UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549 |

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES |

| Investment Company Act file number 811- 6718 |

Dreyfus Investment Grade Funds, Inc.

(Exact name of Registrant as specified in charter) |

c/o The Dreyfus Corporation

200 Park Avenue

New York, New York 10166

(Address of principal executive offices) (Zip code) |

Michael A. Rosenberg, Esq.

200 Park Avenue

New York, New York 10166

(Name and address of agent for service) |

| Registrant's telephone number, including area code: | | (212) 922-6000 |

| Date of fiscal year end: | | 7/31 | | |

| Date of reporting period: | | 7/31/09 | | |

| Item 1. | | Reports to Stockholders. |

-2-

| | Dreyfus

Inflation Adjusted

Securities Fund |

| | ANNUAL REPORT July 31, 2009 |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

| | | Contents |

| |

| | | THE FUND |

| |

|

| 2 | | A Letter from the Chairman and CEO |

| 3 | | Discussion of Fund Performance |

| 6 | | Fund Performance |

| 7 | | Understanding Your Fund’s Expenses |

| 7 | | Comparing Your Fund’s Expenses |

| | | With Those of Other Funds |

| 8 | | Statement of Investments |

| 10 | | Statement of Assets and Liabilities |

| 11 | | Statement of Operations |

| 12 | | Statement of Changes in Net Assets |

| 14 | | Financial Highlights |

| 16 | | Notes to Financial Statements |

| 25 | | Report of Independent Registered |

| | | Public Accounting Firm |

| 26 | | Important Tax Information |

| 27 | | Information About the Review and Approval |

| | | of the Fund’s Management Agreement |

| 32 | | Board Members Information |

| 34 | | Officers of the Fund |

| |

| | | FOR MORE INFORMATION |

| |

|

| | | Back Cover |

Dreyfus

Inflation Adjusted

Securities Fund |

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Inflation Adjusted Securities Fund, covering the 12-month period from August 1, 2008, through July 31, 2009.

The severe recession and banking crisis that dominated the financial markets over much of the past year appear to have eased. Previously frozen credit markets have thawed to an extent, giving businesses improved access to the capital they need to grow. After reaching multi-year lows early in 2009, higher-yielding segments of the bond market staged an impressive rally, while U.S.Treasury securities have experienced significant price volatility since January as a result of recession-related factors and technical supply issues.The U.S. economy remains weak overall, but we have seen encouraging evidence of potential recovery, including signs of healing in the battered housing and manufacturing sectors. Even the unemployment rate, which historically has been a lagging indicator of economic trends, recently showed signs of improvement.

Although these developments give us reasons for optimism, we remain cautious due to the speed and magnitude of the corporate bond market’s 2009 rebound. Indeed, the market’s advance was fueled more by investors’ renewed appetites for risk than improving business fundamentals. We would prefer to see a steadier rise in asset prices supported by more concrete economic data, as the rapid rise increases the possibility that profit-taking could fuel further volatility. In uncertain markets such as this one,even the most seasoned investors can benefit from professional counsel. To determine how your investments should be positioned for any potential challenges and opportunities that lie ahead, we urge you, as always, to talk regularly with your financial advisor.

For information about how the fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance given by the fund’s Portfolio Manager.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

August 17, 2009 |

2

DISCUSSION OF FUND PERFORMANCE

For the period of August 1, 2008, through July 31, 2009, as provided by Robert Bayston, Portfolio Manager

Fund and Market Performance Overview

For the 12-month period ended July 31, 2009, Dreyfus Inflation Adjusted Securities Fund’s Institutional shares produced a total return of –0.30%, and the fund’s Investor shares returned –0.54%.1 In comparison, the fund’s benchmark, the Barclays Capital U.S. Treasury Inflation Protected Securities Index (the “Index”), produced a total return of –0.53% for the same period.2

Treasury Inflation Protected securities (“TIPS”) were particularly hard-hit in September and October of last year, but have since rallied to an extent year to date as the economic downturn bottomed and deflationary concerns eased. Despite this volatility, the fund’s returns were in line with its benchmark Index, which we attribute in part to our relatively long average duration early in the reporting period and the success of our security selection strategy.

The Fund’s Investment Approach

The fund seeks returns that exceed the rate of inflation.To pursue this goal, the fund normally invests at least 80% of its assets in inflation-indexed securities, which are fixed-income securities designed to protect investors from a loss of value due to inflation by periodically adjusting their principal and/or coupon according to the rate of inflation.

The fund invests primarily in high-quality, U.S. dollar-denominated, inflation-indexed securities. To a limited extent, the fund may invest in foreign currency-denominated, inflation-protected securities and other fixed-income securities not adjusted for inflation, including U.S. government bonds and notes, corporate bonds, mortgage-related securities and asset-backed securities.The fund seeks to keep its average effective duration between two and 10 years, and the fund may invest in securities of any maturity without restriction.

The Fund 3

| DISCUSSION OF FUND PERFORMANCE (continued) |

TIPS Rallied as Deflation Concerns Moderated

The reporting period began in the midst of the longest and deepest recession since the 1930s as housing markets slumped, unemployment rates climbed and consumer confidence deteriorated. In addition, by the start of the reporting period, a global banking crisis already had produced steep declines for higher yielding bonds, including mortgage-backed securities, asset-backed securities and corporate bonds.

In contrast, most U.S. government securities had rallied strongly amid a “flight to quality,” causing their yields to fall to unprecedented low levels. However,TIPS proved to be an exception to that trend. Because of the threat that the global economic downturn might lead to bouts of deflation not seen since the Great Depression,TIPS with maturities of approximately 10 years and less began the reporting period out of favor among investors, and their inflation-adjusted yields were significantly higher than nominal Treasuries. In addition, TIPS had been subject to the effects of limited market liquidity and a wave of deleveraging among institutional investors, which also put downward pressure on prices.

Duration and Security Selection Strategies Bolstered Returns

Because we believed at the time that deflation fears were overblown, we attempted to lock in TIPS’ relatively high yields for as long as we deemed practical by maintaining the fund’s average duration in a range that was longer than industry averages.This positioning enabled the fund to participate more fully in a rally amongTIPS when deflation concerns began to moderate. The rally persisted throughout the spring as it became clearer that a meltdown of the international banking system had been averted. Investors began to look forward to an economic recovery and, potentially, a commensurate acceleration of inflation.

Our security selection strategy also produced positive contributions to the fund’s relative performance, as we had focused on seasoned TIPS with relatively high inflation accruals. In our judgment,TIPS with these characteristics were undervalued compared to more recently issued securities. The fund particularly benefited from an emphasis on TIPS with maturities in the 20-year range as yield differences narrowed along the market’s maturity spectrum.

4

Later in the spring, afterTIPS had rallied and became more fairly valued, we began to reduce the fund’s average duration toward a position that is roughly in line with industry averages.

After the Rally, a More Cautious Investment Posture

As of the reporting period’s end, the economic outlook is unclear.We expect the pace of an eventual economic recovery to be limited by reluctant spending among consumers who increasingly are unemployed and have suffered significant wealth deterioration.The Federal Reserve Board has indicated that it does not see an acceleration of inflation as an imminent threat, and it said that it intends to keep short-term interest rates near historically low levels for some time.

Given this backdrop, we do not believe that the springtime TIPS rally is likely to resume. In addition,TIPS currently appear to be fairly valued at price levels that reflect a low to moderate level of inflation.Therefore, we have maintained a generally neutral investment posture.We believe this is a prudent strategy until we see economic data that more clearly indicate the U.S. economy’s future direction.

August 17, 2009

| 1 | Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figures provided reflect the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an agreement in effect through December 1, 2009, at which time it may be extended, terminated or modified. Had these expenses not been absorbed, the fund’s returns would have been lower. |

| |

| 2 | SOURCE: LIPPER — Reflects reinvestment of dividends and, where applicable, capital gain distributions.The Barclays Capital U.S.Treasury Inflation Protected Securities Index is a sub- index of the U.S.Treasury component of the Barclays Capital U.S. Government Index. Securities in the Barclays Capital U.S.Treasury Inflation Protected Securities Index are dollar-denominated, non-convertible, publicly issued, fixed-rate, investment-grade (Moody’s Baa3 or better) U.S. Treasury inflation notes, with at least one year to final maturity and at least $100 million par amount outstanding. |

| |

| | |

| |

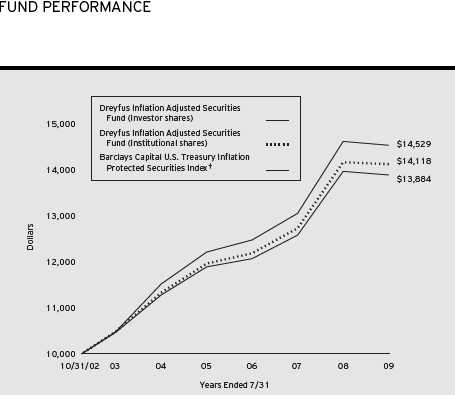

The Fund 5

Comparison of change in value of $10,000 investment in Dreyfus Inflation Adjusted Securities

Fund Investor shares and Institutional shares and the Barclays Capital U.S. Treasury Inflation

Protected Securities Index |

| Average Annual Total Returns as of 7/31/09 | | | | | | |

| | | Inception | | | | | | From |

| | | Date | | 1 Year | | 5 Years | | Inception |

| |

| |

| |

| |

|

| Investor shares | | 10/31/02 | | –0.54% | | 4.25% | | 4.98% |

| Institutional shares | | 10/31/02 | | –0.30% | | 4.50% | | 5.24% |

† Source: Lipper Inc.

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not

reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The above graph compares a $10,000 investment made in Investor and Institutional shares of Dreyfus Inflation Adjusted

Securities Fund on 10/31/02 (inception date) to a $10,000 investment made in the Barclays Capital U.S.Treasury

Inflation Protected Securities Index (the “Index”) on that date.All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph takes into account all applicable fees and expenses.The Index is a sub-

index of the U.S.Treasury component of the Barclays Capital U.S. Government Index. Securities in the Index are

dollar-denominated, non-convertible, publicly-issued, fixed-rate, investment-grade (Moody’s Baa3 or better) U.S.Treasury

inflation notes, with at least one year to final maturity and at least $100 million par amount outstanding. Unlike a

mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index.

Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the

Financial Highlights section of the prospectus and elsewhere in this report. |

6

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Inflation Adjusted Securities Fund from February 1, 2009 to July 31, 2009. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment assuming actual returns for the six months ended July 31, 2009

| | | Investor Shares | | Institutional Shares |

| |

| |

|

| Expenses paid per $1,000† | | $ 2.74 | | $ 1.52 |

| Ending value (after expenses) | | $1,047.50 | | $1,048.70 |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment assuming a hypothetical 5% annualized return for the six months ended July 31, 2009

| | | Investor Shares | | Institutional Shares |

| |

| |

|

| Expenses paid per $1,000† | | $ 2.71 | | $ 1.51 |

| Ending value (after expenses) | | $1,022.12 | | $1,023.31 |

† Expenses are equal to the fund’s annualized expense ratio of .54% for Investor shares and .30% for Institutional

shares, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half

year period). |

The Fund 7

| STATEMENT OF INVESTMENTS | | | | |

| July 31, 2009 | | | | |

| |

| |

|

| |

| |

| |

| |

| | | Principal | | |

| Bonds and Notes—99.7% | | Amount ($) | | Value ($) |

| |

| |

|

| U.S. Treasury Inflation Protected Securities: | | | | |

| 0.63%, 4/15/13 | | 1,947,503 a,b | | 1,924,377 |

| 1.38%, 7/15/18 | | 704,108 a,b | | 686,505 |

| 1.63%, 1/15/15 | | 3,561,218 a,b | | 3,552,315 |

| 1.75%, 1/15/28 | | 673,669 a,b | | 627,775 |

| 1.88%, 7/15/15 | | 3,512,455 a,b | | 3,557,457 |

| 2.00%, 1/15/14 | | 1,889,838 a,b | | 1,929,408 |

| 2.00%, 7/15/14 | | 4,726,035 b | | 4,824,989 |

| 2.00%, 1/15/16 | | 4,147,913 a,b | | 4,217,909 |

| 2.00%, 1/15/26 | | 5,259,769 a,b | | 5,113,484 |

| 2.38%, 4/15/11 | | 4,651,911 a,b | | 4,791,468 |

| 2.38%, 1/15/25 | | 5,143,506 a,b | | 5,256,020 |

| 2.38%, 1/15/27 | | 991,437 a,b | | 1,015,293 |

| 2.50%, 7/15/16 | | 7,242,627 a,b | | 7,611,552 |

| 2.63%, 7/15/17 | | 4,566,564 a,b | | 4,880,515 |

| 3.00%, 7/15/12 | | 5,179,402 a,b | | 5,475,601 |

| 3.63%, 4/15/28 | | 4,887,187 b | | 5,889,061 |

| 3.88%, 4/15/29 | | 2,868,176 a,b | | 3,595,975 |

| Total Bonds and Notes | | | | |

| (cost $64,997,051) | | | | 64,949,704 |

| |

| |

| Other Investment—.1% | | Shares | | Value ($) |

| |

| |

|

| Registered Investment Company; | | | | |

| Dreyfus Institutional Preferred | | | | |

| Plus Money Market Fund | | | | |

| (cost $57,000) | | 57,000 c | | 57,000 |

8

| Investment of Cash Collateral | | | | |

| for Securities Loaned—39.7% | | Shares | | Value ($) |

| |

| |

|

| Registered Investment Company; | | | | |

| Dreyfus Institutional Cash | | | | |

| Advantage Plus Fund | | | | |

| (cost $25,842,012) | | 25,842,012 c | | 25,842,012 |

| |

| Total Investments (cost $90,896,063) | | 139.5% | | 90,848,716 |

| Liabilities, Less Cash and Receivables | | (39.5%) | | (25,714,557) |

| Net Assets | | 100.0% | | 65,134,159 |

a All or a portion of these securities are on loan.At July 31, 2009, the total market value of the fund’s securities on

loan is $25,965,706 and the total market value of the collateral held by the fund is $29,001,239, consisting of

cash collateral of $25,842,012 and U.S. Government and Agency securities valued at $3,159,227.

b Principal amount for accrual purposes is periodically adjusted based on changes in the Consumer Price Index.

c Investment in affiliated money market mutual fund. |

| Portfolio Summary (Unaudited)† | | | | |

| | | Value (%) | | | | Value (%) |

| |

| |

| |

|

| U.S. Government & Agencies | | 99.7 | | Money Market Investments | | 39.8 |

| | | | | | | 139.5 |

| † Based on net assets. | | | | | | |

| See notes to financial statements. | | | | | | |

The Fund 9

STATEMENT OF ASSETS AND LIABILITIES

July 31, 2009

| | | Cost | | Value |

| |

| |

|

| Assets ($): | | | | |

| Investments in securities—See Statement of Investments (including | | |

| securities on loan, valued at $25,965,706)—Note 1(b): | | | | |

| Unaffiliated issuers | | 64,997,051 | | 64,949,704 |

| Affiliated issuers | | 25,899,012 | | 25,899,012 |

| Cash | | | | 336,767 |

| Receivable for investment securities sold | | | | 1,305,889 |

| Receivable for shares of Common Stock subscribed | | | | 570,949 |

| Interest receivable | | | | 173,708 |

| Prepaid expenses | | | | 9,513 |

| | | | | 93,245,542 |

| Liabilities ($): | | | | |

| Due to The Dreyfus Corporation and affiliates—Note 3(b) | | | | 9,916 |

| Liability for securities on loan—Note 1(b) | | | | 25,842,012 |

| Payable for investment securities purchased | | | | 1,537,584 |

| Payable for shares of Common Stock redeemed | | | | 677,484 |

| Accrued expenses | | | | 44,387 |

| | | | | 28,111,383 |

| Net Assets ($) | | | | 65,134,159 |

| Composition of Net Assets ($): | | | | |

| Paid-in capital | | | | 66,674,344 |

| Accumulated distributions in excess of investment income—net | | | | (497) |

| Accumulated net realized gain (loss) on investments | | | | (1,492,341) |

| Accumulated net unrealized appreciation | | | | |

| (depreciation) on investments | | | | (47,347) |

| Net Assets ($) | | | | 65,134,159 |

| |

| |

|

| |

| |

| Net Asset Value Per Share | | | | |

| | | Investor Shares | | Institutional Shares |

| |

| |

|

| Net Assets ($) | | 40,556,968 | | 24,577,191 |

| Shares Outstanding | | 3,386,610 | | 2,052,715 |

| Net Asset Value Per Share ($) | | 11.98 | | 11.97 |

| |

| See notes to financial statements. | | | | |

10

| STATEMENT OF OPERATIONS | | |

| Year Ended July 31, 2009 | | |

| |

|

| |

| |

| |

| |

| Investment Income ($): | | |

| Income: | | |

| Interest | | 502,879 |

| Income from securities lending | | 82,541 |

| Dividends; | | |

| Affiliated issuers | | 2,468 |

| Total Income | | 587,888 |

| Expenses: | | |

| Management fee—Note 3(a) | | 137,665 |

| Shareholder servicing costs—Note 3(b) | | 102,392 |

| Auditing fees | | 40,830 |

| Registration fees | | 33,518 |

| Prospectus and shareholders’ reports | | 10,616 |

| Custodian fees—Note 3(b) | | 7,422 |

| Directors’ fees and expenses—Note 3(c) | | 1,181 |

| Loan commitment fees—Note 2 | | 837 |

| Miscellaneous | | 18,168 |

| Total Expenses | | 352,629 |

| Less—reduction in management fee | | |

| due to undertaking—Note 3(a) | | (136,797) |

| Less—reduction in fees due to earnings credits—Note 1(b) | | (628) |

| Net Expenses | | 215,204 |

| Investment Income—Net | | 372,684 |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | | |

| Net realized gain (loss) on investments | | (1,491,794) |

| Change in net unrealized appreciation (depreciation) on investments | | 1,087,356 |

| Net Realized and Unrealized Gain (Loss) on Investments | | (404,438) |

| Net (Decrease) in Net Assets Resulting from Operations | | (31,754) |

| |

| See notes to financial statements. | | |

The Fund 11

STATEMENT OF CHANGES IN NET ASSETS

| | | | | Year Ended July 31, |

| | |

| |

|

| | | 2009 | | 2008 |

| |

| |

|

| Operations ($): | | | | |

| Investment income—net | | 372,684 | | 1,433,749 |

| Net realized gain (loss) on investments | | (1,491,794) | | 665,250 |

| Change in net unrealized appreciation | | | | |

| (depreciation) on investments | | 1,087,356 | | (1,242,424) |

| Net Increase (Decrease) in Net Assets | | | | |

| Resulting from Operations | | (31,754) | | 856,575 |

| Dividends to Shareholders from ($): | | | | |

| Investment income—net: | | | | |

| Investor Shares | | (378,508) | | (904,889) |

| Institutional Shares | | (219,791) | | (529,563) |

| Net realized gain on investments: | | | | |

| Investor Shares | | (217,001) | | — |

| Institutional Shares | | (125,345) | | — |

| Total Dividends | | (940,645) | | (1,434,452) |

| Capital Stock Transactions ($): | | | | |

| Net proceeds from shares sold: | | | | |

| Investor Shares | | 26,339,642 | | 30,998,869 |

| Institutional Shares | | 19,491,115 | | 10,938,925 |

| Dividends reinvested: | | | | |

| Investor Shares | | 587,130 | | 898,164 |

| Institutional Shares | | 277,721 | | 360,518 |

| Cost of shares redeemed: | | | | |

| Investor Shares | | (12,547,868) | | (7,214,234) |

| Institutional Shares | | (8,611,199) | | (65,381) |

| Increase (Decrease) in Net Assets | | | | |

| from Capital Stock Transactions | | 25,536,541 | | 35,916,861 |

| Total Increase (Decrease) in Net Assets | | 24,564,142 | | 35,338,984 |

| Net Assets ($): | | | | |

| Beginning of Period | | 40,570,017 | | 5,231,033 |

| End of Period | | 65,134,159 | | 40,570,017 |

| Undistributed (distributions in excess of) | | | | |

| investment income—net | | (497) | | 26,984 |

12

| | | | | Year Ended July 31, |

| | |

| |

|

| | | 2009 | | 2008 |

| |

| |

|

| Capital Share Transactions: | | | | |

| Investor Shares | | | | |

| Shares sold | | 2,236,422 | | 2,473,558 |

| Shares issued for dividends reinvested | | 49,400 | | 72,191 |

| Shares redeemed | | (1,080,612) | | (581,927) |

| Net Increase (Decrease) in Shares Outstanding | | 1,205,210 | | 1,963,822 |

| Institutional Shares | | | | |

| Shares sold | | 1,668,857 | | 862,529 |

| Shares issued for dividends reinvested | | 23,554 | | 29,054 |

| Shares redeemed | | (756,913) | | (5,210) |

| Net Increase (Decrease) in Shares Outstanding | | 935,498 | | 886,373 |

| |

| See notes to financial statements. | | | | |

The Fund 13

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | Year Ended July 31, | | |

| | |

| |

| |

|

| Investor Shares | | 2009 | | 2008 | | 2007 | | 2006 | | 2005 |

| |

| |

| |

| |

| |

|

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | | 12.30 | | 11.67 | | 11.69 | | 12.34 | | 12.25 |

| Investment Operations: | | | | | | | | | | |

| Investment income—neta | | .08 | | .79 | | .21 | | .26 | | .25 |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | | (.14) | | .48 | | .27 | | (.06) | | .40 |

| Total from Investment Operations | | (.06) | | 1.27 | | .48 | | .20 | | .65 |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | | (.16) | | (.64) | | (.50) | | (.71) | | (.56) |

| Dividends from net realized | | | | | | | | | | |

| gain on investments | | (.10) | | — | | — | | (.14) | | — |

| Total Distributions | | (.26) | | (.64) | | (.50) | | (.85) | | (.56) |

| Net asset value, end of period | | 11.98 | | 12.30 | | 11.67 | | 11.69 | | 12.34 |

| Total Return (%) | | (.54) | | 11.01 | | 4.24 | | 1.51 | | 5.39 |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | | .87 | | 1.04 | | 2.10 | | 1.88 | | 1.74 |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | | .55 | | .55 | | .53 | | .55 | | .55 |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | | .73 | | 6.39 | | 1.83 | | 2.18 | | 2.00 |

| Portfolio Turnover Rate | | 77.13 | | 90.18 | | 18.17 | | 60.82 | | 118.91 |

| Net Assets, end of period ($ x 1,000) | | 40,557 | | 26,830 | | 2,538 | | 3,269 | | 3,009 |

| |

| a Based on average shares outstanding at each month end. | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | |

14

| | | | | Year Ended July 31, | | |

| | |

| |

| |

|

| Institutional Shares | | 2009 | | 2008 | | 2007 | | 2006 | | 2005 |

| |

| |

| |

| |

| |

|

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | | 12.30 | | 11.66 | | 11.68 | | 12.35 | | 12.25 |

| Investment Operations: | | | | | | | | | | |

| Investment income—neta | | .11 | | .84 | | .24 | | .29 | | .28 |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | | (.15) | | .48 | | .26 | | (.07) | | .41 |

| Total from Investment Operations | | (.04) | | 1.32 | | .50 | | .22 | | .69 |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | | (.19) | | (.68) | | (.52) | | (.75) | | (.59) |

| Dividends from net realized | | | | | | | | | | |

| gain on investments | | (.10) | | — | | — | | (.14) | | — |

| Total Distributions | | (.29) | | (.68) | | (.52) | | (.89) | | (.59) |

| Net asset value, end of period | | 11.97 | | 12.30 | | 11.66 | | 11.68 | | 12.35 |

| Total Return (%) | | (.30) | | 11.29 | | 4.47 | | 1.82 | | 5.60 |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | | .55 | | .77 | | 1.83 | | 1.63 | | 1.49 |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | | .30 | | .30 | | .28 | | .30 | | .30 |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | | .98 | | 6.68 | | 2.08 | | 2.43 | | 2.26 |

| Portfolio Turnover Rate | | 77.13 | | 90.18 | | 18.17 | | 60.82 | | 118.91 |

| Net Assets, end of period ($ x 1,000) | | 24,577 | | 13,740 | | 2,693 | | 3,463 | | 3,405 |

| |

| a Based on average shares outstanding at each month end. | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | |

The Fund 15

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Inflation Adjusted Securities Fund (the “fund”) is a separate diversified series of Dreyfus Investment Grade Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering three series, including the fund.The fund’s investment objective seeks returns that exceed the rate of inflation.The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment advisor.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares, which are sold to the public without a sales charge.The fund is authorized to issue 500 million shares of $.001 par value Common Stock in each of the following classes of shares: Investor and Institutional. Investor shares are subject to a shareholder services plan. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs, the minimum initial investment and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

As of July 31, 2009, MBC Investments Corp., an indirect subsidiary of BNY Mellon, held 204,961 Investor and 209,228 Institutional shares of the fund.

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The fund’s financial statements are prepared in accordance with U.S. generally accepted accounting principles, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

16

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: Investments in securities excluding short-term investments (other than U.S.Treasury Bills), financial futures and options are valued each business day by an independent pricing service (the “Service”) approved by the Board of Directors. Investments for which quoted bid prices are readily available and are representative of the bid side of the market in the judgment of the Service are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such securities) and asked prices (as calculated by the Service based upon its evaluation of the market for such securities). Other investments (which constitute a majority of the portfolio securities) are valued as determined by the Service, based on methods which include consideration of: yields or prices of securities of comparable quality, coupon, maturity and type; indications as to values from dealers; and general market conditions. Restricted securities, as well as securities or other assets for which recent market quotations are not readily available, that are not valued by a pricing service approved by the Board of Directors, or are determined by the fund not to reflect accurately fair value, are valued at fair value as determined in good faith under the direction of the Board of Directors. The factors that may be considered when fair valuing a security include fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold and public trading in similar securities of the issuer or comparable issuers. Short-term investments, excluding U.S. Treasury Bills, are carried at amortized cost, which approximates value. Registered investment companies that are not traded on an exchange are valued at their net asset value. Financial futures and options, which are traded on an exchange, are valued at the last sales price on the securities exchange on which such securities are primarily traded or at the last sales price on the national securities

The Fund 17

| NOTES TO FINANCIAL STATEMENTS (continued) |

market on each business day. Options traded over-the-counter are priced at the mean between the bid and asked price.

The fund adopted Statement of Financial Accounting Standards No. 157 “FairValue Measurements” (“FAS 157”). FAS 157 establishes an authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the fund’s investments relating to FAS 157.These inputs are summarized in the three broad levels listed below.

Level 1—quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of July 31, 2009 in valuing the fund’s investments:

| | | | | Level 2—Other | | Level 3— | | |

| | | Level 1— | | Significant | | Significant | | |

| | | Quoted | | Observable | | Unobservable | | |

| | | Prices | | Inputs | | Inputs | | Total |

| |

| |

| |

| |

|

| Assets ($) | | | | | | | | |

| Investments in Securities: | | | | | | |

| U.S. Treasury | | | | | | | | |

| Securities | | — | | 64,949,704 | | — | | 64,949,704 |

| Mutual Funds | | 25,899,012 | | — | | — | | 25,899,012 |

| Other Financial | | | | | | | | |

| Instruments† | | — | | — | | — | | — |

| Liabilities ($) | | | | | | | | |

| Other Financial | | | | | | | | |

| Instruments† | | — | | — | | — | | — |

† Other financial instruments include derivative instruments, such as futures, forward foreign currency

exchange contracts, swap contracts and options contracts. Amounts shown represent unrealized

appreciation (depreciation), or in the case of options, market value at period end. |

18

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

The fund has arrangements with the custodian and cash management bank whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset custody and cash management fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

Pursuant to a securities lending agreement with The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral is either in the form of cash, which can be invested in certain money market mutual funds managed by the Manager, U.S. Government and Agency securities or letters of credit.The fund is entitled to receive all income on securities loaned, in addition to income earned as a result of the lending transaction. Although each security loaned is fully collateralized, the fund bears the risk of delay in recovery of, or loss of rights in, the securities loaned should a borrower fail to return the securities in a timely manner. During the period ended July 31, 2009, The Bank of New York Mellon earned $44,445 from lending fund portfolio securities, pursuant to the securities lending agreement.

(c) Affiliated issuers: Investments in other investment companies advised by the Manager are defined as “affiliated” in the Act.

(d) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally

The Fund 19

| NOTES TO FINANCIAL STATEMENTS (continued) |

declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended July 31, 2009, the fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended July 31, 2009 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At July 31, 2009, the components of accumulated earnings on a tax basis were as follows: accumulated capital losses $47,768 and unrealized depreciation $542,013. In addition, the fund had $950,404 of capital losses realized after October 31, 2008, which were deferred for tax purposes to the first day of the following fiscal year.

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net securities profits, if any, realized subsequent to July 31, 2009. If not applied, the carryover expires in fiscal 2017.

20

The tax character of distributions paid to shareholders during the fiscal periods ended July 31, 2009 and July 31, 2008 were as follows: ordinary income $940,645 and $1,434,452, respectively.

During the period ended July 31, 2009, as a result of permanent book to tax differences, primarily due to the tax treatment for dividend reclassification, the fund increased accumulated undistributed investment income-net by $198,134, decreased accumulated net realized gain (loss) on investments by $47,168 and decreased paid-in capital by $150,966. Net assets and net asset value per share were not affected by this reclassification.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $145 million unsecured credit facility led by Citibank,N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay its pro rata portion of Facility fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of the borrowing. During the period ended July 31, 2009, the fund did not borrow under the facilities.

NOTE 3—Management Fee and Other Transactions With Affiliates:

(a) Pursuant to a management agreement (“Agreement”) with the Manager, the management fee is computed at the annual rate of .30% of the value of the fund’s average daily net assets and is payable monthly. The Manager has undertaken from August 1, 2008 through December 1, 2009, that if, the aggregate expenses of the fund (exclusive of taxes, brokerage fees, interest expense, commitment fees on borrowings,

The Fund 21

| NOTES TO FINANCIAL STATEMENTS (continued) |

shareholder services plan fees and extraordinary expenses) exceed an annual rate of .30% of the value of the fund’s average daily net assets, the fund may deduct from the payment to be made to the Manager under the Agreement, or the Manager will bear, such excess expense. The reduction in management fee, pursuant to the undertaking, amounted to $136,797 during the period ended July 31, 2009.

(b) Under the Investor Shares Shareholder Services Plan, the fund pays the Distributor at an annual rate of .25% of the value of Investor Shares average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (a securities dealer, financial institution or other industry professional) in respect of these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended July 31, 2009, Investor Shares were charged $76,734 pursuant to the Shareholder Services Plan.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency services for the fund. During the period ended July 31, 2009, the fund was charged $4,831 pursuant to the transfer agency agreement.

The fund compensates The Bank of New York Mellon under a cash management agreement for performing cash management services related to fund subscriptions and redemptions. During the period ended July 31, 2009, the fund was charged $628 pursuant to the cash management agreement. These fees were offset by earnings credits pursuant to the cash management agreement.

22

The fund also compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. During the period ended July 31, 2009, the fund was charged $7,422 pursuant to the custody agreement.

During the period ended July 31, 2009, the fund was charged $5,939 for services performed by the Chief Compliance Officer.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $16,431, shareholder services plan fees $8,571, custodian fees $2,339, chief compliance officer fees $2,227 and transfer agency per account fees $620, which are offset against an expense reimbursement currently in effect in the amount of $20,272.

(c) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales (including paydowns) of investment securities, excluding short-term securities, during the period ended July 31, 2009, amounted to $61,273,799 and $35,162,276, respectively.

The fund adopted Statement of Financial Accounting Standards No. 161 “Disclosures about Derivative Instruments and Hedging Activities” (“FAS 161”). FAS 161 requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of gains and losses on derivative instruments and disclosures about credit-risk-related contingent features in derivative

The Fund 23

| NOTES TO FINANCIAL STATEMENTS (continued) |

agreements. Since the fund held no derivatives during the period ended July 31, 2009, FAS 161 disclosures did not impact the notes to the financial statements.

At July 31, 2009, the cost of investments for federal income tax purposes was $91,390,729; accordingly, accumulated net unrealized depreciation on investments was $542,013, consisting of $311,204 gross unrealized appreciation and $853,217 gross unrealized depreciation.

NOTE 5—Subsequent Events Evaluation:

Dreyfus has evaluated the need for disclosures and/or adjustments resulting from subsequent events through September 25, 2009, the date the financial statements were available to be issued.This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments.

24

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM |

Shareholders and Board of Directors Dreyfus Inflation Adjusted Securities Fund

We have audited the accompanying statement of assets and liabilities, including the statement of investments, of Dreyfus Inflation Adjusted Securities Fund (one of the series comprising Dreyfus Investment Grade Bond Funds, Inc.) as of July 31, 2009, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and financial highlights for each of the years indicated therein.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of July 31, 2009 by correspondence with the custodian and others.We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Inflation Adjusted Securities Fund at July 31, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the indicated years, in conformity with U.S. generally accepted accounting principles.

New York, New York

September 25, 2009 |

The Fund 25

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes the fund hereby designates 100% of ordinary dividends paid during the fiscal year ended July 31, 2009 as qualifying “interest related dividends.” Also for state individual income tax purposes, the fund hereby designates 99.78% of the ordinary income dividends paid during the fiscal year ended July 31, 2009 as attributable to interest income from direct obligations of the United States. Such dividends are currently exempt from taxation for individual income tax purposes in most states, including New York, California and the District of Columbia.Also, the fund hereby designates $.0960 per share as a short-term capital gain distribution paid on December 23, 2008.

26

INFORMATION ABOUT THE REVIEW AND APPROVAL OF

THE FUND’S MANAGEMENT AGREEMENT (Unaudited) |

At a meeting of the Board of Directors of the fund held on July 14 and 15, 2009, the Board considered the re-approval for an annual period (through July 29, 2010) of the Management Agreement with Dreyfus for the fund, pursuant to which Dreyfus provides the fund with investment advisory and administrative services. The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of Dreyfus.

Analysis of Nature, Extent and Quality of Services Provided to the Fund. The Board members received a presentation from representatives of Dreyfus regarding services provided to the fund and other funds in the Dreyfus fund complex, and discussed the nature, extent and quality of the services provided to the fund pursuant to its Management Agreement. Dreyfus’ representatives reviewed the fund’s distribution of accounts and the relationships Dreyfus has with various intermediaries and the different needs of each. Dreyfus’ representatives noted the distribution channels for the fund as well as the diversity of distribution among the funds in the Dreyfus fund complex, and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each distribution channel, including those of the fund. Dreyfus also provided the number of shareholder accounts in the fund, as well as the fund’s asset size.

The Board members also considered Dreyfus’ research and portfolio management capabilities and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements. The Board members also considered Dreyfus’ extensive administrative, accounting and compliance infrastructure.The Board also considered Dreyfus’ brokerage policies and practices and the standards applied in seeking best execution.

The Fund 27

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued) |

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio. The Board members reviewed the performance of the fund’s Investor Shares and comparisons to a group of retail no-load Treasury inflation-protected securities funds (the “Performance Group”) and to a larger universe of funds, consisting of all retail and institutional Treasury inflation-protected securities funds (the “Performance Universe”) selected and provided by Lipper, Inc., an independent provider of investment company data.The Board was provided with a description of the methodology Lipper used to select the Performance Group and Performance Universe, as well as the Expense Group and Expense Universe (discussed below). The Board members discussed the results of the comparisons for various periods ended May 31, 2009.The Board members noted that the fund’s total return performance variously was above and below the Performance Group medians for the periods shown, and was above the Performance Universe medians for the periods shown. The Board members noted that the fund’s yield performance was above the Performance Group and Performance Universe medians for all periods except two. Dreyfus also provided a comparison of the fund’s total returns to the returns of the fund’s benchmark index for each of the calendar years since inception.

The Board members also discussed the fund’s management fee and expense ratio and reviewed the range of management fees and expense ratios as compared to a comparable group of funds (the “Expense Group”) and a broader group of funds (the “Expense Universe”), each selected and provided by Lipper. The Board members noted that the fund’s contractual management fee was lower than the Expense Group median, and the actual management fee (even without taking into account the reduction due to an undertaking to limit the fund’s expenses) and total expense ratio (which included the undertaking by Dreyfus to limit the fund’s expense ratio) were lower than the Expense Group and Expense Universe medians. The Board noted that the fund’s expense ratio was lower due to the undertaking by Dreyfus to waive fees and reimburse expenses.

28

Representatives of Dreyfus stated that there were no other mutual funds managed by Dreyfus or its affiliates with similar investment objectives, policies and strategies, and reviewed with the Board other accounts managed by Dreyfus or its affiliates, with similar investment objectives, policies and strategies as the fund (the “Similar Accounts”). Dreyfus representatives explained the nature of the Similar Accounts and the differences, from Dreyfus’ perspective, in providing services to such Similar Accounts as compared to managing and providing services to the fund. Dreyfus’ representatives also reviewed the costs associated with distribution through intermediaries.The Board analyzed differences in fees paid to Dreyfus and discussed the relationship of the fees paid in light of the services provided. The Board members considered the relevance of the fee information provided for the Similar Accounts to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus’ representatives reviewed the dollar amount of expenses allocated and profit received by Dreyfus and the method used to determine such expenses and profit.The Board considered information, previously provided and discussed, prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus mutual fund complex. The Board members also considered that the methodology had also been reviewed by an independent registered public accounting firm which, like the consultant, found the methodology to be reason-able.The consulting firm also analyzed where any economies of scale might emerge in connection with the management of the fund. The Board members evaluated the profitability analysis in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the benefit of fund investors.The Board

The Fund 29

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued) |

members also considered potential benefits to Dreyfus from acting as investment adviser and noted that there were no soft dollar arrangements with respect to trading the fund’s investments.

It was noted that the Board members should consider Dreyfus’ profitability with respect to the fund as part of their evaluation of whether the fees under the Management Agreement bear a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services and that a discussion of economies of scale is predicated on increasing assets and that, if a fund’s assets had been decreasing, the possibility that Dreyfus may have realized any economies of scale would be less. It also was noted that the profitability percentage for managing the fund was within ranges determined by appropriate court cases to be reasonable given the services rendered and generally superior service levels provided. The Board also noted the fee waiver and expense reimbursement arrangement and its effect on Dreyfus’ profitability.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to continuation of the Management Agreement, with respect to the fund. Based on the discussions and considerations as described above, the Board made the following conclusions and determinations.

- The Board concluded that the nature, extent and quality of the ser- vices provided by Dreyfus are adequate and appropriate.

- The Board generally was satisfied with the fund’s performance and expressed confidence in the fund’s portfolio management team, which continued to apply a consistent investment strategy.

30

- The Board concluded that the fee paid by the fund to Dreyfus was reasonable in light of the services provided, comparative performance, expense and management fee information, including Dreyfus’ under- taking to limit the fund’s expense ratio (which reduced the fund’s actual management fee and expense ratio), costs of the services pro- vided and profits to be realized and benefits derived or to be derived by Dreyfus from its relationship with the fund.

- The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the manage- ment of the fund had been adequately considered by Dreyfus in connection with the management fee rate charged to the fund and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

The Board members considered these conclusions and determinations, along with information received on a routine and regular basis throughout the year, and, without any one factor being dispositive, the Board determined that re-approval of the Management Agreement,with respect to the fund, was in the best interests of the fund and its shareholders.

The Fund 31

32

The Fund 33

34

The Fund 35

NOTES

For More Information

Telephone 1-800-645-6561

Mail The Dreyfus Family of Funds, 144 Glenn Curtiss Boulevard, Uniondale, NY 11556-0144 E-mail Send your request to info@dreyfus.com Internet Information can be viewed online or downloaded at: http://www.dreyfus.com

The fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The fund’s Forms N-Q are available on the SEC’s website at http://www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the fund uses to determine how to vote proxies relating to portfolio securities, and information regarding how the fund voted these proxies for the most recent 12-month period ended June 30 is available at http://www.dreyfus.com and on the SEC’s website at http://www.sec.gov. The description of the policies and procedures is also available without charge, upon request, by calling 1-800-645-6561.

| © 2009 MBSC Securities Corporation |

| | Dreyfus

Intermediate

Term Income Fund |

| | ANNUAL REPORT July 31, 2009 |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

| | | Contents |

| |

| |

| | | THE FUND |

| |

|

| 2 | | A Letter from the Chairman and CEO |

| 3 | | Discussion of Fund Performance |

| 6 | | Fund Performance |

| 8 | | Understanding Your Fund’s Expenses |

| 8 | | Comparing Your Fund’s Expenses |

| | | With Those of Other Funds |

| 9 | | Statement of Investments |

| 37 | | Statement of Financial Futures |

| 38 | | Statement of Options Written |

| 39 | | Statement of Assets and Liabilities |

| 40 | | Statement of Operations |

| 41 | | Statement of Changes in Net Assets |

| 43 | | Financial Highlights |

| 47 | | Notes to Financial Statements |

| 68 | | Report of Independent Registered |

| | | Public Accounting Firm |

| 69 | | Important Tax Information |

| 70 | | Information About the Review and Approval |

| | | of the Fund’s Management Agreement |

| 75 | | Board Members Information |

| 77 | | Officers of the Fund |

| |

| | | FOR MORE INFORMATION |

| |

|

| | | Back Cover |

Dreyfus

Intermediate

Term Income Fund |

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Intermediate Term Income Fund, covering the 12-month period from August 1, 2008, through July 31, 2009.

The severe recession and banking crisis that dominated the financial markets over much of the past year appear to have eased. Previously frozen credit markets have thawed to an extent, giving businesses improved access to the capital they need to grow. After reaching multi-year lows early in 2009, higher-yielding segments of the bond market staged an impressive rally, while U.S.Treasury securities have experienced significant price volatility since January as a result of recession-related factors and technical supply issues.The U.S. economy remains weak overall, but we have seen encouraging evidence of potential recovery, including signs of healing in the battered housing and manufacturing sectors. Even the unemployment rate, which historically has been a lagging indicator of economic trends, recently showed signs of improvement.

Although these developments give us reasons for optimism, we remain cautious due to the speed and magnitude of the corporate bond market’s 2009 rebound. Indeed, the market’s advance was fueled more by investors’ renewed appetites for risk than improving business fundamentals. We would prefer to see a steadier rise in asset prices supported by more concrete economic data, as the rapid rise increases the possibility that profit-taking could fuel further volatility. In uncertain markets such as this one,even the most seasoned investors can benefit from professional counsel. To determine how your investments should be positioned for any potential challenges and opportunities that lie ahead, we urge you, as always, to talk regularly with your financial advisor.

For information about how the fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance given by the fund’s Portfolio Manager.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

August 17, 2009 |

2

DISCUSSION OF FUND PERFORMANCE

For the period of August 1, 2008, through July 31, 2009, as provided by Kent Wosepka, Portfolio Manager

Fund and Market Performance Overview

For the 12-month period ended July 31, 2009, Dreyfus Intermediate Term Income Fund’s Class A shares produced a total return of 4.90%, Class B shares returned 3.95%, Class C shares returned 4.01% and Class I shares returned 5.27%.1 In comparison, the fund’s benchmark, the Barclays Capital U.S. Aggregate Bond Index, achieved a total return of 7.85% for the same period.2

The U.S. bond market encountered extreme volatility in the fall of 2008 due to a global financial crisis and recession, but market declines early in the reporting period were offset by a sustained rally in 2009. The fund produced lower returns than its benchmark, as better relative performance during the rally was not enough to fully offset earlier weakness among corporate bonds and mortgage-backed securities.

The Fund’s Investment Approach

The fund seeks to maximize total return, consisting of capital appreciation and current income.To pursue this goal, the fund normally invests at least 80% of its assets in fixed-income securities of U.S. and foreign issuers rated at least investment grade or the unrated equivalent as determined by Dreyfus.These securities include:U.S.government bonds and notes, corporate bonds, municipal bonds, convertible securities, preferred stocks, inflation-indexed securities, asset-backed securities, mortgage-related securities and foreign bonds.Typically, the fund can be expected to have an average effective maturity ranging from five to 10 years, and an average effective duration ranging between three and eight years. For additional yield, the fund may invest up to 20% of its assets in fixed-income securities rated below investment grade.

2009 Market Rally Erased Earlier Losses

The reporting period began in the midst of a global banking crisis that produced steep declines among higher yielding bonds, including mortgage-backed, asset-backed and corporate securities. In contrast, U.S. Treasury securities rallied strongly amid a “flight to quality,” causing

The Fund 3

| DISCUSSION OF FUND PERFORMANCE (continued) |

their yields to fall to unprecedented low levels. Meanwhile, slumping housing markets, rising unemployment and deteriorating consumer confidence led to the longest and deepest recession since the 1930s.

The Federal Reserve Board (the “Fed”) and U.S. government responded aggressively to the downturn. Government officials rescued a number of struggling corporations, and Congress followed up with the $787 billion American Recovery and Reinvestment Act of 2009.The Fed injected massive amounts of liquidity into the banking system and purchased mortgage- and asset-backed debt through unprecedented programs such as the Term Asset-Backed Securities Loan Facility (TALF). In addition, the Fed completed a series of interest-rate reductions by cutting its target range for the overnight federal funds rate to an all-time low of between 0% to 0.25% by the end of 2008.

As it became clearer in March 2009 that these measures had helped to avert a collapse of the U.S. banking system, investor sentiment began to improve to an extent. Investors capitalized on attractive valuations among higher yielding bonds, sparking springtime rallies that were particularly impressive for investment-grade and high yield corporate bonds. Mortgage-backed securities also rebounded, in part due to massive purchases by the Fed. Conversely, U.S. Treasury securities gave back some of their earlier gains.

Sector Allocation Strategy Produced Mixed Results

The fund began the reporting period with underweighted exposure to U.S. Treasury securities and overweight positions in higher yielding market sectors, including investment-grade corporate bonds and higher-quality mortgage-backed securities. These positions bore the brunt of selling pressure in 2008 as investors deleveraged their portfolios.Although the fund’s investment-grade corporate bond holdings were broadly diversified across industry groups, weakness was especially pronounced among bonds issued by financial companies at the center of the banking crisis.

However, these higher yielding positions led the 2009 market rally. Investment-grade corporate bonds with BBB ratings fared particularly well, while our focus on current-coupon mortgage-backed securities issued by U.S. government agencies benefited from the Fed’s repurchase programs. As they reached more attractive valuations toward year-end 2008, we established larger positions in the fund of

4

commercial mortgages and asset-backed securities, as well as high yield corporate bonds, which are not part of the benchmark but ranked among the market’s better performers over the final five months of the reporting period. At that time, we also set the fund’s average duration in a range that was longer than industry averages, a position that bolstered the fund’s relative performance as intermediate- and longer-term bond yields declined.We subsequently reduced the fund’s average duration toward a market-neutral position.

Maintaining a Disciplined Approach to Security Selection

As of the reporting period’s end, we have maintained the fund’s sector allocation strategy, as we believe that higher yielding bonds have room for further gains. However, we are aware that the bulk of the bond market rally probably is behind us, and we expect the Fed to pare back its remedial programs as the credit markets and U.S. economy recover. Therefore, we believe that security selection will become a more critical determinant of fund performance over the foreseeable future, an environment to which our relative value-oriented approach may be particularly well suited.

August 17, 2009

| | The fund may use derivative instruments, such as options, futures and options on futures, forward

contracts, swaps (including credit default swaps on corporate bonds and asset-backed securities),

options on swaps, and other credit derivatives.A small investment in derivatives could have a

potentially large impact on the fund’s performance.The use of derivatives involves risks different

from, or possibly greater than, the risks associated with investing directly in the underlying assets.

Credit default swaps and similar instruments involve greater risks than if the fund had invested in

the reference obligation directly, since, in addition to general market risks, they are subject to

illiquidity risk, counterparty risk and credit risks. |

| 1 | Total return includes reinvestment of dividends and any capital gains paid, and does not take into consideration the maximum initial sales charge in the case of Class A shares, or the applicable contingent deferred sales charges imposed on redemptions in the case of Class B and Class C shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figure provided for the fund’s Class A shares and Class I shares reflects the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an undertaking in effect through December 31, 2009, at which time it may be extended, terminated or modified. Had these expenses not been absorbed, the fund’s Class A and Class I shares’ returns would have been lower. |

| |

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital gain distributions. The Barclays Capital U. S. Aggregate Bond Index is a widely accepted, unmanaged total return index of corporate, U. S. government and U. S. government agency debt instruments, mortgage-backed securities and asset-backed securities with an average maturity of 1-10 years. |

| |

The Fund 5

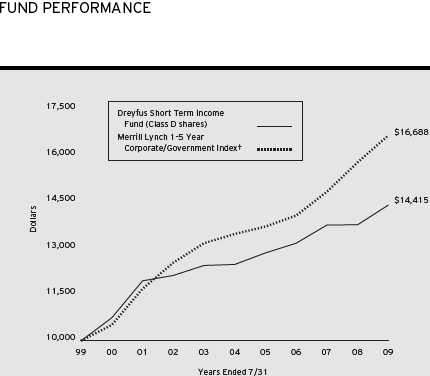

| | † Source: Lipper Inc.

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not

reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The above graph compares a $10,000 investment made in Class A shares of Dreyfus Intermediate Term Income Fund

on 7/31/99 to a $10,000 investment made in the Barclays Capital U.S.Aggregate Index (the “Index”) on that date.

All dividends and capital gain distributions are reinvested. Performance for Class B, Class C and Class I shares will

vary from the performance of Class A shares shown above due to differences in charges and expenses.

The fund invests primarily in debt securities and securities with debt-like characteristics of domestic and foreign issuers

and maintains an average effective maturity ranging between five and ten years and an average effective duration ranging

between three and eight years.The fund’s performance shown in the line graph takes into account all applicable fees and

expenses.The Index is a widely accepted, unmanaged total return index of corporate, U.S. government and U.S.

government agency debt instruments, mortgage-backed securities and asset-backed securities with an average maturity of

1-10 years. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest

directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is

contained in the Financial Highlights section of the prospectus and elsewhere in this report. |

6

| Average Annual Total Returns as of 7/31/09 | | | | | | | | |

| |

| | | Inception | | | | | | | | | | From |

| | | Date | | 1 Year | | 5 Years | | 10 Years | | Inception |

| |

| |

| |

| |

| |

|

| Class A shares | | | | | | | | | | | | |

| with maximum sales charge (4.5%) | | 2/2/96 | | 0.15% | | 3.17% | | 5.03% | | | | — |

| without sales charge | | 2/2/96 | | 4.90% | | 4.12% | | 5.51% | | | | — |

| Class B shares | | | | | | | | | | | | |

| with applicable redemption charge † | | 5/13/08 | | –0.04% | | 3.58%††† | | 5.51%†††,†††† | | — |

| without redemption | | 5/13/08 | | 3.95% | | 3.91%††† | | 5.51%†††,†††† | | — |

| Class C shares | | | | | | | | | | | | |

| with applicable redemption charge †† | | 5/13/08 | | 3.01% | | 3.91%††† | | 5.41%††† | | — |

| without redemption | | 5/13/08 | | 4.01% | | 3.91%††† | | 5.41%††† | | — |

| Class I shares | | 5/31/01 | | 5.27% | | 4.40% | | — | | | | 4.63% |

The Fund 7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Intermediate Term Income Fund from February 1, 2009 to July 31, 2009. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment assuming actual returns for the six months ended July 31, 2009

| | | Class A | | Class B | | Class C | | Class I |

| |

| |

| |

| |

|

| Expenses paid per $1,000† | | $ 4.34 | | $ 8.88 | | $ 8.98 | | $ 2.78 |

| Ending value (after expenses) | | $1,110.70 | | $1,105.60 | | $1,105.90 | | $1,112.20 |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment assuming a hypothetical 5% annualized return for the six months ended July 31, 2009

| | | Class A | | Class B | | Class C | | Class I |

| |

| |