UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811-05426 |

|

AIM Investment Funds (Invesco Investment Funds) |

| (Exact name of registrant as specified in charter) |

|

11 Greenway Plaza, Suite 1000 Houston, Texas 77046 |

| (Address of principal executive offices) (Zip code) |

|

Sheri Morris 11 Greenway Plaza, Suite 1000 Houston, Texas 77046 |

| (Name and address of agent for service) |

| | | | |

| Registrant’s telephone number, including area code: | | (713) 626-1919 | | |

| | | | |

| Date of fiscal year end: | | 11/30 | | |

| | | | |

| Date of reporting period: | | 11/30/22 | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

(a) The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

(b) Not applicable.

| | | | |

| Annual Report to Shareholders | | | November 30, 2022 | |

| | | | |

| Invesco SteelPath MLP Alpha Fund | |

| |

| | | | |

| Nasdaq: | |

| A: MLPAX ∎ C: MLPGX ∎ R: SPMGX ∎ Y: MLPOX ∎ R5: SPMHX ∎ R6: OSPAX | |

Management’s Discussion of Fund Performance

| | | | |

| Performance summary | | | | |

For the fiscal year ended November 30, 2022, Class A shares of Invesco SteelPath MLP Alpha Fund (the Fund), at net asset value (NAV), outperformed the S&P 500® Index. Your Fund’s long-term performance appears later in this report. | |

| |

| | | | |

| | | | |

| Fund vs. Indexes | | | | |

| Total returns, 11/30/21 to 11/30/22, at net asset value (NAV). Performance shown does not include applicable contingent deferred sales charges (CDSC) or front-end sales charges, which would have reduced performance. | |

Class A Shares | | | 37.02 | % |

Class C Shares | | | 36.24 | |

Class R Shares | | | 36.99 | |

Class Y Shares | | | 37.55 | |

Class R5 Shares | | | 37.45 | |

Class R6 Shares | | | 37.59 | |

| S&P 500 Index | | | -9.21 | |

| Alerian MLP Index | | | 42.25 | |

| |

| Source(s): RIMES Technologies Corp. | | | | |

Fund Performance Discussion

The Fund’s Class A shares (without sales charge) produced a total return of 38.20% during the fiscal year ended November 30, 2022. In comparison, master limited partnerships (MLPs), as measured by the Alerian MLP Index (AMZ), generated a total return of 42.25% over the same period. Please note that the returns for the Alerian MLP Index are calculated pre-tax, while the Fund’s returns are calculated post corporate tax. During the same period, the S&P 500 Index produced a total return of -9.21%.

During the fiscal year the global equity markets were shaken by the Russian invasion of Ukraine, heightened inflation concerns, and rising interest rates. Commodity prices increased, generally driving most energy equity prices higher, midstream equities included. Further, efforts to replace Russian sourced natural gas sparked an increase in commitments to purchase US natural gas, or liquified natural gas, firming future natural gas demand expectations.

The sharp increase in the interest rate environment over the period did not appear to impact the midstream energy sector’s price performance materially. The sector has often traded well in rising rate environments despite the sector’s yield component. We believe it is also worth noting that many midstream contracts include annual rate adjustments linked to inflation indexes such as the Producer Price Index or the Consumer Price Index, which may mitigate the impacts of inflation or benefit cash flows in inflationary environments.

Despite the robust price performance, midstream equities continue to trade at discounted valuations relative to historical valuations. A number of sponsors or parent companies have elected to offer to repurchase their underlying midstream entities from the public markets. In 2022, through November, there were seven take-ins announced with a collective market

capitalization of more than $17 billion, which was in addition to several similar transactions in 2021. We estimate that, on average, sponsors paid an approximate 22% premium to the unaffected market price prior to the respective transaction announcements. In addition to sponsor acquisitions, many sector participants have begun executing, or announced plans for, share repurchases, reflecting additional insider investment at today’s valuation levels.

Over the fiscal year, we estimate that a de minimis amount of equity supply entered the market through secondary offerings, initial public offerings, preferred offerings, or at-the-market programs in which primary units trade into the market anonymously throughout the normal trading day. Conversely, Wells Fargo estimates that during the first three quarters of 2022 midstream companies collectively repurchased over $3 billion of equity.1 Midstream companies raised approximately $12 billion of debt capital during the period.1 Most midstream MLPs pay out substantial distributions to investors and, therefore, have historically raised external capital to fund larger growth projects or acquisitions. However, in recent years most sector participants have adjusted their business models to self-fund the equity portion of their investment plans.

Macro Review

West Texas Intermediate (WTI) crude oil prices ended the period at $80.55 per barrel, up 22% over the fiscal year, while global crude prices, as measured by Brent crude oil, traded 21% higher over the fiscal year. During the period crude prices traded well over $100 per barrel before drifting lower. Henry Hub natural gas prices exited November 2022 at $6.93 per million British thermal units, up 52% over the fiscal year after hitting an intra-period high of $10.03 driven by strong export demand resulting from actions associated with the Russia-Ukraine war. Regional price differentials

weakened in the Permian basin and Appalachia as production in each basin was nearing available takeaway capacity.

Mont Belvieu natural gas liquids (NGL) prices ended the fiscal year at $32.97 per barrel, a 14% decrease over the previous fiscal year though NGL pricing hit a decadal high of $59.53 per barrel during the period. Pricing for NGL purity products was mixed, with ethane ending the period 9% higher while butane pricing ended the period 28% lower. Frac spreads, a measure of natural gas processing economics, ended the period at $0.23 per gallon, down 36% over the fiscal year. Generally, the greater the frac spread, the greater the incentive for producers to seek natural gas processing capacity.

The yield curve inverted over the period as short rates rose more than the yields on longer-dated maturities. The 10-year Treasury yield rose by 216 basis points to end the period at 3.61%. The MLP yield spread at fiscal year-end, as measured by the AMZ and the 10-year Treasury bond, narrowed by 338 basis points to 3.44%.

Over the fiscal year, real estate investment trusts and utilities, two competing yield-oriented equity asset classes, posted total returns of -13.54% (as measured by the Dow Jones Equity REIT Total Return Index) and 13.60% (as measured by the Dow Jones Utility Average Index), respectively, as compared to the AMZ’s 42.25% total return.

Subsector Reviews

Performance for all subsectors in the midstream, or energy infrastructure, asset class was positive over the fiscal year. On average, sector participants in the Gathering and Processing subsector provided the best performance over the period supported by rising production volumes and attractive processing economics. The Petroleum Pipeline subsector also outperformed, also benefiting from increasing production volumes and generally improving demand.

The Propane subsector experienced the weakest, albeit positive, performance over the fiscal year given its modest exposure to resumed production growth and generally lower market beta. Similarly, the Other Energy subsector, which includes fuel distribution companies, also lagged the more production and beta sensitive subsectors over the reporting period.

Fund Review

Key contributors to the Invesco SteelPath MLP Alpha Fund for fiscal year ended November 30, 2022 were Energy Transfer, LP (NYSE: ET) and Western Midstream Partners, LP (NYSE: WES).

ET outperformed over the period after reporting strong earnings and increasing 2022 Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) guidance. Additionally, ET announced a dividend

2 Invesco SteelPath MLP Alpha Fund

growth plan with the stated goal of returning the distribution to the pre-pandemic level of $1.22 per unit by 2023. ET was well positioned with one of the largest and most diversified portfolios of midstream assets in the United States, with a strategic footprint in all the major domestic production basins.

WES benefited from better-than-expected financial and operating results, as well as stronger than expected stock buybacks, including a large unit repurchase from its sponsor, Occidental Petroleum (NYSE: OXY). WES is a crude and natural gas gathering and processing midstream company focused on the DJ basin and Permian basin.

Key detractors from the Invesco SteelPath MLP Alpha Fund during the fiscal year were Equitrans Midstream Corp. (NYSE: ETRN) and Kinder Morgan Inc. (NYSE: KMI).

ETRN shares underperformed over the period as legal headwinds associated with the company’s Mountain Valley Pipeline project continued. ETRN’s base business of natural gas gathering and transportation in the Appalachian basin remains strong. Its largest customer is EQT Corporation, the largest natural gas producer in the United States.

KMI shares underperformed over the period as the company faced modest headwinds from rising interest rates due to its floating rate debt and upcoming bond refinancings expected in 2023. KMI is one of the largest energy midstream companies in North America. The company owns and operates nearly 84,000 miles of pipelines and 152 terminals. KMI’s pipelines transport natural gas, refined petroleum products, crude oil, condensates and carbon dioxide. We sold our position in KMI during the fiscal year.

Outlook

Midstream companies are generating significantly more free cash flow today than just a few years ago. The midstream energy sector shift to free cash flow has occurred as most sector participants sought to achieve materially higher distribution coverage as well as to retain internal cash to meet capital spending goals and to reduce leverage. However, we believe sector leverage is now largely in line with company targets and, since capital spending plans for the sector have become relatively moderate, we believe we will likely expect to see cash increasingly directed to distribution/dividend increases or share buybacks.

Further, over the past several years, oil and gas producers, key customers of many midstream assets, have become, in our view, far more financially disciplined than in the past. Historically, today’s high pricing would entice oil and gas producers to massively increase capital spending, potentially resulting in a likewise massive cut to capital spending and balance sheet concerns should prices subsequently retreat. Today, capital spending is being restrained as producers remain

committed to achieving strong return metrics and returning profits to shareholders.

We believe this change in producer financial discipline is healthy for midstream as well. Ratable producer spending means midstream providers are not being asked to rapidly build new capacity that then may be underutilized after a retraction in commodity pricing. Also, should commodity pricing retreat, we believe producers’ spending is likely to be less impacted, which we expect would result in more stable midstream volumes than past periods of commodity price pullbacks.

Despite these macro and company fundamental improvements, midstream equities trade at valuations substantially below the five- and 10-year averages. Therefore, we continue to believe the sector may provide investors an attractive yield and total return experience over the coming years despite the looming threat of a potential recession.

All data, unless otherwise noted, sourced from Bloomberg LP as of 11/30/2022.

1 Source: Wells Fargo, as of 11/30/2022

Portfolio managers:

Stuart Cartner

Brian Watson

The views and opinions expressed in management’s discussion of Fund performance are those of Invesco Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

See important Fund and, if applicable, index disclosures later in this report.

3 Invesco SteelPath MLP Alpha Fund

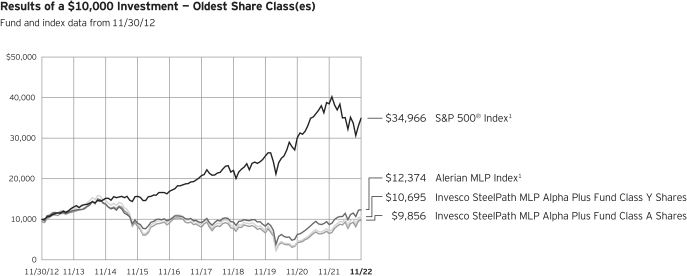

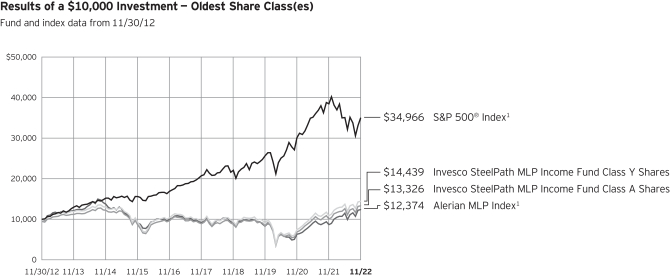

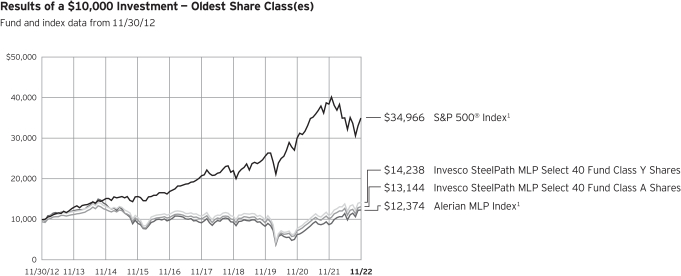

Your Fund’s Long-Term Performance

1 Source: RIMES Technologies Corp.

Past performance cannot guarantee future results.

The data shown in the chart include reinvested distributions, applicable sales charges and Fund expenses including

management fees. Index results include reinvested dividends, but they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses and management fees;

performance of a market index does not. Performance shown in the chart does not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares.

4 Invesco SteelPath MLP Alpha Fund

| | | | |

| Average Annual Total Returns | | | | |

| As of 11/30/22, including maximum applicable sales charges | |

Class A Shares | | | | |

Inception (3/31/10) | | | 3.29 | % |

10 Years | | | 1.68 | |

5 Years | | | 4.14 | |

1 Year | | | 30.47 | |

Class C Shares | | | | |

Inception (8/25/11) | | | 2.79 | % |

10 Years | | | 1.64 | |

5 Years | | | 4.50 | |

1 Year | | | 36.04 | |

Class R Shares | | | | |

10 Years | | | 1.97 | % |

5 Years | | | 5.00 | |

1 Year | | | 37.94 | |

Class Y Shares | | | | |

Inception (3/31/10) | | | 4.00 | % |

10 Years | | | 2.50 | |

5 Years | | | 5.58 | |

1 Year | | | 38.67 | |

Class R5 Shares | | | | |

10 Years | | | 2.35 | % |

5 Years | | | 5.51 | |

1 Year | | | 38.61 | |

Class R6 Shares | | | | |

Inception (6/28/13) | | | 1.11 | % |

5 Years | | | 5.63 | |

1 Year | | | 38.47 | |

Effective after the close of business on May 24, 2019, Class A, Class C, Class Y and Class I shares of the Oppenheimer SteelPath MLP Alpha Fund (the predecessor fund), were reorganized into Class A, Class C, Class Y and Class R6 shares, respectively, of the Invesco Oppenheimer SteelPath MLP Alpha Fund. Note: The Fund was subsequently renamed the Invesco SteelPath MLP Alpha Fund (the Fund). Returns shown above, for periods ending on or prior to May 24, 2019, for Class A, Class C, Class Y and Class R6 shares are those for Class A, Class C, Class Y and Class I shares of the predecessor fund. Share class returns will differ from the predecessor fund because of different expenses.

Class R and R5 shares incepted after the close of business on May 24, 2019. Performance shown on and prior to that date is that of the predecessor fund’s Class A shares at net asset value and includes the 12b-1 fees applicable to Class A shares.

The performance data quoted represent past performance and cannot guarantee future results; current performance may be lower or higher. Please visit invesco.com/performance for the most recent month-end performance. Performance figures reflect reinvested distributions, changes in net asset value and the effect of the maximum sales charge unless otherwise stated.

Performance figures do not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares.

Class A share performance reflects the maximum 5.50% sales charge, and Class C share performance reflects the applicable contingent deferred sales charge (CDSC) for the period involved. The CDSC on Class C shares is 1% for the first year after purchase. Class R, Class Y, Class R5 and Class R6 shares do not have a front-end sales charge or a CDSC; therefore, performance is at net asset value.

The performance of the Fund’s share classes will differ primarily due to different sales charge structures and class expenses.

Fund performance reflects any applicable fee waivers and/or expense reimbursements. Had the adviser not waived fees and/or reimbursed expenses currently or in the past, returns would have been lower.

See current prospectus for more information.

5 Invesco SteelPath MLP Alpha Fund

Supplemental Information

Invesco SteelPath MLP Alpha Fund’s investment objective is to seek total return.

| • | | Unless otherwise stated, information presented in this report is as of November 30, 2022, and is based on total net assets. |

| • | | Unless otherwise noted, all data is provided by Invesco. |

| • | | To access your Fund’s reports/prospectus, visit invesco.com/fundreports. |

About indexes used in this report

| • | | The S&P 500® Index is an unmanaged index considered representative of the US stock market. |

| • | | The Alerian MLP Index is designed to capture the performance of energy master limited partnerships (MLPs). |

| • | | The Fund is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Fund may deviate significantly from the performance of the index(es). |

| • | | A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

This report must be accompanied or preceded by a currently effective Fund prospectus, which contains more complete information, including sales charges and expenses. Investors should read it carefully before investing.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

6 Invesco SteelPath MLP Alpha Fund

Fund Information

| | | | |

| Portfolio Composition | | | |

| |

| By Sector | | % of total net assets | |

Diversified | | | 44.24 | % |

Gathering & Processing | | | 32.43 | |

Petroleum Pipeline Transportation | | | 16.05 | |

Other Energy | | | 2.49 | |

Natural Gas Pipeline Transportation | | | 1.65 | |

Money Market Funds Plus Other Assets Less Liabilities | | | 3.14 | |

| |

| | | | |

Top 10 Master Limited Partnership and Related Entity

Holdings* | |

| |

| | | % of total net assets | |

1. Energy Transfer L.P. | | | 13.91 | % |

2. MPLX L.P. | | | 13.84 | |

3. Targa Resources Corp. | | | 13.62 | |

4. Western Midstream Partners L.P. | | | 12.23 | |

5. Enterprise Products Partners L.P. | | | 9.75 | |

6. Plains All American Pipeline L.P. | | | 6.81 | |

7. Magellan Midstream Partners L.P. | | | 6.06 | |

8. Williams Cos., Inc. | | | 4.83 | |

9. DCP Midstream L.P. | | | 2.40 | |

10. Hess Midstream L.P., Class A | | | 2.19 | |

The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security. * Excluding money market fund holdings, if any. Data presented here are as of November 30, 2022. | |

7 Invesco SteelPath MLP Alpha Fund

Schedule of Investments

November 30, 2022

| | | | | | | | |

| | | Units | | | Value | |

Master Limited Partnerships And Related

Entities–96.86% | |

| Diversified–44.24% | |

Energy Transfer L.P. | | | 9,093,108 | | | $ | 114,027,579 | |

Enterprise Products Partners L.P. | | | 3,221,119 | | | | 79,915,962 | |

MPLX L.P. | | | 3,337,394 | | | | 113,438,022 | |

ONEOK, Inc. | | | 234,099 | | | | 15,665,905 | |

Williams Cos., Inc. | | | 1,140,053 | | | | 39,559,839 | |

| | | | | | | | 362,607,307 | |

| Gathering & Processing–32.43% | |

Crestwood Equity Partners L.P. | | | 551,408 | | | | 16,332,705 | |

DCP Midstream L.P. | | | 501,010 | | | | 19,709,733 | |

Hess Midstream L.P., Class A | | | 573,651 | | | | 17,915,121 | |

Targa Resources Corp. | | | 1,500,720 | | | | 111,638,561 | |

Western Midstream Partners L.P. | | | 3,581,440 | | | | 100,208,688 | |

| | | | | | | | 265,804,808 | |

| Natural Gas Pipeline Transportation–1.65% | |

DT Midstream, Inc. | | | 105,235 | | | | 6,348,828 | |

Equitrans Midstream Corp. | | | 856,784 | | | | 7,188,415 | |

| | | | | | | | 13,537,243 | |

| Other Energy–2.49% | |

Sunoco L.P. | | | 114,752 | | | | 4,927,451 | |

USA Compression Partners L.P. | | | 438,955 | | | | 8,063,603 | |

Westlake Chemical Partners L.P. | | | 318,343 | | | | 7,369,641 | |

| | | | | | | | 20,360,695 | |

| | | | | | | | |

| | | Units | | | Value | |

| Petroleum Pipeline Transportation–16.05% | |

Holly Energy Partners L.P. | | | 680,417 | | | $ | 12,737,406 | |

Magellan Midstream Partners L.P. | | | 942,809 | | | | 49,686,034 | |

Plains All American Pipeline L.P. | | | 4,493,036 | | | | 55,803,507 | |

Plains GP Holdings L.P., Class A | | | 1,004,599 | | | | 13,290,845 | |

| | | | | | | | 131,517,792 | |

Total Master Limited Partnerships And Related Entities

(Cost $469,464,743) | | | | 793,827,845 | |

| | |

| | | Shares | | | | |

Money Market Funds–3.80% | |

Fidelity Treasury Portfolio, Institutional Class, 3.60%

(Cost $31,183,850)(a) | | | 31,183,850 | | | | 31,183,850 | |

TOTAL INVESTMENTS IN SECURITIES–100.66%

(Cost $500,648,593) | | | | 825,011,695 | |

OTHER ASSETS LESS LIABILITIES–(0.66)% | | | | (5,430,536 | ) |

NET ASSETS–100% | | | | | | $ | 819,581,159 | |

Notes to Schedule of Investments:

| (a) | The rate shown is the 7-day SEC standardized yield as of November 30, 2022. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

8 Invesco SteelPath MLP Alpha Fund

Statement of Assets and Liabilities

November 30, 2022

| | | | |

Assets: | | | | |

Investments in unaffiliated securities, at value

(Cost $500,648,593) | | $ | 825,011,695 | |

Receivable for: | | | | |

Investments sold | | | 5,691,862 | |

Fund shares sold | | | 270,368 | |

Dividends | | | 81,171 | |

Investment for trustee deferred compensation and retirement plans | | | 91,752 | |

Prepaid state income tax | | | 317,310 | |

Other assets | | | 80,274 | |

Total assets | | | 831,544,432 | |

| |

| | | | |

Liabilities: | | | | |

Payable for: | | | | |

Fund shares reacquired | | | 999,571 | |

Federal income tax payable | | | 2,074,900 | |

Deferred tax liability, net | | | 7,367,384 | |

Accrued fees to affiliates | | | 1,080,343 | |

Accrued interest expense | | | 10,166 | |

Accrued trustees’ and officers’ fees and benefits | | | 3,872 | |

Accrued other operating expenses | | | 335,285 | |

Trustee deferred compensation and retirement plans | | | 91,752 | |

Total liabilities | | | 11,963,273 | |

Net assets applicable to shares outstanding | | $ | 819,581,159 | |

| |

| | | | |

Net assets consist of: | | | | |

Shares of beneficial interest | | $ | 1,705,832,521 | |

Distributable earnings (loss), net of taxes | | | (886,251,362 | ) |

| | | $ | 819,581,159 | |

| | | | |

Net Assets: | | | | |

Class A | | $ | 366,201,134 | |

Class C | | $ | 113,058,652 | |

Class R | | $ | 723,895 | |

Class Y | | $ | 322,851,262 | |

Class R5 | | $ | 8,530 | |

Class R6 | | $ | 16,737,686 | |

| |

| | | | |

Shares outstanding, no par value, with an unlimited number of shares authorized: | |

Class A | | | 62,672,400 | |

Class C | | | 22,146,052 | |

Class R | | | 125,545 | |

Class Y | | | 52,220,141 | |

Class R5 | | | 1,445 | |

Class R6 | | | 2,679,022 | |

Class A: | | | | |

Net asset value per share | | $ | 5.84 | |

Maximum offering price per share

(net asset value of $5.84 ÷ 94.50%) | | | 6.18 | |

Class C: | | | | |

Net asset value and offering price per share | | $ | 5.11 | |

Class R: | | | | |

Net asset value and offering price per share | | $ | 5.77 | |

Class Y: | | | | |

Net asset value and offering price per share | | $ | 6.18 | |

Class R5: | | | | |

Net asset value and offering price per share | | $ | 5.90 | |

Class R6: | | | | |

Net asset value and offering price per share | | $ | 6.25 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

9 Invesco SteelPath MLP Alpha Fund

Statement of Operations

For the year ended November 30, 2022

| | | | |

Investment income: | | | | |

Distributions and dividends (net of return of capital distributions of $44,852,607) | | $ | 7,178,054 | |

Less: return of capital on distributions and dividends in excess of cost basis | | | (1,521,523 | ) |

Total investment income | | | 5,656,531 | |

| |

| | | | |

Expenses: | | | | |

Advisory fees | | | 8,411,301 | |

Administrative services fees | | | 291,538 | |

Custodian fees | | | 45,548 | |

Distribution fees: | | | | |

Class A | | | 816,300 | |

Class C | | | 1,226,673 | |

Class R | | | 2,484 | |

Transfer agent fees — A, C, R and Y | | | 1,022,628 | |

Transfer agent fees — R5 | | | 4 | |

Transfer agent fees — R6 | | | 4,659 | |

Interest, facilities and maintenance fees | | | 233,311 | |

State income tax expense | | | 41,800 | |

Federal income tax expense | | | 21,264 | |

Trustees’ and officers’ fees and benefits | | | 24,804 | |

Registration and filing fees | | | 99,478 | |

Reports to shareholders | | | 72,627 | |

Professional services fees | | | 129,651 | |

Other | | | 20,395 | |

Total expenses, before waivers and deferred taxes | | | 12,464,465 | |

Less: Expenses reimbursed | | | (573,671 | ) |

Net expenses, before deferred taxes | | | 11,890,794 | |

Net investment income (loss), before deferred taxes | | | (6,234,263 | ) |

Net deferred tax benefit | | | 6,696,919 | |

Current tax (expense)/benefit | | | (2,960,626 | ) |

Net investment income (loss), net of deferred taxes | | | (2,497,970 | ) |

| |

| | | | |

| |

Realized and unrealized gain (loss) from: | | | | |

Net realized gain from: | | | | |

Unaffiliated investment securities | | | 93,182,414 | |

Net deferred tax (expense) benefit | | | 27,142,262 | |

Net realized gain, net of deferred taxes | | | 120,324,676 | |

Change in net unrealized appreciation (depreciation) of: | | | | |

Unaffiliated investment securities | | | 155,411,923 | |

Net deferred tax (expense) benefit | | | (37,392,365 | ) |

Net change in net unrealized appreciation of investment securities, net of deferred taxes | | | 118,019,558 | |

Net realized and unrealized gain, net of deferred taxes | | | 238,344,234 | |

Net increase in net assets resulting from operations | | $ | 235,846,264 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

10 Invesco SteelPath MLP Alpha Fund

Statement of Changes in Net Assets

For the years ended November 30, 2022 and 2021

| | | | | | | | |

| | | 2022 | | | 2021 | |

Operations: | | | | | | | | |

Net investment income (loss), net of deferred taxes | | $ | (2,497,970 | ) | | $ | (16,769,893 | ) |

Net realized gain, net of deferred taxes | | | 120,324,676 | | | | 13,936,173 | |

Change in net unrealized appreciation, net of deferred taxes | | | 118,019,558 | | | | 216,243,120 | |

Net increase in net assets resulting from operations | | | 235,846,264 | | | | 213,409,400 | |

| | |

| | | | | | | | |

| | |

Distributions to shareholders from distributable earnings: | | | | | | | | |

Class A | | | (22,522,216 | ) | | | — | |

Class C | | | (9,396,553 | ) | | | — | |

Class R | | | (35,595 | ) | | | — | |

Class Y | | | (19,510,530 | ) | | | — | |

Class R5 | | | (538 | ) | | | — | |

Class R6 | | | (1,002,385 | ) | | | — | |

Total distributions from distributable earnings | | | (52,467,817 | ) | | | — | |

| | |

| | | | | | | | |

| | |

Return of capital: | | | | | | | | |

Class A | | | — | | | | (21,470,225 | ) |

Class C | | | — | | | | (13,254,588 | ) |

Class R | | | — | | | | (29,145 | ) |

Class Y | | | — | | | | (21,222,692 | ) |

Class R5 | | | — | | | | (538 | ) |

Class R6 | | | — | | | | (1,113,779 | ) |

Total return of capital | | | — | | | | (57,090,967 | ) |

| | |

| | | | | | | | |

| | |

Share transactions-net: | | | | | | | | |

Class A | | | 13,095,644 | | | | 16,514,447 | |

Class C | | | (37,009,644 | ) | | | (55,520,579 | ) |

Class R | | | 225,855 | | | | 109,850 | |

Class Y | | | (14,886,204 | ) | | | (39,002,531 | ) |

Class R6 | | | (1,773,421 | ) | | | (2,228,338 | ) |

Net increase (decrease) in net assets resulting from share transactions | | | (40,347,770 | ) | | | (80,127,151 | ) |

Net increase in net assets | | | 143,030,677 | | | | 76,191,282 | |

| | |

| | | | | | | | |

| | |

Net assets: | | | | | | | | |

Beginning of year | | | 676,550,482 | | | | 600,359,200 | |

End of year | | $ | 819,581,159 | | | $ | 676,550,482 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

11 Invesco SteelPath MLP Alpha Fund

Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended November 30, | |

| Class A | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018* | |

Per share operating data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.56 | | | $ | 3.58 | | | $ | 5.28 | | | $ | 6.56 | | | $ | 7.35 | |

Net investment income (loss)(a) | | | (0.02 | ) | | | (0.11 | ) | | | (0.06 | ) | | | (0.03 | ) | | | (0.09 | ) |

Return of capital(a) | | | 0.25 | | | | 0.24 | | | | 0.29 | | | | 0.34 | | | | 0.39 | |

Net realized and unrealized gain (loss) | | | 1.42 | | | | 1.22 | | | | (1.42 | ) | | | (0.93 | ) | | | (0.43 | ) |

Total from investment operations | | | 1.65 | | | | 1.35 | | | | (1.19 | ) | | | (0.62 | ) | | | (0.13 | ) |

Less: | | | | | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.62 | ) | | | (0.62 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.04 | ) | | | (0.04 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.66 | ) | | | (0.66 | ) |

Net asset value, end of period | | $ | 5.84 | | | $ | 4.56 | | | $ | 3.58 | | | $ | 5.28 | | | $ | 6.56 | |

Total return(b) | | | 37.02 | % | | | 38.26 | % | | | (22.24 | )% | | | (10.69 | )% | | | (2.33 | )% |

Net assets, end of period (000’s omitted) | | $ | 366,201 | | | $ | 274,904 | | | $ | 203,978 | | | $ | 321,237 | | | $ | 459,733 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % | | | 36 | % |

| | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 1.62 | % | | | 1.65 | % | | | 1.87 | % | | | 1.67 | % | | | 1.68 | % |

Expense (waivers) | | | (0.08 | )% | | | (0.10 | )% | | | (0.13 | )% | | | (0.08 | )% | | | (0.11 | )%(c) |

With fee waivers and/or expense reimbursements, before taxes(d) | | | 1.54 | % | | | 1.55 | % | | | 1.74 | % | | | 1.59 | % | | | 1.57 | % |

Deferred/current tax expense (benefit)(e) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | - | % | | | 0.03 | % |

With fee waivers and/or expense reimbursements, after taxes | | | 2.39 | % | | | 2.83 | % | | | 2.51 | % | | | 1.59 | % | | | 1.60 | % |

| |

Ratio of investment income (loss): | | | | | |

Ratio of net investment income (loss), before taxes | | | (0.88 | )% | | | (0.92 | )% | | | (1.57 | )% | | | (0.56 | )% | | | (1.29 | )% |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (0.80 | )% | | | (0.82 | )% | | | (1.44 | )% | | | (0.48 | )% | | | (1.18 | )% |

Deferred tax benefit (expense)(f) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | % | | | — | % |

Ratio of net investment income (loss), after taxes | | | (0.31 | )% | | | (2.37 | )% | | | (1.44 | )% | | | (0.48 | )% | | | (1.18 | )% |

| * | The financial highlights for the year ended November 30, 2018 reflect restated values. See Note 10-Restatement in the Notes to Financial Statements for the year ended November 30, 2018. |

| (a) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (c) | Includes voluntary Transfer Agent waiver of 0.015% effective January 1, 2017 to December 31, 2017. |

| (d) | Includes borrowing, federal income tax, state income tax and franchise tax expense. Without borrowing, state income tax and franchise tax expense, the net expense ratio would be 1.50%, 1.50%, 1.52% 1.55%, and 1.54%, for the years ended November 30, 2022, 2021, 2020, 2019, and 2018, respectively. |

| (e) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (f) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

12 Invesco SteelPath MLP Alpha Fund

Financial Highlights—(continued)

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended November 30, | |

| Class C | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018* | |

Per share operating data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.05 | | | $ | 3.23 | | | $ | 4.87 | | | $ | 6.14 | | | $ | 6.97 | |

Net investment income (loss)(a) | | | (0.05 | ) | | | (0.12 | ) | | | (0.08 | ) | | | (0.07 | ) | | | (0.14 | ) |

Return of capital(a) | | | 0.22 | | | | 0.21 | | | | 0.27 | | | | 0.31 | | | | 0.39 | |

Net realized and unrealized gain (loss) | | | 1.26 | | | | 1.10 | | | | (1.32 | ) | | | (0.85 | ) | | | (0.42 | ) |

Total from investment operations | | | 1.43 | | | | 1.19 | | | | (1.13 | ) | | | (0.61 | ) | | | (0.17 | ) |

Less: | | | | | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.62 | ) | | | (0.62 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.04 | ) | | | (0.04 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.66 | ) | | | (0.66 | ) |

Net asset value, end of period | | $ | 5.11 | | | $ | 4.05 | | | $ | 3.23 | | | $ | 4.87 | | | $ | 6.14 | |

Total return(b) | | | 36.24 | % | | | 37.41 | % | | | (22.94 | )% | | | (11.29 | )% | | | (3.06 | )% |

Net assets, end of period (000’s omitted) | | $ | 113,059 | | | $ | 122,076 | | | $ | 143,085 | | | $ | 266,485 | | | $ | 407,345 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % | | | 36 | % |

| | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 2.37 | % | | | 2.40 | % | | | 2.62 | % | | | 2.44 | % | | | 2.46 | % |

Expense (waivers) | | | (0.08 | )% | | | (0.10 | )% | | | (0.13 | )% | | | (0.08 | )% | | | (0.11 | )%(c) |

With fee waivers and/or expense reimbursements, before taxes(d) | | | 2.29 | % | | | 2.30 | % | | | 2.49 | % | | | 2.36 | % | | | 2.35 | % |

Deferred/current tax expense (benefit)(e) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | — | % | | | 0.03 | % |

With fee waivers and/or expense reimbursements, after taxes | | | 3.14 | % | | | 3.58 | % | | | 3.26 | % | | | 2.36 | % | | | 2.38 | % |

| |

Ratio of investment income (loss): | | | | | |

Ratio of net investment income (loss), before taxes | | | (1.63 | )% | | | (1.67 | )% | | | (2.32 | )% | | | 1.33 | % | | | (2.07 | )% |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (1.55 | )% | | | (1.57 | )% | | | (2.19 | )% | | | (1.25 | )% | | | (1.96 | )% |

Deferred tax benefit (expense)(f) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | % | | | — | % |

Ratio of net investment income (loss), after taxes | | | (1.06 | )% | | | (3.12 | )% | | | (2.19 | )% | | | (1.25 | )% | | | (1.96 | )% |

| * | The financial highlights for the year ended November 30, 2018 reflect restated values. See Note 10-Restatement in the Notes to Financial Statements for the year ended November 30, 2018. |

| (a) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (c) | Includes voluntary Transfer Agent waiver of 0.015% effective January 1, 2017 to December 31, 2017. |

| (d) | Includes borrowing, federal income tax, state income tax and franchise tax expense. Without borrowing, federal income tax, state income tax and franchise tax expense, the net expense ratio would be 2.25%, 2.25%, 2.28%, 2.32%, and 2.32%, for the years ended November 30, 2022, 2021, 2020, 2019, and 2018, respectively. |

| (e) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (f) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

13 Invesco SteelPath MLP Alpha Fund

Financial Highlights—(continued)

| | | | | | | | | | | | | | | | |

| | | Years Ended Novemver 30, | | | Period ended

November 30,

2019(a) | |

| Class R | | 2022 | | | 2021 | | | 2020 | |

Per share operating data | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.51 | | | $ | 3.55 | | | $ | 5.27 | | | $ | 6.80 | |

Net investment income (loss)(b) | | | (0.03 | ) | | | (0.12 | ) | | | (0.06 | ) | | | (0.02 | ) |

Return of capital(b) | | | 0.25 | | | | 0.24 | | | | 0.28 | | | | 0.16 | |

Net realized and unrealized gain (loss) | | | 1.41 | | | | 1.21 | | | | (1.43 | ) | | | (1.29 | ) |

Total from investment operations | | | 1.63 | | | | 1.33 | | | | (1.21 | ) | | | (1.15 | ) |

Less: | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.36 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.02 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.38 | ) |

Net asset value, end of period | | $ | 5.77 | | | $ | 4.51 | | | $ | 3.55 | | | $ | 5.27 | |

Total return(c) | | | 36.99 | % | | | 38 | % | | | (22.69 | )% | | | (17.44 | )% |

Net assets, end of period (000’s omitted) | | $ | 724 | | | $ | 374 | | | $ | 200 | | | $ | 87 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % |

| | | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 1.87 | % | | | 1.90 | % | | | 2.12 | % | | | 1.93 | %(d) |

Expense (waivers) | | | (0.08 | )% | | | (0.10 | )% | | | (0.13 | )% | | | (0.09 | )%(d) |

With fee waivers and/or expense reimbursements, before taxes(e) | | | 1.79 | % | | | 1.80 | % | | | 1.99 | % | | | 1.84 | %(d) |

Deferred/current tax expense (benefit)(f) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | — | %(d) |

With fee waivers and/or expense reimbursements, after taxes | | | 2.64 | % | | | 3.08 | % | | | 2.76 | % | | | 1.84 | %(d) |

|

Ratio of investment income (loss): | |

Ratio of net investment income (loss), before taxes | | | (1.13 | )% | | | (1.17 | )% | | | (1.82 | )% | | | (0.82 | )%(d) |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (1.05 | )% | | | (1.07 | )% | | | (1.69 | )% | | | (0.73 | )%(d) |

Deferred tax benefit (expense)(g) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | %(d) |

Ratio of net investment income (loss), after taxes | | | (0.56 | )% | | | (2.62 | )% | | | (1.69 | )% | | | (0.73 | )%(d) |

| (a) | Commencement date after the close of business on May 24, 2019. |

| (b) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (e) | Includes borrowing, federal income tax, state income tax and franchise tax expense. Without borrowing, federal income tax, state income tax and franchise tax expense, the net expense ratio would be 1.75%, 1.75%, 1.76% and 1.80%, for the years ended November 30, 2022, 2021 and 2020, and the period ended November 30, 2019, respectively. |

| (f) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (g) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

14 Invesco SteelPath MLP Alpha Fund

Financial Highlights—(continued)

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended November 30, | |

| Class Y | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018* | |

Per share operating data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.79 | | | $ | 3.74 | | | $ | 5.48 | | | $ | 6.76 | | | $ | 7.53 | |

Net investment income (loss)(a) | | | (0.00 | ) | | | (0.10 | ) | | | (0.05 | ) | | | (0.01 | ) | | | (0.07 | ) |

Return of capital(a) | | | 0.26 | | | | 0.25 | | | | 0.31 | | | | 0.35 | | | | 0.39 | |

Net realized and unrealized gain (loss) | | | 1.50 | | | | 1.27 | | | | (1.49 | ) | | | (0.96 | ) | | | (0.43 | ) |

Total from investment operations | | | 1.76 | | | | 1.42 | | | | (1.23 | ) | | | (0.62 | ) | | | (0.11 | ) |

Less: | | | | | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.62 | ) | | | (0.62 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.04 | ) | | | (0.04 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.66 | ) | | | (0.66 | ) |

Net asset value, end of period | | $ | 6.18 | | | $ | 4.79 | | | $ | 3.74 | | | $ | 5.48 | | | $ | 6.76 | |

Total return(b) | | | 37.55 | % | | | 38.50 | % | | | (22.15 | )% | | | (10.36 | )% | | | (2.00 | )% |

Net assets, end of period (000’s omitted) | | $ | 322,851 | | | $ | 264,856 | | | $ | 239,896 | | | $ | 555,814 | | | $ | 1,005,677 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % | | | 36 | % |

| | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 1.37 | % | | | 1.40 | % | | | 1.62 | % | | | 1.42 | % | | | 1.43 | % |

Expense (waivers) | | | (0.08 | )% | | | (0.10 | )% | | | (0.13 | )% | | | (0.09 | )% | | | (0.11 | )%(c) |

With fee waivers and/or expense reimbursements, before taxes(d) | | | 1.29 | % | | | 1.30 | % | | | 1.49 | % | | | 1.33 | % | | | 1.32 | % |

Deferred/current tax expense (benefit)(e) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | — | % | | | 0.03 | % |

With fee waivers and/or expense reimbursements, after taxes | | | 2.14 | % | | | 2.58 | % | | | 2.26 | % | | | 1.33 | % | | | 1.35 | % |

| |

Ratio of investment income (loss): | | | | | |

Ratio of net investment income (loss), before taxes | | | (0.63 | )% | | | (0.67 | )% | | | (1.32 | )% | | | (0.31 | )% | | | (1.04 | )% |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (0.55 | )% | | | (0.57 | )% | | | (1.19 | )% | | | (0.22 | )% | | | (0.93 | )% |

Deferred tax benefit (expense)(f) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | % | | | — | % |

Ratio of net investment income (loss), after taxes | | | (0.06 | )% | | | (2.12 | )% | | | (1.19 | )% | | | (0.22 | )% | | | (0.93 | )% |

| * | The financial highlights for the year ended November 30, 2018 reflect restated values. See Note 10-Restatement in the Notes to Financial Statements for the year ended November 30, 2018. |

| (a) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (c) | Includes voluntary Transfer Agent waiver of 0.015% effective January 1, 2017 to December 31, 2017. |

| (d) | Includes borrowing, federal income tax, state income tax and franchise tax expense. Without borrowing and franchise tax expense, the net expense ratio would be 1.25%, 1.25%, 1.27%, 1.29%, and 1.29%, for the years ended November 30, 2022, 2021, 2020, 2019, and 2018, respectively. |

| (e) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (f) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

15 Invesco SteelPath MLP Alpha Fund

Financial Highlights—(continued)

| | | | | | | | | | | | | | | | |

| | | Years Ended Novemver 30, | | | Period ended

November 30,

2019(a) | |

| Class R5 | | 2022 | | | 2021 | | | 2020 | |

Per share operating data | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.59 | | | $ | 3.59 | | | $ | 5.29 | | | $ | 6.80 | |

Net investment income (loss)(b) | | | (0.00 | ) | | | (0.10 | ) | | | (0.05 | ) | | | (0.01 | ) |

Return of capital(b) | | | 0.25 | | | | 0.24 | | | | 0.29 | | | | 0.17 | |

Net realized and unrealized gain (loss) | | | 1.43 | | | | 1.23 | | | | (1.43 | ) | | | (1.29 | ) |

Total from investment operations | | | 1.68 | | | | 1.37 | | | | (1.19 | ) | | | (1.13 | ) |

Less: | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.36 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.02 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.38 | ) |

Net asset value, end of period | | $ | 5.90 | | | $ | 4.59 | | | $ | 3.59 | | | $ | 5.29 | |

Total return(c) | | | 37.45 | % | | | 38.72 | % | | | (22.20 | )% | | | (17.13 | )% |

Net assets, end of period (000’s omitted) | | $ | 9 | | | $ | 7 | | | $ | 5 | | | $ | 8 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % |

| | | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 1.26 | % | | | 1.29 | % | | | 1.49 | % | | | 1.30 | %(d) |

Expense (waivers) | | | — | %(e) | | | — | %(e) | | | (0.01 | )% | | | — | %(d) |

With fee waivers and/or expense reimbursements, before taxes(f) | | | 1.26 | % | �� | | 1.29 | % | | | 1.48 | % | | | 1.30 | %(d) |

Deferred/current tax expense (benefit)(g) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | — | %(d) |

With fee waivers and/or expense reimbursements, after taxes | | | 2.11 | % | | | 2.57 | % | | | 2.25 | % | | | 1.30 | %(d) |

|

Ratio of investment income (loss): | |

Ratio of net investment income (loss), before taxes | | | (0.52 | )% | | | (0.56 | )% | | | (1.19 | )% | | | (0.19 | )%(d) |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (0.52 | )% | | | (0.56 | )% | | | (1.18 | )% | | | (0.19 | )%(d) |

Deferred tax benefit (expense)(h) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | %(d) |

Ratio of net investment income (loss), after taxes | | | (0.03 | )% | | | (2.11 | )% | | | (1.18 | )% | | | (0.19 | )%(d) |

| (a) | Commencement date after the close of business on May 24, 2019. |

| (b) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (e) | Rounds to less than (0.01)%. |

| (f) | Includes borrowing, state income tax and franchise tax expense. Without borrowing, state income tax and franchise tax expense, the net expense ratio would be 1.22%, 1.24%, 1.26% and 1.26%, for the years ended November 30, 2022, 2021 and 2020, and the period ended November 30, 2019, respectively. |

| (g) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (h) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

16 Invesco SteelPath MLP Alpha Fund

Financial Highlights—(continued)

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended November 30, | |

| Class R6 | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018* | |

Per share operating data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 4.84 | | | $ | 3.77 | | | $ | 5.51 | | | $ | 6.80 | | | $ | 7.58 | |

Net investment income (loss)(a) | | | (0.00 | ) | | | (0.10 | ) | | | (0.05 | ) | | | (0.01 | ) | | | (0.07 | ) |

Return of capital(a) | | | 0.26 | | | | 0.25 | | | | 0.32 | | | | 0.36 | | | | 0.39 | |

Net realized and unrealized gain (loss) | | | 1.52 | | | | 1.29 | | | | (1.50 | ) | | | (0.98 | ) | | | (0.44 | ) |

Total from investment operations | | | 1.78 | | | | 1.44 | | | | (1.23 | ) | | | (0.63 | ) | | | (0.12 | ) |

Less: | | | | | | | | | | | | | | | | | | | | |

Return of capital | | | — | | | | (0.37 | ) | | | (0.51 | ) | | | (0.62 | ) | | | (0.62 | ) |

Dividends from net investment income | | | (0.37 | ) | | | — | | | | — | | | | (0.04 | ) | | | (0.04 | ) |

Total distributions | | | (0.37 | ) | | | (0.37 | ) | | | (0.51 | ) | | | (0.66 | ) | | | (0.66 | ) |

Net asset value, end of period | | $ | 6.25 | | | $ | 4.84 | | | $ | 3.77 | | | $ | 5.51 | | | $ | 6.80 | |

Total return(b) | | | 37.59 | % | | | 38.74 | % | | | (22.03 | )% | | | (10.45 | )% | | | (2.11 | )% |

Net assets, end of period (000’s omitted) | | $ | 16,738 | | | $ | 14,333 | | | $ | 13,194 | | | $ | 38,414 | | | $ | 141,917 | |

Portfolio turnover rate | | | 25 | % | | | 31 | % | | | 88 | % | | | 32 | % | | | 36 | % |

| | | |

Ratios/supplemental data based on average net assets: | | | | | | | | | | | | | |

Ratio of expenses: | | | | | | | | | | | | | | | | |

Without fee waivers and/or expense reimbursements, before taxes | | | 1.26 | % | | | 1.29 | % | | | 1.49 | % | | | 1.27 | % | | | 1.25 | % |

Expense (waivers) | | | (0.03 | )% | | | (0.05 | )% | | | (0.06 | )% | | | — | % | | | — | % |

With fee waivers and/or expense reimbursements, before taxes(c) | | | 1.23 | % | | | 1.24 | % | | | 1.43 | % | | | 1.27 | % | | | 1.25 | % |

Deferred/current tax expense (benefit)(d) | | | 0.85 | % | | | 1.28 | % | | | 0.77 | % | | | — | % | | | 0.03 | % |

With fee waivers and/or expense reimbursements, after taxes | | | 2.08 | % | | | 2.52 | % | | | 2.20 | % | | | 1.27 | % | | | 1.28 | % |

| |

Ratio of investment income (loss): | | | | | |

Ratio of net investment income (loss), before taxes | | | (0.52 | )% | | | (0.56 | )% | | | (1.19 | )% | | | (0.16 | )% | | | (0.86 | )% |

Net of expense (waivers) and before deferred tax benefit (expense) | | | (0.49 | )% | | | (0.51 | )% | | | (1.13 | )% | | | (0.16 | )% | | | (0.86 | )% |

Deferred tax benefit (expense)(e) | | | 0.49 | % | | | (1.55 | )% | | | — | % | | | — | % | | | — | % |

Ratio of net investment income (loss), after taxes | | | — | % | | | (2.06 | )% | | | (1.13 | )% | | | (0.16 | )% | | | (0.86 | )% |

| * | The financial highlights for the year ended November 30, 2018 reflect restated values. See Note 10-Restatement in the Notes to Financial Statements for the year ended November 30, 2018. |

| (a) | Per share net investment income (loss) is calculated based on average shares outstanding during the period net of deferred tax expense (benefit). Per share return of capital is calculated based on average shares during the period net of deferred tax expense (benefit) estimated at the combined Federal and State statutory income tax rate. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. Does not include sales charges and is not annualized for periods less than one year, if applicable. |

| (c) | Includes borrowing, state income tax and franchise tax expense. Without borrowing, state income tax and franchise tax expense, the net expense ratio would be 1.19%, 1.19%, 1.21%, 1.23%, and 1.22%, for the years ended November 30, 2022, 2021, 2020, 2019, and 2018, respectively. |

| (d) | Deferred tax expense (benefit) estimate for the ratio calculation is derived from the net investment income (loss), and realized and unrealized gains (losses). |

| (e) | Deferred tax benefit (expense) for the ratio calculation, when applicable, is derived from net investment income (loss) only. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

17 Invesco SteelPath MLP Alpha Fund

Notes to Financial Statements

November 30, 2022

NOTE 1—Significant Accounting Policies

Invesco SteelPath MLP Alpha Fund (the “Fund”) is a series portfolio of AIM Investment Funds (Invesco Investment Funds) (the “Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end series management investment company authorized to issue an unlimited number of shares of beneficial interest. The Fund is classified as non-diversified. Information presented in these financial statements pertains only to the Fund. Matters affecting the Fund or each class will be voted on exclusively by the shareholders of the Fund or each class.

The Fund’s investment objective is to seek total return.

The Fund currently consists of six different classes of shares: Class A, Class C, Class R, Class Y, Class R5 and Class R6. Class Y shares are available only to certain investors. Class A shares are sold with a front-end sales charge unless certain waiver criteria are met. Under certain circumstances, load waived shares may be subject to contingent deferred sales charges (“CDSC”). Class C shares are sold with a CDSC. Class R, Class Y, Class R5 and Class R6 shares are sold at net asset value. Class C shares held for eight years after purchase are eligible for automatic conversion into Class A shares of the same Fund (the “Conversion Feature”). The automatic conversion pursuant to the Conversion Feature will generally occur at the end of the month following the eighth anniversary after a purchase of Class C shares.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance in accordance with Financial Accounting Standards Board Accounting Standards Codification Topic 946, Financial Services – Investment Companies.

The following is a summary of the significant accounting policies followed by the Fund in the preparation of its financial statements.

| A. | Security Valuations – Securities, including restricted securities, are valued according to the following policy. |

A security listed or traded on an exchange is generally valued at its trade price or official closing price that day as of the close of the exchange where the security is principally traded, or lacking any trades or official closing price on a particular day, the security may be valued at the closing bid price on that day. Securities traded in the over-the-counter market are valued based on prices furnished by independent pricing services or market makers. When such securities are valued using prices provided by an independent pricing service they may be considered fair valued. Futures contracts are valued at the daily settlement price set by an exchange on which they are principally traded. U.S. exchange-traded options are valued at the mean between the last bid and asked prices from the exchange on which they are principally traded. Non-U.S. exchange-traded options are valued at the final settlement price set by the exchange on which they trade. Options not listed on an exchange and swaps generally are valued using pricing provided from independent pricing services.

Securities of investment companies that are not exchange-traded (e.g., open end mutual funds) are valued using such company’s end-of-business-day net asset value per share.

Deposits, other obligations of U.S. and non-U.S. banks and financial institutions are valued at their daily account value.

Fixed income securities (including convertible debt securities) generally are valued on the basis of prices provided by independent pricing services. Prices provided by the pricing service may be determined without exclusive reliance on quoted prices, and may reflect appropriate factors such as institution-size trading in similar groups of securities, developments related to specific securities, dividend rate (for unlisted equities), yield (for debt obligations), quality, type of issue, coupon rate (for debt obligations), maturity (for debt obligations), individual trading characteristics and other market data. Pricing services generally value debt obligations assuming orderly transactions of institutional round lot size, but a fund may hold or transact in the same securities in smaller, odd lot sizes. Odd lots often trade at lower prices than institutional round lots, and their value may be adjusted accordingly. Debt obligations are subject to interest rate and credit risks. In addition, all debt obligations involve some risk of default with respect to interest and/or principal payments.

Foreign securities’ (including foreign exchange contracts) prices are converted into U.S. dollar amounts using the applicable exchange rates as of the close of the New York Stock Exchange (“NYSE”). If market quotations are available and reliable for foreign exchange-traded equity securities, the securities will be valued at the market quotations. Invesco Advisers, Inc. (the “Adviser” or “Invesco”) may use various pricing services to obtain market quotations as well as fair value prices. Because trading hours for certain foreign securities end before the close of the NYSE, closing market quotations may become not representative of market value in the Adviser’s judgment (“unreliable”). If, between the time trading ends on a particular security and the close of the customary trading session on the NYSE, a significant event occurs that makes the closing price of the security unreliable, the Adviser may fair value the security. If the event is likely to have affected the closing price of the security, the security will be valued at fair value in good faith in accordance with Board-approved policies and related Adviser procedures (“Valuation Procedures”). Adjustments to closing prices to reflect fair value may also be based on a screening process of an independent pricing service to indicate the degree of certainty, based on historical data, that the closing price in the principal market where a foreign security trades is not the current value as of the close of the NYSE. Foreign securities’ prices meeting the degree of certainty that the price is not reflective of current value will be priced at the indication of fair value from the independent pricing service. Multiple factors may be considered by the independent pricing service in determining adjustments to reflect fair value and may include information relating to sector indices, American Depositary Receipts and domestic and foreign index futures. Foreign securities may have additional risks including exchange rate changes, potential for sharply devalued currencies and high inflation, political and economic upheaval, the relative lack of issuer information, relatively low market liquidity and the potential lack of strict financial and accounting controls and standards.

Unlisted securities will be valued using prices provided by independent pricing services or by another method that the Adviser, in its judgment, believes better reflects the security’s fair value in accordance with the Valuation Procedures.

Securities for which market prices are not provided by any of the above methods may be valued based upon quotes furnished by independent sources. The last bid price may be used to value equity securities. The mean between the last bid and asked prices may be used to value debt obligations, including corporate loans.

Securities for which market quotations are not readily available are fair valued by the Adviser in accordance with the Valuation Procedures. If a fair value price provided by a pricing service is unreliable, the Adviser will fair value the security using the Valuation Procedures. Issuer specific events, market trends, bid/asked quotes of brokers and information providers and other market data may be reviewed in the course of making a good faith determination of a security’s fair value.

The Fund may invest in securities that are subject to interest rate risk, meaning the risk that the prices will generally fall as interest rates rise and, conversely, the prices will generally rise as interest rates fall. Specific securities differ in their sensitivity to changes in interest rates depending on their individual characteristics. Changes in interest rates may result in increased market volatility, which may affect the value and/or liquidity of certain Fund investments.

Valuations change in response to many factors including the historical and prospective earnings of the issuer, the value of the issuer’s assets, general market conditions which are not specifically related to the particular issuer, such as real or perceived adverse economic conditions, changes in the general outlook for revenues or corporate earnings, changes in interest or currency rates, regional or global instability, natural or environmental disasters, widespread disease or other public health issues, war, acts of terrorism, significant governmental actions or adverse investor sentiment generally and market liquidity. Because of the inherent uncertainties of valuation, the values reflected in the financial statements may materially differ from the value received upon actual sale of those investments.

18 Invesco SteelPath MLP Alpha Fund

The price the Fund could receive upon the sale of any investment may differ from the Adviser’s valuation of the investment, particularly for securities that are valued using a fair valuation technique. When fair valuation techniques are applied, the Adviser uses available information, including both observable and unobservable inputs and assumptions, to determine a methodology that will result in a valuation that the Adviser believes approximates market value. Fund securities that are fair valued may be subject to greater fluctuation in their value from one day to the next than would be the case if market quotations were used. Because of the inherent uncertainties of valuation, and the degree of subjectivity in such decisions, the Fund could realize a greater or lesser than expected gain or loss upon the sale of the investment.

| B. | Securities Transactions and Investment Income – Securities transactions are accounted for on a trade date basis. Realized gains or losses on sales are computed on the basis of specific identification of the securities sold. Interest income (net of withholding tax, if any) is recorded on an accrual basis from settlement date and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable. Dividend income (net of withholding tax, if any) is recorded on the ex-dividend date. |

The Fund may periodically participate in litigation related to Fund investments. As such, the Fund may receive proceeds from litigation settlements. Any proceeds received are included in the Statement of Operations as realized gain (loss) for investments no longer held and as unrealized gain (loss) for investments still held.

Brokerage commissions and mark ups are considered transaction costs and are recorded as an increase to the cost basis of securities purchased and/or a reduction of proceeds on a sale of securities. Such transaction costs are included in the determination of net realized and unrealized gain (loss) from investment securities reported in the Statement of Operations and the Statement of Changes in Net Assets and the net realized and unrealized gains (losses) on securities per share in the Financial Highlights. Transaction costs are included in the calculation of the Fund’s net asset value and, accordingly, they reduce the Fund’s total returns. These transaction costs are not considered operating expenses and are not reflected in net investment income reported in the Statement of Operations and the Statement of Changes in Net Assets, or the net investment income per share and the ratios of expenses and net investment income reported in the Financial Highlights, nor are they limited by any expense limitation arrangements between the Fund and the investment adviser.

The Fund allocates income and realized and unrealized capital gains and losses to a class based on the relative net assets of each class.

| C. | Country Determination – For the purposes of making investment selection decisions and presentation in the Schedule of Investments, the investment adviser may determine the country in which an issuer is located and/or credit risk exposure based on various factors. These factors include the laws of the country under which the issuer is organized, where the issuer maintains a principal office, the country in which the issuer derives 50% or more of its total revenues, the country that has the primary market for the issuer’s securities and its “country of risk” as determined by a third party service provider, as well as other criteria. Among the other criteria that may be evaluated for making this determination are the country in which the issuer maintains 50% or more of its assets, the type of security, financial guarantees and enhancements, the nature of the collateral and the sponsor organization. Country of issuer and/or credit risk exposure has been determined to be the United States of America, unless otherwise noted. |

| D. | Dividends and Distributions to Shareholders – Dividends and distributions to shareholders, which are determined in accordance with income tax regulations and may differ from accounting principles generally accepted in the United States of America (“GAAP”), are recorded on the ex-dividend date. The Fund’s dividend distribution policy is intended to provide monthly distributions to its shareholders at a rate that over time is similar to the distribution rate the Fund receives from the master limited partnerships (”MLPs”) in which it invests. The Fund generally pays out dividends that over time approximate the distributions received from the Fund’s portfolio investments based on, among other considerations, distributions the Fund actually received from portfolio investments, distributions it would have received if it had been fully invested at all times, and estimated future cash flows. Such dividends are not tied to the Fund’s investment income and may not represent yield or investment return on the Fund’s portfolio. To the extent that the dividends paid exceed the distributions the Fund receives from its underlying investments, the Fund’s assets will be reduced. The Fund’s tendency to pay out a consistent dividend may change, and the Fund’s level of distributions may increase or decrease. |

The estimated characterization of the distributions paid will be either a qualified dividend or distribution (return of capital). This estimate is based on the Fund’s operating results during the period. The actual characterization of the distributions made during the period will not be determined until after the end of the fiscal year.

| E. | Master Limited Partnerships – The Fund primarily invests in MLPs. MLPs are publicly traded partnerships and limited liability companies taxed as partnerships under the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”). The Fund principally invests in MLPs that derive their revenue primarily from businesses involved in the gathering, transporting, processing, treating, storing, refining, distributing, mining or marketing of natural gas, natural gas liquids, crude oil, refined products or coal (“energy infrastructure MLPs”). The Fund is a partner in each MLP; accordingly, the Fund is required to take into account the Fund’s allocable share of income, gains, losses, deductions, expenses, and tax credits recognized by each MLP. |

The Fund is non-diversified and may invest in securities of fewer issuers than if it were diversified. Thus, the value of the Fund’s shares may vary more widely and the Fund may be subject to greater market and credit risk than if the Fund invested more broadly. The Fund also will concentrate its investments in the energy sector. Energy infrastructure MLPs are subject to a variety of industry specific risk factors that may adversely affect their business or operations, including a decrease in production or reduced volumes of natural gas or other energy commodities available for transporting, processing, storing or distributing; changes in energy commodity prices; a sustained reduced demand for crude oil, natural gas and refined petroleum products; depletion of natural gas reserves or other commodities if not replaced; natural disasters, extreme weather and environmental hazards; rising interest rates, how facilities are constructed, maintained and operated, environmental and safety controls, and the prices they may charge for products and services. In addition, taxes, government regulation, international politics, price, and supply fluctuations, volatile interest rates and energy conservation may cause difficulties for energy infrastructure MLPs.

MLP’s may be less liquid and subject to more abrupt or erratic price movements than conventional publicly traded securities.

| F. | Return of Capital – Distributions received from the Fund’s investments in MLPs generally are comprised of income and return of capital. The Fund records investment income and return of capital based on estimates made at the time such distributions are received. The return of capital portion of the distribution is a reduction to investment income that results in an equivalent reduction in the cost basis of the associated investments and increases net realized gains (losses) and change in unrealized appreciation (depreciation). Such estimates are based on historical information available from each MLP and other industry sources. These estimates will subsequently be revised and may materially differ primarily based on information received from the MLPs after their tax reporting periods are concluded. |

| G. | Federal Income Taxes – The Fund does not intend to qualify as a regulated investment company pursuant to Subchapter M of the Internal Revenue Code, but will rather be taxed as a corporation. As a corporation, the Fund is obligated to pay federal, state and local income tax on taxable income. For the year ended November 30, 2022, the federal income tax rate is 21%. The Fund is currently using an estimated rate of 1.1% for state and local tax, net of federal tax expense. |

19 Invesco SteelPath MLP Alpha Fund

The Fund’s income tax provision consists of the following as of November 30, 2022:

| | | | |

| Current tax (expense) benefit | | | |

Federal | | $ | (2,960,626) | |

State | | | — | |

Total current tax (expense) benefit | | $ | (2,960,626) | |

| |

| Deferred tax (expense) benefit | | | |

Federal | | $ | (47,914,566) | |

State | | | (3,796,259) | |

Valuation allowance | | | 48,157,641 | |

Total deferred tax (expense) benefit | | $ | (3,553,184) | |

The reconciliation between the federal statutory income tax rate of 21% and the tax effect on net investment income (loss) and realized and unrealized gain (loss) follows:

| | | | | | | | |

| | | Amount | | | % Effect | |

Application of Federal statutory income tax rate | | | $(50,895,616 | ) | | | (21.00)% | |

State income taxes net of federal benefit | | | (2,665,961 | ) | | | (1.10)% | |

Effect of state tax rate change | | | (1,548,513 | ) | | | (0.64)% | |

Effect of permanent differences | | | 705,403 | | | | 0.29% | |

Return to provision adjustments | | | (266,764 | ) | | | (0.11)% | |