EXHIBIT (c)(ii)

Consolidated Financial Statements of the Co-Registrant

2011–12 Report on State Finances

of the Queensland Government – 30 June 2012

Incorporating the Outcomes Report and

the AASB 1049 Financial Statements

Contents

| | | | |

| | | Page | |

| |

Message from the Treasurer | | | 2 | |

| |

Scope of the Report | | | 3 | |

| |

Outcomes Report—Uniform Presentation Framework | | | | |

| |

Overview and Analysis | | | 4-01 | |

| |

Operating Statement by Sector | | | 4-06 | |

| |

Balance Sheet by Sector | | | 4-07 | |

| |

Cash Flow Statement by Sector | | | 4-08 | |

| |

General Government Sector Taxes | | | 4-09 | |

| |

General Government Sector Dividend and Income Tax Equivalent Income | | | 4-09 | |

| |

General Government Sector Grant Revenue | | | 4-10 | |

| |

General Government Sector Grant Expenses | | | 4-10 | |

| |

General Government Sector Expenses by Function | | | 4-11 | |

| |

General Government Sector Purchases of Non-financial Assets by Function | | | 4-12 | |

| |

Loan Council Allocation | | | 4-12 | |

| |

Certification of Outcomes Report | | | 4-13 | |

| |

AASB 1049 Financial Statements | | | | |

| |

Overview and Analysis | | | 5-01 | |

| |

Audited Financial Statements | | | | |

| |

Operating Statement | | | 6-01 | |

| |

Balance Sheet | | | 6-03 | |

| |

Statement of Changes in Net Assets (Equity) | | | 6-04 | |

| |

Cash Flow Statement | | | 6-06 | |

| |

Notes to the Financial Statements | | | 6-07 | |

| |

Certification of Queensland State Government Financial Statements | | | 6-97 | |

| |

Independent Auditor’s Report to the Treasurer of Queensland | | | 6-98 | |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 1 |

Message from the Treasurer

This report provides details of Queensland’s General Government Sector’s and Total State Sector’s financial operations and position on both a Uniform Presentation Framework (Outcomes Report) and Australian Accounting Standards basis for the 2011-12 financial year.

In endorsing this report, I place on record my appreciation of the professionalism and co-operation extended to Queensland Treasury and Trade by agency personnel and of the Treasury staff involved in its preparation.

TIM NICHOLLS MP

TREASURER AND

MINISTER FOR TRADE

| | |

| 2 | | Report on State Finances 2011–12 – Government of Queensland |

Scope of the Report

The Report on State Finances, incorporating the Outcomes Report and AASB1049 Financial Statements for the General Government Sector (GGS) and Whole of Government (Total State Sector), provides a comprehensive analysis of Government finances for the 2011-12 financial year.

The Outcomes Report

The Outcomes Report contains financial statements that are prepared and presented in accordance with the Uniform Presentation Framework (UPF) agreed to at the 1991 Premiers’ Conference and revised in 2008 to align with AASB 1049 Whole of Government and General Government Sector Financial Reporting. The primary objective of the UPF is to provide uniform and comparable reporting of Commonwealth, State and Territory governments’ financial information.

Queensland’s annual Budget was prepared in accordance with the UPF, and the Outcomes Report compares achieved financial results with revised forecasts contained in the 2012-13 Budget papers.

The UPF presentation is primarily structured on a sectoral basis with a focus on the General Government and Public Non-financial Corporations Sectors.

The AASB 1049 Financial Statements

The AASB 1049 Financial Statements outline the operations of the Queensland Government on an accrual basis in accordance with Australian Accounting Standard AASB 1049 Whole of Government and General Government Sector Financial Reporting and other applicable standards. The statements present the operating statement, balance sheet and cash flows of the Queensland Total State Sector on a consolidated basis and the GGS on a partially consolidated basis.

AASB 1049 Whole of Government and General Government Sector Financial Reporting was released in October 2007. The standard aims to harmonise the Government Finance Statistics (GFS) and Accounting Standard frameworks. The GFS reporting framework, developed by the Australian Bureau of Statistics (ABS), is based on international statistical standards and allows comprehensive assessments to be made of the economic impact of government. A full set of financial statements is required for both the GGS and Total State Sector. Comparison is with the prior year, though the GGS financial statements also require analysis of variances between original published budget and actuals.

Financial statements for the General Government, Public Non-financial Corporations and Public Financial Corporations sectors are disclosed in the disaggregated information note to the financial statements (Note 2).

A full list of consolidated entities is disclosed in Note 55 of the financial statements.

Where applicable, comparatives have been restated to agree with changes in presentation in the financial statements for the current reporting period and to correct timing differences and/or errors from prior periods.

Related Publications

This report complements other key publications relating to the financial performance of the Queensland Public Sector including:

| | • | | the annual Budget papers; |

| | • | | Budget updates including the Mid Year Fiscal and Economic Review; |

| | • | | the Treasurer’s Consolidated Fund Financial Report; and |

| | • | | the annual reports of the various departments, statutory bodies, Government-owned corporations and other entities that comprise the Queensland Government. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 3 |

2011 - 2012

Outcomes Report

Uniform Presentation Framework of the

Queensland Government – 30 June 2012

Outcomes Report—Overview and Analysis

Overview

The General Government UPF net operating balance for 2011-12 was a deficit of $233 million, compared to the 2012-13 Budget estimated actual deficit of $314 million. The improvement in the result is due to slightly higher revenue across a range of categories, with expenses largely in line with those forecast for 2011-12 in the 2012-13 Budget.

Reflecting the adoption of the fiscal balance measure as a key fiscal target, this Report will provide details of the fiscal balance as well as the net operating balance. The improvement in the net operating balance combined with marginally lower capital purchases results in a General Government fiscal deficit of $5.482 billion compared to the estimated deficit of $5.623 billion.

Non-financial Public Sector capital purchases of $11.939 billion are broadly in line with the 2011-12 estimate in the 2012-13 Budget.

Summary of Key UPF Financial Aggregates

Outlined in the table below are the key aggregates, by sector.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Government | | | Public Non-financial | | | Non-financial Public | |

| | | Sector | | | Corporations Sector | | | Sector | |

| | | Est. Actual | | | Outcome | | | Est. Actual | | | Outcome | | | Est. Actual | | | Outcome | |

| | | $ million | | | $ million | | | $ million | | | $ million | | | $ million | | | $ million | |

Revenue | | | 45,707 | | | | 45,794 | | | | 10,108 | | | | 10,121 | | | | 52,178 | | | | 52,300 | |

Expenses | | | 46,021 | | | | 46,027 | | | | 9,500 | | | | 9,414 | | | | 52,741 | | | | 52,685 | |

Net operating balance | | | (314 | ) | | | (233 | ) | | | 608 | | | | 707 | | | | (563 | ) | | | (385 | ) |

Capital purchases | | | 8,069 | | | | 7,930 | | | | 3,961 | | | | 4,009 | | | | 12,030 | | | | 11,939 | |

Fiscal balance | | | (5,623 | ) | | | (5,482 | ) | | | (1,198 | ) | | | (927 | ) | | | (7,677 | ) | | | (7,267 | ) |

Borrowing | | | 30,017 | | | | 29,513 | | | | 32,656 | | | | 32,007 | | | | 62,672 | | | | 61,521 | |

Note:

| 1. | Numbers may not add due to rounding |

In response to recommendations made by the independent Commission of Audit, the Government revised the State’s fiscal principles. These new fiscal principles were included in a revised Charter of Fiscal Responsibility tabled in Parliament on 11 September 2012.

In keeping with the Charter’s requirement to regularly report progress against these principles, the following table provides an overview of the new fiscal principles and progress against them for the 2011-12 financial year:

In the 2012-13 Budget, the Government budgeted to meet the fiscal principles of :

| | • | | stabilise then significantly reduce debt (Non-financial Public Sector) |

| | • | | achieve and maintain a General Government Sector fiscal balance by 2014-15 |

and has met the fiscal principles of:

| | • | | maintain a competitive tax environment for business |

| | • | | target full funding of long term liabilities such as superannuation in accordance with actuarial advice. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-01 |

Outcomes Report—Overview and Analysis

The fiscal principles of the Queensland Government 2011-12

| | | | | | | | |

Principle | | Indicator | |

| | | | | Est. Actual | | Outcome | |

Stabilise, then significantly reduce debt (Non-financial Public sector) | | Debt to Revenue

Ratio | | 120% | | | 118% | |

| | Net Financial

Liabilities to

Revenue Ratio | | 97% | | | 105% | |

| |

| | | Fiscal balance ($ million) | |

| | | | | Est. Actual

$ million | | Outcome

$ million | |

Achieve and maintain a General Government sector fiscal balance by 2014-15 | | 2011-12 | | (5,623) | | | (5,482) | |

| | |

| | | Taxation revenue per capita | | Outcome | |

Maintain a competitive tax environment for business | | Queensland | | | | $ | 2,338 | |

| | Average of

other states | | | | $ | 2,729 | |

Target full funding of long-term liabilities such as superannuation in accordance with actuarial advice | | According to last actuarial review (as at June 2010), accruing superannuation liabilities were fully funded when the QML transaction was taken into account. The State Actuary reviews the scheme every three years. | |

The primary reason for the increase in the net financial liabilities to revenue ratio is the impact of lower bond yields on the State’s superannuation liability (not available for the 2012-13 Budget), partially offset by lower borrowings and higher than forecast revenues.

For these reasons, the above table which shows the Government’s progress in achieving its fiscal principles, also includes the debt to revenue measure which has a closer bearing to the impact of Government policy than the net financial liabilities to revenue ratio.

There has been an improvement in the State’s debt to revenue ratio primarily as a result of lower borrowings in the PNFC sector.

The improved fiscal balance is due to better than forecast outcomes related to revenue and lower than forecast capital purchases.

| | |

| 4-02 | | Report on State Finances 2011–12 – Government of Queensland |

Outcomes Report—Overview and Analysis

General Government Sector

| | | | | | | | |

General Government Revenue | | 2011-12

Est. Actual

$ million | | | 2011-12

Outcome

$ million | |

Taxation revenue | | | 10,583 | | | | 10,608 | |

Grants revenue | | | 22,606 | | | | 22,652 | |

Sales of goods and services | | | 4,971 | | | | 4,996 | |

Interest income | | | 2,475 | | | | 2,484 | |

Dividend and income tax equivalent income | | | 1,157 | | | | 1,112 | |

Other revenue | | | 3,915 | | | | 3,942 | |

Total Revenue | | | 45,707 | | | | 45,794 | |

Note:

| 1. | Numbers may not add due to rounding |

Total revenue was $87 million higher than the 2011-12 estimated actual. This was largely due to:

| • | | taxation revenue being marginally more than forecast, due to higher than expected motor vehicle registration revenue; |

| • | | lower than expected tax equivalents payments from Stanwell Corporation due to a change in the split between current and deferred tax; |

| • | | other revenue being higher than expected due to higher than estimated non-cash donations. |

| | | | | | | | |

General Government Expenses | | 2011-12

Est. Actual

$ million | | | 2011-12

Outcome

$ million | |

Employee expenses | | | 18,248 | | | | 18,250 | |

Superannuation expenses | | | | | | | | |

Superannuation interest cost | | | 1,221 | | | | 1,216 | |

Other superannuation expenses | | | 2,331 | | | | 2,301 | |

Other operating expenses | | | 8,909 | | | | 8,821 | |

Depreciation and amortisation | | | 2,765 | | | | 2,777 | |

Other interest expenses | | | 1,622 | | | | 1,659 | |

Grant expenses | | | 10,925 | | | | 11,004 | |

Total Expenses | | | 46,021 | | | | 46,027 | |

Note:

| 1. | Numbers may not add due to rounding |

Total expenses were broadly in line with expectations included in the 2012-13 Budget ($6 million greater).

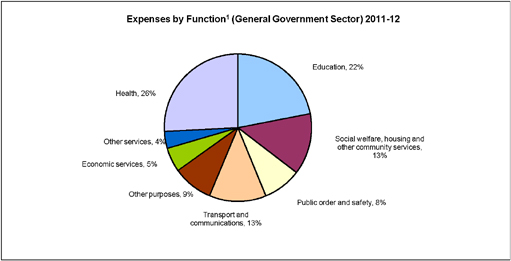

General Government Sector expenditure is focussed on the delivery of core services to the community. As shown in the chart below, education and health account for around 48% of the total.

| 1 | Refer to page 4-11 for further detail of expenses in each function. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-03 |

Outcomes Report—Overview and Analysis

Capital Purchases

General Government sector purchases of non-financial assets (i.e. capital expenditure) totalled $7.93 billion which was $139 million less than the 2012-13 Budget estimate of 2011-12 capital purchases.

Fiscal Balance

The fiscal balance or net lending/borrowing aggregate shows how much of the acquisition of non-financial assets is financed by the net operating balance (excluding depreciation) and how much by borrowing.

The improvement in the net operating balance combined with marginally lower capital purchases results in a fiscal deficit of $5.482 billion compared to the Budget time estimate of $5.623 billion.

Borrowing

Borrowing for the General Government sector was $29.513 billion, $504 million less than forecast in the 2012-13 Budget due to a combination of the improved fiscal balance and a change in the valuation of borrowings to amortised cost.

Net Worth

The General Government’s net worth was $170.653 billion as at 30 June 2012, 0.8% higher than the estimated actual included in the 2012-13 Budget. The increase relates to the revaluation of the investment in other public sector entities and land and other fixed assets, offset by the increase in the State’s superannuation liability.

An accounting standard revision to the valuation of investments in public sector entities with negative equity resulted in an upward valuation of $3.7 billion compared to 2012-13 Budget. Increases in the valuation of non-financial assets were mainly the reversal of previous write downs to infrastructure damaged in the floods which has now been restored. The valuation had not been completed at the time of the Budget.

These increases in net worth were largely offset by the revaluation of the superannuation liability which was finalised after the 2012-13 Budget was published. Under AASB 119 Employee Entitlements a floating discount rate based on Commonwealth bond yields is used to estimate the present value of liabiliites. Bond yield fluctuations lead to major variances in liability estimates over time. In the current global environment, Australian Government bonds are seen as a safe haven for international investors. As such, yields have fallen to historical lows, creating significant volatility in the estimate. The increase in the liability will be reversed as bond yields recover.

The bond yields used to discount the liability have declined since the previous year from 5.3% to 3.2%, and the lower discount rate has largely resulted in an increase in the provision by $5.2 billion.

Operating Result

The operating result represents the result for the State under the Accounting Standards framework. The GGS operating result of negative $391 million differs from the net operating balance as it includes valuation adjustments such as gains and losses on financial and non-financial assets, and deferred tax revenue.

Comprehensive Result—Total Change in Net Worth

The comprehensive result includes revaluation of assets taken to reserves. The deterioration between the estimated actual and the actual result is due mainly to the revaluations, superannuation liabilities, investments and non-financial assets discussed above.

Public Non-financial Corporations (PNFC) Sector

The Public Non-financial Corporations sector comprises bodies such as Government-owned corporations that mainly engage in the production of goods and services (of a non-financial nature) for sale in the market place at prices that aim to recover most of the costs involved:

| • | | The PNFC Sector recorded a net operating surplus of $707 million, $99 million higher than forecast mainly due to lower employee costs and marginally lower income tax equivalent payments to the General Government sector; |

| • | | The fiscal balance was a deficit of $927 million, compared to an estimated deficit of $1.198 billion. The improved position reflects the higher than forecast net operating balance and higher proceeds on the sale of non-financial assets; |

| • | | The net worth of the Sector has increased mainly due to a technical change in the valuation of borrowings. |

| | |

| 4-04 | | Report on State Finances 2011–12 – Government of Queensland |

Outcomes Report—Overview and Analysis

State Financial (Total State) Sector

The Total State Sector includes all State Government departments and statutory authorities, public non-financial corporations, public financial corporations and their controlled entities. All material inter-entity and intra-entity transactions and balances have been eliminated to the extent practicable:

| • | | The net operating balance was a deficit of $2.058 billion for 2011-12; |

| • | | The Total State Sector cash deficit was $8.54 billion for 2011-12 after allowing for purchases of non-financial assets of $12.048 billion; |

| • | | The Total State Sector fiscal deficit was $9.004 billion; and |

| • | | The Total State Sector net worth was $161.958 billion and reflects the effect of market value adjustments on borrowings and superannuation liabilities as a result of lower bond yields. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-05 |

2011-12 Operating Statement by Sector ($million)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

| | Revenue from Transactions | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Taxation revenue | | | 10,583 | | | | 10,608 | | | | — | | | | — | | | | 10,281 | | | | 10,285 | | | | — | | | | 10,280 | |

| | Grants revenue | | | 22,606 | | | | 22,652 | | | | 2,149 | | | | 2,140 | | | | 22,798 | | | | 22,856 | | | | — | | | | 22,815 | |

| | Sales of goods and services | | | 4,971 | | | | 4,996 | | | | 7,352 | | | | 7,348 | | | | 12,070 | | | | 12,062 | | | | 1,651 | | | | 13,461 | |

| | Interest income | | | 2,475 | | | | 2,484 | | | | 130 | | | | 157 | | | | 2,605 | | | | 2,641 | | | | 4,798 | | | | 1,673 | |

| | Dividend and income tax equivalent income | | | 1,157 | | | | 1,112 | | | | 61 | | | | 61 | | | | 94 | | | | 100 | | | | — | | | | 63 | |

| | Other revenue | | | 3,915 | | | | 3,942 | | | | 416 | | | | 415 | | | | 4,329 | | | | 4,356 | | | | 130 | | | | 4,439 | |

| | Total Revenue from Transactions | | | 45,707 | | | | 45,794 | | | | 10,108 | | | | 10,121 | | | | 52,178 | | | | 52,300 | | | | 6,579 | | | | 52,732 | |

| | | | | | | | | |

| Less | | Expenses from Transactions | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Employee expenses | | | 18,248 | | | | 18,250 | | | | 1,776 | | | | 1,618 | | | | 19,936 | | | | 19,767 | | | | 231 | | | | 19,773 | |

| | Superannuation expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Superannuation interest cost | | | 1,221 | | | | 1,216 | | | | — | | | | (22 | ) | | | 1,221 | | | | 1,195 | | | | — | | | | 1,195 | |

| | Other superannuation expenses | | | 2,331 | | | | 2,301 | | | | 213 | | | | 227 | | | | 2,544 | | | | 2,527 | | | | 16 | | | | 2,543 | |

| | Other operating expenses | | | 8,909 | | | | 8,821 | | | | 3,100 | | | | 3,204 | | | | 11,753 | | | | 11,732 | | | | 1,578 | | | | 13,278 | |

| | Depreciation and amortisation | | | 2,765 | | | | 2,777 | | | | 2,072 | | | | 2,064 | | | | 4,837 | | | | 4,841 | | | | 45 | | | | 4,886 | |

| | Other interest expenses | | | 1,622 | | | | 1,659 | | | | 2,049 | | | | 2,088 | | | | 3,466 | | | | 3,542 | | | | 6,304 | | | | 4,033 | |

| | Grants expenses | | | 10,925 | | | | 11,004 | | | | 16 | | | | 14 | | | | 8,985 | | | | 9,081 | | | | 42 | | | | 9,081 | |

| | Other property expenses | | | — | | | | — | | | | 273 | | | | 221 | | | | — | | | | — | | | | 21 | | | | — | |

| | Total Expenses from Transactions | | | 46,021 | | | | 46,027 | | | | 9,500 | | | | 9,414 | | | | 52,741 | | | | 52,685 | | | | 8,236 | | | | 54,789 | |

| | | | | | | | | |

Equals | | Net Operating Balance | | | (314 | ) | | | (233 | ) | | | 608 | | | | 707 | | | | (563 | ) | | | (385 | ) | | | (1,657 | ) | | | (2,058 | ) |

| | Other economic flows - included in operating result | | | (435 | ) | | | (159 | ) | | | (334 | ) | | | (560 | ) | | | (851 | ) | | | (801 | ) | | | 2,117 | | | | (2,397 | ) |

| | Operating Result | | | (749 | ) | | | (391 | ) | | | 274 | | | | 147 | | | | (1,414 | ) | | | (1,185 | ) | | | 460 | | | | (4,455 | ) |

| | Other economic flows - other movements in equity | | | (2,641 | ) | | | (6,830 | ) | | | (1,421 | ) | | | (1,455 | ) | | | (2,011 | ) | | | (6,333 | ) | | | (17 | ) | | | (6,543 | ) |

| | Comprehensive Result - Total Change in Net Worth | | | (3,390 | ) | | | (7,222 | ) | | | (1,147 | ) | | | (1,308 | ) | | | (3,425 | ) | | | (7,518 | ) | | | 443 | | | | (10,998 | ) |

| | | | | | | | | |

| | KEY FISCAL AGGREGATES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

| | Net Operating Balance | | | (314 | ) | | | (233 | ) | | | 608 | | | | 707 | | | | (563 | ) | | | (385 | ) | | | (1,657 | ) | | | (2,058 | ) |

| | | | | | | | | |

| Less | | Net Acquisition of Non-financial Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Purchases of non-financial assets | | | 8,069 | | | | 7,930 | | | | 3,961 | | | | 4,009 | | | | 12,030 | | | | 11,939 | | | | 109 | | | | 12,048 | |

| | Less Sales of non-financial assets | | | 267 | | | | 198 | | | | 177 | | | | 361 | | | | 444 | | | | 559 | | | | — | | | | 559 | |

| | Less Depreciation | | | 2,765 | | | | 2,777 | | | | 2,072 | | | | 2,064 | | | | 4,837 | | | | 4,841 | | | | 45 | | | | 4,886 | |

| | Plus Change in inventories | | | 36 | | | | 55 | | | | 53 | | | | 13 | | | | 89 | | | | 68 | | | | — | | | | 68 | |

| | Plus Other movements in non-financial assets | | | 235 | | | | 238 | | | | 40 | | | | 37 | | | | 276 | | | | 275 | | | | — | | | | 275 | |

| | Equals Total Net Acquisition of Non-financial Assets | | | 5,309 | | | | 5,249 | | | | 1,806 | | | | 1,634 | | | | 7,114 | | | | 6,882 | | | | 64 | | | | 6,947 | |

| | | | | | | | | |

| | Equals Net Lending / (Borrowing) | | | (5,623 | ) | | | (5,482 | ) | | | (1,198 | ) | | | (927 | ) | | | (7,677 | ) | | | (7,267 | ) | | | (1,721 | ) | | | (9,004 | ) |

| Notes | (a) Numbers may not add due to rounding. |

(b) In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation.

| | |

| 4-06 | | Report on State Finances 2011–12 – Government of Queensland |

2011-12 Balance Sheet by Sector ($million)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financial assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and deposits | | | 902 | | | | 865 | | | | 2,362 | | | | 2,401 | | | | 3,264 | | | | 3,267 | | | | 71 | | | | 1,529 | |

Advances paid | | | 569 | | | | 687 | | | | 269 | | | | 256 | | | | 827 | | | | 932 | | | | — | | | | 932 | |

Investments, loans and placements | | | 34,218 | | | | 34,239 | | | | 285 | | | | 473 | | | | 34,502 | | | | 34,712 | | | | 122,156 | | | | 59,781 | |

Receivables | | | 3,890 | | | | 4,087 | | | | 2,087 | | | | 2,097 | | | | 4,706 | | | | 4,995 | | | | 232 | | | | 5,174 | |

Equity | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Investments in other public sector entities | | | 17,226 | | | | 21,602 | | | | — | | | | — | | | | (1,419 | ) | | | 652 | | | | — | | | | — | |

Investments — other | | | 121 | | | | 148 | | | | 3,002 | | | | 2,916 | | | | 3,028 | | | | 3,064 | | | | 1 | | | | 3,065 | |

Total financial assets | | | 56,926 | | | | 61,628 | | | | 8,005 | | | | 8,143 | | | | 44,908 | | | | 47,621 | | | | 122,460 | | | | 70,480 | |

| | | | | | | | |

Non-financial Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Land and other fixed assets | | | 174,426 | | | | 176,187 | | | | 51,880 | | | | 51,949 | | | | 226,305 | | | | 228,135 | | | | 375 | | | | 228,510 | |

Other non-financial assets | | | 5,908 | | | | 5,758 | | | | 1,089 | | | | 1,326 | | | | 681 | | | | 756 | | | | 505 | | | | 757 | |

Total Non-financial Assets | | | 180,333 | | | | 181,945 | | | | 52,969 | | | | 53,275 | | | | 226,985 | | | | 228,891 | | | | 881 | | | | 229,267 | |

| | | | | | | | |

Total assets | | | 237,259 | | | | 243,573 | | | | 60,973 | | | | 61,418 | | | | 271,894 | | | | 276,512 | | | | 123,341 | | | | 299,748 | |

| | | | | | | | |

Liabilities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Payables | | | 3,818 | | | | 3,888 | | | | 2,230 | | | | 2,233 | | | | 4,816 | | | | 4,972 | | | | 170 | | | | 5,090 | |

Superannuation liability | | | 25,461 | | | | 30,626 | | | | (97 | ) | | | 230 | | | | 25,364 | | | | 30,856 | | | | — | | | | 30,856 | |

Other employee benefits | | | 4,911 | | | | 5,096 | | | | 690 | | | | 766 | | | | 5,602 | | | | 5,862 | | | | 90 | | | | 5,952 | |

Deposits held | | | 19 | | | | 1 | | | | 22 | | | | 22 | | | | 41 | | | | 23 | | | | 5,208 | | | | 3,403 | |

Advances received | | | 270 | | | | 425 | | | | 11 | | | | 11 | | | | 270 | | | | 425 | | | | — | | | | 425 | |

Borrowing | | | 30,017 | | | | 29,513 | | | | 32,656 | | | | 32,007 | | | | 62,672 | | | | 61,521 | | | | 116,464 | | | | 85,928 | |

Other liabilities | | | 3,495 | | | | 3,371 | | | | 6,721 | | | | 6,712 | | | | 3,861 | | | | 3,714 | | | | 2,927 | | | | 6,137 | |

Total liabilities | | | 67,991 | | | | 72,920 | | | | 42,233 | | | | 41,982 | | | | 102,625 | | | | 107,374 | | | | 124,859 | | | | 137,790 | |

| | | | | | | | |

Net Worth | | | 169,268 | | | | 170,653 | | | | 18,741 | | | | 19,436 | | | | 169,268 | | | | 169,138 | | | | (1,519 | ) | | | 161,958 | |

Net Financial Worth | | | (11,065 | ) | | | (11,292 | ) | | | (34,228 | ) | | | (33,839 | ) | | | (57,717 | ) | | | (59,753 | ) | | | (2,399 | ) | | | (67,310 | ) |

Net Financial Liabilities | | | 28,291 | | | | 32,894 | | | | N/A | | | | N/A | | | | 56,298 | | | | 60,405 | | | | N/A | | | | 67,310 | |

Net Debt | | | (5,384 | ) | | | (5,851 | ) | | | 29,772 | | | | 28,911 | | | | 24,389 | | | | 23,059 | | | | (555 | ) | | | 27,514 | |

| (a) | Numbers may not add due to rounding. |

| (b) | In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation. |

| (c) | Estimated Actuals have been restated where subsequent changes in classification have occurred, to ensure comparability with estimates. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-07 |

2011-12 Cash Flow Statement by Sector ($million)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

Cash Receipts from Operating Activities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Taxes received | | | 10,615 | | | | 10,656 | | | | — | | | | — | | | | 10,295 | | | | 10,316 | | | | — | | | | 10,311 | |

Grants and subsidies received | | | 22,718 | | | | 22,749 | | | | 2,253 | | | | 2,273 | | | | 22,918 | | | | 22,946 | | | | — | | | | 22,904 | |

Sales of goods and services | | | 5,163 | | | | 5,245 | | | | 7,709 | | | | 7,761 | | | | 12,436 | | | | 12,682 | | | | 1,779 | | | | 14,184 | |

Interest receipts | | | 2,481 | | | | 2,480 | | | | 130 | | | | 157 | | | | 2,611 | | | | 2,637 | | | | 4,786 | | | | 1,658 | |

Dividends and income tax equivalents | | | 1,092 | | | | 1,087 | | | | 61 | | | | 61 | | | | 107 | | | | 123 | | | | — | | | | 63 | |

Other receipts | | | 6,078 | | | | 5,921 | | | | 215 | | | | 314 | | | | 6,293 | | | | 6,234 | | | | 151 | | | | 6,330 | |

Total | | | 48,148 | | | | 48,138 | | | | 10,368 | | | | 10,566 | | | | 54,661 | | | | 54,938 | | | | 6,717 | | | | 55,451 | |

Cash Payments for Operating Activities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Payments for employees | | | (21,264 | ) | | | (21,289 | ) | | | (1,999 | ) | | | (1,753 | ) | | | (23,174 | ) | | | (22,941 | ) | | | (243 | ) | | | (22,959 | ) |

Payments for goods and services | | | (10,748 | ) | | | (10,687 | ) | | | (3,093 | ) | | | (3,418 | ) | | | (13,421 | ) | | | (13,778 | ) | | | (164 | ) | | | (13,898 | ) |

Grants and subsidies | | | (10,962 | ) | | | (11,063 | ) | | | (13 | ) | | | (9 | ) | | | (8,924 | ) | | | (9,000 | ) | | | (42 | ) | | | (9,000 | ) |

Interest paid | | | (1,630 | ) | | | (1,667 | ) | | | (1,804 | ) | | | (1,838 | ) | | | (3,229 | ) | | | (3,305 | ) | | | (6,373 | ) | | | (4,116 | ) |

Other payments | | | (577 | ) | | | (599 | ) | | | (858 | ) | | | (935 | ) | | | (1,098 | ) | | | (1,222 | ) | | | (1,372 | ) | | | (2,528 | ) |

Total | | | (45,181 | ) | | | (45,306 | ) | | | (7,767 | ) | | | (7,954 | ) | | | (49,846 | ) | | | (50,246 | ) | | | (8,193 | ) | | | (52,501 | ) |

| | | | | | | | |

Net Cash Inflows from Operating Activities | | | 2,967 | | | | 2,832 | | | | 2,601 | | | | 2,613 | | | | 4,814 | | | | 4,692 | | | | (1,477 | ) | | | 2,950 | |

| | | | | | | | |

Cash Flows from Investments in Non-financial Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Purchases of non-financial assets | | | (8,069 | ) | | | (7,930 | ) | | | (3,961 | ) | | | (4,009 | ) | | | (12,030 | ) | | | (11,939 | ) | | | (109 | ) | | | (12,048 | ) |

Sales of non-financial assets | | | 267 | | | | 198 | | | | 177 | | | | 361 | | | | 444 | | | | 559 | | | | — | | | | 559 | |

Total | | | (7,802 | ) | | | (7,732 | ) | | | (3,784 | ) | | | (3,648 | ) | | | (11,586 | ) | | | (11,380 | ) | | | (109 | ) | | | (11,489 | ) |

| | | | | | | | |

Net Cash Flows from Investments in Financial | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Assets for Policy Purposes | | | 1,271 | | | | 1,260 | | | | 110 | | | | (8 | ) | | | 120 | | | | (8 | ) | | | — | | | | 6 | |

| | | | | | | | |

Net Cash Flows for Investments in Financial | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Assets for Liquidity Purposes | | | (872 | ) | | | (837 | ) | | | (4 | ) | | | (27 | ) | | | (876 | ) | | | (864 | ) | | | 4,316 | | | | 4,198 | |

| | | | | | | | |

Receipts from Financing Activities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Advances received (net) | | | (174 | ) | | | (19 | ) | | | — | | | | (1 | ) | | | (174 | ) | | | (19 | ) | | | — | | | | (19 | ) |

Borrowing (net) | | | 6,305 | | | | 6,161 | | | | 1,306 | | | | 1,354 | | | | 7,611 | | | | 7,514 | | | | (9,215 | ) | | | (1,457 | ) |

Dividends paid | | | — | | | | — | | | | (753 | ) | | | (753 | ) | | | — | | | | — | | | | (20 | ) | | | — | |

Deposits received (net) | | | 12 | | | | — | | | | 2 | | | | 2 | | | | 14 | | | | 2 | | | | 392 | | | | 578 | |

Other financing (net) | | | (5 | ) | | | — | | | | (1,257 | ) | | | (1,272 | ) | | | (1 | ) | | | (12 | ) | | | 6,162 | | | | 5,403 | |

Total | | | 6,138 | | | | 6,142 | | | | (703 | ) | | | (669 | ) | | | 7,449 | | | | 7,485 | | | | (2,681 | ) | | | 4,505 | |

| | | | | | | | |

Net Increase/(Decrease) in Cash Held | | | 1,702 | | | | 1,664 | | | | (1,780 | ) | | | (1,740 | ) | | | (78 | ) | | | (75 | ) | | | 49 | | | | 170 | |

| | | | | | | | |

Net cash from operating activities | | | 2,967 | | | | 2,832 | | | | 2,601 | | | | 2,613 | | | | 4,814 | | | | 4,692 | | | | (1,477 | ) | | | 2,950 | |

Net cash from investments in non-financial assets | | | (7,802 | ) | | | (7,732 | ) | | | (3,784 | ) | | | (3,648 | ) | | | (11,586 | ) | | | (11,380 | ) | | | (109 | ) | | | (11,489 | ) |

Dividends paid | | | — | | | | — | | | | (753 | ) | | | (753 | ) | | | — | | | | — | | | | (20 | ) | | | — | |

Cash Surplus/(Deficit) | | | (4,836 | ) | | | (4,901 | ) | | | (1,936 | ) | | | (1,788 | ) | | | (6,772 | ) | | | (6,689 | ) | | | (1,606 | ) | | | (8,540 | ) |

Derivation of ABS GFS Cash Surplus/Deficit | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash surplus/(deficit) | | | (4,836 | ) | | | (4,901 | ) | | | (1,936 | ) | | | (1,788 | ) | | | (6,772 | ) | | | (6,689 | ) | | | (1,606 | ) | | | (8,540 | ) |

Acquisitions under finance leases and similar arrangements | | | (67 | ) | | | (95 | ) | | | — | | | | — | | | | (67 | ) | | | (95 | ) | | | — | | | | (95 | ) |

ABS GFS Cash Surplus/(Deficit) Including | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Finance Leases and Similar Arrangements | | | (4,902 | ) | | | (4,996 | ) | | | (1,936 | ) | | | (1,788 | ) | | | (6,838 | ) | | | (6,784 | ) | | | (1,606 | ) | | | (8,635 | ) |

| Notes | (a) Numbers may not add due to rounding. |

(b) In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation.

| | |

| 4-08 | | Report on State Finances 2011–12 – Government of Queensland |

Other General Government UPF Data

Data in the following tables is presented in accordance with the Uniform Presentation Framework.

General Government Sector Taxes

| | | | |

| | | 2011-12

Outcome

$ million | |

Taxes on employers’ payroll and labour force | | | 3,462 | |

Taxes on property | | | | |

Land taxes | | | 1,013 | |

Stamp duties on financial and capital transactions | | | 2,023 | |

Other | | | 573 | |

Taxes on the provision of goods and services | | | | |

Taxes on gambling | | | 998 | |

Taxes on insurance | | | 610 | |

Taxes on use of goods and performance of activities | | | | |

Motor vehicle taxes | | | 1,897 | |

Other | | | 31 | |

Total Taxation Revenue | | | 10,608 | |

Note:

| 1. | Numbers may not add due to rounding. |

General Government Sector

Dividend and Income Tax Equivalent Income

| | | | |

| | | 2011-12

Outcome

$ million | |

Dividend and Income Tax Equivalent income from PNFC sector | | | 1,073 | |

Dividend and Income Tax Equivalent income from PFC sector | | | 36 | |

Other Dividend and Income Tax Equivalent income | | | 2 | |

Total Dividend and Income Tax Equivalent income | | | 1,112 | |

Note:

| 1. | Numbers may not add due to rounding. |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-09 |

Other General Government UPF Data

General Government Sector Grant Revenue

| | | | |

| | | 2011-12

Outcome

$ million | |

Current grant revenue | | | | |

Current grants from the Commonwealth | | | | |

General purpose grants | | | 8,683 | |

Specific purpose grants | | | 5,911 | |

Specific purpose grants for on-passing | | | 2,288 | |

Total current grants from the Commonwealth | | | 16,881 | |

Other contributions and grants | | | 373 | |

Total current grant revenue | | | 17,255 | |

Capital grant revenue | | | | |

Capital grants from the Commonwealth | | | | |

Specific purpose grants | | | 5,351 | |

Specific purpose grants for on-passing | | | 2 | |

Total capital grants from the Commonwealth | | | 5,353 | |

Other contributions and grants | | | 45 | |

Total capital grant revenue | | | 5,398 | |

Total grant revenue | | | 22,652 | |

Note:

| 1. | Numbers may not add due to rounding. |

General Government Sector Grant Expenses

| | | | |

| | | 2011-12

Outcome

$ million | |

Current grant expenses | | | | |

Private and Not-for-profit sector | | | 4,052 | |

Private and Not-for-profit sector on-passing | | | 1,744 | |

Local Government | | | 236 | |

Local Government on-passing | | | 542 | |

Grants to other sectors of Government | | | 2,085 | |

Other | | | 367 | |

Total current grant expense | | | 9,026 | |

Capital grant expenses | | | | |

Private and Not-for-profit sector | | | 440 | |

Local Government | | | 1,250 | |

Households sector on-passing | | | 1 | |

Grants to other sectors of Government | | | 72 | |

Other | | | 215 | |

Total capital grant expenses | | | 1,978 | |

Total grant expenses | | | 11,004 | |

Note:

| 1. | Numbers may not add due to rounding. |

| | |

| 4-10 | | Report on State Finances 2011–12 – Government of Queensland |

General Government Sector Expenses by Function

| | | | | | | | | | |

| | | 2011-12

Outcome

$ million | | | | | 2011-12

Outcome

$ million | |

General Public Services Other general public services Public Order and Safety Police and fire protection services Law courts and legal services Prisons and corrective services Other public order and safety Education Primary and secondary education Tertiary education Pre-school education and education not definable by level Transportation of students Education n.e.c. Health Acute care institutions Mental health institutions Nursing homes for the aged Community health services Public health services Health research Health administration n.e.c. Social Security and Welfare Welfare services Social security and welfare n.e.c. Housing and Community Amenities Housing and community development Water Supply Sanitation and protection of the environment Other community amenities Recreation and Culture Recreation facilities and services Cultural facilities and services Recreation and cultural n.e.c. | |

| 1,706

1,706 3,873 2,406 736 635 97 10,095 7,977 852 1,051 157 59 11,881 7,933 338 284 2,576 416 141 193 3,356 3,312 44 1,779 1,278 166 333 2 1,057 670 325 62 |

| | Fuel and Energy Fuel affairs and services Electricity and other energy Fuel and energy n.e.c. Agriculture, Forestry, Fishing and Hunting Agriculture Forestry, fishing and hunting Mining, manufacturing and construction Mining and mineral resources other

than fuels Construction Transport and Communications Road transport Water transport Rail transport Air transport Other transport Communications Other Economic Affairs Tourism and area promotion Labour and employment affairs Other economic affairs Other Purposes Nominal superannuation interest Public debt transactions General purpose inter-government transactions Natural disaster relief Other purposes n.e.c. | |

| 518

89 420 8 776 719 57 252 94 158 5,756 2,956 58 368 11 2,358 5 912 119 638 155 4,067 1,216 1,666 542 502 141 |

|

| | | | | | | |

| | | Total | | | 46,027 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-11 |

General Government Sector Purchases of Non-financial Assets by

Function and Loan Council Allocation

General Government Sector

Purchases of Non-financial Assets by Function

| | | | |

| | | 2011-12 | |

| | | Outcome | |

| | | $ million | |

General public services | | | 155 | |

Public order and safety | | | 552 | |

Education | | | 643 | |

Health | | | 1,863 | |

Social security and welfare | | | 156 | |

Housing and community amenities | | | 363 | |

Recreation and culture | | | 78 | |

Fuel and energy | | | 1 | |

Agriculture, forestry, fishing and hunting | | | 20 | |

Mining, manufacturing and construction | | | 2 | |

Transport and communications | | | 4,062 | |

Other economic affairs | | | 1 | |

Other purposes | | | 35 | |

Total | | | 7,930 | |

Note:

| 1. | Numbers may not add due to rounding |

Loan Council Allocation

The Australian Loan Council requires all jurisdictions to advise the Loan Council Allocation (LCA) outcome for the last financial year as part of the annual Outcomes Report. The LCA represents each government’s call on financial markets for a given financial year. A tolerance limit of two percent of Non-financial Public Sector receipts applies between the LCA budget update and the outcome. The LCA outcome exceeds the Budget estimate by more than this.

The main reason for the lower GG sector cash deficit is higher grant revenue from the Commonwealth largely in relation to disaster relief funding. The main reason for the lower PNFC Sector cash deficit is lower capital expenditure on electricity and rail infrastructure following reviews of their spending.

| | | | | | | | |

| | | 2011-12 | | | 2011-12 | |

| | | Budget | | | Outcome | |

| | | $ million | | | $ million | |

General Government Sector cash deficit/(surplus) 1 | | | 7,915 | | | | 4,901 | |

PNFC Sector cash deficit/(surplus)1 | | | 3,793 | | | | 1,788 | |

Non-financial Public Sector cash deficit/(surplus)1 | | | 11,710 | | | | 6,689 | |

Acquisitions under finance leases and similar arrangements | | | (67 | ) | | | (95 | ) |

ABS GFS cash deficit/(surplus) | | | 11,776 | | | | 6,784 | |

Net cash flows from investments in financial assets for policy purposes | | | 128 | | | | (8 | ) |

Memorandum items2 | | | 1,992 | | | | 1,692 | |

LOAN COUNCIL ALLOCATION | | | 13,640 | | | | 8,484 | |

Notes:

| 1. | Figures in brackets represent surpluses |

| 2. | Other memorandum items include operating leases and local government borrowings |

| | |

| 4-12 | | Report on State Finances 2011–12 – Government of Queensland |

Certification of Outcomes Report

Management Certification

The foregoing Outcomes Report contains financial statements for the Queensland State Government, prepared and presented in accordance with the Uniform Presentation Framework (UPF) agreed to at the 1991 Premiers’ Conference and revised in 2008 to align with AASB 1049 Whole of Government and General Government Sector Financial Reporting.

This report separately discloses outcomes for the General Government, Public Non-financial Corporations, Public Financial Corporations and State Financial sectors within Queensland. Entities excluded from this report include local governments and universities. Queensland public sector entities consolidated for this report are listed in the AASB 1049 Financial Statements, taking into account intra and inter-agency eliminations.

Only those agencies considered material by virtue of their financial transactions and balances are consolidated in this report.

In our opinion, we certify that the Outcomes Report has been properly drawn up, in accordance with UPF requirements, to present a true and fair view of:

| (i) | the operating statement and cash flows of the Queensland State Government for the financial year; and |

| (ii) | the balance sheet of the Government at 30 June 2012. |

At the date of certification of this report, we are not aware of any material circumstances that would render any particulars included in the Outcomes Report misleading or inaccurate.

| | |

| Dennis Molloy | | Helen Gluer, MBA, BCom, FCPA, FAICD |

| Assistant Under Treasurer | | Under Treasurer |

| Fiscal and Macroeconomics | | Queensland Treasury and Trade |

| Queensland Treasury and Trade | | |

Date 13 December 2012

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 4-13 |

2011-12 AASB 1049 Financial Statements

Overview and Analysis – 30 June 2012

AASB 1049 - Overview and Analysis

The following analysis compares current year General Government Sector (GGS) and Total State Sector performance with last year’s balances, restated for changes in accounting policies, presentational and timing differences and errors.

AASB 1049 Whole of Government and General Government Sector Financial Reporting aims to harmonise the disclosure presentation to be consistent with the Uniform Presentation Framework disclosed in the Outcomes Report.

Summary of Key Financial Aggregates of the Consolidated Financial Statements

The table below provides aggregate information under AASB1049:

| | | | | | | | | | | | | | | | |

| | | General Government | | | Total State | |

| | | Sector | | | Sector | |

| | | 2012 | | | 2011 | | | 2012 | | | 2011 | |

| | | $ million | | | $ million | | | $ million | | | $ million | |

Continuing Revenue from Transactions | | | | | | | | | | | | | | | | |

Taxation revenue | | | 10,608 | | | | 9,981 | | | | 10,280 | | | | 9,619 | |

Grants revenue | | | 22,652 | | | | 20,338 | | | | 22,815 | | | | 20,519 | |

Sales of goods and services | | | 4,996 | | | | 4,172 | | | | 13,461 | | | | 11,476 | |

Interest income | | | 2,484 | | | | 2,368 | | | | 1,673 | | | | 2,016 | |

Dividend and income tax equivalents income | | | 1,112 | | | | 1,232 | | | | 63 | | | | 4 | |

Other revenue | | | 3,942 | | | | 3,921 | | | | 4,439 | | | | 4,246 | |

| | | | | | | | | | | | | | | | |

| | | 45,794 | | | | 42,013 | | | | 52,732 | | | | 47,880 | |

| | | | | | | | | | | | | | | | |

Continuing Expenses from Transactions | | | | | | | | | | | | | | | | |

Employee expenses | | | 18,250 | | | | 16,826 | | | | 19,773 | | | | 18,228 | |

Superannuation expenses | | | 3,517 | | | | 3,411 | | | | 3,738 | | | | 3,633 | |

Other operating expenses | | | 8,821 | | | | 8,646 | | | | 13,278 | | | | 12,776 | |

Depreciation and amortisation | | | 2,777 | | | | 2,507 | | | | 4,886 | | | | 4,612 | |

Other interest expense | | | 1,659 | | | | 1,125 | | | | 4,033 | | | | 4,035 | |

Grants expenses | | | 11,004 | | | | 10,963 | | | | 9,081 | | | | 8,796 | |

| | | | | | | | | | | | | | | | |

| | | 46,027 | | | | 43,479 | | | | 54,789 | | | | 52,079 | |

| | | | | | | | | | | | | | | | |

Net Operating Balance from Continuing Operations | | | (233 | ) | | | (1,466 | ) | | | (2,058 | ) | | | (4,199 | ) |

Net Operating Balance from Discontinued Operations | | | — | | | | — | | | | — | | | | 424 | |

| | | | | | | | | | | | | | | | |

Net Operating Balance | | | (233 | ) | | | (1,466 | ) | | | (2,058 | ) | | | (3,776 | ) |

| | | | | | | | | | | | | | | | |

Other Economic Flows - Included in Operating Result | | | (159 | ) | | | 148 | | | | (2,397 | ) | | | 2,075 | |

| | | | | | | | | | | | | | | | |

Operating Result | | | (391 | ) | | | (1,318 | ) | | | (4,455 | ) | | | (1,700 | ) |

| | | | | | | | | | | | | | | | |

Other Economic Flows - Other Movements in Equity | | | (6,830 | ) | | | 3,606 | | | | (6,543 | ) | | | (932 | ) |

| | | | | | | | | | | | | | | | |

Comprehensive Result | | | (7,222 | ) | | | 2,287 | | | | (10,998 | ) | | | (2,632 | ) |

| | | | | | | | | | | | | | | | |

Purchases of non-financial assets | | | 7,930 | | | | 8,237 | | | | 12,048 | | | | 13,385 | |

Fiscal Balance | | | (5,482 | ) | | | (7,049 | ) | | | (9,004 | ) | | | (11,867 | ) |

Assets | | | 243,573 | | | | 239,957 | | | | 299,748 | | | | 293,408 | |

Liabilities | | | 72,920 | | | | 62,082 | | | | 137,790 | | | | 120,453 | |

| | | | | | | | | | | | | | | | |

Net Worth | | | 170,653 | | | | 177,875 | | | | 161,958 | | | | 172,956 | |

| | | | | | | | | | | | | | | | |

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 5-01 |

AASB 1049 - Overview and Analysis

Net Operating Balance

The GGS net operating balance was a deficit of $233 million compared to a deficit (restated) of $1.466 billion in 2010-11.

The Total State Sector net operating balance was a deficit of $2.058 billion compared to a restated deficit of $3.776 billion in 2010-11.

Revenue

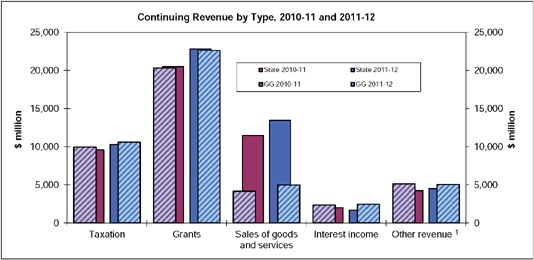

Revenue from transactions has increased from 2010-11 by $3.781 billion to be $45.794 billion in the GGS and totals $52.732 billion in the Total State Sector, an increase of $4.852 billion over 2010-11.

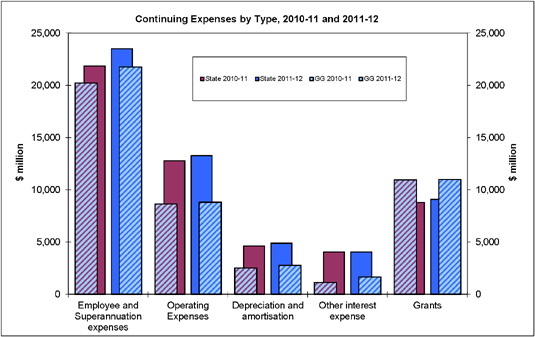

Revenues by type for the GGS and Total State Sector are shown in the following chart:

1 Other revenue includes dividends and tax equivalents income

Taxation revenue increased in 2011-12 by $627 million for GGS and $661 million for the Total State Sector. Payroll tax collections explain the majority of this increase, reflecting growth in employment and wages.

Commonwealth and other grants comprised 49% of GGS revenue and 43% of Total State Sector revenue. Grant revenue overall has increased $2.3 billion from 2010-11. The growth in grants revenue from 2010-11 to 2011-12 is primarily due to increased Commonwealth disaster relief payments ($695 million) and roads infrastructure funding ($1.616 billion) which was largely brought forward from future years, particularly 2012-13. In addition, GST revenue increased by $270 million. Partially offsetting these increases are decreases arising from the winding down of the Nation Building and Jobs Plan funding.

Sales of goods and services increased by $824 million in 2011-12 to $4.996 billion in the GGS and by $1.985 billion in the Total State Sector. The change in the GGS sales is mainly due to a reclassification of Parents and Citizens association contributions from grants revenue to sales of goods and services and increased recoverable works by the Department of Transport and Main Roads. In addition to these changes, sales for the Total State Sector also increased from higher electricity sales, recoverable works for the LNG industry and WorkCover premiums.

Interest income in the Total State Sector was lower in 2011-12 than 2010-11, mainly reflecting lower returns on investments managed by QIC and lower financial asset balances held by QTC as forward funding was drawn down.

GGS dividend and income tax equivalent income decreased by $120 million in 2011-12 mainly due to lower tax receipts from Stanwell Corporation Limited following a one-off gain on the sale of a mining lease in 2010-11. The dividend income for the Total State Sector mainly represents the dividend received from the State’s remaining shares in QR National.

Other revenue increased by $193 million in the Total State Sector mainly due to coal rebates to Stanwell Corporation Limited.

| | |

| 5-02 | | Report on State Finances 2011–12 – Government of Queensland |

AASB 1049 - Overview and Analysis

Expenses

Total expenses for 2011-12 were $46.027 billion for the GGS and $54.789 billion for the Total State Sector, an increase from 2010-11 of $2.549 billion and $2.710 billion respectively.

Expenses by type are shown in the following chart:

Employee expenses increased in 2011-12 for both the GGS and Total State Sector as a result of enterprise bargaining agreements, payments under the previous Government’s voluntary redundancy program and growth, primarily in health and education staff numbers.

In the Total State Sector, other operating expenses grew by $502 million mainly due to increased recoverable works.

Depreciation costs increased by $270 million to $2.777 billion for the GGS reflecting the increased capital stock and a similar increase can be seen in the Total State Sector. The depreciation for the PNFC sector has not increased due to asset sales and impairments during 2010-11.

Other interest expenses increased $534 million to $1.659 billion in the GGS, reflecting the higher average level of borrowings in 2011-12.

Grant expenses are largely unchanged in the GGS from 2010-11 reflecting increased grants to not-for-profit organisations being offset by lower CSO payments and other grants to Government-owned corporations (GOCs). For the Total State Sector, these grants to GOCs are eliminated, leaving the grants to not-for-profit organisations.

Operating Result

The operating result is the surplus or deficit for the year under the Accounting Standards framework. Valuation and other adjustments such as deferred tax and privatisation dividends are shown as other economic flows and are included in the operating result.

The GGS operating result for the 2011-12 year was a deficit of $391 million (2010-11, $1.318 billion deficit). Other economic flows included in the operating result were negative $159 million in 2011-12 compared to a positive $148 million for 2010-11. The flows for 2011-12 largely arose from increases in deferred tax balances and dividends treated as capital returns being more than offset by valuation adjustments to assets and liabilities.

The Total State Sector operating result was a deficit of $4.455 billion (2010-11, $1.7 billion deficit). This result is significantly impacted by market value interest adjustments on borrowings as bond yields have fallen to historic lows (refer subsequent discussion on Liabilities page 5-05).

Fiscal Balance

The GGS fiscal balance was negative $5.482 billion for 2011-12 compared to negative $7.049 billion for 2010-11. The change is mainly the result of the lower net operating deficit combined with lower purchases of non-financial assets (by $307 million) than in 2010-11.

The Total State Sector fiscal balance was negative $9.004 billion for 2011-12 compared to negative $11.867 billion for 2010-11. The change is the result of the net operating deficit being lower by $1.718 billion and purchases of non-financial assets being lower by $1.337 billion.

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 5-03 |

AASB 1049 - Overview and Analysis

Assets

Assets controlled by the GGS at 30 June 2012 totalled $243.573 billion, an increase of $3.616 billion on 2010-11.

Financial assets in the GGS did not vary significantly from 2010-11, however non-financial assets increased by $3.573 billion, mainly in relation to property, plant and equipment ($3.288 billion). The capital purchases for the year were partially offset by downward revaluations of $1.651 billion mainly as a result of lower land values.

Assets controlled by the State at 30 June 2012 totalled $299.748 billion (2011, $293.408 billion). Financial assets of the State increased marginally, as QTC increased its onlending to local government. Property, plant and equipment increased $5.658 billion as purchases from the capital program more than offset revaluation decrements and impairments.

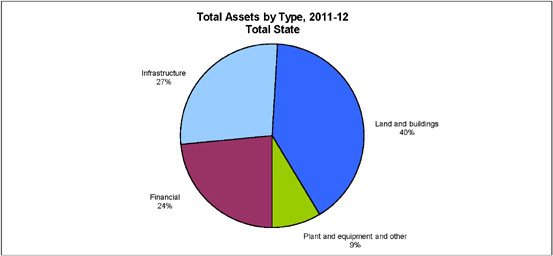

The main types of assets owned by the State are detailed in the following chart:

Of the Total State Sector assets, GGS assets comprise 81%, made up of:

| | | | |

| | | $M | |

Financial | | | 61,628 | |

Infrastructure | | | 41,727 | |

Land and buildings | | | 117,007 | |

Plant and equipment and other | | | 23,211 | |

| | |

| 5-04 | | Report on State Finances 2011–12 – Government of Queensland |

AASB 1049 - Overview and Analysis

Liabilities

Liabilities at 30 June 2012 totalled $72.920 billion for the GGS and $137.790 billion for the Total State Sector, an increase of $10.838 billion over 2010-11 for the GGS and $17.337 billion for the State.

The increase in liabilities for the GGS is largely due to:

| | • | | an increase in interest bearing liabilities of just under $5 billion reflecting increased borrowing by the GGS, primarily to fund major capital projects; |

| | • | | employee benefit obligations such as superannuation and long service leave liabilities increasing by $5.854 million. |

The increase in liabilities for the State is largely due to:

| | • | | Government issued securities, including to finance capital acquisitions by the Non-financial Public Sector and local government increased by $11.116 billion; |

| | • | | employee benefit obligations such as superannuation and long service leave liabilities increasing by $6.249 million. |

The accounting standards require governments to use Commonwealth bond yields in valuing their superannuation liability. The historically low bond yields are having a significant impact on this obligation with bond yields declining from 5.3% in 2010-11 to 3.2% in 2011-12, which is largely the cause of an actuarial loss of $5.532 billion for the Total State Sector. Similarly, the market value of the State’s borrowings has also been been affected by the fall in bond rates resulting in an unrealised loss for the year of $5.2 billion. All Australian jurisdictions have seen their superannuation liabilities and borrowings impacted by these historical lows in bond yields. It is expected these losses will reverse over time as interest rates return to more normal levels.

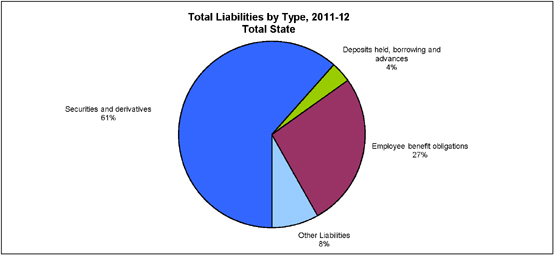

The components of State liabilities are shown in the following chart:

Of the Total State Sector liabilities, GGS liabilities comprise 53%, made up of:

| | | | |

| | | $M | |

Deposits held, borrowing and advances | | | 29,939 | |

Employee benefit obligations | | | 35,722 | |

Other liabilities | | | 7,259 | |

Cash Flow Statement

The GGS recorded net cash flows from operating activities of $2.832 billion and net borrowings and advances of $6.142 billion were used to fund capital purchases of $7.930 billion.

The Total State Sector recorded net cash flows from operating activities for the 2011-12 financial year of $2.950 billion. Capital purchases of $12.048 billion were funded by these operating cash flows as well as net new borrowings of $4.5 billion and forward funding from the previous year.

| | |

| Report on State Finances 2011–12 – Government of Queensland | | 5-05 |

2011-12

Audited Information

Queensland General Government and

Whole of Government Consolidated

Financial Statements

30 June 2012

Operating Statement for Queensland

for the Year Ended 30 June 2012

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | General Government | | | | | | | |

| | | | | | | | Sector | | | Total State Sector | |

| | | | | | | | | 2012 | | | | 2011 | | | | 2012 | | | | 2011 | |

| | | | | Notes | | | $M | | | $M | | | $M | | | $M | |

| | Continuing Operations Revenue from Transactions | | | | | | | | | | | | | | | | | | | | |

| | Taxation revenue | | | 3 | | | | 10,608 | | | | 9,981 | | | | 10,280 | | | | 9,619 | |

| | Grants revenue | | | 4 | | | | 22,652 | | | | 20,338 | | | | 22,815 | | | | 20,519 | |

| | Sales of goods and services | | | 5 | | | | 4,996 | | | | 4,172 | | | | 13,461 | | | | 11,476 | |

| | Interest income | | | 6 | | | | 2,484 | | | | 2,368 | | | | 1,673 | | | | 2,016 | |

| | Dividend and income tax equivalents income | | | 7 | | | | 1,112 | | | | 1,232 | | | | 63 | | | | 4 | |

| | Other revenue | | | 8 | | | | 3,942 | | | | 3,921 | | | | 4,439 | | | | 4,246 | |

| | Continuing Operations Total Revenue from Transactions | | | | | | | 45,794 | | | | 42,013 | | | | 52,732 | | | | 47,880 | |

| Less | | Continuing Operations Expenses from Transactions | | | | | | | | | | | | | | | | | | | | |

| | Employee expenses | | | 9 | | | | 18,250 | | | | 16,826 | | | | 19,773 | | | | 18,228 | |

| | Superannuation expenses | | | | | | | | | | | | | | | | | | | | |

| | Superannuation interest cost | | | 10 | | | | 1,216 | | | | 1,240 | | | | 1,195 | | | | 1,225 | |

| | Other superannuation expenses | | | 10 | | | | 2,301 | | | | 2,171 | | | | 2,543 | | | | 2,408 | |

| | Other operating expenses | | | 11 | | | | 8,821 | | | | 8,646 | | | | 13,278 | | | | 12,776 | |

| | Depreciation and amortisation | | | 12 | | | | 2,777 | | | | 2,507 | | | | 4,886 | | | | 4,612 | |

| | Other interest expense | | | 13 | | | | 1,659 | | | | 1,125 | | | | 4,033 | | | | 4,035 | |

| | Grants expenses | | | 14 | | | | 11,004 | | | | 10,963 | | | | 9,081 | | | | 8,796 | |

| | Continuing Operations Total Expenses from Transactions | | | | | | | 46,027 | | | | 43,479 | | | | 54,789 | | | | 52,079 | |

| Equals | | Net Operating Balance from Continuing Operations | | | | | | | (233 | ) | | | (1,466 | ) | | | (2,058 | ) | | | (4,199 | ) |

| Add | | Net Operating Balance from Discontinued Operations | | | 59 | | | | — | | | | — | | | | — | | | | 424 | |

| Equals | | Net Operating Balance | | | | | | | (233 | ) | | | (1,466 | ) | | | (2,058 | ) | | | (3,776 | ) |

| | Continuing Operations Other Economic Flows - Included in Operating Result | | | | | | | | | | | | | | | | | | | | |

| | Gain on sale of assets and investments | | | 15 | | | | — | | | | 166 | | | | 415 | | | | 569 | |

| | Revaluation increments and impairment loss reversals | | | 16 | | | | 329 | | | | 42 | | | | 611 | | | | 1,874 | |

| | Loss on sale of assets and investments | | | 17 | | | | (83 | ) | | | (34 | ) | | | (405 | ) | | | (735 | ) |

| | Asset write-down, revaluation decrements and impairment loss | | | 18 | | | | (531 | ) | | | (383 | ) | | | (883 | ) | | | (2,573 | ) |

| | Actuarial adjustments to liabilities | | | 19 | | | | (260 | ) | | | 65 | | | | 28 | | | | 56 | |

| | Deferred income tax equivalents | | | | | | | 282 | | | | (1,143 | ) | | | — | | | | — | |

| | Dividends and tax equivalents treated as capital returns | | | 20 | | | | 82 | | | | 1,396 | | | | — | | | | — | |

| | Other | | | 21 | | | | 22 | | | | 39 | | | | (2,165 | ) | | | 2,940 | |

| Equals | | Continuing Operations Other Economic Flows Included in Operating Result | | | | | | | (159 | ) | | | 148 | | | | (2,397 | ) | | | 2,130 | |

| Add | | Discontinued Operations Other Economic Flows Included in Operating Result | | | 22 | | | | — | | | | — | | | | — | | | | (55 | ) |

| Equals | | Total Other Economic Flows Included in Operating Result | | | | | | | (159 | ) | | | 148 | | | | (2,397 | ) | | | 2,075 | |

| | Operating Result from Continuing Operations | | | | | | | (391 | ) | | | (1,318 | ) | | | (4,455 | ) | | | (2,070 | ) |

| Add | | Operating Result from Discontinued Operations | | | 59 | | | | — | | | | — | | | | — | | | | 369 | |

| Equals | | Operating Result | | | | | | | (391 | ) | | | (1,318 | ) | | | (4,455 | ) | | | (1,700 | ) |

| | Other Economic Flows - Other Movements in Equity | | | | | | | | | | | | | | | | | | | | |

| | Adjustments to opening balances | | | * | | | | — | | | | 4,784 | | | | — | | | | 72 | |

| | Revaluations | | | 23 | | | | (7,238 | ) | | | (1,149 | ) | | | (6,531 | ) | | | (1,545 | ) |

| | Other | | | 24 | | | | 408 | | | | (29 | ) | | | (11 | ) | | | 541 | |

| | Total Other Economic Flows | | | | | | | | | | | | | | | | | | | | |

| | Other Movements in Equity | | | | | | | (6,830 | ) | | | 3,606 | | | | (6,543 | ) | | | (932 | ) |

| | Comprehensive Result | | | | | | | (7,222 | ) | | | 2,287 | | | | (10,998 | ) | | | (2,632 | ) |

| | Total Change In Net Worth | | | | | | | (7,222 | ) | | | 2,287 | | | | (10,998 | ) | | | (2,632 | ) |

| * | Refer to Statement of Changes in Net Assets (Equity) |

| | |

| Audited Consolidated Financial Statements 2011–12 – Government of Queensland | | 6-01 |

Operating Statement for Queensland

for the Year Ended 30 June 2012

continued

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | General Government | | | | | | | |

| | | | | | | Sector | | | | Total State Sector | |

| | | | | | | 2012 | | | | 2011 | | | | 2012 | | | | 2011 | |

| | | | Notes | | | $M | | | | $M | | | | $M | | | | $M | |

| | KEY FISCAL AGGREGATES | | | | | | | | | | | | | | | | | | |

| | Net Operating Balance | | | | | (233 | ) | | | (1,466 | ) | | | (2,058 | ) | | | (3,776 | ) |

Less | | Net Acquisition/(Disposal) of Non-Financial Assets | | | | | | | | | | | | | | | | | | |

| | Purchases of non-financial assets | | | | | 7,930 | | | | 8,237 | | | | 12,048 | | | | 13,385 | |

| | Less Sales of non-financial assets | | | | | 198 | | | | 254 | | | | 559 | | | | 661 | |

| | Less Depreciation | | | | | 2,777 | | | | 2,507 | | | | 4,886 | | | | 4,730 | |

| | Plus Change in inventories | | | | | 55 | | | | 80 | | | | 68 | | | | 32 | |

| | Plus Other movement in non-financial assets | | | | | 238 | | | | 27 | | | | 275 | | | | 66 | |

| | Equals Total Net Acquisition/(Disposal) of Non-Financial Assets | | | | | 5,249 | | | | 5,583 | | | | 6,947 | | | | 8,092 | |

| | Equals Net Lending/(Borrowing) | | | | | (5,482 | ) | | | (7,049 | ) | | | (9,004 | ) | | | (11,867 | ) |

This Operating Statement should be read in conjunction with the accompanying notes. Note 2 provides disaggregated information in relation to the above components.

| | |

| 6-02 | | Audited Consolidated Financial Statements 2011–12 – Government of Queensland |

Balance Sheet for Queensland

as at 30 June 2012

| | | | | | | | | | | | | | | | | | | | |

| | | | | | General Government | | | | | | | |

| | | | | | Sector | | | Total State Sector | |

| | | | | | 2012 | | | 2011 | | | 2012 | | | 2011 | |

| | | Notes | | | $M | | | $M | | | $M | | | $M | |

Assets | | | | | | | | | | | | | | | | | | | | |

Financial Assets | | | | | | | | | | | | | | | | | | | | |

Cash and deposits | | | 25 | | | | 865 | | | | 635 | | | | 1,529 | | | | 1,359 | |

Receivables and loans | | | | | | | | | | | | | | | | | | | | |

Receivables | | | 26 | | | | 4,087 | | | | 4,483 | | | | 5,174 | | | | 5,123 | |

Advances paid | | | 26 | | | | 687 | | | | 594 | | | | 932 | | | | 865 | |

Loans paid | | | 26 | | | | 115 | | | | 128 | | | | 7,445 | | | | 5,888 | |

Securities other than shares | | | 27 | | | | 34,124 | | | | 33,224 | | | | 52,336 | | | | 53,402 | |

Shares and other equity investments | | | | | | | | | | | | | | | | | | | | |

Investments in public sector entities | | | 28 | | | | 21,602 | | | | 22,405 | | | | — | | | | — | |

Investments in other entities | | | 28 | | | | 8 | | | | 5 | | | | 2,806 | | | | 2,818 | |

Investments accounted for using equity method | | | 28 | | | | 140 | | | | 112 | | | | 259 | | | | 210 | |

Total Financial Assets | | | | | | | 61,628 | | | | 61,585 | | | | 70,480 | | | | 69,665 | |

Non-Financial Assets | | | | | | | | | | | | | | | | | | | | |

Inventories | | | 31 | | | | 738 | | | | 678 | | | | 1,246 | | | | 1,194 | |

Assets held for sale | | | 32 | | | | 145 | | | | 198 | | | | 149 | | | | 371 | |

Investment properties | | | 33 | | | | 188 | | | | 251 | | | | 500 | | | | 553 | |

Biological assets | | | 34 | | | | 11 | | | | 9 | | | | 11 | | | | 10 | |

Property, plant and equipment | | | 37 | | | | 174,278 | | | | 170,990 | | | | 225,664 | | | | 220,006 | |

Intangibles | | | 38 | | | | 846 | | | | 872 | | | | 1,172 | | | | 1,139 | |

Deferred tax asset | | | | | | | 5,449 | | | | 5,090 | | | | — | | | | — | |

Other non-financial assets | | | 35 | | | | 290 | | | | 283 | | | | 525 | | | | 469 | |

Total Non-Financial Assets | | | | | | | 181,945 | | | | 178,372 | | | | 229,267 | | | | 223,743 | |

Total Assets | | | | | | | 243,573 | | | | 239,957 | | | | 299,748 | | | | 293,408 | |

Liabilities | | | | | | | | | | | | | | | | | | | | |

Payables | | | 39 | | | | 3,888 | | | | 3,851 | | | | 5,090 | | | | 4,785 | |

Employee benefit obligations | | | | | | | | | | | | | | | | | | | | |

Superannuation liability | | | 40 | | | | 30,626 | | | | 25,236 | | | | 30,856 | | | | 25,159 | |

Other employee benefits | | | 40 | | | | 5,096 | | | | 4,632 | | | | 5,952 | | | | 5,400 | |

Deposits held | | | 41 | | | | 1 | | | | 1 | | | | 3,403 | | | | 3,557 | |

Borrowings and advances | | | | | | | | | | | | | | | | | | | | |

Advances received | | | 42 | | | | 425 | | | | 444 | | | | 425 | | | | 444 | |

Borrowings | | | 42 | | | | 29,513 | | | | 24,593 | | | | 1,126 | | | | 884 | |

Securities and derivatives | | | 43 | | | | — | | | | — | | | | 84,802 | | | | 73,686 | |

Deferred tax liability | | | | | | | 1,335 | | | | 1,328 | | | | — | | | | — | |

Provisions | | | 45 | | | | 1,451 | | | | 1,281 | | | | 5,150 | | | | 5,196 | |

Other liabilities | | | 46 | | | | 584 | | | | 717 | | | | 987 | | | | 1,341 | |

Total Liabilities | | | | | | | 72,920 | | | | 62,082 | | | | 137,790 | | | | 120,453 | |

Net Assets | | | | | | | 170,653 | | | | 177,875 | | | | 161,958 | | | | 172,956 | |

Net Worth | | | | | | | | | | | | | | | | | | | | |

Accumulated surplus/(deficit) | | | | | | | 82,995 | | | | 89,222 | | | | 76,192 | | | | 86,809 | |

Reserves | | | | | | | 87,658 | | | | 88,653 | | | | 85,765 | | | | 86,147 | |

Total Net Worth | | | | | | | 170,653 | | | | 177,875 | | | | 161,958 | | | | 172,956 | |

KEY FISCAL AGGREGATES | | | | | | | | | | | | | | | | | | | | |

Net Financial Worth | | | | | | | (11,292 | ) | | | (497 | ) | | | (67,310 | ) | | | (50,787 | ) |

Net Financial Liabilities | | | | | | | 32,894 | | | | 22,902 | | | | 67,310 | | | | 50,787 | |

Net Debt | | | | | | | (5,851 | ) | | | (9,542 | ) | | | 27,514 | | | | 17,057 | |

This Balance Sheet should be read in conjunction with the accompanying notes. Note 2 provides disaggregated information in relation to the components of the net assets.

| | |

| Audited Consolidated Financial Statements 2011–12 – Government of Queensland | | 6-03 |

Statement of Changes in Net Assets (Equity) for Queensland General Government Sector

for the year ended 30 June 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Comprehensive Result for Period | | | | |

| | | Opening Balance | | | Adjustments to Opening Balances | | | Movements | | | Transfers / Entity

Cessation 1 | | | Actuarial Gain / Loss on Superannuation 2 | | | Closing

Balance | |

| | | $M | | | $M | | | $M | | | $M | | | $M | | | $M | |

2012 | | | | | | | | | | | | | | | | | | | | | | | | |

Accumulated surplus | | | 89,222 | | | | — | | | | (391 | ) | | | (530 | ) | | | (5,305 | ) | | | 82,995 | |

Revaluation reserve—financial assets | | | 13,074 | | | | — | | | | (282 | ) | | | 509 | | | | — | | | | 13,300 | |

Revaluation reserve—non-financial assets | | | 75,457 | | | | — | | | | (1,651 | ) | | | 446 | | | | — | | | | 74,252 | |

Other reserves | | | 122 | | | | — | | | | — | | | | (17 | ) | | | — | | | | 105 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total equity at the end of the financial year | | | 177,875 | | | | — | | | | (2,324 | ) | | | 408 | | | | (5,305 | ) | | | 170,653 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | |

| | | | | | | | | Comprehensive Result for Period 6 | | | | |

| | | Opening Balance | | | Adjustments to Opening Balances | | | Movements | | | Transfers / Entity C essation | | | Actuarial Gain / Loss on Superannuation | | | Closing Balance | |

| | | $M | | | $M | | | $M | | | $M | | | $M | | | $M | |

2011 | | | | | | | | | | | | | | | | | | | | | | | | |

Accumulated surplus 3 | | | 89,368 | | | | 477 | | | | (1,318 | ) | | | 12 | | | | 682 | | | | 89,222 | |

Revaluation reserve—financial

assets 4 | | | 10,255 | | | | 4,307 | | | | (1,488 | ) | | | — | | | | | | | | 13,074 | |

Revaluation reserve—non-financial assets 5 | | | 75,831 | | | | — | | | | (344 | ) | | | (30 | ) | | | | | | | 75,457 | |

Other reserves | | | 133 | | | | — | | | | — | | | | (11 | ) | | | | | | | 122 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total equity at the end of the financial year | | | 175,588 | | | | 4,784 | | | | (3,150 | ) | | | (29 | ) | | | 682 | | | | 177,875 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| 1 | The balance in Transfers/Entity cessation relates mainly to the General Government Sector accounting for the North Queensland Bulk Ports Corporation Ltd transfer of $509 million between retained earnings and issued share capital, offset in part by the deconsolidation of ZeroGen Pty Ltd. |

| 2 | The 2011-12 actuarial loss includes an adjustment for defined benefit liabilities of the State Public Sector Superannuation Scheme (QSuper), as well as the tax effect of an actuarial adjustment to the Energy Superannuation Fund. |

The following footnotes relate to prior year adjustments to equity:

| 3 | The opening accumulated surplus has been adjusted by $477 million, mainly as a result of a change in the valuation methodology for borrowings in the General Government sector from fair value to amortised cost (refer to Note 1 (ai)). |

The movement in accumulated surplus for the period includes an increase of $67 million by The Council of The Queensland Institute of Medical Research in relation to a change in accounting treatment of capital grants and an increase of $33 million due to a change in the valuation methodology for borrowings in the General Government sector from fair value to amortised cost (refer to Note 1 (ai)).

| 4 | The opening financial assets revaluation reserve has been adjusted by $4.307 billion, mainly due to an increase of $4.236 billion for the change in accounting treatment of entities having negative net worth (refer to Note 1(q)) and an increase of $70 million in relation to the fair value depreciation and revaluation of certain assets in Queensland Rail. |

The movement in the revaluation reserve for financial assets includes a decrease of $613 million for the change in accounting treatment of entities having negative net worth (refer to Note 1 (q)). This is offset in part by an increase of $516 million in relation to the value of the Public Non-financial Corporation Sectors, mainly as a result of a change in the valuation methodology for borrowings, the merger of Water Secure with SEQ Water and the merger of Tarong Energy Corporation Limited into CS Energy Limited and Stanwell Corporation Limited.

| 5 | The movement in the non-financial assets revaluation reserve includes an increase of $1.799 billion by the Department of Transport and Main Roads to correct the value of infrastructure assets. |

| 6 | Adjustments to opening balances are included as part of the comprehensive result on the face of the Operating Statement as they represent changes to the comprehensive result in prior periods. |

| | |

| 6-04 | | Audited Consolidated Financial Statements 2011–12 – Government of Queensland |

Statement of Changes in Net Assets (Equity) for Queensland Total State Sector

for the year ended 30 June 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Comprehensive Result for Period | | | | |

| | | Opening Balance | | | Adjustments to

Opening Balances | | | Movements | | | Transfers / Entity

Cessation | | | Actuarial Gain / Loss

on Superannuation 1 | | | Closing

Balance | |

| | | $M | | | $M | | | $M | | | $M | | | $M | | | $M | |

2012 | | | | | | | | | | | | | | | | | | | | | | | | |

Accumulated surplus | | | 86,809 | | | | — | | | | (4,455 | ) | | | (629 | ) | | | (5,532 | ) | | | 76,192 | |

Revaluation reserve—financial assets | | | 860 | | | | — | | | | (40 | ) | | | 426 | | | | — | | | | 1,245 | |