UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| OR |

| | |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| OR |

| | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the transition period April 1, 2002 to December 31, 2002 |

Commission File Number 0-17551

DYNAMIC OIL & GAS, INC.

(formerly Dynamic Oil Limited)

(Exact name of Registrant as specified in its charter)

Province of British Columbia (Canada)

(Jurisdiction of incorporation or organization)

205 - 10711 Cambie Road

Richmond, British Columbia V6X 3G5, Canada

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock Without Par Value

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report:

| Title of Each Class | Outstanding at December 31, 2002 |

| Common Stock Without Par Value | 20,272,530 Shares |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YesX No

Indicate by check mark which financial statement item the Company has elected to follow. Item 17.X Item 18.

1

TABLE OF CONTENTS

| | | Page | |

| | | | |

| Glossary of Terms..................................................................................................................................... | 3 | |

| | | | |

| Part I. | | | |

| | | | |

| Item 1. | Identity of Directors, Senior Management and Advisers......................................... | 6 | |

| | | | |

| Item 2. | Offer Statistics and Expected Timetable................................................................... | 6 | |

| | | | |

| Item 3. | Key Information.......................................................................................................... | 6 | |

| | | | |

| Item 4. | Our Information.......................................................................................................... | 14 | |

| | | | |

| Item 5. | Operating and Financial Review and Prospects........................................................ | 33 | |

| | | | |

| Item 6. | Directors, Senior Management and Employees....................................................... | 46 | |

| | | | |

| Item 7. | Major Shareholders and Related Party Transactions.............................................. | 56 | |

| | | | |

| Item 8. | Financial Information................................................................................................. | 56 | |

| | | | |

| Item 9. | The Offer and Listing................................................................................................. | 57 | |

| | | | |

| Item 10. | Additional Information............................................................................................... | 58 | |

| | | | |

| Item 11. | Quantitative and Qualitative Disclosures About Market Risk............................... | 66 | |

| | | | |

| Item 12. | Description of Securities Other than Equity Securities........................................... | 69 | |

| | | | |

| | | | |

| Part II. | | | |

| | | | |

| Item 13. | Defaults, Dividend Arrearages and Delinquencies.................................................. | 69 | |

| | | | |

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds... | 69 | |

| | | | |

| Item 15. | Controls and Procedures............................................................................................ | 69 | |

| | | | |

| Item 16. | [Reserved]................................................................................................................... | 70 | |

| | | | |

| Item 16(A). | Audit Committee Financial Expert............................................................................. | 70 | |

| | | | |

| Item 16(B). | Code of Ethics............................................................................................................. | 70 | |

| | | | |

| Item 16(C). | Principal Accountant Fees and Services.................................................................... | 70 | |

| | | | |

| | | | |

| | | | |

| Part III. | | | |

| | | | |

| Item 17. | Financial Statements................................................................................................... | 70 | |

| | | | |

| Item 18. | Financial Statements................................................................................................... | 71 | |

| | | | |

| Item 19. | Exhibits......................................................................................................................... | 71 | |

2

| Glossary of Terms | |

|

|

| Air drilling | A method of drilling that uses compressed air as a medium for transporting drill cuttings to surface. |

|

|

| Basal Quartz zone | A name generally applied to the Ellerslie formation as it occupies the “bottom” sandstone of the Mannville Group of lower Cretaceous age about 124 millions years of age. |

|

|

| Bbl or Barrel | 42 U.S. gallons liquid volume of crude oil or natural gas liquids. |

|

|

| Bcf | Billion cubic feet of gas. Usual expression of proved reserve gas volume. |

|

|

| Belly River formation | Late Cretaceous Age sandstones and shales deposited from 75 to 84 million years ago. |

|

|

| Blairmore formation | Formation encompassing clastic sediments deposited in the Early Cretaceous Age from about 100 to 120 million years ago. |

|

|

| Blue Sky formation | Sandstones of the Lower Cretaceous, about 112 million years old, occurring in Northern Alberta and NE BC. |

|

|

| BOE | Barrels of Oil Equivalent. Generally one barrel of oil equals six mcf of gas. Allows reserves of oil and gas to be added together. |

|

|

| BOE/d | An expression of barrels of oil equivalent produced per day. |

|

|

| Carbonates | Rocks composed predominantly of Calcium Carbonate (CaCO3). |

|

|

| Condensate | A mixture comprising pentanes and heavier hydrocarbons recovered as a liquid from field separators, scrubbers or other gathering facilities or at the inlet of a processing plant before the gas is processed. |

|

|

| Cretaceous Age | Rocks from 144 million to 66.4 million years of age. |

|

|

| Crown royalty | An amount payable to the government of the applicable Canadian province in relation to the production of petroleum, natural gas or related hydrocarbons from an oil or gas well located on Crown lands. |

|

|

| Crude oil | A mixture, consisting mainly of pentanes and heavier hydrocarbons that may contain sulphur compounds, that is liquid at the conditions under which its volume is measured or estimated, but excluding such liquids obtained from the processing of natural gas. |

|

|

| Depletion | The reduction in petroleum reserves due to production. |

|

|

| Development or developed | Refers to the phase in which a proven oil or gas field is brought into production by drilling and completing production wells and the wells, in most cases, are connected to a petroleum gathering system. |

|

|

| Devonian Age | Rocks from 408 million to 360 million years of age. |

|

|

| Discovery | The location, learned through drilling of a well, where there exists an accumulation of gas, condensate or oil reserves. The size of the reserves may be estimated but not precisely quantified and may or may not be commercially economic, depending on a number of factors. |

|

|

| Drill stem test | A method of packing off the pressure of drilling mud weight to allow a prospective oil or gas formation to flow into the drill stem pipe. Drill stem test results assist in evaluating the potential of the zone to flow or to be pumped commercially. |

|

|

| Dry hole | A well drilled without finding commercially economic quantities of hydrocarbons. |

|

|

| Ellerlsie zone or formation | A name applied to a group of sandstones that are clear and quartzose with good porosity and permeability for oil and gas about 124 millions years of age. |

|

|

| Exploration well | A well drilled in a prospect without knowledge of the underlying sedimentary rock or the contents of the underlying rock. |

|

|

| Farmin | By way of agreement, a party earns (farmin) an interest in lands comprising petroleum and natural gas rights from another party by drilling a well or similar activity that evaluates, explores or develops the lands for the production of petroleum substances. |

|

|

| Farmout | By way of agreement, a party gives up (farmout) an interest in lands comprising petroleum and natural gas rights to another party who earns the interest by drilling a well or similar activity that evaluates, explores or develops the lands for the production of petroleum substances. |

|

|

| Field | An area that is producing, or has been proven to be capable of producing, hydrocarbons. |

|

|

| Field netbacks | Revenues from the sale of all commodities produced, less applicable resource and production royalties, less operating costs. |

|

|

| Formation | A reference to a group of rocks of the same age extending over a substantial area of a basin. |

|

|

3

|

|

| Freehold royalty | An amount payable to a mineral rights holder in relation to the production of petroleum, natural gas or related hydrocarbons from an oil or gas well located on non-Crown lands. |

|

|

| GAAP | Generally accepted accounting principles. |

|

|

| Geology | The science relating to the history and development of the Earth. |

|

|

| Glauconite | A sand group from the Upper Mannville (Lower Cretaceous Age) about 110 million years ago with a green mineral constituent. |

|

|

| Gross acres | The total acreage in which the Company has an interest. |

|

|

| Hackett formation | A sand package that occurs at the base of the Mannville Formation (Lower Cretaceous Age), 118 to 120 million years old. |

|

|

| Hectare | A land measurement equaling 2.471 acres. |

|

|

| Horizontal well | A vertical well bore that is gradually deviated (usually horizontally to 90o) in order to intersect the targeted formation. |

|

|

| Hydrocarbon | The general term for oil, gas, condensate, liquids and other petroleum products. |

|

|

| Jean Marie formation | A patch reef carbonate reservoir within the Winterburn Group of the Upper Devonian Age, about 367 to 369 million years old. The Jean Marie is found in NE British Columbia and is the stratigraphic equivalent to the lower Nisku formation in Alberta. |

|

|

| kilometer | A measurement of distance equaling 0.621 miles or 3,281 feet. |

|

|

| Leduc (D-3) formation | A reefal carbonate reservoir found within Woodbend Group of the Upper Devonian Age, about 369 to 373 million years old. These ancient Leduc reefs were the initial target for oil and gas exploration in Alberta. Leduc No. 1, approximately 30 km. South of St. Albert, was the discovery well for conventional oil in Western Canada. |

|

|

| Logs | Recordings from electrical and radioactive source devices that are run down wellbores to measure petrophysical properties of the adjacent rocks. |

|

|

| Lower Mannville gas | Any gas sands found in the lower half of the Lower Cretaceous Age zones, about 110 million years old. These sands may comprise the Ostracod, Basal Quartz or Ellerlsie zones. |

|

|

| mbbl | 1,000 barrels of oil and/or natural gas liquids. |

|

|

| mboe | 1,000 barrels of oil equivalent. See ‘BOE’ for further details. |

|

|

| mcf | 1,000 cubic feet of natural gas. |

|

|

| mcf/d | 1,000 cubic feet of natural gas production per day. Usually used to express the production rate of a group of gas wells. |

|

|

| meter | A physical measurement equaling 3.281 feet. |

|

|

| Mineral taxes (freehold) | An amount levied by the government of Alberta in relation to the production of petroleum, natural gas or related hydrocarbons from an oil or gas well located on non-government (freehold) lands in Alberta. |

|

|

| mmcf | 1,000,000 cubic feet of natural gas. |

|

|

| mmcf/d | 1,000,000 cubic feet of natural gas production per day. Usually used to express the production rate of a gas well or group of gas wells. |

|

|

| Natural gas | The lighter hydrocarbons and associated non-hydrocarbon substances occurring naturally in an underground reservoir, which under atmospheric conditions are essentially a gas, but that may contain liquids. |

|

|

| NGL’s | Natural gas liquids. Hydrocarbon components recovered from raw natural gas as liquids by processing through extraction plants or recovered from field separators, scrubbers or other gathering facilities. These liquids include the hydrocarbon components ethane, propane, butane and pentane plus, or combinations thereof. |

|

|

| Net acres | The percentage of gross acreage in which the Company has a working interest. |

|

|

| Nisku (D-2) formation | A reefal carbonate reservoir in the Winterburn Group of the Upper Devonian Age, about 367 to 369 million years old. The Nisku is found exclusively within Alberta but it is a stratigraphic equivalent to the Jean Marie formation in British Columbia. |

|

|

| Ostracod zone | Rocks from the Lower Cretaceous Age approximately 119 million years ago comprised of sandstones and marlstones that contain a small fossil named Ostracod. |

|

|

| Ostracod well | A gas well capable of producing commercially from the Lower Cretaceous Age Ostracod zone. |

|

|

| Operator | That party to a joint venture agreement whose responsibility it is to carry out all exploratory, development, maintenance and record-keeping duties on behalf of other joint venture partners in relation to hydrocarbon extraction on the joint-ventured lands. |

|

|

| Overriding royalty | An amount payable to a third party other than crown or freehold in relation to the |

|

|

4

|

|

| | production of petroleum, natural gas or related hydrocarbons from an oil or gas well located on lands in which the interest of the third party usually arises out of a separate agreement. |

|

|

| Pentanes | A hydrocarbon by-product of natural gas generally referred to as condensate that is of the paraffin series having a chemical formula of C5H12 and having all its carbon atoms joined in a straight chain. |

|

|

| Permeability | Capacity of a rock for transmitting a fluid. |

|

|

| Permit or licence area | An area that is granted for a prescribed period of time for exploration, development or production under specific contractual or legislative conditions. |

|

|

| Pipeline | A system of interconnected pipes that gather and transport hydrocarbons from a well or field to a processing plant or to a facility that is built to take the hydrocarbons for further transport, such as a gas liquefaction plant. |

|

|

| Probable reserves | Those reserves that analysis of drilling, geological, geophysical and engineering data do not demonstrate to be proved with current technology and under existing economic conditions, but where such analysis suggests the likelihood of their existence and future recovery. Probable reserves to be obtained will be the increased recovery beyond estimated proved reserves that can be realistically estimated for the pool through enhanced recovery processes that can reasonably be expected to be instituted in the future. |

|

|

| Proved reserves | Those reserves estimated as recoverable with current technology and under existing economic conditions, from that portion of a reservoir that can be reasonably evaluated as economically productive through analysis of drilling, geological, geophysical and engineering data. This includes the reserves to be obtained by enhanced recovery processes demonstrated to be economically and technically successful in the subject reservoir. |

|

|

| Quartzose | Rocks composed of mostly quartz. |

|

|

| Raw gas | Gaseous effluent from a wellhead or pipeline that is not processed. Contains water vapor, carbon dioxide, nitrogen and possibly hydrogen sulphide (H2S) gas. |

|

|

| Reservoir rock | Porous limestones, dolomites or sandstones that can trap oil and/or gas in interconnected holes, like a sponge. |

|

|

| Royalty | A stated or determinable percentage of the proceeds received from the sale of hydrocarbons calculated as prescribed in applicable legislation or in the agreement with the royalty holder. |

|

|

| Seals | Impermeable barriers to hydrocarbon flow such as shale, lime muds, salt or anhydrite. |

|

|

| Seismic | A geophysical technique using low frequency sound waves to determine the subsurface structure of sedimentary rocks. |

|

|

| Sour gas | Raw gas with an amount of hydrogen sulphide (H2S) gas above pipeline requirements of 10 parts H2S per million raw gas. |

|

|

| Source rock | Usually shales and clays with a high carbon content deposited in a marine environment. |

|

|

| Sweet gas | Natural gas containing no hydrogen sulphide (H2S) gas. |

|

|

| Stabilized absolute open flow | The maximum rate of gas production that a wellhead will produce assuming no backpressure when the well is stable. |

|

|

| Tertiary sediment | Soft rock of sands, clays, coals and siltstones from 66.4 to 1.6 million years old. |

|

|

| Undeveloped | Prior to the time in which a proven oil or gas field is brought into production by drilling and completing production wells. |

|

|

| Vertical well | A well bore that intersects the section(s) containing hydrocarbons at about 90o. |

|

|

| Viking gas well | A well capable of commercial gas production from the Upper Cretaceous Viking sands deposited about 97.5 million years ago. |

|

|

| Wabamun (D-1) formation | Cyclical ramp carbonates deposited approximately 360 – 367 million years ago during the Upper Devonian Age period. |

|

|

| Working interest | Those lands in which the Company receives its share acreage net production revenues. |

|

|

5

Part I.

Prior to this filing, our most recently filed annual report covered the twelve-month period ended March 31, 2002. Since then, we changed our fiscal year end to December 31. This report covers the nine-month transition period from April 1, 2002 to December 31, 2002. Where useful for comparison purposes, annualized numbers are presented by applying the nine-month transition numbers multiplied by four-thirds. However, this method does not reflect actual results for the three-month extrapolated period and such results may differ from the result achieved by this calculation. Also, for ease of reading, we may refer to nine-month period ended December 31, 2002 as “Nine-Month Fiscal Transition 2002”; the 12-month period ended March 31, 2002 as “Fiscal 2002”; and the 12-month period ended March 31, 2001 as “Fiscal 2001”.

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

Selected Financial Data

The following tables summarize certain of our financial information that is derived from and should be read in conjunction with our financial statements and “Item 5 – Operating and Financial Review and Prospects” included elsewhere in this Transition Report. The selected financial data has been prepared in accordance with Canadian Generally Accepted Accounting Principles (Canadian GAAP). The financial statements and the notes thereto included in Item 17 in this Transition Report are also prepared under Canadian GAAP. Included in Note 12 to the financial statements is the reconciliation between Canadian GAAP and United States generally accepted accounting principles (U.S. GAAP). Unless otherwise stated in this Transition Report, all references to dollars are to Canadian dollars.

Selected Financial Data Presented According to Canadian GAAP

|

|

|

|

|

|

|

|

|

| |

| | As at | | | | | | | | | |

| | December 31 | | | | As at March 31 | |

|

|

|

|

|

|

|

|

|

| |

| ($ 000’s) | 2002 | | 2002 | | 2001 | | 2000 | | 1999 | |

|

|

|

|

|

|

|

|

|

| |

| Balance Sheets | | | | | | | | | | |

| Working capital (deficiency) | (16,818 | ) | (13,281 | ) | 1,969 | | (3,716 | ) | (1,225 | ) |

| Total assets | 43,647 | | 37,152 | | 29,991 | | 18,811 | | 12,487 | |

| Current liabilities | 23,729 | | 19,625 | | 6,210 | | 7,717 | | 3,950 | |

| Long-term liabilities | 991 | | 824 | | 540 | | 402 | | 404 | |

| Deferred gain on sale | - | | 109 | | 340 | | 652 | | 997 | |

| Future income tax liability | 682 | | - | | 2,955 | | - | | - | |

| Net assets | 18,245 | | 16,593 | | 19,947 | | 10,041 | | 7,136 | |

| Share capital | 20,721 | | 20,915 | | 20,642 | | 20,420 | | 21,080 | |

| Deficit | (2,476 | ) | (4,322 | ) | (695 | ) | (10,379 | ) | (13,944 | ) |

|

|

|

|

|

|

|

|

|

| |

6

|

|

|

|

|

|

|

|

|

| |

| | Nine-Month | | | | | | | | | |

| | Fiscal | | | | | | | | | |

| | Transition | | For the 12-month period ended March 31 | |

|

|

|

|

|

|

|

|

|

| |

| ($ 000’s) | 2002 | | 2002 | | 2001 | | 2000 | | 1999 | |

|

|

|

|

|

|

|

|

|

| |

| Statements of Operations | | | | | | | | | | |

| Gross revenues | 24,123 | | 26,402 | | 34,463 | | 15,770 | | 9,495 | |

| Net revenues | 13,309 | | 14,215 | | 20,524 | | 7,438 | | 3,857 | |

| Cash flow from operations1 | 10,723 | | 11,337 | | 18,168 | | 5,634 | | 2,634 | |

| Cash flow per share, basic ($) | 0.53 | | 0.55 | | 0.91 | | 0.29 | | 0.13 | |

| Cash flow per share, diluted ($) | 0.52 | | 0.55 | | 0.89 | | 0.28 | | 0.13 | |

| Earnings (loss) before taxes | 3,146 | | (5,419 | ) | 14,449 | | 2,871 | | 1,212 | |

| Net earnings (loss) | 1,978 | | (3,519 | ) | 9,714 | | 4,079 | | 1,212 | |

| Common shares – weighted avg. (# 000’s) | 20,357 | | 20,365 | | 19,938 | | 19,710 | | 19,892 | |

| Net (loss) earnings per share, basic ($) | 0.10 | | (0.17 | ) | 0.49 | | 0.21 | | 0.06 | |

| Net (loss) earnings per share, diluted ($) | 0.10 | | (0.17 | ) | 0.48 | | 0.20 | | 0.06 | |

| (1) | Cash flow from operations is a non-GAAP measure that does not have standardized meaning as prescribed by GAAP and is therefore unlikely to be comparable to similar measures presented by other companies. We consider it a key measure as it demonstrates our ability to generate the cash flow necessary to fund future growth through capital investment and to repay debt. Below is the determination of the non-GAAP measure by utilizing existing GAAP measures. |

| | | Nine- | | | | | | | | | |

| | | Month | | | | | | | | | |

| | | Fiscal | | | | | | | | | |

| | | Transition | | % | | Fiscal | | % | | | |

| | ($ 000’s) | 2002 | | Chg | | 2002 | | Chg | | Fiscal 2001 | |

| |

|

|

|

|

|

|

|

|

|

| |

| | Cash flow from operating activities (GAAP measure) | 11,370 | | 16 | | 9,779 | | (49 | ) | 19,264 | |

| | Changes in non-cash working capital (GAAP measure) | (647 | ) | (142 | ) | 1,559 | | 242 | | (1,096 | ) |

| |

|

|

|

|

|

|

|

|

|

| |

| | Cash flow from operations (non-GAAP measure) | 10,723 | | (5 | ) | 11,337 | | (38 | ) | 18,168 | |

| |

|

|

|

|

|

|

|

|

|

| |

Selected Financial Data Presented According to U.S. GAAP

The following tables show the major differences in the application of Canadian GAAP and U.S. GAAP.

|

|

|

|

|

|

|

|

|

| |

| | As at | | | | | | | | | |

| | December 31 | | | | As at March 31 | |

|

|

|

|

|

|

|

|

|

| |

| ($ 000’s) | 2002 | | 2002 | | 2001 | | 2000 | | 1999 | |

|

|

|

|

|

|

|

|

|

| |

| | | | | | | | | | | |

| After adjusting for certain differences, selected balance sheet items under U.S. GAAP would become: | | | | | | | | | | |

| | | | | | | | | | | |

| Balance Sheets | | | | | | | | | | |

| Future income tax asset | - | | 371 | | - | | 242 | | - | |

| Future income tax liability | 541 | | - | | 3,532 | | - | | - | |

| Natural gas and oil interests | 36,236 | | 30,150 | | 21,679 | | 13,721 | | 9,702 | |

| Share capital* | 21,694 | | 21,883 | | 21,610 | | 21,368 | | 21,802 | |

| Deficit | (1,640 | ) | (5,422 | ) | (2,356 | ) | (11,473 | ) | (14,896 | ) |

|

|

|

|

|

|

|

|

|

| |

| * | For further explanation of the reconciling adjustments shown below, see Note 12 attached to the Financial Statements presented under Item 17 to this Transition Report. |

7

|

|

|

|

|

|

|

|

|

| |

| | Nine-Month | | | | | | | | | |

| | Fiscal | | | | | | | | | |

| | Transition | | For the 12-month period ended March 31 | |

|

|

|

|

|

|

|

|

|

| |

| ($ 000’s) | 2002 | | 2002 | | 2001 | | 2000 | | 1999 | |

|

|

|

|

|

|

|

|

|

| |

| Statements of Operations | | | | | | | | | | |

| Net (loss) earnings under Canadian GAAP | 1,978 | | (3,519 | ) | 9,714 | | 4,079 | | 1,212 | |

| Reconciling adjustments* | | | | | | | | | | |

| Compensatory stock options issued | - | | - | | - | | - | | (8 | ) |

| Options issued for services | (5 | ) | - | | (20 | ) | - | | - | |

| Ceiling test adjustment to natural gas properties | (332 | ) | (216 | ) | - | | (145 | ) | - | |

| Income taxes | 141 | | 669 | | (577 | ) | - | | - | |

| Net (loss) earnings under U.S. GAAP | 1,782 | | (3,066 | ) | 9,117 | | 3,934 | | 1,204 | |

| Net (loss) earnings/share, U.S. GAAP basic ($) | 0.09 | | (0.15 | ) | 0.46 | | 0.20 | | 0.06 | |

| Net (loss) earnings/share, U.S. GAAP diluted ($) | 0.09 | | (0.15 | ) | 0.45 | | 0.19 | | 0.06 | |

Dividends

We have never paid or declared dividends on our shares of common stock and we do not intend to do so in the foreseeable future. We intend to use our retained earnings to finance growth.

Exchange Rates

Our financial statements, as provided under Items 8 and 17, are presented in Canadian dollars. For comparison purposes, exchange rates into U.S. dollars (the host country currency) are provided. The following tables set forth the exchange rate as of the latest practicable date, high and low exchange rates for the months indicated and the average exchange rates for the reporting periods indicated, based on the noon U.S. dollar buying rate in New York City for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York (Canadian Dollar = U.S. $1.00).

Exchange Rates for Canadian Versus U.S. Dollars

The exchange rate as of May 5, 2003 was CDN $1.4134 per U.S. $1.00.

| Exchange Rates for Canadian Versus U.S. Dollars | | | | |

| (High/low rates for latest six months) | High | | Low | |

|

|

|

| |

| April, 2003 | 1.4843 | | 1.4336 | |

| March, 2003 | 1.4905 | | 1.4659 | |

| February, 2003 | 1.5303 | | 1.4928 | |

| January, 2003 | 1.5750 | | 1.5220 | |

| December, 2002 | 1.5800 | | 1.5478 | |

| November , 2002 | 1.5903 | | 1.5528 | |

|

|

|

| |

| Exchange Rates for Canadian Versus U.S. Dollars | | | |

| | | Average ($) | |

|

|

|

|

| For the nine-month period ended December 31 | | | |

| 2002 | | 1.56 | |

| For the twelve-month periods ended March 31 | | | |

| 2002 | | 1.57 | |

| 2001 | | 1.50 | |

| 2000 | | 1.47 | |

| 1999 | | 1.50 | |

|

|

|

|

8

Capitalization and Indebtedness

Not applicable.

Reasons for the Offer and Use of Proceeds

Not applicable.

Risk Factors

Business Risk Management

The natural gas and oil industry is highly competitive, particularly in the following areas:

| | • | searching for and developing new reserves of natural gas and crude oil; |

| | • | constructing pipelines and facilities required to transport or process produced commodities, and |

| | • | operating facilities related to the production of natural gas and crude oil. |

Our competitors include major integrated oil and gas companies and numerous other independent oil and gas companies.

Commodity Price Fluctuations

Our products, including natural gas, NGL’s and oil, and other hydrocarbon products, are commodities. Because our contracts do not fix a long-term price for the products we purchase or sell, market changes in the price of such products have a direct and immediate effect (whether favorable or adverse) upon our revenues and profitability. Prices for products may be subject to material change in response to relatively minor changes in supply and demand, general economic conditions and other market conditions over which we have no control. Other conditions affecting our business include the level of domestic oil and gas production, the availability and prices of competing commodities and of alternative energy sources, the availability of local, intraprovincial and interprovincial transportation systems with adequate capacity, the proximity of gas production to gas pipelines and facilities, the availability of pipeline capacity, government regulation, the seasons, the weather and the impact of energy conservation efforts.

Availability of Natural Gas Supply

We must connect new wells to our gathering systems, contract for new natural gas supplies with third party pipelines or acquire additional gathering systems in order to maintain or increase throughput levels to offset current annual production volumes. Historically, while certain individual facilities have experienced decreases in dedicated reserves, we have connected new wells and contracted for new supplies with third-party pipelines that more than offset production depletion of our existing wells. Our ability to connect new wells to existing facilities is dependent upon levels of our oil and gas development activity near existing facilities. Significant competition for connections to newly drilled wells exists in every geographic area served by us. Significant competition also exists for the acquisition of existing gathering systems. There can be no assurance that we will renew our existing supply contracts or that we will be able to acquire new supplies of natural gas at a rate necessary to offset depletion of wells currently under contract. In the event such circumstances were to occur, our field netbacks would decrease until, and if, such circumstances could be resolved.

Dependence on Third Party Pipelines

In Nine-Month Fiscal Transition 2002, substantially all our sales of natural gas were effected through deliveries to local third-party gathering systems to processing plants in Alberta owned by ATCO Midstream Ltd. and Northwestern Utilities Limited. In addition, we rely on access to interprovincial pipelines for the sale and distribution of substantially all of our gas. As a result, a curtailment of our sale of natural gas by pipelines or by third-party gathering systems, an impairment of our ability to transport natural gas on interprovincial pipelines or a material increase in the rates charged to us for the transportation of natural gas by reason of a change in federal or provincial regulations or for any other reason, could have a material adverse effect upon us. In such event, we would have to obtain other transportation arrangements or we would have to construct alternative pipelines. There can be no assurance that we would have economical transportation alternatives or that it would be feasible for us to construct pipelines. In the event such circumstances were to occur, our field netbacks from the affected wells would be suspended until, and if, such circumstances could be resolved.

9

Operating History and Significant Historical Operating Losses

We commenced operations in 1979. We have one major property, that began as a one-well producing property in 1985. By fiscal 1999, the property became our major producing property with up to twenty-four producing natural gas and oil wells. Due to the relatively short five-year production history from the majority of wells on the property, proved reserves and future production attributable to this property are somewhat more susceptible to estimation discrepancies than fields with longer production histories.

We first experienced earnings in fiscal 1999 of $1,211,638. In fiscal 2000 and Fiscal 2001, we reported earnings of $4,078,577 and $9,714,030 respectively and in Fiscal 2002, we returned to a loss of $3,519,085. In Nine-Month Fiscal Transition 2002, we again reported earnings of $1,977,663. As at December 31, 2002, we had an accumulated deficit of $2,475,932. Our future viability should be considered in light of the risks and difficulties frequently encountered by companies engaged in the junior stages of oil and gas exploration, development and production activities.

Dependence on Key Personnel

Our success depends in large part on the personal efforts of our President & Chief Executive Officer, Wayne J. Babcock, our Vice President & Chief Operating Officer, Donald K. Umbach, our Vice President of Exploration, James R. Britton, our Vice-President of Operations, David G. Grohs and our Chief Financial Officer & Corporate Secretary, Michael A. Bardell. The loss of the services of any of these persons could have a material adverse effect on us.

Risks Pertaining to Acquisitions and Joint Ventures

Part of our business strategy is to expand through acquisitions and is therefore dependent upon our ability to complete suitable acquisitions and effectively integrate acquired assets into our operations. Suitable acquisitions, on terms acceptable to us, may not be available in the future or may require us to assume certain liabilities, including, without limitation, environmental liabilities, known or unknown.

Potential Variability in Quarterly Operating Results

Demand for our products will generally increase during the winter because they are often used as heating fuels. The amount of such increased demand will depend to some extent upon the severity of winter. Accordingly, our net operating revenues are likely to increase during winter months although the amount of increase and its effect on profitability cannot be predicted. Because of the seasonality of our business and continuous fluctuations in the prices of our products, our operating results for any past quarterly period may not necessarily be indicative of results for future periods and there can be no assurance that we will be able to maintain steady levels of profitability on a quarterly or annual basis in the future.

Dependence on One Major Property

Currently, our major producing asset is our property located at St. Albert, Alberta. While the St. Albert property as of December 31, 2002 has developed into 16 separate, mutually-exclusive oil and gas pools stacked in 7 productive formations (4 natural gas and 3 crude oil), each pool has its own reserves and future production risk, and thus it is important for us to establish producing fields in other areas. Unless we can successfully drill for or acquire economically viable reserves of natural gas and crude oil in other areas, as our production depletes the reserves at St. Albert, our revenue may be materially adversely affected.

Limited Financial Resources

We expect to continue to produce enough cash flow, along with our bank credit facility, to support land acquisitions, drilling operations, facilities construction and general /administration costs. At this time, we believe that our cash flow and credit facility will be sufficient to support our business activities without securing significant additional financing in the near future. If it were to become necessary to raise significant additional financing, any arrangements that may be entered into could be expensive to us. There can be no assurance that we will be able to raise additional capital in light of factors such as the market demand for our securities, the state of financial markets for independent oil companies (including the markets for debt), oil and gas prices and general market conditions. (See "Operating and Financial Review and Prospects" for a discussion of our capital budget).

10

We expect to continue using our bank credit facility to borrow funds to supplement our available cash. The amount we may borrow under the credit facility may not exceed a borrowing base determined by the lender based on its projections of our future production, future costs of production, taxes, commodity prices and other factors. We cannot control the assumptions the lender uses to calculate the borrowing base. The lender may, without our consent, adjust the borrowing base at any time. If our borrowings under the credit facility exceed the borrowing base, the lender may require that we repay the excess. If this were to occur, we may have to sell assets or seek financing from other sources. We can make no assurances that we would be successful in selling assets at prices acceptable to us or arranging substitute financing. For a description of our bank credit facility and its principal terms and conditions, see "Operating and Financial Review and Prospects” under Item 5, and Note 4 attached to the Financial Statements under Item 17 of this Transition Report.

Exploration and Development Risks

Exploration and development of natural gas and oil involves a high degree of risk that no commercial production will be obtained or that the production will be insufficient to recover drilling and completion costs. The costs of drilling, completing and operating wells is sometimes uncertain, and cost overruns in exploration and development operations can adversely affect the economics of a project. Our drilling operations may be curtailed, delayed or canceled as a result of numerous factors, including title problems, equipment failures, weather conditions, marine accidents, fires and explosions, compliance with governmental requirements, and shortages or delays in the delivery of equipment. Furthermore, completion of a well does not ensure a profit on the investment or a recovery of drilling, completion and tie-in costs.

We have historically invested a significant portion of our capital budget in drilling exploratory wells in search of unproved oil and gas reserves. We cannot be certain that the exploratory wells we drill will be productive or that we will recover all or any portion of our investments. In order to increase the chances for exploratory success, we often invest in seismic or other geoscience data to assist us in identifying potential drilling objectives. Additionally, the cost of drilling, completing and testing exploratory wells is often uncertain at the time of our initial investment. Depending on complications encountered while drilling, the final cost of the well may significantly exceed that which we originally estimated.

Operating Hazards and Uninsured Risks

The oil and gas business involves a variety of operating risks, including fire, explosion, pipe failure, casing collapse, abnormally pressured formations, and environmental hazards such as oil spills, gas leaks and discharges of toxic gases. The occurrence of any of these events with respect to any property operated or owned (in whole or in part) by us could have a material adverse impact on us. We, and the operators of our properties, maintain insurance in accordance with customary industry practices and in amounts that we believe to be reasonable. However, insurance coverage is not always economically feasible and is not obtained to cover all types of operational risks. The occurrence of a significant event that is not fully insured could have a material adverse effect on our financial condition.

Operating Risk

Exploring and developing for natural gas and crude oil involves many risks, some of which are:

| | • | unexpected formations or pressures; |

| | • | equipment failures and other accidents; |

| | • | uncontrolled hydrocarbon releases; |

| | • | adverse weather conditions; |

| | • | government and political actions; |

| | • | premature reservoir declines, and |

| | • | environmental impacts. |

Although we maintain customary industry insurance, we cannot fully insure against all of these risks. Losses resulting from the occurrence of these risks could have a material adverse impact.

As our reserves of natural gas, natural gas liquids and crude oil decline, our success at replacing and adding to them is highly reliant on further exploration and development. To the extent we succeed, our operating cash flows and other capital sources may become insufficient so as to impair our ability to re-invest capital.

11

Drilling Plans Subject to Change

This Transition Report includes descriptions of our future drilling plans with respect to our prospects. A prospect is a property on which our geoscientists have identified what they believe, based on available seismic and geological information, to be indications of hydrocarbons. Our prospects are in various stages of review. Whether or not we ultimately drill a prospect may depend on the following factors: receipt of additional seismic data or reprocessing of existing data; material changes in oil or gas prices; the costs and availability of drilling equipment; success or failure of wells drilled in similar formations or which would use the same production facilities; availability and cost of capital; changes in the estimates of costs to drill or complete wells; our ability to attract other industry partners to acquire a portion of the working interest to reduce exposure to costs and drilling risks; decisions of our joint working interest owners; and restrictions imposed by governmental agencies. We will continue to gather data about our prospects, and it is possible that additional information may cause us to alter our drilling schedule or determine that a prospect should not be pursued at all.

Replacement of Reserves

In general, the rate of production from natural gas and oil properties declines as reserves are depleted. The rate of decline depends on reservoir characteristics and other factors. Except to the extent we acquire properties containing proved reserves or conduct successful exploration and development activities, or both, our estimated proved reserves will decline as reserves are produced. Our future natural gas and oil production, and therefore cash flow and income, are highly dependent upon our level of success in finding or acquiring additional economically recoverable reserves. The business of exploring for, developing and acquiring reserves is capital intensive. To the extent cash flow from operations is reduced and external sources of capital become limited or unavailable, our ability to make the necessary capital investment to maintain or expand our asset base of natural gas and oil reserves could be materially impaired.

Dependence on Few Customers

During Nine-Month Fiscal Transition 2002, our natural gas sales were sold to three customers and, our natural gas liquids and crude oil between three customers who are different than our natural gas customers. We do not believe that the loss of one of our customers would have a material adverse effect on us because of the availability of other customers willing or interested in purchasing our products.

Estimating of Reserves and Future Net Cash Flows Risk

Estimating natural gas, natural gas liquids and crude oil reserves, and future net cash flows includes numerous uncertainties, many of which may be beyond our control. Such estimates are essential in our decision-making, as to whether further investment is warranted. These estimates are derived from several factors and assumptions, some of which are:

| | • | reservoir characteristics based on variable geological, geophysical and engineering assessments; |

| | • | future rates of production based on historical draw-down rates; |

| | • | future net cash flows based on commodity price/quality assumptions, production costs, taxes and investment decisions; |

| | • | recoverable reserves based on estimated future net cash flows, and |

| | • | compliance expectations based on assumed federal, provincial and environmental laws and regulations. |

Ultimately, actual production rates, reserves recovered, commodity prices, production costs, government regulation or taxation may differ materially from those assumed in earlier reserve estimates. Higher or lower differences could materially impact our production, revenues, production costs, depletion expense, taxes and capital expenditures.

Our reserve estimates and net present values reported in the Review of Operations section of this Transition Report are based on estimated constant commodity prices and associated production costs as of the estimate date. Actual future prices and costs may be materially higher or lower.

12

Shortage of Supplies and Equipment

Our ability to conduct operations in a timely and cost effective manner is subject to the availability of natural gas and crude oil field supplies, rigs, equipment and service crews. Although none are expected currently, any shortage of certain types of supplies and equipment could result in delays in our operations as well as in higher operating and capital costs.

Restoration, Safety and Environmental Risk

All our operations are in western Canada and, in particular, the western provinces of Alberta and British Columbia. Certain laws and regulations exist that require companies engaged in petroleum activities to obtain necessary safety and environmental permits to operate. Such legislation may restrict or delay us from conducting operations in certain geographical areas. Further, such laws and regulations may impose liability on us for remedial and clean-up costs, personal injuries related to safety and environmental damages.

To ensure that we provide for future estimated removal and site restoration costs, we recognized $0.2 million in our Statement of Operations and Deficit during Nine-Month Fiscal Transition 2002, bringing our total recognized amount in our December 31, 2002 Balance Sheet to $1.0 million. We engage independent engineering consultants to assist in assessing our total future liabilities related to removal and clean-up costs. While we cannot predict their ultimate cost, we currently estimate the future cost to clean up all our operating facilities to be $2.1 million.

While our safety and environmental activities have been prudent and have enabled us to operate successfully in managing such risks, there can be no assurance that we will always be successful in protecting ourselves from the impact of all such risks. Consistent with our growth in other areas, we seek opportunities for performance improvement in our operating practices.

Government Regulation and Environmental Matters

We are subject to various federal and provincial laws and regulations including environmental laws and regulations. We believe that we are in substantial compliance with such laws and regulations, however, such laws and regulations may change in the future in a manner that will increase the burden and cost of compliance. In addition, we could incur significant liability for damages, cleanup costs and penalties in the event of certain discharges into the environment.

Certain laws and governmental regulations may impose liability on us for personal injuries, clean-up costs, environmental damages and property damages, as well as administrative, civil and criminal penalties. We maintain limited insurance coverage for sudden and accidental environmental damages, but do not maintain insurance coverage for the full potential liability that could be caused by sudden and accidental environmental damage. Accordingly, we may be subject to liability or may be required to cease production from properties in the event of such damages.

The main bodies of regulations that apply to us in the areas in which we have significant field operations are The Oil and Gas Conservation Act of Alberta and The Petroleum and Natural Gas Act of British Columbia.

Kyoto Protocol Risk

The Kyoto Protocol treaty (Protocol) was established to reduce emissions of greenhouse gases (GHG) that are believed to contribute to increasing Earth’s surface temperatures and affecting the global climate change. Canada adopted the Kyoto Protocol in December 1997. The Protocol establishes commitments to reduce GHG internationally and Canada has committed to meet a 6% reduction over base-year 1990 during the period 2008 to 2012. While we believe we are a low-emission producer, it is not possible for us to predict the impact of how Protocol-related issues will ultimately be resolved and to what extent their impact will affect our future unit operating costs and capital expenditures.

Interruption From Severe Weather

Presently, our operations are conducted principally in the central region of Alberta and the northeastern region of British Columbia. The weather during colder seasons in these areas can be extreme and can cause interruption or delays in our drilling and construction operations.

13

Competition

The natural gas and oil industry is highly competitive. We experience competition in all aspects of our business, including acquiring reserves, leases, licenses and concessions, obtaining the equipment and labor needed to conduct operations and market natural gas and oil. Our competitors include multinational energy companies, other independent natural gas and oil concerns and individual producers and operators. Because both natural gas and oil are fungible commodities, the principal form of competition with respect to product sales is price competition. Many competitors have financial and other resources substantially greater than those available to ours and, accordingly, may be better positioned to acquire and exploit prospects, hire personnel and market production. In addition, many of our larger competitors may be better able to respond to factors such as changes in worldwide natural gas or oil prices or levels of production, the cost and availability of alternative fuels or the application of government regulations. Such factors, which are beyond our control, may affect demand for our natural gas and oil production. We expect a high degree of competition to continue.

Item 4. Our Information

Our History and Development

Dynamic Oil & Gas, Inc. (formerly Dynamic Oil Limited) was incorporated under the Company Act of the Province of British Columbia, Canada on March 27, 1979. We have one wholly-owned, inactive subsidiary incorporated in Texas, called Seabird Oil & Gas, Inc.

Our principal executive office is located in rented space at Suite 205-10711 Cambie Road, Richmond, British Columbia V6X 3G5 Canada until May 26, 2003; after which date, our rented space will be at Suite 230-10991 Shellbridge Way, Richmond, British Columbia V6X 3C6. Our telephone number will remain (800) 663-8072.

Principal Capital Expenditures and Exploration Expenses Over the Past Three Reporting Periods

Capital Expenditures

Over the past three reporting periods our capital expenditures aggregated $46.3 million, an amount that is broken down by reporting period and spending category in the following table.

| | Nine-Month Fiscal | | % | | | | % | | | |

| ($000’s) | Transition 2002 | | chg | | Fiscal 2002 | | chg | | Fiscal 2001 | |

|

|

|

|

|

|

|

|

|

| |

| Drilling, completions, tie-ins | 9,146 | | 19 | | 7,678 | | 106 | | 6,939 | |

| Facilities | 780 | | (56 | ) | 1,757 | | (50 | ) | 3,522 | |

| Land acquisitions | 2,568 | | (80 | ) | 12,560 | | 1105 | | 1,042 | |

| Corporate office | 84 | | (28 | ) | 116 | | 47 | | 79 | |

|

|

|

|

|

|

|

|

|

| |

| Total | 12,578 | | (43 | ) | 22,111 | | 91 | | 11,582 | |

|

|

|

|

|

|

|

|

|

| |

In the table above, the total aggregated amount of $46.3 million is itemized further by reporting period as follows:

Nine-Month Fiscal Transition 2002

Our capital expenditures were $12.6 million in Nine-Month Fiscal Transition 2002, a 43% decrease from the amount invested in Fiscal 2002. The main reason for this decrease was due to the acquisition of additional working interests at St. Albert during Fiscal 2002 that were not repeated in Nine-Month Fiscal Transition 2002. In Nine-Month Fiscal Transition 2002, we invested as follows:

| | • | 48% in Alberta development properties to maintain and grow existing production levels; and |

| | • | 52% in British Columbia exploration properties for potential longer-term production growth. |

| | | |

| | We invested our capital in the following specific areas: |

| | Alberta |

| | • | Exploration - drilling, completions and tie-ins totalled $0.2 million, most of which was spent at Halkirk; |

14

| | • | Development of core properties – drilling, completions and tie-ins totalled $3.9 million, 74% of which was spent at St. Albert and 26% at Halkirk; |

| | • | Facilities - $0.8 million to acquire an increased interest in gas processing facilities at St. Albert pursuant to a Sale and Leaseback arrangement, as described in Note 5 to our Financial Statements; and |

| | • | Land – acquisitions totalled $1.2 million, 94% of which was to purchase various working and royalty interests at St. Albert. |

| | British Columbia |

| | • | Exploration – drilling, completions and tie-ins totaled $5.0 million, all of which was spent in the Cypress/Chowade area; and |

| | • | Land - acquisitions totalled $1.4 million, 90% of which was spent at Orion. |

| | | |

| | Fiscal 2002 |

| | We invested our capital in the following specific areas: |

| | Alberta |

| | • | Exploration and Development – drilling, completions and tie-ins totalled $7.7 million, of which 95% was spent at St. Albert; and |

| | • | Facilities and Land – totalled $14.4 million, most of which was spent to acquire additional working interests at St. Albert. |

| | | |

| | Fiscal 2001 |

| | We invested our capital in the following specific areas: |

| | Alberta |

| | • | Exploration and Development – drilling, completions and tie-ins totaled $5.7 million, 53% of which was spent at St. Albert and the balance at Peavey/Morinville; and |

| | • | Facilities and Land – totalled $4.6 million, most of which was spent at Peavey/Morinville and Halkirk. |

| | British Columbia |

| | • | Exploration and Development – drilling, completions and tie-ins totalled $1.3 million, all of which was spent at Orion. |

Exploration Expenses

Our Exploration Expenses are mainly comprised of costs for seismic, new property investigations and unsuccessful drilling attempts. Under our ‘successful efforts’ accounting policy, we reclassify costs for unsuccessful drilling attempts from capital expenditures to exploration expenses. Over the past three reporting periods our exploration expenses aggregated $7.9 million, an amount that is broken down by reporting period and spending category in the following table.

| | Nine Month Fiscal | | % | | | | % | | | |

| ($ 000’s) | Transition 2002 | | chg | | Fiscal 2002 | | chg | | Fiscal 2001 | |

|

|

|

|

|

|

|

|

|

| |

| Drilling | 325 | | (91 | ) | 3,821 | | 472 | | 668 | |

| Seismic data activity | 847 | | 31 | | 649 | | (41 | ) | 1,102 | |

| Other | 187 | | 6 | | 176 | | 14 | | 153 | |

|

|

|

|

|

|

|

|

|

| |

| Total | 1,359 | | (71 | ) | 4,646 | | 142 | | 1,923 | |

|

|

|

|

|

|

|

|

|

| |

In the table above, the total aggregated amount of $7.9 million is itemized further as follows:

| | • | $4.8 million on unsuccessful drilling attempts; |

| | • | $2.6 million on conducting seismic surveys or acquiring seismic survey data; and |

| | • | $0.5 million on investigating new properties. |

15

Capital Expenditures and Exploration Expenses Anticipated in 2003

The capital portion of our 2003 budget is $23.7 million. We plan to invest this capital as follows:

| | • | $8.7 million or 37% in Alberta to maintain and grow production levels on existing core properties; |

| | • | $4.8 million or 20% in British Columbia to bring into production a new core property; |

| | • | $2.8 million or 12% in Alberta to explore for new reserves; |

| | • | $6.5 million or 27% in British Columbia to explore new frontier properties; and |

| | • | $0.9 million or 4% other. |

Of the total budget amount, $10.8 million is for drilling, $6.1 million for new land acquisitions, $5.4 million for completions and tie-ins and $1.4 million for facilities.

Our drilling program for 2003 includes 20 wells, 14 of which are new and six re-entries. Of the 14 new wells, seven are planned for exploratory work in northeast British Columbia, three for exploratory and four for development work in Alberta.

This program is consistent with our strategy to grow reserves and production through the drill bit and is our largest-ever capital spending budget.

The exploration expense portion of our 2003 budget is $2.8 million. It is for the acquisition of 3D and 2D seismic data in areas of Alberta and British Columbia as yet to be resolved.

We expect funds for our capital expenditure and exploration expense plans for 2003 to be sourced from cash flow from our operations and from our bank credit facility (see Note 4 to the Financial Statements under Item 17 in this Transition Report and Liquidity and Capital Resources under Item 5). In the event that our funding sources are insufficient to accomplish the expenditure and exploration plans for 2003, we will be forced to curtail certain of such expenditures.

Recent Material Events

We have no recent material events to report.

Share Repurchases

During the last three reporting periods, we spent $0.7 million on the re-purchase and cancellation of over 0.4 million of our outstanding shares of common stock at prices ranging from $1.54 to $1.72 per share.

Business Overview

General

Our principal business is acquiring, exploring and developing natural gas and crude oil properties. Our natural gas and crude oil properties are located in the Canadian provinces of Alberta, British Columbia and Saskatchewan. Over each of the past three years, we have explored for, produced and marketed natural gas, natural gas liquids and crude oil. We intend to continue this type of business activity.

Concentration of Commodities

We derive our revenue principally from the sale of natural gas, natural gas liquids and crude oil. As a result, our revenues are determined, to a large degree, by prevailing spot prices for natural gas, natural gas liquids and crude oil. The market prices for our commodities are dictated by supply and demand. Accordingly, our cash flow from operations and earnings will be greatly affected by changes in prices for natural gas, natural gas liquids and crude oil. We will experience reduced cash flows and may experience operating losses when prices for natural gas, natural gas liquids and crude oil are low (see Item 5 Operating and Financial Review Prospects and Item 11 Quantitative and Qualitative Disclosures About Market Risk).

16

Under extreme circumstances, our commodity sales may not generate sufficient revenue to meet our financial obligations and to fund planned capital expenditures. Moreover, significant price decreases could negatively affect our reserves by reducing the quantities of reserves that are recoverable on an economic basis, necessitating write-downs to reflect the realizable value of the reserves in the lower-price environment.

We are unable to control the market prices for natural gas, natural gas liquids and crude oil. Such market prices depend on numerous factors that include:

| | • | the extent of domestic production and exportation of natural gas, natural gas liquids and crude oil; |

| | • | the proximity of pipelines or other economically-feasible transportation; |

| | • | the availability of pipeline capacity; |

| | • | the demand for natural gas, natural gas liquids and crude oil by utilities and other end users; |

| | • | the availability of alternative fuel sources; |

| | • | the effects of weather variability; and |

| | • | the effects of regulations pertaining to the transporting, marketing and exporting of natural gas, natural gas liquids and crude oil within Canada. |

Because of these and other factors, we may be unable to market all of the natural gas, natural gas liquids and crude oil that we have available for sale. Additionally, we may be unable to obtain favorable prices for the natural gas, natural gas liquids and crude oil that we produce.

Concentration of Operations

Our main producing property is located at St. Albert, Alberta. Of our total production in Nine-Month Fiscal Transition 2002, 85% came from the St. Albert property. The remainder originated from six other Alberta fields: Halkirk, Peavey/Morinville, Alexander, Simonette, Stanmore and Westlock. In Fiscal 2002, 84% of our production came from the St. Albert field, while the remainder came from six other fields: Peavey/Morinville, Halkirk, Westlock, Simonette and Stanmore. In Fiscal 2001, 82% of our production came from the St. Albert field, while the remainder originated from five other fields: Peavey/Morinville, Westlock, Simonette, Redwater and Stanmore.

Revenue Breakdown

Our total revenue for the past three reporting periods was $85.0 million. Of this total, 78% came from the sales of natural gas, 17% came from the sales of natural gas liquids and 5% came from the sales of crude oil. Additionally, virtually all of such revenue originated from our properties and interests in the Province of Alberta. The breakdown for each of the past three reporting periods is shown in the table below:

Natural Gas, Natural Gas Liquids and Crude Oil Revenue

The following table shows our natural gas, natural gas liquids and crude oil revenue for the periods presented.

| | Nine Month Fiscal | | % | | | | % | | | |

| ($ 000’s) | Transition 2002 | | chg | | Fiscal 2002 | | chg | | Fiscal 2001 | |

|

|

|

|

|

|

|

|

|

| |

| Natural gas | 17,058 | | (19 | ) | 20,944 | | (25 | ) | 28,006 | |

| Natural gas liquids | 4,012 | | (10 | ) | 4,442 | | (25 | ) | 5,935 | |

| Crude oil | 3,053 | | 200 | | 1,016 | | 95 | | 522 | |

|

|

|

|

|

|

|

|

|

| |

| Total | 24,123 | | (9 | ) | 26,402 | | (23 | ) | 34,463 | |

|

|

|

|

|

|

|

|

|

| |

Seasonality and Raw Materials

The seasonality of our main revenue-generating commodity, natural gas, is affected solely by the North American climate. Typically, there are two ‘peak’ seasons and two corresponding ‘shoulder’ seasons for natural gas sales. Winter is generally the higher-demand period due to cold-weather heating requirements. The summer is the next highest period of demand due to hot-weather air conditioning requirements.

Natural gas is becoming increasingly important as an energy source to power natural gas-fired electric power

17

generating facilities (co-gen facilities). We believe that as more co-gen facilities are approved, constructed and put into operation, the demand for natural gas during shoulder seasons will remain relatively strong.

We do not rely on the availability of raw materials,because we operate in an extractive industry.

Marketing

Natural gas -Our natural gas portfolio is split between two primary markets, one is the Alberta Spot Market that trades at the AECO storage hub (www.encanastorage.com/), the other is an aggregator pool called ProGas (www.progas.com).

AECO, an intra-Alberta trading hub, offers producers the opportunity to participate in natural gas transactions for terms of one day, one month, summer and winter blocks, and annually. We are currently selling our uncommitted natural gas volumes into the AECO daily spot market, however, our marketing strategy includes securing monthly and term deals, if optimal.

ProGas, a wholly-owned subsidiary of BP Canada, ‘aggregates’ supplies of natural gas to sell into a basket of daily, short term (less than one year) and long-term contracts, both domestic and export. Producers realize a netback price for their natural gas, which is a blend of all contract types weighted toward NYMEX-based prices.

During Nine-Month Fiscal Transition 2002, we sold 51% of our natural gas to ProGas and 49% into the AECO daily spot market. During Fiscals 2002 and 2001, we sold 53% and 77% to ProGas, respectively, and the balances to AECO.

Natural gas liquids and crude oil -We market our natural gas liquids and crude oil based on monthly prices posted by the major purchasers at Edmonton, Alberta. These prices correlate closely to the price of West Texas Intermediate, allowing for quality adjustments and location differentials.

Supply Contracts or Agreements

Under various supply contracts and agreements, the commitment period under which we are required to supply natural gas and natural gas liquids, ranges from terminable within thirty days notice to no termination prior to exhaustion of hydrocarbon reserves. Under these various contracts and agreements, we are not obligated to provide a fixed quantity of supply, as all supply is on a best-efforts basis.

Competition

Presently, we regularly compete with other companies in bidding for the acquisition of petroleum interests from the Alberta and British Columbia governments and other corporations or individuals holding such interests. Further, we regularly compete for the availability of drilling rigs, production equipment, processing facilities, pipeline capacity and other transportation services. We do not have a competitive position that allows us any material or significant advantages compared to other companies within the same industry. Many competitors have substantially greater financial and other resources than we do. For example, in the 2002 Canadian Energy Survey of 2001 Results prepared by PriceWaterhouseCoopers, we ranked thirty-sixth and thirty-fifth in size out of one hundred Canadian exploration and production companies according to gross revenues and cash flow from operations, respectively.

Governmental Regulations

Government regulations have a material effect on us to the extent that they require us to conduct field operations and hydrocarbon extraction activities within prescribed environmentally-safe, sensitive regulations. Also, government regulations may restrict the commencement or re-commencement of field activities in certain properties in which we hold an interest for the purpose of exploration. Examples of types of governmental laws and regulations that may have a material effect on our business include:

| | • | requirements to acquire permits before commencement of drilling operations; |

| | • | the proximity of hydrocarbon pipelines or other economically-feasible transportation; |

| | • | requirements to restrict the substances that can be released into the environment in connection with drilling and production activities; |

| | • | limitations on, or prohibitions to, drilling in protected areas such as offshore areas; and |

| | • | requirements to mitigate and remediate the effects caused by drilling and production operations. |

18

Properties, Plant and Equipment

We own interests in certain properties located in the Western Provinces of Canada. For purposes of identification, discussion and differentiation, we have named them based on their location. They are as follows:

| Central Alberta | British Columbia | Southern Saskatchewan |

|

|

|

|

| St. Albert | Stanmore | Cypress (northeastern B.C.) | Elmore |

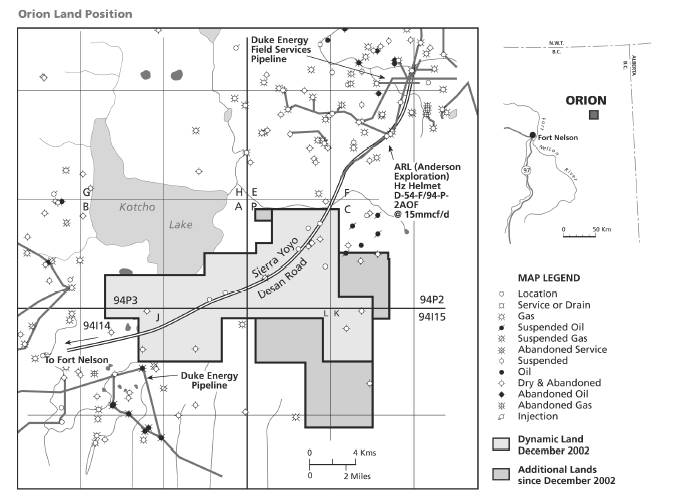

| Halkirk | Westlock | Orion (northeastern B.C.) | Rapdan |

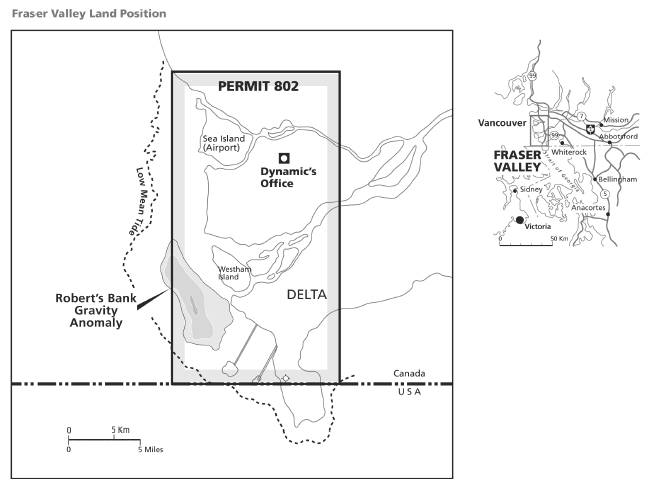

| Peavey/Morinville | Quirk Creek | Fraser Valley (southwestern B.C.) | |

| Alexander | Wimborne | | |

| Simonette | | | |

Our total land holdings increased during the year by a net of 41,917 gross acres (24,493 net) or 28%, to 192,088 gross acres (110,744 net). This increase was spread among three key properties, Wimborne in Alberta, and Cypress/Chowade and Orion in British Columbia. Of our total land interests, 161,918 gross acres (90,496 net) were undeveloped. Our weighted average working interests of all our Alberta properties was 72% versus 52% in British Columbia. In total, our weighted average working interests increased by 1%, to 58%. The remaining 42% was held by joint venture, industry partners, who share a common interest in exploring or developing the properties in question.

We expect to continue to diversify and strengthen our land holdings in fiscal 2003.

Land Holdings (acres)

As at December 31, 2002

| | Developed | | | | Undeveloped | | | | Total | | | | Weighted | |

| Area | Gross | | Net | | Gross | | Net | | Gross | | Net | | Avg WI %(1) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Alberta | | | | | | | | | | | | | | |

| St. Albert | 9,379 | | 6,101 | | 5,372 | | 3,936 | | 14,751 | | 10,037 | | 68% | |

| Halkirk | 3,840 | | 3,456 | | 3,200 | | 3,182 | | 7,040 | | 6,638 | | 94% | |

| Peavey/Morinville | 7,203 | | 4,931 | | 5,069 | | 3,758 | | 12,272 | | 8,689 | | 71% | |

| Quirk Creek | 640 | | 320 | | 10,720 | | 5,360 | | 11,360 | | 5,680 | | 50% | |

| Wimborne | - | | - | | 3,200 | | 3,200 | | 3,200 | | 3,200 | | 100% | |

| Other | 3,689 | | 2,731 | | 3,360 | | 3,072 | | 7,049 | | 5,803 | | 82% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | 24,751 | | 17,539 | | 30,921 | | 22,508 | | 55,672 | | 40,047 | | 72% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| British Columbia | | | | | | | | | | | | | | |

| Cypress/Chowade | 3,499 | | 1,749 | | 12,010 | | 4,028 | | 15,509 | | 5,777 | | 37% | |

| Orion | 1,920 | | 960 | | 64,485 | | 45,682 | | 66,405 | | 46,642 | | 70% | |

| Fraser Valley | - | | - | | 54,502 | | 18,278 | | 54,502 | | 18,278 | | 34% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| | 5,419 | | 2,709 | | 130,997 | | 67,988 | | 136,416 | | 70,697 | | 52% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Total to Dec 31, 2002 | 30,170 | | 20,248 | | 161,918 | | 90,496 | | 192,088 | | 110,744 | | 58% | |

| Total to Mar 31, 2002 | 24,110 | | 17,089 | | 126,061 | | 69,162 | | 150,171 | | 86,251 | | 57% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Increase (decrease) | 6,060 | | 3,159 | | 35,857 | | 21,334 | | 41,917 | | 24,493 | | 1% | |

| Increase (decrease) % | 25% | | 18% | | 28% | | 31% | | 28% | | 28% | | 1% | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| (1) | WI% means our net working interest through joint venture participation. |

In Fiscal 2002 and Fiscal 2001, our total developed acreage comprised 24,110/18,175 gross acres and 17,089/11,078 net acres, respectively, while our total undeveloped acreage comprised 126,061/126,271 gross acres and 69,162/78,949 net acres, respectively. Our weighted average working interest in all properties in Fiscal 2002 and Fiscal 2001 was 57% and 63%, respectively.

19

| | | | | Future | | |

| | Percentage | | New | Prospects | | 2003(4) |

| | Of | | Frontier | For | Reserves | Activity |

| | Production(1) | Core(2) | Exploration(3) | Development | Established | Planned |

|

|

|

|

|

|

|

| Alberta | | | | | | |

| St. Albert | 85 | x | | x | x | x |

| Halkirk | 7 | x | | x | x | x |

| Peavey/Morinville | 3 | | | | x | |

| Alexander | 2 | | | | x | |

| Simonette | 1 | | | | x | |

| Stanmore | 1 | | | | x | |

| Westlock | 1 | | | | x | |

| Quirk Creek | | | x | x | | |

| Wimborne | | | | x | | x |

| |

| | | | | |

| | 100 | | | | | |

| |

| | | | | |

| British Columbia | | | | | | |

| Cypress/Chowade | | x | x | x | x | x |

| Orion | | | x | x | | x |

| Fraser Valley | | | x | x | | |

|

|

|

|

|

|

|

| (1) | Based on total production during Nine-Month Fiscal Transition 2002. |

| (2) | Core properties are those that presently provide or are expected to provide a significant portion of new cash flows. |

| (3) | New frontier exploration represents those properties having no current production and are remote from current known production sources. |

| (4) | For details of 2003 planned activity, see “OUTLOOK FOR 2003”. |

Using the property names as shown in the above table, details of each property as to its location, geological description, land holdings, wells and facilities, key development activities achieved during Nine-Month Fiscal Transition 2002 and our plans for 2003 are described below. Maps are also included to help show the physical location of each property.

| Alberta Properties | | |

|

|

|

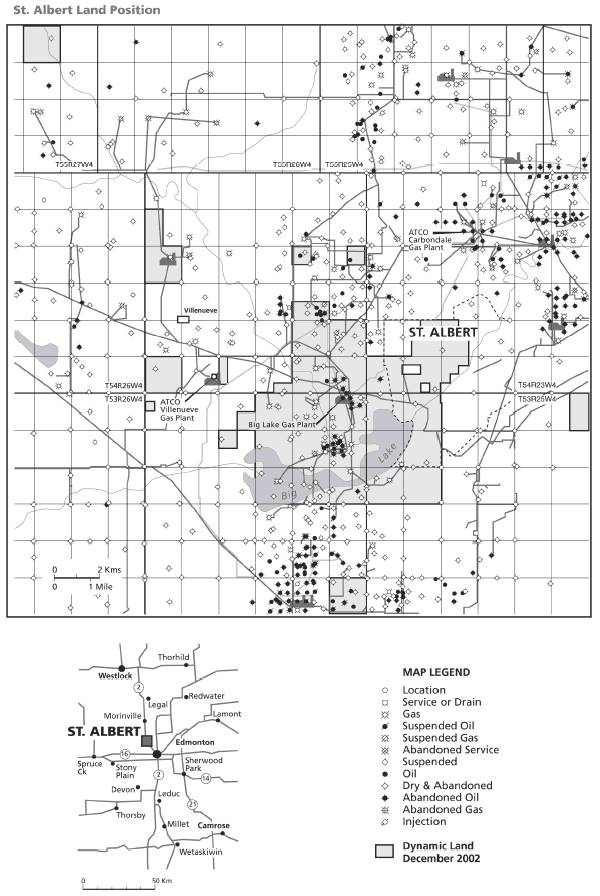

| St. Albert | • | St. Albert is located in central Alberta near the City of Edmonton. |

|

|

|

| Geological Description | • | St Albert is comprised of sixteen separate Cretaceous-aged natural gas and Devonian-aged crude oil pools stacked in seven productive formations, four natural gas and three crude oil. We consider the St. Albert property as several core properties in one, as this high concentration of pools in one property is industry unique. |

| | • | Historically, the property has produced in excess of 22.5 million barrels of crude oil and 109 billion cubic feet of raw natural gas. |

| | • | The area is prospective for remaining recoverable crude oil from six established pools in the Leduc (D-3), Nisku (D-2) and Wabamun (D-1) formations. |

|

|

|

| Land holdings | • | We hold 14,751 acres (10,037 net) under lease. |

|

|

|

| Wells and facilities | • | We own a 75% working interest (WI) in 22 producing natural gas wells; |

| | • | Our ownership ranges from 44% to 77% WI in four producing natural gas wells. |

| | • | We own a 75% WI in eight producing crude oil wells; |

| | • | We own a 75% WI in one oil facility (battery), one solution gas plant, one sour gas compressor, two sweet gas compressors and a 13-km , 6” sour gas pipeline. |

|

|

|

| Operating activities | • | We drilled a successful D-3 oil well (location 06-25) by re-entering a previously suspended well bore, cutting a window in the casing below the Mannville formation and directionally drilling to a new seismically identified bottom hole location. |