Valuation Analysis – Project Giant September 7, 2008 CONFIDENTIAL Presentation to the Board of Directors Exhibit (c)(6) |

2 CONFIDENTIAL Valuation Overview Emory’s role is to recommend to the Board of Directors compensation for Gehl’s common stock to comply with Section DFI-Sec 6.05(1)(a)1a of the regulations of the Wisconsin Department of Financial Institutions in connection with a proposed going private transaction To accomplish this, we have: Met with management and visited the headquarters and manufacturing facilities Reviewed information provided by Gehl Reviewed publicly available information Completed various analyses and studies This recommendation is subject to certain limiting conditions set forth in our opinion letter attached as Appendix As of September 5, 2008 Emory & Co., LLC recommends compensation equal to the fair value of $19.79 per share for the common stock of Gehl Company (“Gehl”) |

3 CONFIDENTIAL Gehl Financial Summary We have summarized Gehl’s projected and historical financial performance Latest Twelve Months 12/31/13 12/31/12 12/31/11 12/31/10 12/31/09 12/31/2008 (c) 6/30/2008 (b) (c) 12/31/07 12/31/06 12/31/05 12/31/04 12/31/2003 (a) Fiscal year End $731,855,000 $729,889,000 $656,496,000 $558,491,000 $469,812,000 $394,012,000 $400,289,000 $457,612,000 $486,217,000 $446,959,000 $325,237,000 $211,828,000 Net Sales $68,065,000 $69,695,000 $56,754,000 $39,269,000 $23,004,000 $15,838,000 $20,462,000 $37,349,000 $42,868,000 $33,356,000 $21,016,000 $4,378,000 Income from Continuing Ops. before Taxes $2,000,000 $2,000,000 $4,080,000 Adjustments $68,065,000 $69,695,000 $56,754,000 $39,269,000 $23,004,000 $17,838,000 $22,462,000 $37,349,000 $42,868,000 $33,356,000 $21,016,000 $8,458,000 Adjusted Pretax Income ($22,122,000) ($22,651,000) ($18,446,000) ($12,763,000) ($7,476,000) ($4,989,000) ($6,380,000) ($12,400,000) ($14,790,000) ($11,218,000) ($6,939,000) ($1,082,000) Actual Taxes ($600,000) ($600,000) ($881,280) Estimated Taxes on Adjustment $45,943,000 $47,044,000 $38,308,000 $26,506,000 $15,528,000 $12,249,000 $15,482,000 $24,949,000 $28,078,000 $22,138,000 $14,077,000 $6,494,720 Net Income 12,000,000 12,000,000 12,000,000 12,000,000 11,975,000 12,253,000 12,279,000 12,459,000 12,421,000 11,054,000 9,134,000 8,069,000 Weighted Average Diluted Shares Outstanding $3.83 $3.92 $3.19 $2.21 $1.30 $1.00 $1.26 $2.00 $2.26 $2.00 $1.54 $0.80 Adjusted Diluted Earnings per Share $267,603,000 $261,030,000 $230,781,000 $208,493,000 $136,461,000 $98,000,000 Stockholders' Equity 12,135,737 12,127,623 12,197,037 12,006,527 9,931,823 8,000,159 Shares Outstanding $22.05 $21.52 $18.92 $17.36 $13.74 $12.25 Book Value per Share ($400,000) $1,964,000 $2,753,000 $2,494,000 $449,000 $890,000 $1,314,000 $772,000 ($663,000) $1,155,000 $526,000 $1,863,000 Interest Expense (Income) $15,383,000 $14,230,000 $13,102,000 $11,998,000 $9,523,000 $4,712,000 $4,355,000 $4,576,000 $4,553,000 $4,945,000 $4,664,000 $4,923,000 Depreciation and Amortization $83,048,000 $85,889,000 $72,609,000 $53,761,000 $32,976,000 $23,440,000 $28,131,000 $42,697,000 $46,758,000 $39,456,000 $26,206,000 $15,244,000 Adjusted EBITDA (a) 2003 earnings exclude asset impairment and other restructuring costs of approximately $4.080 million pretax. Estimated tax for the 2003 adjustment is based on the Company's effective tax rate of 21.6%. (b) Latest twelve months weighted average diluted shares outstanding is estimated as June 30, 2008 amount. (c) Excludes adoption of SFAS 157 charges of approximately $2,000,000 pretax and $1,400,000 aftertax. |

4 CONFIDENTIAL Key Drivers The valuation drivers considered in our valuation of Gehl included, but were not limited to the following: Stock market valuations are down overall and particularly in Gehl’s area Downturn in the U.S. residential construction market Emerging weakness in Europe, particularly Spain Capital expenditures for the new flexible manufacturing plant Rising steel prices Market share gains in both construction and agricultural markets Diversification due to international and agricultural markets |

5 CONFIDENTIAL Valuation Methodologies We have based our recommendation on the following valuation methodologies: Acquisition Premium Analysis Applied an acquisition premium to Gehl’s public market price per share Comparable Transaction Analysis Applied the reconciled multiples of sales, earnings, book value, EBIT, EBITDA to Gehl’s statistic based on similar merger and acquisition transactions Discounted Cash Flow Analysis Determined the present value of future cash flows based on a weighted average cost of capital Leveraged Buyout Analysis Determined the amount a financial buyer would pay to purchase the company given a reasonable rate of return |

6 CONFIDENTIAL Acquisition Premium Analysis Emory took Gehl’s September 5, 2008 market price ($13.66 per share) and added an acquisition premium (35%) Emory examined Gehl’s historical stock prices and trading volume Gehl was compared to eight public companies that were considered somewhat similar to Gehl: We used Gehl’s September 5, 2008 closing market price as an indication of the stock’s marketable minority value Komatsu Ltd. Deere & Company Terex Corporation Alamo Group Inc. Astec Industries, Inc. Oshkosh Corporation CNH Global N.V. Caterpillar Inc. |

7 CONFIDENTIAL Multiple Comparison Gehl’s ratios and multiples were generally within the range of the public companies We used Gehl’s September 5, 2008 closing market price as an indication of the stock’s marketable minority value Comparable Company Group Multiples of: Gehl Mean Median Range LTM Earnings 10.8 x 9.7x 10.6x 5.0x - 13.1x 2008E Earnings 13.7 x 9.0x 9.5x 4.4x - 12.9x 2009E Earnings 10.5 x 8.3x 9.6x 5.1x - 10.6x LTM EBITDA (1) 8.5 x 6.6x 6.8x 3.7x - 9.2x 2008E EBITDA (1) 10.2 x 6.4x 6.6x 3.5x - 8.7x 2009E EBITDA (1) 7.2 x 5.9x 6.1x 3.3x - 7.6x LTM Sales (1) 0.6 x 0.9x 0.8x 0.5x - 1.8x (1) Multiple of Enterprise Value (Market Capitalization + Debt - Cash) |

8 CONFIDENTIAL Multiple Comparison Based on September 5, 2008 closing market prices, except Komatsu which trades on the Tokyo Stock Exchange Enterprise Value / EBITDA Market Enterprise Estimated Estimated Latest 12 Prior Enterprise Value Capitalization Value 2009 2008 Months Fiscal Year to Sales Gehl $166 $239 7.2 x 10.2 x 8.5 x 5.6 x 0.6 x Caterpillar $39,000 $69,214 6.9 x 7.4 x 7.9 x 8.5 x 1.4 x CNH $7,451 $17,164 6.1 x 6.6 x 7.5 x 8.6 x 0.9 x Oshkosh $1,067 $3,994 5.8 x 5.2 x 5.1 x 5.5 x 0.6 x Astec $706 $666 5.2 x 5.5 x 6.0 x 6.6 x 0.7 x Alamo $183 $291 6.2 x 6.5 x 7.6 x 8.6 x 0.5 x Terex $3,777 $4,543 3.3 x 3.5 x 3.7 x 4.4 x 0.5 x Deere $27,145 $47,833 7.6 x 8.7 x 9.2 x 10.4 x 1.8 x Komatsu ¥1,908,783 ¥2,316,922 NA 7.7 x 5.6 x 5.8 x 1.0 x |

9 CONFIDENTIAL Multiple Comparison Based on September 5, 2008 closing market prices, except Komatsu which trades on the Tokyo Stock Exchange Price / Earnings Ratio 2009 2008 Estimated Estimated Latest Latest Average Average Earnings Earnings 12 Months Fiscal Year 3-year 5-year Gehl 10.5 x 13.7 x 10.8 x 6.8 x 6.5 x 7.9 x Caterpillar 9.6 x 10.6 x 10.5 x 11.9 x 13.2 x 16.8 x CNH 7.5 x 8.8 x 10.7 x 13.3 x 22.0 x 43.1 x Oshkosh 5.4 x 4.4 x 5.0 x 4.0 x 5.0 x 6.4 x Astec 10.5 x 11.2 x 11.6 x 12.5 x 17.2 x 30.1 x Alamo 9.6 x 10.2 x 11.7 x 15.0 x 15.8 x 16.3 x Terex 5.1 x 5.4 x 5.5 x 6.5 x 10.0 x 15.6 x Deere 10.6 x 12.9 x 13.1 x 15.8 x 19.7 x 23.1 x Komatsu NA 8.7 x 9.1 x 9.4 x 12.3 x 17.5 x |

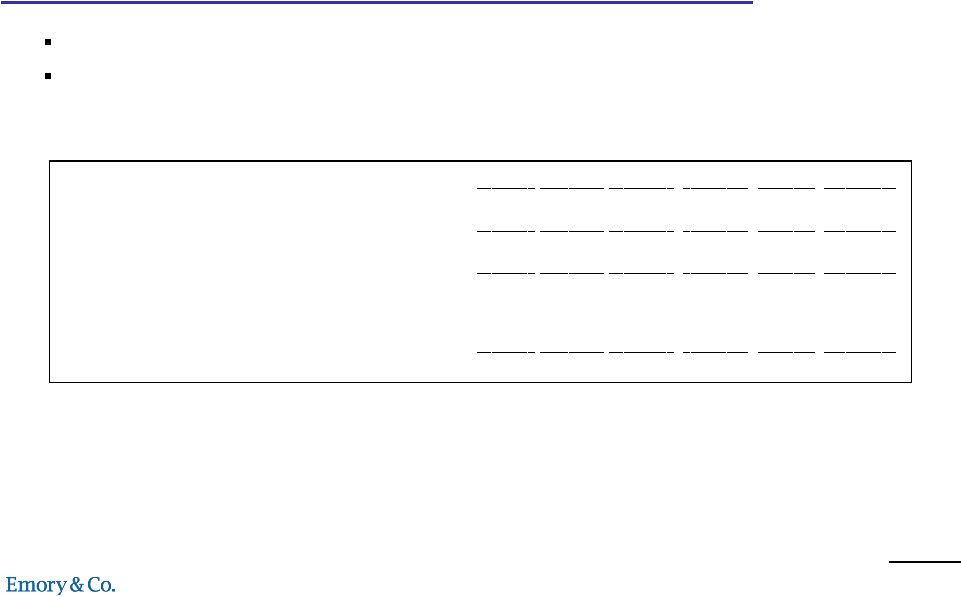

10 CONFIDENTIAL Acquisition Premium Analysis We determined that a 35% premium is appropriate The Acquisition Premium Analysis results in an equity value of $226,000,000 We then reviewed various sources of acquisition premiums Percent Premium for Transactions All Industries 2007 2006 2005 2004 _______ _______ _______ _______ S&P 500 Price to Earnings Ratio 18.0x 18.3x 19.5x 22.3x Average Premium for Purchasing a Controlling Interest 31.6% 31.9% 33.6% 30.9% Number of Transactions 477 440 369 309 Median Premium for Purchase Prices from $100.0 million through $499.9 million 24.5% 22.3% 21.9% 21.2% Number of Transactions 148 145 124 95 Industrial & Farm Equipment & Machinery Industry 2007 2006 2005 2004 _______ _______ _______ _______ Average Price to Earnings Ratio 16.4x 12.9x 26.9x 27.0x Average Premium 22.0% 39.8% 41.0% 20.5% Average TIC / EBITDA 9.9x 9.7x 11.6x 11.2x Average TIC / EBIT 12.5x NA 15.0x 17.5x Number of Transactions 189 208 197 185 EBIT = Earnings before interest expense and taxes EBITDA = Earnings before interest expense, taxes, depreciation and amortization TIC = Base equity price plus interest-bearing debt and preferred stock Source: Factset Mergerstat Comparable Transactions JLG Industries, Inc. Control Premium (1) 34.4% A.S.V., Inc. Control Premium (2) 47.9% Sources: Press Releases and SEC Filings (1) Premium based on offer from Oshkosh Truck Corporation dated October 16, 2006 and JLG Industries, Inc.'s stock price 5 business days prior. (2) Premium based on offer from Terex Corporation dated January 14, 2008 and A.S.V., Inc.'s stock price 5 business days prior. |

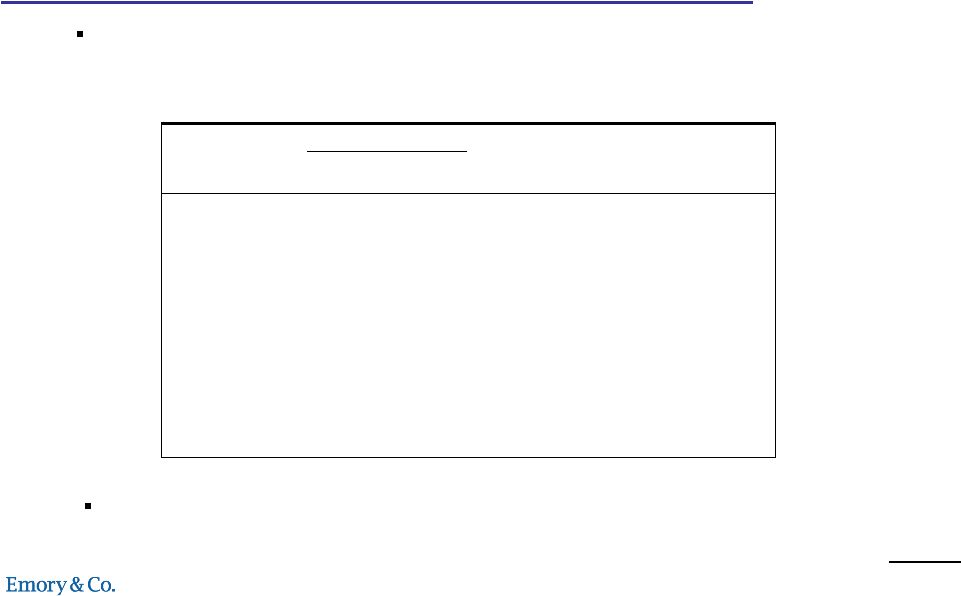

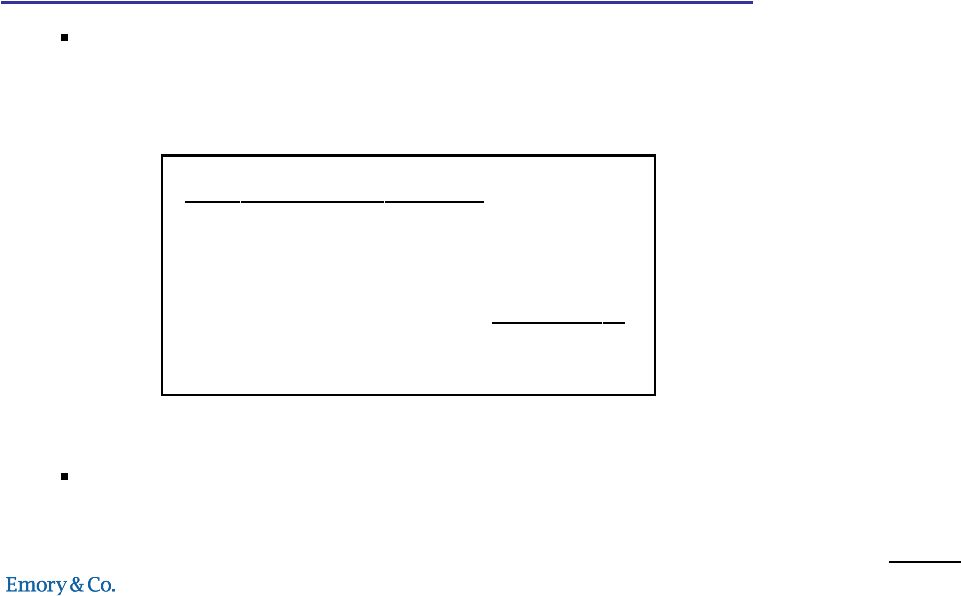

11 CONFIDENTIAL Comparable Transaction Analysis The table below summarizes acquisition valuation multiples for companies with similar characteristics Using the Comparable Transaction Analysis, we determined an equity value of $300,000,000 ($ in millions) Equity Value to: Enterprise Value to: ________________ ________________________ Target / Acquirer Equity Enterprise Net Book Net Book Date Target Description Value Value Sales Income EBIT EBITDA (Equity) Income (Equity) Sales EBIT EBITDA _______ _________________________________________ _________ __________ _________ _______ _______ _______ _________ _______ _______ _______ _______ _______ Jan-08 A.S.V., Inc. / Terex (1) $487.7 $450.5 $199.9 $11.3 $9.5 $12.8 $184.8 43.3 x 2.6 x 2.3 x 47.3 x 35.2 x Manufacturer of track loaders Oct-06 JLG Industries, Inc. / Oshkosh Truck Corp. (1) $3,200.0 $3,123.1 $2,351.0 $161.5 $176.1 $205.2 $717.3 19.8 x 4.5 x 1.3 x 17.7 x 15.2 x Manufacturers of telehandlers Oct-04 Loegering Mfg. Inc. / ASV Inc. NA $18.2 $12.4 NA $0.7 $1.3 $2.4 NA NA 1.5 x 24.8 x 14.5 x Manufacturer of Steel Tracks Aug-03 TRAK International, Inc. / JLG Industries, Inc. $100.0 $100.0 $233.3 Neg NA Neg Neg NM NM 0.4 x NM NM Manufacturer of telescopic material handlers Jan-03 PA Crusher Corp. / K-Tron International, Inc. NA $23.5 $35.2 NA $4.2 $5.1 $9.2 NA NA 0.7 x 5.6 x 4.7 x Manufacturer of crusher and feeding equipment Oct-97 Brunel America Inc. / Gehl Company (2) $27.7 $27.7 $57.5 $1.1 NA $3.3 $9.9 25.2 x 2.8 x 0.5 x NA 8.4 x Designer, Manufacturer and distributor of skid steer loaders Average $953.9 $623.8 $481.5 $57.9 $47.6 $45.5 $184.7 29.4 x 3.3 x 1.1 x 23.9 x 15.6 x Median $293.9 $63.9 $128.7 $11.3 $6.8 $5.1 $9.9 25.2 x 2.8 x 1.0 x 21.3 x 14.5 x Gehl Company $250.0 $322.9 $400.3 $15.5 $23.8 $28.1 $267.6 16.1 x 0.9 x 0.8 x 13.6 x 11.5 x $300.0 $372.9 $400.3 $15.5 $23.8 $28.1 $267.6 19.4 x 1.1 x 0.9 x 15.7 x 13.3 x $350.0 $422.9 $400.3 $15.5 $23.8 $28.1 $267.6 22.6 x 1.3 x 1.1 x 17.8 x 15.0 x (1) Per SEC Filings and press releases. (2) EBITDA is estimated as cash flow. |

12 CONFIDENTIAL Discounted Cash Flow Analysis We discounted free cash flow to Gehl from 2008 – 2013 based on management’s projection At the end of 2013, we assumed that Gehl would be sold based on a multiple of EBITDA Gehl Company Fiscal Years Ending December 31, 2008 2009 2010 2011 2012 2013 Earnings before Interest, Taxes, Depreciation & Amortization (EBITDA) $7,813 $32,976 $53,761 $72,609 $85,889 $83,048 Depreciation & Amortization $1,571 $9,523 $11,998 $13,102 $14,230 $15,383 Earnings before Interest and Taxes (EBIT) $6,243 $23,453 $41,763 $59,507 $71,659 $67,665 Estimated Taxes ($2,029) ($7,622) ($13,573) ($19,340) ($23,289) ($21,991) Earnings before Interest After Taxes (EBIAT) $4,214 $15,831 $28,190 $40,167 $48,370 $45,674 Depreciation and Amortization $1,571 $9,523 $11,998 $13,102 $14,230 $15,383 Changes in Working Capital $14,474 ($30,857) ($39,925) ($43,898) ($35,573) ($954) Capital Expenditures ($7,199) ($25,108) ($8,408) ($8,658) ($8,908) ($9,158) Free Cash Flow $13,060 ($30,611) ($8,145) $713 $18,119 $50,945 |

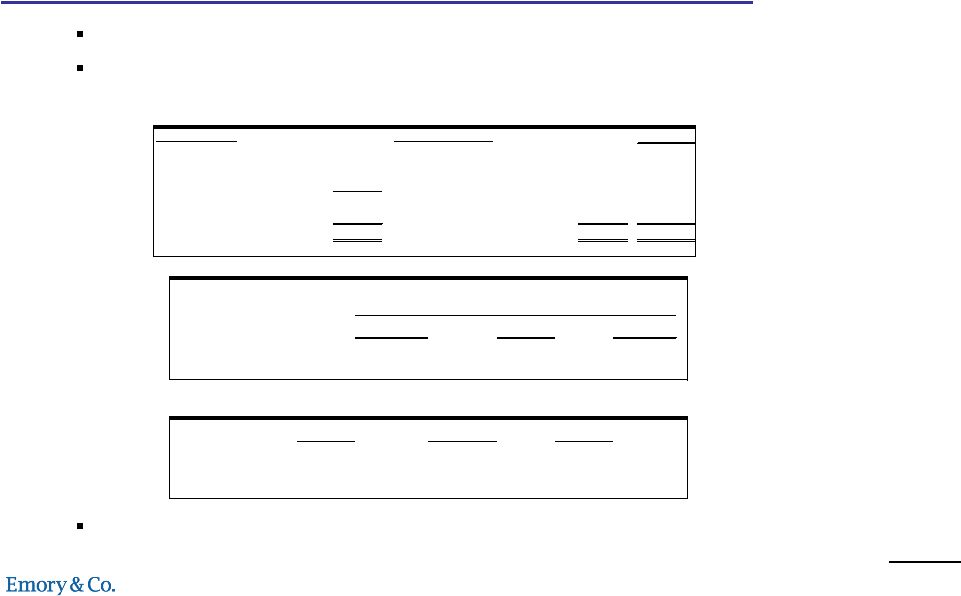

13 CONFIDENTIAL Discounted Cash Flow Analysis We used a weighted average cost of capital of 12.9%, developed by assuming 60% equity financing and 40% debt financing and projections through 2013 Using the Discounted Cash Flow Analysis, we determined an equity value of $228,000,000 Discounted Net Cash Flow with an EBITDA Multiple Terminal Value Terminal Present Value of Less Plus Present Discount EBITDA Cash Terminal Aggregate Existing Excess Value of Rate Multiple Flow Value Value Debt Cash Equity 6.0 x $15,805 $237,560 $253,365 $180,494 14.9% 6.5 x $15,805 $257,357 $273,162 $77,855 $4,984 $200,291 7.0 x $15,805 $277,154 $292,958 $220,087 6.0 x $18,225 $260,883 $279,109 $206,238 12.9% 6.5 x $18,225 $282,623 $300,849 $77,855 $4,984 $227,978 7.0 x $18,225 $304,364 $322,589 $249,718 6.0 x $20,971 $286,976 $307,946 $235,075 10.9% 6.5 x $20,971 $310,891 $331,861 $77,855 $4,984 $258,990 7.0 x $20,971 $334,805 $355,776 $282,905 |

14 CONFIDENTIAL Leveraged Buyout Analysis Using the Leveraged Buyout Analysis, Emory determined an equity value of $220,000,000 The $220,000,000 is based upon a financial buyer with 65% debt and 35% equity, assuming the business is sold in 2013 Projects cash flows based on management’s projection with the additional interest expense related to the new debt Sources and Uses Summary Uses of Funds Sources of Funds % Purchase Price of Equity $220.0 Revolver $6.0 2.0% Plus: Debt Refinanced 77.9 Senior Term Debt 191.8 63.0% Less: Cash 5.0 Subordinated Debt 0.0 0.0% Aggregate Purchase Price 292.9 Equity 106.6 35.0% Transaction Fees and Expenses 11.6 Other 0.0 0.0% Total Uses of Funds $304.5 Total Sources of Funds $304.4 100.0% Return Calculation 2013 EBITDA Exit Multiple 6.0x 6.5x 7.0x Equity IRR 20.5% 24.0% 27.1% Purchases Price Multiple Analysis LTM 2009 2010 EBIT 12.3 x 12.5 x 7.0 x EBITDA 10.4 x 8.9 x 5.4 x |

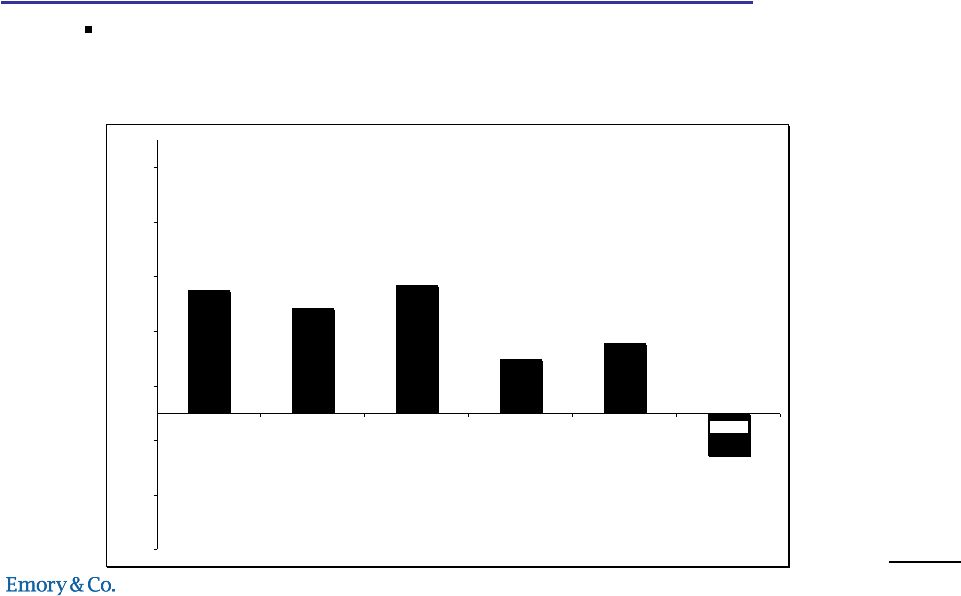

15 CONFIDENTIAL Transaction Premium Implications The following graph shows the premium of the fair value of $19.79 per share as of September 5, 2008 to the historical market price of Gehl Implied Premium Relative to Gehl's Historical Trading Performance 44.9% 38.5% 46.7% 19.9% 25.8% -15.3% -50.0% -30.0% -10.0% 10.0% 30.0% 50.0% 70.0% 90.0% Closing Price September 5, 2008 30 Day 60 Day 90 Day 180 Day 52 Week |

16 CONFIDENTIAL Valuation Summary We have used the following approaches to determine a fair value of $245,000,000 which is converted to a per share value based on fully diluted shares outstanding. As of September 5, 2008, Emory & Co., LLC recommends compensation equal to the fair value of $19.79 per share for the common stock of Gehl Company Method Acquisition Premium Analysis $226,000,000 Comparable Transaction Analysis $300,000,000 Discounted Cash Flow Analysis $228,000,000 Leveraged Buyout Analysis $220,000,000 Reconciled Fair Value $245,000,000 Fair Value per Share $19.79 |

17 CONFIDENTIAL Appendix |

September 7, 2008

CONFIDENTIAL

Board of Directors

Gehl Company

143 Water Street

P.O. Box 179

West Bend, WI 53095-0179

Dear Directors:

The Board of Directors of Gehl Company (“Gehl” or the “Company”) has asked Emory & Co., LLC (“Emory”) to recommend the compensation for 100% of the outstanding common stock of Gehl (the “Opinion”). This is being done to satisfy the condition of Section DFI-Sec 6.05(1)(a)1a of the regulations of the Wisconsin Department of Financial Institutions in connection with a proposed going private transaction (the “Transaction”).

As used in this Opinion, the term “fair value” means the value of the shares of common stock of the Company, excluding any appreciation or depreciation in anticipation of the proposed Transaction, with no minority discount or lack of marketability discount; it is intended to reflect the value of a shareholder’s proportionate interest in the Company without any such discounts.

Emory is a business valuation and merger & acquisition advisory firm that is continually engaged in the valuation of businesses and their securities in connection with mergers and acquisitions, employee stock ownership plans, estate planning, corporate and other purposes. Emory does not beneficially own, nor has it ever beneficially owned, any interest in Gehl.

Emory’s Opinion is intended for the use and benefit of Gehl’s Board of Directors in connection with, and for the purpose of, its consideration of the Transaction. The Opinion is directed only to the recommended compensation for the proposed Transaction from a financial point of view to the holders of Gehl’s common stock, and does not address the merits of the underlying decision by Gehl’s Board of Directors to engage in the Transaction, and does not constitute a recommendation to any shareholder as to how that shareholder should vote with respect to the Transaction.

Board of Directors

Gehl Company

September 7, 2008

Page 2

In arriving at its opinion, Emory, among other things:

| 1. | reviewed Gehl’s most recent Form 10-K and Form 10-Q filed with the U.S. Securities and Exchange Commission; |

| 2. | reviewed Gehl’s audited financial statements for the five years ended December 31, 2007; |

| 3. | reviewed unaudited interim financial statements, which Gehl’s management has identified as being the most current financial statements available; |

| 4. | reviewed certain operating and financial information provided to Emory by management relating to Gehl’s business and prospects; |

| 5. | reviewed research analyst reports on Gehl by Robert W. Baird & Co., Incorporated, Sidoti & Company, LLC, and BMO Capital Markets Corp.; |

| 6. | interviewed certain members of Gehl’s senior management to discuss its operations, historical financial statements, and future prospects; |

| 7. | toured Gehl’s corporate offices in West Bend, Wisconsin, and its manufacturing facilities in Yankton and Madison, South Dakota; |

| 8. | reviewed certain publicly available filings, financial data, stock market performance data, and dividend policies regarding Gehl; |

| 9. | reviewed publicly available financial data and stock market performance data of publicly traded companies Emory considered somewhat similar to Gehl; |

| 10. | reviewed publicly available prices and premiums paid in transactions Emory considered somewhat similar to the Transaction; and |

| 11. | conducted such other studies, analyses, inquiries, and investigations, as Emory deemed appropriate for purposes of its Opinion. |

In providing its opinion, Emory relied upon and assumed, without independent verification, the accuracy and completeness of all financial information that was available to it from public sources and all the financial and other information provided to it by Gehl or its representatives. Emory further relied upon the assurances of Gehl’s management that they were unaware of any facts that would make the information Gehl or its representatives provided incomplete or misleading. Emory assumed the projected financial results were reasonably prepared on bases reflecting the best currently available estimates and judgment of Gehl’s management. Emory did not express an

Board of Directors

Gehl Company

September 7, 2008

Page 3

opinion or any other form of assurance as to the reasonableness of the underlying assumptions. Emory did not solicit any third party indications of interest for the acquisition of all or any part of Gehl. Emory did not advise Gehl’s Board of Directors on alternatives to the Transaction, nor did it review any merger agreement, offer to purchase, recommendation statement, proxy statement, or similar documents that have been or may be prepared for use in connection with the Transaction. Emory’s opinion is necessarily based on economic, market, financial and other conditions as they exist and can be evaluated by it as of the date of this letter. Emory did not perform or obtain an independent appraisal of any of Gehl’s assets or liabilities. Emory did not conduct or provide environmental liability assessments of any kind, so its opinion does not reflect any actual or contingent environmental liabilities. Emory provides no legal, accounting, or tax advice.

Based on the above discussion and its experience, as of September 5, 2008, Emory & Co., LLC recommends compensation equal to the fair value of $19.79 per share for the common stock of Gehl.

Very truly yours,

Emory & Co., LLC