UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06017 |

|

Julius Baer Global Equity Fund Inc |

(Exact name of registrant as specified in charter) |

|

330 Madison Avenue, New York, NY | | 10017 |

(Address of principal executive offices) | | (Zip code) |

Tony Williams |

330 Madison Avenue, New York, NY 10017 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-297-3600 | |

|

Date of fiscal year end: | 10/31 | |

|

Date of reporting period: | 10/31/06 | |

| | | | | | | |

Item 1. Reports to Stockholders.

The annual report is attached.

2

Julius Bär

Annual Report

Julius Baer Funds

Julius Baer Global Equity Fund Inc.

Julius Baer International Equity Fund

Julius Baer International Equity Fund II

Julius Baer Total Return Bond Fund

Julius Baer Global High Income Fund

Julius Baer U.S. Microcap Fund

Julius Baer U.S. Smallcap Fund

Julius Baer U.S. Midcap Fund

Julius Baer U.S. Multicap Fund

October 31, 2006

SHAREHOLDERS LETTER October 31, 2006

December 22, 2006

Dear Shareholder

I am pleased to present the Annual Report for the Julius Baer Funds (the "Funds") for the fiscal year ending October 31, 2006 (the "Reporting Period").

The Reporting Period began with most of the major indices strongly advancing; however, all eyes were on the Federal Reserve's (the "Fed") activity. Not only had it been regularly increasing the Fed Funds rate (a key overnight lending rate) as a tool to curb growing inflationary pressures, but it would begin the new year without Alan Greenspan, who had served for nearly 18 years as its Chairman. Although the market had braced for further tightening to monetary policy, analysts scrutinized every statement uttered by his successor, Ben Bernanke, in the hope of determining when such activity would end. In May, most global equity markets reacted violently to yet another interest rate hike by the Fed. Much of the gains that occurred during the first half of the Reporting Period eroded, particularly in emerging market stocks. For several weeks, markets remained turbulent. The Fed continued its stance by raising rates further in June, but suggested that the current level set may remain steady for a while. With a sense of stability back in the marketplace, most global markets rebounded with most indices generating double digit returns over the Reporting Period. Even the political fallout over U.S./U.K. policy in Iraq has not had significant impact on markets.

Over the last several years, the falling U.S. dollar has helped most international markets outpace the Standard & Poor's 500 Index. As a result, investors continue to actively seek ways to diversify their portfolios. For some time now, such investors have been drawn to our flagship international equity products. Our fixed income funds, both of which have international components and strong track records, are now beginning to attract significant attention. For example, the Julius Baer Total Return Bond Fund raised nearly $294.4 million in new subscriptions, doubling the overall size of the Fund. We believe that this is a positive trend and hope that this will translate into better investment opportunities and cost savings to shareholders.

We are committed to ensuring that the investment parameters for each of the Funds continue to maximize the opportunities to generate returns for shareholders. In the past, we have said that the exposure to emerging markets within the Julius Baer International Equity Fund, Julius Baer International Equity Fund II, and Julius Baer Global Equity Fund, Inc. ("Global Equity Fund") was not then anticipated to exceed 25%. Over the last decade, the emerging market universe has undergone important fundamental changes. Not only has the market capitalization of such

Julius Baer Funds 2006 Annual Report

1

countries doubled during this time frame, but corporate governance standards have been introduced, making many of these markets much less risky. As economies have broadened, the universe has become more diversified in macroeconomic terms. In anticipation of this trend continuing, the Board of Directors has recently agreed to permit an emerging market exposure up to 35%. This applies to all the three Funds mentioned and will be effective from early March following formal notification to shareholders.

Julius Baer Investment Management LLC ("JBIM") is keen to strategically expand its investment set in asset classes where we believe we can add value for our clients over the long term. In July, JBIM launched four new U.S. equity funds focused on micro, small, mid and multi-cap equity. We believe that this represents a natural extension of our ability to deliver added value in U.S. equity investing, previously only available via our core global equity strategy. Mr. Sam Dedio, who joined the firm earlier this year from Deutsche Asset Management where he was Managing Director, Co-lead Portfolio Manager and Co-Head of U.S. Micro, Small and Midcap Investment Management, is managing the Julius Baer U.S. Microcap Fund (JMCAX, JMCIX), the Julius Baer U.S. Smallcap Fund (JSCAX, JSCIX), and the Julius Baer U.S. Midcap Fund (JMDAX, JMDIX). Mr. Dedio has also been co-managing the Julius Baer U.S. Multicap Fund (JMLAX, JMLIX) ("Multicap Fund") with Mr. B rett Gallagher, JBIM's Deputy Chief Investment Officer and the head of our U.S. large cap equity team.

In order to capitalize on JBIM's broader expertise across the U.S. capitalization spectrum and strengthen our core fundamental philosophy, the U.S. portion of the Global Equity Fund will transition toward a more multi-cap approach, although the Fund as a whole will continue to retain a large-cap bias. As a result, Mr. Dedio will take on management of the U.S. component of this product from Mr. Gallagher. Mr. Gallagher will serve in the capacity of Senior Investment Specialist on behalf of our Global Equity strategy, and he will retain his role as JBIM's Deputy Chief Investment Officer. Mr. Gallagher's considerable experience and credibility offer the necessary skill set to effectively serve the broad needs of JBIM's client base and he will continue to remain closely associated with the Funds. Replacing Mr. Gallagher on the Multicap Fund will be Mr. Keith Walter who has been serving under Mr. Gallagher's direction as a portfolio manager and i nvestment analyst since 1999. Prior to his career at JBIM, Mr. Walter was fixed income portfolio manager at both Morgan Stanley and Bankers Trust Company. Despite the short track record of these new funds, we are encouraged by their performance (see Manager's Commentary on the subsequent pages for details) to date and believe that incorporating them into our product mix will deliver a diversified range of strategies that will showcase the talents of our organization.

Julius Baer Funds 2006 Annual Report

2

In a world of change, it is important that we have a good system of checks and balances to ensure that we deliver the very best to our shareholders at all times. JBIM, as well as the Funds' Boards of Directors and Trustees, (the "Boards") share that vision. Thus, it is with great pleasure that I welcome Mr. Robert McGuire to the Boards as an additional independent Director/Trustee. Mr. McGuire is the former New York City Police Commissioner, former Chairman and Chief Executive Officer of Pinkerton's Inc., and former President of Kroll Associates, Inc., an international corporate investigations and security consulting firm. He is also a lawyer with a broad range of governmental and private sector experience. Throughout his career, he has served on numerous boards and commissions and we believe that this coupled with his experience in the mutual fund arena will be a valuable asset for shareholders.

In conclusion, I'd like to express JBIM's appreciation to you as shareholders for your continued support and to wish you and your families a happy and healthy holiday season.

Sincerely,

Tony Williams

Chief Executive Officer

This Material is provided for informational purposes only and does not in any sense constitute a solicitation or offer of the purchase or sale of securities unless preceded or accompanied by a prospectus.

Mutual funding investing involves risk; principle loss is possible.

Distributor: Quasar Distributors, LLC (12/06)

Julius Baer Funds 2006 Annual Report

3

MANAGEMENT'S COMMENTARY

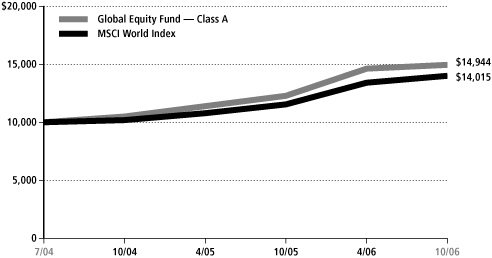

JULIUS BAER GLOBAL EQUITY FUND INC.

Annual Report

Period Ending October 31, 2006

The Julius Baer Global Equity Fund Inc. ("the Fund") enjoyed its second full fiscal year in current form. The Fund, which has previously been known as the closed-end European Warrant Fund, became an open-ended fund on July 1, 2004 and changed its name to reflect the change in strategy and management team. This is the third annual report since the change and the second that covered a full 12-month period.

The Fund (Class A shares) returned 21.56% over the twelve months ending October 31, 2006 which compares favorably to its benchmark, the MSCI World Index (net dividends), which returned 21.32%. Since the change in format on July 1, 2004, the Fund has outperformed its benchmark by 7.74% (51.81% vs. 44.07% cumulative returns).

Market Review

The reporting period was a difficult one for most managers as very few underlying trends (either geographically or sector-wise) were able to persist for the full period. In other words, what worked well in one part of the period tended to underperform in other periods.

The United States was the weakest of the developed markets between October 31, 2005 and May 12, 2006 (-7.80% relative to MSCI World) while it was the strongest from May 12, 2006 through October 31, 2006 (+2.85% relative). Japan was just the opposite, outperforming early on by 10.97% and underperforming subsequently by 12.11%. Europe and the U.K. were the most consistent regions over the full period, outperforming by 3.65% and 7.63% respectively in the first half and by 0.98% and 0.94% in the second. For the full reporting period, we were underweight the U.S., the U.K. and Japan and overweight Continental Europe. The flip-flopping of relative performance from one period to the next made it difficult for any manager to gain traction without dramatically restructuring his or her portfolio mid-way through the year.

Similarly, what worked or failed across the various economic sectors exhibited the same positive/negative relative patterns over the course of the reporting period. The following chart details the performance of both MSCI U.S. and Global sector price-performance in local currency terms for the period October 31, 2005—October 31, 2006.

Julius Baer Funds 2006 Annual Report

4

Equity Sectors (U.S. and World in Local Currency Terms)

| | | 10/31/05-

4/28/06 | | 5/1/06-

10/31/06 | |

| MSCI U.S. - Consumer Staples | | | 1.43 | % | | | 9.07 | % | |

| MSCI Global - Consumer Staples | | | 4.76 | % | | | 7.72 | % | |

| MSCI U.S. - Consumer Discretionary | | | 7.04 | % | | | 8.24 | % | |

| MSCI Global - Consumer Discretionary | | | 13.28 | % | | | 4.19 | % | |

| MSCI U.S. - Health Care | | | 1.58 | % | | | 7.21 | % | |

| MSCI Global - Health Care | | | 4.54 | % | | | 5.27 | % | |

| MSCI U.S. - Utility Sector | | | (0.40 | %) | | | 13.72 | % | |

| MSCI Global - Utility Sector | | | 9.15 | % | | | 12.11 | % | |

| MSCI U.S. - Telecomm Services Sector | | | 12.79 | % | | | 14.99 | % | |

| MSCI Global - Telecomm Services Sector | | | 1.78 | % | | | 11.28 | % | |

| MSCI U.S. - Information Technology | | | 6.90 | % | | | 2.75 | % | |

| MSCI Global - Information Technology | | | 10.59 | % | | | 1.10 | % | |

| MSCI U.S. - Financials | | | 11.58 | % | | | 4.74 | % | |

| MSCI Global - Financials | | | 16.45 | % | | | 3.47 | % | |

| MSCI U.S. - Materials Sector | | | 19.35 | % | | | (0.46 | %) | |

| MSCI Global - Materials Sector | | | 27.63 | % | | | 0.50 | % | |

| MSCI U.S. - Energy Sector | | | 17.99 | % | | | 0.41 | % | |

| MSCI Global - Energy Sector | | | 15.46 | % | | | (3.64 | %) | |

| MSCI U.S. - Industrials | | | 14.97 | % | | | (0.74 | %) | |

| MSCI Global - Industrials | | | 19.35 | % | | | (1.40 | %) | |

Almost without exception (technology being the underperforming exception), the biggest underperformers relative to the index in the first half of the reporting period were leaders in the second half. The theme was to reward the more economically sensitive areas early on, while some caution seemed to build-up after the first calendar quarter as the traditional "late cyclical" sectors (materials, energy and industrials) turned from top performers to laggards and more defensive sectors such as consumer staples, utilities and healthcare rallied to take leadership positions.

Geographic Exposure in the Fund

Our biggest relative weighting geographically over the period was the underweight to Anglo-Saxon economies (primarily the U.S. and the U.K.) due to concerns regarding their overextended consumer base.

We were also underweight in Japan where relative valuations left us scratching our heads as the market roared upwards in 2005, due to what now looks to have been

Julius Baer Funds 2006 Annual Report

5

a momentum-led push. Cooler, more analytical heads have seemed to prevail in 2006 as Japan has lagged other global stock exchanges.

Our emerging markets exposure continues to be substantial with our focus on Central and Eastern Europe which, as we described last year, possess emerging market growth potential with developed market risk. This belief was rewarded during the year as emerging markets were the best performing region for the full period, rising by 38.2% in Eastern Europe, 34.6% in Latin America, and by 35.1% in Asia. Our decision to concentrate on Europe at the expense of Asia and Latin America has to do with the long-term drivers we see in each region. While Asia and Latin America remain export dependent (relying on those Anglo-Saxon consumers we talked about earlier), the dynamic within Eastern Europe remains economic convergence with their richer Western European neighbors.

Global Themes Revisited

Last year, a number of investment themes were detailed. Most of these worked well for the Fund.

Within Continental Europe, we spoke about three themes: consolidation within the Italian banking sector, infrastructure-related companies, and Scandinavian financials.

Shortly after we wrote last year's letter detailing the travails of Italy's central bank chief Antonio Fazio (the governor who was appointed for a life term but who subsequently was forced to resign), ABN Amro of the Netherlands succeeded in its quest to take over Banca Antonveneta SpA. Further bank deals occurred throughout the year, including the two most recent mergers between Banco Popolare di Verona Novara and Banca Popolare di Italiana, and, in turn, between Banca Intesa SpA and Sanpaolo IMI SpA. While this theme is now well-recognized in the markets, we still retain numerous holdings and expect it to persist into the new year.

Acquisitions also heated up in the infrastructure area with BAA PLC, Associated British Ports and Pensinsular & Oriental Steam Navigation Company ("P&O") all being acquired. BAA PLC was taken over by a consortium of companies including Grupo Ferrovial SA of Spain, the Government of Singapore and Caisse de Depot of Canada. Associated British Ports was acquired by another consortium consisting of Macquarie Bank of Australia, 3i Group PLC of the U.K., Infomedia of Australia and Canadian Pension Plan Investment Board. P&O was acquired by DP World, a Dubai-based company. Our preference for companies in this sector is driven by the increased global trade in China, India and other emerging countries that act as the world's factory as well as by the strain on European government budgets which is leading to more public/private partnerships over infrastructure assets.

Julius Baer Funds 2006 Annual Report

6

Scandinavian banks were also a favored sector last year due to their relatively cheap valuations, the better state of their local consumer balance sheets, and their exposure to the faster growth of their Eastern European neighbors. When we first invested in many of these names, they traded at substantial discounts to other European financial companies. Due to outperformance in the past three years, the valuation discount has disappeared, though faster growth still remains a lure.

We believe our caution with respect to Japan was well-founded. We felt the rally in late 2005 was driven by momentum and performance chasing and we could not find fundamental value in most segments of the market, and thus, continued to avoid it. While Japan finished 2005 strong, as stated above, Japan has since struggled and we believe such struggles are likely to continue as valuations remain rich. Some signs of slowdown in the economy are now apparent.

In the emerging markets, we spoke of opportunities in Russia, while at the same time acknowledging the increased level of risks inherent in such investments. Over the course of the reporting period, we experienced both the upside of reward and the downside of risk. The Russian market returned 52.3% over the reporting period, though not without falling by nearly 30% between May 9, 2006 and June 13, 2006. Only committed investors were likely to have reaped the full gains from the market as many short-term holders were certain to have fled during the downturn. We remain exposed to this market, primarily in energy and materials-related issues as well as through ownership in Sberbank, a Russian commercial bank.

China and India were also mentioned in last year's letter and both performed well, rising nearly 55% in the case of China and nearly 65% in the case of India during the reporting period. Our preference was for investment in India, albeit, acknowledging that investment in the country was not easy. We established and increased positions there over the course of the reporting period and like the progress we have seen. We still remain largely absent the mainland Chinese market given our earlier concerns over transparency, the quality of listed companies, and market valuation.

Turkey was a prominent theme this time last year and we continued to enjoy a strong run into the new year (climbing approximately 50% between October 31, 2005 and February 27, 2006). However, as the year continued, we began to see that progress in key areas such as inflation was beginning to slow while the current account continued to widen and equity valuations remained rich. We took this opportunity to reduce our holdings in Turkey and to "upgrade" the quality of our Fund by raising weights in Poland and Russia during the mid-year downturn. Today, Turkey represents approximately 0.6% of the portfolio, down from 1.8% on October 31, 2005.

Julius Baer Funds 2006 Annual Report

7

One theme that has not (yet) worked well, was our shunning of the U.S. consumer who has continued to find ways to spend even as the debt pile (now 24% of disposable income, not including mortgages) and debt servicing (now claiming more than $0.14 of every dollar earned) continues to hover at high levels. In fact, U.S. consumer cyclical stocks outperformed the market by nearly 1% during the reporting period and bested their more defensive consumer staples names by over 4%. While we believe our caution will eventually yield substantial fruit, one must approach this investment play cautiously. Should the U.S. consumer succumb to fatigue, many worry that the knock-on effects to the rest of the world will be substantial. While we agree there will be repercussions (affecting some companies and countries more than others), the worry is less than in previous periods due to the growth of the non-U.S. consumer. Whereas emerging markets consumption was only 40% of the U.S. consumption just three years ago, today it is over 50%. Three years from now it will be even higher. Thus, the world is finding an alternative to the U.S. consumer who has driven not only the U.S., but also global growth over the past years.

Global Themes Refreshed

While many of our global themes retain "legs" and we believe will continue to perform over the next reporting period, some new areas of interest have cropped up since our last review. These include plays on domestic economic recovery in Germany, attractive valuation and growth opportunities in Finland, and global luxury goods.

The economic boom which enveloped most of the world over the past decade seems to have passed by Germany. While real estate prices rose many-fold around the globe, they seemed to have stalled in Germany. We think this situation has changed and we are pursuing a multi-pronged approach to tap the fortunes of Europe's largest economy. Our focus includes builders, real estate (commercial and residential) and banks.

Finland would appear to be a sleepy market to many, known as the home of Nokia and good fishing. To us, Finland remains a source of inexpensive companies that are taking advantages of the growth opportunities with neighbors Russia and the Baltic States. Such a combination has led us to take up positions in a handful of Finnish companies.

Finally, the luxury goods makers have long had a place in our portfolio and we believe this still to be a "fresh" idea. While the Japanese have traditionally made up a large portion of the profits of such companies, the emergence of wealthy Chinese and Indian consumers, along with strong money flows accruing to the Middle East (as a result of high energy prices) have created new demand for companies such as LVMH, Richemont and Bulgari.

Julius Baer Funds 2006 Annual Report

8

The Coming Year

The coming year holds many promises and challenges. Hopefully, the log jam of rapidly changing preferences will end and some of our themes will take flight. While the emerging markets and economic recovery in Germany offer hope for global growth, we remain on guard against the U.S. and U.K. consumer who certainly have done little to correct imbalances in their personal balance sheets. Whether this coming reporting period is the one where exhaustion will catch up with them, or not, remains to be seen. Until that time, we will be cautious on building up positions in sectors or geographies dependent on them.

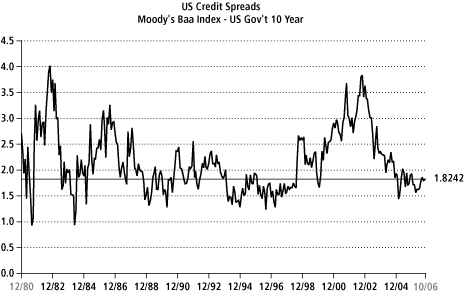

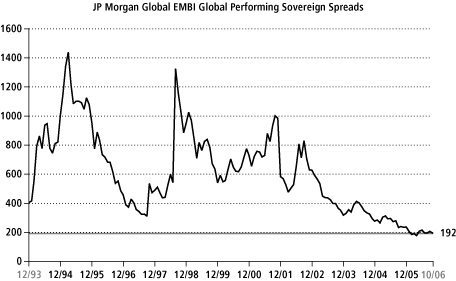

One of the more unusual aspects to the markets over the past few years has been the embrace of risk by investors across all asset classes. In the fixed income world, credit spreads have continued to shrink, allowing lower rated corporate and government issuers to access capital at rates not far from those accorded to better rated credits. The two charts below show the credit spreads for the Moody's Baa Corporate issuers and Sovereign Emerging Markets issuers relative to the U.S. Treasury Bonds (the horizontal line depicts current readings).

Source: Bloomberg

Julius Baer Funds 2006 Annual Report

9

Source: Bloomberg

Also, in the credit default swap market (a kind of insurance pool to insulate fixed income investors against the risk of bond issuer defaults), premiums have fallen dramatically as seen in the chart below. Apparently, investors are not too concerned about credit risk despite what appears to be a slowing economy.

Source: Bloomberg

Such an embrace of risk as we have seen in the equity markets has dominated the larger and (usually) more stable large cap brethren in terms of performance. The following chart shows the relative performances of small versus large cap names globally, which have outperformed by more than 125% (relative to the MSCI World Index) since the trough in February 1999.

Julius Baer Funds 2006 Annual Report

10

Source: Bloomberg

Of course, valuation and growth plays a turn in determining such relative performance and at the start of this period small capitalization stocks sold at the discount to larger cap names and have since grown at a faster rate. Given near parity in valuations today, one wonders if an aversion to risk would mean a turn in the relative performance of "risky" equity assets.

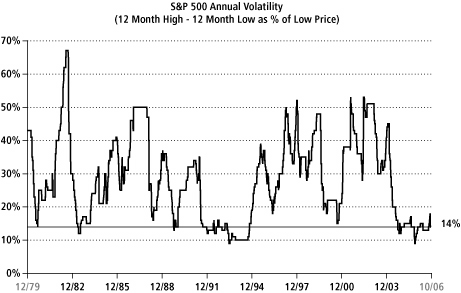

Finally, there appears to be relative complacency across the board with respect to larger capitalization stocks. The following chart shows the percentage difference in the high vs. low price of the S&P 500 Index over rolling 12 month time frames. Today's narrow spread is historically low.

Source: Bloomberg

Julius Baer Funds 2006 Annual Report

11

As we move into the next reporting period, we remain focused on uncovering opportunities and managing risks presented by the global equity markets on behalf of our valued shareholders.

Brett Gallagher

Global Equity Fund Inc. Portfolio Manager

Past performance does not guarantee future results.

Investing internationally involves additional risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The views expressed are subject to change based on market and other conditions. Furthermore, the opinions expressed do not constitute investment advice or recommendation by the individuals, JBIM, the funds, or any affiliated company.

The MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in the Americas, Europe/Middle East, and Asia/Pacific Regions. It is not possible to invest directly in an index.

Please see the Schedule of Investments in this report for complete fund holdings. Fund holdings and/or sector weightings are subject to change at any time and are not recommendations to buy or sell any security mentioned.

Julius Baer Funds 2006 Annual Report

12

MANAGEMENT'S COMMENTARY

JULIUS BAER INTERNATIONAL EQUITY FUND

JULIUS BAER INTERNATIONAL EQUITY FUND II

Annual Report

Period Ending October 31, 2006

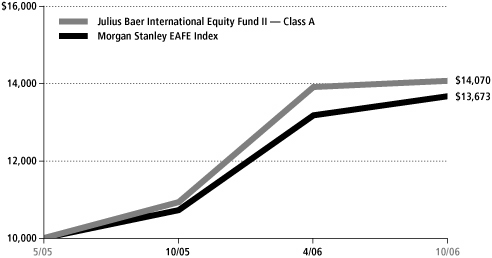

Both the Julius Baer International Equity Fund ("IEF") and the Julius Baer International Equity Fund II ("IE II") outperformed their benchmark, the MSCI EAFE Index ("the Index"), for the period under review. For the twelve months ending October 31, 2006, IEF Class A Shares returned 31.20% and IE II Class A Shares returned 28.73% versus 27.52% for the Index. While IE II only invests in companies with a market capitalization of greater than U.S.$2.5 billion at the time of purchase (and IEF invests in securities of all market capitalizations), whenever feasible, the geographic and sector exposure for the two funds are similar.

Our ability to outperform the benchmark was the result of a number of factors, most notably our exposure to emerging markets. Top contributors included Russia, Poland and Turkey. Within Russia, our position in the nation's largest bank, OAO Sberbank, was a top contributor to our results for the period. Positions held in OAO Gazprom and OAO Lukoil, the country's biggest producers of natural gas and oil, were also among the top contributors. We have long been attracted to the country's energy reserves which trade at a discount to their Western European peers. Additionally, our position in OAO Norilsk Nickel, the world's largest nickel and palladium producer proved beneficial to results. Amid an era of industrialization for China and India, we believe Russia's vast natural resources provide an attractive long term investment opportunity.

Within Poland, our focus on many of the banks supported results. PKO Bank Polski and Bank Pekao, the two largest lenders in Poland exhibited strong results as did Bank Zachodni amid an expanding economic climate which has fuelled increased demand for financial services. However, the position held in Agora by the IEF, Poland's top publisher, detracted from results. The shares declined subsequent to disappointing earnings results for the fourth quarter of 2005.

We were effective in managing our exposure to the Turkish market amid a very turbulent environment. At the start of the period, we had over 3.5% invested. We aggressively reduced our weighting to less than 2% by the end of April and further reduced exposure to approximately 1% by the end of the review period. Concerns over a deteriorating fiscal position in the country and the U.S. Federal Reserve's hike in short term interest rates on May 10 struck many emerging markets hard, including Turkey. However, the market managed to recover somewhat and several of the positions retained over the period exhibited strong results.

Julius Baer Funds 2006 Annual Report

13

Within Continental Europe, holdings in cement, airports and banks were positive contributors to results. The global cement industry has been on a consolidating trend leading to more pricing power. The industry has also become less cyclical due to government spending to prop up demand in weak phases of the business cycle. High barriers to entry have created an industry which has become more defensive in nature. Our positions in LaFarge (France) and Holcim (Switzerland) produced strong results.

We view airports and seaports as quasi-monopolies able to leverage the increase in global travel and trade. Strained European government budgets have led to public/private partnerships with companies engaged in infrastructure construction and we own several throughout Europe and Asia. Our position held in Fraport, the operator of the Frankfurt airport, which is Europe's third busiest, was a top contributor to performance. Toward the end of the period, however the shares came under pressure after having lost a bid for the London City Airport.

The Italian banking industry has been undergoing a wave of consolidations, which we expect to continue. We have been attracted to a number of banks such as Unicredito Italiano which was a strong performer over the period. We continue to see opportunity for restructuring and efficiency gains, as well as growth potential within the credit market as demand for such products begins to converge toward European averages. Several positions held in Swedish banks were also supportive of results. In particular, Skandinaviska Enskilda Banken, Skandinavia's third-largest bank in terms of assets, was a strong performer. The prospect for possible consolidation within the banking sector has provided positive performance.

The utility sector was the strongest performer in the index over the period, powered by mergers and deregulation. The fact that we were underweight Spanish utilities, in particular, detracted from results. However, this was offset by our position in Fortum Oyj, Finland's largest utility, which outperformed over the period.

Within the telecommunication services sector, while we were roughly in line with the average index weight for the period, our stock selection outperformed the Index. We continue to think telecommunications carriers are being challenged due to new entrants, increased regulation and lower pricing power amid technological innovation.

Japan was the weakest of the major developed markets and our underweight to Japanese equities was supportive to results. Investors appeared concerned about the impact any slowdown in consumer demand, especially from the U.S., would have on the country's export sector. While the Japanese economy has made some structural progress, we still believe shares of many Japanese companies are expensive versus comparable stocks in Europe. We find more compelling valuations in Continental Europe where we are overweight relative to the Index.

Looking forward, we remain enthusiastic about long-term opportunities in Eastern and Central Europe. Countries in the region have made significant improvements on many fronts, encouraged by the prospect of European Union ("EU") membership and possible inclusion into the Eurozone. From a policy risk perspective, the ten emerging markets that joined the EU in 2004 differ little in our view from many of their developed

Julius Baer Funds 2006 Annual Report

14

EU counterparts. Structurally, these countries have been highly successful in encouraging domestic demand, which makes them steadily less susceptible to a slowdown elsewhere in the global economy. India is another market, which we have recently increased our investing. We see the market as offering long term growth potential, particularly within the banking sector which should benefit from an increase in loan volumes.

We believe Continental Europe remains relatively strong and our focus continues to be on those industries most prone to the wave of restructuring activity taking place. In Germany, we have been focused on companies that will likely benefit from what we expect to be a strengthening domestic economy. After a long period of underperformance, we feel German asset prices are inexpensive and expect a rebound that will be centered on domestic stocks such as retailers and real estate related companies.

We remain underweight in the United Kingdom. The U.K. is traditionally a defensive market and with the index skewed toward companies in the utility, pharmaceutical, energy and food and beverage industries it has tended to outperform during more difficult economic conditions. However, we remain concerned about the U.K.'s growth prospects and the impact this may have on the corporate sector. Much like the United States, the U.K. has high consumer debt and a declining savings rate, which presents potential vulnerability for the U.K. consumer.

With the 2006 fiscal year now behind us, we remain focused on identifying opportunities around the globe, while keeping the big picture clearly in view. We look forward to reporting our progress to you throughout the year.

Richard Pell

International Equity Fund and International Equity Fund II Portfolio Manager

Past performance does not guarantee future results.

Investing internationally involves additional risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The views expressed are subject to change based on market and other conditions. Furthermore, the opinions expressed do not constitute investment advice or recommendation by the individuals, JBIM, the funds, or any affiliated company.

The MSCI EAFE Index is an unmanaged list of equity securities from Europe, Australasia, and the Far East with all values expressed in U.S. dollars. It is not possible to invest directly in an index or average.

Please see the Schedule of Investments in this report for complete fund holdings. Fund holdings and/or sector weightings are subject to change at any time and are not recommendations to buy or sell any security mentioned.

Julius Baer Funds 2006 Annual Report

15

MANAGEMENT'S COMMENTARY

JULIUS BAER TOTAL RETURN BOND FUND

Annual Report

Period Ending October 31, 2006

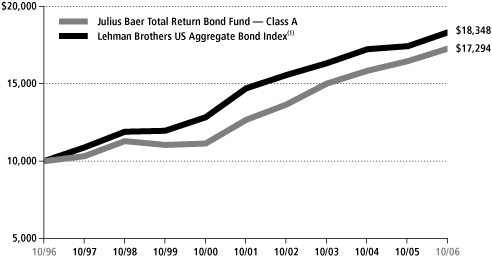

The Julius Baer Total Return Bond Fund (Class A Shares) (the "Fund") returned 4.98% for the twelve months ending October 31, 2006. Over the same period, the benchmark Lehman Brothers U.S. Aggregate Bond Index posted a 5.19% return.

In examining the Fund's relative performance for the annual period, one of the major detractors was a large underweight in U.S. interest rates from June through August. In early June, we expected the U.S. Federal Reserve Bank (the "Fed") to continue tightening, or at least pause, in its measured program of raising interest rates for the prior two years. Our primary concern was the ripple effects from inflation buildup that were expected to pass through the economy. We reasoned that this would push interest rates higher. At the end of June, the Fed hiked the prime short term interest rate to 5.25%, stating that "economic growth is moderating from its quite strong pace earlier this year." Long term rates began to subside. We equated these developments to a break in the Fed's tightening campaign. Consensus among fixed income investors leaned toward a slowdown in the economy and a possible recession in gross domestic product ("GDP") growth in th e near future. This led to a precipitous decline in U.S. interest rates. Our positioning during this time favored foreign bond markets and underweighting the overall duration of the benchmark. Consequently, we erred on the side of caution.

A major contributor to performance over the twelve month period was our currency positioning. As 2006 unfolded, we believed that the U.S. dollar was due to adjust downward, following the substantial rally in 2005. As the dollar weakened from the end of February through the middle of May, we were well positioned to undertake a sizable position in foreign currencies. The Euro, for example, appreciated over 8% during this time.

Outlook

The paramount question on investors' minds for the last twelve months was the health of the U.S. housing market. We think that this concern will probably prevail in the investment community for another year. Numerous studies were done on the housing market over the last few years. Some observers believe that the housing market will continue softening to a considerable extent, and the U.S. economy is heading toward recession. Others contend that current housing market conditions are more indicative of a mild correction and that home prices will strengthen again in the first half of 2007. Our view is more in the middle of these extremes with the

Julius Baer Funds 2006 Annual Report

16

caveat that the housing market may be soft for a much longer time than market consensus expects.

The U.S. housing market has indeed worsened over the reporting period. However, housing—albeit an integral part of the economy—is not the only driver of economic growth. The rest of the economy is progressing fairly well. Consumer spending, which accounts for more than two-thirds of GDP growth, continues at a robust pace. Also, employment continues to be encouraging, with a five-year low unemployment rate of 4.4% in October 2006.

The main reason we do not believe that the housing market will collapse in the immediate future lies in its inefficiency. There is no exchange or market maker to facilitate trades; if the seller and buyer cannot agree on a price, there is no trade. Listed houses may await sale for years. Due to the softness of the housing market over the past year, many potential sellers now face reduced prices compared to what they might have previously commanded. The forced seller (due to a dire need to move, financial hardship, etc.) usually experiences a large drop in their house price compared to higher offers not so long ago. The media tends to report on these types of sales as it makes for interesting reading. However, forced sellers comprise a very small percentage of home sellers and are by no means representative of the norm.

Most homeowners who intend to sell do not presently feel pressured to do so. They are willing to lower their price by a modest amount, but are also prepared to wait for what they consider to be the right price. We think that some potential sellers, knowing that the housing market has softened, have decided to extend residence for another year or two, in hopes of finding a more friendly market at that time. Hence, we believe that this inefficiency will prevent the housing market from cracking and completely undermining economic growth.

There has also been extensive literature over the last few years about the use of adjustable-rate mortgages ("ARMs") in home buying by less financially strong borrowers. ARMs usually have a fixed interest rate for a specified length of time, after which there are periodic rate adjustments. These adjustments are based on the trading levels of certain key market interest rates. The rate during the fixed period can be a very low rate, usually referred to as a "teaser" rate. These teaser rates are low enough to induce a buyer to purchase a higher-priced house. Some observers argue that when the fixed periods for ARMs end, ensuing adjustable rates will increase dramatically. Thereafter, monthly mortgage payments will rise so high that defaults will skyrocket, ultimately leading to a crash in the housing market.

We are unconvinced that such a scenario will fully materialize. Given the current low unemployment levels, we think that homeowners with ARMs would likely be able to meet their mortgage payments. One tactic would be to refinance into a new

Julius Baer Funds 2006 Annual Report

17

ARM with a different teaser rate. Demand for mortgage-backed securities ("MBS") based upon these types of ARMs remains strong from pension funds, insurance companies and hedge funds. Another option for these homeowners is to refinance into a traditional thirty-year fixed mortgage. Against a backdrop of the currently inverted yield curve, it is still a good time to have a fixed rate mortgage with predetermined payment amounts. Thus, we do not subscribe to an impending doomsday outcome for the housing market. However, we do expect that certain homeowners with ARMs will encounter difficulty in making payments, especially those who are unemployed in a stagnant or declining local real estate market.

To summarize our outlook on the housing market, while we expect the current slowdown to detract from GDP, we do not foresee the entire U.S. economy stalling in the near future as a result. Certain local markets that have become overbought and overdeveloped will probably correct significantly. This will be most apparent in markets where rampant speculation occurred. Housing prices may remain soft until the rest of the economy grows enough to continue the gains of the white-hot housing market of the last five years. This could take effect in a few quarters or a few years. Nonetheless, we are confident that housing softness will not be a crushing problem for the U.S. economy over the next few quarters.

Within the investment universe, we continue to believe that the U.S. dollar remains in a long term bear market. The nation's Current Account ("CA") deficit, based on the most recent data available, was at an $874 billion annual rate in the second quarter of 2006. This means the U.S. economy has to attract about $2.4 billion per day in order for the dollar not to lose value. To put this in perspective, a cautionary sign for investors considering exposure to fixed income emerging markets is that the CA deficit to GDP ratio should not exceed 6%. Based on the most recent data available, the CA deficit to GDP ratio for the U.S. stands at 6.6%.

For the U.S. trade deficit—the biggest component of the Current Account deficit—to decrease, there must be a fall in imports and/or a rise in exports. A viable way for this to take place would be for the U.S., as a nation, to save more and scale back imports. The trade deficit would further improve if foreigners, especially in the heavily export-based Far East, lowered their high savings rates and boosted consumption of U.S. imports. Of course, there are downsides to this scenario. A drop in U.S. consumption would adversely affect local businesses, as our economy is consumption driven. An additional problem is that even if there is an increase in foreign consumption of U.S. products, the U.S. economy is far more service than manufacturing-oriented. Many of these services are not easily translatable into foreign sales. Also, higher savings and less consumption of foreign goods by the U.S. consumer require changes in behavior. We thi nk that such behavioral changes are unlikely to happen without a major shift in government policy or the economy itself mandating the change.

Julius Baer Funds 2006 Annual Report

18

A separate school of thought stipulates that the U.S. should impose trade restrictions on foreign goods to protect domestic manufacturers. This might benefit some domestic firms but may also incur retaliatory barriers from trading partners. If protectionism triggers a shrinking in global trade, it may become problematic for the U.S., which is considered a trading leader on the world market, to attract foreign capital. Another view is that the U.S. government should try to bring about a currency devaluation, by using either verbal or actual currency intervention. A risk to this plan is that the government may be perceived as overly activist and the U.S. dollar could lose its status as the global reserve currency. The costs to the U.S. in this scenario could be high, as commodities may cease to be priced versus the U.S. dollar, interest rates may climb as the "risk" of investing in the U.S. would rise, and equity values would most likely decli ne.

An additional concern would be how foreign investors react if the reserve status was lost. If a foreign pension fund or insurance company currently holds, for example, 30% of its investments in the U.S. dollar, it would be considered a low risk position, so 30% would be justifiable. If the risk posed by the U.S. increased, even only in perception, then 30% may be too high an allocation. At the same time, if foreigners believed that they needed to exit a large portion of their U.S. assets, it may result in major problems for the worldwide financial system.

We believe that some combination of the above scenarios may transpire in such a way that the U.S. dollar could continue to lose value over the long term. If this is indeed the outcome, we hope it is a slow process thereby enabling markets to adjust without major disruptions. We believe our strategy of allocating between 0% and 40% in non-U.S. dollar currencies, with a natural habitat around 20%, is a way for U.S. fixed income investors to take advantage of this trend while minimizing currency risk.

In the fixed income markets, we continue to strive to find value in both domestic and international markets. In the U.S. market, we are encountering considerable challenges in finding value at the long end of the Treasury curve. We struggle to find value in 10-year bonds, amid a Federal funds rate of 5.25% (the short end of the yield curve) versus yields of around 4.6% for the 10-year Treasury note (the long end of the yield curve). Though the U.S. economy is clearly showing signs of wobbling, we expect GDP growth to muddle through around the 2.0% level in 2007. We also think that the Fed is committed to restraining inflation. In light of the new Fed chairman's stated intention to target inflation, we believe this Fed—with Mr. Bernanke at the helm—is more likely to be hawkish than it was under Mr. Greenspan. Accordingly, we do not expect the Fed funds rate to dip in the next few months. We think there are better ways to invest in t he U.S. fixed income market than through the long end of the Treasury curve, and we intend to focus on the spread sectors of the market in this capacity.

In the corporate bond sector, we plan to continue to be conservative in our positioning. Beyond the overall credit metrics that are fundamental to buying any corporate bond, we are concerned about the non-quantitative threats of leveraged

Julius Baer Funds 2006 Annual Report

19

buyouts ("LBOs") and mergers and acquisitions ("M&As"). Most shareholders welcome news of a company they have a stake in that is "in play." In contrast, bondholders are terrified of this scenario, due to the likelihood of new management taking on additional debt. Increased debt usually results in a deterioration of the company's credit metrics as well as multi-notch downgrades. As a result, bond values of such companies can tumble by 20% or more. Our approach is to avoid companies that may be perceived as targets of LBOs or M&As. Instead, we prefer to invest in companies whose high market value or capital structure renders them unlikely targets. If corporate bond spreads widen over the next year, we will reevaluate this conservatism as the risk/reward trade-off changes.

Going forward, we look to hold an ample position in mortgaged-backed securities. MBS offer value when the yield curve is not undergoing dramatic changes in shape and interest rates are stable or range bound. As we expect the U.S. economy to muddle through, we think the added yield that is inherent in MBS will enhance our ability to outperform over the next several months.

In conclusion, we believe that our defensive strategy for the Fund should produce higher returns than the benchmark over the long term, aided by our ability to capitalize on opportunities outside of the U.S. as well as our strategic allocations in the fixed income spread sectors.

Donald Quigley

Total Return Bond Fund Portfolio Manager

Past performance does not guarantee future results.

Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer term debt securities. Investing internationally involves additional risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The views expressed are subject to change based on market and other conditions. Furthermore, the opinions expressed do not constitute investment advice or recommendation by the individuals, JBIM, the funds, or any affiliated company.

The Lehman Brothers U.S. Aggregate Bond Index is a benchmark index composed of U.S. securities in Treasury, Government-Related, Corporate, and Securitized sectors. It includes securities that are of investment-grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $250 million. It is not possible to invest directly in an index or average.

Please see the Schedule of Investments in this report for complete fund holdings. Fund holdings and/or sector weightings are subject to change at any time and are not recommendations to buy or sell any security mentioned.

Julius Baer Funds 2006 Annual Report

20

MANAGEMENT'S COMMENTARY

JULIUS BAER GLOBAL HIGH INCOME FUND

Annual Report

Period Ending October 31, 2006

The Julius Baer Global High Income Fund (the "Fund") completed another successful fiscal year in October, turning in a total return of 10.49% (Class A Shares). The year was paced by U.S. economic growth that ran at close to 3%, a somewhat more muted growth rate in Europe, and robust emerging economies, powered by Chinese growth and booming commodity markets. These developments continued trends that were in place for several years. They provided a healthy fundamental backdrop for global markets, which were tempered by U.S. Federal Reserve Bank tightening until the summer, concerns about the affects of rising energy prices, and mounting speculation over how the U.S. housing boom might end.

In this environment, high income securities of all types performed very well, again, defying the prognostications of much of the financial press and a substantial portion of the investing community. Our benchmark, the Merrill Lynch Global High Yield Constrained Index, returned 10.64%. The global credit foundation was strong. Global growth and ample liquidity helped issuers increase their revenues and execute productivity enhancing restructurings which improved margins and cash flow. Emerging sovereigns and corporations benefited from strong export demand, sounder fiscal policies, and improved currency and debt management. Investors met this credit environment with strong demand for issuers of high income securities. Only for a brief period in April and May did investors show any real hesitation. This pause in demand was sparked by concerns that the U.S. Federal Reserve Bank might increase interest rates too much or for too long. The speculat ion sparked a "risk aversion" trade that was more pronounced in energy and commodity-related securities, whose values were extended the most during the preceding years.

Within the global market for high income securities, there were some sectors that fared better than others. U.S. high yield outperformed European high yield as the credit impact of improved fundamentals offset the effects of an increasing interest rate environment. Auto and auto parts bonds both in the U.S. and Europe outperformed the general market, although there was a very wide dispersion of returns within the group. Airline bonds, much maligned in the past, were extremely strong performers. Healthcare bonds, meanwhile, one of the better performers last year, underperformed the market this year. Homebuilders also underperformed, although not until the later part of the period. In general, lower quality bonds (CCC rated and lower) outperformed higher quality bonds. This outperformance of issuers with the lowest margins of cash flow is unusual at this stage in the cycle. Emerging market bonds continued their multi-year run of strong returns , both in

Julius Baer Funds 2006 Annual Report

21

local currency and in hard currency markets. Following the "risk aversion" ripple during April and May, however, bonds of emerging market countries sporting substantial current account deficits tended to lag.

The performance of the Fund (Class A Shares) during this period placed it in the top 16% of high yield bond funds, as measured by Morningstar, Inc. (for the twelve months ending October 31, 2006, the Class A Shares ranked 84 out of 544 high yield bond funds based on total return). In addition to the strength of the overall market, the Fund's performance was enhanced by our positions in the local currency government and money market instruments of several emerging countries including Brazil, Columbia, and Indonesia. Our positions in several large emerging market corporates, such as Norilsk Nickel and CSN also bolstered returns. The Fund built several positions during the year in select auto and auto parts issuers that we believe will ultimately benefit from the on-going restructuring of the industry. Although volatile, these positions on balance helped the Fund's relative return. In a similar manner, we also benefited from positions in the ai rline sector including both defaulted securities and more senior, secured Equipment Trust Certificates.

These positive contributors to performance were somewhat offset during the year by other factors. Although we carried approximately a market weight in more risky CCC bonds for much of the period, we were not particularly aggressive about our issue selection in this area. Our discipline tended to keep us away from CCC issuers dependent on unpredictable events and led us to invest more in smaller CCC issuers that we believe are fundamentally under-rated. The Fund also had a very low representation of hard currency (Euro and U.S. dollar denominated) emerging market bonds, which continued to perform well during the period. Towards the end of the fiscal year, U.S. interest rates declined, benefiting more interest rate sensitive BB bonds in which the Fund was somewhat underweight.

While a number of different high income markets and security types both added and detracted from overall performance, we were careful not to let any one market dominate the Fund's returns, either negatively or positively. This balanced diversification across different geographies and security types forms a cornerstone of our investment philosophy, and we believe it should continue to help the Fund navigate the markets successfully.

As we enter the new fiscal year, the economic fundamentals and the market backdrop continue to be supportive of high income securities globally. Although we expect growth in North America will slow in the coming quarters, we do not expect outright recession. More importantly, we believe global growth will remain strong. Issuers of sovereign and corporate bonds should be able to continue the process of operational and cash flow improvement that has been in place now for several years. As always, even in a generally improving economy, there will be issuers that will become overextended, whole industries that will need to restructure, and difficult periods. Overall, however, we are constructive on the year ahead.

Julius Baer Funds 2006 Annual Report

22

The risks in our outlook still rest in the process of global trade, monetary and currency rebalancing that is required to incorporate China, India, Eastern Europe and other emerging countries into the global economic system. As long as this development continues in a relatively smooth manner, all markets, including the high income security markets, in particular, should benefit. We will be watchful, however, for central bank missteps, political events, and supply imbalances that might disrupt this process.

Greg Hopper

Global High Income Fund Portfolio Manager

Past performance does not guarantee future results.

The securities in which the Fund will invest may be considered more speculative in nature and are sometimes known as "junk bonds." These securities tend to offer higher yields than higher rated securities fixed income securities can present a greater risk of loss of income and principal than higher rated securities. Investing internationally involves additional risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The views expressed are subject to change based on market and other conditions. Furthermore, the opinions expressed do not constitute investment advice or recommendation by the individuals, JBIM, the funds, or any affiliated company.

The Merrill Lynch Global High Yield Constrained Index tracks the performance of below investment grade bonds of corporate issuers domiciled in countries having an investment grade foreign currency long term debt rating (based on a composite of Moody's and S&P). The index is weighted by outstanding issuance, but constrained such that the percentage that any one issuer may not represent more than 3% of the index. It is not possible to invest in an index.

Please see the Schedule of Investments in this report for complete fund holdings. Fund holdings and/or sector weightings are subject to change at any time and are not recommendations to buy or sell any security mentioned.

Cash flow: measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Morningstar Rankings represent a fund's total-return percentile rank relative to all funds that have the same Morningstar Category. The highest percentile rank is 1 and the lowest is 100. It is based on Morningstar total return, which includes both income and capital gains or losses and is not adjusted for sales charges or redemption fees.

Julius Baer Funds 2006 Annual Report

23

MANAGEMENT'S COMMENTARY

JULIUS BAER U.S. MICROCAP FUND

JULIUS BAER U.S. SMALLCAP FUND

JULIUS BAER U.S. MIDCAP FUND

JULIUS BAER U.S. MULTICAP FUND

Annual Report

Period Ending October 31, 2006

Equity Market Commentary

Equity markets were up sharply from the date of the launch of our four new funds on July 24, 2006, through October 31, 2006, with the Russell 2000 Index up 11.39% and the S&P 500 up 9.82%. Following a sharp correction in July, technology stocks rebounded through August and September to lead the rally. This can be attributed to a positive outlook for technology investment spending in both the seasonally strong fourth quarter period and a favorable outlook for 2007. Many corporate balance sheets have record cash levels and managers are under pressure by shareholders and the forces of an increasingly competitive global arena to begin investing capital into higher return propositions, rather than settling for current money-market rates of return. Technology spending continues to be an important part of capital spending, representing about 34% of the total. On the consumer front, spending held steady in 2006, and consumer discretionary stocks also performed well in the review period. Despite facing higher interest rates and greater costs for gasoline and home heating fuel, U.S. consumers continued to robustly purchase goods and services. On the bright side, gasoline prices declined significantly in October and it's been more than a year now since prices began moving sharply higher—consumers have had time to adjust to the higher fuel prices and have economized by optimizing trips and purchasing more fuel-efficient vehicles. With the significant increase in fuel prices that began in mid-2005, many pundits predicted a decline in consumer spending. Our belief is that if reduction occurs, it will be a temporary phenomenon and that consumer expenditures may be actually shifting away from the new housing market into home refurbishment, consumer electronics, clothing and dining out.

Portfolio Strategy and Investment Focus Areas

With smaller U.S. company stocks and indices having performed well for several years in a row versus their larger counterparts, there has been much debate as to when the current cycle of smallcap out-performance will end. Given the concentrated nature of the four funds under review, we are less concerned about the smallcap vs. largecap cycle debate, and more concerned about picking stocks that have the potential to outperform in both favorable and unfavorable equity market environments. To achieve this, we consistently seek out investment opportunities that are characterized by having a product or service that favorably changes consumption behavior. For example,

Julius Baer Funds 2006 Annual Report

24

equity markets earlier in the year were discounting a fairly significant slowdown in spending for the casual dining industry—many casual dining stocks declined markedly in price. Our view is that U.S. consumers changed their behavior significantly over the last several years and are dining out more often and spending more discretionary income to do so. Our belief is that consumers will continue on this course despite a modest decline in foot traffic that may have occurred in the short-run due to higher gasoline prices and rising interest rates. We believe the change in behavior to dining out will be long-lasting and will also benefit from population growth as well as other favorable demographic trends, including income growth and the aging of the "baby boomer" generation. As a result, we initiated our funds with an overweight position in the casual dining industry.

In terms of portfolio positioning, we are constructive on technology and remain overweight the sector as corporations invest in technology spending to upgrade aging computer systems. The last major upgrade cycle that occurred for computer systems in the corporate setting was in the 1998-2001 time frame. Typically, this type of capital equipment is replaced every five to seven years, so our analysis leads us to believe the installed base of technology had aged and spending should improve nicely. In addition, corporate managers are under increasing pressure to deploy ever-growing cash balances and boost productivity. As we look forward into 2007, we expect the market for financial services, primarily retail and commercial banking and asset management, to be favorable. This is attributable to income growth, high employment levels and low absolute interest rate levels. From a long term perspective, we also believe the healthcare sector is attrac tive due to aging demographics and growth in demand for aesthetic procedures, as a result of medical advances. We have a strong belief that in the next decade there will be many changes to the entire healthcare system in the U.S. that will offer companies the ability to gain market share as well as create new market opportunities. Some interesting investment areas on this front include the aforementioned aesthetic procedures such as laser applications, changes to how medical records are managed and maintained, and technological advances in non-invasive surgical procedures.

Julius Baer U.S. Microcap Fund

For the period from inception on July 24 through October 31, 2006 the U.S. Microcap Fund returned 12.60%, which outperformed the Russell 2000 Index return of 11.39% and the Russell Microcap Index return of 11.37%.

Outperformance versus the Russell 2000 benchmark was driven by our stock selection. In particular, our consumer discretionary, financial services and technology holdings performed well, which more than offset unfavorable relative stock performance in the energy and materials sectors. Our sector positioning had a modest negative impact

Julius Baer Funds 2006 Annual Report

25

to performance. In terms of portfolio positioning, the Fund is overweight in the technology and healthcare sectors and underweight in the utilities and materials sectors.

Julius Baer U.S. Smallcap Fund

For the period from inception on July 24 through October 31, 2006 the U.S. Smallcap Fund returned 11.00%, which underperformed the Russell 2000 Index return of 11.39%.

The Fund's modest underperformance relative to its benchmark, the Russell 2000, can be attributed to poor performance within the healthcare and energy sectors, which was mostly offset by strong performance within the technology and financials sectors. Our sector positioning had a modest negative impact to performance. In terms of portfolio positioning, the Fund is overweight in the technology, consumer and healthcare sectors and underweight in the industrials, utilities and telecommunications sectors.

Julius Baer U.S. Midcap Fund

For the period from inception on July 24 through October 31, 2006 the U.S. Midcap Fund returned 10.50%, which outperformed the Russell Midcap Index return of 9.84%.

Outperformance versus the Russell Midcap benchmark was driven by our stock selection. In particular, our technology, consumer discretionary and utilities holdings performed well, which more than offset unfavorable relative stock performance in the healthcare and energy sectors. Our sector positioning had a modest positive impact to performance. In terms of portfolio positioning, the Fund is overweight in the technology and health care sectors and underweight in the utilities and materials sectors.

Julius Baer U.S. Multicap Fund

For the period from inception on July 24 through October 31, 2006 the U.S. Multicap Fund returned 11.00%, which outperformed the Russell 3000 Index return of 9.95%.

Outperformance versus the Russell 3000 benchmark was driven by our stock selection. In particular, our technology and consumer discretionary sector holdings performed well, which more than offset unfavorable relative stock performance in the financials and industrials sectors. Our sector positioning had a modest positive impact to performance. In terms of portfolio positioning, the Fund is overweight in the technology and health care sectors and underweight in the utilities and materials sectors.

Julius Baer Funds 2006 Annual Report

26

In summary, we are in the business of discovering and investing in companies whose stock market values increase with the improvements and success of their respective businesses. We are excited about the collective potential of our portfolio holdings and the tremendous investment opportunities that abound.

Samuel Dedio

U.S. Microcap Fund, U.S. Smallcap Fund, U.S. Midcap Fund and U.S. Multicap Fund Portfolio Manager

Past performance does not guarantee future results.

Please refer to the prospectus for more complete information on the special risks associated with investing in the Julius Baer U.S. Equity Funds, including, but not limited to: stock market risk, smaller companies risk, liquidity risk, foreign investment risk, derivatives risk.

The views expressed are subject to change based on market and other conditions. Furthermore, the opinions expressed do not constitute investment advice or recommendation by the individuals, JBIM, the funds, or any affiliated company.

Please see the Schedule of Investments in this report for complete fund holdings. Fund holdings and/or sector weightings are subject to change at any time and are not recommendations to buy or sell any security mentioned.

The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market, with all values expressed in U.S. dollars.

The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index, which represent approximately 25% of the total market capitalization of the Russell 1000 Index, with all values expressed in U.S. dollars.

The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index, with all values expressed in U.S. dollars.

Julius Baer Funds 2006 Annual Report

27

SHAREHOLDER EXPENSES (Unaudited)

As a stockholder of the Julius Baer Global Equity Fund, or a shareholder of Julius Baer International Equity Fund, Julius Baer International Equity II Fund, Julius Baer Total Return Bond Fund, Julius Baer Global High Income Fund, Julius Baer U.S. Microcap Fund, Julius Baer U.S. Smallcap Fund, Julius Baer U.S. Midcap Fund or Julius Baer U.S. Multicap Fund, you incur ongoing expenses, such as management fees, shareholder service fees, distribution fees and other fund expenses. The following table is intended to help you understand your ongoing expenses (in dollars and cents) of investing in Julius Baer Global Equity Fund, Julius Baer International Equity Fund, Julius Baer International Equity Fund II, Julius Baer Total Return Bond Fund, Julius Baer Global High Income Fund, Julius Baer U.S. Microcap Fund, Julius Baer U.S. Smallcap Fund, Julius Baer U.S. Midcap Fund or Julius Baer U.S. Multicap Fund and to compare these expenses with the ongoing expenses of investing in other funds.

The table is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from May 1, 2006 to October 31, 2006.

Actual Expenses

The first line in the table below provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for the Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line in the table below provides information about the hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account value and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Julius Baer Funds 2006 Annual Report

28

Global Equity Fund Class A

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,021.70 | | | | 1.40 | % | | $ | 7.13 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,018.10 | | | | 1.40 | % | | $ | 7.12 | | |

Global Equity Fund Class I

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,021.70 | | | | 1.15 | % | | $ | 5.86 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,019.40 | | | | 1.15 | % | | $ | 5.85 | | |

International Equity Fund Class A

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,018.00 | | | | 1.16 | % | | $ | 5.90 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,019.40 | | | | 1.16 | % | | $ | 5.90 | | |

International Equity Fund Class I

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,019.20 | | | | 0.92 | % | | $ | 4.68 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,020.60 | | | | 0.92 | % | | $ | 4.69 | | |

International Equity Fund II Class A

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,011.50 | | | | 1.32 | % | | $ | 6.64 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,018.60 | | | | 1.32 | % | | $ | 6.67 | | |

International Equity Fund II Class I

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,013.60 | | | | 1.05 | % | | $ | 5.28 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,020.00 | | | | 1.05 | % | | $ | 5.30 | | |

Total Return Bond Fund Class A

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,040.30 | | | | 0.69 | % | | $ | 3.55 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.70 | | | | 0.69 | % | | $ | 3.52 | | |

Total Return Bond Fund Class I

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,040.50 | | | | 0.44 | % | | $ | 2.26 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,023.00 | | | | 0.44 | % | | $ | 2.24 | | |

Julius Baer Funds 2006 Annual Report

29

Global High Income Fund Class A

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,037.80 | | | | 1.07 | % | | $ | 5.14 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,020.20 | | | | 1.07 | % | | $ | 5.09 | | |

Global High Income Fund Class I

| | | Beginning Account

Value 05/01/06 | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,039.20 | | | | 0.79 | % | | $ | 3.91 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.40 | | | | 0.79 | % | | $ | 3.87 | | |

U.S. Microcap Fund Class A

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,126.00 | | | | 0.97 | % | | $ | 5.19 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,020.30 | | | | 0.97 | % | | $ | 4.94 | | |

U.S. Microcap Fund Class I

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,126.00 | | | | 0.81 | % | | $ | 4.32 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.10 | | | | 0.81 | % | | $ | 4.13 | | |

U.S. Smallcap Fund Class A

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,110.00 | | | | 0.81 | % | | $ | 4.29 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.10 | | | | 0.81 | % | | $ | 4.13 | | |

U.S. Smallcap Fund Class I

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,111.00 | | | | 0.65 | % | | $ | 3.44 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.90 | | | | 0.65 | % | | $ | 3.31 | | |

U.S. Midcap Fund Class A

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,105.00 | | | | 0.73 | % | | $ | 3.85 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.50 | | | | 0.73 | % | | $ | 3.72 | | |

U.S. Midcap Fund Class I

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,106.00 | | | | 0.56 | % | | $ | 3.00 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,022.40 | | | | 0.56 | % | | $ | 2.85 | | |

* Commencement of operations

Julius Baer Funds 2006 Annual Report

30

U.S. Multicap Fund Class A

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,110.00 | | | | 0.70 | % | | $ | 3.72 | | |

| Hypothetical | | $ | 1,000.00 | | | $ | 1,021.70 | | | | 0.70 | % | | $ | 3.57 | | |

U.S. Multicap Fund Class I

| | | Beginning Account

Value 07/24/06* | | Ending Account

Value 10/31/06 | | Annualized

Expense Ratio | | Expense Paid

during Period | |

| Actual | | $ | 1,000.00 | | | $ | 1,111.00 | | | | 0.54 | % | | $ | 2.86 | | |