Exhibit (17)(e)

| | |

| PROSPECTUS | | NOVEMBER 27, 2009 |

DOMINI SOCIAL EQUITY FUND®

INVESTORSHARES (DSEFX),CLASSASHARES (DSEPX),CLASSRSHARES (DSFRX)ANDINSTITUTIONALSHARES (DIEQX)

DOMINI INTERNATIONAL SOCIAL EQUITY FUNDSM

INVESTORSHARES (DOMIX)ANDCLASSASHARES (DOMAX)

DOMINI EUROPEAN SOCIAL EQUITY FUNDSM

INVESTORSHARES (DEUFX)ANDCLASSASHARES (DEEPX)

DOMINI PACASIA SOCIAL EQUITY FUNDSM

INVESTORSHARES (DPAFX)ANDCLASSASHARES (DPAPX)

DOMINI SOCIAL BOND FUND®

INVESTORSHARES (DSBFX)

The Securities and Exchange Commission has not judged whether this fund is a good investment or whether the information in this prospectus is accurate or complete.

Any statement to the contrary is a crime.

NOTFDICINSURED ŸNOBANKGUARANTEE ŸMAYLOSEVALUE

| | |

| Filed pursuant to Rule 497(e) | | Registration Statement Nos. 33-29180 and 811-05823 |

Supplement dated November 27, 2009, to the

Prospectus dated November 27, 2009,

regarding the

Domini European Social Equity FundSM

and Domini PacAsia Social Equity FundSM

(each a “Fund”)

The Board of Trustees of the Domini Funds has approved the reorganization of each Fund into the Domini International Social Equity Fund. Each reorganization is scheduled to be effective as of the close of business on or about March 19, 2010, subject to shareholder approval.

A shareholder meeting regarding the consideration of the reorganizations is scheduled to occur on or about March 9, 2010, and proxy solicitation materials will be provided to the shareholders of each Fund at a later date regarding the proposed reorganizations. Shareholders of the Funds on January 15, 2010, will be eligible to vote on the reorganization. If you purchase shares of either Fund after January 15, 2010 you will not be entitled to vote on the reorganization.

The Domini European Social Equity Fund and Domini PacAsia Social Equity Fund will be terminated and will no longer be available for investment as of the effective date of each reorganization.

If you have any questions concerning this supplement, please contact Domini at 1-800-582-6757.

PLEASE RETAIN THIS SUPPLEMENT WITH YOUR PROSPECTUS FOR FUTURE REFERENCE.

TABLE OF CONTENTS

| | |

| |

| 2 | | The Domini Funds at a Glance |

| | A summary of each Domini Fund’s investment objective, fees and expenses, portfolio turnover, investment strategies, risk, investment results, and management. |

| |

| 2 | | Domini Social Equity Fund |

| |

7 | | Domini International Social Equity Fund (formerly Domini European PacAsia Social Equity Fund) |

| |

| 12 | | Domini European Social Equity Fund |

| |

| 17 | | Domini PacAsia Social Equity Fund |

| |

| 22 | | Domini Social Bond Fund |

| |

| 27 | | Purchase and Sale of Fund Shares, Tax Information, and Payments to Broker-Dealers and Other Financial Intermediaries |

| |

| 28 | | More on the Funds’ Investment Objectives and Strategies |

| |

| 37 | | More on the Risks of Investing in the Funds |

| |

| 42 | | Socially Responsible Investing |

| |

| 44 | | Portfolio Holdings Information |

| |

| 45 | | Who Manages the Funds? |

| |

| 50 | | The Funds’ Distribution Plan |

| |

| A-1 | | Shareholder Manual |

| | Information about buying, selling, and exchanging shares of the Funds, how Fund shares are valued, Fund distributions, the tax consequences of an investment in a Fund, and how applicable sales charges are calculated. |

| |

| B-1 | | Financial Highlights |

| |

| C-1 | | For Additional Information |

THE DOMINI FUNDS AT A GLANCE

DOMINI SOCIAL EQUITY FUND®

Investment objective: The Fund seeks to provide its shareholders with long-term total return.

Fees and expenses of the Fund: The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for Class A sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the Investor or Class A shares of each Domini Fund, except the Domini Social Bond Fund. More information about these and other discounts is available from your financial professional or in the Fund’s prospectus on page A-9 under the heading “How Sales Charges Are Calculated for Class A Shares” and in the Fund’s Statement of Additional Information (“SAI”) on page 33 under the heading “Additional Information Regarding Class A Sales Charges.”

| | | | | | | | |

| Shareholder fees (paid directly from your investment) |

| Share classes | | Investor | | Class A | | Institutional | | Class R |

Maximum sales charge (load) imposed on purchases as a percentage of offering price | | None | | 4.75% | | None | | None |

Redemption fee on shares held less than 30 days (as a percentage of amount redeemed, if applicable) | | 2.00% | | 2.00% | | 2.00% | | 2.00% |

| | | | | | | | |

Annual Fund operating expenses (expenses that you pay each year as a percentage of the value of

your investment) |

| Share classes | | Investor | | Class A | | Institutional | | Class R |

Management fees | | 0.30% | | 0.30% | | 0.30% | | 0.30% |

Distribution (12b-1) fees | | 0.25% | | 0.25% | | N/A | | N/A |

Other expenses | | | | | | | | |

Sponsorship fee | | 0.45% | | 0.45% | | 0.45% | | 0.45% |

Other miscellaneous expenses | | 0.31% | | 2.31% | | 0.05% | | 0.22% |

Total other expenses | | 0.76% | | 2.76% | | 0.50% | | 0.67% |

Total annual Fund operating expenses | | 1.31% | | 3.31% | | 0.80% | | 0.97% |

Fee waiver and expense reimbursements1 | | 0.06% | | 2.13% | | 0.00% | | 0.07% |

Total annual Fund operating expenses after fee waiver and expenses reimbursements | | 1.25% | | 1.18% | | 0.80% | | 0.90% |

| 1 | The Fund’s adviser has contractually agreed to waive certain fees and/or reimburse certain expenses such that Investor, Class A, Institutional, and Class R share expenses will not exceed 1.25%, 1.18%, 0.80%, and 0.90%, respectively. The agreement expires on November 30, 2010, absent an earlier modification by the Fund’s Board. |

2

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated, that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be as follows:

| | | | | | | | | | | | |

| Share classes (whether or not shares are redeemed) | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Investor | | $ | 127 | | $ | 409 | | $ | 712 | | $ | 1,574 |

Class A | | $ | 590 | | $ | 1,255 | | $ | 1,944 | | $ | 3,769 |

Institutional | | $ | 82 | | $ | 255 | | $ | 444 | | $ | 990 |

Class R | | $ | 87 | | $ | 297 | | $ | 525 | | $ | 1,179 |

Portfolio turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 82% of the average value of its portfolio.

Principal investment strategies: Under normal circumstances, the Fund primarily invests in the equity securities of mid- and large-capitalization U.S. companies. Under normal circumstances, at least 80% of the Fund’s assets will be invested in equity securities and related investments with similar economic characteristics. The Fund may also invest in companies organized or traded outside the U.S. (or in equivalent shares such as ADRs). Domini evaluates the Fund’s potential investments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential investments and the securities held by the Fund, and certain limitations on investments, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

Principal Risks: Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly in the short and long term. You may lose all or part of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

| | • | | Foreign Investing Risk. Investments in foreign regions may be more volatile and less liquid than U.S. investments due to adverse political, social, and economic developments, such as nationalization or expropriation of assets, imposition of currency controls or restrictions, |

3

| | confiscatory taxation, and political or financial instability; regulatory differences such as accounting, auditing, and financial reporting standards and practices; and the degree of government oversight and supervision. |

| | • | | Information Risk. There is a risk that information used by the adviser to evaluate the social and environmental performance of issuers, industries, markets, sectors, and regions may not be readily available, complete, or accurate, which could negatively impact the adviser’s ability to apply its social and environmental standards. This may also lead the Fund not to invest in certain issuers, industries, markets, sectors, or regions. |

| | • | | Market Risk. The market prices of Fund securities may go up or down due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the markets, or adverse investor sentiment. When market prices fall, the value of your investment will go down. The recent financial crisis caused a significant decline in the value and liquidity of many securities. |

| | • | | Mid- to Large-Cap Companies Risk. The market prices of companies at different capitalization levels may go up or down due to general market conditions and cycles. The value of your investment will be affected by the Fund’s exposure to mid- and large-cap companies. |

| | • | | Sector Concentration Risk. The Fund may hold a large percentage of securities in a single sector (e.g., financials). If the Fund holds a large percentage of securities in a single sector, its performance will be tied closely to and affected by the performance of that sector. |

| | • | | Socially Responsible Investing Risk. The application of the adviser’s social and environmental standards will affect the Fund’s exposure to certain issuers, industries, sectors, regions, and countries and may impact the relative financial performance of the Fund — positively or negatively — depending on whether such investments are in or out of favor. |

| | • | | Style Risk. The value of your investment may decrease if the subadviser’s quantitative investment approach does not respond well to current market conditions or its judgment regarding the quality, value, or market trends affecting a particular security, industry, or sector or region is incorrect. |

These and other risks are discussed in more detail later in this prospectus or in the SAI. Please note that there are many other factors that could adversely affect your investment and that could prevent the Fund from achieving its goals.

4

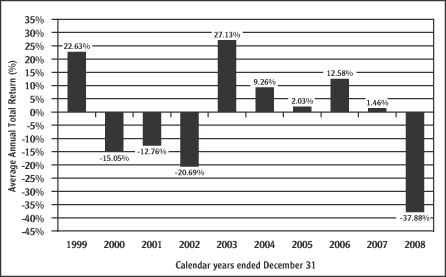

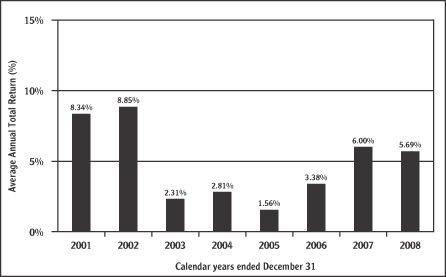

Investment results: The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year for Investor shares and by showing how the Fund’s average annual total returns for 1, 5, and 10 years compare with those of a broad measure of market performance, the Standard and Poor’s 500 Index (S&P 500), an unmanaged index of common stocks. The returns for each class of the Fund will differ from Investor shares because of the different expenses applicable to those share classes. The returns presented in the table for periods prior to the inception of the Class A, Institutional, and Class R shares reflect the performance of the Investor shares. Class A shares and Institutional shares commenced operations on November 28, 2008. Class R shares commenced operations on November 28, 2003. These returns have not been adjusted to take into account the lower expenses applicable to Class A, Institutional, and Class R shares, but for Class A shares, the returns in the table reflect a deduction for the maximum sales charge. Updated information on the Fund’s investment results can be obtained by visiting www.domini.com or by calling 1-800-582-6757.

The Fund’s past results (before and after taxes) are not necessarily an indication of how the Fund will perform in the future.

Highest/lowest quarterly results during this time period were: 17.47% (quarter ended 12/31/99) and –24.04% (quarter ended 12/31/08). The Fund’s year-to-date results as of the most recent calendar quarter ended 9/30/09, were 27.25%.

5

| | | | | | |

| Average annual total returns for periods ended December 31, 2008 (with maximum sales charge) |

| | | 1 Year | | 5 Years | | 10 Years |

Domini Social Equity Fund | | | | | | |

Investor Shares: | | | | | | |

Return before taxes | | -37.88% | | -4.58% | | -3.17% |

Return after taxes on distributions | | -38.03% | | -4.80% | | -3.62% |

Return after taxes on distributions and sale of shares | | -24.37% | | -3.76% | | -2.64% |

Class A shares return before taxes | | -40.88% | | -5.52% | | -3.65% |

Institutional shares return before taxes | | -37.88% | | -4.58% | | -3.17% |

Class R shares return before taxes | | -37.81% | | -4.30% | | -3.03% |

S&P 500 (reflects no deduction for fees, expenses, or taxes) | | -37.00% | | -2.19% | | -1.39% |

After-tax returns are shown only for Investor shares; after-tax returns for other share classes will vary. After-tax returns are calculated using the highest individual marginal federal income tax rates in effect during each year of the periods shown and do not reflect the impact of state and local taxes. Your actual after-tax returns depend on your individual tax situation and likely will differ from the results shown above. In addition, after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as a 401(k) plan or individual retirement account (IRA).

Investment adviser: Domini Social Investments LLC

Subadviser: Wellington Management Company, LLP

Portfolio managers: Donald S. Tunnell, vice president, co-director of the quantitative investment group, and director of quantitative research of Wellington Management, has served on the portfolio management team responsible for the Domini Social Equity Fund since May 2009.

Mammen Chally, CFA, vice president and equity portfolio manager of Wellington Management, has served on the portfolio management team responsible for the Domini Social Equity Fund or the fund in which it formerly invested since 2006.

For important information about purchase and sale of Fund shares, tax information, and financial intermediary compensation, please turn to “Purchase and Sale of Fund Shares, Tax Information, and Payments to Broker-Dealers and Other Financial Intermediaries” on page 27 of the Fund’s prospectus.

6

DOMINI INTERNATIONAL SOCIAL EQUITY FUNDSM

(formerly Domini European PacAsia Social Equity FundSM)

Investment objective: The Fund seeks to provide its shareholders with long-term total return.

Fees and expenses of the Fund: The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for Class A sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the Investor or Class A shares of each Domini Fund, except the Domini Social Bond Fund. More information about these and other discounts is available from your financial professional or in the Fund’s prospectus on page A-9 under the heading “How Sales Charges Are Calculated for Class A Shares” and in the Fund’s Statement of Additional Information (“SAI”) on page 33 under the heading “Additional Information Regarding Class A Sales Charges.”

| | | | |

| Shareholder fees (paid directly from your investment) |

| Share classes | | Investor | | Class A |

Maximum sales charge (load) imposed on purchases as a percentage of offering price | | None | | 4.75% |

Redemption fee on shares held less than 30 days (as a percentage of amount redeemed, if applicable) | | 2.00% | | 2.00% |

| | | | |

Annual Fund operating expenses (expenses that you pay each year as a percentage of the value of

your investment) |

| Share classes | | Investor | | Class A |

Management fees | | 1.00% | | 1.00% |

Distribution (12b-1) fees | | 0.25% | | 0.25% |

Other expenses | | 1.38% | | 5.61% |

Total annual Fund operating expenses | | 2.63% | | 6.86% |

Fee waivers and expense reimbursements1 | | 1.03% | | 5.29% |

Total annual Fund operating expenses after fee waivers and expenses reimbursements | | 1.60% | | 1.57% |

| 1 | The Fund’s adviser has contractually agreed to waive certain fees and/or reimburse certain expenses such that Investor and Class A share expenses will not exceed 1.60% and 1.57%, respectively. The agreement expires on November 30, 2010, absent an earlier modification by the Fund’s Board. |

7

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated, that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be as follows:

| | | | | | | | | | | | |

| Share classes (whether or not shares are redeemed) | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Investor | | $ | 163 | | $ | 720 | | $ | 1,303 | | $ | 2,887 |

Class A | | $ | 627 | | $ | 1,954 | | $ | 3,231 | | $ | 6,224 |

Portfolio turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s turnover rate was 85% of the average value of its portfolio.

Principal investment strategies: Under normal circumstances, the Fund primarily invests in the equity securities of mid- and large-capitalization companies located in Europe, the Asia-Pacific region, and throughout the rest of the world. The Fund’s investments will normally be tied economically to at least 10 different countries other than the U.S. Under normal circumstances, at least 80% of the Fund’s assets will be invested in equity securities and related investments with similar economic characteristics. The Fund will primarily invest in securities of developed market countries throughout the world (or equivalent shares such as ADRs or other securities representing underlying shares of foreign companies) but may invest up to 10% of its assets in emerging market countries. Domini evaluates the Fund’s potential investments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential investments and the securities held by the Fund, and certain limitations on investments, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

Principal risks: Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly in the short and long term. You may lose all or part of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

| | • | | Country Risk. The Fund expects to diversify its investments among various countries throughout the world but it may hold a large number |

8

| | of securities in a single country. Such concentrated investment would increase the risk that economic, political, and social conditions in a country will have a significant impact on Fund performance. |

| | • | | Currency Risk. Fluctuations between the U.S. dollar and foreign currency exchange rates could negatively affect the value of the Fund’s investments. The Fund will benefit when foreign currencies strengthen against the dollar and will be hurt when foreign currencies weaken against the dollar. |

| | • | | Foreign Investing and Emerging Markets Risk. Investments in foreign regions may be more volatile and less liquid than U.S. investments due to adverse political, social, and economic developments, such as nationalization or expropriation of assets, imposition of currency controls or restrictions, confiscatory taxation, and political or financial instability; regulatory differences, such as accounting, auditing, and financial reporting standards and practices; and the degree of government oversight and supervision. These risks may be heightened in connection with investments in emerging-market countries. |

| | • | | Information Risk. There is a risk that information used by the adviser to evaluate the social and environmental performance of issuers, industries, markets, sectors, and regions may not be readily available, complete, or accurate, which could negatively impact the adviser’s ability to apply its social and environmental standards. This may lead the Fund not to invest in certain issuers, industries, markets, sectors, or regions. |

| | • | | Market Risk. The market prices of Fund securities may go up or down due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the markets, or adverse investor sentiment. When market prices fall, the value of your investment will go down. The recent financial crisis caused a significant decline in the value and liquidity of many securities. |

| | • | | Mid-to Large-Cap Companies Risk. The market prices of companies at different capitalization levels may go up or down due to general market conditions and cycles. The value of your investment will be affected by the Fund’s exposure to mid- and large-cap companies. |

| | • | | Sector Concentration Risk. The Fund may hold a large percentage of securities in a single sector (e.g., financials). If the Fund holds a large percentage of securities in a single sector, its performance will be tied closely to and affected by the performance of that sector. |

| | • | | Socially Responsible Investing Risk. The application of the adviser’s social and environmental standards will affect the Fund’s exposure to certain issuers, industries, sectors, regions, and countries and may impact the relative financial performance of the Fund — positively or negatively — depending on whether such investments are in or out of favor. |

| | • | | Style Risk. The value of your investment may decrease if the subadviser’s quantitative investment approach does not respond well to current |

9

| | market conditions or its judgment regarding the quality, value, or market trends affecting a particular security, industry, sector, or region is incorrect. |

These and other risks are discussed in more detail later in this prospectus or in the SAI. Please note that there are many other factors that could adversely affect your investment and that could prevent the Fund from achieving its goals.

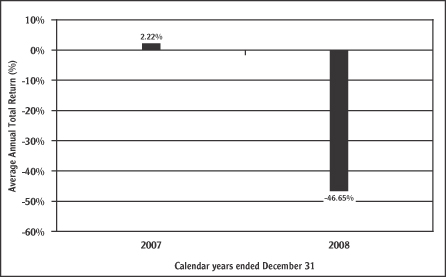

Investment Results: The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year for Investor shares and by showing how the Fund’s average annual total returns for 1, 5, and 10 years, as applicable, compare with those of a broad measure of market performance, the Morgan Stanley Capital International Europe Australasia Index (MSCI EAFE), a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The returns for Class A shares of the Fund will differ from Investor shares because of the different expenses applicable to that share class. Updated information on the Fund’s investment results can be obtained by visiting www.domini.com and by calling 1-800-582-6757.

The Fund’s past results (before and after taxes) are not necessarily an indication of how the Fund will perform in the future.

Highest/Lowest quarterly results during this time period were: 3.64% (quarter ended 6/30/07) and –23.40% (quarter ended 12/31/08). The Fund’s year-to-date results as of the most recent calendar quarter ended 9/30/09, were 28.78%.

10

| | | | |

| Average annual total returns for periods ended December 31, 2008 (with maximum sales charge) |

| | | 1 Year | | Since

Inception (12/27/06) |

Domini International Social Equity Fund | | | | |

Investor Shares: | | | | |

Return before taxes | | -46.65% | | -26.04% |

Return after taxes on distributions | | -46.63% | | -26.10% |

Return after taxes on distributions and sale of shares | | -29.81% | | -21.15% |

Class A shares return before taxes | | -49.18% | | -27.80% |

MSCI EAFE (reflects no deduction for fees, expenses, or taxes) | | -43.06% | | -19.73% |

After-tax returns are shown only for Investor shares; after-tax returns for other share classes will vary. After-tax returns are calculated using the highest individual marginal federal income tax rates in effect during each year of the periods shown and do not reflect the impact of state and local taxes. Your actual after-tax returns depend on your individual tax situation and likely will differ from the results shown above. In addition, after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as a 401(k) plan or individual retirement account (IRA).

Investment adviser: Domini Social Investments LLC

Subadviser: Wellington Management Company, LLP

Portfolio manager: David J. Elliott, CFA, vice president and director of quantitative portfolio management of Wellington Management, has served on the portfolio management team responsible for the Domini International Social Equity Fund since May 2009.

For important information about purchase and sale of Fund shares, tax information, and financial intermediary compensation, please turn to “Purchase and Sale of Fund Shares, Tax Information, and Payments to Broker-Dealers and Other Financial Intermediaries” on page 27 of the prospectus.

11

DOMINI EUROPEAN SOCIAL EQUITY FUNDSM

Investment objective: The Fund seeks to provide its shareholders with long-term total return.

Fees and expenses of the Fund: The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for Class A sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the Investor or Class A shares of each Domini Fund, except the Domini Social Bond Fund. More information about these and other discounts is available from your financial professional or in the Fund’s prospectus on page A-9 under the heading “How Sales Charges Are Calculated for Class A Shares” and in the Fund’s Statement of Additional Information (“SAI”) on page 33 under the heading “Additional Information Regarding Class A Sales Charges.”

| | | | |

| Shareholder fees (paid directly from your investment) |

| Share classes | | Investor | | Class A |

Maximum sales charge (load) imposed on purchases as a percentage of offering price | | None | | 4.75% |

Redemption fee on shares held less than 30 days (as a percentage of amount redeemed, if applicable) | | 2.00% | | 2.00% |

| | | | |

Annual Fund operating expenses (expenses that you pay each year as a percentage of the value of

your investment) |

| Share classes | | Investor | | Class A |

Management fees | | 1.00% | | 1.00% |

Distribution (12b-1) fees | | 0.25% | | 0.25% |

Other expenses | | 0.75% | | 2.60% |

Total annual Fund operating expenses | | 2.00% | | 3.85% |

Fee waivers and expense reimbursements1 | | 0.40% | | 2.28% |

Total annual Fund operating expenses after fee waivers and expenses reimbursements | | 1.60% | | 1.57% |

| 1 | The Fund’s adviser has contractually agreed to waive certain fees and/or reimburse certain expenses such that Investor and Class A share expenses will not exceed 1.60% and 1.57%, respectively. The agreement expires on November 30, 2010, absent an earlier modification by the Fund’s Board. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated, that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be as follows:

| | | | | | | | | | | | |

| Share classes (whether or not shares are redeemed) | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Investor | | $ | 163 | | $ | 589 | | $ | 1,041 | | $ | 2,295 |

Class A | | $ | 627 | | $ | 1,394 | | $ | 2,180 | | $ | 4,223 |

12

Portfolio turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s turnover rate was 98% of the average value of its portfolio.

Principal investment strategies: Under normal circumstances, at least 80% of the Fund’s assets will be invested in equity securities and related investments of European companies. The Fund may invest in companies of any capitalization but under normal market conditions will invest at least 80% of the Fund’s assets in mid- to large-capitalization companies. The Fund may invest in securities of both developed and emerging market countries. The submanager expects most securities to be traded in European markets (or in equivalent shares such as ADRs or other securities representing underlying shares of foreign companies), but some could be traded outside the region. Domini evaluates the Fund’s potential investments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential investments and the securities held by the Fund, and certain limitations on investments, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

Principal risks: Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly in the short and long term. You may lose all or part of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

| | �� | | Country Risk. The Fund expects to diversify its investments among various countries throughout the world but it may hold a large number of securities in a single country. Such concentrated investment would increase the risk that economic, political, and social conditions in a country will have a significant impact on Fund performance. |

| | • | | Currency Risk. Fluctuations between the U.S. dollar and foreign currency exchange rates could negatively affect the value of the Fund’s investments. The Fund will benefit when foreign currencies strengthen against the dollar and will be hurt when foreign currencies weaken against the dollar. |

| | • | | Foreign Investing and Emerging Markets Risk. Investments in foreign regions may be more volatile and less liquid than U.S. investments due to adverse political, social, and economic developments, such as nationalization or expropriation of assets, imposition of currency controls or restrictions, confiscatory taxation, and political or financial |

13

| | instability; regulatory differences, such as accounting, auditing, and financial reporting standards and practices; and the degree of government oversight and supervision. These risks may be heightened in connection with investments in emerging-market countries. |

| | • | | Geographic Concentration Risk. Since the Fund will be largely invested in companies based in Europe, its performance may be affected by market changes or other factors impacting Europe, such as political instability and unpredictable economic conditions. |

| | • | | Information Risk. There is a risk that information used by the adviser to evaluate the social and environmental performance of issuers, industries, markets, sectors, and regions may not be readily available, complete, or accurate, which could negatively impact the adviser’s ability to apply its social and environmental standards. This may lead the Fund not to invest in certain issuers, industries, markets, sectors, or regions. |

| | • | | Market Risk. The market prices of Fund securities may go up or down due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the markets, or adverse investor sentiment. When market prices fall, the value of your investment will go down. The recent financial crisis caused a significant decline in the value and liquidity of many securities. |

| | • | | Mid-to Large-Cap Companies Risk. The market prices of companies at different capitalization levels may go up or down due to general market conditions and cycles. The value of your investment will be affected by the Fund’s exposure to mid- and large-cap companies. |

| | • | | Sector Concentration Risk. The Fund may hold a large percentage of securities in a single sector (e.g., financials). If the Fund holds a large percentage of securities in a single sector, its performance will be tied closely to and affected by the performance of that sector. |

| | • | | Socially Responsible Investing Risk. The application of the adviser’s social and environmental standards will affect the Fund’s exposure to certain issuers, industries, sectors, regions, and countries and may impact the relative financial performance of the Fund — positively or negatively — depending on whether such investments are in or out of favor. |

| | • | | Style Risk. The value of your investment may decrease if the subadviser’s quantitative investment approach does not respond well to current market conditions or its judgment regarding the quality, value, or market trends affecting a particular security, industry, sector, or region is incorrect. |

These and other risks are discussed in more detail later in this prospectus or in the SAI. Please note that there are many other factors that could adversely affect your investment and that could prevent the Fund from achieving its goals.

14

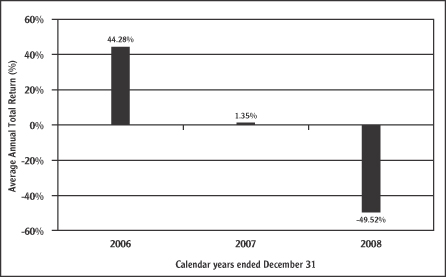

Investment Results: The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year for Investor shares and by showing how the Fund’s average annual total returns for 1, 5, and 10 years, as applicable, compare with those of a broad measure of market performance, the Morgan Stanley Capital International All Country Europe Index (MSCI Europe), a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed market in Europe. The returns for Class A shares of the Fund will differ from Investor shares because of the different expenses applicable to that share class. The returns presented in the table for periods prior to the inception of the Class A shares reflect the performance of the Investor shares. Class A shares commenced operations on November 28, 2008. These returns have not been adjusted to take into account the lower expenses applicable to Class A shares, but in the table have been adjusted to reflect a deduction for the maximum sales charge. Updated information on the Fund’s investment results can be obtained by visiting www.domini.com or by calling 1-800-582-6757.

The Fund’s past results (before and after taxes) are not necessarily an indication of how the Fund will perform in the future.

Highest/Lowest quarterly results during this time period were: 16.44% (quarter ended 3/31/06) and –26.58% (quarter ended 12/31/08). The Fund’s year-to-date results as of the most recent calendar quarter ended 9/30/09, were 30.60%.

15

| | | | |

| Average annual total returns for periods ended December 31, 2008 (with maximum sales charge) |

| | | 1 Year | | Since

Inception (10/03/05) |

Domini European Social Equity Fund | | | | |

Investor Shares: | | | | |

Return before taxes | | -49.52% | | -7.66% |

Return after taxes on distributions | | -49.41% | | -8.46% |

Return after taxes on distributions and sale of shares | | -31.26% | | -5.75% |

Class A shares return before taxes | | -51.92% | | -9.03% |

MSCI Europe (reflects no deduction for fees, expenses, or taxes) | | -46.07% | | -4.92% |

After-tax returns are shown only for Investor shares; after-tax returns for other share classes will vary. After-tax returns are calculated using the highest individual marginal federal income tax rates in effect during each year of the periods shown and do not reflect the impact of state and local taxes. Your actual after-tax returns depend on your individual tax situation and likely will differ from the results shown above. In addition, after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as a 401(k) plan or individual retirement account (IRA).

Investment adviser: Domini Social Investments LLC

Subadviser: Wellington Management Company, LLP

Portfolio manager: David J. Elliott, CFA, vice president and director of quantitative portfolio management of Wellington Management, has served on the portfolio management team responsible for the Domini European Social Equity Fund since May 2009.

For important information about purchase and sale of Fund shares, tax information, and financial intermediary compensation, please turn to “Purchase and Sale of Fund Shares, Tax Information, and Payments to Broker-Dealers and Other Financial Intermediaries” on page 27 of the prospectus.

16

DOMINI PACASIA SOCIAL EQUITY FUNDSM

Investment objective: The Fund seeks to provide its shareholders with long-term total return.

Fees and expenses of the Fund: The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for Class A sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the Investor or Class A shares of each Domini Fund, except the Domini Social Bond Fund. More information about these and other discounts is available from your financial professional or in the Fund’s prospectus on page A-9 under the heading “How Sales Charges Are Calculated for Class A Shares” and in the Fund’s Statement of Additional Information (“SAI”) on page 33 under the heading “Additional Information Regarding Class A Sales Charges.”

| | | | |

| Shareholder fees (paid directly from your investment) |

| Share classes | | Investor | | Class A |

Maximum sales charge (load) imposed on purchases as a percentage of offering price | | None | | 4.75% |

Redemption fee on shares held less than 30 days (as a percentage of amount redeemed, if applicable) | | 2.00% | | 2.00% |

| | | | |

Annual Fund operating expenses (expenses that you pay each year as a percentage of the value of

your investment) |

| Share classes | | Investor | | Class A |

Management fees | | 1.00% | | 1.00% |

Distribution (12b-1) fees | | 0.25% | | 0.25% |

Other expenses | | 1.35% | | 7.26% |

Total annual Fund operating expenses | | 2.60% | | 8.51% |

Fee waivers and expense reimbursements1 | | 1.00% | | 6.94% |

Total annual Fund operating expenses after fee waivers and expenses reimbursements | | 1.60% | | 1.57% |

| 1 | The Fund’s adviser has contractually agreed to waive certain fees and/or reimburse certain expenses such that Investor and Class A share expenses will not exceed 1.60% and 1.57%, respectively. The agreement expires on November 30, 2010, absent an earlier modification by the Fund’s Board. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated, that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be as follows:

| | | | | | | | | | | | |

| Share classes (whether or not shares are redeemed) | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Investor | | $ | 163 | | $ | 713 | | $ | 1,291 | | $ | 2,860 |

Class A | | $ | 627 | | $ | 2,246 | | $ | 3,752 | | $ | 7,080 |

17

Portfolio turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s turnover rate was 88% of the average value of its portfolio.

Principal investment strategies: Under normal circumstances, at least 80% of the Fund’s assets will be invested in equity securities and related investments of companies tied economically to the Asia-Pacific region. The Fund may invest in companies of any capitalization but under normal market conditions will invest at least 80% of the Fund’s assets in mid- to large-capitalization companies. The Fund may invest in securities of both developed and emerging market countries. The Fund’s submanager expects most securities to be traded in Asia-Pacific securities markets (or in equivalent shares such as ADRs or other securities representing underlying shares of foreign companies), but some could be traded outside the region. Domini evaluates the Fund’s potential investments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential investments and the securities held by the Fund, and certain limitations on investments, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

Principal risks: Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly in the short and long term. You may lose all or part of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

| | • | | Country Risk. The Fund expects to diversify its investments among various countries throughout the world but it may hold a large number of securities in a single country. Such concentrated investment would increase the risk that economic, political, and social conditions in a country will have a significant impact on Fund performance. |

| | • | | Currency Risk. Fluctuations between the U.S. dollar and foreign currency exchange rates could negatively affect the value of the Fund’s investments. The Fund will benefit when foreign currencies strengthen against the dollar and will be hurt when foreign currencies weaken against the dollar. |

| | • | | Foreign Investing and Emerging Markets Risk. Investments in foreign regions may be more volatile and less liquid than U.S. investments due to adverse political, social, and economic developments, such as nationalization or expropriation of assets, imposition of currency controls or restrictions, confiscatory taxation, and political or financial |

18

| | instability; regulatory differences, such as accounting, auditing, and financial reporting standards and practices; and the degree of government oversight and supervision. These risks may be heightened in connection with investments in emerging-market countries. |

| | • | | Geographic Concentration Risk. Since the Fund will be largely invested in companies based in the Asia Pacific region, its performance may be affected by market changes or other factors impacting the region, such as political instability and unpredictable economic conditions. |

| | • | | Information Risk. There is a risk that information used by the adviser to evaluate the social and environmental performance of issuers, industries, markets, sectors, and regions may not be readily available, complete, or accurate, which could negatively impact the adviser’s ability to apply its social and environmental standards. This may lead the Fund not to invest in certain issuers, industries, markets, sectors, or regions. |

| | • | | Market Risk. The market prices of Fund securities may go up or down due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the markets, or adverse investor sentiment. When market prices fall, the value of your investment will go down. The recent financial crisis caused a significant decline in the value and liquidity of many securities. |

| | • | | Mid-to Large-Cap Companies Risk. The market prices of companies at different capitalization levels may go up or down due to general market conditions and cycles. The value of your investment will be affected by the Fund’s exposure to mid- and large-cap companies. |

| | • | | Sector Concentration Risk. The Fund may hold a large percentage of securities in a single sector (e.g., financials). If the Fund holds a large percentage of securities in a single sector, its performance will be tied closely to and affected by the performance of that sector. |

| | • | | Socially Responsible Investing Risk. The application of the adviser’s social and environmental standards will affect the Fund’s exposure to certain issuers, industries, sectors, regions, and countries and may impact the relative financial performance of the Fund — positively or negatively — depending on whether such investments are in or out of favor. |

| | • | | Style Risk. The value of your investment may decrease if the subadviser’s quantitative investment approach does not respond well to current market conditions or its judgment regarding the quality, value, or market trends affecting a particular security, industry, sector, or region is incorrect. |

These and other risks are discussed in more detail later in this prospectus or in the SAI. Please note that there are many other factors that could adversely affect your investment and that could prevent the Fund from achieving its goals.

19

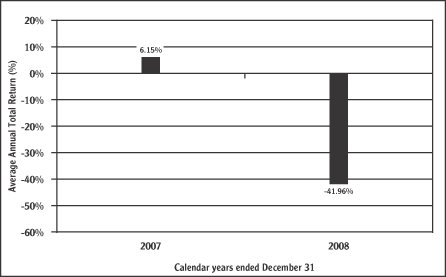

Investment Results: The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year for Investor shares and by showing how the Fund’s average annual total returns for 1, 5, and 10 years, as applicable, compare with those of a broad measure of market performance, the Morgan Stanley Capital International All Country Asia Pacific Index (MSCI AC Asia Pacific), a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets in the Asia-Pacific region. The returns for Class A shares of the Fund will differ from Investor shares because of the different expenses applicable to that share class. The returns presented in the table for periods prior to the inception of the Class A shares reflect the performance of the Investor shares. Class A shares commenced operations on November 28, 2008. These returns have not been adjusted to take into account the lower expenses applicable to Class A shares, but in the table have been adjusted to reflect a deduction for the maximum sales charge. Updated information on the Fund’s investment results can be obtained by visiting www.domini.com and by calling 1-800-582-6757.

The Fund’s past results (before and after taxes) are not necessarily an indication of how the Fund will perform in the future.

Highest/Lowest quarterly results during this time period were: 4.55% (quarter ended 9/30/07) and –19.52% (quarter ended 12/31/08). The Fund’s year-to-date results as of the most recent calendar quarter ended 9/30/09, were 27.55%.

20

| | | | |

| Average annual total returns for periods ended December 31, 2008 (with maximum sales charge) |

| | | 1 Year | | Since

Inception (12/27/06) |

Domini PacAsia Social Equity Fund | | | | |

Investor Shares: | | | | |

Return before taxes | | -41.96% | | -21.42% |

Return after taxes on distributions | | -41.94% | | -21.59% |

Return after taxes on distributions and sale of shares | | -27.02% | | -17.74% |

Class A shares return before taxes | | -44.72% | | -23.30% |

MSCI AC Asia Pacific Index (reflects no deduction for fees, expenses, or taxes) | | -41.62% | | -17.59% |

After-tax returns are shown only for Investor shares; after-tax returns for other share classes will vary. After-tax returns are calculated using the highest individual marginal federal income tax rates in effect during each year of the periods shown and do not reflect the impact of state and local taxes. Your actual after-tax returns depend on your individual tax situation and likely will differ from the results shown above. In addition, after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as a 401(k) plan or individual retirement account (IRA).

Investment adviser: Domini Social Investments LLC

Subadviser: Wellington Management Company, LLP

Portfolio manager: David J. Elliott, CFA, vice president and director of quantitative portfolio management of Wellington Management, has served on the portfolio management team responsible for the Domini PacAsia Social Equity Fund since May 2009.

For important information about purchase and sale of Fund shares, tax information, and financial intermediary compensation, please turn to “Purchase and Sale of Fund Shares, Tax Information, and Payments to Broker-Dealers and Other Financial Intermediaries” on page 27 of the prospectus.

21

DOMINI SOCIAL BOND FUND®

Investment objective: The Fund seeks to provide its shareholders with a high level of current income and total return.

Fees and expenses of the Fund: The table below describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

| | |

| Shareholder fees (paid directly from your investment) |

| Share classes | | Investor |

Redemption fee on shares held less than 30 days (as a percentage of amount redeemed, if applicable) | | 2.00% |

| | |

Annual Fund operating expenses (expenses that you pay each year as a percentage of the value of

your investment) |

| Share classes | | Investor |

Management fees | | 0.40% |

Distribution (12b-1) fees | | 0.25% |

Other expenses | | |

Administrative services fee | | 0.25% |

Other miscellaneous expenses | | 0.47% |

Total other expenses | | 0.72% |

Total annual Fund operating expenses | | 1.37% |

Fee waivers and expense reimbursements1 | | 0.42% |

Total annual Fund operating expenses after fee waivers and expense reimbursements | | 0.95% |

| 1 | The Fund’s adviser has contractually agreed to waive certain fees and/or reimburse certain expenses such that expenses will not exceed 0.95%. The agreement expires on November 30, 2010, absent an earlier modification by the Fund’s Board. |

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated, that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be as follows:

| | | | | | | | | | | | |

| Share classes (whether or not shares are redeemed) | | 1 Year | | 3 Years | | 5 Years | | 10 Years |

Investor | | $ | 97 | | $ | 392 | | $ | 710 | | $ | 1,610 |

Portfolio turnover: The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 33% of the average value of its portfolio.

22

Principal investment strategies: Under normal circumstances, the Fund invests at least 85% of its assets in investment-grade securities and maintains a dollar-weighted average effective maturity of between two and ten years. Under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds, including government and corporate bonds, mortgage-backed and asset-backed securities, and U.S. dollar denominated bonds issued by non-U.S. entities. Some of these instruments may not be insured and may earn below-market rates of return. Some investments may be unrated, lower-rated, or illiquid securities. Domini evaluates the Fund’s potential corporate debt instruments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential corporate investments and the corporate securities held by the Fund, and certain limitations on investment, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

Principal risks: Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly in the short and long term. You may lose all or part of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

| | • | | Credit Risk. Fixed-income securities are subject to credit risk. Credit risk is the possibility that an issuer will fail to make timely payments of interest or principal, or go bankrupt. The lower the ratings of such debt securities, the greater their risks. In addition, lower-rated securities have higher risk characteristics, and changes in economic conditions are likely to cause issuers of these securities to be unable to meet their obligations. Below investment grade securities (sometimes referred to as “junk bonds”) involve greater risk of default or downgrade and are more volatile than investment grade securities. Below investment grade securities may also be less liquid than higher-quality securities. |

| | • | | Government-Sponsored Entities Risk. The Fund’s investments in securities issued by government-sponsored entities such as Fannie Mae, Freddie Mac, and the Federal Home Loan Bank are not guaranteed or insured by the U.S. government and may decline in value. |

| | • | | Information Risk. There is a risk that information used by the adviser to evaluate the social and environmental performance of issuers, industries, markets, and sectors may not be readily available, complete, or accurate, which could negatively impact the adviser’s ability to apply its social and environmental standards. This may also lead the Fund not to invest in certain issuers, industries, markets, or sectors. |

| | • | | Interest Rate Risk. The value of your investment will fluctuate with interest rates. If interest rates rise, the price of a fixed-income security declines and could reduce the value of the Fund’s share price. A rise in |

23

| | rates tends to have a greater impact on securities with longer maturities or higher durations. |

| | • | | Liquidity Risk. Some securities held by the Fund may be difficult to sell, or may be illiquid, particularly during times of market turmoil. Illiquid securities also may be difficult to value. Due to limitations on investments in illiquid securities the Fund may be unable to achieve its desired level of exposure to certain sectors. If the Fund is forced to sell an illiquid asset to meet redemption request or other cash needs, the Fund may be forced to sell such securities at a loss. |

| | • | | Market Risk. The market prices of Fund securities may go up or down due to general market conditions, such as real or perceived adverse economic or political conditions, inflation, changes in interest rates, lack of liquidity in the markets, or adverse investor sentiment. When market prices fall, the value of your investment will go down. The recent financial crisis caused a significant decline in the value and liquidity of many securities. |

| | • | | Prepayment and Extension Risk. Many issuers have a right to prepay their securities. If interest rates fall, an issuer may exercise this right. If this happens, the Fund will be forced to reinvest prepayment proceeds at a time when yields on securities available in the market are lower than the yield on the prepaid security. The Fund also may lose any premium it paid on the security. If interest rates rise, repayments of fixed-income securities may occur more slowly than anticipated by the market. This may drive the prices of these securities down because their interest rates are lower than the current interest rate and they remain outstanding longer. |

| | • | | Socially Responsible Investing Risk. The application of the adviser’s social and environmental standards will affect the Fund’s exposure to certain issuers, industries, and sectors and may impact the relative financial performance of the Fund — positively or negatively — depending on whether such investments are in or out of favor. |

These and other risks are discussed in more detail later in this prospectus or in the SAI. Please note that there are many other factors that could adversely affect your investment and that could prevent the Fund from achieving its goals.

Investment results: The bar chart and table below provide some indication of the risks of investing in the Fund by showing changes in the Fund’s performance from year to year and by showing how the Fund’s average annual total returns for 1, 5, and 10 years, as applicable, compare with those of a broad measure of market performance, the Barclays Capital Intermediate Aggregate Index (BCIA), an unmanaged index of intermediate investment-grade fixed-income securities. Updated information on the Fund’s investment results can be obtained by visiting www.domini.com and by calling 1-800-582-6757.

24

The Fund’s past results (before and after taxes) are not necessarily an indication of how the Fund will perform in the future.

Highest/lowest quarterly results during this time period were: 4.69% (quarter ended 09/30/01) and –2.58% (quarter ended 06/30/04). The Fund’s year-to-date results as of the most recent calendar quarter ended 9/30/09, were 5.84%.

| | | | | | |

| Average annual total returns for periods ended December 31, 2008 |

| | | 1 Year | | 5 Year | | Since

Inception (06/01/00) |

Domini Social Bond Fund | | | | | | |

Investor shares return before taxes | | 5.69% | | 3.87% | | 5.50% |

Investor shares return after taxes on distributions | | 4.26% | | 2.52% | | 3.93% |

Investor shares return after taxes on distributions and sale of shares | | 3.66% | | 2.50% | | 3.77% |

BCIA (reflects no deduction for fees, expenses, or taxes) | | 4.86% | | 4.43% | | 6.17% |

After-tax returns are calculated using the highest individual marginal federal income tax rates in effect during each year of the periods shown and do not reflect the impact of state and local taxes. Your actual after-tax returns depend on your individual tax situation and likely will differ from the results shown above. In addition, after-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as a 401(k) plan or individual retirement account (IRA).

25

Investment adviser: Domini Social Investments LLC

Subadviser: Seix Investment Advisers LLC

Portfolio manager: James Keegan, chief investment officer and member of the investment grade funds’ management team of Seix Investment Advisers LLC, has served as the portfolio manager primarily responsible for the Fund since April 2008.

For important information about purchase and sale of Fund shares, tax information, and financial intermediary compensation, please turn to “Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries” on page 27 of the prospectus.

26

PURCHASE AND SALE OF FUND SHARES, TAX INFORMATION, AND PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES

Purchase and Sale of Fund Shares. You may redeem shares of the Funds each day the New York Stock Exchange is open. You should contact your financial intermediary or Service Organization, or if you hold your shares directly, you should contact the Fund by phone (Shareholder Services at 800-582-6757 for Investor, Institutional, and Class R shares or Fund Services at 800-498-1351 for Class A shares), by mail (Domini Funds, P.O. Box 9785, Providence, RI 02940-9785), or online at www.domini.com.

The Funds’ initial and subsequent investment minimums for eligible shareholders generally are as follows:

| | | | | | | | |

Investment minimum Initial/Additional Investment | | Share classes |

| | Investor | | Class A | | Institutional | | Class R |

Individual and Joint Accounts (nonretirement) | | $2500/$100 | | $2500/$100 | | $2 million/none | | N/A |

Individual Retirement Accounts (IRAs) | | $1500/$100 | | $1500/$100 | | $2 million/none | | N/A |

Uniform Gifts/Transfers to Minor Accounts (UGMA/UTMA); Coverdell Education Savings Accounts | | $1500/$100 | | $1500/$100 | | $2 million/none | | N/A |

Employer-Sponsored Retirement and Benefit Plan Accounts (e.g., 401(k), SEP-IRA, SIMPLE IRA) | | $2500/$100 | | $2500/$100 | | $2 million/none

($10 million/none for defined

contribution plans) | | None |

Accounts for Organizations (e.g., trust, corporation, partnership, endowment, foundation or other entity) | | $2500/$100 | | $2500/$100 | | $2 million/none | | None |

Investment minimums are $1500/$50 for Investor Class and Class A purchases through Automatic Investment Plans. Minimums may be waived for purchases through certain omnibus accounts or may be at a different level established by your broker-dealer, financial institution, or financial intermediary.

Tax information. The Funds’ distributions are taxable, and will be taxed as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account. Such tax-deferred arrangements may be taxed later upon withdrawal of monies from those arrangements. For additional information, please see “Taxes” in the Shareholder Manual and “Taxation” in the Statement of Additional Information.

Payments to broker-dealers and other financial intermediaries. The Fund and its related companies may pay broker-dealers or other financial intermediaries (such as a bank) for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing your broker-dealer or other intermediary or its employees or associated persons to recommend

27

the Fund over another investment. Ask your financial adviser or visit your financial intermediary’s website for more information.

MORE ON THE FUNDS’ INVESTMENT OBJECTIVES AND STRATEGIES

Investment Objectives

Each Fund’s investment objective may be changed by the Fund’s Board of Trustees without shareholder approval, but shareholders will be given notice at least 30 days before any change to the investment objective is implemented. Management currently has no intention to change any Fund’s investment objective.

DOMINI SOCIAL EQUITY FUND

The investment objective of the Domini Social Equity Fund (the Fund) is to provide its shareholders with long-term total return.

As a primary strategy, the Fund invests at least 80% of the Fund’s assets in equity securities and related investments with similar economic characteristics, under normal circumstances. The Fund will provide shareholders with at least 60 days’ prior written notice if it changes this 80% policy. The Fund may invest in companies of any capitalization, but under normal market conditions will invest primarily in mid-cap to large-cap U.S. companies. Domini defines mid- and large-cap companies to be those companies with a market capitalization at the time of purchase between $2 and $10 billion, or greater than $10 billion, respectively. It is expected that at least 80% of the Fund’s assets will be invested in mid- to large-cap companies under normal market conditions.

As a primary strategy, under normal circumstances the Fund invests in stocks of U.S. companies. While the Fund’s subadviser expects that most of the securities held by the Fund will be traded in U.S. securities markets, as an additional strategy some could be traded outside the region (or in equivalent shares such as American Depository Receipts). The Fund may hold up to 15% of its assets in companies organized or principally traded outside the U.S.

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

The investment objective of the Fund is to provide shareholders with long-term total return.

As a primary strategy, under normal circumstances the Fund invests at least 80% of the Fund’s assets in equity securities and related investments with similar economic characteristics. The Fund will provide shareholders with at least 60 days’ prior written notice if it changes this 80% policy. The Fund may invest in companies of any capitalization, but under normal market conditions will invest primarily in mid-cap to large-cap companies. Domini defines mid- and large-cap companies to be those companies with a market capitalization at the time of purchase between $2 and $10 billion, or greater than $10 billion, respectively. It is expected that at least 80% of the Fund’s assets will be invested in mid- to large-cap companies under normal market conditions.

28

As a primary strategy, the Fund invests in stocks of companies located in Europe, the Asia-Pacific region, and throughout the rest of the world. Under normal circumstances, the Fund’s investments will be tied economically to at least 10 countries other than the U.S. The Fund will primarily invest in securities of developed market countries throughout the world (or in equivalent shares such as American Depository Receipts, European Depository Receipts, Global Depository Receipts, or other securities representing underlying shares of foreign companies). As an additional strategy the Fund may invest up to 10% of its assets in emerging-market countries.

DOMINI EUROPEAN SOCIAL EQUITY FUND

The investment objective of the Fund is to provide shareholders with long-term total return. As a primary strategy, under normal circumstances the Fund invests at least 80% of the Fund’s assets in equity securities and related investments of European companies. For purposes of this policy, European companies include (1) companies organized or principally traded in a European country; (2) companies having at least 50% of their assets in, or deriving 50% or more of their revenues or profits from, a European country and (3) issuers who are European governments and agencies or underlying instrumentalities of European governments. For purposes of this policy European countries include those countries represented by companies in the MSCI All Country Europe Index. The Fund will provided shareholders with at least 60 days’ prior written notice if it changes this 80% policy.

The Fund may invest in companies of any capitalization. Under normal market conditions the Fund is expected to invest at least 80% of the Fund’s assets in mid- to large-cap companies. Domini defines mid- and large-cap companies to be those companies with a market capitalization at the time of purchase between $2 and $10 billion, or greater than $10 billion, respectively.

The Fund may invest in securities of both developed and emerging-market countries. While the Fund’s submanager expects that most of the securities held by the Fund will be traded in European securities markets (or in equivalent shares such as American Depository Receipts, European Depository Receipts, Global Depository Receipts, or other securities representing underlying shares of foreign companies), as an additional strategy some could be traded outside the region.

DOMINI PACASIA SOCIAL EQUITY FUND

The investment objective of the Fund is to provide shareholders with long-term total return. As a primary strategy, under normal circumstances the Fund invests at least 80% of the Fund’s assets in equity securities and related investments of companies tied economically to the Asia-Pacific region. For purposes of this policy, these companies may include, but are not limited to (1) companies organized or principally traded in an Asia-Pacific country; (2) companies having at least 50% of their assets in, or deriving 50% or more of their revenues or profits from, an Asia-Pacific country; and (3) issuers who are Asia-Pacific governments and agencies or underlying instrumentalities of

29

Asia-Pacific governments. For purposes of this policy Asia-Pacific countries include those countries represented by companies in the MSCI All Country Asia Pacific Index. The Fund will provided shareholders with at least 60 days’ prior written notice if it changes this 80% policy.

The Fund may invest in companies of any capitalization. Under normal market conditions the Fund is expected to invest at least 80% of the Fund’s assets in mid- to large-cap companies. Domini defines mid- and large-cap companies to be those companies with a market capitalization at the time of purchase between $2 and $10 billion, or greater than $10 billion, respectively.

The Fund may invest in securities of both developed and emerging-market countries. While the Fund’s submanager expects that most of the securities held by the Fund will be traded in Asia-Pacific securities markets (or in equivalent shares such as American Depository Receipts, Global Depository Receipts, or other securities representing underlying shares of foreign companies), as an additional strategy some could be traded outside the region.

DOMINI SOCIAL EQUITY FUND, DOMINI INTERNATIONAL SOCIAL EQUITY FUND, DOMINI EUROPEAN SOCIAL EQUITY FUND,AND DOMINI PACASIA SOCIAL EQUITY FUND

As a primary strategy, the investment approach of each Fund incorporates Domini’s social and environmental standards. Each Fund’s investments are selected from a universe of securities that Domini has identified as eligible for investment based on its evaluation against Domini’s social and environmental standards. Domini evaluates the Fund’s potential investments against its social and environmental standards based on the businesses in which they engage, as well as on the quality of their relations with key stakeholders, including communities, customers, ecosystems, employees, investors, and suppliers. For additional information about the standards Domini uses to evaluate potential investments and the securities held by the Fund, and certain limitations on investments, please see “Socially Responsible Investing.” Domini reserves the right to alter its social and environmental standards or the application of those standards, or to add new standards, at any time without shareholder approval.

The Fund’s subadviser uses a proprietary quantitative model to select investments from among those which Domini has notified the subadviser are eligible for investment. The portfolio construction process seeks to manage risk and ensure that the Fund’s holdings and characteristics are consistent with the Fund’s investment objective. The subadviser’s quantitative stock selection process uses multiple factors to determine a security’s attractiveness. The factors can be grouped loosely into “value” and “momentum” categories. Valuation factors compare securities within sectors based on measures such as price ratios and balance sheet strength. Momentum focuses on stocks with favorable earnings and stock price momentum to assess the appropriate time for purchase. The quantitative analysis favors stocks that appear to be both inexpensive according to the value factors and well-positioned according to

30

earnings growth and price momentum factors. The weight of each factor and category varies by industry and region. The subadviser will seek to buy the most attractive stocks and sell the least attractive stocks, within reasonable turnover constraints. Portfolio sector weights are managed relative to the Fund’s benchmark; consequently, the Fund may invest a significant percentage of its assets in a single sector if that sector represents a large proportion of the benchmark.

Under normal circumstances, the subadviser will seek to remove a security from the Fund’s portfolio within 90 days after receiving a notification from Domini that an investment in such security is not consistent with its social and environmental standards. Such notifications may cause the Fund to dispose of a security at a time when it may be disadvantageous to do so.

As an additional strategy, the Fund may reserve a portion of its portfolio for various reasons including to invest in companies with strong social or environmental profiles or to support shareholder advocacy initiatives at Domini’s discretion. Such investments are not subject to the submanager’s quantitative model.

DOMINI SOCIAL BOND FUND

The investment objective of the Domini Social Bond Fund (the Fund) is to provide its shareholders with a high level of current income and total return.

As a primary strategy, under normal circumstances, the Fund invests at least 85% of its assets in investment-grade securities and maintains a dollar-weighted average effective maturity of between two and ten years.

As a primary strategy, under normal circumstances, the Fund invests at least 80% of the Fund’s assets in bonds, including government and corporate bonds, mortgage-backed and asset-backed securities, and U.S. dollar-denominated bonds issued by non-U.S. entities. The Fund will provide shareholders with at least 60 days’ prior notice if it changes this 80% policy.