UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | | | | | |

| Investment Company Act file number | 811-06441

|

| | |

| AMERICAN CENTURY INTERNATIONAL BOND FUNDS |

| (Exact name of registrant as specified in charter) |

| | |

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 |

| (Address of principal executive offices) | (Zip Code) |

| | |

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 |

| (Name and address of agent for service) |

| | |

| Registrant’s telephone number, including area code: | 816-531-5575 |

| | |

| Date of fiscal year end: | 10-31 |

| | |

| Date of reporting period: | 10-31-2017 |

ITEM 1. REPORTS TO STOCKHOLDERS.

|

| |

| | |

| | Annual Report |

| | |

| | October 31, 2017 |

| | |

| | Emerging Markets Debt Fund |

|

| | |

| President’s Letter | 2 |

|

| Performance | 3 |

|

| Portfolio Commentary | |

|

| Fund Characteristics | |

|

| Shareholder Fee Example | |

|

| Schedule of Investments | |

|

| Statement of Assets and Liabilities | |

|

| Statement of Operations | |

|

| Statement of Changes in Net Assets | |

|

| Notes to Financial Statements | |

|

| Financial Highlights | |

|

| Report of Independent Registered Public Accounting Firm | |

|

| Management | |

|

| Approval of Management Agreement | |

|

| Additional Information | |

|

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Jonathan Thomas

Jonathan Thomas

Dear Investor:

Thank you for reviewing this annual report for the period ended October 31, 2017. Annual reports help convey important information about fund returns, including market factors that affected performance during the reporting period. For additional, updated investment and market insights, we encourage you to visit our website, americancentury.com.

‘Risk-On’ Sentiment Sparked Strong Gains Among Stocks

U.S. stocks delivered robust double-digit gains for the reporting period. The “risk-on” rally began early in the period, following Donald Trump’s election victory in November 2016. Investor expectations for President Trump’s administration to usher in pro-growth policies and reforms drove stock prices higher. In addition, healthy corporate earnings growth and improving gross domestic product (GDP) and other economic data provided additional support for stocks. Against this backdrop, the S&P 500 Index reached several milestone levels during the period and returned 23.63%. In terms of equity styles, riskier and economically sensitive stocks generally remained in favor. For example, small-cap stocks generally outperformed their mid- and large-cap peers, while growth stocks broadly outperformed their value counterparts across the capitalization spectrum. Real estate investment trusts (REITs) advanced, but global property stocks significantly underperformed the broader stock market as interest rates increased, most notably in the U.S., where the Federal Reserve (Fed) raised rates three times during the period.

As stocks soared in the post-election environment, global bonds sold off sharply. President Trump’s policy agenda fueled inflation fears that sent global bond yields sharply higher in late 2016. However, broad bond market performance generally recovered beginning in early 2017, advancing on subdued inflation and continued central bank accommodation to post modest gains for the entire reporting period. Investor preferences for risk also extended to the global fixed-income market, where high-yield corporate and emerging markets bonds were top performers.

As Congress considers tax cuts and other pro-growth reforms and the Fed and other central banks pursue policy normalization, investors likely will face new opportunities and challenges in the months ahead. We continue to believe in a disciplined, diversified, and risk-aware approach, using professionally managed portfolios in pursuit of investment goals. We appreciate your continued trust in us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

|

| | | | |

| Total Returns as of October 31, 2017 |

| | | | Average

Annual Returns | |

| | Ticker Symbol | 1 year | Since Inception | Inception Date |

| Investor Class | AEDVX | 5.11% | 4.96% | 7/29/14 |

| JPMorgan Corporate Emerging Market Bond (CEMBI) Broad Diversified Index | — | 6.18% | 5.14% | — |

| I Class | AEHDX | — | 3.28% | 4/10/17 |

| Y Class | AEYDX | — | 3.33% | 4/10/17 |

| A Class | AEDQX | | | 7/29/14 |

| No sales charge | | 4.84% | 4.72% | |

| With sales charge | | 0.09% | 3.25% | |

| C Class | AEDHX | 4.07% | 3.94% | 7/29/14 |

| R Class | AEDWX | 4.58% | 4.45% | 7/29/14 |

| R5 Class | AEDJX | 5.31% | 5.17% | 7/29/14 |

| R6 Class | AEXDX | 5.37% | 5.25% | 7/29/14 |

Prior to April 10, 2017, the R5 Class was referred to as the Institutional Class.

Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 4.50% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

|

|

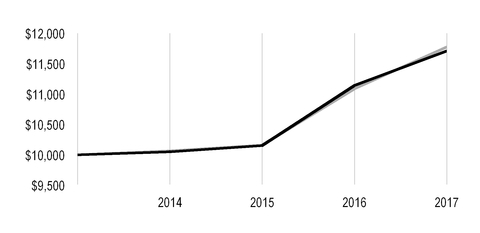

| Growth of $10,000 Over Life of Class |

| $10,000 investment made July 29, 2014 |

| Performance for other share classes will vary due to differences in fee structure. |

|

| |

| Value on October 31, 2017 |

| | Investor Class — $11,710 |

| |

| | JPMorgan CEMBI Broad Diversified Index — $11,776 |

| |

|

| | | | | | | |

| Total Annual Fund Operating Expenses |

| Investor Class | I Class | Y Class | A Class | C Class | R Class | R5 Class | R6 Class |

| 0.97% | 0.87% | 0.77% | 1.22% | 1.97% | 1.47% | 0.77% | 0.72% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Total returns for periods less than one year are not annualized. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. For additional information about the fund, please consult the prospectus.

Portfolio Managers: Margé Karner, Kevin Akioka, John Lovito, and Brian Howell

Performance Summary

Emerging Markets Debt returned 5.11%* for the fiscal year ended October 31, 2017. By comparison, the fund’s benchmark, the JPMorgan Corporate Emerging Market Bond (CEMBI) Broad Diversified Index, returned 6.18% over the same time period. (Portfolio returns reflect operating expenses, while index returns do not.)

Market Review

Emerging markets debt advanced for the reporting period, boosted by synchronized global growth, firming commodity prices, and gradually rising interest rates. Record inflows, driven primarily by strong investor demand for yield, contributed to narrowing emerging market spreads. Strong technical support from investor inflows and a benign global backdrop resulted in resilience of the asset class, despite heightened political risks in some large markets (such as Brazil and South Africa), increased tensions in the Middle East and North Korea, and uncertainty related to monetary policy normalization in the U.S. and in Europe. Positive factors influencing emerging markets debt performance included a rebound in commodity prices (particularly oil and copper), U.S. dollar weakness, and continued strong economic data from China. The outcome of France’s presidential election, where victory for Emmanuel Macron eased market concerns about nationalist populism in Europe, along with growth momentum in developed markets were also positive influences.

In this environment, lower-quality bonds generally outpaced investment-grade securities, as investors gravitated to higher-yielding segments of the market and emerging markets debt. Boosted by appreciating currencies and falling inflation, local sovereign debt generated strong returns. Among U.S. dollar-denominated emerging markets debt, the frontier markets were top performers, and the lowest-rated corporate issuers (B and below) generated more than double the returns compared with investment-grade issuers. Latin America, Argentina, and Brazil were also strong performers, while higher-rated Asian and European countries underperformed.

Defensive Positioning Detracted from Results

As the reporting period progressed, we positioned the portfolio more defensively, lowering risk as valuations became less attractive. We believed the credit spreads of most lower-quality bonds did not appropriately reflect idiosyncratic credit risks and prevailing market risks. This positioning weighed on portfolio performance, as lower-quality debt significantly outperformed investment-grade credit. However, our positioning provided some upside by helping the portfolio avoid problematic debt represented in the index. There were no defaults, distressed exchanges, or bonds trading at distressed levels in the portfolio.

Country Allocations Added Value

The portfolio experienced positive performance from country allocation as well as security selection in several countries. Overweight positions and security selection in Argentina and Mexico were top contributors to the portfolio, while underweight allocations and security selection in South Korea, Hong Kong, and Israel also added to performance. On the negative side, our lack of exposure to

*All fund returns referenced in this commentary are for Investor Class shares. Performance for other share classes will vary due to differences in fee structure; when Investor Class performance exceeds that of the fund's benchmark, other share classes may not. See page 3 returns for all share classes.

strong-performing frontier countries weighed on relative results. Security selection in Brazil and Turkey, where we focused on higher quality issuers due to challenging macroeconomic environments and heightened political risks in those countries, also detracted from relative performance.

Sector Positioning Delivered Mixed Results

An underweight position in the top-performing metals and mining sector detracted from relative results, but security selection within the sector helped offset some of the negative allocation effect. On the positive side, an underweight position and security selection in the consumer sector contributed to performance. This was partly due to not having exposure to certain companies in the index with problematic debt. Underweight positions in the utilities and financials sectors and security selection in the industrials sector contributed to performance. In addition, overweight positions in the oil and gas sector and in sovereign debt helped.

Positioning for the Future

Looking ahead, we believe the extended strong rally in the emerging markets debt asset class combined with Federal Reserve normalization, European Central Bank tapering, U.S. trade policy, and increased geopolitical tension warrant a cautious approach. Although emerging markets fundamentals have improved, we believe valuations in external corporate debt, particularly in the lowest-quality segments, have run ahead of fundamentals. However, we are beginning to see some adjustment, particularly in the high-yield corporate debt sector. We continue to remain selective and limit the exposure to countries and issuers with solid or improving fundamentals that offer an attractive risk/reward profile to investors.

|

| |

| OCTOBER 31, 2017 |

| Portfolio at a Glance |

| Average Duration (effective) | 4.7 years |

| Weighted Average Life | 6.3 years |

| | |

| Holdings by Country | % of net assets |

| Turkey | 12.6% |

| China | 10.7% |

| Russia | 9.2% |

| Brazil | 8.1% |

| Colombia | 5.4% |

| India | 4.3% |

| Hong Kong | 4.3% |

| Qatar | 4.1% |

| Argentina | 4.1% |

| Mexico | 4.0% |

| Other Countries | 28.8% |

| Cash and Equivalents* | 4.4% |

| *Includes temporary cash investments and other assets and liabilities. |

| | |

| Types of Investments in Portfolio | % of net assets |

| Corporate Bonds | 88.8% |

| Sovereign Governments and Agencies | 6.7% |

| Common Stocks | 0.1% |

| U.S. Treasury Securities | —** |

| Temporary Cash Investments | 2.8% |

| Other Assets and Liabilities | 1.6% |

**Category is less than 0.05% of total net assets.

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from May 1, 2017 to October 31, 2017.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or I Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

| | | | |

| | Beginning

Account Value

5/1/17 | Ending

Account Value

10/31/17 | Expenses Paid

During Period(1)

5/1/17 - 10/31/17 |

Annualized

Expense Ratio(1) |

| Actual | | | | |

| Investor Class | $1,000 | $1,022.30 | $4.94 | 0.97% |

| I Class | $1,000 | $1,023.80 | $4.44 | 0.87% |

| Y Class | $1,000 | $1,024.20 | $3.93 | 0.77% |

| A Class | $1,000 | $1,022.00 | $6.22 | 1.22% |

| C Class | $1,000 | $1,018.10 | $10.02 | 1.97% |

| R Class | $1,000 | $1,019.70 | $7.48 | 1.47% |

| R5 Class | $1,000 | $1,023.30 | $3.93 | 0.77% |

| R6 Class | $1,000 | $1,024.50 | $3.67 | 0.72% |

| Hypothetical | | | | |

| Investor Class | $1,000 | $1,020.32 | $4.94 | 0.97% |

| I Class | $1,000 | $1,020.82 | $4.43 | 0.87% |

| Y Class | $1,000 | $1,021.32 | $3.92 | 0.77% |

| A Class | $1,000 | $1,019.06 | $6.21 | 1.22% |

| C Class | $1,000 | $1,015.28 | $10.01 | 1.97% |

| R Class | $1,000 | $1,017.80 | $7.48 | 1.47% |

| R5 Class | $1,000 | $1,021.32 | $3.92 | 0.77% |

| R6 Class | $1,000 | $1,021.58 | $3.67 | 0.72% |

| |

| (1) | Expenses are equal to the class's annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 184, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. Annualized expense ratio reflects actual expenses, including any applicable fee waivers or expense reimbursements and excluding any acquired fund fees and expenses. |

OCTOBER 31, 2017

|

| | | | | | | |

| | | Principal Amount | Value |

| CORPORATE BONDS — 88.8% | | | |

| Algeria — 0.6% | | | |

GTH Finance BV, 7.25%, 4/26/23(1) | | $ | 200,000 |

| $ | 226,971 |

|

| Argentina — 3.2% | | | |

Banco Macro SA, VRN, 6.75%, 11/4/21(2) | | 300,000 |

| 317,100 |

|

| Pampa Energia SA, 7.50%, 1/24/27 | | 200,000 |

| 219,160 |

|

| YPF SA, 6.95%, 7/21/27 | | 300,000 |

| 321,375 |

|

| YPF SA, 8.50%, 7/28/25 | | 300,000 |

| 349,800 |

|

| | | | 1,207,435 |

|

| Brazil — 8.1% | | | |

Azul Investments LLP, 5.875%, 10/26/24(1) | | 300,000 |

| 300,450 |

|

Braskem Netherlands Finance BV, 4.50%, 1/10/28(1) | | 400,000 |

| 398,260 |

|

Globo Comunicacao e Participacoes SA, 5.125%, 3/31/27(1) | | 200,000 |

| 204,500 |

|

| Minerva Luxembourg SA, 6.50%, 9/20/26 | | 300,000 |

| 311,715 |

|

| Petrobras Global Finance BV, 3.00%, 1/15/19 | | 1,000,000 |

| 1,001,790 |

|

| Petrobras Global Finance BV, 7.25%, 3/17/44 | | 300,000 |

| 315,375 |

|

| Petrobras Global Finance BV, 8.75%, 5/23/26 | | 200,000 |

| 242,750 |

|

Suzano Austria GmbH, 5.75%, 7/14/26(1) | | 300,000 |

| 323,850 |

|

| | | | 3,098,690 |

|

| Chile — 2.9% | | | |

| Cencosud SA, 6.625%, 2/12/45 | | 300,000 |

| 328,109 |

|

Colbun SA, 3.95%, 10/11/27(1) | | 200,000 |

| 200,175 |

|

SACI Falabella, 3.75%, 10/30/27(1) | | 300,000 |

| 294,000 |

|

| Transelec SA, 3.875%, 1/12/29 | | 300,000 |

| 299,250 |

|

| | | | 1,121,534 |

|

| China — 9.9% | | | |

| Baidu, Inc., 2.75%, 6/9/19 | | 200,000 |

| 202,163 |

|

| Baidu, Inc., 3.625%, 7/6/27 | | 400,000 |

| 402,912 |

|

| China Overseas Finance Cayman III Ltd., 3.375%, 10/29/18 | | 500,000 |

| 505,843 |

|

| China Overseas Finance Cayman V Ltd., 3.95%, 11/15/22 | | 200,000 |

| 208,377 |

|

| CITIC Ltd., MTN, 6.80%, 1/17/23 | | 200,000 |

| 234,586 |

|

| CNOOC Finance 2013 Ltd., 3.00%, 5/9/23 | | 300,000 |

| 301,842 |

|

| CNPC General Capital Ltd., 2.75%, 5/14/19 | | 400,000 |

| 402,684 |

|

| CRCC Yuxiang Ltd., 3.50%, 5/16/23 | | 200,000 |

| 205,890 |

|

| Sinopec Group Overseas Development 2016 Ltd., 2.125%, 5/3/19 | | 400,000 |

| 398,954 |

|

Sinopec Group Overseas Development Ltd., 2.50%, 4/28/20(1) | | 200,000 |

| 200,317 |

|

Sinopec Group Overseas Development Ltd., 2.25%, 9/13/20(1) | | 500,000 |

| 497,517 |

|

State Grid Overseas Investment 2016 Ltd., 3.50%, 5/4/27(1) | | 200,000 |

| 204,362 |

|

| | | | 3,765,447 |

|

| Colombia — 5.3% | | | |

| Bancolombia SA, 5.125%, 9/11/22 | | 130,000 |

| 137,033 |

|

Bancolombia SA, VRN, 4.875%, 10/18/22(2) | | 400,000 |

| 400,300 |

|

|

| | | | | | | |

| | | Principal Amount | Value |

| Colombia Telecomunicaciones SA, 8.50%, 12/29/49 | | $ | 100,000 |

| $ | 107,250 |

|

| Ecopetrol SA, 5.875%, 5/28/45 | | 300,000 |

| 297,750 |

|

| Grupo Aval Ltd., 4.75%, 9/26/22 | | 250,000 |

| 255,625 |

|

Millicom International Cellular SA, 5.125%, 1/15/28(1) | | 500,000 |

| 505,000 |

|

| SUAM Finance BV, 4.875%, 4/17/24 | | 300,000 |

| 322,950 |

|

| | | | 2,025,908 |

|

| Dominican Republic — 0.9% | | | |

Aeropuertos Dominicanos Siglo XXI SA, 6.75%, 3/30/29(1) | | 300,000 |

| 326,625 |

|

| Guatemala — 0.6% | | | |

| Comcel Trust via Comunicaciones Celulares SA, 6.875%, 2/6/24 | | 200,000 |

| 212,000 |

|

| Hong Kong — 4.3% | | | |

Bank of East Asia Ltd. (The), MTN, VRN, 4.25%, 11/20/19(2) | | 200,000 |

| 204,074 |

|

| China CITIC Bank International Ltd., MTN, 6.875%, 6/24/20 | | 200,000 |

| 217,909 |

|

CK Hutchison International 17 II Ltd., 2.25%, 9/29/20(1) | | 500,000 |

| 498,454 |

|

| CK Hutchison International 17 Ltd., 3.50%, 4/5/27 | | 600,000 |

| 605,149 |

|

| Hutchison Whampoa International 09 Ltd., 7.625%, 4/9/19 | | 100,000 |

| 107,593 |

|

| | | | 1,633,179 |

|

| India — 4.3% | | | |

| Bharti Airtel International (Netherlands) BV, 5.125%, 3/11/23 | | 600,000 |

| 643,788 |

|

| ICICI Bank Ltd., 5.75%, 11/16/20 | | 200,000 |

| 217,556 |

|

| ONGC Videsh Ltd., 4.625%, 7/15/24 | | 200,000 |

| 214,905 |

|

| Reliance Industries Ltd., 4.125%, 1/28/25 | | 250,000 |

| 260,883 |

|

Vedanta Resources plc, 6.125%, 8/9/24(1) | | 300,000 |

| 306,825 |

|

| | | | 1,643,957 |

|

| Indonesia — 1.9% | | | |

Minejesa Capital BV, 4.625%, 8/10/30(1) | | 300,000 |

| 306,751 |

|

| TBG Global Pte Ltd., 5.25%, 2/10/22 | | 400,000 |

| 412,909 |

|

| | | | 719,660 |

|

| Ireland — 0.8% | | | |

C&W Senior Financing Designated Activity Co., 6.875%, 9/15/27(1) | | 300,000 |

| 314,250 |

|

| Israel — 1.5% | | | |

Israel Electric Corp. Ltd., 5.00%, 11/12/24(1) | | 200,000 |

| 215,612 |

|

| Teva Pharmaceutical Finance Netherlands III BV, 2.80%, 7/21/23 | | 400,000 |

| 368,424 |

|

| | | | 584,036 |

|

| Kazakhstan — 0.5% | | | |

KazTransGas JSC, 4.375%, 9/26/27(1) | | 200,000 |

| 197,984 |

|

| Kuwait — 0.8% | | | |

| Kuwait Projects Co. SPC Ltd., 5.00%, 3/15/23 | | 300,000 |

| 318,384 |

|

| Mexico — 4.0% | | | |

Banco Inbursa SA Institucion de Banca Multiple, 4.375%, 4/11/27(1) | | 300,000 |

| 298,500 |

|

Banco Mercantil del Norte SA, VRN, 5.75%, 10/4/26(2) | | 300,000 |

| 306,000 |

|

| Mexichem SAB de CV, 5.875%, 9/17/44 | | 400,000 |

| 415,100 |

|

| Petroleos Mexicanos, 6.50%, 3/13/27 | | 200,000 |

| 218,530 |

|

| Southern Copper Corp., 7.50%, 7/27/35 | | 200,000 |

| 264,849 |

|

| | | | 1,502,979 |

|

|

| | | | | | | |

| | | Principal Amount | Value |

| Nigeria — 1.7% | | | |

| Guaranty Trust Bank plc, MTN, 6.00%, 11/8/18 | | $ | 200,000 |

| $ | 203,144 |

|

IHS Netherlands Holdco BV, 9.50%, 10/27/21(1) | | 400,000 |

| 425,938 |

|

| | | | 629,082 |

|

| Panama — 1.3% | | | |

Banco General SA, 4.125%, 8/7/27(1) | | 300,000 |

| 298,650 |

|

Banistmo SA, 3.65%, 9/19/22(1) | | 200,000 |

| 200,380 |

|

| | | | 499,030 |

|

| Peru — 3.8% | | | |

Banco de Credito del Peru, 2.25%, 10/25/19(1) | | 200,000 |

| 200,500 |

|

Banco Internacional del Peru SAA Interbank, VRN, 6.625%, 3/19/24(2) | | 200,000 |

| 227,000 |

|

Intercorp Financial Services, Inc., 4.125%, 10/19/27(1) | | 300,000 |

| 296,625 |

|

SAN Miguel Industrias Pet SA, 4.50%, 9/18/22(1) | | 300,000 |

| 304,170 |

|

| Transportadora de Gas del Peru SA, 4.25%, 4/30/28 | | 400,000 |

| 414,500 |

|

| | | | 1,442,795 |

|

| Philippines — 0.3% | | | |

| FPT Finance Ltd., 6.375%, 9/28/20 | | 100,000 |

| 109,500 |

|

| Qatar — 4.1% | | | |

| Nakilat, Inc., 6.27%, 12/31/33 | | 208,550 |

| 245,046 |

|

| Ooredoo Tamweel Ltd., 3.04%, 12/3/18 | | 600,000 |

| 604,935 |

|

| Ras Laffan Liquefied Natural Gas Co. Ltd. III, 6.75%, 9/30/19 | | 400,000 |

| 429,975 |

|

| Ras Laffan Liquefied Natural Gas Co. Ltd. III, 6.33%, 9/30/27 | | 250,000 |

| 288,500 |

|

| | | | 1,568,456 |

|

| Republic of Korea — 1.6% | | | |

| Hyundai Capital America, 2.55%, 2/6/19 | | 200,000 |

| 200,406 |

|

| KEB Hana Bank, MTN, 4.375%, 9/30/24 | | 200,000 |

| 209,140 |

|

| Woori Bank, MTN, 4.75%, 4/30/24 | | 200,000 |

| 210,127 |

|

| | | | 619,673 |

|

| Russia — 8.1% | | | |

| Credit Bank of Moscow Via CBOM Finance plc, 7.70%, 2/1/18 | | 400,000 |

| 402,951 |

|

| Gazprom OAO Via Gaz Capital SA, 9.25%, 4/23/19 | | 500,000 |

| 545,518 |

|

| Gazprom OAO Via Gaz Capital SA, 6.51%, 3/7/22 | | 200,000 |

| 221,917 |

|

| Gazprom OAO Via Gaz Capital SA, MTN, 7.29%, 8/16/37 | | 200,000 |

| 243,462 |

|

| Lukoil International Finance BV, 6.125%, 11/9/20 | | 200,000 |

| 217,713 |

|

Lukoil International Finance BV, 4.75%, 11/2/26(1) | | 300,000 |

| 315,778 |

|

| Novolipetsk Steel via Steel Funding DAC, 4.50%, 6/15/23 | | 200,000 |

| 207,437 |

|

| Sberbank of Russia Via SB Capital SA, 5.18%, 6/28/19 | | 400,000 |

| 415,851 |

|

| Sberbank of Russia Via SB Capital SA, 5.125%, 10/29/22 | | 300,000 |

| 313,981 |

|

| VEON Holdings BV, 5.20%, 2/13/19 | | 200,000 |

| 206,200 |

|

| | | | 3,090,808 |

|

| Singapore — 1.1% | | | |

Oversea-Chinese Banking Corp. Ltd., MTN, VRN, 4.00%, 10/15/19(2) | | 200,000 |

| 205,048 |

|

United Overseas Bank Ltd., MTN, VRN, 3.75%, 9/19/19(2) | | 200,000 |

| 204,565 |

|

| | | | 409,613 |

|

| South Africa — 1.1% | | | |

MTN Mauritius Investment Ltd., 6.50%, 10/13/26(1) | | 400,000 |

| 433,300 |

|

|

| | | | | | | |

| | | Principal Amount | Value |

| Thailand — 1.1% | | | |

| Bangkok Bank PCL, 3.875%, 9/27/22 | | $ | 200,000 |

| $ | 210,126 |

|

| Siam Commercial Bank PCL, MTN, 3.50%, 4/7/19 | | 200,000 |

| 203,288 |

|

| | | | 413,414 |

|

| Turkey — 11.8% | | | |

Finansbank AS, 4.875%, 5/19/22(1) | | 200,000 |

| 197,858 |

|

| Finansbank AS, MTN, 6.25%, 4/30/19 | | 200,000 |

| 206,699 |

|

| Tupras Turkiye Petrol Rafinerileri AS, 4.125%, 5/2/18 | | 800,000 |

| 804,839 |

|

Tupras Turkiye Petrol Rafinerileri AS, 4.50%, 10/18/24(1) | | 500,000 |

| 490,063 |

|

| Turk Telekomunikasyon AS, 4.875%, 6/19/24 | | 500,000 |

| 507,002 |

|

| Turk Telekomunikasyon AS, 3.75%, 6/19/19 | | 300,000 |

| 303,406 |

|

| Turkiye Garanti Bankasi AS, MTN, 4.75%, 10/17/19 | | 400,000 |

| 407,435 |

|

Turkiye Garanti Bankasi AS, VRN, 6.125%, 5/24/22(1)(2) | | 600,000 |

| 594,300 |

|

| Turkiye Is Bankasi, 3.75%, 10/10/18 | | 200,000 |

| 200,204 |

|

Turkiye Is Bankasi, 6.125%, 4/25/24(1) | | 300,000 |

| 299,792 |

|

| Yapi ve Kredi Bankasi AS, 5.25%, 12/3/18 | | 200,000 |

| 203,337 |

|

Yapi ve Kredi Bankasi AS, 5.85%, 6/21/24(1) | | 300,000 |

| 296,540 |

|

| | | | 4,511,475 |

|

| Ukraine — 0.6% | | | |

| MHP SE, 8.25%, 4/2/20 | | 200,000 |

| 216,677 |

|

| United Arab Emirates — 2.6% | | | |

| Abu Dhabi National Energy Co. PJSC, 3.625%, 1/12/23 | | 200,000 |

| 203,000 |

|

| Abu Dhabi National Energy Co. PJSC, MTN, 5.875%, 12/13/21 | | 300,000 |

| 331,860 |

|

| ADCB Finance Cayman Ltd., MTN, 4.50%, 3/6/23 | | 200,000 |

| 210,605 |

|

| DP World Ltd., MTN, 6.85%, 7/2/37 | | 200,000 |

| 248,123 |

|

| | | | 993,588 |

|

TOTAL CORPORATE BONDS

(Cost $33,243,526) | | | 33,836,450 |

|

| SOVEREIGN GOVERNMENTS AND AGENCIES — 6.7% | | | |

| Argentina — 0.9% | | | |

| Provincia de Buenos Aires, 7.875%, 6/15/27 | | 300,000 |

| 333,300 |

|

| China — 0.8% | | | |

| Avi Funding Co. Ltd., MTN, 3.80%, 9/16/25 | | 300,000 |

| 309,515 |

|

| Greece — 2.1% | | | |

Hellenic Republic Government Bond, 4.375%, 8/1/22(1) | EUR | 700,000 |

| 814,446 |

|

| Jordan — 0.5% | | | |

Jordan Government International Bond, 7.375%, 10/10/47(1) | | $ | 200,000 |

| 209,935 |

|

| Russia — 1.1% | | | |

| Russian Foreign Bond - Eurobond, 4.25%, 6/23/27 | | 200,000 |

| 204,181 |

|

| Russian Foreign Bond - Eurobond, 5.00%, 4/29/20 | | 200,000 |

| 211,844 |

|

| | | | 416,025 |

|

| Saudi Arabia — 0.5% | | | |

Saudi Government International Bond, 2.375%, 10/26/21(1) | | 200,000 |

| 196,803 |

|

| Turkey — 0.8% | | | |

| Turkey Government International Bond, 4.875%, 10/9/26 | | 300,000 |

| 293,495 |

|

TOTAL SOVEREIGN GOVERNMENTS AND AGENCIES

(Cost $2,543,286) | | | 2,573,519 |

|

|

| | | | | | | |

| | | Shares/Principal Amount | Value |

| COMMON STOCKS — 0.1% | | | |

| Colombia — 0.1% | | | |

Frontera Energy Corp.(3)

(Cost $202,817) | | 1,039 |

| $ | 31,064 |

|

U.S. TREASURY SECURITIES† | | | |

United States† | | | |

U.S. Treasury Notes, 2.25%, 8/15/27

(Cost $9,891) | | $ | 10,000 |

| 9,891 |

|

| TEMPORARY CASH INVESTMENTS — 2.8% | | | |

| Repurchase Agreement, BMO Capital Markets Corp., (collateralized by various U.S. Treasury obligations, 0.375% - 1.375%, 1/15/27 - 2/15/45, valued at $364,754), in a joint trading account at 0.88%, dated 10/31/17, due 11/1/17 (Delivery value $356,792) | | | 356,783 |

|

| Repurchase Agreement, Fixed Income Clearing Corp., (collateralized by various U.S. Treasury obligations, 2.50%, 5/15/46, valued at $304,464), at 0.34%, dated 10/31/17, due 11/1/17 (Delivery value $297,003) | | | 297,000 |

|

| State Street Institutional U.S. Government Money Market Fund, Premier Class | | 326,837 |

| 326,837 |

|

U.S. Treasury Bills 1.05%, 11/9/17(4)(5) | | $ | 100,000 |

| 99,979 |

|

TOTAL TEMPORARY CASH INVESTMENTS

(Cost $1,080,598) | | | 1,080,599 |

|

TOTAL INVESTMENT SECURITIES — 98.4%

(Cost $37,080,118) | | | 37,531,523 |

|

| OTHER ASSETS AND LIABILITIES — 1.6% | | | 592,578 |

|

| TOTAL NET ASSETS — 100.0% | | | $ | 38,124,101 |

|

|

| | | | | | | | | | |

| FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS |

| Currency Purchased | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation

(Depreciation) |

| USD | 806,871 |

| EUR | 684,361 |

| JPMorgan Chase Bank N.A. | 12/20/17 | $ | 7,501 |

|

| USD | 2,269,745 |

| MXN | 40,813,647 |

| JPMorgan Chase Bank N.A. | 12/20/17 | 158,219 |

|

| MXN | 40,813,647 |

| USD | 2,157,740 |

| JPMorgan Chase Bank N.A. | 12/20/17 | (46,214 | ) |

| | | | | | | $ | 119,506 |

|

|

| | | | | | | | | | | | |

| FUTURES CONTRACTS PURCHASED |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Underlying

Contract

Value | Unrealized

Appreciation

(Depreciation) |

| U.S. Treasury 5-Year Notes | 41 | December 2017 | | $ | 4,100,000 |

| $ | 4,804,688 |

| $ | (54,225 | ) |

| U.S. Treasury Long Bonds | 4 | December 2017 | | $ | 400,000 |

| 609,875 |

| (11,572 | ) |

| | | | | | $ | 5,414,563 |

| $ | (65,797 | ) |

|

| | | | | | | | | | | | |

| FUTURES CONTRACTS SOLD |

| Reference Entity | Contracts | Expiration

Date | Notional

Amount | Underlying

Contract

Value | Unrealized

Appreciation

(Depreciation) |

| U.S. Treasury 10-Year Ultra Notes | 26 | December 2017 | | $ | 2,600,000 |

| $ | 3,481,969 |

| $ | 30,973 |

|

|

| | | | | | | | | | | | | | | |

| CREDIT DEFAULT SWAP AGREEMENTS |

| Counterparty/Reference Entity | Type | Fixed Rate

Received

(Paid) | Termination

Date | Notional

Amount | Premiums Paid (Received) | Unrealized

Appreciation

(Depreciation) | Value* |

| Bank of America N.A. / Colombia Government International Bond | Buy | (1.00)% | 12/20/21 | $ | 500,000 |

| $ | 10,339 |

| $ | (14,405 | ) | $ | (4,066 | ) |

| Bank of America N.A. / Markit CDX Emerging Markets Index Series 28 | Buy | (1.00)% | 12/20/22 | $ | 1,500,000 |

| 62,517 |

| (12,333 | ) | 50,184 |

|

| Bank of America N.A. / Republic of Chile | Buy | (1.00)% | 12/20/22 | $ | 1,500,000 |

| (32,148 | ) | (5,751 | ) | (37,899 | ) |

| Morgan Stanley / Republic of Turkey | Buy | (1.00)% | 12/20/22 | $ | 1,300,000 |

| 49,652 |

| 334 |

| 49,986 |

|

| | | | | | $ | 90,360 |

| $ | (32,155 | ) | $ | 58,205 |

|

*The value for credit default swap agreements serve as an indicator of the current status of the payment/performance risk and represent the likelihood of an expected liability or profit at the period end. Increasing values in absolute terms when compared to the notional amount of the credit default swap agreement represent a deterioration of the referenced entity's credit soundness and an increased likelihood or risk of a credit event occurring as defined in the agreement.

|

| | |

| NOTES TO SCHEDULE OF INVESTMENTS |

| CDX | - | Credit Derivatives Indexes |

| EUR | - | Euro |

| MTN | - | Medium Term Note |

| MXN | - | Mexican Peso |

| USD | - | United States Dollar |

| VRN | - | Variable Rate Note. Interest reset date is indicated. Rate shown is effective at the period end. |

| |

| † | Category is less than 0.05% of total net assets. |

| |

| (1) | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration, normally to qualified institutional investors. The aggregate value of these securities at the period end was $11,395,481, which represented 29.9% of total net assets. |

| |

| (2) | Coupon rate adjusts periodically based upon a predetermined schedule. Interest reset date is indicated. Rate shown is effective at the period end. |

| |

| (4) | The rate indicated is the yield to maturity at purchase. |

| |

| (5) | Security, or a portion thereof, has been pledged at the custodian bank or with a broker for margin requirements on forward foreign currency exchange contracts, futures contracts and/or swap agreements. At the period end, the aggregate value of securities pledged was $17,996. |

See Notes to Financial Statements.

|

|

| Statement of Assets and Liabilities |

|

| | | |

| OCTOBER 31, 2017 | |

| Assets | |

| Investment securities, at value (cost of $37,080,118) | $ | 37,531,523 |

|

| Receivable for capital shares sold | 86,310 |

|

| Unrealized appreciation on forward foreign currency exchange contracts | 165,720 |

|

| Swap agreements, at value (including net premiums paid (received) of $112,169) | 100,170 |

|

| Interest receivable | 370,590 |

|

| | 38,254,313 |

|

| | |

| Liabilities | |

| Payable for investments purchased | 9,939 |

|

| Payable for capital shares redeemed | 996 |

|

| Payable for variation margin on futures contracts | 1,289 |

|

| Unrealized depreciation on forward foreign currency exchange contracts | 46,214 |

|

| Swap agreements, at value (including net premiums paid (received) of $(21,809)) | 41,965 |

|

| Accrued management fees | 26,462 |

|

| Distribution and service fees payable | 2,870 |

|

| Dividends payable | 477 |

|

| | 130,212 |

|

| | |

| Net Assets | $ | 38,124,101 |

|

| | |

| Net Assets Consist of: | |

| Capital paid in | $ | 36,709,118 |

|

| Undistributed net investment income | 22,630 |

|

| Undistributed net realized gain | 888,494 |

|

| Net unrealized appreciation | 503,859 |

|

| | $ | 38,124,101 |

|

|

| | | | | | |

| | Net Assets | Shares Outstanding | Net Asset Value Per Share |

| Investor Class |

| $6,634,232 |

| 635,800 |

| $10.43 |

| I Class |

| $38,195 |

| 3,660 |

| $10.44 |

| Y Class |

| $5,166 |

| 495 |

| $10.44 |

| A Class |

| $6,618,778 |

| 634,640 |

| $10.43* |

| C Class |

| $1,144,374 |

| 109,919 |

| $10.41 |

| R Class |

| $1,205,251 |

| 115,638 |

| $10.42 |

| R5 Class |

| $5,985,762 |

| 573,627 |

| $10.43 |

| R6 Class |

| $16,492,343 |

| 1,579,852 |

| $10.44 |

*Maximum offering price $10.92 (net asset value divided by 0.955).

See Notes to Financial Statements.

|

| | | |

| YEAR ENDED OCTOBER 31, 2017 |

| Investment Income (Loss) | |

| Income: | |

| Interest | $ | 1,585,865 |

|

| | |

| Expenses: | |

| Management fees | 292,680 |

|

| Distribution and service fees: | |

| A Class | 15,896 |

|

| C Class | 11,166 |

|

| R Class | 5,781 |

|

| Trustees' fees and expenses | 2,236 |

|

| Other expenses | 1,260 |

|

| | 329,019 |

|

| | |

| Net investment income (loss) | 1,256,846 |

|

| | |

| Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss) on: | |

| Investment transactions | 993,500 |

|

| Forward foreign currency exchange contract transactions | (185,138 | ) |

| Futures contract transactions | 133,547 |

|

| Swap agreement transactions | (39,674 | ) |

| Foreign currency translation transactions | 15,481 |

|

| | 917,716 |

|

| | |

| Change in net unrealized appreciation (depreciation) on: | |

| Investments | (308,439 | ) |

| Forward foreign currency exchange contracts | 119,506 |

|

| Futures contracts | (50,513 | ) |

| Swap agreements | (32,155 | ) |

| Translation of assets and liabilities in foreign currencies | (73 | ) |

| | (271,674 | ) |

| | |

| Net realized and unrealized gain (loss) | 646,042 |

|

| | |

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ | 1,902,888 |

|

See Notes to Financial Statements.

|

|

| Statement of Changes in Net Assets |

|

| | | | | | |

| YEARS ENDED OCTOBER 31, 2017 AND OCTOBER 31, 2016 |

| Increase (Decrease) in Net Assets | October 31, 2017 | October 31, 2016 |

| Operations | | |

| Net investment income (loss) | $ | 1,256,846 |

| $ | 1,046,093 |

|

| Net realized gain (loss) | 917,716 |

| 427,241 |

|

| Change in net unrealized appreciation (depreciation) | (271,674 | ) | 1,232,877 |

|

| Net increase (decrease) in net assets resulting from operations | 1,902,888 |

| 2,706,211 |

|

| | | |

| Distributions to Shareholders | | |

| From net investment income: | | |

| Investor Class | (136,419 | ) | (85,827 | ) |

| I Class | (429 | ) | — |

|

| Y Class | (98 | ) | — |

|

| A Class | (195,891 | ) | (202,338 | ) |

| C Class | (26,040 | ) | (27,956 | ) |

| R Class | (32,720 | ) | (33,205 | ) |

| R5 Class | (204,399 | ) | (207,030 | ) |

| R6 Class | (635,782 | ) | (507,314 | ) |

| From net realized gains: | | |

| Investor Class | (18,280 | ) | — |

|

| A Class | (36,596 | ) | — |

|

| C Class | (6,473 | ) | — |

|

| R Class | (6,555 | ) | — |

|

| R5 Class | (33,080 | ) | — |

|

| R6 Class | (99,926 | ) | — |

|

| Decrease in net assets from distributions | (1,432,688 | ) | (1,063,670 | ) |

| | | |

| Capital Share Transactions | | |

| Net increase (decrease) in net assets from capital share transactions (Note 5) | 4,094,966 |

| 4,891,529 |

|

| | | |

| Net increase (decrease) in net assets | 4,565,166 |

| 6,534,070 |

|

| | | |

| Net Assets | | |

| Beginning of period | 33,558,935 |

| 27,024,865 |

|

| End of period | $ | 38,124,101 |

| $ | 33,558,935 |

|

| | | |

| Undsitributed net investment income | $ | 22,630 |

| — |

|

See Notes to Financial Statements.

|

|

| Notes to Financial Statements |

OCTOBER 31, 2017

1. Organization

American Century International Bond Funds (the trust) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Massachusetts business trust. Emerging Markets Debt Fund (the fund) is one fund in a series issued by the trust. The fund’s investment objective is to seek total return.

The fund offers the Investor Class, I Class, Y Class, A Class, C Class, R Class, R5 Class (formerly Institutional Class) and R6 Class. The A Class may incur an initial sales charge. The A Class and C Class may be subject to a contingent deferred sales charge. Sale of the I Class and Y Class commenced on April 10, 2017.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The fund is an investment company and follows accounting and reporting guidance in accordance with accounting principles generally accepted in the United States of America. This may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates. Management evaluated the impact of events or transactions occurring through the date the financial statements were issued that would merit recognition or disclosure.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share at the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open. The Board of Trustees has adopted valuation policies and procedures to guide the investment advisor in the fund’s investment valuation process and to provide methodologies for the oversight of the fund’s pricing function.

Fixed income securities are valued at the evaluated mean as provided by independent pricing services or at the mean of the most recent bid and asked prices as provided by investment dealers. Sovereign governments and agencies, corporate bonds, and U.S. Treasury and Government Agency securities are valued using market models that consider trade data, quotations from dealers and active market makers, relevant yield curve and spread data, creditworthiness, trade data or market information on comparable securities, and other relevant security specific information. Fixed income securities initially expressed in local currencies are translated into U.S. dollars at the mean of the appropriate currency exchange rate at the close of the NYSE as provided by an independent pricing service.

Equity securities that are listed or traded on a domestic securities exchange are valued at the last reported sales price or at the official closing price as provided by the exchange. Equity securities traded on foreign securities exchanges are generally valued at the closing price of such securities on the exchange where primarily traded or at the close of the NYSE, if that is earlier. If no last sales price is reported, or if local convention or regulation so provides, the mean of the latest bid and asked prices may be used. Securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official closing price. Equity securities initially expressed in local currencies are translated into U.S. dollars at the mean of the appropriate currency exchange rate at the close of the NYSE as provided by an independent pricing service.

Open-end management investment companies are valued at the reported net asset value per share. Repurchase agreements are valued at cost, which approximates fair value. Exchange-traded futures contracts are valued at the settlement price as provided by the appropriate clearing corporation. Swap agreements are valued at an evaluated mean as provided by independent pricing services or independent brokers. Forward foreign currency exchange contracts are valued at the mean of the appropriate forward exchange rate at the close of the NYSE as provided by an independent pricing service.

If the fund determines that the market price for an investment is not readily available or the valuation methods mentioned above do not reflect an investment’s fair value, such investment is valued as determined in good faith by the Board of Trustees or its delegate, in accordance with policies and procedures adopted by the Board of Trustees. In its determination of fair value, the fund may review several factors including, but not limited to, market information regarding the specific investment or comparable investments and correlation

with other investment types, futures indices or general market indicators. Circumstances that may cause the fund to use these procedures to value an investment include, but are not limited to: an investment has been declared in default or is distressed; trading in a security has been suspended during the trading day or a security is not actively trading on its principal exchange; prices received from a regular pricing source are deemed unreliable; or there is a foreign market holiday and no trading occurred.

The fund monitors for significant events occurring after the close of an investment’s primary exchange but before the fund’s net asset value per share is determined. Significant events may include, but are not limited to: corporate announcements and transactions; governmental action and political unrest that could impact a specific investment or an investment sector; or armed conflicts, natural disasters and similar events that could affect investments in a specific country or region. The fund also monitors for significant fluctuations between domestic and foreign markets, as evidenced by the U.S. market or such other indicators that the Board of Trustees, or its delegate, deems appropriate. If significant fluctuations in foreign markets are identified, the fund may apply a model-derived factor to the closing price of equity securities traded on foreign securities exchanges. The factor is based on observable market data as provided by an independent pricing service.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums. Inflation adjustments related to inflation-linked debt securities are reflected as interest income.

Foreign Currency Translations — All assets and liabilities initially expressed in foreign currencies are translated into U.S. dollars at prevailing exchange rates at period end. The fund may enter into spot foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of investment securities, dividend and interest income, spot foreign currency exchange contracts, and expenses are translated at the rates of exchange prevailing on the respective dates of such transactions. Net realized and unrealized foreign currency exchange gains or losses related to investment securities are a component of net realized gain (loss) on investment transactions and change in net unrealized appreciation (depreciation) on investments, respectively.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Trustees. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Segregated Assets — In accordance with the 1940 Act, the fund segregates assets on its books and records to cover certain types of investments, including, but not limited to, futures contracts, forward commitments, when-issued securities, swap agreements and certain forward foreign currency exchange contracts. ACIM monitors, on a daily basis, the securities segregated to ensure the fund designates a sufficient amount of liquid assets, marked-to-market daily. The fund may also receive assets or be required to pledge assets at the custodian bank or with a broker for margin requirements on futures contracts, forward commitments, swap agreements and certain forward foreign currency exchange contracts.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. Accordingly, no provision has been made for income taxes. The fund files U.S. federal, state, local and non-U.S. tax returns as applicable. The fund's tax returns are subject to examination by the relevant taxing authority until expiration of the applicable statute of limitations, which is generally three years from the date of filing but can be longer in certain jurisdictions. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income, if any, are declared daily and paid monthly. Distributions from net realized gains, if any, are generally declared and paid annually.

Indemnifications — Under the trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Certain officers and trustees of the trust are also officers and/or directors of American Century Companies, Inc. (ACC). The trust's investment advisor, ACIM, the trust's distributor, American Century Investment Services, Inc. (ACIS), and the trust's transfer agent, American Century Services, LLC, are wholly owned, directly or indirectly, by ACC. ACIM owns 45% of the shares of the fund. Various funds issued by American Century Investment Trust and American Century Strategic Asset Allocations, Inc. own, in aggregate, 41% of the shares of the fund. Related parties do not invest in the fund for the purpose of exercising management or control.

Management Fees — The trust has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent trustees (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class's daily net assets and paid monthly in arrears. The difference in the fee among the classes is a result of their separate arrangements for non-Rule 12b-1 shareholder services. It is not the result of any difference in advisory or custodial fees or other expenses related to the management of the fund’s assets, which do not vary by class.

The annual management fee for each class is as follows:

|

| | | | | | | |

| Investor Class | I Class | Y Class | A Class | C Class | R Class | R5 Class | R6 Class |

| 0.96% | 0.86% | 0.76% | 0.96% | 0.96% | 0.96% | 0.76% | 0.71% |

Distribution and Service Fees — The Board of Trustees has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay ACIS an annual distribution and service fee of 0.25%. The plans provide that the C Class will pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the period ended October 31, 2017 are detailed in the Statement of Operations.

Trustees’ Fees and Expenses — The Board of Trustees is responsible for overseeing the investment advisor’s management and operations of the fund. The trustees receive detailed information about the fund and its investment advisor regularly throughout the year, and meet at least quarterly with management of the investment advisor to review reports about fund operations. The fund’s officers do not receive compensation from the fund.

4. Investment Transactions

Purchases of investment securities, excluding short-term investments, for the period ended October 31, 2017 totaled $51,862,711, of which $936,083 represented U.S. Treasury and Government Agency obligations.

Sales of investment securities, excluding short-term investments, for the period ended October 31, 2017 totaled $46,087,146, of which $925,976 represented U.S. Treasury and Government Agency obligations.

5. Capital Share Transactions

Transactions in shares of the fund were as follows (unlimited number of shares authorized):

|

| | | | | | | | | | |

| | Year ended

October 31, 2017(1) | Year ended

October 31, 2016 |

| | Shares | Amount | Shares | Amount |

| Investor Class | | | | |

| Sold | 582,422 |

| $ | 6,023,796 |

| 274,466 |

| $ | 2,798,069 |

|

| Issued in reinvestment of distributions | 14,657 |

| 150,735 |

| 8,240 |

| 82,673 |

|

| Redeemed | (338,952 | ) | (3,465,672 | ) | (97,759 | ) | (978,196 | ) |

| | 258,127 |

| 2,708,859 |

| 184,947 |

| 1,902,546 |

|

| I Class | | | N/A |

| |

| Sold | 3,639 |

| 37,719 |

| | |

| Issued in reinvestment of distributions | 41 |

| 429 |

| | |

| Redeemed | (20 | ) | (204 | ) | | |

| | 3,660 |

| 37,944 |

| | |

| Y Class | | | N/A |

| |

| Sold | 485 |

| 5,000 |

| | |

| Issued in reinvestment of distributions | 10 |

| 98 |

| | |

| | 495 |

| 5,098 |

| | |

| A Class | | | | |

| Sold | 11,352 |

| 118,176 |

| 6,539 |

| 63,694 |

|

| Issued in reinvestment of distributions | 22,681 |

| 232,487 |

| 20,228 |

| 201,870 |

|

| Redeemed | (8,319 | ) | (86,038 | ) | — |

| — |

|

| | 25,714 |

| 264,625 |

| 26,767 |

| 265,564 |

|

| C Class | | | | |

| Sold | 962 |

| 10,000 |

| 847 |

| 8,260 |

|

| Issued in reinvestment of distributions | 3,180 |

| 32,497 |

| 2,801 |

| 27,893 |

|

| Redeemed | (2,044 | ) | (21,053 | ) | (44 | ) | (446 | ) |

| | 2,098 |

| 21,444 |

| 3,604 |

| 35,707 |

|

| R Class | | | | |

| Sold | 4,099 |

| 42,218 |

| 1,674 |

| 16,835 |

|

| Issued in reinvestment of distributions | 3,835 |

| 39,275 |

| 3,322 |

| 33,128 |

|

| Redeemed | (951 | ) | (9,915 | ) | — |

| — |

|

| | 6,983 |

| 71,578 |

| 4,996 |

| 49,963 |

|

| R5 Class | | | | |

| Issued in reinvestment of distributions | 23,143 |

| 237,479 |

| 20,682 |

| 206,541 |

|

| R6 Class | | | | |

| Sold | 349,756 |

| 3,540,873 |

| 353,521 |

| 3,601,101 |

|

| Issued in reinvestment of distributions | 71,619 |

| 735,307 |

| 50,626 |

| 506,132 |

|

| Redeemed | (339,248 | ) | (3,528,241 | ) | (166,923 | ) | (1,676,025 | ) |

| | 82,127 |

| 747,939 |

| 237,224 |

| 2,431,208 |

|

| Net increase (decrease) | 402,347 |

| $ | 4,094,966 |

| 478,220 |

| $ | 4,891,529 |

|

| |

| (1) | April 10, 2017 (commencement of sale) through October 31, 2017 for the I Class and Y Class. |

6. Fair Value Measurements

The fund’s investments valuation process is based on several considerations and may use multiple inputs to determine the fair value of the investments held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels.

| |

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical investments. |

| |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for comparable investments, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.). These inputs also consist of quoted prices for identical investments initially expressed in local currencies that are adjusted through translation into U.S. dollars. |

| |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments. There were no significant transfers between levels during the period.

The following is a summary of the level classifications as of period end. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

|

| | | | | | | | |

| | Level 1 | Level 2 | Level 3 |

| Assets | | | |

| Investment Securities | | | |

| Corporate Bonds | — |

| $ | 33,836,450 |

| — |

|

| Sovereign Governments and Agencies | — |

| 2,573,519 |

| — |

|

| Common Stocks | $ | 31,064 |

| — |

| — |

|

| U.S. Treasury Securities | — |

| 9,891 |

| — |

|

| Temporary Cash Investments | 326,837 |

| 753,762 |

| — |

|

| | $ | 357,901 |

| $ | 37,173,622 |

| — |

|

| Other Financial Instruments | | | |

| Futures Contracts | $ | 30,973 |

| — |

| — |

|

| Swap Agreements | — |

| $ | 100,170 |

| — |

|

| Forward Foreign Currency Exchange Contracts | — |

| 165,720 |

| — |

|

| | $ | 30,973 |

| $ | 265,890 |

| — |

|

| �� | | | |

| Liabilities | | | |

| Other Financial Instruments | | | |

| Futures Contracts | $ | 65,797 |

| — |

| — |

|

| Swap Agreements | — |

| $ | 41,965 |

| — |

|

| Forward Foreign Currency Exchange Contracts | — |

| 46,214 |

| — |

|

| | $ | 65,797 |

| $ | 88,179 |

| — |

|

7. Derivative Instruments

Credit Risk — The fund is subject to credit risk in the normal course of pursuing its investment objectives. The value of a bond generally declines as the credit quality of its issuer declines. Credit default swap agreements enable a fund to buy/sell protection against a credit event of a specific issuer or index. A fund may attempt to enhance returns by selling protection or attempt to mitigate credit risk by buying protection. The buyer/seller of credit protection against a security or basket of securities may pay/receive an up-front or periodic payment to compensate for/against potential default events. A fund will segregate cash, cash equivalents or other appropriate liquid securities on its records in amounts sufficient to meet requirements. Changes in value, including the periodic amounts of interest to be paid or received on swap agreements, are recorded as unrealized appreciation (depreciation) on swap agreements. Upon entering into a centrally cleared swap, a fund is required to deposit cash or securities (initial margin) with a financial intermediary in an

amount equal to a certain percentage of the notional amount. Subsequent payments (variation margin) are made or received daily, in cash, by a fund. The variation margin is equal to the daily change in the value and is a component of unrealized gains and losses. Realized gain or loss is recorded upon receipt or payment of a periodic settlement or termination of swap agreements. Net realized and unrealized gains or losses occurring during the holding period of swap agreements are a component of net realized gain (loss) on swap agreement transactions and change in net unrealized appreciation (depreciation) on swap agreements, respectively. The risks of entering into swap agreements include the possible lack of liquidity, failure of the counterparty to meet its obligations, and that there may be unfavorable changes in the underlying investments or instruments. The fund's average notional amount held during the period was $2,350,000.

Foreign Currency Risk — The fund is subject to foreign currency exchange rate risk in the normal course of pursuing its investment objectives. The value of foreign investments held by a fund may be significantly affected by changes in foreign currency exchange rates. The dollar value of a foreign security generally decreases when the value of the dollar rises against the foreign currency in which the security is denominated and tends to increase when the value of the dollar declines against such foreign currency. A fund may enter into forward foreign currency exchange contracts to reduce a fund's exposure to foreign currency exchange rate fluctuations or to gain exposure to the fluctuations in the value of foreign currencies. The net U.S. dollar value of foreign currency underlying all contractual commitments held by a fund and the resulting unrealized appreciation or depreciation are determined daily. Realized gain or loss is recorded upon the termination of the contract. Net realized and unrealized gains or losses occurring during the holding period of forward foreign currency exchange contracts are a component of net realized gain (loss) on forward foreign currency exchange contract transactions and change in net unrealized appreciation (depreciation) on forward foreign currency exchange contracts, respectively. A fund bears the risk of an unfavorable change in the foreign currency exchange rate underlying the forward contract. Additionally, losses, up to the fair value, may arise if the counterparties do not perform under the contract terms. The fund's average U.S. dollar exposure to foreign currency risk derivative instruments held during the period was $2,629,004.

Interest Rate Risk — The fund is subject to interest rate risk in the normal course of pursuing its investment objectives. The value of bonds generally declines as interest rates rise. A fund may enter into futures contracts based on a bond index or a specific underlying security. A fund may purchase futures contracts to gain exposure to increases in market value or sell futures contracts to protect against a decline in market value. Upon entering into a futures contract, a fund will segregate cash, cash equivalents or other appropriate liquid securities on its records in amounts sufficient to meet requirements. Subsequent payments (variation margin) are made or received daily, in cash, by a fund. The variation margin is equal to the daily change in the contract value and is recorded as unrealized gains and losses. A fund recognizes a realized gain or loss when the futures contract is closed or expires. Net realized and unrealized gains or losses occurring during the holding period of futures contracts are a component of net realized gain (loss) on futures contract transactions and change in net unrealized appreciation (depreciation) on futures contracts, respectively. One of the risks of entering into futures contracts is the possibility that the change in value of the contract may not correlate with the changes in value of the underlying securities. The fund's average notional exposure to these interest rate risk derivative instruments held during the period was $7,450,000 futures contracts purchased and $983,333 future contracts sold.

Value of Derivative Instruments as of October 31, 2017

|

| | | | | | | | |

| | Asset Derivatives | Liability Derivatives |

| Type of Risk Exposure | Location on Statement of Assets and Liabilities | Value | Location on Statement of Assets and Liabilities | Value |

| Credit Risk | Swap agreements | $ | 100,170 |

| Swap agreements | $ | 41,965 |

|

| Foreign Currency Risk | Unrealized appreciation on forward foreign currency exchange contracts | 165,720 |

| Unrealized depreciation on forward foreign currency exchange contracts | 46,214 |

|

| Interest Rate Risk | Receivable for variation margin on futures contracts* | — |

| Payable for variation margin on futures contracts* | 1,289 |

|

| | | $ | 265,890 |

| | $ | 89,468 |

|

| |

| * | Included in the unrealized appreciation (depreciation) on futures contracts as reported in the Schedule of Investments. |

Effect of Derivative Instruments on the Statement of Operations for the Year Ended October 31, 2017

|

| | | | | | | | |

| | Net Realized Gain (Loss) | Change in Net Unrealized Appreciation (Depreciation) |

| Type of Risk Exposure | Location on Statement of Operations | Value | Location on Statement of Operations | Value |

| Credit Risk | Net realized gain (loss) on swap agreement transactions | $ | (39,674 | ) | Change in net unrealized appreciation (depreciation) on swap agreements | $ | (32,155 | ) |

| Foreign Currency Risk | Net realized gain (loss) on forward foreign currency exchange contract transactions | (185,138 | ) | Change in net unrealized appreciation (depreciation) on forward foreign currency exchange contracts | 119,506 |

|

| Interest Rate Risk | Net realized gain (loss) on futures contract transactions | 133,547 |

| Change in net unrealized appreciation (depreciation) on futures contracts | (50,513 | ) |

| | | $ | (91,265 | ) | | $ | 36,838 |

|

8. Risk Factors

There are certain risks involved in investing in foreign securities. These risks include those resulting from future adverse political, social and economic developments, fluctuations in currency exchange rates, the possible imposition of exchange controls, and other foreign laws or restrictions. Investing in emerging markets may accentuate these risks.

The fund may invest in lower-rated debt securities, which are subject to substantial risks including liquidity risk and credit risk.

The fund’s investment process may result in high portfolio turnover, which could mean high transaction costs, affecting both performance and capital gains tax liabilities to investors.

9. Federal Tax Information

The tax character of distributions paid during the years ended October 31, 2017 and October 31, 2016 were as follows:

|

| | | | | | |

| | 2017 | 2016 |

| Distributions Paid From | | |

| Ordinary income | $ | 1,432,688 |

| $ | 1,063,670 |

|

| Long-term capital gains | — |

| — |

|

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

As of period end, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

|

| | | |

| Federal tax cost of investments | $ | 37,080,118 |

|

| Gross tax appreciation of investments | $ | 684,134 |

|

| Gross tax depreciation of investments | (232,729 | ) |

| Net tax appreciation (depreciation) of investments | 451,405 |

|

Net tax appreciation (depreciation) on derivatives and translation of assets and liabilities in foreign currencies | (26,628 | ) |

| Net tax appreciation (depreciation) | $ | 424,777 |

|

| Undistributed ordinary income | $ | 668,411 |

|

Accumulated long-term gains

| $ | 321,795 |

|

The difference between book-basis and tax-basis unrealized appreciation (depreciation) is attributable primarily to the realization for tax purposes of unrealized gains (losses) on certain foreign currency exchange contracts.

10. Recently Issued Accounting Standards

In March 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update No.2017-08, “Receivables - Nonrefundable Fees and Other Costs (Subtopic 310-20), Premium Amortization on Purchased Callable Debt Securities” (ASU 2017-08). ASU 2017-08 amends the amortization period for certain purchased callable debt securities held at a premium, shortening such period to the earliest call date. The amendments are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. Management is currently evaluating the impact that adopting ASU 2017-08 will have on

the financial statements.

|

| | | | | | | | | | | | | | | |

| For a Share Outstanding Throughout the Years Ended October 31 (except as noted) |

| Per-Share Data | Ratios and Supplemental Data |

| | | Income From Investment Operations: | Distributions From: | | | Ratio to Average Net Assets of: | | |

| | Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net

Investment

Income | Net

Realized

Gains | Total Distributions | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) |

| Investor Class |

| 2017 | $10.32 | 0.35 | 0.16 | 0.51 | (0.34) | (0.06) | (0.40) | $10.43 | 5.11% | 0.97% | 3.39% | 154% |

| $6,634 |

|

| 2016 | $9.75 | 0.36 | 0.57 | 0.93 | (0.36) | — | (0.36) | $10.32 | 9.77% | 0.97% | 3.59% | 97% |

| $3,898 |

|

2015(3) | $9.88 | 0.11 | (0.13) | (0.02) | (0.11) | — | (0.11) | $9.75 | (0.22)% | 0.97%(4) | 3.19%(4) | 35% |

| $1,878 |

|

2015(5) | $10.00 | 0.28 | (0.11) | 0.17 | (0.29) | — | (0.29) | $9.88 | 1.72% | 0.97%(4) | 3.18%(4) | 46% |

| $3,312 |

|

| I Class |

2017(6) | $10.30 | 0.20 | 0.14 | 0.34 | (0.20) | — | (0.20) | $10.44 | 3.28% | 0.87%(4) | 3.38%(4) | 154%(7) |

| $38 |

|

| Y Class |