UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 01136

| Guggenheim Funds Trust |

| (Exact name of registrant as specified in charter) |

702 King Farm Boulevard, Suite 200

Rockville, Maryland 20850 |

| (Address of principal executive offices) (Zip code) |

Amy J. Lee

Guggenheim Funds Trust

702 King Farm Boulevard, Suite 200

Rockville, Maryland 20850 |

| (Name and address of agent for service) |

Registrant's telephone number, including area code: 1-301-296-5100

Date of fiscal year end:September 30

Date of reporting period:September 30, 2019

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

| Item 1. | Reports to Stockholders. |

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

9.30.2019

Guggenheim Funds Annual Report

Guggenheim Funds Trust-Equity |

Guggenheim Alpha Opportunity Fund | | |

Guggenheim Large Cap Value Fund | | |

Guggenheim Market Neutral Real Estate Fund | | |

Guggenheim Risk Managed Real Estate Fund | | |

Guggenheim Small Cap Value Fund | | |

Guggenheim StylePlus—Large Core Fund | | |

Guggenheim StylePlus—Mid Growth Fund | | |

Guggenheim World Equity Income Fund | | |

Beginning on January 1, 2021, paper copies of the Funds’ annual and semi-annual shareholder reports may no longer be sent by mail, unless you specifically request paper copies of the reports from a fund or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and other communications from a fund electronically by calling 800.820.0888, going to GuggenheimInvestments.com/myaccount, or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. If you hold shares of a fund directly, you can inform the Fund that you wish to receive paper copies of reports by calling 800.820.0888. If you hold shares of a fund through a financial intermediary, please contact the financial intermediary to make this election. Your election to receive reports in paper will apply to all Guggenheim Funds in which you are invested and may apply to all funds held with your financial intermediary.

GuggenheimInvestments.com | SBE-ANN-0919x0920 |

| | |

DEAR SHAREHOLDER | 2 |

ECONOMIC AND MARKET OVERVIEW | 4 |

ABOUT SHAREHOLDERS’ FUND EXPENSES | 6 |

ALPHA OPPORTUNITY FUND | 9 |

LARGE CAP VALUE FUND | 30 |

MARKET NEUTRAL REAL ESTATE FUND | 41 |

RISK MANAGED REAL ESTATE FUND | 53 |

SMALL CAP VALUE FUND | 69 |

STYLEPLUS—LARGE CORE FUND | 81 |

STYLEPLUS—MID GROWTH FUND | 93 |

WORLD EQUITY INCOME FUND | 106 |

NOTES TO FINANCIAL STATEMENTS | 119 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 134 |

OTHER INFORMATION | 136 |

INFORMATION ON BOARD OF TRUSTEES AND OFFICERS | 145 |

GUGGENHEIM INVESTMENTS PRIVACY NOTICE | 150 |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 1 |

Dear Shareholder:

Security Investors, LLC and Guggenheim Partners Investment Management, LLC (together, “Investment Advisers”), are pleased to present the shareholder report for eight equity funds (the “Fund” or “Funds”). The report covers the annual fiscal period ended September 30, 2019.

The Investment Advisers are part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC, (“Guggenheim”) a global, diversified financial services firm.

Guggenheim Funds Distributors, LLC is the distributor of the Funds. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim and the Investment Advisers.

We encourage you to read the Economic and Market Overview section of the report, which follows this letter, and then the Managers’ Commentary for each Fund.

We are committed to providing innovative investment solutions and appreciate the trust you place in us.

Sincerely,

Security Investors, LLC

Guggenheim Partners Investment Management, LLC

October 31, 2019

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objectives, risks, charges, expenses and other information, which should be considered carefully before investing. Obtain a prospectus and summary prospectus (if available) at guggenheiminvestments.com or call 800.820.0888.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/ or legal professional regarding your specific situation.

Alpha Opportunity Fund is subject to a number of risks and is not suitable for all investors. ● Investments in securities and derivatives, in general, are subject to market risks that may cause their prices to fluctuate over time. An investment in the Fund may lose money. There can be no guarantee the Fund will achieve it investment objective. ●The Fund’s use of derivatives such as futures, options and swap agreements may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. ● Certain of the derivative instruments, such as swaps and structured notes, are also subject to the risks of counterparty default and adverse tax treatment. ●The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. ● The Fund’s use of short selling involves increased risk and costs, including paying more for a security than it received from its sale and the risk of unlimited losses. ●In certain circumstances the Fund may be subject to liquidity risk and it may be difficult for the Fund to purchase and sell particular investments within a reasonable time at a fair price. ●In certain circumstances, it may be difficult for the Fund to purchase and sell particular investments within a reasonable time at a fair price. ●The Fund’s fixed income investments will change in value in response to interest rate changes and other factors. ● See the prospectus for more information on these and additional risks.

Large Cap Value Fund may not be suitable for all investors. ● An investment in the Fund will fluctuate and is subject to investment risks, which means an investor could lose money. ● The intrinsic value of the underlying stocks may never be realized, or the stock may decline in value. The Fund is subject to risk that large-capitalization stocks may underperform other segments of the equity market or the equity markets as a whole.

Market Neutral Real Estate Fund may not be suitable for all investors. ● Investing involves risk, including the possible loss of principal. ● There are no assurances that any fund will achieve its objective and/or strategy. ● The Fund’s investments in real estate securities subject the Fund to the same risks as direct investments in real estate, which is particularly sensitive to economic downturns. ● The Fund’s use of derivatives such as futures, options, and swap agreements may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. ● When market conditions are deemed appropriate, the Fund will leverage to the full extent permitted by its investment policies and restrictions and applicable law. Leveraging will exaggerate the effect on net asset value of any increase or decrease in the market value of the Fund’s portfolio. ● The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. ● The Fund’s use of short selling involves increased risk and costs. The Fund risks paying more for a security than it received from its sale. ● The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. ● The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political, or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risk). ● The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. ● Investing in sector funds is more volatile than investing in broadly diversified funds, as there is a greater risk due to the concentration of the funds’ holdings in issuers of the same or similar offerings. ● This Fund is considered non-diversified and can invest a greater portion of its assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single security could cause greater fluctuations in the value of fund shares than would occur

2 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

in a more diversified fund. ● Short selling involves increased risks and costs. You risk paying more for a security than you received from its sale. This strategy may not be suitable for all investors. ● The Fund is subject to active trading risks that may increase volatility and impact its ability to achieve its investment objective. ● You may have a gain or loss when you sell your shares. ● It is important to note that the Fund is not guaranteed by the U.S. government. ● Please read the prospectus for more detailed information regarding these and other risks.

Risk Managed Real Estate Fund may not be suitable for all investors. ● Investments in securities in general are subject to market risks that may cause their prices to fluctuate over time ● Investing involves risk, including the possible loss of principal. ● There are no assurances that any fund will achieve its objective and/or strategy. ● The Fund’s investments in real estate securities subject the Fund to the same risks as direct investments in real estate, which is particularly sensitive to economic downturns. ● The Fund’s use of derivatives such as futures, options and swap agreements may expose the Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. ● When market conditions are deemed appropriate, the Fund will leverage to the full extent permitted by its investment policies and restrictions and applicable law. Leveraging will exaggerate the effect on net asset value of any increase or decrease in the market value of the Fund’s portfolio. ● The more the Fund invests in leveraged instruments, the more the leverage will magnify any gains or losses on those investments. ● The Fund’s use of short selling involves increased risk and costs. The Fund risks paying more for a security than it received from its sale. ● The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. ● The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risk). ● The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. ● Investing in sector funds is more volatile than investing in broadly diversified funds, as there is a greater risk due to the concentration of the funds’ holdings in issuers of the same or similar offerings. ● This Fund is considered non-diversified and can invest a greater portion of its assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single security could cause greater fluctuations in the value of fund shares than would occur in a more diversified fund. ● Short selling involves increased risks and costs. You risk paying more for a security than you received from its sale. This strategy may not be suitable for all investors. ● The Fund is subject to active trading risks that may increase volatility and impact its ability to achieve its investment objective. ● You may have a gain or loss when you sell you shares. ● It is important to note that the Fund is not guaranteed by the U.S. government. ● Please read the prospectus for more detailed information regarding these and other risks.

Small Cap Value Fund may not be suitable for all investors. ● An investment in the Fund will fluctuate and is subject to investment risks, which means investors could lose money. ● The intrinsic value of the underlying stocks may never be realized, or the stock may decline in value. ● Investing in securities of small-capitalization companies may involve a greater risk of loss and more abrupt fluctuations in market price than investments in larger-capitalization companies.

StylePlus—Large Core Fund may not be suitable for all investors. ● Investments in large capitalization stocks may underperform other segments of the equity market or the equity market as a whole. ● Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions regarding the growth potential of the issuing companies. Value stocks are subject to the risk that the intrinsic value of the stock may never be realized by the market or that the price goes down.● The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. ● The Fund’s use of leverage, through borrowings or instruments such as derivatives, may cause the Fund to be more volatile than if it had not been leveraged. ● The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. ● The Fund may invest in foreign securities which carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risk). ● The Fund may invest in fixed income securities whose market value will change in response to interest rate changes and market conditions among other factors. In general, bond prices rise when interest rates fall and vice versa. ● The Fund’s exposure to high yield securities may subject the Fund to greater volatility. ● The Fund may invest in bank loans and asset-backed securities, including mortgage backed, which involve special types of risks. ● The Fund may invest in restricted securities which may involve financial and liquidity risk. ● You may have a gain or loss when you sell your shares. ● It is important to note that the Fund is not guaranteed by the U.S. government. ● Please read the prospectus for more detailed information regarding these and other risks.

StylePlus—Mid Growth Fund may not be suitable for all investors. ● Investments in mid-sized company securities may present additional risks such as less predictable earnings, higher volatility and less liquidity than larger, more established companies. ● Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions regarding the growth potential of the issuing companies. ● The Fund may invest in derivative instruments, which may be more volatile and less liquid, increasing the risk of loss when compared to traditional securities. Certain of the derivative instruments are also subject to the risks of counterparty default and adverse tax treatment. ● The Fund’s use of leverage, through borrowings or instruments such as derivatives, may cause the Fund to be more volatile than if it had not been leveraged. ● The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. ● The Fund may invest in foreign securities which carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets securities are generally subject to an even greater level of risk). ● The Fund may invest in fixed income securities whose market value will change in response to interest rate changes and market conditions, among other factors. In general, bond prices rise when interest rates fall and vice versa. ● The Fund’s exposure to high yield securities may subject the Fund to greater volatility. ● The Fund may invest in bank loans and asset-backed securities, including mortgage backed, which involve special types of risks. ● The Fund may invest in restricted securities which may involve financial and liquidity risk. ● You may have a gain or loss when you sell your shares. ● It is important to note that the Fund is not guaranteed by the U.S. government. ● Please read the prospectus for more detailed information regarding these and other risks.

World Equity Income Fund may not be suitable for all investors. ●Investments in securities in general are subject to market risks that may cause their prices to fluctuate over time. ●The Fund’s investments in foreign securities carry additional risks when compared to U.S. securities, due to the impact of diplomatic, political or economic developments in the country in question (investments in emerging markets are generally subject to an even greater level of risk). Additionally, the Fund’s exposure to foreign currencies subjects the Fund to the risk that those currencies will decline in value relative to the U.S. Dollar. ● The Fund’s investments in derivatives may pose risks in addition to those associated with investing directly in securities or other investments, including illiquidity of the derivatives, imperfect correlations with underlying investments or the Fund’s other portfolio holdings, lack of availability and counterparty risk. ●The Fund’s use of leverage, through instruments such as derivatives, may cause the Fund to be more volatile than if it had not been leveraged. ●The Fund’s investments in other investment vehicles subject the Fund to those risks and expenses affecting the investment vehicle. ●The Fund may have significant exposure to securities in a particular capitalization range e.g., large-, mid- or small-cap securities. As a result, the Fund may be subject to the risk that the pre-denominate capitalization range may underperform other segments of the equity market or the equity market as a whole. ● Please read the prospectus for more detailed information regarding these and other risks.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 3 |

ECONOMIC AND MARKET OVERVIEW (Unaudited) | September 30, 2019 |

Economic data has been mixed over the past few months. On the positive side, we saw a pickup in the housing market as measured by housing starts and home sales, which could be a delayed response to lower mortgage rates. Industrial production had the strongest month-over-month gain in a year, partially boosted by an increase in oil production in Hurricane Barry’s wake. The unemployment rate fell to a 50-year low of 3.5% in September 2019, despite a continued moderation in payroll gains.

On the negative side, the Institute for Supply Management (“ISM”) Manufacturing Index plunged to the weakest reading since June 2009. The ISM Non-Manufacturing Index also came in well below expectations, the lowest since August 2016. Within both the manufacturing and non-manufacturing ISM indexes, analysts look at the employment component of the survey for an early read on other labor market indicators. Here we find more cause for concern: The non-manufacturing survey’s employment component is now barely above 50 while the manufacturing employment sub-index stands at 46.3, well into contraction territory. Combined, the outlook for output and hiring has dimmed, signaling trouble ahead for consumers.

Retail sales have been steady, but Commerce Department data showed that total consumer spending on goods and services increased only 0.1% month-over-month in August 2019, the smallest gain in six months. It is hard to identify the primary reason why consumers may already be turning more conservative on spending. Income growth looks steady, the equity market is higher year-to-date, and rates are lower, all of which should be boosting consumer confidence. Sentiment surveys, however, show that fewer consumers believe now is a good time to buy homes, vehicles, and household durables, and headline consumer confidence measures have ticked down. We believe trade policy and political concerns are weighing on sentiment, and these headwinds are set to ramp up further. Additional U.S. tariffs on China are due to take effect on December 15, 2019, and the U.S. House of Representatives is pressing forward with its impeachment inquiry into President Trump.

Guggenheim’s dashboard of U.S. recession indicators continues to point to a recession beginning as early as the first half of 2020, and we think the economic data is corroborating this view. Two of the more notable indicators pointing to high recession risk are the three-month/10-year U.S. Treasury yield curve, which has been inverted for 16 consecutive weeks through period end, and the Leading Economic Indicators Index which has slowed from a year-over-year growth rate of 6.6% in September 2018 to 1.1% as of August 2019. The indicators Guggenheim tracks as part of our recession probability model indicate a nearly 50% chance that a recession will come before mid-2020, and a 70% chance that it will arrive by mid-2021.

Over the period, the U.S. Treasury curve continued its overall flattening trend, as the difference between the two-year U.S. Treasury and 10-year U.S. Treasury narrowed to 5 basis points. Equity markets remained volatile, buoyed by a 25 basis point cut in July and September 2019 by the U.S. Federal Reserve (the “Fed”) and relatively strong U.S. economic data, but weighed down by trade war uncertainty and fears of a global slowdown.

With downside risks growing, markets have become more sensitive to the Fed’s communications about the future stance of monetary policy. Despite the two rate cuts, Fed policymakers are deeply divided. It is still unclear whether the Fed will deliver the aggressive and preemptive policy action that would prolong the current expansion.

For the 12-month period ended September 30, 2019, the Standard & Poor’s 500® (“S&P 500”) Index* returned 4.25%. The MSCI Europe-Australasia-Far East (“EAFE”) Index* returned -0.82%. The return of the MSCI Emerging Markets Index* was -1.63%.

In the bond market, the Bloomberg Barclays U.S. Aggregate Bond Index* posted a 10.30% return for the period, while the Bloomberg Barclays U.S. Corporate High Yield Index* returned 6.36%. The return of the ICE Bank of America (“BofA”) Merrill Lynch 3-Month U.S. Treasury Bill Index* was 2.39% for the 12-month period.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

4 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

ECONOMIC AND MARKET OVERVIEW (Unaudited)(concluded) | September 30, 2019 |

*Index Definitions

Indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees, or expenses.

Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, mortgage-backed securities or “MBS” (agency fixed-rate and hybrid adjustable-rate mortgage, or “ARM”, pass-throughs), asset-backed securities (“ABS”), and commercial mortgage-backed securities (“CMBS”) (agency and non-agency).

Bloomberg Barclays U.S. Corporate High Yield Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB +/BB + or below.

FTSE NAREIT Equity REITs Total Return Index (“FNRE”) is one of the FTSE NAREIT US Real Estate Index Series that contains all Equity REITs not designated as Timber REITs or Infrastructure REITs. FTSE NAREIT US Real Estate Index Series is designed to present investors with a comprehensive family of REIT performance indexes that spans the commercial real estate space across the US economy. The index series provides investors with exposure to all investment and property sectors. In addition, the more narrowly focused property sector and sub-sector indexes provide the facility to concentrate commercial real estate exposure in more selected markets. The National Association of Real Estate Investment Trusts (NAREIT) is the trade association for REITs and publicly traded real estate companies with an interest in the US property and investment markets.

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market Index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income.

MSCI EAFE Index is a capitalization-weighted measure of stock markets in Europe, Australasia, and the Far East.

MSCI Emerging Markets Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance in the global emerging markets.

MSCI World Index (Net) is calculated with net dividends reinvested. It is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

Morningstar Long/Short Equity Category Average is the average return of funds Morningstar places in a given category based on their portfolio statistics and compositions over the past three years. Long-short portfolios hold sizeable stakes in both long and short positions in equities, exchange traded funds, and related derivatives. Some funds that fall into this category will shift their exposure to long and short positions depending on their macro outlook or the opportunities they uncover through bottom-up research. At least 75% of the assets are in equity securities or derivatives, and funds in the category will typically have beta values to relevant benchmarks of between 0.3 and 0.8 over a three-year period.

Russell 1000® Value Index is a measure of the performance for the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Index measures the performance of the largest 3,000 U.S. companies, representing approximately 98% of the investable U.S. equity market.

Russell Midcap Growth® Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values.

S&P 500® is a broad-based index, the performance of which is based on the performance of 500 widely held common stocks chosen for market size, liquidity, and industry group representation.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 5 |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited) | |

All mutual funds have operating expenses, and it is important for our shareholders to understand the impact of costs on their investments. Shareholders of a fund incur two types of costs: (i) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, other distributions, and exchange fees, and (ii) ongoing costs, including management fees, administrative services, and shareholder reports, among others. These ongoing costs, or operating expenses, are deducted from a fund’s gross income and reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets, which is known as the expense ratio. The following examples are intended to help investors understand the ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire six-month period beginning March 31, 2019 and ending September 30, 2019.

The following tables illustrate the Funds’ costs in two ways:

Table 1. Based on actual Fund return: This section helps investors estimate the actual expenses paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fifth column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. Investors may use the information here, together with the amount invested, to estimate the expenses paid over the period. Simply divide the Fund’s account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number provided under the heading “Expenses Paid During Period.”

Table 2. Based on hypothetical 5% return: This section is intended to help investors compare a fund’s cost with those of other mutual funds. The table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid during the period. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on the 5% return. Investors can assess a fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

The calculations illustrated above assume no shares were bought or sold during the period. Actual costs may have been higher or lower, depending on the amount of investment and the timing of any purchases or redemptions.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments, and contingent deferred sales charges (“CDSC”) on redemptions, if any. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

More information about the Funds’ expenses, including annual expense ratios for periods up to five years (subject to the Fund’s inception date), can be found in the Financial Highlights section of this report. For additional information on operating expenses and other shareholder costs, please refer to the appropriate Fund prospectus.

6 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(continued) | |

| Expense

Ratio1 | Fund

Return | Beginning

Account Value

March 31, 2019 | Ending

Account Value

September 30, 2019 | Expenses

Paid During

Period2 |

Table 1. Based on actual Fund return3 | | | | | |

Alpha Opportunity Fund | | | | | |

A-Class | 1.66% | (3.70%) | $ 1,000.00 | $ 963.00 | $ 8.17 |

C-Class | 2.51% | (4.05%) | 1,000.00 | 959.50 | 12.33 |

P-Class | 1.70% | (3.68%) | 1,000.00 | 963.20 | 8.37 |

Institutional Class | 1.32% | (3.50%) | 1,000.00 | 965.00 | 6.50 |

Large Cap Value Fund | | | | | |

A-Class | 1.15% | 0.18% | 1,000.00 | 1,001.80 | 5.77 |

C-Class | 1.90% | (0.18%) | 1,000.00 | 998.20 | 9.52 |

P-Class | 1.15% | 0.18% | 1,000.00 | 1,001.80 | 5.77 |

Institutional Class | 0.90% | 0.30% | 1,000.00 | 1,003.00 | 4.52 |

Market Neutral Real Estate Fund | | | | | |

A-Class | 1.65% | 3.89% | 1,000.00 | 1,038.90 | 8.43 |

C-Class | 2.40% | 3.49% | 1,000.00 | 1,034.90 | 12.24 |

P-Class | 1.65% | 3.90% | 1,000.00 | 1,039.00 | 8.43 |

Institutional Class | 1.40% | 4.01% | 1,000.00 | 1,040.10 | 7.16 |

Risk Managed Real Estate Fund | | | | | |

A-Class | 2.35% | 10.29% | 1,000.00 | 1,102.90 | 12.39 |

C-Class | 3.00% | 9.85% | 1,000.00 | 1,098.50 | 15.78 |

P-Class | 2.08% | 10.30% | 1,000.00 | 1,103.00 | 10.97 |

Institutional Class | 2.01% | 10.46% | 1,000.00 | 1,104.60 | 10.60 |

Small Cap Value Fund | | | | | |

A-Class | 1.30% | 3.13% | 1,000.00 | 1,031.30 | 6.62 |

C-Class | 2.05% | 2.71% | 1,000.00 | 1,027.10 | 10.42 |

P-Class | 1.30% | 3.01% | 1,000.00 | 1,030.10 | 6.62 |

Institutional Class | 1.05% | 3.20% | 1,000.00 | 1,032.00 | 5.35 |

StylePlus—Large Core Fund | | | | | |

A-Class | 1.27% | 5.08% | 1,000.00 | 1,050.80 | 6.53 |

C-Class | 2.12% | 4.64% | 1,000.00 | 1,046.40 | 10.88 |

P-Class | 1.36% | 5.04% | 1,000.00 | 1,050.40 | 6.99 |

Institutional Class | 1.05% | 5.18% | 1,000.00 | 1,051.80 | 5.40 |

StylePlus—Mid Growth Fund | | | | | |

A-Class | 1.47% | 3.63% | 1,000.00 | 1,036.30 | 7.50 |

C-Class | 2.21% | 3.18% | 1,000.00 | 1,031.80 | 11.26 |

P-Class | 1.54% | 3.57% | 1,000.00 | 1,035.70 | 7.86 |

Institutional Class | 1.34% | 3.66% | 1,000.00 | 1,036.60 | 6.84 |

World Equity Income Fund | | | | | |

A-Class | 1.22% | 3.81% | 1,000.00 | 1,038.10 | 6.23 |

C-Class | 1.97% | 3.39% | 1,000.00 | 1,033.90 | 10.04 |

P-Class | 1.22% | 3.75% | 1,000.00 | 1,037.50 | 6.23 |

Institutional Class | 0.97% | 3.96% | 1,000.00 | 1,039.60 | 4.96 |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 7 |

ABOUT SHAREHOLDERS’ FUND EXPENSES (Unaudited)(concluded) | |

| Expense

Ratio1 | Fund

Return | Beginning

Account Value

March 31, 2019 | Ending

Account Value

September 30, 2019 | Expenses

Paid During

Period2 |

Table 2. Based on hypothetical 5% return (before expenses) | | | | |

Alpha Opportunity Fund | | | | | |

A-Class | 1.66% | 5.00% | $ 1,000.00 | $ 1,016.75 | $ 8.39 |

C-Class | 2.51% | 5.00% | 1,000.00 | 1,012.48 | 12.66 |

P-Class | 1.70% | 5.00% | 1,000.00 | 1,016.55 | 8.59 |

Institutional Class | 1.32% | 5.00% | 1,000.00 | 1,018.45 | 6.68 |

Large Cap Value Fund | | | | | |

A-Class | 1.15% | 5.00% | 1,000.00 | 1,019.30 | 5.82 |

C-Class | 1.90% | 5.00% | 1,000.00 | 1,015.54 | 9.60 |

P-Class | 1.15% | 5.00% | 1,000.00 | 1,019.30 | 5.82 |

Institutional Class | 0.90% | 5.00% | 1,000.00 | 1,020.56 | 4.56 |

Market Neutral Real Estate Fund | | | | | |

A-Class | 1.65% | 5.00% | 1,000.00 | 1,016.80 | 8.34 |

C-Class | 2.40% | 5.00% | 1,000.00 | 1,013.04 | 12.11 |

P-Class | 1.65% | 5.00% | 1,000.00 | 1,016.80 | 8.34 |

Institutional Class | 1.40% | 5.00% | 1,000.00 | 1,018.05 | 7.08 |

Risk Managed Real Estate Fund | | | | | |

A-Class | 2.35% | 5.00% | 1,000.00 | 1,013.29 | 11.86 |

C-Class | 3.00% | 5.00% | 1,000.00 | 1,010.03 | 15.12 |

P-Class | 2.08% | 5.00% | 1,000.00 | 1,014.64 | 10.50 |

Institutional Class | 2.01% | 5.00% | 1,000.00 | 1,014.99 | 10.15 |

Small Cap Value Fund | | | | | |

A-Class | 1.30% | 5.00% | 1,000.00 | 1,018.55 | 6.58 |

C-Class | 2.05% | 5.00% | 1,000.00 | 1,014.79 | 10.35 |

P-Class | 1.30% | 5.00% | 1,000.00 | 1,018.55 | 6.58 |

Institutional Class | 1.05% | 5.00% | 1,000.00 | 1,019.80 | 5.32 |

StylePlus—Large Core Fund | | | | | |

A-Class | 1.27% | 5.00% | 1,000.00 | 1,018.70 | 6.43 |

C-Class | 2.12% | 5.00% | 1,000.00 | 1,014.44 | 10.71 |

P-Class | 1.36% | 5.00% | 1,000.00 | 1,018.25 | 6.88 |

Institutional Class | 1.05% | 5.00% | 1,000.00 | 1,019.80 | 5.32 |

StylePlus—Mid Growth Fund | | | | | |

A-Class | 1.47% | 5.00% | 1,000.00 | 1,017.70 | 7.44 |

C-Class | 2.21% | 5.00% | 1,000.00 | 1,013.99 | 11.16 |

P-Class | 1.54% | 5.00% | 1,000.00 | 1,017.35 | 7.79 |

Institutional Class | 1.34% | 5.00% | 1,000.00 | 1,018.35 | 6.78 |

World Equity Income Fund | | | | | |

A-Class | 1.22% | 5.00% | 1,000.00 | 1,018.95 | 6.17 |

C-Class | 1.97% | 5.00% | 1,000.00 | 1,015.19 | 9.95 |

P-Class | 1.22% | 5.00% | 1,000.00 | 1,018.95 | 6.17 |

Institutional Class | 0.97% | 5.00% | 1,000.00 | 1,020.21 | 4.91 |

1 | This ratio represents annualized net expenses, which may include short dividend and interest expense. Excluding these expenses, the operating expense ratio for the Risk Managed Real Estate Fund would be 1.28%, 2.05%, 1.30% and 0.96% for the A-Class, C-Class, P-Class and Institutional Class, respectively. Excludes expenses of the underlying funds in which the Funds invest, if any. |

2 | Expenses are equal to the Fund’s annualized expense ratio, net of any applicable fee waivers, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

3 | Actual cumulative return at net asset value for the period March 31, 2019 to September 30, 2019. |

8 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

MANAGERS’ COMMENTARY (Unaudited) | September 30, 2019 |

Dear Shareholder:

Guggenheim Alpha Opportunity Fund (the “Fund”) is managed by a team of seasoned professionals, including Farhan Sharaff, Senior Managing Director and Assistant Chief Investment Officer, Equities, and Portfolio Manager; Jayson Flowers, Senior Managing Director and Portfolio Manager; Samir Sanghani, CFA, Managing Director and Portfolio Manager; and Burak Hurmeydan, Ph.D., Director and Portfolio Manager. In the paragraphs below, the team discusses the performance of the Fund for the 12-month period ended September 30, 2019.

For the one year period ended September 30, 2019, Guggenheim Alpha Opportunity Fund returned -7.97%1, compared with the 2.39% return of its benchmark, the ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index. The Fund’s secondary benchmark is the Morningstar Long/Short Equity Category Average. Its return for the 12 months was -1.99%.

Investment Approach

The Fund is managed as an opportunistic long/short strategy, which employs forward-looking, fundamental analysis to measure the market’s expected return for each stock in the universe. Quantitative techniques are then applied to evaluate market- and company-specific risk factors embedded in each stock and to assess which specific risk factors (such as size, growth, or sectors) are being overvalued or undervalued by the market. Finally, a portfolio is constructed within guidelines that is long the stocks that give the portfolio both the broad risk characteristics and company-specific risks that are perceived to be undervalued and is short stocks for which those characteristics are perceived to be overpriced.

The Fund will ordinarily hold simultaneous long and short positions in equity securities or securities markets that provide exposure up to a level equal to 150% of the Fund’s net assets for both the long and short positions. The Fund intends to maintain a low overall net exposure (the difference between the notional value of long positions and the notional value of short positions), typically varying between 50% net long and 30% net short in order to maintain low correlation to traditional equity markets and lower-than-market volatility, and seek to provide consistent absolute return. The overall net exposure will change as market opportunities change, and may, based on the Fund’s view of current market conditions, be outside this range.

Derivatives in the Fund are used to take short positions as well as long exposure above 100% of NAV (that is, to take leverage).

Performance Review

The period began with a major market pullback and spike in volatility, before rebounding strongly in the first months of 2019. The economy had begun to slow, and the trade war continued to escalate, leading the U.S. Federal Reserve (the “Fed”) to change its tone from hawkish to dovish, signaling that rate cuts were now on the horizon. The Fed course reversal became a large driver of the risk-market, as the fears of steady rate rises causing a recession quickly dissipated. Equity markets took a short-term hit in May when trade threats against China and Mexico escalated. But like most other dips over the last few years, it was short and quickly reversed, as the administration lowered its trade rhetoric. As global growth expectations decreased while the risk of trade wars and disorderly BREXIT increased, investors continued moving towards safer assets such as long-term U.S. Treasurys and high-quality stocks. In August, the yield curve between the 2-year and 10-year U.S. Treasury rates briefly inverted, a historical indicator that has presaged past recessions. The Fed fully abandoned last year’s hawkish stance and cut short term rates two times during the period while calling it a “midcycle adjustment to policy.”

At period end, the Fund held about 115% of assets in long securities, and 91% short, for a net-dollar exposure of 24%. This level of net exposure is lower than the prior few years, primarily because of the Guggenheim macro view that economic data are pointing toward a high probability of recession. While the positive net market exposure resulted in some positive market attribution, the Fund is decidedly less exposed to the broad market returns than in prior years (and likewise less exposed to the market than most long/short equity managers). Indeed, much of the Fund’s returns for the period are mostly explained by sector and style positioning.

The realized net beta (sensitivity of daily Fund returns to the S&P 500 index) averaged around 0.28 during the year. The long positions (on a standalone unlevered basis) averaged a return of -1.0%, compared to the Russell 3000 index return of 2.9%. Short positions returned 6.7% on a stand-alone basis. Thus, our negative returns results from poor alpha on both longs and shorts.

The Fund’s sector positioning was a slight detractor for the year, contributing -0.35% to attribution. The largest sector detractor was the net short position in Real Estate, which performed quite strongly on beta-adjusted terms despite looking quite expensive vis-à-vis other defensive sectors. Mostly offsetting that drag were overweights in Consumer Staples and Utilities, which also outperformed the market on a beta-adjusted basis.

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 9 |

MANAGERS’ COMMENTARY (Unaudited)(concluded) | September 30, 2019 |

The Fund’s fundamental style tilts were the primary negative contributor to the period’s returns, resulting in about -5.80% of the contribution. The Fund’s tilts towards cheaper names underperformed, while tilts towards higher free cash flow and higher profitability helped offset that drag a little.

A performance factor for the period was the unprecedented persistence of value names underperforming expensive stocks. The magnitude of cumulative Value style underperformance is reaching historic levels last seen in the 1999 Tech bubble.

The Fund’s strategy is to determine attractiveness of broad groups of stocks relative to their fundamentals. The Value factor has seen its risk premium (or embedded valuation) improve as the returns have struggled–implying that the valuation of the stocks (both cheaper and expensive) have spread much further than fundamentals of the companies. To what extent this ‘behavioral’ cycle will continue is a key question–and one that is very difficult to answer. In every market environment there are elements of the macro-economic cycle that are somewhat predictable, and elements that are new and completely unpredictable (global quantitative easing, negative long rates, and trade wars being the most unique factors this time around). These unique elements can drive market sentiment in ways that are hard to predict.

Focusing on corporate fundamentals tends to produce slightly more predictability. Companies must invest in operations & research to produce sales and earnings–and there are some bounds on how much and how little the companies can earn on that capital before competition comes in to erode them. Given some bounded limits on corporate earnings power, we find that the valuations awarded the most expensive tiers of the equity market have far surpassed the likely long-term earnings power.

We find some comfort during a poor performance period in knowing that, in past periods of Value drawdown, the forward performance of the factor has been tremendous due to the rewinding of all the excess valuations.

The Fund has not wavered in its valuation-disciplined approach to finding long and short equity opportunities. We continue to utilize ways for our dynamic factor approach to help mitigate these types of intermittent factor waves but have not been able to completely offset them in the current cycle. The Fund is primarily set up to take advantage of valuation disparities caused by behavioral cycles–by taking opposing long and short style and sector exposures where extremes exist–and trying to deliver positive returns that are not correlated with overall market direction. We see today large disparities that have historically provided strong fuel for opportunistic returns in the past and plan to stick with the discipline to reap those rewards going forward.

In early September, we saw a huge reversal of the above trend over the course of a few days. The weekly move in ‘momentum’ and ‘value’ factors were of magnitudes not seen in a decade. A key question is whether this heightened volatility is a precursor to further value/momentum reversal, or just a short-term trading fluke. The equity style reversal in September may have simply been a knee jerk reaction to the quick pop in interest rates at that time (the compression in yields has highly correlated with the bias towards expensive stocks). History also shows that strong momentum creates crowding in narrow market leaders, and that crowding can turn into a rush to exit as soon as the leading names become more volatile.

Positioning

At period end, the Fund’s net dollar exposure was 24%, the lower end of where we have been historically. The Fund maintains its large style bias towards cheaper valuation names, while maintaining moderate free cash flow bias and profitability bias–both of which are styles that have historically helped protect against macro risk in the event of recession. Guggenheim’s macro research team is still wary of recession in the next year or so and vulnerability in overall markets–and the Fund has likewise taken a cautious positioning with quality style characteristics and lower overall market exposure.

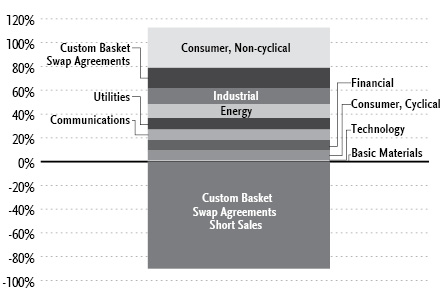

From an industry perspective, the Fund now holds a net short in the Technology sector after prior years of being positioned net long. The flip in exposure occurred during this year in response to relative attractiveness of the names vis-à-vis other sector opportunities. The net short in Financials has begun to shrink after remaining quite negative for a few years. The largest sector net long exposures are in Healthcare, Consumer Staples, and Transportation. The largest net short exposures exist in Real Estate, Materials, and IT sectors.

Performance displayed represents past performance which is no guarantee of future results.

1 | Performance figures are based on Class A shares and do not reflect deduction of the sales charges or taxes that a shareholder would pay on distributions or the redemption of shares. |

The opinions and forecast expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

10 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | September 30, 2019 |

ALPHA OPPORTUNITY FUND

OBJECTIVE: Seeks long-term growth of capital.

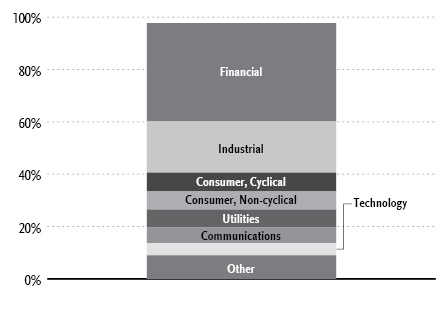

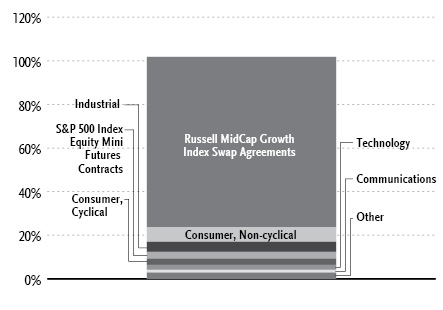

Holdings Diversification (Market Exposure as % of Net Assets)

“Holdings Diversification (Market Exposure as % of Net Assets)” excludes any temporary cash investments.

Inception Dates: |

A-Class | July 7, 2003 |

C-Class | July 7, 2003 |

P-Class | May 1, 2015 |

Institutional Class | November 7, 2008 |

Ten Largest Holdings (% of Total Net Assets) |

ONEOK, Inc. | 1.4% |

Equity Commonwealth | 1.3% |

Archer-Daniels-Midland Co. | 1.3% |

Apartment Investment & Management Co. — Class A | 1.3% |

Chevron Corp. | 1.2% |

Exxon Mobil Corp. | 1.2% |

Amgen, Inc. | 1.2% |

Kinder Morgan, Inc. | 1.2% |

Medical Properties Trust, Inc. | 1.2% |

Verizon Communications, Inc. | 1.2% |

Top Ten Total | 12.5% |

| | |

“Ten Largest Holdings” excludes any temporary cash or derivative investments. |

| | THE GUGGENHEIM FUNDS ANNUAL REPORT | 11 |

PERFORMANCE REPORT AND FUND PROFILE (Unaudited)(concluded) | September 30, 2019 |

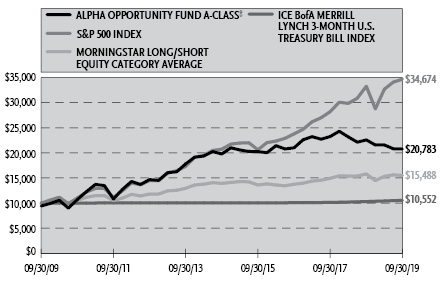

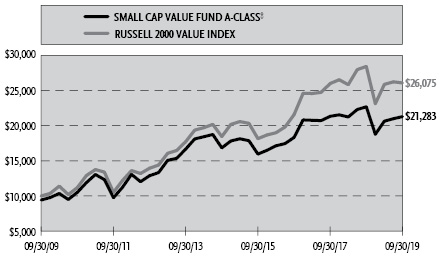

Cumulative Fund Performance*

Average Annual Returns*

Periods Ended September 30, 2019

| 1 Year | 5 Year | 10 Year |

A-Class Shares | (7.97%) | 0.99% | 8.23% |

A-Class Shares with sales charge‡ | (12.32%) | 0.01% | 7.59% |

C-Class Shares | (8.73%) | 0.23% | 7.41% |

C-Class Shares with CDSC§ | (9.64%) | 0.23% | 7.41% |

Institutional Class Shares | (7.57%) | 1.45% | 8.66% |

Morningstar Long/Short Equity Category Average | (1.99%) | 2.15% | 4.47% |

S&P 500 Index | 4.25% | 10.84% | 13.24% |

S&P 500 Index-Blended** | 2.39% | 5.80% | 10.63% |

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | 2.39% | 0.98% | 0.54% |

| | 1 Year | Since

Inception

(05/01/15) |

P-Class Shares | | (7.99%) | (0.21%) |

Morningstar Long/Short Equity Category Average | | (1.99%) | 1.69% |

S&P 500 Index | | 4.25% | 10.39% |

S&P 500 Index-Blended** | | 2.39% | 4.73% |

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | | 2.39% | 1.11% |

* | The performance data above represents past performance that is not predictive of future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns are historical and include changes in principal and reinvested dividends and capital gains and do not reflect the effect of taxes. The ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index, S&P 500 Index, and the Morningstar Long/Short Equity Category Average are unmanaged indices and, unlike the Fund, have no management fees or operating expenses to reduce their reported returns. The graph is based on A-Class shares only; performance for C-Class, P-Class and Institutional Class will vary due to differences in fee structures. |

** | Effective March 13, 2017, the Fund changed its principal investment strategy. As a result of the investment strategy change, the Fund’s new benchmark is the ICE BofA Merrill Lynch 3-Month Treasury Bill Index. The Fund’s performance was previously compared to the S&P 500 Index. The S&P 500 Index-Blended uses performance data for the S&P 500 Index from 03/31/09 to 03/12/17, and the ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill index from 03/13/17 to 09/30/19. |

‡ | Effective February 22, 2011, the maximum sales charge decreased from 5.75% to 4.75%. A 5.75% maximum sales charge is used in the calculation of the Average Annual Returns based on subscriptions made prior to February 22, 2011, and a 4.75% maximum sales charge will be used to calculate performance for periods based on subscriptions made on or after February 22, 2011. |

§ | Fund returns include a CDSC of 1% if redeemed within 12 months of purchase. |

12 | THE GUGGENHEIM FUNDS ANNUAL REPORT | |

SCHEDULE OF INVESTMENTS | September 30, 2019 |

ALPHA OPPORTUNITY FUND | |

| | Shares | | | Value | |

COMMON STOCKS† - 95.9% |

| | | | | | | | | |

Consumer, Non-cyclical - 33.9% |

Archer-Daniels-Midland Co.1 | | | 28,659 | | | $ | 1,177,025 | |

Amgen, Inc.1 | | | 5,555 | | | | 1,074,948 | |

McKesson Corp. | | | 7,691 | | | | 1,051,052 | |

Ingredion, Inc.1 | | | 12,160 | | | | 993,958 | |

Merck & Company, Inc.1 | | | 11,599 | | | | 976,404 | |

Gilead Sciences, Inc.1 | | | 14,841 | | | | 940,623 | |

Molson Coors Brewing Co. — Class B1 | | | 15,705 | | | | 903,038 | |

Zimmer Biomet Holdings, Inc.1 | | | 6,320 | | | | 867,547 | |

CVS Health Corp. | | | 13,581 | | | | 856,554 | |

Pilgrim’s Pride Corp.* | | | 25,127 | | | | 805,195 | |

Pfizer, Inc.1 | | | 22,000 | | | | 790,460 | |

PepsiCo, Inc. | | | 5,652 | | | | 774,889 | |

Cal-Maine Foods, Inc. | | | 18,605 | | | | 743,363 | |

Kimberly-Clark Corp. | | | 5,223 | | | | 741,927 | |

Becton Dickinson and Co. | | | 2,742 | | | | 693,616 | |

Tyson Foods, Inc. — Class A | | | 7,635 | | | | 657,679 | |

Sysco Corp. | | | 7,592 | | | | 602,805 | |

Hill-Rom Holdings, Inc. | | | 5,699 | | | | 599,706 | |

Baxter International, Inc. | | | 6,822 | | | | 596,720 | |

AMERCO | | | 1,529 | | | | 596,371 | |

Colgate-Palmolive Co. | | | 8,107 | | | | 595,945 | |

H&R Block, Inc. | | | 24,559 | | | | 580,083 | |

Hologic, Inc.* | | | 11,290 | | | | 570,032 | |

Philip Morris International, Inc. | | | 7,458 | | | | 566,286 | |

Kroger Co.1 | | | 21,696 | | | | 559,323 | |

Darling Ingredients, Inc.* | | | 29,076 | | | | 556,224 | |

Eli Lilly & Co. | | | 4,691 | | | | 524,595 | |

Thermo Fisher Scientific, Inc. | | | 1,780 | | | | 518,461 | |

General Mills, Inc. | | | 9,396 | | | | 517,907 | |

Post Holdings, Inc.* | | | 4,871 | | | | 515,547 | |

Medtronic plc1 | | | 4,656 | | | | 505,735 | |

Hormel Foods Corp. | | | 10,264 | | | | 448,845 | |

Johnson & Johnson | | | 3,253 | | | | 420,873 | |

Biogen, Inc.* | | | 1,735 | | | | 403,943 | |

JM Smucker Co. | | | 3,663 | | | | 403,003 | |

Cardinal Health, Inc.1 | | | 8,490 | | | | 400,643 | |

Jazz Pharmaceuticals plc* | | | 3,089 | | | | 395,824 | |

Bio-Rad Laboratories, Inc. — Class A*,1 | | | 1,107 | | | | 368,343 | |

Integer Holdings Corp.* | | | 4,859 | | | | 367,146 | |

AmerisourceBergen Corp. — Class A | | | 4,422 | | | | 364,063 | |

ManpowerGroup, Inc. | | | 4,270 | | | | 359,705 | |

Lamb Weston Holdings, Inc. | | | 4,856 | | | | 353,128 | |

STERIS plc | | | 2,411 | | | | 348,365 | |

US Foods Holding Corp.* | | | 8,078 | | | | 332,006 | |

Campbell Soup Co. | | | 7,045 | | | | 330,551 | |

Herbalife Nutrition Ltd.* | | | 8,717 | | | | 330,026 | |

Kellogg Co. | | | 5,077 | | | | 326,705 | |

Regeneron Pharmaceuticals, Inc.* | | | 1,098 | | | | 304,585 | |

TrueBlue, Inc.* | | | 13,668 | | | | 288,395 | |

Central Garden & Pet Co. — Class A* | | | 10,001 | | | | 277,278 | |

Alexion Pharmaceuticals, Inc.* | | | 2,679 | | | | 262,381 | |

Innoviva, Inc.* | | | 23,237 | | | | 244,918 | |

Kraft Heinz Co.1 | | | 8,096 | | | | 226,162 | |

B&G Foods, Inc. | | | 11,949 | | | | 225,955 | |

Total Consumer, Non-cyclical | | | | | | | 30,236,861 | |

| | | | | | | | | |

Industrial - 13.5% |

United Parcel Service, Inc. — Class B | | | 7,989 | | �� | | 957,242 | |

FedEx Corp.1 | | | 5,819 | | | | 847,072 | |

Landstar System, Inc. | | | 6,374 | | | | 717,585 | |

Cummins, Inc. | | | 3,888 | | | | 632,461 | |

CSX Corp.1 | | | 8,749 | | | | 606,043 | |

Werner Enterprises, Inc. | | | 16,015 | | | | 565,330 | |

Knight-Swift Transportation Holdings, Inc. | | | 15,111 | | | | 548,529 | |

Schneider National, Inc. — Class B | | | 25,176 | | | | 546,823 | |

Norfolk Southern Corp. | | | 2,694 | | | | 484,004 | |

Saia, Inc.* | | | 5,055 | | | | 473,654 | |

Heartland Express, Inc. | | | 21,532 | | | | 463,153 | |

Old Dominion Freight Line, Inc. | | | 2,609 | | | | 443,452 | |

Forward Air Corp. | | | 6,489 | | | | 413,479 | |

Echo Global Logistics, Inc.* | | | 17,847 | | | | 404,235 | |

Kennametal, Inc. | | | 12,669 | | | | 389,445 | |

Waters Corp.* | | | 1,715 | | | | 382,839 | |

J.B. Hunt Transport Services, Inc.1 | | | 3,399 | | | | 376,099 | |

Agilent Technologies, Inc. | | | 4,847 | | | | 371,426 | |

Marten Transport Ltd. | | | 17,680 | | | | 367,390 | |

Kansas City Southern1 | | | 2,702 | | | | 359,393 | |

Union Pacific Corp. | | | 1,908 | | | | 309,058 | |

Parker-Hannifin Corp. | | | 1,388 | | | | 250,687 | |

Vishay Intertechnology, Inc. | | | 14,558 | | | | 246,467 | |

Avnet, Inc. | | | 5,330 | | | | 237,105 | |

Textron, Inc. | | | 4,712 | | | | 230,699 | |

Oshkosh Corp. | | | 2,843 | | | | 215,499 | |

Caterpillar, Inc. | | | 1,706 | | | | 215,485 | |

Total Industrial | | | | | | | 12,054,654 | |

| | | | | | | | | |

Energy - 11.9% |

ONEOK, Inc.1 | | | 16,404 | | | | 1,208,811 | |

Chevron Corp.1 | | | 9,231 | | | | 1,094,797 | |

Exxon Mobil Corp.1 | | | 15,379 | | | | 1,085,911 | |

Kinder Morgan, Inc. | | | 52,149 | | | | 1,074,791 | |

Phillips 661 | | | 9,034 | | | | 925,082 | |

HollyFrontier Corp.1 | | | 16,671 | | | | 894,232 | |

Valero Energy Corp.1 | | | 10,262 | | | | 874,733 | |

Marathon Petroleum Corp. | | | 12,871 | | | | 781,913 | |

Williams Companies, Inc. | | | 29,486 | | | | 709,433 | |

Delek US Holdings, Inc. | | | 18,784 | | | | 681,859 | |

Targa Resources Corp. | | | 9,780 | | | | 392,862 | |

Renewable Energy Group, Inc.* | | | 21,820 | | | | 327,409 | |

Cheniere Energy, Inc.* | | | 4,161 | | | | 262,393 | |

PBF Energy, Inc. — Class A | | | 7,835 | | | | 213,034 | |

Unit Corp.* | | | 35,705 | | | | 120,683 | |

Total Energy | | | | | | | 10,647,943 | |

| | | | | | | | | |

Utilities - 9.5% |

Pinnacle West Capital Corp. | | | 10,483 | | | | 1,017,585 | |

Portland General Electric Co. | | | 17,668 | | | | 995,945 | |

Ameren Corp.1 | | | 12,155 | | | | 973,008 | |

FirstEnergy Corp.1 | | | 19,640 | | | | 947,237 | |

PPL Corp. | | | 28,335 | | | | 892,269 | |

SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 13 |

SCHEDULE OF INVESTMENTS (continued) | September 30, 2019 |

ALPHA OPPORTUNITY FUND | |

| | Shares | | | Value | |

National Fuel Gas Co.1 | | | 18,010 | | | $ | 845,029 | |

Exelon Corp. | | | 13,043 | | | | 630,107 | |

Avista Corp. | | | 10,542 | | | | 510,655 | |

AES Corp.1 | | | 28,462 | | | | 465,069 | |

OGE Energy Corp. | | | 9,765 | | | | 443,136 | |

Southern Co. | | | 6,431 | | | | 397,243 | |

Public Service Enterprise Group, Inc. | | | 5,898 | | | | 366,148 | |

Total Utilities | | | | | | | 8,483,431 | |

| | | | | | | | | |

Communications - 8.9% |

Verizon Communications, Inc. | | | 17,435 | | | | 1,052,377 | |

Omnicom Group, Inc.1 | | | 11,764 | | | | 921,121 | |

AT&T, Inc.1 | | | 21,990 | | | | 832,101 | |

AMC Networks, Inc. — Class A*,1 | | | 13,606 | | | | 668,871 | |

Shenandoah Telecommunications Co. | | | 19,062 | | | | 605,600 | |

Discovery, Inc. — Class A* | | | 21,928 | | | | 583,943 | |

Scholastic Corp. | | | 14,872 | | | | 561,567 | |

John Wiley & Sons, Inc. — Class A | | | 12,025 | | | | 528,378 | |

Cogent Communications Holdings, Inc. | | | 9,076 | | | | 500,087 | |

ATN International, Inc. | | | 5,884 | | | | 343,449 | |

News Corp. — Class A | | | 22,489 | | | | 313,047 | |

Meredith Corp. | | | 8,071 | | | | 295,883 | |

TEGNA, Inc. | | | 16,996 | | | | 263,948 | |

Alphabet, Inc. — Class C* | | | 200 | | | | 243,800 | |

Facebook, Inc. — Class A* | | | 1,146 | | | | 204,080 | |

Total Communications | | | | | | | 7,918,252 | |

| | | | | | | | | |

Financial - 8.8% |

Equity Commonwealth REIT1 | | | 34,668 | | | | 1,187,379 | |

Apartment Investment & Management Co. — Class A REIT1 | | | 22,555 | | | | 1,176,018 | |

Medical Properties Trust, Inc. REIT | | | 54,023 | | | | 1,056,690 | |

HCP, Inc. REIT | | | 25,275 | | | | 900,548 | |

Hartford Financial Services Group, Inc.1 | | | 8,209 | | | | 497,547 | |

Deluxe Corp. | | | 9,378 | | | | 461,023 | |

Host Hotels & Resorts, Inc. REIT | | | 23,883 | | | | 412,937 | |

Northern Trust Corp. | | | 3,920 | | | | 365,814 | |

Summit Hotel Properties, Inc. REIT | | | 31,187 | | | | 361,769 | |

JPMorgan Chase & Co. | | | 2,342 | | | | 275,630 | |

Principal Financial Group, Inc. | | | 4,498 | | | | 257,016 | |

State Street Corp. | | | 4,089 | | | | 242,028 | |

Bank of New York Mellon Corp. | | | 5,131 | | | | 231,973 | |

Citigroup, Inc. | | | 3,206 | | | | 221,470 | |

Comerica, Inc. | | | 3,320 | | | | 219,087 | |

Total Financial | | | | | | | 7,866,929 | |

| | | | | | | | | |

Consumer, Cyclical - 8.1% |

Delta Air Lines, Inc.1 | | | 13,988 | | | | 805,709 | |

Southwest Airlines Co. | | | 13,576 | | | | 733,240 | |

Allison Transmission Holdings, Inc. | | | 15,334 | | | | 721,465 | |

United Airlines Holdings, Inc.*,1 | | | 7,527 | | | | 665,462 | |

JetBlue Airways Corp.* | | | 38,368 | | | | 642,664 | |

World Fuel Services Corp. | | | 14,816 | | | | 591,751 | |

Toll Brothers, Inc. | | | 10,986 | | | | 450,975 | |

Alaska Air Group, Inc. | | | 6,784 | | | | 440,349 | |

BorgWarner, Inc. | | | 11,632 | | | | 426,662 | |

Brinker International, Inc. | | | 8,573 | | | | 365,810 | |

General Motors Co. | | | 8,658 | | | | 324,502 | |

Lear Corp. | | | 2,746 | | | | 323,753 | |

Walgreens Boots Alliance, Inc. | | | 5,599 | | | | 309,681 | |

PACCAR, Inc. | | | 3,332 | | | | 233,273 | |

Lions Gate Entertainment Corp. — Class A* | | | 19,914 | | | | 184,204 | |

Total Consumer, Cyclical | | | | | | | 7,219,500 | |

| | | | | | | | | |

Technology - 0.8% |

Skyworks Solutions, Inc. | | | 3,672 | | | | 291,006 | |

Diodes, Inc.* | | | 6,190 | | | | 248,528 | |

Oracle Corp.1 | | | 3,960 | | | | 217,919 | |

Total Technology | | | | | | | 757,453 | |

| | | | | | | | | |

Basic Materials - 0.5% |

Westlake Chemical Corp. | | | 3,378 | | | | 221,327 | |

Domtar Corp. | | | 5,576 | | | | 199,676 | |

Total Basic Materials | | | | | | | 421,003 | |

| | | | | | | | | |

Total Common Stocks | | | | | | | | |

(Cost $83,769,680) | | | | | | | 85,606,026 | |

| | | | | | | | | |

MONEY MARKET FUND† - 6.6% |

Goldman Sachs Financial Square Treasury Instruments Fund — Institutional Shares 1.79%2 | | | 5,866,464 | | | | 5,866,464 | |

Total Money Market Fund | | | | | | | | |

(Cost $5,866,464) | | | | | | | 5,866,464 | |

| | | | | | | | | |

Total Investments - 102.5% | | | | | | | | |

(Cost $89,636,144) | | | | | | $ | 91,472,490 | |

Other Assets & Liabilities, net - (2.5)% | | | | | | | (2,222,028 | ) |

Total Net Assets - 100.0% | | | | | | $ | 89,250,462 | |

14 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

SCHEDULE OF INVESTMENTS (continued) | September 30, 2019 |

ALPHA OPPORTUNITY FUND | |

Custom Basket Swap Agreements | | | | |

Counterparty | Reference Obligation | Financing Rate

Pay (Receive) | | Payment

Frequency | | | Maturity

Date | | | Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

OTC Custom Basket Swap Agreements†† | | | | | | | | |

Goldman Sachs International | GS Equity Custom Basket | 2.28% (Federal Funds Rate + 0.45%) | At Maturity | | | 05/06/24 | | | $ | 7,581,749 | | | $ | 208,633 | |

Morgan Stanley Capital Services LLC | MS Equity Custom Basket | 2.25% (Federal Funds Rate + 0.40%) | At Maturity | | | 02/01/24 | | | | 7,581,719 | | | | 187,779 | |

| | | | | | | | | | | | | $ | 15,163,468 | | | $ | 396,412 | |

| | | | | | | | | | | | | | | | | | | |

OTC Custom Basket Swap Agreements Sold Short†† | | | | | | | | | | | | | | | | |

Morgan Stanley Capital Services LLC | MS Equity Custom Basket | (1.55)% (Federal Funds Rate - 0.30%) | At Maturity | | | 02/01/24 | | | $ | 40,857,931 | | | $ | (1,869,155 | ) |

Goldman Sachs International | GS Equity Custom Basket | (1.63)% (Federal Funds Rate - 0.20%) | At Maturity | | | 05/06/24 | | | | 39,316,842 | | | | (794,924 | ) |

| | | | | | | | | | | | | $ | 80,174,773 | | | $ | (2,664,079 | ) |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

MS EQUITY LONG CUSTOM BASKET | | | | | | | | |

Communications | | | | | | | | | | | | |

TEGNA, Inc. | | | 1,700 | | | | 0.36 | % | | $ | 6,814 | |

Omnicom Group, Inc. | | | 957 | | | | 1.00 | % | | | 5,205 | |

Verizon Communications, Inc. | | | 1,419 | | | | 1.14 | % | | | 4,450 | |

News Corp. — Class A | | | 1,830 | | | | 0.34 | % | | | 2,945 | |

ATN International, Inc. | | | 479 | | | | 0.37 | % | | | 1,695 | |

Alphabet, Inc. — Class C | | | 16 | | | | 0.26 | % | | | 1,374 | |

Facebook, Inc. — Class A | | | 93 | | | | 0.22 | % | | | 1,136 | |

John Wiley & Sons, Inc. — Class A | | | 978 | | | | 0.57 | % | | | (512 | ) |

Scholastic Corp. | | | 1,210 | | | | 0.60 | % | | | (571 | ) |

Discovery, Inc. — Class A | | | 1,784 | | | | 0.63 | % | | | (2,179 | ) |

Cogent Communications Holdings, Inc. | | | 997 | | | | 0.72 | % | | | (3,225 | ) |

AMC Networks, Inc. — Class A | | | 1,107 | | | | 0.72 | % | | | (7,810 | ) |

Meredith Corp. | | | 657 | | | | 0.32 | % | | | (13,532 | ) |

Shenandoah Telecommunications Co. | | | 1,551 | | | | 0.65 | % | | | (22,195 | ) |

Total Communications | | | | | | | | | | | (26,405 | ) |

| | | | | | | | | | | | | |

Consumer, Cyclical | | | | | | | | | | | | |

World Fuel Services Corp. | | | 1,548 | | | | 0.82 | % | | | 16,659 | |

Delta Air Lines, Inc. | | | 1,138 | | | | 0.86 | % | | | 8,734 | |

United Airlines Holdings, Inc. | | | 612 | | | | 0.71 | % | | | 6,047 | |

Alaska Air Group, Inc. | | | 552 | | | | 0.47 | % | | | 5,476 | |

Toll Brothers, Inc. | | | 894 | | | | 0.48 | % | | | 4,744 | |

Southwest Airlines Co. | | | 1,105 | | | | 0.79 | % | | | 4,619 | |

Allison Transmission Holdings, Inc. | | | 1,248 | | | | 0.77 | % | | | 2,747 | |

JetBlue Airways Corp. | | | 3,123 | | | | 0.69 | % | | | 2,134 | |

Brinker International, Inc. | | | 697 | | | | 0.39 | % | | | 1,614 | |

PACCAR, Inc. | | | 271 | | | | 0.25 | % | | | 1,270 | |

General Motors Co. | | | 704 | | | | 0.35 | % | | | (1,727 | ) |

Walgreens Boots Alliance, Inc. | | | 455 | | | | 0.33 | % | | | (3,132 | ) |

Lear Corp. | | | 223 | | | | 0.35 | % | | | (3,329 | ) |

BorgWarner, Inc. | | | 946 | | | | 0.46 | % | | | (3,643 | ) |

Lions Gate Entertainment Corp. — Class A | | | 8,752 | | | | 1.07 | % | | | (8,178 | ) |

Total Consumer, Cyclical | | | | | | | | | | | 34,035 | |

| | | | | | | | | | | | | |

Consumer, Non-cyclical | | | | | | | | | | | | |

Pilgrim’s Pride Corp. | | | 2,045 | | | | 0.86 | % | | | 22,473 | |

Tyson Foods, Inc. — Class A | | | 862 | | | | 0.98 | % | | | 21,295 | |

Kimberly-Clark Corp. | | | 425 | | | | 0.80 | % | | | 12,586 | |

McKesson Corp. | | | 1,308 | | | | 2.36 | % | | | 12,321 | |

CVS Health Corp. | | | 1,105 | | | | 0.92 | % | | | 11,049 | |

Zimmer Biomet Holdings, Inc. | | | 514 | | | | 0.93 | % | | | 9,667 | |

Sysco Corp. | | | 618 | | | | 0.65 | % | | | 8,504 | |

Molson Coors Brewing Co. — Class B | | | 3,732 | | | | 2.83 | % | | | 8,117 | |

Medtronic plc | | | 378 | | | | 0.54 | % | | | 6,940 | |

Merck & Company, Inc. | | | 944 | | | | 1.05 | % | | | 6,539 | |

Hologic, Inc. | | | 919 | | | | 0.61 | % | | | 5,181 | |

Colgate-Palmolive Co. | | | 659 | | | | 0.64 | % | | | 4,815 | |

Baxter International, Inc. | | | 555 | | | | 0.64 | % | | | 4,754 | |

US Foods Holding Corp. | | | 657 | | | | 0.36 | % | | | 4,406 | |

Hill-Rom Holdings, Inc. | | | 463 | | | | 0.64 | % | | | 4,096 | |

Cardinal Health, Inc. | | | 1,657 | | | | 1.03 | % | | | 3,741 | |

General Mills, Inc. | | | 764 | | | | 0.56 | % | | | 3,622 | |

Central Garden & Pet Co. — Class A | | | 814 | | | | 0.30 | % | | | 3,464 | |

SEE NOTES TO FINANCIAL STATEMENTS. | THE GUGGENHEIM FUNDS ANNUAL REPORT | 15 |

SCHEDULE OF INVESTMENTS (continued) | September 30, 2019 |

ALPHA OPPORTUNITY FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

AMERCO | | | 124 | | | | 0.64 | % | | $ | 3,390 | |

Kellogg Co. | | | 413 | | | | 0.35 | % | | | 3,352 | |

PepsiCo, Inc. | | | 460 | | | | 0.83 | % | | | 3,314 | |

Campbell Soup Co. | | | 573 | | | | 0.35 | % | | | 3,281 | |

Amgen, Inc. | | | 452 | | | | 1.15 | % | | | 2,966 | |

Kroger Co. | | | 1,765 | | | | 0.60 | % | | | 2,570 | |

Becton Dickinson and Co. | | | 223 | | | | 0.74 | % | | | 2,424 | |

Eli Lilly & Co. | | | 381 | | | | 0.56 | % | | | 2,001 | |

Hormel Foods Corp. | | | 835 | | | | 0.48 | % | | | 1,959 | |

Lamb Weston Holdings, Inc. | | | 395 | | | | 0.38 | % | | | 1,768 | |

Biogen, Inc. | | | 141 | | | | 0.43 | % | | | 1,567 | |

ManpowerGroup, Inc. | | | 347 | | | | 0.39 | % | | | 763 | |

Philip Morris International, Inc. | | | 607 | | | | 0.61 | % | | | 99 | |

Jazz Pharmaceuticals plc | | | 251 | | | | 0.42 | % | | | (207 | ) |

Thermo Fisher Scientific, Inc. | | | 144 | | | | 0.55 | % | | | (227 | ) |

JM Smucker Co. | | | 298 | | | | 0.43 | % | | | (250 | ) |

STERIS plc | | | 196 | | | | 0.37 | % | | | (547 | ) |

Gilead Sciences, Inc. | | | 1,208 | | | | 1.01 | % | | | (680 | ) |

AmerisourceBergen Corp. — Class A | | | 1,383 | | | | 1.50 | % | | | (1,035 | ) |

Post Holdings, Inc. | | | 396 | | | | 0.55 | % | | | (1,299 | ) |

Regeneron Pharmaceuticals, Inc. | | | 89 | | | | 0.33 | % | | | (1,619 | ) |

TrueBlue, Inc. | | | 1,112 | | | | 0.31 | % | | | (1,916 | ) |

Johnson & Johnson | | | 264 | | | | 0.45 | % | | | (2,188 | ) |

Kraft Heinz Co. | | | 659 | | | | 0.24 | % | | | (3,052 | ) |

B&G Foods, Inc. | | | 972 | | | | 0.24 | % | | | (3,178 | ) |

Integer Holdings Corp. | | | 395 | | | | 0.39 | % | | | (3,284 | ) |

Archer-Daniels-Midland Co. | | | 2,332 | | | | 1.26 | % | | | (3,311 | ) |

Darling Ingredients, Inc. | | | 2,366 | | | | 0.60 | % | | | (4,016 | ) |

Innoviva, Inc. | | | 1,891 | | | | 0.26 | % | | | (5,957 | ) |

Cal-Maine Foods, Inc. | | | 1,514 | | | | 0.80 | % | | | (6,157 | ) |

Alexion Pharmaceuticals, Inc. | | | 218 | | | | 0.28 | % | | | (6,160 | ) |

H&R Block, Inc. | | | 1,999 | | | | 0.62 | % | | | (8,788 | ) |

Pfizer, Inc. | | | 1,790 | | | | 0.85 | % | | | (10,901 | ) |

Ingredion, Inc. | | | 989 | | | | 1.07 | % | | | (11,057 | ) |

Herbalife Nutrition Ltd. | | | 1,266 | | | | 0.63 | % | | | (17,468 | ) |

Total Consumer, Non-cyclical | | | | | | | | | | | 89,727 | |

| | | | | | | | | | | | | |

Financial | | | | | | | | | | | | |

HCP, Inc. | | | 2,057 | | | | 0.97 | % | | | 7,580 | |

Medical Properties Trust, Inc. | | | 4,397 | | | | 1.13 | % | | | 7,251 | |

Deluxe Corp. | | | 763 | | | | 0.49 | % | | | 6,497 | |

Hartford Financial Services Group, Inc. | | | 668 | | | | 0.53 | % | | | 6,043 | |

Equity Commonwealth | | | 2,821 | | | | 1.27 | % | | | 5,478 | |

JPMorgan Chase & Co. | | | 190 | | | | 0.29 | % | | | 3,441 | |

Apartment Investment & Management Co. — Class A | | | 1,835 | | | | 1.26 | % | | | 3,289 | |

Northern Trust Corp. | | | 319 | | | | 0.39 | % | | | 1,277 | |

Summit Hotel Properties, Inc. | | | 2,538 | | | | 0.39 | % | | | 612 | |

State Street Corp. | | | 332 | | | | 0.26 | % | | | 112 | |

Bank of New York Mellon Corp. | | | 417 | | | | 0.25 | % | | | 35 | |

Citigroup, Inc. | | | 261 | | | | 0.24 | % | | | (458 | ) |

Principal Financial Group, Inc. | | | 366 | | | | 0.28 | % | | | (707 | ) |

Comerica, Inc. | | | 270 | | | | 0.23 | % | | | (1,113 | ) |

Host Hotels & Resorts, Inc. | | | 1,943 | | | | 0.44 | % | | | (1,543 | ) |

Total Financial | | | | | | | | | | | 37,794 | |

| | | | | | | | | | | | | |

Industrial | | | | | | | | | | | | |

Saia, Inc. | | | 656 | | | | 0.81 | % | | | 21,672 | |

United Parcel Service, Inc. — Class B | | | 650 | | | | 1.03 | % | | | 7,134 | |

Knight-Swift Transportation Holdings, Inc. | | | 1,230 | | | | 0.59 | % | | | 6,052 | |

Kansas City Southern | | | 332 | | | | 0.58 | % | | | 5,885 | |

J.B. Hunt Transport Services, Inc. | | | 464 | | | | 0.68 | % | | | 5,731 | |

Marten Transport Ltd. | | | 1,439 | | | | 0.39 | % | | | 5,690 | |

Old Dominion Freight Line, Inc. | | | 212 | | | | 0.48 | % | | | 5,668 | |

Heartland Express, Inc. | | | 2,406 | | | | 0.68 | % | | | 5,628 | |

Cummins, Inc. | | | 316 | | | | 0.68 | % | | | 4,476 | |

Landstar System, Inc. | | | 518 | | | | 0.77 | % | | | 4,202 | |

Agilent Technologies, Inc. | | | 394 | | | | 0.40 | % | | | 3,469 | |

Schneider National, Inc. — Class B | | | 2,704 | | | | 0.77 | % | | | 2,854 | |

Werner Enterprises, Inc. | | | 1,303 | | | | 0.61 | % | | | 2,740 | |

Echo Global Logistics, Inc. | | | 1,452 | | | | 0.43 | % | | | 2,448 | |

Parker-Hannifin Corp. | | | 113 | | | | 0.27 | % | | | 1,797 | |

Avnet, Inc. | | | 433 | | | | 0.25 | % | | | 821 | |

Oshkosh Corp. | | | 231 | | | | 0.23 | % | | | 707 | |

Forward Air Corp. | | | 528 | | | | 0.44 | % | | | 418 | |

Caterpillar, Inc. | | | 138 | | | | 0.23 | % | | | 229 | |

Textron, Inc. | | | 383 | | | | 0.25 | % | | | (473 | ) |

Norfolk Southern Corp. | | | 219 | | | | 0.52 | % | | | (604 | ) |

CSX Corp. | | | 923 | | | | 0.84 | % | | | (1,368 | ) |

Vishay Intertechnology, Inc. | | | 1,184 | | | | 0.26 | % | | | (1,693 | ) |

Union Pacific Corp. | | | 155 | | | | 0.33 | % | | | (1,747 | ) |

Waters Corp. | | | 139 | | | | 0.41 | % | | | (3,634 | ) |

Kennametal, Inc. | | | 1,031 | | | | 0.42 | % | | | (4,591 | ) |

FedEx Corp. | | | 473 | | | | 0.91 | % | | | (14,436 | ) |

Total Industrial | | | | | | | | | | | 59,075 | |

| | | | | | | | | | | | | |

16 | THE GUGGENHEIM FUNDS ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS. |

SCHEDULE OF INVESTMENTS (continued) | September 30, 2019 |

ALPHA OPPORTUNITY FUND | |

| | Shares | | | Percentage

Notional

Amount | | | Value and

Unrealized

Appreciation

(Depreciation) | |

Energy | | | | | | | | | | | | |

Kinder Morgan, Inc. | | | 4,244 | | | | 1.15 | % | | $ | 9,491 | |

ONEOK, Inc. | | | 1,335 | | | | 1.30 | % | | | 8,046 | |

Marathon Petroleum Corp. | | | 1,047 | | | | 0.84 | % | | | 7,053 | |

Delek US Holdings, Inc. | | | 1,528 | | | | 0.73 | % | | | 5,283 | |

HollyFrontier Corp. | | | 1,356 | | | | 0.96 | % | | | 3,958 | |

Phillips 66 | | | 735 | | | | 0.99 | % | | | 3,771 | |

Valero Energy Corp. | | | 835 | | | | 0.94 | % | | | 446 | |

Targa Resources Corp. | | | 796 | | | | 0.42 | % | | | (1,163 | ) |

Chevron Corp. | | | 751 | | | | 1.17 | % | | | (3,147 | ) |

Williams Companies, Inc. | | | 2,400 | | | | 0.76 | % | | | (7,576 | ) |

Exxon Mobil Corp. | | | 1,251 | | | | 1.17 | % | | | (10,226 | ) |