UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-7170

TCW Funds, Inc.

(Exact name of registrant as specified in charter)

865 South Figueroa Street, Suite 1800, Los Angeles, CA 90017

(Address of principal executive offices)

Patrick W. Dennis, Esq.

Assistant Secretary

865 South Figueroa Street, Suite 1800

Los Angeles, CA 90017

(Name and address of agent for service)

Registrant’s telephone number, including area code: (213) 244-0000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2016

| Item 1. | Report to Shareholders. |

OCTOBER 31

2016

ANNUAL REPORT

TCW EQUITY FUNDS

TCW Focused Equities Fund TCW Global Real Estate Fund TCW Growth Equities Fund TCW High Dividend Equities Fund

TCW New America Premier Equities Fund TCW Relative Value Dividend Appreciation Fund TCW Relative Value Large Cap Fund TCW Relative Value Mid Cap Fund TCW Select Equities Fund TCW Small Cap Growth Fund

ASSET ALLOCATION FUND

TCW Conservative Allocation Fund

TCW Funds, Inc.

| 1 | ||||

| 4 | ||||

| 30 | ||||

| 30 | ||||

| 32 | ||||

| 36 | ||||

| 39 | ||||

| 43 | ||||

| 47 | ||||

| 51 | ||||

| 55 | ||||

| 59 | ||||

| 63 | ||||

| 66 | ||||

| 71 | ||||

| 74 | ||||

| 77 | ||||

| 83 | ||||

| 102 | ||||

| 124 | ||||

| 125 | ||||

| 128 | ||||

| 130 | ||||

Proxy Voting Guidelines and Availability of Quarterly Portfolio Schedule | 133 | |||

| 134 | ||||

| 135 | ||||

| The Letter to Shareholders and/or Management Discussions contained in this Annual Report are the opinions of each Fund’s portfolio managers and are not the opinions of TCW Funds, Inc. or its Board of Directors. Various matters discussed in the Letter to Shareholders and/or Management Discussions constitute forward-looking statements within the meaning of the federal securities laws. Actual results and the timing of certain events could differ materially from those projected or contemplated by these forward-looking statements due to a number of factors, including general economic conditions, overall availability of securities for investment by a Fund, the level of volatility in the securities markets and in the share price of a Fund, and other risk factors discussed in the SEC filings of TCW Funds, Inc. The data presented in the Letter to Shareholders and/or Management Discussions represents past performance and cannot be used to predict future results. |

|

| David S. DeVito President, Chief Executive Officer and Director |

Dear Valued Investors,

It is my pleasure to present the 2016 annual report for the TCW Funds, Inc. covering the 12-month period ended October 31, 2016. I would like to express our appreciation for your continued investment in the TCW Funds as well as welcome new shareholders to our fund family. As of October 31, 2016, the TCW Funds held total net assets of approximately $19.2 billion.

This report contains information and portfolio management discussions of our TCW Equity Funds and our TCW Allocation Fund.

The U.S. Stock Market

U.S. stocks (S&P 500 Index) posted a 4.50% total return for the year ended October 31, 2016. Equities ended the year in very much the same mode as they began the year, grappling in each case with the prospect of a Fed interest rate hike at its December meeting. Indeed, the macroeconomic narrative for much of the year centered around the Fed’s attempts to proceed with the normalization of interest rates after over seven years of extraordinary monetary accommodation and near-zero rates. Yet, concerns about anemic U.S. GDP growth, the growth slowdown in China, mixed results from Abenomics in Japan, and renewed concerns about the health of the Eurozone’s banking sector forced the Fed to relent on its original intentions to raise interest rates multiple times over the course of the year. Also, the uncertainty associated with the surprise Brexit vote result in the UK at the end of June led to an additional bout of financial market volatility, as did the run-up to the recent U.S. presidential election.

Despite the challenging macroeconomic backdrop, stocks were able to advance as the Fed’s accommodative stance provided continued support to risk assets including equities, and stock market leadership was squarely focused on bond proxies such as utility stocks. Given the defensive tone of the market, our equity funds struggled to

keep pace with their respective benchmarks during the period. Our growth-oriented funds were generally hurt by the substantial multiple compression experienced by growth names in the technology and healthcare sectors, especially given the pre-election headline risk associated with the latter, while many names in our value-oriented funds were hurt by global growth fears and the impact of a weaker U.S. dollar. Stocks finished the year appearing fairly valued, trading at roughly 16 times forward earnings, which is just slightly above the average over the past three decades.

Looking Ahead

On the positive side, earnings growth expectations may have troughed at the mid-single digit level for calendar year 2016, but admittedly the U.S. economy’s economic growth prospects will have to show improvement in order for consensus estimates for double-digit earnings growth in 2017 to materialize. The election victory of President-elect Trump represents a tectonic shift in the U.S. political landscape and portends major realignments in the policy priorities of the country with broad implications for the economy and financial markets. While the uncertainty associated with this dramatic shift in the political backdrop is likely to result in heightened volatility in the near term — particularly with respect to specific industries as proposed policy details become known — corporate America is well-positioned to avail itself of opportunities that may develop in the coming months and years, which bodes well for stocks over the medium and longer term.

An Update on the TCW Equity Funds

There were a few updates to our fund family over the past twelve months that we would like to note for our investors:

| • | Effective February 1, 2016, TCW launched the TCW New America Premier Equities Fund (TGUSX/TGUNX). The Fund seeks long-term capital appreciation by investing |

1

Letter to Shareholders (Continued) |

in a portfolio of companies the portfolio manager believes are enduring, cash generating businesses whose leaders prudently manage their environmental, social and financial resources and whose shares are attractively valued relative to the free cash flow generated by the businesses. The Fund is managed by Joseph Shaposhnik, Senior Vice President. |

| • | Effective September 30, 2016 the TCW Concentrated Value Fund (TGFFX/ TGFVX) changed its name to the TCW Focused Equities Fund. |

We know that you have many choices when it comes to the management of your financial assets. On behalf of everyone at TCW, I would like to thank you for making the TCW Funds part of your long-term investment plan. We

truly value our relationship with you. If you have any questions or require further information, I invite you to visit our website at www.tcw.com, or call our shareholder services department at 800-386-3829.

I wish you all the best in the coming year and look forward to further correspondence with you through our semi-annual report in 2017.

Sincerely,

David S. DeVito

President, Chief Executive Officer and Director

2

(THIS PAGE INTENTIONALLY LEFT BLANK)

3

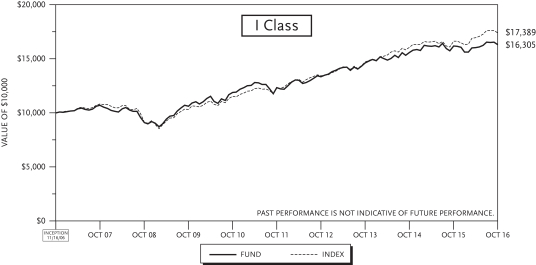

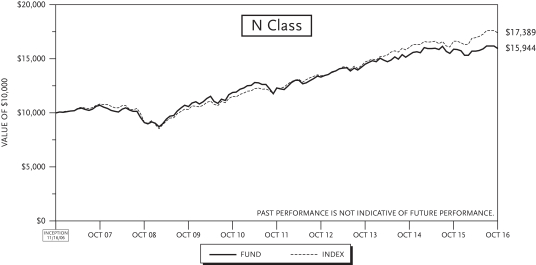

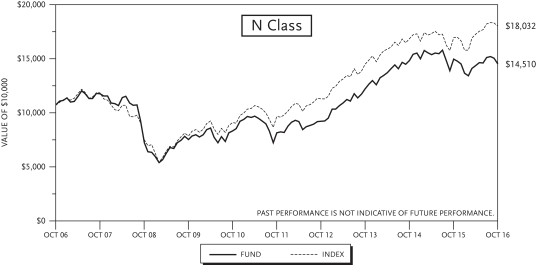

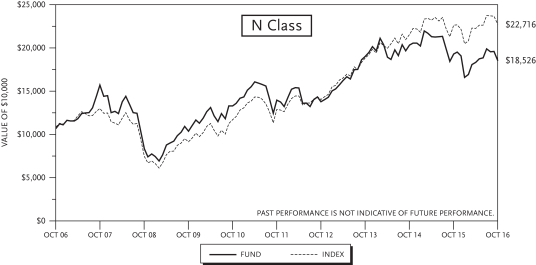

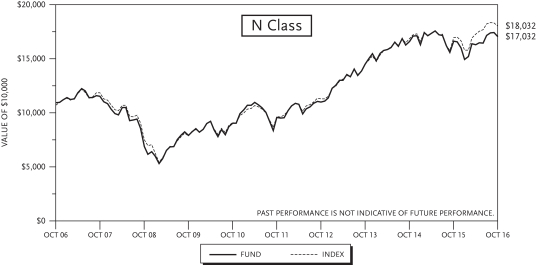

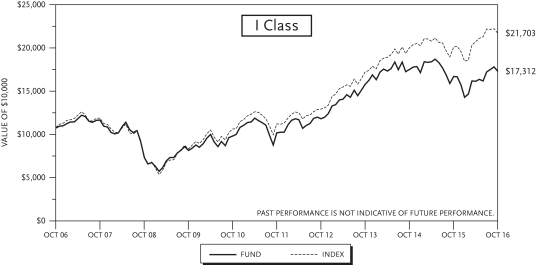

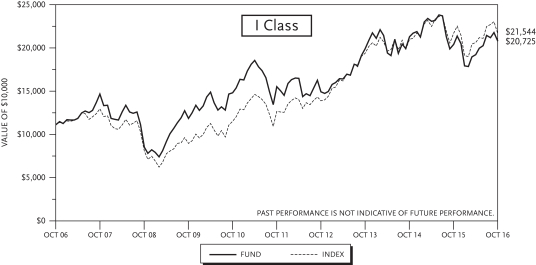

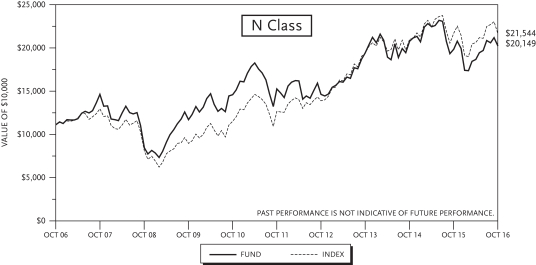

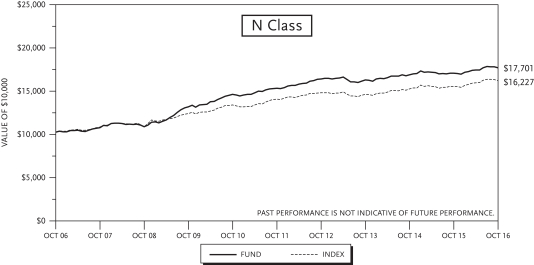

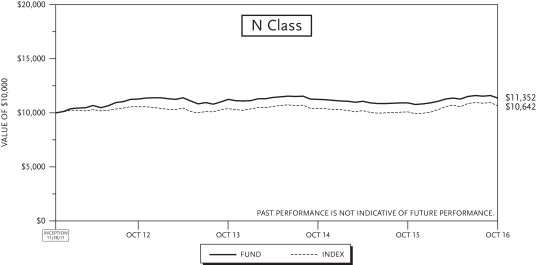

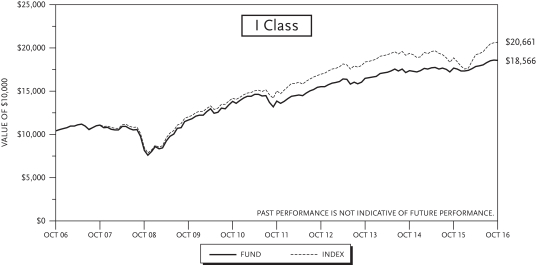

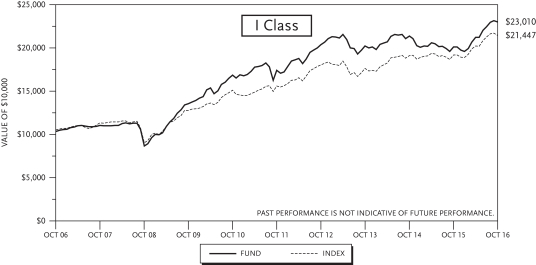

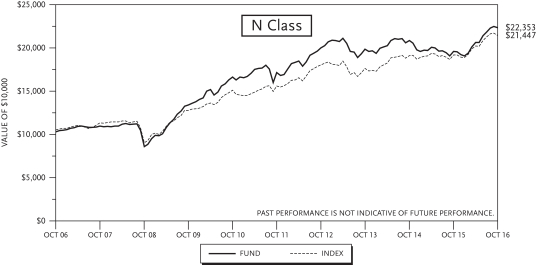

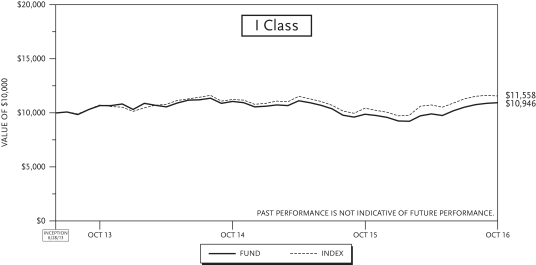

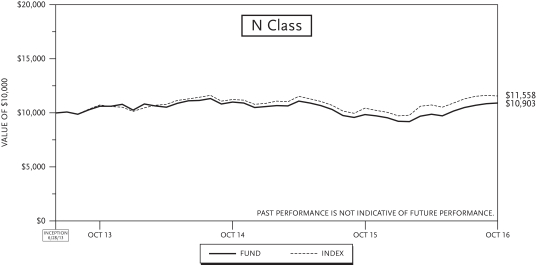

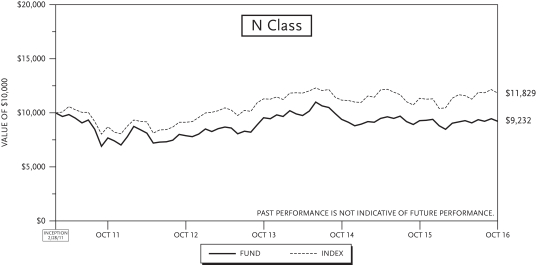

TCW Conservative Allocation Fund

For the year ended October 31, 2016, the TCW Conservative Allocation Fund (the “Fund”) gained 0.78% and 0.31% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s blended benchmark of 40% S&P 500 Index and 60% Bloomberg Barclay U.S. Aggregate Bond Index returned 4.54% over the same period.

The Fund posted positive returns over the past year with a majority of the returns coming from both U.S. equities and U.S. fixed income. The strongest returns came from TCW I Gargoyle Hedged Value and MetWest Total Return Bond Funds. At the asset allocation level, the decision to overweight U.S. fixed income helped relative performance.

As of October, the allocation for the Fund was 39% in equities and 61% in fixed income, giving the Fund a slight underweight to equities and overweight in fixed income relative to its blended index. Over the past 12 months, the Fund has gradually reduced the allocation to U.S. equities, especially the allocations to mid-cap funds, as we feel that some profit taking is best. For the fixed income allocations we remain concentrated within high grade debt favoring mortgage-backed securities. The Fund had small allocations to both high yield and emerging market debt over the past year. Within fixed income allocation, the Fund has recently decreased the duration of its fixed income holdings; for example, an allocation to MetWest Low Duration Fund was added in the third quarter, as we anticipate higher interest rates in the near term.

Over the past year, U.S. equity markets continue to climb reaching all-time highs. The key drivers for these higher returns have been stronger than expected economic data along with strong corporate earnings growth. In addition, central banks are globally maintaining accommodative monetary policies, which are keeping global interest rates low. With the employment landscape improving, the housing sector continuing to show strength, consumer confidence rebounding, low interest rates globally, and expanding GDP growth, we feel confident the recovery will continue to expand and lead to a favorable backdrop for the equity markets. The fixed income markets continue to benefit from a globally low interest rate environment and easy monetary policies worldwide. We do however anticipate the Federal Reserve to increase interest rate in the near term.

4

TCW Conservative Allocation Fund

Management Discussions (Continued)

| Annualized Return(1) | ||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | Inception | |||||||||||||

TCW Conservative Allocation Fund | ||||||||||||||||

Class I – 11/16/2006 | 0.78 | % | 3.74 | % | 5.77 | % | 5.03 | % | ||||||||

Class N – 11/16/2006 | 0.31 | % | 3.20 | % | 5.30 | % | 4.79 | % | ||||||||

40% S&P 500 Index/60% Bloomberg Barclays U.S. Aggregate Bond Index | 4.54 | % | 5.75 | % | 7.20 | % | 5.71 | % | ||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

5

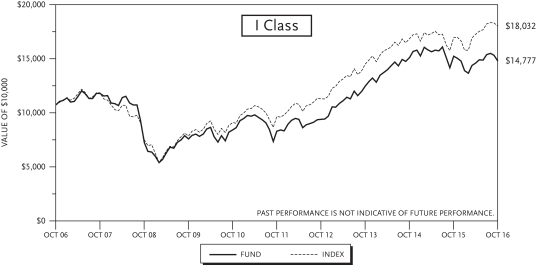

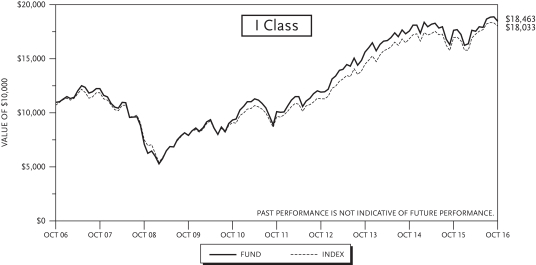

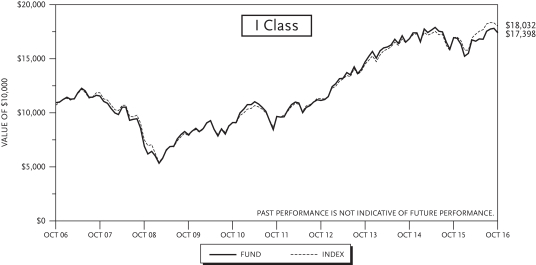

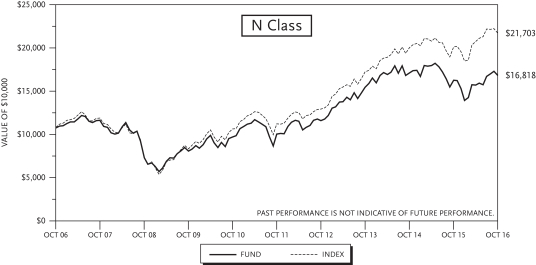

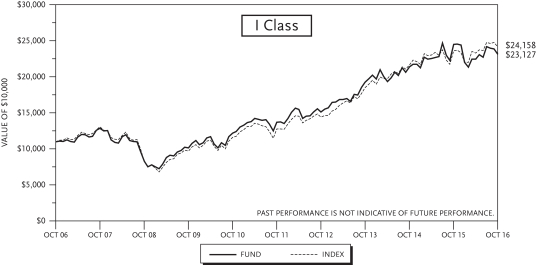

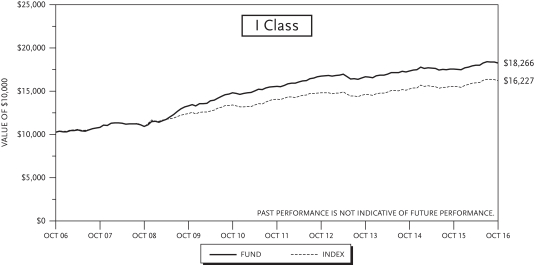

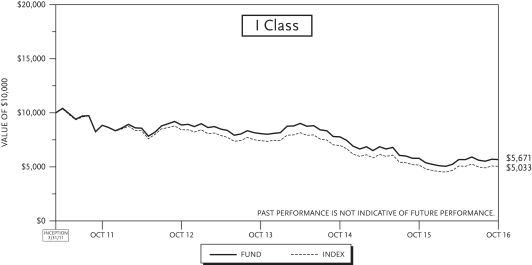

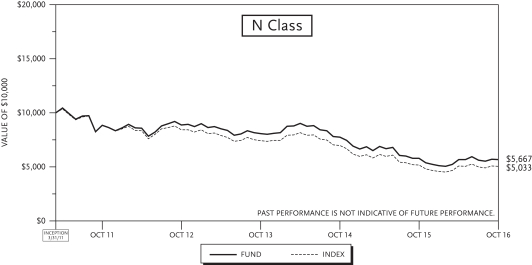

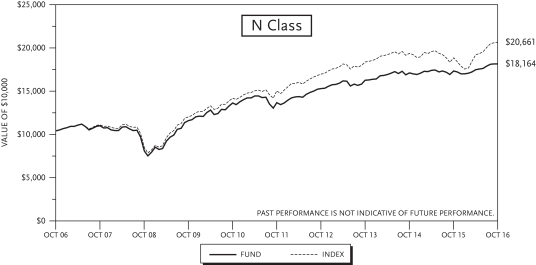

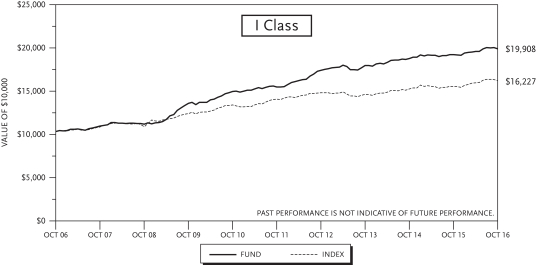

TCW Focused Equities Fund

Management Discussions

For the year ended October 31, 2016, the TCW Focused Equities Fund (formerly TCW Concentrated Value Fund) (“the Fund”) declined 3.04% and 3.08% for its I Class and N Class Shares, respectively. The performance of the Fund’s classes varies because of differing expenses. During the same period, the Russell 1000 Value Index rose 6.37%.

During the year, nearly all of the negative attribution was a result of poor stock selection. This stock selection was partially offset by favorable sector allocation. Healthcare was the worst performing sector in the portfolio and generated nearly half of the underperformance for the year. The underperformance of healthcare started in September 2015 and accelerated during 2016 as a result of the controversy over increasing drug prices. There were companies in the sector that were guilty of increasing prices too quickly but our companies were not involved. Yet no company escaped unscathed and Allergan was the worst performing stock, down 32% for the year followed by McKesson, which was down 28%. Allergan’s negative performance also occurred when the regulators stepped in and called off the merger between Pfizer and Allergan. McKesson, a drug distribution company, does not set prices for drugs but as pricing gets called into question their margins are impacted. Although Celgene and Amgen did not perform as badly as the two companies above, they were negatively impacted by this situation nonetheless. Consumer staples were the second worst performing sector in the portfolio and it also had a healthcare theme to the negative attribution with our investment in CVS. Although CVS is a drug store, they generate substantial profits from their pharmacy benefit manager business. This business also was impacted by the drug pricing issue and the company lowered guidance for 2016 and 2017 due to their forecast of lower prices. Lastly on the negative side of the ledger was the materials sector. The bulk of the underperformance in this sector occurred due to the underperformance of Sealed Air. In last year’s Fund write up we noted that Sealed Air was the best performing stock in the portfolio as they executed flawlessly. However, this year they surprised investors by reducing their cash flow guidance as a result of market conditions and a sluggish economy. We still have faith in management as they are taking actions to create further shareholder value. The best performing sector in the portfolio was the consumer discretion sector, which was the worst performing sector last year. Our patience paid off in the gaming and retail stocks this year as they generated a nearly 20% return. We believe our patience with the underperforming healthcare stocks will be rewarded in 2017.

There were three themes that dominated the markets for most of 2016. First was the drug pricing issue talked about above as healthcare was a substantial underperformer in 2016. Second was the timing of the 2nd rate hike by the Federal Reserve. When the year began the consensus view was that the Fed would raise the Fed Funds rate 2 or 3 times during the year, but as of 10/31 they hadn’t raised rates yet. A rise in the Fed Funds rate is fully expected in December with a probability of over 90% as of this writing. Third was the search for yield. As the 10 year bond yield remained very low throughout the year, investors were searching for yield and found that yield in the utilities, telecom and staples sectors as those were the three best performing sectors in the market during the year ended 10/31/16. Since the election, yields have risen considerably due to the perceived policies of the new President-elect and the 10 year yield now stands at 2.33%, which is the highest yield this year.

6

TCW Focused Equities Fund

Management Discussions (Continued)

We believe that the portfolio owns high quality stocks and it is prudent to be patient. The objective is to create a portfolio that has a good risk/reward profile and to remain balanced so as to be poised to do well in both up markets as well as down markets. We remain confident that investing in attractively valued companies with strong management teams that are expected to increase their return on invested capital and free cash flow generation will yield favorable long-term results.

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Focused Equities Fund (formerly TCW Concentrated Value Fund) | ||||||||||||||||||||||||

Class I – 10/29/2004 | (3.04 | )% | 5.88 | % | 12.21 | % | 3.26 | % | 5.02 | % | 7.14 | % | ||||||||||||

Class N – 07/20/1998 | (3.08 | )% | 5.88 | % | 12.22 | % | 3.07 | % | 5.12 | %(2) | 6.06 | % | ||||||||||||

Russell 1000 Value Index | 6.37 | % | 7.59 | % | 13.31 | % | 5.35 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

| (2) | Performance data includes the performance of the predecessor entity for periods before the Fund’s registration became effective. The predecessor entity was not registered under the 1940 Act and, therefore, was not subject to certain investment restrictions that are imposed by the 1940 Act. If the predecessor entity had been registered under the 1940 Act, the predecessor entity’s performance may have been lower. |

7

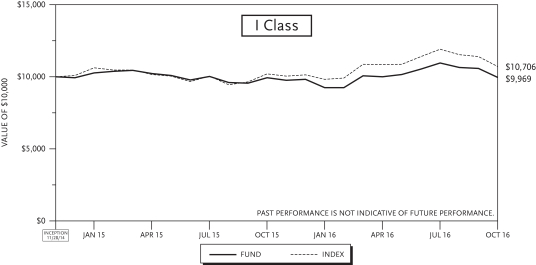

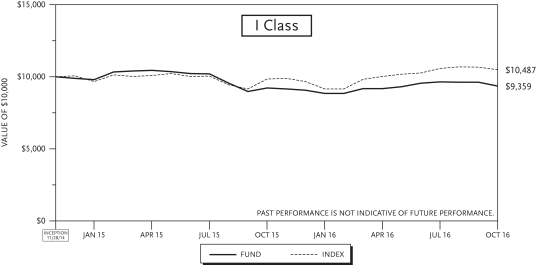

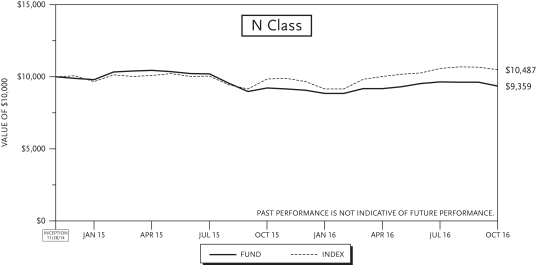

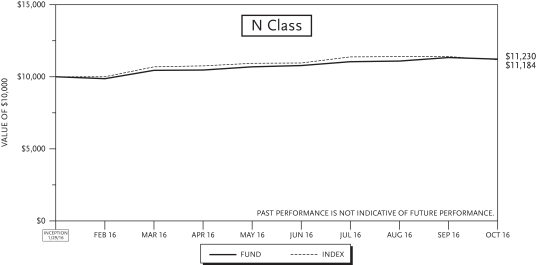

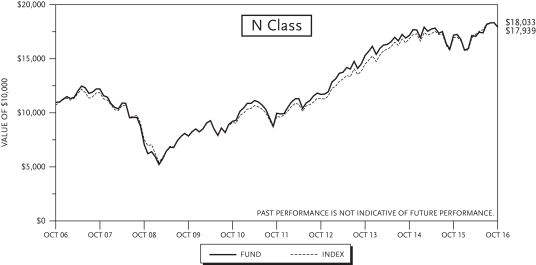

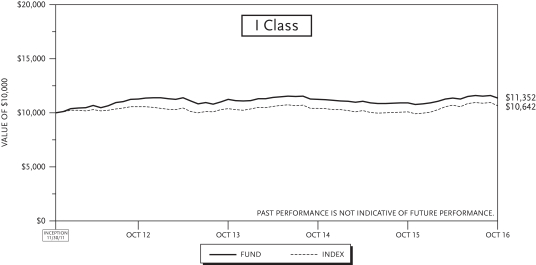

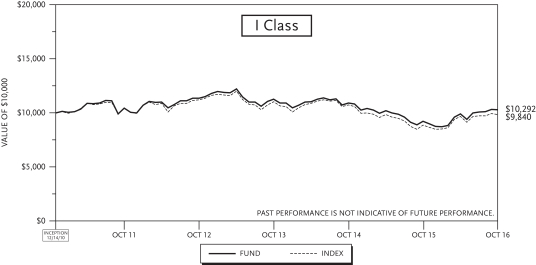

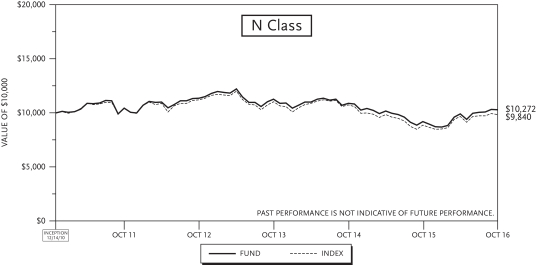

TCW Global Real Estate Fund

Management Discussions

For the year ended October 31, 2016, the TCW Global Real Estate Fund (the “Fund”) gained 0.31% and 0.41% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the S&P Global REIT Index, had a return of 5.00% over the same period.

The year for global real estate equities was volatile. The beginning of the period was particularly tumultuous, as the lead-up to and fallout from the Fed’s December 2015 rate hike and the prospect of a major slowdown in global growth loomed large over the space. For the period ranging from 10/31/2015 to mid-February, the index was down 7.1%. However, with 4Q15 earnings reconfirming the strength of REIT fundamentals and with the Fed backing off the previously communicated pace of its tightening campaign, REITs reflated massively – the sector posted total returns of 20.13% from March through the end of the period. Finally, uncertainty with regard to the U.S. elections and renewed concerns over rising rates weighed on the sector, with the index posting returns of -10.17% for the final 3 months of the reporting period.

On an attribution basis, the Fund’s underperformance relative to its benchmark during the period was both a result of negative stock selection and sector allocation. Allocation was impeded by the 40-Act rule, which imposes a sub-sector maximum of 25%, resulting in an underweight of retail REITs (24.54% vs. 29.10% for the S&P Global REIT Index). From a relative standpoint, the Fund’s largest sector overweight was in Mortgage REITs (up 17.71%), which benefitted performance. The Fund’s largest sector underweight was in Diversified REITs (down 1.16% vs. up 5.95% for the index), which hurt performance. From a stock selection perspective, notable detractors included Toll Brothers Inc., British Land Plc, and Lennar Corporation, which accounted for over half of the Fund’s underperformance relative to its benchmark. Conversely, positive contributors to the Fund’s performance included Nippon Prologis REIT, Chimera Investment Corporation, and Northstar Realty Finance.

With regard to outlook, we remain cautious on REITs despite the recent selloff in the space. History has demonstrated that it pays to heed cues and warnings from the credit markets, as credit tends to lead stocks, especially at inflections. Fixed income markets are suggestive that the credit cycle is nearing an end. Debt growth (particularly in the commodity and pro-cyclical sectors) has been high, and the reach for yield has lowered underwriting standards. Typically what follows is a widening of spreads, which portends defaults are ahead. This, in turn, causes banks and other financial institutions to tighten conditions and scale back lending activity, further fueling a cycle of retraction.

While today’s equity multiples may make sense in a world where low interest rates over the long-term are a given, investors have already begun to view that premise with skepticism. In addition, the global political climate and rise of nationalism/protectionism — previously a largely ignored factor — is likely to impede economic growth and weigh on the markets.

However, there could be some positive offsets as well. The supply/demand picture remains balanced, and REITs could benefit from a “flight to quality” if investors were to shun riskier asset classes. The U.S. housing market seems to be sustaining its growth, which could add to employment and GDP and lengthen the cycle. Also, it appears that central banks across the globe will continue to take the required steps to provide ample liquidity for the proper functioning of financial markets. Thus, a disaster-type crash scenario is fairly unlikely. In a yield-starved world, the REIT sector’s current 4.3% dividend yield could provide some degree of valuation support not too far below current levels.

8

TCW Global Real Estate Fund

Management Discussions (Continued)

Overall, we believe that the net impact of all of these factors skews risk-reward ratios to the downside. As a result, we have adopted a defensive stance in our portfolios, and thus look for companies and REIT sub-sectors with low demand elasticity (which translates into pricing power), lower cyclicality, high earnings or cash flow visibility, and some form of valuation support. We value your support and thank you for your trust.

| Annualized Return(1) | ||||||||

| 1 Yr Return | Inception | |||||||

TCW Global Real Estate Fund | ||||||||

Class I – 11/28/2014 | 0.31 | % | (0.16 | )% | ||||

Class N – 11/28/2014 | 0.41 | % | (0.16 | )% | ||||

S&P Global REIT Index | 5.00 | % | 3.62 | % | ||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

9

TCW Growth Equities Fund

Management Discussions

For the year ended October 31, 2016, the TCW Growth Equities Fund (the “Fund”) had a negative return of 3.93% on both I Class and N Class shares. The Fund’s benchmark, the Russell Midcap Growth Index, returned a positive 0.40% over the same period.

U.S. equities started 2016 in decline and have mostly been on the upswing since mid-February. Following the Federal Reserve’s first interest rate hike in nearly a decade in December, equity markets pushed to record highs on better U.S. economic data and a rebound from record low oil prices. The markets seemed to shrug off the political uncertainty surrounding the U.S. presidential election and Britain’s vote to leave the European Union. Underlying the seemingly bullish market, however, investor sentiment remained bearish as money managers continued to rest on high cash levels and as funds extended their flow out of equities into bonds. IPO activity did pick up modestly in the latter portion of the year, but volume is still down year-over-year. Uncertainty around interest rates, the regulatory environment, and political outcomes in Europe and in the U.S. have kept IPO activity relatively slow. On the other hand, healthy balance sheets and low interest rates funded considerable M&A activity, especially among small- and mid-cap companies.

On an attribution basis, the Fund’s underperformance during the period was primarily a result of negative stock selection in the healthcare, consumer discretionary and financials sectors. Negative stock selection in the consumer staples sector was offset by positive allocation in the sector. Stock selection was positive in the industrials sector. At the end of the period, the Fund’s largest sector weighting was information technology, followed by consumer discretionary. Notable detractors included athenahealth, Valeant Pharmaceuticals and Alkermes in healthcare; Skechers, The Habit Restaurants and Under Armour in consumer discretionary; Boston Beer Company in consumer staples; FireEye and Twitter in information technology; and WisdomTree Investments in financials. On the other hand, contributors of note were names such as Wynn Resorts and Dick’s Sporting Goods in consumer discretionary; Keurig Green Mountain in consumer staples; MarketAxess in financials; Demandware, Proofpoint, Cornerstone OnDemand and ServiceNow in information technology; and HEICO Corporation in industrials. Demandware was acquired by Salesforce.com and Keurig Green Mountain was acquired by an investor group led by JAB Holding Company. ARM Holdings was acquired by Softbank.

At a macroeconomic level, while conditions in China and emerging markets are still the primary headwinds to a global recovery, we are optimistic on the overall strength of the U.S. economy compared to the rest of the world. The U.S. consumer remains relatively resilient as evidenced by new home sales, personal income, and personal consumption expenditures, which are all up year-over-year. In aggregate, despite a few volatile monthly data points, we believe the latest economic data supports that the wider U.S. economy is advancing, albeit at a modest pace. With respect to our investments, we believe “quality,” growth over value, and domestically focused names should outperform in a volatile environment. We seek to invest in companies with highly innovative and differentiated products and services, along with strong balance sheets, positive earnings, and sustainable business models. We continue to anticipate healthy M&A activity and believe there is a robust pipeline of M&A-ready companies. M&A activity in 2015 was largely financially motivated, i.e., large companies buying other large companies through inexpensive financing. As we have

10

TCW Growth Equities Fund

Management Discussions (Continued)

already seen so far this year, we think small- and mid-cap companies with differentiated businesses will be attractive to larger companies looking for strategic assets to drive top-line growth.

| Annualized Return(1) | ||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception | ||||||||||||||||

TCW Growth Equities Fund | ||||||||||||||||||||

Class I – 02/27/2004 | (3.93 | )% | (0.86 | )% | 5.79 | % | 5.70 | % | 6.10 | % | ||||||||||

Class N – 02/27/2004 | (3.93 | )% | (0.83 | )% | 5.80 | % | 5.67 | % | 6.07 | % | ||||||||||

Russell Midcap Growth Index | 0.40 | % | 6.48 | % | 12.02 | % | 7.65 | % | 8.36 | % | ||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

11

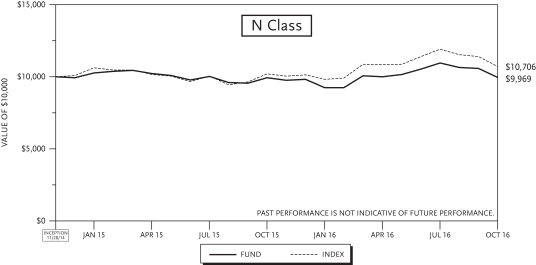

TCW High Dividend Equities Fund

Management Discussions

For the year ended October 31, 2016, the TCW High Dividend Equities Fund (the “Fund”) gained 1.35% and 1.46% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the Russell 3000 Value Index, had a return of 6.55% over the same period.

The year for dividend equities was volatile. The beginning of the period was particularly tumultuous, as the lead-up to and fallout from the Fed’s December 2015 rate hike and the prospect of a major slowdown in global growth loomed large over the space. For the period ranging from 10/31/2015 to mid-February, the index was down 10.46%. However, with 4Q15 earnings surpassing expectations and the Fed backing off the previously communicated pace of its tightening campaign, equities reflated – the index posted total returns of 14.57% from March through the end of the period.

On an attribution basis, the Fund’s underperformance relative to its benchmark during the period was both a result of negative stock selection and sector allocation. From a relative standpoint, the Fund’s largest sector overweight was in Consumer Staples (up 11.63% vs. 12.92% for the index), which benefitted performance. The Fund’s largest sector underweight was in Energy (down 8.96% vs. up 1.91% for the index), which hurt performance. From a stock selection perspective, notable detractors included CVS Health Corporation, Qualcomm Inc., and Cardinal Health Inc. Conversely, positive contributors to the Fund’s performance included Altria Group Inc., Republic Services Inc., and Chubb Limited.

With regard to outlook, we remain cautious despite the recent selloff in our investment universe. History has demonstrated that it pays to heed cues and warnings from the credit markets, as credit tends to lead stocks, especially at inflections. Fixed income markets are suggestive that the credit cycle is nearing an end. Debt growth (particularly in the commodity and pro-cyclical sectors) has been high, and the reach for yield has lowered underwriting standards. Typically what follows is a widening of spreads, which portends defaults are ahead. This, in turn, causes banks and other financial institutions to tighten conditions and scale back lending activity, further fueling a cycle of retraction.

While today’s equity multiples may make sense in a world where low interest rates over the long-term are a given, investors have already begun to view that premise with skepticism (as can be seen by the recent performance of yield sensitive sectors such as REITs and Utilities). In addition, the global political climate and rise of nationalism/protectionism — previously a largely ignored factor — is likely to impede economic growth and weigh on the markets.

However, there could be some positive offsets as well. The U.S. could benefit from a “flight to quality” if investors were to shun riskier markets. The housing market seems to be sustaining its growth, which could add to employment and GDP and lengthen the cycle. Also, it appears that central banks across the globe will continue to take the required steps to provide ample liquidity for the proper functioning of financial markets. Thus, a disaster-type crash scenario is fairly unlikely.

Overall, we believe that the net impact of all of these factors skews risk-reward ratios to the downside. As a result, we have adopted a defensive stance in our portfolios, and thus look for companies with low demand

12

TCW High Dividend Equities Fund

Management Discussions (Continued)

elasticity (which translates into pricing power), lower cyclicality, high earnings or cash flow visibility, and some form of valuation support. We value your support and thank you for your trust.

| Annualized Return(1) | ||||||||

| 1 Yr Return | Inception | |||||||

TCW High Dividend Equities Fund | ||||||||

Class I – 11/28/2014 | 1.35 | % | (3.40 | )% | ||||

Class N – 11/28/2014 | 1.46 | % | (3.40 | )% | ||||

Russell 3000 Value Index | 6.55 | % | 2.51 | % | ||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

13

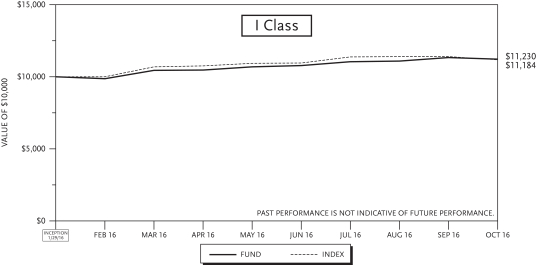

TCW New America Premier Equities Fund

Management Discussions

For the period January 29, 2016 (inception date of the Fund) through October 31, 2016, the TCW New America Premier Equities Fund (the “Fund”) increased by 12.30% on both its I Class and N Class shares. The Fund’s benchmark, the Russell 1000 Index, returned 11.84% over the same period.

The Fund benefitted from owning Illinois Tool Works, Comcast, and Air Products. These three high free cash flow yielding businesses were top contributors to the Fund’s outperformance, while Dr. Pepper Snapple Group, Inc., Roper Technologies, and Sealed Air Corporation were negative contributors. The Fund continued to own these six securities at the close of trading on October 31, 2016.

We believe that controlling risk, not generating returns, is our primary objective. Since inception our returns have been generated while exposing our clients to lower volatility, downside risk and tracking error relative to the benchmark. It is our goal to continue to generate strong returns while taking on lower than market volatility and risk.

Investment Philosophy

The Fund seeks to outperform the broad U.S. indices in both rising and falling markets with less risk and volatility. We seek to accomplish this objective by investing in a concentrated portfolio of businesses that carefully manage their environmental and social resources and that employ best in class corporate governance practices. We invest in businesses that have high barriers to entry, are stable, generate substantial free cash flow and are managed by prudent leaders.

Risk control. Our primary objective, as stewards of your capital, is to control risk while seeking attractive returns. We control risk in a unique manner; initially we apply our proprietary ESG quantitative framework to identify better managed businesses that have lower quantifiable and unquantifiable risks. Subsequently, we hone our efforts on those businesses that we believe operate in stable industries with attractive industry structures, businesses that produce products that are critical to their customers, and businesses that we believe are led by proven, appropriately incentivized leaders. We endeavor to further control valuation risk by purchasing securities at attractive prices relative to the current free cash flow generation of the businesses. We believe that businesses that fit our profile produce fairly stable cash flow streams and are less prone to macroeconomic fluctuations, competitive pressures and valuation risks.

Consistency. It is also our objective to deliver a consistently positive outcome. We would view outsized outperformance in one year and poor performance in the subsequent year as a poor outcome for our clients. Our bottoms up investment process is focused on selecting undervalued businesses that we believe should perform well in most market environments and hold up well in negative periods. We believe consistency in approach and consistency in outcome gives us the best chance of minimizing a left tail outcome in any given year. It is our view that if we can consistently deliver above average risk adjusted performance over a long period of time the outcome likely would be outperformance relative to our peers over the full period. That is our goal.

Environmental, Social, Governance Analysis: Traditional fundamental analysis does not capture risks associated with managing environmental resources nor does it assess the performance of businesses from the perspective of resource efficiency. Traditional analysis does not typically assess the risks associated with a heterogeneous workforce nor does it assess the competence, quality and engagement level of the Board of Directors. Our investment framework not only pays close attention to these issues, we also quantify, score, and rank companies and exclude businesses based on these risk factors.

14

TCW New America Premier Equities Fund

Management Discussions (Continued)

While those risks are not quantified through traditional financial analysis, we have found a significant correlation between companies that manage their resources prudently and businesses that sport strong financial metrics. Based on our research and investment criteria, businesses that meet our rigorous ESG performance requirements typically have higher free cash flow yields, higher total yields, higher margins and lower levels of financial leverage.

Focus on Dominant, Predictable Businesses with High Barriers to Entry: In the long run the investment performance of a portfolio is inextricably linked to the underlying performance of the earnings and cash flows of the businesses comprising the portfolio. We believe one of the greatest risks in investing is valuing a business based on an erroneous view of the future free cash flows of the business. Such a circumstance results in an investor typically overpaying for a business and therefore generating a poor return on the investment.

In fast growing businesses or in industries that are undergoing rapid changes it is extraordinarily difficult and often dangerous to make an investment in a business when the long-term cash generation potential of the enterprise has a wide spectrum of outcomes. We seek to avoid companies and industries that are undergoing rapid changes.

What we do seek, however, are stable businesses that have dominant market positions, and whose long- term cash flows we believe can be predicted reasonably well. The qualitative characteristics that we seek, including attractive industry structures, pricing power and dominant market positions, make us confident in our forecast of the future cash flows of the businesses and therefore provide greater confidence that our valuation of the business is reasonably accurate.

The famed value investor Benjamin Graham once said, “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” Our view is that the market weighs cash flows and in order to consistently purchase a security for less than what it is worth, one should have high confidence in the future free cash flows of a business.

15

TCW New America Premier Equities Fund

Management Discussions (Continued)

Cumulative Inception(1) | ||||

TCW New America Premier Equities Fund | ||||

Class I – 1/29/2016 | 12.30 | % | ||

Class N – 1/29/2016 | 12.30 | % | ||

Russell 1000 Index | 11.84 | % | ||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

16

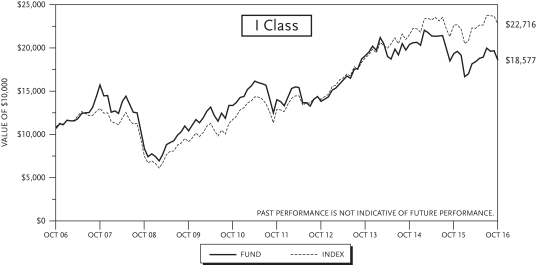

TCW Relative Value Dividend Appreciation Fund

Management Discussions

For the year ended October 31, 2016, the TCW Relative Value Dividend Appreciation Fund (the “Fund”) gained 4.66% and 4.43% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the Russell 1000 Value Index, returned 6.37% over the same period.

Market Outlook

After dipping to 49.4 in August, the Institute of Supply Management’s Purchasing Managers Index “ISM PMI” bounced back in September and further in October to 51.9, and the new orders and production components also climbed back above 50 after their respective dips in August; a level of 50 or greater connotes expansion. Similarly, after a slowdown in August, auto sales have showed some resurgence with October’s number coming in at a 17.9 million seasonally adjusted annual rate (SAAR). While housing data softened in September, the housing market is showing signs of strength as new home purchases by millennials scarred by the Great Financial Crisis appear to have picked up. Buyers have purchased new single-family houses at an annualized rate of nearly 600,000, near its highest rate since the winter of 2008 (July 2016 registered 629,000), and housing starts have been running at a one million annual pace every month since April 2015, a marked improvement from the 478,000 rate in the spring of 2009. According to Realtor.com, first-time buyers now comprise one-half of those looking to purchase a home in 2017, up from 33% last year. New home buyers should provide a significant boost to sales which would then translate to a bounce in household spending.

With the relatively strong 3Q GDP figure, solid monthly jobs gains, and continuing rise in year-over-year wage growth there is a stronger likelihood for a rate hike in December. The consensus is for one to two modest hikes in 2017. After tepid growth in the first half of the year, the first estimate for 3Q U.S. economic activity came in at a robust 2.9% annualized rate quarter-over-quarter as a build up in inventory and a soybean-related spike in exports offset softer household spending, which grew at a slower pace after the prior quarter’s healthy 4.3% pace. Inventories accounted for 0.6 percentage points to GDP growth as stockpiles were rebuilt ending a streak in which negative changes in inventories weighed on growth for five consecutive quarters. Job growth thus far this year, while not as robust as in 2015, has been solid running at a 180,000 monthly average pace and the unemployment rate now stands at 4.9%. Average hourly earnings have risen to 2.8% year-over-year, the four-week moving average for jobless claims is at lows not seen since the early 1970s, and temporary employment figures (a harbinger for future full-time hires) remain solid.

The S&P 500 earnings recession may have come to an end with year-over-year earnings coming in at flat to low single-digits on the positive side; previous estimates had called for negative low single-digits. The Conference Board Consumer Confidence Index softened to 98.6 in October from 103.5 in September potentially due to acrimony surrounding the FBI and the election; a level of 100 or higher connotes an expansionary economy. Household incomes rose for the first time in eight years. According to the Census Bureau, in 2015 middle-class Americans and the poor enjoyed their best year of economic improvement in decades, a spike that broke a years-long streak of disappointment for American workers. Real median household income increased 5.2% to $56,500 in 2015 from $53,700 in 2014. This increase was the largest, in percentage terms, since the Bureau began tracking median income statistics in the 1960s.

The U.S. remains in a slow to low 1-3% GDP growth rate, even with a potential Brexit global growth hair cut of 0.25% to 0.50% over the next year. The U.S. continues to be an attractive market and safe haven for investors given uncertainty in Europe and Japan as well as decelerating growth in China. These and other

17

TCW Relative Value Dividend Appreciation Fund

Management Discussions (Continued)

factors are important supports for U.S. growth, making the odds of a near-term recession remain less than 40% in our view. Generally, recessions do not occur with an accommodative Fed or when oil prices are low. Historically, since the end of World War II, the market has rebounded post presidential elections into year-end by nearly two percentage points, regardless of the party victor, 70% of the time. With the election decided, by the end of the year stronger U.S. earnings growth will be more evident. This, along with an accommodative Federal Reserve policy slowly moving to interest rate normalization, should be positive for the market.

Fund Review

Over the course of the year ended October 31, the Fund’s top ten conviction-weighted holdings outperformed the portfolio and both benchmarks over the period returning +9.1%, on average, led by Chevron, Microsoft, Royal Philips, Merck, and JP Morgan Chase. The Fund’s Energy names were the best relative performers led by Chevron, Baker Hughes, and Nabors Industries, while its Consumer Staples stocks performed admirably led by Sysco and Campbell Soup. DuPont, recent initiation WestRock, and Avery Dennison were the stalwarts among the portfolio’s Materials stocks leading to the relative outperformance in the sector. Other positive performers included ADT, Microchip Technology, Quest Diagnostics, Johnson Controls (acquirer of Tyco), Corning, and Regal Entertainment. Avery Dennison was completely sold as it reached its valuation target while ADT was eliminated after news it was being acquired by a private equity firm at a significant premium. On the downside, the portfolio’s Telecommunication Services names underperformed due in large part to Deutsche Telekom, while Ameriprise Financial was largely responsible for the loss suffered in Financials and was completely sold post fiscal year end. Gap, Time, and Lennar were the biggest laggards in the Consumer Discretionary Care space, as was Seagate Technology in Information Technology. Other notable detractors included Gilead Sciences, Citigroup, New York Community Bancorp, Textron, and MetLife.

18

TCW Relative Value Dividend Appreciation Fund

Management Discussions (Continued)

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Relative Value Dividend Appreciation Fund | ||||||||||||||||||||||||

Class I – 10/29/2004 | 4.66 | % | 5.73 | % | 12.83 | % | 5.35 | % | 6.79 | % | 7.14 | % | ||||||||||||

Class N – 09/19/1986 | 4.43 | % | 5.45 | % | 12.52 | % | 5.05 | % | 9.05 | % | 10.11 | % | ||||||||||||

Russell 1000 Value Index | 6.37 | % | 7.59 | % | 13.31 | % | 5.35 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

19

TCW Relative Value Large Cap Fund

Management Discussions

For the year ended October 31, 2016, the TCW Relative Value Large Cap Fund (the “Fund”) gained 2.61% and 2.42% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the Russell 1000 Value Index, returned 6.37% over the same period.

Market Outlook

After dipping to 49.4 in August, the Institute of Supply Management’s Purchasing Managers Index “ISM PMI” bounced back in September and further in October to 51.9, and the new orders and production components also climbed back above 50 after their respective dips in August; a level of 50 or greater connotes expansion. Similarly, after a slowdown in August, auto sales have showed some resurgence with October’s number coming in at a 17.9 million seasonally adjusted annual rate (SAAR). While housing data softened in September, the housing market is showing signs of strength as new home purchases by millennials scarred by the Great Financial Crisis appear to have picked up. Buyers have purchased new single-family houses at an annualized rate of nearly 600,000, near its highest rate since the winter of 2008 (July 2016 registered 629,000), and housing starts have been running at a one million annual pace every month since April 2015, a marked improvement from the 478,000 rate in the spring of 2009. According to Realtor.com, first-time buyers now comprise one-half of those looking to purchase a home in 2017, up from 33% last year. New home buyers should provide a significant boost to sales which would then translate to a bounce in household spending.

With the relatively strong 3Q GDP figure, solid monthly jobs gains, and continuing rise in year-over-year wage growth there is a stronger likelihood for a rate hike in December. The consensus is for one to two modest hikes in 2017. After tepid growth in the first half of the year, the first estimate for 3Q U.S. economic activity came in at a robust 2.9% annualized rate quarter-over-quarter as a build up in inventory and a soybean-related spike in exports offset softer household spending, which grew at a slower pace after the prior quarter’s healthy 4.3% pace. Inventories accounted for 0.6 percentage points to GDP growth as stockpiles were rebuilt ending a streak in which negative changes in inventories weighed on growth for five consecutive quarters. Job growth thus far this year, while not as robust as in 2015, has been solid running at a 180,000 monthly average pace and the unemployment rate now stands at 4.9%. Average hourly earnings have risen to 2.8% year-over-year, the four-week moving average for jobless claims is at lows not seen since the early 1970s, and temporary employment figures (a harbinger for future full-time hires) remain solid.

The S&P 500 earnings recession may have come to an end with year-over-year earnings coming in at flat to low single-digits on the positive side; previous estimates had called for negative low single-digits. The Conference Board Consumer Confidence Index softened to 98.6 in October from 103.5 in September potentially due to acrimony surrounding the FBI and the election; a level of 100 or higher connotes an expansionary economy. Household incomes rose for the first time in eight years. According to the Census Bureau, in 2015 middle-class Americans and the poor enjoyed their best year of economic improvement in decades, a spike that broke a years-long streak of disappointment for American workers. Real median household income increased 5.2% to $56,500 in 2015 from $53,700 in 2014. This increase was the largest, in percentage terms, since the Bureau began tracking median income statistics in the 1960s.

The U.S. remains in a slow to low 1-3% GDP growth rate, even with a potential Brexit global growth hair cut of 0.25% to 0.50% over the next year. The U.S. continues to be an attractive market and safe haven for investors given uncertainty in Europe and Japan as well as decelerating growth in China. These and other

20

TCW Relative Value Large Cap Fund

Management Discussions (Continued)

factors are important supports for U.S. growth, making the odds of a near-term recession remain less than 40% in our view. Generally, recessions do not occur with an accommodative Fed or when oil prices are low. Historically, since the end of World War II, the market has rebounded post presidential elections into year-end by nearly two percentage points, regardless of the party victor, 70% of the time. With the election decided, by the end of the year stronger U.S. earnings growth will be more evident. This, along with an accommodative Federal Reserve policy slowly moving to interest rate normalization, should be positive for the market.

Fund Review

Over the course of the year ended October 31, the Fund’s top ten conviction-weighted holdings outperformed the portfolio and both benchmarks over the period returning +5.3%, on average, led by Chevron, Microsoft, JP Morgan Chase, and Cisco Systems. The Fund’s Information Technology names were the best relative performers led by Applied Materials, Corning, Micron Technology, and Microsoft, while its Energy stocks performed admirably led by Chevron, Baker Hughes, and Newfield Exploration. Sysco was the stalwart among the portfolio’s Consumer Staples stocks leading to the relative outperformance in the sector. The portfolio was well positioned for either outcome of the U.S. presidential election and went to a natural underweight in Health Care at the end of September, which was positive, given the two candidates’ polemic positions. Other positive performers included ADT, Johnson Controls (acquirer of Tyco), and Terex in Industrials, Utility company American Electric Power, and Zions Bancorporation in Financials. American Electric Power was completely sold as it appreciated to the point of meeting its valuation target, while ADT was eliminated after news it was being acquired by a private equity firm at a significant premium. On the downside, the portfolio’s Consumer Discretionary names underperformed due in large part to Gap, Lennar, and Dana. Ameriprise Financial was largely responsible for the loss suffered in Financials and was completely sold while Gilead Sciences and Anthem were the biggest laggards in the Health Care space. Other notable detractors include Sealed Air in Materials, Textron in Industrials, and Chesapeake Energy, which was completely sold after a fundamental review in February.

21

TCW Relative Value Large Cap Fund

Management Discussions (Continued)

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Relative Value Large Cap Fund | ||||||||||||||||||||||||

Class I – 12/31/2003 | 2.61 | % | 5.79 | % | 12.50 | % | 4.74 | % | 7.00 | % | 7.24 | % | ||||||||||||

Class N – 12/31/1997 | 2.42 | % | 5.53 | % | 12.23 | % | 4.52 | % | 5.93 | % | 6.68 | % | ||||||||||||

Russell 1000 Value Index | 6.37 | % | 7.59 | % | 13.31 | % | 5.35 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

22

TCW Relative Value Mid Cap Fund

Management Discussions

For the year ended October 31, 2016, the TCW Relative Value Mid Cap Fund (the “Fund”) posted a return of 3.53% and 3.30% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the Russell Midcap Value Index, returned 7.84% over the same period.

Market Outlook

After dipping to 49.4 in August, the Institute of Supply Management’s Purchasing Managers Index “ISM PMI” bounced back in September and further in October to 51.9, and the new orders and production components also climbed back above 50 after their respective dips in August; a level of 50 or greater connotes expansion. Similarly, after a slowdown in August, auto sales have showed some resurgence with October’s number coming in at a 17.9 million seasonally adjusted annual rate (SAAR). While housing data softened in September, the housing market is showing signs of strength as new home purchases by millennials scarred by the Great Financial Crisis appear to have picked up. Buyers have purchased new single-family houses at an annualized rate of nearly 600,000, near its highest rate since the winter of 2008 (July 2016 registered 629,000), and housing starts have been running at a one million annual pace every month since April 2015, a marked improvement from the 478,000 rate in the spring of 2009. According to Realtor.com, first-time buyers now comprise one-half of those looking to purchase a home in 2017, up from 33% last year. New home buyers should provide a significant boost to sales which would then translate to a bounce in household spending.

With the relatively strong 3Q GDP figure, solid monthly jobs gains, and continuing rise in year-over-year wage growth there is a stronger likelihood for a rate hike in December. The consensus is for one to two modest hikes in 2017. After tepid growth in the first half of the year, the first estimate for 3Q U.S. economic activity came in at a robust 2.9% annualized rate quarter-over-quarter as a build up in inventory and a soybean-related spike in exports offset softer household spending, which grew at a slower pace after the prior quarter’s healthy 4.3% pace. Inventories accounted for 0.6 percentage points to GDP growth as stockpiles were rebuilt ending a streak in which negative changes in inventories weighed on growth for five consecutive quarters. Job growth thus far this year, while not as robust as in 2015, has been solid running at a 180,000 monthly average pace and the unemployment rate now stands at 4.9%. Average hourly earnings have risen to 2.8% year-over-year, the four-week moving average for jobless claims is at lows not seen since the early 1970s, and temporary employment figures (a harbinger for future full-time hires) remain solid.

The Russell Midcap earnings recession may have come to an end with year-over-year earnings coming in at flat to low single-digits on the positive side; previous estimates had called for negative low single-digits. The Conference Board Consumer Confidence Index softened to 98.6 in October from 103.5 in September potentially due to acrimony surrounding the FBI and the election; a level of 100 or higher connotes an expansionary economy. Household incomes rose for the first time in eight years. According to the Census Bureau, in 2015 middle-class Americans and the poor enjoyed their best year of economic improvement in decades, a spike that broke a years-long streak of disappointment for American workers. Real median household income increased 5.2% to $56,500 in 2015 from $53,700 in 2014. This increase was the largest, in percentage terms, since the Bureau began tracking median income statistics in the 1960s.

The U.S. remains in a slow to low 1-3% GDP growth rate, even with a potential Brexit global growth hair cut of 0.25% to 0.50% over the next year. The U.S. continues to be an attractive market and safe haven for investors given uncertainty in Europe and Japan as well as decelerating growth in China. These and other

23

TCW Relative Value Mid Cap Fund

Management Discussions (Continued)

factors are important supports for U.S. growth, making the odds of a near-term recession remain less than 40% in our view. Generally, recessions do not occur with an accommodative Fed or when oil prices are low. Historically, since the end of World War II, the market has rebounded post presidential elections into year-end by nearly two percentage points, regardless of the party victor, 70% of the time. With the election decided, by the end of the year stronger U.S. earnings growth will be more evident. This along with an accommodative Federal Reserve policy slowly moving to interest rate normalization should be positive for the market.

Fund Review

Over the course of the year ended October 31, the Fund’s top ten conviction-weighted holdings was accretive to the Fund’s performance returning +12.4%, on average, led by Worthington Industries, Popular, Quest Diagnostics, Coach, and KeyCorp. The Fund’s Materials stocks also contributed positive return, led by Worthington Industries and Axiall, as well as Campbell Soup and Sysco in Consumer Staples. Quest Diagnostics was a bright spot in Health Care aiding in the portfolio’s outperformance in the sector, one that struggled during the one year period, while Windstream’s robust return along with aid from the recently initiated Zayo Group were the primary drivers in Telecommunication Services. On the downside, the portfolio’s Information Technology names were the worst relative performers due in large part to Seagate Technology, Polycom, Western Digital, and NetApp. Toll Brothers, Gap, Beazer Homes, and Lennar were the largest detractors among the portfolio’s Consumer Discretionary names while Jones Lang LaSalle (now reassigned to the newly carved out Real Estate sector), Invesco, and GEO Group struggled in Financials. Other notable detractors include Chesapeake Energy, which was completely sold after a fundamental review in February, and SPX Flow.

24

TCW Relative Value Mid Cap Fund

Management Discussions (Continued)

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Relative Value Mid Cap Fund | ||||||||||||||||||||||||

Class I – 11/1/1996 | 3.53 | % | 3.15 | % | 11.16 | % | 4.89 | % | 9.95 | %(2) | 10.45 | % | ||||||||||||

Class N – 10/31/2000 | 3.30 | % | 2.91 | % | 10.89 | % | 4.59 | % | 7.17 | % | 9.72 | % | ||||||||||||

Russell Midcap Value Index | 7.84 | % | 7.97 | % | 14.07 | % | 7.19 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

| (2) | Performance data includes the performance of the predecessor entity for periods before the Fund’s registration became effective. The predecessor entity was not registered under the 1940 Act and, therefore, was not subject to certain investment restrictions that are imposed by the 1940 Act. If the predecessor entity had been registered under the 1940 Act, the predecessor entity’s performance may have been lower. |

25

TCW Select Equities Fund

Management Discussions

For the year ended October 31, 2016, the TCW Select Equities Fund (the “Fund”) had a negative return of 5.56% and 5.81% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, Russell 1000 Growth Index, returned 2.28% over the same period.

Fiscal 2016 began with the S&P 500 rallying +8.4% in October, marking the best monthly gain in five years. Economic data remained mixed in November and December 2015 but the key event was the Fed’s decision in December to finally move off the zero-bound and raise the target range for the federal funds rate by 25 basis points, the first rate tightening since June 2006. Stock market volatility ensued and the first six weeks of calendar 2016 marked the worst stock market start to a calendar year in U.S. history. The Bank of Japan surprised the market by introducing negative interest rates, potentially opening up Pandora’s Box as to the technical limits of QE. By the end of February, ~1/3 of global sovereign debt traded with a negative interest rate. In Europe, the ECB delivered a package of policy measures that included cutting its benchmark rate to 0.0%, announced a larger-than-expected €20B increase in its monthly asset purchases to €80B, and amended the composition of its QE program to include investment grade euro-denominated bonds. In April the yen hit a 17-month high despite NIRP (negative interest rate policy). Meanwhile in the U.S., the FOMC remained dovish as Fed Chair Yellen noted that global economic and financial developments continue to pose risks for the economy and the inflation outlook had become more uncertain and 1Q16 GDP increased only +0.8%. Increased volatility returned to the markets in June when the British voted to exit the EU (“Brexit”) but the S&P 500 finished June in modestly positive territory. Economic data remained mixed through the summer and fall and although U.S. GDP of +2.9% in 3Q16 represented a sequential improvement, U.S. GDP remained stubbornly low post the Great Recession. As the fiscal year ended, focus turned to the U.S. Presidential election.

Net of expenses, the Fund underperformed for the year primarily as a result of negative security selection results, particularly in the health care, consumer discretionary and information technology sectors. Athenahealth, Inc. underperformed as the company failed to announce a large enterprise deal in 2016 and bookings growth moderated due to a more challenging end market landscape. Chipotle Mexican Grill, Inc. retreated due to a handful of E. coli outbreaks, which severely negatively impacted traffic and sales. Our biggest stock detractor during the year came from the information technology sector: LinkedIn Corporation dropped after the company issued weak FY2016 guidance and noted a meaningfully slowing in its Marketing and Subscriptions segments.

Our biggest stock contributors during the year came from the information technology and financials sectors. Facebook Inc. rallied as the company posted robust broad-based growth across several advertiser segments and verticals. ARM Holdings plc jumped when it was announced that SoftBank Group intended to acquire the company in an all-cash transaction for a 43% premium to its last closing price. Equinix, Inc., the largest network neutral co-location data center provider in the world, rallied due to strong revenues per cabinet, decreasing customer churn and solid higher-margin interconnection revenues. In the financials sector, Chubb moved higher as its announced deal with ACE in 2015 created a global P&C industry leader

26

TCW Select Equities Fund

Management Discussions (Continued)

and provided revenue and expense synergy opportunities that offset a weakening pricing environment in its end market.

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Select Equities Fund | ||||||||||||||||||||||||

Class I – 07/01/1991 | (5.56 | )% | 6.29 | % | 11.07 | % | 7.73 | % | 9.49 | %(2) | 8.70 | % | ||||||||||||

Class N – 2/26/1999 | (5.81 | )% | 6.01 | % | 10.76 | % | 7.43 | % | 5.09 | % | 4.00 | % | ||||||||||||

Russell 1000 Growth Index | 2.28 | % | 9.36 | % | 13.65 | % | 8.22 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

| (2) | Performance data includes the performance of the predecessor entity for periods before the Fund’s registration became effective. The predecessor entity was not registered under the 1940 Act and, therefore, was not subject to certain investment restrictions that are imposed by the 1940 Act. If the predecessor entity had been registered under the 1940 Act, the predecessor entity’s performance may have been lower. |

27

TCW Small Cap Growth Fund

Management Discussions

For the year ended October 31, 2016, the TCW Small Cap Growth Fund (the “Fund”) gained 1.94% and 1.92% on its I Class and N Class shares, respectively. The performance of the Fund’s classes varies because of differing expenses. The Fund’s benchmark, the Russell 2000 Growth Index, declined 0.49% over the same period.

U.S. equities started 2016 in decline and have mostly been on the upswing since mid-February. Following the Federal Reserve’s first interest rate hike in nearly a decade in December, equity markets pushed to record highs on better U.S. economic data and a rebound from record low oil prices. The markets seemed to shrug off the political uncertainty surrounding the U.S. presidential election and Britain’s vote to leave the European Union. Underlying the seemingly bullish market, however, investor sentiment remains bearish as money managers continue to rest on high cash levels and as funds extended their flow out of equities into bonds. IPO activity did pick up modestly in the latter portion of the year, but volume is still down year-over-year. Uncertainty around interest rates, the regulatory environment, and political outcomes in Europe and in the U.S. have kept IPO activity relatively slow. On the other hand, healthy balance sheets and low interest rates funded considerable M&A activity, especially among small- and mid-cap companies.

On an attribution basis, the Fund’s outperformance was primarily a result of positive stock selection in the healthcare and industrials sectors. Stock selection also helped in information technology and energy. Partially offsetting this was negative stock selection in consumer discretionary, consumer staples and financials. At the end of the period, the Fund’s largest sector weighting was the information technology sector, followed by healthcare. Contributors of note included Cepheid and LDR Holding Corporation in healthcare, John Bean Technologies, HEICO Corporation and B/E Aerospace in industrials, Demandware and Cornerstone OnDemand in information technology and MarketAxess in financials. LDR Holding was acquired by Zimmer Biomet and B/E Aerospace agreed to be acquired by Rockwell Collins. Demandware was acquired by Salesforce.com and Marketo was acquired by Vista Equity Partners. On the other hand, notable detractors were names such as Skechers, The Habit Restaurants and Gentherm in consumer discretionary, Boston Beer Company in consumer staples, WisdomTree Investments in financials, Eagle Pharmaceuticals, Valeant Pharmaceuticals and athenahealth in healthcare, and FireEye in information technology.

At a macroeconomic level, while conditions in China and emerging markets are still the primary headwinds to a global recovery, we are optimistic on the overall strength of the U.S. economy compared to the rest of the world. The U.S. consumer remains relatively resilient as evidenced by new home sales, personal income, and personal consumption expenditures, which are all up year-over-year. In aggregate, despite a few volatile monthly data points, we believe the latest economic data support that the wider U.S. economy is advancing, albeit at a modest pace. With respect to our investments, we believe “quality,” growth over value, and domestically focused names should outperform in a volatile environment. We seek to invest in companies with highly innovative and differentiated products and services, along with strong balance sheets, positive earnings, and sustainable business models. We continue to anticipate healthy M&A activity and believe there is a robust pipeline of M&A-ready companies. M&A activity in 2015 was largely financially motivated, i.e., large companies buying other large companies through inexpensive financing. As we have

28

TCW Small Cap Growth Fund

Management Discussions (Continued)

already seen so far this year, we think small- and mid-cap companies with differentiated businesses will be attractive to larger companies looking for strategic assets to drive top-line growth.

| Annualized Return(1) | ||||||||||||||||||||||||

| 1 Yr Return | 3 Yr Return | 5 Yr Return | 10 Yr Return | Inception Fund | Inception Index | |||||||||||||||||||

TCW Small Cap Growth Fund | ||||||||||||||||||||||||

Class I – 12/01/1989 | 1.94 | % | 1.52 | % | 6.03 | % | 6.50 | % | 8.63 | %(2) | 7.30 | % | ||||||||||||

Class N – 2/26/1999 | 1.92 | % | 1.36 | % | 5.79 | % | 6.21 | % | 3.56 | % | 6.07 | % | ||||||||||||

Russell 2000 Growth Index | (0.49 | )% | 3.70 | % | 11.34 | % | 6.92 | % | ||||||||||||||||

| (1) | The total returns do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. |

| (2) | Performance data includes the performance of the predecessor entity for periods before the Fund’s registration became effective. The predecessor entity was not registered under the 1940 Act and, therefore, was not subject to certain investment restrictions that are imposed by the 1940 Act. If the predecessor entity had been registered under the 1940 Act, the predecessor entity’s performance may have been lower. |

29

TCW Conservative Allocation Fund

| Number of Shares | Investment Companies | Value | ||||||

Diversified Equity Funds (39.0% of Net Assets) | ||||||||

| 195,801 | TCW / Gargoyle Hedged Value Fund — I Class (1) | $ | 1,707,381 | |||||

| 120,731 | TCW Global Real Estate Fund — I Class (1) | 1,137,284 | ||||||

| 351,990 | TCW High Dividend Equities Fund — I Class (1) | 3,136,227 | ||||||

| 77,502 | TCW International Growth Fund — I Class (1) | 758,743 | ||||||

| 124,211 | TCW Relative Value Large Cap Fund — I Class (1) | 2,655,623 | ||||||

| 96,331 | TCW Select Equities Fund — I Class (1) | 2,510,378 | ||||||

|

| |||||||

Total Diversified Equity Funds | 11,905,636 | |||||||

|

| |||||||

Diversified Fixed Income Funds (60.2%) | ||||||||

| 354,750 | Metropolitan West Low Duration Bond Fund — I Class (1) | 3,104,061 | ||||||

| 391,564 | Metropolitan West Total Return Bond Fund — I Class (1) | 4,279,794 | ||||||

| 75,764 | TCW Global Bond Fund — I Class (1) | 748,545 | ||||||

| 995,444 | TCW Total Return Bond Fund — I Class (1) | 10,282,941 | ||||||

|

| |||||||

Total Diversified Fixed Income Funds | 18,415,341 | |||||||

|

| |||||||

Total Investment Companies (Cost: $28,113,725) (99.2%) | 30,320,977 | |||||||

|

| |||||||

Total Investments (Cost: $28,113,725) (99.2%) | 30,320,977 | |||||||

Excess of Other Assets over Liabilities (0.8%) | 257,982 | |||||||

|

| |||||||

Net Assets (100.0%) | $ | 30,578,959 | ||||||

|

| |||||||

Notes to the Schedule of Investments:

| (1) | Affiliated issuer. |

See accompanying notes to financial statements.

30

TCW Conservative Allocation Fund

Investments by Industry | October 31, 2016 |

| Industry | Percentage of Net Assets | |||

Diversified Fixed Income Funds | 60.2 | % | ||

Diversified Equity Funds | 39.0 | |||

|

| |||

Total | 99.2 | % | ||

|

| |||

See accompanying notes to financial statements.

31

Schedule of Investments

| Number of Shares | Common Stock | Value | ||||||

Aerospace & Defense (4.5% of Net Assets) | ||||||||

| 1,930 | Honeywell International, Inc. | $ | 211,683 | |||||

| 855 | TransDigm Group, Inc. (1) | 232,953 | ||||||

|

| |||||||

Total Aerospace & Defense | 444,636 | |||||||

|

| |||||||

Banks (13.6%) | ||||||||

| 3,535 | JPMorgan Chase & Co. | 244,834 | ||||||

| 3,150 | M&T Bank Corp. | 386,599 | ||||||

| 6,520 | US Bancorp | 291,835 | ||||||

| 9,065 | Wells Fargo & Co. | 417,081 | ||||||

|

| |||||||

Total Banks | 1,340,349 | |||||||

|

| |||||||

Beverages (2.7%) | ||||||||

| 2,315 | Anheuser-Busch InBev NV (Belgium) (SP ADR) | 267,359 | ||||||

|

| |||||||

Biotechnology (5.6%) | ||||||||

| 1,780 | Amgen, Inc. | 251,265 | ||||||

| 2,900 | Celgene Corp. (1) | 296,322 | ||||||

|

| |||||||

Total Biotechnology | 547,587 | |||||||

|

| |||||||

Capital Markets (2.9%) | ||||||||

| 1,585 | Goldman Sachs Group, Inc. (The) | 282,510 | ||||||

|

| |||||||

Chemicals (5.9%) | ||||||||

| 2,415 | Air Products & Chemicals, Inc. | 322,209 | ||||||

| 2,280 | Ecolab, Inc. | 260,308 | ||||||

|

| |||||||

Total Chemicals | 582,517 | |||||||

|

| |||||||

Containers & Packaging (2.8%) | ||||||||

| 6,090 | Sealed Air Corp. | 277,887 | ||||||

|

| |||||||

Energy Equipment & Services (1.0%) | ||||||||

| 1,235 | Schlumberger, Ltd. | 96,614 | ||||||

|

| |||||||

Food & Staples Retailing (2.6%) | ||||||||

| 3,060 | CVS Health Corp. | 257,346 | ||||||

|

| |||||||

Food Products (3.5%) | ||||||||

| 1,285 | Mead Johnson Nutrition Co. | 96,079 | ||||||

| 5,425 | Mondelez International, Inc. | 243,800 | ||||||

|

| |||||||

Total Food Products | 339,879 | |||||||

|

| |||||||

Health Care Providers & Services (2.4%) | ||||||||

| 1,840 | McKesson Corp. | 233,993 | ||||||

|

| |||||||

Hotels, Restaurants & Leisure (4.9%) | ||||||||

| 4,975 | Las Vegas Sands Corp. | 287,953 | ||||||

| 3,740 | Starbucks Corp. | 198,482 | ||||||

|

| |||||||

Total Hotels, Restaurants & Leisure | 486,435 | |||||||

|

| |||||||

See accompanying notes to financial statements.

32

TCW Focused Equities Fund

October 31, 2016 |

| Number of Shares | Common Stock | Value | ||||||

Industrial Conglomerates (5.0%) | ||||||||

| 4,230 | Danaher Corp. | $ | 332,266 | |||||

| 950 | Roper Technologies, Inc. | 164,645 | ||||||

|

| |||||||

Total Industrial Conglomerates | 496,911 | |||||||

|

| |||||||

Insurance (3.4%) | ||||||||

| 2,640 | Chubb, Ltd. (Switzerland) | 335,280 | ||||||

|

| |||||||

Internet Software & Services (3.1%) | ||||||||

| 395 | Alphabet, Inc. — Class C (1) | 309,893 | ||||||

|

| |||||||

Machinery (2.5%) | ||||||||

| 2,885 | IDEX Corp. | 249,379 | ||||||

|

| |||||||

Multiline Retail (3.0%) | ||||||||

| 3,870 | Dollar Tree, Inc. (1) | 292,378 | ||||||

|

| |||||||

Oil, Gas & Consumable Fuels (10.9%) | ||||||||

| 4,710 | Devon Energy Corp. | 178,462 | ||||||

| 4,805 | EOG Resources, Inc. | 434,468 | ||||||

| 3,925 | Occidental Petroleum Corp. | 286,172 | ||||||

| 6,140 | Williams Cos., Inc. (The) | 179,288 | ||||||

|

| |||||||

Total Oil, Gas & Consumable Fuels | 1,078,390 | |||||||

|

| |||||||

Pharmaceuticals (6.2%) | ||||||||

| 5,285 | AbbVie, Inc. | 294,797 | ||||||

| 1,517 | Allergan plc (Ireland) (1) | 316,962 | ||||||

|

| |||||||

Total Pharmaceuticals | 611,759 | |||||||

|

| |||||||

Road & Rail (3.5%) | ||||||||

| 3,890 | Union Pacific Corp. | 343,020 | ||||||

|

| |||||||

Software (3.6%) | ||||||||

| 3,335 | Adobe Systems, Inc. (1) | 358,546 | ||||||

|

| |||||||

Specialty Retail (1.7%) | ||||||||

| 1,220 | Advance Auto Parts, Inc. | 170,898 | ||||||

|

| |||||||

Textiles, Apparel & Luxury Goods (1.8%) | ||||||||

| 1,660 | PVH Corp. | 177,587 | ||||||

|

| |||||||

Total Common Stock (Cost: $8,835,161) (97.1%) | 9,581,153 | |||||||

|

| |||||||

| Master Limited Partnership | ||||||||

Oil, Gas & Consumable Fuels (2.0%) | ||||||||

| 2,586 | EQT Midstream Partners LP | 193,614 | ||||||

|

| |||||||

Total Master Limited Partnership (Cost: $182,391) (2.0%) | 193,614 | |||||||

|

| |||||||

See accompanying notes to financial statements.

33

TCW Focused Equities Fund

Schedule of Investments (Continued)

| Number of Shares | Money Market Investments | Value | ||||||

| 65,451 | State Street Institutional U.S. Government Money Market Fund — Premier Class, 0.25% (2) | $ | 65,451 | |||||

|

| |||||||

Total Money Market Investments (Cost: $65,451) (0.7%) | 65,451 | |||||||

|

| |||||||

Total Investments (Cost: $9,083,003) (99.8%) | 9,840,218 | |||||||

Excess of Other Assets over Liabilities (0.2%) | 21,104 | |||||||

|

| |||||||

Net Assets (100.0%) | $ | 9,861,322 | ||||||

|

| |||||||

Notes to the Schedule of Investments:

| (1) | Non-income producing security. |

| (2) | Rate disclosed is the 7-day net yield as of October 31, 2016. |

| SP ADR - Sponsored | American Depositary Receipt. Shares of a foreign based corporation held in U.S. banks that are issued with the cooperation of the company whose stock underlies the ADR and entitles the shareholder to all dividends, capital gains and voting rights. |

See accompanying notes to financial statements.

34

TCW Focused Equities Fund

Investments by Industry | October 31, 2016 |

| Industry | Percentage of Net Assets | |||

Aerospace & Defense | 4.5 | % | ||

Banks | 13.6 | |||

Beverages | 2.7 | |||

Biotechnology | 5.6 | |||

Capital Markets | 2.9 | |||

Chemicals | 5.9 | |||

Containers & Packaging | 2.8 | |||

Energy Equipment & Services | 1.0 | |||

Food & Staples Retailing | 2.6 | |||

Food Products | 3.5 | |||

Health Care Providers & Services | 2.4 | |||

Hotels, Restaurants & Leisure | 4.9 | |||

Industrial Conglomerates | 5.0 | |||

Insurance | 3.4 | |||

Internet Software & Services | 3.1 | |||

Machinery | 2.5 | |||

Multiline Retail | 3.0 | |||

Oil, Gas & Consumable Fuels | 12.9 | |||

Pharmaceuticals | 6.2 | |||

Road & Rail | 3.5 | |||

Software | 3.6 | |||

Specialty Retail | 1.7 | |||

Textiles, Apparel & Luxury Goods | 1.8 | |||

Money Market Investments | 0.7 | |||

|

| |||

Total | 99.8 | % | ||

|

| |||

See accompanying notes to financial statements.

35

Schedule of Investments

| Number of Shares | Common Stock | Value | ||||||

Australia (4.7% of Net Assets) |

| |||||||

| 33,873 | Scentre Group | $ | 108,447 | |||||

| 12,134 | Westfield Corp. | 82,027 | ||||||

|

| |||||||

Total Australia (Cost: $195,383) | 190,474 | |||||||

|

| |||||||

China (4.4%) |

| |||||||

| 31,000 | China Overseas Land & Investment, Ltd. | 95,175 | ||||||

| 11,332 | Link REIT (The) | 80,623 | ||||||

|

| |||||||

Total China (Cost: $161,726) | 175,798 | |||||||

|

| |||||||

France (4.7%) |

| |||||||

| 1,720 | Klepierre | 70,193 | ||||||

| 492 | Unibail — Rodamco SE | 116,619 | ||||||

|

| |||||||

Total France (Cost: $208,530) | 186,812 | |||||||

|

| |||||||

Germany (Cost: $84,644) (2.5%) |

| |||||||