Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06161

Allianz Funds

(Exact name of registrant as specified in charter)

| 1633 Broadway, New York, New York | 10019 | |

| (Address of principal executive offices) | (Zip code) |

Lawrence G. Altadonna

1633 Broadway,

New York, New York 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year end: June 30

Date of reporting period: December 31, 2017

Table of Contents

ITEM 1. REPORT TO SHAREHOLDERS

Allianz Funds

SHARE CLASSES A, C, R, P, INSTITUTIONAL, R6, ADMINISTRATIVE

Semiannual Report

December 31, 2017

AllianzGI Emerging Markets Opportunities Fund

AllianzGI Focused Growth Fund

AllianzGI Global Natural Resources Fund

AllianzGI Global Small-Cap Fund

AllianzGI Health Sciences Fund

AllianzGI Income & Growth Fund

AllianzGI Mid-Cap Fund

AllianzGI NFJ Dividend Value Fund

AllianzGI NFJ International Value Fund

AllianzGI NFJ Large-Cap Value Fund

AllianzGI NFJ Mid-Cap Value Fund

AllianzGI NFJ Small-Cap Value Fund

AllianzGI Small-Cap Blend Fund

AllianzGI Technology Fund

This material is authorized for use only when preceded or accompanied by the current Allianz Funds prospectus. Investors should consider the investment objectives, risks, charges and expenses of each Fund carefully before investing. This and other information is contained in the Funds’ prospectus or summary prospectus. Please read the prospectus carefully before you invest or send money.

Receive this report electronically and eliminate paper mailings.

To enroll, go to us.allianzgi.com/edelivery.

Table of Contents

A Word About Risk: A fund may be subject to various risks as described in its prospectus. Some of those risks may include, but are not limited to, the following: fixed-income risk, liquidity risk, derivatives risk, smaller company risk, non-US investment risk, focused investment risk and specific sector investment risks. Below investment grade securities involve a greater risk to principal than investment grade securities. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. The market for certain securities may become illiquid, which could prevent a fund from purchasing or selling these securities at an advantageous time or price and possibly delay redemptions of fund shares. Use of derivative instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit and counterparty risk, management risk and the risk that a fund is unable to close out a position when it is most advantageous to do so. Portfolios investing in derivatives could lose more than the principal amount invested in those instruments. Investing in foreign securities may entail risk due to foreign economic and political developments; this risk may be enhanced when investing in emerging markets. Smaller companies may be more volatile than larger companies and may entail more risk. Concentrating investments in individual sectors may add additional risk and additional volatility compared to a diversified equity portfolio. The principal values of the funds are not guaranteed at any time. Please refer to the applicable fund’s current prospectus for complete details.

Table of Contents

Thomas J. Fuccillo

President & CEO

Dear Shareholder,

Economic growth in the US improved during the six-month fiscal reporting period ended December 31, 2017. This trend also occurred outside the US, and global inflation remained well-contained. Against this backdrop, US and international equities generated strong results. Elsewhere, the US bond market posted a positive return during the reporting period.

The Six-Month Fiscal Period in Review

For the six-month period ended December 31, 2017, US stocks rose 11.42%, as measured by the S&P 500 Index. Two measures of stock performance in developed international and global markets produced positive results, in dollar-denominated terms, with the MSCI EAFE (Europe, Australasia and Far East) Index returning 9.86% and the MSCI World Index gaining 10.61%. Elsewhere, the MSCI Emerging Markets Index rose 15.92% in dollar-denominated terms. With respect to bonds, the Bloomberg Barclays US Credit Index returned 2.41% and the Bloomberg Barclays Global High Yield Index returned 3.73%. The Bloomberg Barclays US Government Bond Index returned 0.43%, while the broader bond market, as measured by the Bloomberg Barclays US Aggregate Bond Index, returned 1.24%.

Turning to the US economy, gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of economic activity and the principal indicator of economic performance, expanded at a 3.1% annual pace during the second quarter of 2017. GDP growth then improved to an annual pace of 3.2% during the third quarter of 2017. Finally, the Commerce Department’s initial estimate — released after the reporting period had ended — showed that GDP grew at an annual pace of 2.6% for the fourth quarter of 2017.

After raising interest rates in March 2017 and June 2017, the US Federal Reserve (the “Fed”) raised rates to a range between 1.25% and 1.50% at its meeting in December 2017. Meanwhile, in October 2017 the Fed started to gradually reduce its balance sheet — a process that will likely take several years. The Fed’s actions during the year were well-telegraphed and there were minimal market disruptions.

Economic growth outside the US largely accelerated during the period. Despite this, a number of central banks, including the European Central Bank and the Bank of Japan maintained their accommodative monetary policies. One exception was the Bank of England, as it raised rates from 0.25% to 0.50% in November 2017 — the first increase since July 2007.

| 2 | December 31, 2017 | | Semiannual Report |

Table of Contents

Outlook

Since the depths of the global financial crisis, central banks have supported financial markets and the economies they serve through expansionary monetary policies, increasing their balance sheets to previously unheard-of sizes. In our opinion, the strong growth in corporate profits and diminishing fears of deflation show that this approach has worked, and central banks will be careful not to stifle current gains.

So, while we anticipate the scale of central bank support will diminish in 2018 — led by the Fed — we expect the overall shift to be slow and the precise actions to vary from one central bank to the next. In our view, interest rates will stay low overall in 2018. Consequently, we believe investors should continue to keep a careful eye on inflation, particularly because official data appear to understate rises in real-world costs. In addition to macroeconomic considerations, we feel several dominant investment themes, including geopolitical risk and business disruption, will persist in 2018.

Following muted conditions for much of last year, we have seen increased market volatility in recent weeks. This does not appear to be driven by a change in underlying market fundamentals, but rather driven by concerns that improving economic growth may trigger an uptick in inflation and more aggressive monetary policy tightening by the Fed.

Against this backdrop, we will continue to use our fundamental research and insights — and our strong global network — to help our clients balance risk and reward. Where appropriate, we will also seek to capitalize on volatility spikes and prepare to trim exposure to risky assets if cyclical data start to lose momentum.

On behalf of Allianz Global Investors U.S. LLC, thank you for investing with us. We encourage you to consult with your financial advisor and to visit our website, us.allianzgi.com, for additional information. We remain dedicated to serving your investment needs.

Sincerely,

Thomas J. Fuccillo

President & CEO

Past performance is no guarantee of future results. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

Receive this report electronically and eliminate paper mailings.

To enroll, go to us.allianzgi.com/edelivery.

| Semiannual Report | | December 31, 2017 | 3 |

Table of Contents

Unaudited

AllianzGI Emerging Markets Opportunities Fund

For the period of July 1, 2017 through December 31, 2017, as provided by Lu Yu, CFA, CIPM, Portfolio Manager.

Fund Insights

For the six-month period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Emerging Markets Opportunities Fund (the “Fund”) returned 15.39%, underperforming the MSCI Emerging Markets Index (the “benchmark”), which returned 15.92%.

Market Overview

Emerging market equities were beneficiaries of higher demand expectations and optimism over the health of the global economy. The double-digit advance in emerging markets earnings growth and an attractive valuation level translated to performance which topped developed markets during the period. Results for the benchmark were positive in five out of six months, which we believe is a testament to the strength of emerging markets equities.

Results for the benchmark were led by a rally in the energy sector, which rebounded alongside an increase in oil and natural gas prices, followed by advances in real estate, health care and materials. Meanwhile, telecommunications and industrials were modestly positive during the period. China was among the top country performers as economic growth exceeded expectations and Russian equities were helped by a turnaround in energy prices. Conversely, Pakistan fell under pressure after being promoted from frontier markets to emerging markets at the onset of the reporting period and Mexico was negatively impacted by two earthquakes and uncertainty over the future of the North American Free Trade Agreement (“NAFTA”).

Portfolio Review

The Fund seeks to deliver outperformance over time by investing in emerging market companies that are benefiting from change not yet fully reflected in the market. The investment team believes that investor behavioral biases contribute to market inefficiencies, which can be exploited through a transparent and repeatable investment process.

During the reporting period, the Fund’s results modestly trailed the benchmark due to more conservative stock selection, as the market was primarily led by high-beta, growth-oriented securities.

From a sector standpoint, industrials was the top performer thanks to stock picking in the airlines industry. Selections in consumer discretionary and a relative underweight allocation to consumer staples also contributed to results. Information technology was the primary source of underperformance due to selections in electronic equipment names as well as an underweight to the internet software & services industry. Selections in energy and financials trailed more modestly. Country results were buoyed by significant stock selection in Turkey, followed by an underweight to Mexico. Meanwhile, more conservative stock picking in South Korea and a relative underweight to Brazil offset results.

Outlook

Our positive viewpoint on emerging markets remains unwavered as we believe investors’ prior skepticism is increasingly turning toward optimism, consistent with past earnings growth cycles. Emerging markets have outperformed developed markets in each of the last two years and continue to trade at a meaningful price-to-earnings discount. This suggests the market has yet to fully buy into the recovery story. In addition, Wall Street analysts are forecasting double-digit earnings growth for emerging markets in 2018 and 2019, which is higher than developed markets for both periods. We believe this combination of positive sentiment, an attractive valuation level and resilient earnings growth suggests there is ample performance potential for the asset class over the coming periods.

| 4 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Emerging Markets Opportunities Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

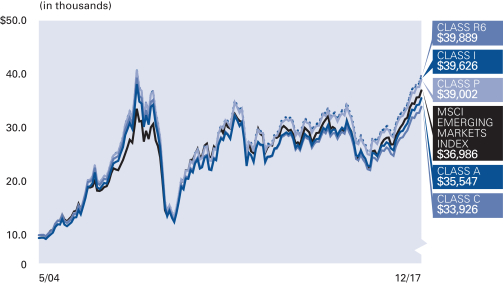

| AllianzGI Emerging Markets Opportunities Fund Class A | 15.39% | 37.90% | 4.50% | 0.30% | 10.23% | |||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund Class A (adjusted) | 9.04% | 30.31% | 3.32% | –0.27% | 9.77% | ||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund Class C | 14.96% | 36.85% | 3.72% | –0.45% | 9.40% | |||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund Class C (adjusted) | 13.96% | 35.85% | 3.72% | –0.45% | 9.40% | ||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund Class P | 15.54% | 38.25% | 4.77% | 0.56% | 10.53% | ||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund Institutional Class | 15.61% | 38.36% | 4.87% | 0.68% | 10.65% | ||||||||||||||||

| AllianzGI Emerging Markets Opportunities Fund R6 | 15.63% | 38.45% | 4.93% | 0.73% | 10.71% | ||||||||||||||||

| MSCI Emerging Markets Index | 15.92% | 37.28% | 4.35% | 1.68% | 10.10% | ||||||||||||||||

| Lipper Emerging Markets Funds Average | 14.19% | 34.57% | 4.26% | 1.49% | 9.59% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 5/27/04. Benchmark comparisons began on the fund inception date. Lipper comparisons began on 5/31/04.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s gross expense ratios are 1.62% for Class A shares, 2.37% for Class C shares, 1.37% for Class P shares, 1.27% for Institutional Class and 1.22% for Class R6 shares. These ratios do not include an expense reduction, contractually agreed through at least October 31, 2018. The Fund’s expense ratios net of these reductions and waivers are 1.27% for Class A shares, 2.02% for Class C shares, 1.02% for Class P shares, 0.92% for Institutional Class shares and 0.87% for Class R6 shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 5/27/04. Benchmark comparisons began on the fund inception date.

Country Allocation (as of December 31, 2017)

| China | 33.8% | |||

| Korea (Republic of) | 13.1% | |||

| India | 7.0% | |||

| Taiwan | 6.8% | |||

| Hong Kong | 6.2% | |||

| Turkey | 5.8% | |||

| Russian Federation | 5.4% | |||

| South Africa | 3.8% | |||

| Other | 16.9% | |||

| Cash & Equivalents — Net | 1.2% |

| Semiannual Report | | December 31, 2017 | 5 |

Table of Contents

Unaudited

AllianzGI Emerging Markets Opportunities Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class C | Class P | Institutional Class | Class R6 | ||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (12/31/17) | $1,153.90 | $1,149.60 | $1,155.40 | $1,156.10 | $1,156.30 | |||||

| Expenses Paid During Period | $6.89 | $10.94 | $5.54 | $5.00 | $4.73 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class C | Class P | Institutional Class | Class R6 | ||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (12/31/17) | $1,018.80 | $1,015.02 | $1,020.06 | $1,020.57 | $1,020.82 | |||||

| Expenses Paid During Period | $6.46 | $10.26 | $5.19 | $4.69 | $4.43 | |||||

For each class of the Fund, expenses (net of fee waivers) are equal to the annualized expense ratio for the class (1.27% for Class A, 2.02% for Class C, 1.02% for Class P, 0.92% for Institutional Class and 0.87% for R6 Class), multiplied by the average account value over the period, multiplied by 184/365.

| 6 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 7 |

Table of Contents

Unaudited

For the period of July 1, 2017 through December 31, 2017, as provided by Karen Hiatt, CFA, Lead Portfolio Manager.

Fund Insights

For the six-month period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Focused Growth Fund (the “Fund”) returned 14.87%, outperforming the Russell 1000 Growth Index (the “benchmark”), which returned 14.23%.

Market Overview

US equities delivered double-digit gains over the second half of the year. Large-cap indices touched a series of fresh peaks and smaller companies also reached a record high in the closing days of the year. Share prices were buoyed by better-than-expected company earnings, renewed merger & acquisition activity, and optimism over the prospects for tax reform. In December, the Senate finally approved plans for $1.5 trillion of tax cuts, the most sweeping overhaul of the US tax system in more than three decades. Consistent with overall annual performance, growth stocks outperformed their value counterparts over the second half of the year.

Portfolio Review

The Fund’s relative performance was largely driven by stock selection in the consumer staples and technology sectors. While overall performance in the consumer staples sector lagged the benchmark’s return, the Fund’s stock selection within the sector helped relative performance. The Fund’s overweight positions in Estee Lauder and Monster Beverage, as well as not owning laggards such as Altria Group and Coca-Cola, boosted relative returns. Meanwhile, stocks in the technology sector generally delivered robust returns throughout the period, largely due to strong earnings growth. The Fund’s positions in Square, Visa, and Applied Materials were among the strongest contributors to relative performance.

Conversely, stock selection in the financials and consumer discretionary sectors detracted from relative returns. Positions in First Republic and Signature Bank were the largest detractors in the group. Due to company-specific challenges and limited upside potential relative to other holdings, the Fund exited positions in both stocks. Within the consumer discretionary sector, strong relative performance from positons in Burlington Stores and Home Depot was offset by weaker performance from Expedia and Newell Brands. Expedia is going through a management transition and increasing spending to fend off competition, while Newell Brands is going through an extended process of integrating acquisitions. The team exited both positions during the period.

We believe the portfolio holdings have attractive long-term growth prospects, and we remain comfortable with our overall positioning, despite short-term periods of volatility.

From a sector allocation perspective, an underweight in consumer staples and no exposure to the real estate sector helped relative performance. Conversely, an overweight in consumer discretionary and an underweight in industrials hurt relative performance.

Outlook

We maintain a positive view on US equities for 2018. In 2017, stocks generally performed well due to better than expected earnings growth, and we expect this to continue in 2018. While we may see modest pressure on equity multiples, we expect continued improvements in earnings growth to more than offset multiple compression. With tax reform completed, along with solid economic data and consumer sentiment, we estimate S&P 500 earnings should grow in the 10% to 15% range and GDP growth should reach 2.75% to 3.0% in 2018.

We believe that the market will ultimately reward companies that deliver consistent growth and increase shareholder value over time. Our focus continues to be on applying rigorous fundamental research to identify companies with strong or under-appreciated growth prospects and attractive risk-reward characteristics.

| 8 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Focused Growth Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

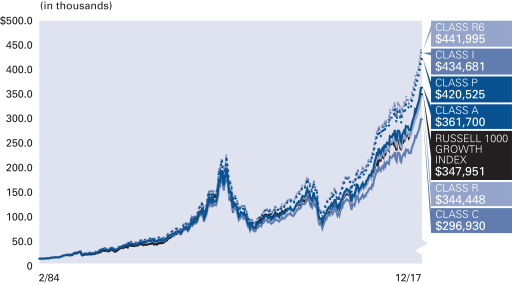

| AllianzGI Focused Growth Fund Class A | 14.87% | 31.45% | 17.35% | 9.40% | 11.37% | |||||||||||||||||

| AllianzGI Focused Growth Fund Class A (adjusted) | 8.55% | 24.22% | 16.03% | 8.78% | 11.18% | ||||||||||||||||

| AllianzGI Focused Growth Fund Class C | 14.44% | 30.45% | 16.47% | 8.58% | 10.54% | |||||||||||||||||

| AllianzGI Focused Growth Fund Class C (adjusted) | 13.44% | 29.45% | 16.47% | 8.58% | 10.54% | ||||||||||||||||

| AllianzGI Focused Growth Fund Class R | 14.72% | 31.09% | 17.05% | 9.13% | 11.02% | ||||||||||||||||

| AllianzGI Focused Growth Fund Class P | 15.01% | 31.72% | 17.64% | 9.69% | 11.68% | ||||||||||||||||

| AllianzGI Focused Growth Fund Institutional Class | 15.05% | 31.88% | 17.76% | 9.79% | 11.79% | ||||||||||||||||

| AllianzGI Focused Growth Fund R6 | 15.11% | 31.94% | 17.81% | 9.85% | 11.84% | ||||||||||||||||

| AllianzGI Focused Growth Fund Administrative Class | 14.93% | 31.57% | 17.47% | 9.52% | 11.50% | |||||||||||||||||

| Russell 1000 Growth Index | 14.23% | 30.21% | 17.33% | 10.00% | 11.06% | ||||||||||||||||

| Lipper Large-Cap Growth Funds Average | 12.22% | 29.57% | 15.70% | 8.44% | 8.58% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 2/24/84. Benchmark and Lipper performance comparisons began on 2/29/84.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s gross expense ratios are 1.11% for Class A shares, 1.86% for Class C shares, 1.36% for Class R shares, 0.86% for Class P shares, 0.76% for Institutional Class, 0.71% for Class R6 shares, and 1.01% for Administrative Class shares. These ratios do not include an expense reduction, contractually agreed through at least October 31, 2018. The Fund’s expense ratios net of this reduction are 0.99% for Class A shares, 1.76% for Class C shares, 1.26% for Class R shares, 0.76% for Class P shares, 0.66% for Institutional Class shares, 0.61% for Class R6 shares, and 0.91% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 2/24/84. Benchmark performance comparisons began on 2/29/84.

Industry/Sectors (as of December 31, 2017)

| Internet Software & Services | 12.1% | |||

| Software | 8.5% | |||

| Technology Hardware, Storage & Peripherals | 7.1% | |||

| IT Services | 6.9% | |||

| Specialty Retail | 6.1% | |||

| Internet & Catalog Retail | 6.1% | |||

| Semiconductors & Semiconductor Equipment | 6.0% | |||

| Biotechnology | 5.2% | |||

| Other | 41.8% | |||

| Cash & Equivalents — Net | 0.2% |

| Semiannual Report | | December 31, 2017 | 9 |

Table of Contents

Unaudited

AllianzGI Focused Growth Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (12/31/17) | $1,148.70 | $1,144.40 | $1,147.20 | $1,150.10 | $1,150.50 | $1,151.10 | $1,149.30 | |||||||

| Expenses Paid During Period | $5.42 | $9.57 | $6.87 | $4.17 | $3.63 | $3.36 | $4.98 | |||||||

| Hypothetical Performance | ||||||||||||||

| (5% return before expenses) | ||||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (12/31/17) | $1,020.16 | $1,016.28 | $1,018.80 | $1,021.32 | $1,021.83 | $1,022.08 | $1,020.57 | |||||||

| Expenses Paid During Period | $5.09 | $9.00 | $6.46 | $3.92 | $3.41 | $3.16 | $4.69 | |||||||

For each class of the Fund, expenses (net of fee waivers) are equal to the annualized expense ratio for the class (1.00% for Class A, 1.77% for Class C, 1.27% for Class R, 0.77% for Class P, 0.67% for Institutional Class, 0.62% for Class R6 and 0.92% for Administrative Class), multiplied by the average account value over the period, multiplied by 184/365.

| 10 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 11 |

Table of Contents

Unaudited

AllianzGI Global Natural Resources Fund

For the reporting period of July 1, 2017, through December 31, 2017, as provided by Paul Strand, CFA, Portfolio Manager.

Fund Insights

For the six-month reporting period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Global Natural Resources Fund (the “Fund”) returned 15.32%, underperforming the 60% MSCI World Energy/40% MSCI World Materials (the “benchmark”), which returned 16.79%.

Market overview

Crude oil markets rebounded sharply in the second half of 2017, bouncing off the lows for Brent crude seen in June of under $45 per barrel, touching over $65 per barrel at the end of the year. Crude oil rebounded as evidence suggests OPEC was adhering to its supply cutbacks, global demand/supply statistics turned more favorable and there appeared to be a better deployment of capital discipline among the US shale producers. However, partly because of the first half drop in energy prices the MSCI World Energy Index was the worst performing MSCI sector index for the 2017 calendar year, up only about 6%. By comparison, the MSCI World Index, the broad market gauge, rose over 20% for the year. Meanwhile, some upward moves in the prices of copper and base metals such as aluminum, nickel and iron ore, coupled with relatively accommodative global monetary conditions and strong metal demand from China, helped the MSCI World Materials Index to surge to nearly a 30% gain for calendar year 2018.

Portfolio review

The Fund’s underperformance was driven by adverse allocation effects from an overweight in both alternative energy and oilfield services. The Fund’s use of option call writing had a negligible impact on performance for the period.

The energy positions in oil and gas exploration and production (“E&P”), pressure pumping and integrated oil contributed the most to relative performance. In general, the E&P stocks were boosted by the second-half rebound in crude prices. The pressure pumping position, Propetro Holding Corp., was helped by improved pricing with the general pick up in US land rig activity. An underweight in Exxon Mobile Corp. positively impacted performance as the integrated oil companies tend to lag the higher beta energy industries in the context of higher crude prices. Finally, Chemours Company, a titanium dioxide producer, which is a raw material for paints, benefitted from favorable pricing.

The performance detractors were generally eclectic in nature including some positions in oil and gas exploration and production, a sand supplier to US-based land rigs and alternative energy. The wind turbine positions were hurt by overcapacity and the resulting unfavorable pricing in the industry. The E&P positions were negatively impacted by quarterly earnings misses and a shift toward more natural gas production than oil. Lastly a sand supplier was hit by capacity expansions, including some private companies.

Outlook

We believe the Fund is poised to benefit from the continued rebound in the energy sector including an improvement from what we believe was the overly pessimistic investor sentiment in the first half of the year. Over the intermediate term (one to two years), we expect oil prices to normalize to at least in the $55 to $65 range. Given our belief that the global economy and global energy demand will grow at least moderately over the next couple of years, and the fact that we believe that there is a substantial disconnect between current oil prices and energy stock valuations, we are currently overweight energy as we enter 2018. Furthermore, given our outlook for steady global economic growth, we are also maintaining our positioning in the materials sector. Additionally, we continue to hold a favorable view of the growth of EVs (electric vehicles), and have exposure to this theme through companies exposed to lithium and battery production. Finally, despite the Portfolio’s first half setback to performance from the energy exposure, we believe that the energy positioning will ultimately benefit the strategy, as natural global demand growth will lift energy prices longer term beyond our intermediate normalized forecast of $55 to $65. The Fund remains globally diversified.

We continue to favor our diversified, thematic and opportunistic approach to investing in natural resource-related companies, and maintain our belief that over the long term the performance of the equities should outperform the underlying commodities. Risks to the Fund include a relapse in the global economy, disruption to world bond markets and a sustained drop in commodity prices.

| 12 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Global Natural Resources Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

| AllianzGI Global Natural Resources Fund Class A | 15.32% | –0.94% | 0.13% | –2.95% | 6.06% | |||||||||||||||||

| AllianzGI Global Natural Resources Fund Class A (adjusted) | 8.98% | –6.39% | –0.99% | –3.50% | 5.62% | ||||||||||||||||

| AllianzGI Global Natural Resources Fund Class C | 14.84% | –1.66% | –0.63% | –3.66% | 5.28% | |||||||||||||||||

| AllianzGI Global Natural Resources Fund Class C (adjusted) | 13.84% | –2.64% | –0.63% | –3.66% | 5.28% | ||||||||||||||||

| AllianzGI Global Natural Resources Fund Class P | 15.39% | –0.74% | 0.36% | –2.70% | 6.34% | ||||||||||||||||

| AllianzGI Global Natural Resources Fund Institutional Class | 15.48% | –0.57% | 0.48% | –2.61% | 6.44% | ||||||||||||||||

| 60% MSCI World Energy/40% MSCI World Materials | 16.79% | 14.24% | 3.24% | 0.51% | 6.97% | ||||||||||||||||

| MSCI World Index | 10.61% | 22.40% | 11.64% | 5.03% | 7.32% | ||||||||||||||||

| Custom Commodity Equity Benchmark | 14.69% | 18.62% | 4.93% | 1.72% | 8.89% | ||||||||||||||||

| Lipper Global Natural Resources Funds Average | 15.33% | 8.73% | 0.11% | –4.03% | 5.07% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 6/30/04. Benchmark and Lipper comparisons began on the fund inception date.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s expense ratios are 1.42% for Class A shares, 2.17% for Class C shares, 1.17% for Class P shares and 1.07% for Institutional Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 6/30/04. Benchmark comparisons began on the fund inception date.

Country Allocation (as of December 31, 2017)

| United States | 60.4% | |||

| United Kingdom | 14.0% | |||

| Canada | 7.6% | |||

| France | 5.3% | |||

| Australia | 3.5% | |||

| Japan | 2.4% | |||

| Germany | 1.9% | |||

| Chile | 1.2% | |||

| Other | 2.6% | |||

| Cash & Equivalents — Net (including Options Written) | 1.1% |

| Semiannual Report | | December 31, 2017 | 13 |

Table of Contents

Unaudited

AllianzGI Global Natural Resources Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||

| Class A | Class C | Class P | Institutional Class | |||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||

| Ending Account Value (12/31/17) | $1,153.20 | $1,148.40 | $1,153.90 | $1,154.80 | ||||

| Expenses Paid During Period | $7.76 | $11.81 | $6.35 | $5.87 | ||||

| Hypothetical Performance | ||||||||

| (5% return before expenses) | ||||||||

| Class A | Class C | Class P | Institutional Class | |||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||

| Ending Account Value (12/31/17) | $1,018.00 | $1,014.22 | $1,019.31 | $1,019.76 | ||||

| Expenses Paid During Period | $7.27 | $11.07 | $5.96 | $5.50 | ||||

For each class of the Fund, expenses are equal to the annualized expense ratio for the class (1.43% for Class A, 2.18% for Class C, 1.17% for Class P and 1.08% for Institutional Class), multiplied by the average account value over the period, multiplied by 184/365.

| 14 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 15 |

Table of Contents

Unaudited

AllianzGI Global Small-Cap Fund

For the period of July 1, 2017 through December 31, 2017, as provided by Andrew Neville, Lead Portfolio Manager.

Fund Insights

For the six-month period ended December 31, 2017, the Class A shares at net asset value (“NAV”) of the AllianzGI Global Small-Cap Fund (the “Fund”) returned 14.05%, outperforming the MSCI World Small-Cap Index, (the “benchmark”), which returned 11.79%.

Market Overview

Global equities rallied strongly over the second half of 2017. Optimism over the health of the global economy and US tax reform helped stocks overcome heightened political tensions. Small-cap stocks in equity markets around the world performed ahead of their larger cap counterparts.

Economic data indicated the global economy was in robust health, with the US, Eurozone and Japan all recording third-quarter growth of at least 2.5% on an annualized basis. As widely expected, the US Federal Reserve (the “Fed”) raised interest rates by 25 basis points and started to unwind the $4.5 trillion of Treasury bonds and mortgage-backed securities amassed as part of its quantitative easing programs. While the European Central Bank kept interest rates on hold and extended its stimulus measures until September 2018, it halved the size of its monthly asset purchases starting in January 2018.

Portfolio review

The portfolio performed well ahead of the benchmark over the course of the second half of 2017 achieving a strong absolute return. The European, Asia-Pacific and Japanese sleeve portfolios performed well ahead of their regional markets whilst the US sleeve portfolio closed the period in line with the local market.

Sector positioning was a slight positive contributor to performance driven by the overweight in industrials and the underweight in real estate. Country-wise, the portfolio’s exposure to China and Taiwan within the Asian sleeve portfolio, the overweight in Germany within the European sleeve portfolio and the underweight in Canada were all meaningful positive contributors.

Successful stock selection, however, accounted for most of the outperformance achieved in the reporting period. Selection was particularly strong within the Asia-Pacific and Japanese sleeves of the portfolio. Sector-wise, stock selection contributed most within industrials, information technology and energy. On a single stock basis, the most meaningful positive contributors to performance were spread across all parts of the portfolio including the positions in Daifuku (Japan), Alcoa Corp., XPO Logistics (both US), Intermediate Capital (UK) and Santos (Australia).

Outlook

We believe the global economy is likely to remain on a moderate growth course, which should lead to further rises in corporate profits and share prices. We believe markets should also continue to benefit from the growth-oriented monetary policy of the world’s central banks, even though the Fed has already begun to raise interest rates. In Europe, unlike the US, rate rises are not yet on the horizon, and we believe Asian central banks are also likely to maintain a generous money supply for the time being. However, this could harbor a risk for equity markets, due to the increasing likelihood that peak liquidity will be reached in 2018. A significant shift in monetary policy could lead to a correction on the equity markets, as well as increased volatility in exchange rates.

| 16 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Global Small-Cap Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

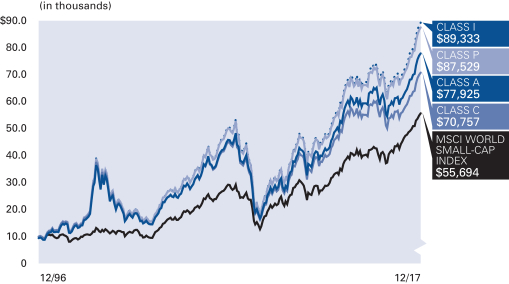

| AllianzGI Global Small-Cap Fund Class A | 14.05% | 26.86% | 12.55% | 6.07% | 10.57% | |||||||||||||||||

| AllianzGI Global Small-Cap Fund Class A (adjusted) | 7.79% | 19.89% | 11.29% | 5.47% | 10.27% | ||||||||||||||||

| AllianzGI Global Small-Cap Fund Class C | 13.63% | 25.92% | 11.72% | 5.27% | 9.76% | |||||||||||||||||

| AllianzGI Global Small-Cap Fund Class C (adjusted) | 12.63% | 24.92% | 11.72% | 5.27% | 9.76% | ||||||||||||||||

| AllianzGI Global Small-Cap Fund Class P | 14.20% | 27.20% | 12.84% | 6.35% | 10.89% | ||||||||||||||||

| AllianzGI Global Small-Cap Fund Institutional Class | 14.26% | 27.32% | 12.95% | 6.45% | 10.99% | ||||||||||||||||

| MSCI World Small-Cap Index | 11.79% | 22.66% | 13.20% | 7.70% | 8.52% | ||||||||||||||||

| Lipper Global Small-/Mid-Cap Funds Average | 12.45% | 26.26% | 12.49% | 5.91% | 9.31% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 12/31/96. Benchmark and Lipper comparisons began on the fund inception date.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s expense ratios are 1.62% for Class A shares, 2.37% for Class C shares, 1.37% for Class P shares and 1.27% for Institutional Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 12/31/96. Benchmark comparisons began on the fund inception date.

Country Allocation (as of December 31, 2017)

| United States | 48.8% | |||

| Japan | 15.0% | |||

| United Kingdom | 5.9% | |||

| Germany | 4.8% | |||

| Switzerland | 3.1% | |||

| Sweden | 2.5% | |||

| France | 2.2% | |||

| Austria | 1.7% | |||

| Other | 14.0% | |||

| Cash & Equivalents — Net | 2.0% |

| Semiannual Report | | December 31, 2017 | 17 |

Table of Contents

Unaudited

AllianzGI Global Small-Cap Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||

| Class A | Class C | Class P | Institutional Class | |||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||

| Ending Account Value (12/31/17) | $1,140.50 | $1,136.30 | $1,142.00 | $1,142.60 | ||||

| Expenses Paid During Period | $8.74 | $12.76 | $7.40 | $6.86 | ||||

| Hypothetical Performance | ||||||||

| (5% return before expenses) | ||||||||

| Class A | Class C | Class P | Institutional Class | |||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||

| Ending Account Value (12/31/17) | $1,017.04 | $1,013.26 | $1,018.30 | $1,018.80 | ||||

| Expenses Paid During Period | $8.24 | $12.03 | $6.97 | $6.46 | ||||

For each class of the Fund, expenses are equal to the annualized expense ratio for the class (1.62% for Class A, 2.37% for Class C, 1.37% for Class P and 1.27% for Institutional Class), multiplied by the average account value over the period, multiplied by 184/365.

| 18 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 19 |

Table of Contents

Unaudited

AllianzGI Health Sciences Fund

For the period of July1, 2017 through December, 2017, as provided by John Schroer, CFA, Lead Portfolio Manager.

Fund Insights

For the six-month reporting period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Health Sciences Fund (the “Fund”) returned 0.48%, underperforming the MSCI World Health Care Index (the “benchmark”), which returned 3.31%.

Market overview

For the six month period, global health care stocks underperformed the broader averages. The benchmark rose 1.0% versus the S&P 500 and the MSCI World indices’ larger gains. Overall, technology, materials and energy were some of the better performing sectors as investors focused on the more cyclical sectors of the global economy. Health care and utilities were among the worst performing sectors.

US stock markets surged to new all-time highs in December as the congressional passage of tax reform, signs of economic acceleration and pro-business deregulation buoyed markets. Worldwide, global equity markets continue to be supported by relatively accommodative monetary policies and low global interest rates. On monetary policy, the US Federal Reserve (the “Fed”) lifted interest rates an additional quarter point in mid-December. The Fed has indicated that it will raise short term interest rates an additional three times in 2018, and that it will do so very deliberately so as not to disrupt global capital markets. Other developed world central banks, such as the Bank of England, Bank of Japan and the European Central Bank are moving slowly to normalize monetary policy as well.

Portfolio review

Overall, the Fund’s underperformance was primarily driven by adverse stock selection in biotechnology.

An overweight in a large-cap managed-care company, UnitedHealth Group, was the biggest contributor for the six month period. The stock benefitted from solid quarterly earnings reports throughout the year and a strong year in general for stock returns for the large-cap managed-care industry. Another larger contributor to performance was a small-cap biotechnology holding, Exelixis Inc., which was helped by some positive pipeline reports for its advanced tumor treatments. The Fund also benefitted from zero-weights in a variety of drug-related companies, including the generics company, Teva Pharmaceutical, which was victimized by pricing pressure, subsequent earnings deterioration and worries about an overly leveraged balance sheet.

The largest individual detractors to performance were several biotechnology positions and pharmaceutical positions in specialty pharmaceuticals. These biopharmaceutical names encountered quarterly earnings release misses or diminished revenue outlooks, and/or various pipeline disappointments.

Outlook

2017 was a solid year for absolute returns in the global health care sector. Through mid-January of 2018, global stock markets and health care stocks continue to move higher. While we don’t see any immediate warning signs for a significant correction for the health care sector, the November 2018 congressional elections will soon be in focus. In our opinion, these elections could be a catalyst for an increase in general stock market risk and volatility. Additionally, we believe the present calm in the regulatory environment for drug price controls could be altered if the Democratic Party wins the majority control of either the House or Senate. Nonetheless, longer term we are bullish on the secular growth case for health care in general, as a variety of demographic factors support continued growth in global health care spending.

Our focus continues to be on companies and health care industries delivering innovative and profitable drug treatments and cost effective, productivity-enhancing medical solutions. These factors are driving solid long-term earnings growth and, in our opinion, attractive overall valuations for global health care stocks.

| 20 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Health Sciences Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

| AllianzGI Health Sciences Fund Class A | 0.48% | 17.32% | 15.16% | 10.32% | 11.60% | |||||||||||||||||

| AllianzGI Health Sciences Fund Class A (adjusted) | –5.05% | 10.87% | 13.86% | 9.70% | 11.30% | ||||||||||||||||

| AllianzGI Health Sciences Fund Class C | 0.12% | 16.46% | 14.30% | 9.49% | 10.77% | |||||||||||||||||

| AllianzGI Health Sciences Fund Class C (adjusted) | –0.88% | 15.46% | 14.30% | 9.49% | 10.77% | ||||||||||||||||

| AllianzGI Health Sciences Fund Institutional Class | 0.66% | 17.75% | 15.57% | 10.70% | 12.02% | ||||||||||||||||

| MSCI World Health Care Index | 3.31% | 19.80% | 13.88% | 8.94% | 8.59% | ||||||||||||||||

| Lipper Health/Biotech Funds Average | 5.81% | 25.82% | 18.23% | 12.49% | 12.47% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 12/31/96. Benchmark and Lipper comparisons began on the fund inception date.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s expense ratios are 1.46% for Class A shares, 2.21% for Class C shares and 1.11% for Institutional Class Shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 12/31/96. Benchmark comparisons began on the fund inception date.

Industry/Sectors (as of December 31, 2017)

| Biotechnology | 32.6% | |||

| Pharmaceuticals | 28.9% | |||

| Health Care Providers & Services | 16.8% | |||

| Health Care Equipment & Supplies | 12.1% | |||

| Life Sciences Tools & Services | 3.0% | |||

| Diversified Consumer Services | 0.7% | |||

| Cash & Equivalents — Net | 5.9% |

| Semiannual Report | | December 31, 2017 | 21 |

Table of Contents

Unaudited

AllianzGI Health Sciences Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||||||||||

| Class A | Class C | Institutional Class | ||||||||||||||||||

Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | |||||||||||||||||

Ending Account Value (12/31/17) | $1,004.80 | $1,001.20 | $1,006.60 | |||||||||||||||||

Expenses Paid During Period | $7.43 | $11.20 | $5.66 | |||||||||||||||||

| Hypothetical Performance | ||||||||||||||||||||

| (5% return before expenses) | ||||||||||||||||||||

| Class A | Class C | Institutional Class | ||||||||||||||||||

Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | |||||||||||||||||

Ending Account Value (12/31/17) | $1,017.80 | $1,014.01 | $1,019.56 | |||||||||||||||||

Expenses Paid During Period | $7.48 | $11.27 | $5.70 | |||||||||||||||||

For each class of the Fund, expenses are equal to the annualized expense ratio for the class (1.47% for Class A, 2.22% for Class C and 1.12% for Institutional Class ), multiplied by the average account value over the period, multiplied by 184/365.

| 22 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 23 |

Table of Contents

Unaudited

AllianzGI Income & Growth Fund

For the period of July 1, 2017, through December 31, 2017, as provided by Doug Forsyth, CFA, Portfolio Manager.

Fund Insights

For the six-month period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Income & Growth Fund (the “Fund”) returned 6.54%. During the same period, the S&P 500 Index gained 11.42% and the overall U.S. bond market, as measured by the Bloomberg Barclays US Aggregate Bond Index, returned 1.24%. The convertible universe returned 5.39%, as measured by the ICE BofA Merrill Lynch All US Convertibles Index; and high yield bonds, as measured by the ICE BofA Merrill Lynch US High Yield Master II Index, rose 2.45%. Lastly, the Russell 1000 Growth Index increased 14.23%.

Market Overview

Several factors influenced the three key markets including economic trends, corporate fundamentals, the US Federal Reserve’s (the “Fed’s”) actions and commentary, tax reform and rising commodity prices.

Strong US economic trends supported the market over the period. Housing prices rose and existing home sales reached the highest level in a decade. Manufacturing and nonmanufacturing indexes signaled expanding activity and US GDP growth exceeded 3% for the second straight quarter. In addition, consumer spending benefited from benign inflation and steady job gains.

Credit trends showed sustained improvement as most high-yield bond and convertible bond issuers reported financial results and provided outlooks that met or exceeded expectations. In particular, net leverage and interest coverage for the high-yield market were better quarter over quarter and year over year. With respect to large-cap equities, the third quarter marked another period of year-over-year earnings growth.

The Fed increased its benchmark interest rate by 25 basis points in December for a third time this year, to a range of 1.25% to 1.50%. A measured approach by the Fed, extended accommodation by central banks overseas and the expectation of monetary policy continuity under designated new Federal Reserve Board Chair Jerome Powell were market-supportive developments.

All three markets also benefited from optimism tied to tax reform progress and the resulting expectation of greater corporate profitability. The final tax bill included several positive elements such as a reduction in the corporate tax rate and the immediate expensing of capital expenditures. On balance, the prospect of US companies capturing tax savings lifted investor sentiment.

A synchronized global recovery and continued improvement in industry dynamics helped commodity-related sectors, which were among the market’s best performers. Crude oil settled above $60 a barrel, a two-year high, amid ebbing oversupply fears capped by rising demand and an extension of the production-cut agreement. Copper and other base metals also gained.

Against this backdrop, the trend of subdued volatility continued to persist as had been documented throughout the calendar year. The Chicago Board Options Exchange Volatility Index hit long-term lows multiple times and troughed intra-day with a sub-9 reading near the Christmas holiday.

Portfolio Review

The Fund provided consistent income—the primary goal of the fund—and a positive total return over the trailing six-month period.

In the equity sleeve, industrials, health care and consumer discretionary were the greatest contributors to relative performance. Conversely, only the energy sector detracted.

In the convertible sleeve, sectors that contributed positively to relative performance were energy, consumer staples and financials. On the other hand, technology, health care and industrials pressured relative performance.

In the high yield sleeve, industries that aided relative performance were retail, cable & satellite television and food & drug retailers. In contrast, energy, telecommunications and support-services hampered relative performance.

The covered call strategy captured some gains, but many option profits were offset as the covered call option sleeve was actively managed.

Outlook

US equity markets continue to record new all-time highs, volatility is near all-time lows and we believe the global economic outlook continues to improve. Historically, these factors have been positive indicators for corporate earnings growth and supportive of investments in risk assets.

| 24 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Income & Growth Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

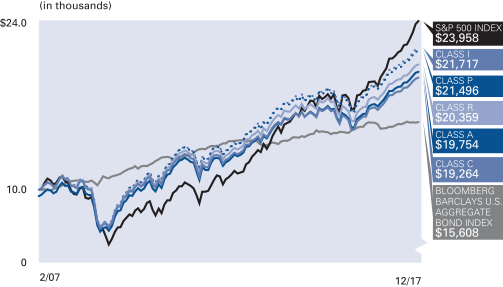

| AllianzGI Income & Growth Fund Class A | 6.54% | 13.45% | 8.61% | 6.70% | 7.04% | |||||||||||||||||

| AllianzGI Income & Growth Fund Class A (adjusted) | 0.68% | 7.21% | 7.39% | 6.10% | 6.48% | ||||||||||||||||

| AllianzGI Income & Growth Fund Class C | 6.19% | 12.63% | 7.80% | 5.91% | 6.24% | |||||||||||||||||

| AllianzGI Income & Growth Fund Class C (adjusted) | 5.19% | 11.63% | 7.80% | 5.91% | 6.24% | ||||||||||||||||

| AllianzGI Income & Growth Fund Class R | 6.42% | 13.17% | 8.33% | 6.44% | 6.78% | ||||||||||||||||

| AllianzGI Income & Growth Fund Class P | 6.70% | 13.79% | 8.88% | 6.98% | 7.32% | ||||||||||||||||

| AllianzGI Income & Growth Fund Institutional Class | 6.70% | 13.87% | 8.98% | 7.08% | 7.42% | ||||||||||||||||

| S&P 500 Index | 11.42% | 21.83% | 15.79% | 8.50% | 8.39% | ||||||||||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 1.24% | 3.54% | 2.10% | 4.01% | 4.19% | ||||||||||||||||

| Lipper Flexible Portfolio Funds Average | 6.23% | 12.73% | 6.18% | 4.43% | 4.91% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 2/28/07. Benchmark and Lipper comparisons began on the fund inception date.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s expense ratios are 1.29% for Class A shares, 2.04% for Class C shares, 1.54% for Class R shares, 1.04% for Class P shares and 0.94% for Institutional Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 2/28/07. Benchmark comparisons began on the fund inception date.

Industry/Sectors (as of December 31, 2017)

| Software | 7.3% | |||

| Oil, Gas & Consumable Fuels | 5.7% | |||

| Media | 5.7% | |||

| Semiconductors | 5.1% | |||

| Internet | 4.3% | |||

| Biotechnology | 4.0% | |||

| Pharmaceuticals | 4.0% | |||

| Telecommunications | 3.8% | |||

| Other | 57.1% | |||

| Cash & Equivalents — Net (including Options Written) | 3.0% |

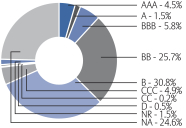

S&P Ratings* (as of December 31, 2017)

| * | As a percentage of fixed-income investments. Bond ratings refer to the underlying holdings of the Fund and are categorized from highest to lowest credit quality using ratings provided by S&P Global Ratings (“S&P”). S&P’s ratings have been selected for several reasons, including the portfolio managers’ usage of S&P ratings methodology among other credit quality information in managing the Fund, access to background information and other materials provided by S&P, as well as the Fund’s consideration of industry practice. The Fund also displays S&P credit ratings information in materials provided in client presentations. See “Important Information” for more detail on the selection of S&P for the Fund’s ratings presentation. Securities not rated by S&P and bonds that do not currently have a rating available are designated in the chart as “NR” and “NA”, respectively. |

| Semiannual Report | | December 31, 2017 | 25 |

Table of Contents

Unaudited

AllianzGI Income & Growth Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class C | Class R | Class P | Institutional Class | ||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (12/31/17) | $1,065.40 | $1,061.90 | $1,064.20 | $1,067.00 | $1,067.00 | |||||

| Expenses Paid During Period | $6.72 | $10.60 | $8.01 | $5.42 | $4.90 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | ||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (12/31/17) | $1,018.70 | $1,014.92 | $1,017.44 | $1,019.96 | $1,020.47 | |||||

| Expenses Paid During Period | $6.56 | $10.36 | $7.83 | $5.30 | $4.79 | |||||

For each class of the Fund, expenses (net of fee waivers) are equal to the annualized expense ratio for the class (1.29% for Class A, 2.04% for Class C, 1.54% for Class R, 1.04% for Class P and 0.94% for Institutional Class), multiplied by the average account value over the period, multiplied by 184/365.

| 26 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 27 |

Table of Contents

Unaudited

For the period July 1, 2017 through December 31, 2017, as provided by Steven Klopukh, CFA, Lead Portfolio Manager.

Fund Insights

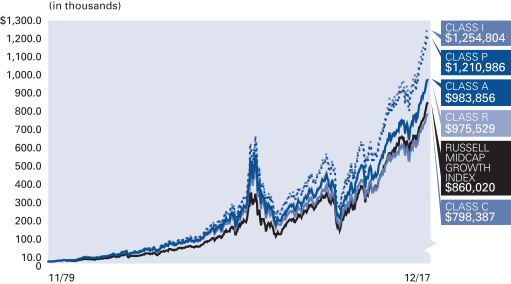

For the six-month period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI Mid-Cap Fund (the “Fund”) returned 10.90%, underperforming the Russell Midcap Growth Index (the “benchmark”), which returned 12.45%.

Market Overview

US equities posted strong returns over the period, with major indices continuing to reach new highs. Large- and mid-caps outperformed small-caps, and growth beat their value counterparts across the market cap spectrum. Share prices were supported by better-than-expected earnings, renewed merger and acquisitions activity, and optimism over the prospects for tax reform. The Senate approved plans for $1.5 trillion of tax cuts, the most sweeping overhaul of the US tax system in more than three decades.

Portfolio Review

Stock selection added notably to returns within consumer staples and industrials, although this was offset by stock selection in consumer discretionary and health care. Sector allocation overall was a modest detractor from returns.

The top contributor to relative returns was XPO Logistics, Inc., a global freight, transportation and logistics company, specializing in e-commerce. We initiated a position in June 2017. XPO enjoys a niche in delivering large items to the home, such as furniture or large consumer appliances, and then even unpacking and installing some items. Share gains were helped by news that Home Depot had expressed interest in acquiring the company. The fit would be complementary for Home Depot and keep XPO out of the hands of Amazon, which is expanding into the sale of larger items.

In contrast, consumer and commercial products company Newell Brands was the top detractor from relative returns. It is known for brands including Coleman, Sharpie pens, First Alert, and Mr. Coffee. Its e-commerce business was strong although there were significant declines in back-to-school related sales from its writing business segment. The company is absorbing commodity price increases while it works through excess inventories. The stock is trading at a discount to peers and versus its historical average. We saw an attractive risk/reward at these levels and added to the position on weakness.

As of December 31, 2017, the largest sector allocation was in information technology, followed by industrials and health care. The Fund held no stocks in energy, telecommunication services or utilities.

Outlook

US equity markets are coming off of a remarkably strong 2017. Since bottoming in early 2009, we have witnessed one of the longest equity market rallies. While concerns have focused on US equity valuations, they have been supported by low interest rates, double digit earnings growth, and the prospect, finally realized, of tax reform. We believe lower corporate tax rates should significantly help more domestically focused companies. Mid-cap stocks generally tend to pay higher effective tax rates and could be greater beneficiaries of lower tax rates and repatriation.

Uncertainties include just how fast interest rates across the yield curve will rise, and whether inflationary pressures ultimately become more visible. One key development that we would welcome is a return to more normal monetary policy. As central banks wind down their balance sheets, we believe share price performance is more likely to be driven by company fundamentals than by liquidity. This should, in our view, usher in more of a stock picker’s market, favoring active management.

As always, we continue to focus on stock selection, seeking to invest in high-quality, mid-cap companies with superior growth prospects that are attractively valued. Our portfolio emphasizes free cash flow yield and responsible capital allocation.

| 28 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Mid-Cap Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

| AllianzGI Mid-Cap Fund Class A | 10.90% | 24.93% | 15.12% | 8.18% | 12.95% | |||||||||||||||||

| AllianzGI Mid-Cap Fund Class A (adjusted) | 4.80% | 18.06% | 13.82% | 7.57% | 12.78% | ||||||||||||||||

| AllianzGI Mid-Cap Fund Class C | 10.24% | 23.83% | 14.24% | 7.38% | 12.17% | |||||||||||||||||

| AllianzGI Mid-Cap Fund Class C (adjusted) | 9.26% | 22.83% | 14.24% | 7.38% | 12.17% | ||||||||||||||||

| AllianzGI Mid-Cap Fund Class R | 10.75% | 24.22% | 14.83% | 7.94% | 12.76% | ||||||||||||||||

| AllianzGI Mid-Cap Fund Class P | 10.92% | 25.27% | 15.37% | 8.47% | 13.40% | ||||||||||||||||

| AllianzGI Mid-Cap Fund Institutional Class | 10.85% | 25.11% | 15.44% | 8.55% | 13.50% | ||||||||||||||||

| AllianzGI Mid-Cap Fund Administrative Class | 10.58% | 24.83% | 15.16% | 8.27% | 13.20% | |||||||||||||||||

| Russell Midcap Growth Index | 12.45% | 25.27% | 15.30% | 9.10% | 12.38% | ||||||||||||||||

| Lipper Mid-Cap Growth Funds Average | 10.46% | 24.63% | 13.79% | 7.64% | 10.07% | |||||||||||||||||

| Lipper Multi-Cap Growth Funds Average | 11.88% | 28.04% | 14.82% | 8.13% | — | |||||||||||||||||

* Cumulative return

† The Fund began operations on 11/6/79. Benchmark and primary Lipper performance comparisons began on 10/31/79; secondary Lipper performance is available for trailing 10 years.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s expense ratios are 1.14% for Class A shares, 1.89% for Class C shares, 1.39% for Class R shares, 0.89% for Class P shares, 0.79% for Institutional Class shares and 1.04% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 11/6/79. Benchmark performance comparisons began on 10/31/79.

Industry/Sectors (as of December 31, 2017)

| Software | 8.7% | |||

| Electronic Equipment, Instruments & Components | 7.7% | |||

| Health Care Equipment & Supplies | 7.1% | |||

| Semiconductors & Semiconductor Equipment | 6.1% | |||

| Chemicals | 4.7% | |||

| Capital Markets | 4.0% | |||

| Life Sciences Tools & Services | 3.9% | |||

| Professional Services | 3.8% | |||

| Other | 53.3% | |||

| Cash & Equivalents — Net | 0.7% |

| Semiannual Report | | December 31, 2017 | 29 |

Table of Contents

Unaudited

AllianzGI Mid-Cap Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Administrative Class | |||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (12/31/17) | $1,109.00 | $1,102.40 | $1,107.50 | $1,109.20 | $1,108.50 | $1,105.80 | ||||||

| Expenses Paid During Period | $6.06 | $10.02 | $7.38 | $4.73 | $4.20 | $5.52 | ||||||

| Hypothetical Performance | ||||||||||||

| (5% return before expenses) | ||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Administrative Class | |||||||

| Beginning Account Value (7/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (12/31/17) | $1,019.46 | $1,015.68 | $1,018.20 | $1,020.72 | $1,021.22 | $1,019.96 | ||||||

| Expenses Paid During Period | $5.80 | $9.60 | $7.07 | $4.53 | $4.02 | $5.30 | ||||||

For each class of the Fund, expenses are equal to the annualized expense ratio for the class (1.14% for Class A, 1.89% for Class C, 1.39% for Class R, 0.89% for Class P, 0.79% for Institutional Class and 1.04% for Administrative Class), multiplied by the average account value over the period, multiplied by 184/365.

| 30 | December 31, 2017 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | December 31, 2017 | 31 |

Table of Contents

Unaudited

AllianzGI NFJ Dividend Value Fund

For the period July 1, 2017 through December 31, 2017, as provided by the Dallas Investment team.

Fund Insights

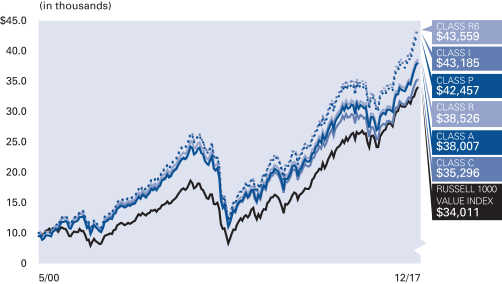

For the six-month period ended December 31, 2017, Class A shares at net asset value (“NAV”) of the AllianzGI NFJ Dividend Value Fund (the “Fund”) returned 11.30%, outperforming the Russell 1000 Value Index (the “benchmark”), which returned 8.61%.

Market Overview

Over the reporting period, US equities delivered double-digit gains as large-cap indices touched a series of fresh peaks and smaller companies reached a record high in the closing days of the year. Share prices were buoyed by better-than-expected company earnings, renewed merger & acquisition activity, and optimism over the prospects for tax reform. In December, the Senate approved plans for USD 1.5 trillion of tax cuts, the most sweeping overhaul of the US tax system in more than three decades. In general, growth stocks outperformed their value counterparts. The US Federal Reserve (the “Fed”) continued to gradually normalize monetary policy, announcing it would start to reduce the USD 4.5 trillion of Treasury bonds and mortgage-backed backed securities it amassed through its quantitative easing programs. In December, the Fed raised interest rates by 25 basis points to a range of 1.25%-1.50%, and maintained its forecasts for three further rises in 2018 followed by two in 2019.

Portfolio Review

The Fund delivered a double-digit gain of 11.30% (A-shares, net of fees) over the trailing six-month period, outperforming its benchmark, which returned 8.61%. Relative performance results were due to positive stock selection and sector allocation. Selection across the consumer staples, health care and utilities sectors was strong, and offset holdings in the materials and consumer discretionary sectors that failed to keep pace with benchmark shares. During the latter half of the year, interest rate sensitive areas of the market stumbled, and the Fund’s underweights in the bond-proxy sectors, such as real estate and consumer staples, contributed to performance. An overweight in information technology was also additive, as tech names continued to perform well over the second half of the year. The lone detractor from an allocation standpoint was the Fund’s overweight in Industrials—the second weakest sector in the benchmark with a paltry 2% return during the reporting period.

Outlook

The 2017 calendar year was a notable period for equities, with markets reaching all-time highs in ten out of twelve months during the year. Monetary policy was also noteworthy in 2017, with the Fed removing liquidity from the system and some global central banks beginning their tightening cycles (e.g. Bank of England, European Central Bank and People’s Bank of China). The addition of US tax reform, which passed at year end, to a tightening environment, in our view, may be conducive to increased volatility across equity markets. Though the Chicago Board Options Exchange Volatility Index ended the year at 11, its long term average is close to double that at 20.5. With interest rates beginning to move upward, investors may find themselves looking beyond equities to access sufficient portfolio returns. Increased volatility typically ushers in lower correlations and higher dispersions in risk assets, and we believe active managers will be important resources to help investors sift through market winners and losers.

We believe our dividend and value-oriented equity portfolios have the potential to provide additional protection when investing in equities. Our dividend focus, for example, positions our portfolios with an inherent advantage relative to the benchmark, as dividends provide a tangible return and more predictable current income. Historical studies also suggest that dividend-paying stocks have exhibited less volatility than non-dividend paying securities. We believe these characteristics have been an important contributing factor to our portfolios’ history of downside relative performance. As US equity markets continue their meteoric rise, our team continues to identify investment opportunities with compelling valuations and stable earnings growth. Though we cannot predict when today’s bull market will run its course, we can design portfolios that seek attractive valuations that we believe will participate on the upside and aim to protect on the downside for our investors.

| 32 | December 31, 2017 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI NFJ Dividend Value Fund (cont’d)

Average Annual Total Return for the period ended December 31, 2017

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class A | 11.30% | 15.70% | 11.56% | 5.15% | 8.21% | |||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class A (adjusted) | 5.18% | 9.33% | 10.30% | 4.55% | 7.86% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class C | 10.91% | 14.85% | 10.72% | 4.36% | 7.40% | |||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class C (adjusted) | 10.03% | 13.94% | 10.72% | 4.36% | 7.40% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class R | 11.19% | 15.44% | 11.28% | 4.89% | 7.94% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Class P | 11.49% | 15.99% | 11.85% | 5.42% | 8.54% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Institutional Class | 11.47% | 16.08% | 11.95% | 5.52% | 8.64% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund R6 | 11.54% | 16.21% | 12.00% | 5.57% | 8.70% | ||||||||||||||||

| AllianzGI NFJ Dividend Value Fund Administrative Class | 11.34% | 15.81% | 11.67% | 5.26% | 8.37% | |||||||||||||||||

| Russell 1000 Value Index | 8.61% | 13.66% | 14.04% | 7.10% | 7.18% | ||||||||||||||||

| Lipper Equity Income Funds Average | 9.20% | 15.45% | 12.31% | 6.99% | 6.81% | |||||||||||||||||

* Cumulative return

† The Fund began operations on 5/8/00. Benchmark comparisons began on the fund inception date. Lipper comparisons began on 4/30/00.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1% contingent deferred sales charge (CDSC) on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Please see pages 60-62 for more information. The Fund’s gross expense ratios are 1.09% for Class A shares, 1.84% for Class C shares, 1.34% for Class R shares, 0.84% for Class P shares, 0.74% for Institutional Class shares, 0.69% for R6 shares and 0.99% for Administrative Class shares. These ratios do not include an expense reduction, contractually agreed through at least October 31, 2018. The Fund’s expense ratios net of this reduction are 0.94% for Class A shares, 1.69% for Class C shares, 1.19% for Class R shares, 0.69% for Class P shares, 0.59% for Institutional Class shares, 0.54% for Class R6 shares and 0.84% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated August 30, 2017, as supplemented to date.

Cumulative Returns Through December 31, 2017

The Fund began operations on 5/8/00. Benchmark comparisons began on the fund inception date.

Industry/Sectors (as of December 31, 2017)

| Banks | 15.8% | |||

| Oil, Gas & Consumable Fuels | 10.1% | |||

| Insurance | 6.0% | |||

| Diversified Telecommunication Services | 4.1% | |||

| Aerospace & Defense | 4.0% | |||