CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:

(811-05635)

Exact name of registrant as specified in charter:

Putnam Diversified Income Trust

Address of principal executive offices:

One Post Office Square, Boston, Massachusetts 02109

Name and address of agent for service:

Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109

Copy to:

Bryan Chegwidden, Esq. Ropes & Gray LLP 1211 Avenue of the Americas New York, New York 10036

Registrant’s telephone number, including area code:

(617) 292-1000

Date of fiscal year end:

September 30, 2015

Date of reporting period:

October 1, 2014 – March 31, 2015

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Putnam Diversified Income Trust

Semiannual report 3 | 31 | 15

Message from the Trustees

1

About the fund

2

Performance snapshot

4

Interview with your fund’s portfolio manager

5

Your fund’s performance

12

Your fund’s expenses

14

Terms and definitions

16

Other information for shareholders

17

Financial statements

18

Consider these risks before investing: International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons including general financial market conditions, changing market perceptions of the risk of default, changes in government intervention, and factors related to a specific issuer or industry. These factors may also lead to periods of high volatility and reduced liquidity in the bond markets. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

The month of March 2015 marked the six-year milestone of the bull market in U.S. stocks, and this June will be the sixth anniversary of the beginning of the U.S. economic recovery as dated by the National Bureau of Economic Research, which has traced the chronology of U.S. business cycles back to 1854.

While six years is above the historical average on both counts, reaching these milestones does not necessarily indicate anything about the sustainability of the expansion or the market advance. However, we believe it is an unusually long period for the Federal Reserve to have refrained from raising interest rates. The Fed now appears poised to act, and speculation is mounting about where equity and fixed-income markets around the world could go from this point forward. Your portfolio manager provides a perspective in the following pages.

At this juncture of the market cycle, you might consult your financial advisor who can help you review your goals and risk profile, and explain the importance of timely adjustments to keep your portfolio equipped for all seasons.

As you make progress toward your long-term financial goals, markets may move in different directions. With Putnam, you are aligned with a group of portfolio managers and analysts who are experienced in navigating through changing markets with consistent strategies. They are dedicated to active, fundamental research and to helping you meet your financial needs.

As always, thank you for investing with Putnam.

Respectfully yours,

Robert L. Reynolds President and Chief Executive Officer Putnam Investments

Jameson A. Baxter Chair, Board of Trustees

May 11, 2015

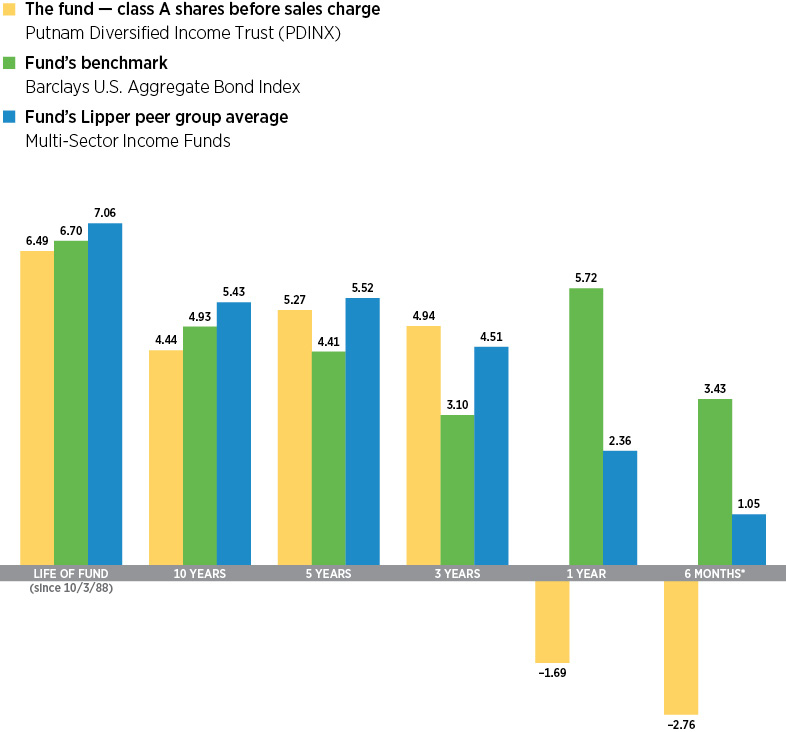

Performance snapshot

Annualized total return (%) comparison as of 3/31/15

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 12–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

*Returns for the six-month period are not annualized, but cumulative.

4 Diversified Income Trust

Interview with your fund’s portfolio manager

D. William Kohli

Bill, what was the bond market environment like during the six months ended March 31, 2015?

The period was punctuated by episodes of interest-rate volatility, but interest rates generally moved lower. We were not surprised to see some degree of interest rate volatility, given that the Federal Reserve ended its bond-buying program in October 2014 and the European Central Bank [ECB] officially announced its version of quantitative easing in January. Additionally, with U.S. gross domestic product growing at a 5% annual rate in the third quarter of 2014 — its strongest pace in 11 years — investors sought to fine-tune their forecasts as to when the Fed may begin raising short-term interest rates.

In January, the combination of a stock market pullback, weaker-than-expected U.S. economic data, and continued worries about deflation in Europe fueled investors’ appetite for government bonds. Against this backdrop, the yield on the benchmark 10-year U.S. Treasury fell to 1.64%, its low for the period. In February, concern that the Fed might start raising rates in June hampered Treasuries, causing prices to fall and yields to move higher. During March, however, dovish comments by Fed Chair Janet Yellen reassured investors that the central bank was likely to take a go-slow approach toward raising interest rates, which helped Treasuries modestly rebound during the final weeks of the period. The 10-year Treasury yield finished

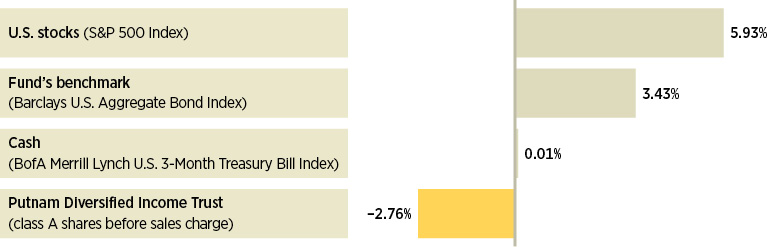

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/15. See pages 4 and 12–13 for additional fund performance information. Index descriptions can be found on page 17.

Diversified Income Trust 5

the period at 1.92%, down from 2.49% at the beginning of the period.

The U.S. dollar continued to strengthen, rising more than 14% on an absolute basis during the six-month reporting period and outpacing every other major currency, according to the WSJ Dollar Index. The dollar’s surge against the euro was driven by the ECB’s launch of a larger-than-expected monetary easing program at the same time that the U.S. central bank stated its intention to raise interest rates.

After declining since midsummer 2014, oil prices settled into a trading range in February and March. Prices fluctuated in the low-to-mid $50-per-barrel range on signs that U.S. production may be peaking and global demand may be rising.

The fund lagged its benchmark by a significant margin during the period. What factors hampered its relative performance?

It’s important to point out that the fund’s benchmark comprises securities from various U.S.-government and corporate investment-grade sectors, and many of these sectors performed well during the six-month reporting period. Our strategy of investing in a variety of out-of-benchmark sectors, which has served the fund well over the long term, was largely unrewarded during the period. However, our biggest overall detractor was

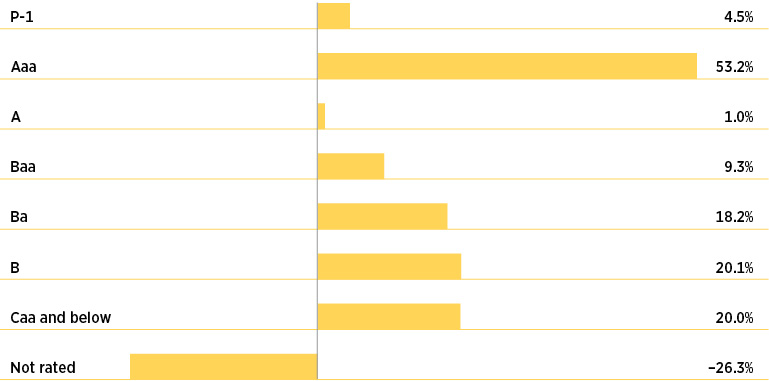

Credit quality overview

Credit qualities are shown as a percentage of the fund’s net assets as of 3/31/15. A bond rated Baa or higher (Prime-3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s (S&P) or, if unrated by S&P, by Fitch ratings, and then included in the closest equivalent Moody’s rating based on analysis of these agencies’ respective ratings criteria. Moody’s ratings are used in recognition of its prominence among rating agencies and breadth of coverage of rated securities. To-be-announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings may vary over time.

Derivative instruments, including forward currency contracts, are only included to the extent of any unrealized gain or loss on such instruments and are shown in the not-rated category. Cash is also shown in the not-rated category. Derivative offset values are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

6 Diversified Income Trust

“Globally, economies are currently in one of the most disparate growth cycles since the mid-to-late 1990s.”

Bill Kohli

the fund’s interest-rate and yield-curve positioning in the United States. The portfolio was defensively positioned for a rising-rate environment, resulting in an overall duration — a key measure of interest-rate sensitivity — that was moderately negative on a net basis. Unfortunately, because rates trended lower during the period, this positioning worked against the fund’s performance.

Elsewhere, our prepayment strategies, which we implemented with securities such as agency interest-only collateralized mortgage obligations [IO CMOs], also detracted. In January, the Obama administration announced that the Federal Housing Administration [FHA] would reduce the annual mortgage insurance premiums it charges to borrowers making small down payments. Investors reacted to this development by pricing in the possibility of faster mortgage prepayment speeds, which dampened the returns of existing prepayment-sensitive mortgage-backed securities. What’s more, this announcement came during a time when Treasury yields

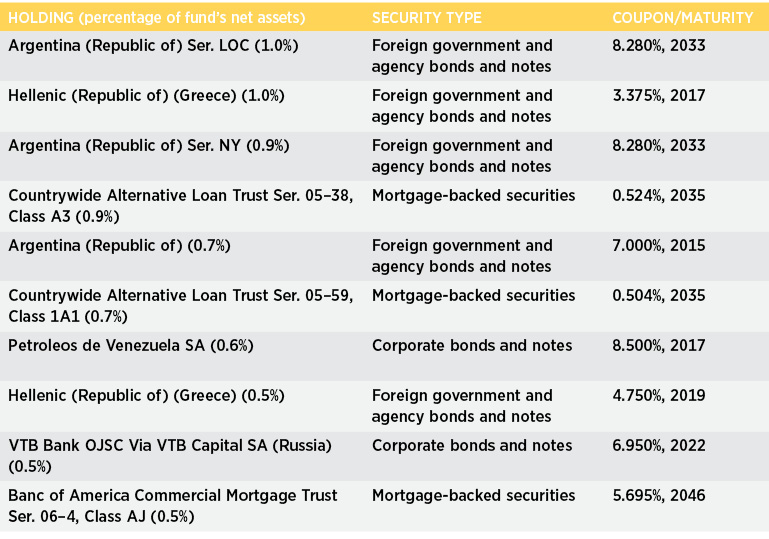

Top 10 holdings

This table shows the fund’s top 10 individual holdings and the percentage of the fund’s net assets that each represented as of 3/31/15. Short-term holdings, TBA commitments, and derivatives, if any, are excluded. Holdings may vary over time.

Diversified Income Trust 7

were sharply declining, compounding the negatives for IO CMOs. The asset class rebounded in February, but could not fully overcome January’s significant downturn.

Our investments in emerging-market [EM] debt, specifically U.S. dollar-denominated holdings in Venezuela and Russia, modestly hampered the fund’s performance. During the first half of the period, declining oil prices soured investor sentiment toward the bonds of these oil-exporting countries. Continued uncertainty regarding Ukraine also weighed on Russia’s bonds.

Within foreign sovereign debt, our exposure to Greece detracted as Greek yields rose sharply. Increasing uncertainty about Greece’s prospects for accessing new financing and its ability to remain within the European Union weighed on the country’s bonds.

Positions in high-yield bonds had a neutral impact on the fund’s return. Following a volatile period during 2014’s fourth quarter, high-yield bonds rallied in late January and February, fueled by oil prices settling into a trading range.

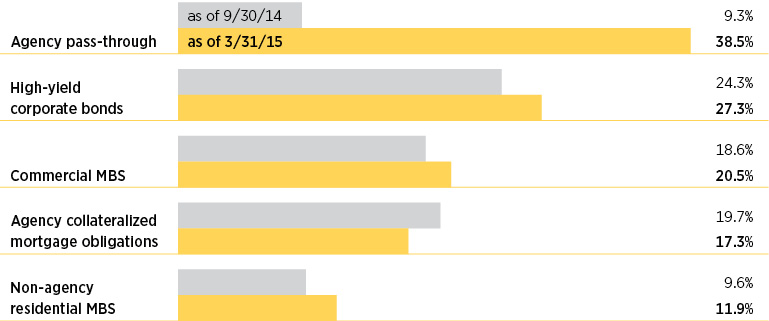

Comparison of top sector weightings

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

8 Diversified Income Trust

Turning to the positive side, which investments helped the fund’s performance?

Active currency positioning was the biggest contributor, as a long position in the U.S. dollar combined with short positions in most other major market currencies bolstered the fund’s performance. One exception to this strategy was a long position in the British pound sterling, which weakened relative to the U.S. dollar and slightly dampened the positive overall effect of our currency positioning.

Our mortgage credit investments, specifically positions in subordinated mezzanine commercial mortgage-backed securities [CMBS] and non-agency residential mortgage-backed securities [RMBS], also helped performance. Mezzanine CMBS benefited from supportive commercial real estate fundamentals, an improving U.S. economy, and persistent investor demand for higher-yielding bonds. Within non-agency RMBS, our holdings of Alternative-A [Alt-A] securities were helped by a strengthening housing market, coupled with solid investor demand amid shrinking supply. Alt-A securities are created from mortgage pools that occupy the space between riskier subprime mortgages and less risky prime mortgages.

How did you use derivatives during the period?

We used bond futures and interest-rate swaps to take tactical positions at various points along the yield curve, and to hedge the risk associated with the fund’s curve positioning. We also employed interest-rate swaps to help manage the fund’s duration and yield-curve positioning, and to gain exposure to interest rates in various countries. In addition, total return swaps were utilized as a hedging tool, and to help manage the portfolio’s sector exposure, as well as its inflation risk. Lastly, we used currency forward contracts to hedge the foreign exchange risk associated with non-U.S. bonds, and to efficiently gain exposure to foreign currencies.

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates. In other examples, the managers may use options and futures contracts to hedge against a variety of risks by establishing a combination of long and short exposures to specific equity markets or sectors.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

Diversified Income Trust 9

The fund reduced its dividend rate during the period. What factors led to that decision?

Prior to 2014, the fund had maintained a stable dividend rate for several years. Recently, however, it became necessary to decrease the dividend rate due to lower available yields across fixed-income market sectors and the need to maintain a somewhat greater cash balance. As a result, the fund’s dividend per class A share was trimmed from $0.032 to $0.027 in October 2014. Similar reductions were made to other share classes.

What is your outlook for the coming months, and how are you positioning the fund?

We remain positive on U.S. economic growth, but it appears the recovery has reverted to a moderate pace after surging in the middle of last year. We believe this slowdown is partly because consumption has not increased as much as was expected. During the past year, rising hourly wages and lower gasoline prices benefited lower-wage workers, which we thought would bolster personal consumption expenditures. However, rather than spending more, these consumers increased their savings. According to the Commerce Department, personal spending increased slightly in February, but was down in December and January. At the same time, the personal savings rate continued to climb, reaching 5.8% in February, its highest level since the end of 2012. As the effects of an unseasonably cold winter in the Northeast and Midwest dissipate, we think consumption will improve.

We believe the Fed is likely to begin raising rates during 2015, possibly in September. Many investors believe the Fed will wait until later in 2015, or even into 2016, before it begins hiking rates. Consequently, there appears to be a considerable disconnect between what the market is forecasting and the Fed’s own outlook, which could spark some volatility. In our view, however, once the central bank begins to raise the federal funds rate, it will make every effort to do so in an orderly, well-communicated fashion in an effort to avoid major financial market disruption.

Globally, economies are currently in one of the most disparate growth cycles since the mid-to-late 1990s. Capital is flowing from the eurozone and elsewhere into the United States, seeking to capitalize on opportunities in stocks, high-yield bonds, mortgage-backed securities, and government debt. As a result, developing markets are under pressure since many of those economies require capital inflows to maintain their fiscal and monetary programs. Because of this, we are not enthusiastic about near-term prospects in emerging markets overall, although we continue to find what we believe are attractive country-specific investment opportunities.

Within this environment, we plan to maintain our diversified mortgage, corporate, and sovereign credit exposure primarily through allocations to mezzanine CMBS, high-yield bonds, and peripheral European sovereign bonds, respectively. As for prepayment risk, we expect to maintain our holdings of IO CMOs. We do not believe the new FHA policy is likely to have a major impact on the overall pace of residential refinancing. What’s more, we continue to find prepayment risk attractive, given the potential for higher interest rates as the U.S. economic recovery matures. We’re also excited about ongoing opportunities we see in the foreign-exchange market. Many of the fundamental drivers of currency performance, such as divergent trends in U.S. and foreign economic growth and monetary policies, appear to be gaining momentum.

Thanks for your time and for bringing us up to date, Bill.

10 Diversified Income Trust

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager D. William Kohli is Co-Head of Fixed Income at Putnam. He has an M.B.A. from the Haas School of Business at the University of California, Berkeley, and a B.A. from the University of California, San Diego. Bill joined Putnam in 1994 and has been in the investment industry since 1986.

In addition to Bill, your fund’s portfolio managers are Michael J. Atkin, Kevin F. Murphy, Michael V. Salm, and Paul D. Scanlon, CFA.

IN THE NEWS

Although the U.S. economy is showing positive trends, uneven growth in consumer spending remains a bit perplexing. Despite rising personal income and lower energy costs, consumer spending in the United States rose by only 0.1% in February after dropping 0.2% in January, according to the Commerce Department. Harsh winter weather during those months, with heavy snowfalls blanketing the Northeast and Midwest, may have discouraged millions of Americans from heading to stores. Amid weak spending, the pace of hiring also slowed to 126,000 new jobs in March, the lowest since December 2013. These soft readings, however, might be as temporary as the weather. The personal savings rate rose from 5.5% in January to 5.8% in February, with Americans reaching their highest levels in savings in more than two years. In short, consumers have money to spend, and a rebound in economic activity, along the lines of that seen in 2014, may be likely.

Diversified Income Trust 11

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2015, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R5, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 3/31/15

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

(inception dates)

(10/3/88)

(3/1/93)

(2/1/99)

(12/1/94)

(12/1/03)

(11/1/13)

(11/1/13)

(7/1/96)

Before sales charge

After sales charge

Before CDSC

After CDSC

Before CDSC

After CDSC

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Annual average

(life of fund)

6.49%

6.33%

6.24%

6.24%

5.68%

5.68%

6.20%

6.06%

6.21%

6.66%

6.67%

6.66%

10 years

54.37

48.19

45.66

45.66

42.81

42.81

50.45

45.56

49.73

57.66

57.92

57.68

Annual average

4.44

4.01

3.83

3.83

3.63

3.63

4.17

3.83

4.12

4.66

4.68

4.66

5 years

29.26

24.09

24.50

22.62

24.56

24.56

27.60

23.45

27.62

30.76

30.98

30.78

Annual average

5.27

4.41

4.48

4.16

4.49

4.49

5.00

4.30

5.00

5.51

5.55

5.51

3 years

15.57

10.94

13.07

10.12

13.03

13.03

14.69

10.97

14.78

16.44

16.64

16.46

Annual average

4.94

3.52

4.18

3.26

4.17

4.17

4.68

3.53

4.70

5.20

5.26

5.21

1 year

–1.69

–5.62

–2.44

–7.13

–2.45

–3.38

–1.96

–5.15

–1.96

–1.41

–1.26

–1.41

6 months

–2.76

–6.65

–3.02

–7.79

–3.03

–3.98

–2.92

–6.08

–2.80

–2.65

–2.50

–2.65

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance reflects conversion to class A shares after eight years.

12 Diversified Income Trust

Comparative index returns For periods ended 3/31/15

Barclays U.S. Aggregate Bond Index

Lipper Multi-Sector Income Funds category average*

Annual average (life of fund)

6.70%

7.06%

10 years

61.74

71.07

Annual average

4.93

5.43

5 years

24.10

31.26

Annual average

4.41

5.52

3 years

9.60

14.23

Annual average

3.10

4.51

1 year

5.72

2.36

6 months

3.43

1.05

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

*Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/15, there were 280, 256, 182, 145, 93, and 5 funds, respectively, in this Lipper category.

Fund price and distribution information For the six-month period ended 3/31/15

Distributions

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Number

6

6

6

6

6

6

6

6

Income

$0.162

$0.134

$0.135

$0.153

$0.152

$0.173

$0.174

$0.173

Capital gains

—

—

—

—

—

—

—

—

Total

$0.162

$0.134

$0.135

$0.153

$0.152

$0.173

$0.174

$0.173

Share value

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

9/30/14

$7.89

$8.22

$7.81

$7.76

$7.77

$8.03

$7.80

$7.82

$7.82

$7.82

3/31/15

7.51

7.82

7.44

7.39

7.39

7.64

7.43

7.44

7.45

7.44

Current rate (end of period)

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Current dividend rate 1

4.31%

4.14%

3.55%

3.73%

4.22%

4.08%

4.04%

4.68%

4.67%

4.68%

Current 30-day SEC yield 2

N/A

4.43

3.86

3.86

N/A

4.22

4.36

4.89

4.96

4.87

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

Diversified Income Trust 13

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Total annual operating expenses for the fiscal year ended 9/30/14

0.97%

1.72%

1.72%

1.22%

1.22%

0.71%*

0.64%*

0.72%

Annualized expense ratio for the six-month period ended 3/31/15

0.95%

1.70%

1.70%

1.20%

1.20%

0.69%

0.62%

0.70%

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

*Other expenses for class R5 and class R6 shares have been annualized.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from October 1, 2014, to March 31, 2015. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Expenses paid per $1,000*†

$4.67

$8.35

$8.35

$5.90

$5.90

$3.39

$3.05

$3.44

Ending value (after expenses)

$972.40

$969.80

$969.70

$970.80

$972.00

$973.50

$975.00

$973.50

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

14 Diversified Income Trust

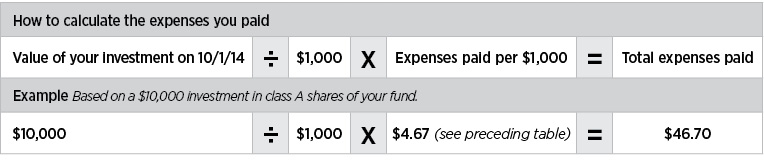

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended March 31, 2015, use the following calculation method. To find the value of your investment on October 1, 2014, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Expenses paid per $1,000*†

$4.78

$8.55

$8.55

$6.04

$6.04

$3.48

$3.13

$3.53

Ending value (after expenses)

$1,020.19

$1,016.45

$1,016.45

$1,018.95

$1,018.95

$1,021.49

$1,021.84

$1,021.44

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

Diversified Income Trust 15

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to employer-sponsored retirement plans.

Class R5 and R6 shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

•Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

•Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

•Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

•Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

•Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

16 Diversified Income Trust

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2014, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2015, Putnam employees had approximately $494,000,000 and the Trustees had approximately $141,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

Diversified Income Trust 17

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

18 Diversified Income Trust

The fund’s portfolio 3/31/15 (Unaudited)

U.S. GOVERNMENT AND AGENCY MORTGAGE OBLIGATIONS (53.0%)*

Principal amount

Value

U.S. Government Guaranteed Mortgage Obligations (—%)

Government National Mortgage Association Pass-Through Certificates 6 1/2s, November 20, 2038

$471,901

$544,713

544,713

U.S. Government Agency Mortgage Obligations (53.0%)

Federal Home Loan Mortgage Corporation Pass-Through Certificates 4s, TBA, April 1, 2045

44,000,000

47,004,373

Federal National Mortgage Association Pass-Through Certificates

5 1/2s, TBA, April 1, 2045

23,000,000

25,903,750

4 1/2s, TBA, May 1, 2045

252,000,000

274,207,500

4 1/2s, TBA, April 1, 2045

338,000,000

368,736,875

4s, TBA, April 1, 2045

289,000,000

309,026,804

3 1/2s, TBA, May 1, 2045

433,000,000

453,787,377

3 1/2s, TBA, April 1, 2045

488,000,000

512,666,887

3s, TBA, April 1, 2045

1,207,000,000

1,234,157,500

3,225,491,066

Total U.S. government and agency mortgage obligations (cost $3,203,864,674)

Total foreign government and agency bonds and notes (cost $636,092,240)

$539,579,316

SENIOR LOANS (2.4%)* c

Principal amount

Value

Basic materials (0.1%)

Atkore International, Inc. bank term loan FRN 4 1/2s, 2021

$1,786,500

$1,764,169

HD Supply, Inc. bank term loan FRN Ser. B, 4s, 2018

957,961

959,158

Ineos US Finance, LLC bank term loan FRN 3 3/4s, 2018

675,920

671,817

Oxea Sarl bank term loan FRN 8 1/4s, 2020 (Germany)

507,000

468,975

WR Grace & Co. bank term loan FRN 2 3/4s, 2021

1,670,495

1,669,003

WR Grace & Co. bank term loan FRN Ser. DD, 2 3/4s, 2021

601,125

600,588

6,133,710

Capital goods (0.1%)

ADS Waste Holdings, Inc. bank term loan FRN Ser. B, 3 3/4s, 2019

1,965,360

1,942,637

Gates Global, LLC/Gates Global Co. bank term loan FRN 4 1/4s, 2021

2,251,685

2,241,834

4,184,471

Communication services (0.2%)

Asurion, LLC bank term loan FRN 8 1/2s, 2021

4,695,000

4,713,583

Asurion, LLC bank term loan FRN Ser. B1, 5s, 2019

1,759,115

1,763,828

Level 3 Financing, Inc. bank term loan FRN Ser. B1, 4s, 2020

1,360,000

1,361,983

Level 3 Financing, Inc. bank term loan FRN Ser. B5, 4 1/2s, 2022

3,105,000

3,118,861

10,958,255

Consumer cyclicals (1.2%)

Caesars Entertainment Operating Co., Inc. bank term loan FRN Ser. B6, 9.005s, 2017

10,444,111

9,536,779

Caesars Entertainment Operating Co., Inc. bank term loan FRN Ser. B7, 11 3/4s, 2017

1,258,675

1,143,821

Caesars Growth Properties Holdings, LLC bank term loan FRN 6 1/4s, 2021

4,461,288

3,943,778

CCM Merger, Inc. bank term loan FRN Ser. B, 4 1/2s, 2021

3,376,881

3,385,324

Dollar Tree Stores, Inc. bank term loan FRN Ser. B, 4 1/4s, 2022

1,195,000

1,207,136

Garda World Security Corp. bank term loan FRN Ser. B, 4s, 2020 (Canada)

1,186,412

1,179,985

Garda World Security Corp. bank term loan FRN Ser. DD, 4s, 2020 (Canada)

303,501

301,857

Getty Images, Inc. bank term loan FRN Ser. B, 4 3/4s, 2019

5,128,815

4,313,333

Hilton Worldwide Finance, LLC bank term loan FRN Ser. B, 3 1/2s, 2020

2,507,961

2,510,200

iHeartCommunications, Inc. bank term loan FRN Ser. D, 6.922s, 2019

6,774,000

6,433,607

JC Penney Corp., Inc. bank term loan FRN 5s, 2019

9,244,410

9,090,334

Navistar, Inc. bank term loan FRN Ser. B, 5 3/4s, 2017

3,741,308

3,756,898

Neiman Marcus Group, Ltd., Inc. bank term loan FRN 4 1/4s, 2020

7,735,596

7,702,194

PetSmart, Inc. bank term loan FRN Ser. B, 5s, 2022

4,675,000

4,707,935

ROC Finance, LLC bank term loan FRN 5s, 2019

6,222,101

6,004,328

Diversified Income Trust 53

SENIOR LOANS (2.4%)* c cont.

Principal amount

Value

Consumer cyclicals cont.

Talbots, Inc. (The) bank term loan FRN 8 1/4s, 2021

$930,000

$885,825

Tribune Media Co. bank term loan FRN Ser. B, 4s, 2020

2,028,650

2,027,636

Univision Communications, Inc. bank term loan FRN 4s, 2020

4,560,273

4,550,300

Visteon Corp. bank term loan FRN Class B, 3 1/2s, 2021

1,692,213

1,688,512

74,369,782

Consumer staples (0.2%)

BC ULC bank term loan FRN Ser. B, 4 1/2s, 2021 (Canada)

3,270,862

3,301,235

CEC Entertainment, Inc. bank term loan FRN Ser. B, 4s, 2021

2,376,000

2,343,924

Del Monte Foods, Inc. bank term loan FRN 8 1/4s, 2021

1,435,000

1,291,500

H.J. Heinz Co. bank term loan FRN Ser. B2, 3 1/4s, 2020

930,279

930,163

Libbey Glass, Inc. bank term loan FRN Ser. B, 3 3/4s, 2021

1,488,750

1,479,445

Revlon Consumer Products Corp. bank term loan FRN Ser. B, 4s, 2019

2,990,598

2,987,796

WNA Holdings, Inc. bank term loan FRN 8 1/2s, 2020

1,000,000

986,250

13,320,313

Energy (—%)

Fieldwood Energy, LLC bank term loan FRN 8 3/8s, 2020

2,311,000

1,681,253

Shelf Drilling Holdings, Ltd. bank term loan FRN 10s, 2018 ‡‡

1,346,000

901,820

2,583,073

Health care (0.2%)

Grifols Worldwide Operations USA, Inc. bank term loan FRN 3.172s, 2021

3,960,000

3,954,555

MPH Acquisition Holdings, LLC bank term loan FRN Ser. B, 3 3/4s, 2021

2,551,892

2,543,234

Ortho-Clinical Diagnostics, Inc. bank term loan FRN Ser. B, 4 3/4s, 2021

1,424,238

1,409,773

Par Pharmaceutical Cos., Inc. bank term loan FRN Class B2, 4s, 2019

1,514,986

1,511,830

Patheon, Inc. bank term loan FRN Ser. B, 4 1/4s, 2021 (Netherlands)

2,578,883

2,563,841

Valeant Pharmaceuticals International, Inc. bank term loan FRN Ser. E, 3 1/2s, 2020

1,064,623

1,064,124

13,047,357

Technology (0.3%)

Avaya, Inc. bank term loan FRN Ser. B3, 4.676s, 2017

3,057,144

3,007,848

Avaya, Inc. bank term loan FRN Ser. B6, 6 1/2s, 2018

3,276,488

3,266,023

Dell International, LLC bank term loan FRN Ser. B, 4 1/2s, 2020

4,174,848

4,196,883

First Data Corp. bank term loan FRN 4.174s, 2021

61,131

61,372

First Data Corp. bank term loan FRN Ser. B, 3.674s, 2018

824,435

823,576

Freescale Semiconductor, Inc. bank term loan FRN Ser. B5, 5s, 2021

3,664,200

3,681,213

15,036,915

Transportation (0.1%)

Air Medical Group Holdings, Inc. bank term loan FRN 7 5/8s, 2018 ‡‡

3,750,000

3,768,750

3,768,750

Utilities and power (—%)

Texas Competitive Electric Holdings Co., LLC bank term loan FRN 4.662s, 2017

3,098,000

1,851,610

Texas Competitive Electric Holdings Co., LLC bank term loan FRN 4.662s, 2017

31,795

19,003

1,870,613

Total senior loans (cost $149,612,742)

$145,273,239

54 Diversified Income Trust

PURCHASED SWAP OPTIONS OUTSTANDING (1.1%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.175/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.175

$412,098,000

$5,645,743

(2.0875)/3 month USD-LIBOR-BBA/Jul-25

Jul-15/2.0875

206,049,000

3,618,220

(2.685)/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.685

402,015,100

2,327,667

1.816/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.816

402,015,100

498,499

Barclays Bank PLC

(2.1625)/3 month USD-LIBOR-BBA/May-25

May-15/2.1625

402,015,100

3,364,866

(2.31)/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

80,403,020

2,663,752

2.31/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

80,403,020

944,735

Citibank, N.A.

2.20/3 month USD-LIBOR-BBA/May-25

May-15/2.20

439,954,600

7,892,786

2.172/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.172

206,049,000

2,812,569

2.043/3 month USD-LIBOR-BBA/May-25

May-15/2.043

201,007,550

2,096,509

1.4015/3 month USD-LIBOR-BBA/May-20

May-15/1.4015

804,030,200

2,090,479

(2.13)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.13

402,015,100

1,612,081

1.294/3 month USD-LIBOR-BBA/May-20

May-15/1.294

804,030,200

1,181,924

1.3735/3 month USD-LIBOR-BBA/May-20

May-15/1.3735

402,015,100

908,554

1.266/3 month USD-LIBOR-BBA/May-20

May-15/1.266

402,015,100

506,539

1.802/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.802

402,015,100

438,196

Credit Suisse International

2.25/3 month USD-LIBOR-BBA/May-25

May-15/2.25

621,470,200

13,187,598

2.09125/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09125

411,334,000

3,414,072

2.09/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09

411,334,000

3,381,165

1.795/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.795

403,037,400

411,098

Goldman Sachs International

2.655/3 month USD-LIBOR-BBA/May-45

May-15/2.655

100,503,775

6,313,647

(2.82)/3 month USD-LIBOR-BBA/Jan-46

Jan-16/2.82

78,040,450

2,946,027

1.84/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.84

301,511,000

648,249

1.76/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.76

301,511,000

355,783

Total purchased swap options outstanding (cost $62,019,834)

$69,260,758

PURCHASED OPTIONS OUTSTANDING (0.1%)*

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/$102.57

$204,000,000

$1,838,856

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/103.07

224,000,000

1,730,176

Total purchased options outstanding (cost $6,821,250)

$3,569,032

CONVERTIBLE BONDS AND NOTES (—%)*

Principal amount

Value

iStar Financial, Inc. cv. sr. unsec. unsub. notes 3s, 2016 R

$910,000

$1,077,781

Total convertible bonds and notes (cost $952,257)

$1,077,781

Diversified Income Trust 55

SHORT-TERM INVESTMENTS (11.0%)*

Principal amount/shares

Value

Putnam Money Market Liquidity Fund 0.09% L

Shares 12,188,174

$12,188,174

Putnam Short Term Investment Fund 0.09% L

Shares 341,186,155

341,186,155

SSgA Prime Money Market Fund Class N 0.02% P

Shares 46,348,000

46,348,000

U.S. Treasury Bills with an effective yield of 0.03%, April 9, 2015 # Δ §

$39,400,000

39,399,764

U.S. Treasury Bills with an effective yield of 0.02%, July 2, 2015 Δ

750,000

749,938

U.S. Treasury Bills with an effective yield of 0.02%, April 23, 2015 Δ §

41,700,000

41,699,453

U.S. Treasury Bills with an effective yield of 0.01%, May 21, 2015 Δ §

23,300,000

23,299,628

U.S. Treasury Bills with an effective yield of 0.01%, May 14, 2015 # Δ §

124,200,000

124,198,960

U.S. Treasury Bills with effective yields ranging from 0.10% to 0.11%, July 23, 2015 # Δ §

39,618,000

39,613,007

U.S. Treasury Bills with effective yields ranging from 0.01% to 0.02%, May 7, 2015 # Δ §

3,104,000

3,103,950

Total short-term investments (cost $671,779,111)

$671,787,029

TOTAL INVESTMENTS

Total investments (cost $9,439,625,782)

$9,329,099,887

Key to holding’s currency abbreviations

AUD

Australian Dollar

BRL

Brazilian Real

CAD

Canadian Dollar

CHF

Swiss Franc

EUR

Euro

GBP

British Pound

JPY

Japanese Yen

KRW

South Korean Won

MXN

Mexican Peso

NOK

Norwegian Krone

NZD

New Zealand Dollar

PLN

Polish Zloty

SEK

Swedish Krona

USD/$

United States Dollar

ZAR

South African Rand

Key to holding’s abbreviations

bp

Basis Points

EMTN

Euro Medium Term Notes

FRB

Floating Rate Bonds: the rate shown is the current interest rate at the close of the reporting period

FRN

Floating Rate Notes: the rate shown is the current interest rate or yield at the close of the reporting period

IFB

Inverse Floating Rate Bonds, which are securities that pay interest rates that vary inversely to changes in the market interest rates. As interest rates rise, inverse floaters produce less current income. The rate shown is the current interest rate at the close of the reporting period.

IO

Interest Only

MTN

Medium Term Notes

OAO

Open Joint Stock Company

56 Diversified Income Trust

OJSC

Open Joint Stock Company

OTC

Over-the-counter

PO

Principal Only

REGS

Securities sold under Regulation S may not be offered, sold or delivered within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933.

TBA

To Be Announced Commitments

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from October 1, 2014 through March 31, 2015 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification 820 Fair Value Measurements and Disclosures and references to “OTC”, if any, represent over-the-counter.

*

Percentages indicated are based on net assets of $6,086,532,427.

†

This security is non-income-producing.

††

The interest rate and date shown parenthetically represent the new interest rate to be paid and the date the fund will begin accruing interest at this rate.

‡‡

Income may be received in cash or additional securities at the discretion of the issuer.

#

This security, in part or in entirety, was pledged and segregated with the broker to cover margin requirements for futures contracts at the close of the reporting period.

Δ

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on certain derivative contracts at the close of the reporting period.

§

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on the initial margin on certain centrally cleared derivative contracts at the close of the reporting period.

c

Senior loans are exempt from registration under the Securities Act of 1933, as amended, but contain certain restrictions on resale and cannot be sold publicly. These loans pay interest at rates which adjust periodically. The interest rates shown for senior loans are the current interest rates at the close of the reporting period. Senior loans are also subject to mandatory and/or optional prepayment which cannot be predicted. As a result, the remaining maturity may be substantially less than the stated maturity shown (Notes 1 and 6).

F

This security is valued at fair value following procedures approved by the Trustees. Securities may be classified as Level 2 or Level 3 for ASC 820 based on the securities’ valuation inputs (Note 1).

i

This security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts (Note 1).

L

Affiliated company (Note 5). The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

P

This security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts. The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period (Note 1).

R

Real Estate Investment Trust.

At the close of the reporting period, the fund maintained liquid assets totaling $4,306,206,862 to cover certain derivative contracts and delayed delivery securities.

Debt obligations are considered secured unless otherwise indicated.

144A after the name of an issuer represents securities exempt from registration under Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

See Note 1 to the financial statements regarding TBA commitments.

The dates shown on debt obligations are the original maturity dates.

Diversified Income Trust 57

DIVERSIFICATION BY COUNTRY

Distribution of investments by country of risk at the close of the reporting period, excluding collateral received, if any (as a percentage of Portfolio Value):

United States

87.2%

Argentina

2.4

Greece

2.1

Russia

1.3

Canada

1.0

Venezuela

1.0

Luxembourg

0.7

United Kingdom

0.7

Indonesia

0.5

Mexico

0.5

Other

2.6

Total

100.0%

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $2,504,201,645) (Unaudited)

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

Bank of America N.A.

Australian Dollar

Buy

4/15/15

$17,173,461

$17,220,870

$(47,409)

British Pound

Buy

6/17/15

16,275,423

17,026,835

(751,412)

Canadian Dollar

Sell

4/15/15

44,550,360

47,033,922

2,483,562

Euro

Sell

6/17/15

21,877,662

24,098,432

2,220,770

Norwegian Krone

Buy

6/17/15

2,214,472

1,854,263

360,209

Barclays Bank PLC

Australian Dollar

Buy

4/15/15

18,845,897

19,167,168

(321,271)

British Pound

Buy

6/17/15

15,412,532

15,325,730

86,802

Canadian Dollar

Sell

4/15/15

59,533,998

62,186,196

2,652,198

Euro

Sell

6/17/15

8,448,498

9,313,627

865,129

Japanese Yen

Sell

5/20/15

15,310,810

15,616,150

305,340

Mexican Peso

Buy

4/15/15

29,662,138

30,498,809

(836,671)

New Zealand Dollar

Sell

4/15/15

12,499,073

12,107,945

(391,128)

Singapore Dollar

Sell

5/20/15

31,007,588

30,793,261

(214,327)

Swedish Krona

Buy

6/17/15

13,351,174

14,404,072

(1,052,898)

Swiss Franc

Sell

6/17/15

19,405,125

19,720,751

315,626

Citibank, N.A.

Australian Dollar

Buy

4/15/15

27,183,418

26,922,628

260,790

Brazilian Real

Buy

4/2/15

1,547,054

1,539,121

7,933

Brazilian Real

Sell

4/2/15

1,547,054

1,809,602

262,548

Brazilian Real

Sell

7/2/15

1,505,427

1,498,164

(7,263)

British Pound

Buy

6/17/15

14,880,268

15,426,218

(545,950)

Canadian Dollar

Sell

4/15/15

43,767,327

46,001,704

2,234,377

Chilean Peso

Buy

4/15/15

30,952,877

30,833,027

119,850

Danish Krone

Sell

6/17/15

29,145,507

30,474,153

1,328,646

Euro

Sell

6/17/15

16,108,021

16,820,017

711,996

Japanese Yen

Sell

5/20/15

2,619,386

2,663,934

44,548

Mexican Peso

Buy

4/15/15

31,392,085

31,123,852

268,233

New Zealand Dollar

Sell

4/15/15

23,462,651

23,903,490

440,839

Norwegian Krone

Buy

6/17/15

4,377,912

3,297,497

1,080,415

Philippine Peso

Buy

5/20/15

15,027,887

15,266,238

(238,351)

Swiss Franc

Sell

6/17/15

34,783,102

35,392,662

609,560

58 Diversified Income Trust

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $2,504,201,645) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

Credit Suisse International

Australian Dollar

Sell

4/15/15

$15,663,132

$16,446,721

$783,589

British Pound

Buy

6/17/15

4,966,959

6,161,348

(1,194,389)

Canadian Dollar

Sell

4/15/15

58,700,284

59,926,004

1,225,720

Euro

Sell

6/17/15

6,024,632

6,133,881

109,249

Indian Rupee

Buy

5/20/15

65,674,498

66,041,783

(367,285)

Japanese Yen

Sell

5/20/15

5,619,441

5,734,114

114,673

New Zealand Dollar

Buy

4/15/15

24,891,598

25,372,263

(480,665)

Norwegian Krone

Sell

6/17/15

2,465,819

2,576,500

110,681

Swedish Krona

Sell

6/17/15

14,545,399

14,994,903

449,504

Swiss Franc

Sell

6/17/15

3,401,615

3,459,937

58,322

Deutsche Bank AG

Australian Dollar

Buy

4/15/15

5,572,959

5,439,407

133,552

British Pound

Buy

6/17/15

23,588,495

24,455,860

(867,365)

Canadian Dollar

Sell

4/15/15

54,867,221

56,622,819

1,755,598

Euro

Sell

6/17/15

7,855,206

9,572,870

1,717,664

New Zealand Dollar

Buy

4/15/15

31,662,038

31,154,853

507,185

Norwegian Krone

Sell

6/17/15

11,660,060

12,184,226

524,166

Polish Zloty

Sell

6/17/15

16,896,714

17,105,853

209,139

Swedish Krona

Sell

6/17/15

1,616

1,666

50

Swiss Franc

Sell

6/17/15

2,772,058

2,818,683

46,625

Turkish Lira

Sell

6/17/15

1,137,803

637,741

(500,062)

Goldman Sachs International

Australian Dollar

Buy

4/15/15

14,287,815

14,484,772

(196,957)

British Pound

Buy

6/17/15

15,185,689

15,744,617

(558,928)

Canadian Dollar

Sell

4/15/15

41,597,350

43,175,186

1,577,836

Euro

Sell

6/17/15

25,460,990

26,588,953

1,127,963

New Zealand Dollar

Buy

4/15/15

31,870,580

32,560,338

(689,758)

Norwegian Krone

Sell

6/17/15

13,467,312

14,092,177

624,865

Swedish Krona

Sell

6/17/15

3,961,743

4,084,768

123,025

HSBC Bank USA, National Association

Australian Dollar

Sell

4/15/15

491,495

1,181,560

690,065

British Pound

Buy

6/17/15

7,225,894

7,492,095

(266,201)

Canadian Dollar

Sell

4/15/15

49,262,370

51,371,056

2,108,686

Chinese Yuan (Onshore)

Buy

5/20/15

31,367,416

31,487,101

(119,685)

Euro

Sell

6/17/15

13,997,484

16,455,693

2,458,209

New Taiwan Dollar

Sell

5/20/15

31,283,645

30,965,387

(318,258)

New Zealand Dollar

Buy

4/15/15

15,621,284

15,949,553

(328,269)

Swedish Krona

Buy

6/17/15

1,425,849

1,470,631

(44,782)

JPMorgan Chase Bank N.A.

Australian Dollar

Buy

4/15/15

14,654,723

14,954,394

(299,671)

British Pound

Buy

6/17/15

12,125,689

12,487,024

(361,335)

Canadian Dollar

Sell

4/15/15

45,697,791

47,443,372

1,745,581

Diversified Income Trust 59

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $2,504,201,645) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

JPMorgan Chase Bank N.A. cont.

Euro

Sell

6/17/15

$26,449,739

$28,647,969

$2,198,230

Indian Rupee

Buy

5/20/15

30,849,789

31,034,425

(184,636)

Japanese Yen

Sell

5/20/15

27,601,810

28,158,193

556,383

Malaysian Ringgit

Sell

5/20/15

195,936

488,499

292,563

Mexican Peso

Buy

4/15/15

29,907,166

30,153,681

(246,515)

New Zealand Dollar

Sell

4/15/15

17,972,351

17,805,669

(166,682)

Norwegian Krone

Buy

6/17/15

2,024,453

2,110,359

(85,906)

Philippine Peso

Buy

5/20/15

15,027,885

15,269,696

(241,811)

Singapore Dollar

Sell

5/20/15

32,158,053

32,752,496

594,443

South Korean Won

Sell

5/20/15

30,799,557

30,706,687

(92,870)

Swedish Krona

Buy

6/17/15

3,682,488

4,464,171

(781,683)

Swiss Franc

Buy

6/17/15

3,652,654

3,363,289

289,365

Royal Bank of Scotland PLC (The)

Australian Dollar

Buy

4/15/15

23,340,126

24,355,319

(1,015,193)

British Pound

Buy

6/17/15

7,400,696

8,394,830

(994,134)

Canadian Dollar

Sell

4/15/15

44,777,320

47,017,726

2,240,406

Euro

Sell

6/17/15

18,838,868

21,399,637

2,560,769

New Zealand Dollar

Sell

4/15/15

14,289,253

13,348,885

(940,368)

Norwegian Krone

Buy

6/17/15

7,249,006

6,297,797

951,209

Singapore Dollar

Sell

5/20/15

62,278,356

63,430,046

1,151,690

Swedish Krona

Buy

6/17/15

501,591

930,988

(429,397)

State Street Bank and Trust Co.

Australian Dollar

Sell

4/15/15

6,472,232

7,147,505

675,273

British Pound

Buy

6/17/15

2,025,718

3,030,265

(1,004,547)

Canadian Dollar

Sell

4/15/15

48,228,695

49,545,298

1,316,603

Chilean Peso

Buy

4/15/15

37,879

473,163

(435,284)

Euro

Sell

6/17/15

25,293,400

27,063,104

1,769,704

Hungarian Forint

Buy

6/17/15

29,273,268

29,974,955

(701,687)

Israeli Shekel

Buy

4/15/15

63,290,657

64,698,710

(1,408,053)

Israeli Shekel

Sell

4/15/15

63,290,657

63,145,330

(145,327)

Japanese Yen

Sell

5/20/15

15,131,093

15,439,825

308,732

Malaysian Ringgit

Sell

5/20/15

250,143

386,645

136,502

New Zealand Dollar

Buy

4/15/15

16,849,457

16,486,124

363,333

Norwegian Krone

Sell

6/17/15

6,555,637

6,848,357

292,720

Singapore Dollar

Sell

5/20/15

29,854,286

30,410,314

556,028

Swedish Krona

Sell

6/17/15

14,812,772

15,265,713

452,941

Swiss Franc

Buy

6/17/15

2,303,115

2,342,689

(39,574)

Turkish Lira

Sell

6/17/15

2,445,636

1,287,960

(1,157,676)

UBS AG

Australian Dollar

Sell

4/15/15

23,592,190

24,956,533

1,364,343

British Pound

Buy

6/17/15

23,946,402

24,851,384

(904,982)

Canadian Dollar

Sell

4/15/15

32,359,793

34,686,764

2,326,971

60 Diversified Income Trust

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $2,504,201,645) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

UBS AG cont.

Chilean Peso

Buy

4/15/15

$37,879

$482,234

$(444,355)

Euro

Sell

6/17/15

14,398,000

15,882,268

1,484,268

Japanese Yen

Sell

5/20/15

9,969,416

10,177,960

208,544

New Taiwan Dollar

Sell

5/20/15

31,283,649

30,834,036

(449,613)

New Zealand Dollar

Buy

4/15/15

45,399,289

45,592,183

(192,894)

Norwegian Krone

Buy

6/17/15

30,168,695

29,916,351

252,344

Norwegian Krone

Sell

6/17/15

29,767,892

30,765,153

997,261

Swedish Krona

Buy

6/17/15

272,338

1,283,322

(1,010,984)

WestPac Banking Corp.

Australian Dollar

Sell

4/15/15

10,422,452

10,987,246

564,794

Canadian Dollar

Buy

4/15/15

36,795,425

38,810,576

(2,015,151)

Canadian Dollar

Sell

4/15/15

36,352,398

38,944,282

2,591,884

Euro

Sell

6/17/15

22,668,898

24,006,326

1,337,428

New Zealand Dollar

Buy

4/15/15

28,315,309

28,910,712

(595,403)

South Korean Won

Buy

5/20/15

1,245,557

1,267,549

(21,992)

Total

$35,989,042

FUTURES CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Number of contracts

Value

Expiration date

Unrealized appreciation/ (depreciation)

Euro-Bobl 5 yr (Short)

2,195

$305,477,379

Jun-15

$(760,448)

Euro-Bund 10 yr (Long)

1,548

264,254,034

Jun-15

3,741,435

Euro-Buxl 30 yr (Short)

269

50,952,930

Jun-15

(3,431,050)

U.S. Treasury Bond 30 yr (Long)

143

23,434,125

Jun-15

124,803

U.S. Treasury Bond Ultra 30 yr (Long)

459

77,972,625

Jun-15

(341,845)

U.S. Treasury Note 2 yr (Short)

1,611

353,060,719

Jun-15

(733,611)

U.S. Treasury Note 5 yr (Short)

3,265

392,488,713

Jun-15

(1,806,817)

U.S. Treasury Note 10 yr (Short)

911

117,433,594

Jun-15

(858,893)

Total

$(4,066,426)

WRITTEN SWAP OPTIONS OUTSTANDING at 3/31/15 (premiums $98,151,719) (Unaudited)

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.916/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.916

$402,015,100

$402

(1.9125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.9125

412,098,000

605,784

2.955/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.955

804,030,200

2,106,559

(2.04375)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.04375

412,098,000

2,274,781

1.66/3 month USD-LIBOR-BBA/Jul-20

Jul-15/1.66

412,098,000

3,568,769

Diversified Income Trust 61

WRITTEN SWAP OPTIONS OUTSTANDING at 3/31/15 (premiums $98,151,719) (Unaudited) cont.

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Barclays Bank PLC

2.3775/3 month USD-LIBOR-BBA/May-25

May-15/2.3775

$402,015,100

$1,202,025

2.265/3 month USD-LIBOR-BBA/May-25

May-15/2.265

402,015,100

2,110,579

Citibank, N.A.

2.902/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.902

402,015,100

2,010

(1.602)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.602

402,015,100

60,302

2.28/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.28

402,015,100

426,136

(1.932)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.932

206,049,000

432,703

2.205/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.205

402,015,100

864,332