UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: | 811-06652 |

|

|

Exact name of registrant as specified in charter: | Aberdeen Investment Funds |

|

|

Address of principal executive offices: | 1900 Market Street, Suite 200 |

| Philadelphia, PA 19103 |

|

|

Name and address of agent for service: | Ms. Andrea Melia |

| Aberdeen Standard Investments Inc. |

| 1900 Market Street, Suite 200 |

| Philadelphia, PA 19103 |

|

|

Registrant’s telephone number, including area code: | 866-667-9231 |

|

|

Date of fiscal year end: | October 31 |

|

|

Date of reporting period: | April 30, 2020 |

Item 1. Reports to Shareholders.

![]()

Aberdeen Investment Funds

Semi-Annual Report

April 30, 2020

Aberdeen Select International Equity Fund

Class A – BJBIX ¢ Institutional Class – JIEIX

Aberdeen Global Equity Impact Fund

Class A – JETAX ¢ Institutional Class – JETIX

Aberdeen Total Return Bond Fund

Class A – BJBGX ¢ Institutional Class – JBGIX

Aberdeen Global High Income Fund

Class A – BJBHX ¢ Institutional Class – JHYIX

Beginning with reports for the period ending April 30, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from Aberdeen Investment Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund or your financial intermediary electronically following the instructions included with this disclosure or by contacting your financial intermediary or the Funds.

You may elect to receive all future reports in paper free of charge. You can inform the Funds or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by following the instructions included with this disclosure or by contacting the Funds at (866) 667-9231 or your financial intermediary. Your election to receive reports in paper will apply to all funds held with your financial intermediary or with the Trust.

![]()

Table of Contents

|

|

|

|

Market Review |

| Page 1 |

|

|

|

|

|

Aberdeen Select International Equity Fund |

| Page 3 |

|

|

|

|

|

Aberdeen Global Equity Impact Fund (formerly, Aberdeen Select International Equity Fund II) |

| Page 9 |

|

|

|

|

|

Aberdeen Total Return Bond Fund |

| Page 15 |

|

|

|

|

|

Aberdeen Global High Income Fund |

| Page 29 |

|

|

|

|

|

Financial Statements |

| Page 39 |

|

|

|

|

|

Notes to Financial Statements |

| Page 54 |

|

|

|

|

|

Shareholder Expense Examples |

| Page 74 |

|

Investors should carefully consider a fund’s investment objectives, risks, fees, charges and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Investment Funds is distributed by Aberdeen Fund Distributors LLC, Member FINRA, 1900 Market Street, Suite 200, Philadelphia, PA 19103.

Aberdeen Standard Investments Inc. (“ASII”) (formerly, Aberdeen Asset Management Inc.) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23, 1995.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for each fund of Aberdeen Investment Funds (each a “Fund” and collectively, the “Funds”) is included in the Funds’ semi-annual and annual reports to shareholders. Aberdeen Investment Funds also files complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds’ Form N-PORT filings are available on the Commission’s website at www.sec.gov and the Funds make the information on the exhibit to Form N-PORT available to shareholders upon request without change by calling 1-866-667-9231.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the Commission’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-866-667-9231; and (ii) on the Commission’s website at www.sec.gov.

Market Review

The six-month period ended April 30, 2020, was extremely challenging for global financial markets, as the onset of coronavirus (COVID-19) disrupted economic activities. Investors feared that the subsequent economic impact would result in a recession deeper than the global financial crisis (GFC) of 2008-2009. Global equity and fixed-income markets performed well in the first half of the reporting period as trade tensions between the U.S. and China eased and prospects of a partial deal between the world’s two largest economies improved. This changed in late February 2020, however, as the spread of the COVID-19 pandemic from China to other parts of the world rattled global markets. This was further compounded by a plunge in oil prices after Saudi Arabia and Russia failed to reach an agreement on production cuts amid a drop in demand. The monetary policy tightening by many central banks globally in the fourth quarter of 2019, gave way to policy easing as governments worldwide rolled out emergency fiscal stimulus, and central banks lowered interest rates.

By the end of the reporting period, some positive signs emerged as COVID-19 infection rates tapered globally. The phased-in reopening of the Chinese economy, along with the easing of social-distancing measures in some U.S. states and European countries, lifted investors’ risk appetite. Global equity prices moved higher in April 2020, while bond yields and currencies stabilized as liquidity issues abated. However, oil prices continued to decline. The drop in demand negated the largest coordinated output cut in history by the Organization of Petroleum Exporting Countries (OPEC) and its key partners. The price of West Texas Intermediate (WTI) Crude oil futures briefly turned negative on April 20, 2020, due to the lack of storage capacity.

Global equity prices finished the six-month reporting period in negative territory, with the Morgan Stanley Capital International (MSCI) World Index,1 a global equity market benchmark, returning –7.68%. U.S. large-cap company shares, as represented by the broader-market S&P 500 Index,2 were the strongest performers among developed markets for the period, returning –3.2%, while the Asia-Pacific region, as measured by the MSCI AC Asia-Pacific ex-Japan Index,3 returned –7.5% for the period. Japanese and European equities underperformed the overall global stock market, with the Tokyo Stock Price Index (TOPIX)4 and the MSCI Europe Index5 posting returns of –10.2% and –15.5%, respectively, for the reporting period.

In the U.S., the Federal Reserve (Fed) responded to the market carnage by implementing two separate emergency rate cuts totaling 50 and 100 basis points (bps), respectively, in March 2020, lowering the federal funds target rate to a range of 0% to 0.25%. In a statement issued following its monetary policy meeting on April 28-29, the Fed noted that it is “committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.” The pandemic significantly hampered the U.S. economy in the first quarter of 2020. U.S. gross domestic product (GDP) decreased at an annualized rate of 5.0% in the first three months of the year, down sharply from the 2.1% increase in the fourth quarter of 2019.6

The Asia-Pacific region held up relatively well amid the pandemic in the first four months of 2020. Investors’ fears of a global recession grew as widespread lockdowns to curb the spread of the virus crippled

economic activity worldwide. Volatile oil prices attributable to the pandemic-induced drop in demand and worries about excess output further dampened investor sentiment. Central banks and governments in the Asia-Pacific region cut their respective benchmark interest rates, and implemented fiscal stimulus. These actions, along with slowing infection rates and easing lockdown restrictions near the end of the reporting period, enabled the Asia Pacific market to recoup some losses in April.

Emerging-market equities, as represented by the MSCI Emerging Markets Index,7 underperformed their developed-market counterparts, returning –10.5% for the reporting period. The asset class was affected disproportionately by the slump in the oil price globally. In the first half of the reporting period, geopolitical tensions in the Middle East caused the Brent Crude oil price to rise. However, with energy demand already weakening amid the COVID-19 pandemic fallout, a pact between oil-producing nations to limit supply collapsed. This subsequent plunge in crude prices further battered investor sentiment for emerging-market stocks.

International real estate stocks, as measured by the Financial Times Stock Exchange European Public Real Estate Association/National Association of Real Estate Investment Trusts (FTSE EPRA/NAREIT) Global ex U.S. Index,8 returned –20.8% for the reporting period, significantly underperforming the –13.2% return of the broader international equity market, as represented by the MSCI AC World ex-USA Index.9 Emerging markets were the weakest performers amid currency pressures and concern about the willingness of populist governments in countries such as Mexico and Brazil to respond decisively to the pandemic. Relative ‘safe-haven’ countries, including Switzerland, Germany and Belgium, were the strongest performers for the reporting period. Those sectors that were disproportionately hampered by the COVID-19-induced lockdowns, such as retail and hospitality, notably lagged the overall international real estate equity market for the period, while shares of logistics, residential and communications infrastructure companies performed relatively well.

Fixed-income securities were not immune to the volatility in the global financial markets during the reporting period, and there was divergent performance across geographical regions. The U.S. market was the strongest performer globally, with the Bloomberg Barclays U.S. Aggregate Index10 returning 4.9% over the period. The U.S. market benefited from the “risk-off” environment in the second half of the reporting period, as investors sought what they perceived to be ‘safe-haven’ assets. This factor, combined with the Fed’s aggressive monetary policy easing, led to a steep decline in yields across the U.S. Treasury curve. Yields on two- three-, five- and ten-year Treasury notes fell 132, 128, 115 and 105 bps to 0.20%, 0.24%, 0.36% and 0.64%, respectively, over the six-month reporting period, with the ten- to two-year spread widening by 27 bps to +44 bps. Conversely, emerging-market debt, as measured by the J.P. Morgan EMBI Global Diversified Index,11 returned –10.1% over the reporting period, and was the primary market laggard. As market volatility increased and oil prices plummeted, investors’ fears rose regarding the ability of certain economies within the emerging-market asset class to service debt obligations, most notably Argentina and Lebanon.

Market Review (concluded)

Outlook

The downturn in the global financial markets in the first quarter of 2020 was historic. Within the span of a few weeks, the dramatic spread of the COVID-19 pandemic across developed markets resulted in increasing containment measures, leading to a significant repricing of all asset classes. Certain macroeconomic indicators recently have implied that economic activity has returned, especially in China and parts of Asia that were the first to be hit by the virus. However, we refrain from concluding that things are “back to normal.”

In our view, the pandemic and associated shutdowns of economic activity have created an enormous negative growth shock that may cause deep recessions worldwide. However, with new infections declining in many regions, the attention of governments globally is turning to exit strategies and the nature of the economic recovery. We believe that the exits from lockdowns will be gradual, but even a tentative reopening of some economies should spur a strong rebound in growth.

COVID-19

The respiratory illness COVID-19 caused by a novel coronavirus has resulted in a global pandemic and major disruption to economies and markets around the world, including the United States. Financial markets have experienced extreme volatility and severe losses, and trading in many instruments has been disrupted. Liquidity for many instruments has been greatly reduced for periods of time. Some interest rates are very low and in some cases yields are negative. Some sectors of the economy and individual issuers have experienced particularly large losses. These circumstances may continue for an extended period of time, and may continue to affect adversely the value and liquidity of the fund’s investments. The ultimate economic fallout from the pandemic, and the long-term impact on economies, markets, industries and individual issuers, including the Funds, are not

known. Governments and central banks, including the Federal Reserve in the U.S., have taken extraordinary and unprecedented actions to support local and global economies and the financial markets. The impact of these measures, and whether they will be effective to mitigate the economic and market disruption, will not be known for some time.

Aberdeen Standard Investments

___________________________________

1 | The MSCI World Index tracks the performance of large- and mid-cap stocks across 23 developed-market countries. |

2 | The S&P 500 Index is an unmanaged index considered representative of the U.S. stock market. |

3 | The MSCI AC Asia Pacific ex Japan Index tracks the performance of large and mid-cap stocks across two of three developed-market countries (excluding Japan) and nine emerging markets countries in Asia. |

4 | The Tokyo Stock Price Index (TOPIX) is a market capitalization-weighted index of large- and mid-sized companies listed on the Tokyo Stock Exchange. |

5 | The MSCI Europe Index tracks the performance of large- and mid-cap stocks across 15 developed-market countries in Europe. |

6 | Source: U.S. Department of Commerce, May 2020 |

7 | The MSCI Emerging Markets Index tracks the performance of large and mid-cap stocks across 24 emerging-market countries. |

8 | The FTSE EPRA/NAREIT Global ex U.S. Index is an unmanaged index considered representative of real estate companies and real estate investment trusts (REITs) outside the U.S. |

9 | The MSCI AC World ex-USA Index tracks the performance of large- and mid-cap stocks across 22 developed-market countries outside of the U.S., as well as 26 emerging-market countries. |

10 | The Bloomberg Barclays U.S. Aggregate Index is a broad-based flagship benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. |

11 | The J .P. Morgan EMBI Global Diversified Index is a comprehensive global local emerging markets index comprising liquid, fixed-rate, domestic currency government bonds. |

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Aberdeen Select International Equity Fund (Unaudited)

The Aberdeen Select International Equity Fund (Institutional Class shares net of fees) returned –15.13% for the six-month period ending April 30, 20120 versus –13.22% for its benchmark, the MSCI All Country (AC) World ex USA Index (Net Dividends), during the same period.

International equities declined over the six-month period ended April 30, 2020. Stock prices advanced in the first half of the period as tensions between U.S. and China eased and prospects of a partial deal between the world’s two largest economies improved. At the beginning of 2020, the U.S. broader-market S&P 500 Index1 touched a record high in the wake of the U.S.-China trade truce and generally positive economic data. In late February, however, the spread of COVID-19 pandemic from China rattled global stock markets. In response, the U.S. government unveiled a US$2 trillion stimulus program and the U.S. Federal Reserve implemented emergency interest-rate cuts, which provided some respite for investors. Many other global central banks followed suit. On the corporate front, many companies withdrew earlier forecasts as countries closed their borders and imposed lockdowns. An oil-price plunge further battered investor sentiment after a Saudi Arabia-Russian pact to limit supply collapsed amid slowing demand due to the pandemic. Global equity markets rebounded towards the end of the period in April, aided by unprecedented monetary and fiscal stimulus globally, and a slowdown in the rate of new COVID-19 infections in many countries.

The Fund underperformed its benchmark, the MSCI AC World ex USA Index (Net Dividends), for the reporting period.

At the stock level, holdings in UK-based cinema operator Cineworld Group PLC and European aircraft manufacturer Airbus SE detracted from Fund performance as a result of the pandemic. Cineworld was forced to close its cinemas amid lockdowns in the UK and U.S., where the company does business. Uncertainty surrounding the duration of lockdowns and how social distancing measures will be applied to cinemas in the future fueled investors’ concerns around Cineworld’s liquidity. Airbus, a position that we initiated during the period, was hampered by travel restrictions and border closures. We continue to look beyond the short-term challenges to the company’s long-term goal of becoming more efficient. In Australia, the Fund’s holding in Treasury Wine Estates (TWE) also had a negative impact on performance as the wine-maker experienced key management departures and competition in North America. Bush fires in Australia also posed a risk to the company’s vineyards and harvests. Though these near-term uncertainties weighed on the stock price, we maintain our belief in TWE’s future growth, especially as it gains premium market share in China.

Conversely, the Fund’s position in Denmark-based drug-maker Novo Nordisk A/S was a key contributor to performance for the reporting period as investors perceived its business model and earnings to be relatively insulated against disruptions from the COVID-19 pandemic.

Novo Nordisk’s sales appeared to be more resilient than those of many of its peers, given the company’s relatively higher reliance on home-administered drugs. The firm controls almost one-third of the global market in diabetes treatment products, and half of the insulin market. Over the long term, we believe that an increasingly overweight and aging population in developed markets should continue to drive demand for these products. The Fund’s holding in Genus PLC enhanced Fund performance as the UK-based animal genetics company benefited from signs of rising global pork and dairy prices, which would increase demand for its products that assist in breeding higher-quality livestock. Finally, shares of the Fund’s position in Japanese drugstore chain operator Welcia advanced as the company continued to post solid same-store sales over the reporting period.

During the reporting period, we sought to take advantage of share-price volatility to add new stocks to the Fund. We established a new positon in Anglo-Swedish drug-maker AstraZeneca PLC, as we believe that its upcoming product launches and pipeline news could help boost profits. We also initiated a holding Airbus (as previously noted), which we believe has a stronger product portfolio than its U.S.-based competitor, Boeing Co. We are aware that COVID-19 has negative implications for air traffic, but we believe that future gains in market share could allow Airbus to become efficient and, therefore, more profitable and likely to generate more cash. In addition, we purchased shares of Alstom S.A. We believe that the French rail transportation firm should see sustained order momentum as its products benefit from decarbonization trends and increased government spending to support the economy. We added to the Fund’s existing position in German utility RWE AG. The company generates wind, solar and biomass-derived power and, in our view, should deliver better growth and returns as capital is allocated towards clean energy and away from fossil fuels. We believe that the shares will perform better when RWE demonstrates that it can build and monetize assets, recycling the funds into future ventures.

In contrast, we exited the Fund’s positions in several companies over the reporting period. Japanese drug-maker Shionogi & Co. Ltd.’s share price continued to discount future potential from specific products that may take longer to materialize. Furthermore, the company’s management recently revised downwards its forecasts for other areas of its portfolio. Canada-based diversified entertainment company Entertainment One Ltd. reached an agreement to be purchased by U.S.-based toymaker Hasbro Inc. (which the Fund does not hold). We also sold the Fund’s shares in Japanese baby care and mother care products maker Pigeon Corp. as we believe that investors’ expectations for its growth were higher than it would be capable of delivering. Finally, we exited the Fund’s holding in Norway-based telecommunications company Telenor ASA due to regulatory changes in its domestic market and increasing competition that we had not anticipated.

1 The S&P 500 Index is an unmanaged index considered representative of the broader U.S. stock market. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

| 2020 Semi-Annual Report |

Aberdeen Select International Equity Fund (Unaudited) (concluded)

Effective February 28, 2020, the Fund’s Board of Trustees approved a change in the Fund’s primary benchmark from the MSCI AC World ex USA Index (Gross Dividends) to the MSCI AC World ex USA Index (Net Dividends). The change from a gross to a net dividend benchmark is in line with industry practice and is more appropriate for the Fund, as it is also calculated net of withholding taxes, to which the Fund is generally subject. The change in benchmark does not affect the investment objective of the Fund, nor the way in which the portfolio is managed.

In light of the recent bouts of volatility driven by pandemic fears, we have reassessed the Fund’s underlying holdings to consider the potential impact of the COVID-19 pandemic. We are talking to management teams and updating our strategy as the situation unfolds. Most of the companies have experienced, or are expecting, an adverse impact on earnings and cash flows. Nevertheless, we take a long-term view. We believe that, in most cases, these are high-quality companies whose economic moats2 and structural drivers remain intact. In our view, they are also broadly supported by reasonable margins and solid balance sheets, with capable management teams at the helm. Furthermore, we believe that global equity valuations are generally at compelling levels, presenting opportunities to add to our preferred Fund holdings or initiate new positions. We believe that our diversification3 strategy has kept the Fund’s performance resilient thus far. Fund holdings whose businesses performed relatively well during the reporting period counterbalanced others in sectors in which the pandemic has had a more negative impact.

Certain macro indicators recently have implied that economic activity has returned, especially in China and parts of Asia that were the first to be hit by the virus. However, we refrain from concluding that things are back to normal. Some businesses will be disrupted for a long period, while others stand to benefit post-COVID-19. In such fluid times, we believe that good bottom-up analysis and stock selection are even more crucial. In our view, we have the advantage of an effective proprietary research platform, and a well-resourced and experienced Fund management team that has navigated many past crises. We remain disciplined in putting capital to work to ensure the Fund’s largest weights are in those high-quality companies that in our view have the highest potential returns. We believe that this will continue to benefit the Fund’s performance.

Portfolio Management:

Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A Shares pay a Rule 12b-1 fee of up to 0.25% of net assets. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeenstandard.com/en-us/us/investor/fund-centre.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Stocks issued by large cap companies subject the Fund to the risk that those stocks may underperform stocks issued by companies with smaller capitalizations or the market as a whole.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

2 A moat is a competitive advantage that one company has over other companies in the same industry.

3 Diversification does not ensure a profit or protect against a loss in a declining market

2020 Semi-Annual Report |

|

Aberdeen Select International Equity Fund (Unaudited)

Average Annual Total Return | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. |

Class A | (15.21%) | (13.90%) | (1.10%) | 0.10% |

Institutional Class | (15.13%) | (13.70%) | (0.85%) | 0.35% |

* Performance shown for periods after December 16, 2016 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2008) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”). The receipt of these extraordinary payments increased the Fund’s performance for all periods that include December 2016, February 2017, July 2017, October 2017, February 2019 March 2019 and September 2019 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. For Class A, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (18.11%), (18.78%), (3.93%) and (1.34%), respectively, for the six-month, 1-year, 5-year, and 10-year periods ended April 30, 2020. For Institutional Class, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (18.00%), (18.59%), (3.73%) and (1.12%), respectively, for the six-month, 1-year, 5-year, and 10-year periods ended April 30, 2020.There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see Note 2(g) and the Fund’s prospectus dated February 28, 2020 for further information.

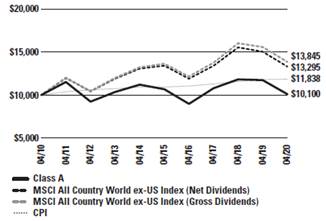

Performance of a $10,000 Investment (as of April 30, 2020)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund, Morgan Stanley Capital International (MSCI) All Country World ex-USA Index (ACWI ex-USA) (net dividends) MSCI ACWI ex-USA (gross dividends)

and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2020. Effective February 28, 2020, the MSCI All Country World ex-USA Index (net dividends) replaced the MSCI All Country World ex-USA Index (gross dividends) as the Fund’s primary benchmark. The Adviser believes that the change from a gross to a net dividend benchmark is in line with industry practice and is more appropriate for the Fund, as it is calculated net of withholding taxes to which the Fund is generally subject. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-USA Index (net dividends) and the MSCI ACWI ex-USA (gross dividends) capture large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States (U.S.) and 24 Emerging Markets (EM) countries). With 2,163 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

| 2020 Semi-Annual Report |

Aberdeen Select International Equity Fund (Unaudited)

Portfolio Summary (as a percentage of net assets)

April 30, 2020 (Unaudited)

Asset Allocation |

|

|

Common Stocks |

| 107.6% |

Preferred Stocks |

| 0.8% |

Short-Term Investment |

| 0.3% |

Liabilities in Excess of Other Assets |

| (8.7%) |

|

| 100.0% |

The following table summarizes the composition of the Fund’s portfolio, in S&P Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 69 industries and 158 sub-industries. As of April 30, 2020, the Fund did not have more than 25% of its assets invested in any single industry or industry group. The sectors as classified by GICS, are comprised of several industries.

Top Sectors |

|

Industrials | 20.3% |

Consumer Staples | 16.2% |

Consumer Discretionary | 14.8% |

Health Care | 13.6% |

Financials | 13.1% |

Communication Services | 7.7% |

Utilities | 7.6% |

Materials | 4.1% |

Energy | 4.0% |

Real Estate | 3.8% |

Other | (5.2%) |

| 100.0% |

Top Holdings* |

|

Alibaba Group Holding Ltd., ADR | 4.4% |

Novo Nordisk AS, Class B | 4.2% |

Nestle SA | 4.1% |

Koninklijke DSM NV | 4.1% |

Vonovia SE | 3.8% |

Enel SpA | 3.8% |

RWE AG | 3.8% |

Genus PLC | 3.6% |

BAE Systems PLC | 3.3% |

AIA Group Ltd. | 3.1% |

Other | 61.8% |

| 100.0% |

* For the purpose of listing top holdings, Short-Term Investments are included as part of Other.

Top Countries |

|

United Kingdom | 14.7% |

France | 14.7% |

China | 13.9% |

Japan | 8.0% |

Germany | 7.6% |

Switzerland | 6.9% |

Netherlands | 6.1% |

Italy | 6.0% |

Canada | 4.6% |

Denmark | 4.2% |

Other | 13.3% |

| 100.0% |

Statement of Investments

April 30, 2020 (Unaudited)

Aberdeen Select International Equity Fund

|

|

|

|

|

| |

|

| Shares |

| Value |

| |

COMMON STOCKS (107.6%) |

|

|

|

|

| |

AUSTRALIA (3.1%) |

|

|

|

|

| |

Consumer Staples (2.2%) |

|

|

|

|

| |

Treasury Wine Estates Ltd. |

| 357,852 |

| $ | 2,353,721 |

|

Health Care (0.9%) |

|

|

|

|

| |

Cochlear Ltd. |

| 8,699 |

| 1,034,289 |

| |

|

|

|

| 3,388,010 |

| |

CANADA (4.6%) |

|

|

|

|

| |

Consumer Discretionary (2.1%) |

|

|

|

|

| |

Restaurant Brands International, Inc. |

| 46,340 |

| 2,260,488 |

| |

Consumer Staples (2.5%) |

|

|

|

|

| |

Alimentation Couche-Tard, Inc., Class B |

| 96,800 |

| 2,701,040 |

| |

|

|

|

| 4,961,528 |

| |

CHINA (13.9%) |

|

|

|

|

| |

Communication Services (2.8%) |

|

|

|

|

| |

Tencent Holdings Ltd. |

| 58,200 |

| 3,059,541 |

| |

Consumer Discretionary (8.4%) |

|

|

|

|

| |

Alibaba Group Holding Ltd., ADR (a) |

| 23,784 |

| 4,820,303 |

| |

Li Ning Co. Ltd. |

| 446,000 |

| 1,408,233 |

| |

Shenzhou International Group Holdings Ltd. |

| 251,600 |

| 2,903,875 |

| |

|

|

|

| 9,132,411 |

| |

Financials (2.7%) |

|

|

|

|

| |

Ping An Insurance Group Co. of China Ltd., H Shares |

| 295,000 |

| 3,001,996 |

| |

|

|

|

| 15,193,948 |

| |

DENMARK (4.2%) |

|

|

|

|

| |

Health Care (4.2%) |

|

|

|

|

| |

Novo Nordisk AS, Class B |

| 71,972 |

| 4,591,096 |

| |

FRANCE (14.7%) |

|

|

|

|

| |

Communication Services (4.2%) |

|

|

|

|

| |

Ubisoft Entertainment SA (a) |

| 32,055 |

| 2,384,309 |

| |

Vivendi SA |

| 100,534 |

| 2,172,856 |

| |

|

|

|

| 4,557,165 |

| |

Energy (2.4%) |

|

|

|

|

| |

TOTAL SA |

| 74,002 |

| 2,626,506 |

| |

Financials (1.7%) |

|

|

|

|

| |

AXA SA |

| 106,065 |

| 1,885,464 |

| |

Industrials (6.4%) |

|

|

|

|

| |

Airbus SE (a) |

| 24,500 |

| 1,551,303 |

| |

Alstom SA |

| 55,500 |

| 2,276,553 |

| |

Vinci SA |

| 38,400 |

| 3,145,802 |

| |

|

|

|

| 6,973,658 |

| |

|

|

|

| 16,042,793 |

| |

GERMANY (7.6%) |

|

|

|

|

| |

Real Estate (3.8%) |

|

|

|

|

| |

Vonovia SE |

| 84,400 |

| 4,173,482 |

| |

|

|

|

|

|

| |

|

| Shares |

| Value |

| |

Utilities (3.8%) |

|

|

|

|

| |

RWE AG |

| 144,300 |

| $ | 4,151,177 |

|

|

|

|

| 8,324,659 |

| |

HONG KONG (3.1%) |

|

|

|

|

| |

Financials (3.1%) |

|

|

|

|

| |

AIA Group Ltd. |

| 362,200 |

| 3,324,187 |

| |

ISRAEL (3.0%) |

|

|

|

|

| |

Information Technology (3.0%) |

|

|

|

|

| |

NICE Ltd. (a) |

| 19,837 |

| 3,257,819 |

| |

ITALY (6.0%) |

|

|

|

|

| |

Industrials (2.2%) |

|

|

|

|

| |

Prysmian SpA |

| 127,337 |

| 2,402,593 |

| |

Utilities (3.8%) |

|

|

|

|

| |

Enel SpA |

| 608,500 |

| 4,156,325 |

| |

|

|

|

| 6,558,918 |

| |

JAPAN (8.0%) |

|

|

|

|

| |

Consumer Discretionary (2.7%) |

|

|

|

|

| |

Sony Corp. |

| 45,500 |

| 2,928,110 |

| |

Consumer Staples (2.1%) |

|

|

|

|

| |

Welcia Holdings Co. Ltd. |

| 30,500 |

| 2,214,250 |

| |

Health Care (2.0%) |

|

|

|

|

| |

Asahi Intecc Co. Ltd. |

| 82,800 |

| 2,193,475 |

| |

Industrials (1.2%) |

|

|

|

|

| |

Nihon M&A Center, Inc. |

| 41,000 |

| 1,337,518 |

| |

|

|

|

| 8,673,353 |

| |

LATVIA (0.0%) |

|

|

|

|

| |

Financials (0.0%) |

|

|

|

|

| |

AS Parex Banka (a)(b)(c)(d) |

| 1,424,182 |

| – |

| |

MACAU (1.6%) |

|

|

|

|

| |

Consumer Discretionary (1.6%) |

|

|

|

|

| |

Sands China Ltd. |

| 434,000 |

| 1,757,047 |

| |

NETHERLANDS (6.1%) |

|

|

|

|

| |

Financials (2.0%) |

|

|

|

|

| |

ASR Nederland NV |

| 81,176 |

| 2,183,887 |

| |

Materials (4.1%) |

|

|

|

|

| |

Koninklijke DSM NV |

| 36,596 |

| 4,485,273 |

| |

|

|

|

| 6,669,160 |

| |

NORWAY (3.0%) |

|

|

|

|

| |

Consumer Staples (3.0%) |

|

|

|

|

| |

Mowi ASA |

| 188,845 |

| 3,234,349 |

| |

POLAND (2.5%) |

|

|

|

|

| |

Consumer Staples (2.5%) |

|

|

|

|

| |

Dino Polska SA (a)(e) |

| 63,337 |

| 2,678,508 |

| |

Statement of Investments (concluded)

April 30, 2020 (Unaudited)

Aberdeen Select International Equity Fund

|

|

|

|

|

| |

|

| Shares |

| Value |

| |

COMMON STOCKS (continued) |

|

|

|

|

| |

REPUBLIC OF IRELAND (1.3%) |

|

|

|

|

| |

Industrials (1.3%) |

|

|

|

|

| |

Ryanair Holdings PLC, ADR (a) |

| 21,500 |

| $ | 1,364,605 |

|

SWEDEN (3.3%) |

|

|

|

|

| |

Industrials (3.3%) |

|

|

|

|

| |

Assa Abloy AB, Class B |

| 105,047 |

| 1,880,544 |

| |

Sandvik AB (a) |

| 114,300 |

| 1,758,324 |

| |

|

|

|

| 3,638,868 |

| |

SWITZERLAND (6.9%) |

|

|

|

|

| |

Consumer Staples (4.1%) |

|

|

|

|

| |

Nestle SA |

| 42,710 |

| 4,523,417 |

| |

Financials (2.8%) |

|

|

|

|

| |

Zurich Insurance Group AG |

| 9,571 |

| 3,034,527 |

| |

|

|

|

| 7,557,944 |

| |

UNITED KINGDOM (14.7%) |

|

|

|

|

| |

Communication Services (0.7%) |

|

|

|

|

| |

Cineworld Group PLC |

| 979,287 |

| 807,362 |

| |

Energy (1.6%) |

|

|

|

|

| |

BP PLC |

| 448,300 |

| 1,766,487 |

| |

Health Care (6.5%) |

|

|

|

|

| |

AstraZeneca PLC |

| 30,600 |

| 3,200,515 |

| |

Genus PLC |

| 91,005 |

| 3,909,781 |

| |

|

|

|

| 7,110,296 |

| |

Industrials (5.9%) |

|

|

|

|

| |

BAE Systems PLC |

| 555,461 |

| 3,542,970 |

| |

RELX PLC |

| 124,676 |

| 2,837,147 |

| |

|

|

|

| 6,380,117 |

| |

|

|

|

| 16,064,262 |

| |

Total Common Stocks |

|

|

| 117,281,054 |

| |

|

|

|

|

|

| |

|

| Shares |

| Value |

| |

PREFERRED STOCKS (0.8%) |

|

|

|

|

| |

BRAZIL (0.8%) |

|

|

|

|

| |

Financials (0.8%) |

|

|

|

|

| |

Banco Bradesco SA, Preferred Shares |

| 264,000 |

| $ | 929,697 |

|

Total Preferred Stocks |

|

|

| 929,697 |

| |

SHORT-TERM INVESTMENT (0.3%) |

|

|

|

|

| |

UNITED STATES (0.3%) |

|

|

|

|

| |

State Street Institutional U.S. Government Money Market Fund, Premier Class, 0.22% (f) |

| 300,297 |

| 300,297 |

| |

Total Investments |

|

|

| 118,511,048 |

| |

Liabilities in Excess of Other Assets—(8.7)% |

|

|

| (9,482,365 | ) | |

Net Assets—100.0% |

|

|

| $ | 109,028,683 |

|

(a) Non-income producing security.

(b) The Fund’s adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. Illiquid securities held by the Fund represent 0.00% of net assets as of April 30, 2020.

(c) Level 3 security. See Note 2(a) of the accompanying Notes to Financial Statements.

(d) Illiquid security.

(e) Denotes a security issued under Regulation S or Rule 144A.

(f) Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of April 30, 2020.

(g) See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities.

ADR American Depositary Receipt

PLC Public Limited Company

Aberdeen Global Equity Impact Fund (Unaudited)

The Aberdeen Global Equity Impact Fund (Institutional Class shares net of fees) returned –3.12% for the six-month period ending April 30, 2019, versus –7.68% for its benchmark, the MSCI All Country (AC) World Index (Net Dividends), during the same period.

Global equities declined over the six-month period ended April 30, 2020. Stock prices advanced in the first half of the period as tensions between U.S. and China eased and prospects of a partial deal between the world’s two largest economies improved. At the beginning of 2020, the U.S. broader-market S&P 500 Index1 touched a record high in the wake of the U.S.-China trade truce and generally positive economic data. In late February, however, the spread of the coronavirus (COVID-19) pandemic from China rattled global stock markets. In response, the U.S. government unveiled a US$2 trillion stimulus program and the U.S. Federal Reserve implemented emergency interest-rate cuts, which provided some respite for investors. Many other global central banks followed suit. On the corporate front, many companies withdrew earlier forecasts as countries closed their borders and imposed lockdowns. An oil-price plunge further battered investor sentiment after a Saudi Arabia-Russian pact to limit supply collapsed amid slowing demand due to the pandemic. Global equity markets rebounded towards the end of the period in April, aided by unprecedented monetary and fiscal stimulus globally, and a slowdown in the rate of new COVID-19 infections in many countries.

The Fund’s relative outperformance versus its benchmark, the MSCI AC World Index (Net Dividends), for the reporting period was due mainly to positive stock selection in the U.S. and UK, as well as an overweight allocation to Denmark.

At the stock level, U.S. real estate investment trust (REIT) Equinix Inc. was a key contributor to Fund performance as the company provides data warehouses that benefited from the COVID-19 outbreak and increased demand for cloud computing. Equinix delivered positive results for the first quarter of its 2020 fiscal year, and issued a forecast indicating that the higher pandemic-driven demand will likely be sustained even after the crisis subsides. Equinix remains committed to powering its data centers with renewable energy, which we believe will gain in importance as global demand for data centers increases. U.S. managed care firm UnitedHealth Group Inc. was buoyed by expectations that there would be no significant change to the U.S.’s current healthcare policy. Shares of the Fund’s holding in South Korean battery maker Samsung SDI Co, Ltd. rose in tandem with forecasts of high sales growth for electric vehicles.

Conversely, the Fund’s position in Banco Bradesco detracted from performance during the reporting period as the Brazilian lender’s stock price moved lower due to slowing economic growth and investors’ fears of asset-quality deterioration. The company’s management has made provisions for bad debt arising from the pandemic. While investors appeared to view this negatively, we believe that the loan-loss provisions will leave Banco Bradesco in a better position to

emerge from the crisis, and allows the bank to focus on deepening the penetration of basic financial services to underserved customers. Similarly, shares of Bank Rakyat Indonesia Tbk PT were hampered by investors’ concerns over an economic slowdown that is likely to hit its customers, which comprise mainly small companies and consumers. We believe that the stock’s valuation is now attractive when balanced against a longer-term perspective, and that the bank might benefit from pandemic-related economic stimulus. The lack of exposure to internet retailing giant Amazon.com Inc., and technology giants Microsoft Corp. and Apple Inc., also weighed modestly on performance for the reporting period. The Fund does not hold these stocks because their business models do not meet our criteria.

During the reporting period, we sought to take advantage of market volatility to initiate holdings in six companies. In our view, French rail transportation firm Alstom S.A.’s organic growth should accelerate as its green mobility solutions benefit from decarbonization trends. We established a new position in Goodman Group Ltd., as we believe that the Australian property firm will see strong underlying growth in net asset value and cash flow, given its growing fund management business. In our opinion, the firm demonstrates good environmental commitments, and 75% of its portfolio is certified “green,” with new developments built to be fully sustainable. Israeli garment printing solutions provider Kornit Digital Ltd. serves the textile industry. The company’s stock price came under short term pressure due to coronavirus-related concerns about consumer demand. The printing technology by the U.S. exchange–listed firm reduces water and chemical use, and is being rapidly adopted by large textile manufacturers. Kornit Digital’s services have the potential to significantly improve water use and efficiency in an industry with a poor track record, aligning with our water and sanitation investment pillar. We initiated a holding in AstraZeneca PLC as we believe that investors have not fully appreciated the Anglo-Swedish drug-maker’s multiple product launches and positive product pipeline news. The company’s focus on key priority health conditions that are highlighted by the World Health Organization and United Nations, as well as robust pricing policy and access-to-medicine initiatives, fit well within our health and Social Care investment pillars. Tetra Tech Inc. is the leading water services firm in the U.S. and offers resource management services to a broad range of industries, directly benefiting water-stressed regions, including Florida, Texas and California. The focus on water efficiency and reduction of wastage aligns with our water and sanitation investment pillar. Tetra Tech has been successful in moving towards higher-end services and focusing on higher-growth opportunities. Finally, we established a new position in Ireland-based building materials supplier Kingspan Group PLC, as we believe that demand for better thermal efficiency in the construction sector will support an attractive growth outlook. This is well aligned with our sustainable real estate and infrastructure investment pillar.

1 The S&P 500 Index is an unmanaged index considered representative of the broader U.S. stock market. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

2020 Semi-Annual Report 9

Aberdeen Global Equity Impact Fund (Unaudited) (concluded)

Effective February 28, 2020, the Fund’s Board of Trustees approved a change in the Fund’s primary benchmark from the MSCI AC World Index (Gross Dividends) to the MSCI AC World Index (Net Dividends). The change from a gross to a net dividend benchmark is in line with industry practice and is more appropriate for the Fund, as it is also calculated net of withholding taxes, to which the Fund is generally subject. The change in benchmark does not affect the investment objective of the Fund, nor the way in which the portfolio is managed.

The Fund seeks to deliver positive returns and to invest in companies whose products and services have a positive environmental or social impact, factors that have become even more important in light of the COVID-19 pandemic. We use the United Nation’s Sustainable Development Goals as guiding principles. Specifically, we identify companies which in our view provide products and services that deliver measurable output in making a positive impact, as well as those which we believe have a clear intention to solve a global issue and are spending money to make an impact in the future. In light of the recent bouts of volatility driven by pandemic fears, we have reassessed the Fund’s underlying holdings to consider COVID-19’s potential impact. We are talking to management teams and updating our strategy as the situation unfolds. Most companies have experienced, or are expecting, an adverse impact on earnings and cash flows. Nevertheless, we take a long-term view. In most cases, these are high-quality companies whose economic moats2 and structural drivers remain intact. In our opinion, they are also broadly supported by reasonable margins and solid balance sheets, with capable management at the helm.

Certain macro indicators recently have implied that economic activity has returned, especially in China and parts of Asia that were the first to be hit by the virus. However, we refrain from concluding that things are back to normal. Some businesses will be disrupted for a long period, while others stand to benefit post-COVID-19. In such fluid times, we believe that good bottom-up analysis and stock selection are even more crucial. In our view, we have the advantage of an effective proprietary research platform, and a well-resourced and experienced Fund management team that has navigated many past crises. We remain disciplined in putting capital to work to ensure the Fund’s largest weights are in those high-quality companies that we believe have the highest potential returns. We believe that this will continue to benefit the Fund’s performance.

Portfolio Management:

Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A Shares pay a Rule 12b-1 fee of up to 0.25% of net assets. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeenstandard.com/en-us/us/investor/fund-centre.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small- and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

In implementing the Fund’s ESG (Environmental, Social and Governance) impact investment strategy, the Adviser may select or exclude securities of issuers in certain industries, sectors, regions or countries for reasons other than the issuer’s investment performance. For this reason, the Fund may underperform other funds that do not implement an ESG impact strategy.

The definition of “impact investing” will vary according to an investor’s beliefs and values. There is no guarantee that the Adviser’s definition of impact investing, security selection criteria or investment judgment will reflect the beliefs or values of any particular investor.

Please read the prospectus for more detailed information regarding these and other risks.

2 A moat is a competitive advantage that one company has over other companies in the same industry.

10 2020 Semi-Annual Report

Aberdeen Global Equity Impact Fund (Unaudited)

Average Annual Total Return | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. |

|

Class A | (3.22%) | 1.15% | 1.12% | 1.62% |

|

Institutional Class | (3.12%) | 1.42% | 1.38% | 1.87% |

|

* Performance shown for periods after February 1, 2017 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2009) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”). The receipt of these extraordinary payments increased the Fund’s performance for all periods that include February 2017, October 2017, August 2018, February 2019 and September 2019 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. For Class A, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (4.09%), (0.91%), (0.25%), and 0.92%, respectively, for the six-month, 1-year, 5-year, and 10-year periods ended April 30, 2020. For Institutional Class, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (3.89%), (0.52%), 0.03%, and 1.19%, respectively, for the six-month, 1-year, 5-year, and 10-year periods ended April 30, 2020.There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see the Fund’s prospectus dated February, 28, 2020 for further information.

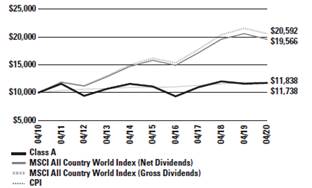

Performance of a $10,000 Investment (as of April 30, 2020)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Global Equity Impact Fund, Morgan Stanley Capital International (MSCI) All Country World Index (ACWI) (net dividends) MSCI ACWI (gross dividends) and the Consumer Price Index (CPI) over

a 10-year period ended April 30, 2020. Effective February 28, 2020, the MSCI All Country World Index (ACWI) (net dividends) replaced the MSCI All Country World Index (ACWI) (gross dividends) as the Fund’s primary benchmark. The Adviser believes that the change from a gross to a net dividend benchmark is in line with industry practice and is more appropriate for the Fund, as it is calculated net of withholding taxes to which the Fund is generally subject. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI is an unmanaged index considered representative of developed and emerging market stock markets.

MSCI ACWI captures large and mid-cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. With 2,774 constituents, the index covers approximately 85% of the global investable equity opportunity set.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

2020 Semi-Annual Report 11

Aberdeen Global Equity Impact Fund (Unaudited)

Portfolio Summary (as a percentage of net assets)

April 30, 2020 (Unaudited)

Asset Allocation |

|

|

Common Stocks | 103.9% |

|

Money Market Funds | 0.3% |

|

Liabilities in Excess of Other Assets | (4.2%) |

|

| 100.0% |

|

The following table summarizes the composition of the Fund’s portfolio, in S&P Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 69 industries and 158 sub-industries. As of April 30, 2020, the Fund did not have more than 25% of its assets invested in any single industry or industry group. The sectors as classified by GICS, are comprised of several industries.

Top Sectors |

|

|

|

Health Care |

| 23.2% |

|

Industrials |

| 22.2% |

|

Information Technology |

| 16.0% |

|

Real Estate |

| 11.0% |

|

Financials |

| 9.0% |

|

Materials |

| 7.5% |

|

Communication Services |

| 6.3% |

|

Utilities |

| 5.3% |

|

Consumer Discretionary |

| 3.4% |

|

Other |

| (3.9%) |

|

|

| 100.0% |

|

Top Holdings |

|

|

|

UnitedHealth Group, Inc. |

| 4.1% |

|

Prologis, Inc., REIT |

| 3.9% |

|

Safaricom PLC |

| 3.7% |

|

Equinix, Inc., REIT |

| 3.6% |

|

Umicore SA |

| 3.6% |

|

John Laing Group PLC |

| 3.2% |

|

Mastercard, Inc., Class A |

| 3.2% |

|

NextEra Energy, Inc. |

| 3.0% |

|

Wuxi Biologics Cayman, Inc. |

| 3.0% |

|

salesforce.com, Inc. |

| 2.9% |

|

Other |

| 65.8% |

|

|

| 100.0% |

|

Top Countries |

|

|

|

United States |

| 36.4% |

|

United Kingdom |

| 14.2% |

|

France |

| 8.2% |

|

Denmark |

| 6.8% |

|

China |

| 5.5% |

|

Netherlands |

| 4.2% |

|

Australia |

| 3.8% |

|

Kenya |

| 3.7% |

|

Belgium |

| 3.5% |

|

Hong Kong |

| 2.7% |

|

Other |

| 11.0% |

|

|

| 100.0% |

|

12 2020 Semi-Annual Report

Statement of Investments

April 30, 2020 (Unaudited)

Aberdeen Global Equity Impact Fund

|

| Shares |

| Value |

| |

COMMON STOCKS (103.9%) |

|

|

|

|

| |

AUSTRALIA (3.8%) |

|

|

|

|

| |

Industrials (2.1%) |

|

|

|

|

| |

Cleanaway Waste Management Ltd. |

| 925,500 |

| $ | 1,116,637 |

|

Real Estate (1.7%) |

|

|

|

|

| |

Goodman Group, REIT |

| 108,200 |

| 921,565 |

| |

|

|

|

| 2,038,202 |

| |

BELGIUM (3.5%) |

|

|

|

|

| |

Materials (3.5%) |

|

|

|

|

| |

Umicore SA |

| 44,100 |

| 1,911,316 |

| |

BRAZIL (1.8%) |

|

|

|

|

| |

Consumer Discretionary (0.8%) |

|

|

|

|

| |

YDUQS Part |

| 78,200 |

| 436,450 |

| |

Financials (1.0%) |

|

|

|

|

| |

Banco Bradesco SA |

| 162,008 |

| 523,154 |

| |

|

|

|

| 959,604 |

| |

CHINA (5.5%) |

|

|

|

|

| |

Financials (2.5%) |

|

|

|

|

| |

Ping An Insurance Group Co. of China Ltd., H Shares |

| 133,000 |

| 1,353,443 |

| |

Health Care (3.0%) |

|

|

|

|

| |

Wuxi Biologics Cayman, Inc. (a)(b) |

| 104,500 |

| 1,626,690 |

| |

|

|

|

| 2,980,133 |

| |

DENMARK (6.8%) |

|

|

|

|

| |

Health Care (2.5%) |

|

|

|

|

| |

Novo Nordisk AS, Class B |

| 21,100 |

| 1,345,969 |

| |

Industrials (2.0%) |

|

|

|

|

| |

Vestas Wind Systems AS |

| 12,700 |

| 1,090,589 |

| |

Utilities (2.3%) |

|

|

|

|

| |

Orsted AS (a) |

| 12,400 |

| 1,252,529 |

| |

|

|

|

| 3,689,087 |

| |

FRANCE (8.2%) |

|

|

|

|

| |

Financials (1.8%) |

|

|

|

|

| |

AXA SA |

| 54,400 |

| 967,041 |

| |

Health Care (0.9%) |

|

|

|

|

| |

Orpea |

| 4,700 |

| 522,794 |

| |

Industrials (5.5%) |

|

|

|

|

| |

Alstom SA |

| 38,200 |

| 1,566,925 |

| |

Schneider Electric SE |

| 15,000 |

| 1,386,185 |

| |

|

|

|

| 2,953,110 |

| |

|

|

|

| 4,442,945 |

| |

GERMANY (2.7%) |

|

|

|

|

| |

Information Technology (1.2%) |

|

|

|

|

| |

Infineon Technologies AG |

| 34,200 |

| 635,809 |

| |

|

| Shares |

| Value |

|

Materials (1.5%) |

|

|

|

|

|

Covestro AG (a) |

| 24,000 |

| $806,187 |

|

|

|

|

| 1,441,996 |

|

HONG KONG (2.7%) |

|

|

|

|

|

Financials (2.7%) |

|

|

|

|

|

AIA Group Ltd. |

| 161,000 |

| 1,477,620 |

|

INDONESIA (1.0%) |

|

|

|

|

|

Financials (1.0%) |

|

|

|

|

|

Bank Rakyat Indonesia Persero Tbk PT |

| 2,842,700 |

| 517,051 |

|

ISRAEL (1.3%) |

|

|

|

|

|

Industrials (1.3%) |

|

|

|

|

|

Kornit Digital Ltd. (b) |

| 21,100 |

| 699,993 |

|

KENYA (3.7%) |

|

|

|

|

|

Communication Services (3.7%) |

|

|

|

|

|

Safaricom PLC |

| 7,337,600 |

| 1,974,523 |

|

NETHERLANDS (4.2%) |

|

|

|

|

|

Information Technology (1.7%) |

|

|

|

|

|

ASML Holding NV |

| 3,100 |

| 905,464 |

|

Materials (2.5%) |

|

|

|

|

|

Koninklijke DSM NV |

| 11,000 |

| 1,348,181 |

|

|

|

|

| 2,253,645 |

|

NORWAY (2.6%) |

|

|

|

|

|

Communication Services (2.6%) |

|

|

|

|

|

Telenor ASA |

| 91,000 |

| 1,395,852 |

|

REPUBLIC OF IRELAND (0.8%) |

|

|

|

|

|

Industrials (0.8%) |

|

|

|

|

|

Kingspan Group PLC |

| 9,000 |

| 458,613 |

|

SOUTH KOREA (2.5%) |

|

|

|

|

|

Information Technology (2.5%) |

|

|

|

|

|

Samsung SDI Co. Ltd. |

| 5,600 |

| 1,322,921 |

|

TAIWAN (2.5%) |

|

|

|

|

|

Industrials (2.5%) |

|

|

|

|

|

Voltronic Power Technology Corp. |

| 57,200 |

| 1,357,835 |

|

UNITED KINGDOM (14.2%) |

|

|

|

|

|

Consumer Discretionary (1.4%) |

|

|

|

|

|

Countryside Properties PLC (a) |

| 153,200 |

| 780,522 |

|

Health Care (7.4%) |

|

|

|

|

|

AstraZeneca PLC |

| 14,900 |

| 1,558,421 |

|

Clinigen Healthcare Ltd. |

| 140,000 |

| 1,273,102 |

|

GlaxoSmithKline PLC |

| 55,400 |

| 1,155,788 |

|

|

|

|

| 3,987,311 |

|

Statement of Investments (concluded)

April 30, 2020 (Unaudited)

Aberdeen Global Equity Impact Fund

|

| Shares |

| Value |

| |

COMMON STOCKS (continued) |

|

|

|

|

| |

UNITED KINGDOM (continued) |

|

|

|

|

| |

Industrials (5.4%) |

|

|

|

|

| |

John Laing Group PLC (a) |

| 373,600 |

| $ | 1,713,949 |

|

RELX PLC |

| 52,500 |

| 1,184,494 |

| |

|

|

|

| 2,898,443 |

| |

|

|

|

| 7,666,276 |

| |

UNITED STATES (36.1%) |

|

|

|

|

| |

Consumer Discretionary (1.2%) |

|

|

|

|

| |

Chegg, Inc. (b) |

| 15,400 |

| 658,350 |

| |

Health Care (9.4%) |

|

|

|

|

| |

HMS Holdings Corp. (b) |

| 52,700 |

| 1,511,172 |

| |

Merck & Co., Inc. |

| 16,800 |

| 1,332,912 |

| |

UnitedHealth Group, Inc. |

| 7,600 |

| 2,222,772 |

| |

|

|

|

| 5,066,856 |

| |

Industrials (2.6%) |

|

|

|

|

| |

Tetra Tech, Inc. |

| 7,300 |

| 549,544 |

| |

Trane Technologies PLC |

| 9,700 |

| 847,974 |

| |

|

|

|

| 1,397,518 |

| |

Information Technology (10.6%) |

|

|

|

|

| |

Accenture PLC, Class A |

| 6,900 |

| 1,277,811 |

| |

Autodesk, Inc. (b) |

| 6,100 |

| 1,141,493 |

| |

Mastercard, Inc., Class A |

| 6,200 |

| 1,704,814 |

| |

salesforce.com, Inc. (b) |

| 9,800 |

| 1,587,110 |

| |

|

|

|

| 5,711,228 |

| |

Real Estate (9.3%) |

|

|

|

|

| |

American Tower Corp., REIT |

| 4,100 |

| 975,800 |

| |

Equinix, Inc., REIT |

| 2,900 |

| 1,958,080 |

| |

Prologis, Inc., REIT |

| 23,600 |

| 2,105,828 |

| |

|

|

|

| 5,039,708 |

| |

Utilities (3.0%) |

|

|

|

|

| |

NextEra Energy, Inc. |

| 7,100 |

| 1,640,952 |

| |

|

|

|

| 19,514,612 |

| |

Total Common Stocks |

|

|

| 56,102,224 |

| |

|

| Shares |

| Value |

| |

MONEY MARKET FUNDS (0.3%) |

|

|

|

|

| |

UNITED STATES (0.3%) |

|

|

|

|

| |

State Street Institutional U.S. Government Money Market Fund, Premier Class, 0.22% (c) |

| 164,673 |

| $ | 164,673 |

|

Total Money Market Funds |

|

|

| 164,673 |

| |

Total Investments |

|

|

| 56,266,897 |

| |

Liabilities in Excess of Other Assets—(4.2)% |

|

|

| (2,272,705 | ) | |

Net Assets—100.0% |

|

|

| $ | 53,994,192 |

|

(a) Denotes a security issued under Regulation S or Rule 144A.

(b) Non-income producing security.

(c) Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of April 30, 2020.

(d) See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities.

PLC Public Limited Company

REIT Real Estate Investment Trust

See accompanying Notes to Financial Statements.

14 | 2020 Semi-Annual Report |

|

Aberdeen Total Return Bond Fund (Unaudited)

Aberdeen Total Return Bond Fund (Institutional Class shares net of fees) returned 4.39% for the six-month period ended April 30, 2020, versus the 4.86% return of its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, during the same period.

Global financial markets experienced significant bouts of volatility during the six-month period ended April 30, 2020. Over the first half of the reporting period, investor sentiment was bolstered by generally positive economic data reports and news of a “phase one” agreement in the U.S.-China trade dispute. Credit spreads, particularly those of corporate bonds, approached and remained near decade-high tight levels until mid-February 2020. However, in February and March 2020, global financial markets experienced the quickest bearish turn on record. In March, the spread of the COVID-19 pandemic beyond Asia forced many countries from Europe to the U.S. to essentially shut down. The collapse of oil prices attributable to the lack of demand and price war between the Organization of the Petroleum Exporting Countries (OPEC) and Russia intensified investors’ fear of a bankruptcy wave in the energy sector and beyond. Weak economic data outside the U.S. and a flood of 30 million initial unemployment claims in the U.S. over a six-week span shed light on the unprecedented shock to the global economy from both the supply and demand sides of the economic coin. The daunting prospect of a COVID-19 induced deep recession ignited a financial crisis which, to some extent, was more severe than that during the global financial crisis (GFC) of the late 2000s. The spikes in volatility in global government bond markets and credit spreads due to liquidity crunch and malfunctioning of the market were more pronounced.

Global policymakers scrambled – repeatedly and with unseen speed and scale – to mitigate the economic and financial fallout from the pandemic and related containment measures. The U.S. Federal Reserve’s (Fed) two emergency interest-rate cuts in March 2020, reduced the federal funds rate by an aggregate of 150 basis points (bps) to a range of 0% to 0.25%. The Fed also expanded its quantitative easing program, not only in purchasing “unlimited” quantity to government-related instruments, but also to include investment-grade1 corporate bonds for the first time. The central bank also resurrected its Term Asset-Backed Securities Loan Facility (TALF) from 2008, but with more restrictive provisions. In April 2020, the Fed further expanded its lending programs to $2.3 trillion, including high-yield credits in a further break with tradition. An unfolding labor-market crisis led the U.S. Congress to pass a third relief package followed by an addition to the Paycheck Protection Program (PPP) totaling near $3 trillion. The package included funding for the Fed to leverage lending to corporations; loan/grants to small- and medium-sized enterprises (SMEs); direct cash payments to individuals; tax breaks; expanded unemployment benefits; and aid to healthcare

providers and state and local governments. Central banks around the world, particularly in developed-market countries, all embarked on massive monetary and fiscal policy support ranging 3% to 17% of their respective gross domestic products (GDP). In April 2020 alone, G42 central bank balance sheets expanded by $4.4 trillion and their fiscal packages increased by over $2 trillion. The aggressive monetary and fiscal policy support brought some stabilization to the markets towards the end of the reporting period as investors perceived that the risk of an economic depression and a financial calamity had diminished.

The broader U.S. fixed-income market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, returned 4.86% over reporting period amid investors’ fears surrounding the impact of the worldwide spread of the COVID-19 pandemic on the global economy. In the “risk-off” market environment during the reporting period, U.S. Treasury securities outperformed all other fixed income assets, returning 7.95%, as measured by the Bloomberg Barclays U.S. Treasury Index.3 The flight to safety in the market, as well as Fed’s monetary policy actions, led to dramatic declines in yields across the U.S. Treasury curve. Yields on two- three-, five- and ten-year Treasury notes fell 132, 128, 115 and 105 basis points (bps) to 0.20%, 0.24%, 0.36% and 0.64%, respectively, over the six-month reporting period, with the ten- to two-year spread widening by 27 bps to +44 bps. Non-Treasury assets experienced a tremendous amount of volatility and registered the most abrupt declines and quickest recoveries. For example, following a strong performance in the last two months of 2019, the highly indebted corporate bond sector, as measured by the Bloomberg Barclay’s Corporate Bond Index,4 was range-bound until mid-February 2020, when the index underperformed versus the Bloomberg Barclays U.S. Treasury Index by more than 18% over the next 22 business days. After the announcement of policy supports, corporate bonds recover more than 10% against comparable-duration5 Treasuries over the next 26 business days.