirements as those with government or government-sponsored entity guarantees and, therefore, mortgage loans |

| | | underlying privately issued mortgage-related securities may have less favorable collateral, credit risk, liquidity risk or other underwriting characteristics, and wider variances in interest rate, term, size, purpose and borrower characteristics. |

| ∎ | | Non-correlation risk.The return of the Fund’s assets managed pursuant to an indexing approach (Indexed Assets) may not match the return of the index the Fund seeks to track with respect to the Indexed Assets (Underlying Index) for a number of reasons. For example, the Fund incurs operating expenses not applicable to the Underlying Index, and incurs costs in buying and selling securities, especially when rebalancing securities holdings to reflect changes in the Underlying Index. In addition, the performance of the Indexed Assets and the Underlying Index may vary due to asset valuation differences and differences between the Indexed Assets and the Underlying Index resulting from legal restrictions, costs or liquidity constraints. |

| ∎ | | Preferred securities risk.Preferred securities are subject to issuer-specific and market risks applicable generally to equity securities. Preferred securities also may be subordinated to bonds or other debt instruments, subjecting them to a greater risk ofnon-payment, may be less liquid than many other securities, such as common stocks, and generally offer no voting rights with respect to the issuer. |

| ∎ | | REIT risk/real estate risk.Investments in real estate related instruments may be affected by economic, legal, cultural, environmental or technological factors that affect property values, rents or occupancies of real estate related to the Fund’s holdings. Shares of real estate related companies, which tend to be small- andmid-cap companies, may be more volatile and less liquid. |

| ∎ | | Sampling risk.The Fund’s use of a sampling methodology with respect to assets managed pursuant to an indexing approach (Indexed Assets) may result in the Indexed Assets including a smaller number of securities than are in the index the Fund seeks to track with respect to the Indexed Assets (Underlying Index), and in the Indexed Assets including securities that are not included in the Underlying Index. As a result, an adverse development to an issuer of securities |

|

| 11 Invesco Multi-Asset Income Fund |

| | included in the Indexed Assets could result in a greater decline in the Fund’s NAV than would be the case if all of the securities in the Underlying Index were included in the Indexed Assets. The Fund’s use of a sampling methodology may also include the risk that the Indexed Assets may not track the return of the Underlying Index as well as they would have if the Indexed Assets included all of the securities in the Underlying Index. To the extent the assets in the Indexed Assets are smaller, these risks will be greater. |

| ∎ | | Short position risk.Because the Fund’s potential loss on a short position arises from increases in the value of the asset sold short, the Fund will incur a loss on a short position, which is theoretically unlimited, if the price of the asset sold short increases from the short sale price. The counterparty to a short position or other market factors may prevent the Fund from closing out a short position at a desirable time or price and may reduce or eliminate any gain or result in a loss. In a rising market, the Fund’s short positions will cause the Fund to underperform the overall market and its peers that do not engage in shorting. If the Fund holds both long and short positions, and both positions decline simultaneously, the short positions will not provide any buffer (hedge) from declines in value of the Fund’s long positions. Certain types of short positions involve leverage, which may exaggerate any losses, potentially more than the actual cost of the investment, and will increase the volatility of the Fund’s returns. |

| ∎ | | Subsidiary risk.By investing in the Subsidiary, the Fund is indirectly exposed to risks associated with the Subsidiary’s investments. The Subsidiary is not registered under the Investment Company Act of 1940, as amended (1940 Act), and, except as otherwise noted in this prospectus, is not subject to the investor protections of the 1940 Act. Changes in the laws of the United States and/or the Cayman Islands, under which the Fund and the Subsidiary, respectively, are organized, could result in the inability of the Fund and/or the Subsidiary to operate as described in this prospectus and the SAI, and could negatively affect the Fund and its shareholders. |

| ∎ | | US government obligations risk.Obligations of US government agencies and authorities receive varying levels of support and may not be backed by |

| | | the full faith and credit of the US government, which could affect the Fund’s ability to recover should they default. No assurance can be given that the US government will provide financial support to its agencies and authorities if it is not obligated by law to do so. |

About indexes used in this report

| ∎ | | TheBloomberg Barclays U.S. Aggregate Indexis an unmanaged index considered representative of the US investment grade, fixed-rate bond market. |

| ∎ | | TheCustom Invesco Multi-Asset Income Indexis composed of the following indexes: S&P 500 Index and Bloomberg Barclays U.S. Universal Index. |

| ∎ | | TheLipper Mixed-Asset Target Allocation Conservative Funds Indexis an unmanaged index considered representative of mixed-asset target allocation conservative funds tracked by Lipper. |

| ∎ | | TheS&P 500® Indexis an unmanaged index considered representative of the US stock market. |

| ∎ | | TheBloomberg Barclays U.S. Universal Indexis composed of US dollar-denominated, taxable bonds that are rated investment grade or below investment grade. |

| ∎ | | The Fund is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Fund may deviate significantly from the performance of the index(es). |

| ∎ | | A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

Other information

| ∎ | | The returns shown in management’s discussion of Fund performance are based on net asset values (NAVs) calculated for shareholder transactions. Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes, and as such, the NAVs for shareholder transactions and the returns based on those NAVs may differ from the NAVs and returns reported in the Financial Highlights. |

| ∎ | | Industry classifications used in this report are generally according to the Global Industry Classification Standard, which was developed by and is the exclusive property and a service mark of MSCI Inc. and Standard & Poor’s. |

|

| 12 Invesco Multi-Asset Income Fund |

Schedule of Investments(a)

October 31, 2019

| | | | | | | | |

| | | Principal

Amount | | | Value | |

U.S. Dollar Denominated Bonds & Notes-56.25% | |

| |

Aerospace & Defense-0.68% | | | | | |

| | |

Bombardier, Inc. (Canada), | | | | | | | | |

8.75%, 12/01/2021(b) | | $ | 138,000 | | | $ | 146,625 | |

5.75%, 03/15/2022(b) | | | 173,000 | | | | 170,405 | |

6.13%, 01/15/2023(b) | | | 516,000 | | | | 505,680 | |

7.50%, 03/15/2025(b) | | | 862,000 | | | | 827,520 | |

7.88%, 04/15/2027(b) | | | 253,000 | | | | 239,717 | |

TransDigm UK Holdings PLC, 6.88%, 05/15/2026 | | | 801,000 | | | | 857,070 | |

TransDigm, Inc., | | | | | | | | |

6.50%, 07/15/2024 | | | 245,000 | | | | 253,881 | |

6.50%, 05/15/2025 | | | 150,000 | | | | 156,188 | |

6.25%, 03/15/2026(b) | | | 833,000 | | | | 894,434 | |

Triumph Group, Inc., | | | | | | | | |

5.25%, 06/01/2022 | | | 350,000 | | | | 345,625 | |

7.75%, 08/15/2025 | | | 800,000 | | | | 802,000 | |

| | | | | | | | 5,199,145 | |

| |

Agricultural & Farm Machinery-0.12% | | | | | |

| | |

Titan International, Inc., 6.50%, 11/30/2023 | | | 1,100,000 | | | | 904,750 | |

| | |

Airlines-0.06% | | | | | | | | |

| | |

Air Canada (Canada), 7.75%, 04/15/2021(b) | | | 425,000 | | | | 457,406 | |

| | |

Alternative Carriers-0.28% | | | | | | | | |

| | |

CenturyLink, Inc., | | | | | | | | |

Series S, 6.45%, 06/15/2021 | | | 535,000 | | | | 564,425 | |

Series Y, 7.50%, 04/01/2024 | | | 677,000 | | | | 770,088 | |

Level 3 Financing, Inc.,

5.38%, 05/01/2025 | | | 496,000 | | | | 513,980 | |

5.25%, 03/15/2026 | | | 277,000 | | | | 289,811 | |

| | | | | | | | 2,138,304 | |

| |

Aluminum-0.04% | | | | | |

| | |

Novelis Corp., 6.25%, 08/15/2024(b) | | | 284,000 | | | | 298,200 | |

| | |

Apparel Retail-0.17% | | | | | | | | |

| | |

L Brands, Inc., | | | | | | | | |

| | |

5.63%, 02/15/2022 | | | 396,000 | | | | 418,275 | |

6.88%, 11/01/2035 | | | 270,000 | | | | 230,850 | |

6.75%, 07/01/2036 | | | 30,000 | | | | 25,050 | |

Michaels Stores, Inc., 8.00%, 07/15/2027(b) | | | 627,000 | | | | 621,326 | |

| | | | | | | | 1,295,501 | |

| |

Apparel, Accessories & Luxury Goods-0.09% | | | | | |

| | |

William Carter Co. (The), 5.63%, 03/15/2027(b) | | | 614,000 | | | | 656,980 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Asset Management & Custody Banks-0.12% | | | | | |

| | |

Prime Security Services Borrower, LLC/Prime Finance, Inc., | | | | | | | | |

9.25%, 05/15/2023(b) | | $ | 414,000 | | | $ | 436,304 | |

5.75%, 04/15/2026(b) | | | 198,000 | | | | 203,569 | |

RegionalCare Hospital Partners Holdings, Inc.,

8.25%, 05/01/2023(b) | | | 300,000 | | | | 320,437 | |

| | | | | | | | 960,310 | |

| |

Auto Parts & Equipment-0.10% | | | | | |

| | |

Dana, Inc., 5.50%, 12/15/2024 | | | 520,000 | | | | 536,250 | |

Flexi-Van Leasing, Inc., 10.00%, 02/15/2023(b) | | | 281,000 | | | | 268,355 | |

| | | | | | | | 804,605 | |

| |

Automobile Manufacturers-0.27% | | | | | |

| | |

Ford Motor Credit Co., LLC, | | | | | | | | |

5.60%, 01/07/2022 | | | 461,000 | | | | 486,076 | |

5.11%, 05/03/2029 | | | 479,000 | | | | 485,458 | |

J.B. Poindexter & Co., Inc., 7.13%, 04/15/2026(b) | | | 1,072,000 | | | | 1,122,920 | |

| | | | | | | | 2,094,454 | |

| |

Automotive Retail-0.40% | | | | | |

| | |

Capitol Investment Merger Sub 2 LLC, 10.00%, 08/01/2024(b) | | | 726,000 | | | | 749,595 | |

Lithia Motors, Inc., 5.25%, 08/01/2025(b) | | | 177,000 | | | | 186,071 | |

Murphy Oil USA, Inc., | | | | | | | | |

5.63%, 05/01/2027 | | | 590,000 | | | | 636,148 | |

4.75%, 09/15/2029 | | | 237,000 | | | | 247,961 | |

Penske Automotive Group, Inc., 5.50%, 05/15/2026 | | | 1,168,000 | | | | 1,224,940 | |

| | | | | | | | 3,044,715 | |

| |

Broadcasting-0.46% | | | | | |

| | |

AMC Networks, Inc., | | | | | | | | |

5.00%, 04/01/2024 | | | 404,000 | | | | 412,508 | |

4.75%, 08/01/2025 | | | 286,000 | | | | 289,933 | |

Clear Channel Worldwide Holdings, Inc.,

9.25%, 02/15/2024(b) | | | 1,013,000 | | | | 1,116,199 | |

Gray Television, Inc., 7.00%, 05/15/2027(b) | | | 449,000 | | | | 493,011 | |

iHeartCommunications, Inc., | | | | | | | | |

8.38%, 05/01/2027 | | | 515,000 | | | | 554,912 | |

5.25%, 08/15/2027(b) | | | 336,000 | | | | 347,491 | |

TV Azteca, S.A.B. de C.V. (Mexico), 8.25%, 08/09/2024(b) | | | 350,000 | | | | 329,879 | |

| | | | | | | | 3,543,933 | |

| | |

Building Products-0.06% | | | | | | | | |

| | |

Advanced Drainage Systems, Inc., 5.00%, 09/30/2027(b) | | | 84,000 | | | | 86,100 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

13 Invesco Multi-Asset Income Fund

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Building Products-(continued) | | | | | |

| | |

Standard Industries, Inc., 6.00%, 10/15/2025(b) | | $ | 384,000 | | | $ | 405,120 | |

| | | | | | | | 491,220 | |

| |

Cable & Satellite-1.91% | | | | | |

| | |

Altice Financing S.A. (Luxembourg), | | | | | | | | |

6.63%, 02/15/2023(b) | | | 400,000 | | | | 411,880 | |

7.50%, 05/15/2026(b) | | | 600,000 | | | | 639,000 | |

Altice Luxembourg S.A. (Luxembourg),

10.50%, 05/15/2027(b) | | | 410,000 | | | | 464,838 | |

CCO Holdings LLC/CCO Holdings Capital Corp., | | | | | | | | |

5.75%, 09/01/2023 | | | 510,000 | | | | 521,475 | |

5.75%, 02/15/2026(b) | | | 2,155,000 | | | | 2,281,067 | |

CSC Holdings, LLC, | | | | | | | | |

7.75%, 07/15/2025(b) | | | 340,000 | | | | 365,500 | |

10.88%, 10/15/2025(b) | | | 700,000 | | | | 791,235 | |

5.50%, 05/15/2026(b) | | | 415,000 | | | | 438,344 | |

6.50%, 02/01/2029(b) | | | 927,000 | | | | 1,039,978 | |

DISH DBS Corp., | | | | | | | | |

5.88%, 11/15/2024 | | | 2,145,000 | | | | 2,158,406 | |

7.75%, 07/01/2026 | | | 164,000 | | | | 165,861 | |

Hughes Satellite Systems Corp., | | | | | | | | |

7.63%, 06/15/2021 | | | 357,000 | | | | 385,560 | |

5.25%, 08/01/2026 | | | 686,000 | | | | 737,450 | |

Intelsat Jackson Holdings S.A. (Luxembourg), | | | | | | | | |

5.50%, 08/01/2023 | | | 1,077,000 | | | | 1,012,380 | |

8.00%, 02/15/2024(b) | | | 175,000 | | | | 180,950 | |

8.50%, 10/15/2024(b) | | | 404,000 | | | | 407,915 | |

9.75%, 07/15/2025(b) | | | 235,000 | | | | 245,208 | |

Telenet Finance Luxembourg Notes S.a r.l. (Belgium), 5.50%, 03/01/2028(b) | | | 200,000 | | | | 213,700 | |

UPC Holding B.V. (Netherlands), 5.50%, 01/15/2028(b) | | | 200,000 | | | | 204,500 | |

UPCB Finance IV Ltd. (Netherlands), 5.38%, 01/15/2025(b) | | | 400,000 | | | | 414,500 | |

Virgin Media Finance PLC (United Kingdom), 6.00%, 10/15/2024(b) | | | 400,000 | | | | 414,000 | |

Virgin Media Secured Finance PLC (United Kingdom), 5.50%, 08/15/2026(b) | | | 200,000 | | | | 210,750 | |

VTR Finance B.V. (Chile), 6.88%, 01/15/2024(b) | | | 539,000 | | | | 553,823 | |

Ziggo B.V. (Netherlands), 5.50%, 01/15/2027(b) | | | 400,000 | | | | 422,492 | |

| | | | | | | | 14,680,812 | |

| | |

Casinos & Gaming-0.60% | | | | | | | | |

| | |

Boyd Gaming Corp., | | | | | | | | |

6.38%, 04/01/2026 | | | 278,000 | | | | 296,417 | |

6.00%, 08/15/2026 | | | 180,000 | | | | 191,475 | |

Cirsa Finance International S.a.r.l (Spain), 7.88%, 12/20/2023(b) | | | 200,000 | | | | 212,154 | |

Codere Finance 2 (Luxembourg) S.A. (Spain), 7.63%,

11/01/2021(b) | | | 200,000 | | | | 172,887 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Casinos & Gaming-(continued) | | | | | |

| | |

Melco Resorts Finance Ltd. (Hong Kong), 5.63%, 07/17/2027(b) | | $ | 256,000 | | | $ | 267,640 | |

MGM China Holdings Ltd. (Macau), 5.88%, 05/15/2026(b) | | | 206,000 | | | | 218,360 | |

MGM Resorts International, | | | | | | | | |

6.63%, 12/15/2021 | | | 45,000 | | | | 48,881 | |

7.75%, 03/15/2022 | | | 150,000 | | | | 168,375 | |

4.63%, 09/01/2026 | | | 1,242,000 | | | | 1,307,205 | |

Scientific Games International, Inc., 10.00%, 12/01/2022 | | | 383,000 | | | | 394,969 | |

Studio City Finance Ltd. (Macau), 7.25%, 02/11/2024(b) | | | 447,000 | | | | 476,055 | |

Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp., | | | | | | | | |

5.50%, 03/01/2025(b) | | | 684,000 | | | | 728,460 | |

5.25%, 05/15/2027(b) | | | 150,000 | | | | 156,563 | |

| | | | | | | | 4,639,441 | |

| |

Coal & Consumable Fuels-0.12% | | | | | |

| | |

SunCoke Energy Partners L.P./SunCoke Energy Partners Finance Corp.,

7.50%, 06/15/2025(b) | | | 1,101,000 | | | | 941,355 | |

| |

Commodity Chemicals-0.17% | | | | | |

| | |

Koppers, Inc., 6.00%, 02/15/2025(b) | | | 506,000 | | | | 506,992 | |

Nufarm Australia Ltd./Nufarm Americas, Inc. (Australia), 5.75%, 04/30/2026(b) | | | 247,000 | | | | 249,470 | |

Olin Corp., 5.63%, 08/01/2029 | | | 521,000 | | | | 542,241 | |

| | | | | | | | 1,298,703 | |

| |

Communications Equipment-0.06% | | | | | |

| | |

CommScope Technologies LLC, 6.00%, 06/15/2025(b) | | | 503,000 | | | | 452,826 | |

| |

Construction & Engineering-0.09% | | | | | |

| | |

William Lyon Homes, Inc., | | | | | | | | |

6.00%, 09/01/2023 | | | 116,000 | | | | 120,640 | |

6.63%, 07/15/2027(b) | | | 533,000 | | | | 563,647 | |

| | | | | | | | 684,287 | |

| | |

Consumer Finance-0.47% | | | | | | | | |

| | |

Ally Financial, Inc., | | | | | | | | |

8.00%, 03/15/2020 | | | 280,000 | | | | 285,830 | |

5.13%, 09/30/2024 | | | 1,100,000 | | | | 1,211,331 | |

Navient Corp., | | | | | | | | |

8.00%, 03/25/2020 | | | 705,000 | | | | 721,744 | |

7.25%, 01/25/2022 | | | 230,000 | | | | 250,343 | |

7.25%, 09/25/2023 | | | 1,015,000 | | | | 1,112,673 | |

| | | | | | | | 3,581,921 | |

| | |

Copper-0.32% | | | | | | | | |

| | |

First Quantum Minerals Ltd. (Zambia), 7.50%, 04/01/2025(b) | | | 833,000 | | | | 838,206 | |

Freeport-McMoRan, Inc., 5.40%, 11/14/2034 | | | 1,010,000 | | | | 991,063 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

14 Invesco Multi-Asset Income Fund

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Copper-(continued) | | | | | | | | |

Taseko Mines Ltd. (Canada), 8.75%, 06/15/2022(b) | | $ | 746,000 | | | $ | 660,210 | |

| | | | | | | | 2,489,479 | |

|

Data Processing & Outsourced Services-0.07% | |

| | |

Cardtronics Inc./Cardtronics USA, Inc., 5.50%, 05/01/2025(b) | | | 515,000 | | | | 534,313 | |

| | |

Distributors-0.14% | | | | | | | | |

| | |

Core & Main Holdings L.P., 9.38% PIK Rate, 8.63% Cash Rate, 09/15/2024(b)(c) | | | 1,081,000 | | | | 1,079,649 | |

| | |

Diversified Banks-14.31% | | | | | | | | |

| | |

Barclays Bank PLC (United Kingdom), 7.63%, 11/21/2022 | | | 200,000 | | | | 223,843 | |

BNP Paribas Issuance B.V. (France), 6.64%, 11/22/2019(b) | | | 14,900,000 | | | | 14,974,236 | |

Citigroup Global Markets Holdings, Inc., 17.87%, 12/06/2019(b) | | | 15,300,000 | | | | 15,157,326 | |

Credit Agricole S.A. (France), 8.13%(b)(d) | | | 447,000 | | | | 536,429 | |

JPMorgan Chase Bank, N.A., Series EMV3, 0.00%, 11/08/2019(e) | | | 19,000,000 | | | | 18,261,677 | |

Royal Bank of Canada (Canada), | | | | | | | | |

7.58%, 11/15/2019 | | | 14,800,000 | | | | 14,873,738 | |

1.73%, 11/20/2019(b) | | | 14,900,000 | | | | 14,741,366 | |

Royal Bank of Scotland Group PLC (The) (United Kingdom), 6.13%, 12/15/2022 | | | 285,000 | | | | 311,019 | |

Societe Generale S.A. (France), 7.38%(b)(d) | | | 246,000 | | | | 259,530 | |

Standard Chartered PLC (United Kingdom), 7.50%(b)(d) | | | 207,000 | | | | 220,196 | |

Toronto-Dominion Bank (The) (Canada), 6.08%, 12/02/2019 | | | 15,300,000 | | | | 15,235,620 | |

UBS AG (Switzerland), 16.70%, 12/09/2019(b) | | | 15,300,000 | | | | 15,300,000 | |

| | | | | | | | 110,094,980 | |

| |

Diversified Capital Markets-1.90% | | | | | |

| | |

Credit Suisse AG (Switzerland), 9.00%, 11/12/2019 | | | 14,550,000 | | | | 14,641,436 | |

| | |

Diversified Chemicals-0.17% | | | | | | | | |

| | |

Braskem Netherlands Finance B.V. (Brazil), | | | | | | | | |

4.50%, 01/31/2030(b) | | | 355,000 | | | | 352,337 | |

5.88%, 01/31/2050(b) | | | 410,000 | | | | 408,155 | |

Chemours Co. (The), 7.00%, 05/15/2025 | | | 220,000 | | | | 212,850 | |

Trinseo Materials Operating S.C.A./Trinseo Materials Finance, Inc., 5.38%, 09/01/2025(b) | | | 354,000 | | | | 343,380 | |

| | | | | | | | 1,316,722 | |

| |

Diversified Metals & Mining-0.18% | | | | | |

| | |

Hudbay Minerals, Inc. (Canada), 7.63%, 01/15/2025(b) | | | 587,000 | | | | 600,574 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Diversified Metals & Mining-(continued) | | | | | |

| | |

Teck Resources Ltd. (Canada), 6.13%, 10/01/2035 | | $ | 390,000 | | | $ | 439,102 | |

Vedanta Resources Ltd. (India), 6.38%, 07/30/2022(b) | | | 350,000 | | | | 347,375 | |

| | | | | | | | 1,387,051 | |

| | |

Diversified REITs-0.16% | | | | | | | | |

| | |

Colony Capital, Inc., Conv., | | | | | | | | |

3.88%, 01/15/2021 | | | 31,000 | | | | 30,535 | |

5.00%, 04/15/2023 | | | 258,000 | | | | 252,546 | |

iStar, Inc., 4.75%, 10/01/2024 | | | 926,000 | | | | 957,253 | |

| | | | | | | | 1,240,334 | |

|

Diversified Support Services-0.06% | |

| | |

IAA, Inc., 5.50%, 06/15/2027(b) | | | 431,000 | | | | 462,851 | |

|

Electric Utilities-0.18% | |

| | |

DPL, Inc., 4.35%, 04/15/2029(b) | | | 339,000 | | | | 338,915 | |

NextEra Energy Capital Holdings, Inc., Series K, Investment Units, 5.25%, 06/01/2076 | | | 38,200 | | | | 1,038,276 | |

| | | | | | | | 1,377,191 | |

| |

Electrical Components & Equipment-0.09% | | | | | |

| | |

EnerSys, 5.00%, 04/30/2023(b) | | | 693,000 | | | | 718,121 | |

| |

Electronic Equipment & Instruments-0.10% | | | | | |

| | |

Itron, Inc., 5.00%, 01/15/2026(b) | | | 443,000 | | | | 459,612 | |

MTS Systems Corp., 5.75%, 08/15/2027(b) | | | 290,000 | | | | 304,500 | |

| | | | | | | | 764,112 | |

| |

Environmental & Facilities Services-0.07% | | | | | |

| | |

GFL Environmental, Inc. (Canada), 7.00%, 06/01/2026(b) | | | 156,000 | | | | 165,750 | |

Waste Pro USA, Inc., 5.50%, 02/15/2026(b) | | | 381,000 | | | | 395,287 | |

| | | | | | | | 561,037 | |

| |

Fertilizers & Agricultural Chemicals-0.06% | | | | | |

| | |

OCI N.V. (Netherlands), 6.63%, 04/15/2023(b) | | | 460,000 | | | | 481,735 | |

| |

Financial Exchanges & Data-0.03% | | | | | |

| | |

MSCI, Inc., 5.25%, 11/15/2024(b) | | | 185,000 | | | | 191,013 | |

| | |

Food Distributors-0.08% | | | | | | | | |

| | |

US Foods, Inc.,

5.88%, 06/15/2024(b) | | | 568,000 | | | | 587,170 | |

| | |

Food Retail-0.25% | | | | | | | | |

| | |

Albertsons Cos. LLC/Safeway, Inc./New Albertson’s, Inc./Albertson’s LLC, | | | | | | | | |

6.63%, 06/15/2024 | | | 737,000 | | | | 776,614 | |

7.50%, 03/15/2026(b) | | | 306,000 | | | | 341,573 | |

5.88%, 02/15/2028(b) | | | 341,000 | | | | 367,001 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

15 Invesco Multi-Asset Income Fund

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Food Retail-(continued) | | | | | |

| | |

Simmons Foods, Inc., 5.75%, 11/01/2024(b) | | $ | 419,000 | | | $ | 411,667 | |

| | | | | | | | 1,896,855 | |

| | |

Forest Products-0.06% | | | | | | | | |

| | |

Norbord, Inc. (Canada), 5.75%, 07/15/2027(b) | | | 425,000 | | | | 440,938 | |

| | |

Gas Utilities-0.22% | | | | | | | | |

| | |

AmeriGas Partners, L.P./AmeriGas Finance Corp., 5.88%, 08/20/2026 | | | 360,000 | | | | 400,500 | |

Suburban Propane Partners, L.P./Suburban Energy Finance Corp., 5.50%, 06/01/2024 | | | 1,222,000 | | | | 1,255,238 | |

| | | | | | | | 1,655,738 | |

| | |

Health Care Equipment-0.01% | | | | | | | | |

| | |

Teleflex, Inc., 4.88%, 06/01/2026 | | | 56,000 | | | | 58,993 | |

| | |

Health Care Facilities-0.87% | | | | | | | | |

| | |

Acadia Healthcare Co., Inc., 6.50%, 03/01/2024 | | | 575,000 | | | | 598,000 | |

Community Health Systems, Inc., | | | | | | | | |

6.25%, 03/31/2023 | | | 738,000 | | | | 721,856 | |

8.00%, 03/15/2026(b) | | | 373,000 | | | | 365,540 | |

HCA, Inc., | | | | | | | | |

7.50%, 02/15/2022 | | | 116,000 | | | | 128,992 | |

5.38%, 02/01/2025 | | | 270,000 | | | | 297,338 | |

5.25%, 04/15/2025 | | | 749,000 | | | | 836,454 | |

5.88%, 02/15/2026 | | | 790,000 | | | | 890,725 | |

5.38%, 09/01/2026 | | | 169,000 | | | | 184,633 | |

5.50%, 06/15/2047 | | | 878,000 | | | | 1,001,018 | |

Tenet Healthcare Corp., | | | | | | | | |

8.13%, 04/01/2022 | | | 350,000 | | | | 380,187 | |

6.75%, 06/15/2023 | | | 1,235,000 | | | | 1,313,731 | |

| | | | | | | | 6,718,474 | |

| | |

Health Care REITs-0.07% | | | | | | | | |

| | |

MPT Operating Partnership L.P./MPT Finance Corp., 5.00%, 10/15/2027 | | | 477,000 | | | | 504,428 | |

| | |

Health Care Services-0.47% | | | | | | | | |

| | |

Eagle Holding Co. II, LLC, 8.38% PIK Rate, 7.63% Cash Rate, 05/15/2022(b)(c) | | | 612,000 | | | | 618,885 | |

Envision Healthcare Corp., 8.75%, 10/15/2026(b) | | | 223,000 | | | | 126,553 | |

Hadrian Merger Sub, Inc., 8.50%, 05/01/2026(b) | | | 581,000 | | | | 573,011 | |

MPH Acquisition Holdings LLC, 7.13%, 06/01/2024(b) | | | 1,084,000 | | | | 1,016,250 | |

Polaris Intermediate Corp., 9.25% PIK Rate, 8.50% Cash Rate, 12/01/2022(b)(c) | | | 697,000 | | | | 588,965 | |

Surgery Center Holdings, Inc., 10.00%, 04/15/2027(b) | | | 365,000 | | | | 370,475 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Health Care Services-(continued) | | | | | |

| | |

Team Health Holdings, Inc., 6.38%, 02/01/2025(b) | | $ | 465,000 | | | $ | 302,250 | |

| | | | | | | | 3,596,389 | |

| | |

Home Improvement Retail-0.10% | | | | | | | | |

| | |

Hillman Group, Inc. (The), 6.38%, 07/15/2022(b) | | | 808,000 | | | | 747,400 | |

| | |

Homebuilding-0.46% | | | | | | | | |

| | |

Ashton Woods USA LLC/Ashton Woods Finance Co., 9.88%, 04/01/2027(b) | | | 472,000 | | | | 528,640 | |

Beazer Homes USA, Inc., 5.88%, 10/15/2027 | | | 72,000 | | | | 70,920 | |

KB Home, 8.00%, 03/15/2020 | | | 199,000 | | | | 203,537 | |

Lennar Corp., | | | | | | | | |

8.38%, 01/15/2021 | | | 50,000 | | | | 53,500 | |

5.38%, 10/01/2022 | | | 702,000 | | | | 753,772 | |

5.25%, 06/01/2026 | | | 255,000 | | | | 281,456 | |

Meritage Homes Corp., | | | | | | | | |

7.15%, 04/15/2020 | | | 65,000 | | | | 66,463 | |

6.00%, 06/01/2025 | | | 216,000 | | | | 242,460 | |

5.13%, 06/06/2027 | | | 250,000 | | | | 270,000 | |

PulteGroup, Inc., 6.38%, 05/15/2033 | | | 13,000 | | | | 14,853 | |

Taylor Morrison Communities, Inc., 5.75%, 01/15/2028(b) | | | 358,000 | | | | 396,932 | |

Taylor Morrison Communities, Inc./Taylor Morrison Holdings II, Inc., 5.88%, 04/15/2023(b) | | | 569,000 | | | | 617,365 | |

| | | | | | | | 3,499,898 | |

| | |

Household Products-0.36% | | | | | | | | |

| | |

Energizer Holdings, Inc., | | | | | | | | |

6.38%, 07/15/2026(b) | | | 85,000 | | | | 90,848 | |

7.75%, 01/15/2027(b) | | | 308,000 | | | | 341,880 | |

Reynolds Group Issuer, Inc./LLC, | | | | | | | | |

5.13%, 07/15/2023(b) | | | 41,000 | | | | 42,166 | |

7.00%, 07/15/2024(b) | | | 1,288,000 | | | | 1,335,495 | |

Spectrum Brands, Inc., 5.75%, 07/15/2025 | | | 935,000 | | | | 979,413 | |

| | | | | | | | 2,789,802 | |

|

Independent Power Producers & Energy Traders-0.28% | |

| | |

AES Corp. (The), 5.50%, 04/15/2025 | | | 279,000 | | | | 290,425 | |

Calpine Corp., | | | | | | | | |

5.38%, 01/15/2023 | | | 384,000 | | | | 391,181 | |

5.50%, 02/01/2024 | | | 400,000 | | | | 402,500 | |

NRG Energy, Inc., | | | | | | | | |

7.25%, 05/15/2026 | | | 200,000 | | | | 219,756 | |

6.63%, 01/15/2027 | | | 463,000 | | | | 503,512 | |

5.25%, 06/15/2029(b) | | | 340,000 | | | | 365,925 | |

| | | | | | | | 2,173,299 | |

| | |

Industrial Machinery-0.32% | | | | | | | | |

| | |

Cleaver-Brooks, Inc., 7.88%, 03/01/2023(b) | | | 963,000 | | | | 912,442 | |

EnPro Industries, Inc., 5.75%, 10/15/2026 | | | 737,000 | | | | 781,220 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

16 Invesco Multi-Asset Income Fund

| | | | | | | | |

| | | Principal

Amount | | | Value | |

Industrial Machinery-(continued) | | | | | |

| | |

Mueller Industries, Inc., 6.00%, 03/01/2027 | | $ | 780,000 | | | $ | 793,650 | |

| | | | | | | | 2,487,312 | |

|

Integrated Oil & Gas-0.11% | |

| | |

Petrobras Global Finance B.V. (Brazil), 5.75%, 02/01/2029 | | | 591,000 | | | | 658,728 | |

Petroleos Mexicanos (Mexico), 6.49%, 01/23/2027(b) | | | 197,000 | | | | 210,544 | |

| | | | | | | | 869,272 | |

|

Integrated Telecommunication Services-0.43% | |

| | |

Altice France S.A. (France), 7.38%, 05/01/2026(b) | | | 600,000 | | | | 644,007 | |

Cincinnati Bell, Inc., | | | | | | | | |