| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-05635) |

| | |

| Exact name of registrant as specified in charter: | Putnam Diversified Income Trust |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Robert T. Burns, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | Bryan Chegwidden, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, New York 10036 |

| | |

| Registrant's telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | September 30, 2017 |

| | |

| Date of reporting period: | October 1, 2016 — March 31, 2017 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

Diversified Income

Trust

Semiannual report

3 | 31 | 17

Consider these risks before investing: International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value when interest rates decline and decline in value when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. Bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, changing market perceptions including perceptions about the risk of default and expectations about monetary policy or interest rates, changes in government intervention in the financial markets, and factors related to a specific issuer or industry. These and other factors may lead to increased volatility and reduced liquidity in the fund’s portfolio. You can lose money by investing in the fund.

Message from the Trustees

May 11, 2017

Dear Fellow Shareholder:

The early months of 2017 have been generally positive for investor sentiment and financial market performance. Many market indexes have achieved new record highs with relatively low volatility, in contrast to the bouts of uncertainty and turbulence that tested global financial markets in 2016. It is worth noting, however, that the exuberance that greeted the new year calmed somewhat as investors reconsidered a number of ongoing macroeconomic and political risks. In addition, many bond investors remained cautious as the potential for inflation increased.

As always, we believe investors should continue to focus on time-tested strategies: maintain a well-diversified portfolio, keep a long-term view, and do not overreact to short-term market fluctuations. To help ensure that your portfolio is aligned with your goals, we also believe it is a good idea to speak regularly with your financial advisor. In the following pages, you will find an overview of your fund’s performance for the reporting period as well as an outlook for the coming months.

We would like to take this opportunity to announce the arrival of Catharine Bond Hill and Manoj P. Singh to your fund’s Board of Trustees. Dr. Hill and Mr. Singh bring extensive professional and directorship experience to their role as Trustees, and we are pleased to welcome them.

Thank you for investing with Putnam.

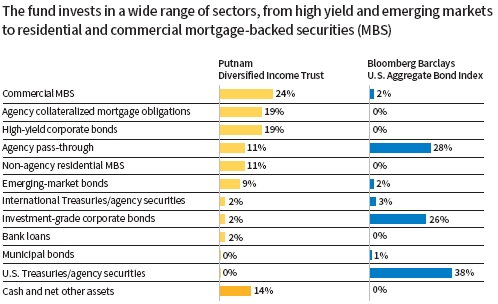

The opportunities in today’s fixed-income markets are far from uniform. That’s why Putnam Diversified Income Trust’s managers actively position the portfolio in securities from a broad range of sectors that the team believes offer the most compelling risk/return profiles — including areas beyond those in the benchmark index.

|

| 2 Diversified Income Trust |

Allocations are shown as a percentage of the fund’s and/or benchmark’s net assets as of 3/31/17. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the use of different classifications of securities for presentation purposes and rounding. Allocations may not total 100% because the table includes the notional value of certain derivatives (the economic value for purposes of calculating periodic payment obligations), in addition to the market value of securities. Holdings and allocations may vary over time. For more information on current fund holdings, see pages 19–70.

|

| Diversified Income Trust 3 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See below and pages 11–12 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

* Returns for the six-month period are not annualized, but cumulative.

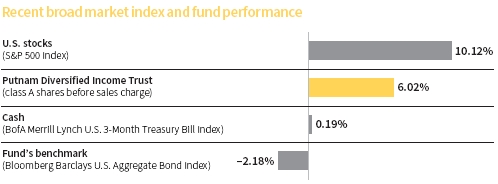

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/17. See above and pages 11–12 for additional fund performance information. Index descriptions can be found on page 16.

|

| 4 Diversified Income Trust |

Bill Kohli is Chief Investment Officer, Fixed Income, at Putnam. He has an M.B.A. from the Haas School of Business, University of California, Berkeley, and a B.A. from the University of California, San Diego. Bill joined Putnam in 1994 and has been in the investment industry since 1988.

In addition to Bill, your fund’s portfolio managers are Michael J. Atkin; Robert L. Davis, CFA; Brett S. Kozlowski, CFA; Michael V. Salm; and Paul D. Scanlon, CFA.

Bill, what was the fund’s investment environment like during the six-month reporting period ended March 31, 2017?

The environment was generally supportive for riskier assets, but with interest rates rising, it was challenging for U.S. Treasuries and other rate-sensitive categories.

In the months immediately after the U.S. presidential election, investors were optimistic about the potential for tax cuts and increases in infrastructure and defense spending under the incoming Trump administration. Later in the period, however, the administration delayed a vote on a bill that could have repealed and replaced the Affordable Care Act. This delay triggered uncertainty about the administration’s ability to get its tax-reform and fiscal-stimulus plans passed by Congress.

Economic data in both the United States and globally were positive overall. In particular, fourth-quarter U.S. gross domestic product [GDP] was revised upward from a 1.9% to a 2.1% annual rate, according to the Commerce Department. This follows growth of 3.5% in the third quarter. In February, the Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures Price Index, rose

|

| Diversified Income Trust 5 |

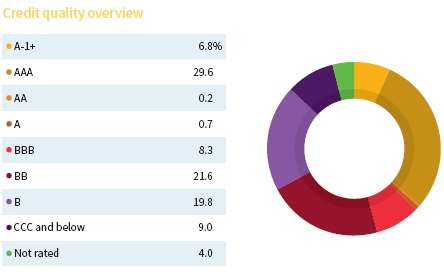

Credit qualities are shown as a percentage of the fund’s net assets as of 3/31/17. A bond rated BBB or higher (A-3 or higher, for short-term debt) is considered investment grade. This chart reflects the highest security rating provided by one or more of Standard & Poor’s, Moody’s, and Fitch. To-be-announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings may vary over time.

Cash, derivative instruments, and net other assets are shown in the not-rated category. Payables and receivables for TBA mortgage commitments are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

2.1% from a year earlier, the first time inflation exceeded the central bank’s target in nearly five years. The jobless rate in the 19-country eurozone declined to 9.5% in February, the lowest level since 2009.

The Fed increased its target for short-term interest rates by a quarter percentage point twice during the period, raising the federal funds rate to a range of 0.75% to 1%. At the central bank’s mid-March policy meeting, Fed Chair Janet Yellen expressed confidence in the economy and reaffirmed that the board may implement two more increases this year.

After reaching a 14-year high in early January, the U.S. dollar declined by 3.5% in the first quarter of 2017, reflecting increased investor caution toward the currency amid uncertainties surrounding the Trump administration’s policy platform.

The fund topped its benchmark by a sizable margin during the six-month period, and also outpaced its Lipper peer group average. What factors bolstered its relative performance?

With respect to relative performance, I think it’s important to point out that the fund’s benchmark comprises a mix of U.S. Treasury, government-agency, and investment-grade corporate securities. Treasuries and other government securities were hampered by rising interest rates during the period. Meanwhile, the fund’s interest-rate and yield-curve strategies, along with out-of-benchmark credit holdings, performed well and fueled its strong performance. In fact, all of the fund’s major strategy segments contributed to results — there were no detractors on an absolute basis.

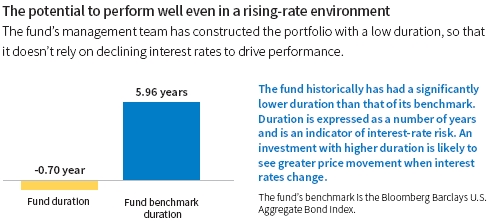

Looking at individual strategies, our interest-rate and yield-curve positioning in the United States and overseas was the biggest contributor to performance. We continued our efforts to de-emphasize interest-rate risk by keeping the

|

| 6 Diversified Income Trust |

portfolio’s duration — a key measure of interest-rate sensitivity — close to or below zero. This strategy was particularly helpful in November when intermediate- and long-term Treasury yields rose sharply in response to the U.S. presidential election outcome and President-elect Trump’s proposed fiscal policy.

Internationally, interest rates also rose in Europe, particularly in the United Kingdom, so our duration positioning aided performance there. Our holdings of Greek government debt provided a further boost. The country’s bonds rallied on increased investor optimism that the securities might be included in the European Central Bank’s bond purchase program.

An out-of-benchmark stake in high-yield bonds was another leading contributor, despite modest spread widening in March [bond prices decline as yield spreads widen]. After a strong 2016, the sector continued to post positive returns in the early months of 2017, as the search for yield continued. Optimistic sentiment toward the asset class was fueled by investor expectations that economic growth could potentially accelerate if the Trump administration is successful at implementing tax cuts and more-robust fiscal policy. Relatively stable global oil prices during most of the period also provided a tailwind.

How did the fund’s mortgage credit holdings influence performance?

Mortgage credit was another bright spot. In January, our positions in mezzanine commercial mortgage-backed securities [CMBS] that were issued before the 2008 financial crisis performed particularly well. However, gains

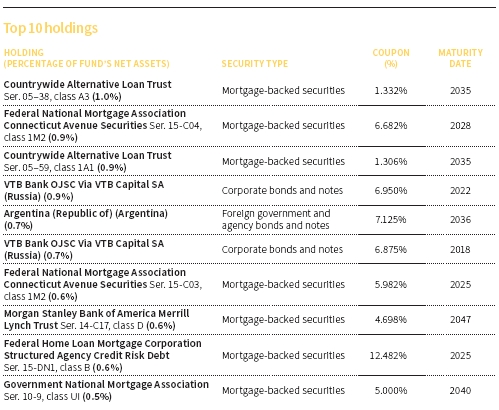

This table shows the fund’s top 10 individual holdings and the percentage of the fund’s net assets that each represented as of 3/31/17. Short-term investments, TBA commitments, and derivatives, if any, are excluded. Holdings may vary over time.

|

| Diversified Income Trust 7 |

from the sector were pared in February when headlines concerning retail store closures prompted some investors to express a bearish view on certain parts of the CMBS market due to the sector’s exposure to retail properties. Although we agree that retailers face challenges amid evolving shopper preferences and a shift from traditional brick-and-mortar to online commerce, we believe the CMBS held by the fund have enough credit protection to withstand the changes that are occurring in retail.

Within non-agency residential mortgage-backed securities [RMBS], our investments in agency credit risk-transfer securities [CRTS] aided results, as did pay-option adjustable-rate mortgage-backed securities [pay-option ARMS]. With CRTS, a combination of relatively high yields and high-quality collateral continued to attract investors to what we believe is a growing market. Furthermore, CRTS provided investors with a productive alternative to deploy their capital as other parts of the non-agency RMBS market continued to shrink. Pay-option ARMS benefited from the generally favorable risk environment during the period, as well as the fact that there was no new supply of these bonds coming to market.

What about the fund’s holdings of emerging-market debt?

They also contributed. Positions in Russia, Venezuela, Brazil, and Mexico were the most productive, partly helped by stable oil prices and persistent investor demand for high-yielding securities. Brazil’s bonds also received a boost when the country’s central bank cut its benchmark interest rate by more than investors were expecting, as Brazil continues its efforts to recover from a deep recession.

Elsewhere, our active-currency and prepayment strategies were modest contributors for the period.

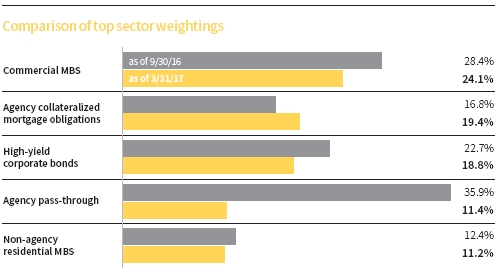

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the use of different classifications of securities for presentation purposes, and rounding. Holdings and allocations may vary over time.

|

| 8 Diversified Income Trust |

How did you use derivatives during the period?

We used bond futures and interest-rate swaps to take tactical positions at various points along the yield curve, and to hedge the risk associated with the fund’s curve positioning. We employed interest-rate swaps to gain exposure to rates in various countries. We also utilized options to hedge the fund’s interest-rate risk, to isolate the prepayment risk associated with our CMO holdings, and to help manage overall downside risk. In addition, we used total return swaps as a hedging tool, and to help manage the portfolio’s sector exposure, as well as its inflation risk. Lastly, we used currency forward contracts to hedge the foreign exchange risk associated with non-U.S. bonds and to efficiently gain exposure to foreign currencies.

What is your outlook for the coming months?

As we look at the world today, we see economic activity picking up and inflation levels beginning to rise. Higher commodity prices appear to be leading to fairly persistent pricing pressures in the United States and elsewhere. In our view, global economies appear to be normalizing, and we think this is particularly true in the United States. Given this apparent normalization, we think the level of interest rates remains too low.

Within this environment, we think the Fed’s tone has changed somewhat. For some time now, the central bank has emphasized that its policy was data-dependent — particularly data related to employment and inflation levels. After years of employing stimulative monetary policy in an effort to ward off deflation, we believe the Fed has now shifted its focus to inflation. This new phase of monetary policy

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

|

| Diversified Income Trust 9 |

is driven, in our view, by a central bank that is becoming more concerned with the possibility that the economy could outperform forecasts. Consequently, we expect the Fed to increase rates at least twice more this year, and we believe these increases could occur sooner than the market is currently forecasting.

We also believe the Fed could soon begin the process of reducing its holdings of U.S. Treasuries and mortgage-backed securities. In our view, the central bank may want to move toward a smaller portfolio for several reasons. For one, the economy appears to be on stronger footing, which may lead the Fed to see less need for support from a large bond portfolio. Additionally, the Fed’s reduction of its bond portfolio could relieve pressure on possible new leadership in 2018, in our view, when Janet Yellen’s term ends. Finally, we believe Fed officials may want room to ramp the portfolio back up in a crisis if needed.

How do you plan to position the fund in light of this outlook?

Despite positive duration positioning in the United States, our non-U.S., quantitatively driven, negative-duration strategies have kept the fund’s total duration close to zero. We plan to keep these strategies in place for now. We also extended our strategy of seeking to capitalize on potentially steeper global yield curves. We think this overall positioning could benefit the fund if interest rates continue to trend higher in the months ahead.

We plan to continue seeking opportunities in corporate and mortgage credit that we believe offer relative value. Within those market areas, we continue to have a constructive outlook for high-yield bonds, based on what we think is a generally supportive fundamental and technical backdrop for the asset class. We also continue to like CMBS due to what we believe are attractive spreads available there.

We plan to maintain the fund’s exposure to select emerging-market countries, seeking to benefit from the relatively high income levels available in markets in which we believe we’re being adequately compensated for risk.

Lastly, we will seek to maintain a sufficient cash allocation to provide a cushion against bouts of market volatility, as well as any disruptions in the global market’s supply/demand environment.

Thanks for your time and for bringing us up to date, Bill.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk. Statements in the Q&A concerning the fund’s performance or portfolio composition relative to those of the fund’s Lipper peer group may reference information produced by Lipper Inc. or through a third party.

|

| 10 Diversified Income Trust |

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2017, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

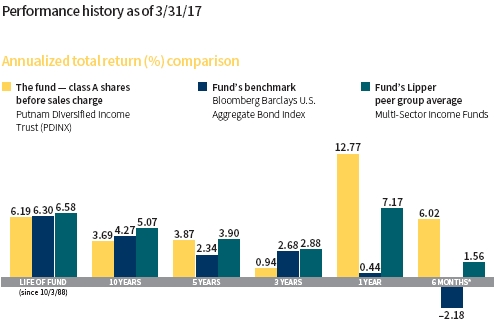

Fund performance Total return for periods ended 3/31/17

| | | | | | | | | |

| | Annual | | | | | | | | |

| | average | | Annual | | Annual | | Annual | | |

| | (life of fund) | 10 years | average | 5 years | average | 3 years | average | 1 year | 6 months |

|

| Class A (10/3/88) | | | | | | | | | |

| Before sales charge | 6.19% | 43.70% | 3.69% | 20.90% | 3.87% | 2.85% | 0.94% | 12.77% | 6.02% |

|

| After sales charge | 6.04 | 37.95 | 3.27 | 16.07 | 3.02 | –1.26 | –0.42 | 8.25 | 1.78 |

|

| Class B (3/1/93) | | | | | | | | | |

| Before CDSC | 5.95 | 35.54 | 3.09 | 16.57 | 3.11 | 0.58 | 0.19 | 11.89 | 5.68 |

|

| After CDSC | 5.95 | 35.54 | 3.09 | 14.72 | 2.78 | –2.07 | –0.69 | 6.89 | 0.68 |

|

| Class C (2/1/99) | | | | | | | | | |

| Before CDSC | 5.38 | 32.98 | 2.89 | 16.56 | 3.11 | 0.60 | 0.20 | 11.98 | 5.57 |

|

| After CDSC | 5.38 | 32.98 | 2.89 | 16.56 | 3.11 | 0.60 | 0.20 | 10.98 | 4.57 |

|

| Class M (12/1/94) | | | | | | | | | |

| Before sales charge | 5.90 | 40.39 | 3.45 | 19.58 | 3.64 | 2.21 | 0.73 | 12.61 | 5.86 |

|

| After sales charge | 5.78 | 35.82 | 3.11 | 15.69 | 2.96 | –1.11 | –0.37 | 8.95 | 2.42 |

|

| Class R (12/1/03) | | | | | | | | | |

| Net asset value | 5.91 | 39.57 | 3.39 | 19.57 | 3.64 | 2.13 | 0.71 | 12.50 | 5.97 |

|

| Class R6 (11/1/13) | | | | | | | | | |

| Net asset value | 6.38 | 47.25 | 3.95 | 22.92 | 4.21 | 4.06 | 1.34 | 13.28 | 6.25 |

|

| Class Y (7/1/96) | | | | | | | | | |

| Net asset value | 6.37 | 46.74 | 3.91 | 22.50 | 4.14 | 3.71 | 1.22 | 13.17 | 6.06 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance reflects conversion to class A shares after eight years.

|

| Diversified Income Trust 11 |

Comparative index returns For periods ended 3/31/17

| | | | | | | | | |

| | Annual | | | | | | | | |

| | average | | Annual | | Annual | | Annual | | |

| | (life of fund) | 10 years | average | 5 years | average | 3 years | average | 1 year | 6 months |

|

| Bloomberg Barclays | | | | | | | | | |

| U.S. Aggregate Bond | 6.30% | 51.97% | 4.27% | 12.25% | 2.34% | 8.27% | 2.68% | 0.44% | –2.18% |

| Index | | | | | | | | | |

|

| Lipper Multi-Sector | | | | | | | | | |

| Income Funds | 6.58 | 65.82 | 5.07 | 21.30 | 3.90 | 8.93 | 2.88 | 7.17 | 1.56 |

| category average* | | | | | | | | | |

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/17, there were 339, 326, 242, 184, 100, and 6 funds, respectively, in this Lipper category.

Fund price and distribution information For the six-month period ended 3/31/17

| | | | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | ClassR6 | Class Y |

|

| Number | 6 | 6 | 6 | 6 | 6 | 6 | 6 |

|

| Income | $0.198 | $0.172 | $0.172 | $0.191 | $0.190 | $0.210 | $0.207 |

|

| Capital gains | — | — | — | — | — | — | — |

|

| Total | $0.198 | $0.172 | $0.172 | $0.191 | $0.190 | $0.210 | $0.207 |

|

| | Before | After | Net | Net | Before | After | Net | Net | Net |

| | sales | sales | asset | asset | sales | sales | asset | asset | asset |

| Share value | charge | charge | value | value | charge | charge | value | value | value |

|

| 9/30/16 | $6.86 | $7.15 | $6.79 | $6.75 | $6.75 | $6.98 | $6.78 | $6.80 | $6.80 |

|

| 3/31/17 | 7.07 | 7.36 | 7.00 | 6.95 | 6.95 | 7.18 | 6.99 | 7.01 | 7.00 |

|

| | Before | After | Net | Net | Before | After | Net | Net | Net |

| Current rate | sales | sales | asset | asset | sales | sales | asset | asset | asset |

| (end of period) | charge | charge | value | value | charge | charge | value | value | value |

|

| Current dividend rate1 | 5.60% | 5.38% | 4.97% | 5.01% | 5.53% | 5.35% | 5.49% | 5.99% | 6.00% |

|

| Current 30-day SEC yield2 | N/A | 4.18 | 3.60 | 3.60 | N/A | 3.97 | 4.10 | 4.70 | 4.61 |

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

|

| 12 Diversified Income Trust |

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R6 | Class Y |

|

| Total annual operating expenses for the | | | | | | | |

| fiscal year ended 9/30/16 | 1.00% | 1.75% | 1.75% | 1.25% | 1.25% | 0.65% | 0.75% |

|

| Annualized expense ratio for the | | | | | | | |

| six-month period ended 3/31/17 | 0.99% | 1.74% | 1.74% | 1.24% | 1.24% | 0.64% | 0.74% |

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in each class of the fund from 10/1/16 to 3/31/17. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R6 | Class Y |

|

| Expenses paid per $1,000*† | $5.09 | $8.92 | $8.92 | $6.36 | $6.37 | $3.29 | $3.80 |

|

| Ending value (after expenses) | $1,060.20 | $1,056.80 | $1,055.70 | $1,058.60 | $1,059.70 | $1,062.50 | $1,060.60 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/17. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

|

| Diversified Income Trust 13 |

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended 3/31/17, use the following calculation method. To find the value of your investment on 10/1/16, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R6 | Class Y |

|

| Expenses paid per $1,000*† | $4.99 | $8.75 | $8.75 | $6.24 | $6.24 | $3.23 | $3.73 |

|

| Ending value (after expenses) | $1,020.00 | $1,016.26 | $1,016.26 | $1,018.75 | $1,018.75 | $1,021.74 | $1,021.24 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/17. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

|

| 14 Diversified Income Trust |

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are closed to new investments and are only available by exchange from another Putnam fund. They are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC.

Class R shares are not subject to an initial sales charge or CDSC and are only available to employer-sponsored retirement plans.

Class R6 shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

• Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

• Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties,

|

| Diversified Income Trust 15 |

refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

• Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

• Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

• Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

|

| 16 Diversified Income Trust |

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2016, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2017, Putnam employees had approximately $486,000,000 and the Trustees had approximately $137,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

|

| Diversified Income Trust 17 |

Financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

|

| 18 Diversified Income Trust |

The fund’s portfolio 3/31/17 (Unaudited)

| | |

| U.S. GOVERNMENT AND AGENCY | Principal | |

| MORTGAGE OBLIGATIONS (78.2%)* | amount | Value |

|

| U.S. Government Guaranteed Mortgage Obligations (—%) | | |

|

| Government National Mortgage Association Pass-Through Certificates | | |

| 6.50%, 11/20/38 | $285,430 | $325,964 |

|

| | | 325,964 |

|

| U.S. Government Agency Mortgage Obligations (78.2%) | | |

|

| Federal Home Loan Mortgage Corporation Pass-Through Certificates | | |

| 4.00%, TBA, 4/1/47 | 44,000,000 | 46,155,314 |

|

| Federal National Mortgage Association Pass-Through Certificates | | |

|

| 5.50%, TBA, 4/1/47 | 23,000,000 | 25,551,563 |

|

| 4.50%, TBA, 4/1/47 | 32,000,000 | 34,317,501 |

|

| 4.00%, TBA, 4/1/47 | 27,000,000 | 28,322,579 |

|

| 3.50%, TBA, 5/1/47 | 790,000,000 | 806,509,736 |

|

| 3.50%, TBA, 4/1/47 | 962,000,000 | 984,095,986 |

|

| 3.00%, TBA, 4/1/47 | 637,000,000 | 631,625,313 |

|

| 2.50%, TBA, 4/1/47 | 91,000,000 | 86,762,813 |

|

| | | 2,643,340,805 |

|

| Total U.S. government and agency mortgage obligations (cost $2,637,911,799) | $2,643,666,769 |

|

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* | amount | Value |

|

| Agency collateralized mortgage obligations (17.8%) | | |

|

| Federal Home Loan Mortgage Corporation | | |

|

| IFB Ser. 3408, Class EK, 22.122%, 4/15/37 | $267,277 | $408,517 |

|

| IFB Ser. 2979, Class AS, 20.929%, 3/15/34 | 2,904 | 2,916 |

|

| IFB Ser. 4104, Class S, IO, 5.188%, 9/15/42 | 10,534,319 | 2,083,015 |

|

| IFB Ser. 326, Class S2, IO, 5.038%, 3/15/44 | 17,788,455 | 3,612,216 |

|

| IFB Ser. 311, Class S1, IO, 5.038%, 8/15/43 | 16,035,023 | 3,231,009 |

|

| Ser. 4077, Class IK, IO, 5.00%, 7/15/42 | 18,773,442 | 3,906,340 |

|

| Ser. 3687, Class CI, IO, 5.00%, 11/15/38 | 8,443,344 | 916,804 |

|

| Ser. 4122, Class TI, IO, 4.50%, 10/15/42 | 11,353,256 | 2,408,026 |

|

| Ser. 4000, Class PI, IO, 4.50%, 1/15/42 | 15,282,363 | 2,845,576 |

|

| Ser. 4024, Class PI, IO, 4.50%, 12/15/41 | 19,839,948 | 3,701,023 |

|

| Ser. 4635, Class PI, IO, 4.00%, 12/15/46 | 38,962,760 | 6,987,581 |

|

| Ser. 4462, IO, 4.00%, 4/15/45 | 19,114,364 | 3,846,766 |

|

| Ser. 4193, Class PI, IO, 4.00%, 3/15/43 | 52,483,471 | 8,467,368 |

|

| Ser. 4213, Class GI, IO, 4.00%, 11/15/41 | 28,797,511 | 4,218,835 |

|

| Ser. 4020, Class IA, IO, 4.00%, 3/15/27 | 16,916,435 | 1,883,983 |

|

| Ser. 4484, Class TI, IO, 3.50%, 11/15/44 | 20,556,095 | 3,560,316 |

|

| Ser. 4122, Class CI, IO, 3.50%, 10/15/42 | 19,259,429 | 2,554,879 |

|

| Ser. 4105, Class HI, IO, 3.50%, 7/15/41 | 9,115,966 | 1,070,444 |

|

| Ser. 4199, Class CI, IO, 3.50%, 12/15/37 | 47,276,452 | 4,004,315 |

|

| Ser. 4165, Class TI, IO, 3.00%, 12/15/42 | 24,127,462 | 2,504,431 |

|

| Ser. 4210, Class PI, IO, 3.00%, 12/15/41 | 17,726,716 | 1,312,885 |

|

| FRB Ser. 57, Class 1AX, IO, 0.372%, 7/25/43 | 12,187,512 | 133,514 |

|

| Ser. 3314, PO, zero %, 11/15/36 | 43,262 | 42,255 |

|

| Ser. 3326, Class WF, zero %, 10/15/35 | 35,784 | 26,937 |

|

| Ser. 1208, Class F, PO, zero %, 2/15/22 | 18,116 | 16,455 |

|

|

| Diversified Income Trust 19 |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Agency collateralized mortgage obligations cont. | | |

|

| Federal National Mortgage Association | | |

|

| IFB Ser. 06-8, Class HP, 20.967%, 3/25/36 | $764,503 | $1,203,259 |

|

| IFB Ser. 05-83, Class QP, 14.842%, 11/25/34 | 218,238 | 269,270 |

|

| Ser. 16-3, Class NI, IO, 6.00%, 2/25/46 | 25,840,756 | 6,215,575 |

|

| Ser. 399, Class 2, IO, 5.50%, 11/25/39 | 49,163 | 11,021 |

|

| Ser. 374, Class 6, IO, 5.50%, 8/25/36 | 1,859,439 | 359,438 |

|

| IFB Ser. 12-36, Class SN, IO, 5.468%, 4/25/42 | 11,622,551 | 2,153,659 |

|

| IFB Ser. 13-18, Class SB, IO, 5.168%, 10/25/41 | 17,820,491 | 2,313,100 |

|

| Ser. 378, Class 19, IO, 5.00%, 6/25/35 | 2,105,967 | 384,339 |

|

| IFB Ser. 13-103, Class SK, IO, 4.938%, 10/25/43 | 20,047,728 | 4,289,769 |

|

| IFB Ser. 11-101, Class SA, IO, 4.918%, 10/25/41 | 44,117,321 | 6,783,038 |

|

| Ser. 12-127, Class BI, IO, 4.50%, 11/25/42 | 12,853,049 | 3,062,603 |

|

| Ser. 12-30, Class HI, IO, 4.50%, 12/25/40 | 16,390,808 | 2,068,356 |

|

| Ser. 404, Class 2, IO, 4.50%, 5/25/40 | 169,546 | 36,778 |

|

| Ser. 366, Class 22, IO, 4.50%, 10/25/35 | 906,295 | 38,418 |

|

| Ser. 15-88, Class QI, IO, 4.00%, 10/25/44 | 16,496,554 | 2,574,896 |

|

| Ser. 13-41, Class IP, IO, 4.00%, 5/25/43 | 28,900,468 | 4,883,601 |

|

| Ser. 13-115, Class CI, IO, 4.00%, 2/25/43 | 23,878,651 | 3,358,222 |

|

| Ser. 13-44, Class PI, IO, 4.00%, 1/25/43 | 10,788,434 | 1,691,593 |

|

| Ser. 13-60, Class IP, IO, 4.00%, 10/25/42 | 12,549,702 | 2,175,152 |

|

| Ser. 12-96, Class PI, IO, 4.00%, 7/25/41 | 4,140,037 | 648,287 |

|

| Ser. 405, Class 2, IO, 4.00%, 10/25/40 | 188,296 | 39,918 |

|

| Ser. 16-70, Class QI, IO, 3.50%, 10/25/46 | 58,990,495 | 9,551,151 |

|

| Ser. 13-18, Class IN, IO, 3.50%, 3/25/43 | 40,534,684 | 5,933,386 |

|

| Ser. 13-70, Class CI, IO, 3.50%, 1/25/43 | 11,260,732 | 1,343,405 |

|

| Ser. 13-49, Class IP, IO, 3.50%, 12/25/42 | 29,387,388 | 3,388,366 |

|

| Ser. 13-40, Class YI, IO, 3.50%, 6/25/42 | 27,451,213 | 3,797,060 |

|

| Ser. 12-123, Class DI, IO, 3.50%, 5/25/41 | 38,227,571 | 6,082,007 |

|

| Ser. 12-151, Class PI, IO, 3.00%, 1/25/43 | 52,714,739 | 6,088,552 |

|

| Ser. 12-145, Class TI, IO, 3.00%, 11/25/42 | 19,108,162 | 1,484,704 |

|

| Ser. 13-35, Class IP, IO, 3.00%, 6/25/42 | 13,347,422 | 1,134,531 |

|

| Ser. 13-35, Class PI, IO, 3.00%, 2/25/42 | 40,039,545 | 3,459,417 |

|

| Ser. 13-53, Class JI, IO, 3.00%, 12/25/41 | 25,651,852 | 2,780,661 |

|

| Ser. 13-30, Class IP, IO, 3.00%, 10/25/41 | 22,054,083 | 1,576,205 |

|

| FRB Ser. 01-50, Class B1, IO, 0.402%, 10/25/41 | 239,032 | 2,839 |

|

| FRB Ser. 02-W8, Class 1, IO, 0.302%, 6/25/42 | 8,833,473 | 104,897 |

|

| Ser. 99-51, Class N, PO, zero %, 9/17/29 | 62,189 | 52,861 |

|

| Federal National Mortgage Association Grantor Trust | | |

|

| Ser. 98-T2, Class A4, IO, 6.50%, 10/25/36 | 33,205 | 4,551 |

|

| Ser. 00-T6, IO, 0.716%, 3/30/30 | 5,812,854 | 123,523 |

|

| Government National Mortgage Association | | |

|

| IFB Ser. 13-129, Class SN, IO, 5.172%, 9/20/43 | 13,096,735 | 2,068,367 |

|

| IFB Ser. 13-99, Class VS, IO, 5.172%, 7/16/43 | 15,620,072 | 2,518,112 |

|

| IFB Ser. 10-20, Class SC, IO, 5.172%, 2/20/40 | 10,339,891 | 1,790,869 |

|

| IFB Ser. 16-77, Class SC, IO, 5.122%, 10/20/45 | 37,136,556 | 6,999,056 |

|

| IFB Ser. 14-60, Class SE, IO, 5.122%, 4/20/44 | 23,081,245 | 3,667,610 |

|

| IFB Ser. 13-182, Class SY, IO, 5.122%, 12/20/43 | 14,766,675 | 2,926,755 |

|

| Ser. 16-126, Class PI, IO, 5.00%, 2/20/46 | 29,580,395 | 6,366,589 |

|

| Ser. 14-132, IO, 5.00%, 9/20/44 | 20,126,040 | 4,119,549 |

|

|

| 20 Diversified Income Trust |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Agency collateralized mortgage obligations cont. | | |

|

| Government National Mortgage Association | | |

|

| Ser. 14-163, Class NI, IO, 5.00%, 2/20/44 | $20,931,872 | $4,050,359 |

|

| Ser. 14-4, Class PI, IO, 5.00%, 12/16/43 | 12,866,692 | 2,485,330 |

|

| Ser. 14-25, Class MI, IO, 5.00%, 11/20/43 | 14,629,696 | 2,725,951 |

|

| Ser. 13-3, Class IT, IO, 5.00%, 1/20/43 | 7,656,213 | 1,623,799 |

|

| Ser. 13-6, Class IC, IO, 5.00%, 1/20/43 | 6,405,211 | 1,347,336 |

|

| Ser. 12-146, IO, 5.00%, 12/20/42 | 13,810,784 | 2,953,160 |

|

| Ser. 13-6, Class CI, IO, 5.00%, 12/20/42 | 4,682,071 | 896,382 |

|

| Ser. 13-130, Class IB, IO, 5.00%, 12/20/40 | 8,024,198 | 551,227 |

|

| Ser. 13-16, Class IB, IO, 5.00%, 10/20/40 | 3,286,214 | 192,933 |

|

| Ser. 11-41, Class BI, IO, 5.00%, 5/20/40 | 5,483,032 | 440,791 |

|

| Ser. 10-35, Class UI, IO, 5.00%, 3/20/40 | 22,857,510 | 4,831,506 |

|

| Ser. 10-20, Class UI, IO, 5.00%, 2/20/40 | 17,456,341 | 3,657,627 |

|

| Ser. 10-9, Class UI, IO, 5.00%, 1/20/40 | 85,557,638 | 18,185,618 |

|

| Ser. 09-121, Class UI, IO, 5.00%, 12/20/39 | 53,085,723 | 11,330,617 |

|

| Ser. 15-105, Class LI, IO, 5.00%, 10/20/39 | 27,280,348 | 5,834,448 |

|

| Ser. 15-79, Class GI, IO, 5.00%, 10/20/39 | 24,367,618 | 5,207,189 |

|

| IFB Ser. 14-119, Class SA, IO, 4.622%, 8/20/44 | 39,671,329 | 6,149,056 |

|

| Ser. 13-182, Class IQ, IO, 4.50%, 12/16/43 | 21,570,651 | 4,395,020 |

|

| Ser. 13-34, Class IH, IO, 4.50%, 3/20/43 | 23,226,601 | 4,842,677 |

|

| Ser. 13-183, Class JI, IO, 4.50%, 2/16/43 | 21,740,466 | 2,968,595 |

|

| Ser. 14-108, Class IP, IO, 4.50%, 12/20/42 | 5,441,836 | 943,614 |

|

| Ser. 17-42, Class IC, IO, 4.50%, 8/20/41 | 28,238,616 | 5,761,773 |

|

| Ser. 11-140, Class BI, IO, 4.50%, 12/20/40 | 3,304,352 | 194,895 |

|

| Ser. 13-167, IO, 4.50%, 9/20/40 | 13,062,553 | 2,133,401 |

|

| Ser. 10-35, Class AI, IO, 4.50%, 3/20/40 | 13,637,280 | 2,695,818 |

|

| Ser. 10-35, Class QI, IO, 4.50%, 3/20/40 | 33,206,886 | 6,687,834 |

|

| Ser. 10-20, Class BI, IO, 4.50%, 2/16/40 | 27,130,234 | 5,800,173 |

|

| Ser. 10-9, Class QI, IO, 4.50%, 1/20/40 | 20,651,022 | 4,135,718 |

|

| Ser. 14-71, Class PI, IO, 4.50%, 12/20/39 | 28,906,591 | 4,916,433 |

|

| Ser. 10-168, Class PI, IO, 4.50%, 11/20/39 | 8,132,609 | 868,563 |

|

| Ser. 10-158, Class IP, IO, 4.50%, 6/20/39 | 10,457,997 | 908,591 |

|

| Ser. 10-98, Class PI, IO, 4.50%, 10/20/37 | 1,271,236 | 22,247 |

|

| Ser. 16-138, Class DI, IO, 4.00%, 10/20/46 | 30,928,022 | 5,629,828 |

|

| Ser. 15-60, Class PI, IO, 4.00%, 4/20/45 | 18,383,688 | 3,699,717 |

|

| Ser. 15-89, Class IP, IO, 4.00%, 2/20/45 | 65,415,995 | 10,130,321 |

|

| Ser. 15-64, Class YI, IO, 4.00%, 11/20/44 | 36,660,175 | 6,743,639 |

|

| Ser. 15-79, Class MI, IO, 4.00%, 5/20/44 | 14,970,966 | 2,406,134 |

|

| Ser. 14-4, Class BI, IO, 4.00%, 1/20/44 | 18,180,753 | 3,853,298 |

|

| Ser. 14-4, Class IC, IO, 4.00%, 1/20/44 | 17,024,468 | 3,130,709 |

|

| Ser. 14-163, Class PI, IO, 4.00%, 10/20/43 | 19,644,697 | 2,511,195 |

|

| Ser. 13-165, Class IL, IO, 4.00%, 3/20/43 | 11,127,781 | 1,938,571 |

|

| Ser. 13-27, Class IJ, IO, 4.00%, 2/20/43 | 12,261,261 | 2,260,731 |

|

| Ser. 13-24, Class PI, IO, 4.00%, 11/20/42 | 6,785,094 | 1,110,737 |

|

| Ser. 12-106, Class QI, IO, 4.00%, 7/20/42 | 20,602,880 | 3,284,593 |

|

| Ser. 12-56, Class IB, IO, 4.00%, 4/20/42 | 7,580,952 | 1,373,789 |

|

| Ser. 12-8, Class PI, IO, 4.00%, 5/20/41 | 26,408,558 | 3,974,686 |

|

| Ser. 16-156, Class PI, IO, 3.50%, 11/20/46 | 57,735,459 | 7,533,554 |

|

| Ser. 17-17, Class DI, IO, 3.50%, 9/20/43 | 22,917,603 | 3,339,608 |

|

|

| Diversified Income Trust 21 |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Agency collateralized mortgage obligations cont. | | |

|

| Government National Mortgage Association | | |

|

| Ser. 13-102, Class IP, IO, 3.50%, 6/20/43 | $15,269,443 | $1,877,851 |

|

| Ser. 13-76, IO, 3.50%, 5/20/43 | 40,475,799 | 6,778,077 |

|

| Ser. 15-168, Class IG, IO, 3.50%, 3/20/43 | 31,031,813 | 5,036,215 |

|

| Ser. 13-28, IO, 3.50%, 2/20/43 | 11,352,701 | 1,679,401 |

|

| Ser. 13-54, Class JI, IO, 3.50%, 2/20/43 | 25,765,936 | 4,128,476 |

|

| Ser. 13-37, Class JI, IO, 3.50%, 1/20/43 | 23,528,870 | 3,785,795 |

|

| Ser. 13-27, Class PI, IO, 3.50%, 12/20/42 | 17,838,745 | 2,882,028 |

|

| Ser. 12-140, Class IC, IO, 3.50%, 11/20/42 | 41,984,941 | 8,632,398 |

|

| Ser. 12-128, Class IA, IO, 3.50%, 10/20/42 | 33,715,307 | 6,700,715 |

|

| Ser. 12-92, Class AI, IO, 3.50%, 4/20/42 | 17,444,842 | 1,712,079 |

|

| Ser. 14-62, Class CI, IO, 3.50%, 2/20/42 | 26,998,647 | 3,081,761 |

|

| Ser. 13-37, Class LI, IO, 3.50%, 1/20/42 | 32,232,856 | 4,311,725 |

|

| Ser. 15-131, Class BI, IO, 3.50%, 6/20/41 | 39,685,709 | 5,059,928 |

|

| Ser. 15-52, Class KI, IO, 3.50%, 11/20/40 | 45,692,075 | 6,504,632 |

|

| Ser. 15-17, Class LI, IO, 3.50%, 5/16/40 | 34,173,920 | 3,841,149 |

|

| Ser. 13-79, Class XI, IO, 3.50%, 11/20/39 | 38,364,580 | 5,123,781 |

|

| Ser. 12-48, Class AI, IO, 3.50%, 2/20/36 | 15,152,161 | 1,710,865 |

|

| Ser. 13-37, Class UI, IO, 3.00%, 2/20/42 | 20,148,927 | 2,618,555 |

|

| Ser. 13-41, Class MI, IO, 3.00%, 11/20/41 | 18,753,301 | 2,270,087 |

|

| Ser. 16-H23, Class NI, IO, 2.591%, 10/20/66 | 120,434,954 | 16,716,372 |

|

| Ser. 16-H24, Class JI, IO, 2.496%, 11/20/66 | 25,216,828 | 3,325,469 |

|

| Ser. 16-H04, Class HI, IO, 2.36%, 7/20/65 | 67,149,947 | 7,312,629 |

|

| Ser. 15-H18, Class BI, IO, 2.204%, 7/20/65 | 57,009,345 | 6,259,626 |

|

| Ser. 16-H17, Class KI, IO, 2.197%, 7/20/66 | 32,811,593 | 3,998,913 |

|

| Ser. 16-H16, Class EI, IO, 2.175%, 6/20/66 | 47,229,222 | 6,007,557 |

|

| Ser. 17-H06, Class MI, IO, 2.17%, 2/20/67 | 51,937,647 | 6,611,662 |

|

| Ser. 15-H15, Class BI, IO, 2.147%, 6/20/65 | 88,005,760 | 10,034,593 |

|

| Ser. 15-H24, Class AI, IO, 2.141%, 9/20/65 | 47,770,680 | 4,843,947 |

|

| Ser. 15-H20, Class BI, IO, 2.085%, 8/20/65 | 61,239,174 | 6,638,326 |

|

| Ser. 15-H10, Class BI, IO, 2.008%, 4/20/65 | 42,549,862 | 4,637,722 |

|

| Ser. 16-H06, Class CI, IO, 1.906%, 2/20/66 | 53,630,510 | 4,140,275 |

|

| Ser. 15-H12, Class AI, IO, 1.843%, 5/20/65 | 99,649,303 | 9,379,391 |

|

| Ser. 15-H23, Class DI, IO, 1.831%, 9/20/65 | 48,567,373 | 4,714,872 |

|

| Ser. 15-H15, Class AI, IO, 1.791%, 6/20/65 | 54,748,753 | 5,173,757 |

|

| FRB Ser. 15-H08, Class CI, IO, 1.78%, 3/20/65 | 77,809,852 | 7,215,152 |

|

| Ser. 15-H23, Class BI, IO, 1.715%, 9/20/65 | 89,610,488 | 8,038,061 |

|

| Ser. 15-H03, Class CI, IO, 1.711%, 1/20/65 | 83,434,956 | 7,346,281 |

|

| Ser. 14-H25, Class BI, IO, 1.676%, 12/20/64 | 58,865,493 | 5,033,000 |

|

| Ser. 16-H14, IO, 1.66%, 6/20/66 | 65,151,524 | 5,375,001 |

|

| Ser. 16-H12, Class AI, IO, 1.651%, 7/20/65 | 70,395,328 | 5,995,500 |

|

| Ser. 16-H18, IO, 1.632%, 8/20/66 | 73,589,570 | 5,850,371 |

|

| Ser. 15-H01, Class BI, IO, 1.555%, 1/20/65 | 52,888,756 | 3,728,657 |

|

| Ser. 14-H06, Class BI, IO, 1.47%, 2/20/64 | 53,277,175 | 3,271,219 |

|

| Ser. 12-H29, Class AI, IO, 1.461%, 10/20/62 | 35,320,029 | 1,836,642 |

|

| Ser. 12-H29, Class FI, IO, 1.461%, 10/20/62 | 35,320,029 | 1,836,642 |

|

| Ser. 06-36, Class OD, PO, zero %, 7/16/36 | 14,549 | 12,196 |

|

| Ser. 06-64, PO, zero %, 4/16/34 | 15,592 | 15,391 |

|

| | | 601,416,254 |

|

| 22 Diversified Income Trust |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Commercial mortgage-backed securities (16.9%) | | |

|

| Banc of America Commercial Mortgage Trust | | |

|

| FRB Ser. 07-3, Class AJ, 5.761%, 6/10/49 | $9,003,000 | $9,138,045 |

|

| Ser. 06-4, Class AJ, 5.695%, 7/10/46 | 7,033,011 | 7,019,249 |

|

| Ser. 06-1, Class B, 5.49%, 9/10/45 | 1,407,989 | 1,401,090 |

|

| Banc of America Commercial Mortgage Trust 144A FRB Ser. 07-5, | | |

| Class XW, IO, 0.339%, 2/10/51 | 125,734,470 | 158,752 |

|

| Banc of America Merrill Lynch Commercial Mortgage, Inc. | | |

|

| FRB Ser. 05-1, Class B, 5.28%, 11/10/42 | 7,045,000 | 6,029,322 |

|

| FRB Ser. 05-1, Class C, 5.28%, 11/10/42 | 8,629,000 | 5,210,708 |

|

| Bear Stearns Commercial Mortgage Securities Trust | | |

|

| FRB Ser. 07-T26, Class AJ, 5.566%, 1/12/45 | 11,024,000 | 10,693,280 |

|

| Ser. 05-PWR7, Class D, 5.304%, 2/11/41 | 4,190,000 | 4,105,949 |

|

| Ser. 05-PWR7, Class C, 5.235%, 2/11/41 | 4,945,000 | 4,926,209 |

|

| Ser. 05-PWR7, Class B, 5.214%, 2/11/41 | 6,277,097 | 6,283,374 |

|

| Ser. 05-PWR9, Class C, 5.055%, 9/11/42 | 3,639,228 | 3,675,329 |

|

| Bear Stearns Commercial Mortgage Securities Trust 144A FRB | | |

| Ser. 06-PW11, Class C, 5.693%, 3/11/39 | 8,260,000 | 4,170,061 |

|

| CD Mortgage Trust 144A | | |

|

| FRB Ser. 07-CD5, Class E, 6.159%, 11/15/44 | 8,486,000 | 8,235,184 |

|

| FRB Ser. 07-CD5, Class XS, IO, 0.151%, 11/15/44 | 76,152,492 | 9,570 |

|

| CFCRE Commercial Mortgage Trust 144A FRB Ser. 11-C2, Class E, | | |

| 5.755%, 12/15/47 | 13,980,000 | 13,909,124 |

|

| Citigroup Commercial Mortgage Trust FRB Ser. 06-C4, Class B, | | |

| 5.995%, 3/15/49 | 2,528,369 | 2,510,190 |

|

| Citigroup Commercial Mortgage Trust 144A FRB Ser. 14-GC21, | | |

| Class D, 4.836%, 5/10/47 | 7,280,000 | 6,014,008 |

|

| COBALT CMBS Commercial Mortgage Trust FRB Ser. 07-C3, | | |

| Class AJ, 5.88%, 5/15/46 | 5,019,000 | 5,063,857 |

|

| COMM Mortgage Trust Ser. 06-C8, Class AJ, 5.377%, 12/10/46 | 7,262,471 | 7,267,555 |

|

| COMM Mortgage Trust 144A | | |

|

| FRB Ser. 14-CR18, Class D, 4.737%, 7/15/47 | 17,857,000 | 14,464,170 |

|

| FRB Ser. 13-CR9, Class D, 4.256%, 7/10/45 | 5,143,000 | 4,517,611 |

|

| Ser. 12-LC4, Class E, 4.25%, 12/10/44 | 10,009,000 | 7,575,812 |

|

| Ser. 13-LC13, Class E, 3.719%, 8/10/46 | 11,140,000 | 7,658,750 |

|

| Ser. 14-CR18, Class E, 3.60%, 7/15/47 | 11,801,000 | 7,527,858 |

|

| Credit Suisse Commercial Mortgage Trust FRB Ser. 06-C5, Class AX, | | |

| IO, 0.652%, 12/15/39 | 23,250,900 | 81,378 |

|

| Credit Suisse Commercial Mortgage Trust 144A FRB Ser. 08-C1, | | |

| Class AJ, 6.062%, 2/15/41 | 10,825,000 | 9,850,750 |

|

| Credit Suisse First Boston Mortgage Securities Corp. | | |

|

| Ser. 05-C5, Class F, 5.10%, 8/15/38 | 4,760,000 | 4,742,756 |

|

| Ser. 05-C3, Class B, 4.882%, 7/15/37 | 4,276,355 | 4,258,822 |

|

| Crest, Ltd. 144A Ser. 03-2A, Class E2, 8.00%, 12/28/38 | | |

| (Cayman Islands) | 5,365,083 | 5,469,702 |

|

| CSAIL Commercial Mortgage Trust 144A FRB Ser. 15-C1, Class D, | | |

| 3.80%, 4/15/50 | 11,242,000 | 9,476,624 |

|

| GMAC Commercial Mortgage Securities, Inc. Trust Ser. 04-C3, | | |

| Class B, 4.965%, 12/10/41 | 579,328 | 581,420 |

|

|

| Diversified Income Trust 23 |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Commercial mortgage-backed securities cont. | | |

|

| GS Mortgage Securities Corp. II 144A | | |

|

| FRB Ser. 13-GC10, Class D, 4.41%, 2/10/46 | $1,693,000 | $1,583,632 |

|

| FRB Ser. 05-GG4, Class XC, IO, 1.477%, 7/10/39 | 2,693,559 | 3,502 |

|

| GS Mortgage Securities Trust 144A | | |

|

| FRB Ser. 12-GC6, Class D, 5.653%, 1/10/45 | 1,316,248 | 1,283,868 |

|

| Ser. 11-GC3, Class E, 5.00%, 3/10/44 | 8,510,000 | 7,864,942 |

|

| JPMBB Commercial Mortgage Securities Trust 144A | | |

|

| FRB Ser. 13-C15, Class D, 5.047%, 11/15/45 | 2,970,000 | 2,809,434 |

|

| FRB Ser. 14-C18, Class E, 4.314%, 2/15/47 | 7,852,000 | 5,498,756 |

|

| FRB Ser. 14-C25, Class D, 3.948%, 11/15/47 | 9,103,000 | 6,989,283 |

|

| FRB Ser. 14-C26, Class D, 3.926%, 1/15/48 | 19,738,000 | 16,072,397 |

|

| Ser. 14-C25, Class E, 3.332%, 11/15/47 | 15,725,000 | 9,603,258 |

|

| JPMorgan Chase Commercial Mortgage Securities Trust | | |

|

| FRB Ser. 07-CB20, Class AJ, 6.178%, 2/12/51 | 3,877,500 | 3,970,948 |

|

| FRB Ser. 06-LDP7, Class B, 5.939%, 4/17/45 | 9,729,000 | 1,769,705 |

|

| JPMorgan Chase Commercial Mortgage Securities Trust 144A | | |

|

| FRB Ser. 07-CB20, Class B, 6.278%, 2/12/51 | 9,775,000 | 9,181,658 |

|

| FRB Ser. 07-CB20, Class C, 6.278%, 2/12/51 | 9,324,000 | 8,205,120 |

|

| FRB Ser. 11-C3, Class E, 5.622%, 2/15/46 | 10,985,000 | 11,168,450 |

|

| FRB Ser. 12-C8, Class E, 4.677%, 10/15/45 | 3,743,999 | 3,432,907 |

|

| FRB Ser. 13-C13, Class D, 4.053%, 1/15/46 | 2,509,000 | 2,353,405 |

|

| Ser. 13-C13, Class E, 3.986%, 1/15/46 | 13,925,000 | 9,567,868 |

|

| Ser. 13-C10, Class E, 3.50%, 12/15/47 | 14,081,000 | 10,265,049 |

|

| FRB Ser. 13-LC11, Class E, 3.25%, 4/15/46 | 9,312,000 | 6,280,944 |

|

| LB Commercial Mortgage Trust 144A | | |

|

| Ser. 99-C1, Class G, 6.41%, 6/15/31 | 1,481,777 | 1,519,679 |

|

| Ser. 98-C4, Class J, 5.60%, 10/15/35 | 3,535,000 | 3,608,175 |

|

| LB-UBS Commercial Mortgage Trust | | |

|

| Ser. 06-C6, Class D, 5.502%, 9/15/39 | 3,660,000 | 801,796 |

|

| FRB Ser. 06-C6, Class C, 5.482%, 9/15/39 | 25,155,000 | 7,591,276 |

|

| LSTAR Commercial Mortgage Trust 144A FRB Ser. 15-3, Class C, | | |

| 3.229%, 4/20/48 | 9,081,000 | 7,573,009 |

|

| Merrill Lynch Mortgage Trust | | |

|

| FRB Ser. 08-C1, Class AJ, 6.301%, 2/12/51 | 2,001,000 | 2,037,618 |

|

| Ser. 04-KEY2, Class D, 5.046%, 8/12/39 | 2,973,642 | 2,944,864 |

|

| Mezz Cap Commercial Mortgage Trust 144A | | |

|

| FRB Ser. 04-C1, Class X, IO, 9.321%, 1/15/37 | 148,064 | 10,764 |

|

| FRB Ser. 07-C5, Class X, IO, 4.546%, 12/15/49 | 2,780,325 | 16,682 |

|

| ML-CFC Commercial Mortgage Trust 144A Ser. 06-4, Class AJFX, | | |

| 5.147%, 12/12/49 | 314,369 | 314,903 |

|

| Morgan Stanley Bank of America Merrill Lynch Trust 144A | | |

|

| Ser. 14-C17, Class D, 4.698%, 8/15/47 | 24,488,000 | 20,525,873 |

|

| FRB Ser. 12-C6, Class G, 4.50%, 11/15/45 | 4,901,000 | 3,680,161 |

|

| FRB Ser. 13-C7, Class D, 4.264%, 2/15/46 | 2,611,000 | 2,378,196 |

|

| Ser. 14-C15, Class F, 4.00%, 4/15/47 | 8,998,000 | 6,068,959 |

|

| Ser. 13-C13, Class F, 3.707%, 11/15/46 | 7,659,000 | 5,377,251 |

|

| Ser. 14-C17, Class E, 3.50%, 8/15/47 | 14,427,000 | 9,024,089 |

|

| Ser. 15-C24, Class D, 3.257%, 5/15/48 | 17,620,000 | 12,193,792 |

|

|

| 24 Diversified Income Trust |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Commercial mortgage-backed securities cont. | | |

|

| Morgan Stanley Capital I Trust | | |

|

| FRB Ser. 07-T27, Class AJ, 5.791%, 6/11/42 | $2,776,000 | $2,870,939 |

|

| Ser. 07-HQ11, Class C, 5.558%, 2/12/44 | 21,393,000 | 9,440,089 |

|

| Ser. 06-HQ10, Class B, 5.448%, 11/12/41 | 5,060,000 | 5,055,006 |

|

| FRB Ser. 06-HQ8, Class D, 5.399%, 3/12/44 | 8,329,000 | 3,367,665 |

|

| Morgan Stanley Capital I Trust 144A | | |

|

| FRB Ser. 08-T29, Class F, 6.301%, 1/11/43 | 7,212,000 | 7,155,025 |

|

| FRB Ser. 04-RR, Class F7, 6.00%, 4/28/39 | 3,912,273 | 3,842,595 |

|

| STRIPS CDO 144A Ser. 03-1A, Class N, IO, 5.00%, 3/24/18 | | |

| (Cayman Islands) | 1,590,000 | 35,775 |

|

| TIAA Real Estate CDO, Ltd. 144A Ser. 03-1A, Class E, | | |

| 8.00%, 12/28/38 | 4,487,377 | 336,553 |

|

| UBS-Barclays Commercial Mortgage Trust 144A | | |

|

| Ser. 12-C2, Class F, 4.885%, 5/10/63 | 6,674,000 | 4,795,269 |

|

| FRB Ser. 13-C6, Class D, 4.345%, 4/10/46 | 1,362,000 | 1,212,861 |

|

| Ser. 13-C6, Class E, 3.50%, 4/10/46 | 18,360,000 | 12,668,400 |

|

| Wachovia Bank Commercial Mortgage Trust | | |

|

| FRB Ser. 06-C26, Class AJ, 6.087%, 6/15/45 | 20,649,000 | 15,412,414 |

|

| Ser. 07-C30, Class AJ, 5.413%, 12/15/43 | 6,568,714 | 6,597,132 |

|

| FRB Ser. 05-C21, Class D, 5.294%, 10/15/44 | 17,760,000 | 17,632,087 |

|

| FRB Ser. 07-C34, IO, 0.40%, 5/15/46 | 40,996,653 | 61,495 |

|

| Wells Fargo Commercial Mortgage Trust 144A | | |

|

| Ser. 12-LC5, Class E, 4.777%, 10/15/45 | 8,280,000 | 6,607,440 |

|

| FRB Ser. 13-LC12, Class D, 4.296%, 7/15/46 | 14,132,111 | 12,829,936 |

|

| Ser. 14-LC16, Class D, 3.938%, 8/15/50 | 11,962,000 | 9,935,612 |

|

| Ser. 13-LC12, Class E, 3.50%, 7/15/46 | 15,829,000 | 10,556,360 |

|

| WF-RBS Commercial Mortgage Trust 144A | | |

|

| FRB Ser. 11-C5, Class E, 5.673%, 11/15/44 | 508,000 | 514,248 |

|

| Ser. 12-C6, Class E, 5.00%, 4/15/45 | 7,840,000 | 6,183,408 |

|

| Ser. 11-C3, Class E, 5.00%, 3/15/44 | 8,644,000 | 7,143,402 |

|

| FRB Ser. 14-C19, Class E, 4.97%, 3/15/47 | 6,483,000 | 4,755,929 |

|

| FRB Ser. 13-UBS1, Class E, 4.627%, 3/15/46 | 11,752,000 | 8,548,405 |

|

| FRB Ser. 13-C15, Class D, 4.48%, 8/15/46 | 9,609,996 | 8,480,246 |

|

| FRB Ser. 12-C10, Class D, 4.455%, 12/15/45 | 6,987,000 | 6,157,294 |

|

| Ser. 14-C19, Class D, 4.234%, 3/15/47 | 3,448,000 | 2,889,752 |

|

| Ser. 13-C12, Class E, 3.50%, 3/15/48 | 15,114,000 | 11,479,083 |

|

| | | 572,163,142 |

|

| Residential mortgage-backed securities (non-agency) (11.2%) | | |

|

| BCAP, LLC Trust 144A | | |

|

| FRB Ser. 11-RR3, Class 3A6, 3.072%, 11/27/36 | 11,661,747 | 7,929,988 |

|

| FRB Ser. 12-RR5, Class 4A8, 0.948%, 6/26/35 | 8,282,853 | 7,996,677 |

|

| Bear Stearns Asset Backed Securities I Trust FRB Ser. 04-FR3, | | |

| Class M6, 5.857%, 9/25/34 | 256,410 | 119,472 |

|

| Bellemeade Re Ltd. 144A FRB Ser. 15-1A, Class M2, 5.282%, | | |

| 7/25/25 (Bermuda) | 9,438,261 | 9,627,026 |

|

| Countrywide Alternative Loan Trust | | |

|

| FRB Ser. 06-OA7, Class 1A1, 2.28%, 6/25/46 | 2,755,008 | 2,618,635 |

|

| FRB Ser. 06-OA7, Class 1A2, 1.578%, 6/25/46 | 17,960,045 | 15,789,573 |

|

| FRB Ser. 05-38, Class A3, 1.332%, 9/25/35 | 39,454,389 | 34,268,425 |

|

|

| Diversified Income Trust 25 |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Residential mortgage-backed securities (non-agency) cont. | | |

|

| Countrywide Alternative Loan Trust | | |

|

| FRB Ser. 05-59, Class 1A1, 1.306%, 11/20/35 | $33,280,089 | $29,439,487 |

|

| FRB Ser. 06-OA10, Class 4A1, 1.172%, 8/25/46 | 14,081,308 | 11,969,111 |

|

| Federal Home Loan Mortgage Corporation | | |

|

| Structured Agency Credit Risk Debt FRN Ser. 15-DN1, Class B, | | |

| 12.482%, 1/25/25 | 15,602,022 | 20,037,735 |

|

| Structured Agency Credit Risk Debt FRN Ser. 16-DNA2, Class B, | | |

| 11.482%, 10/25/28 | 2,529,742 | 2,986,066 |

|

| Structured Agency Credit Risk Debt FRN Ser. 16-DNA1, Class B, | | |

| 10.982%, 7/25/28 | 765,779 | 888,073 |

|

| Structured Agency Credit Risk Debt FRN Ser. 15-DNA3, Class B, | | |

| 10.332%, 4/25/28 | 11,978,735 | 13,927,569 |

|

| Structured Agency Credit Risk Debt FRN Ser. 15-DNA2, Class B, | | |

| 8.532%, 12/25/27 | 11,460,960 | 12,921,687 |

|

| Structured Agency Credit Risk Debt FRN Ser. 16-HQA2, Class M3, | | |

| 6.132%, 11/25/28 | 2,950,000 | 3,273,029 |

|

| Structured Agency Credit Risk Debt FRN Ser. 17-DNA1, Class B1, | | |

| 5.932%, 7/25/29 | 5,110,000 | 5,101,109 |

|

| FRB Ser. 17-HQA1, Class M2, 4.532%, 8/25/29 | 2,010,000 | 2,011,568 |

|

| Federal National Mortgage Association | | |

|

| Connecticut Avenue Securities FRB Ser. 16-C02, Class 1B, | | |

| 13.232%, 9/25/28 | 13,999,424 | 18,100,779 |

|

| Connecticut Avenue Securities FRB Ser. 16-C03, Class 1B, | | |

| 12.732%, 10/25/28 | 7,745,000 | 9,726,372 |

|

| Connecticut Avenue Securities FRB Ser. 16-C01, Class 1B, | | |

| 12.732%, 8/25/28 | 11,787,000 | 14,851,395 |

|

| Connecticut Avenue Securities FRB Ser. 16-C03, Class 2M2, | | |

| 6.882%, 10/25/28 | 9,077,000 | 10,329,276 |

|

| Connecticut Avenue Securities FRB Ser. 15-C04, Class 1M2, | | |

| 6.682%, 4/25/28 | 26,931,500 | 30,445,864 |

|

| Connecticut Avenue Securities FRB Ser. 17-C02, Class 2B1, | | |

| 6.477%, 9/25/29 | 3,949,000 | 3,984,227 |

|

| Connecticut Avenue Securities FRB Ser. 16-C03, Class 1M2, | | |

| 6.282%, 10/25/28 | 1,320,000 | 1,482,135 |

|

| Connecticut Avenue Securities FRB Ser. 15-C03, Class 1M2, | | |

| 5.982%, 7/25/25 | 18,823,000 | 20,694,627 |

|

| Connecticut Avenue Securities FRB Ser. 15-C03, Class 2M2, | | |

| 5.982%, 7/25/25 | 9,376,364 | 10,230,985 |

|

| Connecticut Avenue Securities FRB Ser. 15-C01, Class 2M2, | | |

| 5.532%, 2/25/25 | 6,245,342 | 6,631,928 |

|

| Connecticut Avenue Securities FRB Ser. 16-C07, Class 2M2, | | |

| 5.332%, 4/25/29 | 3,300,000 | 3,486,866 |

|

| Connecticut Avenue Securities FRB Ser. 15-C01, Class 1M2, | | |

| 5.282%, 2/25/25 | 6,650,748 | 7,054,305 |

|

| Connecticut Avenue Securities FRB Ser. 16-C06, Class 1M2, | | |

| 5.232%, 4/25/29 | 510,000 | 539,121 |

|

| Connecticut Avenue Securities FRB Ser. 16-C04, Class 1M2, | | |

| 5.232%, 1/25/29 | 1,680,000 | 1,775,424 |

|

| Connecticut Avenue Securities FRB Ser. 15-C02, Class 1M2, | | |

| 4.982%, 5/25/25 | 1,964,567 | 2,066,955 |

|

|

| 26 Diversified Income Trust |

| | |

| | Principal | |

| MORTGAGE-BACKED SECURITIES (45.9%)* cont. | amount | Value |

|

| Residential mortgage-backed securities (non-agency) cont. | | |

|

| Federal National Mortgage Association | | |

|

| Connecticut Avenue Securities FRB Ser. 15-C02, Class 2M2, | | |

| 4.982%, 5/25/25 | $3,114,896 | $3,273,027 |

|

| Connecticut Avenue Securities FRB Ser. 17-C02, Class 2M2, | | |

| 4.627%, 9/25/29 | 5,667,000 | 5,703,536 |

|

| Connecticut Avenue Securities FRB Ser. 14-C03, Class 1M2, | | |

| 3.982%, 7/25/24 | 2,097,000 | 2,162,459 |

|

| Federal National Mortgage Association 144A Connecticut Avenue | | |

| Securities FRB Ser. 17-C01, Class 1B1, 6.732%, 7/25/29 | 10,840,000 | 11,448,124 |

|

| Green Tree Home Improvement Loan Trust Ser. 95-D, Class B2, | | |

| 7.45%, 9/15/25 | 288 | 288 |

|

| GSAA Home Equity Trust FRB Ser. 06-8, Class 2A2, 1.162%, 5/25/36 | 13,804,395 | 7,048,524 |

|

| Structured Asset Mortgage Investments II Trust FRB Ser. 06-AR7, | | |

| Class A1A, 1.192%, 8/25/36 | 3,479,281 | 2,922,596 |

|

| WaMu Mortgage Pass-Through Certificates Trust | | |

|

| FRB Ser. 05-AR10, Class 1A3, 2.784%, 9/25/35 | 2,288,823 | 2,264,344 |

|

| FRB Ser. 05-AR13, Class A1C3, 1.472%, 10/25/45 | 17,662,266 | 16,483,801 |

|

| FRB Ser. 05-AR19, Class A1C4, 1.382%, 12/25/45 | 4,287,634 | 3,724,024 |

|

| | | 377,336,212 |

|

| Total mortgage-backed securities (cost $1,614,213,608) | | $1,550,915,608 |

|

| | |

| | Principal | |

| CORPORATE BONDS AND NOTES (30.3%)* | amount | Value |

|

| Basic materials (3.5%) | | |

|

| A Schulman, Inc. company guaranty sr. unsec. unsub. notes | | |

| 6.875%, 6/1/23 | $1,104,000 | $1,145,400 |

|

| Allegheny Technologies, Inc. sr. unsec. unsub. notes | | |

| 9.375%, 6/1/19 | 2,255,000 | 2,469,225 |

|

| Alpha 3 BV/Alpha US Bidco, Inc. 144A company guaranty sr. unsec. | | |

| notes 6.25%, 2/1/25 (Netherlands) | 2,980,000 | 3,002,350 |

|

| ArcelorMittal SA sr. unsec. unsub. bonds 10.60%, 6/1/19 (France) | 890,000 | 1,054,650 |

|

| ArcelorMittal SA sr. unsec. unsub. bonds 6.125%, 6/1/25 (France) | 1,760,000 | 1,951,400 |

|

| ArcelorMittal SA sr. unsec. unsub. notes 7.75%, 10/15/39 (France) | 404,000 | 458,540 |

|

| Axalta Coating Systems, LLC 144A company guaranty sr. unsec. | | |

| unsub. notes 4.875%, 8/15/24 | 1,465,000 | 1,501,625 |

|

| Beacon Roofing Supply, Inc. company guaranty sr. unsec. unsub. | | |

| notes 6.375%, 10/1/23 | 2,021,000 | 2,152,365 |

|

| Blue Cube Spinco, Inc. company guaranty sr. unsec. unsub. notes | | |

| 9.75%, 10/15/23 | 1,316,000 | 1,575,910 |

|

| BMC East, LLC 144A company guaranty sr. notes 5.50%, 10/1/24 | 2,570,000 | 2,614,975 |

|

| Boise Cascade Co. 144A company guaranty sr. unsec. notes | | |

| 5.625%, 9/1/24 | 2,921,000 | 2,964,815 |

|

| Builders FirstSource, Inc. 144A company guaranty sr. unsec. notes | | |

| 10.75%, 8/15/23 | 3,853,000 | 4,479,113 |

|

| Builders FirstSource, Inc. 144A company guaranty sr. unsub. notes | | |

| 5.625%, 9/1/24 | 1,900,000 | 1,928,500 |

|

| BWAY Holding Co. 144A sr. notes 5.50%, 4/15/24 | 2,020,000 | 2,036,423 |

|

| BWAY Holding Co. 144A sr. unsec. notes 7.25%, 4/15/25 | 2,535,000 | 2,535,000 |

|