Item 1: Report to Shareholders| Institutional Foreign Bond Funds | June 30, 2007 |

The views and opinions in this report were current as of June 30, 2007. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

Managers’ Letter

T. Rowe Price Institutional Foreign Bond Funds

Dear Investor

We would like to welcome the new shareholders to the Institutional International Bond Fund, which opened for investors on May 31, 2007.

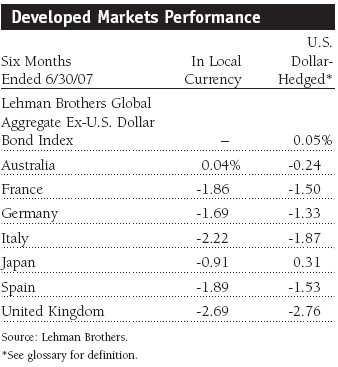

Concerns about rising interest rates, stronger-than-expected global economic growth, and fears of higher inflation helped to keep bond returns modest in non-U.S. developed and emerging markets during the first six months of 2007. Although the U.S. Federal Reserve has held its target short-term rate steady at 5.25% since June 2006, the European Central Bank (ECB), Bank of Japan (BOJ), and Bank of England raised their target rates, which helped push bond prices down. (Bond yields and prices move in opposite directions.) Emerging markets fundamentals—political stability, steady economic growth, and improving inflation trends—remained intact, but the markets became choppier as investors’ appetite for risk waxed and waned, depending on the latest news about subprime mortgages and the Chinese stock market. The dollar, burdened with large trade and budget deficits, fell against the euro but gained against the yen.

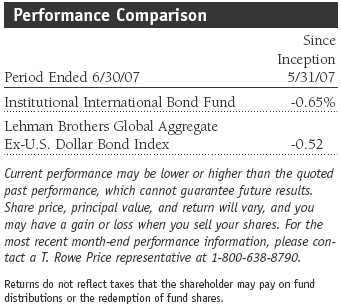

For the period ended June 30, 2007, the Institutional International Bond Fund posted a one-month return of -0.65% compared with -0.52% for the Lehman Brothers Global Aggregate Ex-U.S. Dollar Bond Index.

• Rising interest rates and concerns about global inflationary pressures hurt bond returns for the first half of 2007, and the weaker dollar helped returns for the U.S. investors.

• The Institutional Emerging Markets Bond Fund beat its benchmark, but the return was modest. The Institutional International Bond Fund began operations on May 31, 2007.

• Higher bond yields impeded global bond market performance, but the weaker dollar helped U.S. investors offset the bond market’s weak returns.

• Central banks remain concerned that strong growth could fuel future inflation, and a number of them are likely to raise rates in the second half of 2007, creating an environment where global yields could rise modestly.

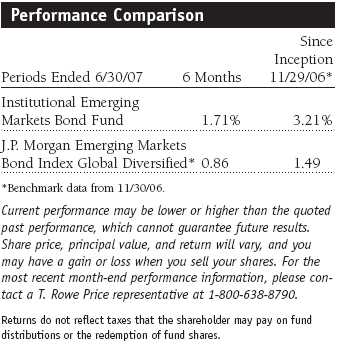

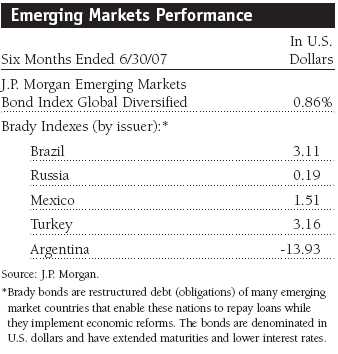

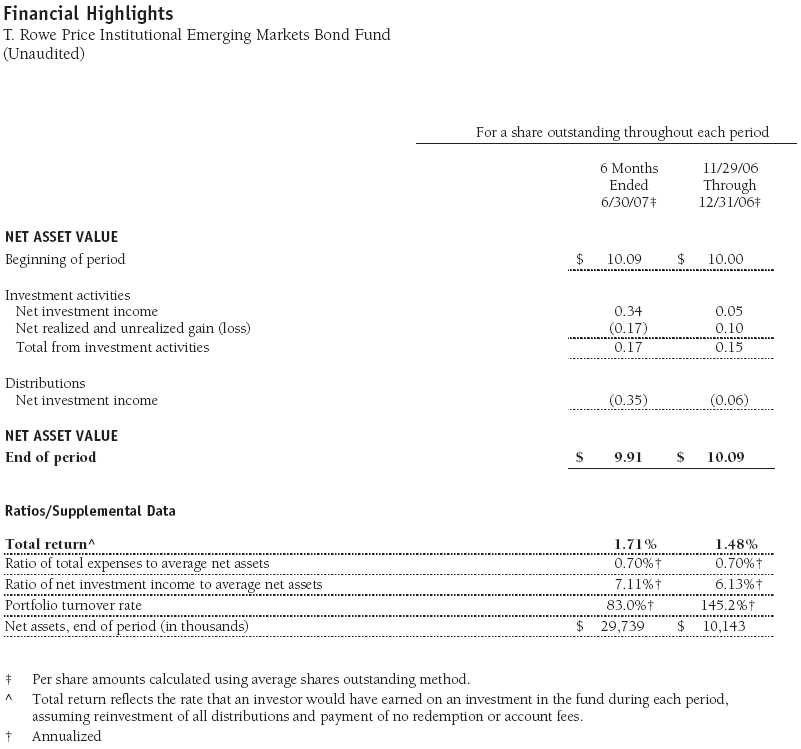

The Institutional Emerging Markets Bond Fund outperformed its benchmark, the J.P. Morgan Emerging Markets Bond Index Global Diversified. For the six-month period, the fund returned 1.71%, compared with 0.86% for the benchmark, and for the since-inception period, the fund posted a gain of 3.21%, compared with the benchmark’s 1.49% increase. As of this report, the fund’s benchmark is the J.P. Morgan Emerging Markets Bond Index Global Diversified.

Market Environment

The Federal Reserve’s steady policy and periodic statements about its inflation concerns created a range-bound U.S. Treasuries market. However, in early June, yields spiked to their highest levels in five years. Rising Treasury yields rippled through global markets and drove them lower. Strong economic growth, fears of rising inflation, and expectations of additional ECB rate increases weighed heavily on most euro zone bond markets. In response to Europe’s solid growth and dropping unemployment, the ECB raised its overnight borrowing rate to 4.0%, its highest level since September 2001.

In Japan, most of the economic data indicated that the nation’s longest postwar recovery was still in place. First-quarter GDP growth was 0.7%, which was slower than the pace set in the fourth quarter of 2006, but employment dropped to its lowest level since 1998. Anticipating that the economy would continue to strengthen, the BOJ raised its target rate to 0.50% in February, and the market expects another hike later this year.

Although most of the world’s fixed-income markets posted mixed returns in local currencies, the weaker dollar helped returns for U.S. investors in most markets. The dollar strengthened against the yen, detracting from returns for U.S. investors in Japan.

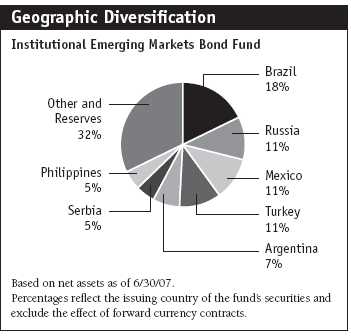

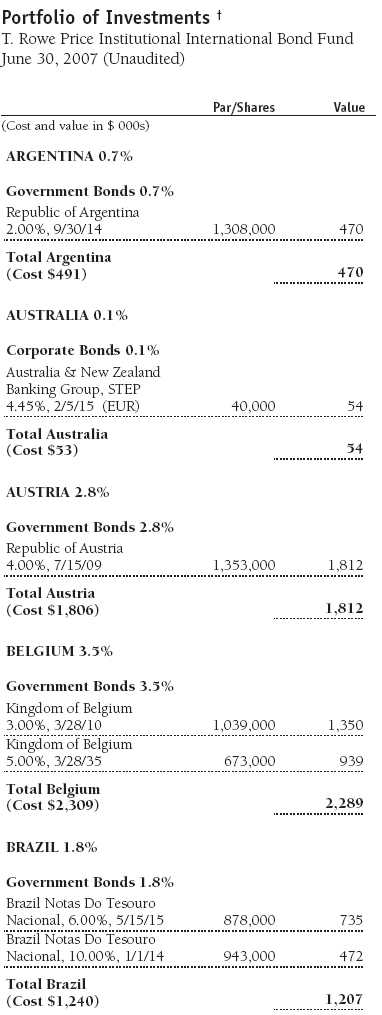

Emerging markets debt showed positive returns during the quarter, holding up well despite several bouts of risk aversion. Ecuador was the best-performing market during the period, while Venezuela lagged as a result of President Hugo Chavez’s threats to nationalize key industries, such as utilities. Brazilian external and local debt market performance was strong. Lower-than-expected inflation data encouraged the Brazilian central bank to cut rates, and strengthening fundamentals—larger international reserves and falling external debt—added to the positive investor sentiment. Argentina was another strong performer, despite concerns relating to the government’s manipulation of inflation numbers. Markets recovered, however, as the country’s rate of growth continued to surpass investors’ expectations. Although Mexico’s absolute returns were positive, its market lagged the broader emerging markets debt universe.

In developing Europe, higher oil prices and growing foreign exchange reserves bolstered the Russian market. Russia’s external debt markets lagged the broader market, however. Turkey’s central bank anticipated the latest inflation spike and raised rates in March. By June, the government reported lower-than-expected inflation numbers, and the market performed strongly on the belief that the central bank will cut interest rates later this year.

Institutional International Bond Fund

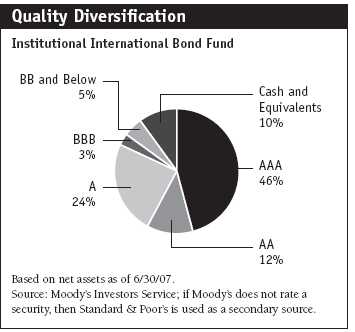

Higher bond yields during June impeded performance and resulted in the Institutional International Bond Fund posting a modest loss at the end of its first month of operations. The declining dollar helped to offset the negative effect of the weakness in global bond markets. At the end of the reporting period, European bonds represented the largest proportion of the fund’s holdings, followed by Japan. For a complete listing of our holdings at the end of the reporting period, please refer to the fund’s Financial Statements.

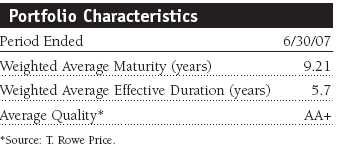

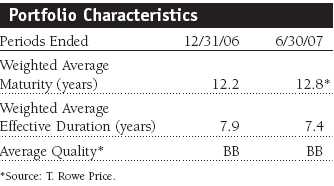

In this rising-rate environment, we believe there is opportunity in emerging markets. We took positions in local debt markets in Latin America, Africa, and the Pacific Rim. The portfolio’s average weighted credit quality was high at AA+, and the average weighted maturity stood at 9.2 years. We also ended the period with a healthy balance in cash and cash equivalents to take advantage of any increase in short-term rates.

Institutional Emerging Markets Bond Fund

After several years of strong performance, emerging market bonds became much more volatile, creating a more difficult environment for the fund. Even though the fundamental environment—improved fiscal conditions and strong commodity markets—was unchanged in most developing countries, their bond markets had to contend with a number of challenges. Higher U.S. Treasury yields, a collapsing U.S. subprime mortgage market, the repercussions from several abrupt declines in China’s stock market, and investors who became much more skittish about investing in higher-risk investments all weighed on the markets.

Despite these headwinds, we were able to post a respectable return for the first half of the year. Our allocation to local market bonds helped our absolute returns and our performance relative to the benchmark. We continued purchasing bonds denominated in local currencies, and we anticipate that local-currency bonds will become more prevalent in emerging markets as governments pay down debt, judiciously manage their economies, and build their reserves. As a result, they will be borrowing less in foreign currencies, and this trend should deepen emerging economies’ domestic currency markets.

Brazil was our largest holding, and the country’s bonds rallied on the belief that the central bank would cut rates earlier than anticipated and also because of a credit upgrade that raises the country’s rating to one level below investment grade. We also got a boost from an allocation to Turkey, which is showing progress in returning stability to the country’s economy and financial system. Mexico was another positive contributor thanks to President Felipe Calderon’s reform program and the Bank of Mexico’s willingness to use preemptive measures to dampen any signs of inflation. Our holding of Argentina’s GDP warrants, which were issued after the country’s 2005 default and rewarded bond holders if certain economic benchmarks were met or exceeded, have paid off handsomely. We avoided Venezuela. Deficits are growing and we believe President Chavez’s takeover policies mean a shrinking private sector and fewer checks on his power.

We were hurt by avoiding Ecuador and by being overweight in Iraq. We were concerned about the threats Ecuador’s new government was making about restructuring debt, and we eliminated our holdings in January. The restructuring threats quieted shortly after our sale, and Ecuador’s bonds rallied. Although oil production has improved and International Monetary Fund officials have commended the Iraqi government for its fiscal discipline, the market has been more focused on Iraq’s continued high level of street fighting and political turmoil, which have weighed on the nation’s bonds.

During the first half of the year, we added to holdings of local bonds in Turkey, where higher interest rates and the relative strength of the lira should result in improved inflation trends for the remainder of the year. We remain underweight in Asia, but we have kept overweight positions in Vietnam and Indonesia, where economic growth trends are solid. We trimmed some of our Argentina holdings and realized gains. We are holding our current off-index position in Jamaica. The country’s GDP has been steadily growing and its fiscal conditions have been improving. We expect that Jamaican bonds will eventually become part of the emerging markets index. Based on Venezuela’s deteriorating fundamentals and the market’s generally negative perceptions, we established a small short position, which means we would benefit should Venezuelan bonds continue to fall in value.

Our strategy remains focused on fundamental credit analysis and establishing high-conviction positions where warranted. We remain less focused on near-term trading events and prefer to build a diverse portfolio of longer-term positions. This approach is appropriate for our fundamental investment style and enables us to hold down turnover and trading costs.

Outlook

We expect U.S. growth to remain below its full potential for the remainder of the year, which should help contain core inflation. As long as non-core factors such as energy, food, and imported goods remain moderate, we believe the Fed will keep its short-term target rate steady. Europe’s strong economic momentum is likely to continue, and we believe the ECB is poised to take measures—at least one more rate hike this year—to keep inflation under control. Japan is likely to continue its current tightening cycle as it normalizes its interest rates. We believe life insurance and pension fund demand will support longer-maturity Japanese government bonds, and the higher short-term rates and recovering economy will push shorter-term government bond yields higher. The U.S. trade deficit is likely to grow and higher global interest rates should exert additional pressure on the dollar. We expect the dollar to continue to weaken against the euro and lose some of its recent strength again st the yen.

Emerging markets debt should trade in a narrow range for the remainder of the year, but investors’ mercurial appetite for risk could make markets volatile. With improving economic fundamentals and fiscal conditions, we believe that local emerging bond markets offer better value than dollar-denominated issues. Over the longer term, conditions look favorable in emerging debt markets. Debt buybacks are likely to continue, and large trade surpluses should help many emerging countries to withstand the natural volatility in these markets. These factors are supportive, and we believe that emerging markets will remain a fertile ground for investors.

Respectfully submitted,

Ian Kelson

President of the International Fixed Income Division and

chairman of the Institutional International Bond Fund’s

Investment Advisory Committee

Michael Conelius

Chairman of the Investment Advisory Committee for the

Institutional Emerging Markets Bond Fund

July 24, 2007

The committee chairmen have day-to-day responsibility for the portfolios and work with committee members in developing and executing the funds’ investment programs.

| Risks of International Bond Investing |

Funds that invest overseas generally carry more risk than funds that invest strictly in U.S. assets, including unpredictable changes in currency values. Investments in emerging markets are subject to abrupt and severe price declines, and should be regarded as speculative. The economic and political structures of developing nations, in most cases, do not compare favorably with the U.S. or other developed countries in terms of wealth and stability, and their financial markets often lack liquidity. Some countries also have legacies of hyperinflation, currency devaluations, and governmental interference in markets.

International investments are subject to currency risk, a decline in the value of a foreign currency versus the U.S. dollar, which reduces the dollar value of securities denominated in that currency. The overall impact on a fund’s holdings can be significant and long-lasting depending on the currencies represented in the portfolio, how each one appreciates or depreciates in relation to the U.S. dollar, and whether currency positions are hedged. Further, exchange rate movements are unpredictable and it is not possible to effectively hedge the currency risks of many developing countries.

Bonds are also subject to interest rate risk, the decline in bond prices that usually accompanies a rise in interest rates, and credit risk, the chance that any fund holding could have its credit rating downgraded, or that a bond issuer will default (fail to make timely payments of interest or principal), potentially reducing the fund’s income level and share price.

30-Day SEC Yield: The 30-day SEC Yield represents net investment income earned by a fund over a 30-day period, expressed as an annual percentage rate based on the fund’s share price at the end of the 30-day period.

Average maturity: For a bond fund, this is the weighted average of the stated maturity dates of the portfolio’s securities. In general, the longer the average maturity, the greater the fund’s sensitivity to interest rate changes, which can mean greater price fluctuation. A shorter average maturity usually means less interest rate sensitivity, and consequently, a less volatile portfolio.

Basis point: One one-hundredth of one percentage point, or 0.01%.

Duration: A measure of a bond or bond fund’s sensitivity to changes in interest rates. For example, a fund with a duration of six years would fall about 6% in response to a one-percentage-point rise in rates, and vice versa.

Hedged: The buying and selling of forward exchange contracts to lock in a currency’s value. In an unhedged position, no steps are taken to protect against currency fluctuations.

J.P. Morgan Emerging Markets Bond Index Global: Tracks U.S. dollar government bonds of 31 foreign countries.

J.P. Morgan Global Government Bond Broad Index, Non-U.S. Dollar: Tracks government bonds in 12 international markets.

Lehman Brothers Global Aggregate Ex-U.S. Dollar Bond Index: Tracks an international basket of bonds that contains 65% government, 14% corporate, 13% agency, and 8% mortgage-related bonds.

Yield curve: A graphic depiction of the relationship between yields and maturity dates for a set of similar securities, such as Treasuries or municipal securities. Securities with longer maturities usually have a higher yield. If short-term securities offer a higher yield, then the curve is said to be “inverted.” If short- and long-term bonds are offering equivalent yields, then the curve is said to be “flat.”

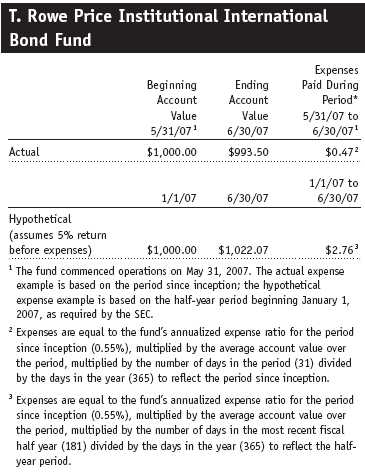

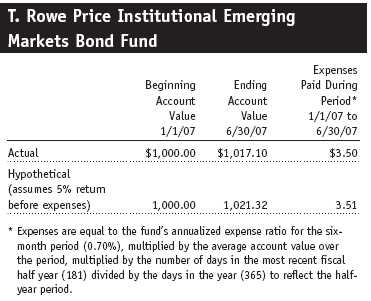

Portfolio Highlights

Performance and Expenses

T. Rowe Price Institutional Foreign Bond Funds

Fund Expense Example

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and actual expenses. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

Notes to Financial Statements

T. Rowe Price Institutional International Bond Fund

June 30, 2007 (Unaudited)

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

T. Rowe Price Institutional International Funds, Inc. (the corporation), is registered under the Investment Company Act of 1940 (the 1940 Act). The Institutional International Bond Fund (the fund), a nondiversified, open-end management investment company, is one portfolio established by the corporation. The fund commenced operations on May 31, 2007. The fund seeks to provide current income and capital appreciation.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Valuation The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business. Debt securities are generally traded in the over-the-counter market. Securities with original maturities of one year or more are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service, which considers yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities. Securities with original maturities of less than one year are valued at amortized cost in local currency, which approximates fair value when combined with accrued interest.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation. Financial futures contracts are valued at closing settlement prices. Forward currency exchange contracts are valued using the prevailing forward exchange rate. Swap agreements are valued at prices furnished by dealers who make markets in such securities.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

Most foreign markets close before the close of trading on the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, which in turn will affect the fund’s share price, the fund will adjust the previous closing prices to reflect the fair value of the securities as of the close of the NYSE, as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors. A fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. In deciding whether to make fair value adjustments, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund uses outside pricing services to provide it with closing market prices and information used for adjusting those prices. The fund cannot predict when and how often it will use closing prices and when it will adjust those prices to reflect fair value. As a means of evaluating its fair value process, the fund routinely compares closing market prices, the next day’s opening prices in the same markets, and adjusted prices.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Redemption Fees A 2% fee is assessed on redemptions of fund shares held for 90 days or less to deter short-term trading and to protect the interests of long-term shareholders. Redemption fees are withheld from proceeds that shareholders receive from the sale or exchange of fund shares. The fees are paid to the fund, and are recorded as an increase to paid-in capital. The fees may cause the redemption price per share to differ from the net asset value per share.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Any income tax-related interest and penalties would be classified as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Payments (“variation margin”) made or received to settle the daily fluctuations in the value of futures contracts are recorded as unrealized gains or losses until the contracts are closed. Unsettled variation margin on futures contracts is reflected as other assets or liabilities, and unrealized gains and lo sses on futures contracts are reflected as the change in net unrealized gain or loss in the accompanying financial statements. Unrealized gains and losses on forward currency exchange contracts are reflected as the change in net unrealized gain or loss in the accompanying financial statements. Net periodic receipts or payments required by swaps are accrued daily and recorded as realized gain or loss in the accompanying financial statements. Fluctuations in the fair value of swaps are reflected in the change in net unrealized gain or loss and are reclassified to realized gain or loss upon termination prior to maturity. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared on a daily basis and paid monthly. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

New Accounting Pronouncements Effective June 29, 2007, the fund adopted Financial Accounting Standards Board (“FASB”) Interpretation No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes, a clarification of FASB Statement No. 109, Accounting for Income Taxes. FIN 48 establishes financial accounting and disclosure requirements for recognition and measurement of tax positions taken or expected to be taken on an income tax return. The adoption of FIN 48 had no impact on the fund’s net assets or results of operations.

In September 2006, the FASB released the Statement of Financial Accounting Standard No. 157 (“FAS 157”), Fair Value Measurements. FAS 157 clarifies the definition of fair value and establishes the framework for measuring fair value, as well as proper disclosure of this methodology in the financial statements. It will be effective for the fund’s fiscal year beginning January 1, 2008. Management is evaluating the effects of FAS 157; however, it is not expected to have a material impact on the fund’s net assets or results of operations.

NOTE 2 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

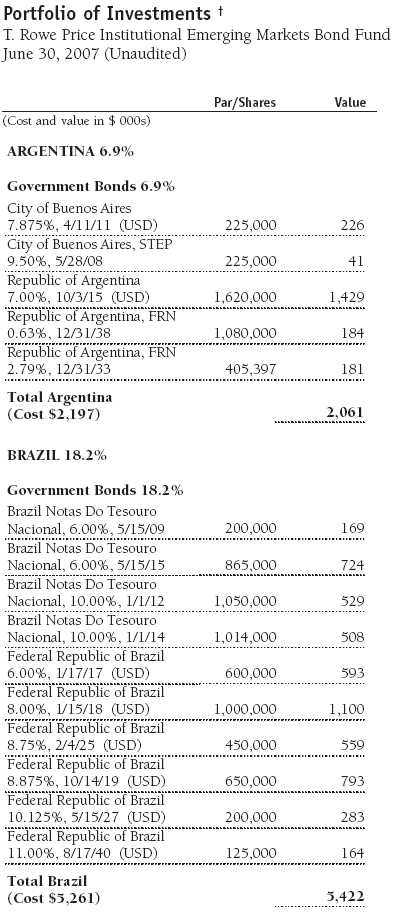

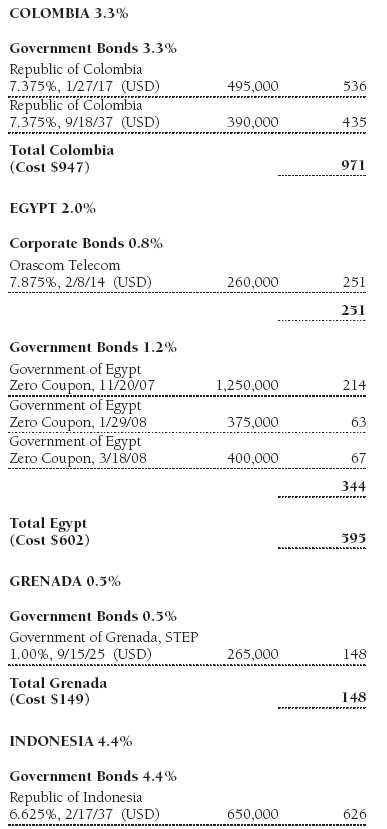

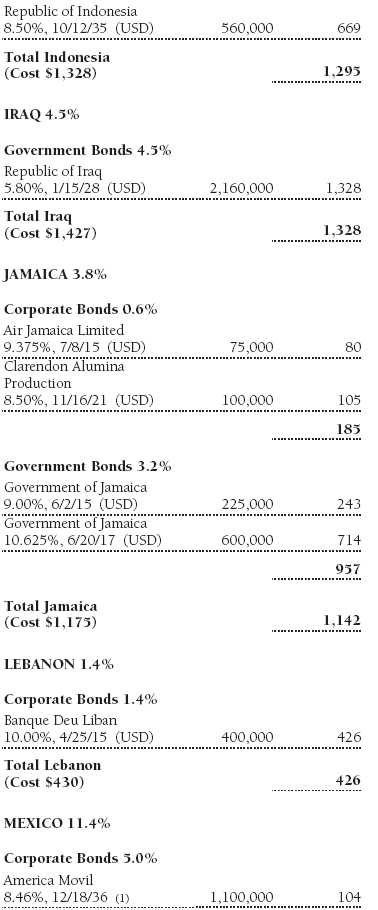

Emerging Markets At June 30, 2007, approximately 11% of the fund’s net assets were invested in securities of companies located in emerging markets or issued by governments of emerging market countries or denominated in or linked to the currencies of emerging market countries. Future economic or political developments could adversely affect the liquidity or value, or both, of such securities.

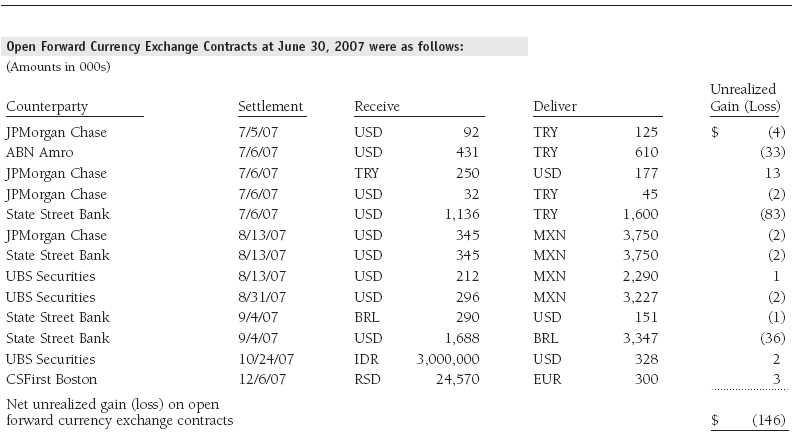

Forward Currency Exchange Contracts During the period ended June 30, 2007, the fund was a party to forward currency exchange contracts under which it is obligated to exchange currencies at specified future dates and exchange rates. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from movements in currency values.

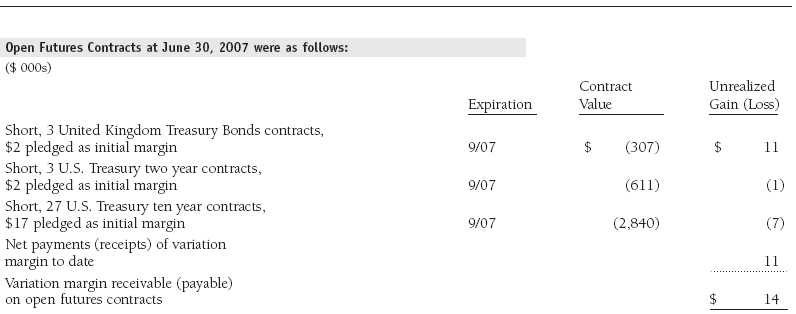

Futures Contracts During the period ended June 30, 2007, the fund was a party to futures contracts, which provide for the future sale by one party and purchase by another of a specified amount of a specific financial instrument at an agreed upon price, date, time, and place. Risks arise from possible illiquidity of the futures market and from movements in security values and/or interest rates.

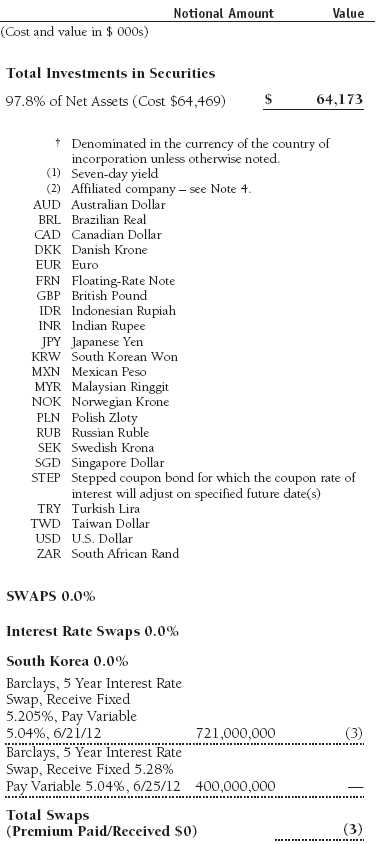

Swaps During the period ended June 30, 2007, the fund was a party to interest rate swaps under which it is obligated to exchange cash flows based on the difference between specified interest rates applied to a notional principal amount for a specified period of time. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from movements in interest rates.

Other Purchases and sales of portfolio securities, other than short-term securities, aggregated $62,103,000 and $8,601,000, respectively, for the period ended June 30, 2007.

NOTE 3 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Federal income tax regulations differ from generally accepted accounting principles; therefore, distributions determined in accordance with tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character. Financial records are not adjusted for temporary differences. The amount and character of tax-basis distributions and composition of net assets are finalized at fiscal year-end; accordingly, tax-basis balances have not been determined as of June 30, 2007.

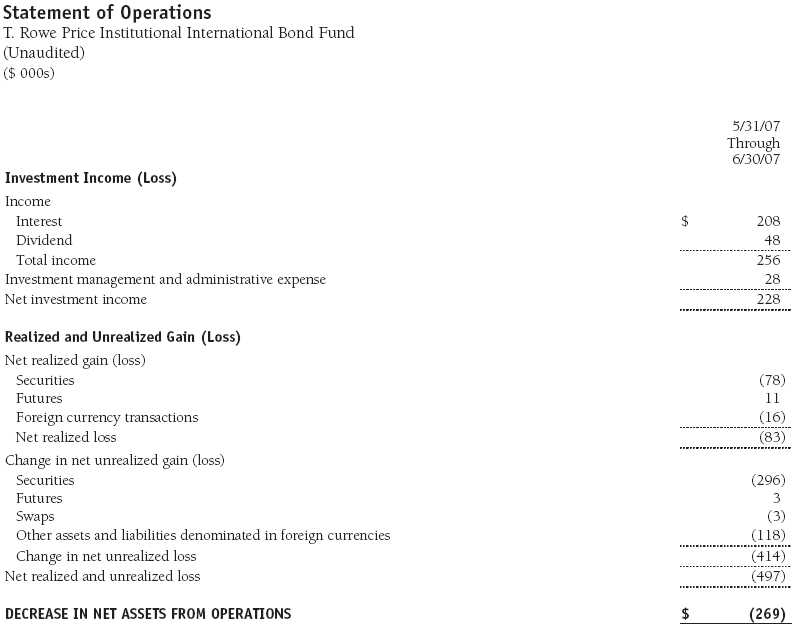

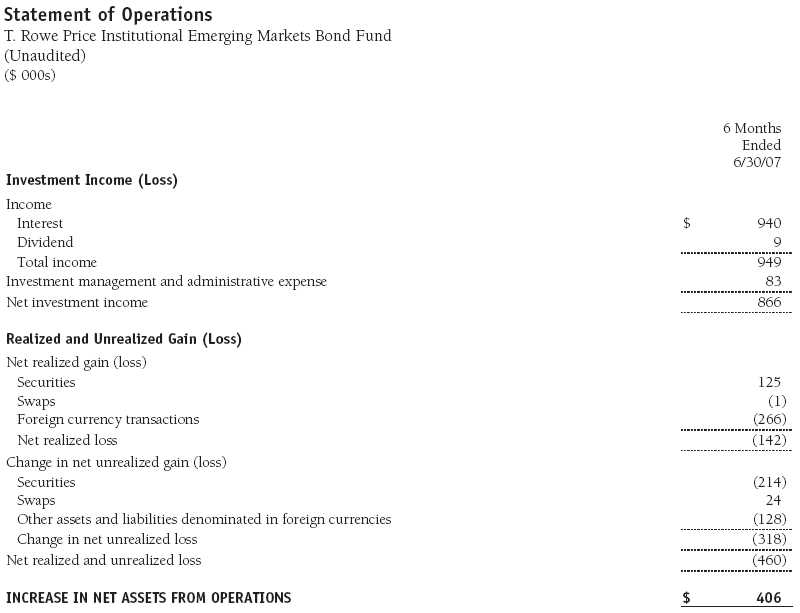

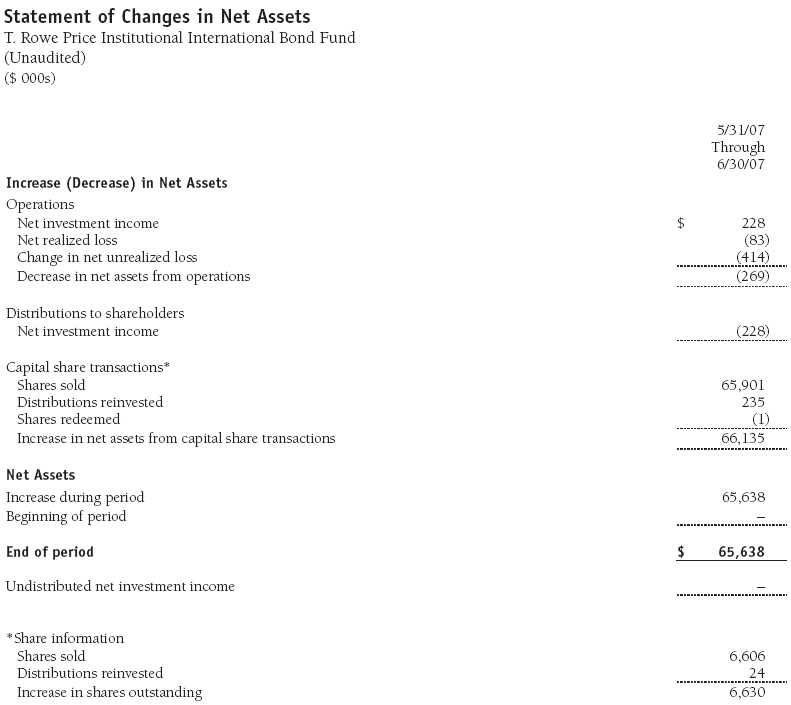

At June 30, 2007, the cost of investments for federal income tax purposes was $64,469,000. Net unrealized loss aggregated $414,000 at period-end, of which $155,000 related to appreciated investments and $569,000 related to depreciated investments.

NOTE 4 - RELATED PARTY TRANSACTIONS

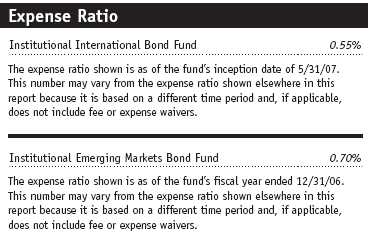

The fund is managed by T. Rowe Price International, Inc. (the manager), a wholly owned subsidiary of T. Rowe Price Associates, Inc. (Price Associates), which is wholly owned by T. Rowe Price Group, Inc. The investment management and administrative agreement between the fund and the manager provides for an all-inclusive annual fee equal to 0.55% of the fund’s average daily net assets. The fee is computed daily and paid monthly. The agreement provides that investment management, shareholder servicing, transfer agency, accounting, custody services, and directors’ fees and expenses are provided to the fund, and interest, taxes, brokerage commissions, and extraordinary expenses are paid directly by the fund.

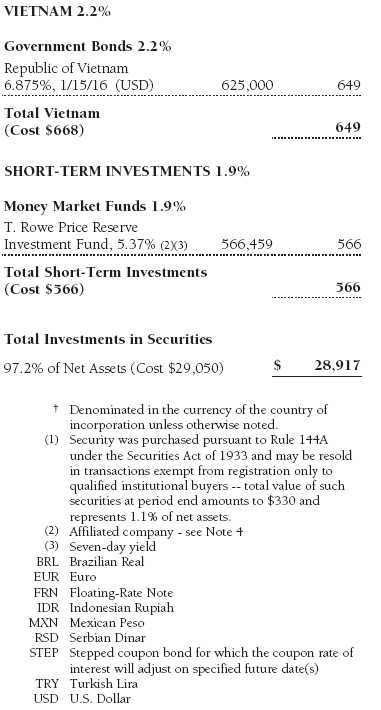

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and affiliates of the fund. The T. Rowe Price Reserve Investment Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates, and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Investment Funds pay no investment management fees. During the month ended June 30, 2007, dividend income from the T. Rowe Price Reserve Investment Funds totaled $48,000, and the value of shares of the T. Rowe Price Reserve Investment Funds held at June 30, 2007 was $5,019,000.

Mutual funds and other accounts managed by T. Rowe Price and its affiliates may invest in the fund; however, no T. Rowe Price fund may invest for the purpose of exercising management or control over the fund. At June 30, 2007, approximately 99% of the fund’s outstanding shares were held by T. Rowe Price funds.

Notes to Financial Statements

T. Rowe Price Institutional Emerging Markets Bond Fund

June 30, 2007 (Unaudited)

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

T. Rowe Price Institutional International Funds, Inc. (the corporation), is registered under the Investment Company Act of 1940 (the 1940 Act). The Institutional Emerging Markets Bond Fund (the fund), a nondiversified, open-end management investment company, is one portfolio established by the corporation. The fund commenced operations on November 29, 2006. The fund seeks to provide high income and capital appreciation.

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Valuation The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business. Debt securities are generally traded in the over-the-counter market. Securities with original maturities of one year or more are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service, which considers yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities. Securities with original maturities of less than one year are valued at amortized cost in local currency, which approximates fair value when combined with accrued interest.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation. Forward currency exchange contracts are valued using the prevailing forward exchange rate. Swap agreements are valued at prices furnished by dealers who make markets in such securities.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

Most foreign markets close before the close of trading on the NYSE. If the fund determines that developments between the close of a foreign market and the close of the NYSE will, in its judgment, materially affect the value of some or all of its portfolio securities, which in turn will affect the fund’s share price, the fund will adjust the previous closing prices to reflect the fair value of the securities as of the close of the NYSE, as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors. A fund may also fair value securities in other situations, such as when a particular foreign market is closed but the fund is open. In deciding whether to make fair value adjustments, the fund reviews a variety of factors, including developments in foreign markets, the performance of U.S. securities markets, and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The fund uses outside pricing services to provide it with closing market prices and information used for adjusting those prices. The fund cannot predict when and how often it will use closing prices and when it will adjust those prices to reflect fair value. As a means of evaluating its fair value process, the fund routinely compares closing market prices, the next day’s opening prices in the same markets, and adjusted prices.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Redemption Fees A 2% fee is assessed on redemptions of fund shares held for 90 days or less to deter short-term trading and to protect the interests of long-term shareholders. Redemption fees are withheld from proceeds that shareholders receive from the sale or exchange of fund shares. The fees are paid to the fund, and are recorded as an increase to paid-in capital. The fees may cause the redemption price per share to differ from the net asset value per share.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Any income tax-related interest and penalties would be classified as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Unrealized gains and losses on forward currency exchange contracts are reflected as the change in net unrealized gain or loss in the accompanying financial statements. Net periodic receipts or payments required by swaps are accrued daily and recorded as realized gain or loss in the accompanying financial statements. Flu ctuations in the fair value of swaps are reflected in the change in net unrealized gain or loss and are reclassified to realized gain or loss upon termination prior to maturity. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared on a daily basis and paid monthly. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

New Accounting Pronouncements Effective June 29, 2007, the fund adopted Financial Accounting Standards Board (“FASB”) Interpretation No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes, a clarification of FASB Statement No. 109, Accounting for Income Taxes. FIN 48 establishes financial accounting and disclosure requirements for recognition and measurement of tax positions taken or expected to be taken on an income tax return. The adoption of FIN 48 had no impact on the fund’s net assets or results of operations.

In September 2006, the FASB released the Statement of Financial Accounting Standard No. 157 (“FAS 157”), Fair Value Measurements. FAS 157 clarifies the definition of fair value and establishes the framework for measuring fair value, as well as proper disclosure of this methodology in the financial statements. It will be effective for the fund’s fiscal year beginning January 1, 2008. Management is evaluating the effects of FAS 157; however, it is not expected to have a material impact on the fund’s net assets or results of operations.

NOTE 2 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Emerging Markets At June 30, 2007, approximately 86% of the fund’s net assets were invested in securities of companies located in emerging markets or denominated in or linked to the currencies of emerging market countries. Future economic or political developments could adversely affect the liquidity or value, or both, of such securities.

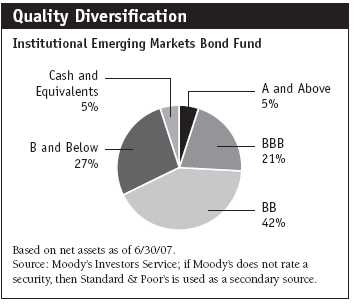

Noninvestment-Grade Debt Securities At June 30, 2007, approximately 72% of the fund’s net assets were invested in noninvestment-grade debt securities, commonly referred to as “high-yield” or “junk” bonds. A real or perceived economic downturn or higher interest rates could adversely affect the liquidity or value, or both, of such securities because such events could lessen the ability of issuers to make principal and interest payments.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Although certain of these securities may be readily sold, for example, under Rule 144A, others may be illiquid, their sale may involve substantial delays and additional costs, and prompt sale at an acceptable price may be difficult.

Forward Currency Exchange Contracts During the six months ended June 30, 2007, the fund was a party to forward currency exchange contracts under which it is obligated to exchange currencies at specified future dates and exchange rates. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from movements in currency values.

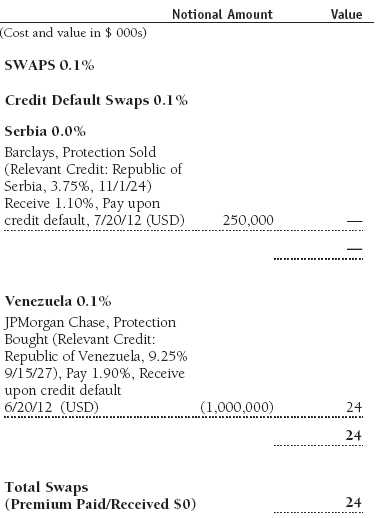

Swaps During the six months ended June 30, 2007, the fund was a party to credit default swaps under which it buys or sells credit protection against a defined-issuer credit event. Upon a defined-issuer credit event, the fund is required to either deliver the notional amount of the contract in cash and take delivery of the relevant credit or deliver cash approximately equal to the notional amount of the contract less market value of the relevant credit at the time of the credit event. Risks arise from the possible inability of counterparties to meet the terms of their agreements and from changes in creditworthiness of the relevant underlying issuer.

Other Purchases and sales of portfolio securities, other than short-term securities, aggregated $28,849,000 and $10,203,000, respectively, for the six months ended June 30, 2007.

NOTE 3 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Federal income tax regulations differ from generally accepted accounting principles; therefore, distributions determined in accordance with tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character. Financial records are not adjusted for temporary differences. The amount and character of tax-basis distributions and composition of net assets are finalized at fiscal year-end; accordingly, tax-basis balances have not been determined as of June 30, 2007.

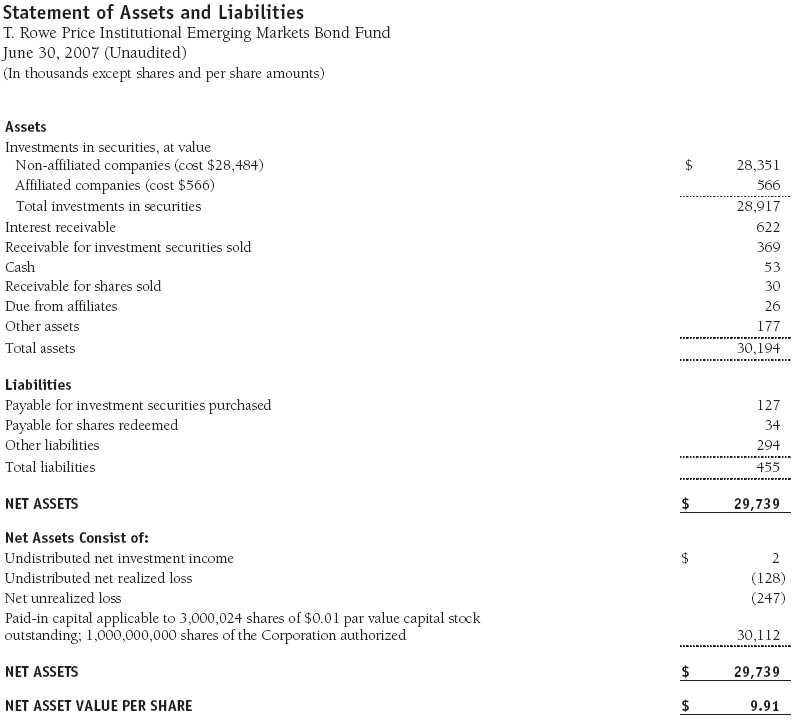

At June 30, 2007, the cost of investments for federal income tax purposes was $29,050,000. Net unrealized loss aggregated $247,000 at period-end, of which $545,000 related to appreciated investments and $792,000 related to depreciated investments.

NOTE 4 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price International, Inc. (the manager), a wholly owned subsidiary of T. Rowe Price Associates, Inc. (Price Associates), which is wholly owned by T. Rowe Price Group, Inc. The investment management and administrative agreement between the fund and the manager provides for an all-inclusive annual fee equal to 0.70% of the fund’s average daily net assets. The fee is computed daily and paid monthly. The agreement provides that investment management, shareholder servicing, transfer agency, accounting, custody services, and directors’ fees and expenses are provided to the fund, and interest, taxes, brokerage commissions, and extraordinary expenses are paid directly by the fund.

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and affiliates of the fund. The T. Rowe Price Reserve Investment Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates, and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Investment Funds pay no investment management fees. During the six months ended June 30, 2007, dividend income from the T. Rowe Price Reserve Investment Funds totaled $9,000, and the value of shares of the T. Rowe Price Reserve Investment Funds held at June 30, 2007, and December 31, 2006, was $566,000 and $69,000, respectively.

As of June 30, 2007, T. Rowe Price Group, Inc., and/or its wholly owned subsidiaries owned 1,041,510 shares of the fund, representing 35% of the fund’s net assets.

| Information on Proxy Voting Policies, Procedures, and Records |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information, which you may request by calling 1-800-225-5132 or by accessing the SEC’s Web site, www.sec.gov. The description of our proxy voting policies and procedures is also available on our Web site, www.troweprice.com. To access it, click on the words “Company Info” at the top of our homepage for individual investors. Then, in the window that appears, click on the “Proxy Voting Policy” navigation button in the top left corner.

Each fund’s most recent annual proxy voting record is available on our Web site and through the SEC’s Web site. To access it through our Web site, follow the directions above, then click on the words “Proxy Voting Record” at the bottom of the Proxy Voting Policy page.

| How to Obtain Quarterly Portfolio Holdings |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s Web site (www.sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 450 Fifth St. N.W., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| Approval of Investment Management Agreement |

On March 7, 2007, the fund’s Board of Directors (Board) unanimously approved the investment advisory contract (Contract) between the fund and its investment manager, T. Rowe Price International, Inc. (Manager). The Board considered a variety of factors in connection with its review of the Contract, also taking into account information provided by the Manager during the course of the year, as discussed below:

Services Provided by the Manager

The Board considered the nature, quality, and extent of the services provided to the fund by the Manager. These services included, but were not limited to, management of the fund’s portfolio and a variety of related activities, as well as financial and administrative services, reporting, and communications. The Board also reviewed the background and experience of the Manager’s senior management team and investment personnel involved in the management of the fund. The Board concluded that it was satisfied with the nature, quality, and extent of the services provided by the Manager.

Investment Performance of the Fund

Because the fund began operations in 2006, the Board did not review information on the fund’s investment performance.

Costs, Benefits, Profits, and Economies of Scale

The Board reviewed detailed information regarding the revenues received by the Manager under the Contract and other benefits that the Manager (and its affiliates) may have realized from its relationship with the fund, including research received under “soft dollar” agreements. The Board noted that soft dollars were not used to pay for third-party, non-broker research. The Board also received information on the estimated costs incurred and profits realized by the Manager and its affiliates from advising T. Rowe Price mutual funds, as well as estimates of the gross profits realized from managing the fund in particular. The Board concluded that the Manager’s profits were reasonable in light of the services provided to the fund. The Board also considered whether the fund or other funds benefit under the fee levels set forth in the Contract from any economies of scale realized by the Manager. Under the Contract, the fund pays a fee to the Manager composed of two components—a group fee rate based on the aggregate assets of certain T. Rowe Price mutual funds (including the fund) that declines at certain asset levels and an individual fund fee rate that is assessed on the assets of the fund. The Board concluded that the advisory fee structure for the fund continued to provide for a reasonable sharing of benefits from economies of scale with the fund’s investors.

Fees

The Board reviewed the fund’s management fee rate, operating expenses, and total expense ratio and compared them with fees and expenses of other comparable funds based on information and data supplied by Lipper. The information provided to the Board showed that the fund’s management fee and expense ratio were below the median of comparable funds. The Board also reviewed the fee schedules for comparable privately managed accounts of the Manager and its affiliates. Management informed the Board that the Manager’s responsibilities for privately managed accounts are more limited than its responsibilities for the fund and other T. Rowe Price mutual funds that it or its affiliates advise. On the basis of the information provided, the Board concluded that the fees paid by the fund under the Contract were reasonable.

Approval of the Contract

As noted, the Board approved the continuation of the Contract. No single factor was considered in isolation or to be determinative to the decision. Rather, the Board concluded, in light of a weighting and balancing of all factors considered, that it was in the best interests of the fund to approve the continuation of the Contract, including the fees to be charged for services thereunder.

Item 2. Code of Ethics.

A code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions is filed as an exhibit to the registrant’s annual Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the registrant’s most recent fiscal half-year.

Item 3. Audit Committee Financial Expert.

Disclosure required in registrant’s annual Form N-CSR.

Item 4. Principal Accountant Fees and Services.

Disclosure required in registrant’s annual Form N-CSR.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Schedule of Investments.

Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is filed with the registrant’s annual Form N-CSR.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

| | |

SIGNATURES |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the |

| undersigned, thereunto duly authorized. |

| |

| T. Rowe Price Institutional International Funds, Inc. |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | August 17, 2007 |

| |

| |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, this report has been signed below by the following persons on behalf of |

| the registrant and in the capacities and on the dates indicated. |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | August 17, 2007 |

| |

| |

| |

| By | /s/ Joseph A. Carrier |

| | Joseph A. Carrier |

| | Principal Financial Officer |

| |

| Date | August 17, 2007 |