UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR/A

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05878

Franklin Value Investors Trust

(Exact name of registrant as specified in charter)

One Franklin Parkway, San Mateo, CA 94403-1906

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant’s telephone number, including area code: 650 312-2000

Date of fiscal year end: 10/31

Date of reporting period: 10/31/18

| Item 1. | Reports to Stockholders. |

Franklin Templeton Investments

Successful investing begins with ambition. And achievement only comes when you reach for it. That’s why we continually strive to deliver better outcomes for investors. No matter what your goals are, our deep, global investment expertise allows us to offer solutions that can help.

During our more than 70 years of experience, we’ve managed through all kinds of markets—up, down and those in between. We’re always preparing for what may come next. It’s because of this, combined with our strength as one of the world’s largest asset managers that we’ve earned the trust of millions of investors around the world.

Dear Shareholder:

During the 12 months ended October 31, 2018, many U.S. equity markets finished higher, although the more important event was the return of volatility to financial markets. The Russell 3000® Value and Russell 2000® Value indexes posted total returns of +2.78% and-0.59%, respectively, while the Standard & Poor’s 500® Index (S&P 500®) delivered a +7.35% total return.1

Positive corporate and economic fundamentals helped drive the overall gains in equity markets during the period. The primary tailwinds were strong U.S. corporate earnings growth, healthy consumer and business investment spending, and the positive effect of major U.S. tax cuts. In addition, the global economy continued its steady expansion since the financial crisis of 2008–2009. Unemployment continued to decline in the U.S. and other developed markets, while U.S. wage growth showed some signs of accelerating.

However, volatility reasserted itself in 2018. As measured by the Chicago Board Options Exchange Volatility Index (VIX), 2017 was the least volatile year on record for the S&P 500, but the VIX surged in early February 2018 to its highest level since the summer of 2015, and climbed again in October 2018.2 Higher bond yields, a flattening U.S. Treasury yield curve and the gradual reversal of ultra-loose monetary policy by the U.S. Federal Reserve (Fed) were key drivers of market turbulence.Small-cap stocks were also adversely affected by widening

U.S. credit spreads—the difference in yield between U.S. Treasury and corporate bonds—after steadily narrowing since 2016. Heightened trade tensions between the U.S. and China, geopolitical events, and a growing belief in the latter stages of the period that corporate earnings and economic growth will likely decelerate in 2019 were additional drags on equity markets.

Valuation is an essential factor in our analysis and we always ask ourselves if current and potential investments represent an attractive balance of risk and reward. The Russell 2000® Value Index hit anall-time high in August 2018, while the Russell 3000® Value Index and S&P 500 Index reached new highs in September 2018, but U.S. stocks fell sharply in October 2018. In all market conditions, we maintain a focus on individual investments and the prospects for each business in the context of its valuation and the backdrop of potential political and economic risks.

In U.S. equity markets, growth stocks outperformed value stocks during the period. The differences in performance were partly driven by the rally in information technology stocks, which provided a meaningful boost to growth indexes until they suffered a correction in October. We do not know if the October decline portends a shift in the fortunes of growth stocks or is simply a temporary setback. Historically, periods of

1. Source: Morningstar.

Frank Russell Company is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

2. The VIX Index measures U.S. stock market volatility based on prices of S&P 500 options.

See www.franklintempletondatasources.com for additional data provider information.

Not FDIC Insured | May Lose Value | No Bank Guarantee |

| franklintempleton.com | Not part of the annual report | 1 | ||

strong performance by growth stocks have been followed by relatively weaker performance relative to value stocks.

Another factor that contributed to the outperformance of growth stocks was the relatively greater exposure that value indexes have to areas of the economy that we believe are facing disruption from new technology. This factor may override more typical cyclical forces that have previously worked to the benefit of value investors with long time horizons and patience. Exacerbating the disruption is the reality that many new technology companies are able to innovate without the need to show immediate profits.

Amid dynamic markets and evolving economic conditions, we believe active, professional investment management serves investors well. We also recognize the important role of financial advisors in today’s markets and encourage investors to continue to seek their advice. Amid changing markets and economic conditions, we are confident investors with a well-diversified portfolio and a patient, long-term outlook will be well positioned for the years ahead.

On the following pages, the Fund’s portfolio management team reviews investment decisions that pertain to performance during the past 12 months in light of the economic environment and other factors. Please remember all securities markets fluctuate, as do mutual fund share prices. We thank you for investing with Franklin Templeton, welcome your questions and comments, and look forward to continuing to serve your investment needs in the years ahead.

Sincerely,

Peter A. Langerman

Chief Executive Officer – Investment Management

Franklin Value Investors Trust

This letter reflects our analysis and opinions as of October 31, 2018, unless otherwise indicated. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

| 3 | ||||

| 4 | ||||

| 11 | ||||

| 18 | ||||

| 25 | ||||

| 49 | ||||

| 54 | ||||

| 70 | ||||

| 71 | ||||

| 72 | ||||

|

| 77

|

| |

Visitfranklintempleton.comfor fund updates, to access your account, or to find helpful financial planning tools.

2 | Not part of the annual report | franklintempleton.com | ||

The U.S. economy grew during the 12 months under review. The economy grew faster in 2018’s second quarter than in the first, driven by consumer spending, business investment, exports and government spending, but moderated in the third quarter due to declines in exports and housing investment. The manufacturing and services sectors expanded during the period. The unemployment rate declined from 4.1% in October 2017 to a nearly49-year low of 3.7% atperiod-end.1 Annual inflation, as measured by the Consumer Price Index, increased from 2.0% in October 2017 to 2.5% atperiod-end.1

The U.S. Federal Reserve (Fed) raised its target range for the federal funds rate 0.25% at its December 2017 meeting and continued to reduce its balance sheet as part of its ongoing plan to normalize monetary policy. In his congressional testimonies in February and July 2018, as well as at the Fed symposium in August, Fed Chair Jerome Powell reiterated the Fed’s intention to gradually raise interest rates. As widely expected, the Fed further raised its target range for the federal funds rate 0.25% each at its March, June and September 2018 meetings, to 2.00%–2.25%. At its September meeting, the Fed raised its forecast for U.S. economic growth in 2018 and 2019 and projected one more rate increase in 2018. Minutes from the Fed’s September meeting (released in October) indicated that a few Fed officials expected monetary policy to become modestly restrictive of economic growth, while some officials seemed to favor increasing the federal funds rate temporarily above what they consider to be its longer-term level to reduce the risk of overshooting the Fed’s inflation objective. In contrast, some Fed officials indicated they would not favor a restrictive policy unless they see clear signs of an overheating economy and rising inflation.

U.S. equity markets overall rose during the period, benefiting from mostly upbeat economic data, and better U.S. corporate earnings, as well as the passage of the U.S. tax reform bill. After reaching record highs in January 2018, U.S. stocks declined amid concerns that strong economic growth and rising inflation would lead the Fed to increase its target rate faster than expected, as well as fears of tighter regulation of information technology and technology-related companies. Other factors that curbed investor sentiment included tensions between the U.S. and North Korea at certain times during the period, political uncertainties in the U.S., the Trump administration’s protectionist policies, and the potential impact of escalating U.S.-China trade tensions on global growth and

corporate earnings. Partially offsetting these concerns were an overall easing of tensions in the Korean peninsula in the latter part of the period, intermittent U.S.-China trade negotiations, an agreement between the U.S. and the European Union to try to reduce trade barriers, and a potential trade deal between the U.S., Mexico and Canada. After reaching a newall-time high in September 2018, the broad U.S. stock market, as measured by the Standard & Poor’s 500 Index (S&P 500), experienced heightened volatility in October amid investor concerns about the Fed’s interest-rate path, rising U.S. Treasury yields, trade, a potentially moderating economy and several big companies’ weaker-than-expected fourth-quarter 2018 revenue guidance. In this environment, the S&P 500 generated a +7.35% total return for the12-month period.2

The foregoing information reflects our analysis and opinions as of October 31, 2018. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

1. US Source: Bureau of Labor Statistics.

| franklintempleton.com | Annual Report | 3 | ||

Franklin Balance Sheet Investment Fund

This annual report for Franklin Balance Sheet Investment Fund covers the fiscal year ended October 31, 2018.

Your Fund’s Goal and Main Investments

The Fund seeks high total return, of which capital appreciation and income are components, by investing most of its assets in equity securities of companies of any size that we believe are undervalued in the marketplace at the time of purchase but have the potential for capital appreciation. The Fund invests predominantly in common stocks.

Performance Overview

The Fund’s Class A shares had a-0.15% cumulative total return for the 12 months under review. In comparison, the Russell 3000® Value Index, which measures performance of those Russell 3000® Index companies with generally lowerprice-to-book ratios and lower forecasted growth values than companies listed in other stock indexes, generated a +2.78% total return for the same period.1 You can find more of the Fund’s performance data in the Performance Summary beginning on page 7.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

Investment Strategy

Our strategy uses lowprice-to-book value as its primary reference valuation measure. Book value per share is a company’s net worth or shareholders’ equity on an accounting or “book” basis, divided by shares outstanding. The equity securities bought by the Fund will typically be purchased at a low price relative to book value. This strategy is not aimed at short-term trading gains, and we do not attempt to mirror the component securities of the benchmark index. Rather, we try to identify individual companies that meet our investment criteria, with a three- to five-year investment horizon. We may invest in companies of any size, across the entire market capitalization spectrum including smaller and midsize companies.

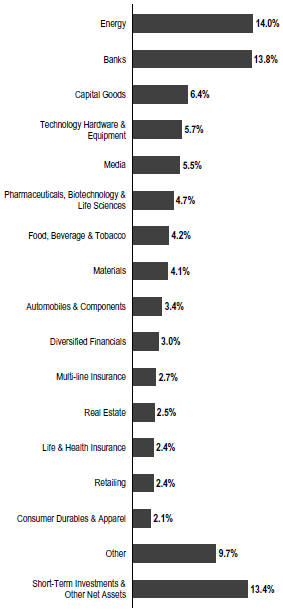

Portfolio Composition

Based on Total Net Assets as of 10/31/18

1. Source: Morningstar.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 30.

4 | Annual Report | franklintempleton.com | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

Manager’s Discussion

During the 12 months under review, holdings that positively contributed to Fund performance included Iridium Communications, DSW and Discovery.

Iridium Communications is a satellite, voice and data communications company with a long-term U.S. Department of Defense contract and a stake in Aireon,2 a joint venture that could track much of the world’s commercial aviation in real time. During the period, Iridium reported strong results and raised its 2018 full-year guidance. In addition, it deployed more of its NEXT satellite constellation, while Aireon received maritime distress certification, which will enable it to better penetrate the monopolistic maritime market. Iridium’s entire constellation of NEXT satellites is scheduled to go into orbit by the end of 2018. Accordingly, we believe Iridium could benefit from greater growth prospects, an extended period of low capital expenditures, higher free cash flow, reduced leverage and market recognition of Aieron’s value.

DSW is a leading fashion-focused women’s footwear retailer with more than 500 stores in the U.S. The stock price began to rally in March 2018, driven by solid same-store sales and higher margins. The positive financial results were due in part to innovativein-store initiatives that are resonating with its customers, astute inventory selection and scaled back discounting. In our view, DSW has solid growth potential, strong financial characteristics, and anin-store experience that appeals to its customers and defends against encroachment from online competitors. These factors lead us to believe DSW’s improving financial performance could be sustainable, and we still viewed the stock’s valuation as attractive atperiod-end.

Discovery is a global media company with a portfolio of television networks and brands, along with corresponding online content distribution. The stock price rallied inmid-2018 after the announcement that John Malone, the chairman of Liberty Media2 and a member of Discovery’s board, increased his position in the company. In addition, media stocks, including Discovery, got a boost from AT&T2 obtaining regulatory approval to buy Time Warner,2 as investors believed the decision meant further industry consolidation was more likely to occur. Further positive news came in September 2018 when Discovery announced that some of its networks would be added toover-the-top (OTT) providers Hulu2 and Sling2. Investors believed the agreements could help operating

earnings and cash flows amid the structural trend of cable subscribers migrating to OTT providers.

Detractors from Fund performance included McDermott International, American International Group (AIG) and Toll Brothers.

McDermott International is an energy-oriented engineering and construction company that has undergone what we considered an impressive turnaround in recent years. In the face of this turnaround and amid strengthening end markets for its construction services, McDermott announced the acquisition of Chicago Bridge and Iron2 in December 2017. Thestock-for-stock merger was met with immediate skepticism on the part of the investment community, a skepticism that turned out to be well founded, as subsequent quarterly results of the merged companies have shown excessive charges related to Chicago Bridge and Iron’s legacy contracts. These charges have created balance sheet concerns, forcing McDermott to announce the sale of its tank storage business, as well as initiate a private placement preferred stock offering that carried a punitive interest rate. Despite the recent negative news, we continued to have confidence in the management team’s track record in turnarounds. We believe the acquisition of Chicago Bridge and Iron is based on a sound strategic rationale and that the merger could lead to steadier and stronger earnings potential that is not reflected in the current valuation of the shares atperiod-end.

Shares of U.S.-based insurer AIG moved lower due to the announcement in November 2017 of additional commercial reserves and an increase in the loss estimate on current business, a trend of generally weak earnings and management’s limited success in turning around AIG’s operating performance. The reserve charges were particularly disappointing given AIG’s prior actions to set aside resources to meet losses related to prior-year accident claims. In October 2018, the stock price finished the12-month period on a down note due to larger-than-expected catastrophe related losses announced ahead of quarterly results. The losses were due to multiple typhoons in Japan, Hurricane Florence and mudslides in California. Investors tend to look beyond uncharacteristic weather-related losses, but we believe AIG’s series of operating challenges and negative surprises in recent years played a role in how sharply the stock price declined.

2. Not a Fund holding.

See www.franklintempletondatasources.com for additional data provider information.

| franklintempleton.com | Annual Report | 5 | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

Toll Brothers is a residential construction company that specializes in building luxury homes. The stock price began to decline in early 2018 due to investor fears that the Fed’s interest-rate tightening cycle might derail the recovery in the U.S. housing market, as well as higher construction costs and labor shortages. Investor concern grew as U.S. housing data showed a slowdown in sales activity. Although Toll Brothers, along with many other homebuilders, reported solid quarterly results during the third quarter of 2018, higher interest rates and a deterioration in home sales weighed on the share prices of homebuilders. Atperiod-end we still viewed Toll Brothers as attractive on a fundamental basis. The longer-term housing market outlook remains fairly positive due to demographic factors, namely first-time millennial homebuyers, while Toll Brothers appears to have adopted a balanced capital allocation process and a focus on return on equity.

Top 10 Holdings

10/31/18

Company Sector/Industry | % of Total Net Assets | |

Corning Inc. Technology Hardware & Equipment | 4.6% | |

JPMorgan Chase & Co. Banks | 4.4% | |

Kinder Morgan Inc. Energy | 3.8% | |

Bank of America Corp. Banks | 3.6% | |

Discovery Inc. Media | 2.7% | |

General Motors Co. Automobiles & Components | 2.7% | |

Chevron Corp. Energy | 2.0% | |

Royal Dutch Shell PLC (U.K.) Energy | 1.9% | |

Bio-Rad Laboratories Inc. Pharmaceuticals, Biotechnology & Life Sciences | 1.8% | |

Allergan PLC Pharmaceuticals, Biotechnology & Life Sciences | 1.7% |

During the reporting period, several large new purchases included Kinder Morgan, an energy infrastructure company; Perrigo, a manufacturer of health care products andover-the-counter pharmaceuticals; Dick’s Sporting Goods, a sports equipment retailer; Everest Re Group, a reinsurance company; and the aforementioned Discovery. We also added to existing positions including The Hartford Financial Services Group, an insurance and financial services provider; Johnson Controls International, a conglomerate that produces

automotive parts and climate control equipment; and the aforementioned AIG.

In contrast, the Fund’s largest liquidations included Metlife, Comerica and the aforementioned Iridium Communications. We also reduced several holdings including Royal Dutch Shell, Morgan Stanley and MKS Instruments.

As fellow shareholders, we find recent absolute and relative performance disappointing, but it is not uncommon for the Fund to lag the equity market at times given our deep value approach that will often deviate from the sector weightings of our benchmark. Relative to its benchmark, the Fund was hurt by stock selection in the financials (specifically the insurance industry) and information technology sectors, while a combination of an underweighted exposure and stock selection in the health care sector also hurt performance. We remain committed to our disciplined, value investing approach as we seek to generate attractive risk-adjusted returns for our shareholders.

Thank you for your participation in Franklin Balance Sheet Investment Fund. We look forward to continuing to serve your investment needs.

|

Grace Hoefig Portfolio Manager |

The foregoing information reflects our analysis, opinions and portfolio holdings as of October 31, 2018, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

6 | Annual Report | franklintempleton.com | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

Performance Summary as of October 31, 2018

The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 10/31/181

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Sales charges will vary depending on the size of the investment and the class of share purchased. The maximum is 5.50% and the minimum is 0%.Class A:5.50% maximum initial sales charge;Advisor Class:no sales charges. For other share classes, visitfranklintempleton.com.

| Share Class | Cumulative Total Return2 | Average Annual Total Return3 | ||||||||

A4 | ||||||||||

1-Year | -0.15% | -5.64% | ||||||||

5-Year | +27.32% | +3.77% | ||||||||

10-Year | +158.56% | +9.35% | ||||||||

Advisor | ||||||||||

1-Year | +0.07% | +0.07% | ||||||||

5-Year | +28.89% | +5.21% | ||||||||

10-Year | +168.76% | +10.39% | ||||||||

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

See page 9 for Performance Summary footnotes.

| franklintempleton.com | Annual Report | 7 | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

PERFORMANCE SUMMARY

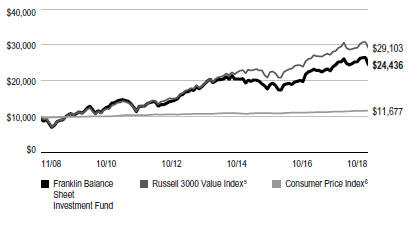

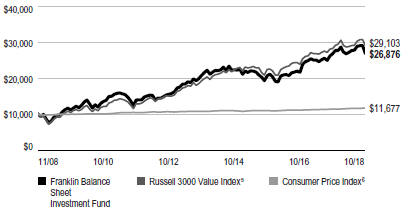

Total Return Index Comparison for a Hypothetical $10,000 Investment1

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged indexes include reinvestment of any income or distributions. They differ from the Fund in composition and do not pay management fees or expenses. One cannot invest directly in an index.

Class A(11/1/08–10/31/18)

Advisor Class(11/1/08–10/31/18)

See page 9 for Performance Summary footnotes.

8 | Annual Report | franklintempleton.com | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

PERFORMANCE SUMMARY

Distributions(11/1/17–10/31/18)

| Share Class | Net Investment Income | Short-Term Capital Gain | Long-Term Capital Gain | Total | ||||||||

A | $0.4618 | $0.2693 | $2.4379 | $3.1690 | ||||||||

C | $0.1668 | $0.2693 | $2.4379 | $2.8740 | ||||||||

R | $0.3266 | $0.2693 | $2.4379 | $3.0338 | ||||||||

R6 | $0.6306 | $0.2693 | $2.4379 | $3.3378 | ||||||||

Advisor | $0.5276 | $0.2693 | $2.4379 | $3.2348 | ||||||||

Total Annual Operating Expenses7

| ||||||||||||

| Share Class | With Waiver | Without Waiver | ||||||||||

A | 0.92% | 0.97% | ||||||||||

Advisor | 0.67% | 0.72% | ||||||||||

Each class of shares is available to certain eligible investors and has different annual fees and expenses, as described in the prospectus.

All investments involve risks, including possible loss of principal. Value securities may not increase in price as anticipated or may decline further in value. While smaller and midsize companies may offer substantial opportunities for capital growth, they may also involve heightened risks and should be considered speculative. Historically, smaller- andmidsize- company securities have been more volatile in price than larger-company securities, especially over the short term. In addition, the Fund may invest up to 25% of its total assets in foreign securities, which involve special risks, including currency fluctuations and economic and political uncertainty. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has a fee waiver associated with any investment it makes in a Franklin Templeton money fund and/or other Franklin Templeton fund, contractually guaranteed through 2/28/19. Fund investment results reflect the fee waiver; without this waiver, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Prior to 9/10/18, these shares were offered at a higher initial sales charge of 5.75%, thus actual returns would have differed. Total returns with sales charges have been restated to reflect the current maximum initial sales charge of 5.50%.

5. Source: Morningstar. The Russell 3000 Value Index is market capitalization weighted and measures performance of those Russell 3000 Index companies with lowerprice-to-book ratios and lower forecasted growth values.

6. Source: Bureau of Labor Statistics, bls.gov/cpi. The Consumer Price Index is a commonly used measure of the inflation rate.

7. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

See www.franklintempletondatasources.com for additional data provider information.

| franklintempleton.com | Annual Report | 9 | ||

FRANKLIN BALANCE SHEET INVESTMENT FUND

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions; and (2) ongoing Fund costs, including management fees, distribution and service(12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value” for each class of shares. You can estimate the expenses you paid during the period by following these steps (ofcourse, your account value and expenses will differ from those in this illustration):Divide your account value by $1,000 (ifyour account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (ifActual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| Actual (actual return after expenses) | Hypothetical (5% annual return before expenses) | |||||||||||

| Share Class | Beginning Account Value 5/1/18 | Ending Account Value 10/31/18 | Expenses Paid During 5/1/18–10/31/181,2 | Ending Account Value 10/31/18 | Expenses Paid During | Net Annualized Expense Ratio2 | ||||||

|

|

|

| |||||||||

A | $1,000 | $986.20 | $4.26 | $1,020.92 | $4.33 | 0.85% | ||||||

C | $1,000 | $982.30 | $7.99 | $1,017.14 | $8.13 | 1.60% | ||||||

R | $1,000 | $985.00 | $5.50 | $1,019.66 | $5.60 | 1.10% | ||||||

R6 | $1,000 | $987.70 | $2.51 | $1,022.68 | $2.55 | 0.50% | ||||||

Advisor | $1,000 | $987.20 | $3.01 | $1,022.18 | $3.06 | 0.60% | ||||||

1. Expenses are equal to the annualized expense ratio for thesix-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 184/365 to reflect theone-half year period.

2. Reflects expenses after fee waivers and expense reimbursements. Does not include acquired fund fees and expenses.

10 | Annual Report | franklintempleton.com | ||

This annual report for Franklin MicroCap Value Fund covers the fiscal year ended October 31, 2018. The Fund closed to new investors (with the exception of certain retirement accounts) in January 2004 and has remained closed except for two days inmid-February 2013, when the Fund was opened on a limited basis. Existing shareholders may add to or reduce their investments in the Fund; however, once an account is reduced to zero, it may not be reopened unless the Fund reopens.

Your Fund’s Goal and Main Investments

The Fund seeks high total return, of which capital appreciation and income are components, by investing at least 80% of its net assets in securities of companies with market capitalizations under $500 million at the time of purchase that we believe are undervalued in the marketplace and have the potential for capital appreciation. The Fund invests predominantly in common stocks.

Performance Overview

The Fund’s Class A shares had a-8.11% cumulative total return for the 12 months under review. In comparison, the Russell 2000® Value Index, which measures performance of those Russell 2000® Index companies with generally lowerprice-to-book ratios and lower forecasted growth values than companies listed in other stock indexes, had a-0.59% total return for the same period.1 You can find more of the Fund’s performance data in the Performance Summary beginning on page 14.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

Investment Strategy

Our strategy is to buy shares of financially sound, well-established companies at a lowprice-to-book value. In the case of financial companies, we look for consistently increasing book value over time. We limit purchases to companies with market capitalizations of less than $500 million, which we define as “microcap.” Book value per share is a company’s net worth or shareholders’ equity on an accounting or “book”

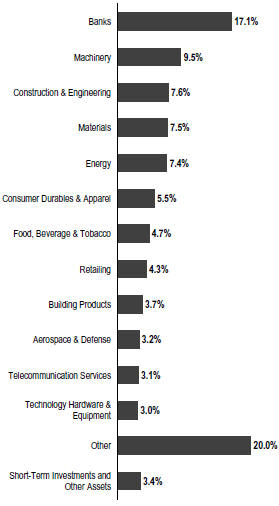

Portfolio Composition

Based on Total Net Assets as of 10/31/18

basis, divided by shares outstanding. This strategy is not aimed at short-term trading gains, nor do we consider the composition of any index. Rather, we try to identify individual companies that meet our investment criteria, and we assume at purchase that we will hold the positions for several years.

Manager’s Discussion

During the 12 months under review, holdings that positively contributed to Fund performance included Renewable Energy

1. Source: Morningstar.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 37.

| franklintempleton.com | Annual Report | 11 | ||

FRANKLIN MICROCAP VALUE FUND

| Top 10 Holdings | ||||

| 10/31/18 | ||||

Company Sector/Industry | % of Total Net Assets | |||

Seneca Foods Corp. Food, Beverage & Tobacco | 4.2% | |||

Ameresco Inc. Construction & Engineering | 2.9% | |||

Delta Apparel Inc. Consumer Durables & Apparel | 2.9% | |||

Miller Industries Inc. Machinery | 2.8% | |||

Healthcare Services Group Inc. Commercial & Professional Services | 2.8% | |||

Bar Harbor Bankshares Banks | 2.7% | |||

Ducommun Inc. Aerospace & Defense | 2.7% | |||

Hurco Cos. Inc. Machinery | 2.5% | |||

The Monarch Cement Co. Materials | 2.4% | |||

Alamo Group Inc. Machinery | 2.3% | |||

Group, Ameresco and Rocky Brands. Ameresco is listed among the Fund’s largest positions in the Top 10 Holdings table on this page.

Renewable Energy Group produces biomass-based diesel fuel from natural fats and sugars, much of it recycled food waste. Renewable’s second-quarter 2018 results were, in management’s words, a “step change in earnings power.” Free cash flow in the quarter jumped to nearly half the company’s market capitalization as of the day before the announcement. These positive results were attained without renewal in 2018 of the Biodiesel Mixture Excise Tax Credit (BTC). We expect the BTC, a key subsidy for renewable fuels, to be reinstated retroactively early in 2019.

Ameresco provides renewable energy and energy efficiency solutions to large consumers of purchased power, primarily in the public sector. Ameresco’s revenue, earnings and order backlog have been trending upward, as it has accumulated a portfolio of energy assets capable of providing a stable, growing stream of cash flows from long-term sales contracts. We believe Ameresco is a rare value stock that benefits from technological change. For example, the energy savings afforded

by switching to LED lighting or owning dedicated solar installations creates demand for Ameresco’s services.

After several years of uneven sales and financial returns, Rocky Brands, a footwear and apparel designer and manufacturer, sharpened its focus on its strengths, such as military, outdoor and work boots. The company also upgraded its online presence to better address current consumer preferences. Beginning in the second half of 2017, those efforts began to pay off with better sales and margins. We think Rocky’s brands have the potential to be significantly better recognized as authentic brands in their various categories.

Detractors from Fund performance included Aegean Marine Petroleum Network,2 Spartan Motors and First Internet Bancorp.

Aegean Marine Petroleum Network buys, stores and delivers fuel and lubricants to ships. We believe our losses in the stock were the result of highly questionable financial transactions that pointed to potential self-dealing on the part of company insiders. Problems began to surface in early 2017, but the real nature of the problems was not evident for another year. In February 2018, the company announced a plan to buy a private company controlled by Aegean’s former chairman on terms that we believed were manifestly unfair to Aegean. We stayed involved because of an activist campaign to change the board of directors and block the deal. The action succeeded, and the deal was abandoned. However, disclosures following a forensic examination convinced us to sell our position.

Spartan Motors makes specialty delivery and emergency response vehicles and chassis. In 2017, the company won the largest contract in its history to supply the United States Postal Service with more than 2,000 cargo body fleet vehicles, and more recently the company was selected to provide part of Amazon’s (not a Fund holding) 20,000 delivery vehicle order. However, despite impressive revenue growth in 2018, parts shortages and U.S. tariffs on imported steel and aluminum greatly reduced Spartan’s margins. Management expects the headwinds to continue into 2019.

First Internet Bancorp is an internet-based bank that seeks to minimize expenses through reliance on digital transactions. Unlike conventional banks with retail branches, First Internet Bancorp uses its online presence to attract deposits and generate loans. The bank has grown its loan book much faster than its peers, necessitating four equity raises in two years.

2. Sold by period-end.

See www.franklintempletondatasources.com for additional data provider information.

12 | Annual Report | franklintempleton.com | ||

FRANKLIN MICROCAP VALUE FUND

Asset quality has held up well to date despite the rapid growth, but investors are wary as the credit cycle ages and the pace of loan growth continues. Another problem is the Fed’s moves to raise interest rates have compressed lending margins for banks, especially for those that rely on wholesale funding such as First Internet Bancorp.

During the reporting period, we initiated positions in LSI Industries, a lighting, graphics and display components company; FreightCar America, a manufacturer of railway freight cars; Powell Industries, a provider of electrical energy equipment; and REX American Resources, an ethanol producer and retailer. We also added to some positions including Pacific Ethanol, a renewable fuels and alcohol products company; Houston Wire & Cable, an industrial wire and cable distributor; Titan Machinery, an agriculture and construction equipment dealer; Ultralife, a maker of specialized batteries and communications systems; and Flexsteel Industries, a furniture company.

We exited positions including Hardinge, Protective Insurance, Hawaiian Telcom, Golden Entertainment, Omega Protein and the aforementioned Aegean Marine Petroleum Network. The Fund also reduced its holdings in Shoe Carnival, Sterling Construction, Hurco and the aforementioned Renewable Energy, Spartan Motors and Williams Industrial Services Group.

We are disappointed with the relative and absolute performance of our Fund, particularly because stock selection accounts for the biggest part of the shortfall. Relative to its benchmark, the Fund was hurt by stock selection in the industrials and energy sectors, as well as a combination of underweighted exposure and stock selection in the health care sector. Starting over a year ago, we made changes to our process aimed at improving the quality of our holdings, primarily centered on balance sheet strength. The changes take time to implement in a portfolio such as ours, given the nature of our deep value strategy. We are confident that our actions are lowering risk in the Fund without diminishing what we consider opportunities. Like yourselves, we are shareholders. We are committed to returning the Fund to outperformance at lower-than-market risk.

Thank you for your participation in Franklin MicroCap Value Fund. We look forward to continuing to serve your investment needs.

|

Bruce C. Baughman, CPA Portfolio Manager |

The foregoing information reflects our analysis, opinions and portfolio holdings as of October 31, 2018, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

| franklintempleton.com | Annual Report | 13 | ||

FRANKLIN MICROCAP VALUE FUND

Performance Summary as of October 31, 2018

The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 10/31/181

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Sales charges will vary depending on the size of the investment and the class of share purchased. The maximum is 5.50% and the minimum is 0%.Class A:5.50% maximum initial sales charge;Advisor Class:no sales charges. For other share classes, visitfranklintempleton.com.

| Share Class | Cumulative Total Return2 | Average Annual Total Return3 | ||||||

A4 | ||||||||

1-Year | -8.11% | -13.16% | ||||||

5-Year | +19.40% | +2.44% | ||||||

10-Year | +174.53% | +10.00% | ||||||

Advisor | ||||||||

1-Year | -7.90% | -7.90% | ||||||

5-Year | +20.85% | +3.86% | ||||||

10-Year | +181.21% | +10.89% | ||||||

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

See page 16 for Performance Summary footnotes.

14 | Annual Report | franklintempleton.com | ||

FRANKLIN MICROCAP VALUE FUND

PERFORMANCE SUMMARY

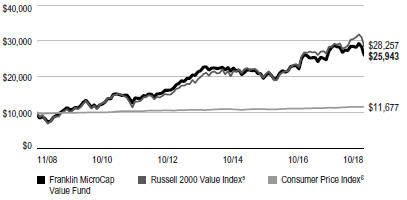

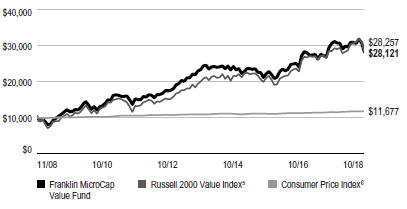

Total Return Index Comparison for a Hypothetical $10,000 Investment1

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged indexes include reinvestment of any income or distributions. They differ from the Fund in composition and do not pay management fees or expenses. One cannot invest directly in an index.

Class A(11/1/08–10/31/18)

Advisor Class(11/1/08–10/31/18)

See page 16 for Performance Summary footnotes.

| franklintempleton.com | Annual Report | 15 | ||

FRANKLIN MICROCAP VALUE FUND

PERFORMANCE SUMMARY

| Distributions(11/1/17–10/31/18) | ||||||||||||||||

Share Class

| Net Investment Income

| Short-Term Capital Gain

| Long-Term Capital Gain

| Total

| ||||||||||||

A | $0.0008 | $0.0344 | $2.5942 | $2.6294 | ||||||||||||

R6 | $0.1330 | $0.0344 | $2.5942 | $2.7616 | ||||||||||||

Advisor | $0.0905 | $0.0344 | $2.5942 | $2.7191 | ||||||||||||

| Total Annual Operating Expenses7 | ||||||||

Share Class

| With Waiver

| Without Waiver

| ||||||

A | 1.16% | 1.17% | ||||||

Advisor | 0.92% | 0.93% | ||||||

Each class of shares is available to certain eligible investors and has different annual fees and expenses, as described in the prospectus.

All investments involve risks, including possible loss of principal. The Fund’s ability to invest in smaller company securities that may have limited liquidity involves additional risks, such as relatively small revenues, limited product lines and small market share. Historically, these stocks have exhibited greater price volatility than larger company stocks, especially over the short term. In addition, the Fund may invest up to 25% of its total assets in foreign securities, which involve special risks, including currency fluctuations and economic and political uncertainty. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has a fee waiver associated with any investment it makes in a Franklin Templeton money fund and/or other Franklin Templeton fund, contractually guaranteed through 2/28/19. Fund investment results reflect the fee waiver; without this waiver, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Prior to 9/10/18, these shares were offered at a higher initial sales charge of 5.75%, thus actual returns would have differed. Total returns with sales charges have been restated to reflect the current maximum initial sales charge of 5.50%.

5. Source: Morningstar. The Russell 2000 Value Index is market capitalization weighted and measures performance of those Russell 2000 Index companies with lowerprice-to-book ratios and lower forecasted growth values.

6. Source: Bureau of Labor Statistics, bls.gov/cpi. The Consumer Price Index is a commonly used measure of the inflation rate.

7. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

See www.franklintempletondatasources.com for additional data provider information.

16 | Annual Report | franklintempleton.com | ||

FRANKLIN MICROCAP VALUE FUND

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions; and (2) ongoing Fund costs, including management fees, distribution and service(12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value” for each class of shares. You can estimate the expenses you paid during the period by following these steps (ofcourse, your account value and expenses will differ from those in this illustration):Divide your account value by $1,000 (ifyour account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (ifActual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| Actual (actual return after expenses) | Hypothetical (5% annual return before expenses) | |||||||||||

| Share Class | Beginning Account Value 5/1/18 | Ending Account Value 10/31/18 | Expenses Paid During 5/1/18–10/31/181,2 | Ending Account Value 10/31/18 | Expenses Paid During 5/1/18–10/31/181,2 | Net Annualized Expense Ratio2 | ||||||

|

|

|

| |||||||||

A | $1,000 | $947.30 | $5.64 | $1,019.41 | $5.85 | 1.15% | ||||||

R6 | $1,000 | $948.70 | $4.03 | $1,021.07 | $4.18 | 0.82% | ||||||

Advisor | $1,000 | $948.50 | $4.42 | $1,020.67 | $4.58 | 0.90% | ||||||

1. Expenses are equal to the annualized expense ratio for thesix-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 184/365 to reflect theone-half year period.

2. Reflects expenses after fee waivers and expense reimbursements. Does not include acquired fund fees and expenses.

| franklintempleton.com | Annual Report | 17 | ||

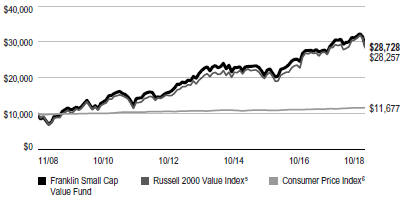

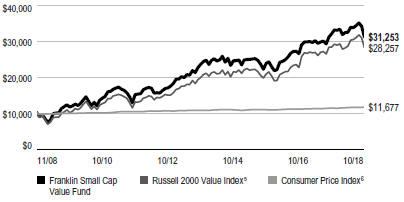

This annual report for Franklin Small Cap Value Fund covers the fiscal year ended October 31, 2018. The reorganization of Franklin MidCap Value Fund into Franklin Small Cap Value Fund, as approved by shareholders, was completed on December 1, 2017. Shares of Franklin MidCap Value Fund share classes A, C, R and Advisor were exchanged for shares in Franklin Small Cap Value Fund share classes A, C, R and Advisor, respectively. We welcome the former shareholders of Franklin MidCap Value Fund that now own shares of Franklin Small Cap Value Fund.

Your Fund’s Goal and Main Investments

The Fund seeks long-term total return by investing most of its assets in equity securities that the Fund’s investment manager believes are undervalued at the time of purchase and have the potential for capital appreciation. Under normal market conditions, the Fund invests at least 80% of its net assets in investments of small-capitalization(small-cap) companies. We definesmall-cap companies as those with market capitalizations that are similar in size at the time of purchase to those in the Russell 2000® Index.1 The Fund invests predominantly in common stocks.

Performance Overview

The Fund’s Class A shares had a-3.04% cumulative total return for the 12 months under review. In comparison, the Russell 2000® Value Index, which measures performance of those Russell 2000® Index companies with generally lowerprice-to-book ratios and lower forecasted growth values than companies listed in other stock indexes, had a-0.59% total return for the same period.1,2 You can find more of the Fund’s performance data in the Performance Summary beginning on page 21.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

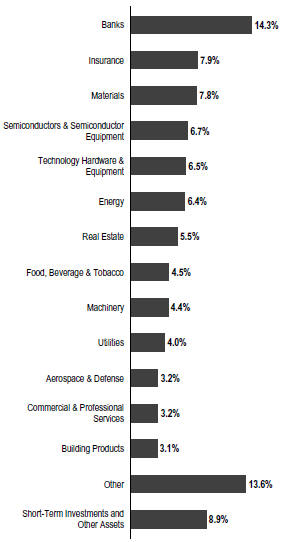

Portfolio Composition

Based on Total Net Assets as of 10/31/18

Investment Strategy

Our strategy is to invest insmall-cap companies that we believe are undervalued at the time of purchase and have the potential for capital appreciation. A stock is undervalued, or is a “value,” when it trades at less than the price at which the investment

1. The Russell 2000 Index is market capitalization weighted and measures performance of the 2,000 smallest companies in the Russell 3000 Index, which represent a small amount of the total market capitalization of the Russell 3000 Index.

2. Source: Morningstar.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI).

The SOI begins on page 45.

18 | Annual Report | franklintempleton.com | ||

FRANKLIN SMALL CAP VALUE FUND

manager believes it would trade if the market reflected all factors relating to the company’s worth. Following this strategy, the Fund invests in companies that the investment manager believes have, for example: stock prices that are low relative to current, or historical or future earnings, book value, cash flow or sales; recent sharp price declines but the potential for good long-term earnings prospects; and valuable intangibles not reflected in the stock price. The Fund also may invest in equity real estate investment trusts (REITs).

The Fund may invest up to 25% of its total assets in foreign securities.

Manager’s Discussion

During the 12 months under review, holdings that positively contributed to Fund performance included Zebra Technologies, Esterline Technologies and Energen. Zebra Technologies is listed among the Fund’s largest positions in the Top 10 Holdings table on page 20.

Zebra Technologies is a leader in the automatic identification and data capture market. Shares of Zebra Technologies rose during the year, as it reported an acceleration in year-over-year organic revenue growth, improved its gross profit margins, and made substantial progress on reducing and refinancing its debt. These positive developments helped improve the company’s earnings power. Atperiod-end we remained optimistic about Zebra Technologies’ growth prospects due to its ability to improve customer supply chains through its leadership position in mobile computing, barcode printing, data capture and RFID technologies.

Shares of Esterline Technologies, an aerospace and defense component supplier, jumped in July 2018 after reports that it was exploring a possible sale. The aerospace industry has been undergoing a consolidation phase fueled by a combination of possible increases in U.S. defense spending, growing passenger air traffic and increased industry competitiveness. In addition to speculation of a potential sale, Esterline posted improved results in August 2018 for its fiscal third quarter, including 20% operating margins in its materials business. In October 2018, the company announced an agreement to be purchased by Transdigm3 at a nearly 40% premium to its share price.

Energen is an oil and gas exploration and production company. The stock price generally followed rising crude oil prices. In addition, shares of Energen were boosted in June 2018 due to

news that activist investor Carl Icahn increased his stake in the company and in August 2018 after the announcement of an agreement to be purchased by Diamondback Energy3 at a meaningful premium. Analysts expected the acquisition to enable Diamondback Energy to consolidate its position in the Permian Basin and benefit from economies of scale.

Detractors from Fund performance included LCI Industries, Astec Industries and Versum Materials.

LCI Industries is a leading original equipment manufacturer and replacement components producer for recreational vehicles (RVs), manufactured homes and watercraft. The stock price declined as an increase in RV dealer inventories led investors to expect a reduction in production to bring supplies back in line with the pace of demand. In addition, an increase in interest rates also dampened investor sentiment. However, LCI has spent several years diversifying its business beyond RVs, and we believe its efforts lessened the negative impact. According to our analysis, consumers remain interested in the RV lifestyle, and we believe that orders will rebound and investor sentiment will improve.

Astec Industries, a leading manufacturer of road paving and mining equipment, saw its shares hurt by a decline in orders and a substantial charge related to its wood pellet business. We continued to see opportunities for Astec to increase earnings and free cash flow generation. Astec is also taking steps to improve margins and capital allocation, including retaining an outside consulting firm to assist in reducing procurement costs.

Versum Materials is a specialty materials and equipment company that primarily supplies manufacturers of logic and memory semiconductors. The company continued to post strong revenue growth and operating margins during the period, but its shares fell due to investor concerns regarding the semiconductor product cycle. The industry is experiencing a cyclical downturn as signaled by abuild-up of inventory levels and a decrease in the average selling prices of products among Versum’s key memory customers. We remain optimistic about the company’s growth prospects as industry developments in semiconductor engineering and innovation, such as increasing memory and computing capacity on physically smaller chips, have driven up demand for specialty materials.

During the reporting period, we added some new positions with the largest purchases including Synaptics, a developer of human interface hardware and software; Carpenter Technology,

3. Not a Fund holding.

See www.franklintempletondatasources.com for additional data provider information.

| franklintempleton.com | Annual Report | 19 | ||

FRANKLIN SMALL CAP VALUE FUND

| Top 10 Holdings | ||||

| 10/31/18 | ||||

Company Sector/Industry | % of Total Net Assets | |||

Old Republic International Corp. Insurance | 3.2% | |||

First Horizon National Corp. Banks | 2.7% | |||

Zebra Technologies Corp. Technology Hardware & Equipment | 2.7% | |||

The Hanover Insurance Group Inc. Insurance | 2.7% | |||

Gibraltar Industries Inc. Building Products | 2.5% | |||

Columbia Banking System Inc. Banks | 2.4% | |||

Regal Beloit Corp. Electrical Equipment | 2.2% | |||

Maple Leaf Foods Inc. (Canada) Food, Beverage & Tobacco | 2.2% | |||

Hunting PLC (U.K.) Energy | 2.2% | |||

Brinker International Inc. Consumer Services | 2.2% | |||

a producer of stainless steels and special corrosion-resistant alloys; Advanced Energy Industries, a developer of power supplies and solutions for semiconductor and industrial manufacturers; Retail Properties of America, a real estate investment trust that owns and manages high-quality shopping centers; and Finisar, a supplier of optical communication products. The Fund also added to several holdings including Caleres, a footwear company; Black Hills, an electric and gas utility company; Brinker International, a company that owns casual dining restaurant chains; and the aforementioned Esterline Technologies and Astec Industries.

In contrast, the Fund exited positions including BRP, Spirit Airlines, Validus Holdings, Gerresheimer and SAIA. We also reduced holdings in several positions including Simpson Manufacturing, AAR, Rowan Companies and McGrath RentCorp.

As fellow shareholders, we find recent absolute and relative performance disappointing, but it is not uncommon for the Fund to lag the equity market at times. Relative to its benchmark, the Fund was hurt by stock selection in the consumer discretionary and information technology sectors, while its underweighted exposure to the health care sector also hurt performance. We remain committed to our disciplined, value investing approach as we seek to generate attractive risk-adjusted returns for our shareholders.

Thank you for your participation in Franklin Small Cap Value Fund. We look forward to continuing to serve your investment needs.

|  | |

Steven B. Raineri Lead Portfolio Manager | ||

Christopher Meeker, CFA | ||

Portfolio Management Team |

The foregoing information reflects our analysis, opinions and portfolio holdings as of October 31, 2018, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

20 | Annual Report | franklintempleton.com | ||

FRANKLIN SMALL CAP VALUE FUND

Performance Summary as of October 31, 2018

The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 10/31/181

Cumulative total return excludes sales charges. Average annual total return includes maximum sales charges. Sales charges will vary depending on the size of the investment and the class of share purchased. The maximum is 5.50% and the minimum is 0%.Class A:5.50% maximum initial sales charge;Advisor Class:no sales charges. For other share classes, visitfranklintempleton.com.

| Share Class | Cumulative Total Return2 | Average Annual Total Return3 | ||||||

A4 | ||||||||

1-Year | -3.04% | -8.38% | ||||||

5-Year | +30.32% | +4.25% | ||||||

10-Year | +203.96% | +11.13% | ||||||

Advisor | ||||||||

1-Year | -2.81% | -2.81% | ||||||

5-Year | +32.08% | +5.72% | ||||||

10-Year | +212.53% | +12.07% | ||||||

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recentmonth-end performance, go tofranklintempleton.comor call(800)342-5236.

See page 23 for Performance Summary footnotes.

| franklintempleton.com | Annual Report | 21 | ||

FRANKLIN SMALL CAP VALUE FUND

PERFORMANCE SUMMARY

Total Return Index Comparison for a Hypothetical $10,000 Investment1

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged indexes include reinvestment of any income or distributions. They differ from the Fund in composition and do not pay management fees or expenses. One cannot invest directly in an index.

Class A(11/1/08–10/31/18)

Advisor Class(11/1/08–10/31/18)

See page 23 for Performance Summary footnotes.

22 | Annual Report | franklintempleton.com | ||

FRANKLIN SMALL CAP VALUE FUND

PERFORMANCE SUMMARY

| Distributions(11/1/17–10/31/18) | ||||||||||||||||

Share Class

| Net Investment

| Short-Term

| Long-Term

| Total

| ||||||||||||

A | $0.4205 | $0.6718 | $3.8289 | $4.9212 | ||||||||||||

C | $0.0602 | $0.6718 | $3.8289 | $4.5609 | ||||||||||||

R | $0.2118 | $0.6718 | $3.8289 | $4.7125 | ||||||||||||

R6 | $0.6468 | $0.6718 | $3.8289 | $5.1475 | ||||||||||||

Advisor | $0.4708 | $0.6718 | $3.8289 | $4.9715 | ||||||||||||

| Total Annual Operating Expenses7 | ||||||||

| Share Class | With Waiver

| Without Waiver

| ||||||

A | 1.05% | 1.07% | ||||||

Advisor | 0.80% | 0.82% | ||||||

Each class of shares is available to certain eligible investors and has different annual fees and expenses, as described in the prospectus.

All investments involve risks, including possible loss of principal. The Fund’s investments in smaller company stocks carry special risks as such stocks have historically exhibited greater price volatility than larger company stocks, particularly over the short term. Additionally, smaller companies often have relatively small revenues, limited product lines and small market share. In addition, the Fund may invest up to 25% of its total assets in foreign securities, which involve special risks, including currency fluctuations and economic and political uncertainty. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has a fee waiver associated with any investment it makes in a Franklin Templeton money fund and/or other Franklin Templeton fund, contractually guaranteed through 2/28/19. Fund investment results reflect the fee waiver; without this waiver, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Prior to 9/10/18, these shares were offered at a higher initial sales charge of 5.75%, thus actual returns would have differed. Total returns with sales charges have been restated to reflect the current maximum initial sales charge of 5.50%.

5. Source: Morningstar. The Russell 2000 Value Index measures performance of those Russell 2000 Index companies with lowerprice-to-book ratios and lower forecasted growth values.

6. Source: Bureau of Labor Statistics, bls.gov/cpi. The Consumer Price Index is a commonly used measure of the inflation rate.

7. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

See www.franklintempletondatasources.com for additional data provider information.

| franklintempleton.com | Annual Report | 23 | ||

FRANKLIN SMALL CAP VALUE FUND

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions; and (2) ongoing Fund costs, including management fees, distribution and service(12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value” for each class of shares. You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 =$64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| Actual (actual return after expenses) | Hypothetical (5% annual return before expenses) | |||||||||||

| Share Class | Beginning Account Value 5/1/18 | Ending Account Value 10/31/18 | Expenses Paid During 5/1/18–10/31/181,2 | Ending Account Value 10/31/18 | Expenses Paid During Period 5/1/18–10/31/181,2 | Net Annualized Expense Ratio2 | ||||||

|

|

|

| |||||||||

A | $1,000 | $958.40 | $5.13 | $1,019.96 | $5.30 | 1.04% | ||||||

C | $1,000 | $954.80 | $8.82 | $1,016.18 | $9.10 | 1.79% | ||||||

R | $1,000 | $957.30 | $6.36 | $1,018.70 | $6.56 | 1.29% | ||||||

R6 | $1,000 | $960.50 | $2.96 | $1,022.18 | $3.06 | 0.60% | ||||||

Advisor | $1,000 | $959.20 | $3.90 | $1,021.22 | $4.02 | 0.79% | ||||||

1. Expenses are equal to the annualized expense ratio for thesix-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 184/365 to reflect theone-half year period.

2. Reflects expenses after fee waivers and expense reimbursements. Does not include acquired fund fees and expenses.

24 | Annual Report | franklintempleton.com | ||

FRANKLIN VALUE INVESTORS TRUST

Franklin Balance Sheet Investment Fund

| Year Ended October 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

Class A | ||||||||||||||||||||

Per share operating performance | ||||||||||||||||||||

(for a share outstanding throughout the year) | ||||||||||||||||||||

Net asset value, beginning of year | $41.08 | $35.40 | $40.06 | $51.55 | $53.98 | |||||||||||||||

Income from investment operationsa: | ||||||||||||||||||||

Net investment incomeb | 0.45 | 0.38 | c | 0.22 | 0.19 | 0.46 | d | |||||||||||||

Net realized and unrealized gains (losses) | (0.43 | ) | 7.79 | 1.17 | (3.92 | ) | 3.06 | |||||||||||||

Total from investment operations | 0.02 | 8.17 | 1.39 | (3.73 | ) | 3.52 | ||||||||||||||

Less distributions from: | ||||||||||||||||||||

Net investment income | (0.46 | ) | (0.18 | ) | (0.28 | ) | (0.17 | ) | (0.65 | ) | ||||||||||

Net realized gains | (2.71 | ) | (2.31 | ) | (5.77 | ) | (7.59 | ) | (5.30 | ) | ||||||||||

Total distributions | (3.17 | ) | (2.49 | ) | (6.05 | ) | (7.76 | ) | (5.95 | ) | ||||||||||

Net asset value, end of year | $37.93 | $41.08 | $35.40 | $40.06 | $51.55 | |||||||||||||||

Total returne | (0.15)% | 23.63% | 4.44% | (7.73)% | 6.97% | |||||||||||||||

Ratios to average net assets | ||||||||||||||||||||

Expenses before waiver and payments by affiliates | 0.91% | 0.92% | 0.94% | 0.95% | 0.90% | |||||||||||||||

Expenses net of waiver and payments by affiliates | 0.86% | f | 0.87% | f | 0.91% | f | 0.94% | 0.89% | f | |||||||||||

Net investment income | 1.13% | 0.97% | c | 0.62% | 0.45% | 0.89% | d | |||||||||||||

Supplemental data | ||||||||||||||||||||

Net assets, end of year (000’s) | $772,976 | $841,367 | $795,663 | $915,285 | $1,221,903 | |||||||||||||||

Portfolio turnover rate | 29.85% | 24.68% | 30.25% | 26.31% | 25.08% | |||||||||||||||

aThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

bBased on average daily shares outstanding.

cNet investment income per share includes approximately $0.09 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.73%.

dNet investment income per share includes approximately $0.15 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.61%.

eTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable.

fBenefit of expense reduction rounds to less than 0.01%.

| franklintempleton.com | The accompanying notes are an integral part of these financial statements. | Annual Report | 25 | ||

FRANKLIN VALUE INVESTORS TRUST

FINANCIAL HIGHLIGHTS

Franklin Balance Sheet Investment Fund(continued)

| Year Ended October 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

Class C | ||||||||||||||||||||

Per share operating performance | ||||||||||||||||||||

(for a share outstanding throughout the year) | ||||||||||||||||||||

Net asset value, beginning of year | $39.27 | $34.01 | $38.70 | $50.22 | $52.77 | |||||||||||||||

Income from investment operationsa: | ||||||||||||||||||||

Net investment income (loss)b | 0.15 | 0.08 | c | (0.04 | ) | (0.12 | ) | 0.07 | d | |||||||||||

Net realized and unrealized gains (losses) | (0.41 | ) | 7.49 | 1.12 | (3.81 | ) | 2.99 | |||||||||||||

Total from investment operations | (0.26 | ) | 7.57 | 1.08 | (3.93 | ) | 3.06 | |||||||||||||

Less distributions from: | ||||||||||||||||||||

Net investment income | (0.17 | ) | — | — | — | (0.31 | ) | |||||||||||||

Net realized gains | (2.71 | ) | (2.31 | ) | (5.77 | ) | (7.59 | ) | (5.30 | ) | ||||||||||

Total distributions | (2.88 | ) | (2.31 | ) | (5.77 | ) | (7.59 | ) | (5.61 | ) | ||||||||||

Net asset value, end of year | $36.13 | $39.27 | $34.01 | $38.70 | $50.22 | |||||||||||||||

Total returne | (0.91)% | 22.73% | 3.65% | (8.41)% | 6.17% | |||||||||||||||

Ratios to average net assets | ||||||||||||||||||||

Expenses before waiver and payments by affiliates | 1.66% | 1.67% | 1.69% | 1.70% | 1.65% | |||||||||||||||