UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number : 811-06113

The Caldwell & Orkin Funds, Inc.

(Exact name of registrant as specified in charter)

100 S. Ashley Drive, Suite 895

Tampa, Florida 33602

(Address of principal executive offices) (Zip code)

Derek Pilecki

100 S. Ashley Drive, Suite 895

Tampa, Florida 33602

(Name and address of agent for service)

Copies to:

Jesse Halle

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

Registrant’s telephone number, including area code: 1-813-282-7870

Date of fiscal year end: April 30

Date of reporting period: October 31, 2023

Item 1. Reports to Stockholders.

(a)

| Table of Contents | Caldwell & Orkin - Gator Capital Long/Short Fund |

| October 31, 2023 (Unaudited) | |

| Management’s Discussion of Fund Performance | 2 |

| | |

| Investment Results | 8 |

| | |

| Fund Holdings | 9 |

| | |

| Schedule of Investments | 10 |

| | |

| Schedule of Securities Sold Short | 13 |

| | |

| Statement of Assets and Liabilities | 16 |

| | |

| Statement of Operations | 17 |

| | |

| Statements of Changes in Net Assets | 18 |

| | |

| Financial Highlights | 19 |

| | |

| Notes to Financial Statements | 20 |

| | |

| Disclosure of Fund Expenses | 27 |

| | |

| Director Approval of the Investment Advisory Agreement | 28 |

| | |

| Privacy Policy Disclosure | 30 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

December 19. 2023

Dear Fellow Shareholder:

The Caldwell & Orkin – Gator Capital Long/Short Fund (the “Fund”) increased 5.68% over the six-month period ending on October 31, 2023. The S&P 500 Total Return Index (“S&P 500”) increased 1.39% during the same period. For the 12-month period ending October 31, 2023, the Fund increased 15.86% while the S&P 500 increased 10.14%.

Past performance is no guarantee of future results.

Management Discussion and Analysis

The Fund outperformed the S&P 500 during the first half of fiscal year 2023. The Fund’s long exposure to Financial stocks and short exposure to Financial stocks were the main drivers of performance.

The top five equity contributors during the first half of fiscal year 2023 were First Citizens Bancshares, Inc. (long), Pinnacle Financial Partners Inc. (long), Hingham Institution for Savings (short), Capitol Federal Financial (short), and Meta Platforms Inc. (long).

The top five equity detractors during the first half of fiscal year 2023 were Progressive Corp. (short), Barclays PLC (long), Empire State Realty Trust Inc. (short), Anywhere Real Estate Inc. (long), and Warner Bros. Discovery Inc. (long).

We ended the first half of the 2023 fiscal year with gross long exposure of 89% and gross short exposure of 36% for a total gross exposure of 125% and a net exposure of 53%.

First Citizens Bancshares (NASDAQ: FCNCA)

One of the Fund’s largest positions is First Citizens Bancshares (“First Citizens” or “FCNCA”). We acquired our stake over the past three years. Initially, we owned and traded around a small position in CIT Group Inc. (“CIT”) during the summer of 2020. We felt CIT was undervalued and management was making progress in reducing risk during the Covid-19 pandemic. In late 2020, CIT agreed to be acquired by First Citizens. We added to our CIT stake the morning of the acquisition announcement because we thought the acquisition was so financially attractive that First Citizens’ shares would rally and pull CIT’s shares higher. Our CIT shares were exchanged for First Citizens shares when the merger completed. We held onto our First Citizens shares because we admired the management team, we felt the bank was undervalued, and we projected the bank would benefit from higher interest rates. Then, earlier this year, First Citizens was the winning bidder in the FDIC’s auction of the failed Silicon Valley Bank (“SVB”). We added significantly to the Fund’s First Citizens position on the following Monday morning because the deal was unbelievably favorable for First Citizens.

First Citizens’s stock price rose more than 50% that day and has risen another 40% in the months since the SVB acquisition. We have not sold any shares. We believe the stock still has the potential to double over the next three years. Despite this attractive upside, we think the downside is minimal. Our downside scenario is an unchanged stock price in three years.

| 2 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

Here is our detailed investment thesis for First Citizens:

FCNCA trades at a discount to other large regional banks on a Price-to-Tangible Book value (“P/TBV”) basis. It also trades at a slight discount on a Price-to-Earnings (“P/E”) basis looking at sell-side 2024 earnings estimates (see chart below).

| | | 12/19 | | | | 2024 | | |

| Ticker | | Price | | Mkt Cap | | Est P/E | | P/TB |

| USB | | 30.64 | | 68.4 | | 10.8 | | 2.19 |

| PNC | | 111.24 | | 61.5 | | 12.4 | | 1.97 |

| TFC | | 27.62 | | 48.6 | | 10.5 | | 1.95 |

| FITB | | 22.89 | | 23.9 | | 10.9 | | 2.55 |

| MTB | | 108.94 | | 22.9 | | 9.4 | | 1.33 |

| HBAN | | 9.44 | | 18.5 | | 10.4 | | 1.78 |

| RF | | 14.01 | | 18.0 | | 9.8 | | 2.16 |

| FCNCA | | 1348.52 | | 20.6 | | 7.6 | | 1.10 |

| Median | | | | | | 10.5 | | 1.96 |

| Source: Bloomberg | | | | | | | | |

Usually when a bank trades at a discount to peers on a P/TBV basis, it is because it has lower returns than peers. At first glance this appears to be the case with First Citizens. It is projected to earn a 14% Return on Equity (“ROE”) in 2024 where its peers are projected to earn higher ROEs. However, when we adjust for the excess capital that First Citizens is holding, we believe it has a ROE similar to its peers and does not deserve to trade at a discount.

We believe there are other possible reasons why First Citizens trades at a discount to its peers. The main reason is it is not a member of the S&P 500 Index, so it does not have the demand from passive index investors. Other minor reasons for First Citizens’ valuation discount are a lack of familiarity within the investment community due to limited but growing sell-side coverage, not hosting quarterly earnings conferences calls until recently, not attending brokerage investment conferences, high nominal stock price and limited trading volume, and a low dividend compared to peers.

One additional unusual reason for the valuation discount is the dual-class share structure of First Citizens Bank. The Holding family controls the Class B voting shares. This dual-class structure may discourage some investors from owning the stock. We disagree with this thinking. First, the Holding family has demonstrated an extraordinary commitment to shareholder returns. First Citizens is the best performing stock of its peer group over the last 30 years. We view the Holding family as owner-operators. We note that many of the best performing stocks have had owner-operators: Berkshire, Microsoft, Amazon, etc. There is data that proves companies with owner-operators outperform because management is able to focus on long-term value creation. We think this applies to the Holding family controlling First Citizens.

| Semi-Annual Report | October 31, 2023 | 3 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

Another criticism of the dual-class share structure is the difficulty in applying outside pressure to gain voting control and/or board seats. I believe this is a non-issue for banks. The difficulty of a hostile takeover in banking is high. There hasn’t been a successful hostile takeover of a bank since Bank of New York acquired Irving Trust in 1988. Plus, the regulators limit ownership levels of banks before an investor has to register as a Financial Holding Company. Overall, we see the First Citizens dual-class share structure as a non-issue.

First Citizens’ stock outperformance in 2023 may be distracting some investors from the potential returns still offered by the stock. First Citizens’ stock has returned 78% this year. Its peers have had negative returns between 20% and 35% this year. We know it is natural for investors to say, “We missed it,” when a stock has performed like First Citizens’ stock has. The last thing these investors want is to buy First Citizens after the run and have it underperform once they buy it. In other words, they don’t want to be wrong twice on the stock. As we will discuss below, we believe there is significant downside protection in First Citizens because of the defensive nature of its balance sheet.

First Citizens has a very liquid balance sheet, which is perfect for the current environment. For example, First Citizens has 17.6% of its assets in cash compared to Truist at 5.6%. This liquid balance sheet gives First Citizens plenty of opportunity to take advantage of the wider loan spreads available in the current environment. The extra liquidity also reduces pressure to pay up for deposits. The high cash balance is the best indication that shareholders have a measure of protection from First Citizens’ balance sheet.

First Citizens’ balance sheet is defensive and well-positioned for growth. The bank has almost no borrowings beyond the $35 billion FDIC note that has a five year term. First Citizens’ management did not invest in long-dated fixed rate securities, so unlike many other banks, it is not carrying a portfolio of underwater bonds. Also, First Citizens loan book is balanced between floating-rate and fixed-rate loans. This balance was created through the strategic acquisitions of CIT and SVB. The CIT franchise produced excess loans and the legacy SVB franchise produced excess deposits. We believe First Citizens is positioned well for the current consensus outlook for rates of “Higher for Longer”.

Investors are not assuming any growth at First Citizens based on its stock price trading just above tangible book value. Based on sell-side models, expectations are for minimal growth in First Citizens’s legacy banking operations and that SVB will shrink going forward. We think this is wrong because we think prospects for the former SVB operations are strong. Certainly, the SVB franchise is diminished as several business development personnel have been poached by competitors. We think multiple competitors are targeting the venture capital community.

The current environment in the venture capital community is not ideal, but SVB was a powerful growth franchise. To offset these concerns, we note that the current deposit balances at SVB are already down close to 80% from year-end levels. So, we believe customers who want to leave SVB have already left. Also, we believe there is substantial goodwill within the venture capital community for SVB. SVB is intertwined with the venture community and continues to have strong relationships with the community. Lastly, we believe venture capital as an industry

| 4 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

will grow faster than the overall economy. We think there is a good chance that SVB will continue to grow under First Citizens ownership. At the current valuation, we view this growth potential as a free option.

Regional banks as a group may re-rate higher. In addition to First Citizens trading at a discount to peer large regional banks, we believe regional banks trade at the low end of their historical valuations. Large regional banks trade for about 7.4x 2024 EPS estimates, we believe the normal valuation for this group is between 10x and 14x. We understand that at this point in the cycle banks should trade cheap, but time marches on and cycles can change quickly. We expect the group multiple to re-rate higher as the industry works through higher interest rates and the credit cycle peaks.

We do see some risks to our First Citizens investment thesis:

Aggressive rate cuts by the Fed. First Citizens is among the most asset-sensitive of the large regional banks. If the Federal Reserve were to aggressively cut short-term interest rates in response to weak economic conditions, this would hurt First Citizens’s earnings. We think this scenario is unlikely given the recent bout of inflation that the Federal Reserve has been battling and the Fed’s “Higher For Longer” mantra.

Continued calls for increase capital requirements for banks. Bank regulators continue to make statements that banks need higher capital requirements. While we disagree with this sentiment, we acknowledge the potential reduction in returns for bank investors with higher capital requirements. We do believe First Citizens is well-positioned to comply with higher capital requirements due its excess capital position. We would expect First Citizens’ management to operate the bank with a significant capital cushion.

First Citizens may be over-earning in the near-term. First Citizens is experiencing two temporary benefits to earnings. One, as part of the SVB acquisition, First Citizens issued a 5-year note to the FDIC for a below market interest rate of 3.5%. Two, First Citizens marked-to-market the SVB loan portfolio at a discount to account for credit risk. As the old SVB loans payoff, First Citizens recognizes the discount into income. Both of these factors are causing First Citizens to over-earn in the near-term.

First Citizens is facing significant integration risks with the SVB deal. The SVB acquisition was a large deal. SVB was a complex bank in a new business line. Multiple competitors are poaching SVB personnel. The SVB customer base went through a traumatic event in March as it was uncertain whether they would lose their deposits in the SVB failure. We worry about the integration risks that First Citizens faces with SVB. But, we are reassured that First Citizens has significant experience integrating complex and geographically disperse acquisitions.

Future M&A deals are unlikely to create as much value for First Citizens as the SVB deal did. Going forward the opportunity for value creating acquisitions is less likely now that the bank is much bigger than it was 15 years ago or even earlier this year. First Citizens has a successful M&A track record that includes a number of FDIC deals as well as the heavily discounted acquisition of CIT Group. The SVB acquisition was a monster deal that doubled First Citizens’ capital. While the opportunity for future FDIC deals is diminished, we believe the FDIC is happy

| Semi-Annual Report | October 31, 2023 | 5 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

to have another bidder besides JP Morgan Chase for large deals. We have been surprised about the lack of outcry over the extraordinary deal First Citizens got in buying SVB. We think the SVB deal clearly shows the FDIC executives are comfortable with First Citizens management team.

Quantitative Tightening effect on banking industry deposit balances. Even though Federal Reserve’s Federal Open Market Committee seems close to the end of this interest rate tightening cycle, they continue to implement Quantitative Tightening by allowing the Fed’s portfolio of securities holdings to mature with limited reinvestment. Just as Quantitative Easing by the Fed accelerated deposit growth in the banking system, Quantitative Tightening is a strong headwind for deposit growth. SVB had some of the strongest deposit growth during Quantitative Easing, so we expect it will have deposit pressures with continued Quantitative Tightening. Of course, there are other factors that will influence legacy SVB’s deposit base such as: the strength of the venture capital cycle, competitive intensity from other banks attacking SVB’s old franchise, and SVB’s customer’s willingness to return to SVB under First Citizens’ ownership.

Legacy SVB’s business is dependent on the venture capital cycle and it does not look great in the short-term. Venture capital goes through cycles and it seems like late-2021 represented the peak of the latest cycle. The amount of venture capital raised in 2022 and 2023 is down significantly. There are many start-ups who have had to cut expenses and conserve capital. Venture capital exits are few and far between. Given the strength of the stock market in 2023, we are surprised the IPO market has not recovered. There is potential upside from excitement about artificial intelligence.

We think First Citizens is still an attractive holding despite its outperformance to date in 2023. We estimate First Citizens’ tangible book value will be $1,800 at the end of 2026. We think FCNCA can trade at 1.5x tangible book value at the end of 2026 or $2,700, which is double the current share price.

Conclusion

Thank you for entrusting us with a portion of your wealth. We are grateful for investors like you who believe and trust in our strategy. As always, we welcome the opportunity to speak with you and discuss the Fund.

Sincerely,

Derek S. Pilecki, CFA

Portfolio Manager

The discussion of individual companies should not be considered a recommendation of such companies by the Fund’s investment adviser.

| 6 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Management’s Discussion of Fund Performance |

| | October 31, 2023 (Unaudited) |

The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment returns and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please call 800-467-7903 or visit www.CaldwellOrkin.com for current month-end performance.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

Investors should consider the investment objective, risks, and charges and expenses of the Fund before investing. The prospectus and, the summary prospectus contains this and other information about the Fund and should be read carefully before investing. The prospectus may be obtained at Please call 800-467-7903 or visit www.CaldwellOrkin.com.

| Semi-Annual Report | October 31, 2023 | 7 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Investment Results |

| | October 31, 2023 (Unaudited) |

| | Average Annual Total Returns(a) as of October 31, 2023 | |

| | | Six Months | | One Year | | Three Year | | Five Year | | Ten Year | |

| | | | | | | | | | | | |

| | Caldwell & Orkin - Gator Capital Long/Short Fund | 5.68% | | 15.86% | | 18.99% | | 10.49% | | 4.92% | |

| | S&P 500® Total Return Index(b) | 1.39% | | 10.14% | | 10.36% | | 11.01% | | 11.18% | |

| | Eurekahedge Long Short Equities Hedge Fund Index(c) | (0.99)% | | 3.10% | | 4.52% | | 5.47% | | 5.33% | |

| | | | | | | | | | | | |

| | | |

| | Total annualized Fund operating expenses for the Caldwell & Orkin - Gator Capital Long/Short Fund (the “Fund”) was 3.14% as described in the Prospectus, dated August 28, 2023. This amount includes Acquired Fund Fees and Expenses, as well as interest and dividend expenses related to short sales, which if excluded would result in an annual operating expense rate of 2.00%. Additional information about the Fund’s current fees and expenses for the six months ended October 31, 2023 is contained in the Financial Highlights. | |

| (a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable period. If such fee reductions had not occurred, the quoted performance would have been lower. The table does not reflect the deduction of taxes. The Fund’s returns represent past performance and do not guarantee future results. Total returns for periods less than one year are not annualized. |

| (b) | The S&P 500® Total Return Index is a capitalization-weighted, unmanaged index of 500 large U.S. companies chosen for market capitalization, liquidity and industry group representation and includes reinvested dividends. You cannot invest directly in an index. |

| (c) | The Eurekahedge Long Short Equities Hedge Fund Index (“Eurekahedge Index”) is an unmanaged index comprised of long/short equity hedge funds. According to its sponsor, Eurekahedge Pte. Ltd., the Eurekahedge Index is an equally weighted index of 895 constituent funds designed to provide a broad measure of the performance of underlying hedge fund managers. The returns of the Eurekahedge Index do not include sales charges or fees, which would lower performance. You cannot invest directly in an index. |

You should consider the Fund’s investment objectives, risks, charges and expenses carefully before you invest. The Fund’s prospectus contains important information about the Fund’s investment objectives, potential risks, management fees, charges and expenses, and other information and should be read carefully before investing. You may obtain a current copy of the Fund’s prospectus or performance data current to the most recent month-end by calling (800) 467-7903.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

| 8 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

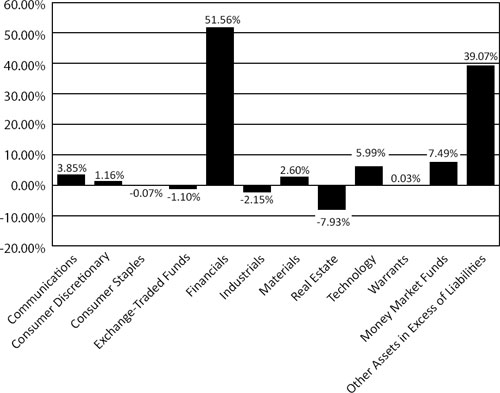

| Caldwell & Orkin - Gator Capital Long/Short Fund | Fund Holdings |

| | October 31, 2023 (Unaudited) |

Net Sector Exposure

October 31, 2023*

| * | Sector weightings are calculated as a percentage of net assets and include short positions. Portfolio holdings are subject to change. |

The Caldwell & Orkin - Gator Capital Long/Short Fund’s (the “Fund”) investment objective is to provide long-term capital growth with a short-term focus on capital preservation.

Availability of Portfolio Schedule – (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT, within sixty days after the end of the period. The Fund’s Form N-PORT reports are available at the SEC’s website at www.sec.gov and on the Fund’s website at www.gatorcapital.com.

| Semi-Annual Report | October 31, 2023 | 9 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Investments |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| COMMON STOCKS — LONG — 80.67% | | | | | | | | |

| Banks — 37.33% | | | | | | | | |

| Axos Financial, Inc.(a) | | | 17,500 | | | $ | 630,525 | |

| Banc of California, Inc. | | | 56,600 | | | | 634,486 | |

| Bridgewater Bancshares, Inc.(a) | | | 24,000 | | | | 231,120 | |

| Business First Bancshares, Inc. | | | 2,040 | | | | 39,862 | |

| ConnectOne Bancorp, Inc. | | | 14,142 | | | | 230,373 | |

| Dime Community Bancshares, Inc. | | | 7,063 | | | | 129,889 | |

| Financial Institutions, Inc. | | | 13,100 | | | | 207,504 | |

| First BanCorp. | | | 42,000 | | | | 560,700 | |

| First Business Financial Services, Inc. | | | 7,500 | | | | 230,250 | |

| First Citizens BancShares, Inc., Class A | | | 471 | | | | 650,329 | |

| First Internet Bancorp | | | 10,000 | | | | 163,700 | |

| Meridian Bancorp, Inc. | | | 12,688 | | | | 126,880 | |

| OFG Bancorp | | | 19,991 | | | | 592,133 | |

| Old Second Bancorp, Inc. | | | 43,900 | | | | 595,284 | |

| OP Bancorp(a) | | | 38,573 | | | | 325,942 | |

| Pinnacle Financial Partners, Inc. | | | 11,000 | | | | 685,960 | |

| UMB Financial Corp. | | | 15,000 | | | | 940,800 | |

| Webster Financial Corp. | | | 15,000 | | | | 569,550 | |

| Western Alliance Bancorp | | | 16,000 | | | | 657,600 | |

| Wintrust Financial Corp. | | | 5,101 | | | | 380,994 | |

| | | | | | | | 8,583,881 | |

| Casinos & Gaming — 1.68% | | | | | | | | |

| Las Vegas Sands Corp. | | | 6,000 | | | | 284,760 | |

| Melco Resorts & Entertainment Ltd. - ADR(a) | | | 12,000 | | | | 101,280 | |

| | | | | | | | 386,040 | |

| Coal Mining — 1.16% | | | | | | | | |

| SunCoke Energy, Inc. | | | 28,000 | | | | 266,280 | |

| | | | | | | | | |

| Communications Equipment — 1.41% | | | | | | | | |

| Juniper Networks, Inc. | | | 12,000 | | | | 323,040 | |

| | | | | | | | | |

| Computer Hardware & Storage — 2.06% | | | | | | | | |

| Dell Technologies, Inc., Class C | | | 4,000 | | | | 267,640 | |

| Hewlett Packard Enterprise Co. | | | 13,500 | | | | 207,630 | |

| | | | | | | | 475,270 | |

See accompanying notes which are an integral part of these financial statements.

| 10 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Investments |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| Consumer Finance — 7.34% | | | | | | | | |

| OneMain Holdings, Inc. | | | 12,500 | | | $ | 449,125 | |

| SLM Corp. | | | 68,000 | | | | 884,000 | |

| Synchrony Financial | | | 12,600 | | | | 353,430 | |

| | | | | | | | 1,686,555 | |

| Data & Transaction Processors — 1.95% | | | | | | | | |

| Visa, Inc., Class A | | | 1,900 | | | | 446,690 | |

| | | | | | | | | |

| Diversified Banks — 2.03% | | | | | | | | |

| Barclays PLC, Sponsored - ADR | | | 72,500 | | | | 466,175 | |

| | | | | | | | | |

| Film & TV — 1.15% | | | | | | | | |

| Warner Bros. Discovery, Inc.(a) | | | 26,500 | | | | 263,410 | |

| | | | | | | | | |

| Infrastructure Software — 1.11% | | | | | | | | |

| VMware, Inc., Class A(a) | | | 1,762 | | | | 256,635 | |

| | | | | | | | | |

| Insurance Brokers & Services — 0.19% | | | | | | | | |

| Kingstone Companies, Inc.(a) | | | 22,629 | | | | 43,900 | |

| | | | | | | | | |

| Internet Media & Services — 2.62% | | | | | | | | |

| Meta Platforms, Inc., Class A(a) | | | 2,000 | | | | 602,540 | |

| | | | | | | | | |

| Investment Companies — 1.01% | | | | | | | | |

| BBX Capital, Inc.(a) | | | 32,801 | | | | 231,903 | |

| | | | | | | | | |

| Life Insurance — 5.30% | | | | | | | | |

| Genworth Financial, Inc., Class A(a) | | | 55,600 | | | | 333,044 | |

| Jackson Financial, Inc., Class A | | | 24,100 | | | | 884,711 | |

| | | | | | | | 1,217,755 | |

| Private Equity — 3.99% | | | | | | | | |

| The Carlyle Group, Inc. | | | 20,000 | | | | 550,800 | |

| Victory Capital Holdings, Inc., Class A | | | 12,400 | | | | 365,304 | |

| | | | | | | | 916,104 | |

| Real Estate Services — 1.22% | | | | | | | | |

| Anywhere Real Estate, Inc.(a) | | | 60,000 | | | | 280,200 | |

| | | | | | | | | |

| Steel Producers — 1.44% | | | | | | | | |

| United States Steel Corp. | | | 9,750 | | | | 330,428 | |

See accompanying notes which are an integral part of these financial statements.

| Semi-Annual Report | October 31, 2023 | 11 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Investments |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| Wealth Management — 7.68% | | | | | | | | |

| Ameriprise Financial, Inc. | | | 2,500 | | | $ | 786,425 | |

| Stifel Financial Corp. | | | 12,000 | | | | 684,000 | |

| Virtus Investment Partners, Inc. | | | 1,600 | | | | 294,768 | |

| | | | | | | | 1,765,193 | |

| TOTAL COMMON STOCKS — LONG — | | | | | | | | |

| (Cost $17,213,401) | | | | | | | 18,541,999 | |

| PREFERRED STOCKS — LONG — 8.72% | | | | | | | | |

| Specialty Finance — 8.72% | | | | | | | | |

| AG Mortgage Investment Trust, Inc., Series C, 8.00% | | | 36,000 | | | | 678,960 | |

| Chimera Investment Corp., Series B | | | 14,391 | | | | 303,506 | |

| Chimera Investment Corp., Series D, 8.00% | | | 19,717 | | | | 398,086 | |

| Federal National Mortgage Association, Series O, 7.00%(a) | | | 9,625 | | | | 37,826 | |

| Federal National Mortgage Association, Series R, 7.63%(a) | | | 20,250 | | | | 39,488 | |

| SLM Corp., Series B, 1.70% | | | 8,276 | | | | 546,133 | |

| | | | | | | | 2,003,999 | |

| TOTAL PREFERRED STOCKS — LONG — | | | | | | | | |

| (Cost $1,942,854) | | | | | | | 2,003,999 | |

| WARRANTS — LONG — 0.03% | | | | | | | | |

| Ampco-Pittsburgh Corp., Expires 08/01/25, Strike Price $6 | | | 26,300 | | | | 6,575 | |

| | | | | | | | | |

| TOTAL WARRANTS — LONG — | | | | | | | | |

| (Cost $7,889) | | | | | | | 6,575 | |

| MONEY MARKET FUNDS — 7.49% | | | | | | | | |

| First American Treasury Obligations Fund - Class X, 5.27%(b) | | | 1,722,183 | | | | 1,722,183 | |

| | | | | | | | | |

| TOTAL MONEY MARKET FUNDS | | | | | | | | |

| (Cost $1,722,183) | | | | | | | 1,722,183 | |

| TOTAL INVESTMENTS — 96.91% | | | | | | | | |

| (Cost $20,886,328) | | | | | | | 22,274,756 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 3.08% | | | | | | | 707,625 | |

| NET ASSETS — 100.00% | | | | | | $ | 22,982,381 | |

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of October 31, 2023. |

ADR - American Depositary Receipt

See accompanying notes which are an integral part of these financial statements.

| 12 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Securities Sold Short |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| COMMON STOCKS — SHORT — (34.89)% | | | | | | | | |

| Application Software — (0.18)% | | | | | | | | |

| Root, Inc.(a) | | | (4,663 | ) | | $ | (42,154 | ) |

| | | | | | | | | |

| Automobiles — (0.52)% | | | | | | | | |

| Tesla, Inc.(a) | | | (600 | ) | | | (120,504 | ) |

| | | | | | | | | |

| Banks — (15.46)% | | | | | | | | |

| Bank of Hawaii Corp. | | | (15,000 | ) | | | (740,850 | ) |

| Capitol Federal Financial, Inc. | | | (102,500 | ) | | | (533,000 | ) |

| City Holding Co. | | | (883 | ) | | | (80,159 | ) |

| Commerce Bancshares, Inc. | | | (4,520 | ) | | | (198,247 | ) |

| First Financial Bankshares, Inc. | | | (6,250 | ) | | | (150,313 | ) |

| Flushing Financial Corp. | | | (20,300 | ) | | | (250,502 | ) |

| Hingham Institution for Savings | | | (3,000 | ) | | | (445,740 | ) |

| Northwest Bancshares, Inc. | | | (9,142 | ) | | | (95,260 | ) |

| Park National Corp. | | | (1,700 | ) | | | (172,363 | ) |

| Renasant Corp. | | | (11,800 | ) | | | (287,802 | ) |

| Seacoast Banking Corporation of Florida | | | (8,500 | ) | | | (171,785 | ) |

| United Bankshares, Inc. | | | (15,100 | ) | | | (429,444 | ) |

| | | | | | | | (3,555,465 | ) |

| Commercial Vehicles — (0.05)% | | | | | | | | |

| Nikola Corp.(a) | | | (10,000 | ) | | | (10,800 | ) |

| | | | | | | | | |

| Data & Transaction Processors — (0.55)% | | | | | | | | |

| Affirm Holdings, Inc.(a) | | | (7,143 | ) | | | (125,788 | ) |

| | | | | | | | | |

| Diversified Banks — (1.15)% | | | | | | | | |

| Bank of America Corp. | | | (10,000 | ) | | | (263,400 | ) |

| | | | | | | | | |

| Industrial Wholesale & Rental — (2.10)% | | | | | | | | |

| SiteOne Landscape Supply, Inc.(a) | | | (3,500 | ) | | | (482,195 | ) |

See accompanying notes which are an integral part of these financial statements.

| Semi-Annual Report | October 31, 2023 | 13 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Securities Sold Short |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| Infrastructure Software — (0.08)% | | | | | | | | |

| Upstart Holdings, Inc.(a) | | | (800 | ) | | $ | (19,224 | ) |

| | | | | | | | | |

| Internet Media & Services — (0.42)% | | | | | | | | |

| Opendoor Technologies, Inc.(a) | | | (50,800 | ) | | | (96,520 | ) |

| | | | | | | | | |

| Multi Asset Class REITs — (1.67)% | | | | | | | | |

| Vornado Realty Trust | | | (20,000 | ) | | | (384,000 | ) |

| | | | | | | | | |

| Non-Alcoholic Beverages — (0.03)% | | | | | | | | |

| Oatly Group AB - ADR(a) | | | (15,651 | ) | | | (7,597 | ) |

| | | | | | | | | |

| Office REITs — (7.07)% | | | | | | | | |

| Boston Properties, Inc. | | | (5,200 | ) | | | (278,564 | ) |

| Corporate Office Properties Trust | | | (15,000 | ) | | | (342,000 | ) |

| Cousins Properties, Inc. | | | (16,000 | ) | | | (285,920 | ) |

| Empire State Realty Trust, Inc., Class A | | | (56,000 | ) | | | (453,040 | ) |

| JBG SMITH Properties | | | (20,700 | ) | | | (266,409 | ) |

| | | | | | | | (1,625,933 | ) |

| P&C Insurance — (0.07)% | | | | | | | | |

| Lemonade, Inc.(a) | | | (1,442 | ) | | | (15,775 | ) |

| | | | | | | | | |

| Packaged Food — (0.04)% | | | | | | | | |

| Beyond Meat, Inc.(a) | | | (1,600 | ) | | | (9,552 | ) |

| | | | | | | | | |

| Property & Casualty Insurance — (2.53)% | | | | | | | | |

| Progressive Corp. (The) | | | (3,675 | ) | | | (580,981 | ) |

| | | | | | | | | |

| Real Estate Services — (0.41)% | | | | | | | | |

| Compass, Inc., Class A(a) | | | (47,400 | ) | | | (93,852 | ) |

| | | | | | | | | |

| Wealth Management — (2.56)% | | | | | | | | |

| Charles Schwab Corp. (The) | | | (11,300 | ) | | | (588,051 | ) |

| | | | | | | | | |

| TOTAL COMMON STOCKS SHORT | | | | | | | | |

| (Proceeds Received $11,071,955) | | | | | | | (8,021,791 | ) |

See accompanying notes which are an integral part of these financial statements.

| 14 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Schedule of Securities Sold Short |

| | October 31, 2023 (Unaudited) |

| | | Shares | | | Fair Value | |

| EXCHANGE-TRADED FUNDS — SHORT — (1.10)% | | | | | | | | |

| Direxion Daily Financial Bear 3X Shares | | | (11,700 | ) | | $ | (253,188 | ) |

| TOTAL EXCHANGE-TRADED FUNDS | | | | | | | | |

| (Proceeds Received $499,663) | | | | | | | (253,188 | ) |

| TOTAL SECURITIES SOLD SHORT — (35.99)% | | | | | | | | |

| (Proceeds Received $11,571,618) | | | | | | $ | (8,274,979 | ) |

| (a) | Non-income producing security. |

ADR - American Depositary Receipt

See accompanying notes which are an integral part of these financial statements.

| Semi-Annual Report | October 31, 2023 | 15 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Statement of Assets and Liabilities |

| | October 31, 2023 (Unaudited) |

| ASSETS | | | | |

| Investments is securities at fair value (cost $20,886,328) | | $ | 22,274,756 | |

| Deposit held by broker for securities sold short | | | 8,997,306 | |

| Receivable for fund shares sold | | | 88 | |

| Dividends and interest receivable | | | 18,277 | |

| Prepaid expenses | | | 16,956 | |

| Total Assets | | | 31,307,383 | |

| | | | | |

| LIABILITIES | | | | |

| Bank overdraft | | | 5,727 | |

| Securities sold short, at value (proceeds received $11,571,618) | | | 8,274,979 | |

| Payable for dividends declared on short sales | | | 1,890 | |

| Payable to Adviser | | | 15,133 | |

| Payable to Administrator | | | 5,707 | |

| Other accrued expenses | | | 21,515 | |

| Total Liabilities | | | 8,324,951 | |

| | | | | |

| Net Assets | | $ | 22,982,381 | |

| | | | | |

| Net Assets consist of: | | | | |

| Paid-in capital | | | 18,439,132 | |

| Accumulated earnings | | | 4,543,249 | |

| Net Assets | | $ | 22,982,381 | |

| | | | | |

| Shares outstanding, par value $0.10 per share (30,000,000 authorized shares) | | | 710,132 | |

| | | | | |

| Net asset value, offering price and redemption price per share(a) | | $ | 32.36 | |

| (a) | Redemption price may differ from net asset value if redemption fee is applied. |

See accompanying notes which are an integral part of these financial statements.

| 16 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Statement of Operations |

| For the six months ended October 31, 2023 (Unaudited) |

| INVESTMENT INCOME | | | | |

| Dividend income (net of foreign taxes withheld of $4,274) | | $ | 480,879 | |

| Interest income | | | 58,234 | |

| Total investment income | | | 539,113 | |

| | | | | |

| EXPENSES | | | | |

| Investment Advisory fees | | | 111,310 | |

| Legal | | | 22,446 | |

| Director’s fees and expenses | | | 18,853 | |

| Miscellaneous | | | 17,846 | |

| Administration | | | 14,376 | |

| Fund accounting | | | 12,893 | |

| Registration | | | 11,351 | |

| Transfer agent | | | 10,129 | |

| Compliance Services | | | 9,301 | |

| Audit and tax preparation | | | 8,948 | |

| Report printing | | | 6,232 | |

| Insurance | | | 4,633 | |

| Custodian | | | 3,706 | |

| Sub transfer agent fees | | | 1,183 | |

| Pricing | | | 854 | |

| Dividend expense on securities sold short | | | 122,877 | |

| Total expenses | | | 376,938 | |

| Fees contractually waived | | | (32,387 | ) |

| Net operating expenses | | | 344,551 | |

| Net investment income | | | 194,562 | |

| | | | | |

| NET REALIZED AND CHANGE IN UNREALIZED GAIN (LOSS) ON INVESTMENTS | | | | |

| Net realized gain from: | | | | |

| Investments | | | 691,185 | |

| Change in unrealized appreciation on: | | | | |

| Investments | | | 265,247 | |

| NET REALIZED AND CHANGE IN UNREALIZED GAIN ON INVESTMENTS AND SECURITIES SOLD SHORT | | | 956,432 | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 1,150,994 | |

See accompanying notes which are an integral part of these financial statements.

| Semi-Annual Report | October 31, 2023 | 17 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Statements of Changes in Net Assets |

| | | For the Six | | | | |

| | | Months Ended | | | | |

| | | October 31, 2023 | | | For the Year Ended | |

| | | (Unaudited) | | | April 30, 2023 | |

| INCREASE (DECREASE) IN NET ASSETS DUE TO: | | | | | | | | |

| Operations | | | | | | | | |

| Net investment income (loss) | | $ | 194,562 | | | $ | (23,658 | ) |

| Net realized gain on investments, securities sold short and foreign currency transactions | | | 691,185 | | | | 1,036,540 | |

| Net change in unrealized appreciation (depreciation) of investments, securities sold short and foreign currency translations | | | 265,247 | | | | (155,038 | ) |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | | 1,150,994 | | | | 857,844 | |

| | | | | | | | | |

| CAPITAL TRANSACTIONS | | | | | | | | |

| Proceeds from shares sold | | | 1,992,938 | | | | 1,424,532 | |

| Amount paid for shares redeemed | | | (525,566 | ) | | | (1,798,559 | ) |

| Proceeds from redemption fees (Note 1) | | | — | | | | 2,410 | |

| NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM CAPITAL TRANSACTIONS | | | 1,467,372 | | | | (371,617 | ) |

| TOTAL INCREASE IN NET ASSETS | | | 2,618,366 | | | | 486,227 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of period | | | 20,364,015 | | | | 19,877,788 | |

| End of period | | $ | 22,982,381 | | | $ | 20,364,015 | |

| | | | | | | | | |

| SHARE TRANSACTIONS | | | | | | | | |

| Shares sold | | | 61,419 | | | | 49,562 | |

| Shares redeemed | | | (16,309 | ) | | | (62,809 | ) |

| Net increase (decrease) in shares outstanding | | | 45,110 | | | | (13,247 | ) |

See accompanying notes which are an integral part of these financial statements.

| 18 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Financial Highlights |

(For a share outstanding during each period)

| | | For the Six | | | | | | | | | | | | | | | | |

| | | Months | | | For the | | | For the | | | For the | | | For the | | | For the | |

| | | Ended | | | Year | | | Year | | | Year | | | Year | | | Year | |

| | | October 31, | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | 2023 | | | April 30, | | | April 30, | | | April 30, | | | April 30, | | | April 30, | |

| | | (Unaudited) | | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Selected Per Share Data | | | | | | | | | | | | | | | | | | | | | | | | |

| Net asset value, beginning of period | | $ | 30.62 | | | $ | 29.31 | | | $ | 29.17 | | | $ | 15.21 | | | $ | 20.86 | | | $ | 20.61 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss)(a) | | | 0.27 | | | | (0.04 | ) | | | (0.32 | ) | | | (0.10 | ) | | | (0.20 | ) | | | (0.19 | ) |

| Net realized and unrealized gain (loss) on investments | | | 1.47 | | | | 1.35 | | | | 0.46 | | | | 14.06 | | | | (5.45 | ) | | | 0.44 | (b) |

| Total from investment operations | | | 1.74 | | | | 1.31 | | | | 0.14 | | | | 13.96 | | | | (5.65 | ) | | | 0.25 | |

| Paid-in capital from redemption fees | | | — | (c) | | | — | (c) | | | — | (c) | | | — | (c) | | | — | (c) | | | — | (c) |

| Net asset value, end of period | | $ | 32.36 | | | $ | 30.62 | | | $ | 29.31 | | | $ | 29.17 | | | $ | 15.21 | | | $ | 20.86 | |

| Total Return(d) | | | 1.99 | % (e) | | | 4.47 | % | | | 0.48 | % | | | 91.78 | % | | | (27.09 | )% | | | 1.21 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (000 omitted) | | $ | 22,982 | | | $ | 20,364 | | | $ | 19,878 | | | $ | 20,963 | | | $ | 12,259 | | | $ | 23,272 | |

| Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of net expenses to average net assets(f) | | | 3.09 | % (g) | | | 3.13 | % | | | 3.07 | % | | | 3.56 | % | | | 3.60 | % | | | 3.19 | % |

| Ratio of expenses to average net assets before waiver by Adviser | | | 3.38 | % (g) | | | 3.55 | % | | | 3.38 | % | | | 4.10 | % | | | 4.08 | % | | | 3.31 | % |

| Ratio of net investment income (loss) to average net assets | | | 1.75 | % (g) | | | (0.12 | )% | | | (1.07 | )% | | | (0.47 | )% | | | (1.00 | )% | | | (0.92 | )% |

| Portfolio Turnover Rate | | | 54 | % (e) | | | 52 | % | | | 55 | % | | | 38 | % | | | 87 | % | | | 240 | % |

| (a) | Calculated using average shares outstanding. |

| (b) | The amount shown for a share outstanding throughout the period does not accord with the change in aggregate gains and losses in the portfolio of securities during the period because of timing of sales and purchases of fund shares in relation to fluctuating market values during the period. |

| (c) | Rounds to less than $0.005 per share. |

| (d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

| (f) | Excluding dividend and interest expense, the ratios of net expenses to average net assets were 2.00% for the six months ended October 31, 2023 and 2.00%, 2.00%, 2.00%, 2.00% and 2.00% for the fiscal years ended April 30, 2023, 2022, 2021, 2020 and 2019, respectively. |

See accompanying notes which are an integral part of these financial statements.

| Semi-Annual Report | October 31, 2023 | 19 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

The Caldwell & Orkin - Gator Capital Long/Short Fund (the “Fund”), formerly the Caldwell & Orkin Market Opportunity Fund, is the only investment portfolio of The Caldwell & Orkin Funds, Inc. (the “Company”), an open-end, diversified management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and incorporated under the laws of the State of Maryland on August 15, 1989. The Fund’s investment objective is to provide long-term capital growth with a short-term focus on capital preservation. Gator Capital Management, LLC (the “Adviser”), the Fund’s investment adviser, uses a fundamental driven, multi-dimensional investment process focusing on active allocation, security selection and surveillance to achieve the Fund’s investment objective.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Regulatory Update – Tailored Shareholder Reports for Mutual Funds and Exchange-Traded Funds (“ETFs”) – Effective January 24, 2023, the Securities and Exchange Commission adopted rule and form amendments to require mutual funds and ETFs to transmit concise and visually engaging streamlined annual and semiannual reports to shareholders that highlight key information. Other information, including financial statements, will no longer appear in a streamlined shareholder report but must be available online, delivered free of charge upon request, and filed on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024. At this time, management is evaluating the impact of these amendments on the shareholder reports for the Fund.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Securities Valuation

Securities are stated at the closing price on the date at which the net asset value (“NAV”) is being determined. If the date of determination is not a trading date, or the closing price is not otherwise available, the last bid price is used for a fair value instead. Debt securities are valued at the price provided by an independent pricing service. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund

| 20 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

values its securities and other assets at fair value as determined by the Adviser, as the Fund’s valuation designee, in accordance with procedures adopted by the Board of Trustees (the “Board”) pursuant to Rule 2a-5 under the 1940 Act, as amended.

Securities Transactions and Related Investment Income

The Fund follows industry practice and records securities transactions on trade date for financial reporting purposes. Dividend income is recorded on the ex-dividend date. Realized gains and losses from investment transactions are determined using the specific identification method. Interest income which includes amortization of premium and accretion of discount, is accrued as earned.

Fair Value Measurements

A three-tier hierarchy has been established to classify fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| ● | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date |

| ● | Level 2 – quoted prices which are not active quoted prices for similar assets or liabilities in active markets or inputs other than quoted process that are observable (either directly or indirectly) for substantially the full term of the asset of liability |

| ● | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

| Semi-Annual Report | October 31, 2023 | 21 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

The following is a summary of the inputs used as of October 31, 2023 in valuing the Fund’s investments carried at value:

| Investments in Securities | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets | | | | | | | | | | | | |

| Common Stocks | | $ | 18,541,999 | | | $ | — | | | $ | — | | | $ | 18,541,999 | |

| Preferred Stocks | | | 2,003,999 | | | | — | | | | — | | | | 2,003,999 | |

| Warrants | | | — | | | | 6,575 | | | | — | | | | 6,575 | |

| Money Market Funds | | | 1,722,183 | | | | — | | | | — | | | | 1,722,183 | |

| Total | | $ | 22,268,181 | | | $ | 6,575 | | | $ | — | | | $ | 22,274,756 | |

| | | | | | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | | | | |

| Securities Sold Short | | | | | | | | | | | | | | | | |

| Common Stocks | | $ | (8,021,791 | ) | | $ | — | | | $ | — | | | $ | (8,021,791 | ) |

| Exchange-Traded Funds | | | (253,188 | ) | | | — | | | | — | | | | (253,188 | ) |

| Total | | $ | (8,274,979 | ) | | $ | — | | | $ | — | | | $ | (8,274,979 | ) |

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type.

The Fund did not hold any assets at any time during the reporting period in which significant unobservable inputs were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

Share Valuation

The NAV per share of the Fund is calculated by dividing the sum of the value of the securities held by the Fund, plus cash or other assets, minus all liabilities (including estimated accrued expenses) by the total number of shares outstanding for the Fund, rounded to the nearest cent. The Fund’s shares will not be priced on the days on which the New York Stock Exchange is closed for trading. The offering and redemption price per share for the Fund is equal to the Fund’s NAV per share.

The Fund charges a 2.00% redemption fee on shares held less than 90 days. These fees are deducted from the redemption proceeds otherwise payable to the shareholder. The Fund will retain the fee charged as paid-in capital and such fees become part of the Fund’s daily NAV calculation. For the six months ended October 31, 2023 the Fund recorded $0 in redemption fee proceeds.

Federal Income Taxes

The Fund makes no provision for federal income tax or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also

| 22 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

The Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income and/or capital gains earned or repatriated. Taxes are accrued and applied to net investment income, net realized gains and unrealized appreciation as such income and/or gains are earned.

The Fund recognizes tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management of the Fund has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the previous three tax year ends and the interim tax period since then, as applicable) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements and does not expect this to change over the next twelve months. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year, the Fund did not incur any interest or penalties.

| 3. | FEES AND OTHER TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS |

The Fund has entered into a management agreement (the “Management Agreement”) with the Adviser pursuant to which the Adviser provides space, facilities, equipment and personnel necessary to perform administrative and investment management services for the Fund. The Management Agreement provides that the Adviser is responsible for the management of the Fund’s portfolio. For such services and expenses assumed by the Adviser, the Fund pays a monthly advisory fee at incremental annual rates as follows:

| Advisory Fee | Average Daily Net Assets |

| 1.00% | Up to $250 million |

| 0.90% | In excess of $250 million but not greater than $500 million |

| 0.80% | In excess of $500 million |

The Adviser has agreed to reimburse the Fund through August 30, 2024 to the extent necessary to prevent the Fund’s annual ordinary operating expenses (excluding taxes, expenses related to the execution of portfolio transactions and the investment activities of the Fund such as, for example, interest, dividend expenses on securities sold short, brokerage commissions and fees and expenses charged to the Fund by any investment company in which the Fund invests and extraordinary charges such as litigation costs) from exceeding 2.00% of the Fund’s average net assets. For the six months ended October 31, 2023, the Adviser waived fees and reimbursed expenses in the amount of $32,387 for the Fund. During the six months ended October 31, 2023, the Adviser earned 111,310 from the Fund, before the waiver described above.

| Semi-Annual Report | October 31, 2023 | 23 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

Ultimus Fund Solutions, LLC (“the Administrator”) provides fund accounting, fund administration and transfer agency services under a Master Services Agreement to the Fund. The Fund pays the Administrator fees for its services under the Master Services Agreement. In addition, the Fund pays out-of-pocket expenses including, but not limited to postage, supplies and costs of pricing the Fund’s securities. For the six months ended October 31, 2023, the Administrator earned fees of $14,376 for administration services, $12,893 for fund accounting services, $10,129 for transfer agent services.

Ultimus Fund Distributors, LLC (the “Distributor”) serves as distributor to the Fund. The Fund does not pay the Distributor for these services. The Distributor is a wholly-owned subsidiary of the Administrator.

Certain officers of the Fund are also officers of the Administrator and the Distributor.

The Fund pays each Director, in cash, an annual fee of $8,000 per year, plus $1,500 for each in-person meeting attended and $1,000 for each telephonic meeting attended. The Fund also reimburses Directors’ actual out-of-pocket expenses relating to attendance at meetings.

| 5. | INVESTMENT PORTFOLIO TRANSACTIONS |

During the six months ended October 31, 2023, the Fund purchased $8,908,565 and sold $5,986,293 of securities, excluding securities sold short and short-term investments.

Short Sales and Segregated Cash

Short sales are transactions in which the Fund sells a security it does not own, in anticipation of a decline in the market value of that security. To initiate such a transaction, the Fund must borrow the security to deliver to the buyer upon the short sale; the Fund is then obligated to replace the security borrowed by purchasing it in the open market at some later date, completing the transaction.

The Fund will incur a loss if the market price of the security increases between the date of the short sale and the date on which the Fund replaces the borrowed security. The Fund will realize a gain if the security declines in value between those dates.

All short sales must be fully collateralized. The Fund maintains the collateral in segregated accounts consisting of cash and/or U.S. Government securities sufficient to collateralize the market value of its short positions. Typically, the segregated cash with brokers and other financial institutions exceeds the minimum required. Deposits with brokers for securities sold short are invested in money market instruments. Segregated cash is held at the custodian in the name of the broker per a tri-party agreement between the Fund, the custodian, and the broker.

| 24 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

The Fund may also sell short “against the box”, i.e., the Fund enters into a short sale as described above, while holding an offsetting long position in the same security which it sold short. If the Fund enters into a short sale against the box, it will segregate an equivalent amount of securities owned by the Fund as collateral while the short sale is outstanding.

The Fund limits the value of its short positions (excluding short sales “against the box”) to 60% of the Fund’s total net assets. At October 31, 2023, the Fund had approximately 36% of its total net assets in short positions.

For the six months ended October 31, 2023, the cost of investments purchased to cover short sales and the proceeds from investments sold short were $323,739 and $1,284,252, respectively.

| 6. | FEDERAL TAX INFORMATION |

As of October 31, 2023, the net unrealized appreciation (depreciation) of investments, including short securities, for tax purposes was as follows:

| Gross unrealized appreciation | | $ | 7,025,500 | |

| Gross unrealized depreciation | | | (2,340,434 | ) |

| Net unrealized appreciation on investments | | $ | 4,685,066 | |

| Tax cost of investments | | $ | 9,314,711 | |

At April 30, 2023, the Fund’s most recent fiscal year end, the components of accumulated earnings (deficit) on a tax basis were as follows:

| Accumulated capital losses | | $ | (826,614 | ) |

| Unrealized appreciation | | | 4,218,869 | |

| Total accumulated earnings (deficit) | | $ | 3,392,255 | |

The difference between book basis and tax basis unrealized appreciation is attributable primarily to the tax deferral of wash losses and investments in partnerships and certain other investments.

As of April 30, 2023, the Fund has available for tax purposes an unused capital loss carryforward of $826,614 of short-term capital losses with no expiration, which is available to offset against future taxable net capital gains. During the fiscal year ended April 30, 2023, the Fund utilized $1,021,400 of available capital loss carryforward.

GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. For the tax year ended April 30, 2023, the Fund increased accumulated earnings by $120,296 and decreased paid-in capital by $120,296. These reclassifications are due primarily to the net operating loss incurred by the Fund.

| Semi-Annual Report | October 31, 2023 | 25 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Notes to Financial Statements |

| | October 31, 2023 (Unaudited) |

| 7. | COMMITMENTS AND CONTINGENCIES |

Under the Fund’s organizational documents, its officers and directors are indemnified against certain liability arising out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with service providers that may contain general indemnification clauses, which may permit indemnification to the extent permissible under applicable law. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date at which these financial statements were issued. Based upon this evaluation, management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

| 26 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Disclosure of Fund Expenses |

| | October 31, 2023 (Unaudited) |

We believe it is important for you to understand the impact of fees and expenses on your investment in the Fund. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs related to the purchase and redemption of Fund shares, including redemption fees and brokerage commissions (if applicable); and (2) ongoing costs, including management fees, administrative expenses, portfolio transaction costs and other Fund expenses. A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The below example is based on an investment of $1,000 made at the beginning of the period and held for the six-month period from May 1, 2023 through October 31, 2023. The table below illustrates the Fund’s expenses in two ways:

Based on Actual Fund Returns

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Based on a Hypothetical 5% Return for Comparison Purposes

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if transaction costs were included, your costs would have been higher.

| | | Beginning | | Ending | | Expenses | | Annualized |

| | | Account Value | | Account Value | | Paid During | | Expense |

| | | May 1, 2023 | | October 31, 2023 | | the Period(a) | | Ratio |

| Actual | | $1,000.00 | | $1,056.80 | | $16.04 | | 3.09% |

| Hypothetical(b) | | $1,000.00 | | $1,009.61 | | $15.67 | | 3.09% |

| (a) | Expenses are equal to the Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| (b) | Hypothetical assumes 5% annual return before expenses. |

| Semi-Annual Report | October 31, 2023 | 27 |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Director Approval of the Investment Advisory Agreement |

| | October 31, 2023 (Unaudited) |

At a meeting held in person on June 23, 2023, at which all of the Directors were present, the Board, including the Directors who are not “interested persons,” as defined by the Investment Company Act of 1940, as amended (the “1940 Act”) (the “Independent Directors”), of Caldwell & Orkin Funds, Inc. (the “Company”), voting separately, reviewed and approved the investment advisory agreement with Gator Capital Management, LLC (the “Adviser”) (the “Advisory Agreement”). In the course of their deliberations, the Board was advised by legal counsel. The Board received and reviewed a substantial amount of information provided by the Adviser in response to requests of the Board and legal counsel.

In considering the approval of the Advisory Agreement and reaching their conclusions with respect thereto, the Board was briefed by counsel on its fiduciary duties and responsibilities in reviewing and approving the Advisory Agreement and the types of information that should be reviewed by them and their responsibilities in making an informed decision regarding the approval of the Advisory Agreement. The Board also reviewed and analyzed various factors that the Directors determined were relevant, including: (1) the nature, extent and quality of the services to be provided by the Adviser to the Caldwell & Orkin – Gator Capital Long/Short Fund (the “Fund”) and the Adviser’s experience managing registered investment companies; (2) the performance of the Adviser in managing investments for clients of the Adviser other than the Fund; (3) the costs of the services to be provided and profits to be realized by the Adviser from its relationship with the Fund, as well as fee rates charged by the Adviser and other advisers for comparable strategies; (4) the extent to which economies of scale may be realized as the Fund grows and whether management fee levels reflect these economies of scale for the benefit of the Fund’s investors; and (5) other benefits to be derived by the Adviser from its relationship with the Fund. The Board’s analysis of the foregoing factors included, but was not limited to, the following:

Nature, Extent and Quality of Services. The Board considered the operating and investment advisory services provided by the Adviser to the Fund, including, without limitation, its investment advisory services, its coordination of services for the Fund among the Fund’s service providers, its compliance procedures and practices, its efforts to promote the Fund and assist in its distribution and its provision of officers for the Company. Based on the foregoing information, the Board determined that the nature, extent and quality of the management and advisory services provided by the Adviser were appropriate for the Fund.

Performance of the Fund and the Adviser. The Board considered the investment performance of the Adviser in managing investments for the Fund on an absolute basis and also compared the performance of the Fund with the performance of the peer group funds managed by other advisers and the Fund’s benchmarks. In addition, the Board considered the consistency of the Adviser’s management of the Fund with the Fund’s investment objective and policies, and long-term performance of the Fund. Following its evaluation of the Adviser’s performance and that of the Fund in such capacities, the Board concluded that the performance of both the Adviser and the Fund was satisfactory.

| 28 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Caldwell & Orkin - Gator Capital Long/Short Fund | Director Approval of the Investment Advisory Agreement |

| | October 31, 2023 (Unaudited) |

Cost of Services and Projected Profits of the Adviser with respect to the Fund. In reviewing the cost of services and the profitability that the Adviser derives from its relationship with the Fund, the Board considered that continuing the Advisory Agreement would result in no changes to the fees charged to the Fund, and that the services provided in exchange for such fees would be appropriate. Additionally, the Board discussed the Adviser’s staffing, personnel and methods of operating; the financial condition of the Adviser and the level of commitment to the Fund and the Adviser by the principals of the Adviser; the asset level of the Fund; and the overall fees and expenses of the Fund.

The Board compared the fees and expenses of the Fund to other funds similar in terms of the type of fund, the style of investment management, the size of the fund and the nature of the fund’s investment strategy, among other factors. The Board observed that the management fee charged by the Adviser is generally below the average charged by its peers (as chosen by the Adviser) and that the Fund’s expense ratio was higher than the average of its peers. In addition, the Directors took note of the expense limitation provisions within the Advisory Agreement and the financial capacity of the Adviser to fulfill its obligations under the Advisory Agreement. Following these comparisons and considerations as well as further discussion of the foregoing, the Board determined that the fees paid to the Adviser by the Fund under the Advisory Agreement are appropriate and within the range of what would have been negotiated at arm’s length.

Economies of Scale. Following discussion of the Fund’s asset level, expectations for growth, levels of fees and the expense limitation agreement, the Board concluded that the Fund’s fee arrangement was appropriate, and that the Fund’s overall fee structure provided for savings and protection for shareholders at lower asset levels through the Fund’s expense limitation agreement that is part of the Advisory Agreement.

Other Benefits Derived by the Adviser from its Relationship with the Fund. The Board considered that, other than the advisory fee and name exposure/promotion, there are no material “fall-out” or ancillary benefits that accrue to the Adviser as a result of its relationship with the Fund. Based on the foregoing information, the Board concluded that such potential benefits are immaterial to its consideration and approval of the Advisory Agreement.

After considering the above factors as well as other factors and in reliance on the totality of information provided by the Adviser and Fund management, the Board unanimously approved the Advisory Agreement for an additional one-year period.

| Semi-Annual Report | October 31, 2023 | 29 |

CUSTOMER PRIVACY NOTICE

| FACTS | WHAT DOES CALDWELL & ORKIN FUNDS, INC. DO WITH YOUR PERSONAL INFORMATION? |

| | |

| Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

| |

| What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include: ■ Social Security number ■ Assets ■ Retirement Assets ■ Transaction History ■ Checking Account Information ■ Purchase History ■ Account Balances ■ Account Transactions ■ Wire Transfer Instructions When you are no longer our customer, we continue to share your information as described in this notice. |

| |

| How? | All financial companies need to share your personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons Caldwell & Orkin Funds, Inc. chooses to share; and whether you can limit this sharing. |

| |

| Reasons we can share your personal information | Does Caldwell &

Orkin Funds, Inc.

share? | Can you limit

this sharing? |

For our everyday business purposes – Such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus | Yes | No |

For our marketing purposes – to offer our products and services to you | Yes | No |

| For joint marketing with other financial companies | No | We don’t share |

For our affiliates’ everyday business purposes – information about your transactions and experiences | No | No |

For our affiliates’ everyday business purposes – information about your creditworthiness | No | We don’t share |

| For nonaffiliates to market to you | No | We don’t share |

| For our affiliates’ marketing purposes | Yes | Yes* |

| | | | |

| Questions? | Call (800) 467-7903 |

| |

To limit our

sharing | *Call (813) 282-7870 Please note:

If you are a new customer, we can begin sharing your information 30 days from the date we sent this notice. When you are no longer our customer, we continue to share your information as described in this notice. However, you can contact us at any time to limit our sharing. |

| 30 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/ |

| Page 2 | |

| Who we are |

Who is providing this

notice? | Caldwell & Orkin Funds, Inc. Caldwell & Orkin - Gator Capital Long/Short Fund Ultimus Fund Distributors, LLC (Distributor) Ultimus Fund Solutions, LLC (Administrator) |

| What we do |

How does Caldwell

& Orkin Funds, Inc.

protect my personal

information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings. Our service providers are held accountable for adhering to strict policies and procedures to prevent any misuse of your nonpublic personal information. |

How does Caldwell

& Orkin Funds, Inc.

collect my personal

information? | We collect your personal information, for example, when you ■ Open an account ■ Provide account information ■ Give us your contact information ■ Make deposits or withdrawals from your account ■ Make a wire transfer ■ Tell us where to send the money ■ Tell us who receives the money ■ Show your government-issued ID ■ Show your driver’s license We also collect your personal information from other companies. |

Why can’t I limit all

sharing? | Federal law gives you the right to limit only ■ Sharing for affiliates’ everyday business purposes – information about your creditworthiness ■ Affiliates from using your information to market to you ■ Sharing for nonaffiliates to market to you State laws and individual companies may give you additional rights to limit sharing. |

| |

| Definitions |

| Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies. ■ Gator Capital Management, LLC the investment adviser to Caldwell & Orkin Funds, Inc., could be deemed an affiliate. |

| Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies ■ Caldwell & Orkin Funds, Inc. does not share with nonaffiliates so they can market to you. |

| Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you. ■ Caldwell & Orkin Funds, Inc. does not jointly market. |

| Semi-Annual Report | October 31, 2023 | 31 |

This Page is Intentionally Left Blank.

This Page is Intentionally Left Blank.

| CALDWELL & ORKIN - GATOR CAPITAL LONG/SHORT FUND |

| Semi-Annual Report to Shareholders |

BOARD OF DIRECTORS Frederick T. Blumer,