| OMB APPROVAL |

OMB Number: 3235-0570 Expires: January 31, 2014 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number ___811-05646_________________

New Century Portfolios

(Exact name of registrant as specified in charter)

100 William Street, Suite 200 Wellesley, Massachusetts 02481

(Address of principal executive offices) (Zip code)

Nicole M. Tremblay, Esq.

Weston Financial Group, Inc. 100 William Street, Suite 200 Wellesley, MA 02481

(Name and address of agent for service)

Registrant's telephone number, including area code: (781) 235-7055

Date of fiscal year end: October 31, 2013

Date of reporting period: October 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

New Century Capital New Century Balanced New Century International New Century Alternative Strategies ANNUAL REPORT Year Ended October 31, 2013 100 William Street, Suite 200, Wellesley MA 02481 781-239-0445 888-639-0102 Fax 781-237-1635 |

CONTENTS

| LETTER TO SHAREHOLDERS | 2-4 |

| PERFORMANCE CHARTS | 5-8 |

| NEW CENTURY PORTFOLIOS | |

| New Century Capital Portfolio | |

| Portfolio Information | 9 |

| Schedule of Investments | 10-11 |

| New Century Balanced Portfolio | |

| Portfolio Information | 12 |

| Schedule of Investments | 13-14 |

| New Century International Portfolio | |

| Portfolio Information | 15 |

| Schedule of Investments | 16-17 |

| New Century Alternative Strategies Portfolio | |

| Portfolio Information | 18 |

| Schedule of Investments | 19-21 |

| Statements of Assets and Liabilities | 22 |

| Statements of Operations | 23 |

| Statements of Changes in Net Assets | 24-25 |

| Financial Highlights | 26-29 |

| Notes to Financial Statements | 30-39 |

| Report of Independent Registered Public Accounting Firm | 40 |

| Board of Trustees and Officers | 41-42 |

| About Your Portfolios’ Expenses | 43-45 |

| Trustees’ Approval of Investment Advisory Agreements | 46-50 |

LETTER TO SHAREHOLDERS | December 2013 |

We are pleased to present our 24th Annual Report. The report summarizes the 12-month period ended October 31, 2013. In addition, this report presents important financial information for each of the New Century Portfolios. We invite you to visit our website at www.newcenturyportfolios.com for additional information.

As we look back over the 12 months ended October 31, 2013, U.S. markets finished with robust returns as demonstrated by the increase in the S&P 500 Index by 27.18%. During this past summer, markets fluctuated over the potential “tapering” of the Federal Reserve’s Quantitative Easing program and intense discussions over the U.S. debt ceiling caused a government shutdown. Nevertheless, with Ben Bernanke’s handling, broad domestic indexes regained the global lead in the second half of fiscal 2013. International markets also produced positive returns. For example, developed international markets, as measured by the MSCI EAFE Index, gained 26.88% and the MSCI Emerging Markets Index increased 6.53% during the year ended October 31, 2013. Even though market activity is forecasted to be tepid, the European debt crisis appears to be behind us and the Eurozone is slowly coming out of a recession. However, a number of emerging market economies are coming off cyclical peaks and global growth is in low but in positive gear. (IMF Executive Summary October 2013). Although, mediocre global growth has also impacted the price of commodities.

Several themes were implemented within the New Century Portfolios over the year. We began tilting towards active managers and away from passive managers. During a bear market, investors typically flee unstable lower quality stocks. Conversely, these same stocks rally strongly in the initial phase of a market recovery. As the cycle matures, participants approach investing more cautiously and evaluate investments according to fundamentals. Companies with good earnings growth and solid balance sheets typically start to outperform, benefiting active management. As the S&P 500 Index has already garnered 184% since the 2009 market low through October 31, 2013, active management may now come to the forefront. As such, the New Century Capital, Balanced and International Portfolios have begun replacing a number of passive index positions with actively managed mutual funds.

We have also attempted to temper the effects of rising interest rates. Even though the Federal Reserve will not likely begin tapering until the spring of 2014, some investors may anticipate this move. In the period between May and September 2013, the 10-year Treasury yields soared from 1.7% to 3.0% as the word “taper” dominated the headlines. Over the year the Portfolios sold longer duration funds and invested proceeds in strategies that are less impacted by rising interest rates. In fixed income, the Portfolios shifted to shorter durations or funds that have wider investment mandates. In equities, dividend focused mandates were sold in favor of other types of value or more growth-tilted strategies. These trades were most evident in New Century Capital and New Century Balanced Portfolios. Within New Century Alternative Strategies Portfolio, the long/short, arbitrage, global macro styles were seen to be effective themes to employ.

On the international front, we favor developed markets. We believe European stock valuations are below average and could benefit from early cycle dynamics. The Global PMI suggests manufacturing momentum could continue for larger international economies. Emerging markets indexes have suffered under the weight of China’s structural reform and

2

a lower growth mandate, however a recent policy shift has assisted with stabilizing growth. In May, expectations of a “taper” and higher U.S. Treasury yields caused carry trades to unwind, resulting in capital outflows from emerging markets. Over the year, New Century Capital, Balanced and International Portfolios have shifted some exposure away from emerging markets to the developed markets.

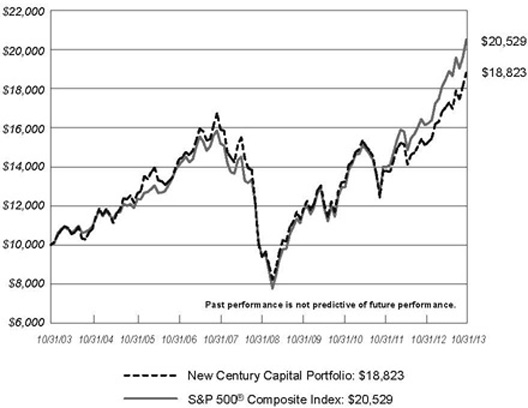

For the fiscal year ended October 31, 2013, New Century Capital Portfolio (NCCPX) returned 24.45% vs. 27.18% for the S&P 500 Index, the Portfolio’s benchmark index. This large-cap domestic Portfolio opportunistically invests in smaller-cap, sector and international areas. The Portfolio’s mid- and smaller-cap funds added the most to returns. In a year of strong equity performance, riskier mid- and smaller-cap indexes outperformed large-cap indexes. New Century Capital Portfolio’s growth tilt was also beneficial as some of the largest contributors to performance were funds in the large growth style. The sector group was a minor detractor relative to the benchmark. Healthcare funds were strong performers, but they were offset by commodity-related funds such as gold and energy. Finally, the allocation to international funds served as a drag on performance.

New Century Balanced Portfolio (NCIPX) outperformed the Morningstar Moderate Allocation category for the fiscal year ended October 31, 2013. New Century Balanced Portfolio gained 15.97% vs. 15.85% for the Morningstar Moderate Allocation category. Compared to the Morningstar Moderate Allocation category, the Portfolio’s allocation to stocks vs. bonds, and selection of fixed income sectors explained most of the outperformance. Active fixed income managers with flexible mandates were particularly beneficial to the Portfolio. Similar to the New Century Capital Portfolio, the equity portion’s slight growth tilt was also additive to overall performance.

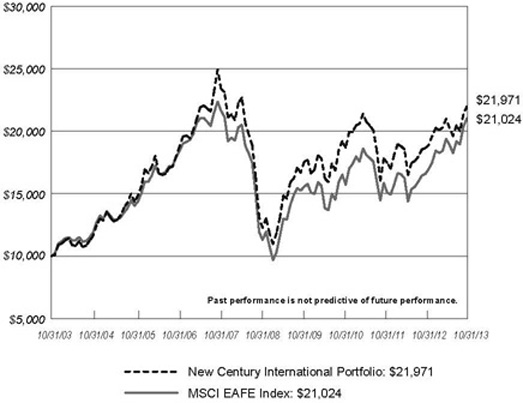

New Century International Portfolio (NCFPX) finished its fiscal year ended October 31, 2013 with a 17.95% gain. In comparison, the MSCI EAFE Index rallied 26.88% and the MSCI ACWI ex USA Index garnered 20.29%. The latter index is an appropriate benchmark considering the Portfolio’s emerging markets exposure. Meanwhile, the Morningstar Foreign Large Blend category rallied on average by 23.08%. Over the year the Portfolio reduced underperforming emerging markets exposure to slightly below the ACWI benchmark exposure. Further, the Portfolio’s emerging markets and Latin America exposures detracted from the annual performance. In the second half of the year, exposure to Japan was increased in order to capture returns of one of the strongest performing countries in 2013. Overall, New Century International Portfolio is bullish on Europe, long-term optimistic on emerging markets, and neutral on Japan.

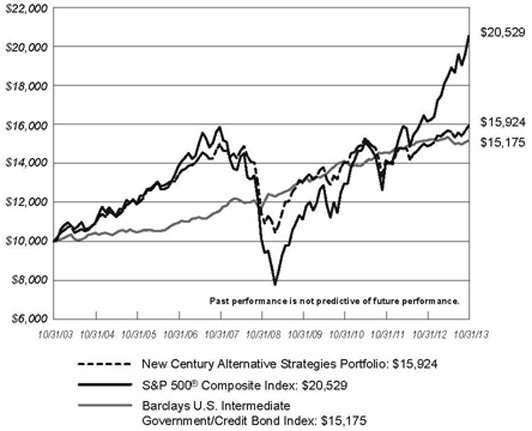

New Century Alternative Strategies Portfolio (NCHPX) gained 6.99% vs. the Morningstar Multi-Alternative category’s 3.69% as of October 31, 2013. This four star fund1 has continued to outperform the average fund in its Morningstar category for the one, three, five and ten-year periods ended October 31, 2013. New Century Alternative Strategies Portfolio opportunistically invests among a broad-based portfolio of different alternative asset classes. Over the fiscal year ended October 31, 2013, New Century Alternative Strategies Portfolio mitigated volatility by selling funds in highly correlated strategies and redeploying the proceeds to different sources of alpha. The natural resource category was a detractor, whereas the Portfolio benefited from exposure to the long/short equities, global macro and

3

asset allocation categories. Further, redeployment of assets into better performing funds within categories and timely purchases of discounted closed-end funds after the summer’s market pullback were also beneficial.

As we embark on the 2014 fiscal year, we have positioned New Century Portfolios for the continuation of several trends – better markets for active managers, volatility in interest rates and recovering developed international markets. A significant event in 2014 will likely be the slowing of the Federal Reserve’s Quantitative Easing program. We remain vigilant for opportunities this event may bring.

We appreciate your business and thank you for your trust in New Century Portfolios.

Sincerely,

|  |

Nicole M. Tremblay, Esq. President, CEO | Susan K. Arnold Portfolio Manager |

|  |

Andre M. Fernandes Portfolio Manager | Ronald A. Sugameli Portfolio Manager |

1 Morningstar Ratings reflect risk-adjusted performance and are derived from weighted average of the Fund’s 3-, 5- and 10-year (if applicable) Ratings. For the periods ended October 31, 2013, the Portfolio received 4-Stars Overall and for the 3- and 5-year periods among 142, 142 and 87 funds respectively. The Morningstar Ratings formula measures the amount of variation in a fund’s performance and gives more emphasis to downward variations. Ratings are subject to change every month. The top 10% of the funds in the category receive 5 stars; the next 22.5% 4 stars; the next 35% 3 stars; the next 22.5% 2 stars; and the last 10% 1 star.

Investors should take into consideration the investment objectives, risks, charges and expenses of the New Century Portfolios carefully before investing. The prospectus contains these details and other information and should be read carefully before investing. Principal value of an investment will fluctuate and shares when redeemed may be worth more or less than your original investment. Past performance is not indicative of future results. Portfolio and opinions expressed herein are subject to change.

4

NEW CENTURY CAPITAL PORTFOLIO PERFORMANCE CHARTS (Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

in New Century Capital Portfolio and S&P 500® Composite Index

Average Annual Total Returns For Periods Ended October 31, 2013 | ||||

1 Year | 5 Years | 10 Years | ||

New Century Capital Portfolio (a) | 24.45% | 13.42% | 6.53% | |

S&P 500® Composite Index * | 27.18% | 15.17% | 7.46% | |

| (a) | The total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. |

| * | The S&P 500® Composite Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

5

NEW CENTURY BALANCED PORTFOLIO PERFORMANCE CHARTS (Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

in New Century Balanced Portfolio, S&P 500® Composite Index and

Barclays U.S. Intermediate Government/Credit Bond Index

Average Annual Total Returns For Periods Ended October 31, 2013 | ||||

1 Year | 5 Years | 10 Years | ||

New Century Balanced Portfolio (a) | 15.97% | 11.23% | 5.87% | |

S&P 500® Composite Index * | 27.18% | 15.17% | 7.46% | |

Barclays U.S. Intermediate Government/Credit Bond Index * | -0.03% | 5.37% | 4.26% | |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. |

| * | The S&P 500® Composite Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Barclays U.S. Intermediate Government/Credit Bond Index is the non-securitized component of the U.S. Aggregate Index, and includes Treasuries, government-related issues, and corporate. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

6

NEW CENTURY INTERNATIONAL PORTFOLIO PERFORMANCE CHARTS (Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

in New Century International Portfolio and MSCI EAFE Index

Average Annual Total Returns For Periods Ended October 31, 2013 | |||

1 Year | 5 Years | 10 Years | |

New Century International Portfolio (a) | 17.95% | 10.92% | 8.19% |

| MSCI EAFE Index * | 26.88% | 11.99% | 7.71% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. |

| * | The MSCI EAFE (Europe, Australasia and Far East) Index is a free float weighted capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

7

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO PERFORMANCE CHARTS (Unaudited) |

Comparison of the Change in Value of a $10,000 Investment

in New Century Alternative Strategies Portfolio, S&P 500® Composite Index

and Barclays U.S. Intermediate Government/Credit Bond Index

Average Annual Total Returns For Periods Ended October 31, 2013 | |||

1 Year | 5 Years | 10 Years | |

New Century Alternative Strategies Portfolio (a) | 6.99% | 6.77% | 4.76% |

S&P 500® Composite Index * | 27.18% | 15.17% | 7.46% |

Barclays U.S. Intermediate Government/Credit Bond Index * | -0.03% | 5.37% | 4.26% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. |

| * | The S&P 500® Composite Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Barclays U.S. Intermediate Government/Credit Bond Index is the non-securitized component of the U.S. Aggregate Index, and includes Treasuries, government-related issues, and corporate. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

8

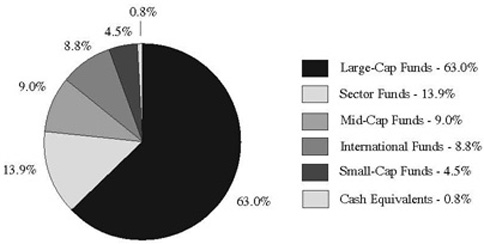

NEW CENTURY CAPITAL PORTFOLIO PORTFOLIO INFORMATION (Unaudited) October 31, 2013 |

Asset Allocation (% of Net Assets) |

| Top Ten Long-Term Holdings |

| Security Description | % of Net Assets | |

| Wells Fargo Advantage Growth Fund - Administrator Class | 6.6% | |

| Vanguard Dividend Growth Fund - Investor Shares | 6.4% | |

| MFS Growth Fund - Class I | 6.2% | |

| Putnam Equity Income Fund - Class Y | 5.2% | |

| Vanguard 500 Index Fund - Signal Shares | 5.0% | |

| iShares S&P 500 Value Index Fund | 4.4% | |

| iShares Dow Jones U.S. Energy Sector Index Fund | 4.0% | |

| iShares Core S&P 500 ETF | 3.9% | |

| Gabelli Asset Fund (The) - Class I | 3.9% | |

| Fidelity Select Health Care Portfolio | 3.7% |

9

NEW CENTURY CAPITAL PORTFOLIO SCHEDULE OF INVESTMENTS October 31, 2013 |

INVESTMENT COMPANIES — 99.2% | Shares | Value | ||||||

| Large-Cap Funds — 63.0% | ||||||||

American Funds AMCAP Fund - Class A | 141,961 | $ | 3,893,982 | |||||

| Columbia Dividend Opportunity Fund - Class A | 290,005 | 3,013,155 | ||||||

Gabelli Asset Fund (The) - Class I | 67,398 | 4,414,538 | ||||||

iShares Core S&P 500 ETF (a) | 25,050 | 4,426,335 | ||||||

iShares Russell 1000 Index Fund (a) | 40,000 | 3,930,800 | ||||||

iShares S&P 500 Growth Index Fund (a) | 41,800 | 3,911,644 | ||||||

iShares S&P 500 Value Index Fund (a) | 60,800 | 4,970,400 | ||||||

| JPMorgan Value Advantage Fund - Institutional Class | 118,250 | 3,153,725 | ||||||

MFS Equity Opportunities Fund - Class I | 58,571 | 1,500,000 | ||||||

MFS Growth Fund - Class I (b) | 107,775 | 7,008,605 | ||||||

Putnam Equity Income Fund - Class Y | 279,505 | 5,858,419 | ||||||

| RidgeWorth Large Cap Value Equity Fund - I Shares | 110,620 | 1,993,363 | ||||||

Vanguard 500 Index Fund - Signal Shares | 42,217 | 5,654,179 | ||||||

| Vanguard Dividend Growth Fund - Investor Shares | 353,316 | 7,274,771 | ||||||

Weitz Partners Value Fund (b) | 88,133 | 2,724,205 | ||||||

Wells Fargo Advantage Growth Fund - Administrator Class (b) | 137,143 | 7,398,888 | ||||||

| 71,127,009 | ||||||||

| Sector Funds — 13.9% | ||||||||

Fidelity Select Health Care Portfolio | 22,045 | 4,139,569 | ||||||

iShares Dow Jones U.S. Energy Sector Index Fund (a) | 91,400 | 4,487,740 | ||||||

Ivy Science and Technology Fund - Class I (b) | 51,869 | 2,735,594 | ||||||

PowerShares Dynamic Pharmaceuticals Portfolio (a) | 67,000 | 3,208,630 | ||||||

SPDR Gold Trust (a) (b) (c) | 9,000 | 1,149,660 | ||||||

| 15,721,193 | ||||||||

| Mid-Cap Funds — 9.0% | ||||||||

iShares S&P MidCap 400 Growth Index Fund (a) | 12,600 | 1,808,730 | ||||||

iShares S&P MidCap 400 Value Index Fund (a) | 31,600 | 3,557,212 | ||||||

Putnam Equity Spectrum Fund - Class Y | 50,518 | 1,980,298 | ||||||

SPDR S&P MidCap 400 ETF Trust (a) | 11,702 | 2,744,353 | ||||||

| 10,090,593 | ||||||||

| International Funds — 8.8% | ||||||||

| Aberdeen Emerging Markets Fund - Institutional Class | 84,636 | 1,295,781 | ||||||

Harding, Loevner International Equity Portfolio - Institutional Class | 109,470 | 1,967,181 | ||||||

| Oppenheimer Developing Markets Fund - Class Y | 41,942 | 1,587,927 | ||||||

| Oppenheimer International Growth Fund - Class Y | 104,350 | 3,875,564 | ||||||

| Wells Fargo Advantage Intrinsic World Equity Fund - Administrator Class | 52,549 | 1,146,085 | ||||||

| 9,872,538 | ||||||||

See accompanying notes to financial statements.

10

NEW CENTURY CAPITAL PORTFOLIO SCHEDULE OF INVESTMENTS (Continued) |

INVESTMENT COMPANIES — 99.2% (Continued) | Shares | Value | ||||||

| Small-Cap Funds — 4.5% | ||||||||

Brown Capital Management Small Company Fund - Institutional Class (b) | 15,316 | $ | 1,109,053 | |||||

iShares S&P SmallCap 600 Growth Index Fund (a) | 15,200 | 1,706,048 | ||||||

iShares S&P SmallCap 600 Value Index Fund (a) | 21,800 | 2,305,132 | ||||||

| 5,120,233 | ||||||||

Total Investment Companies (Cost $75,551,537) | $ | 111,931,566 | ||||||

MONEY MARKET FUNDS — 2.3% | Shares | Value | ||||||

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.06% (d) (Cost $2,544,729) | 2,544,729 | $ | 2,544,729 | |||||

Total Investments at Value — 101.5% (Cost $78,096,266) | $ | 114,476,295 | ||||||

| Liabilities in Excess of Other Assets — (1.5%) | (1,648,151 | ) | ||||||

Net Assets — 100.0% | $ | 112,828,144 | ||||||

| (a) | Exchange-traded fund. |

| (b) | Non-income producing security. |

| (c) | For federal income tax purposes, structured as a grantor trust. |

| (d) | The rate shown is the 7-day effective yield as of October 31, 2013. |

See accompanying notes to financial statements.

11

NEW CENTURY BALANCED PORTFOLIO PORTFOLIO INFORMATION (Unaudited) October 31, 2013 |

Asset Allocation (% of Net Assets) |

| Top Ten Long-Term Holdings |

| Security Description | % of Net Assets | |

| Loomis Sayles Bond Fund - Institutional Class | 7.7% | |

| First Eagle Global Fund - Class A | 7.4% | |

| Wells Fargo Advantage Growth Fund - Administrator Class | 6.3% | |

| iShares Core S&P 500 ETF | 6.0% | |

| SPDR S&P MidCap 400 ETF Trust | 5.9% | |

| Harding, Loevner International Equity Portfolio - Institutional Class | 5.8% | |

| Templeton Global Bond Fund - Class A | 5.7% | |

| Dodge & Cox Income Fund | 5.2% | |

| American Funds AMCAP Fund - Class A | 4.8% | |

| JPMorgan Value Advantage Fund - Institutional Class | 4.4% |

12

NEW CENTURY BALANCED PORTFOLIO SCHEDULE OF INVESTMENTS October 31, 2013 |

INVESTMENT COMPANIES — 98.3% | Shares | Value | ||||||

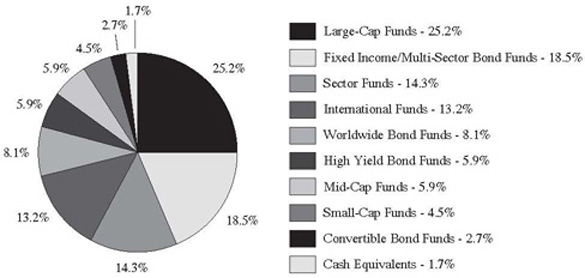

| Large-Cap Funds — 25.2% | ||||||||

American Funds AMCAP Fund - Class A | 124,832 | $ | 3,424,145 | |||||

iShares Core S&P 500 ETF (a) | 24,400 | 4,311,480 | ||||||

| John Hancock Disciplined Value Fund - Class I | 148,176 | 2,636,053 | ||||||

| JPMorgan Value Advantage Fund - Institutional Class | 117,463 | 3,132,733 | ||||||

Wells Fargo Advantage Growth Fund - Administrator Class (b) | 83,207 | 4,488,999 | ||||||

| 17,993,410 | ||||||||

| Fixed Income/Multi-Sector Bond Funds — 18.5% | ||||||||

Dodge & Cox Income Fund | 270,183 | 3,685,300 | ||||||

| Loomis Sayles Bond Fund - Institutional Class | 359,252 | 5,507,334 | ||||||

PIMCO Income Fund - Institutional Class | 201,604 | 2,495,861 | ||||||

| Vanguard Intermediate-Term Investment-Grade Fund - Admiral Shares | 154,362 | 1,526,640 | ||||||

| 13,215,135 | ||||||||

| Sector Funds — 14.3% | ||||||||

Consumer Staples Select Sector SPDR Fund (a) | 67,300 | 2,850,155 | ||||||

Fidelity Select Health Care Portfolio | 13,918 | 2,613,598 | ||||||

iShares Dow Jones U.S. Energy Sector Index Fund (a) | 46,500 | 2,283,150 | ||||||

Oppenheimer MLP Select 40 Fund - Institutional Class (b) | 147,755 | 1,802,615 | ||||||

SPDR Gold Trust (a) (b) (c) | 5,300 | 677,022 | ||||||

| 10,226,540 | ||||||||

| International Funds — 13.2% | ||||||||

First Eagle Global Fund - Class A | 95,582 | 5,249,367 | ||||||

Harding, Loevner International Equity Portfolio - Institutional Class | 231,605 | 4,161,946 | ||||||

| 9,411,313 | ||||||||

| Worldwide Bond Funds — 8.1% | ||||||||

| Loomis Sayles Global Bond Fund - Institutional Class | 100,018 | 1,670,298 | ||||||

Templeton Global Bond Fund - Class A | 312,494 | 4,106,164 | ||||||

| 5,776,462 | ||||||||

| High Yield Bond Funds — 5.9% | ||||||||

| Loomis Sayles Institutional High Income Fund | 277,329 | 2,348,974 | ||||||

| Oppenheimer Senior Floating Rate Fund - Class A | 222,944 | 1,870,503 | ||||||

| 4,219,477 | ||||||||

| Mid-Cap Funds — 5.9% | ||||||||

SPDR S&P MidCap 400 ETF Trust (a) | 17,980 | 4,216,670 | ||||||

| Small-Cap Funds — 4.5% | ||||||||

Brown Capital Management Small Company Fund - Institutional Class (b) | 7,079 | 512,601 | ||||||

iShares S&P SmallCap 600 Growth Index Fund (a) | 8,100 | 909,144 | ||||||

iShares S&P SmallCap 600 Value Index Fund (a) | 17,200 | 1,818,728 | ||||||

| 3,240,473 | ||||||||

See accompanying notes to financial statements.

13

NEW CENTURY BALANCED PORTFOLIO SCHEDULE OF INVESTMENTS (Continued) |

INVESTMENT COMPANIES — 98.3% (Continued) | Shares | Value | ||||||

| Convertible Bond Funds — 2.7% | ||||||||

| Allianz AGIC Convertible Fund - Institutional Shares | 56,647 | $ | 1,927,122 | |||||

Total Investment Companies (Cost $53,304,339) | $ | 70,226,602 | ||||||

MONEY MARKET FUNDS — 1.9% | Shares | Value | ||||||

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.06% (d) (Cost $1,338,159) | 1,338,159 | $ | 1,338,159 | |||||

Total Investments at Value — 100.2% (Cost $54,642,498) | $ | 71,564,761 | ||||||

| Liabilities in Excess of Other Assets — (0.2%) | (107,769 | ) | ||||||

Net Assets — 100.0% | $ | 71,456,992 | ||||||

| (a) | Exchange-traded fund. |

| (b) | Non-income producing security. |

| (c) | For federal income tax purposes, structured as a grantor trust. |

| (d) | The rate shown is the 7-day effective yield as of October 31, 2013. |

See accompanying notes to financial statements.

14

NEW CENTURY INTERNATIONAL PORTFOLIO PORTFOLIO INFORMATION (Unaudited) October 31, 2013 |

Asset Allocation (% of Net Assets) |

| Top Ten Long-Term Holdings |

| Security Description | % of Net Assets | |

| Columbia European Equity Fund - Class A | 7.3% | |

| Matthews Japan Fund - Institutional Class | 7.0% | |

| iShares MSCI Germany Index Fund | 6.4% | |

| Franklin Mutual European Fund - Class A | 6.3% | |

| Harding, Loevner International Equity Portfolio- Institutional Class | 6.0% | |

| Oakmark International Fund - Class I | 6.0% | |

| Matthews Pacific Tiger Fund - Investor Class | 5.6% | |

| iShares MSCI Switzerland Index Fund | 5.4% | |

| iShares MSCI United Kingdom Index Fund | 5.1% | |

| Vanguard MSCI Europe ETF | 5.0% |

15

NEW CENTURY INTERNATIONAL PORTFOLIO SCHEDULE OF INVESTMENTS October 31, 2013 |

INVESTMENT COMPANIES — 99.4% | Shares | Value | ||||||

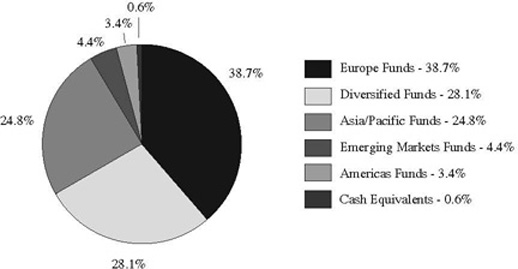

| Europe Funds — 38.7% | ||||||||

Columbia European Equity Fund - Class A | 605,650 | $ | 4,572,660 | |||||

Franklin Mutual European Fund - Class A | 155,037 | 3,931,742 | ||||||

iShares MSCI Germany Index Fund (a) | 137,000 | 4,020,950 | ||||||

iShares MSCI Sweden Index Fund (a) | 58,000 | 1,983,020 | ||||||

iShares MSCI Switzerland Index Fund (a) | 105,600 | 3,401,376 | ||||||

iShares MSCI United Kingdom Index Fund (a) | 156,546 | 3,185,711 | ||||||

Vanguard MSCI Europe ETF (a) | 55,200 | 3,134,256 | ||||||

| 24,229,715 | ||||||||

| Diversified Funds — 28.1% | ||||||||

| Columbia Acorn International Select Fund - Class A | 68,807 | 1,977,517 | ||||||

| Harbor International Fund - Institutional Class | 16,993 | 1,202,914 | ||||||

Harding, Loevner International Equity Portfolio - Institutional Class | 210,638 | 3,785,163 | ||||||

iShares MSCI EAFE Growth Index Fund (a) | 10,900 | 761,801 | ||||||

iShares MSCI EAFE Value Index Fund (a) | 11,800 | 667,644 | ||||||

iShares S&P Global Energy Sector Index Fund (a) | 22,400 | 958,272 | ||||||

MFS International Value Fund - Class I | 34,470 | 1,208,875 | ||||||

Oakmark International Fund - Class I | 140,788 | 3,761,848 | ||||||

| Oppenheimer International Growth Fund - Class Y | 26,995 | 1,002,598 | ||||||

Templeton Institutional Funds - Foreign Smaller Companies Series | 103,413 | 2,282,337 | ||||||

| 17,608,969 | ||||||||

| Asia/Pacific Funds — 24.8% | ||||||||

iShares MSCI Australia Index Fund (a) | 42,500 | 1,133,475 | ||||||

iShares MSCI Pacific ex-Japan Index Fund (a) | 49,700 | 2,471,084 | ||||||

| Matthews China Dividend Fund - Investor Class | 83,403 | 1,116,764 | ||||||

Matthews Japan Fund - Institutional Class | 268,349 | 4,382,135 | ||||||

Matthews Pacific Tiger Fund - Investor Class | 136,891 | 3,516,723 | ||||||

WisdomTree Japan Hedged Equity Fund (a) | 61,700 | 2,941,856 | ||||||

| 15,562,037 | ||||||||

| Emerging Markets Funds — 4.4% | ||||||||

| Aberdeen Emerging Markets Fund - Institutional Class | 89,510 | 1,370,395 | ||||||

Vanguard MSCI Emerging Markets ETF (a) | 33,200 | 1,390,084 | ||||||

| 2,760,479 | ||||||||

| Americas Funds — 3.4% | ||||||||

Fidelity Canada Fund | 11,611 | 670,289 | ||||||

JPMorgan Latin America Fund - Select Class | 78,740 | 1,466,929 | ||||||

| 2,137,218 | ||||||||

Total Investment Companies (Cost $45,130,012) | $ | 62,298,418 | ||||||

See accompanying notes to financial statements.

16

NEW CENTURY INTERNATIONAL PORTFOLIO SCHEDULE OF INVESTMENTS (Continued) |

MONEY MARKET FUNDS — 0.4% | Shares | Value | ||||||

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.06% (b) (Cost $278,696) | 278,696 | $ | 278,696 | |||||

Total Investments at Value — 99.8% (Cost $45,408,708) | $ | 62,577,114 | ||||||

| Other Assets in Excess of Liabilities — 0.2% | 130,427 | |||||||

Net Assets — 100.0% | $ | 62,707,541 | ||||||

| (a) | Exchange-traded fund. |

| (b) | The rate shown is the 7-day effective yield as of October 31, 2013. |

See accompanying notes to financial statements.

17

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO PORTFOLIO INFORMATION (Unaudited) October 31, 2013 |

Asset Allocation (% of Net Assets) |

| Top Ten Long-Term Holdings |

| Security Description | % of Net Assets | |

| Touchstone Merger Arbitrage Fund - Institutional Shares | 7.7% | |

| MainStay Marketfield Fund - Class I | 7.2% | |

| Calamos Market Neutral Income Fund - Class A | 5.5% | |

| First Eagle Global Fund - Class A | 5.2% | |

| FPA Crescent Fund | 5.1% | |

| Wasatch Long/Short Fund | 4.6% | |

| Berwyn Income Fund | 4.5% | |

| 361 Managed Futures Strategy Fund - Class I | 4.0% | |

| Templeton Global Bond Fund - Class A | 3.6% | |

| TFS Market Neutral Fund | 3.6% |

18

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO SCHEDULE OF INVESTMENTS October 31, 2013 |

INVESTMENT COMPANIES — 93.9% | Shares | Value | ||||||

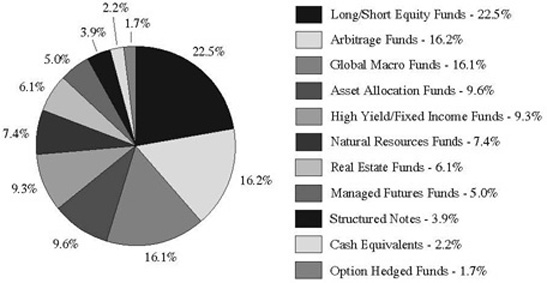

| Long/Short Equity Funds — 22.5% | ||||||||

| BlackRock Emerging Markets Long/Short Equity Fund - Institutional Shares | 182,127 | $ | 1,966,972 | |||||

MainStay Marketfield Fund - Class I (b) | 492,754 | 8,928,708 | ||||||

| Robeco Boston Partners Long/Short Research Fund - Institutional Class | 176,196 | 2,440,310 | ||||||

TFS Market Neutral Fund (b) | 276,049 | 4,469,226 | ||||||

Wasatch Long/Short Fund (b) | 350,729 | 5,730,906 | ||||||

Weitz Partners III Opportunity Fund - Institutional Class (b) | 265,916 | 4,236,044 | ||||||

| 27,772,166 | ||||||||

| Arbitrage Funds — 16.2% | ||||||||

Arbitrage Fund (The) - Class I | 9,885 | 127,127 | ||||||

| Calamos Market Neutral Income Fund - Class A | 520,897 | 6,818,546 | ||||||

Gabelli ABC Fund - Advisor Class | 166,667 | 1,718,333 | ||||||

Merger Fund (The) | 106,557 | 1,733,683 | ||||||

| Touchstone Merger Arbitrage Fund - Institutional Shares | 858,648 | 9,556,755 | ||||||

| 19,954,444 | ||||||||

| Global Macro Funds — 16.1% | ||||||||

BlackRock Global Allocation Fund - Class A | 79,253 | 1,730,887 | ||||||

Eaton Vance Global Macro Absolute Return Advantage Fund - Class I | 177,690 | 1,707,601 | ||||||

First Eagle Global Fund - Class A | 116,324 | 6,388,493 | ||||||

Ivy Asset Strategy Fund - Class A | 105,638 | 3,205,063 | ||||||

John Hancock Global Absolute Return Strategies Fund - Class I | 283,546 | 3,121,847 | ||||||

Mutual Global Discovery Fund - Class Z | 108,098 | 3,741,288 | ||||||

| 19,895,179 | ||||||||

| Asset Allocation Funds — 9.6% | ||||||||

Berwyn Income Fund | 372,500 | 5,494,372 | ||||||

FPA Crescent Fund | 191,266 | 6,309,858 | ||||||

| 11,804,230 | ||||||||

| High Yield/Fixed Income Funds — 9.3% | ||||||||

Aberdeen Asia-Pacific Income Fund, Inc. (d) | 210,000 | 1,352,400 | ||||||

Blackrock Credit Allocation Income Trust (d) | 100,000 | 1,297,000 | ||||||

Ivy High Income Fund - Class A | 221,335 | 1,941,107 | ||||||

PIMCO Income Fund - Institutional Class | 197,692 | 2,447,424 | ||||||

Templeton Global Bond Fund - Class A | 341,723 | 4,490,238 | ||||||

| 11,528,169 | ||||||||

| Natural Resources Funds — 7.4% | ||||||||

Market Vectors Gold Miners ETF (a) | 43,000 | 1,079,730 | ||||||

Oppenheimer MLP Select 40 Fund - Institutional Class (b) | 127,657 | 1,557,417 | ||||||

| PIMCO CommodityRealReturn Strategy Fund - Class A | 270,051 | 1,504,181 | ||||||

RS Global Natural Resources Fund - Class A (b) | 25,949 | 981,642 | ||||||

SPDR Gold Trust (a) (b) (c) | 10,500 | 1,341,270 | ||||||

| Tortoise MLP & Pipeline Fund - Institutional Class | 120,166 | 1,836,144 | ||||||

See accompanying notes to financial statements.

19

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO SCHEDULE OF INVESTMENTS (Continued) |

INVESTMENT COMPANIES — 93.9% (Continued) | Shares | Value | ||||||

| Natural Resources Funds — 7.4% (Continued) | ||||||||

Vanguard Precious Metals and Mining Fund - Investor Shares | 73,522 | $ | 791,828 | |||||

| 9,092,212 | ||||||||

| Real Estate Funds — 6.1% | ||||||||

CBRE Clarion Global Real Estate Income Fund (d) | 100,000 | 837,000 | ||||||

ING Global Real Estate Fund - Class I | 157,454 | 2,968,009 | ||||||

Vanguard REIT ETF (a) | 54,000 | 3,732,480 | ||||||

| 7,537,489 | ||||||||

| Managed Futures Funds — 5.0% | ||||||||

361 Managed Futures Strategy Fund - Class I (b) | 429,271 | 4,940,905 | ||||||

MutualHedge Frontier Legends Fund - Class I (b) | 137,597 | 1,254,888 | ||||||

| 6,195,793 | ||||||||

| Option Hedged Funds — 1.7% | ||||||||

BlackRock Enhanced Capital & Income Fund (d) | 50,000 | 676,000 | ||||||

BlackRock Enhanced Equity Dividend Trust (d) | 90,000 | 694,800 | ||||||

Gateway Fund - Class A | 24,885 | 710,717 | ||||||

| 2,081,517 | ||||||||

Total Investment Companies (Cost $99,254,215) | $ | 115,861,199 | ||||||

STRUCTURED NOTES — 3.9% | Par Value | Value | ||||||

| JPMorgan Chase & Co., Return Note Linked to JPMorgan ETF Efficiente 5 PR Index, due 06/23/2014 | $ | 1,500,000 | $ | 1,518,450 | ||||

JPMorgan Chase & Co., Return Note Linked to the JPMorgan Strategic Volatility Dynamic Index (Series 1), due 09/30/2014 (b) | 1,500,000 | 1,284,150 | ||||||

RBC Capital Markets, Absolute Return Barrier Equity Security Linked Note, due 05/15/2014 (b) | 1,600,000 | 2,067,360 | ||||||

Total Structured Notes (Cost $4,600,000) | $ | 4,869,960 | ||||||

See accompanying notes to financial statements.

20

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO SCHEDULE OF INVESTMENTS (Continued) |

MONEY MARKET FUNDS — 2.8% | Shares | Value | ||||||

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.06% (e) (Cost $3,478,464) | 3,478,464 | $ | 3,478,464 | |||||

Total Investments at Value — 100.6% (Cost $107,332,679) | $ | 124,209,623 | ||||||

| Liabilities in Excess of Other Assets — (0.6%) | (799,086 | ) | ||||||

Net Assets — 100.0% | $ | 123,410,537 | ||||||

| (a) | Exchange-traded fund. |

| (b) | Non-income producing security. |

| (c) | For federal income tax purposes, structured as a grantor trust. |

| (d) | Closed-end fund. |

| (e) | The rate shown is the 7-day effective yield as of October 31, 2013. |

See accompanying notes to financial statements.

21

NEW CENTURY PORTFOLIOS STATEMENTS OF ASSETS AND LIABILITIES October 31, 2013 |

New Century Capital Portfolio | New Century Balanced Portfolio | New Century International Portfolio | New Century Alternative Strategies Portfolio | |||||||||||||

| ASSETS | ||||||||||||||||

| Investments in securities: | ||||||||||||||||

| At acquisition cost | $ | 78,096,266 | $ | 54,642,498 | $ | 45,408,708 | $ | 107,332,679 | ||||||||

| At value (Note 1A) | $ | 114,476,295 | $ | 71,564,761 | $ | 62,577,114 | $ | 124,209,623 | ||||||||

| Dividends receivable | 36 | 22,441 | 10 | 20,237 | ||||||||||||

| Receivable for investment securities sold | — | — | 200,000 | — | ||||||||||||

| Receivable for capital shares sold | 3,550 | 2,656 | 1,601 | 374,177 | ||||||||||||

| Other assets | 5,462 | 3,509 | 3,002 | 6,318 | ||||||||||||

| TOTAL ASSETS | 114,485,343 | 71,593,367 | 62,781,727 | 124,610,355 | ||||||||||||

| LIABILITIES | ||||||||||||||||

Payable for investment securities purchased | 1,500,000 | 17,742 | — | 1,080,944 | ||||||||||||

| Payable for capital shares redeemed | 27,156 | 37,301 | — | 16,496 | ||||||||||||

| Payable to Adviser (Note 2) | 95,004 | 61,773 | 54,376 | 80,341 | ||||||||||||

| Payable to Distributor (Note 3) | 23,000 | 11,500 | 13,000 | 11,500 | ||||||||||||

| Other accrued expenses and liabilities | 12,039 | 8,059 | 6,810 | 10,537 | ||||||||||||

| TOTAL LIABILITIES | 1,657,199 | 136,375 | 74,186 | 1,199,818 | ||||||||||||

| NET ASSETS | $ | 112,828,144 | $ | 71,456,992 | $ | 62,707,541 | $ | 123,410,537 | ||||||||

| Net assets consist of: | ||||||||||||||||

| Paid-in capital | $ | 66,921,762 | $ | 50,504,666 | $ | 40,898,512 | $ | 113,325,197 | ||||||||

Accumulated undistributed net investment income (loss) | — | 185,621 | 361,321 | (233,684 | ) | |||||||||||

Accumulated undistributed net realized gains (losses) on investments | 9,526,353 | 3,844,442 | 4,279,302 | (6,557,920 | ) | |||||||||||

Net unrealized appreciation on investments | 36,380,029 | 16,922,263 | 17,168,406 | 16,876,944 | ||||||||||||

| Net assets | $ | 112,828,144 | $ | 71,456,992 | $ | 62,707,541 | $ | 123,410,537 | ||||||||

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 5,422,521 | 4,284,965 | 3,860,191 | 9,476,451 | ||||||||||||

Net asset value, offering price and redemption price per share (a) | $ | 20.81 | $ | 16.68 | $ | 16.24 | $ | 13.02 | ||||||||

| (a) | Redemption price may differ from the net asset value per share depending upon the length of time held (Note 1B). |

See accompanying notes to financial statements.

22

NEW CENTURY PORTFOLIOS STATEMENTS OF OPERATIONS For the Year Ended October 31, 2013 |

New Century Capital Portfolio | New Century Balanced Portfolio | New Century International Portfolio | New Century Alternative Strategies Portfolio | |||||||||||||

| INVESTMENT INCOME | ||||||||||||||||

| Dividends | $ | 1,462,706 | $ | 1,771,790 | $ | 1,262,611 | $ | 1,791,873 | ||||||||

| Interest | — | — | — | 43,071 | ||||||||||||

| Total investment income | 1,462,706 | 1,771,790 | 1,262,611 | 1,834,944 | ||||||||||||

| EXPENSES | ||||||||||||||||

| Investment advisory fees (Note 2) | 1,008,864 | 681,529 | 600,445 | 907,545 | ||||||||||||

| Distribution costs (Note 3) | 239,677 | 128,113 | 107,550 | 218,046 | ||||||||||||

| Accounting fees | 46,239 | 38,528 | 36,829 | 49,575 | ||||||||||||

| Administration fees (Note 2) | 37,891 | 26,659 | 24,001 | 43,893 | ||||||||||||

| Legal and audit fees | 29,153 | 22,852 | 21,113 | 35,110 | ||||||||||||

| Trustees’ fees and expenses (Note 2) | 30,416 | 20,033 | 17,780 | 35,683 | ||||||||||||

| Transfer agent fees | 24,638 | 21,119 | 20,386 | 25,857 | ||||||||||||

| Custody and bank service fees | 19,907 | 14,962 | 14,624 | 22,175 | ||||||||||||

| Postage & supplies | 9,755 | 5,277 | 5,370 | 7,744 | ||||||||||||

| Insurance expense | 7,646 | 5,472 | 4,621 | 9,700 | ||||||||||||

| Other expenses | 12,405 | 9,491 | 9,196 | 12,243 | ||||||||||||

| Total expenses | 1,466,591 | 974,035 | 861,915 | 1,367,571 | ||||||||||||

| NET INVESTMENT INCOME (LOSS) | (3,885 | ) | 797,755 | 400,696 | 467,373 | |||||||||||

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | ||||||||||||||||

| Net realized gains on investments | 10,120,888 | 4,244,536 | 7,854,026 | 1,535,433 | ||||||||||||

Capital gain distributions from regulated investment companies | 440,532 | 432,660 | 225,293 | 889,507 | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments | 11,827,607 | 4,608,660 | 1,406,537 | 5,147,864 | ||||||||||||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 22,389,027 | 9,285,856 | 9,485,856 | 7,572,804 | ||||||||||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 22,385,142 | $ | 10,083,611 | $ | 9,886,552 | $ | 8,040,177 | ||||||||

See accompanying notes to financial statements.

23

NEW CENTURY PORTFOLIOS STATEMENTS OF CHANGES IN NET ASSETS |

New Century Capital Portfolio | New Century Balanced Portfolio | |||||||||||||||

Year Ended October 31, 2013 | Year Ended October 31, 2012 | Year Ended October 31, 2013 | Year Ended October 31, 2012 | |||||||||||||

| FROM OPERATIONS | ||||||||||||||||

| Net investment income (loss) | $ | (3,885 | ) | $ | (47,114 | ) | $ | 797,755 | $ | 783,443 | ||||||

| Net realized gains from security transactions | 10,120,888 | 3,780,693 | 4,244,536 | 1,615,147 | ||||||||||||

Capital gain distributions from regulated investment companies | 440,532 | 400,834 | 432,660 | 396,073 | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments | 11,827,607 | 4,043,331 | 4,608,660 | 2,640,566 | ||||||||||||

| Net increase in net assets from operations | 22,385,142 | 8,177,744 | 10,083,611 | 5,435,229 | ||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||||||||||

| From net investment income (Note 1E) | — | — | (794,645 | ) | (828,337 | ) | ||||||||||

From net realized gains on security transactions (Note 1E) | (4,174,787 | ) | (497,600 | ) | — | — | ||||||||||

Decrease in net assets from distributions to shareholders | (4,174,787 | ) | (497,600 | ) | (794,645 | ) | (828,337 | ) | ||||||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||||||||||

Net assets received in conjunction with fund merger (Note 1) | 12,773,191 | — | — | — | ||||||||||||

| Proceeds from shares sold | 3,510,261 | 2,037,610 | 2,946,146 | 2,998,862 | ||||||||||||

Proceeds from redemption fees collected (Note 1B) | 724 | — | 1 | 545 | ||||||||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 4,040,782 | 476,833 | 768,274 | 792,109 | ||||||||||||

| Payments for shares redeemed | (13,370,844 | ) | (11,132,882 | ) | (8,371,973 | ) | (6,155,077 | ) | ||||||||

Net increase (decrease) in net assets from capital share transactions | 6,954,114 | (8,618,439 | ) | (4,657,552 | ) | (2,363,561 | ) | |||||||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | 25,164,469 | (938,295 | ) | 4,631,414 | 2,243,331 | |||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of year | 87,663,675 | 88,601,970 | 66,825,578 | 64,582,247 | ||||||||||||

| End of year | $ | 112,828,144 | $ | 87,663,675 | $ | 71,456,992 | $ | 66,825,578 | ||||||||

ACCUMULATED UNDISTRIBUTED NET INVESTMENT INCOME (LOSS) | $ | — | $ | (47,114 | ) | $ | 185,621 | $ | 182,511 | |||||||

| CAPITAL SHARE ACTIVITY | ||||||||||||||||

Shares issued in conjunction with fund merger (Note 1) | 708,515 | — | — | — | ||||||||||||

| Shares sold | 191,859 | 119,985 | 193,485 | 215,916 | ||||||||||||

| Shares reinvested | 236,580 | 29,877 | 52,478 | 59,467 | ||||||||||||

| Shares redeemed | (708,926 | ) | (656,370 | ) | (552,033 | ) | (437,060 | ) | ||||||||

| Net increase (decrease) in shares outstanding | 428,028 | (506,508 | ) | (306,070 | ) | (161,677 | ) | |||||||||

| Shares outstanding, beginning of year | 4,994,493 | 5,501,001 | 4,591,035 | 4,752,712 | ||||||||||||

| Shares outstanding, end of year | 5,422,521 | 4,994,493 | 4,284,965 | 4,591,035 | ||||||||||||

See accompanying notes to financial statements.

24

NEW CENTURY PORTFOLIOS STATEMENTS OF CHANGES IN NET ASSETS |

New Century International Portfolio | New Century Alternative Strategies Portfolio | |||||||||||||||

Year Ended October 31, 2013 | Year Ended October 31, 2012 | Year Ended October 31, 2013 | Year Ended October 31, 2012 | |||||||||||||

| FROM OPERATIONS | ||||||||||||||||

| Net investment income | $ | 400,696 | $ | 603,454 | $ | 467,373 | $ | 1,335,732 | ||||||||

Net realized gains from security transactions | 7,854,026 | 993,696 | 1,535,433 | 2,581,537 | ||||||||||||

Capital gain distributions from regulated investment companies | 225,293 | 99,741 | 889,507 | 654,879 | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments | 1,406,537 | 835,231 | 5,147,864 | 1,345,836 | ||||||||||||

| Net increase in net assets from operations | 9,886,552 | 2,532,122 | 8,040,177 | 5,917,984 | ||||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||||||||||

| From net investment income (Note 1E) | (642,497 | ) | (434,898 | ) | (668,997 | ) | (1,636,766 | ) | ||||||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||||||||||

| Proceeds from shares sold | 2,276,174 | 1,830,688 | 15,300,515 | 14,278,169 | ||||||||||||

Proceeds from redemption fees collected (Note 1B) | 3 | 179 | 2,722 | 5,870 | ||||||||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 631,930 | 429,919 | 656,678 | 1,604,814 | ||||||||||||

| Payments for shares redeemed | (6,710,756 | ) | (8,354,017 | ) | (17,192,246 | ) | (17,739,389 | ) | ||||||||

Net decrease in net assets from capital share transactions | (3,802,649 | ) | (6,093,231 | ) | (1,232,331 | ) | (1,850,536 | ) | ||||||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | 5,441,406 | (3,996,007 | ) | 6,138,849 | 2,430,682 | |||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of year | 57,266,135 | 61,262,142 | 117,271,688 | 114,841,006 | ||||||||||||

| End of year | $ | 62,707,541 | $ | 57,266,135 | $ | 123,410,537 | $ | 117,271,688 | ||||||||

ACCUMULATED UNDISTRIBUTED NET INVESTMENT INCOME (LOSS) | $ | 361,321 | $ | 603,122 | $ | (233,684 | ) | $ | (32,060 | ) | ||||||

| CAPITAL SHARE ACTIVITY | ||||||||||||||||

| Shares sold | 152,928 | 137,479 | 1,205,497 | 1,195,574 | ||||||||||||

| Shares reinvested | 43,581 | 33,852 | 53,258 | 139,792 | ||||||||||||

| Shares redeemed | (449,438 | ) | (624,997 | ) | (1,360,199 | ) | (1,492,107 | ) | ||||||||

| Net decrease in shares outstanding | (252,929 | ) | (453,666 | ) | (101,444 | ) | (156,741 | ) | ||||||||

| Shares outstanding, beginning of year | 4,113,120 | 4,566,786 | 9,577,895 | 9,734,636 | ||||||||||||

| Shares outstanding, end of year | 3,860,191 | 4,113,120 | 9,476,451 | 9,577,895 | ||||||||||||

See accompanying notes to financial statements.

25

NEW CENTURY CAPITAL PORTFOLIO FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | ||||||||||||||||||||

Years Ended October 31, | ||||||||||||||||||||

2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| PER SHARE OPERATING PERFORMANCE | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 17.55 | $ | 16.11 | $ | 15.41 | $ | 13.26 | $ | 11.76 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss) | (0.00 | ) | (0.01 | ) | (0.04 | ) | (0.03 | ) | 0.03 | |||||||||||

Net realized and unrealized gains on investments | 4.11 | 1.54 | 0.74 | 2.21 | 1.50 | |||||||||||||||

| Total from investment operations | 4.11 | 1.53 | 0.70 | 2.18 | 1.53 | |||||||||||||||

| Less distributions: | ||||||||||||||||||||

| Distributions from net investment income | — | — | — | (0.03 | ) | (0.03 | ) | |||||||||||||

| Distributions from net realized gains | (0.85 | ) | (0.09 | ) | — | — | — | |||||||||||||

| Total distributions | (0.85 | ) | (0.09 | ) | — | (0.03 | ) | (0.03 | ) | |||||||||||

| Proceeds from redemption fees collected | 0.00 | (a) | — | — | 0.00 | (a) | 0.00 | (a) | ||||||||||||

| Net asset value, end of year | $ | 20.81 | $ | 17.55 | $ | 16.11 | $ | 15.41 | $ | 13.26 | ||||||||||

TOTAL RETURN (b) | 24.45% | 9.57% | 4.54% | 16.47% | 13.05% | |||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of year (000’s) | $ | 112,828 | $ | 87,664 | $ | 88,602 | $ | 93,266 | $ | 85,000 | ||||||||||

Ratio of expenses to average net assets (c) | 1.43% | 1.46% | 1.42% | 1.40% | 1.41% | |||||||||||||||

Ratio of net investment income (loss) to average net assets (c) (d) | (0.00% | ) | (0.05% | ) | (0.25% | ) | (0.20% | ) | 0.27% | |||||||||||

| Portfolio turnover | 28% | 7% | 60% | 10% | 4% | |||||||||||||||

| (a) | Amount rounds to less than $0.01 per share. |

| (b) | Total return is a measure of the change in the value of an investment in the Portfolio over the years covered, which assumes dividends or capital gains distributions, if any, are reinvested in shares of the Portfolio. Returns shown do not reflect the taxes a shareholder would pay on Portfolio distributions, if any, or the redemption of Portfolio shares. |

| (c) | The ratios of expenses and net investment income (loss) to average net assets do not reflect the Portfolio’s proportionate share of expenses of the underlying investment companies in which the Portfolio invests (Note 2). |

| (d) | Recognition of net investment income (loss) by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests (Note 2). |

See accompanying notes to financial statements.

26

NEW CENTURY BALANCED PORTFOLIO FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | ||||||||||||||||||||

Years Ended October 31, | ||||||||||||||||||||

2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| PER SHARE OPERATING PERFORMANCE | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 14.56 | $ | 13.59 | $ | 13.22 | $ | 11.93 | $ | 10.54 | ||||||||||

| Income from investment operations: | ||||||||||||||||||||

| Net investment income | 0.18 | 0.17 | 0.20 | 0.15 | 0.22 | |||||||||||||||

Net realized and unrealized gains on investments | 2.12 | 0.97 | 0.37 | 1.30 | 1.39 | |||||||||||||||

| Total from investment operations | 2.30 | 1.14 | 0.57 | 1.45 | 1.61 | |||||||||||||||

| Less distributions: | ||||||||||||||||||||

| Distributions from net investment income | (0.18 | ) | (0.17 | ) | (0.20 | ) | (0.16 | ) | (0.22 | ) | ||||||||||

| Proceeds from redemption fees collected | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | — | — | ||||||||||||

| Net asset value, end of year | $ | 16.68 | $ | 14.56 | $ | 13.59 | $ | 13.22 | $ | 11.93 | ||||||||||

TOTAL RETURN (b) | 15.97% | 8.54% | 4.29% | 12.23% | 15.57% | |||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of year (000’s) | $ | 71,457 | $ | 66,826 | $ | 64,582 | $ | 64,880 | $ | 61,578 | ||||||||||

Ratio of expenses to average net assets (c) | 1.43% | 1.45% | 1.43% | 1.44% | 1.45% | |||||||||||||||

Ratio of net investment income to average net assets (c) (d) | 1.17% | 1.18% | 1.39% | 1.20% | 2.07% | |||||||||||||||

| Portfolio turnover | 21% | 13% | 17% | 7% | 13% | |||||||||||||||

| (a) | Amount rounds to less than $0.01 per share. |

| (b) | Total return is a measure of the change in the value of an investment in the Portfolio over the years covered, which assumes dividends or capital gains distributions, if any, are reinvested in shares of the Portfolio. Returns shown do not reflect the taxes a shareholder would pay on Portfolio distributions, if any, or the redemption of Portfolio shares. |

| (c) | The ratios of expenses and net investment income to average net assets do not reflect the Portfolio’s proportionate share of expenses of the underlying investment companies in which the Portfolio invests (Note 2). |

| (d) | Recognition of net investment income by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests (Note 2). |

See accompanying notes to financial statements.

27

NEW CENTURY INTERNATIONAL PORTFOLIO FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | ||||||||||||||||||||

Years Ended October 31, | ||||||||||||||||||||

2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| PER SHARE OPERATING PERFORMANCE | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 13.92 | $ | 13.41 | $ | 14.53 | $ | 12.70 | $ | 10.08 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income | 0.11 | 0.15 | 0.10 | 0.09 | 0.13 | |||||||||||||||

Net realized and unrealized gains (losses) on investments | 2.37 | 0.46 | (1.14 | ) | 1.82 | 2.61 | ||||||||||||||

| Total from investment operations | 2.48 | 0.61 | (1.04 | ) | 1.91 | 2.74 | ||||||||||||||

| Less distributions: | ||||||||||||||||||||

| Distributions from net investment income | (0.16 | ) | (0.10 | ) | (0.08 | ) | (0.08 | ) | (0.12 | ) | ||||||||||

| Proceeds from redemption fees collected | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | ||||||||||

| Net asset value, end of year | $ | 16.24 | $ | 13.92 | $ | 13.41 | $ | 14.53 | $ | 12.70 | ||||||||||

TOTAL RETURN (b) | 17.95% | 4.60% | (7.22% | ) | 15.07% | 27.45% | ||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of year (000’s) | $ | 62,708 | $ | 57,266 | $ | 61,262 | $ | 68,947 | $ | 89,449 | ||||||||||

Ratios of expenses to average net assets (c) | 1.43% | 1.50% | 1.46% | 1.45% | 1.44% | |||||||||||||||

Ratios of net investment income to average net assets (c) (d) | 0.67% | 1.03% | 0.63% | 0.57% | 1.23% | |||||||||||||||

| Portfolio turnover | 32% | 4% | 13% | 4% | 11% | |||||||||||||||

| (a) | Amount rounds to less than $0.01 per share. |

| (b) | Total return is a measure of the change in the value of an investment in the Portfolio over the years covered, which assumes dividends or capital gains distributions, if any, are reinvested in shares of the Portfolio. Returns shown do not reflect the taxes a shareholder would pay on Portfolio distributions, if any, or the redemption of Portfolio shares. |

| (c) | The ratios of expenses and net investment income to average net assets do not reflect the Portfolio’s proportionate share of expenses of the underlying investment companies in which the Portfolio invests (Note 2). |

| (d) | Recognition of net investment income by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests (Note 2). |

See accompanying notes to financial statements.

28

NEW CENTURY ALTERNATIVE STRATEGIES PORTFOLIO FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | ||||||||||||||||||||

Years Ended October 31, | ||||||||||||||||||||

2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| PER SHARE OPERATING PERFORMANCE | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 12.24 | $ | 11.80 | $ | 11.87 | $ | 11.11 | $ | 10.14 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income | 0.05 | 0.14 | 0.17 | 0.08 | 0.14 | |||||||||||||||

Net realized and unrealized gains (losses) on investments | 0.80 | 0.47 | (0.09 | ) | 0.83 | 1.15 | ||||||||||||||

| Total from investment operations | 0.85 | 0.61 | 0.08 | 0.91 | 1.29 | |||||||||||||||

| Less distributions: | ||||||||||||||||||||

| Distributions from net investment income | (0.07 | ) | (0.17 | ) | (0.15 | ) | (0.15 | ) | (0.32 | ) | ||||||||||

| Proceeds from redemption fees collected | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | ||||||||||

| Net asset value, end of year | $ | 13.02 | $ | 12.24 | $ | 11.80 | $ | 11.87 | $ | 11.11 | ||||||||||

TOTAL RETURN (b) | 6.99% | 5.26% | 0.62% | 8.21% | 13.16% | |||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of year (000’s) | $ | 123,411 | $ | 117,272 | $ | 114,841 | $ | 135,287 | $ | 139,168 | ||||||||||

Ratio of expenses to average net assets (c) | 1.13% | 1.11% | 1.09% | 1.10% | 1.06% | |||||||||||||||

Ratio of net investment income to average net assets (c) (d) | 0.39% | 1.15% | 1.48% | 0.74% | 1.46% | |||||||||||||||

| Portfolio turnover | 25% | 32% | 31% | 22% | 27% | |||||||||||||||

| (a) | Amount rounds to less than $0.01 per share. |

| (b) | Total return is a measure of the change in the value of an investment in the Portfolio over the years covered, which assumes dividends or capital gains distributions, if any, are reinvested in shares of the Portfolio. Returns shown do not reflect the taxes a shareholder would pay on Portfolio distributions, if any, or the redemption of Portfolio shares. |

| (c) | The ratios of expenses and net investment income to average net assets do not reflect the Portfolio’s proportionate share of expenses of the underlying investment companies in which the Portfolio invests (Note 2). |

| (d) | Recognition of net investment income by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests (Note 2). |

See accompanying notes to financial statements.

29

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS October 31, 2013 |

| (1) | SIGNIFICANT ACCOUNTING POLICIES |

New Century Portfolios (“New Century”) is organized as a Massachusetts business trust which is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company and currently offers shares of four series: New Century Capital Portfolio, New Century Balanced Portfolio, New Century International Portfolio and New Century Alternative Strategies Portfolio (together, the “Portfolios” and each, a “Portfolio”). New Century Capital Portfolio and New Century Balanced Portfolio commenced operations on January 31, 1989. New Century International Portfolio commenced operations on November 1, 2000, and New Century Alternative Strategies Portfolio commenced operations on May 1, 2002.

Weston Financial Group, Inc. (the “Adviser”), a wholly-owned subsidiary of The Washington Trust Company, serves as the investment adviser to each Portfolio. Weston Securities Corporation (the “Distributor”), a wholly-owned subsidiary of Washington Trust Bancorp, Inc., serves as the distributor and principal underwriter to each Portfolio.

On February 28, 2013, New Century Capital Portfolio consummated a tax-free merger with New Century Opportunistic Portfolio, a former series of New Century. Pursuant to the terms of the merger agreement, each share of New Century Opportunistic Portfolio was converted into an equivalent dollar amount of shares of New Century Capital Portfolio, based on each Portfolio’s respective net asset value as of February 28, 2013 ($11.52 and $18.03, respectively), resulting in each share of New Century Opportunistic Portfolio receiving 0.638960 shares of New Century Capital Portfolio. New Century Capital Portfolio issued 708,515 shares to shareholders of New Century Opportunistic Portfolio. Net assets of New Century Capital and New Century Opportunistic Portfolios as of the merger date were $92,126,682 and $12,773,191, respectively, including unrealized appreciation on investments of $26,607,892 and $3,792,313, respectively. In addition, New Century Opportunistic Portfolio’s net assets included accumulated net realized capital losses on investments of $1,123,635. Total net assets of New Century Capital Portfolio immediately after the merger were $104,899,873.

The investment objective of New Century Capital Portfolio is to provide capital growth, with a secondary objective to provide income, while managing risk. This Portfolio seeks to achieve its objective by investing primarily in shares of other registered investment companies, including exchange traded funds (“ETFs”), that emphasize investments in equity securities (domestic and foreign).

The investment objective of New Century Balanced Portfolio is to provide income, with a secondary objective to provide capital growth, while managing risk. This Portfolio seeks to achieve its objective by investing primarily in shares of other registered investment companies, including ETFs, that emphasize investments in equity securities (domestic

30

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

and foreign), fixed income (domestic and foreign), or in a composite of such securities. This Portfolio maintains at least 25% of its assets in fixed income securities by selecting registered investment companies that invest in such securities.

The investment objective of New Century International Portfolio is to provide capital growth, with a secondary objective to provide income, while managing risk. This Portfolio seeks to achieve its objective by investing primarily in shares of registered investment companies, including ETFs, that emphasize investments in equity and fixed income securities (foreign, worldwide, emerging markets and domestic).

The investment objective of New Century Alternative Strategies Portfolio is to provide long-term capital appreciation, with a secondary objective to earn income, while managing risk. This Portfolio seeks to achieve its objective by investing primarily in shares of other registered investment companies, including ETFs, and closed-end funds, that emphasize alternative strategies.

The price of shares of each Portfolio fluctuates daily and there is no assurance that the Portfolios will be successful in achieving their stated investment objectives.

The following is a summary of significant accounting policies consistently followed by the Portfolios in the preparation of their financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

| A. | Investment Valuation |

Investments in shares of other open-end investment companies are valued at their net asset value as reported by such companies. The net asset value as reported by open-end investment companies may be based on fair value pricing; to understand the fair value pricing process used by such companies, consult their most current prospectus. The Portfolios may also invest in closed-end investment companies, exchange-traded funds, and to a certain extent, directly in securities when the Adviser deems it appropriate. Investments in closed-end investment companies, exchange-traded funds and direct investments in securities are valued at market prices, as described in the paragraph below.

Investments in securities traded on a national securities exchange or included in NASDAQ are generally valued at the last reported sales price, the closing price or the official closing price; and securities traded in the over-the-counter market and listed securities for which no sale is reported on that date are valued at the last reported bid price. It is expected that fixed income securities will ordinarily be traded in the over-the-counter market. When market quotations are not readily available, fixed income securities may be valued on the basis of prices provided by an independent pricing service. Other assets and securities for which no quotations are readily available or for which quotations the Adviser believes do not reflect market value are valued at their fair value as determined in good faith by the Adviser under the procedures established by the Board of Trustees, and will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Factors considered

31

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

in determining the value of portfolio investments subject to fair value determination include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; infrequency of sales; thinness of market; the size of reported trades; a temporary lapse in the provision of prices by any reliable pricing source; and actions of the securities or future markets, such as the suspension or limitation of trading. Short term investments (those with remaining maturities of 60 days or less) may be valued at amortized cost which approximates market value.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements. Various inputs are used in determining the value of the Portfolios’ investments. These inputs are summarized in the three broad levels listed below:

| • | Level 1 – quoted prices in active markets for identical securities |

| • | Level 2 – other significant observable inputs |

| • | Level 3 – significant unobservable inputs |

For example, Structured Notes held by the New Century Alternative Strategies Portfolio are typically classified as Level 2 since the values for such securities are customarily based on prices provided by an independent pricing service that utilizes various “other significant observable inputs” including bid and ask quotations, prices of similar securities, underlying index values and interest rates, among other factors.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level of the fair value hierarchy within which the fair value measurement of that security is determined to fall in its entirety is the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value each Portfolio’s investments by security type as of October 31, 2013:

| New Century Capital Portfolio | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Investment Companies | $ | 111,931,566 | $ | — | $ | — | $ | 111,931,566 | ||||||||

Money Market Funds | 2,544,729 | — | — | 2,544,729 | ||||||||||||

Total | $ | 114,476,295 | $ | — | $ | — | $ | 114,476,295 | ||||||||

| New Century Balanced Portfolio | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Investment Companies | $ | 70,226,602 | $ | — | $ | — | $ | 70,226,602 | ||||||||

Money Market Funds | 1,338,159 | — | — | 1,338,159 | ||||||||||||

Total | $ | 71,564,761 | $ | — | $ | — | $ | 71,564,761 | ||||||||

32

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

| New Century International Portfolio | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Investment Companies | $ | 62,298,418 | $ | — | $ | — | $ | 62,298,418 | ||||||||

Money Market Funds | 278,696 | — | — | 278,696 | ||||||||||||

Total | $ | 62,577,114 | $ | — | $ | — | $ | 62,577,114 | ||||||||

| New Century Alternative Strategies Portfolio | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Investment Companies | $ | 115,861,199 | $ | — | $ | — | $ | 115,861,199 | ||||||||

Structured Notes | — | 4,869,960 | — | 4,869,960 | ||||||||||||

Money Market Funds | 3,478,464 | — | — | 3,478,464 | ||||||||||||

Total | $ | 119,339,663 | $ | 4,869,960 | $ | — | $ | 124,209,623 | ||||||||

Refer to each Portfolio’s schedule of investments for a listing of the securities valued using Level 1 and Level 2 inputs. As of October 31, 2013, the Portfolios did not have any transfers in and out of any Level. In addition, the Portfolios did not have derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of October 31, 2013. It is the Portfolios’ policy to recognize transfers into and out of any Level at the end of the reporting period.

| B. | Share Valuation |

The net asset value per share of each Portfolio is calculated daily by dividing the total value of each Portfolio’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of each Portfolio is equal to the net asset value per share, except that shares of each Portfolio are subject to a redemption fee of 2% if redeemed within 30 days of the date of purchase. This redemption fee applies to all shareholders and accounts; however, each Portfolio reserves the right to waive such redemption fees on employer sponsored retirement accounts. No redemption fee is imposed on the exchange of shares among the various Portfolios of the Trust, the redemption of shares representing reinvested dividends or capital gain distributions, or on amounts representing capital appreciation of shares. During the years ended October 31, 2013 and 2012, proceeds from redemption fees totaled $724 and $0, respectively, for New Century Capital Portfolio, $1 and $545, respectively, for New Century Balanced Portfolio, $3 and $179, respectively, for New Century International Portfolio and $2,722 and $5,870, respectively, for New Century Alternative Strategies Portfolio. Any redemption fees collected are credited to paid-in capital of the applicable Portfolio.

| C. | Investment Transactions |

Investment transactions are recorded on a trade date basis for financial reporting purposes. Gains and losses on securities sold are determined on a specific identification method.

33

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

| D. | Income Recognition |

Interest, if any, is accrued on portfolio investments daily. Dividend income and capital gain distributions are recorded on the ex-dividend date or as soon as the information is available if after the ex-date.

| E. | Distributions to Shareholders |

Dividends arising from net investment income, if any, are declared and paid semi-annually to shareholders of New Century Balanced and New Century Alternative Strategies Portfolios. Dividends from net investment income, if any, are declared and paid annually to shareholders of New Century Capital and New Century International Portfolios. Net realized short-term capital gains, if any, may be distributed throughout the year and net realized long-term capital gains, if any, are distributed annually. Income distributions and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

The tax character of distributions paid during the years ended October 31, 2013 and October 31, 2012 was as follows:

Years Ended | Ordinary Income | Long-Term Capital Gains | Total Distributions | |||||||||

| New Century Capital Portfolio | ||||||||||||

October 31, 2013 | $ | — | $ | 4,174,787 | $ | 4,174,787 | ||||||

October 31, 2012 | $ | — | $ | 497,600 | $ | 497,600 | ||||||

| New Century Balanced Portfolio | ||||||||||||

October 31, 2013 | $ | 794,645 | $ | — | $ | 794,645 | ||||||

October 31, 2012 | $ | 828,337 | $ | — | $ | 828,337 | ||||||

| New Century International Portfolio | ||||||||||||

October 31, 2013 | $ | 642,497 | $ | — | $ | 642,497 | ||||||

October 31, 2012 | $ | 434,898 | $ | — | $ | 434,898 | ||||||

| New Century Alternative Strategies Portfolio | ||||||||||||

October 31, 2013 | $ | 668,997 | $ | — | $ | 668,997 | ||||||

October 31, 2012 | $ | 1,636,766 | $ | — | $ | 1,636,766 | ||||||

| F. | Cost of Operations |

The Portfolios bear all costs of their operations other than expenses specifically assumed by the Adviser. Expenses directly attributable to a Portfolio are charged to that Portfolio; other expenses are allocated proportionately among the Portfolios in relation to the net assets of each Portfolio.

34

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

| G. | Use of Estimates |

In preparing financial statements in accordance with GAAP, management is required to make estimates and assumptions that affect the reported amount of assets and liabilities, the disclosure of contingent assets and liabilities, and revenues and expenses during the reporting period. Actual results could differ from those estimates.

| (2) | INVESTMENT ADVISORY FEES, ADMINISTRATIVE AGREEMENT AND TRUSTEES’ FEES |

Each Portfolio has a separate Investment Advisory Agreement with the Adviser. Investment advisory fees for each Portfolio are computed daily and paid monthly. The investment advisory fees for New Century Capital, New Century Balanced and New Century International Portfolios are computed at an annualized rate of 1.00% (100 basis points) on the first $100 million of average daily net assets and 0.75% (75 basis points) of average daily net assets exceeding that amount. The investment advisory fees for New Century Alternative Strategies Portfolio are computed at an annualized rate of 0.75% (75 basis points) of average daily net assets.

The Adviser has contractually agreed to limit the total expenses (excluding interest, taxes, brokerage, acquired fund fees and expenses and extraordinary expenses) to an annual rate of 1.50% of average net assets for each of the Portfolios. The total expenses do not include a Portfolio’s proportionate share of expenses of the underlying investment companies (i.e. acquired fund fees and expenses) in which such Portfolio invests. This contractual agreement is in place until March 1, 2014. During the fiscal year ended October 31, 2013, no such reduction of advisory fees was necessary with respect to any Portfolio.

Any advisory fee reductions and/or any other operating expenses absorbed by the Adviser pursuant to the expense limitation agreement shall be reimbursed by the Portfolio to the Adviser, if so requested by the Adviser, provided the aggregate amount of the Portfolio’s current total operating expenses for such year does not exceed the applicable existing limitation on Portfolio expenses, and the reimbursement is made within three years after the year in which the Adviser incurred the expense.

Fees paid by the Portfolios pursuant to an Administration Agreement with the Adviser to administer the ordinary course of the Portfolios’ business are paid monthly based on actual expenses incurred in the overseeing of the Portfolios’ affairs.

The Portfolios pay each Trustee who is not affiliated with the Adviser a $16,000 annual retainer, paid quarterly, and a per meeting fee of $5,000. The Portfolios will also pay each Trustee who is not affiliated with the Adviser a $5,000 special meeting fee if held independently of a regularly scheduled meeting. Any Trustee who is affiliated with the Adviser and any officer of New Century does not receive compensation from the Portfolios at this time.

35

NEW CENTURY PORTFOLIOS NOTES TO FINANCIAL STATEMENTS (Continued) October 31, 2013 |

| (3) | DISTRIBUTION PLAN AND OTHER TRANSACTIONS WITH RELATED PARTIES |

The Portfolios have adopted a Distribution Plan (the “Plan”) under Section 12(b) of the Investment Company Act of 1940 and Rule 12b-1 thereunder. Under the Plan, each Portfolio may pay up to 0.25% (25 basis points) of its average daily net assets to the Distributor for activities primarily intended to result in the sale of shares. Under its terms, the Plan shall remain in effect from year to year, provided such continuance is approved annually by a vote of a majority of the Trustees and a majority of those Trustees who are not “interested persons” of the Portfolios and who have no direct or indirect financial interest in the operation of the Plan or in any agreement related to the Plan.

During the year ended October 31, 2013, the Distributor received $239,677, $128,113, $107,550 and $218,046 from New Century Capital, New Century Balanced, New Century International and New Century Alternative Strategies Portfolios, respectively, pursuant to the Plan. As described below, these net amounts were offset by the sales commissions and other compensation received by the Distributor.