UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: | 811-06652 | |

| Exact name of registrant as specified in charter: | Aberdeen Investment Funds | |

| Address of principal executive offices: | 1735 Market Street, 32nd Floor | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | Ms. Andrea Melia | |

| Aberdeen Asset Management Inc. | ||

| 1735 Market Street, 32nd Floor | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | 866-667-9231 | |

| Date of fiscal year end: | October 31 | |

| Date of reporting period: | April 30, 2017 | |

Item 1. Reports to Shareholders.

Aberdeen Investment Funds

Semi-Annual Report

April 30, 2017

Aberdeen Select International Equity Fund

Aberdeen Select International Equity Fund II

Aberdeen Total Return Bond Fund

Aberdeen Global High Income Fund

| Page 1 | ||||

| Page 2 | ||||

| Page 8 | ||||

| Page 14 | ||||

| Page 27 | ||||

| Page 37 | ||||

| Page 52 | ||||

| Page 73 | ||||

Investors should carefully consider a fund’s investment objectives, risks, fees, and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Select International Equity Fund, Aberdeen Select International Equity Fund II, Aberdeen Total Return Bond Fund, and Aberdeen Global High Income Fund, (each a “Fund” and collectively the “Funds”) are distributed by Aberdeen Fund Distributors, LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (AAMI) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23,1995. Registration with the Securities and Exchange Commission does not imply any certain level of skill or training.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for the Funds is included in the Funds’ semi-annual and annual reports to shareholders. The Funds file complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at http://www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330. The Funds make their most recent Forms N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the SEC’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 866-667-9231; and (ii) on the SEC’s website at www.sec.gov.

The vicissitudes of global financial markets over the six-month period ended April 30, 2017 appeared to be slotted between a pair of opposite political bookends. Early in the period in November 2016, Republican Donald Trump surprisingly won the U.S. presidential election, defeating his Democratic party opponent, former U.S. Senator and Secretary of State Hillary Clinton. Trump’s victory seemed to be a continuation of the populist political movement that led to the UK’s vote to leave the European Union (Brexit) five months earlier. Trump had promoted a generally populist message aimed at garnering support from working-class Americans in rural areas in the South and Midwest regions of the U.S. Indeed, his campaign’s promise to “drain the swamp” in the nation’s capital, Washington, D.C., appealed to disaffected blue-collar voters who expressed frustration at being “left behind” during the U.S. economic recovery. However, the new president soon faced numerous political challenges – most notably the ongoing investigation of several members of his administration into possible collusion with the Russian government during the presidential election. Consequently, the myriad distractions hindered Trump’s ability to carry out his policy initiatives over the first four months of his term. Fast-forwarding to the end of the reporting period, the French presidential election took center stage. Global markets were bolstered when independent centrist candidate Emmanuel Macron was the top vote-getter in the first round of the election in late April 2017. Macron subsequently won the final round of the presidential election in early May by a nearly two-to-one margin over far-right candidate Marine Le Pen, who – mirroring Trump – had campaigned on a populist agenda.

The Morgan Stanley Capital International (MSCI) World Index,1 a global equity market benchmark, rose 12.4% for the reporting period. Shares of U.S. large-cap companies significantly outperformed their Asian counterparts for the period, but lagged the performance of large-cap European stocks. The U.S. broader-market Standard & Poor’s (S&P) 500 Index was up 13.3% for the period, while the MSCI Europe and MSCI All Country (AC) Asia Pacific indices returned 14.5% and 8.1%, respectively. Global emerging markets, as measured by the MSCI Emerging Markets Index, advanced 9.0% for the reporting period, but underperformed their developed-market peers.

Major U.S. equity market indices moved sharply higher over the reporting period despite numerous stretches of uncertainty spurred by investors’ concerns regarding the policies and controversial political developments surrounding the Trump administration. In this “risk-on” environment over the six-month period, shares of small-cap companies, as represented by the Russell 2000 Index, climbed 18.4%, considerably outpacing the 13.3% return of the S&P 500 Index. While the period was marked by mixed economic news – improving employment data but more modest economic growth – most U.S. companies reported strong operating results and generally upbeat outlooks. During the first quarter 2017 earnings reporting season, 75% of S&P 500 Index companies exceeded consensus earnings estimates, and 54% posted better-than-expected revenue.2

UK and European stocks rebounded from the sell-off following the Brexit vote in mid-2016, with both markets posting double-digit gains over the reporting period. Early in the period, markets were rattled by UK Prime Minister Theresa May’s announcement of a hard deadline to begin formal negotiations for the country to exit the European Union, which sent the British pound tumbling to a 31-year low. Article 503 was triggered near the end of the reporting period. The regional markets subsequently rallied late in the period following the results of the French presidential election.

Asian equity markets also saw strong performance over the reporting period. Investor risk appetite initially was weak due to uncertainty over Trump’s surprising U.S. presidential election win, a hard Brexit for the UK, and the U.S. Federal Reserve’s (Fed) hint at three more interest-rate hikes after raising its benchmark rate in December 2016. These issues deepened investors’ concerns over increased volatility across Asian markets. China initially faced headwinds amid worries regarding the weakening yuan, accelerating capital outflows and tightening regulations. However, the market rallied soon thereafter, buttressed by positive economic data reports. At the start of 2017, a strengthening global economy and expectations of a gradual Fed tightening of monetary policy buoyed investor sentiment. Asian markets rebounded swiftly from a sell-off late in the reporting period caused by doubts over Trump’s proposed tax reforms, bolstered by upbeat earnings momentum and exports across the region. The Fed maintained a cautious outlook after it again tightened monetary policy, as widely expected, in March 2017. The Bank of Japan (BoJ) left its benchmark interest rate unchanged at -0.1% during the reporting period, and maintained its 80 trillion yen (approximately US$716 billion) asset-purchase program.

Performance in emerging stock markets was mixed during the six-month reporting period. India was a strong performer, as investors grew more confident that the ruling government’s recent election wins in four out of five states, particularly the country’s largest state, Uttar Pradesh, would provide Prime Minister Narendra Modi the necessary mandate to implement his reform agenda. In the Europe, Middle East and Africa (EMEA) region, Russia was buoyed by stabilizing energy prices and a return to economic growth for the first time in two years. There was weakness in the Latin American stock market over the period. Brazilian equities seesawed on anxiety over whether President Michel Temer’s proposed pension reforms would garner Parliamentary approval, while the central bank continued to cut interest rates. Conversely, Mexico’s central bank raised rates for a fifth consecutive time in March 2017, in an effort to combat inflation.

Global fixed-income markets were volatile over the reporting period. Investment-grade bonds, as represented by the Bloomberg Barclays Global Aggregate Bond Index, declined 1.6% for the period. However, high-yield issues significantly outperformed their investment-grade counterparts, with the Bank of America Merrill Lynch Global High Yield Constrained Index gaining 5.5% for the period. Events in the U.S. dominated the news, most notably Trump’s presidential election victory. This halted the global bond market rally in late 2016, as investors considered the possibility that Trump would increase fiscal spending and lift the inflation outlook. Investors subsequently rotated back into bonds amid growing uncertainty over U.S. trade policies and their potential impact on the global recovery. Towards the end of the reporting period, Asian government bonds rallied further as political tensions escalated following U.S. military strikes in Syria and several botched missile tests by North Korea.

Outlook

We remain generally bullish on the global economy. The politically charged environment in the U.S. notwithstanding, we believe that global gross domestic product growth will accelerate over the remainder of 2017 and remain stable in 2018. In our opinion, the most powerful dynamic is the self-fueling, synchronized and thoroughly virtuous global economic recovery. After dragging each other down after 2008, global economies now appear to be pulling each other up as stronger growth, higher inflation, and – most importantly, in our view – improving confidence whet investors’ risk appetite. We are more optimistic about the outlook for global trade, as data for the start of 2017 indicated a pickup in activity in several regions. Nevertheless, in our view, this trade recovery partially reflects temporary factors such as economic stimulus measures in China, while policy uncertainty in the U.S. is elevated. Consequently, we do not think that the outlook is without risks. Although global inflation pressures recently have weakened, we still anticipate that the Fed will raise its benchmark interest rate twice more in 2017, and three times in 2018, and may begin tapering reinvestments of portfolio holdings around the beginning of next year. However, we think that the European Central Bank (ECB) and the BoJ are a long way from meaningful monetary policy tightening. We believe that the ECB may taper quantitative easing in 2018, while the BoJ most likely will maintain its 0% target for 10-year government bond yields.

Aberdeen Asset Management

| 1 | Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | Source: FactSet, “Earnings Insight,” May 2017. |

| 3 | Article 50 contains the procedures to be followed by a country seeking to leave the European Union voluntarily. |

| 2017 Semi-Annual Report | 1 |

Aberdeen Select International Equity Fund (Unaudited)

The Aberdeen Select International Equity Fund (Institutional Class shares net of fees) returned 16.78%1 for the six-month period ended April 30, 2017, versus 10.62% for its benchmark, the MSCI All Country (AC) World ex USA Index, during the same period. For broader comparison, the average return of the Fund’s peer category of International Large-Cap Growth Funds (comprising 41 funds), as measured by Lipper, Inc., was 10.22% for the period.

Global equities rose during the six-month period ended April 30, 2017. Initial uncertainty over the U.S. presidential election in November 2016 gave way to bullishness after Donald Trump’s surprising victory. Several major global equity market indices reached record highs and the U.S. dollar rallied on speculation over potential fiscal stimulus from the incoming Trump administration. Investors’ risk appetite for emerging markets was also renewed. However, the “Trump trade” tapered somewhat by the end of the reporting period amid concerns that political wrangling would hamstring U.S. policymakers, particularly after the failed bill to reform healthcare and uncertainty over a tax overhaul. Supported by firmer economic data, the U.S. Federal Reserve (Fed) raised its benchmark interest rate twice, in December 2016 and in March 2017. Elsewhere, investor sentiment was buoyed by the European Central Bank’s decision to extend its bond-buying program through 2017, albeit at a smaller magnitude after March. Early in the reporting period, markets were rattled by UK Prime Minister Theresa May’s announcement of a hard deadline to begin formal negotiations for the country to exit the European Union (EU), which sent the sterling tumbling to a 31-year low. Article 501 was triggered near the end of the period. Global markets rallied after independent French presidential election candidate Emannuel Macron won the first round of voting in April 2017, with far-right Marine Le Pen placing second. Macron subsequently defeated Le Pen in the final round of the election in May 2017.

Among the Fund’s individual holdings, Prudential was a key contributor to performance for the reporting period, as the UK-based insurer delivered healthy growth in its Asian business and is also a beneficiary of rising global interest rates. Shares of Samsung Electronics performed well despite the arrest of corporate heir-apparent Lee Jae-Yong, which we feel reflects investors’ confidence in the quality of its management. The company posted its best quarterly earnings in over three years for the fourth quarter of its 2016 fiscal year, and announced a share buyback totalling 2.3 trillion won (roughly US$2.0 billion). Additionally, industrial equipment maker Atlas Copco benefited from the recovery in commodity prices and a general improvement in market sentiment for the sector overall.

Conversely, the Fund’s position in Japan Tobacco was a notable detractor from performance, as the company was hampered by strong competition from Philip Morris International (which the Fund does not hold) with regard to “heat-not-burn” products in Japan. Daito Trust Construction’s shares fell on investors’ concerns about the company’s earnings release for the third quarter of its 2017 fiscal year, due to a trend of declining orders for rental apartments. Shares of soft-drink maker Fomento Economico Mexicano (FEMSA) sold off sharply along with the wider Mexican market, which was bogged down by the ”Trump effect” given its extensive trade linkages with its northern neighbor. However, investor sentiment has improved since the start of 2017.

During the reporting period, we initiated a position in Ultrapar, a well-managed and attractively-valued Brazilian chemicals and fuel distribution company, in our view. We also established a new position in India’s HDFC Bank, a conservatively-managed and well-financed lender that we believe has a solid position in a relatively underdeveloped banking market.

The Fund’s receipt of payment of Article 63 European Union (EU) Tax Reclaims related to prior years (2005-2008), the receipt of which was uncertain, was a significant contributor to Fund performance during the reporting period. The receipt of these extraordinary payments increased the Fund’s performance during the period in a manner that may not recur in the future. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. In the tax years for which the Fund filed Article 63 EU Tax Reclaims, certain shareholders were able to reduce their federal income taxes based upon the amount of taxes that these Funds paid to foreign jurisdictions. The receipt by the Fund of the Article 63 EU Tax Reclaim payments will also result in tax liability to the relevant Fund to offset the tax benefits that shareholders received in the past. The precise amount of the tax is uncertain and subject to settlement negotiations with the U.S. Internal Revenue Service (IRS). An estimated tax amount was accrued during the period and detracted from the Fund’s performance. A final determination by the U.S. IRS that the actual tax payable exceeds the amount currently accrued may have a significantly negative impact on the Fund’s expenses, net asset value and performance.

Volatility in global markets remains alarmingly low with the Chicago Board Options Exchange (CBOE) Volatility Index (VIX)2 near record lows as of the end of the reporting period. While Emannuel Macron’s victory in the French presidential election has removed a degree of uncertainty, across the Atlantic, the waters remain muddied by the lack of clarity in U.S. President Trump’s policy initiatives. On the economic front, the latest data coming out of the U.S. and Europe have been positive, and Asian exports continue to show signs of improvement. We think that all of this suggests a more concerted revival in economic growth than was earlier hoped. Nonetheless, we feel that investors are still wary of record- high valuations in many parts of the world, with geopolitical risks and oil price uncertainty likely to persist in the near future. Nevertheless, we remain committed to our fundamentals-focused stock-picking approach, building and maintaining a portfolio of companies that we believe can reap rewards over the long term.

| 1 | Article 50 includes the procedures to be followed by a country seeking to leave the European Union voluntarily. |

| 2 | The CBOE Volatility Index is a measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. |

| 2 | Semi-Annual Report 2017 |

Aberdeen Select International Equity Fund (Unaudited) (concluded)

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Stocks issued by large cap companies subject the Fund to the risk that those stocks may underperform stocks issued by companies with smaller capitalizations or the market as a whole.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 2017 Semi-Annual Report | 3 |

Aberdeen Select International Equity Fund (Unaudited)

Average Annual Total Return* (For periods ended April 30, 2017) | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. | ||||||||||

Class A | 16.65% | 20.16% | 3.15% | (2.18% | ) | |||||||||

Institutional Class | 16.78% | 20.41% | 3.41% | (1.94% | ) | |||||||||

| † | Not Annualized |

| * | Performance shown for periods after December 16, 2016 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2008) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”), the receipt of which was uncertain. The receipt of these extraordinary payments increased the Fund’s performance for all periods that include December 2016 and February 2017 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see the Fund’s prospectus dated February 28, 2017, as amended May 17, 2017, for further information. |

| 4 | Semi-Annual Report 2017 |

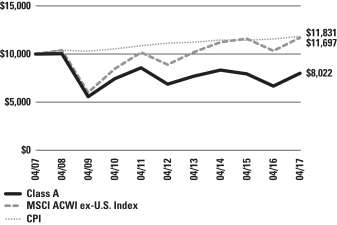

Aberdeen Select International Equity Fund (Unaudited)

Performance of a $10,000 Investment (as of April 30, 2017)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund, Morgan Stanley Capital International All Country World ex-USA Index (MSCI ACWI ex-USA Index), and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2017. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States (U.S.) and 23 Emerging Markets (EM) countries). With 1,852 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2017 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 89.2% | |||

Preferred Stocks | 8.0% | |||

Short-Term Investment | 4.3% | |||

Closed-End Funds | –% | 1 | ||

Government Bonds | –% | 1 | ||

Liabilities in Excess of Other Assets | (1.5% | ) | ||

| 100.0% | ||||

| 1 | Represents a security that is fair valued at zero pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub-industries. As of April 30, 2017, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Consumer Staples | 14.9% | |||

Health Care | 13.7% | |||

Financials | 12.6% | |||

Industrials | 11.7% | |||

Information Technology | 10.3% | |||

Telecommunication Services | 9.0% | |||

Materials | 6.8% | |||

Consumer Discretionary | 6.5% | |||

Energy | 6.2% | |||

Real Estate | 5.5% | |||

Other | 2.8% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Roche Holding AG | 4.0% | |||

Novartis AG | 3.9% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.5% | |||

Japan Tobacco, Inc. | 3.3% | |||

Samsung Electronics Co. Ltd., Preferred Shares | 3.0% | |||

AIA Group Ltd. | 3.0% | |||

Shin-Etsu Chemical Co. Ltd. | 2.9% | |||

Whitbread PLC | 2.6% | |||

Henkel AG & Co. KGaA, Preferred Shares | 2.6% | |||

Fomento Economico Mexicano SAB de CV, ADR | 2.5% | |||

Other | 68.7% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

United Kingdom | 21.7% | |||

Japan | 12.6% | |||

Switzerland | 10.4% | |||

Germany | 8.8% | |||

Hong Kong | 7.3% | |||

United States | 6.7% | |||

Singapore | 4.6% | |||

Taiwan | 3.5% | |||

Republic of South Korea | 3.4% | |||

Brazil | 3.4% | |||

Other | 17.6% | |||

| 100.0% | ||||

| 2017 Semi-Annual Report | 5 |

Statement of Investments

April 30, 2017 (Unaudited)

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (89.2%) | ||||||||

AUSTRALIA (1.2%) | ||||||||

Health Care (1.2%) | ||||||||

CSL Ltd. (a) | 26,700 | $ | 2,647,573 | |||||

BRAZIL (1.0%) | ||||||||

Energy (1.0%) | ||||||||

Ultrapar Participacoes SA, ADR | 103,300 | 2,291,194 | ||||||

CANADA (2.9%) | ||||||||

Materials (1.4%) | ||||||||

Potash Corp. of Saskatchewan, Inc. | 188,800 | 3,183,895 | ||||||

Telecommunication Services (1.5%) | ||||||||

TELUS Corp. | 101,900 | 3,390,570 | ||||||

| 6,574,465 | ||||||||

FRANCE (1.5%) | ||||||||

Consumer Staples (1.5%) | ||||||||

L’Oreal SA (a) | 17,300 | 3,445,288 | ||||||

GERMANY (6.2%) | ||||||||

Health Care (4.6%) | ||||||||

Bayer AG (a) | 38,100 | 4,714,229 | ||||||

Fresenius Medical Care AG & Co. KGaA (a) | 64,900 | 5,761,124 | ||||||

| 10,475,353 | ||||||||

Materials (1.6%) | ||||||||

Linde AG (a) | 19,900 | 3,575,800 | ||||||

| 14,051,153 | ||||||||

HONG KONG (7.3%) | ||||||||

Financials (3.0%) | ||||||||

AIA Group Ltd. (a) | 1,000,600 | 6,925,588 | ||||||

Industrials (3.4%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 84,600 | 5,444,252 | ||||||

MTR Corp. Ltd. (a) | 382,200 | 2,198,862 | ||||||

| 7,643,114 | ||||||||

Real Estate (0.9%) | ||||||||

Swire Pacific Ltd., Class A (a) | 201,000 | 1,938,211 | ||||||

| 16,506,913 | ||||||||

INDIA (1.0%) | ||||||||

Financials (1.0%) | ||||||||

HDFC Bank Ltd., ADR | 28,300 | 2,252,963 | ||||||

ISRAEL (2.4%) | ||||||||

Information Technology (2.4%) | ||||||||

Check Point Software Technologies Ltd. (b) | 53,500 | 5,564,535 | ||||||

ITALY (1.4%) | ||||||||

Energy (1.4%) | ||||||||

Tenaris SA, ADR | 102,900 | 3,213,567 | ||||||

JAPAN (12.6%) | ||||||||

Consumer Discretionary (1.5%) | ||||||||

Shimano, Inc. (a) | 21,500 | 3,290,444 | ||||||

Consumer Staples (3.3%) | ||||||||

Japan Tobacco, Inc. (a) | 227,400 | $ | 7,566,904 | |||||

Industrials (1.5%) | ||||||||

FANUC Corp. (a) | 16,700 | 3,400,054 | ||||||

Information Technology (1.4%) | ||||||||

Keyence Corp. (a) | 8,100 | 3,256,314 | ||||||

Materials (2.9%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (a) | 76,100 | 6,614,431 | ||||||

Real Estate (2.0%) | ||||||||

Daito Trust Construction Co. Ltd. (a) | 31,500 | 4,635,321 | ||||||

| 28,763,468 | ||||||||

LATVIA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

AS Parex Banka (a)(b)(c) | 1,424,182 | – | ||||||

MEXICO (2.5%) | ||||||||

Consumer Staples (2.5%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 64,200 | 5,780,568 | ||||||

PHILIPPINES (0.9%) | ||||||||

Real Estate (0.9%) | ||||||||

Ayala Land, Inc. (a) | 2,972,600 | 2,100,657 | ||||||

REPUBLIC OF SOUTH KOREA (0.4%) | ||||||||

Consumer Staples (0.4%) | ||||||||

Amorepacific Group (a) | 8,507 | 982,834 | ||||||

SINGAPORE (4.6%) | ||||||||

Financials (0.9%) | ||||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 308,729 | 2,162,244 | ||||||

Real Estate (1.7%) | ||||||||

City Developments Ltd. (a) | 487,900 | 3,765,001 | ||||||

Telecommunication Services (2.0%) | ||||||||

Singapore Telecommunications Ltd. (a) | 1,686,100 | 4,514,161 | ||||||

| 10,441,406 | ||||||||

SOUTH AFRICA (1.4%) | ||||||||

Telecommunication Services (1.4%) | ||||||||

MTN Group Ltd. (a) | 340,700 | 3,222,109 | ||||||

SWEDEN (2.1%) | ||||||||

Industrials (2.1%) | ||||||||

Atlas Copco AB, A Shares (a) | 127,000 | 4,744,090 | ||||||

SWITZERLAND (10.4%) | ||||||||

Consumer Staples (2.5%) | ||||||||

Nestle SA (a) | 74,300 | 5,722,620 | ||||||

Health Care (7.9%) | ||||||||

Novartis AG (a) | 115,000 | 8,853,283 | ||||||

Roche Holding AG (a) | 34,500 | 9,027,420 | ||||||

| 17,880,703 | ||||||||

| 23,603,323 | ||||||||

See accompanying Notes to Financial Statements.

| 6 | Semi-Annual Report 2017 |

Statement of Investments (concluded)

April 30, 2017 (Unaudited)

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

TAIWAN (3.5%) | ||||||||

Information Technology (3.5%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 1,232,000 | $ | 7,936,414 | |||||

THAILAND (1.8%) | ||||||||

Financials (1.8%) | ||||||||

Kasikornbank PCL (a) | 767,400 | 4,100,327 | ||||||

UNITED KINGDOM (21.7%) | ||||||||

Consumer Discretionary (2.6%) | ||||||||

Whitbread PLC (a) | 114,600 | 5,987,514 | ||||||

Consumer Staples (2.1%) | ||||||||

British American Tobacco PLC (a) | 68,800 | 4,648,354 | ||||||

Energy (3.8%) | ||||||||

John Wood Group PLC (a) | 345,500 | 3,396,290 | ||||||

Royal Dutch Shell PLC, B Shares (a) | 197,000 | 5,241,571 | ||||||

| 8,637,861 | ||||||||

Financials (3.5%) | ||||||||

Prudential PLC (a) | 214,400 | 4,758,358 | ||||||

Standard Chartered PLC (a)(b) | 349,000 | 3,261,543 | ||||||

| 8,019,901 | ||||||||

Industrials (4.7%) | ||||||||

Experian PLC (a) | 216,400 | 4,655,359 | ||||||

Rolls-Royce Holdings PLC (b) | 24,963,600 | 32,333 | ||||||

Rolls-Royce Holdings PLC (a)(b) | 351,600 | 3,695,846 | ||||||

Weir Group PLC (The) (a) | 91,800 | 2,365,251 | ||||||

| 10,748,789 | ||||||||

Materials (0.9%) | ||||||||

BHP Billiton PLC (a) | 132,300 | 2,016,939 | ||||||

Telecommunication Services (4.1%) | ||||||||

Inmarsat PLC (a) | 354,100 | 3,744,921 | ||||||

Vodafone Group PLC (a) | 2,154,100 | 5,548,186 | ||||||

| 9,293,107 | ||||||||

| 49,352,465 | ||||||||

UNITED STATES (2.4%) | ||||||||

Consumer Discretionary (2.4%) | ||||||||

Samsonite International SA (a) | 1,401,800 | 5,400,209 | ||||||

VENEZUELA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

Banco Venezolano de Credito SA (a)(b)(c) | 156 | – | ||||||

Industrials (0.0%) | ||||||||

Cemex Venezuela SACA-I (a)(b)(c) | 15,843,815 | – | ||||||

| – | ||||||||

Total Common Stocks | 202,975,521 | |||||||

CLOSED-END FUNDS (0.0%) | ||||||||

RUSSIA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

Renaissance Pre-IPO Fund (a)(b)(c) | 92,634 | $ | – | |||||

Total Closed-End Funds | – | |||||||

GOVERNMENT BONDS (0.0%) | ||||||||

VENEZUELA (0.0%) | ||||||||

Bonos de la Deuda Publica Nacional (VEF), 16.00%, 08/23/2018 (a)(c) | 49,500,000 | – | ||||||

Bonos de la Deuda Publica Nacional (VEF), 18.00%, 04/12/2018 (a)(c) | 20,000,000 | – | ||||||

| – | ||||||||

Total Government Bonds | – | |||||||

PREFERRED STOCKS (8.0%) | ||||||||

BRAZIL (2.4%) | ||||||||

Financials (2.4%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares | 523,100 | 5,518,705 | ||||||

GERMANY (2.6%) | ||||||||

Consumer Staples (2.6%) | ||||||||

Henkel AG & Co. KGaA, Preferred Shares (a) | 42,700 | 5,809,916 | ||||||

REPUBLIC OF SOUTH KOREA (3.0%) | ||||||||

Information Technology (3.0%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | 4,500 | 6,929,658 | ||||||

Total Preferred Stocks | 18,258,279 | |||||||

SHORT-TERM INVESTMENT (4.3%) | ||||||||

UNITED STATES (4.3%) | ||||||||

State Street Institutional U.S. Government Money Market Fund (d) | 9,815,448 | 9,815,448 | ||||||

Total Short-Term Investment | 9,815,448 | |||||||

Total Investments | 231,049,248 | |||||||

Liabilities in Excess of Other Assets—(1.5)% | (3,304,302 | ) | ||||||

Net Assets—100.0% | $ | 227,744,946 | ||||||

| (a) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | The Fund’s adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. Illiquid securities held by the Fund represent 0.00% of net assets as of April 30, 2017. |

| (d) | Registered investment company advised by State Street Global Advisors. |

| (e) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

| VEF | Venezuelan Bolivar |

See accompanying Notes to Financial Statements.

| 2017 Semi-Annual Report | 7 |

Aberdeen Select International Equity Fund II (Unaudited)

The Aberdeen Select International Equity Fund II (Institutional Class shares net of fees) returned 14.14% for the six-month period ended April 30, 2017, versus 10.62% for its benchmark, the MSCI All Country (AC) World ex USA Index, during the same period. For broader comparison, the average return of the Fund’s peer category of International Large-Cap Growth Funds (comprising 41 funds), as measured by Lipper, Inc., was 10.22% for the period.

Global equities rose during the six-month period ended April 30, 2017. Initial uncertainty over the U.S. presidential election in November 2016 gave way to bullishness after Donald Trump’s surprising victory. Several major global equity market indices reached record highs and the U.S. dollar rallied on speculation over potential fiscal stimulus from the incoming Trump administration. Investors’ risk appetite for emerging markets was also renewed. However, the “Trump trade” tapered somewhat by the end of the reporting period amid concerns that political wrangling would hamstring U.S. policymakers, particularly after the failed bill to reform healthcare and uncertainty over a tax overhaul. Supported by firmer economic data, the U.S. Federal Reserve (Fed) raised its benchmark interest rate twice, in December 2016 and in March 2017. Elsewhere, investor sentiment was buoyed by the European Central Bank’s decision to extend its bond-buying program through 2017, albeit at a smaller magnitude after March. Early in the reporting period, markets were rattled by UK Prime Minister Theresa May’s announcement of a hard deadline to begin formal negotiations for the country to exit the European Union (EU), which sent the sterling tumbling to a 31-year low. Article 501 was triggered near the end of the period. Global markets rallied after independent French presidential election candidate Emannuel Macron won the first round of voting in April 2017, with far-right Marine Le Pen placing second. Macron subsequently defeated Le Pen in the final round of the election in May 2017.

Among the Fund’s individual holdings, Prudential was a key contributor to performance for the reporting period, as the UK-based insurer delivered healthy growth in its Asian business and is also a beneficiary of rising global interest rates. Shares of Samsung Electronics performed well despite the arrest of corporate heir-apparent Lee Jae-Yong, which we feel reflects investors’ confidence in the quality of its management. The company posted its best quarterly earnings in over three years for the fourth quarter of its 2016 fiscal year, and announced a share buyback totalling 2.3 trillion won (roughly US$2.0 billion). Additionally, industrial equipment maker Atlas Copco benefited from the recovery in commodity prices and a general improvement in market sentiment for the sector overall.

Conversely, the Fund’s position in Japan Tobacco was a notable detractor from performance, as the company was hampered by strong competition from Philip Morris International (which the Fund does not hold) with regard to “heat-not-burn” products in Japan. Daito Trust Construction’s shares fell on investors’ concerns about the company’s earnings release for the third quarter of its 2017 fiscal year, due to a trend of declining orders for rental apartments. Shares of soft-drink maker Fomento Economico Mexicano (FEMSA) sold off sharply along with the wider Mexican market, which was bogged down by the ”Trump effect” given its extensive trade linkages with its northern neighbor. However, investor sentiment has improved since the start of 2017.

During the reporting period, we initiated a position in Ultrapar, a well-managed and attractively-valued Brazilian chemicals and fuel distribution company, in our view. We also established a new position in India’s HDFC Bank, a conservatively-managed and well-financed lender that we believe has a solid position in a relatively underdeveloped banking market.

The Fund’s receipt of payment of Article 63 European Union (EU) Tax Reclaims related to prior years (2005-2008), the receipt of which was uncertain, was a significant contributor to Fund performance during the reporting period. The receipt of these extraordinary payments increased the Fund’s performance during the period in a manner that may not recur in the future. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. In the tax years for which the Fund filed Article 63 EU Tax Reclaims, certain shareholders were able to reduce their federal income taxes based upon the amount of taxes that these Funds paid to foreign jurisdictions. The receipt by the Fund of the Article 63 EU Tax Reclaim payments will also result in tax liability to the relevant Fund to offset the tax benefits that shareholders received in the past. The precise amount of the tax is uncertain and subject to settlement negotiations with the U.S. Internal Revenue Service (IRS). An estimated tax amount was accrued during the period and detracted from the Fund’s performance. A final determination by the U.S. IRS that the actual tax payable exceeds the amount currently accrued may have a significantly negative impact on the Fund’s expenses, net asset value and performance.

Volatility in global markets remains alarmingly low with the Chicago Board Options Exchange (CBOE) Volatility Index (VIX)2 near record lows as of the end of the reporting period. While Emannuel Macron’s victory in the French presidential election has removed a degree of uncertainty, across the Atlantic, the waters remain muddied by the lack of clarity in U.S. President Trump’s policy initiatives. On the economic front, the latest data coming out of the U.S. and Europe have been positive, and Asian exports continue to show signs of improvement. We think that all of this suggests a more concerted revival in economic growth than was earlier hoped. Nonetheless, we feel that investors are still wary of record- high valuations in many parts of the world, with geopolitical risks and oil price uncertainty likely to persist in the near future. Nevertheless, we remain committed to our fundamentals-focused stock-picking approach, building and maintaining a portfolio of companies that we believe can reap rewards over the long term.

| 1 | Article 50 includes the procedures to be followed by a country seeking to leave the European Union voluntarily. |

| 2 | The CBOE Volatility Index is a measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. |

| 8 | Semi-Annual Report 2017 |

Aberdeen Select International Equity Fund II (Unaudited) (concluded)

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A Shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small- and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Stocks issued by large cap companies subject the Fund to the risk that those stocks may underperform stocks issued by companies with smaller capitalizations or the market as a whole.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 2017 Semi-Annual Report | 9 |

Aberdeen Select International Equity Fund II (Unaudited)

Average Annual Total Return* (For periods ended April 30, 2017) | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. | ||||||||||

Class A | 14.13% | 17.61% | 3.10% | (1.46% | ) | |||||||||

Institutional Class | 14.14% | 17.86% | 3.36% | (1.21% | ) | |||||||||

| † | Not Annualized |

| * | Performance shown for periods after February 1, 2017 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2009) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”), the receipt of which was uncertain. The receipt of these extraordinary payments increased the Fund’s performance for all periods that include February 2017 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see the Fund’s prospectus dated February 28, 2017, as amended May 17, 2017, for further information. |

| 10 | Semi-Annual Report 2017 |

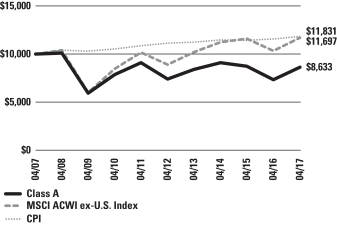

Aberdeen Select International Equity Fund II (Unaudited)

Performance of a $10,000 Investment (as of April 30, 2017)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund II, Morgan Stanley Capital International All Country World ex-USA Index (MSCI ACWI ex-USA Index), and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2017. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States (U.S.) and 23 Emerging Markets (EM) countries). With 1,852 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2017 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 90.2% | |||

Preferred Stocks | 7.7% | |||

Short-Term Investment | 2.7% | |||

Liabilities in Excess of Other Assets | (0.6% | ) | ||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub-industries. As of April 30, 2017, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Consumer Staples | 15.3% | |||

Health Care | 14.0% | |||

Financials | 12.7% | |||

Industrials | 12.3% | |||

Information Technology | 10.6% | |||

Telecommunication Services | 8.8% | |||

Materials | 6.7% | |||

Consumer Discretionary | 6.3% | |||

Energy | 5.6% | |||

Real Estate | 5.6% | |||

Other | 2.1% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Roche Holding AG | 4.2% | |||

Novartis AG | 4.0% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.6% | |||

Japan Tobacco, Inc. | 3.4% | |||

AIA Group Ltd. | 3.3% | |||

Samsung Electronics Co. Ltd., Preferred Shares | 3.1% | |||

Shin-Etsu Chemical Co. Ltd. | 3.0% | |||

Fomento Economico Mexicano SAB de CV, ADR | 2.7% | |||

Henkel AG & Co. KGaA, Preferred Shares | 2.6% | |||

Jardine Matheson Holdings Ltd. | 2.5% | |||

Other | 67.6% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

United Kingdom | 21.1% | |||

Japan | 13.0% | |||

Switzerland | 10.7% | |||

Germany | 8.7% | |||

Hong Kong | 7.8% | |||

United States | 5.0% | |||

Singapore | 4.7% | |||

Taiwan | 3.6% | |||

Republic of South Korea | 3.5% | |||

Brazil | 3.0% | |||

Other | 18.9% | |||

| 100.0% | ||||

| 2017 Semi-Annual Report | 11 |

Statement of Investments

April 30, 2017 (Unaudited)

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (90.2%) | ||||||||

AUSTRALIA (1.2%) | ||||||||

Health Care (1.2%) | ||||||||

CSL Ltd. (a) | 12,000 | $ | 1,189,921 | |||||

BRAZIL (1.0%) | ||||||||

Energy (1.0%) | ||||||||

Ultrapar Participacoes SA, ADR | 44,100 | 978,138 | ||||||

CANADA (2.8%) | ||||||||

Materials (1.4%) | ||||||||

Potash Corp. of Saskatchewan, Inc. | 81,400 | 1,372,717 | ||||||

Telecommunication Services (1.4%) | ||||||||

TELUS Corp. | 40,700 | 1,354,232 | ||||||

| 2,726,949 | ||||||||

FRANCE (1.6%) | ||||||||

Consumer Staples (1.6%) | ||||||||

L’Oreal SA (a) | 7,500 | 1,493,622 | ||||||

GERMANY (6.1%) | ||||||||

Health Care (4.6%) | ||||||||

Bayer AG (a) | 16,100 | 1,992,103 | ||||||

Fresenius Medical Care AG & Co. KGaA (a) | 27,400 | 2,432,277 | ||||||

| 4,424,380 | ||||||||

Materials (1.5%) | ||||||||

Linde AG (a) | 8,000 | 1,437,507 | ||||||

| 5,861,887 | ||||||||

HONG KONG (7.8%) | ||||||||

Financials (3.3%) | ||||||||

AIA Group Ltd. (a) | 452,200 | 3,129,873 | ||||||

Industrials (3.6%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 38,200 | 2,458,279 | ||||||

MTR Corp. Ltd. (a) | 183,500 | 1,055,707 | ||||||

| 3,513,986 | ||||||||

Real Estate (0.9%) | ||||||||

Swire Pacific Ltd., Class A (a) | 91,000 | 877,499 | ||||||

| 7,521,358 | ||||||||

INDIA (1.0%) | ||||||||

Financials (1.0%) | ||||||||

HDFC Bank Ltd., ADR | 12,300 | 979,203 | ||||||

ISRAEL (2.4%) | ||||||||

Information Technology (2.4%) | ||||||||

Check Point Software Technologies Ltd. (b) | 22,500 | 2,340,225 | ||||||

ITALY (1.2%) | ||||||||

Energy (1.2%) | ||||||||

Tenaris SA, ADR | 38,200 | 1,192,986 | ||||||

JAPAN (13.0%) | ||||||||

Consumer Discretionary (1.5%) | ||||||||

Shimano, Inc. (a) | 9,500 | 1,453,917 | ||||||

Consumer Staples (3.4%) | ||||||||

Japan Tobacco, Inc. (a) | 98,900 | $ | 3,290,971 | |||||

Industrials (1.6%) | ||||||||

FANUC Corp. (a) | 7,600 | 1,547,330 | ||||||

Information Technology (1.5%) | ||||||||

Keyence Corp. (a) | 3,600 | 1,447,251 | ||||||

Materials (3.0%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (a) | 33,100 | 2,876,973 | ||||||

Real Estate (2.0%) | ||||||||

Daito Trust Construction Co. Ltd. (a) | 13,400 | 1,971,851 | ||||||

| 12,588,293 | ||||||||

MEXICO (2.7%) | ||||||||

Consumer Staples (2.7%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 29,400 | 2,647,176 | ||||||

PHILIPPINES (1.0%) | ||||||||

Real Estate (1.0%) | ||||||||

Ayala Land, Inc. (a) | 1,342,300 | 948,567 | ||||||

REPUBLIC OF SOUTH KOREA (0.4%) | ||||||||

Consumer Staples (0.4%) | ||||||||

Amorepacific Group (a) | 3,562 | 411,526 | ||||||

SINGAPORE (4.7%) | ||||||||

Financials (1.0%) | ||||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 138,362 | 969,045 | ||||||

Real Estate (1.7%) | ||||||||

City Developments Ltd. (a) | 220,300 | 1,700,000 | ||||||

Telecommunication Services (2.0%) | ||||||||

Singapore Telecommunications Ltd. (a) | 710,400 | 1,901,939 | ||||||

| 4,570,984 | ||||||||

SOUTH AFRICA (1.4%) | ||||||||

Telecommunication Services (1.4%) | ||||||||

MTN Group Ltd. (a) | 144,500 | 1,366,583 | ||||||

SWEDEN (2.3%) | ||||||||

Industrials (2.3%) | ||||||||

Atlas Copco AB, A Shares (a) | 58,600 | 2,189,005 | ||||||

SWITZERLAND (10.7%) | ||||||||

Consumer Staples (2.5%) | ||||||||

Nestle SA (a) | 31,300 | 2,410,741 | ||||||

Health Care (8.2%) | ||||||||

Novartis AG (a) | 50,200 | 3,864,650 | ||||||

Roche Holding AG (a) | 15,600 | 4,081,963 | ||||||

| 7,946,613 | ||||||||

| 10,357,354 | ||||||||

See accompanying Notes to Financial Statements.

| 12 | Semi-Annual Report 2017 |

Statement of Investments (concluded)

April 30, 2017 (Unaudited)

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

TAIWAN (3.6%) | ||||||||

Information Technology (3.6%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 543,000 | $ | 3,497,949 | |||||

THAILAND (1.9%) | ||||||||

Financials (1.9%) | ||||||||

Kasikornbank PCL (a) | 346,500 | 1,851,398 | ||||||

UNITED KINGDOM (21.1%) | ||||||||

Consumer Discretionary (2.5%) | ||||||||

Whitbread PLC (a) | 45,411 | 2,372,592 | ||||||

Consumer Staples (2.1%) | ||||||||

British American Tobacco PLC (a) | 30,100 | 2,033,655 | ||||||

Energy (3.4%) | ||||||||

John Wood Group PLC (a) | 125,800 | 1,236,623 | ||||||

Royal Dutch Shell PLC, B Shares (a) | 78,700 | 2,093,968 | ||||||

| 3,330,591 | ||||||||

Financials (3.5%) | ||||||||

Prudential PLC (a) | 91,400 | 2,028,516 | ||||||

Standard Chartered PLC (a)(b) | 148,100 | 1,384,053 | ||||||

| 3,412,569 | ||||||||

Industrials (4.8%) | ||||||||

Experian PLC (a) | 93,200 | 2,004,988 | ||||||

Rolls-Royce Holdings PLC (a)(b) | 158,800 | 1,669,227 | ||||||

Rolls-Royce Holdings PLC (b) | 11,274,800 | 14,603 | ||||||

Weir Group PLC (The) (a) | 36,600 | 943,009 | ||||||

| 4,631,827 | ||||||||

Materials (0.8%) | ||||||||

BHP Billiton PLC (a) | 51,300 | 782,078 | ||||||

Telecommunication Services (4.0%) | ||||||||

Inmarsat PLC (a) | 146,900 | 1,553,598 | ||||||

Vodafone Group PLC (a) | 885,000 | 2,279,441 | ||||||

| 3,833,039 | ||||||||

| 20,396,351 | ||||||||

UNITED STATES (2.3%) | ||||||||

Consumer Discretionary (2.3%) | ||||||||

Samsonite International SA (a) | 574,600 | 2,213,554 | ||||||

Total Common Stocks | 87,323,029 | |||||||

PREFERRED STOCKS (7.7%) | ||||||||

BRAZIL (2.0%) | ||||||||

Financials (2.0%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares | 183,750 | 1,938,563 | ||||||

GERMANY (2.6%) | ||||||||

Consumer Staples (2.6%) | ||||||||

Henkel AG & Co. KGaA, Preferred Shares (a) | 18,600 | 2,530,783 | ||||||

REPUBLIC OF SOUTH KOREA (3.1%) | ||||||||

Information Technology (3.1%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | 1,960 | $ | 3,018,251 | |||||

Total Preferred Stocks | 7,487,597 | |||||||

SHORT-TERM INVESTMENT (2.7%) | ||||||||

UNITED STATES (2.7%) | ||||||||

State Street Institutional U.S. Government Money Market Fund (c) | 2,583,165 | 2,583,165 | ||||||

Total Short-Term Investment | 2,583,165 | |||||||

Total Investments | 97,393,791 | |||||||

Liabilities in Excess of Other Assets—(0.6)% | (614,956 | ) | ||||||

Net Assets—100.0% | $ | 96,778,835 | ||||||

| (a) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | Registered investment company advised by State Street Global Advisors. |

| (d) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

See accompanying Notes to Financial Statements.

| 2017 Semi-Annual Report | 13 |

Aberdeen Total Return Bond Fund (Unaudited)

The Aberdeen Total Return Bond Fund (Institutional Class shares net of fees) returned -0.31% for the six-month period ended April 30, 2017, versus the -0.67% return of its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the same period. For broader comparison, the average return of the Fund’s peer category of Core Bond Funds (consisting of 153 funds), as measured by Lipper, Inc., was -0.35% for the period.

The U.S. fixed-income market, as measured by the Bloomberg Barclays U.S. Aggregate Bond Index, finished in negative territory for the six-month period ended April 30, 2017. The reporting period was marked by numerous stretches of volatility in global financial markets in response to central bank monetary policy moves and political developments – most notably presidential elections in the U.S. and France. In the U.S., Treasury yields moved significantly higher over the period. The yields on the two-, five- and ten-year notes rose by corresponding margins of 42, 51 and 46 basis points (bps), ending the period at 1.26%, 1.82% and 2.28%, respectively. Consequently, the two- to ten-year yield curve widened just 3 bps over the period. The upswing in yields (and accompanying decline in bond prices) was attributable primarily to the U.S. Federal Reserve’s (Fed) gradual tightening of monetary policy and generally positive U.S. economic data reports.

Donald Trump’s victory in the U.S. presidential election in November 2016 surprised the global financial markets and created many uncertainties related to his policies and their implementation. In the run-up to the election, the markets tended to treat news that suggested a higher probability of a Trump victory as bond-bullish and risk-negative. However, this pattern quickly reversed after the election result, replaced by a bond-bearish, risk-positive trend. In our view, this suggested that investors were focused on the possibility of higher business confidence and fiscal policy easing boosting economic growth, while they viewed protectionism largely as inflationary. A reflation theme dominated, resulting in increases in U.S. yields, the U.S. dollar, global developed-market equities, commodities and a tightening of U.S. credit spreads.

In addition to investors’ persistent belief that the new Trump administration would aggressively pursue tax reform, there were several developments that provided a strong anchor for global fixed-income markets over the reporting period. First, the global synchronized economic recovery was supportive despite the mixed economic data in the U.S. According to the U.S. Department of Commerce, gross domestic product rose 1.2% for the first quarter of 2017, down from the 2.1% rate posted in the fourth quarter of 2016, as declines in private inventory investment and consumer spending offset increases in exports and nonresidential fixed investment. The U.S. Department of Labor reported that the U.S. economy added an average of 149,000 jobs per month over the six-month reporting period, down from the 163,000 average monthly increase for the same time frame a year earlier. Global trade was very strong over the reporting period, with growth in China, Europe and Japan all experiencing activity that surprised to the upside.

Additionally, the Fed raised its benchmark interest rate in two increments of 25 bps in December 2016 and March 2017, to a range of 0.75% to 1.00%. However, the central bank progressed along the normalization process without tightening financial conditions by skillfully managing market expectations. The Federal Open Market Committee (FOMC) noted the continued improvement in the economy and the labor market. Nonetheless, the FOMC commented that inflation recently has moved closer to its 2% target rate, but “longer-term inflation expectations are little changed, on balance.” All these statements appeared to reinforce the consensus market opinion that the Fed will take a path of gradual tightening of monetary policy.

On the international front, anti-European Union (EU) politicians did not make many inroads in Austria, the Netherlands or France during the reporting period. Centrist candidate Emmanuel Macron was the top vote-getter in the first round of the hotly contested French presidential election in April 2017. The election had been considered a referendum on the populist political movement that began with the UK’s approval of Brexit in June 2016, and continued with Trump’s victory in the U.S. five months later. Economic growth and improved investor sentiment not seen since the European sovereign debt crisis began in late 2009 were notable positive factors in the global fixed-income markets’ performance over the reporting period. Many emerging-market economies benefited from the uptrend in global markets over the period; even Brazil and Russia experienced a bottoming of growth and financial constraints. Consequently, over the first four months of 2017, European interest rates and currencies rose while emerging markets recorded one of their strongest performances since 2013 after having experienced some significant stress immediately following the U.S. presidential election.

Fund performance relative to its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the reporting period benefited from strong results from most of its alpha1 sources in the Fund’s Core U.S. market segment.2 The most significant contributor to performance within the segment was strong results from security selection in nearly all sectors, particularly in investment-grade corporate bonds. Fund performance also was bolstered by positive security selection in U.S. agency mortgage-backed securities (MBS), commercial mortgage-backed securities (CMBS), asset-backed securities (ABS) and U.S. Treasuries. The Fund’s sector allocations also produced meaningful alpha for the reporting period. The underweight to U.S. Treasury securities and MBS enhanced Fund performance, as these sectors were the weakest performers within the Fund’s benchmark index over the period. Additionally, Fund performance benefited from the exposure to collateralized mortgage obligations (CMOs), which are not represented in the benchmark index, as these securities outperformed Treasuries as well as agency MBS over the reporting period. Conversely, the Fund’s large overweight position in ABS and a one-time accounting adjustment3 slightly detracted from performance.

Investments in markets outside the U.S. weighed on Fund performance for the reporting period, with losses stemming mostly from foreign currencies as the U.S. dollar strengthened. The Fund’s positions in Mexico were the primary detractors from performance, as the currency took the brunt of damage from fear of U.S.

| 14 | Semi-Annual Report 2017 |

Aberdeen Total Return Bond Fund (Unaudited) (continued)

protectionist trade policies under the Trump administration. Positions in Indonesian bonds and currency also experienced difficulties in the emerging market-related sell-off despite the Indonesian market’s strong fundamentals. The Fund’s holdings in Australian bonds lagged those in the U.S. when strong demand from China weighed on our currency-hedged interest-rate position. The Fund’s positions in its Satellite segment produced a positive absolute return for the reporting period. The holdings in currency-hedged Canadian and New Zealand government bonds collectively outperformed the return of the Bloomberg Barclays U.S. Aggregate Bond Index over the reporting period as their spreads compressed relative to comparable-duration4 U.S. Treasuries.

We employed derivatives over the reporting period, including U.S. Treasury futures, in an effort to manage the Fund’s overall yield-curve and interest-rate exposure, as well as foreign exchange forwards5 in an effort to gain exposure to foreign markets and to hedge risks from sovereign bond holdings. The performance of the Fund’s currency positions largely offset each other over the period, while our use of futures bolstered the Fund’s performance in global interest-rate allocation and yield-curve positioning. The derivatives positions did not have a significant impact on Fund performance for the reporting period.

We entered the reporting period with a cautious stance in anticipation of political risks. However, the Fund performed relatively well even when risk assets performed strongly in the immediate aftermath of Trump’s U.S. presidential election victory, attributable to the holdings in securities that we believe have attractive risk/reward profiles while hedging the macroeconomic risk. For example, the Fund’s holdings in high-beta6 corporate issues in the energy sector performed very well. The reason for us to invest with conviction was that Fund performance was counterbalanced by the exposure to Canadian government bonds, which tend to appreciate when crude oil prices decline. We also reduced the Fund’s duration in international markets and increased duration in the U.S. when U.S. rates rose sharply toward the end of the reporting period. We subsequently covered the Fund’s short duration position in the U.S when the 10-year U.S. Treasury yield rose to 2.6% in mid-March 2017.

With U.S. Treasury yields and the excess spreads provided by risk assets remaining relatively low, we believe that it is especially important to employ active management of the Fund’s global duration and asset allocation. At the end of the reporting period on April 30, 2017, the Fund was positioned with a short duration relative to that of its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, in the U.S., while we have sought to cushion some risk by shifting assets to foreign currency bonds, particularly in commodity-exporting countries. Regarding sectors, we believe that securitized products continue to offer diverse opportunities, most notably non-U.S. agency MBS. In our view, high-quality ABS present a favorable risk/reward profile, and the key to the CMBS market is being selective. Corporate credit fundamentals remain sound, in our opinion, albeit with uncertainties relating to “Trumponomics.” We think that rising interest rates and tight credit spreads could drive a continuation in the increase in mergers-and-acquisitions activity that occurred in the first quarter of 2017. Finally, we believe that emerging markets as an asset class remain more resilient than they were during the “taper tantrum”8 in the U.S. in 2013. Current account and budget deficits have improved, real interest rates9 are higher, and central banks have more room to maneuver with inflation contained. However, we believe that higher leverage and dependence on cheap global capital could possibly create rapid adverse reactions to changes in investor sentiment. Consequently, we retain our selective and opportunistic investment approach.

Improving global trade is boosting economic growth, but we think that there are still reasons for caution. The U.S. economy had a weak first quarter of 2017, but most likely will pick up over the rest of the year, in our opinion. We expect the Trump administration’s fiscal stimulus package to be delayed, shifting some growth momentum toward 2018. We believe that a tight U.S. labor market, sound economic growth and supportive financial conditions may lead the Fed to continue normalizing monetary policy. In our judgment, the Fed will tighten monetary policy in two more increments of 25 bps over the remainder of 2017 by modestly increasing its benchmark interest rate and reducing its balance sheet. We feel that the European growth outlook is generally improving, but policies by European Central Bank (ECB) and Bank of England will remain supportive. Asia and the emerging markets should record positive returns, in our view, but the risks from protectionist U.S. policy have not receded. We think that stability will remain the Chinese government leaders’ top priority leading up to 19th Communist Party Congress in late 2017. While emerging markets may face pressure from rising U.S. Treasury yields, we think that the fortune of local

| 1 | Alpha is a measure of performance that takes the volatility of a mutual fund and compares its risk-adjusted performance to a benchmark index. |

| 2 | The Fund’s investment universe includes six global fixed-income market segments: Core (U.S. investment-grade fixed income); Major (Eurozone, Japan and the UK, among others); Satellites (including, but not limited to Canada, Hong Kong and Switzerland); Convergence (Czech Republic, Hungary and Poland, among others); Commodity (including, but not limited to, Australia, Chile and Russia); and Low Correlation (Brazil, China and Mexico, among others). |

| 3 | There was a $0.02 per share reduction in the daily net asset value from February 17 to February 21, 2017. In addition to reflecting normal market movements and Fund performance, this reduction reflected an accounting adjustment related to a change in the Fund’s valuation procedures, which now align with the valuation procedures across Aberdeen’s fund range. |

| 4 | Duration is an estimate of bond price sensitivity to changes in interest rates. The higher the duration, the greater the change (i.e., higher risk) in relation to interest-rate movements. |

| 5 | A foreign exchange forward is a binding contract in the foreign exchange market that locks in the exchange rate for the purchase or sale of a currency on a future date. |

| 6 | Beta is a measure of the volatility of a portfolio in comparison to a benchmark index. |

| 7 | “Taper tantrum” refers to the sharp rise in U.S. Treasury yields and concurrent decline in bond prices following then-U.S. Federal Reserve Chair Ben Bernanke’s suggestion that the central bank might begin to taper easing of monetary policy. |

| 8 | The real interest rate is the net interest rate after adjusting for the effects of inflation. |

| 2017 Semi-Annual Report | 15 |

Aberdeen Total Return Bond Fund (Unaudited) (concluded)

government bonds and currencies, especially those of commodity exporters, will depend on global growth and capital-flow momentum. In our view, the combined impact most likely will be a gradual rise in interest rates and a generally supportive risk environment.

However, we believe that there are both a downside and upside to this central case. We think that the ultimate outcome is dependent upon the resolution of the following issues. First, how will the growth gap between robust expectation and lackluster economic data reports be closed? Second, how will President Trump and the Republican-controlled Congress choose their priorities and implement their policies regarding tax, fiscal stimulus and regulatory reform given the ongoing investigation of Trump’s associates? Next, after defeating far-right candidate Marine Le Pen in the French presidential election in early May 2017, can Emmanuel Macron successfully implement his economic reform agenda? If so, we believe that Eurozone economic growth could be stronger than our already above-consensus forecast. However, will populist politics emerge in Italy, and where will the next geopolitical flashpoints emerge? Finally, how will global central banks proceed to reduce monetary accommodation? We feel that there are new complexities in addition to the consideration of the Fed’s monetary policy, such as fiscal policy, raising rates versus balance-sheet reduction, and the composition of the FOMC. We believe that the ECB may consider less expansionary monetary policy in light of stronger economic growth and higher inflation expectations. China, a key driver of the recent global economic improvement, is now experiencing tighter monetary conditions.

Portfolio Management:

Aberdeen North American Fixed Income Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in the market value of an investment), credit (changes in the financial condition of the issuer, borrower, counterparty, or underlying collateral), prepayment (debt issuers may repay or refinance their loans or obligations earlier than anticipated), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware which include those associated with fixed income securities, as well as increased susceptibility to adverse economic developments.

Derivatives are speculative and may hurt the Fund’s performance. They present the risk of disproportionately increased losses and/or reduced gains when the financial asset or measure to which the derivative is linked changes in unexpected ways.

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Municipal securities can be affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal securities.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 16 | Semi-Annual Report 2017 |

Aberdeen Total Return Bond Fund (Unaudited)

Average Annual Total Return (For periods ended April 30, 2017) | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. | ||||||||||

Class A | (0.51%) | 1.61% | 2.15% | 4.44% | ||||||||||

Institutional Class | (0.31%) | 1.90% | 2.43% | 4.71% | ||||||||||

| † | Not Annualized |

| 2017 Semi-Annual Report | 17 |

Aberdeen Total Return Bond Fund (Unaudited)

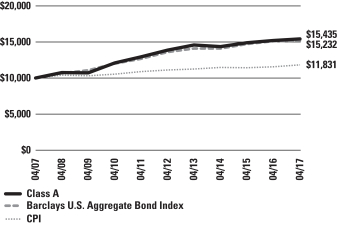

Performance of a $10,000 Investment (as of April 30, 2017)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Total Return Bond Fund, Bloomberg Barclays U.S. Aggregate Bond Index and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2017. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The Bloomberg Barclays U.S. Aggregate Bond Index (the “U.S. Aggregate”) is a broad-based flagship benchmark that measures the investment grade, U.S. Dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Provided the necessary inclusion rules are met, U.S. Aggregate eligible securities also contribute to the multi-currency Bloomberg Barclays Global Aggregate Bond Index and the Bloomberg Barclays U.S. Universal Index, which includes high yield and emerging markets debt.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2017 (Unaudited)

| Asset Allocation | ||||