UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-01976

Sequoia Fund, Inc.

(Exact name of registrant as specified in charter)

9 West 57th Street, Suite 5000

New York, NY 10019

(Address of principal executive offices) (Zip code)

John B. Harris

Ruane, Cunniff & Goldfarb L.P.

9 West 57th Street

Suite 5000

New York, NY 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)686-6884

Date of fiscal year end: December 31, 2019

Date of reporting period: December 31, 2019

Item 1. Reports to Stockholders.

Report to Stockholders

ANNUAL REPORT

DECEMBER 31, 2019

Beginning on February 12, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Fund’s website (www.sequoiafund.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically through your financial intermediary, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically at any time by contacting your financial intermediary.

You may elect to receive all future reports in paper form free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you may inform the Fund that you wish to continue to receive paper copies of your shareholder reports by calling1-800-686-6884.

| | |

| |

Sequoia Fund | | December 31, 2019 |

| | |

| |

Sequoia Fund | | December 31, 2019 |

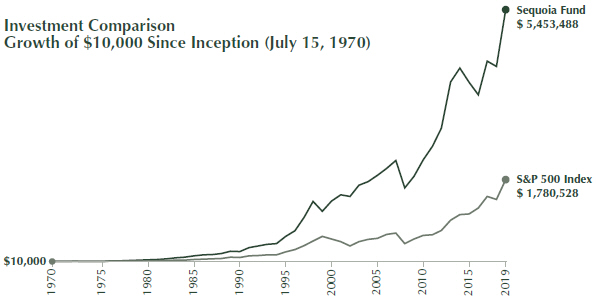

Illustration of an Assumed Investment of $10,000 (Unaudited)

The graph below covers the period from July 15, 1970 (the date Sequoia Fund, Inc. (the ”Fund“) shares were first offered to the public) through December 31, 2019.

Sequoia Fund’s results as of December 31, 2019 appear below with results of the S&P 500 Index for the same periods:

| | | | | | |

Year ended December 31, 2019 | | Sequoia Fund | | S&P 500 Index* | | |

1 Year | | 29.12% | | 31.49% | | |

5 Years (Annualized) | | 5.43% | | 11.70% | | |

10 Years (Annualized) | | 11.43% | | 13.56% | | |

Since inception (Annualized)** | | 13.59% | | 11.05% | | |

The results shown in the graph and table, which assume reinvestment of distributions, represent past performance and do not guarantee future results. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance shown. Investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

*The S&P 500 Index is an unmanaged, capitalization-weighted index of the common stocks of 500 major U.S. corporations. The Index does not incur expenses. It is not possible to invest directly in the Index.

**Inception Date: July 15, 1970.

|

| |

Please consider the investment objectives, risks and charges and expenses of the Fund carefully before investing. The Fund’s prospectus and summary prospectus contain this and other information about the Fund. You may obtain year to date performance as of the most recent quarter end, and copies of the prospectus and summary prospectus, by calling1-800-686-6884, or on the Fund’s website at www.sequoiafund.com. Please read the prospectus and summary prospectus carefully before investing. |

Shares of the Fund are distributed by Foreside Financial Services, LLC (Member of FINRA). An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. |

3

| | |

| |

Sequoia Fund | | December 31, 2019 |

Shareholder Letter

Dear Shareholder:

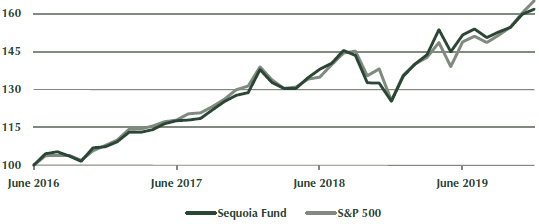

Since June 2016, the team presently managing the Fund has overseen a cumulative total return of 62%— nearly identical to the 65% return of the S&P 500. While we remain pleased that the Fund has kept up with a strong market during a challenging period for anyone who purports to invest with discipline, we remain equally frustrated that we seem to be running what has to be the world’s most unusual index fund.

Our portfolio contains 24 stocks, ten of which account for nearly 60% of net assets. It looks almost nothing like an Index that includes 500 stocks, the ten largest of which comprise nearly 25% of total value. Last year, we joked that none of us went far enough in math to calculate the odds of two such remarkably different vehicles advancing at such a similar speed for such a long period— except that we knew they were low. This year, having spent another twelve months tethered to the Index by an improbably short leash, we dusted off old textbooks in hopes of satisfying our curiosity with some precision. A mere 100,000 Monte Carlo simulations later, we learned that over three consecutiveone-year periods, the chances are less than 1 in 100 that a randomly-generated portfolio exhibiting Sequoia’s statistical characteristics would earn consecutive annual returns within two percentage points of the Index return. It’s surely even less likely that the Fund’s monthly movements would be as indistinguishable from those of the Index as they appear in the chart below.

Sequoia Fund vs. the S&P 500

Cumulative total return from June 30, 2016 through December 31, 2019, indexed to 100

Though our crystal ball is no more accurate than yours, we are certain that this pattern will not persist indefinitely. At some point, the Fund’s performance will diverge markedly from that of the broader market. Because we continue to find the quality, growth prospects and valuation of our holdings much more appealing than that of the 500 stocks that comprise the Index— an entity that by its very nature is meant to define “average”— we look forward to a future of much-increased tracking error.

In the meantime, while much is written these days about how the investing landscape has changed, we emphatically reject the notion that trends like indexing, increased competition or the ascendancy of “growth” stocks versus “value” stocks have diminished the potential for a value-oriented fund manager to outperform. The core philosophy that guides our decisions is the same one that has enabled Sequoia to beat the market by roughly 2.5 percentage points per annum over nearly fifty years, and by a similar margin over the last twenty years. We believe this approach has maintained its effectiveness across changing market environments, economic circumstances, political trends and generations of leadership because it is rooted in a set of principles that are timeless. The first is that most businesses— regardless of what they do or how fast they grow— have a value that can be estimated within a range of reasonableness. The second is that while the stock market does a generally good job of assessing value over the long term, it can make egregious mistakes over the short term.

The idea that a bigger, faster and more competitive market is not necessarily a more efficient one should be obvious to anyone who lived through Black Monday in 1987...or the bursting of thedot-com bubble from 2000 to 2002...or the financial crisis in 2008 and 2009...or the more recentnear-20% intra-year plunges that accompanied the EU mini-crisis in 2011, the collapse of the oil price in late 2015 and the fears surrounding (modest) interest rate increases that emerged in late 2018. Beyond these broad market movements, 2019 alone saw the stock prices of twenty S&P 500 constituents change by 75% or more, with another 55 moving more than 50%. We wonder: Did the intrinsic value of 75 of the country’s largest companies really change so drastically over the course of a single, relatively benign year? And is Apple, the very definition of a mature business— with revenues that actually shrank during its last fiscal year— really worth twice as much today as it was twelve months ago?

While these and many other examples indicate that the stock market is every bit as fallible as it has always been, we know from experience that exploiting its shortcomings with some degree of consistency over long periods of time is by no means easy. To maintain your edge in a world of relentless competition and incessant— if not accelerating— change, you have to constantly adapt and improve.

Forty years ago, if you understood the difference between a business and a stock and were temperamentally capable of a certain degree of patience, then armed with a working telephone and a newspaper subscription, you stood a very good chance of outrunning Mr. Market.

4

| | |

| |

Sequoia Fund | | December 31, 2019 |

Shareholder Letter (Continued)

If you also had a willingness to do some extra homework and an appreciation for the fact that reality is sometimes more nuanced than a spreadsheet, you could leave him in your dust. Today, similar success requires more effort. An army of finance professors, behavioral economists and practitioners like us have documented Mr. Market’s foibles extensively. Many professional investors do the kind of homework we have long done, and if you don’t want to do it yourself, you can now essentially hire outsiders to do it for you. Indexing has caused stocks to move more in tandem, making the cadence of opportunity more episodic and less idiosyncratic. While it may still be possible to beat the market in this more challenging environment with nothing more than an even keel and a few useful rules of thumb, the odds of succeeding on a shoestring are a lot longer than they used to be. Sustained outperformance increasingly demands that you attract and retain outstanding talent, equip it with the resources of a first-rate think tank and surround it with a culture that celebrates and enables creativity, curiosity, intellectual diversity, rigorous debate and unbiased judgment.

If this sounds like dispiriting news, it really shouldn’t. It’s just the way of the world. Think of the time, effort and money it takes to support success in today’s sports world. Baseball teams assemble their rosters using statistical techniques that would probably leave Joe DiMaggio scratching his head and scrutinize the physics of their hitters’ swings with a precision that would surely make Babe Ruth laugh. Standout athletes now surround themselves with such elaborate retinues of trainers, nutritionists, psychologists, agents and consultants that they routinely celebrate victories by thanking their “team.” They enlist all of this assistance because they’re playing much tougher games than their predecessors did. But modern marvels like Roger Federer, Tiger Woods, Mikaela Shiffrin, Michael Phelps or Tom Brady’s Patriots have been every bit as dominant relative to their peers as the greats of the past. The increased demands of competition have not pulled them toward mediocrity because they have adapted to change. Business is no different: the beauty of our relentlessly competitive free market system is that it forces its participants to constantly raise the level of their game.

This is why our team, process and holdings all look very different than they did twenty years ago— and why the Ruane Cunniff of 1999 looked very different than the firm that Bill and Rick started in 1970. In the Fund’s earliest days, our predecessors confined themselves mainly to buying the country’s great consumer franchises for single-digit multiples of their earnings. Twenty years ago, sensible as it was at the time, a quarter of our capital was invested in two financial institutions that performed wonderfully for us...but would essentially go bankrupt within a decade. Today, over 40% of our capital is invested in outstanding technology companies of various types. Tomorrow, the picture will probably look very different than it does today. We certainly hope so, because standing still as the world advances is no less dangerous now than it would have been in the past.

However the future unfolds, we will always evaluate stocks as stakes in businesses rather than symbols that blink on a screen. We will always believe that you can only make predictions about the prospects of a company if you are willing to own it for years rather than days— and that it’s hard to make long-term predictions about any business that doesn’t have competitive advantages and capable management. We will always hold fast to the conviction that the single most important driver of investment success is the discipline of buying stocks at prices that incorporate a margin of safety relative to the conservatively estimated value of the businesses that they represent. These philosophical underpinnings of our approach won’t change because they’re a tool for exploiting common biases that don’t change. Millions of years of evolution have hardwired them into the human psyche.

But if we want to maintain our competitive edge in a dynamic world, the way we apply our core principles must constantly evolve. Our circle of competence must expand to encompass new industries and business models. Our research engine must adjust to a world in which commerce is increasingly global, Instagram follower counts can sometimes matter as much as same-store sales growth and algorithms leveraging an explosion of new “alternative” datasets can spot business trends with greater speed and accuracy than any human analyst. The process by which we make our judgments must become ever more sensitive to the presence of potential “value traps” in a world where rapid change, volatile politics and extreme monetary conditions make the evaluation of risk and return more nuanced and complex than ever.

In spite of the frustrating three-plus years we have now spent masquerading as an index fund, we believe the flexible mindset that has defined our history remains alive and well, which is why we also believe that the Fund’s prospects for outperformance are as bright as they’ve ever been. Time will of course tell if our optimism is well founded, but even if it isn’t, the good news is that we’ve hedged our bets by taking one evolutionary step that the Fund has been far too slow to embrace: running more fully invested. Sequoia’s cash balance has averaged 20% of its net assets since inception and 14% over the last twenty years. The comparable figure today is less than 3% of net assets. If we keep it that way, we can do as well as we always have even if the stocks we select don’t beat the market by as wide a margin as they once did. Our admittedly ambitious goal, however, is to generate as much “alpha” as ever with our stock-picking and then amplify its impact by carrying as little cash as is prudently possible.

To anticipate a question, we aren’t sure whether a more fully invested posture will alter the Fund’s record of strong outperformance in weak markets. The answer will ultimately depend on which companies we own when trouble surfaces. What we know for sure is that we would gladly trade worse performance in bear markets for better performance over full cycles. Over the last twenty years, anon-taxable Sequoia investor has earned 54% more money than a comparable investor in an S&P 500 index fund. Had Sequoia’s cash position during this period averaged 5% of net assets rather than 14%, the investor would have earned over 80%. On a $1 million initial investment, that adds up to nearly $1 million of extra profit— a destination that to our eyes is well worth a bumpier voyage.

• • • • • • • • • •

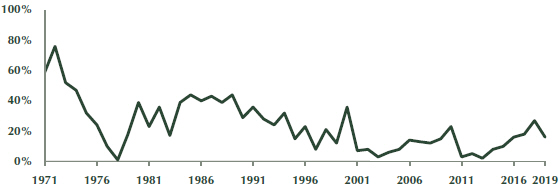

As we expected going into the year, and as indicated by the chart below, the portfolio experienced less change during 2019 than it had over the preceding few years. Turnover was 16%, well below the Fund’s 24% average annual turnover since inception. We continue to believe that our long average holding period makes Sequoia one of the mosttax-efficient investment vehicles of its kind.

5

| | |

| |

Sequoia Fund | | December 31, 2019 |

Shareholder Letter (Continued)

Sequoia Fund Annual Turnover

By industry convention, turnover is expressed as either total purchases or total sales— whichever is lower— divided by average Fund net assets

Our best guess— and it’s nothing more than a guess— is that turnover should remain subdued for a while. Natural market fluctuations always seem to surface a few chances each year to evolve the portfolio in ways that enhance its quality, growth potential and valuation, but by and large, we like what we own. That said, we are both willing and able to react if changed circumstances create broader opportunity.

This is a meatier statement than it might seem, for two reasons. First, as already mentioned, while we don’t think that the trend toward passive investing has made it harder to beat the market, we do think it has increased correlations, creating a dynamic whereby Mr. Market tends to offer opportunity in bunches rather than single servings. Historically, we have done a better job of reacting to item sales than storewide discounts, so to speak. If the latter become the more prevalent producer of investment bargains, we will have to adapt our process and mindset to allow for greater agility. We believe that we have, but we need to prove it during the next generalized downturn.

Even if you’re emotionally prepared to seize bargains by the case rather than the can, you have to be able to act when opportunity emerges. Flexibility comes naturally when you carry lots of cash, but it requires attention when you run more fully invested. To maintain optionality in the portfolio without paying the high cost of holding cash in a world where cash earns next to nothing, we keep an eye on both the liquidity and economic sensitivity of our holdings. While more liquid, less cyclical investments will not shield you from losses in a down market the way cash will, they do afford you the same potentially valuable flexibility to capitalize on opportunity because they give you the ability to swap moderately attractive investments for outstanding ones. We like that many of our large holdings would be easy to sell in an unsettled environment, and we think a significant subset of them are likely to hold up better in a downturn than the stocks of many other businesses on our shopping list.

We should also note, however, that we like less liquid holdings such as Credit Acceptance and Hiscox every bit as much as more easily marketable positions like Alphabet and Berkshire. We would be happy to have more of them in the portfolio, but only if we felt that in exchange for reduced flexibility, we were getting appropriately compensated in the form of business quality and valuation.

• • • • • • • • • •

Notable positive contributors during 2019 included Eurofins Scientific, Facebook, Jacobs, Liberty Broadband, Mastercard, and Melrose, all of which returned more than 50% for the year. a2Milk, Carmax, Constellation Software and Formula One advanced more than 35%. Alphabet, Amazon, Berkshire, Booking, Credit Acceptance, Naspers/Prosus, Schwab and Vivendi made gains but trailed the S&P. Decliners for the year were Hiscox, Rolls-Royce and Wayfair.

Much more importantly, business progress was encouraging across virtually all of our investees. Carmax took important steps to expand its omni-channel initiatives. Jacobs made major advances migrating its business mix from lower-value construction to higher-value outsourced services. Schwab agreed to a landmark acquisition that will further consolidate its powerful position in the brokerage and investment advisory industry. Formula One continued its journey toward a new set of rules that should eventually make its product more competitive and thus more valuable to advertisers, media partners and race organizers. Mastercard, Liberty Broadband and Vivendi continued to exploit secular trends in favor of electronic commerce and media streaming, and it was largely business as usual at Berkshire, Constellation and Melrose, our capital allocator-driven conglomerates. a2Milk logged another year of torrid growth at fantastic profit margins, though we were dismayed to see CEO Jayne Hrdlicka leave the business late in the year and will be paying close attention to both the selection of her successor and the broader dynamic of interaction between the company’s board and management.

Internet platforms Alphabet, Facebook, Amazon and Tencent (via Naspers/Prosus) all reported largely excellent financial results, although the regulatory clouds gathering above them are growing larger and darker. We are watching the weather here closely, but for the moment, we think the stock market has done a reasonably good job of accounting for it. Our working assumption is that both regulatory developments and proactive initiatives are likely to alter the big platforms’ business models in ways that diminish future earning power in furtherance of achieving a better balance of stakeholder interests. As long-term investors concerned as much with the sustainability as the trajectory of future financial performance, we would welcome these kinds of changes. Even if they depress profits, we’re not so sure they will negatively

6

| | |

| |

Sequoia Fund | | December 31, 2019 |

Shareholder Letter (Continued)

impact the companies’ share prices, which we think would be higher today in the absence of understandable regulatory concerns. These are some of the best businesses the world has ever seen, capable of remarkable growth at unprecedented scale— in no small part because they provide enormous value to billions of users. If they properly address legitimate stakeholder complaints that they arguably ignored during their adolescence, we think they have the potential to mature into even more valuable enterprises than they are today.

Rolls-Royce is our other long-term holding fighting through difficult weather. It has become abundantly clear over the last year that as they developed their latest generation of products, both the airplane manufacturers and their engine suppliers pushed the technological envelope too far. For Rolls, the consequences have involved enormous cost and distraction. We are cautiously optimistic that the company has finally gotten its arms around the particularly acute problems that have plagued the engine it developed for the Boeing 787. Crucially, the Airbus A350 engine that will become the preponderant driver of earnings growth over the next two decades appears to be performing well during its early time “on wing.” If787-related remediation expenses abate as expected over the next18-24 months, and if A350 engine performance stays healthy, Rolls should have a very strong period of cash earnings growth ahead of it and today’s stock price should look very attractive in a few years. We are the first to acknowledge, however, that every time the sun has broken through the clouds during our long and frustrating involvement here, new storms have rolled in.

Though well over a decade of painful memories are hard to ignore, we have tried to keep our extensively researched analysis of Rolls fact-based and forward-looking, and an encouraging view from that perspective led us to modestly increase our position during 2019. While Rolls was the only existing holding to which we added materially during the year, we trimmed several, including Alphabet, Amazon, Berkshire, Booking, Carmax, Constellation, Formula One, Jacobs, Liberty Broadband and Mastercard— all on account of valuation, position sizing or some combination thereof. As discussed in previous letters, we sold the entirety of our positions in Electronic Arts and Vopak due to changes in our fundamental assessments. We also sold the last of our roughly twenty-year investment in Mohawk, largely in response to shifts in the structure of flooring industry demand that we have discussed previously.

• • • • • • • • • •

2019 turned out to be a productive year for new investments, which included Arista Networks, Eurofins Scientific, Wayfair and two additional companies that will remain undisclosed until we are able to establish full positions. This bumper crop certainly reflects some blind luck— a year only means so much when you buy as infrequently as we do— but we also see it as an encouraging indication of the creativity and vitality of our team and research process.

Arista designs network switches, routers and associated software that play a critical role in the internet infrastructure of large enterprises, and especially “cloud titans” such as Microsoft, Facebook and Amazon. Run by one of the more impressive management teams we have encountered, Arista essentially stole a march on incumbent leader Cisco at the high end of the market by combining innovative software with exceptional execution. Extremely high customer concentration— the company calls its big accounts “titans” for a reason— can make this a volatile business over the short term, which is why we were able to buy our stake after admiring Arista for many years. Over the long term, we expect continued adoption of cloud services, media streaming andAI-driven “hyperscale” computing to drive strong demand for Arista’s products and ultimately attractive earnings growth relative to the price we paid for our shares. We also expect the company to maintain its competitive advantage in its core high-speed switching markets while it continues a nascent push into corporate datacenters and campus networks.

Eurofins is a global provider of testing, inspection and certification services in areas ranging from food safety to environmental monitoring to pharmaceutical manufacturing. Like Constellation Software, the company is run by a founder with a gift for allocating capital within an industry that exhibits an appealing mix of resilient demand, steady growth, sticky customer relationships and a relatively low sensitivity to pricing. Founder and CEO Gilles Martin has compiled one of the most impressive records of value creation in recent corporate history by consolidating a fragmented market wherein scale yields manifold advantages.

Martin and his family still own more than a third of Eurofins’ outstanding shares, and he has tended in the past to run Eurofins like the family business it once was. This has drawn criticism from a handful of analysts who claim, sometimes fairly, that Eurofins let the development of its corporate governance practices lag the torrid growth of its operations. The company has proactively addressed the most substantive of these criticisms over the past year, and exhaustive research has convinced us that Mr. Market’s remaining concerns are focused much more on style than substance. Timely purchases during a recent period of particularly acute skepticism have netted us a gain of about 40% thus far. Though the valuation of the company is less attractive today than when we invested, we think observers may still underappreciate how much more profitable and professional Eurofins could become as it matures.

Because it makes large losses competinghead-on with Amazon, Wayfair is an even more controversial company than Eurofins. Also like Eurofins, it’s a business we researched for years before recently exploiting a period of heightened investor anxiety in order to buy a stake at what we think was an attractive price. Only a year ago, an adoring Mr. Market seemed to have anointed Wayfair the undisputed king of online home furnishings retail, with near-unlimited potential in a massive category featuring as much as a half-trillion dollars of annual sales that have historically come at healthy margins. Today, with ballooning losses tied to ambitious simultaneous investments in logistics, selection and geographic expansion, the crown appears broken and the predominant narrative questions whether the company will ever be able to build a profitable franchise competing with Amazon in a commoditizing category.

While we think management should have paced its recent investments more modestly, we also think they were strategically wise, and importantly, we expect their cost to reduce significantly in coming quarters. Though reality is a bit more complicated, the idea here is that by and large, you can only build a national logistics footprint once, you can only expand your assortment to cover all categories of home furnishings once and you can also only build the overhead required to support European expansion once. The company’s decision to take on all three of these mostly finite tasks at the same time has had the effect of obscuring unit economics that we see as fundamentally

7

| | |

| |

Sequoia Fund | | December 31, 2019 |

Shareholder Letter (Continued)

sound. If we’re correct, then as sales continue to grow and the company “laps” this recent period of unusually elevated investment, cash flow dynamics should improve rapidly, potentially inducing another, more optimistic swing in Mr. Market’s mood.

While 2020 will be an important year in which a team we respect needs to deliver on its commitments and get back to living within its means, we don’t see why Amazon and Wayfair can’t both be long-term winners in a segment that is one of the largest and most profitable in all of mass retail. Crucially, it is also a segment in which the average consumer cares as much or more about browsing an endless selection and getting inspired about how to decorate a space as she does about buying a specific product at the lowest possible price and getting it delivered as quickly and conveniently as possible. Or to put it more simply, most people don’t want to decorate their homes in the same way— or at the same places— that they buy their laundry detergent. This is why many offline “category killers,” both regional and national, have thrived for decades in home furnishings, and why we think Amazon is about as likely to “own” home furnishings online as Walmart and Target are offline.

We like that Wayfair has already achieved a degree of scale and scope in the online world that vastly exceeds what any existing category specialists have achieved in the offline world. We also like that the network effects inherent in the company’s marketplace business model should enable it to offer a breadth of selection and quality of user experience that competitors will struggle to match. Though Wayfair is already orders of magnitude larger than its offline counterparts, if it can eventually earn a fraction of the profit margin that they have earned for years, we will have paid less than twenty times potentialafter-tax earning power for a dominant category leader that could grow enormously over the next decade.

• • • • • • • • • •

Though we will continue making incremental improvements in coming years because anything done well can always be done better, we marked the conclusion of our three-year business modernization project at the end of last summer with the closure of our affiliated broker-dealer and the completion of a conversion to a new custody platform for our managed account clients. Beyond these recent steps, since 2016 we have welcomed a new COO, CFO and head of business development; implemented new IT systems for order allocation, trade reconciliation and portfolio accounting; architected new processes for managing movements of cash and securities; unveiled new client reporting tools and templates; built a new website; completed an extensive data cleansing exercise; overhauled our entity structure and recapitalized our ownership. It is hard to overstate how much effort our business team invested into this massive, multifaceted undertaking. It is also hardly a surprise. Any longtime Ruane Cunniff client understands that above and beyond is our business team’s definition of business as usual.

Our investment team, which now numbers nearly thirty, is larger and more capable than ever. A big reason why is the growth and maturation of our impressive next generation of talent, exemplified in many ways by our longtime colleague Will Pan, whose humility, insight and wisdom belie his age. We are happy to announce that Will was elected our ninth employee partner at the end of last year.

Our annual Investor Day will take place on Friday, May 15, 2020 in the Grand Ballroom of the Plaza Hotel in New York City, the same venue as last year. We are both humbled and excited to report that in addition to our usual program, this year we will be celebrating Sequoia Fund’s 50th anniversary. We will have more to say about this milestone in coming months. As it approaches, and as we ponder its significance, we find ourselves ever more appreciative of the fact that no constituency is more responsible for enabling Ruane Cunniff’s longevity and success than our truly extraordinary family of clients. We send you all our very warmest wishes for a happy, healthy and successful new year.

Sincerely,

The Ruane, Cunniff & Goldfarb Investment Committee,

| | | | | | |

| |

| |

| |

|

| | | |

Arman Gokgol-Kline | | John B. Harris | | Trevor Magyar | | D. Chase Sheridan |

January 22, 2020

8

| | |

| |

Sequoia Fund | | December 31, 2019 |

Management’s Discussion of Fund Performance (Unaudited)

The table below shows the12-month stock total return for the top ten equity positions at the end of 2019.

| | | | | | | | | | | | |

| | | % of | | | | | | % of | |

| | | Net | | | | | | Net | |

| | | Assets | | | Total | | | Assets | |

Company | | 12/31/19 | | | Return | | | 12/31/18 | |

Alphabet, Inc. | | | 12.0 | % | | | 28.2 | % | | | 12.1 | % |

Berkshire Hathaway, Inc. | | | 8.3 | % | | | 11.0 | % | | | 10.0 | % |

CarMax, Inc. | | | 6.2 | % | | | 39.8 | % | | | 8.0 | % |

Mastercard, Inc. | | | 5.3 | % | | | 59.2 | % | | | 6.1 | % |

Constellation Software, Inc. | | | 4.9 | % | | | 48.5 | % | | | 5.3 | % |

Jacobs Engineering Group, Inc. | | | 4.6 | % | | | 55.0 | % | | | 4.6 | % |

Credit Acceptance Corp. | | | 4.6 | % | | | 15.9 | % | | | 4.6 | % |

Liberty Broadband Corp. | | | 4.4 | % | | | 73.5 | % | | | 3.6 | % |

Facebook, Inc. | | | 4.3 | % | | | 56.6 | % | | | 3.2 | % |

Liberty Media Corp. | | | 4.3 | % | | | 49.7 | % | | | 4.1 | % |

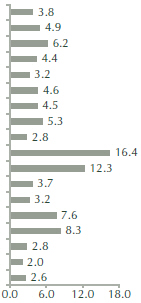

Sector Breakdown as of December 31, 2019 (% of net assets)

| | |

Aerospace & Defense | |

|

Application Software |

Automotive Retail |

Cable & Satellite |

Communications Equipment |

Construction & Engineering |

Consumer Finance |

Data Processing & Outsourced Services |

Heavy Electrical Equipment |

Interactive Media & Services |

Internet & Direct Marketing Retail |

Investment Banking & Brokerage |

Life Sciences Tools & Services |

Movies & Entertainment |

Multi-Sector Holdings |

Packaged Foods & Meats |

Property & Casualty Insurance |

Undisclosed |

The total return for the Sequoia Fund in 2019 was 29.12%. This compares with the 31.49% return of the S&P 500 Index.

Our preference is to make concentrated commitments of capital in a limited number of companies that have superior long-term economic prospects and that sell at what we believe are attractive prices. Because Sequoia is deliberately not representative of the overall market, in any given year the performance of the Fund may vary significantly from that of the broad market indices.

The top ten equity positions constituted approximately 59% of Sequoia’s net assets on December 31, 2019. Atyear-end,

the Fund was 98.6% invested in common stocks and 1.4% invested in cash.

Alphabet’s revenue grew 18.3% in 2019, to $162 billion. The primary drivers of Alphabet’s remarkable growth were once again mobile search, YouTube and Google Cloud Services. In a first, Alphabet disclosed revenue figures for YouTube and Google Cloud in the company’s fiscal 2019 financial report. YouTube generated $15.1 billion in revenue in 2019, up 36% over 2018. Google Cloud generated $8.9 billion in 2019, a 53% improvement over 2018. Google Cloud’s growth looks set to continue; the company disclosed an order backlog of $11.4 billion.

Growth at such a rapid pace for a company of Alphabet’s scale is hard to comprehend and even harder to sustain. Search advertising revenue is Alphabet’s most mature business and its biggest economic engine by far, and it grew 15% year over year. That is nothing short of heroic for atwenty-year-old business segment generating roughly $100 billion of annual revenue.

The rapid growth of younger business segments that remain in their investment phase has naturally pressured Alphabet’s operating margin over the past several years, causing revenue to outpace operating income. 2019 was no exception to this trend. We estimate Alphabet’s operating profit after taxes grew 13% in 2019, after certain adjustments that filter out noise in the reported figures. The wisdom of trading operating margin for revenue growth will be determined by the long-term return on Alphabet’s myriad current investments, and for many of these it will be years before the results are in. Google Cloud in particular will require significant investment as Google battles Amazon Web Services (“AWS”) and Microsoft Azure for its share of the cloud computing services market. It is worth noting that AWS achieved an operating margin nearly equal to Alphabet’s current operating margin when it was about the size of the current Google Cloud business. We are hopeful that Google Cloud will generate a healthy and expanding margin as the size of the business increases.

In the fourth quarter, Alphabet announced that founders Larry Page and Sergey Brin would step back from their respective roles as Alphabet’s CEO and President. Sundar Pichai, already CEO of Google, Alphabet’s most important business, will take over as CEO of parent company Alphabet and assume responsibility for the company’s Other Bets in addition to his previous responsibilities. It will be interesting to see how Alphabet’s “moonshot” projects, collected under the banner of Other Bets, will develop under Pichai’s leadership. While Alphabet’s manynon-advertising initiatives help the company attract and retain talent, and a few of them have the potential to grow into sizeable businesses in the long term, we believe

9

| | |

| |

Sequoia Fund | | December 31, 2019 |

Management’s Discussion of Fund Performance (Unaudited) (Continued)

there is scope to improve Alphabet’s focus when it comes to the allocation of resources to Other Bets.

This coming June will mark theten-year anniversary of our investment in Alphabet. As we write this, the investment has returned 20% annually, a remarkable result given that Alphabet enjoyed a market capitalization exceeding $150 billion at the time of our investment. This record is a credit to the company and a testament to the remarkable power of Alphabet’s business and that of dominant internet platforms generally. Our appreciation of the unusual ability of these platforms to generate durable growth at enormous scale has informed our subsequent investments in Amazon, Facebook and Wayfair, all of which are market leaders in their respective niches.

With great power comes great responsibility. It is clear that certain scaled internet-based platforms, including Alphabet’s YouTube video platform, possess the wherewithal to shape the cultural landscape in profound and often unpredictable ways. To monitor the body of user-generated content on YouTube requires an enormous investment in people and technology, and it is little wonder that YouTube and other social platforms prefer to be characterized as neutral distributors of third-party content rather than as publishers, given that the latter designation carries the implication of editorial control and its attendant obligations. Over time, cultural and political developments have rendered a laissez-faire approach to content distribution increasingly untenable, leading YouTube and its peers to invest significant sums to improve the security and monitoring of their platforms. It is a certainty that billions of dollars of further investment will be required, but taming problematic content is a profoundly important goal from both a societal and a business standpoint. Progress in this area will make the dominant social platforms more sustainable, more trusted, and harder to disrupt.

In light of the substantial increase in the company’s valuation in 2019, we modestly reduced the size of our Alphabet position. However, Alphabet remains a compelling business with an attractive valuation, and it remains the largest position in the Sequoia portfolio.

Berkshire had a quiet year with aggregate earnings likely up about 5%. Deploying cash at attractive valuations was challenging because of a strong stock market fueled in part by a decline in interest rates. Berkshire did manage to negotiate the purchase of $10 billion of Occidental Petroleum preferred stock, which pays an attractive 8% dividend and comes with $5 billion of warrants attached. Some existing holdings experienced challenges, including Kraft (competition from private label), GEICO (competition from Progressive), Wells Fargo (continued fallout from the phantom account scandal) and the BNSF railroad (competition from trucks, bad weather,

tariffs, and low natural gas prices). We were encouraged to see leadership changes at three of the four above named companies, and a fourth is probably in the offing. On the plus side, Berkshire’s largest public holding, Apple, has seen its stock price more than double during the year as profit trends stabilized on the back of strong sales of AirPods and other wearables. (The value of Berkshire’s stake in Apple today is worth as much as all of Berkshire traded for 20 years ago.) Berkshire continues to sell at a meaningful valuation discount to other stocks after backing out a cash hoard equal to 25% of the company’s market cap.

Carmax posted 10% revenue growth, fueled by sixteen new stores and solid same-store sales growth. Helped along by aggressive share repurchase and a lower tax rate, earnings rose 19%. Carmax believes the future of used car retailing belongs to omni channel retailers like itself that can sell cars at stores and online. Carmax took several steps to transition to the omni model last year. It replaced hundreds of commissioned salespeople with customer experience managers who, working from four regional locations, handle orders and questions from customers. It reduced the arduous paperwork involved in car buying by moving to electronic documents ande-signatures. It expanded home delivery to half its markets, and began offering onlinepre-approvals for loans and online appraisals ontrade-ins. Although Carmax’s development of omni channel represents the biggest makeover in the company’s history, it has so far managed the transition without diminishing margins. We believe many competitors will struggle to keep up and that omni increases the size of Carmax’s competitive moat.

Mastercard reported a strong result in 2019. Net revenue grew 16% on a currency-neutral basis. With operating leverage, a lower tax rate and share buybacks, diluted earnings per share grew 23% on a currency-neutral basis. We continue to believe the longstanding secular tailwinds for Mastercard remain intact. At the same time, we continue to monitor potential technological threats as well as regulatory and legal developments in various geographies. Taken altogether, we believe Mastercard’s current valuation is fair for a superior business with a history of positive surprises. We nonetheless trimmed our position during the year as the stock price outpaced our estimate of growth in intrinsic value.

Constellation Software continues to scour the world for niche software companies, finding acquisitions in new verticals like crash/crime scene diagramming and new geographies like Brazil. The company has done a remarkable job scaling its acquisition strategy, but management realizes that to sop up its growing cash flows it will need to find new arenas to deploy capital. One such arena is larger acquisitions, where Constellation faces more competing bids from private equity

10

| | |

| |

Sequoia Fund | | December 31, 2019 |

Management’s Discussion of Fund Performance (Unaudited) (Continued)

firms and strategic buyers. In 2019, Constellation’s board approved a lower yet still attractive return hurdle for large acquisitions in order to participate more in this market. We look forward to seeing if this effort proves fruitful in 2020.

When we originally bought shares of Constellation, the rest of the market had not assigned them much value for continued growth by purchasing yet more vertical software companies. Over time, the company’s ability to make superior rates of return on these acquisitions seems to have become well-appreciated as the market has assigned higher and higher valuations to the stock.

At times, the shares in our estimation have traded too dearly unless the company can somehow shift acquisitions to an even higher gear. Management has signaled the difficulty of allocating ever-larger incoming cash flows while maintaining strict valuation discipline, most pointedly with a $20 special dividend issued in the first half of 2019.Though our preference is to take the full journey with this exceptional team, we have from time to time sold some shares to buyers with more exuberant expectations.

Credit Acceptance had an outstanding year. Sales rose 16% and operating earnings rose 30%. Earnings per share grew 22%, held back by a return to a normal tax rate after an unusually low rate the prior year. The market for subprime auto loans remains highly competitive. Despite that, the company’s underwriting discipline remains strong. A change in accounting rules will sharply curtail the company’s GAAP earnings in the coming year, but the change in accounting optics has no bearing on the economics of the business. Market concerns about how car loans will perform in a recession kept Credit Acceptance’s valuation at an attractive level for most of 2019. Because Credit Acceptance has a disciplined and differentiated approach to underwriting loans, we believe it would continue to thrive in a recessionary environment and may well grow market share as competitors struggle with losses.

Jacobs Engineering Group, a professional services firm, turned in strong performance for the fiscal year. It grew revenues 11% organically and grew diluted earnings per share roughly 15%. When CEO Steve Demetriou joined in 2015, he laid out aback-to-basics strategy of eschewing commoditized, risky projects in favor of high-margin, predictable business. Management has been hard at work realizing this vision and the company whizzed past several milestones in 2019. It divested its Energy, Chemicals & Resources division at an attractive price, freeing the company of its least profitable and most cyclical segment. Management used the proceeds to expand Jacobs’ portfolio in the attractive government services space with the acquisitions of KeyW and Wood Group’s Nuclear business. Further, nearly two years after the transformative

acquisition of CH2M, it is safe to say the integration has been a success. The company celebrated in November with a rebranding from “Jacobs Engineering” to “Jacobs Solutions,” a well-deserved recognition that Jacobs is now a low risk, capital-light solutions provider serving attractiveend-markets.

Charter Communications, which we own via Liberty Broadband, demonstrated how theslow-and-steady world of cable internet can still produce stellar results. We estimate revenue only grew 3% in 2019 as the steady bleed oflow-margin video subscribers continued. However, cash operating profit grew 45% on continued broadband growth and declining capital expenditures. That, combined with Charter’s disciplined practice of returning capital via share buybacks, meant free cash flow per share grew over 75% in 2019. We are pleased with the performance, but we do not expect sucheye-popping growth going forward. Capital expenditures had been elevated due to merger integrations and an extensive network upgrade. With these investments complete, future margin improvements should be more incremental. That said, overall profit growth should be more than satisfactory. Internet has become an everyday utility of growing importance and Charter’s broadband offering should continue to take share from AT&T and Verizon.

Formula One Management announced in October 2019 that all 10 participating teams had unanimously approved the sport’s new Sporting, Technical and Commercial Regulations. As we mentioned in last year’s letter, given the practical realities of implementing a new successor Concord Agreement in 2021, Formula One needed to secure at least high-level agreement on the key elements of a new governing deal in 2019. There are five parts to the Concord Agreement: Sporting, Technical, Commercial, Financial and Governing Regulations. The Sporting, Technical and Commercial regulations needed to be confirmed about 18 months ahead of implementation to allow for the teams and league to make necessary changes ahead of expiration of the current agreements at the end of the 2020 season.

We are encouraged by the progress achieved during the 2019 negotiations. As part of the new Sporting, Technical and Commercial Regulations, the league made important strides toward enhancing the competitiveness of the sport, which should bolster fan engagement. Most importantly, as part of the new Commercial Regulations, the sport will adopt a new cost cap starting in the 2021 season that should reduce the spending gap separating the top teams and the middle of the field. In addition, the new Technical Regulations increase the sharing of intellectual property and improve the ability of cars to pass one another on the track, a key aspect of exciting racing. There are still some important components to be worked out, including profit splits between the teams and the league itself, as well as Governance Regulations that hopefully reduce

11

| | |

| |

Sequoia Fund | | December 31, 2019 |

Management’s Discussion of Fund Performance (Unaudited) (Continued)

the power of the leading teams to stifle rule changes that improve competition.

Financially, a new broadcast contract in the UK helped drive revenue and profit growth in 2019. We expect revenue and profits to continue to advance in 2020, thanks to new sponsorship and advertising contracts that will take effect, as well as the addition of one new race to the calendar, bringing the total to 22.

Facebook grew revenues 27% in 2019. Despite unrelenting bad publicity, much of it warranted, engagement with the Facebook family of apps remains healthy. Instagram continues to attract new users across the world. The popularity of the ”Stories“ format and the introduction of shopping in the app should contribute to years of rapid growth. The average time spent in the ”Blue“ Facebook app stabilized during the year. Facebook’s efforts to emphasize meaningful social interactions rather than passive media consumption are bearing fruit and should enhance the durability of the social network. While regulation remains a risk for the company, at ~25x our estimated earnings power, Facebook remains one of the cheapest high-growth companies we follow.

12

| | |

| |

Sequoia Fund | | December 31, 2019 |

Annual Fund Operating Expenses (Unaudited)

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund.

Shareholder Fees(fees paid directly from your investment)

The Fund does not impose any sales charges, exchange fees or redemption fees.

Annual Fund Operating Expenses(expenses that are deducted from Fund assets)

| | | | | | |

| | | | | |

| | Management Fees | | | 1.00% | |

| | Other Expenses | | | 0.06% | |

| | | | | | |

| | Total Annual Fund Operating Expenses* | | | 1.06% | |

| | Expense Reimbursement by Investment Adviser* | | | -0.06% | |

| | | | | | |

| | Net Annual Fund Operating Expenses* | | | 1.00% | |

| | | | | | |

*It is the intention of Ruane, Cunniff & Goldfarb L.P. (the ”Investment Adviser“) to ensure the Fund does not pay in excess of 1.00% in Net Annual Fund Operating Expenses. This reimbursement is a provision of the Investment Adviser’s investment advisory contract with the Fund and the reimbursement will be in effect only so long as that investment advisory contract is in effect. The expense ratio presented is from the Prospectus dated May 1, 2019. For the year ended December 31, 2019, the Fund’s annual operating expenses and annual advisory fees, net of the reimbursement, were 1.00% and 0.93%, respectively.

Fees and Expenses of the Fund (Unaudited)

Shareholder Expense Example

As a shareholder of the Fund, you incur ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2019 through December 31, 2019).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled ‘‘Expenses Paid During Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and will not help you determine the relative total costs of owning different funds.

| | | | | | |

| | | | | | | Expenses |

| | | Beginning | | Ending | | Paid During |

| | | Account | | Account | | Period** |

| | | Value | | Value | | July 1, 2019 |

| | | July 1, | | December 31, | | through December 31, |

| | | 2019 | | 2019 | | 2019 |

| Actual | | $1,000 | | $1,067.22 | | $5.21 |

Hypothetical (5% return per year before expenses) | | $1,000 | | $1,020.16 | | $5.09 |

** Expenses are equal to the Fund’s annualized net expense ratio of 1.00%, multiplied by the average account value over the period, multiplied by 184/ 365 (to reflect theone-half year period).

13

| | |

| |

Sequoia Fund | | December 31, 2019 |

Schedule of Investments

December 31, 2019

(Percentages are of the Fund’s Net Assets)

Common Stocks (98.6%)

| | | | | | | | |

| Shares | | | | | Value (Note 1) | |

| | | | | | | | |

| | | | Aerospace & Defense (3.8%) | | | | |

| | 16,675,950 | | | Rolls-Royce Holdings PLC (United Kingdom) | | $ | 150,912,775 | |

| | | | | | | | |

| | | | Application Software (4.9%) | | | | |

| | 199,611 | | | Constellation Software, Inc. (Canada) | | | 193,863,470 | |

| | | | | | | | |

| | | | Automotive Retail (6.2%) | | | | |

| | 2,835,584 | | | CarMax, Inc.(a) | | | 248,595,649 | |

| | | | | | | | |

| | | | Cable & Satellite (4.4%) | | | | |

| | 423,063 | | | Liberty Broadband Corp.-Class A(a) | | | 52,696,727 | |

| | 969,350 | | | Liberty Broadband Corp.-Class C(a) | | | 121,895,762 | |

| | | | | | | | |

| | | | | | | 174,592,489 | |

| | | | | | | | |

| | | | Communications Equipment (3.2%) | | | | |

| | 627,157 | | | Arista Networks, Inc.(a) | | | 127,563,734 | |

| | | | | | | | |

| | | | Construction & Engineering (4.6%) | | | | |

| | 2,029,358 | | | Jacobs Engineering Group, Inc | | | 182,297,229 | |

| | | | | | | | |

| | | | Consumer Finance (4.5%) | | | | |

| | 410,229 | | | Credit Acceptance Corp.(a) | | | 181,456,594 | |

| | | | | | | | |

| | | | Data Processing & Outsourced Services (5.3%) | | | | |

| | 701,051 | | | Mastercard, Inc.-Class A | | | 209,326,818 | |

| | | | | | | | |

| | | | Heavy Electrical Equipment (2.8%) | | | | |

| | 34,904,064 | | | Melrose Industries PLC (United Kingdom) | | | 111,008,368 | |

| | | | | | | | |

| | | | Interactive Media & Services (16.4%) | | | | |

| | 143,715 | | | Alphabet, Inc.-Class A(a) | | | 192,490,434 | |

| | 214,733 | | | Alphabet, Inc.-Class C(a) | | | 287,102,316 | |

| | 837,473 | | | Facebook, Inc.-Class A(a) | | | 171,891,333 | |

| | | | | | | | |

| | | | | | | 651,484,083 | |

| | | | | | | | |

| | | | Internet & Direct Marketing Retail (12.3%) | | | | |

| | 56,616 | | | Amazon.com, Inc.(a) | | | 104,617,309 | |

| | 59,202 | | | Booking Holdings, Inc.(a) | | | 121,584,923 | |

| | 1,772,898 | | | Prosus NV (Netherlands)(a) | | | 132,306,118 | |

| | 1,457,072 | | | Wayfair, Inc.-Class A(a) | | | 131,675,597 | |

| | | | | | | | |

| | | | | | | 490,183,947 | |

| | | | | | | | |

| | | | Investment Banking & Brokerage (3.7%) | | | | |

| | 3,143,365 | | | The Charles Schwab Corp | | | 149,498,439 | |

| | | | | | | | |

| | | | Life Sciences Tools & Services (3.2%) | | | | |

| | 232,437 | | | Eurofins Scientific SE (Luxembourg) | | | 128,850,662 | |

| | | | | | | | |

| | | | Movies & Entertainment (7.6%) | | | | |

| | 49,478 | | | Liberty Media Corp.-Liberty Formula One - Series A(a) | | | 2,166,147 | |

| | 3,699,797 | | | Liberty Media Corp.-Liberty Formula One - Series C(a) | | | 170,061,169 | |

| | 4,473,446 | | | Vivendi SA (France) | | | 129,561,835 | |

| | | | | | | | |

| | | | | | | 301,789,151 | |

| | | | | | | | |

| | | | Multi-Sector Holdings (8.3%) | | | | |

| | 597 | | | Berkshire Hathaway, Inc.-Class A(a) | | | 202,735,230 | |

| | 560,857 | | | Berkshire Hathaway, Inc.-Class B(a) | | | 127,034,111 | |

| | | | | | | | |

| | | | | | | 329,769,341 | |

| | | | | | | | |

The accompanying notes form an integral part of these Financial Statements.

14

| | |

| |

Sequoia Fund | | December 31, 2019 |

Schedule of Investments (Continued)

December 31, 2019

| | | | | | | | |

| Shares | | | | | Value (Note 1) | |

| | | | | | | | |

| | | | Packaged Foods & Meats (2.8%) | | | | |

| | 10,957,493 | | | a2 Milk Co. Ltd. (New Zealand)(a) | | $ | 109,958,632 | |

| | | | | | | | |

| | | | Property & Casualty Insurance (2.0%) | | | | |

| | 4,168,266 | | | Hiscox Ltd. (Bermuda) | | | 78,623,610 | |

| | | | | | | | |

| | | | Miscellaneous Securities (2.6%)(b) | | | 103,625,003 | |

| | | | | | | | |

| | |

| | | | Total Common Stocks(Cost $2,187,981,068) | | | 3,923,399,994 | |

| | | | | | | | |

| | | | Total Investments (98.6%) (Cost $2,187,981,068)(c) | | | 3,923,399,994 | |

| | |

| | | | Other Assets Less Liabilities (1.4%) | | | 56,698,159 | |

| | | | | | | | |

| | | | Net Assets (100.0%) | | $ | 3,980,098,153 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (b) | “Miscellaneous Securities” include holdings that are not restricted, have been held for not more than one year prior to December 31, 2019, and have not previously been publicly disclosed. |

| (c) | The cost for federal income tax purposes is $2,182,081,859. The difference between book cost and tax cost is attributable to financial and tax accounting differences on a corporatespin-off. |

Generally accepted accounting principles establish a disclosure hierarchy that categorizes the inputs to valuation techniques used to value the investments at measurement date. These inputs are summarized in the three levels listed below:

| | Level 1 – | unadjusted quoted prices in active markets for identical securities. |

| | Level 2 – | other significant observable inputs (including, but not limited to, quoted prices for similar securities, interest rates, prepayment speeds and credit risk) |

| | Level 3 – | unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Transfers between levels are recognized at the end of the reporting period. As of the year ended December 31, 2019, all financial instruments listed in the Schedule of Investments are considered Level 1. During the year ended December 31, 2019, there were no transfers between Levels and there were no Level 3 securities held by the Fund.

The accompanying notes form an integral part of these Financial Statements.

15

| | |

| |

Sequoia Fund | | December 31, 2019 |

Statement of Assets and Liabilities

December 31, 2019

| | | | |

Assets | | | | |

Investments in securities, at value (cost $2,187,981,068) (Note 1) | | $ | 3,923,399,994 | |

Cash on deposit | | | 61,766,110 | |

Receivable for investments sold | | | 1,016,099 | |

Receivable for capital stock sold | | | 312,965 | |

Dividends and interest receivable | | | 555,977 | |

Other assets | | | 144,894 | |

| | | | |

Total assets | | | 3,987,196,039 | |

| | | | |

Liabilities | | | | |

Payable for investments purchased | | | 2,951,906 | |

Payable for capital stock repurchased | | | 781,029 | |

Accrued investment advisory fee | | | 3,180,870 | |

Accrued professional fees | | | 70,560 | |

Accrued other expenses | | | 113,521 | |

| | | | |

Total liabilities | | | 7,097,886 | |

| | | | |

Net Assets | | $ | 3,980,098,153 | |

| | | | |

| |

Net Assets Consist of | | | | |

Capital (par value and paid in surplus) $.10 par value capital stock, 100,000,000 shares authorized, 25,307,026 shares outstanding | | $ | 2,155,519,685 | |

Total distributable earnings (loss) | | | 1,824,578,468 | |

| | | | |

Net Assets | | $ | 3,980,098,153 | |

| | | | |

| |

Net asset value per share | | $ | 157.27 | |

| | | | |

The accompanying notes form an integral part of these Financial Statements.

16

| | |

| |

Sequoia Fund | | December 31, 2019 |

Statement of Operations

Year Ended December 31, 2019

| | | | |

Investment Income | | | | |

Income | | | | |

Dividends, net of $1,640,693 foreign tax withheld | | $ | 20,993,326 | |

Interest | | | 1,662,771 | |

| | | | |

Total investment income | | | 22,656,097 | |

| | | | |

Expenses | | | | |

Investment advisory fee (Note 2) | | | 38,746,895 | |

Professional fees | | | 1,119,842 | |

Transfer agent fees | | | 788,864 | |

Independent Directors fees and expenses | | | 497,852 | |

Custodian fees | | | 125,000 | |

Other | | | 900,721 | |

| | | | |

Total expenses | | | 42,179,174 | |

Less professional fees reimbursed by insurance company (Note 5) | | | 650,000 | |

| | | | |

Expenses before reimbursement by Investment Adviser | | | 41,529,174 | |

Less expenses reimbursed by Investment Adviser (Note 2) | | | 2,632,279 | |

| | | | |

Net expenses | | | 38,896,895 | |

| | | | |

Net investment loss | | | (16,240,798 | ) |

| | | | |

Realized and Unrealized Gain (Loss) on Investments and Foreign Currency Transactions | | | | |

Realized gain (loss) on | | | | |

Investments (Note 3) | | | 327,790,904 | |

Foreign currency transactions | | | (951,874 | ) |

| | | | |

Net realized gain on investments and foreign currency transactions | | | 326,839,030 | |

Net change in unrealized appreciation/(depreciation) on | | | | |

Investments | | | 654,186,186 | |

Foreign currency translations | | | 39,685 | |

| | | | |

Net increase in unrealized appreciation/(depreciation) on investments and foreign currency translations | | | 654,225,871 | |

| | | | |

Net realized and unrealized gain on investments and foreign currency transactions and translations | | | 981,064,901 | |

| | | | |

Net increase in net assets from operations | | $ | 964,824,103 | |

| | | | |

The accompanying notes form an integral part of these Financial Statements.

17

| | |

| |

Sequoia Fund | | December 31, 2019 |

Statements of Changes in Net Assets

| | | | | | | | |

| | | Year Ended | |

| | | December 31, | |

| | | 2019 | | | 2018 | |

Increase (Decrease) in Net Assets | | | | | | | | |

From operations | | | | | | | | |

Net investment loss | | $ | (16,240,798 | ) | | $ | (17,846,062 | ) |

Net realized gain on investments and foreign currency transactions | | | 326,839,030 | | | | 1,008,505,577 | |

Net increase (decrease) in unrealized appreciation/(depreciation) on investments and foreign currency translations | | | 654,225,871 | | | | (1,071,362,189 | ) |

| | | | | | | | |

Net increase (decrease) in net assets from operations | | | 964,824,103 | | | | (80,702,674 | ) |

| | | | | | | | |

Distributions to shareholders from: | | | | | | | | |

Total distributable earnings | | | (317,910,420 | ) | | | (790,789,876 | ) |

| | | | | | | | |

Capital share transactions | | | | | | | | |

Shares sold | | | 79,309,117 | | | | 133,367,761 | |

Shares issued to shareholders on reinvestment of net income and net realized gain distributions | | | 248,963,356 | | | | 656,695,555 | |

Shares repurchased | | | (430,595,536 | ) | | | (728,875,560 | ) |

| | | | | | | | |

Net increase (decrease) from capital share transactions | | | (102,323,063 | ) | | | 61,187,756 | |

| | | | | | | | |

Total increase (decrease) in net assets | | | 544,590,620 | | | | (810,304,794 | ) |

Net Assets | | | | | | | | |

Beginning of year | | | 3,435,507,533 | | | | 4,245,812,327 | |

| | | | | | | | |

End of year | | $ | 3,980,098,153 | | | $ | 3,435,507,533 | |

| | | | | | | | |

| | |

Share transactions | | | | | | | | |

Shares sold | | | 524,680 | | | | 784,118 | |

Shares issued to shareholders on reinvestment of net income and net realized gain distributions | | | 1,628,764 | | | | 4,783,658 | |

Shares repurchased | | | (2,833,962 | ) | | | (4,621,843 | ) |

| | | | | | | | |

Net increase (decrease) from capital share transactions | | | (680,518 | ) | | | 945,933 | |

| | | | | | | | |

The accompanying notes form an integral part of these Financial Statements.

18

| | |

| |

Sequoia Fund | | December 31, 2019 |

Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016 | | | 2015 | |

| Per Share Operating Performance (for a share outstanding throughout the year) | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 132.20 | | | $ | 169.55 | | | $ | 161.28 | | | $ | 207.26 | | | $ | 235.00 | |

| | | | | | | | | | | | | | | | | | | | |

Income from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.62 | ) | | | (0.69 | ) | | | (0.59 | ) | | | (0.43 | ) | | | (1.08 | ) |

Net realized and unrealized gains (losses) on investments | | | 38.50 | | | | (2.67 | ) | | | 32.12 | | | | (15.16 | ) | | | (16.15 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net asset value from operations | | | 37.88 | | | | (3.36 | ) | | | 31.53 | | | | (15.59 | ) | | | (17.23 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Less distributions from | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (1.16 | )(a) | | | — | | | | — | | | | — | | | | — | |

Net realized gains | | | (11.65 | ) | | | (33.99 | ) | | | (23.26 | ) | | | (30.39 | ) | | | (10.51 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | (12.81 | ) | | | (33.99 | ) | | | (23.26 | ) | | | (30.39 | ) | | | (10.51 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 157.27 | | | $ | 132.20 | | | $ | 169.55 | | | $ | 161.28 | | | $ | 207.26 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total Return | | | 29.12 | % | | | (2.62 | )% | | | 20.07 | %(b) | | | (6.90 | )% | | | (7.31 | )% |

| | | | | |

Ratios/Supplementary data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in millions) | | $ | 3,980 | | | $ | 3,436 | | | $ | 4,246 | | | $ | 4,096 | | | $ | 6,741 | |

Ratio of expenses to average net assets | | | | | | | | | | | | | | | | | | | | |

Before expenses reimbursed by Investment Adviser (c) | | | 1.07 | % | | | 1.06 | % | | | 1.07 | % | | | 1.07 | % | | | 1.03 | % |

After expenses reimbursed by Investment Adviser | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % |

Ratio of net investment loss to average net assets | | | (0.42 | )% | | | (0.42 | )% | | | (0.35 | )% | | | (0.22 | )% | | | (0.42 | )% |

Portfolio turnover rate | | | 16 | % | | | 27 | % | | | 18 | % | | | 16 | % | | | 10 | % |

| (a) | The difference of net investment income/(loss) for financial and tax reporting is attributable to financial and accounting differences on a corporate spin–off. As a result, the Fund was required to make a distribution from net investment income for tax purposes. |

| (b) | Includes the impact of proceeds received and credited to the Fund resulting from a class action settlement, which enhanced the Fund’s performance for the year ended December 31, 2017 by 0.05%. |

| (c) | Reflects reductions of 0.02%, 0.05%, 0.02% and 0.02% for expenses reimbursed by insurance company for the years ended December 31, 2019, 2018, 2017 and 2016, respectively. |

The accompanying notes form an integral part of these Financial Statements.

19

| | |

| |

Sequoia Fund | | December 31, 2019 |

Notes to Financial Statements

Note 1— Significant Accounting Policies

Sequoia Fund, Inc. (the ‘‘Fund’’) is registered under the Investment Company Act of 1940, as amended, as anon-diversified,open-end management investment company. The investment objective of the Fund is long-term growth of capital. The Fund follows investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services— Investment Companies. The following accounting policies conform to U.S. generally accepted accounting principles (“GAAP”). The Fund consistently follows such policies in the preparation of its financial statements.

| A. | Valuation of investments: Investments are carried at fair value as determined under the supervision of the Fund’s Board of Directors. Securities traded on a national securities exchange are valued at the last reported sales price on the principal exchange on which the security is listed; securities traded in the NASDAQ Stock Market (”NASDAQ“) are valued in accordance with the NASDAQ Official Closing Price. Securities for which there is no sale or Official Closing Price are valued at the mean of the last reported bid and asked prices. |

Securities traded on a foreign exchange are valued at the closing price on the last business day of the period on the principal exchange on which the security is primarily traded. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the New York Stock Exchange on the date of valuation.

U.S. Treasury Bills with remaining maturities of 60 days or less are valued at their amortized cost. U.S. Treasury Bills that when purchased have a remaining maturity in excess of 60 days are valued on the basis of market quotations and estimates until the sixtieth day prior to maturity, at which point they are valued at amortized cost. Fixed-income securities, other than U.S. Treasury Bills, are valued at the last quoted sales price or, if adequate trading volume is not present, at the mean of the last bid and asked prices.

When reliable market quotations are insufficient or not readily available at the time of valuation or when Ruane, Cunniff & Goldfarb L.P. (the ”Investment Adviser“) determines that the prices or values available do not represent the fair value of a security, such security is valued as determined in good faith by the Investment Adviser, in conformity with procedures adopted by and subject to review by the Fund’s Board of Directors.

| B. | Foreign currency translations: Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the date of valuation. Purchases and sales of foreign securities are translated into U.S. dollars at the rates of exchange prevailing when such securities are acquired or sold. Income and expenses are translated into U.S. dollars at the rates of exchange prevailing when accrued. The Fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss from investments. Reported net realized gains or losses on foreign currency transactions arise from the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized gains and losses on foreign currency transactions and translations arise from changes in the fair values of assets and liabilities, other than investments in securities at fiscal period end, resulting from changes in exchange rates. |

| C. | Investment transactions and investment income: Investment transactions are accounted for on the trade date and dividend income is recorded on theex-dividend date. Interest income is accrued as earned. Premiums and discounts on fixed income securities are amortized over the life of the respective security. The net realized gain or loss on security transactions is determined for accounting and tax purposes on the specific identification basis. |

| D. | Federal income taxes: The Fund’s policy is to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies, and it intends to distribute all of its taxable income to its stockholders. Therefore, no federal income tax provision is required. |

20

| | |

| |

Sequoia Fund | | December 31, 2019 |

Notes to Financial Statements (Continued)

| E. | Use of estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. |

| F. | Dividends and distributions: Dividends and distributions are recorded by the Fund on theex-dividend date. |

Note 2— Investment Advisory Contract and Payments to Affiliates

The Investment Adviser provides the Fund with investment advice and administrative services pursuant to an investment advisory contract (the “Advisory Contract”) with the Fund.

Under the terms of the Advisory Contract, the Investment Adviser receives an investment advisory fee equal to 1% per annum of the Fund’s average daily net asset value. Under the Advisory Contract, the Investment Adviser is contractually obligated to reimburse the Fund for the amount, if any, by which the operating expenses of the Fund (including the investment advisory fee) in any year exceed the sum of 11⁄2% of the average daily net asset value of the Fund for such year up to a maximum of $30,000,000 of net assets, plus 1% of the average daily net asset value in excess of $30,000,000. The expenses incurred by the Fund exceeded the limitation for the year ended December 31, 2019 and the Investment Adviser reimbursed the Fund $2,258,279. Such reimbursement is not subject to recoupment by the Investment Adviser.