UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06652

Exact name of registrant as specified in charter:

Aberdeen Investment Funds

Address of principal executive offices:

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Name and address of agent for service:

Ms. Andrea Melia

Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Registrant’s telephone number, including area code: 866-667-9231

Date of fiscal year end: October 31

Date of reporting period: April 30, 2015

Item 1. Reports to Shareholders.

Aberdeen Investment Funds

Semi-Annual Report

April 30, 2015

Aberdeen Select International Equity Fund

Aberdeen Select International Equity Fund II

Aberdeen Total Return Bond Fund

Aberdeen Global High Income Fund

| Page 1 | ||||

| Page 2 | ||||

| Page 3 | ||||

| Page 9 | ||||

| Page 15 | ||||

| Page 28 | ||||

| Page 39 | ||||

| Page 54 | ||||

| Page 73 | ||||

Investors should carefully consider a fund’s investment objectives, risks, fees, and expenses before investing any money. To obtain this and other fund information, please call 1-866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Select International Equity Fund, Aberdeen Select International Equity Fund II, Aberdeen Total Return Bond Fund, and Aberdeen Global High Income Fund, (collectively the “Aberdeen Investment Funds”) are distributed by Aberdeen Fund Distributors, LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (AAMI) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23,1995.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for Aberdeen Investment Funds is included in the Funds’ semi-annual and annual reports to shareholders. Aberdeen Investment Funds file complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at http://www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330. The Funds make their most recent Forms N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the SEC’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-866-667-9231; and (ii) on the SEC’s website at www.sec.gov.

April 30, 2015

Dear Valued Shareholder,

Welcome to the Aberdeen Investment Funds Semi-Annual Report covering the activities for the six-month period ended April 30, 2015.

Market overview

There were numerous global market gyrations during the period in response to economic data releases, declining energy prices and ongoing U.S. dollar strength. However, no single global entity generated more interest than the U.S. Federal Reserve (Fed). Investors worldwide seemed to hang on every word from Fed Chair Janet Yellen and the Federal Open Market Committee (FOMC) in an effort to gauge the direction of U.S. interest rates. By the end of the period, the consensus was that the Fed would delay increasing the federal funds rate until later in the year, given the less-than-robust economic data reports.

In Aberdeen’s view, U.S. equities remain underpinned by justifiable valuations and reasonable corporate performance. Low interest rates continue to provide support to the broader asset class given what should prove a measured – if not protracted – rise in interest rates over the next several years. We think that the outlook for the Eurozone has brightened, underpinned by still-low commodity prices and a weak euro. Although valuations have started to appear full, loose monetary policies and historically low bond yields are likely to continue supporting stock markets. Finally, the normalization of Fed policy is based on the assumption of a sustainable U.S. recovery, which we think should bode well for export-led economies in Asia. The Asia region still boasts some of the world’s fastest-growing economies, despite slower expansion. At the corporate level, there are few signs of an earnings recovery, but companies are making progress in cutting costs to operate more efficiently.

Anne Richards, Aberdeen’s Chief Investment Officer, provides you with a detailed insight on the investment marketplace in the Global Market Review and Outlook on the following page.

Thank you for choosing Aberdeen Investment Funds. We value your investment with us.

Kind Regards,

Bev Hendry

President

Aberdeen Investment Funds

2015 Semi-Annual Report

1

There were divergent performances among geographical regions and asset classes within global financial markets for the six-month reporting period ended April 30, 2015. Regarding stocks, the MSCI World Index, the global large-cap equity market benchmark, gained 5.4% for the period. In a reversal of an earlier trend in the developed markets, U.S. equities underperformed relative to shares of European and Asian large-cap companies. The U.S broad-market S&P 500 Index returned 4.4% for the period versus the 5.8% gain of the MSCI All-Country (AC) World ex U.S. Index. The emerging markets lagged their developed peers during the reporting period due largely to the sharp downturn in the Latin American stock market. Nonetheless, the MSCI Emerging Markets Index rose 4.0% mainly on the strong performance of Chinese equities. The global markets encountered several bouts of volatility amid the rise in oil and commodity prices for much of the period; varying economic news; concerns about ongoing geopolitical tensions in the Middle East; worries over slowing growth in Europe and Asia; and the beginning of aggressive quantitative easing (QE) programs from the European Central Bank (ECB) and the Bank of Japan. Additionally, there was much speculation throughout the period regarding U.S. Federal Reserve (Fed) monetary policy and the timing of any interest rate increases.

U.S. stocks benefited from generally positive economic data and corporate earnings reports over the period. These positive factors offset pressure on companies with significant international exposure, which were negatively affected by the ongoing strength in the U.S. dollar – making U.S. exports relatively less attractive to overseas consumers. This factor had a negative impact on the nation’s gross domestic product (GDP), which declined 0.7% in the first quarter of 2015, attributable mainly to an upturn in imports. GDP grew by a more robust, albeit still below historical trend, rate of 2.2% quarter-over-quarter for the last three months of 2014. At its meeting towards the end of the reporting period in April 2015, the Fed acknowledged the slowdown in economic growth and maintained the federal funds rate near 0%.

UK stocks posted gains over the six-month period but underperformed their European counterparts. UK economic growth did not meet expectations while inflation was virtually flat over the period. The European market benefited from generally positive economic data and an improving outlook for Eurozone manufacturing. Furthermore, the ECB began its larger-than-expected QE program. However, investor confidence was dampened by worries about a possible Greek exit from the Eurozone. Shortly after the close of the reporting period in early May, UK Prime Minister David Cameron’s Conservative Party won a majority in the House of Commons, significantly outpolling the opposition Labor Party. The victory ensures that Cameron will be able to form a new government without the need for a coalition or a formal agreement with other parties.

There were particular deviations in performance in the global emerging equity markets during the reporting period, as strength in China offset a notable decline in Latin America. Expectations of looser monetary policy, as well as the decision to allow Chinese funds to invest in Hong Kong-listed shares without a special license, were the primary drivers of the market in China. Following an earlier downturn, Russian stocks rallied in the second half of the reporting period, buoyed by steadier oil prices and the ceasefire with Ukraine, which alleviated fears of further Western sanctions. Conversely, the slump in Latin American stocks over the period was attributable largely to lower oil prices, which weighed on net energy exporters such as Colombia and Mexico. Brazilian equities and the real, the national currency unit, lost ground due to dissatisfaction over the state of the economy and the unfolding corruption scandal of Petrobras, the state-owned oil company. This culminated in mass demonstrations calling for President Dilma Rousseff’s impeachment during the reporting period.

The global fixed income markets encountered mixed performance over the period, but ended with an overall negative return, as measured by the benchmark Barclays Global Aggregate Bond Index. The performance of the asset class was hampered mainly by European bonds, which declined amid concerns regarding Greece’s future in the Eurozone. U.S. investment-grade securities recorded modest gains and outperformed their international counterparts, as yields declined in all but the shortest segments of the U.S. Treasury yield curve. The overall returns of investment-grade corporate bonds exceeded those of high yield issues, with the Bank of America Merrill Lynch (BofA ML) Global Broad Market Corporate Index advancing 2.4% versus the 2.0% return of the BofA ML Global High Yield Constrained Index for the period. In the emerging markets, the direction of oil prices negatively drove investor sentiment in certain credits. However, the J.P. Morgan EMBI Global Diversified Index rose 1.4% as those countries less affected by the volatility of commodity prices benefited from yield-hungry investors looking to diversify away from developed markets.

Outlook

Hopes of continued loose monetary policy have provided some relief to global stock markets. However, we think that the effect is likely to be temporary, especially in economies where structural weaknesses persist. We believe that stock prices are starting to appear frothy, especially against the backdrop of a global economic slowdown. Consequently, we think that share prices may be due for a correction when the Fed eventually decides to hike interest rates. Within the global fixed income universe, we foresee broad-based yield-curve flattening across core markets, while the levels of nominal yields remain depressed due to weak inflation and large-scale asset purchase programs in Europe and Japan. Even as the Fed moves towards hiking interest rates in the U.S., we think that it is unlikely that the U.S. – European yield spread will widen materially as higher U.S. Treasury yields most likely will attract demand.

Anne Richards

Chief Investment Officer

Aberdeen Asset Management

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Semi-Annual Report 2015

2

Aberdeen Select International Equity Fund (Unaudited)

Aberdeen Select International Equity Fund (Class A shares at net asset value net of fees) returned -0.48% for the six-month period ended April 30, 2015, versus 5.78% for its benchmark, the MSCI All Country World ex U.S. Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of International Multi-Cap Growth Funds (consisting of 113 funds) was 5.97% for the period.

International equities rose during the six-month review period, buoyed by loose global monetary policy. Although the U.S. Federal Reserve (Fed) officially ended its bond-buying program, the Bank of Japan’s increased stimulus, along with the launch of the European Central Bank’s quantitative easing, kept markets awash with liquidity. China also continued to lower benchmark rates and lenders’ reserve ratios in a bid to spur economic growth, after 2014 gross domestic product (GDP) missed official targets for the first time in 17 years. However, Brent crude oil prices sank to a five-year low after the Organization of the Petroleum Exporting Countries (OPEC), following Saudi Arabia’s lead, resisted calls for a cut in output and left production targets unchanged. The sustained drop in oil prices caused turmoil in Russia’s financial markets and the rouble’s collapse, which reverberated worldwide. Sentiment was further dampened by escalating instability in the Middle East and growing doubts that Greece would reach an agreement with creditors in time to unlock about €7 billion (roughly US$7.8 billion) in bailout funds. Nonetheless, international equities rebounded towards the end of the period, as weaker-than-expected U.S. economic activity sparked hopes of a delayed interest rate hike.

Brazilian miner Vale was a key detractor from Fund performance for the reporting period. Its credit rating was downgraded by Standard and Poor’s (S&P), reflecting the credit rating agency’s expectations that it will be hampered in the near term by depressed iron ore prices. Another Brazilian holding, Banco Bradesco, also hindered Fund performance as dissatisfaction over the state of the economy and the unfolding corruption scandal of state-owned oil company Petrobras weighed on the broader market. Despite reporting decent quarterly results that were driven by healthy interest and fee income, shares of the lender fell along with other local banks on worries that the government’s decision to hike taxes on personal loans may slow lending growth. Stock selection in the UK also hindered Fund performance. Utility company Centrica underperformed its peers due to weak full-year 2014 results and management’s decision to cut dividends by a third in order to maintain the group’s investment-grade rating. Engineering services provider Weir Group’s share price fell after analyst downgrades on the back of lower commodity prices.

Meanwhile, falling crude prices have curtailed capital expenditure in the energy sector, which has in turn hurt the bottom lines of oil services companies such as Tenaris. Reduced U.S. drilling activity, as well as de-stocking in the Middle East and Africa, also weighed on the steel pipe-maker’s results. The oil price slump affected holdings such as Royal Dutch Shell and Tenaris. Shell announced plans to cut spending by US$15 billion over the next three years amid a decline in earnings, while oil and gas pipe-maker Tenaris posted weaker-than-expected results because of lower sales of its premium pipes. Reduced U.S. drilling activity, as well as de-stocking in the Middle East and Africa, weighed on the steel pipe-maker’s results.

Conversely, top contributors to Fund performance included Japanese robot-maker Fanuc, Hong Kong-based insurance company AIA, and Swiss drug-maker Novartis. Fanuc’s shares rose after management announced plans to set up a shareholder relations department, in the wake of the government’s new corporate governance rules. The company subsequently released full-year 2014 results that generally met the market’s expectations, raised its dividend payout ratio1 from 30% to 60%, and adopted a flexible share-buyback policy. AIA delivered excellent full-year results on the back of resilient volumes and widening margins. Swiss pharmaceutical firm Novartis reported virtually flat year-over-year sales and operating income for its full-year results, but proposed a 6% dividend increase and indicated a positive outlook for 2015 as a result of recent drug successes and a portfolio overhaul.

During the reporting period, we initiated positions in three stocks: Israel-based IT services company Check Point Software, German healthcare services provider Fresenius Medical Care, and Singapore lender OCBC. In our view, Check Point Software has a strong market position within infrastructure software and network security, while we believe that Fresenius Medical Care is well placed to benefit from aging population trends and steady growth in the global dialysis market. We believe that OCBC is a well-managed bank with a solid capital base and good cost-to-income ratio. In contrast, we sold the Fund’s shares in Petrobras because of the deterioration in its business quality. We also exited the positions in UK utility company Centrica due to increased regulatory and political interference; integrated energy company Eni on our concerns over the sustainability of its dividend and PetroChina following a period of relative share price strength.

Hopes of continued loose monetary policy have provided some relief to global stock markets. However, we think that the effect is likely to be temporary, especially in economies where structural weaknesses persist. While some of the Fund’s holdings have benefited from the run-up in the global equity markets, we believe that stock prices are starting to appear frothy, especially against the backdrop of a global economic slowdown. Consequently, we believe that share prices may be due for a correction when the Fed eventually decides to hike interest rates. Despite the challenging operating environment, however, results from the Fund’s holdings have been relatively resilient, in our view. We remain confident in their ability to grow earnings over the long term.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that

| 1 | The dividend payout ratio represents the percentage of earnings paid to shareholders in dividends. |

2015 Semi-Annual Report

3

Aberdeen Select International Equity Fund (Unaudited) (concluded)

an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Semi-Annual Report 2015

4

Aberdeen Select International Equity Fund (Unaudited)

Average Annual Total Return (For periods ended April 30, 2015) | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. | ||||||||||

Class A | (0.48%) | (4.73% | ) | 1.32% | 3.31% | |||||||||

Institutional Class1 | (0.35%) | (4.51% | ) | 1.56% | 3.57% | |||||||||

| † | Not Annualized |

| 1 | Formerly Class I |

2015 Semi-Annual Report

5

Aberdeen Select International Equity Fund (Unaudited)

Performance of a $10,000 Investment (as of April 30, 2015)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund, Morgan Stanley Capital International All Country World ex-U.S. Index (MSCI ACWI ex-U.S. Index), and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2015. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-U.S. Index captures large, mid, small and micro cap respresentation across 22 of 23 Developed Markets (DM) countries* (excluding the United States). With 8,059 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2015 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 85.2% | |||

Preferred Stocks | 10.4% | |||

Repurchase Agreement | 3.1% | |||

Government Bonds | 0.1% | |||

Exchange Traded Funds | 0.0% | 1 | ||

Other assets in excess of liabilities | 1.2% | |||

| 100.0% | ||||

| 1 | Represents a security that is fair valued at zero pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 10 sectors, 24 industry groups, 68 industries and 154 sub-industries. As of April 30, 2015, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Financials | 18.4% | |||

Industrials | 17.5% | |||

Consumer Staples | 15.0% | |||

Materials | 10.9% | |||

Health Care | 9.9% | |||

Information Technology | 9.7% | |||

Telecommunication Services | 6.8% | |||

Energy | 6.4% | |||

Utilities | 1.0% | |||

Other | 4.4% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Roche Holding AG | 4.5% | |||

Novartis AG | 4.4% | |||

Samsung Electronics Co. Ltd., Preferred Shares | 3.7% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.7% | |||

Nestle SA | 3.6% | |||

Japan Tobacco, Inc. | 3.5% | |||

British American Tobacco PLC | 3.4% | |||

Royal Dutch Shell PLC, B Shares | 3.0% | |||

FANUC Corp. | 2.9% | |||

Shin-Etsu Chemical Co. Ltd. | 2.8% | |||

Other | 64.5% | |||

| 100.0% | ||||

| Top Countries | ||||

United Kingdom | 22.2% | |||

Switzerland | 16.5% | |||

Japan | 10.3% | |||

Hong Kong | 5.3% | |||

Singapore | 5.2% | |||

Canada | 4.9% | |||

France | 4.6% | |||

Brazil | 4.6% | |||

Sweden | 4.4% | |||

Republic of South Korea | 3.7% | |||

Other | 18.3% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

Semi-Annual Report 2015

6

Statement of Investments

April 30, 2015 (Unaudited)

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (85.2%) | ||||||||

BULGARIA (0.4%) | ||||||||

Financials (0.4%) | ||||||||

LEV Insurance (a)(b)(c)(d) | $ | 4,078,860 | $ | 1,596,422 | ||||

CANADA (4.9%) | ||||||||

Industrials (1.9%) | ||||||||

Canadian National Railway Co. | 112,400 | 7,257,323 | ||||||

Materials (2.0%) | ||||||||

Potash Corp. of Saskatchewan, Inc. | 232,400 | 7,589,358 | ||||||

Telecommunication Services (1.0%) | ||||||||

TELUS Corp. | 117,400 | 4,060,590 | ||||||

| 18,907,271 | ||||||||

FRANCE (4.6%) | ||||||||

Consumer Staples (2.1%) | ||||||||

Casino Guichard-Perrachon SA (d) | 92,100 | 8,144,172 | ||||||

Industrials (1.5%) | ||||||||

Schneider Electric SE (d) | 80,200 | 5,994,820 | ||||||

Utilities (1.0%) | ||||||||

GDF Suez (d) | 181,300 | 3,688,800 | ||||||

| 17,827,792 | ||||||||

GERMANY (2.4%) | ||||||||

Health Care (1.0%) | ||||||||

Fresenius Medical Care AG & Co. KGaA (d) | 45,300 | 3,807,085 | ||||||

Materials (1.4%) | ||||||||

Linde AG (d) | 29,000 | 5,666,878 | ||||||

| 9,473,963 | ||||||||

HONG KONG (5.3%) | ||||||||

Financials (3.4%) | ||||||||

AIA Group Ltd. (d) | 1,394,600 | 9,274,752 | ||||||

Swire Pacific Ltd., Class A (d) | 288,500 | 3,894,776 | ||||||

| 13,169,528 | ||||||||

Industrials (1.9%) | ||||||||

Jardine Matheson Holdings Ltd. (d) | 118,200 | 7,302,741 | ||||||

| 20,472,269 | ||||||||

ISRAEL (1.0%) | ||||||||

Information Technology (1.0%) | ||||||||

Check Point Software Technologies Ltd. (c) | 44,700 | 3,731,556 | ||||||

ITALY (1.9%) | ||||||||

Energy (1.9%) | ||||||||

Tenaris SA, ADR | 244,800 | 7,527,600 | ||||||

JAPAN (10.3%) | ||||||||

Consumer Staples (3.5%) | ||||||||

Japan Tobacco, Inc. (d) | 388,900 | 13,580,724 | ||||||

Financials (1.1%) | ||||||||

Daito Trust Construction Co. Ltd. (d) | 35,700 | 4,157,287 | ||||||

Industrials (2.9%) | ||||||||

FANUC Corp. (d) | $ | 51,200 | 11,262,089 | |||||

Materials (2.8%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (d) | 174,100 | 10,642,523 | ||||||

| 39,642,623 | ||||||||

LATVIA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

AS Parex Banka (b)(c)(d) | 1,424,182 | 2 | ||||||

MEXICO (2.4%) | ||||||||

Consumer Staples (2.4%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 102,900 | 9,311,421 | ||||||

SERBIA (0.0%) | ||||||||

Industrials (0.0%) | ||||||||

Toza Markovic ad Kikinda (a)(b)(c)(d) | 78,160 | 0 | ||||||

SINGAPORE (5.2%) | ||||||||

Financials (2.6%) | ||||||||

City Developments Ltd. (d) | 739,000 | 5,945,955 | ||||||

Oversea-Chinese Banking Corp. Ltd. (d) | 519,500 | 4,183,468 | ||||||

| 10,129,423 | ||||||||

Telecommunication Services (2.6%) | ||||||||

Singapore Telecommunications Ltd. (d) | 2,936,600 | 9,812,931 | ||||||

| 19,942,354 | ||||||||

SOUTH AFRICA (2.1%) | ||||||||

Telecommunication Services (2.1%) | ||||||||

MTN Group Ltd. (d) | 413,600 | 8,304,638 | ||||||

SWEDEN (4.4%) | ||||||||

Financials (1.5%) | ||||||||

Nordea Bank AB (d) | 447,900 | 5,690,634 | ||||||

Industrials (1.6%) | ||||||||

Atlas Copco AB, A Shares (d) | 198,462 | 6,194,591 | ||||||

Information Technology (1.3%) | ||||||||

Telefonaktiebolaget LM Ericsson, B Shares (d) | 458,600 | 5,015,606 | ||||||

| 16,900,831 | ||||||||

SWITZERLAND (16.5%) | ||||||||

Consumer Staples (3.6%) | ||||||||

Nestle SA (d) | 178,400 | 13,841,023 | ||||||

Financials (2.4%) | ||||||||

Zurich Insurance Group AG (c)(d) | 30,100 | 9,290,460 | ||||||

Health Care (8.9%) | ||||||||

Novartis AG (d) | 168,800 | 17,229,773 | ||||||

Roche Holding AG (d) | 60,400 | 17,283,768 | ||||||

| 34,513,541 | ||||||||

Industrials (1.6%) | ||||||||

Schindler Holding AG (d) | 36,500 | 6,174,627 | ||||||

| 63,819,651 | ||||||||

See accompanying Notes to Financial Statements.

2015 Semi-Annual Report

7

Statement of Investments (concluded)

April 30, 2015 (Unaudited)

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

TAIWAN (3.7%) | ||||||||

Information Technology (3.7%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (d) | $ | 2,944,000 | $ | 14,173,215 | ||||

UNITED KINGDOM (20.1%) | ||||||||

Consumer Staples (3.4%) | ||||||||

British American Tobacco PLC (d) | 239,300 | 13,147,998 | ||||||

Energy (4.5%) | ||||||||

John Wood Group PLC (d) | 570,412 | 6,010,111 | ||||||

Royal Dutch Shell PLC, B Shares (d) | 360,000 | 11,525,684 | ||||||

| 17,535,795 | ||||||||

Financials (4.4%) | ||||||||

HSBC Holdings PLC (d) | 860,967 | 8,600,628 | ||||||

Standard Chartered PLC (d) | 500,000 | 8,186,099 | ||||||

| 16,786,727 | ||||||||

Industrials (4.0%) | ||||||||

Experian PLC (d) | 449,000 | 8,019,262 | ||||||

Rolls-Royce Holdings PLC (c) | 73,785,300 | 113,260 | ||||||

Weir Group PLC (The) (d) | 253,600 | 7,291,118 | ||||||

| 15,423,640 | ||||||||

Materials (2.7%) | ||||||||

BHP Billiton PLC (d) | 432,700 | 10,400,577 | ||||||

Telecommunication Services (1.1%) | ||||||||

Vodafone Group PLC (d) | 1,247,298 | 4,394,488 | ||||||

| 77,689,225 | ||||||||

VENEZUELA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

Banco Provincial SA-Banco Universal (b) | 18,422 | 108,100 | ||||||

Banco Venezolano de Credito SA (b)(c)(d) | 156 | 0 | ||||||

| 108,100 | ||||||||

Industrials (0.0%) | ||||||||

Cemex Venezuela SACA-I (b)(c)(d) | 15,843,815 | 0 | ||||||

| 108,100 | ||||||||

Total Common Stocks | 329,428,933 | |||||||

EXCHANGE TRADED FUNDS (0.0%) | ||||||||

RUSSIA (0.0%) | ||||||||

Renaissance Pre-IPO Fund (b)(c)(d) | 92,634 | 0 | ||||||

Total Exchange Traded Funds | 0 | |||||||

GOVERNMENT BONDS (0.1%) | ||||||||

VENEZUELA (0.1%) | ||||||||

Bonos de la Deuda Publica Nacional (VEF), 17.25%, 12/31/2015 (b) | 10,000,000 | 40,086 | ||||||

Bonos de la Deuda Publica Nacional (VEF), 16.00%, 08/23/2018 (b) | 49,500,000 | 231,284 | ||||||

Bonos de la Deuda Publica Nacional (VEF), 18.00%, 04/12/2018 (b) | 20,000,000 | 96,455 | ||||||

| 367,825 | ||||||||

Total Government Bonds | 367,825 | |||||||

PREFERRED STOCKS (10.4%) | ||||||||

BRAZIL (4.6%) | ||||||||

Financials (2.6%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares | 957,200 | 10,232,468 | ||||||

Materials (2.0%) | ||||||||

Vale SA, ADR, Preferred Shares | 1,248,400 | 7,552,820 | ||||||

| 17,785,288 | ||||||||

REPUBLIC OF SOUTH KOREA (3.7%) | ||||||||

Information Technology (3.7%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (d) | 14,000 | 14,205,679 | ||||||

UNITED KINGDOM (2.1%) | ||||||||

Industrials (2.1%) | ||||||||

Rolls-Royce Holdings PLC (c)(d) | 523,300 | 8,342,919 | ||||||

Total Preferred Stocks | 40,333,886 | |||||||

REPURCHASE AGREEMENT (3.1%) | ||||||||

UNITED STATES (3.1%) | ||||||||

Repurchase Agreement, Fixed Income Clearing Corp., 0.00%, dated 04/30/2015, due 05/01/2015, repurchase price $11,864,599 collateralized by U.S. Treasury Note, maturing 12/31/2021; total market value of $12,102,500 | 11,864,599 | 11,864,599 | ||||||

Total Repurchase Agreement | 11,864,599 | |||||||

Total Investments | 381,995,243 | |||||||

Other assets in excess of liabilities—1.2% | 4,491,385 | |||||||

Net Assets—100.0% | $ | 386,486,628 | ||||||

| (a) | Investment in affiliate. |

| (b) | The Fund’s adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. Illiquid securities held by the Fund represent 0.54% of net assets as of April 30, 2015. |

| (c) | Non-income producing security. |

| (d) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (e) | See Notes to Financial Statements for tax unrealized appreciation/depreciation of securities. |

| ADR | American Depositary Receipt |

See accompanying Notes to Financial Statements.

Semi-Annual Report 2015

8

Aberdeen Select International Equity Fund II (Unaudited)

Aberdeen Select International Equity Fund II (Class A shares at net asset value net of fees) returned -0.12% for the six-month period ended April 30, 2015, versus 5.78% for its benchmark, the MSCI All Country World ex U.S. Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of International Multi-Cap Growth Funds (consisting of 113 funds) was 5.97% for the period.

International equities rose during the six-month review period, buoyed by loose global monetary policy. Although the U.S. Federal Reserve (Fed) officially ended its bond-buying program, the Bank of Japan’s increased stimulus, along with the launch of the European Central Bank’s quantitative easing, kept markets awash with liquidity. China also continued to lower benchmark rates and lenders’ reserve ratios in a bid to spur economic growth, after 2014 gross domestic product (GDP) missed official targets for the first time in 17 years. However, Brent crude oil prices sank to a five-year low after the Organization of the Petroleum Exporting Countries (OPEC), following Saudi Arabia’s lead, resisted calls for a cut in output and left production targets unchanged. The sustained drop in oil prices caused turmoil in Russia’s financial markets and the rouble’s collapse, which reverberated worldwide. Sentiment was further dampened by escalating instability in the Middle East and growing doubts that Greece would reach an agreement with creditors in time to unlock about €7 billion (roughly US$7.8 billion) in bailout funds. Nonetheless, international equities rebounded towards the end of the period, as weaker-than-expected U.S. economic activity sparked hopes of a delayed interest rate hike.

Brazilian miner Vale was a key detractor from Fund performance for the reporting period. Its credit rating was downgraded by Standard and Poor’s (S&P), reflecting the credit rating agency’s expectations that it will be hampered in the near term by depressed iron ore prices. Another Brazilian holding, Banco Bradesco, also hindered Fund performance as dissatisfaction over the state of the economy and the unfolding corruption scandal of state-owned oil company Petrobras weighed on the broader market. Despite reporting decent quarterly results that were driven by healthy interest and fee income, shares of the lender fell along with other local banks on worries that the government’s decision to hike taxes on personal loans may slow lending growth. Stock selection in the UK also hindered Fund performance. Utility company Centrica underperformed its peers due to weak full-year 2014 results and management’s decision to cut dividends by a third in order to maintain the group’s investment-grade rating. Engineering services provider Weir Group’s share price fell after analyst downgrades on the back of lower commodity prices.

Meanwhile, falling crude prices have curtailed capital expenditure in the energy sector, which has in turn hurt the bottom lines of oil services companies such as Tenaris. Reduced U.S. drilling activity, as well as de-stocking in the Middle East and Africa, also weighed on the steel pipe-maker’s results. The oil price slump affected holdings such as Royal Dutch Shell and Tenaris. Shell announced plans to cut spending by US$15 billion over the next three years amid a decline in earnings, while oil and gas pipe-maker Tenaris posted weaker-than-expected results because of lower sales of its premium pipes. Reduced U.S. drilling activity, as well as de-stocking in the Middle East and Africa, weighed on the steel pipe-maker’s results.

Conversely, top contributors to Fund performance included Japanese robot-maker Fanuc, Hong Kong-based insurance company AIA, and Swiss drug-maker Novartis. Fanuc’s shares rose after management announced plans to set up a shareholder relations department, in the wake of the government’s new corporate governance rules. The company subsequently released full-year 2014 results that generally met the market’s expectations, raised its dividend payout ratio1 from 30% to 60%, and adopted a flexible share-buyback policy. AIA delivered excellent full-year results on the back of resilient volumes and widening margins. Swiss pharmaceutical firm Novartis reported virtually flat year-over-year sales and operating income for its full-year results, but proposed a 6% dividend increase and indicated a positive outlook for 2015 as a result of recent drug successes and a portfolio overhaul.

During the reporting period, we initiated positions in three stocks: Israel-based IT services company Check Point Software, German healthcare services provider Fresenius Medical Care, and Singapore lender OCBC. In our view, Check Point Software has a strong market position within infrastructure software and network security, while we believe that Fresenius Medical Care is well placed to benefit from aging population trends and steady growth in the global dialysis market. We believe that OCBC is a well-managed bank with a solid capital base and good cost-to-income ratio. In contrast, we sold the Fund’s shares in Petrobras because of the deterioration in its business quality. We also exited the positions in UK utility company Centrica due to increased regulatory and political interference; integrated energy company Eni on our concerns over the sustainability of its dividend and PetroChina following a period of relative share price strength.

Hopes of continued loose monetary policy have provided some relief to global stock markets. However, we think that the effect is likely to be temporary, especially in economies where structural weaknesses persist. While some of the Fund’s holdings have benefited from the run-up in the global equity markets, we believe that stock prices are starting to appear frothy, especially against the backdrop of a global economic slowdown. Consequently, we believe that share prices may be due for a correction when the Fed eventually decides to hike interest rates. Despite the challenging operating environment, however, results from the Fund’s holdings have been relatively resilient, in our view. We remain confident in their ability to grow earnings over the long term.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A Shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that

| 1 | The dividend payout ratio represents the percentage of earnings paid to shareholders in dividends. |

2015 Semi-Annual Report

9

Aberdeen Select International Equity Fund II (Unaudited) (concluded)

an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small- and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Semi-Annual Report 2015

10

Aberdeen Select International Equity Fund II (Unaudited)

Average Annual Total Return (For periods ended April 30, 2015) | Six Month† | 1 Yr. | 5 Yr. | Inception1 | ||||||||||

Class A | (0.12%) | (4.05%) | 2.11% | 3.73% | ||||||||||

Institutional Class2 | 0.01% | (3.84%) | 2.36% | 4.01% | ||||||||||

| † | Not Annualized |

| 1 | Fund commenced operations on May 04, 2005. |

| 2 | Formerly Class I |

2015 Semi-Annual Report

11

Aberdeen Select International Equity Fund II (Unaudited)

Performance of a $10,000 Investment (as of April 30, 2015)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund II, Morgan Stanley Capital International All Country World ex-U.S. Index (MSCI ACWI ex-U.S. Index), and the Consumer Price Index (CPI) since inception. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-U.S. Index captures large, mid, small and micro cap respresentation across 22 of 23 Developed Markets (DM) countries* (excluding the United States). With 8,059 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2015 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 86.9% | |||

Preferred Stocks | 10.6% | |||

Repurchase Agreement | 0.2% | |||

Other assets in excess of liabilities | 2.3% | |||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 10 sectors, 24 industry groups, 68 industries and 154 sub-industries. As of April 30, 2015, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Financials | 18.7% | |||

Industrials | 17.6% | |||

Consumer Staples | 15.1% | |||

Materials | 10.8% | |||

Health Care | 10.1% | |||

Information Technology | 9.8% | |||

Telecommunication Services | 7.4% | |||

Energy | 7.0% | |||

Utilities | 1.0% | |||

Other | 2.5% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Roche Holding AG | 4.6% | |||

Novartis AG | 4.5% | |||

Japan Tobacco, Inc. | 3.8% | |||

Samsung Electronics Co. Ltd., Preferred Shares | 3.8% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.6% | |||

Nestle SA | 3.6% | |||

British American Tobacco PLC | 3.3% | |||

Royal Dutch Shell PLC, B Shares | 2.9% | |||

Singapore Telecommunications Ltd. | 2.7% | |||

Shin-Etsu Chemical Co. Ltd. | 2.7% | |||

Other | 64.5% | |||

| 100.0% | ||||

| Top Countries | ||||

United Kingdom | 22.3% | |||

Switzerland | 16.6% | |||

Japan | 10.4% | |||

Hong Kong | 5.5% | |||

Singapore | 5.4% | |||

Canada | 5.2% | |||

Sweden | 5.1% | |||

France | 4.5% | |||

Brazil | 4.4% | |||

Republic of South Korea | 3.8% | |||

Other | 16.8% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

Semi-Annual Report 2015

12

Statement of Investments

April 30, 2015 (Unaudited)

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (86.9%) | ||||||||

CANADA (5.2%) | ||||||||

Industrials (1.9%) | ||||||||

Canadian National Railway Co. | $ | 60,300 | $ | 3,893,386 | ||||

Materials (2.1%) | ||||||||

Potash Corp. of Saskatchewan, Inc. | 126,000 | 4,114,712 | ||||||

Telecommunication Services (1.2%) | ||||||||

TELUS Corp. | 70,700 | 2,445,347 | ||||||

| 10,453,445 | ||||||||

FRANCE (4.5%) | ||||||||

Consumer Staples (2.0%) | ||||||||

Casino Guichard-Perrachon SA (a) | 44,000 | 3,890,810 | ||||||

Industrials (1.5%) | ||||||||

Schneider Electric SE (a) | 39,500 | 2,952,561 | ||||||

Utilities (1.0%) | ||||||||

GDF Suez (a) | 99,400 | 2,022,431 | ||||||

| 8,865,802 | ||||||||

GERMANY (2.6%) | ||||||||

Health Care (1.0%) | ||||||||

Fresenius Medical Care AG & Co. KGaA (a) | 23,000 | 1,932,957 | ||||||

Materials (1.6%) | ||||||||

Linde AG (a) | 16,300 | 3,185,176 | ||||||

| 5,118,133 | ||||||||

HONG KONG (5.5%) | ||||||||

Financials (3.6%) | ||||||||

AIA Group Ltd. (a) | 707,800 | 4,707,206 | ||||||

Swire Pacific Ltd., Class A (a) | 188,000 | 2,538,017 | ||||||

| 7,245,223 | ||||||||

Industrials (1.9%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 61,200 | 3,781,114 | ||||||

| 11,026,337 | ||||||||

ISRAEL (1.0%) | ||||||||

Information Technology (1.0%) | ||||||||

Check Point Software Technologies Ltd. (b) | 24,600 | 2,053,608 | ||||||

ITALY (2.5%) | ||||||||

Energy (2.5%) | ||||||||

Tenaris SA, ADR | 159,400 | 4,901,550 | ||||||

JAPAN (10.4%) | ||||||||

Consumer Staples (3.8%) | ||||||||

Japan Tobacco, Inc. (a) | 219,600 | 7,668,622 | ||||||

Financials (1.2%) | ||||||||

Daito Trust Construction Co. Ltd. (a) | 20,500 | 2,387,237 | ||||||

Industrials (2.7%) | ||||||||

FANUC Corp. (a) | 24,300 | 5,345,093 | ||||||

Materials (2.7%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (a) | $ | 87,900 | 5,373,221 | |||||

| 20,774,173 | ||||||||

MEXICO (2.4%) | ||||||||

Consumer Staples (2.4%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 52,600 | 4,759,774 | ||||||

SINGAPORE (5.4%) | ||||||||

Financials (2.7%) | ||||||||

City Developments Ltd. (a) | 395,000 | 3,178,149 | ||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 259,700 | 2,091,332 | ||||||

| 5,269,481 | ||||||||

Telecommunication Services (2.7%) | ||||||||

Singapore Telecommunications Ltd. (a) | 1,624,000 | 5,426,752 | ||||||

| 10,696,233 | ||||||||

SOUTH AFRICA (2.2%) | ||||||||

Telecommunication Services (2.2%) | ||||||||

MTN Group Ltd. (a) | 220,100 | 4,419,369 | ||||||

SWEDEN (5.1%) | ||||||||

Financials (1.8%) | ||||||||

Nordea Bank AB (a) | 286,600 | 3,641,294 | ||||||

Industrials (1.9%) | ||||||||

Atlas Copco AB, A Shares (a) | 121,200 | 3,783,014 | ||||||

Information Technology (1.4%) | ||||||||

Telefonaktiebolaget LM Ericsson, B Shares (a) | 250,900 | 2,744,037 | ||||||

| 10,168,345 | ||||||||

SWITZERLAND (16.6%) | ||||||||

Consumer Staples (3.6%) | ||||||||

Nestle SA (a) | 91,800 | 7,122,231 | ||||||

Financials (2.4%) | ||||||||

Zurich Insurance Group AG (a)(b) | 15,300 | 4,722,393 | ||||||

Health Care (9.1%) | ||||||||

Novartis AG (a) | 88,500 | 9,033,382 | ||||||

Roche Holding AG (a) | 32,100 | 9,185,579 | ||||||

| 18,218,961 | ||||||||

Industrials (1.5%) | ||||||||

Schindler Holding AG (a) | 18,200 | 3,078,855 | ||||||

| 33,142,440 | ||||||||

TAIWAN (3.6%) | ||||||||

Information Technology (3.6%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 1,498,000 | 7,211,779 | ||||||

UNITED KINGDOM (19.9%) | ||||||||

Consumer Staples (3.3%) | ||||||||

British American Tobacco PLC (a) | 120,400 | 6,615,207 | ||||||

See accompanying Notes to Financial Statements.

2015 Semi-Annual Report

13

Statement of Investments (concluded)

April 30, 2015 (Unaudited)

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

Energy (4.5%) | ||||||||

John Wood Group PLC (a) | $ | 294,800 | $ | 3,106,142 | ||||

Royal Dutch Shell PLC, B Shares (a) | 183,400 | 5,871,696 | ||||||

| 8,977,838 | ||||||||

Financials (4.5%) | ||||||||

HSBC Holdings PLC (a) | 436,213 | 4,357,549 | ||||||

Standard Chartered PLC (a) | 276,603 | 4,528,599 | ||||||

| 8,886,148 | ||||||||

Industrials (3.8%) | ||||||||

Experian PLC (a) | 229,200 | 4,093,574 | ||||||

Rolls-Royce Holdings PLC (b) | 41,778,300 | 64,130 | ||||||

Weir Group PLC (The) (a) | 119,300 | 3,429,930 | ||||||

| 7,587,634 | ||||||||

Materials (2.5%) | ||||||||

BHP Billiton PLC (a) | 210,500 | 5,059,675 | ||||||

Telecommunication Services (1.3%) | ||||||||

Vodafone Group PLC (a) | 730,300 | 2,572,997 | ||||||

| 39,699,499 | ||||||||

Total Common Stocks | 173,290,487 | |||||||

PREFERRED STOCKS (10.6%) | ||||||||

BRAZIL (4.4%) | ||||||||

Financials (2.5%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares | 462,600 | 4,945,194 | ||||||

Materials (1.9%) | ||||||||

Vale SA, ADR, Preferred Shares | 628,900 | 3,804,845 | ||||||

| 8,750,039 | ||||||||

REPUBLIC OF SOUTH KOREA (3.8%) | ||||||||

Information Technology (3.8%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | $ | 7,500 | 7,610,185 | |||||

UNITED KINGDOM (2.4%) | ||||||||

Industrials (2.4%) | ||||||||

Rolls-Royce Holdings PLC (a)(b) | 296,300 | 4,723,881 | ||||||

Total Preferred Stocks | 21,084,105 | |||||||

REPURCHASE AGREEMENT (0.2%) | ||||||||

UNITED STATES (0.2%) | ||||||||

Repurchase Agreement, Fixed Income Clearing Corp., 0.00%, dated 04/30/2015, due 05/01/2015, repurchase price $452,675, collateralized by U.S. Treasury Note, maturing 12/31/2021; total market value of $463,500 | 452,675 | 452,675 | ||||||

Total Repurchase Agreement | 452,675 | |||||||

Total Investments | 194,827,267 | |||||||

Other assets in excess of liabilities—2.3% | 4,585,488 | |||||||

Net Assets—100.0% | $ | 199,412,755 | ||||||

| (a) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | See Notes to Financial Statements for tax unrealized appreciation/depreciation of securities. |

| ADR | American Depositary Receipt |

See accompanying Notes to Financial Statements.

Semi-Annual Report 2015

14

Aberdeen Total Return Bond Fund (Unaudited)

The Aberdeen Total Return Bond Fund (Class A shares at net asset value net of fees) returned 1.66% for the six-month period ended April 30, 2015, versus the 2.06% return of its benchmark, the Barclays U.S. Aggregate Bond Index, for the same period. For broader comparison, the average return of the Fund’s Lipper peer category of Core Bond Funds (consisting of 169 funds) was 1.80% for the period.

The combination of a strengthening U.S. dollar, falling oil prices, economic growth concerns in Europe and Asia, and rolling troubled hotspots caused volatility to spike in global risk markets during the reporting period. Nonetheless, the U.S. broader-market Barclays U.S. Aggregate Bond Index recorded a gain of 2.06% for the six-month period ended April 30, 2015, as yields declined in all but the shortest segments of the U.S. Treasury yield curve. The yields on the one-year Treasury bill and two-year note rose 13 and 8 basis points (bps) – or 0.13% and 0.08% – to 0.24% and 0.58%, respectively, over the period. At the same time, yields on the three-, five- and ten-year notes decreased by corresponding margins of 4, 19 and 30 bps, ending the period at 0.91%, 1.43% and 2.05%, respectively. Consequently, the two- to ten-year yield curve narrowed over the period.

Despite the reversal of the prolonged decline in oil and commodity prices late in the reporting period, the energy sector was the weakest performer within the benchmark Barclays U.S. Corporate Index,1 which we typically use as a proxy for spread sectors. U.S. energy bonds have grown to become the largest component of the corporate market, representing 14% of the benchmark Barclays U.S. Aggregate Bond Index – doubling over the last 10 years. This growth in debt issuance has helped to fund an ambitious expansion plan over the past several years as U.S. energy companies have been aggressively issuing debt to fund capital expenditures.

There was much speculation regarding the direction of the Fed’s monetary policy throughout the reporting period. At its December 2014 meeting, the Federal Open Market Committee (FOMC) removed the reference to “considerable time” from its forward guidance. However, its overall statement was balanced; citing healthy U.S. growth tempered with below–historical-trend inflation due to declining energy prices. New Fed Chair Janet Yellen spoke favorably about the U.S. economic outlook in her testimony before the Senate Banking committee in late February. However, in a statement issued following its meeting on March 17-18, the FOMC commented that it expects inflation to “rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of energy price declines and other factors dissipate.” Finally, in April, the Fed acknowledged the slowdown in economic growth, but noted that “with appropriate policy accommodation, economic activity will expand at a moderate pace.” The FOMC maintained the fed funds rate near 0% while reiterating its position that it will increase the federal funds rate when it believes that there is further improvement in the labor market and a modest decline in the inflation rate to its 2% target.

The upturn in the U.S. economy paused in the first quarter of the year. The Commerce Department’s initial estimate of gross domestic product (GDP) growth came in at an annualized rate of 0.2% – well below the 2.2% gain seen in the fourth quarter of 2014. An uptick in consumer spending was offset by a sharp decline in exports, which continued to face headwinds from a strong U.S. dollar. In early May, the U.S. Department of Labor reported that non-farm payrolls expanded by 223,000 in April, while the unemployment rate dipped marginally to 5.4% – its lowest level in seven years. Tempering the outlook somewhat, however, the job gains for March were adjusted significantly downward and the labor force participation rate2 remained near its 37-year trough.

The Fund’s short duration3 in the U.S. relative to that of the benchmark Barclays U.S. Aggregate Bond Index detracted from performance for the reporting period. We have positioned the Fund with a negative bias toward the short-to-intermediate sector of the U.S. Treasury yield curve (two-to-eight-year duration), while we maintain the modest overweight in the sector of the curve beyond eight years. We continue to believe that the yield curve will flatten as long-term rates will be anchored by the low inflationary backdrop and the higher yields in the U.S. that should continue to entice foreign capital to the U.S. from abroad. The Fund’s exposure to both Mexico and Brazil also had a negative impact on performance. The majority of the Fund’s foreign currency exposure from these bond holdings is hedged back to the U.S. dollar. We had been maintaining unhedged positions in both the Brazilian real and the Mexican peso. However, we believed that these two countries were somewhat vulnerable to declining oil prices and decided to fully hedge these two foreign exchange (FX) positions.

On the positive side, Fund performance was bolstered by the overweight exposure versus the benchmark to the long end of the U.S. Treasury yield curve. Both security selection and an overweight allocation in commercial mortgage-backed securities (MBS), as well as security selection in the non-agency MBS sector, also contributed positively to the Fund’s relative return.

Regarding the use of derivatives during the reporting period, we employed U.S. Treasury futures to manage the Fund’s overall curve and interest rate exposure, and we used currency forwards to hedge some of the Fund’s foreign exchange holdings. This resulted in a contribution of approximately 0.70% to the Fund’s total return for the period.

The biggest change to the Fund’s positioning over the reporting period was the reduction in the global duration underweight relative

| 1 | The Barclays U.S. Corporate Index tracks the performance of publicly issued U.S. corporate and specified foreign debentures that are registered with the Securities and Exchange Commission and meet specific maturity, liquidity, and quality requirements. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | The labor force participation rate is expressed as a percentage of the U.S. population aged 16 years and older working or actively seeking work. |

| 3 | Duration is an estimate of bond price sensitivity to changes in interest rates. The higher the duration, the greater the change (i.e., higher risk) in relation to interest-rate movements. |

2015 Semi-Annual Report

15

Aberdeen Total Return Bond Fund (Unaudited) (concluded)

to the benchmark Barclays U.S. Aggregate Bond Index. As yields declined towards the end of 2014, we decreased the underweight duration because the market was not performing as we expected, and we chose to control risk in case rates continued to fall.

At the end of the period on April 30, 2015, the Fund’s largest holdings were in the corporate and MBS sectors. Relative to the benchmark, the most notable overweight positions included non-U.S. dollar assets (which are not represented in the index), asset-backed securities (ABS) and commercial MBS. In contrast, the Fund was most underweight in U.S. Treasuries and MBS.

In our view, whether U.S. growth rebounds in the second quarter of the year is of more importance than a reading of a single quarter. It is somewhat alarming that, after a disappointing first-quarter GDP number, the growth indicators for the second quarter are well below both previous consensus expectations and the rebound that we’ve experienced over the last several years following a poor GDP reporting period. Reactions by consumers and businesses to lower energy prices diverged rather significantly in both speed and scale than economists had predicted. We also wonder if the growth and inflation responses to a stronger U.S. dollar substantially differ from historical patterns. We will be monitoring data closely going forward to determine if we are on a new “slower growth path” from the already disappointing 2.2% average rate that we’ve seen since 2009.

We continue to believe that a secular stagnation theme will be the most likely scenario dominating economic growth prospects. The consequences of the global financial crises, combined with too much debt, a slowdown in productivity growth, and demographic trends all point to a growth trend below historical average. We come to this conclusion because after approximately six years of unprecedented monetary stimulus that essentially has produced an effective federal funds rate of minus 2-3%, real GDP has still disappointed and has continued below trend. We have had some bright spots over the last several years where growth accelerated; however, the long-awaited lift above the “escape velocity” has not occurred.

Portfolio Management:

Aberdeen North American Fixed Income Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in the market value of an investment), credit (changes in the financial condition of the issuer, borrower, counterparty, or underlying collateral), prepayment (debt issuers may repay or refinance their loans or obligations earlier than anticipated), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Investments in asset-backed and mortgage-backed securities include additional risks that investors should be aware which include those associated with fixed income securities, as well as increased susceptibility to adverse economic developments.

Derivatives are speculative and may hurt the Fund’s performance. They present the risk of disproportionately increased losses and/or reduced gains when the financial asset or measure to which the derivative is linked changes in unexpected ways.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities and are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Municipal securities can be affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal securities.

Please read the prospectus for more detailed information regarding these and other risks.

Semi-Annual Report 2015

16

Aberdeen Total Return Bond Fund (Unaudited)

Average Annual Total Return (For periods ended April 30, 2015) | Six Month† | 1 Yr. | 5 Yr. | 10 Yr. | ||||||||||

Class A | 1.66% | 3.69% | 4.25% | 4.91% | ||||||||||

Institutional Class1 | 1.74% | 3.92% | 4.52% | 5.17% | ||||||||||

| † | Not Annualized |

| 1 | Formerly Class I |

2015 Semi-Annual Report

17

Aberdeen Total Return Bond Fund (Unaudited)

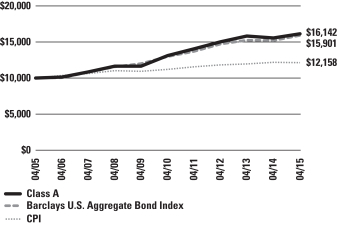

Performance of a $10,000 Investment (as of April 30, 2015)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Total Return Bond Fund, Barclays U.S. Aggregate Bond Index and the Consumer Price Index (CPI) over a 10-year period ended April 30, 2015. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. Dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Performance returns reflect fee waivers and reimbursements in effect without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

April 30, 2015 (Unaudited)

| Asset Allocation | ||||

Corporate Bonds | 31.5% | |||

Commercial Mortgage-Backed Securities | 20.2% | |||

Government Bonds | 10.8% | |||

U.S. Agencies | 10.5% | |||

U.S. Treasuries | 9.9% | |||

Asset-Backed Securities | 9.0% | |||

Municipal Bonds | 4.6% | |||

Repurchase Agreement | 3.9% | |||

Government Agencies | 0.2% | |||

Liabilities in excess of other assets | (0.6% | ) | ||

| 100.0% | ||||

The following chart summarizes the composition of the Fund’s portfolio, expressed as a percentage of net assets. The industries listed below may include more than one industry group. As of April 30, 2015, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Industries | ||||

Commercial Banks | 9.5% | |||

Diversified Financial Services | 2.0% | |||

Banks | 1.9% | |||

Oil, Gas & Consumable Fuels | 1.7% | |||

Energy Equipment & Services | 1.6% | |||

Electric Utilities | 1.6% | |||

Media | 1.3% | |||

Pharmaceutical | 1.2% | |||

Transportation | 1.2% | |||

Beverages | 1.1% | |||

Other | 76.9% | |||

| 100.0% | ||||

| Top Holdings* | ||||

U.S. Treasury Inflation Index Notes 04/15/2019 | 2.1% | |||

Italy Buoni Poliennali Del Tesoro 03/01/2024 | 1.9% | |||

U.S. Treasury Bonds 08/15/2044 | 1.9% | |||

U.S. Treasury Notes 02/15/2025 | 1.7% | |||

U.S. Treasury Notes 05/15/2015 | 1.4% | |||

Spain Government Bond 04/30/2025 | 1.0% | |||

Italy Buoni Poliennali Del Tesoro 03/01/2030 | 1.0% | |||

International Finance Corp. 05/15/2015 | 1.0% | |||

National Australia Bank Ltd. 03/08/2018 | 1.0% | |||

Brazil Letras do Tesouro Nacional 01/01/2017 | 1.0% | |||

Other | 86.0% | |||

| 100.0% | ||||

| Top Countries | ||||

United States | 76.6% | |||

Italy | 3.4% | |||

Australia | 2.9% | |||

Canada | 2.2% | |||

Supranational | 1.9% | |||

Mexico | 1.9% | |||

Netherlands | 1.8% | |||

Brazil | 1.7% | |||

New Zealand | 1.7% | |||

Spain | 1.0% | |||

Other | 4.9% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

Semi-Annual Report 2015

18

Statement of Investments

April 30, 2015 (Unaudited)

Aberdeen Total Return Bond Fund

| Shares or Principal Amount | Value (US$) | |||||||

ASSET-BACKED SECURITIES (9.0%) | ||||||||

CANADA (0.7%) | ||||||||

Ford Auto Securitization Trust, Series 2014-R2, Class A1 (CAD), 1.35%, 03/15/2016 (a) | $ | 149,237 | $ | 123,953 | ||||

Golden Credit Card Trust, Series 2012-5A, Class A (USD), 0.79%, 09/15/2017 (b) | 5,970,000 | 5,975,272 | ||||||

Master Credit Card Trust II, Series 2012-2A, Class A (USD), 0.78%, 04/21/2017 (b) | 4,640,000 | 4,642,684 | ||||||

| 10,741,909 | ||||||||

UNITED STATES (8.3%) | ||||||||

Ally Auto Recivables Trust | ||||||||

Series 2012-3, Class A3 (USD), 0.85%, 08/15/2016 | 770,504 | 770,794 | ||||||

Series 2013-1, Class A3, ABS (USD), 0.63%, 05/15/2017 | 6,105,219 | 6,108,122 | ||||||

American Homes 4 Rent, Series 2015-SFR1, Class A, ABS (USD), 3.47%, 04/17/2052 (b) | 4,480,000 | 4,604,806 | ||||||

Barclays Dryrock Issuance Trust, Series 2015-1, Class A (USD), 2.20%, 12/15/2022 | 3,860,000 | 3,894,037 | ||||||

BMW Floorplan Master Owner Trust, Series 2012-1A, Class A (USD), 0.58%, 09/15/2017 (b)(c) | 6,170,000 | 6,184,537 | ||||||

Chase Issuance Trust, Series 2007-B1, | 5,210,000 | 5,185,714 | ||||||

Chesapeake Funding LLC, Series 2013-1A, Class A (USD), 0.63%, 01/07/2025 (b)(c) | 2,321,162 | 2,322,632 | ||||||

Citibank Credit Card Issuance Trust, Series 2013-A10, Class A10, ABS (USD), 0.73%, 02/07/2018 | 4,970,000 | 4,976,739 | ||||||

CNH Equipment Trust, Series 2013-A, | 1,430,411 | 1,431,614 | ||||||

CNH Wholesale Master Note Trust, Series 2013-2A, Class A (USD), 0.78%, 08/15/2019 (b)(c) | 7,530,000 | 7,538,460 | ||||||

Dryrock Issuance Trust, Series 2012-2, | 4,290,000 | 4,291,083 | ||||||

Ford Credit Auto Lease Trust, Series 2013-A, Class A4 (USD), 0.78%, 04/15/2016 | 4,405,000 | 4,408,343 | ||||||

Ford Credit Auto Owner Trust | ||||||||

Series 2013-B, Class A3 (USD), 0.57%, 10/15/2017 | 1,421,107 | 1,421,462 | ||||||

Series 2015-1, Class A, ABS (USD), 2.12%, 07/15/2026 (b) | 5,540,000 | 5,587,417 | ||||||

GE Dealer Floorplan Master Note Trust | ||||||||

Series 2012-4, Class A (USD), 0.62%, 10/20/2017 (c) | 3,210,000 | 3,210,472 | ||||||

Series 2013-1, Class A (USD), 0.58%, 04/20/2018 (c) | 1,970,000 | 1,970,921 | ||||||

Series 2015-2, Class A (USD), 0.83%, 01/20/2022 (c) | 6,610,000 | 6,603,212 | ||||||

GM Financial Automobile Leasing Trust, Series 2014-2A, Class A3 (USD), 1.22%, 01/22/2018 (b) | 4,380,000 | 4,380,039 | ||||||

Mercedes Benz Auto Lease Trust, Series 2014-A, Class A2A, ABS (USD), 0.48%, 06/15/2016 | 3,022,549 | 3,022,709 | ||||||

Navistar Financial Dealer Note Master Trust | ||||||||

Series 2013-2, Class A (USD), 0.86%, 09/25/2018 (b)(c) | 4,170,000 | 4,173,474 | ||||||

Series 2014-1, Class A (USD), 0.93%, 10/25/2019 (b)(c) | 4,570,000 | 4,576,720 | ||||||

Nissan Auto Receivables Owner Trust, Series 2013-B, Class A3 (USD), 0.84%, 11/15/2017 | 2,223,044 | 2,227,284 | ||||||

SLM Student Loan Trust | ||||||||

Series 2011-1, Class A1 (USD), 0.70%, 03/25/2026 (c) | 1,851,727 | 1,860,004 | ||||||

Series 2011-2, Class A1 (USD), 0.78%, 11/25/2027 (c) | 4,780,644 | 4,779,870 | ||||||

Series 2013-2, Class A (USD), 0.63%, 09/25/2026 (c) | 3,290,052 | 3,282,769 | ||||||

Synchrony Credit Card Master Note Trust, Series 2015-1, Class A, ABS (USD), 2.37%, 03/15/2023 | 4,560,000 | 4,631,904 | ||||||

United States Small Business Administration | ||||||||

Series 2005-P10B, Class 1 (USD), 4.94%, 08/10/2015 | 763,788 | 772,554 | ||||||

Series 2006-P10A, Class 1 (USD), 5.41%, 02/10/2016 | 14,512 | 14,861 | ||||||

Series 2007-P10A, Class 1 (USD), 5.46%, 02/10/2017 | 855,596 | 906,117 | ||||||

Volkswagen Auto Lease Trust, Series 2013-A, Class A3 (USD), 0.84%, 07/20/2016 | 3,147,390 | 3,149,812 | ||||||

Volkswagen Auto Loan Enhanced Trust | ||||||||

Series 2013-1, Class A3 (USD), 0.56%, 08/21/2017 | 2,595,152 | 2,595,318 | ||||||

Series 2013-2, Class A3 (USD), 0.70%, 04/20/2018 | 4,970,000 | 4,966,054 | ||||||

Series 2014-1, Class A2 (USD), 0.42%, 03/20/2017 | 4,073,863 | 4,073,578 | ||||||

Volvo Financial Equipment LLC, Series 2013-1A, Class A3 (USD), 0.74%, 03/15/2017 (b) | 4,260,678 | 4,260,880 | ||||||

| 124,184,312 | ||||||||

Total Asset-Backed Securities | 134,926,221 | |||||||

COMMERCIAL MORTGAGE-BACKED SECURITIES (20.2%) |

| |||||||

UNITED STATES (20.2%) | ||||||||

Alternative Loan Trust | ||||||||

Series 2004-28CB, Class 3A1 (USD), 6.00%, 01/25/2035 | 3,395,435 | 3,351,846 | ||||||

Series 2005-86CB, Class A8 (USD), 5.50%, 02/25/2036 | 3,033,116 | 2,879,415 | ||||||

Avenue of Americas Mortgage Trust, Series 2015-1177, Class A (USD), 2.96%, 12/13/2029 (b)(c) | 3,080,000 | 3,156,241 | ||||||

Banc of America Commercial Mortgage Trust, Series 2006-5, Class AM (USD), 5.45%, 09/10/2047 | 3,550,000 | 3,722,177 | ||||||

Banc of America Merrill Lynch Trust, Series 2015-200, Class A (USD), 3.22%, 04/14/2033 (b)(c) | 2,780,000 | 2,851,023 | ||||||

See accompanying Notes to Financial Statements.

2015 Semi-Annual Report

19

Statement of Investments (continued)

April 30, 2015 (Unaudited)

Aberdeen Total Return Bond Fund

| Shares or Principal Amount | Value (US$) | |||||||

Banc of America Mortgage Trust, Series 2004-7, Class 2A3 (USD), 5.75%, 08/25/2034 | $ | 681,275 | $ | 711,800 | ||||

Barclays Commercial Mortgage Securities Trust, Series 2015-SLP, Class B (USD), 1.78%, 02/15/2028 (b)(c) | 3,760,000 | 3,772,583 | ||||||

Bear Stearns Adjustable Rate Mortgage Trust, Series 2004-3, Class 4A (USD), 2.63%, 07/25/2034 (c) | 1,051,220 | 1,035,676 | ||||||

Bear Stearns Commercial Mortgage Securities Trust | ||||||||

Series 2005-PW10, Class AM (USD), 5.45%, 12/11/2040 (c) | 4,082,000 | 4,164,281 | ||||||

Series 2007-PW17, Class AM (USD), 0.87%, 06/11/2050 (b)(c) | 6,054,750 | 5,960,402 | ||||||

CD Commercial Mortgage Trust, Series 2007-CD4, Class A4 (USD), 5.32%, 12/11/2049 | 4,435,000 | 4,659,588 | ||||||

CHL Mortgage Pass-Through Trust, Series 2005-21, Class A2 (USD), 5.50%, 10/25/2035 | 947,438 | 953,914 | ||||||

Citigroup Commercial Mortgage Trust, Series 2007-C6, Class AM (USD), 5.90%, 12/10/2049 (c) | 3,600,000 | 3,843,455 | ||||||

Citigroup Mortgage Loan Trust | ||||||||

Series 2014-A, Class A (USD), 4.00%, 01/25/2035 (b)(c) | 3,692,982 | 3,861,776 | ||||||

Series 2005-11, Class A3 (USD), 2.50%, 11/25/2035 (c) | 1,894,754 | 1,883,719 | ||||||

Series 2014-J1, Class A1 (USD), 3.50%, 06/25/2044 (b)(c) | 5,889,384 | 6,089,980 | ||||||

COMM 2013-300P Mortgage Trust, Series 2013-300P, Class A1, (USD), 4.35%, 08/10/2030 (b) | 5,790,000 | 6,443,459 | ||||||

COMM 2014-TWC Mortgage Trust, Series 2014-TWC, Class B (USD), 1.78%, 02/13/2032 (b)(c) | 3,810,000 | 3,815,149 | ||||||

Commercial Mortgage Pass Through Certificates | ||||||||

Series 2006-C4, Class A3 (USD), 5.47%, 09/15/2039 | 3,834,628 | 3,998,957 | ||||||

Series 2014-CR20, Class AM (USD), 3.94%, 11/10/2047 | 2,090,000 | 2,219,457 | ||||||

Commercial Mortgage Trust, Series 2007-GG11, Class A4 (USD), 5.74%, 12/10/2049 | 4,255,000 | 4,579,120 | ||||||

Credit Suisse First Boston Mortgage Securities Corp., Series 2004-8, Class 5A1 (USD), 6.00%, 12/25/2034 | 3,085,221 | 3,207,906 | ||||||

Credit Suisse Mortgage Capital Trust | ||||||||

Series 2013-6, Class2A1 (USD), 3.50%, 08/25/2043 (b)(c) | 5,267,978 | 5,401,427 | ||||||

Series 2013-7, Class A11 (USD), 3.50%, 08/25/2043 (b)(c) | 5,934,758 | 6,074,667 | ||||||

Credit Suisse Mortgage Trust | ||||||||

Series 2013-7, Class A2 (USD), 3.00%, 08/25/2043 (b)(c) | 1,296,150 | 1,280,542 | ||||||

Series 2015-WIN1 (USD), 3.50%, 12/25/2044 (b)(c) | 4,850,751 | 4,968,515 | ||||||

EverBank Mortgage Loan Trust, Series 2013-2, Class A (USD), 3.00%, 06/25/2043 (b)(c) | 5,172,964 | 5,169,932 | ||||||

FDIC Guaranteed Notes Trust | ||||||||

Series 2010-C1, Class A (USD), 2.98%, 12/06/2020 (b) | 2,456,412 | 2,519,680 | ||||||

Series 2010-S2, Class 2A (USD), 2.57%, 07/29/2047 (b) | 2,621,974 | 2,658,537 | ||||||

FDIC Trust, Series 2010-R1, Class A (USD), 2.18%, 05/25/2050 (b) | 2,080,187 | 2,097,876 | ||||||

FREMF Mortgage Trust | ||||||||

Series 2011-K704, Class B (USD), 4.69%, 10/25/2030 (b)(c) | 5,730,000 | 6,134,527 | ||||||

Series 2011-K703, Class B (USD), 5.05%, 07/25/2044 (b)(c) | 5,270,000 | 5,687,221 | ||||||

Series 2011-K11, Class B (USD), 4.42%, 12/25/2048 (b)(c) | 1,821,000 | 1,976,960 | ||||||

GRACE Mortgage Trust, Series 2014, Class A (USD), 3.37%, 06/10/2028 (b) | 3,990,000 | 4,200,636 | ||||||

GS Mortgage Securites Corp. Trust | ||||||||

Series 2012-SHOP, Class A (USD), 2.93%, 06/05/2031 (b) | 5,740,000 | 5,961,001 | ||||||

Series 2012-ALOH, Class A (USD), 3.55%, 04/10/2034 (b) | 2,830,000 | 3,011,716 | ||||||

GSR Mortgage Loan Trust, Series 2005-6F, Class 1A6 (USD), 5.25%, 07/25/2035 | 2,181,617 | 2,263,466 | ||||||

Hilton USA Trust 2013-HLT, Series 2013-HLT, Class CFX, (USD), 3.71%, 11/05/2030 (b)(c) | 2,845,000 | 2,894,671 | ||||||

IndyMac INDA Mortgage Loan Trust | ||||||||

Series 2005-AR2, Class 3A1 (USD), 2.65%, 01/25/2036 (c) | 2,955,249 | 2,648,566 | ||||||

Series 2006-AR1, Class A1 (USD), 4.77%, 08/25/2036 (c) | 407,541 | 398,252 | ||||||

JP Morgan Chase Commercial Mortgage Securities Trust, Series 2014-INN, Class A (USD), 1.10%, 06/15/2029 (b)(c) | 5,420,000 | 5,408,686 | ||||||

JP Morgan Mortgage Trust | ||||||||

Series 2005-A2, Class 3A2 (USD), 2.40%, 04/25/2035 (c) | 1,869,070 | 1,819,746 | ||||||