UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-6094 |

|

THE LATIN AMERICA EQUITY FUND, INC. |

(Exact name of registrant as specified in charter) |

|

Eleven Madison Avenue, New York, New York | | 10010 |

(Address of principal executive offices) | | (Zip code) |

|

J. Kevin Gao, Esq. The Latin America Equity Fund, Inc. Eleven Madison Avenue New York, New York 10010 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (212) 325-2000 | |

|

Date of fiscal year end: | December 31st | |

|

Date of reporting period: | January 1, 2006 to December 31, 2006 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

THE LATIN AMERICA

EQUITY FUND, INC.

ANNUAL REPORT

DECEMBER 31, 2006

LAQ-AR-1206

LETTER TO SHAREHOLDERS

January 31, 2007

Dear Shareholder:

For the year ended December 31, 2006, The Latin America Equity Fund, Inc. (the "Fund") had an increase in its net asset value (NAV) of 48.66%, assuming reinvestment of dividends and distributions, net of all fees, expenses and taxes. By comparison, the Morgan Stanley Capital International Latin America Index* ("MSCI Latin America") had an increase of 43.15% (total return index, net of foreign taxation) for the period. Based on market price, the Fund's shares rose 61.62% during the year.

Additionally, the Fund paid two dividends during the calendar year. The first for US$0.95 was paid on September 15, 2006. The second for US$4.48 per share was paid on January 5, 2007. Taken together, these two dividends represent a dividend yield of 17.8% based on the share price of $30.46 at the start of the year. The Fund's discount to its NAV decreased throughout the year from 13.59% on December 31, 2005, to 6.06% as of December 29, 2006.

Latin America: Leading an Outperforming Asset Class

2006 was another very positive year for emerging market equities around the world due to robust global growth, strong commodity prices, low levels of risk aversion, and supportive liquidity conditions. The MSCI Emerging Markets Index returned 32.17%, eclipsing developed equity market returns.

Latin America outperformed the broader emerging markets group, with the MSCI Latin America Index returning 43.15% for the period ended December 31, 2006.

A Year of Political Change

From a political point of view, 2006 was an interesting year. Ten presidential elections were held in the region. Hugo Chávez in Venezuela made concerted efforts to lead the region leftward, drawing on traditional populist economic policies and away from market-led solutions to economic problems. High oil prices coupled with an increasingly firm grip on sources of power and patronage in Venezuela gave him ample room to use oil revenues for these purposes. He opposed all U.S. foreign policy objectives in the region and went out of his way to provoke the United States.

From a market perspective, Mr. Chávez's efforts are irrelevant, given that Venezuela is not represented in the MSCI Indexes. From this perspective, he is relevant only to the extent that he is able to influence other countries in the region. In this, Mr. Chávez was successful in Bolivia and Ecuador, whose presidential candidates aligned themselves with his position. He tried and failed to influence a closely fought election in Perú, but succeeded only in seriously damaging his relations with the eventual winner, Alan García. Mexico was more challenging for Mr. Chávez to influence and Presidential candidate Andrés Manuel López Obrador was astute enough to keep Mr. Chávez at arm's length. Mr. López Obrador eventually lost a tightly contested election to Felipe Calderón. In the aftermath of the election, markets worried that Mr. López Obrador's claims that the election was fraudulent could lead to an institutional breakdown in Mexico. However, as it became evident that Mr. López Obrador's threats to disrupt the handover were having a high political price, he backed down and the transition took place peacefully.

1

LETTER TO SHAREHOLDERS (CONTINUED)

In Brazil, there was no serious threat to President Lula from the left, so there was less at stake than in other contests for most market participants. The election did go to a second round after Geraldo Alckmin had a better than expected showing in the first round. However, in the second round, Lula stretched his lead and won comfortably. During the campaign period much attention was paid to the relatively slow rate of economic growth during Lula's first term of office. Additionally, Lula used privatization to attack his opponent, suggesting that in his second term we may see a shift in the government's approach to using private capital to stimulate investment.

Strong Macroeconomic Fundamentals

For the year, from an economic perspective, certain themes were shared across the region. The first and perhaps most important was the great improvement in external accounts. Strong commodity prices helped greatly, but lower barriers to trade and competitive currencies also helped to create the conditions for robust trade surpluses. In the case of Mexico, in particular, remittances from Latin Americans working abroad were partly responsible for current account surpluses.

Exchange rate policy has also been instrumental in ensuring current account surpluses. Most Latin American currencies now float freely, but thanks to strong economic fundamentals many currencies were once again revalued against the U.S. dollar in the course of 2006.

Against this backdrop, Latin America has also been deleveraging, both at the government and corporate levels. In particular, Latin America has reduced the amount of U.S. dollar borrowing outstanding. The net result is that the region is far less dependent on foreign capital flows than was once the case.

With the exception of Argentina and Venezuela, inflation has come down across the board. Monetary stability has led to significant improvements in the financial systems of many Latin American countries—spurring wider usage of the formal banking system and credit creation.

Again with the exception of Venezuela, governments across the region have made great improvements on the fiscal side, doing a better job at collecting taxes and restraining expenditures.

Even though economic growth across the region was moderate, the stability of economic conditions helped companies to deliver margin improvements and strong earnings growth for 2006.

Brazil Led Latin Equity Markets in 2006

Turning to the equity markets, Brazil was a standout in 2006, reaching all-time highs on the back of a supportive environment for commodity prices. This led to encouraging inflation reports and the anticipation of interest rate cuts after an extended cycle of tightening. These factors countered worries over political scandals that plagued the market in the run up to the Presidential elections.

The second most significant component of the MSCI Latin America index, Mexico, also performed well, returning 41.4%. Supported by low inflation and interest rates, strong domestic consumption was driven by credit growth and remittances from the United States. Additionally, corporate earnings were strong, boosted by a recovering U.S. economy.

2

LETTER TO SHAREHOLDERS (CONTINUED)

Among the smaller markets, Argentina and Peru were very strong while Chile and Colombia underperformed. In the case of Chile, despite high prices for copper and excellent macroeconomic conditions, specific supply side problems had an impact on economic output that caused the equity market to lag in the first half of the year. Colombia, in our opinion, remains one of the most interesting markets in the region for the medium and longer term. We expect liquidity to increase and anticipate that Colombia will represent a larger part of the MSCI Latin America Index in the future. We remain invested in Colombia.

Performance: Participating in a multi-sector rally

The Fund outperformed the MSCI Latin America Index by 551 basis points, net of fees and expenses. Our overweight position in América Telecom (5.3% of the Fund as of December 31, 2006) was beneficial to performance, particularly after the announcement of the merger between América Telecom and América Móvil (3.2% of the Fund as of December 31, 2006). In Brazil an overweight and strong stock selection contributed to returns. In particular, our positions in railroad operator ALL América Latina Logística (1.4% of the Fund as of December 31, 2006), sugar and ethanol producer Cosan S.A. (1.1% of the Fund as of December 31, 2006), and the Mexican fast food operator Alsea (0.5% of the Fund as of December 31, 2006) all contributed strongly to returns. On the negative side of the ledger, our underweights in the Mexican bank Banorte (0.0% of the Fund as of December 31, 2006) and the specialist pipe manufacturer Tenaris (1.6% of the Fund as of December 31, 2006) detracted from returns.

The Portfolio and Outlook

Even though we have now completed our fourth consecutive year of positive equity market returns for the region, we continue to be bullish on the outlook for Latin American equities. This bullishness is predicated on the assumption that as a whole, the region should be able to maintain continuity of macroeconomic policy in the years ahead. If past performance were a guide to future performance, investors would have ample reason to be nervous at this stage of the cycle. That said, however, we are firm believers that the benefits of economic stability over a protracted period of time can be profound and long lasting.

The best advertisement for the impact of stability is to look at the progress Chile has made over the last two decades by virtue of pursuing the same coherent macroeconomic policies. Even Chile, however, still has much to do to improve standards of living and standards of education for its citizens as the wealth that has been generated over the years permeates throughout the economy. Those challenges represent ongoing opportunities for investors.

A popular misconception about Latin America is that the region depends mainly on the export of natural resources to the rest of the world. This is an oversimplification. We believe many of the best investment opportunities are ones that involve bringing first world products and services to consumers who have never had the opportunity to enjoy those products and services. We believe that, if economic stability can be maintained, the potential for growth of domestic consumption is enormous.

We also see significant potential in infrastructure investments. This includes electricity generation and transmission, roads, ports, railway, airports and airlines. Faced with the need to improve antiquated infrastructure in their countries, but constrained on the fiscal side, many governments in the region are turning to the private sector to lead investment. Again, anyone who has traveled the excellent new highways that have been built with private capital in Chile in recent years knows that this development model can work.

3

LETTER TO SHAREHOLDERS (CONTINUED)

Capital market conditions have remained buoyant throughout 2006, with greater liquidity and fund flows encouraging much new issue activity. This has given investors a much broader range of investment options, often in sectors of the economy to which it had previously been impossible to gain exposure. We believe that the new issue activity is more a positive than a negative, given that the total amount of capital raised in 2006 was significantly less than the amount of corporate cash flow dedicated to dividends and share buy backs.

We have maintained our overweight position in Brazil during the course of the year while we increased our exposure to Chile and Colombia. We reduced exposure to Argentina and Peru; however, Mexico remains our most significant underweight.

It is hard to generalize our sector exposure since our approach to stock selection is essentially a bottom up approach that can often mean being overweight in a sector in one country while underweight in the same sector in another. Broadly speaking, we are underweight in materials stocks—many of which we believe are trading at peak cycle multiples. We are generally overweight in consumption, financials and infrastructure stocks.

Looking forward in 2007, we expect to see more volatility as the markets question valuation and growth expectations more closely. Valuations, although not stretched, in our opinion, particularly relative to developed equity markets, are much higher than they were and high relative to historic trading levels. Even though this coming year is not an electoral year, we believe that markets will continue to be sensitive to ongoing politics— particularly as they relate to ongoing economic reforms. This is specifically the case for Mexico and Brazil, where much still remains to be done to secure economic growth for future years.

Other than these political risks, the main risks seem to us to be external, in particular the risk of external shocks from slowing global demand and/or lower commodities prices. At the other end of the risk spectrum, Latin America's success at restructuring corporate and government balance sheets—and the region's diminished dependency on foreign capital—means, in our opinion, that Latin America is much less sensitive to rising U.S. interest rates than it has been in the past. However, rising rates clearly would have an impact on risk appetite for higher yielding asset classes.

Additionally, we do not expect to see significant further market re-rating and believe, consequently, that share prices will have to be driven by corporate earnings going forward. We also believe that there is less potential for local currency re-rating against the U.S. dollar. This means that investors should not, in our opinion, expect to see the same rate of returns that we have experienced over the last four years.

Nevertheless, we believe that overall macro economic fundamentals remain healthy, the global macro backdrop remains supportive, and we are optimistic that 2007 should be another positive year for Latin American equities.

Respectfully,

| |  | |

|

Matthew J.K. Hickman

Chief Investment Officer** | | Keith M. Schappert

Chief Executive Officer and President*** | |

|

4

LETTER TO SHAREHOLDERS (CONTINUED)

International investing entails special risk considerations, including currency fluctuations, lower liquidity, economic and political risks, and differences in accounting methods; these risks are generally heightened for emerging-market investments.

In addition to historical information, this report contains forward-looking statements, which may concern, among other things, domestic and foreign market, industry and economic trends and developments and government regulation and their potential impact on the Fund's investments. These statements are subject to risks and uncertainties and actual trends, developments and regulations in the future and their impact on the Fund could be materially different from those projected, anticipated or implied. The Fund has no obligation to update or revise forward-looking statements.

We wish to remind shareholders about the Fund's dividend reinvestment program known as the InvestlinkSM Program (the "Program"). The Program is sponsored and administered by Computershare Trust Company N.A. ("Computershare"), not by the Fund. Computershare will act as program administrator (the "Program Administrator") of the Program. The purpose of the Program is to provide existing shareholders with a simple and convenient way to invest additional funds and reinvest dividends in shares of the Fund's common stock. The enrollment form and information relating to the Program (including the terms and conditions) may be obtained by calling the Program Administrator at one of the following telephone numbers: (800) 730-6001 (U.S and Canada) or (781) 575-3100 (outside U.S. and Canada). All correspondence regarding the Program should be directed to: Computershare Trust Company, N.A., InvestLinkSM Program, P.O. Box 43010, Provi dence, RI 02940-3010.

* The Morgan Stanley Capital International Latin America Index is a free float-adjusted market capitalization index that is designed to measure equity-market performance in Latin America that includes reinvestment of dividends (net of taxes). It is the exclusive property of Morgan Stanley Capital International Inc. Investors cannot invest directly in an index.

** Matthew J.K. Hickman, Director, is a portfolio manager specializing in Latin American equities and is primarily responsible for management of the Fund's assets. He joined in 2003 from Compass Group Investment Advisors, where he was general manager of the private wealth management division based in Santiago, Chile. Previously, he was a financial advisor in Credit Suisse First Boston's Private Client Services channel; an equity analyst focusing on Latin American telecommunications companies and several Latin American country markets at ABN AMRO, Lehman Brothers, Bear, Stearns and James Capel; and an equity analyst and member of the management team for the Five Arrows Chile Fund at Rothschild Asset Management. Mr. Hickman holds a BA in modern languages from Cambridge University and a diploma in corporate finance from London Business School. He is fluent in Spanish, Portuguese and French. He is also the Chief Investment Officer of The Chile F und, Inc.

*** Keith M. Schappert is Executive Vice Chairman and Head of Asset Management for Americas of Credit Suisse and CEO/President of the Fund. Mr. Schappert joined Credit Suisse in 2006 from Federated Investment Advisory Companies, where he was CEO and President from 2002. Prior to Federated, Mr. Schappert was CEO and President of JP Morgan Investment Management from 1994 to 2001.

5

NOTICE TO SHAREHOLDERS

At the time The Latin America Equity Fund, Inc. (the "Fund") commenced operations in 1991, the Prospectus did not contemplate the use of options strategies as such strategies were not commonly used by investment companies. Since then the use of options by funds has proliferated. Credit Suisse now believes that the use of the options strategies discussed below may permit it to better manage the risk and returns of the Fund and effective March 1, 2007, the Fund may, in the discretion of the portfolio managers, use option strategies for hedging purposes or to increase return. Options strategies also entail risks which are detailed below.

SECURITIES OPTIONS. The Fund may write covered put and call options on stock and debt securities and may purchase such options that are traded on foreign and U.S. exchanges, as well as over-the-counter ("OTC") options. The Fund realizes fees (referred to as "premiums") for granting the rights evidenced by the options it has written. A put option embodies the right of its purchaser to compel the writer of the option to purchase from the option holder an underlying security at a specified price for a specified time period or at a specified time. In contrast, a call option embodies the right of its purchaser to compel the writer of the option to sell to the option holder an underlying security at a specified price for a specified time period or at a specified time.

The potential loss associated with purchasing an option is limited to the premium paid, and the premium would partially offset any gains achieved from its use. However, for an option writer the exposure to adverse price movements in the underlying security or index is potentially unlimited during the exercise period. Writing securities options may result in substantial losses to the Fund, force the sale or purchase of portfolio securities at inopportune times or at less advantageous prices, limit the amount of appreciation the Fund could realize on its investments or require the Fund to hold securities it would otherwise sell.

The principal reason for writing covered options on a security is to attempt to realize, through the receipt of premiums, a greater return than would be realized on the securities alone. In return for a premium, the Fund as the writer of a covered call option forfeits the right to any appreciation in the value of the underlying security above the strike price for the life of the option (or until a closing purchase transaction can be effected). When the Fund writes call options, it retains the risk of a decline in the price of the underlying security. The size of the premiums that the Fund may receive may be adversely affected as new or existing institutions, including other investment companies, engage in or increase their option-writing activities.

If security prices rise, a put writer would generally expect to profit, although its gain would be limited to the amount of the premium it received. If security prices remain the same over time, it is likely that the writer will also profit, because it should be able to close out the option at a lower price. If security prices decline, the put writer would expect to suffer a loss. This loss may be less than the loss from purchasing the underlying instrument directly to the extent that the premium received offsets the effects of the decline.

The Fund may purchase and write options in combination with each other to adjust the risk and return characteristics of the Fund's overall position. For example, the Fund may purchase a put option and write a covered call option on the same underlying instrument. This technique, called a "collar," enables the Fund to be protected to some extent against a market decline while maintaining the potential for limited upside appreciation. In this strategy the cost of purchasing a put option is offset with the premium received from writing the call option. However, by selling the call option, the Fund gives up the ability for potentially unlimited profit.

6

NOTICE TO SHAREHOLDERS (CONTINUED)

In the case of options written by the Fund that are deemed covered by virtue of the Fund's holding convertible or exchangeable preferred stock or debt securities, the time required to convert or exchange and obtain physical delivery of the underlying common stock with respect to which the Fund has written options may exceed the time within which the Fund must make delivery in accordance with an exercise notice. In these instances, the Fund may purchase or temporarily borrow the underlying securities for purposes of physical delivery. By so doing, the Fund will not bear any market risk, since the Fund will have the absolute right to receive from the issuer of the underlying security an equal number of shares to replace the borrowed securities, but the Fund may incur additional transaction costs or interest expenses in connection with any such purchase or borrowing.

Options written by the Fund will normally have expiration dates between one and nine months from the date written. The exercise price of the options may be below, equal to or above the market values of the underlying securities at the times the options are written. To secure its obligation to deliver the underlying security when it writes a call option, the Fund will be required to deposit in escrow the underlying security or other assets in accordance with the rules of the Options Clearing Corporation and of the securities exchange on which the option is written.

There is no assurance that sufficient trading interest will exist to create a liquid secondary market on a securities exchange for any particular option or at any particular time, and for some options no such secondary market may exist. As a result, it might not be possible to effect closing transactions in particular options. Moreover, the Fund's ability to terminate options positions established in the OTC market may be more limited than for exchange-traded options and may also involve the risk that securities dealers participating in OTC transactions would fail to meet their obligations to the Fund. The Fund, however, will purchase OTC options only from dealers whose debt securities, as determined by Credit Suisse, are considered to be investment grade. If, as a covered call option writer, the Fund is unable to effect a closing purchase transaction in a secondary market, it will not be able to sell the underlying security and would contin ue to be at market risk on the security.

SECURITIES INDEX OPTIONS. The Fund may purchase or write exchange-listed and OTC put and call options on securities indexes. A securities index measures the movement of a certain group of securities by assigning relative values to the securities included in the index, fluctuating with changes in the market values of the securities included in the index. Securities index options can be based on a broad market index or a narrower market index, a particular industry or market segment. Options on securities indexes are similar to options on securities, and have the same risks as described above.

Index put options are contracts that give the holder of the option, in exchange for a premium, the right to receive a cash payment from the seller of the index option in the event the value of the index is below the exercise price of the index put option upon its expiration. The Fund would ordinarily realize a gain on a put option it has purchased if (i) at the end of the index option period, the value of an index decreased below the exercise price of the index put option sufficiently to more than cover the premium and transaction costs or (ii) the Fund sells the index put option prior to its expiration at a price that is higher than its cost. The Fund may purchase index put options to protect the Fund from a decline in value of a portfolio holding or a group of portfolio holdings over a short period of time. If a put option purchased by the Fund is not sold or realized when it has remaining value, the Fund will lose its entire investment in the index put option. Also, where an index put option is purchased to hedge all or part of the Fund's portfolio, the price of the index put option may move more or less than the value of the index.

7

NOTICE TO SHAREHOLDERS (CONTINUED)

Index call options are contracts that give the holder of the option, in exchange for a premium, the right to receive a cash payment from the seller of the index option in the event the value of the index is above the exercise price of the index call option upon its expiration. The Fund would ordinarily realize a gain on a call option it has purchased if (i) at the end of the index option period, the value of an index has increased above the exercise price of the index call option sufficiently to more than cover the premium and transaction costs or (ii) the Fund sells the index call option prior to its expiration at a price that is higher than its cost. The Fund may purchase call options on an index primarily as a temporary substitute for taking positions in certain securities that comprise a relevant index. The Fund may also purchase call options on an index to protect against increases in the price of securities underlying that index that t he Fund intends to purchase pending its ability to invest in such securities in an orderly manner.

In seeking to hedge all or a portion of its investments or as a means of participating in a securities market without making direct purchases of securities, the Fund may also write put and call options on securities indices listed on U.S. or foreign securities exchanges or traded in the over-the-counter market, which indices include securities held in the Fund's portfolio.

Because the value of an index option depends upon movements in the level of the index rather than the price of a particular stock, whether the Fund will realize a gain or loss from the purchase or writing of options on an index depends upon movements in the level of stock prices in the stock market generally or, in the case of certain indices, in an industry or market segment, rather than movements in the price of a particular stock. Accordingly, successful use by the Fund of options on stock indices will be subject to Credit Suisse's ability to predict correctly movements in the direction of the stock market generally or of a particular industry. This requires different skills and techniques than predicting changes in the price of individual stocks.

Options on securities indices entail risks in addition to the risks of options on securities. The absence of a liquid secondary market to close out options positions on securities indices is more likely to occur, although the Fund generally will only purchase or write such an option if Credit Suisse believes the option can be closed out. Use of options on securities indices also entails the risk that trading in such options may be interrupted if trading in certain securities included in the index is interrupted. The Fund will not purchase such options unless Credit Suisse believes the market is sufficiently developed such that the risk of trading in such options is no greater than the risk of trading in options on securities.

In addition, because options on securities indices require settlement in cash, Credit Suisse may be forced to liquidate portfolio securities to meet settlement obligations.

8

THE LATIN AMERICA EQUITY FUND, INC.

Portfolio Summary

December 31, 2006 (unaudited)

GEOGRAPHIC ASSET BREAKDOWN

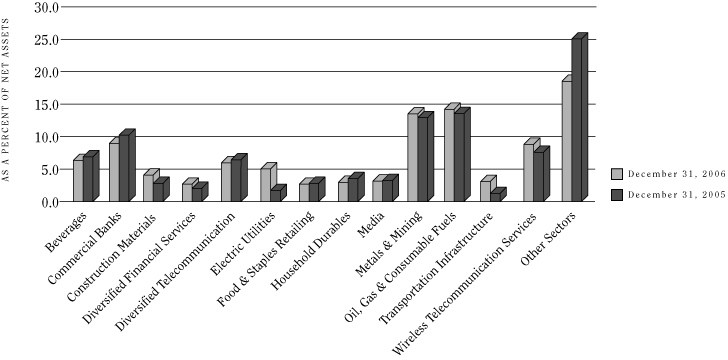

SECTOR ALLOCATION

9

THE LATIN AMERICA EQUITY FUND, INC.

Portfolio Summary

December 31, 2006 (unaudited) (continued)

TOP 10 HOLDINGS, BY ISSUER (UNAUDITED)

| | | Holding | | Sector | | Country | | Percent of

Net Assets | |

| | 1. | | | Petróleo Brasileiro S.A. | | Oil, Gas & Consumable Fuels | | Brazil | | | 14.2 | | |

| | 2. | | | Companhia Vale do Rio Doce | | Metals & Mining | | Brazil | | | 9.4 | | |

| | 3. | | | América Telecom, S.A. de C.V. | | Wireless Telecommunication Services | | Mexico | | | 5.3 | | |

| | 4. | | | Cemex S.A. de C.V. | | Construction Materials | | Mexico | | | 4.1 | | |

| | 5. | | | Tele Norte Leste Participações S.A. | | Diversified Telecommunication | | Brazil | | | 3.7 | | |

| | 6. | | | América Móvil S.A. de C.V. | | Wireless Telecommunication Services | | Mexico | | | 3.2 | | |

| | 7. | | | Fomento Economico Mexicano, S.A. de C.V. | | Beverages | | Mexico | | | 2.2 | | |

| | 8. | | | Companhia de Bebidas das Americas | | Beverages | | Brazil | | | 2.2 | | |

| | 9. | | | Banco Bradesco S.A. | | Commercial Banks | | Brazil | | | 2.1 | | |

| | 10. | | | Grupo Televisa S.A. | | Media | | Mexico | | | 2.0 | | |

10

THE LATIN AMERICA EQUITY FUND, INC.

Schedule of Investments

December 31, 2006

| Description | | No. of

Shares | | Value | |

| EQUITY OR EQUITY-LINKED SECURITIES-100.75% | |

| Argentina-2.12% | |

| Energy Equipment & Services-1.65% | |

| Tenaris S.A., ADR | | | 96,400 | | | $ | 4,809,396 | | |

| Thrifts & Morgage Finance-0.47% | |

| Banco Hipotecario S.A., ADR† | | | 192,700 | | | | 1,382,603 | | |

Total Argentina

(Cost $3,463,460) | | | | | | | 6,191,999 | | |

| Brazil-61.00% | |

| Airlines-0.85% | |

| Tam S.A., PN | | | 79,700 | | | | 2,482,459 | | |

| Beverages-2.23% | |

Companhia de Bebidas das

Americas, ADR | | | 22,600 | | | | 992,140 | | |

Companhia de Bebidas das

Americas, ADR, PN | | | 113,200 | | | | 5,524,160 | | |

| | | | 6,516,300 | | |

| Commercial Banks-7.33% | |

| Banco Bradesco S.A., PN | | | 151,600 | | | | 6,142,108 | | |

Banco Itaú Holding

Financeira S.A., PN | | | 139,900 | | | | 5,071,785 | | |

| Investimentos Itaú S.A., PN | | | 890,700 | | | | 4,555,711 | | |

União de Bancos Brasileiros

S.A., GDR | | | 60,800 | | | | 5,651,968 | | |

| | | | 21,421,572 | | |

| Computers and Peripherals-0.27% | |

| Positivo Informatica SA | | | 72,500 | | | | 781,030 | | |

| Containers & Packaging-0.42% | |

| Klabin S.A., PN | | | 493,000 | | | | 1,235,386 | | |

| Diversified Financial Services-1.12% | |

| Bradespar S.A., PN | | | 69,500 | | | | 3,287,822 | | |

| Diversified Telecommunication-5.67% | |

Brasil Telecom Participações

S.A. | | | 159,605,140 | | | | 2,616,478 | | |

| Description | | No. of

Shares | | Value | |

| Diversified Telecommunication (continued) | |

Telecomunicações de São Paulo

S.A., PN | | | 78,800 | | | $ | 2,029,977 | | |

| Telemar Norte Leste S.A., PNA | | | 51,200 | | | | 1,165,489 | | |

Tele Norte Leste Participações

S.A., ON | | | 412,036 | | | | 10,749,604 | | |

| | | | 16,561,548 | | |

| Electric Utilities-4.13% | |

Centrais Elétricas

Brasileiras S.A., PNB | | | 123,400,000 | | | | 2,768,553 | | |

Companhia Energética de

Minas Gerais, ADR | | | 57,100 | | | | 2,752,220 | | |

Companhia Energética de

Minas Gerais, PN | | | 14,500,000 | | | | 713,047 | | |

| EDP - Energias do Brasil S.A. | | | 112,700 | | | | 1,741,967 | | |

Eletropaulo Metropolitana

S.A., PNB† | | | 16,510,000 | | | | 842,899 | | |

| Terna Participações S.A.† | | | 289,200 | | | | 3,264,506 | | |

| | | | 12,083,192 | | |

| Food Products-1.87% | |

Cosan S.A. Industria e

Comercio† | | | 151,700 | | | | 3,176,108 | | |

| Perdigao S.A. | | | 163,700 | | | | 2,298,701 | | |

| | | | 5,474,809 | | |

| Food & Staples Retailing-0.54% | |

Companhia Brasileira de

Distribuição Grupo Pão

de Acucar, ADR | | | 45,800 | | | | 1,564,986 | | |

| Healthcare Providers & Services-0.93% | |

Diagnosticos da America

S.A.† | | | 127,000 | | | | 2,715,480 | | |

Independent Power Producers &

Energy Traders-0.62% | |

| Tractebel Energia S.A. | | | 215,800 | | | | 1,819,391 | | |

| Insurance-0.36% | |

| Clean Energy Brazil PLC† | | | 507,000 | | | | 1,031,966 | | |

Clean Energy Brazil PLC,

warrants† | | | 126,750 | | | | 33,489 | | |

| | | | 1,065,455 | | |

See accompanying notes to financial statements.

11

THE LATIN AMERICA EQUITY FUND, INC.

Schedule of Investments

December 31, 2006 (continued)

| Description | | No. of

Shares | | Value | |

| Internet & Catalog Retail-1.34% | |

| Submarino S.A.† | | | 119,300 | | | $ | 3,910,917 | | |

| Machinery-0.53% | |

| Iochpe Maxion S.A., PN | | | 77,400 | | | | 657,991 | | |

| Weg S.A., PN | | | 124,200 | | | | 886,561 | | |

| | | | 1,544,552 | | |

| Media-1.12% | |

Net Servicos de Comunicacao

SA, PN† | | | 159,406 | | | | 1,812,077 | | |

| Vivax S.A.† | | | 80,100 | | | | 1,463,185 | | |

| | | | 3,275,262 | | |

| Metals & Mining-10.44% | |

Companhia Vale do Rio Doce,

ADR, PNA | | | 1,047,000 | | | | 27,483,750 | | |

| Gerdau S.A., PN | | | 72,000 | | | | 1,177,293 | | |

Usinas Siderúrgicas de Minas

Gerais S.A., PNA | | | 49,000 | | | | 1,847,541 | | |

| | | | 30,508,584 | | |

| Multiline Retail-0.64% | |

| Lojas Americanas S.A., PN | | | 33,600,000 | | | | 1,880,656 | | |

| Oil, Gas & Consumable Fuels-14.24% | |

| Petróleo Brasileiro S.A., ADR | | | 448,700 | | | | 41,621,412 | | |

| Paper & Forest Products-0.61% | |

| Aracruz Celulose S.A., ADR | | | 29,000 | | | | 1,775,960 | | |

| Personal Products-0.38% | |

| Natura Cosmeticos S.A. | | | 78,900 | | | | 1,114,208 | | |

| Real Estate Management & Development-1.12% | |

Cyrela Brazil Realty S.A.

Empreendimentos e

Particpações | | | 193,000 | | | | 1,843,218 | | |

| Klabin Segall S.A.† | | | 169,577 | | | | 1,421,746 | | |

| | | | 3,264,964 | | |

| Road & Rail-2.00% | |

| All America Latina Logistica | | | 407,600 | | | | 4,232,549 | | |

| Localiza Rent a Car SA | | | 54,000 | | | | 1,625,059 | | |

| | | | 5,857,608 | | |

| Description | | No. of

Shares | | Value | |

| Textiles, Apparel & Luxury Goods-0.71% | |

Companhia de Tecidos Norte de

Minas S.A., PN | | | 17,600,000 | | | $ | 2,060,890 | | |

| Transportation Infrastructure-1.16% | |

Obrascon Huarte Lain

Brasil S.A.† | | | 211,100 | | | | 3,401,330 | | |

| Wireless Telecommunication Services-0.37% | |

| Vivo Participações S.A., ADR | | | 261,021 | | | | 1,070,186 | | |

Total Brazil

(Cost $93,140,189) | | | | | | | 178,295,959 | | |

| Chile-7.02% | |

| Beverages-1.28% | |

Compañia Cervecerías

Unidas S.A. | | | 197,880 | | | | 1,176,684 | | |

Compañia Cervecerías

Unidas S.A., ADR | | | 46,700 | | | | 1,386,990 | | |

Embotelladora Andina

S.A., PNA | | | 294,613 | | | | 774,380 | | |

Embotelladora Andina

S.A., PNB | | | 140,000 | | | | 399,812 | | |

| | | | 3,737,866 | | |

| Commercial Banks-0.99% | |

| Banco de Chile | | | 16,906,065 | | | | 1,461,116 | | |

| Banco Santander Chile S.A. | | | 30,613,969 | | | | 1,426,447 | | |

| | | | 2,887,563 | | |

| Diversified Telecommunication-0.25% | |

Compañia de Telecomunicaciones

de Chile S.A., Series A | | | 367,916 | | | | 725,809 | | |

| Electric Utilities-0.89% | |

| Enersis S.A. | | | 3,780,000 | | | | 1,204,842 | | |

| Enersis S.A., ADR | | | 88,300 | | | | 1,412,800 | | |

| | | | 2,617,642 | | |

| Food & Staples Retailing-0.30% | |

| Cencosud S.A. | | | 280,000 | | | | 875,904 | | |

See accompanying notes to financial statements.

12

THE LATIN AMERICA EQUITY FUND, INC.

Schedule of Investments

December 31, 2006 (continued)

| Description | | No. of

Shares | | Value | |

Independent Power Producers &

Energy Traders-0.62% | |

Empresa Nacional de Electricidad

S.A. | | | 1,474,568 | | | $ | 1,807,714 | | |

| Industrial Conglomerates-0.54% | |

| Empresas Copec S.A. | | | 123,000 | | | | 1,575,833 | | |

| Multiline Retail-0.24% | |

| S.A.C.I. Falabella, S.A. | | | 199,850 | | | | 702,150 | | |

| Paper & Forest Products-0.57% | |

| Empresas CMPC S.A. | | | 50,000 | | | | 1,681,447 | | |

| Water Utilities-1.34% | |

Inversiones Aguas Metropolitanas

S.A., ADR†† | | | 159,300 | | | | 3,912,504 | | |

Total Chile

(Cost $12,600,187) | | | | | | | 20,524,432 | | |

| Colombia-2.17% | |

| Commercial Banks-0.00% | |

| BanColombia S.A., ADR | | | 3 | | | | 93 | | |

| Diversified Financial Services-1.54% | |

Corporacion Financiera

Colombiana | | | 157,732 | | | | 1,594,398 | | |

Suramericana de

Inversiones S.A. | | | 318,346 | | | | 2,910,917 | | |

| | | | 4,505,315 | | |

| Metals & Mining-0.63% | |

| Acerias Paz del Rio S.A.† | | | 76,244,300 | | | | 1,838,237 | | |

Total Colombia

(Cost $3,869,258) | | | | | | | 6,343,645 | | |

| Latin America-0.34% | |

| Venture Capital-0.34% | |

J.P. Morgan Latin America

Capital Partners (Cayman),

L.P.†‡ | | | 948,642 | | | | 247,064 | | |

| Description | | No. of

Shares | | Value | |

| Venture Capital (continued) | |

J.P. Morgan Latin America Capital

Partners (Delaware), L.P.†‡# | | | 1,489,801 | | | $ | 733,101 | | |

Total Latin America

(Cost $1,181,771) | | | | | | | 980,165 | | |

| Mexico-26.89% | |

| Beverages-2.82% | |

Fomento Económico Mexicano,

S.A. de C.V., ADR | | | 56,312 | | | | 6,518,677 | | |

Grupo Modelo, S.A. de C.V.,

Series C | | | 311,900 | | | | 1,722,711 | | |

| | | | 8,241,388 | | |

| Construction Materials-4.07% | |

| Cemex S. A. de C.V., ADR | | | 351,256 | | | | 11,900,553 | | |

| Diversified Telecommunication-0.04% | |

| Axtel, S.A. de C.V., CPO† | | | 36,200 | | | | 110,336 | | |

| Food & Staples Retailing-1.81% | |

Wal-Mart de México, S.A. de C.V.,

Series V | | | 727,840 | | | | 3,195,211 | | |

Wal-Mart de México, S.A. de C.V.,

Series V, ADR | | | 47,945 | | | | 2,104,781 | | |

| | | | 5,299,992 | | |

| Hotels, Restaurants & Leisure-0.54% | |

| Alsea, S.A. de C.V. | | | 287,200 | | | | 1,562,147 | | |

| Household Durables-2.96% | |

| Consorcio ARA, S.A. de C.V. | | | 293,000 | | | | 1,989,074 | | |

Corporación GEO, S.A. de C.V.,

Series B† | | | 660,900 | | | | 3,302,394 | | |

Urbi, Desarrollos Urbanos,

S.A. de C.V.† | | | 929,400 | | | | 3,347,828 | | |

| | | | 8,639,296 | | |

| Media-2.03% | |

| Grupo Televisa S.A., ADR | | | 180,300 | | | | 4,869,903 | | |

| Grupo Televisa S.A., CPO | | | 198,400 | | | | 1,072,546 | | |

| | | | 5,942,449 | | |

See accompanying notes to financial statements.

13

THE LATIN AMERICA EQUITY FUND, INC.

Schedule of Investments

December 31, 2006 (continued)

| Description | | No. of

Shares | | Value | |

| Metals & Mining-2.23% | |

| Baja Mining Corp.† | | | 1,282,000 | | | $ | 1,454,189 | | |

Grupo Mexico SA de C.V.,

Class B | | | 1,386,060 | | | | 5,069,593 | | |

| | | | 6,523,782 | | |

| Transportation Infrastructure-1.91% | |

Grupo Aeroportuario del Centro

Norte, S.A.B. DE C.V.† | | | 111,045 | | | | 2,471,862 | | |

Grupo Aeroportuario del Pacifico

S.A. de C.V., ADR | | | 79,500 | | | | 3,115,605 | | |

| | | | 5,587,467 | | |

| Wireless Telecommunication Services-8.48% | |

América Móvil S.A. de C.V.,

Series L, ADR | | | 206,600 | | | | 9,342,452 | | |

America Telecom, S.A. de C.V.,

Series A1 Shares† | | | 1,706,599 | | | | 15,433,144 | | |

| | | | 24,775,596 | | |

Total Mexico

(Cost $41,725,496) | | | | | | | 78,583,006 | | |

| Peru-0.23% | |

| Metals & Mining-0.23% | |

Compania de Minas Buenaventura

S.A.u., ADR

(Cost $624,764) | | | 24,200 | | | | 679,052 | | |

| Venezuela-0.64% | |

| Commercial Banks-0.64% | |

Mercantil Servicios Financieros,

C.A., ADR

(Cost $1,237,752) | | | 259,700 | | | | 1,879,683 | | |

| Global-0.34% | |

| Venture Capital-0.34% | |

Emerging Markets Ventures I

L.P.†‡#

(Cost $1,289,614) | | | 2,237,292 | | | | 1,012,733 | | |

TOTAL EQUITY OR EQUITY-LINKED

SECURITIES (Cost $159,132,491) | | | | | | | 294,490,674 | | |

| Description | | No. of

Shares | | Value | |

| SHORT-TERM INVESTMENTS-0.85% | |

| Chilean Mutual Fund-0.03% | |

Fondo Mutuo Security Check

(Cost $92,751) | | | 16,763 | | | $ | 96,070 | | |

| | | Principal

Amount

(000's) | | | |

| Grand Cayman-0.82% | |

Bank of America London,

overnight deposit,

5.73%, 1/2/2007*

(Cost $2,379,000) | | $ | 2,379 | | | | 2,379,000 | | |

TOTAL SHORT-TERM INVESTMENTS

(Cost $2,471,751) | | | | | 2,475,070 | | |

Total Investments-101.60%

(Cost $161,604,242) (Notes B,E,G) | | | | | 296,965,744 | | |

Liabilities in Excess of Cash and

Other Assets-(1.60)% | | | | | (4,679,982 | ) | |

| NET ASSETS-100.00% | | | | $ | 292,285,762 | | |

† Non-income producing security.

†† SEC Rule 144A security. Such securities are traded only among "qualified institutional buyers."

‡ Restricted security, not readily marketable; security is valued at fair value as determined in good faith by, or under the direction of, the Board of Directors, under procedures established by the Board of Directors. (See Notes B and H).

# As of December 31, 2006, the aggregate amount of open commitments for the Fund is $954,171. (See Note H).

* Variable rate account. Rate resets on a daily basis: amounts are available on the same business day.

ADR American Depositary Receipts.

CPO Ordinary Participation Certificates.

GDR Global Depositary Receipts.

ON Ordinary Shares.

PN Preferred Shares.

PNA Preferred Shares, Series A.

PNB Preferred Shares, Series B.

See accompanying notes to financial statements.

14

THE LATIN AMERICA EQUITY FUND, INC.

Statement of Assets and Liabilities

December 31, 2006

| ASSETS | |

| Investments, at value (Cost $161,604,242) (Notes B,E,G) | | $ | 296,965,744 | | |

| Cash (including $50,018 of foreign currencies with a cost of $60,376) | | | 50,434 | | |

| Receivables: | |

| Investments sold | | | 25,044,552 | | |

| Dividends | | | 1,471,666 | | |

| Prepaid expenses | | | 5,020 | | |

| Total Assets | | | 323,537,416 | | |

| LIABILITIES | |

| Payables: | |

| Dividends and distributions (Note B) | | | 28,323,635 | | |

| Investments purchased | | | 2,044,452 | | |

| Investment advisory fees (Note C) | | | 591,258 | | |

| Administration fees (Note C) | | | 49,464 | | |

| Directors' fees | | | 6,932 | | |

| Chilean repatriation taxes | | | 51,273 | | |

| Other accrued expenses | | | 184,640 | | |

| Total Liabilities | | | 31,251,654 | | |

| NET ASSETS (applicable to 6,322,240 shares of common stock outstanding) (Note D) | | $ | 292,285,762 | | |

| NET ASSETS CONSIST OF | |

Capital stock, $0.001 par value; 6,322,240 shares issued and outstanding

(100,000,000 shares authorized) | | $ | 6,322 | | |

| Paid-in capital | | | 140,606,867 | | |

| Undistributed net investment income | | | 395,786 | | |

| Accumulated net realized gain on investments and foreign currency related transactions | | | 15,894,094 | | |

Net unrealized appreciation in value of investments and translation of other

assets and liabilities denominated in foreign currencies | | | 135,382,693 | | |

| Net assets applicable to shares outstanding | | $ | 292,285,762 | | |

| NET ASSET VALUE PER SHARE ($292,285,762 ÷ 6,322,240) | | $ | 46.23 | | |

| MARKET PRICE PER SHARE | | $ | 43.43 | | |

See accompanying notes to financial statements.

15

THE LATIN AMERICA EQUITY FUND, INC.

Statement of Operations

For the Year Ended December 31, 2006

| INVESTMENT INCOME | |

| Income (Note B): | |

| Dividends | | $ | 7,794,563 | | |

| Interest | | | 127,533 | | |

| Less: Net investment loss allocated from partnerships | | | (100,779 | ) | |

| Less: Foreign taxes withheld | | | (681,894 | ) | |

| Total Investment Income | | | 7,139,423 | | |

| Expenses: | |

| Investment advisory fees (Note C) | | | 2,159,520 | | |

| Custodian fees | | | 326,960 | | |

| Administration fees (Note C) | | | 254,963 | | |

| Audit and tax fees | | | 85,001 | | |

| Directors' fees | | | 82,912 | | |

| Accounting fees | | | 77,794 | | |

| Printing (Note C) | | | 59,381 | | |

| Legal fees | | | 54,998 | | |

| Insurance | | | 20,579 | | |

| Shareholder servicing fees | | | 20,499 | | |

| Stock exchange listing fees | | | 1,304 | | |

| Miscellaneous | | | 11,999 | | |

| Brazilian taxes (Note B) | | | 24,965 | | |

| Chilean repatriation taxes (Note B) | | | (14,859 | ) | |

| Total Expenses | | | 3,166,016 | | |

| Less: Fee waivers (Note C) | | | (4,000 | ) | |

| Net Expenses | | | 3,162,016 | | |

| Net Investment Income | | | 3,977,407 | | |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS AND

FOREIGN CURRENCY RELATED TRANSACTIONS | |

| Net realized gain/(loss) from: | |

| Investments | | | 41,395,408 | | |

| Foreign currency related transactions | | | (113,310 | ) | |

Net change in unrealized appreciation in value of investments and translation

of other assets and liabilities denominated in foreign currencies | | | 58,504,337 | | |

| Net realized and unrealized gain on investments and foreign currency related transactions | | | 99,786,435 | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 103,763,842 | | |

See accompanying notes to financial statements.

16

THE LATIN AMERICA EQUITY FUND, INC.

Statement of Changes in Net Assets

| | | For the Years Ended

December 31, | |

| | | 2006 | | 2005 | |

| INCREASE IN NET ASSETS | |

| Operations: | |

| Net investment income | | $ | 3,977,407 | | | $ | 3,861,207 | | |

| Net realized gain on investments and foreign currency related transactions | | | 41,282,098 | | | | 45,732,308 | | |

Net change in unrealized appreciation in value of investments and

translation of other assets and liabilities denominated in

foreign currencies | | | 58,504,337 | | | | 23,975,296 | | |

| Net increase in net assets resulting from operations | | | 103,763,842 | | | | 73,568,811 | | |

| Dividends and distributions to shareholders: | |

| Net investment income | | | (3,540,454 | ) | | | (3,161,120 | ) | |

| Net realized gain on investments | | | (30,789,309 | ) | | | (1,770,227 | ) | |

| Total dividends and distributions to shareholders | | | (34,329,763 | ) | | | (4,931,347 | ) | |

| Total increase in net assets | | | 69,434,079 | | | | 68,637,464 | | |

| NET ASSETS | |

| Beginning of year | | | 222,851,683 | | | | 154,214,219 | | |

| End of year* | | $ | 292,285,762 | | | $ | 222,851,683 | | |

* Includes undistibuted net investment income of $395,786 and $179,490, respectively.

See accompanying notes to financial statements.

17

THE LATIN AMERICA EQUITY FUND, INC.

Financial Highlights§

Contained below is per share operating performance data for a share of common stock outstanding, total investment return, ratios to average net assets and other supplemental data for each year indicated. This information has been derived from information provided in the financial statements and market price data for the Fund's shares.

| | | For the Years Ended December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | | 2000 | | 1999 | |

| PER SHARE OPERATING PERFORMANCE | |

| Net asset value, beginning of year | | $ | 35.25 | | | $ | 24.39 | | | $ | 17.74 | | | $ | 11.55 | | | $ | 15.06 | | | $ | 16.60 | | | $ | 18.57 | | | $ | 10.96 | | |

| Net investment income/(loss) | | | 0.63 | | | | 0.61 | | | | 0.45 | † | | | 0.34 | † | | | 0.01 | ** | | | 0.41 | * | | | (0.11 | )† | | | 0.07 | † | |

Net realized and unrealized gain/(loss) on investments

and foreign currency related transactions | | | 15.78 | | | | 11.03 | | | | 6.66 | | | | 5.99 | | | | (3.41 | ) | | | (1.50 | ) | | | (2.44 | ) | | | 7.07 | | |

| Net increase/(decrease) in net assets resulting from operations | | | 16.41 | | | | 11.64 | | | | 7.11 | | | | 6.33 | | | | (3.40 | ) | | | (1.09 | ) | | | (2.55 | ) | | | 7.14 | | |

| Dividends and distributions to shareholders: | |

| Net investment income | | | (0.56 | ) | | | (0.50 | ) | | | (0.46 | ) | | | (0.14 | ) | | | (0.21 | ) | | | (0.57 | ) | | | (0.08 | ) | | | — | | |

Net realized gain on investments and

foreign currency related transactions | | | (4.87 | ) | | | (0.28 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | |

| Total dividends and distributions to shareholders | | | (5.43 | ) | | | (0.78 | ) | | | (0.46 | ) | | | (0.14 | ) | | | (0.21 | ) | | | (0.57 | ) | | | (0.08 | ) | | | — | | |

| Anti-dilutive impact due to capital shares tendered or repurchased | | | — | | | | — | | | | — | | | | — | | | | 0.10 | # | | | 0.12 | # | | | 0.66 | | | | 0.47 | | |

| Net asset value, end of year | | $ | 46.23 | | | $ | 35.25 | | | $ | 24.39 | | | $ | 17.74 | | | $ | 11.55 | | | $ | 15.06 | | | $ | 16.60 | | | $ | 18.57 | | |

| Market value, end of year | | $ | 43.43 | | | $ | 30.46 | | | $ | 21.64 | | | $ | 15.26 | | | $ | 9.67 | | | $ | 12.15 | | | $ | 12.875 | | | $ | 13.76 | | |

| Total investment return (a) | | | 61.62 | % | | | 44.06 | % | | | 45.04 | % | | | 59.15 | % | | | (18.83 | )% | | | (1.07 | )% | | | (5.87 | )% | | | 75.65 | % | |

| RATIOS/SUPPLEMENTAL DATA | |

| Net assets, end of year (000 omitted) | | $ | 292,286 | | | $ | 222,852 | | | $ | 154,214 | | | $ | 112,178 | | | $ | 73,045 | | | $ | 112,009 | | | $ | 145,281 | | | $ | 123,262 | | |

| Ratio of expenses to average net assets (b) | | | 1.44 | % | | | 1.33 | % | | | 1.41 | % | | | 1.37 | % | | | 3.06 | % | | | 1.51 | % | | | 2.13 | % | | | 2.14 | % | |

| Ratio of expenses to average net assets, excluding fee waivers | | | 1.45 | % | | | 1.33 | % | | | 1.41 | % | | | 1.37 | % | | | 3.06 | % | | | 1.51 | % | | | 2.19 | % | | | 2.22 | % | |

| Ratio of expenses to average net assets, excluding taxes | | | 1.19 | % | | | 1.26 | % | | | 1.40 | % | | | 1.49 | % | | | 1.52 | % | | | 1.40 | % | | | 2.03 | % | | | 2.05 | % | |

| Ratio of net investment income/(loss) to average net assets | | | 1.49 | % | | | 2.13 | % | | | 2.36 | % | | | 2.49 | %(c) | | | 0.21 | % | | | 2.52 | % | | | (0.55 | )% | | | 0.46 | % | |

| Portfolio turnover rate | | | 46.05 | % | | | 75.60 | % | | | 69.80 | % | | | 62.62 | % | | | 75.28 | % | | | 101.73 | % | | | 125.83 | % | | | 161.71 | % | |

§ Per share amounts prior to November 10, 2000 have been restated to reflect a conversion factor of 0.9175 for shares issued in connection with the merger of The Latin America Investment Fund, Inc. and The Latin America Equity Fund, Inc.

* Based on actual shares outstanding on November 21, 2001 (prior to the 2001 tender offer) and December 31, 2001.

** Based on actual shares outstanding on November 6, 2002 (prior to the 2002 tender offer) and December 31, 2002.

† Based on average shares outstanding.

‡ Includes a $0.01 per share decrease to the Fund's net asset value per share resulting from the dilutive impact of shares issued pursuant to the Fund's automatic dividend reinvestment program.

# Impact of the Fund's self-tender program.

(a) Total investment return at market value is based on the changes in market price of a share during the period and assumes reinvestment of dividends and distributions, if any, at actual prices pursuant to the Fund's dividend reinvestment program.

(b) Ratios reflect actual expenses incurred by the Fund. Amounts are net of fee waivers and inclusive of taxes.

(c) Ratio includes the effect of a reversal of Chilean repatriation tax accrual; excluding the reversal, the ratio would have been 2.36%.

See accompanying notes to financial statements.

18

THE LATIN AMERICA EQUITY FUND, INC.

Financial Highlights

| | |

| | | 1998 | | 1997 | |

| PER SHARE OPERATING PERFORMANCE | |

| Net asset value, beginning of year | | $ | 18.77 | | | $ | 18.41 | | |

| Net investment income/(loss) | | | 0.16 | | | | 0.16 | | |

Net realized and unrealized gain/(loss) on investments

and foreign currency related transactions | | | (7.85 | )‡ | | | 2.01 | | |

| Net increase/(decrease) in net assets resulting from operations | | | (7.69 | ) | | | 2.17 | | |

| Dividends and distributions to shareholders: | |

| Net investment income | | | (0.12 | ) | | | (0.17 | ) | |

Net realized gain on investments and

foreign currency related transactions | | | — | | | | (1.64 | ) | |

| Total dividends and distributions to shareholders | | | (0.12 | ) | | | (1.81 | ) | |

| Anti-dilutive impact due to capital shares tendered or repurchased | | | — | | | | — | | |

| Net asset value, end of year | | $ | 10.96 | | | $ | 18.77 | | |

| Market value, end of year | | $ | 7.834 | | | $ | 14.918 | | |

| Total investment return (a) | | | (46.63 | )% | | | 10.29 | % | |

| RATIOS/SUPPLEMENTAL DATA | |

| Net assets, end of year (000 omitted) | | $ | 86,676 | | | $ | 148,130 | | |

| Ratio of expenses to average net assets (b) | | | 2.41 | % | | | 1.89 | % | |

| Ratio of expenses to average net assets, excluding fee waivers | | | 2.60 | % | | | 2.02 | % | |

| Ratio of expenses to average net assets, excluding taxes | | | 1.77 | % | | | 1.65 | % | |

| Ratio of net investment income/(loss) to average net assets | | | 1.12 | % | | | 0.77 | % | |

| Portfolio turnover rate | | | 142.35 | % | | | 111.83 | % | |

19

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS

December 31, 2006

Note A. Organization

The Latin America Equity Fund, Inc. (the "Fund") is registered under the Investment Company Act of 1940, as amended, as a closed-end, non-diversified management investment company.

Note B. Significant Accounting Policies

Use of Estimates: The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America ("GAAP") requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Security Valuation: The net asset value of the Fund is determined daily as of the close of regular trading on the New York Stock Exchange, Inc. (the "Exchange") on each day the Exchange is open for business. Equity investments are valued at market value, which is generally determined using the closing price on the exchange or market on which the security is primarily traded at the time of valuation (the "Valuation Time"). If no sales are reported, equity investments are generally valued at the most recent bid quotation as of the Valuation Time or at the lowest ask quotation in the case of a short sale of securities. Debt securities with a remaining maturity greater than 60 days are valued in accordance with the price supplied by a pricing service, which may use a matrix, formula or other objective method that takes into consideration market indices, yield c urves and other specific adjustments. Debt obligations that will mature in 60 days or less are valued on the basis of amortized cost, which approximates market value, unless it is determined that this method would not represent fair value. Investments in mutual funds are valued at the mutual fund's closing net asset value per share on the day of valuation.

Securities and other assets for which market quotations are not readily available, or whose values have been materially affected by events occurring before the Fund's Valuation Time, but after the close of the securities' primary market, are valued at fair value as determined in good faith by, or under the direction of, the Board of Directors under procedures established by the Board of Directors. The Fund may utilize a service provided by an independent third party which has been approved by the Board of Directors to fair value certain securities. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities. At December 31, 2006, the Fund held 0.68% of its net assets in securities valued at fair value as determined in good faith under procedures established by the Board of Directors with an aggregate cost of $2,471,385 and fai r value of $1,992,898. The Fund's estimate of fair value assumes a willing buyer and a willing seller neither acting under the compulsion to buy or sell. Although these securities may be resold in privately negotiated transactions, the prices realized on such sales could differ from the prices originally paid by the Fund or the current carrying values, and the difference could be material.

Short-Term Investment: The Fund sweeps available cash into a short-term time deposit available through Brown Brothers Harriman & Co., the Fund's custodian. The short-term time deposit is a variable rate account classified as a short-term investment.

Investment Transactions and Investment Income: Investment transactions are accounted for on a trade date basis. The cost of investments sold is determined by use of the specific identification method for both financial reporting and U.S. income tax purposes. Interest income is accrued as earned; dividend income is recorded on the ex-dividend date.

20

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

December 31, 2006

Taxes: No provision is made for U.S. income or excise taxes as it is the Fund's intention to continue to qualify as a regulated investment company and to make the requisite distributions to its shareholders sufficient to relieve it from all or substantially all U.S. income and excise taxes.

Income received by the Fund from sources within Latin America may be subject to withholding and other taxes imposed by such countries. Also, certain Latin American countries impose taxes on funds remitted or repatriated from such countries.

Brazil imposes a Contribução Provisoria sobre Movimentaçãoes Financieras ("CPMF") tax that applies to foreign exchange transactions related to dividends carried out by financial institutions. The tax rate is 0.38%. For the year ended December 31, 2006, the Fund incurred $24,965 of such expense.

For Chilean securities the Fund accrues foreign taxes on realized gains and repatriation taxes in an amount equal to what the Fund would owe if the securities were sold and the proceeds repatriated on the valuation date as a liability and reduction of realized/unrealized gains. Taxes on foreign income are recorded when the related income is recorded. For the year ended December 31, 2006, the Fund accrued no such expense.

Foreign Currency Translations: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars on the following basis:

(I) market value of investment securities, assets and liabilities at the valuation date rate of exchange; and

(II) purchases and sales of investment securities, income and expenses at the relevant rates of exchange prevailing on the respective dates of such transactions.

The Fund does not isolate that portion of gains and losses on investments in equity securities which is due to changes in the foreign exchange rates from that which is due to changes in market prices of equity securities. Accordingly, realized and unrealized foreign currency gains and losses with respect to such securities are included in the reported net realized and unrealized gains and losses on investment transactions balances.

The Fund reports certain foreign currency related transactions and foreign taxes withheld on security transactions as components of realized gains for financial reporting purposes, whereas such foreign currency related transactions are treated as ordinary income for U.S. federal income tax purposes.

Net unrealized currency gains or losses from valuing foreign currency denominated assets and liabilities at period end exchange rates are reflected as a component of net unrealized appreciation/depreciation in value of investments, and translation of other assets and liabilities denominated in foreign currencies.

Net realized foreign exchange gains or losses represent foreign exchange gains and losses from transactions in foreign currencies and forward foreign currency contracts, exchange gains or losses realized between the trade date and settlement date on security transactions, and the difference between the amounts of interest and dividends recorded on the Fund's books and the U.S. dollar equivalent of the amounts actually received.

Distributions of Income and Gains: The Fund distributes at least annually to shareholders substantially all of its net investment income and net realized short-term capital gains, if any. The Fund determines annually whether to distribute any net realized long-term capital gains in excess of net realized short-term capital losses, including capital loss carryovers, if any. An additional distribution may be made to the extent necessary to avoid the payment of a 4% U.S. federal excise tax. Dividends and distributions to shareholders are recorded by the Fund on the ex-dividend date.

21

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

December 31, 2006

The character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for U.S. income tax purposes due to U.S. generally accepted accounting principles/tax differences in the character of income and expense recognition.

Partnership Accounting Policy: The Fund records its pro-rata share of the income/(loss) and capital gains/(losses) allocated from the underlying partnerships and adjusts the cost of the underlying partnerships accordingly. These amounts are included in the Fund's Statement of Operations.

Other: The Fund invests in securities of foreign countries and governments which involve certain risks in addition to those inherent in domestic investments. Such risks generally include, among others, currency risk (fluctuations in currency exchange rates), information risk (key information may be inaccurate or unavailable) and political risk (expropriation, nationalization or the imposition of capital or currency controls or punitive taxes). Other risks in investing in foreign securities include liquidity and valuation risks.

Some countries require governmental approval for the repatriation of investment income, capital or the proceeds of sales of securities by foreign investors. In addition, if there is a deterioration in a country's balance of payments or for other reasons, a country may impose temporary restrictions on foreign capital remittances abroad. Amounts repatriated prior to the end of specified periods may be subject to taxes as imposed by a foreign country.

The Latin American securities markets are substantially smaller, less liquid and more volatile than the major securities markets in the United States. A high proportion of the securities of many companies in Latin American countries may be held by a limited number of persons, which may limit the number of securities available for the investment by the Fund. The limited liquidity of Latin American country securities markets may also affect the Fund's ability to acquire or dispose of securities at the price and time it wishes to do so.

The Fund, subject to local investment limitations, may invest up to 10% of its assets (at the time of commitment) in illiquid equity securities, including securities of private equity funds (whether in corporate or partnership form) that invest primarily in emerging markets. When investing through another investment fund, the Fund will bear its proportionate share of the expenses incurred by the fund, including management fees. Such securities are expected to be illiquid which may involve a high degree of business and financial risk and may result in substantial losses. Because of the current absence of any liquid trading market for these investments, the Fund may take longer to liquidate these positions than would be the case for publicly traded securities. Although these securities may be resold in privately negotiated transactions, the prices realized on such sales could be substantially less than those originally paid by the Fund or the current carrying values and these differences could be material. Further, companies whose securities are not publicly traded may not be subject to the disclosure and other investor protection requirements applicable to companies whose securities are publicly traded.

Note C. Agreements

Credit Suisse Asset Management, LLC ("Credit Suisse") serves as the Fund's investment adviser with respect to all investments. Credit Suisse receives as compensation for its advisory services from the Fund, an annual fee, calculated weekly and paid quarterly, equal to 1.00% of the first $100 million of the Fund's average weekly market value or net assets (whichever is lower), 0.90% of the next $50 million and 0.80% of amounts over $150 million. For the year ended December 31, 2006, Credit Suisse earned $2,159,520 for advisory services, of which Credit Suisse waived $4,000. Credit Suisse also provides certain administrative services to the Fund and is

22

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

December 31, 2006

reimbursed by the Fund for costs incurred on behalf of the Fund (up to $20,000 per annum). For the year ended December 31, 2006, Credit Suisse was reimbursed $20,000 for administrative services rendered to the Fund.

CELFIN CAPITAL Servicios Financieros S.A. ("Celfin") serves as the Fund's sub-adviser with respect to Chilean investments. As compensation for its services, Celfin is paid a fee, out of the advisory fees payable to Credit Suisse, calculated weekly and paid quarterly at an annual rate of 0.10% of the Fund's average weekly market value or net assets (whichever is lower). For the year ended December 31, 2006, these sub-advisory fees amounted to $239,311.

For the year ended December 31, 2006, Celfin earned approximately $62 in brokerage commissions from portfolio transactions executed on behalf of the Fund.

Bear Stearns Funds Management Inc. ("BSFM") serves as the Fund's U.S. administrator. The Fund pays BSFM a monthly fee that is calculated weekly based on the Fund's average weekly net assets. For the year ended December 31, 2006, BSFM earned $146,388 for administrative services.

Celfin Capital S.A. Administradora de Fondos de Capital Extranjero ("AFCE") serves as the Fund's Chilean administrator. For its services, AFCE is paid an annual fee by the Fund equal to the greater of 2,000 Unidad de Fomentos ("U.F.s") (approximately $69,000 at December 31, 2006) or 0.10% of the Fund's average weekly market value or net assets invested in Chile (whichever is lower) and an annual reimbursement of out-of-pocket expenses not to exceed 500 U.F.s. In addition, an accounting fee is also paid to AFCE. For the year ended December 31, 2006, the administration fees and accounting fees amounted to $86,001 and $6,800 respectively.

Merrill Corporation ("Merrill"), an affiliate of Credit Suisse, has been engaged by the Fund to provide certain financial printing services. For the year ended December 31, 2006, Merrill was paid $25,888 for its services to the Fund.

The Independent Directors receive fifty percent (50%) of their annual retainer in the form of shares purchased by the Fund's transfer agent in the open market. Directors as a group own less than 1% of the Fund's outstanding shares.

Note D. Capital Stock

The authorized capital stock of the Fund is 100,000,000 shares of common stock, $0.001 par value. Of the 6,322,240 shares outstanding at December 31, 2006, Credit Suisse owned 13,746 shares.

Note E. Investment In Securities

For the year ended December 31, 2006, purchases and sales of securities, other than short-term investments, were $100,599,452 and $121,252,080, respectively.

Note F. Credit Facility

The Fund, together with other funds/portfolios advised by Credit Suisse (collectively, the "Participating Funds"), participates in a $75 million committed, unsecured, line of credit facility ("Credit Facility") with Deutsche Bank, A.G. as administrative agent and syndication agent and State Street Bank and Trust Company as operations agent for temporary or emergency purposes. Under the terms of the Credit Facility, the Participating Funds pay an aggregate commitment fee at a rate of 0.10% per annum on the average unused amount of the Credit Facility, which is allocated among the Participating Funds in such manner as is determined by the governing Boards of the Participating Funds. In addition, the Participating Funds pay interest on borrowings at the Federal Funds rate plus 0.50%. During the year ended December 31, 2006, the Fund had no borrowings under the Credit Facility.

23

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

December 31, 2006

Note G. Federal Income Taxes

Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from GAAP.

The tax character of dividends paid during the years ended December 31 for the Fund were as follows:

| Ordinary Income | | Long-Term Capital Gains | |

| 2006 | | 2005 | | 2006 | | 2005 | |

| $ | 11,000,697 | | | $ | 3,161,120 | | | $ | 23,329,066 | | | $ | 1,770,227 | | |

The tax basis of components of distributable earnings differ from the amounts reflected in the Statement of Assets and Liabilities by temporary book/tax differences. These differences are primarily due to losses deferred on wash sales. At December 31, 2006, the components of distributable earnings on a tax basis for the Fund were as follows:

| Undistributed ordinary income | | $ | 2,903,629 | | |

| Accumulated net realized gain | | | 13,659,994 | | |

| Unrealized appreciation | | | 135,108,950 | | |

| Total distributable earnings | | $ | 151,672,573 | | |

At December 31, 2006, the identified cost for federal income tax purposes, as well as the gross unrealized appreciation from investments for those securities having an excess of value over cost, gross unrealized depreciation from investments for those securities having an excess of cost over value and the net unrealized appreciation from investments were $161,877,985, $135,873,421, $(785,662) and $135,087,759, respectively.

At December 31, 2006, the Fund reclassified $(220,657) from accumulated net realized gain on investments and foreign currency related transactions to undistributed net investment income. Net assets were not affected by this reclassification.

Note H. Restricted Securities

Certain of the Fund's investments are restricted as to resale and are valued at fair value as determined in good faith by, or under the direction of, the Board of Directors under procedures established by the Board of Directors in the absence of readily ascertainable market values.

| Security | | Number

of

Units/Shares | | Acquisition

Date(s) | | Cost | | Fair

Value at

12/31/06 | | Value Per

Unit/Share | | Percent

of Net

Assets | | Distributions

Received | | Open

Commitments | |

Emerging Markets

Ventures I L.P. | | | 2,226,890 | | | 01/22/98-07/01/05 | | $ | 1,280,541 | | | $ | 1,008,024 | | | | 0.45 | | | | 0.34 | | | | | | |

| | | | 10,402 | | | 01/10/06 | | | 9,073 | | | | 4,709 | | | | 0.45 | | | | 0.00 | | | | | | |

| | | | 2,237,292 | | | | | | 1,289,614 | | | | 1,012,733 | | | | | | | | 0.34 | | | $ | 1,796,362 | | | $ | 262,708 | | |

J.P. Morgan Latin

America Capital

Partners

(Cayman), L.P. | | | 914,628 | | | 04/10/00-08/02/05 | | | 458,883 | | | | 238,205 | | | | 0.26 | | | | 0.09 | | | | | | |

| | | | 30,021 | | | 06/27/06 | | | 27,387 | | | | 7,819 | | | | 0.26 | | | | 0.00 | | | | | | |

| | | | 3,993 | | | 12/21/06 | | | 3,304 | | | | 1,040 | | | | 0.26 | | | | 0.00 | | | | | | |

| | | | 948,642 | | | | | | 489,574 | | | | 247,064 | | | | | | | | 0.09 | | | $ | 1,369,272 | | | | — | | |

24

THE LATIN AMERICA EQUITY FUND, INC.

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

December 31, 2006

| Security | | Number

of

Units/Shares | | Acquisition

Date(s) | | Cost | | Fair

Value at

12/31/06 | | Value Per

Unit/Share | | Percent

of Net

Assets | | Distributions

Received | | Open

Commitments | |

J.P. Morgan Latin

America Capital

Partners

(Delaware), L.P. | | | 1,470,896 | | | 04/10/00-08/02/05 | | $ | 674,631 | | | $ | 723,798 | | | | 0.49 | | | | 0.25 | | | | | | |

| | | | 13,371 | | | 03/09/06 | | | 12,032 | | | | 6,580 | | | | 0.49 | | | | 0.00 | | | | | | |

| | | | 5,534 | | | 12/21/06 | | | 5,534 | | | | 2,723 | | | | 0.49 | | | | 0.00 | | | | | | |

| | | | 1,489,801 | | | | | | 692,197 | | | | 733,101 | | | | | | | | 0.25 | | | $ | 1,305,115 | | | | 691,463 | | |

| Total | | | | | | | | $ | 2,471,385 | | | $ | 1,992,898 | | | | | | | | 0.68 | | | $ | 4,470,749 | | | $ | 954,171 | | |

The Fund may incur certain costs in connection with the disposition of the above securities.

Note I. Contingencies

In the normal course of business, the Fund may provide general indemnifications pursuant to certain contracts and organizational documents. The Fund's maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated: however, based on experience, the risk of loss from such claims is considered remote.

Note J. Recent Accounting Pronouncements

During June 2006, the Financial Accounting Standards Board ("FASB") issued FASB Interpretation 48 ("FIN 48" or the "Interpretation"), Accounting for Uncertainty in Income Taxes—an interpretation of FASB statement 109. FIN 48 supplements FASB Statement 109, Accounting for Income Taxes, by defining the confidence level that a tax position must meet in order to be recognized in the financial statements. FIN 48 prescribes a comprehensive model for how a fund should recognize, measure, present, and disclose in its financial statements uncertain tax positions that the fund has taken or expects to take on a tax return. FIN 48 requires that the tax effects of a position be recognized only if it is "more likely than not" to be sustained based solely on its technical merits. Management must be able to conclude that the tax law, regulations, case law, and other objective information regarding the technical merits sufficiently support the position's sustainability with a likelihood of more than 50 percent. FIN 48 is effective for fiscal periods beginning after December 15, 2006. At adoption, the financial statements must be adjusted to reflect only those tax positions that are more likely than not to be sustained as of the adoption date.