UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

INVESTMENT COMPANY ACT FILE NUMBER: | | 811-05443 |

| |

| EXACT NAME OF REGISTRANT AS SPECIFIED IN CHARTER: | | Calamos Investment Trust |

| |

ADDRESS OF PRINCIPAL EXECUTIVE OFFICES: | | 2020 Calamos Court, Naperville Illinois 60563-2787 |

| |

NAME AND ADDRESS OF AGENT FOR SERVICE: | | John P Calamos, Sr., President, Calamos Advisors LLC 2020 Calamos Court, Naperville, Illinois 60563-2787 |

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (630) 245-7200

DATE OF FISCAL YEAR END: October 31, 2016

DATE OF REPORTING PERIOD: November 1, 2015 through April 30, 2016

Item 1. Report to Shareholders

Experience and Foresight

About Calamos Investments

For over 35 years, we have helped investors like you manage and build wealth to meet long-term objectives. Because investors have different time horizons, risk tolerances and goals, we offer funds to suit a variety of asset allocation needs. Our 20 mutual funds include equity, fixed income, convertible and alternative funds. We offer U.S. funds as well as global and international choices.

We are dedicated to helping our clients build and protect wealth. We understand when you entrust us with your assets, you also entrust us with your achievements, goals and aspirations. We believe we best honor this trust by making investment decisions guided by integrity, by discipline and by our conscientious research.

We believe an active, risk-conscious approach is essential for wealth creation. In the 1970s, we pioneered the use of convertible securities as a means to control risk in volatile markets. We followed with strategies that combine convertibles and stocks, with the aim of participating in equity market upside with potentially less volatility than an all-stock portfolio. In the 1990s, we introduced our first stock fund, which invests in growth companies both large and small. Across our funds, our investment process seeks to manage risk at multiple levels and draws upon our experience investing through many market cycles. In a rapidly changing environment, we believe that this active management is essential.

We are global in our perspective. We believe globalization offers tremendous opportunities for countries and companies all over the world. In our U.S., global and international portfolios, we are seeking to capitalize on the potential growth of the global economy.

We believe there are opportunities in all markets. Our history traces back to the 1970s, a period of significant volatility and economic concerns. We have invested through multiple market cycles, each with its own challenges. Out of this experience comes our belief that the flipside of volatility is opportunity.

Letter to Shareholders

JOHN P. CALAMOS, SR.

Chairman and Global CIO

Dear Fellow Shareholder:

Welcome to your semiannual report for the six-month period ended April 30, 2016. In this report, you will find commentary from the Calamos portfolio management teams, as well as a listing of portfolio holdings, financial statements and highlights, and detailed information about the performance and positioning of the Calamos Funds.

Market Review

The reporting period proved to be an extremely turbulent time in the financial markets, as changing sentiment fueled volatility and market rotation. During the final months of 2015, investors remained concerned about low commodity prices, global economic growth forecasts, and the implications of central bank policies—including the Federal Reserve’s move to raise short-term interest rates for the first time since 2006.

As 2016 began, markets fell sharply as investor apprehension increased. By mid-February, investors appeared more confident about the health of the U.S. economy and the likelihood of fewer Federal Reserve increases, while commodity prices stabilized. This increased optimism drove a rally in emerging markets, high yield bonds, and value and cyclical stocks. (A stronger economic environment can provide tailwinds for cyclically oriented companies and fewer hurdles for companies with less robust growth prospects.)

In this challenging environment, the S&P 500 Index gained 0.43% for the semiannual period. On the whole, stocks from developed markets landed in negative territory, as measured by the MSCI World Index’s return of -0.74%. Emerging market stocks were essentially flat, with a -0.01% return for the MSCI Emerging Markets Index. Global convertibles outpaced their U.S. counterparts, as the U.S. index reflected the added headwinds faced by small and mid-cap companies during the period. The BofA Merrill Lynch Global 300 Convertible Index returned 0.83%, while the BofA Merrill Lynch All U.S. Convertibles Index returned -2.88%.

Outlook

We do not believe a U.S. recession is imminent, but think the pace of expansion is likely to be measured in 2016. Similarly, we expect that the global economy will grow, but not at a robust pace overall. Around the world, we believe fiscal policy remains an overarching cause of concern, as a lack of clarity on key regulatory issues casts a shadow over a number of sectors. We believe investors will be challenged by a host of

Letter to Shareholders

uncertainties, including global growth concerns, the policies of the Federal Reserve and other central banks, the U.S. presidential election, commodity prices, and geopolitical uncertainties.

Our teams continue to identify opportunities in this slower-growth environment, but they recognize that selectivity and risk management remain crucial. We believe investment opportunities exist across many asset classes, but selectivity remains paramount. During the reporting period, swings in market sentiment illustrated investors’ tendency to respond dramatically to events and data. Our portfolio management teams are holding to their long-term discipline, seeking to capitalize on short-term investor emotion as they position the funds for longer-term opportunities.

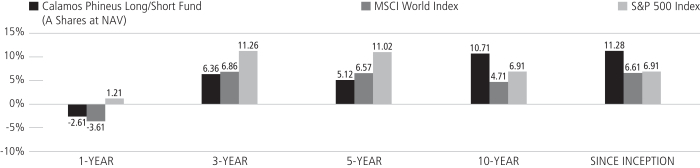

Introducing Calamos Phineus Long/Short Fund

Throughout the years, we have been proud to provide individual investors with access to institutional-caliber investment strategies, including in the alternatives asset class. When we launched Calamos Convertible Fund in 1985, we were one of the first asset managers to offer a convertible mutual fund, at a time when convertibles could be considered an alternative investment. In 1990, we launched Calamos Market Neutral Income Fund, which offers access to sophisticated strategies not broadly available to individual investors. Continuing this tradition, we introduce Calamos Phineus Long/Short Fund. In 2015, Calamos Investments acquired Phineus Partners, an established long/short manager, and we are pleased to provide investors with this time-tested long/short approach. I invite you to learn more about the fund (page 67) and to ask your financial advisor if the fund is appropriate for your needs.

Conclusion

The market environment is always changing. To keep up-to-date on our views of the global financial markets and the opportunities that are emerging, I encourage you to visit our website on an ongoing basis. You’ll find our blog and videos from our team, as well as a variety of pieces designed to help you and your financial advisor make sound asset allocation decisions that align with your long-term goals and risk tolerance.

As always, we thank you for your continued trust. All of us at Calamos Investments are honored that you have chosen us to help you achieve your financial goals.

Sincerely,

John P. Calamos, Sr.

Founder, Chairman and Global Chief Investment Officer

| | | | |

| 2 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Letter to Shareholders

Before investing, carefully consider a fund’s investment objectives, risks, charges and expenses. Please see the prospectus containing this and other information or call 800.582.6959. Please read the prospectus carefully. Performance data represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

The MSCI World Index is a market-capitalization weighted index composed of companies representative of the market structure of developed market countries in North America, Europe and the Asia/Pacific region. The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index considered broadly representative of emerging market equity performance. The index represents companies within the constituent emerging markets that are available to investors worldwide. The BofA Merrill Lynch All U.S. Convertibles Ex-Mandatory Index represents the U.S. convertible securities market excluding mandatory convertibles. The BofA Merrill Lynch Global 300 Convertible Index is a global convertible index composed of companies representative of the market structure of countries in North America, Europe and the Asia/Pacific region. Sources: Lipper, Inc.; Morningstar, Inc.

Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index. Investments in overseas markets pose special risks, including currency fluctuation and political risks. These risks are generally intensified for investments in emerging markets. Countries, regions, and sectors mentioned are presented to illustrate countries, regions, and sectors in which a fund may invest. Fund holdings are subject to change daily. The Funds are actively managed.

The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the securities mentioned. The information contained herein, while not guaranteed as to accuracy or completeness, has been obtained from sources we believe to be reliable. There are certain risks involved with investing in convertible securities in addition to market risk, such as call risk, dividend risk, liquidity risk and default risk, that should be carefully considered prior to investing. This information is being provided for informational purposes only and should not be considered investment advice or an offer to buy or sell any security in the portfolio. Investments in alternative strategies may not be suitable for all investors.

This report is intended for informational purposes only and should not be considered investment advice.

Calamos Growth Fund

OVERVIEW

The fund invests in the equities of U.S. companies from a range of market capitalizations that we believe offer the best potential for growth.

KEY FEATURES

| | ¡ | | Utilizes more than two decades of extensive research experience in growth investing | |

| | ¡ | | Active management focuses on top-down views and bottom-up fundamentals | |

| | ¡ | | Research-driven approach identifies opportunities by combining top-down analysis with a focus on key growth characteristics | |

PORTFOLIO FIT

This actively managed fund seeks to provide attractive returns through its emphasis on higher growth companies primarily in large and mid cap arenas.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CVGRX |

B Shares | | CVGBX |

C Shares | | CVGCX |

I Shares | | CGRIX |

R Shares | | CGRRX |

| | | |

|

| FUND CUSIP NUMBERS |

A Shares | | 128119302 |

B Shares | | 128119740 |

C Shares | | 128119856 |

I Shares | | 128119807 |

R Shares | | 128119435 |

| | | |

CALAMOS GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

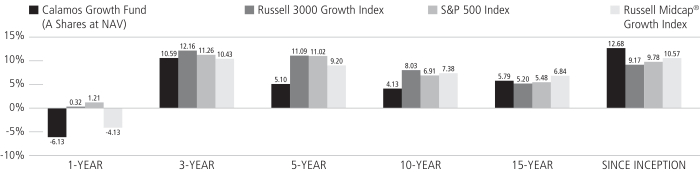

For the six-month period ended April 30, 2016, Calamos Growth Fund declined 6.37% (Class A shares at net asset value), versus a 1.64% decrease for the Russell 3000 Growth Index. For the same period the S&P 500 Index rose 0.43% and the Russell Midcap Growth Index lost 1.54%.

U.S. equities experienced a steep sell-off that started just prior to the end of calendar year 2015 through February 11, 2016. Concerns regarding falling commodity prices, China’s economic growth and potential currency devaluations, and U.S. earnings fueled recessionary fears and led investors toward safe haven investments and out of higher-growth businesses, which hurt the Fund.

As modest-yet-positive economic data was reported during the first quarter of 2016, investors returned to the equity market with a preference for value, cyclical and higher-dividend stocks. We generally take underweight positions in these categories because of their lower-growth prospects over time. As a consequence, our quality-growth focus lagged the market. When Federal Reserve Chair Janet Yellen spoke in mid-March letting investors know that the Fed foresaw two interest rate hikes and would consider global risks in their interest rate moves, growth stocks returned to favor and the Fund made a strong comeback in March, though not enough to offset earlier losses.

Since its inception on September 4, 1990, the Fund has returned 12.68% on an annualized basis (Class A shares at net asset value). We believe this demonstrates the Fund’s ability to outdistance the growth and broad indices over full market cycles. Over the same period, the Russell 3000 Growth Index returned 9.17%, while the S&P 500 Index and the Russell Midcap Growth Index returned 9.77% and 10.57%, respectively.

What factors influenced performance?

The Fund’s security selection in health care detracted the most value from performance. Specifically, selection in pharmaceuticals and health care services disappointed. Pharmaceutical names have come under pressure as negative headlines and politicians target drug pricing.

The Fund’s selection in consumer discretionary hindered performance. Holdings within the movies and entertainment industry and the cable and satellite industry detracted most. We have been favoring media and experiences as opposed to brick-and-mortar retail. Although we believe that the U.S. consumer is in better health owing to improvements in the labor and housing markets, we have preferred to focus on low-cost providers in the retail space. This tact paid off as discount retail stores contributed positively during the period.

Even though energy was the worst-performing sector in the Russell 3000 Growth Index, as oil prices came under severe pressure, our selection within energy contributed positively to the Fund’s results. We avoided areas that were most negatively impacted during the period and saw positive returns from our energy names.

Selection in industrials also benefited the fund, though the underweight hurt to a small extent. Specifically, aerospace and defense as well as airlines were most additive. We

| | | | |

| 4 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Growth Fund

believe the defense space may see increases in outlays as the geopolitical arena remains volatile.

How is the Fund positioned?

In this all-cap growth equity Fund, we seek to invest in U.S. companies that we believe have the best prospects for growth including higher sustainable growth, high relative growth, or acceleration in growth. The Fund offers a diversified approach and participates in long-term growth trends by focusing on companies with solid fundamentals, global brands, strong growth catalysts and attractive valuations. We continue to actively manage our sector exposures in conjunction with our fundamental, bottom-up research.

Our investments reflect a positive long-term outlook for equities, but we maintain a somewhat cautious view in light of economic and political conditions. We believe a combination of secular and cyclical growth holdings is appropriate, given our view that we are in a slow-growth phase of the economic cycle, yet conditions are improving for some cyclical areas of the economy. We are emphasizing companies with improving fundamentals, increasing returns on invested capital as well as more stable growth areas of the market, all the while being mindful of valuations in those spaces.

We have increased our allocation within industrials, adding to areas such as defense and environmental services. We believe that defense is an area that will continue to see growth as worrisome geopolitical events elevate fears and outlays to support the space. Industrials selection was additive to Fund performance as mentioned previously and narrowed our underweight relative to the Russell 3000 Growth Index. Conversely, we reduced investments within the consumer discretionary space, moving from a slight overweight to an underweight position relative to the benchmark. While we believe the U.S. consumer to be in decent health by virtue of increased employment and a strengthened housing market, we believe consumers will be a bit more selective in purchases, to the detriment of traditional retail and brick-and-mortar stores. We still have a considerable position in consumer discretionary names, with home improvement and entertainment names among our current favorites within the space.

What closing thoughts do you have for Fund shareholders?

The weakened U.S. dollar, a recovery in oil, and efforts from central banks around the world to reflate the global economy could create tailwinds for cyclical areas of the market. We have increased our investments in energy and industrials, as well as semiconductors within information technology. It appears that growth will remain scarce, so we believe investors will be willing to pay for those businesses that can offer superior growth. We expect to be a bit more cautious concerning valuations as higher-valued stocks may have a greater potential to sell off if volatility returns. We don’t believe that the market’s rotation to low-quality stocks is a sustained shift where companies with very low returns on capital can continue to fare well. However, cyclical growth stocks may continue to be attractive as economic growth picks up, even at a slower pace.

| | | | |

| SECTOR WEIGHTINGS | |

Information Technology | | | 30.3 | % |

Consumer Discretionary | | | 20.6 | |

Health Care | | | 16.1 | |

Industrials | | | 9.9 | |

Financials | | | 4.3 | |

Consumer Staples | | | 3.8 | |

Energy | | | 3.4 | |

Telecommunication Services | | | 1.8 | |

Materials | | | 0.7 | |

| | | | | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

Calamos Growth Fund

ANNUALIZED RETURN: SINCE INCEPTION (9/4/90) THROUGH 4/30/16

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com. Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average. All performance shown assumes reinvestment of dividends and capital gains distributions. Performance is for the Fund’s Class A shares at net asset value and does not include the Fund’s maximum front-end sales charge of 4.75%—had it been included, the Fund’s return would have been lower. The Fund also offers Class B, Class C, Class I and Class R shares, the performance of which may vary. Source: State Street Corporation and Lipper, Inc.

| | | | |

| 6 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Growth Fund

GROWTH OF $10,000: FOR THE 10-YEAR PERIOD ENDED 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | | | | | | |

| | | 6

MONTHS | | 1

YEAR | | 5

YEARS | | 10 YEARS

OR ^SINCE

INCEPTION |

Class A Shares – Inception 9/4/90 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -6.37 | % | | | | -6.13 | % | | | | 5.10 | % | | | | 4.13 | % |

With Sales Charge | | | | -10.81 | | | | | -10.59 | | | | | 4.08 | | | | | 3.63 | |

Class B Shares – Inception 9/11/00 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -6.71 | | | | | -6.82 | | | | | 4.32 | | | | | 3.51 | |

With Sales Charge | | | | -10.07 | | | | | -10.18 | | | | | 4.16 | | | | | 3.51 | |

Class C Shares – Inception 9/3/96 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -6.71 | | | | | -6.85 | | | | | 4.32 | | | | | 3.35 | |

With Sales Charge | | | | -7.33 | | | | | -7.47 | | | | | 4.32 | | | | | 3.35 | |

Class I Shares – Inception 9/18/97 | | | | -6.25 | | | | | -5.90 | | | | | 5.36 | | | | | 4.39 | |

Class R Shares – Inception 3/1/07 | | | | -6.46 | | | | | -6.35 | | | | | 4.84 | | | | | 4.93 | ^ |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.32%; Class B and C shares is 2.07%; Class I shares is 1.07%; Class R shares is 1.57%.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Performance shown reflects the effects of an expense reimbursement that improved results and was in effect until March 31, 2000. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares and returns for Class B and C have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graphs do not reflect the income taxes that you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The Russell 3000® Growth Index measures the performance of companies with higher price-to-book ratios and higher forecasted growth values. Index data shown for the Annualized Return Since Inception graph is from 8/31/90, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. Index data shown for the Annualized Return Since Inception graph is from 8/31/90, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

The Russell Midcap® Growth Index measures the performance of mid-sized companies with growth characteristics. Index data shown for the Annualized Return Since Inception graph is from 8/31/90, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

Index returns assume reinvestment of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

Calamos Opportunistic Value Fund

OVERVIEW

The fund invests in the equities of small, midsize and large U.S companies that we believe are undervalued according to certain financial measurements of their intrinsic values.

KEY FEATURES

| | ¡ | | Utilizes bottom-up stock picking and a benchmark-agnostic approach, which focuses on good businesses with solid cash flow and value prices | |

PORTFOLIO FIT

The fund is a core value option that may balance a growth allocation and complement other value strategies. Our flexibility in analyzing all companies regardless of sector helps us avoid the cyclicality inherent in a deep value strategy or momentum growth strategy.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CVAAX |

B Shares | | CVABX |

C Shares | | CVACX |

I Shares | | CVAIX |

R Shares | | CVARX |

| |

|

| FUND CUSIP NUMBERS |

A Shares | | 128119666 |

B Shares | | 128119658 |

C Shares | | 128119641 |

I Shares | | 128119633 |

R Shares | | 128119419 |

| | | |

CALAMOS OPPORTUNISTIC VALUE FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

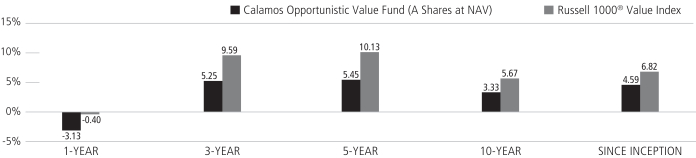

For the six-month period ended April 30, 2016, the Fund dipped 0.92% (Class A shares at net asset value) versus a gain of 1.93% for the Russell 1000 Value Index.

The Fund performed broadly in line with the Russell 1000 Value Index through the first half of the reporting period as U.S. equities experienced a steep sell-off that started just prior to the end of 2015 through February 11, 2016. Concerns of falling commodity prices, China’s economic growth and potential currency devaluations, and U.S. earnings setbacks fueled recessionary fears and led investors into safe-haven investments and out of higher-growth businesses. The market rebound in mid-February through March favored deeper cyclical and value oriented names that performed well once investors came to accept that the global economy was not falling into a recession. The Fund’s performance improved in March, but lost ground relative to the index.

What factors influenced performance?

The U.S. equity market saw a dramatic sell-off during the reporting period, with the Russell 1000 Value Index falling more than 12% by February 11. As modest-yet-positive economic data was reported midway through the quarter, it appears that investors switched gears and returned to the equity market with a preference for deeper value, cyclical and higher-dividend stocks. Federal Reserve Chair Janet Yellen spoke in mid-March letting investors know that the Fed foresaw two rather than four interest rate hikes and, additionally, would consider global risks in deciding interest rate moves. The Fed’s stance appeared to have helped the market return to more balanced leadership between cyclical and secular growth-oriented companies.

Investors in the value space showed a strong preference for lower-beta and higher-dividend stocks. Based upon economic sectors, our selection in energy and industrials were the biggest detractors to performance versus the Russell 1000 Value Index. In the energy space, which was affected by a rapid decline in oil prices worldwide, selection in refining and marketing as well as exploration and production weighed down results. Industrials saw improvement as cyclicals enjoyed success when investor demand returned. The Fund’s overweight to the sector was beneficial, but selections in electrical components and equipment holdings, despite showing strong absolute results, lagged those of the benchmark. Human resource and employment services names also impeded relative performance. The Fund’s selection within information technology added value as IT consulting and data processing and outsourced services strongly outperformed their benchmark brethren. Selection within telecommunications services also worked well for the Fund, as the market favored securities offering higher dividends as is common in telecommunications services.

How is the Fund positioned?

The Fund seeks to identify attractively valued, temporarily out of favor stocks or mispriced companies with good future business prospects. In essence, we believe that the Fund’s positioning reflects good businesses trading at value prices.

We continue to actively manage our sector exposures in conjunction with our fundamental, bottom-up research. Our research has pointed us toward opportunities in

| | | | |

| 8 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Opportunistic Value Fund

the consumer discretionary and industrials sectors, and the Fund is positioned as such. Within consumer discretionary, we have found opportunities in the movies and entertainment and specialty stores. In Industrials, our research led us to favor industrial machinery. Our most significant underweight is in the utilities sector, where we do have ownership, but have concerns of overheating valuations vis-a-vis higher-dividend and perceived safe-haven investments. During the period, we added to consumer staples, narrowing our underweight to the sector. As mentioned previously, we have concerns over the higher valuations assigned to some areas within the value universe of stocks as investors favor higher-quality, lower-volatility earnings stories. In response, we have constructed a portfolio with favorable valuation metrics such as price-to-sales and price-to-cash flow measures.

What closing thoughts do you have for Fund shareholders?

One commonly held assumption is that today’s financial landscape is fragile. We understand the concerns regarding the economy and have strategically positioned the Fund in areas of the equity market we believe have appreciation potential. Value stocks may offer opportunities as it appears to us that investors have priced in extremely modest expectations for many businesses, and have bid up other safe-haven investments. For example, we think that many consumer staples stocks trade at premiums to the market and to their own history despite negligible growth. Investors appear to be paying for the stability and defensiveness of these companies rather than their long-term potential.

Our focus remains on solid businesses with sustainable cash flows, trading at attractive prices. We are mindful of valuations and have been trimming positions where valuations may subject stocks to increased volatility. In addition, we have used market pullbacks in an attempt to selectively add to positions offering solid fundamentals.

| | | | |

SECTOR WEIGHTINGS | |

Financials | | | 27.6 | % |

Energy | | | 13.0 | |

Health Care | | | 11.9 | |

Information Technology | | | 11.6 | |

Industrials | | | 11.4 | |

Consumer Discretionary | | | 6.8 | |

Consumer Staples | | | 6.2 | |

Utilities | | | 4.5 | |

Materials | | | 2.3 | |

Telecommunication Services | | | 2.3 | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

ANNUALIZED RETURN: SINCE INCEPTION (1/2/02) THROUGH 4/30/16

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com. Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average. All performance shown assumes reinvestment of dividends and capital gains distributions. Performance is for the Fund’s Class A shares at net asset value and does not include the Fund’s maximum front-end sales charge of 4.75%—had it been included, the Fund’s return would have been lower. The Fund also offers Class B, Class C, Class I and Class R shares, the performance of which may vary. Performance shown reflects an expense reimbursement that improved results. Source: State Street Corporation and Lipper, Inc.

Calamos Opportunistic Value Fund

GROWTH OF $10,000: FOR THE 10-YEAR PERIOD ENDED 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | | | | | | |

| | | 6

MONTHS | | 1

YEAR | | 5

YEARS | | 10 YEARS

OR ^SINCE

INCEPTION |

Class A Shares – Inception 1/2/02 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -0.92 | % | | | | -3.13 | % | | | | 5.45 | % | | | | 3.33 | % |

With Sales Charge | | | | -5.64 | | | | | -7.70 | | | | | 4.43 | | | | | 2.83 | |

Class B Shares – Inception 1/2/02 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -1.25 | | | | | -3.85 | | | | | 4.67 | | | | | 2.71 | |

With Sales Charge | | | | -5.82 | | | | | -8.30 | | | | | 4.33 | | | | | 2.71 | |

Class C Shares – Inception 1/2/02 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -1.35 | | | | | -3.91 | | | | | 4.66 | | | | | 2.56 | |

With Sales Charge | | | | -2.26 | | | | | -4.80 | | | | | 4.66 | | | | | 2.56 | |

Class I Shares – Inception 3/1/02 | | | | -0.82 | | | | | -2.91 | | | | | 5.72 | | | | | 3.58 | |

Class R Shares – Inception 3/1/07 | | | | -0.99 | | | | | -3.37 | | | | | 5.19 | | | | | 2.80 | ^ |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.60%; Class B shares is 2.34%; Class C shares is 2.35%; Class I shares is 1.34%; Class R shares is 1.86%. The Fund’s investment advisor has contractually agreed to reimburse Fund expenses through March 1, 2017, to the extent necessary so that Total Annual Fund Operating Expenses (excluding taxes, interest, short interest, short dividend expenses, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses, if any) of Class A, Class B, Class C, Class I and Class R are limited to 1.15%, 1.90%, 1.90%, 0.90% and 1.40% of average net assets, respectively.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Performance shown reflects the effects of an expense reimbursement that improved results and was in effect until March 31, 2004. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares and returns for Class B and C shares have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graphs do not reflect the income taxes that you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The Russell 1000® Value Index measures the performance of those companies in the Russell 1000® Index with lower price-to-book ratios and lower forecasted growth values. Index data shown for the Annualized Return Since Inception graph is from 12/31/01, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

Index returns assume reinvestment of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

| | | | |

| 10 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Focus Growth Fund

CALAMOS FOCUS GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

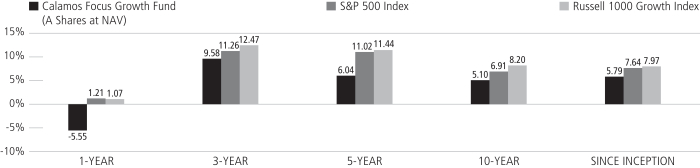

For the six-month period ended April 30, 2016, the Fund declined 5.66% (Class A Shares at net asset value) versus a return of 0.43% for the S&P 500 Index and a loss of 1.37% for the Russell 1000 Growth Index.

The Fund had performed broadly in line with the U.S. equity market as well as growth stocks through early February, but lagged during a value-oriented market rally in the last two months of the reporting period. The sectors that led the rally in March and April included energy, materials, industrials and financials.

Since its inception on December 1, 2003, the Fund has returned 5.79% NAV versus returns of 7.64% for the S&P 500 Index and 7.97% for the Russell 1000 Growth Index.

What factors influenced performance?

The Fund was challenged in a period characterized by a dramatic and broad sell-off in the marketplace in January. Investors appeared to be concerned about global growth, a rising U.S. dollar, and the dollar’s effects on U.S. corporate earnings. The Russell 1000 Growth Index had declined 11.16% from January 1, 2016 through February 11, 2016 (the market’s low for the reporting period). The subsequent rally was led by cyclical areas of the market (energy, materials, and industrials) and value stocks, counter to the Fund’s growth bias and positioning.

Holdings within the health care sector lagged those of the Russell 1000 Growth Index. The biotechnology industry came under pressure as drug price increases made negative news headlines, and the names held within the Fund subsequently underperformed. Additionally, our ownership of higher growth pharmaceuticals fell out of favor as more conservative pharmaceutical names drew investor attention in the reporting period. Selection within the cable and satellite industry of consumer discretionary also detracted from results. Selection within energy added to performance, as names held within the portfolio finished in positive territory for the period, while the sector was the biggest laggard in the Russell 1000 Growth Index. Additionally, selection within industrials performed well for the Fund, most notably within defense and environmental services.

How is the Fund positioned?

This large cap growth equity Fund invests in a diversified, yet concentrated portfolio of common stocks. We seek to invest in U.S. companies that we believe have the best prospects for growth, including higher sustainable growth, high relative growth, or acceleration in growth. We aim to participate in long-term growth trends by focusing on companies with solid or improving fundamentals, global brands, strong growth catalysts and attractive valuations.

We believe our investments reflect a positive long-term outlook for equities, but we maintain a somewhat cautious view in light of economic and political conditions. We believe a combination of secular and cyclical growth holdings is appropriate, given our view that we are in a slow-growth phase of the economic cycle, yet conditions are improving for some cyclical areas of the economy. We are emphasizing companies that

OVERVIEW

The fund invests in a select portfolio of equities issued by “blue chip” U.S. companies that offer opportunities for growth.

KEY FEATURES

| | ¡ | | Active management utilizes over 20 years of extensive research experience in growth investing | |

| | ¡ | | The compact portfolio comprises only those large cap stocks in which we have the greatest confidence of sustained growth | |

| | ¡ | | Stresses company fundamentals, including global presence, strong or accelerated earnings growth, and solid returns on invested capital | |

PORTFOLIO FIT

The fund is a core growth allocation centered on a compact equity portfolio of large cap stocks.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CBCAX |

B Shares | | CBCBX |

C Shares | | CBXCX |

I Shares | | CBCIX |

R Shares | | CBCRX |

| | | |

|

| FUND CUSIP NUMBERS |

A Shares | | 128119625 |

B Shares | | 128119617 |

C Shares | | 128119591 |

I Shares | | 128119583 |

R Shares | | 128119427 |

| | | |

Calamos Focus Growth Fund

| | | | |

| SECTOR WEIGHTINGS | |

Information Technology | | | 35.2 | % |

Consumer Discretionary | | | 20.2 | |

Health Care | | | 14.8 | |

Industrials | | | 9.0 | |

Consumer Staples | | | 3.9 | |

Financials | | | 3.8 | |

Energy | | | 3.0 | |

Telecommunication Services | | | 2.3 | |

Materials | | | 0.7 | |

| | | | | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

we believe have improving fundamentals and increasing returns on invested capital. We also look for more stable growth areas of the market, while being mindful of valuations in those spaces.

We increased our allocation within industrials, adding to areas such as defense and environmental services. We believe that defense is an area that will continue to see growth as worrisome geopolitical events elevate fears and outlays to support the space. The additions to industrials was additive to Fund performance as mentioned previously and we narrowed our underweight relative to the Russell 1000 Growth Index. Conversely, we reduced investments within the consumer discretionary space, moving from a slight overweight to an underweight position relative to the benchmark. While we believe the U.S. consumer to be in decent health by virtue of increased employment and a strengthened housing market, we believe consumers will be a bit more selective in purchases, to the detriment of traditional retail and brick-and-mortar stores. We still have a considerable position in consumer discretionary names, with home improvement and entertainment names among our current favorites within the space.

What closing thoughts do you have for Fund shareholders?

The weakened U.S. dollar, a recovery in oil, and efforts from central banks around the world to reflate the global economy could create tailwinds for cyclical areas of the market. We have increased our investments in energy and industrials, as well as semiconductors within information technology. Growth may remain scarce, so we believe investors may be willing to pay for those businesses that can offer superior growth. We expect to be a bit more cautious concerning valuations as higher-valued stocks may have a greater potential to sell off if volatility returns. We don’t believe that the market’s rotation to low-quality stocks is a sustained shift where companies with very low returns on capital can continue to fare well. However, cyclical growth stocks may continue to be attractive as economic growth picks up.

ANNUALIZED RETURN: SINCE INCEPTION (12/1/03) THROUGH 4/30/16

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com. Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average. All performance shown assumes reinvestment of dividends and capital gains distributions. Performance is for the Fund’s Class A shares at net asset value and does not include the Fund’s maximum front-end sales charge of 4.75%—had it been included, the Fund’s return would have been lower. The Fund also offers Class B, Class C, Class I and Class R shares, the performance of which may vary. Performance shown reflects an expense reimbursement that improved results. Source: State Street Corporation and Lipper, Inc.

| | | | |

| 12 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Focus Growth Fund

GROWTH OF $10,000: FOR THE 10-YEAR PERIOD ENDED 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | | | | | | |

| | | 6

MONTHS | | 1

YEAR | | 5

YEARS | | 10 YEARS

OR ^SINCE

INCEPTION |

Class A Shares – Inception 12/1/03 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -5.66 | % | | | | -5.55 | % | | | | 6.04 | % | | | | 5.10 | % |

With Sales Charge | | | | -10.13 | | | | | -10.03 | | | | | 5.02 | | | | | 4.59 | |

Class B Shares – Inception 12/1/03 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -6.00 | | | | | -6.23 | | | | | 5.24 | | | | | 4.46 | |

With Sales Charge | | | | -9.79 | | | | | -10.01 | | | | | 4.94 | | | | | 4.46 | |

Class C Shares – Inception 12/1/03 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -6.00 | | | | | -6.23 | | | | | 5.26 | | | | | 4.31 | |

With Sales Charge | | | | -6.76 | | | | | -6.99 | | | | | 5.26 | | | | | 4.31 | |

Class I Shares – Inception 12/1/03 | | | | -5.57 | | | | | -5.31 | | | | | 6.31 | | | | | 5.36 | |

Class R Shares – Inception 3/1/07 | | | | -5.71 | | | | | -5.71 | | | | | 5.79 | | | | | 4.73 | ^ |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.58%; Class B and C shares is 2.33%; Class I shares is 1.33%; Class R shares is 1.85%. The Fund’s investment advisor has contractually agreed to reimburse Fund expenses through March 1, 2017 to the extent necessary so that Total Annual Fund Operating Expenses (excluding taxes, interest, short interest, short dividend expenses, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses, if any) of Class A, Class B, Class C, Class I and Class R are limited to 1.15%, 1.90%, 1.90%, 0.90% and 1.40% of average net assets, respectively.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Performance shown reflects the effects of an expense reimbursement that improved results and was in effect until March 31, 2004. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares and returns for Class B and C shares have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graphs do not reflect the income taxes that you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. Index data shown for the Since Inception Growth of $10,000 graph is from 11/30/03, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price to-book ratios and higher forecasted growth values. Index data shown for the Since Inception Growth of $10,000 graph is from 11/30/03, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

Index returns assume reinvestment of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

Calamos Discovery Growth Fund

OVERVIEW

The fund invests in small and midsize U.S. companies that we believe offer the best potential for growth.

KEY FEATURES

| | ¡ | | Employs bottom-up stock selection based on a combination of quantitative and fundamental research drivers | |

| | ¡ | | Applies in-depth research to add value in the inefficient small and mid cap market | |

| | ¡ | | Emphasizes risk management and portfolio construction in a process that seeks greater risk-adjusted returns over a full market cycle | |

PORTFOLIO FIT

The fund is a SMID cap growth equity allocation option.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CADGX |

B Shares | | CBDGX |

C Shares | | CCDGX |

I Shares | | CIDGX |

R Shares | | CRDGX |

| | | |

|

| FUND CUSIP NUMBERS |

A Shares | | 128120102 |

B Shares | | 128120201 |

C Shares | | 128120300 |

I Shares | | 128120409 |

R Shares | | 128120508 |

| | | |

CALAMOS DISCOVERY GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

For the six-month period ended April 30, 2016, the Fund declined 8.80% (Class A shares at net asset value) versus a loss of 3.05% for the Russell 2500 Growth Index.

The Fund performed in line with the Russell 2500 Growth Index through the first half of the reporting period as U.S. equities experienced a steep sell-off that started just prior to the end of 2015 and continued until February 11, 2016. Concerns of falling commodity prices, China’s economic growth and potential currency devaluations, and U.S. earnings fueled recessionary fears and led investors into safe-haven investments and out of higher-growth businesses. The Fund lagged as the market rebound in mid-February favored cyclical and value-oriented names that performed well once investors seemed to accept that the global economy was not falling into a recession.

What factors influenced performance?

The mid cap growth space saw a dramatic sell-off during the reporting period, with the Russell 2500 Growth Index falling more than 20% by February 11. As modest-yet-positive economic data was reported midway through the first quarter of 2016, investors switched gears and returned to the equity market with a preference for value, cyclical and higher-dividend stocks. In mid-March, Federal Reserve Chair Janet Yellen told investors that the Fed foresaw two rather than four interest rate hikes and would consider global risks in deciding interest rate moves. After those comments, growth stocks returned to favor for the month, much as they had for most of 2015.

Investors in this space showed a strong preference for lower-beta and higher-dividend stocks. Based upon economic sectors, our selection in consumer discretionary and information technology were the biggest detractors to relative performance versus the Russell 2500 Growth Index. Selection in auto parts and equipment and restaurants took the biggest hit within consumer discretionary. Within information technology, Internet software and services names lagged those of the benchmark.

Alternatively, selection within health care and energy, the two worst-performing sectors within the index for the period, added to the Fund’s relative performance. Selection in pharmaceuticals and health care equipment worked well as did underweighting the biotechnology industry, which came under severe pressure during the period. Turning to energy, stocks within the exploration and services industry outperformed, and the Fund also benefitted from avoiding other areas within energy that were severely challenged.

How is the Fund positioned?

This Fund seeks to invest in small and midsize U.S. companies that we believe have the best prospects for high sustainable or accelerated growth. The Fund takes a diversified and active approach that participates in long-term growth trends and focuses on companies with solid fundamentals, global brands, strong growth catalysts and attractive valuations. Our investments reflect what we believe to be a positive long-term outlook for equities. We believe a combination of secular and cyclical growth holdings is appropriate, given our view that we are in a business cycle characterized by

| | | | |

| 14 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Discovery Growth Fund

low inflation and moderate global growth. The Fund holds these secular and cyclical opportunities where we believe expectations for growth are unreasonably low, creating the investment opportunity. We are emphasizing companies with sound growth fundamentals, increasing returns on invested capital and attractive valuations.

We continue to actively manage our sector exposures in conjunction with our fundamental, bottom-up research. Our largest absolute weightings by sector include opportunities within the information technology, consumer discretionary and health care sectors. We believe that technology offers great long-term growth opportunities as well as some cyclical investments as well. We also believe the U.S. consumer is in overall good health as the employment and housing markets have improved, yet we are selective in the consumer discretionary space, with a preference for low-cost providers in the retail space and more experiential discretionary purchases such as entertainment. We believe health care still offers great opportunity, but we have been cautious on account of negative drug pricing headlines and highly politicized public concerns. We have added to cyclical areas such as energy and industrials, albeit at small absolute levels.

What closing thoughts do you have for Fund shareholders?

We believe the U.S. market will have modestly positive returns and may represent a compelling equity market in a low-return world. We do not foresee a recession in the U.S., but trends in housing and employment point to a slow-growth economy. The market will remain volatile and is anxiously awaiting further news from the Federal Reserve as to the path of potential interest rate moves and indications of strong, self-sustaining economic expansion.

The weakened U.S. dollar, a recovery in oil, and efforts from central banks around the world to reflate the global economy could create tailwinds for cyclical areas of the market. In response, we have increased our investments in energy and industrials. Growth may remain scarce, so we believe investors will be willing to pay for those businesses that can offer superior growth. We expect to be a bit more cautious around valuation as higher-valued stocks may have greater potential for selling off if volatility returns. We don’t believe that the market’s rotation to low-quality stocks is a sustained shift where companies with low returns on capital can continue to fare well. However, cyclical growth stocks may continue to be attractive as economic growth picks up, even at a slower pace.

| | | | |

| SECTOR WEIGHTINGS | |

Information Technology | | | 29.0 | % |

Health Care | | | 25.1 | |

Consumer Discretionary | | | 18.7 | |

Industrials | | | 10.0 | |

Financials | | | 9.0 | |

Energy | | | 3.6 | |

Telecommunication Services | | | 2.4 | |

Materials | | | 1.3 | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

Calamos Discovery Growth Fund

GROWTH OF $10,000: SINCE INCEPTION (6/1/10) THROUGH 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | | | | | | |

| | | 6

MONTHS | | 1

YEAR | | 5

YEARS | | SINCE

INCEPTION |

Class A Shares – Inception 6/1/2010 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -8.80 | % | | | | -17.35 | % | | | | -1.16 | % | | | | 6.47 | % |

With Sales Charge | | | | -13.12 | | | | | -21.30 | | | | | -2.11 | | | | | 5.59 | |

Class B Shares – Inception 6/1/2010 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -9.22 | | | | | -18.03 | | | | | -1.89 | | | | | 5.68 | |

With Sales Charge | | | | -13.71 | | | | | -22.09 | | | | | -2.19 | | | | | 5.55 | |

Class C Shares – Inception 6/1/2010 | | | | | | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -9.14 | | | | | -17.97 | | | | | -1.89 | | | | | 5.68 | |

With Sales Charge | | | | -10.04 | | | | | -18.78 | | | | | -1.89 | | | | | 5.68 | |

Class I Shares – Inception 6/1/2010 | | | | -8.66 | | | | | -17.10 | | | | | -0.89 | | | | | 6.75 | |

Class R Shares – Inception 6/1/2010 | | | | -8.92 | | | | | -17.51 | | | | | -1.39 | | | | | 6.22 | |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.64%; Class B and Class C shares is 2.39%; Class I shares is 1.39%; Class R shares is 1.89%. The Fund’s investment advisor has contractually agreed to reimburse Fund expenses through March 1, 2017, to the extent necessary so that Total Annual Fund Operating Expenses (excluding taxes, interest, short interest, short dividend expenses, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses, if any) of Class A, Class B, Class C, Class I and Class R are limited to 1.50%, 2.25%, 2.25%, 1.25% and 1.75% of average net assets, respectively.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares and returns for Class B and C shares have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graph does not reflect the income taxes you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The Russell 2500™ Growth Index measures the performance of the small- to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. Source: Lipper, Inc.

Index returns assume reinvestments of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

| | | | |

| 16 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Dividend Growth Fund

CALAMOS DIVIDEND GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

For the six-month period ended April 30, 2016, the Fund decreased 1.02% (Class A shares at net asset value) versus a 0.43% gain for the S&P 500 Index and a 0.22% gain for the Russell 1000 Index.

The Fund performed in line with the U.S. equity market as U.S. equities experienced a steep sell-off that started prior to the end of 2015 through February 11, 2016. Concerns of falling commodity prices, China’s economic growth and potential currency devaluations, and U.S. earnings setbacks fueled recessionary fears and led investors toward safe-haven investments and out of higher-growth businesses. The Fund lagged slightly as the market rebound favored cyclical and value-oriented names that performed well after investors appeared to accept that the global economy was not falling into a recession.

What factors influenced performance?

The Fund’s slight overweights to the telecommunications services and utilities sectors bolstered performance as these sectors typically represent higher-dividend-paying securities and were the two leading sectors within the S&P 500 Index for the reporting period. Selection in the consumer discretionary sector also provided a lift to Fund performance as stocks from the advertising and home improvement retail spaces were beneficial. Conversely, stock selection in energy detracted from performance as a small allocation to the oil and-gas storage and transportation industry disappointed. Energy names rebounded strongly during the period, and were led by large cap integrated oil and gas names. Selection within the consumer staples sector lagged because of our lack of holdings in the strong performing packaged foods and meats industry.

How is the Fund positioned?

The Fund’s investments reflect our positive yet cautious long-term outlook for equities and our preference for dividend-paying companies with sound fundamentals and attractive valuations. Furthermore, we seek companies that have an ability to increase dividends over time, either through increasing profits or more efficient use of capital. We continue to actively manage our sector exposures in conjunction with our fundamental, bottom-up research approach. The Fund has slight overweights to telecommunications services and the utilities sectors, while remaining underweight energy, information technology and financials. The Fund’s largest allocations in absolute terms are in the information technology, financials and health care sectors.

OVERVIEW

The fund invests in companies that we believe have the ability to increase dividends over time, either through increasing profits or more efficient use of capital.

KEY FEATURES

| | ¡ | | Utilizes bottom-up stock picking and a benchmark-agnostic approach, which focuses on good businesses with solid cash flow and value prices | |

PORTFOLIO FIT

The fund seeks to provide a regular stream of income and dividend-paying equity investments that tend to be less volatile than non-dividend payers.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CADVX |

C Shares | | CCDVX |

I Shares | | CIDVX |

R Shares | | CRDVX |

|

| FUND CUSIP NUMBERS |

A Shares | | 128120839 |

C Shares | | 128120821 |

I Shares | | 128120813 |

R Shares | | 128120797 |

Calamos Dividend Growth Fund

| | | | |

| SECTOR WEIGHTINGS | |

Information Technology | | | 18.0 | % |

Health Care | | | 14.7 | |

Financials | | | 14.6 | |

Consumer Discretionary | | | 12.8 | |

Industrials | | | 9.8 | |

Consumer Staples | | | 9.5 | |

Energy | | | 5.5 | |

Utilities | | | 3.6 | |

Telecommunication Services | | | 3.5 | |

Materials | | | 2.1 | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

Our focus remains on solid businesses with sustainable cash flows, trading at attractive prices. We are mindful of valuations and have been trimming positions where valuations may subject stocks to increased volatility. In addition, we have used market pullbacks in an attempt to selectively add to positions offering solid fundamentals.

| | | | |

| 18 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Dividend Growth Fund

GROWTH OF $10,000: SINCE INCEPTION (8/5/13) THROUGH 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | |

| | | 6

MONTHS | | 1

YEAR | | SINCE

INCEPTION |

Class A Shares – Inception 8/5/2013 | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -1.02 | % | | | | -1.67 | % | | | | 3.22 | % |

With Sales Charge | | | | -5.68 | | | | | -6.36 | | | | | 1.39 | |

Class C Shares – Inception 8/5/2013 | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -1.34 | | | | | -2.37 | | | | | 2.45 | |

With Sales Charge | | | | -2.30 | | | | | -3.32 | | | | | 2.45 | |

Class I Shares – Inception 8/5/2013 | | | | -0.93 | | | | | -1.39 | | | | | 3.46 | |

Class R Shares – Inception 8/5/2013 | | | | -1.22 | | | | | -1.97 | | | | | 2.93 | |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.74%; Class C shares is 2.51%; Class I shares is 1.49%; Class R shares is 1.99%. The Fund’s Investment Adviser has contractually agreed to reimburse Fund expenses through March 1, 2017 to the extent necessary so that Total Annual Fund Operating Expenses (excluding taxes, interest, short interest, short dividend expenses, brokerage commissions, acquired fund fees and expenses and extraordinary expenses, if any) of Class A, Class C, Class I and Class R are limited to 1.35%, 2.10%, 1.10% and 1.60% of average net assets, respectively. This agreement is not terminable by either party.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares. Returns for Class C shares have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graph does not reflect the income taxes that you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. Index data shown for the Annualized Return Since Inception graph is from 8/31/13, since comparative index data is only available for full monthly periods. Source: Lipper, Inc.

The Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership.

Index returns assume reinvestment of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

Calamos Mid Cap Growth Fund

OVERVIEW

The fund invests primarily in equity securities issued by midsize U.S. companies that we believe offer the best opportunities for growth.

KEY FEATURES

| | ¡ | | Utilizes more than two decades of extensive research experience in growth investing | |

| | ¡ | | Focuses on top-down views and bottom-up fundamentals | |

| | ¡ | | Identifies opportunities by combining top-down analysis with a focus on key growth characteristics | |

PORTFOLIO FIT

The fund seeks to diversify an equity allocation with a primarily mid cap growth strategy that provides exposure to companies with historically higher growth rates and returns than larger companies.

| | |

| FUND NASDAQ SYMBOLS |

A Shares | | CMXAX |

C Shares | | CMXCX |

I Shares | | CMXIX |

R Shares | | CMXRX |

|

| FUND CUSIP NUMBERS |

A Shares | | 128120870 |

C Shares | | 128120862 |

I Shares | | 128120854 |

R Shares | | 128120847 |

CALAMOS MID CAP GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund performed?

For the six-month period ended April 30, 2016, the Fund declined 7.59% (Class A shares at net asset value) versus a decrease of 1.54% for the Russell Midcap Growth Index.

In this Fund, we target mid cap companies with established track records and strong revenue and earnings profiles with high or accelerated growth. Many of these businesses were out of favor during the reporting period as investors showed a preference for perceived safe haven investments including dividend-paying securities.

What factors influenced performance?

The mid cap growth space had a dramatic sell-off during the reporting period, with the Russell Midcap Growth Index falling more than 15% by February 11. Concerns of falling commodity prices, China’s economic growth and potential currency devaluations, and U.S. earnings fueled recessionary fears and led investors into safe-haven investments and out of higher-growth businesses. As modest yet positive economic data was reported during the quarter, investors returned to the equity market, with a preference for value, cyclical and higher-dividend stocks. In mid-March, Federal Reserve Chair Janet Yellen told investors that the Fed foresaw two rather than four interest rate hikes and would consider global risks in deciding interest rate moves. After those comments, growth stocks returned to favor for the month, much as they had for most of 2015.

Investors in this space showed a strong preference for lower-beta and higher-dividend stocks. Based upon economic sectors, our selection in financials and health care were the biggest detractors to performance versus the Russell Midcap Growth Index. Specifically, an overweight to and selection among real estate services names and selection within consumer finance weighed on performance. Real estate investment trusts (REITs), which the Fund did not own, did well as dividend-paying securities. Selection in potentially higher-growth biotechnology and pharmaceutical names trailed in the health care sector; pressure mounted on drug companies as concerns over pricing weighed on their outlook.

Selection in the energy sector added value during the period, as did some well-timed additions to the once beleaguered sector. The Fund benefitted from positions in the exploration and production space as well as avoiding some of the heavy equipment industry within energy. The Fund also benefitted from selection within the telecommunications services sector as wireless services names performed well.

How is the Fund positioned?

This Fund seeks to invest in midsize U.S. companies that we believe have the best prospects for high sustainable or accelerated growth. The Fund offers a diversified and active approach, and seeks to participate in long-term growth trends by focusing on companies that we believe have solid fundamentals, global brands, strong growth catalysts and attractive valuations. Our investments reflect what we believe to be a positive long-term outlook for equities. We believe a combination of secular and

| | | | |

| 20 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

Calamos Mid Cap Growth Fund

cyclical growth holdings is appropriate, given our view that we are in a business cycle characterized by low inflation and moderate global growth. The Fund holds these secular and cyclical opportunities where we believe expectations for growth are unreasonably low, creating investment opportunities. We are emphasizing companies with sound growth fundamentals, increasing returns on invested capital and attractive valuations.

We continue to actively manage our sector exposures in conjunction with our fundamental, bottom-up research. Our largest absolute weightings by sector include opportunities within the information technology, consumer discretionary and health care sectors. We believe that technology offers great long term growth opportunities as well as some cyclical investments as well. We also believe the U.S. consumer is overall in good health as the employment and housing markets have improved, but we are selective in the consumer discretionary space, with a preference for low-cost providers in the retail space and more experiential discretionary purchases such as entertainment. We think that health care still offers great opportunities, but we have been cautious on account of negative drug pricing headlines and highly politicized public concerns. We have added to cyclical areas such as energy, materials and industrials, albeit at small absolute levels.

What closing thoughts do you have for Fund shareholders?

We believe the U.S. market will have modestly positive returns and may represent a compelling equity market in a low-return world. We do not foresee a recession in the U.S., but trends in housing and employment point to a slow-growth economy. We believe the market will remain volatile and is anxiously awaiting news from the Federal Reserve as to the path of potential interest rate moves and indications of strong, self-sustaining economic expansion.

The weakened U.S. dollar, a recovery in oil, and efforts from central banks around the world to reflate the global economy can create tailwinds for cyclical areas of the market. In response, we have increased our investments in energy and industrials. Growth may remain scarce, so we believe investors will be willing to pay for those businesses that can offer superior growth. We expect to be a bit more cautious around valuation as higher-valued stocks may have greater potential for sell-offs if volatility returns. We don’t believe that the market’s rotation to low-quality stocks is a sustained shift where companies with low returns on capital can continue to fare well. However, cyclical growth stocks may continue to be attractive as economic growth picks up, even at a slower pace.

| | | | |

| SECTOR WEIGHTINGS | |

Consumer Discretionary | | | 24.8 | % |

Information Technology | | | 23.9 | |

Health Care | | | 19.3 | |

Industrials | | | 12.6 | |

Financials | | | 9.3 | |

Telecommunication Services | | | 4.0 | |

Energy | | | 3.5 | |

Materials | | | 0.9 | |

Sector weightings are subject to change daily and are calculated as a percentage of net assets. The table excludes cash or cash equivalents, any government/sovereign bonds or broad based index hedging securities the Fund may hold.

Calamos Mid Cap Growth Fund

GROWTH OF $10,000: SINCE INCEPTION (8/5/13) THROUGH 4/30/16

AVERAGE ANNUAL TOTAL RETURN† AS OF 4/30/16

| | | | | | | | | | | | | | | |

| | | 6

MONTHS

| | 1

YEAR | | SINCE

INCEPTION |

Class A Shares – Inception 8/5/2013 | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -7.59 | % | | | | -16.19 | % | | | | 0.01 | % |

With Sales Charge | | | | -11.98 | | | | | -20.14 | | | | | -1.76 | |

Class C Shares – Inception 8/5/2013 | | | | | | | | | | | | | | | |

Without Sales Charge | | | | -7.93 | | | | | -16.84 | | | | | -0.74 | |

With Sales Charge | | | | -8.79 | | | | | -17.61 | | | | | -0.74 | |

Class I Shares – Inception 8/5/2013 | | | | -7.45 | | | | | -16.02 | | | | | 0.27 | |

Class R Shares – Inception 8/5/2013 | | | | -7.64 | | | | | -16.42 | | | | | -0.22 | |

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by visiting www.calamos.com.

As of the prospectus dated 2/29/16, the Fund’s gross expense ratio for Class A shares is 1.69%; Class C shares is 2.46%; Class I shares is 1.45%; Class R shares is 1.97%. The Fund’s Investment Adviser has contractually agreed to reimburse the Fund expenses through March 1, 2017, to the extent necessary so that Total Annual Fund Operating Expenses (excluding taxes, interest, short interest, short dividend expenses, brokerage commissions, acquired funds fees and expenses and extraordinary expenses, if any) of Class A, Class C, Class I and Class R are limited to 1.25%, 2.00%, 1.00% and 1.50% of average net assets, respectively. This agreement is not terminable by either party.

| † | Average annual total return measures net investment income and capital gain or loss from portfolio investments as an annualized average assuming reinvestment of dividends and capital gains distributions. Load-adjusted returns are adjusted for the maximum front-end sales load of 4.75% for Class A shares. Returns for Class C shares have been adjusted for the contingent deferred sales charge (CDSC). |

NOTES:

The graph does not reflect the income taxes that you would pay on fund distributions or the redemption of fund shares. Fund performance includes reinvestment of dividends and adjustment for the maximum sales charge for Class A shares. The performance of other classes will vary from the performance of the class shown based on the difference in sales charges and fees paid by shareholders investing in different share classes.

The Russell Midcap Growth Index measures the performance of midcap growth companies.

Index returns assume reinvestment of dividends and do not reflect deduction of fees and expenses. It is not possible to invest directly in an index.

| | | | |

| 22 | | CALAMOS OPEN-END FAMILY OF FUNDS SEMIANNUAL REPORT | | |

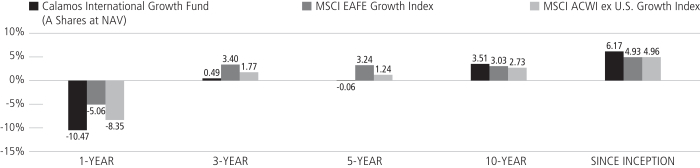

Calamos International Growth Fund

CALAMOS INTERNATIONAL GROWTH FUND

INVESTMENT TEAM DISCUSSION

How has the Fund Performed?

For the six-month period ended April 30, 2016, Calamos International Growth Fund declined 5.55% (Class A shares at net asset value) versus a 1.05% decrease for the MSCI ACWI ex-U.S. Growth Index and 1.44% loss for the MSCI EAFE Growth Index.