Budget Strategy and Outlook 2021-22

Economic outlook

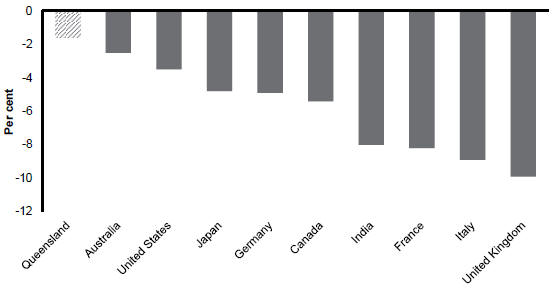

The severe health and economic shock caused by the COVID-19 pandemic saw the global economy contract by 3.3 per cent in 2020, according to the International Monetary Fund, a much greater impact than the 0.1 per cent decline in global activity recorded in 2009 at the height of the Global Financial Crisis.

The national economy fell into recession in 2020, for the first time since 1991. However, Queensland and Australia’s relative success in containing the spread of COVID-19, in addition to significant fiscal and monetary policy support, meant the economic impacts nationally were less severe than in many other countries.

Reflecting the success of Queensland’s health response, Queensland’s domestic economy has rebounded strongly, with business and consumer confidence currently at elevated levels.

However, several ongoing risks remain, including those related to the global vaccine rollout, ongoing geopolitical and trade tensions, particularly between the Unites States and China, and challenges in Australia’s trade relationship with China.

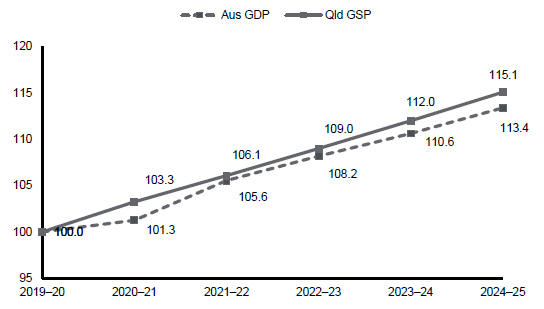

Reflecting the improved domestic conditions, GSP is forecast to rebound 31⁄4 per cent in 2020–21, significantly stronger than the 1⁄4 per cent growth expected at the time of the 2020–21 Budget. Robust ongoing growth of 23⁄4 per cent is forecast for 2021–22 and in each subsequent year across the forward estimates.

Following a 7 per cent rebound in September quarter 2020, Queensland’s domestic activity continued to grow across the December and March quarters, to be 3 per cent above the pre-COVID-19 level of March quarter 2020. This was almost double the 1.7 per cent growth in the rest of Australia over the year, and substantially higher than the 1.9 per cent in New South Wales, while domestic activity in Victoria was still 0.3 per cent below its pre-COVID-19 level.

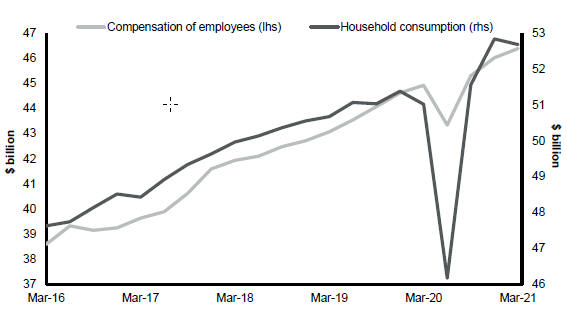

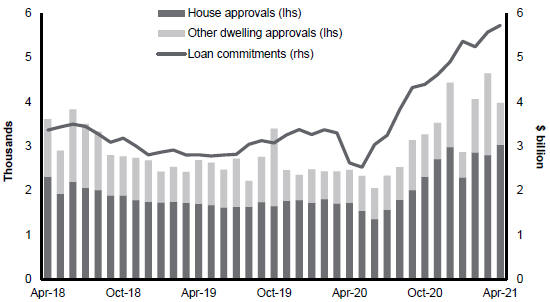

The strength of the Queensland economy has been underpinned by elevated activity in consumer spending and the housing sector.

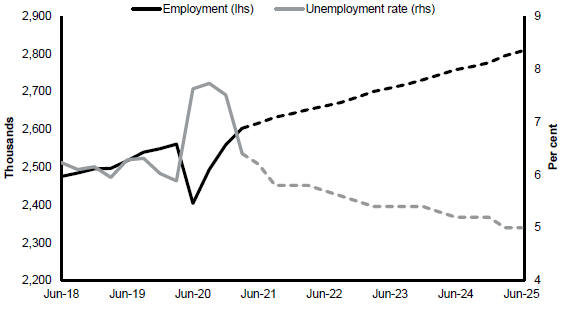

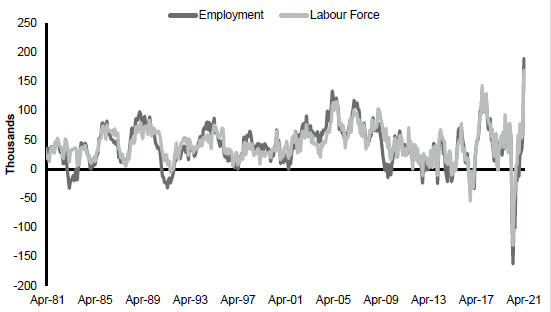

Queensland’s labour market has also improved substantially, with employment in April 2021 having rebounded by 253,200 persons since May 2020, to be 54,900 persons above the pre-pandemic level in March 2020. In comparison, employment in the rest of Australia in April 2021 was still 9,000 below the level in March 2020.

Reflecting the current strength in jobs growth and the broader economic recovery, year-average employment growth in 2020–21 is now forecast to be 21⁄4 per cent, much higher than the 1 per cent forecast in the 2020–21 Budget.

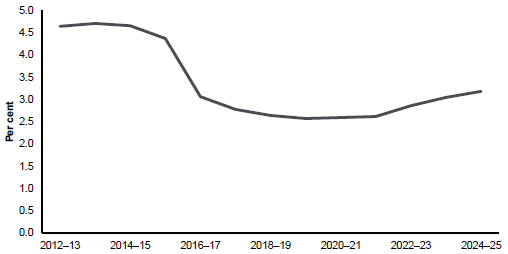

This strong jobs growth means the quarterly unemployment rate is now forecast to fall to 6 1⁄4 per cent in June quarter 2021, while the year-average unemployment rate in 2020–21 is now expected to be 7 per cent, down from the 71⁄2 per cent forecast at the previous Budget.

Ongoing strong employment growth of 3 per cent in 2021–22 is expected to drive down the unemployment rate to 53⁄4 per cent by June quarter 2022, with the unemployment rate steadily improving across the forecast period to be 5 per cent by June quarter 2025.

10

Translating and interpreting assistance

Translating and interpreting assistance